global packaging: sizing demand and opportunities for pet bottles

TRANSCRIPT

GLOBAL PACKAGING:

SIZING DEMAND AND OPPORTUNITIES FOR PET BOTTLES

ROSEMARIE DOWNEY

GLOBAL HEAD OF PACKAGING RESEARCH

© Euromonitor International

2

• Global provider of Strategic Market Intelligence

• 12 Regional offices - 800+ analysts in 80 countries

• Cross-country comparable data and analysis

• Consumer focused industries, countries and

consumers

• 5 - 10 year forecasts with matching trend analysis

• All retail channels covered

• Subscription services, reports and consulting

About Euromonitor International

EUROMONITOR INTERNATIONAL London

Singapore

Shanghai

Dubai

Vilnius

Cape Town

Santiago

Tokyo

Sydney

Chicago

Bangalore

Sao Paulo

PASSPORT PACKAGING

GLOBAL MARKETPLACE FOR PET

2015 VIEW ON OPPORTUNITIES FOR PET

© Euromonitor International

4

Vietnam

Saudi Arabia

Colombia

Packaging Coverage

EUROMONITOR INTERNATIONAL

7 Industries 54 countries

Alcoholic Drinks

Beauty & Personal Care

Dog & Cat Food

Food

Home Care

Hot Drinks

Soft Drinks

3 new researched countries:

Pack sizes

26 closure types

7 multipack types

Returnables

40 pack types

… with detail on

© Euromonitor International

5 EUROMONITOR INTERNATIONAL

Metal Beverage Can Can be drunk from directly

PET Bottle Brick Liquid Carton Square shape

Flexible Aluminium /Plastic

Common in ground coffee

Flexible plastic Tea carton overwrap

and coffee pods

Folding Cartons Common in tea

HDPE Bottle Cloudy look

Aluminium/Plastic Pouches

Mainly for children juice drinks

Thin Wall Containers Especially in Asia

40 Pack Types and the Most Popular for Non-alcoholic Drinks are…

Glass Bottle

© Euromonitor International

6

Key Closure Types for Drinks

EUROMONITOR INTERNATIONAL

-3

0

3

6

9

1

5

25

125

625

PlasticScrew

Closures

Metal Crowns

MetalScrew

Closures

LiquidCarton

Closures

Corks Peel-OffLidding*

BeveragePush-Pull

BeverageFlip-Top

Metal LugClosures

Zip/PressClosures

% C

AG

R (

20

15-2

02

0)

Vo

lum

e in

bil

lio

n u

nit

s

Core Closure Types for Global Retail Beverages (2015-2020)

2015 Volume % CAGR 2015-2020

* Peel-Off Lidding includes Peel-Off Foil, Peel-Off Plastic and Peel-Off Paper

PASSPORT PACKAGING

GLOBAL MARKETPLACE FOR PET

2015 VIEW ON OPPORTUNITIES FOR PET

© Euromonitor International

8

0

1

2

3

4

0

500

1,000

1,500

2,000

Food Drinks Tobacco Beauty &Personal

Care

Tissue &Hygiene

HomeCare

Dog & CatFood

% C

AG

R

Bil

lio

n U

nit

s

Billion Units 2015 % CAGR 2015-2019

Global Retail Packaging by Industry in 2015 and Growth to 2019

Food and Drink: Core to Global Packaging Demand and Growing

8% Food 4.3 units of retail packaging sold in 2015

73% of packaging in food

and drinks alone

37% share of drinks

held by PET

Tr

illi

on

GLOBAL MARKETPLACE FOR PET

© Euromonitor International

9

Clear Importance of Plastics Packaging in Food and Drink

0 200 400 600 800 1000 1200

Flexible Aluminium/Plastic

Metal Food Cans

HDPE Bottles

Flexible Paper

Folding Cartons

Liquid Cartons

Thin Wall Plastic Containers

Metal Beverage Cans

Glass Bottles

PET Bottles

Flexible Plastic

Billion Units

Global Leading Pack Types for Food and Drink in 2015 and Growth 2015-2019

2015 Billion Units

2015-2019 unit volume growth

4.2% CAGR to 2019

4% CAGR to 2019

3.2% CAGR to 2019

3.1% CAGR to 2019

+80 bn

0.8% CAGR to 2019

2.2% CAGR to 2019

GLOBAL MARKETPLACE FOR PET

© Euromonitor International

10

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

10%

40%

45%

50%

55%

60%

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

% a

nn

ua

l g

row

th

% P

ET

Bo

ttle

in

So

ft D

rin

ks

PET Bottles vs. Total Packaging Growth in Soft Drinks

PET % Total Packaging Growth % PET Bottle Growth

Global Evolution and Impact of PET in Soft Drinks Remains Strong

GLOBAL MARKETPLACE FOR PET

#1 55% of all soft

drinks sold in 2014 through retail were

in PET bottles

4.3% growth for PET bottles in 2015

175 growth for PET

bottles since 2004

Bil

lio

n

© Euromonitor International

11

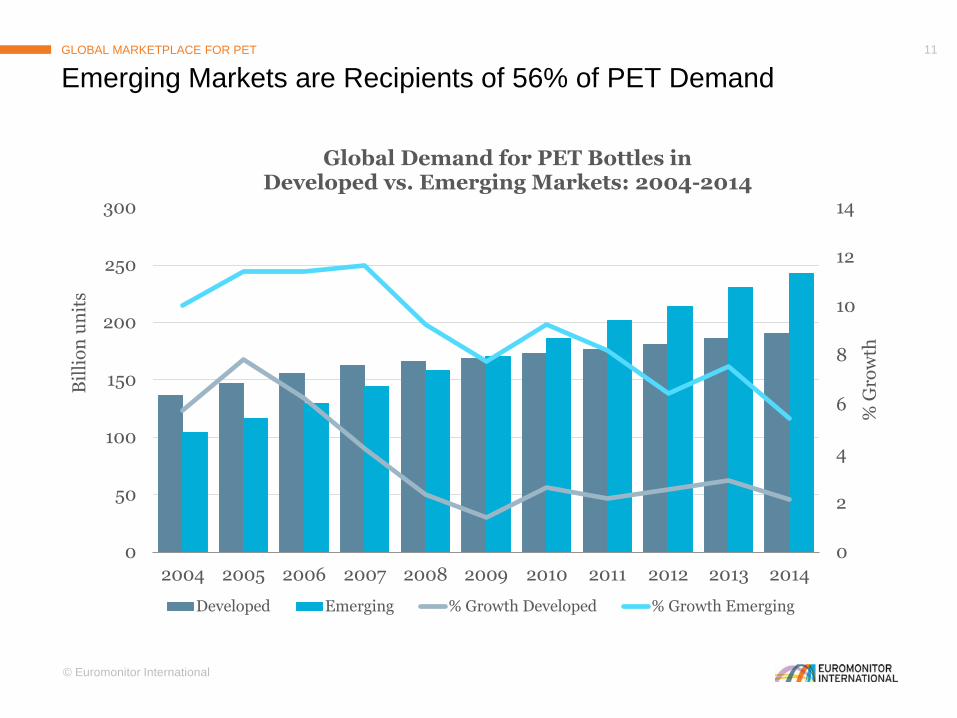

Emerging Markets are Recipients of 56% of PET Demand

GLOBAL MARKETPLACE FOR PET

0

2

4

6

8

10

12

14

0

50

100

150

200

250

300

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

% G

row

th

Bil

lio

n u

nit

s

Global Demand for PET Bottles in Developed vs. Emerging Markets: 2004-2014

Developed Emerging % Growth Developed % Growth Emerging

43%

© Euromonitor International

12

-5 5 15 25 35 45

Russia

Thailand

Japan

Mexico

Vietnam

Brazil

Indonesia

India

USA

China

2015-2019 billion units growth

Top 10 Countries for PET Bottle Volume Growth 2015-2019, % CAGR

+ 39 billion units

Where to Go for Best PET Volume Growth

% CAGR 2015-19

+ 39 billion units

11%

6%

2%

7%

Billion Units

GLOBAL MARKETPLACE FOR PET

PASSPORT PACKAGING

GLOBAL MARKETPLACE FOR PET

2015 VIEW ON OPPORTUNITIES FOR PET

© Euromonitor International

14

2015 Key Drivers Shaping PET Performance and Potential

2015 VIEW ON OPPORTUNITIES FOR PET

Emerging Markets for Biggest Volume Gains

Polarisation in Pack Sizing: Rightsizing

Premium and Value-add Opportunities

Consumer Health and Wellness Preferences

Innovation to Support Brand Presence

© Euromonitor International

15

PET Position in Key Categories Shows Ample Opportunity for Growth

2015 VIEW ON OPPORTUNITIES FOR PET

-1

0

1

2

3

4

5

6

-50

0

50

100

150

200

250

300

% C

AG

R 2

015

-20

19

Bil

lio

n u

nit

s

PET Bottle Penetration in Key Categories 2015 and Prospects 2015-2019

Billion units 2015 2015 Other Pack Types % CAGR 2015-2019

PET strength in bottled water versus other pack types and good

for onward growth

PET holds opportunities in Tea, Oils and Dairy

© Euromonitor International

16

2005-2015: Bottled water sales dynamic

To represent just under half of all soft drinks volumes by 2019

0

50

100

150

200

250

300

350

400

2005 2010 2015 2019

Bil

lio

n l

itr

es

Global Volumes of Still Bottled Water vs. Other Soft

Drinks 2005-2019

Still Bottled water All Other Soft Drinks

Still Water’s Absolute Importance to Consumer Beverage Preferences

2015 VIEW ON OPPORTUNITIES FOR PET

Value-add expansion to be pursued

Additional Consumption of PET in Bottled Water by Type

2015-2019

Carbonated Bottled Water Flavoured Bottled Water

Functional Bottled Water Still Bottled Water

+50bn units

30%

45%

35%

41%

© Euromonitor International

17

Canada: Fastest growth country for sparkling water 2014-15 – 1 litre

Australia: Mount Franklin re-design, Summer 2015

US: Bullet design caffeinated water – 500ml

China: Heritage of source and design from Nongfu Spring

Desire for Added Benefits via Carbonation, Quality and Weight

Spain: Showing recovery – 1.2 litre

2015 VIEW ON OPPORTUNITIES FOR PET

© Euromonitor International

18

Healthy Option for on The Go…

…and Family Value Too

0

2

4

6

8

10

12

0

1

2

3

4

5

6

% g

ro

wth

20

14-1

5

Ad

dit

ion

al

co

ns

um

pti

on

(b

illi

on

un

its

)

Global Bottled Water: PET Pack Size Performance

2014-2015

PET bottle growth, billion units % growth 2014-15

Polarisation in Pack Sizing Increasingly Apparent in Still Water

2015 VIEW ON OPPORTUNITIES FOR PET

© Euromonitor International

19

-2

0

2

4

6

8

10

-100

0

100

200

300

400

500

600

% g

ro

wth

20

14-2

015

Mil

lio

n u

nit

s g

ro

wth

Global Carbonates: PET Pack Size Performance

2014-2015

2014-15 PET bottle growth (mn units) % growth 2014-15

Reduce Sweetness and Size

In Carbonates, Control over Sugar Intake Sees Shift to Smaller Sizes

2015 VIEW ON OPPORTUNITIES FOR PET

Variation in Smaller Sizes

1. Fits lifestyle 2. Affordable 3. Procures value and volume gains

Canada

591ml->500ml

China

300ml

Various

500ml

© Euromonitor International

20

0

20

40

60

80

100

120

Glass Bottles Metal Beverage Cans PET Bottles

Carbonates Packaging by Core Pack Type 2010-2019

Bil

lio

n U

nit

s

Flavour and Feel Factors, Room for Big Value for Money Lines Too

2015 VIEW ON OPPORTUNITIES FOR PET

Natural Flavour

Visual Impact

Value for Money

© Euromonitor International

21

PET Bottle Growth in Ready-to-Drink Tea by Region

Asia Pacific Latin America North America

Eastern Europe Western Europe Australasia

Middle East/Africa

Innovation in Natural Tea Flavours Hits Premium Health Note

2015 VIEW ON OPPORTUNITIES FOR PET

+ 8 billion bottles

2015-2019

Gerolsteiner

Germany

750ml

April 2015

Pepsi-Lipton Tea Netherlands

500ml

April 2015

© Euromonitor International

22

0

2

4

6

8

10

12

14

16

18

Oils andFats

DrinkingMilk

Products

TableSauces

Yoghurt

Bil

lio

n U

nit

s

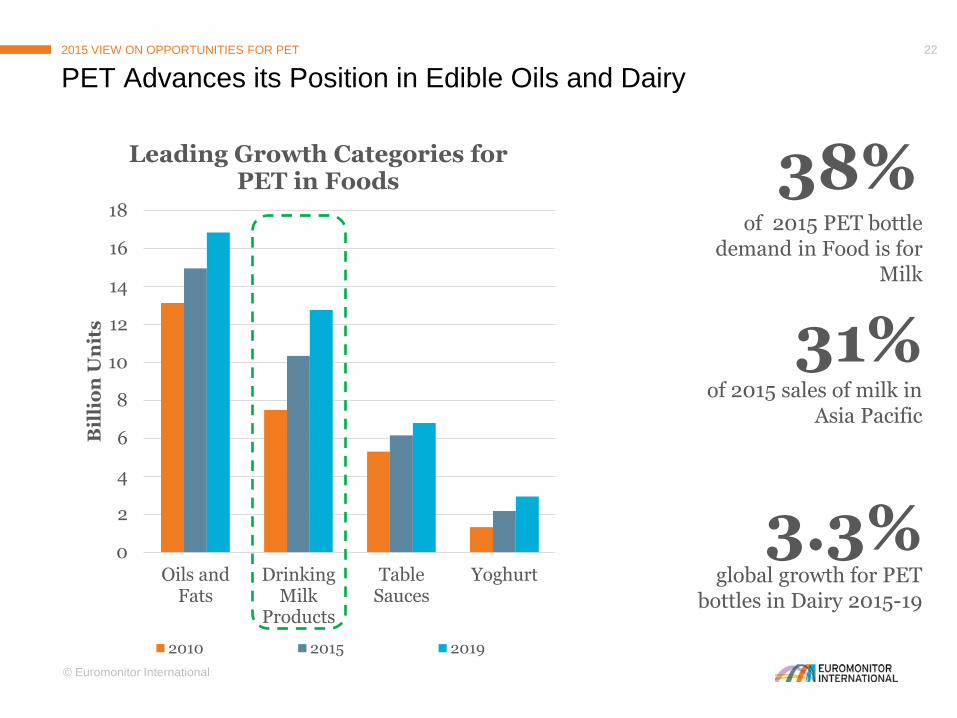

Leading Growth Categories for PET in Foods

2010 2015 2019

PET Advances its Position in Edible Oils and Dairy

2015 VIEW ON OPPORTUNITIES FOR PET

31% of 2015 sales of milk in

Asia Pacific

3.3% global growth for PET

bottles in Dairy 2015-19

38% of 2015 PET bottle

demand in Food is for Milk

© Euromonitor International

23

Asia Speciality Drink

Bottled Water (Still, Carbonated, Flavoured, Functional)

Carbonates (Cola and Non-Cola)

Juice (100% juice, Up to 24% juice and Nectar juice)

RTD Coffee

RTD Tea (Still and Carbonates)

Sports and Energy Drinks

Product Definitions for Soft Drinks

APPENDIX

THANK YOU FOR LISTENING Rosemarie Downey

Global Head of Packaging Research

www.euromonitor.com