global survey on voluntary sustainability standards...

TRANSCRIPT

Research Institute of Organic AgricultureForschungsinstitut für biologischen Landbau

Global survey on Voluntary Sustainability Standards (VSS)Key figuresJulia Lernoud and Helga WillerResearch Institute of Organic Agriculture (FiBL), Frick, Switzerland, February 2017

Institut de recherche de l’agriculture biologique

www.fibl.org

Partners

› Research Institute of Organic Agriculture (FiBL)

› International Trade Centre (ITC)

› International Institute for Sustainable Development

2

› The Swiss State Secretariat for Economic Affairs SECO

Supporter

www.fibl.org

List of VSS

› 4C Association› Better Cotton Initiative (BCI)› Bonsucro› Cotton Made in Africa› Fairtrade International› Forest Stewardship Council (FSC)› GLOBALG.A.P.› IFOAM – Organics International› Programme for the Endorsement of Forest Certification (PEFC)› ProTerra Foundation› Rainforest Alliance/Sustainable Agriculture Network› Roundtable for Sustainable Palm Oil (RSPO)› Round Table for Responsible Soy (RTRS)› UTZ Certified

3

www.fibl.org

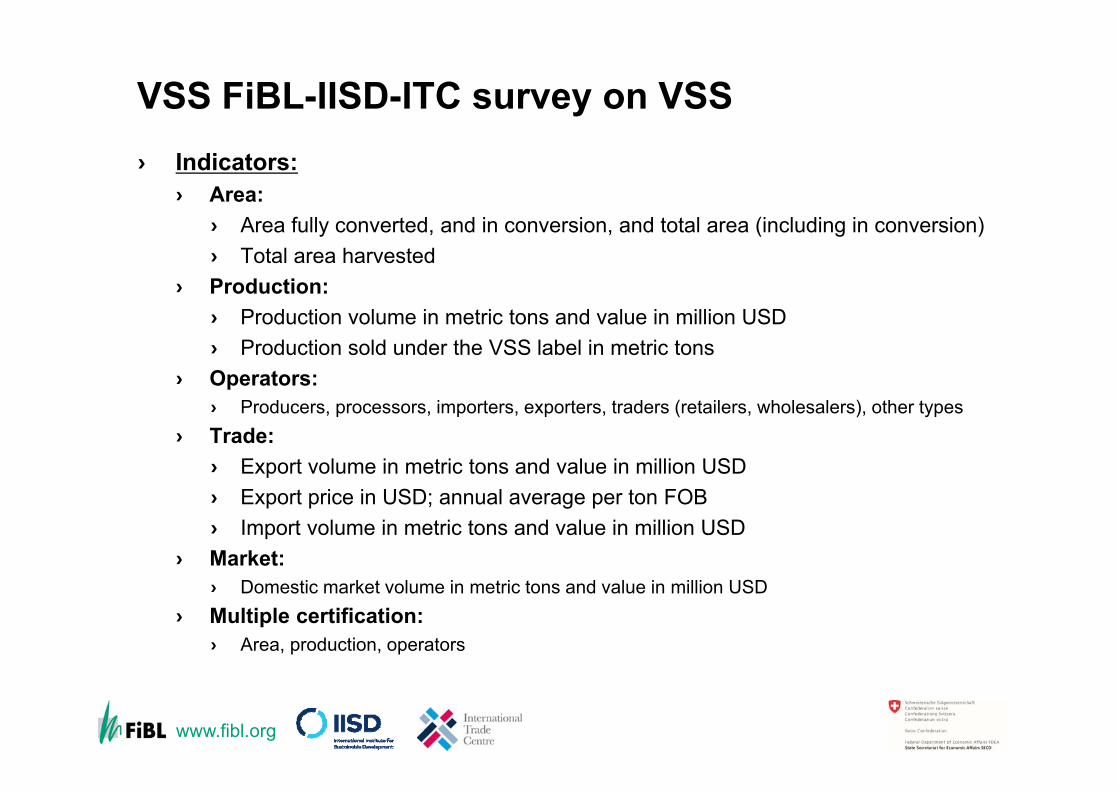

VSS FiBL-IISD-ITC survey on VSS› Indicators:

› Area:› Area fully converted, and in conversion, and total area (including in conversion)› Total area harvested

› Production:› Production volume in metric tons and value in million USD› Production sold under the VSS label in metric tons

› Operators:› Producers, processors, importers, exporters, traders (retailers, wholesalers), other types

› Trade:› Export volume in metric tons and value in million USD› Export price in USD; annual average per ton FOB› Import volume in metric tons and value in million USD

› Market:› Domestic market volume in metric tons and value in million USD

› Multiple certification:› Area, production, operators

4

www.fibl.org

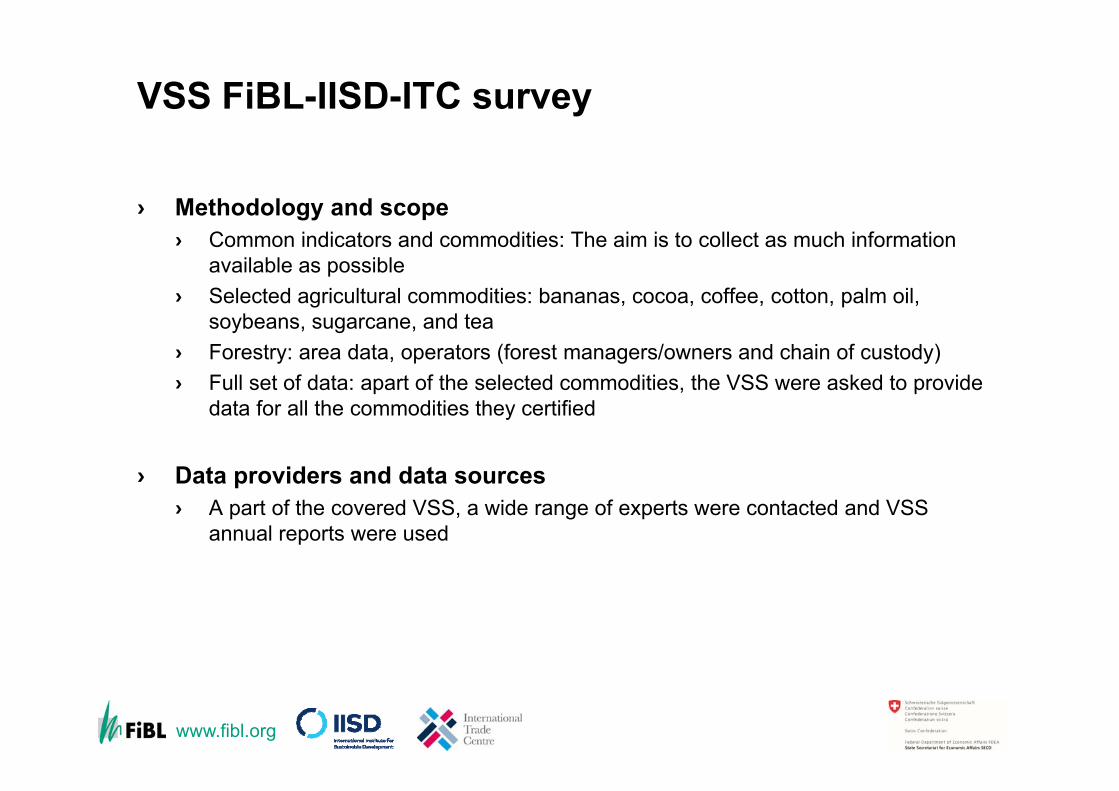

VSS FiBL-IISD-ITC survey

› Methodology and scope› Common indicators and commodities: The aim is to collect as much information

available as possible› Selected agricultural commodities: bananas, cocoa, coffee, cotton, palm oil,

soybeans, sugarcane, and tea› Forestry: area data, operators (forest managers/owners and chain of custody)› Full set of data: apart of the selected commodities, the VSS were asked to provide

data for all the commodities they certified

› Data providers and data sources› A part of the covered VSS, a wide range of experts were contacted and VSS

annual reports were used

5

www.fibl.org

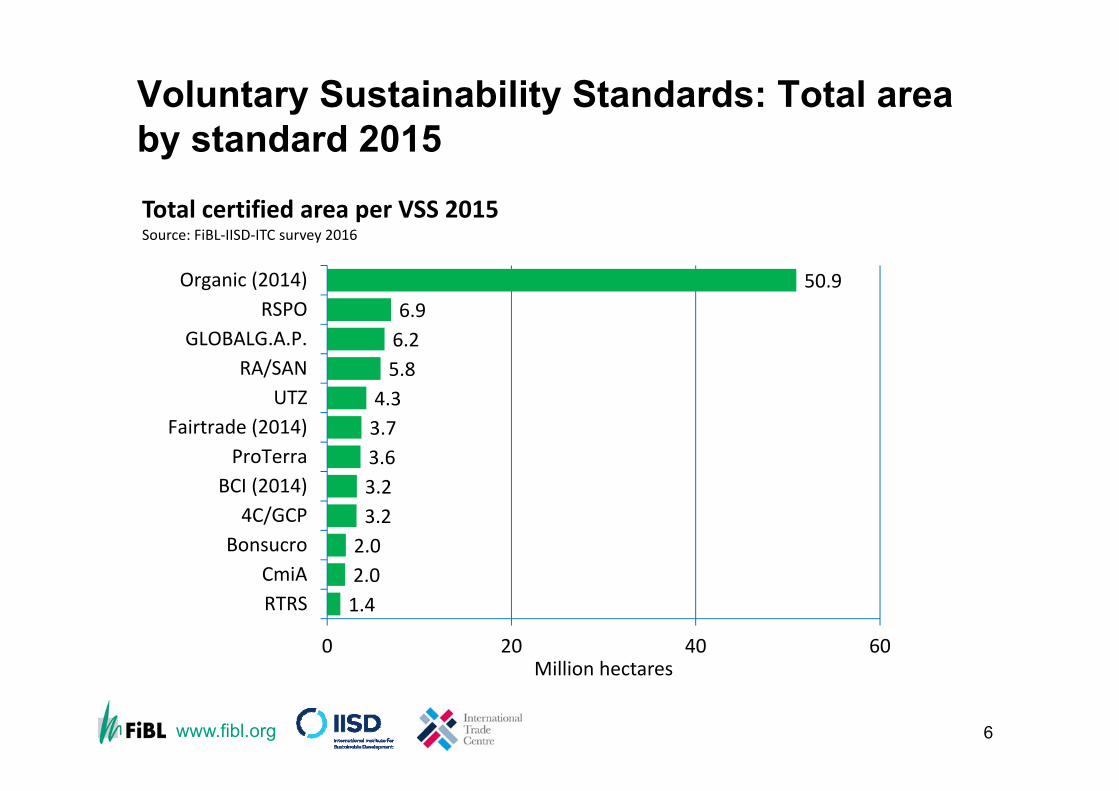

Voluntary Sustainability Standards: Total area by standard 2015

6

1.42.02.03.23.23.63.74.35.86.26.9

50.9

0 20 40 60

RTRSCmiA

Bonsucro4C/GCP

BCI (2014)ProTerra

Fairtrade (2014)UTZ

RA/SANGLOBALG.A.P.

RSPOOrganic (2014)

Million hectares

Total certified area per VSS 2015Source: FiBL‐IISD‐ITC survey 2016

www.fibl.org

Cocoa

Other

Rainforest Alliance

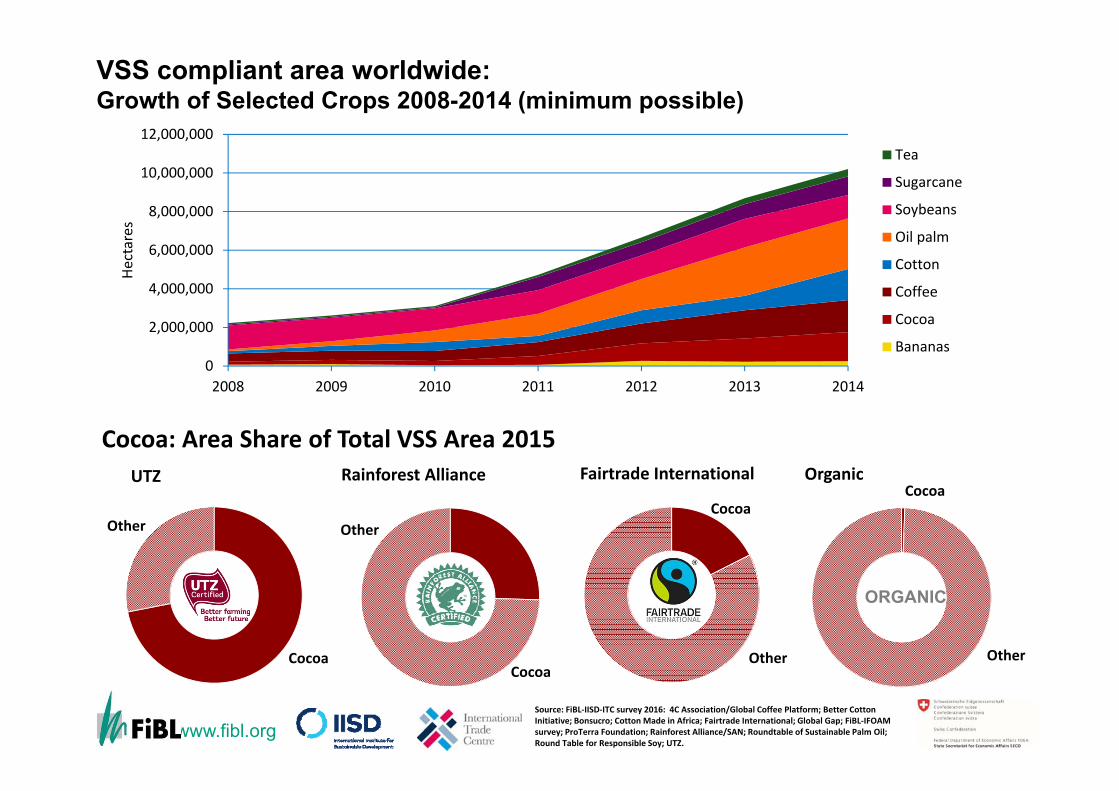

VSS compliant area worldwide: Growth of Selected Crops 2008-2014 (minimum possible)

0

2,000,000

4,000,000

6,000,000

8,000,000

10,000,000

12,000,000

2008 2009 2010 2011 2012 2013 2014

Hectares

Tea

Sugarcane

Soybeans

Oil palm

Cotton

Coffee

Cocoa

Bananas

Cocoa: Area Share of Total VSS Area 2015

Cocoa

Other

Fairtrade InternationalCocoa

Other

Organic

Cocoa

Other

UTZ

ORGANIC

Source: FiBL‐IISD‐ITC survey 2016: 4C Association/Global Coffee Platform; Better Cotton Initiative; Bonsucro; Cotton Made in Africa; Fairtrade International; Global Gap; FiBL‐IFOAM survey; ProTerra Foundation; Rainforest Alliance/SAN; Roundtable of Sustainable Palm Oil; Round Table for Responsible Soy; UTZ.

www.fibl.org

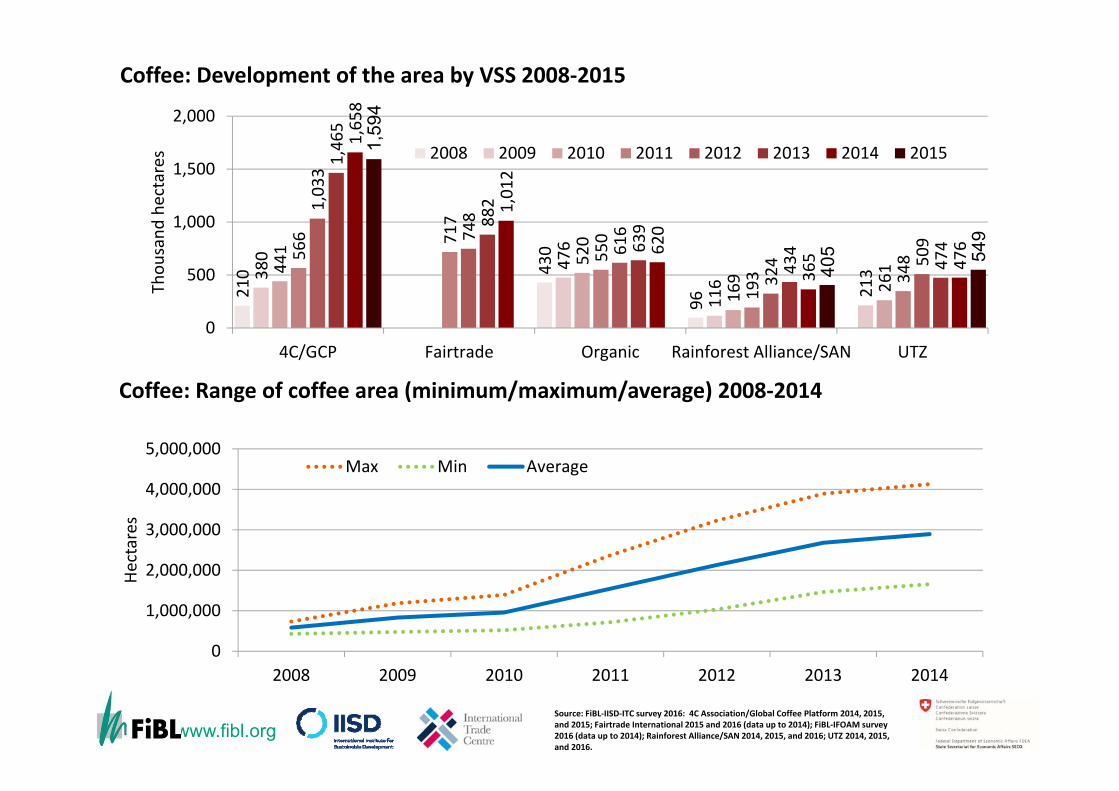

210 43

0

96

380 476

116 21344

1 520

169 261

566 717

550

193 348

1,033

748

616

324 50

9

1,465

882

639

434

474

1,658

1,012

620

365 476

1,59

4

405 54

9

0

500

1,000

1,500

2,000

4C/GCP Fairtrade Organic Rainforest Alliance/SAN UTZ

Thou

sand

hectares

Coffee: Development of the area by VSS 2008‐2015

2008 2009 2010 2011 2012 2013 2014 2015

8

0

1,000,000

2,000,000

3,000,000

4,000,000

5,000,000

2008 2009 2010 2011 2012 2013 2014

Hectares

Coffee: Range of coffee area (minimum/maximum/average) 2008‐2014

Max Min Average

Source: FiBL‐IISD‐ITC survey 2016: 4C Association/Global Coffee Platform 2014, 2015, and 2015; Fairtrade International 2015 and 2016 (data up to 2014); FiBL‐IFOAM survey 2016 (data up to 2014); Rainforest Alliance/SAN 2014, 2015, and 2016; UTZ 2014, 2015, and 2016.

www.fibl.org

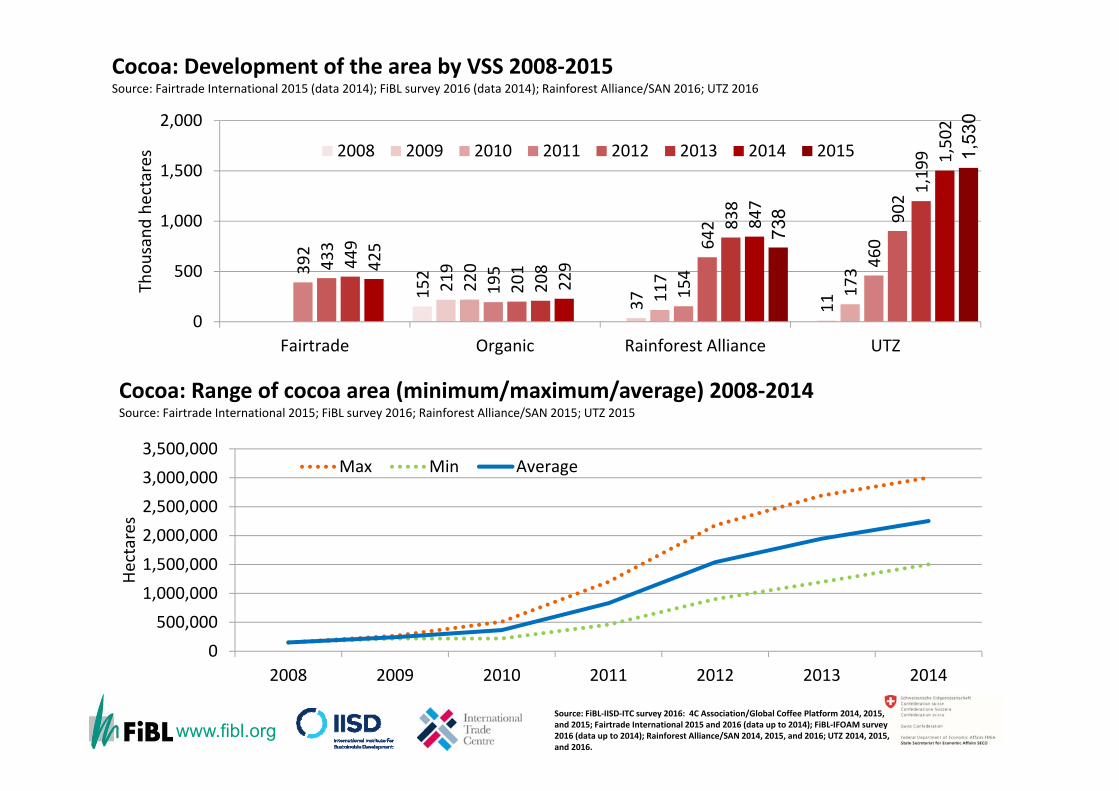

152

219

37 11

220

117

17339

2

195

154

460

433

201

642 90

2

449

208

838

1,199

425

229

847

1,502

738

1,53

0

0

500

1,000

1,500

2,000

Fairtrade Organic Rainforest Alliance UTZ

Thou

sand

hectares

Cocoa: Development of the area by VSS 2008‐2015Source: Fairtrade International 2015 (data 2014); FiBL survey 2016 (data 2014); Rainforest Alliance/SAN 2016; UTZ 2016

2008 2009 2010 2011 2012 2013 2014 2015

9

0500,000

1,000,0001,500,0002,000,0002,500,0003,000,0003,500,000

2008 2009 2010 2011 2012 2013 2014

Hectares

Cocoa: Range of cocoa area (minimum/maximum/average) 2008‐2014Source: Fairtrade International 2015; FiBL survey 2016; Rainforest Alliance/SAN 2015; UTZ 2015

Max Min Average

Source: FiBL‐IISD‐ITC survey 2016: 4C Association/Global Coffee Platform 2014, 2015, and 2015; Fairtrade International 2015 and 2016 (data up to 2014); FiBL‐IFOAM survey 2016 (data up to 2014); Rainforest Alliance/SAN 2014, 2015, and 2016; UTZ 2014, 2015, and 2016.

www.fibl.org

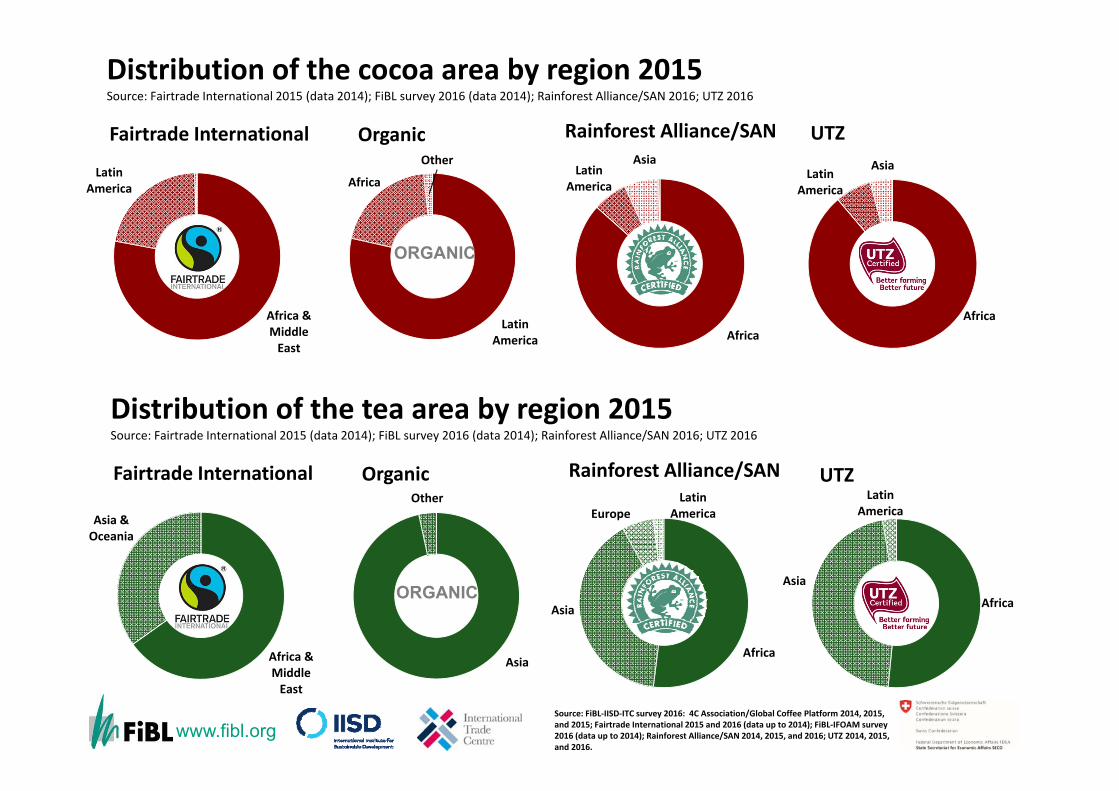

Africa & Middle East

Latin America

Fairtrade International

Africa

Latin America

Asia

UTZ

Latin America

Africa

Other

Organic

Africa

Latin America

Asia

Rainforest Alliance/SAN

Distribution of the cocoa area by region 2015Source: Fairtrade International 2015 (data 2014); FiBL survey 2016 (data 2014); Rainforest Alliance/SAN 2016; UTZ 2016

Africa & Middle East

Asia & Oceania

Fairtrade International

Africa

Asia

Latin America

UTZ

Asia

Other

Organic

Africa

Asia

EuropeLatin

America

Rainforest Alliance/SAN

Distribution of the tea area by region 2015Source: Fairtrade International 2015 (data 2014); FiBL survey 2016 (data 2014); Rainforest Alliance/SAN 2016; UTZ 2016

ORGANIC

ORGANIC

Source: FiBL‐IISD‐ITC survey 2016: 4C Association/Global Coffee Platform 2014, 2015, and 2015; Fairtrade International 2015 and 2016 (data up to 2014); FiBL‐IFOAM survey 2016 (data up to 2014); Rainforest Alliance/SAN 2014, 2015, and 2016; UTZ 2014, 2015, and 2016.

www.fibl.org

The organic and the Fairtrade markets

› Since 2000, when the global market for organic food was at approximately 16.5 billion euros (Organic Monitor), it has more than quadrupled, reaching approx. 75 euros in 2015. According to Fairtrade International, global Fairtrade sales reached 7.3 billion euros 2015.

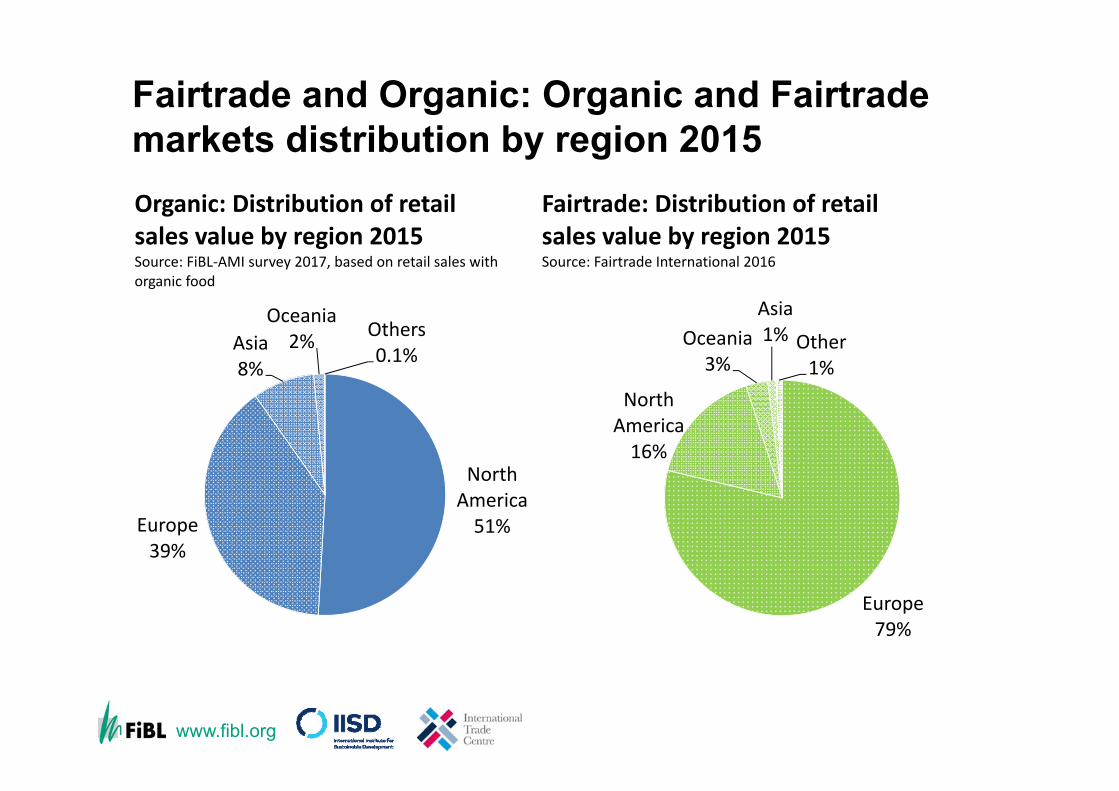

› About 90 percent of the sales of organic and Fairtrade products are in Europe and North America. North America is the largest organic market, with over 50 percent of the global organic market, while Europe represents almost 80 percent of Fairtrade retail sales.

› The variety of Fairtrade products is smaller than that of organic products. Currently, consumers can find almost all food products in organic quality, while the scope of Fairtrade products is smaller.

› When considering processed foods, another big difference emerges between organic and Fairtrade products. For a processed product to be labelled as organic, at least 95 percent of the ingredients of the final product need to be from organic-certified raw materials (IFOAM – Organics International 2014). In comparison, for a Fairtrade composite food product to carry the Fairtrade label, the product needs to have at least 50 percent of its ingredients Fairtrade-certified (Fairtrade International 2003).

11

www.fibl.org

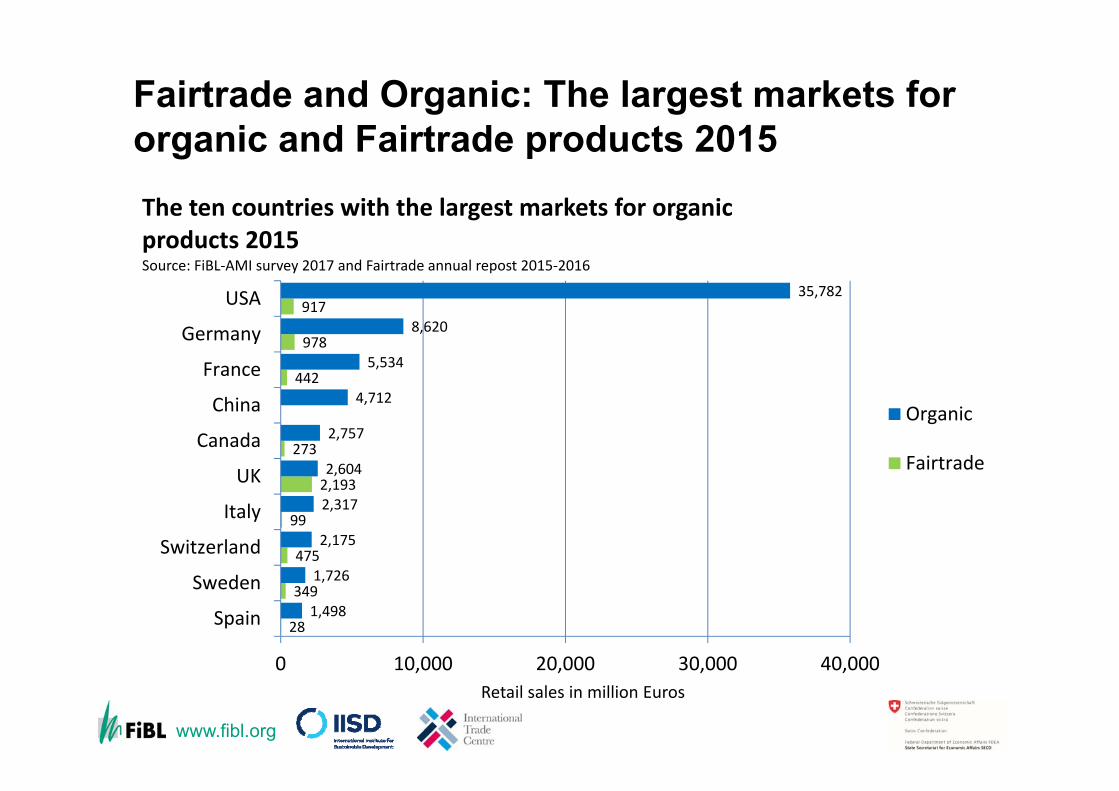

Fairtrade and Organic: The largest markets for organic and Fairtrade products 2015

12

28

349

475

99

2,193

273

442

978

917

1,498

1,726

2,175

2,317

2,604

2,757

4,712

5,534

8,620

35,782

0 10,000 20,000 30,000 40,000

Spain

Sweden

Switzerland

Italy

UK

Canada

China

France

Germany

USA

Retail sales in million Euros

The ten countries with the largest markets for organic products 2015Source: FiBL‐AMI survey 2017 and Fairtrade annual repost 2015‐2016

Organic

Fairtrade

www.fibl.org

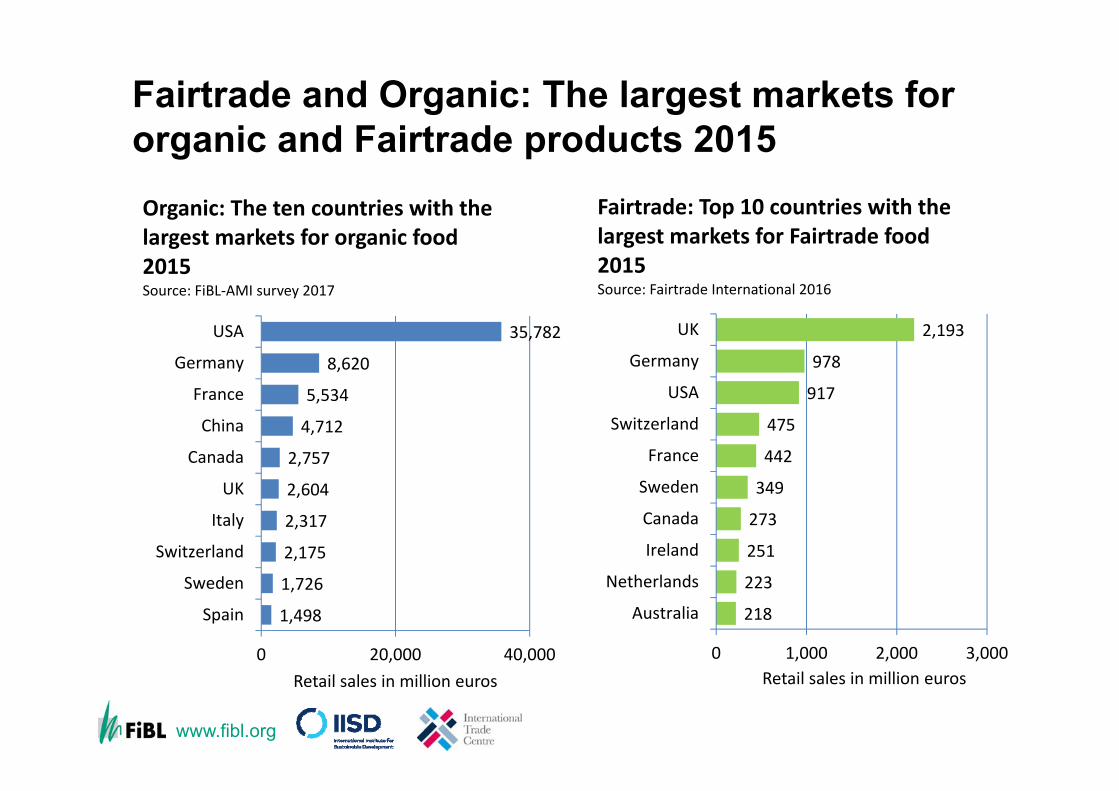

1,498

1,726

2,175

2,317

2,604

2,757

4,712

5,534

8,620

35,782

0 20,000 40,000

Spain

Sweden

Switzerland

Italy

UK

Canada

China

France

Germany

USA

Retail sales in million euros

Organic: The ten countries with the largest markets for organic food 2015Source: FiBL‐AMI survey 2017

218

223

251

273

349

442

475

917

978

2,193

0 1,000 2,000 3,000

Australia

Netherlands

Ireland

Canada

Sweden

France

Switzerland

USA

Germany

UK

Retail sales in million euros

Fairtrade: Top 10 countries with the largest markets for Fairtrade food 2015Source: Fairtrade International 2016

Fairtrade and Organic: The largest markets for organic and Fairtrade products 2015

www.fibl.org

North America51%Europe

39%

Asia8%

Oceania2% Others

0.1%

Organic: Distribution of retail sales value by region 2015Source: FiBL‐AMI survey 2017, based on retail sales with organic food

Global market: Distribution of total retail sales value by single markets (total: 47.8 billion) Euros 2013

Europe79%

North America16%

Oceania3%

Asia1% Other

1%

Fairtrade: Distribution of retail sales value by region 2015Source: Fairtrade International 2016

Fairtrade and Organic: Organic and Fairtrade markets distribution by region 2015

www.fibl.org

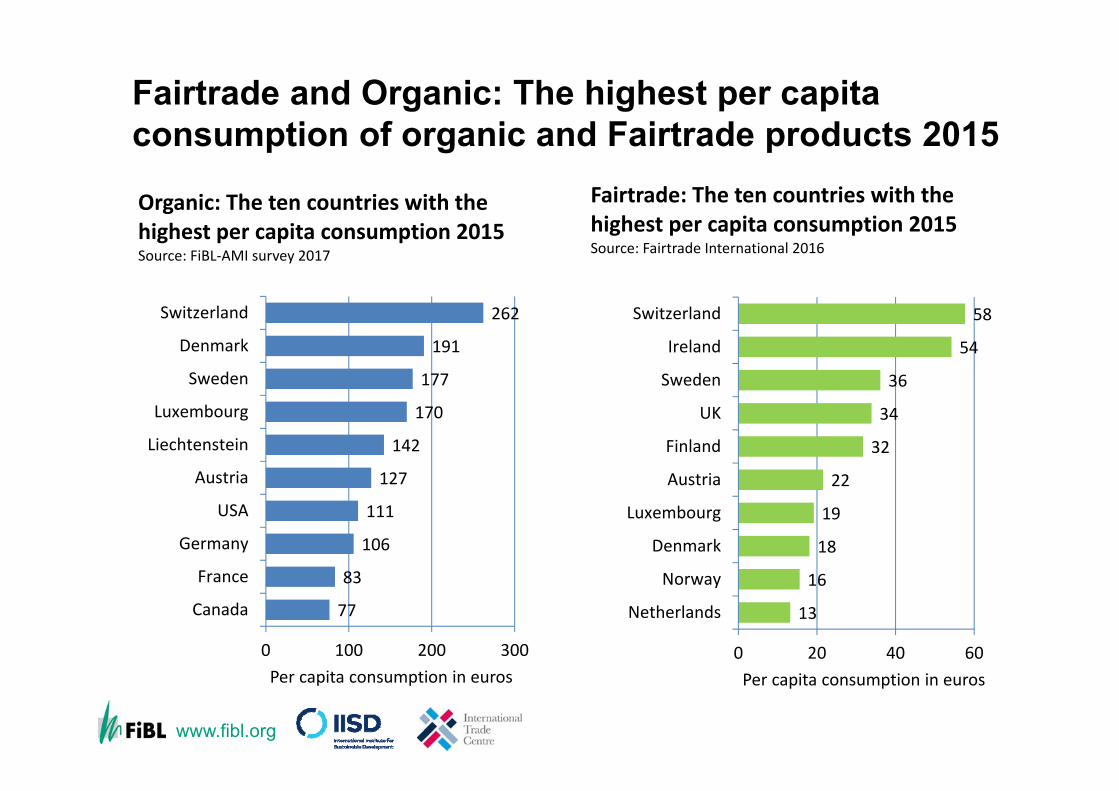

77

83

106

111

127

142

170

177

191

262

0 100 200 300

Canada

France

Germany

USA

Austria

Liechtenstein

Luxembourg

Sweden

Denmark

Switzerland

Per capita consumption in euros

Organic: The ten countries with the highest per capita consumption 2015Source: FiBL‐AMI survey 2017

The ten countries with the largest per capita consumption for 2013

13

16

18

19

22

32

34

36

54

58

0 20 40 60

Netherlands

Norway

Denmark

Luxembourg

Austria

Finland

UK

Sweden

Ireland

Switzerland

Per capita consumption in euros

Fairtrade: The ten countries with the highest per capita consumption 2015Source: Fairtrade International 2016

Fairtrade and Organic: The highest per capita consumption of organic and Fairtrade products 2015

www.fibl.org

The State of Sustainable MarketsStatistics and Emerging Trends 2015

16

› Julia Lernoud, Jason Potts, Gregory Sampson, Vivek Voora, Helga Willer and Joseph Wozniak (2015): The State of Sustainable Markets – Statistics and Emerging Trends 2015. ITC, Geneva.

› http://www.intracen.org/publication/The-State-of-Sustainable-Markets/

› The 2017 edition of “The State of Sustainable Markets” will be launched at the 2017 ISEAL Conference, Zurich, June 2017

www.fibl.org

Conclusions

› Most of the VSS are growing very fast reaching high growth rates, but organic still has the lead with the most hectares certified worldwide

› Most of the VSS focus on a small range of products, and organic covers almost the whole product range

› Multiple certification takes place in almost all of the selected commodities, which makes it challenging to avoid double counting

› Market data: retail sales and international trade data is not available for most of the VSS

17