gemstone lapidary.pdf

DESCRIPTION

reportTRANSCRIPT

Pre-Feasibility Study

Prime Minister’s Small Business Loan Scheme (Gemstone Lapidary)

Small and Medium Enterprises Development Authority

Ministry of Industries & Production Government of Pakistan

www.smeda.org.pk

HEAD OFFICE 4th Floor, Building No. 3, Aiwan e Iqbal, Egerton Road,

Lahore Tel 92 42 111 111 456, Fax 92 42 36304926-7

REGIONAL OFFICE PUNJAB

REGIONAL OFFICE SINDH

REGIONAL OFFICE KPK

REGIONAL OFFICE BALOCHISTAN

3rd Floor, Building No. 3,

Aiwan e Iqbal, Egerton Road Lahore,

Tel: (042) 111-111-456 Fax: (042)6304926-7

5TH Floor, Bahria Complex II, M.T. Khan Road,

Karachi. Tel: (021) 111-111-456

Fax: (021) 5610572 [email protected]

Ground Floor State Life Building

The Mall, Peshawar. Tel: (091) 9213046-47

Fax: (091) 286908 [email protected]

Bungalow No. 15-A Chaman Housing Scheme

Airport Road, Quetta. Tel: (081) 831623, 831702

Fax: (081) 831922 [email protected]

September 2013

Pre-Feasibility Study Gemstone Lapidary

Table of Contents 1. DISCLAIMER .......................................................................................................................................... 2

2. PURPOSE OF THE DOCUMENT ......................................................................................................... 3

3. INTRODUCTION TO SMEDA .............................................................................................................. 3

4. INTRODUCTION TO SCHEME ........................................................................................................... 4 5. EXECUTIVE SUMMARY ...................................................................................................................... 4

6. BRIEF DESCRIPTION OF PROJECT & PRODUCT ........................................................................ 4

7. CRITICAL FACTORS ............................................................................................................................ 5

8. INSTALLED & OPERATIONAL CAPACITY .................................................................................... 5

9. GEOGRAPHICAL POTENTIAL FOR INVESTMENT/SUITABLE LOCATIONS ........................ 5

10. POTENTIAL TARGET MARKETS/CITIES ................................................................................. 6 11. PRODUCTION PROCESS FLOW .................................................................................................. 7

12. PROJECT COST SUMMARY ......................................................................................................... 7 12.1. PROJECT ECONOMICS .................................................................................................................................. 7 12.2. PROJECT FINANCING ................................................................................................................................... 8 12.3. PROJECT COST ............................................................................................................................................. 8 12.4. SPACE REQUIREMENT.................................................................................................................................. 8 12.5. MACHINERY AND EQUIPMENT ..................................................................................................................... 9 12.6. RAW MATERIAL REQUIREMENTS .............................................................................................................. 10 12.7. ROUGH GEMSTONES .................................................................................................................................. 10 12.8. LAPIDARY CONSUMABLES INVENTORY ..................................................................................................... 10 12.9. HUMAN RESOURCE REQUIREMENT ........................................................................................................... 11 12.10. REVENUE GENERATION ............................................................................................................................. 11 12.11. OTHER COSTS............................................................................................................................................ 11

13. CONTACTS ...................................................................................................................................... 12

14. ANNEXURE ..................................................................................................................................... 13 14.1. INCOME STATEMENT ................................................................................................................................. 13 14.2. STATEMENT OF CASH FLOW ............................................................................................................. 14 14.3. BALANCE SHEET .................................................................................................................................. 15 14.4. USEFUL PROJECT MANAGEMENT TIPS ........................................................................................... 16 14.5. USEFUL LINKS ...................................................................................................................................... 17

15. KEY ASSUMPTIONS ..................................................................................................................... 19

September 2013

1

Pre-Feasibility Study Gemstone Lapidary

1. DISCLAIMER This information memorandum is to introduce the subject matter and provide a general idea and information on the said matter. Although, the material included in this document is based on data/information gathered from various reliable sources; however, it is based upon certain assumptions which may differ from case to case. The information has been provided on as is where is basis without any warranties or assertions as to the correctness or soundness thereof. Although, due care and diligence has been taken to compile this document, the contained information may vary due to any change in any of the concerned factors, and the actual results may differ substantially from the presented information. SMEDA, its employees or agents do not assume any liability for any financial or other loss resulting from this memorandum in consequence of undertaking this activity. The contained information does not preclude any further professional advice. The prospective user of this memorandum is encouraged to carry out additional diligence and gather any information which is necessary for making an informed decision, including taking professional advice from a qualified consultant/technical expert before taking any decision to act upon the information.

For more information on services offered by SMEDA, please contact our website: www.smeda.org.pk

September 2013

2

Pre-Feasibility Study Gemstone Lapidary

2. PURPOSE OF THE DOCUMENT The objective of the pre-feasibility study is primarily to facilitate potential entrepreneurs in project identification for investment. The project pre-feasibility may form the basis of an important investment decision and in order to serve this objective, the document/study covers various aspects of project concept development, start-up, and production, marketing, finance and business management.

The purpose of this document is to facilitate potential investors in Gemstone Lapidary by providing them with a general understanding of the business with the intention of supporting potential investors in crucial investment decisions.

The need to come up with pre-feasibility reports for undocumented or minimally documented sectors attains greater imminence as the research that precedes such reports reveal certain thumb rules; best practices developed by existing enterprises by trial and error, and certain industrial norms that become a guiding source regarding various aspects of business set-up and it’s successful management.

Apart from carefully studying the whole document one must consider critical aspects provided later on, which form basis of any Investment Decision.

3. INTRODUCTION TO SMEDA The Small and Medium Enterprises Development Authority (SMEDA) was established in October 1998 with an objective to provide fresh impetus to the economy through development of Small and Medium Enterprises (SMEs).

With a mission "to assist in employment generation and value addition to the national income, through development of the SME sector, by helping increase the number, scale and competitiveness of SMEs" , SMEDA has carried out ‘sectoral research’ to identify policy, access to finance, business development services, strategic initiatives and institutional collaboration and networking initiatives.

Preparation and dissemination of prefeasibility studies in key areas of investment has been a successful hallmark of SME facilitation by SMEDA.

Concurrent to the prefeasibility studies, a broad spectrum of business development services is also offered to the SMEs by SMEDA. These services include identification of experts and consultants and delivery of need based capacity building programs of different types in addition to business guidance through help desk services.

September 2013

3

Pre-Feasibility Study Gemstone Lapidary

4. INTRODUCTION TO SCHEME Prime Minister’s ‘Small Business Loans Scheme’, for young entrepreneurs, with an allocated budget of Rs. 5.0 Billion for the year 2013-14, is designed to provide subsidised financing at 8% mark-up per annum for one hundred thousand (100,000) beneficiaries, through designated financial institutions, initially through National Bank of Pakistan (NBP) and First Women Bank Ltd. (FWBL).

Small business loans with tenure upto 7 years, and a debt : equity of 90 : 10 will be disbursed to SME beneficiaries across Pakistan, covering; Punjab, Sindh, Khyber Pakhtunkhwah, Balochistan, Gilgit Baltistan, Azad Jammu &Kashmir and Federally Administered Tribal Areas (FATA).

5. EXECUTIVE SUMMARY While, Lahore & Karachi with its large Gold and Gem studded jewellery making industry are suitable locations,Gems Lapidaryis proposed to be located at Peshawar since major trade/export is taking place in this city. Within Peshawar, Namak Mandi area is preferable as large Gem Cluster exists here. These jewelry markets are the main customers of the cut and polished gemstones. The proposed unit will process rough Gemstones, initially semi precious gems stones like Aquamarine, Peridot, Tourmaline etc. TheseGemstones mainly come from mines in Chitral, Mardan and Gilgit Baltistan in addition to gems from Afghanistan and other nearby locations.

Proposed unit will have the capacity to process 3,000 units (Cut & Polished Gemstones, (average 3carat weight per stone). In the first year of operation, the unit would run on 60% of the total production capacity which is processing 1,800 pieces.

The total cost of the project is Rs. 2.08 million, with capital cost of Rs. 1.19 million and operation cost of Rs. 0.89 million. Given the cost assumptions, IRR and payback are 37% and three yearsrespectively, thus making the project a profitable venture. The most critical considerations or factors for success of the project are:

1. Awareness about current market trends i.e the type of stone & type of cut required by the customers, which in this case are jewellers.

2. Availability of skilled labour.

6. BRIEF DESCRIPTION OF PROJECT & PRODUCT • Technology: This proposed unit with modern processing machines includ

faceting, cutting and polishing will produce cut and polished precious and semi-precious gem stones of both calibrated and non-calibrated types.

September 2013

4

Pre-Feasibility Study Gemstone Lapidary

• Location:The unit will be located in or near gems trading clusters such as Namak Mandi in Peshawar or Lahore and Karachi also where access to raw gemstones is easy.

• Product:The unit would initially process semi precious gem stones like Aquamarine, Tourmaline, Peridot etc which comes from Chitral and Northern areas.

• Target Market: An enormous export market for the Pakistani gemstones exists in Europe, USA, Middle East, Hong Kong, Taiwan, etc. It is of significance that the Gem industry and the Government of Pakistan are recognizing the potential for the local value addition and consequently import duty on lapidary equipment has been waived off.

• Employment:The proposed project will provide direct employment to 9 people.

• Profitability: Financial analysis shows the unit shall be profitable from the very first year of operation.

7. CRITICAL FACTORS The commercial viability of the Gemstone Lapidary depends primarily on the regular orders from the customers. Following are some other points that have to be ensured to make the business successful:

1. Awareness about current market trends i.e the type of stone & type of cuts required by the customers, which in this case are the jewellers.

2. Availability of skilled labour. 3. Timely delivery of orders 4. Availability of raw material (rough, uncut and unpolished gemstones).

8. INSTALLED & OPERATIONAL CAPACITY The installed capacity shall be 3,000 pieces per year. The project will run with approximately 60% capacity in first year of its operations with annual increase of 3% in production, constraint being skill levels.

9. GEOGRAPHICAL POTENTIAL FOR INVESTMENT/SUITABLE LOCATIONS

The most appropriate location for setting up a Gem lapidary would be Peshawar since major trade/export is taking place in this city. Within Peshawar, Namak Mandi area is preferable as large Gem Cluster exists here. Similarly, Lahore & Karachi with its large Gold and Gem studded jewellery making industry are other suitable locations. Chitral and Mingora as well as Gilgit and Skardu are also suitable locations for establishment of Gems Lapidary due to proximity of raw material sources.

September 2013

5

Pre-Feasibility Study Gemstone Lapidary

10. POTENTIAL TARGET MARKETS/CITIES Initially the products, mainly semi-precious nature gemstones will be processed by focusing on demand of the jewellery manufactures of Karachi, Lahore and Peshawar. After having reasonable domestic customers base, export market can be targeted provided exports standards are met. The main export markets for Pakistani Gemstone are U.A.E, United Kingdom, Thailand, Canada, Italy, China, Netherlands, Saudi Arabia, USA, Hong Kong and Germany

September 2013

6

Pre-Feasibility Study Gemstone Lapidary

11. PRODUCTION PROCESS FLOW The process of Lapidary includes grading, cutting and polishing of Gemstones. Raw stones are either purchased from the market or provided by the customers (Jewellers). Individual stone is then examined (graded) and cut into smaller stones along its major line of fracture and inclusions. The smaller pieces are then mounted on cutting tools, which are then faceted on faceting machines. The final operation involves polishing of the faceted stones. Polished stones are then delivered to the customers or sold in the market. 12. PROJECT COST SUMMARY A detailed financial model has been developed to analyze the commercial viability of Gemstone Lapidary under the Prime Minister’s Small Business Loan Scheme. Various cost and revenue related assumptions along with results of the analysis are outlined in this section.

12.1. PROJECT ECONOMICS A target processing and production of 3000 units (cut & polished gemstones) whereby units processed and produced by Gemstone lapidary in year one will be around 1800 units (cut & polished Gemstones) running at 60% production capacity. The following table shows internal rates of return and payback period.

Table 1 - Project Economics Description Details

Internal Rate of Return (IRR) 37% Payback Period (yrs) 3 years Net Present Value (NPV) 4,671,546

Some of the critical factors influencing the commercial viability of this Gemstone Lapidary depend primarily on the regular orders from the customers and supply of rough Gems from mines. Apart from this awareness about current market trends i.e. the type

RawStones of Customers

Purchaseof RawStones

Grading Cutting Polishing

DeliverytoCustomers

SaletoMarket

September 2013

7

Pre-Feasibility Study Gemstone Lapidary

of stone & type of cut required by the consumers, delivering orders on time, availability of raw material (gemstones), reliability and contacts with the traders proximity to the Gem cluster for easy availability of raw material must be taken care off for smooth running of the project A return on the investment and profitability of the project is highly dependent on the above mentioned factors.

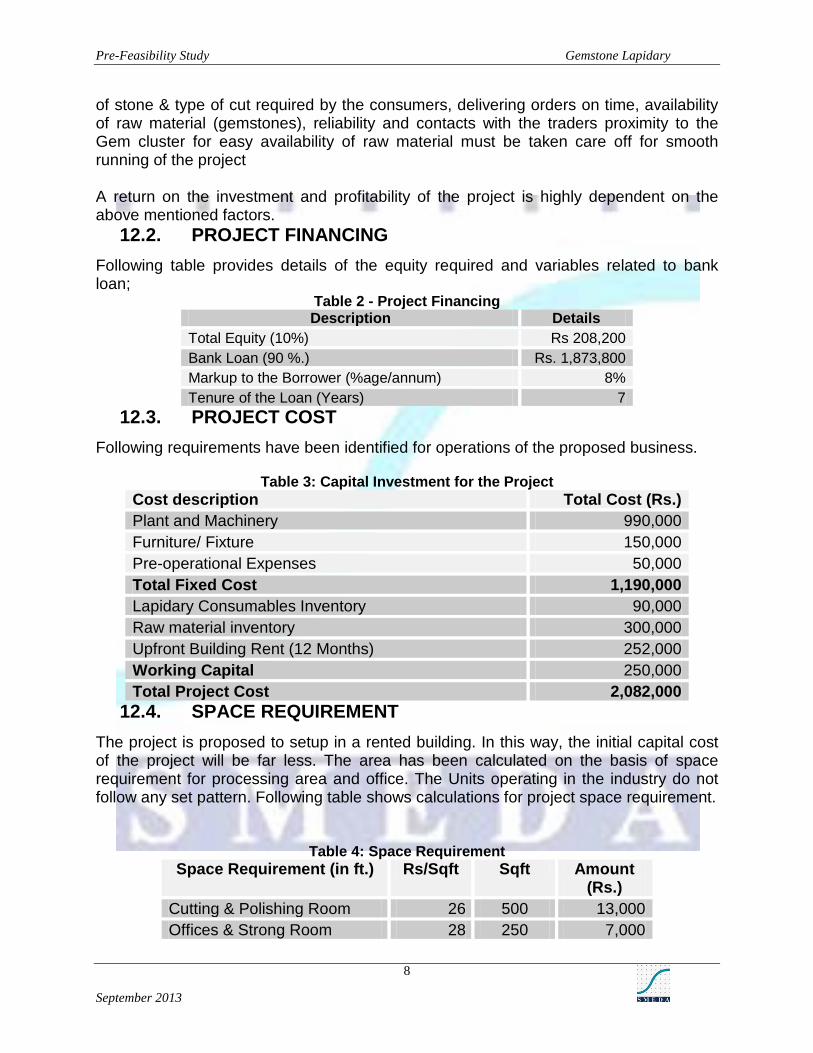

12.2. PROJECT FINANCING Following table provides details of the equity required and variables related to bank loan;

Table 2 - Project Financing Description Details

Total Equity (10%) Rs 208,200 Bank Loan (90 %.) Rs. 1,873,800 Markup to the Borrower (%age/annum) 8% Tenure of the Loan (Years) 7

12.3. PROJECT COST Following requirements have been identified for operations of the proposed business.

Table 3: Capital Investment for the Project

Cost description Total Cost (Rs.) Plant and Machinery 990,000 Furniture/ Fixture 150,000 Pre-operational Expenses 50,000 Total Fixed Cost 1,190,000 Lapidary Consumables Inventory 90,000 Raw material inventory 300,000 Upfront Building Rent (12 Months) 252,000 Working Capital 250,000 Total Project Cost 2,082,000

12.4. SPACE REQUIREMENT The project is proposed to setup in a rented building. In this way, the initial capital cost of the project will be far less. The area has been calculated on the basis of space requirement for processing area and office. The Units operating in the industry do not follow any set pattern. Following table shows calculations for project space requirement.

Table 4: Space Requirement Space Requirement (in ft.) Rs/Sqft Sqft Amount

(Rs.) Cutting & Polishing Room 26 500 13,000 Offices & Strong Room 28 250 7,000

September 2013

8

Pre-Feasibility Study Gemstone Lapidary

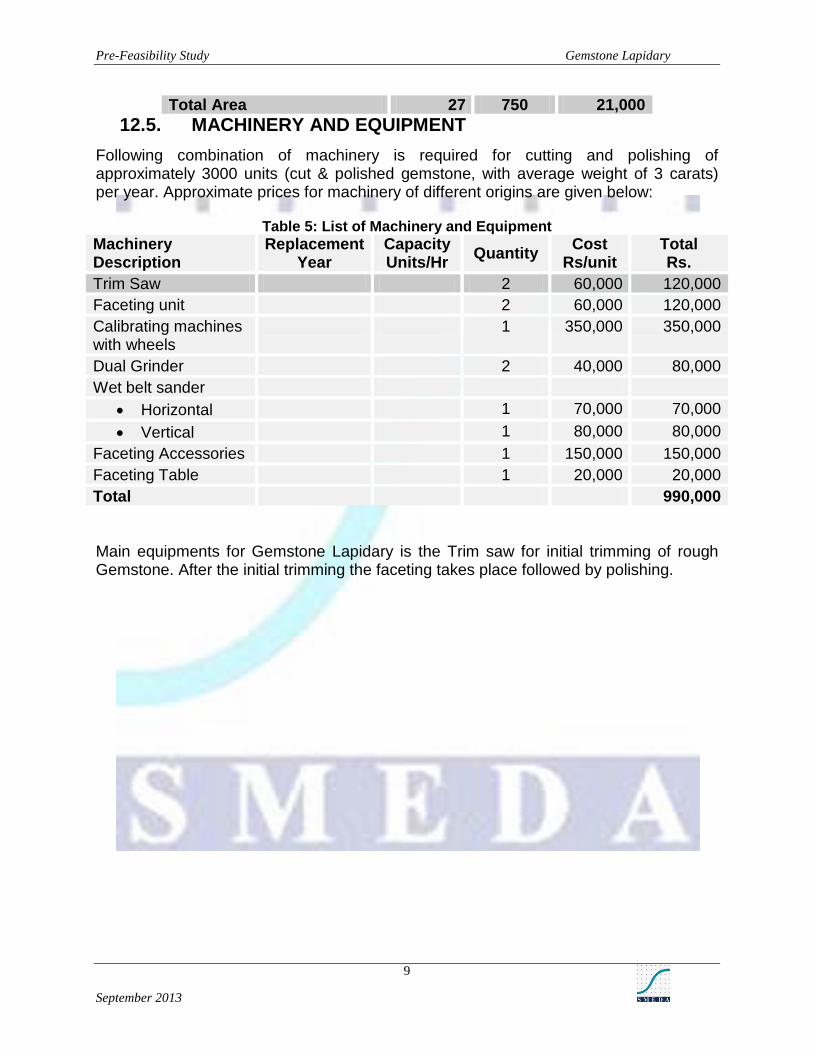

Total Area 27 750 21,000 12.5. MACHINERY AND EQUIPMENT

Following combination of machinery is required for cutting and polishing of approximately 3000 units (cut & polished gemstone, with average weight of 3 carats) per year. Approximate prices for machinery of different origins are given below:

Table 5: List of Machinery and Equipment

Machinery Description

Replacement Year

Capacity Units/Hr Quantity Cost

Rs/unit Total Rs.

Trim Saw 2 60,000 120,000 Faceting unit 2 60,000 120,000 Calibrating machines with wheels

1 350,000 350,000

Dual Grinder 2 40,000 80,000 Wet belt sander

• Horizontal 1 70,000 70,000 • Vertical 1 80,000 80,000

Faceting Accessories 1 150,000 150,000 Faceting Table 1 20,000 20,000 Total 990,000 Main equipments for Gemstone Lapidary is the Trim saw for initial trimming of rough Gemstone. After the initial trimming the faceting takes place followed by polishing.

September 2013

9

Pre-Feasibility Study Gemstone Lapidary

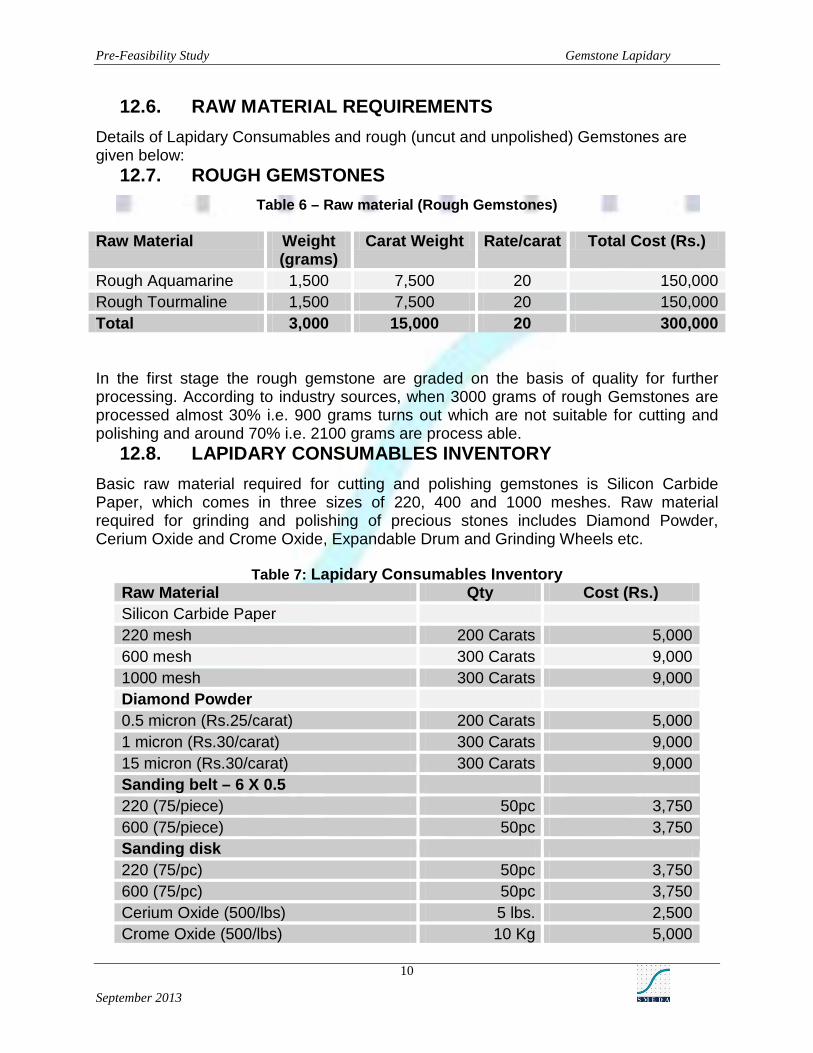

12.6. RAW MATERIAL REQUIREMENTS Details of Lapidary Consumables and rough (uncut and unpolished) Gemstones are given below:

12.7. ROUGH GEMSTONES Table 6 – Raw material (Rough Gemstones)

Raw Material Weight

(grams) Carat Weight Rate/carat Total Cost (Rs.)

Rough Aquamarine 1,500 7,500 20 150,000 Rough Tourmaline 1,500 7,500 20 150,000 Total 3,000 15,000 20 300,000 In the first stage the rough gemstone are graded on the basis of quality for further processing. According to industry sources, when 3000 grams of rough Gemstones are processed almost 30% i.e. 900 grams turns out which are not suitable for cutting and polishing and around 70% i.e. 2100 grams are process able.

12.8. LAPIDARY CONSUMABLES INVENTORY Basic raw material required for cutting and polishing gemstones is Silicon Carbide Paper, which comes in three sizes of 220, 400 and 1000 meshes. Raw material required for grinding and polishing of precious stones includes Diamond Powder, Cerium Oxide and Crome Oxide, Expandable Drum and Grinding Wheels etc.

Table 7: Lapidary Consumables Inventory

Raw Material Qty Cost (Rs.) Silicon Carbide Paper 220 mesh 200 Carats 5,000 600 mesh 300 Carats 9,000 1000 mesh 300 Carats 9,000 Diamond Powder 0.5 micron (Rs.25/carat) 200 Carats 5,000 1 micron (Rs.30/carat) 300 Carats 9,000 15 micron (Rs.30/carat) 300 Carats 9,000 Sanding belt – 6 X 0.5 220 (75/piece) 50pc 3,750 600 (75/piece) 50pc 3,750 Sanding disk 220 (75/pc) 50pc 3,750 600 (75/pc) 50pc 3,750 Cerium Oxide (500/lbs) 5 lbs. 2,500 Crome Oxide (500/lbs) 10 Kg 5,000

September 2013

10

Pre-Feasibility Study Gemstone Lapidary

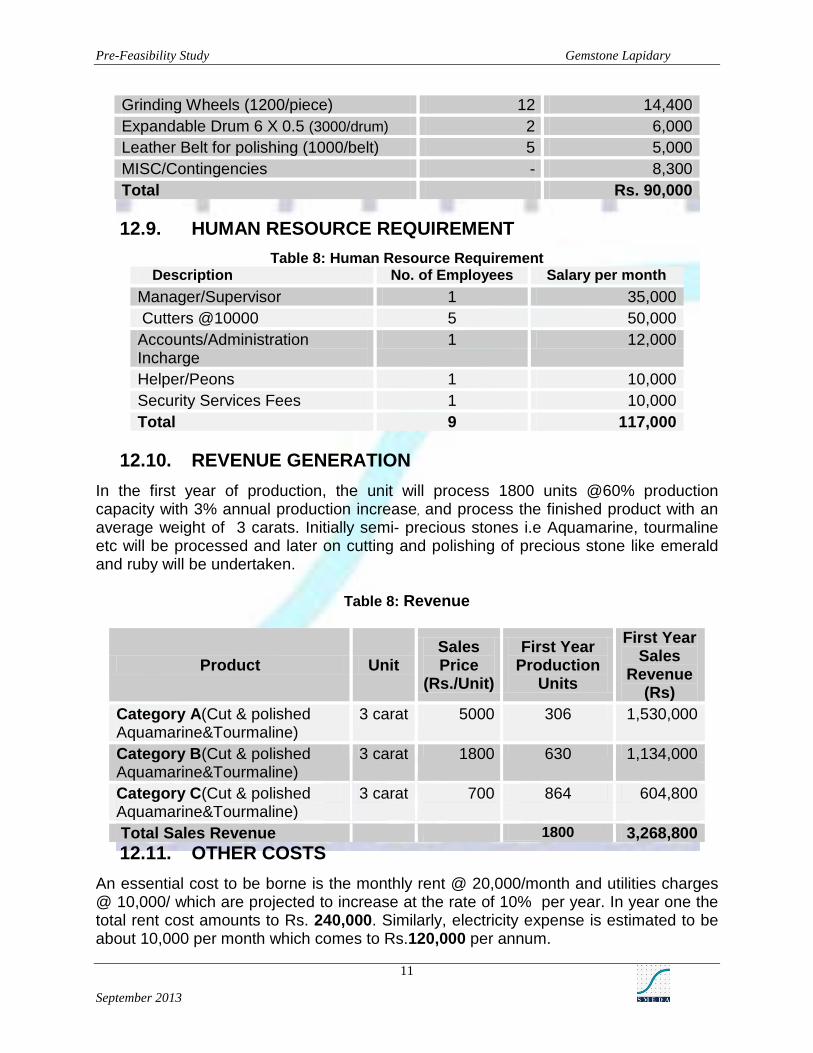

Grinding Wheels (1200/piece) 12 14,400 Expandable Drum 6 X 0.5 (3000/drum) 2 6,000 Leather Belt for polishing (1000/belt) 5 5,000 MISC/Contingencies - 8,300 Total Rs. 90,000

12.9. HUMAN RESOURCE REQUIREMENT

Table 8: Human Resource Requirement Description No. of Employees Salary per month

Manager/Supervisor 1 35,000 Cutters @10000 5 50,000 Accounts/Administration Incharge

1 12,000

Helper/Peons 1 10,000 Security Services Fees 1 10,000 Total 9 117,000

12.10. REVENUE GENERATION

In the first year of production, the unit will process 1800 units @60% production capacity with 3% annual production increase, and process the finished product with an average weight of 3 carats. Initially semi- precious stones i.e Aquamarine, tourmaline etc will be processed and later on cutting and polishing of precious stone like emerald and ruby will be undertaken.

Table 8: Revenue

Product Unit Sales Price

(Rs./Unit)

First Year Production

Units

First Year Sales

Revenue (Rs)

Category A(Cut & polished Aquamarine&Tourmaline)

3 carat 5000 306 1,530,000

Category B(Cut & polished Aquamarine&Tourmaline)

3 carat 1800 630 1,134,000

Category C(Cut & polished Aquamarine&Tourmaline)

3 carat 700 864 604,800

Total Sales Revenue 1800 3,268,800 12.11. OTHER COSTS

An essential cost to be borne is the monthly rent @ 20,000/month and utilities charges @ 10,000/ which are projected to increase at the rate of 10% per year. In year one the total rent cost amounts to Rs. 240,000. Similarly, electricity expense is estimated to be about 10,000 per month which comes to Rs.120,000 per annum.

September 2013

11

Pre-Feasibility Study Gemstone Lapidary

13. CONTACTS

1. Mr. Pervez Ellahi Malik

M/S Malik Gems International

Namak Mandi Peshawar

Ph# 0321-8592517

091-5252517

2. Mr. Afzal Khan

Lapidary Instructor

GJTMC, Peshawar

Ph# 091-5269253

3. Mr. Naveed Masood

Director GGIP,

Peshawar

Ph# 091-9213197

0333-9155097

September 2013

12

Pre-Feasibility Study Gemstone Lapidary

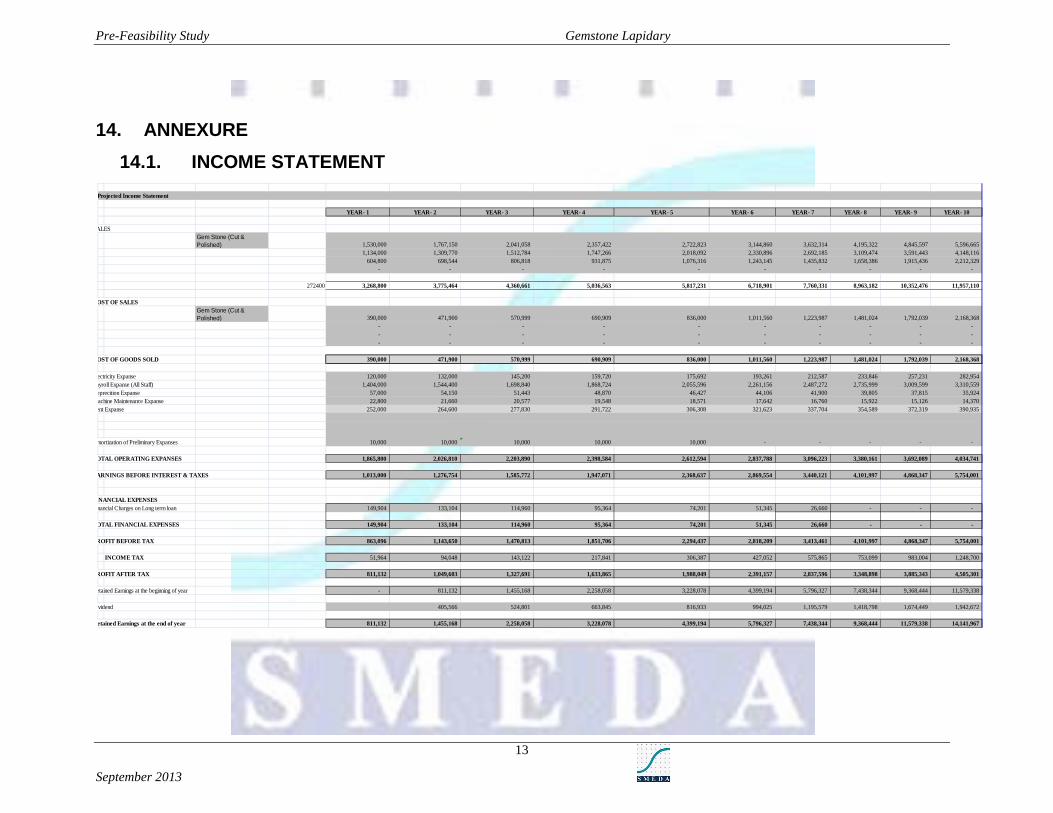

14. ANNEXURE 14.1. INCOME STATEMENT

Projected Income Statement

YEAR- 1 YEAR- 2 YEAR- 3 YEAR- 4 YEAR- 5 YEAR- 6 YEAR- 7 YEAR- 8 YEAR- 9 YEAR- 10

ALESGem Stone (Cut & Polished) 1,530,000 1,767,150 2,041,058 2,357,422 2,722,823 3,144,860 3,632,314 4,195,322 4,845,597 5,596,665

1,134,000 1,309,770 1,512,784 1,747,266 2,018,092 2,330,896 2,692,185 3,109,474 3,591,443 4,148,116 604,800 698,544 806,818 931,875 1,076,316 1,243,145 1,435,832 1,658,386 1,915,436 2,212,329

- - - - - - - - - -

272400 3,268,800 3,775,464 4,360,661 5,036,563 5,817,231 6,718,901 7,760,331 8,963,182 10,352,476 11,957,110

OST OF SALESGem Stone (Cut & Polished) 390,000 471,900 570,999 690,909 836,000 1,011,560 1,223,987 1,481,024 1,792,039 2,168,368

- - - - - - - - - - - - - - - - - - - - - - - - - - - - - -

OST OF GOODS SOLD 390,000 471,900 570,999 690,909 836,000 1,011,560 1,223,987 1,481,024 1,792,039 2,168,368

ectricity Expanse 120,000 132,000 145,200 159,720 175,692 193,261 212,587 233,846 257,231 282,954 ayroll Expanse (All Staff) 1,404,000 1,544,400 1,698,840 1,868,724 2,055,596 2,261,156 2,487,272 2,735,999 3,009,599 3,310,559 eprecition Expanse 57,000 54,150 51,443 48,870 46,427 44,106 41,900 39,805 37,815 35,924 achine Maintenance Expanse 22,800 21,660 20,577 19,548 18,571 17,642 16,760 15,922 15,126 14,370

ent Expanse 252,000 264,600 277,830 291,722 306,308 321,623 337,704 354,589 372,319 390,935

mortization of Preliminary Expanses 10,000 10,000 10,000 10,000 10,000 - - - - -

OTAL OPERATING EXPANSES 1,865,800 2,026,810 2,203,890 2,398,584 2,612,594 2,837,788 3,096,223 3,380,161 3,692,089 4,034,741

ARNINGS BEFORE INTEREST & TAXES 1,013,000 1,276,754 1,585,772 1,947,071 2,368,637 2,869,554 3,440,121 4,101,997 4,868,347 5,754,001

INANCIAL EXPENSESnancial Charges on Long term loan 149,904 133,104 114,960 95,364 74,201 51,345 26,660 - - -

OTAL FINANCIAL EXPENSES 149,904 133,104 114,960 95,364 74,201 51,345 26,660 - - -

ROFIT BEFORE TAX 863,096 1,143,650 1,470,813 1,851,706 2,294,437 2,818,209 3,413,461 4,101,997 4,868,347 5,754,001

INCOME TAX 51,964 94,048 143,122 217,841 306,387 427,052 575,865 753,099 983,004 1,248,700

ROFIT AFTER TAX 811,132 1,049,603 1,327,691 1,633,865 1,988,049 2,391,157 2,837,596 3,348,898 3,885,343 4,505,301

etained Earnings at the beginning of year - 811,132 1,455,168 2,258,058 3,228,078 4,399,194 5,796,327 7,438,344 9,368,444 11,579,338

ividend 405,566 524,801 663,845 816,933 994,025 1,195,579 1,418,798 1,674,449 1,942,672

etained Earnings at the end of year 811,132 1,455,168 2,258,058 3,228,078 4,399,194 5,796,327 7,438,344 9,368,444 11,579,338 14,141,967

September 2013

13

Pre-Feasibility Study Gemstone Lapidary

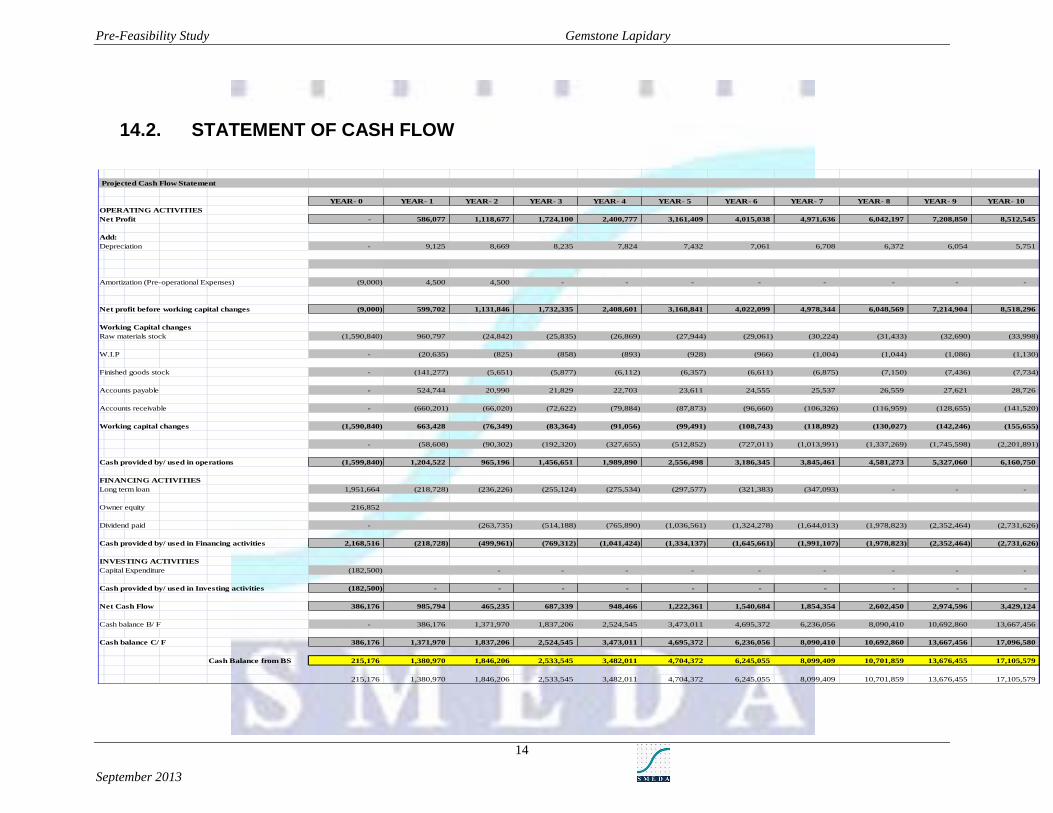

14.2. STATEMENT OF CASH FLOW Projected Cash Flow Statement

YEAR- 0 YEAR- 1 YEAR- 2 YEAR- 3 YEAR- 4 YEAR- 5 YEAR- 6 YEAR- 7 YEAR- 8 YEAR- 9 YEAR- 10OPERATING ACTIVITIESNet Profit - 586,077 1,118,677 1,724,100 2,400,777 3,161,409 4,015,038 4,971,636 6,042,197 7,208,850 8,512,545

Add: Depreciation - 9,125 8,669 8,235 7,824 7,432 7,061 6,708 6,372 6,054 5,751

Amortization (Pre-operational Expenses) (9,000) 4,500 4,500 - - - - - - - -

Net profit before working capital changes (9,000) 599,702 1,131,846 1,732,335 2,408,601 3,168,841 4,022,099 4,978,344 6,048,569 7,214,904 8,518,296

Working Capital changesRaw materials stock (1,590,840) 960,797 (24,842) (25,835) (26,869) (27,944) (29,061) (30,224) (31,433) (32,690) (33,998)

W.I.P - (20,635) (825) (858) (893) (928) (966) (1,004) (1,044) (1,086) (1,130)

Finished goods stock - (141,277) (5,651) (5,877) (6,112) (6,357) (6,611) (6,875) (7,150) (7,436) (7,734)

Accounts payable - 524,744 20,990 21,829 22,703 23,611 24,555 25,537 26,559 27,621 28,726

Accounts receivable - (660,201) (66,020) (72,622) (79,884) (87,873) (96,660) (106,326) (116,959) (128,655) (141,520)

Working capital changes (1,590,840) 663,428 (76,349) (83,364) (91,056) (99,491) (108,743) (118,892) (130,027) (142,246) (155,655)

- (58,608) (90,302) (192,320) (327,655) (512,852) (727,011) (1,013,991) (1,337,269) (1,745,598) (2,201,891)

Cash provided by/ used in operations (1,599,840) 1,204,522 965,196 1,456,651 1,989,890 2,556,498 3,186,345 3,845,461 4,581,273 5,327,060 6,160,750

FINANCING ACTIVITIESLong term loan 1,951,664 (218,728) (236,226) (255,124) (275,534) (297,577) (321,383) (347,093) - - -

Owner equity 216,852

Dividend paid - (263,735) (514,188) (765,890) (1,036,561) (1,324,278) (1,644,013) (1,978,823) (2,352,464) (2,731,626)

Cash provided by/ used in Financing activities 2,168,516 (218,728) (499,961) (769,312) (1,041,424) (1,334,137) (1,645,661) (1,991,107) (1,978,823) (2,352,464) (2,731,626)

INVESTING ACTIVITIESCapital Expenditure (182,500) - - - - - - - - -

Cash provided by/ used in Investing activities (182,500) - - - - - - - - - -

Net Cash Flow 386,176 985,794 465,235 687,339 948,466 1,222,361 1,540,684 1,854,354 2,602,450 2,974,596 3,429,124

Cash balance B/ F - 386,176 1,371,970 1,837,206 2,524,545 3,473,011 4,695,372 6,236,056 8,090,410 10,692,860 13,667,456

Cash balance C/ F 386,176 1,371,970 1,837,206 2,524,545 3,473,011 4,695,372 6,236,056 8,090,410 10,692,860 13,667,456 17,096,580

Cash Balance from BS 215,176 1,380,970 1,846,206 2,533,545 3,482,011 4,704,372 6,245,055 8,099,409 10,701,859 13,676,455 17,105,579

215,176 1,380,970 1,846,206 2,533,545 3,482,011 4,704,372 6,245,055 8,099,409 10,701,859 13,676,455 17,105,579

September 2013

14

Pre-Feasibility Study Gemstone Lapidary

14.3. BALANCE SHEET

PROJECTIONS

Projected Balance Sheet

YEAR-0 YEAR - 1 YEAR - 2 YEAR - 3 YEAR - 4 YEAR - 5 YEAR - 6 YEAR - 7 YEAR - 8 YEAR - 9 YEAR - 10

ASSETS

Current Assets

Cash & Bank Balance 250,000 1,091,738 1,547,543 2,134,100 2,857,207 3,748,040 4,818,379 6,093,555 7,972,682 10,112,863 12,582,265

Raw materials stock 390,000 38,464 46,542 56,315 68,142 82,452 99,766 120,717 146,068 176,742 213,858

W.I.P - 1,278 1,546 1,871 2,264 2,740 3,315 4,011 4,853 5,873 7,106

Finished goods stock - 8,750 10,588 12,811 15,501 18,756 22,695 27,461 33,228 40,206 48,649

Receivables 272,400 314,622 363,388 419,714 484,769 559,908 646,694 746,932 862,706 996,426

640,000 1,412,630 1,920,841 2,568,485 3,362,828 4,336,757 5,504,064 6,892,438 8,903,763 11,198,390 13,848,304 TOTAL CURRENT ASSETS

Fixed Assets

At Cost less: Acc. Depreciation 1,140,000 1,083,000 1,028,850 977,408 928,537 882,110 838,005 796,105 756,299 718,484 682,560

Intangible Assets

Upfront Insurance 252,000 180,000 160,000 140,000 120,000 100,000 80,000 60,000 40,000 20,000

Pre-operational Expenses Worth 50,000 40,000 30,000 20,000 10,000 TOTAL ASSETS 2,082,000 2,715,630 3,139,691 3,705,893 4,421,365 5,318,867 6,422,069 7,748,543 9,700,062 11,936,875 14,530,864

LIABILITIES AND EQUITY

Current Liabilities

Current maturity of long term loan 226,801 244,945 264,541 285,704 308,561 333,246 - - - -

Accounts Payable - 32,500 39,325 47,583 57,576 69,667 84,297 101,999 123,419 149,337 180,697

TOTAL CURRENT LIABILITIES - 259,301 284,270 312,124 343,280 378,227 417,542 101,999 123,419 149,337 180,697

Non current Liabilities

Long term Loan 1,873,800 1,436,997 1,192,052 927,511 641,806 333,246 - - - - -

EQUITY

Paid up Capital 208,200 208,200 208,200 208,200 208,200 208,200 208,200 208,200 208,200 208,200 208,200

Retained Earnings - 811,132 1,455,168 2,258,058 3,228,078 4,399,194 5,796,327 7,438,344 9,368,444 11,579,338 14,141,967

Total Equity 208,200 1,019,332 1,663,368 2,466,258 3,436,278 4,607,394 6,004,527 7,646,544 9,576,644 11,787,538 14,350,167

TOTAL LIABILITIES & EQUITY 2,082,000 2,715,630 3,139,691 3,705,893 4,421,365 5,318,867 6,422,069 7,748,543 9,700,062 11,936,875 14,530,864

September 2013

15

Pre-Feasibility Study Gemstone Lapidary

14.4. USEFUL PROJECT MANAGEMENT TIPS Technology

• Required spare parts & consumables:Suppliers credit agreements and availability as per schedule of maintenance be ensured before start of operations

• Energy Requirement: Should not be overestimated or installed in excess and alternate source of energy for critical operations be arranged in advance

• Machinery Suppliers: Should be asked for training and after sales services under the contract with the machinery suppliers. They must be communicated about the timely availability with clear mutual understanding of the required time period.

• Quality Assurance Equipment & Standards:Whatever means required products quality standards need to be defined on the packaging and a system to check them instituted, this improves credibility

Marketing

• Product Development & Packaging:Expert's help may be engaged for product/service and packaging design & development

• Sales & Distribution Network:Strong contacts with the civil works contractors focusing upon house constructions for middle class people and owners of retail shops.

• Price - Bulk Discounts, Cost plus Introductory Discounts:Price should never be allowed to compromise quality. Price during introductory phase may be lower and used as promotional tool. Product cost estimates should be carefully documented before price setting. Government controlled prices shall be displayed.

Human Resources

• Adequacy & Competencies: Skilled and experienced staff should be considered an investment even to the extent of offering share in business profit.

• Performance Based Remuneration:Attempt to manage human resource cost should be focused through performance measurement and performance based compensation.

• Training & Skill Development:Encouraging training and skill of self & employees through experts and exposure of best practices is route to success.

September 2013

16

Pre-Feasibility Study Gemstone Lapidary

Least cost options for Training and Skill Development (T&SD) may be linked with compensation benefits and awards.

14.5. USEFUL LINKS

Prime Minister’s Office

www.pmo.gov.pk

Small & Medium Enterprises Development Authority (SMEDA)

www.smeda.org.pk

National Bank of Pakistan (NBP)

www.nbp.com.pk

First Women Bank Limited (FWBL)

www.fwbl.com.pk

Government of Pakistan

www.pakistan.gov.pk

Ministry of Industries & Production

www.moip.gov.pk

Ministry of Education, Training & Standards in Higher Education

http://moptt.gov.pk

Government of Punjab

www.punjab.gov.pk

Government of Sindh

www.sindh.gov.pk

Government of Khyber Pakhtoonkhwa

www.khyberpakhtunkhwa.gov.pk

Government of Balochistan

www.balochistan.gov.pk

Government of Gilgit Baltistan

www.gilgitbaltistan.gov.pk

Government of Azad Jammu &Kashmir

www.ajk.gov.pk

September 2013

17

Pre-Feasibility Study Gemstone Lapidary

Trade Development Authority of Pakistan (TDAP)

www.tdap.gov.pk

Security Exchange Commission of Pakistan (SECP)

www.secp.gov.pk

Federation of Pakistan Chambers of Commerce and Industry (FPCCI)

www.fpcci.com.pk

State Bank of Pakistan (SBP)

www.sbp.org.pk

Pakistan Institute of Fashion Design(PIFD)

www.pifd.edu.pk

Pakistan Fashion Design Council (PFDC)

www.pfdc.org

September 2013

18

Pre-Feasibility Study Gemstone Lapidary

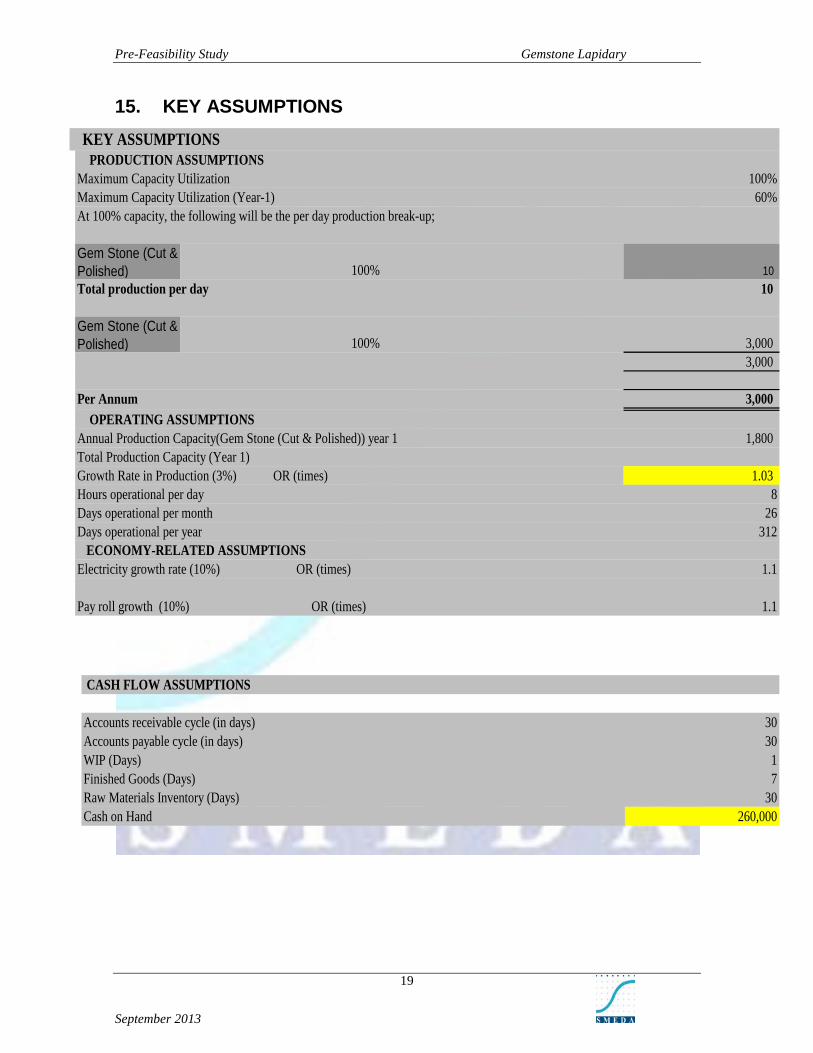

15. KEY ASSUMPTIONS

PRODUCTION ASSUMPTIONSMaximum Capacity Utilization 100%Maximum Capacity Utilization (Year-1) 60%At 100% capacity, the following will be the per day production break-up;

Gem Stone (Cut & Polished) 100% 10 Total production per day 10

Gem Stone (Cut & Polished) 100% 3,000

3,000

Per Annum 3,000 OPERATING ASSUMPTIONSAnnual Production Capacity(Gem Stone (Cut & Polished)) year 1 1,800 Total Production Capacity (Year 1)Growth Rate in Production (3%) OR (times) 1.03 Hours operational per day 8Days operational per month 26Days operational per year 312 ECONOMY-RELATED ASSUMPTIONSElectricity growth rate (10%) OR (times) 1.1

Pay roll growth (10%) OR (times) 1.1

KEY ASSUMPTIONS

CASH FLOW ASSUMPTIONS

Accounts receivable cycle (in days) 30Accounts payable cycle (in days) 30WIP (Days) 1Finished Goods (Days) 7Raw Materials Inventory (Days) 30Cash on Hand 260,000

September 2013

19

Pre-Feasibility Study Gemstone Lapidary

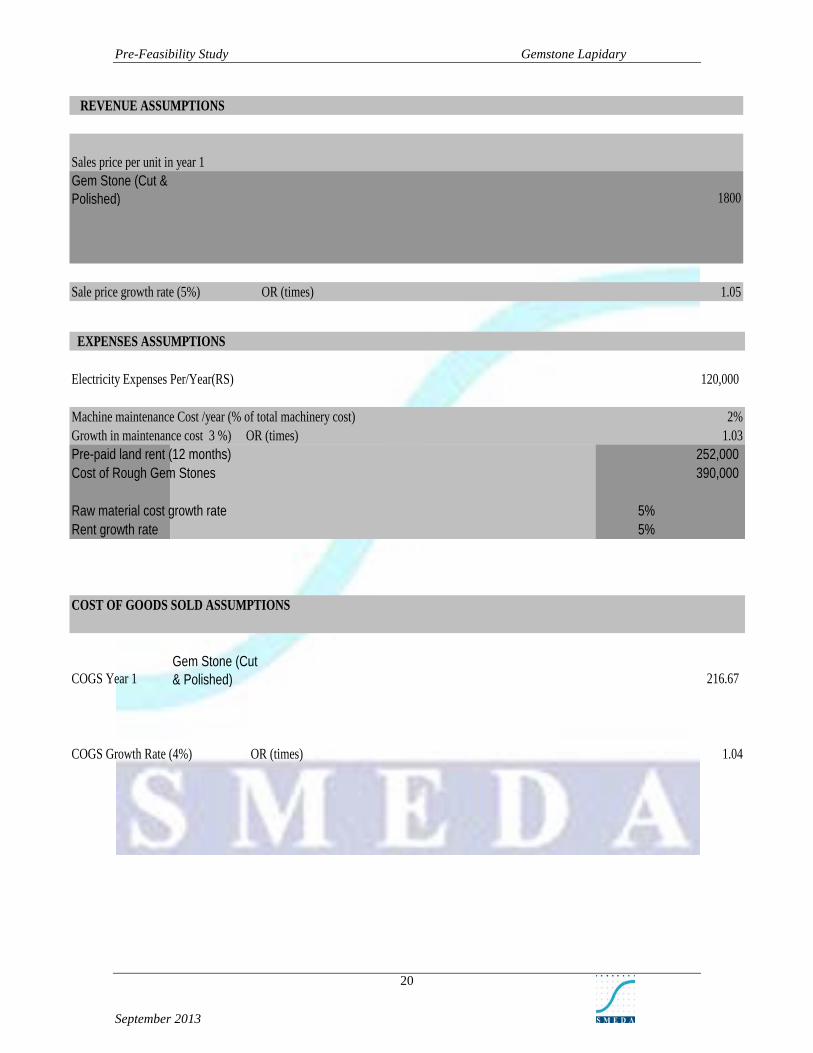

REVENUE ASSUMPTIONS

Sales price per unit in year 1Gem Stone (Cut & Polished) 1800

Sale price growth rate (5%) OR (times) 1.05

EXPENSES ASSUMPTIONS

Electricity Expenses Per/Year(RS) 120,000

Machine maintenance Cost /year (% of total machinery cost) 2%Growth in maintenance cost 3 %) OR (times) 1.03Pre-paid land rent (12 months) 252,000 Cost of Rough Gem Stones 390,000

Raw material cost growth rate 5%Rent growth rate 5%

COST OF GOODS SOLD ASSUMPTIONS

COGS Year 1Gem Stone (Cut & Polished) 216.67

COGS Growth Rate (4%) OR (times) 1.04

September 2013

20

Pre-Feasibility Study Gemstone Lapidary

FINANCIAL ASSUMPTIONS

Project Life (Years) 10Debt 90%Equity 10%Interest rate on long term loan 8%Debt tenure (years) 7Debt payments per year 1

September 2013

21