gasb 68 and 71 planning for the second year

TRANSCRIPT

1

2

3

4

5

6

7

8

9

Changes to the Accounting Valuations

10

11

12

13

Calculating CertainDeferred Outflows/Inflows

and NPL Sensitivity Disclosure

14

15

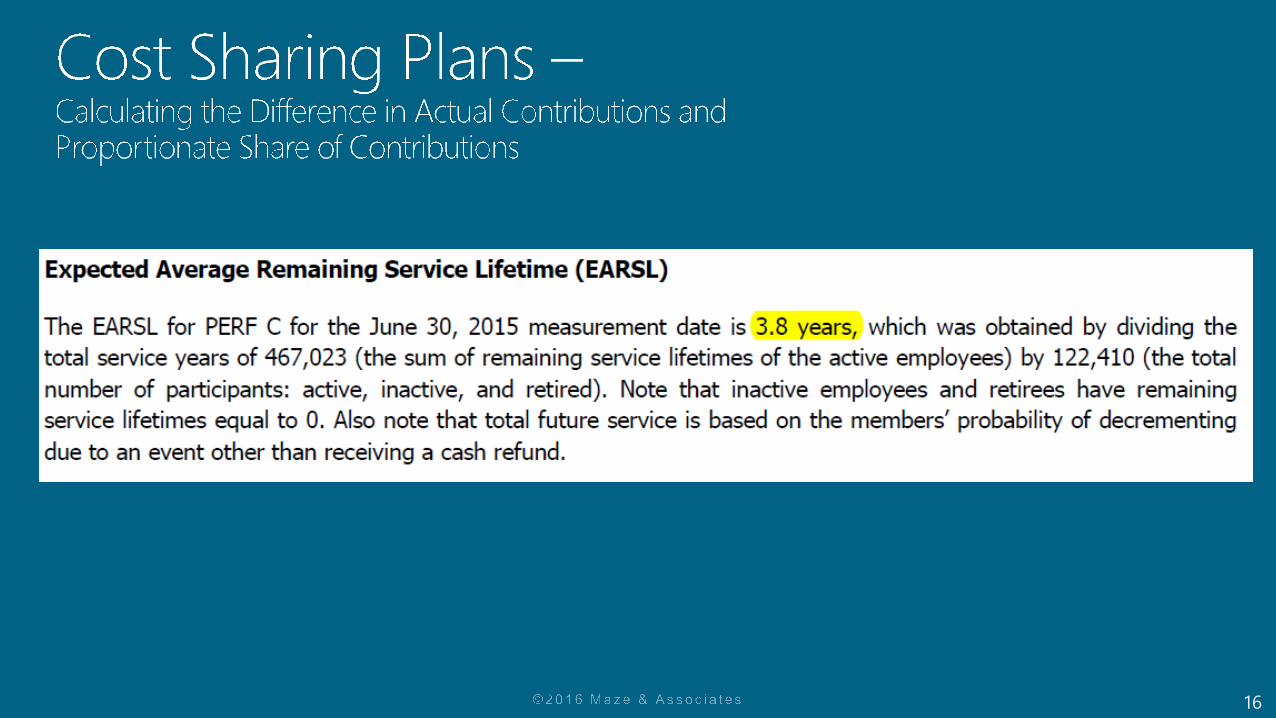

16

17

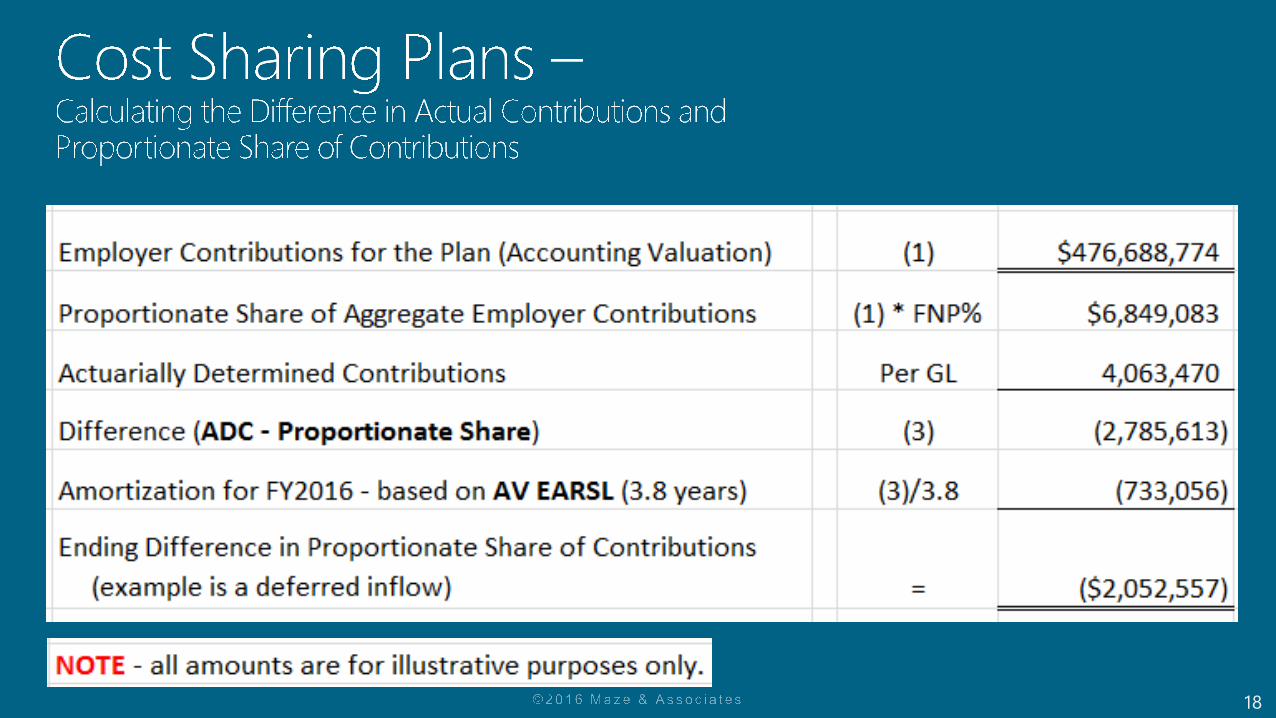

18

19

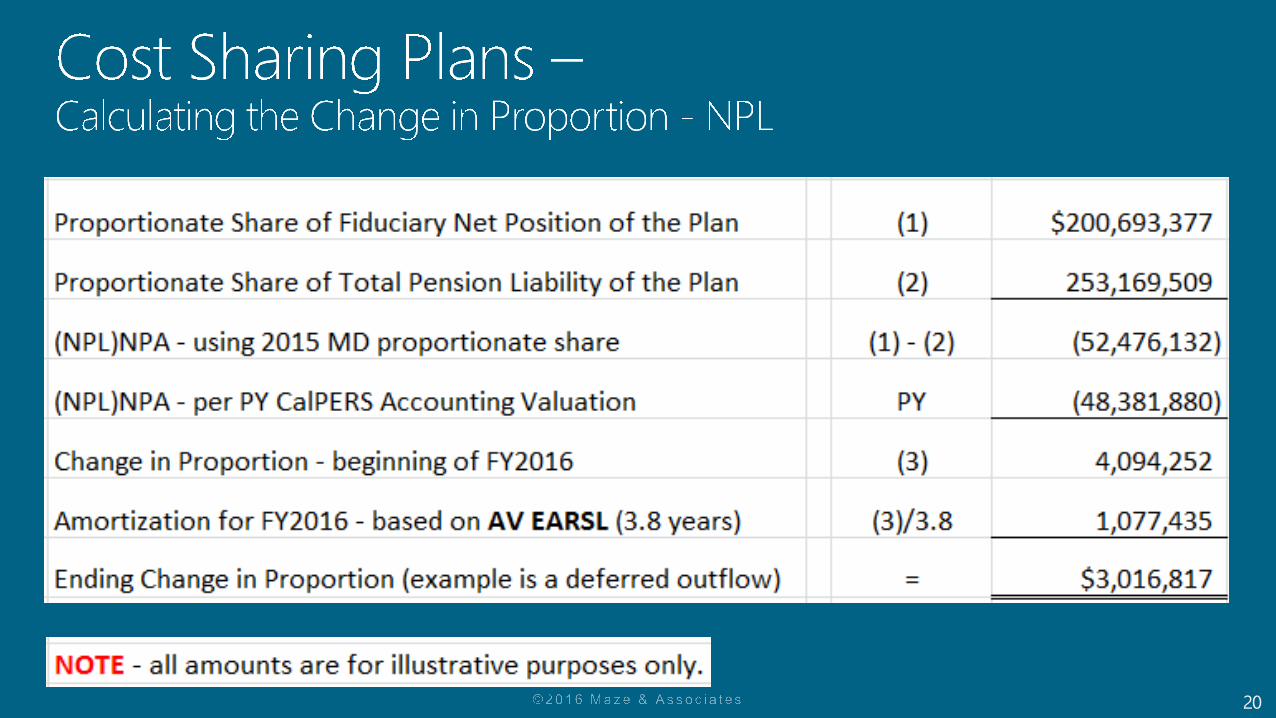

20

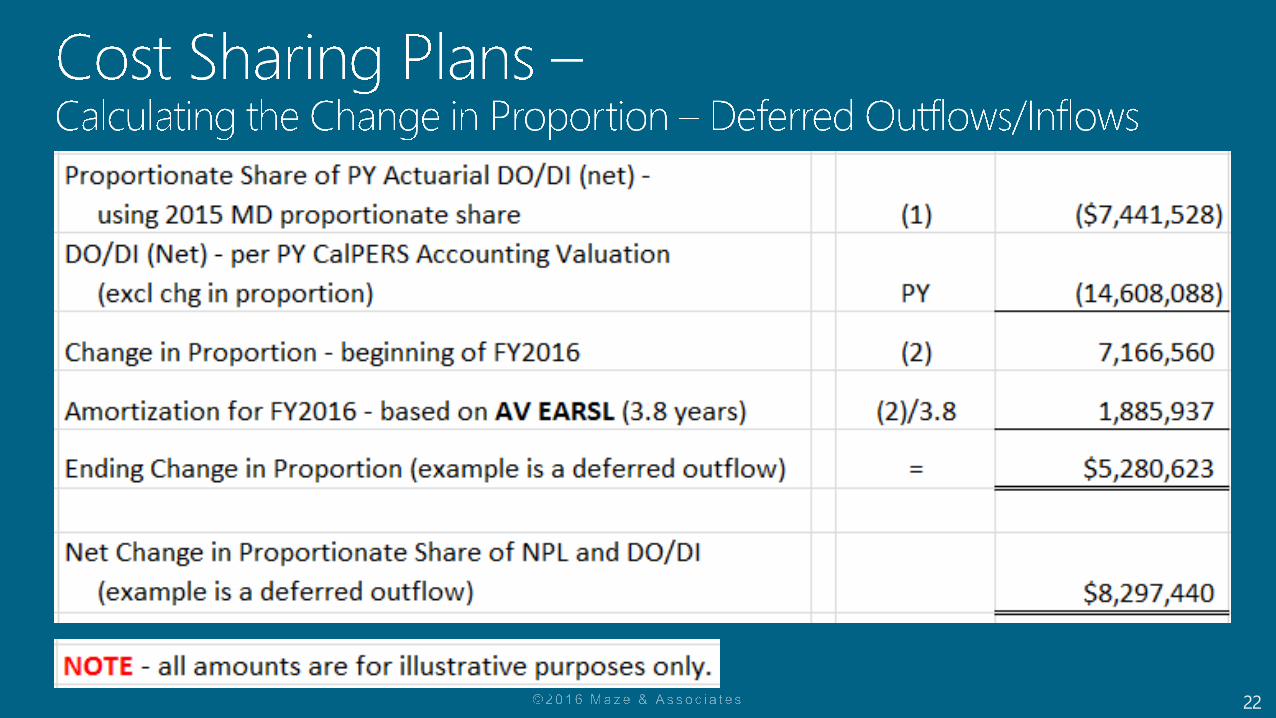

21

22

23

24

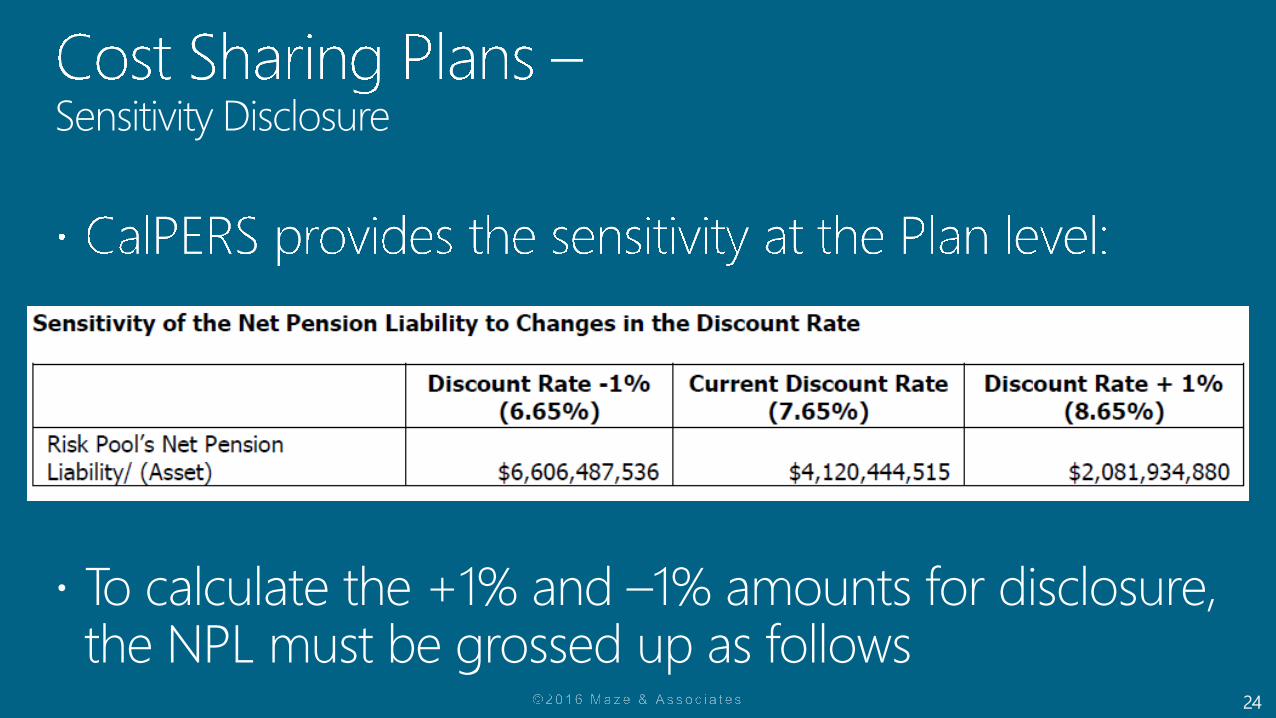

Sensitivity Disclosure

To calculate the +1% and –1% amounts for disclosure, the NPL must be grossed up as follows

25

Sensitivity Disclosure Calculation – EXAMPLE ONLY

26

27

28

29

30

31

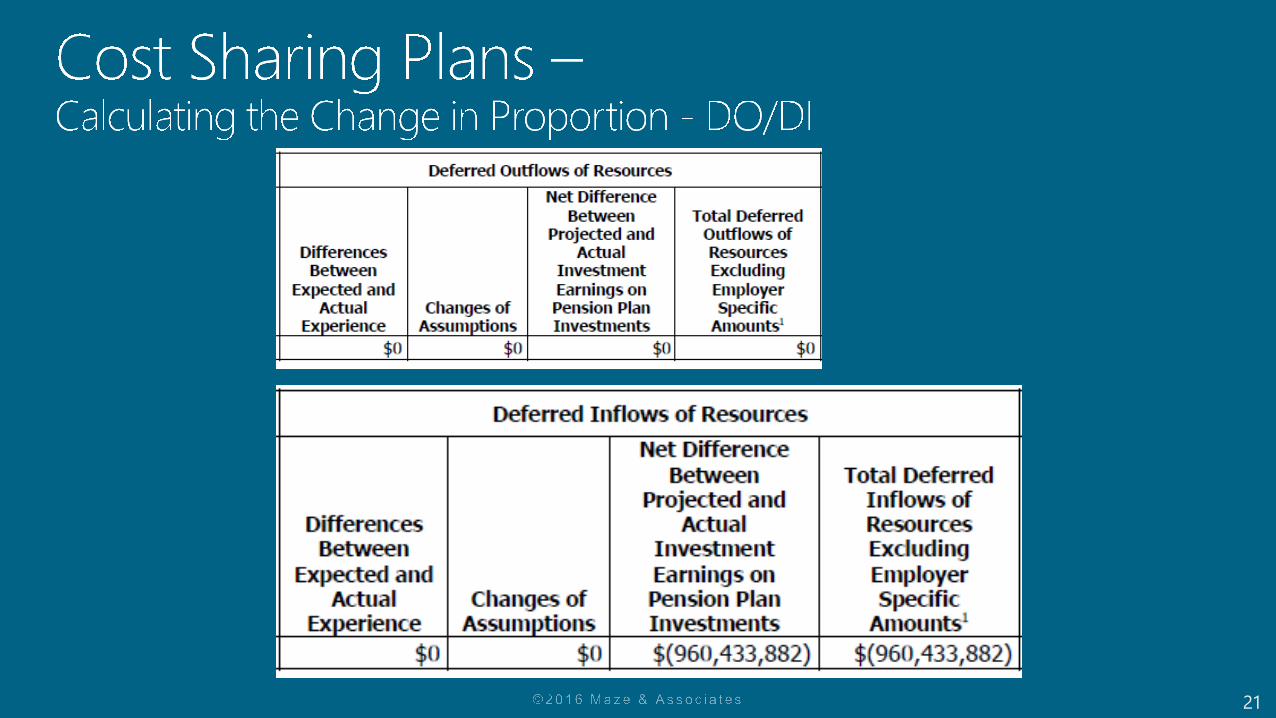

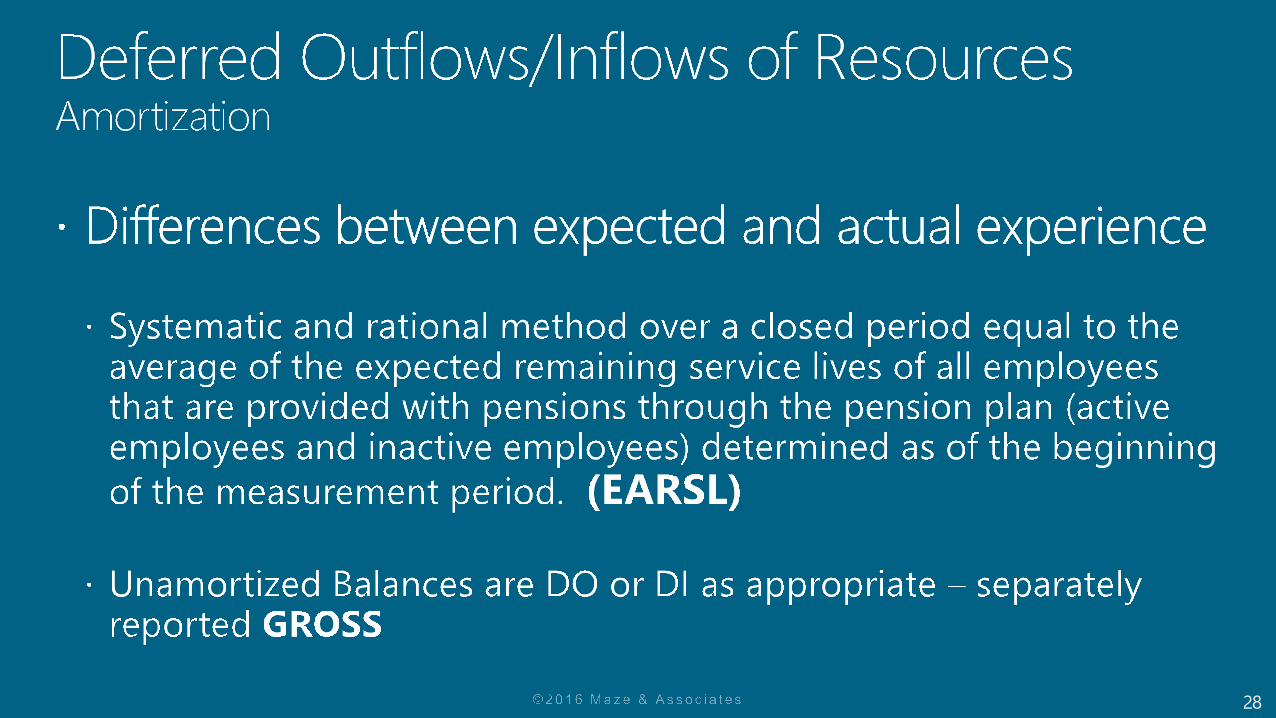

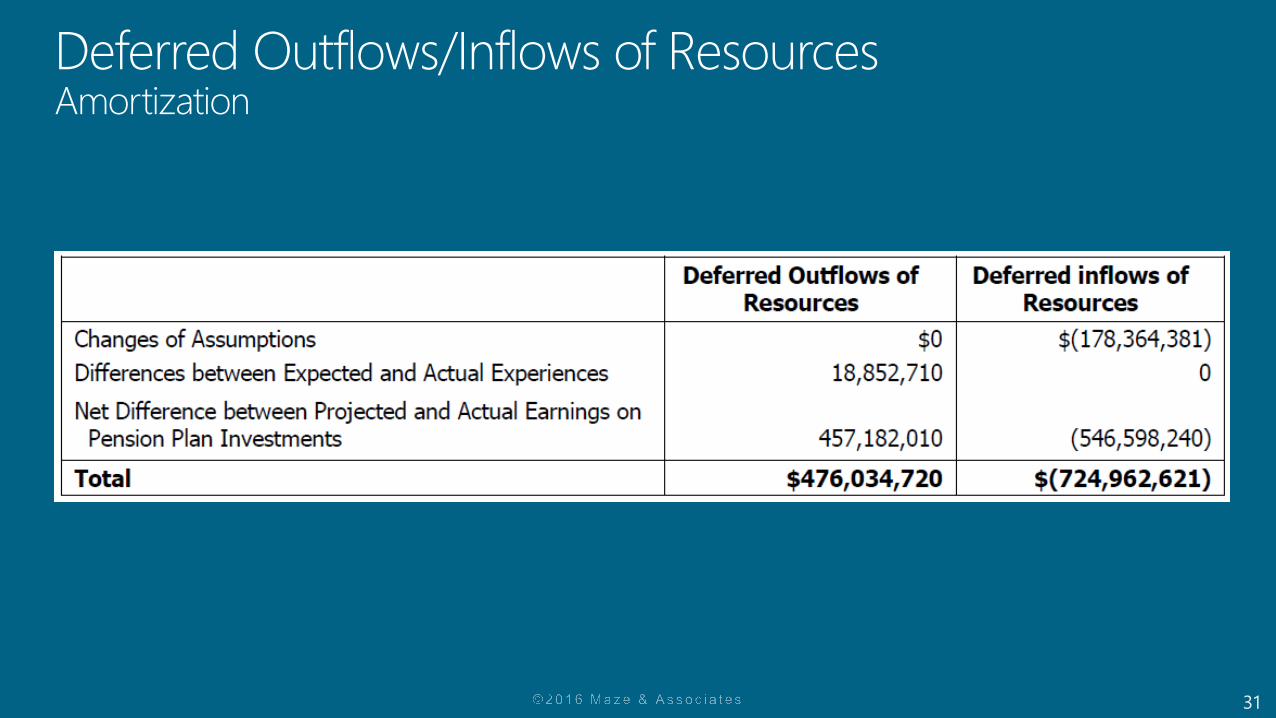

Deferred Outflows/Inflows of ResourcesAmortization

32

(EARSL)

33

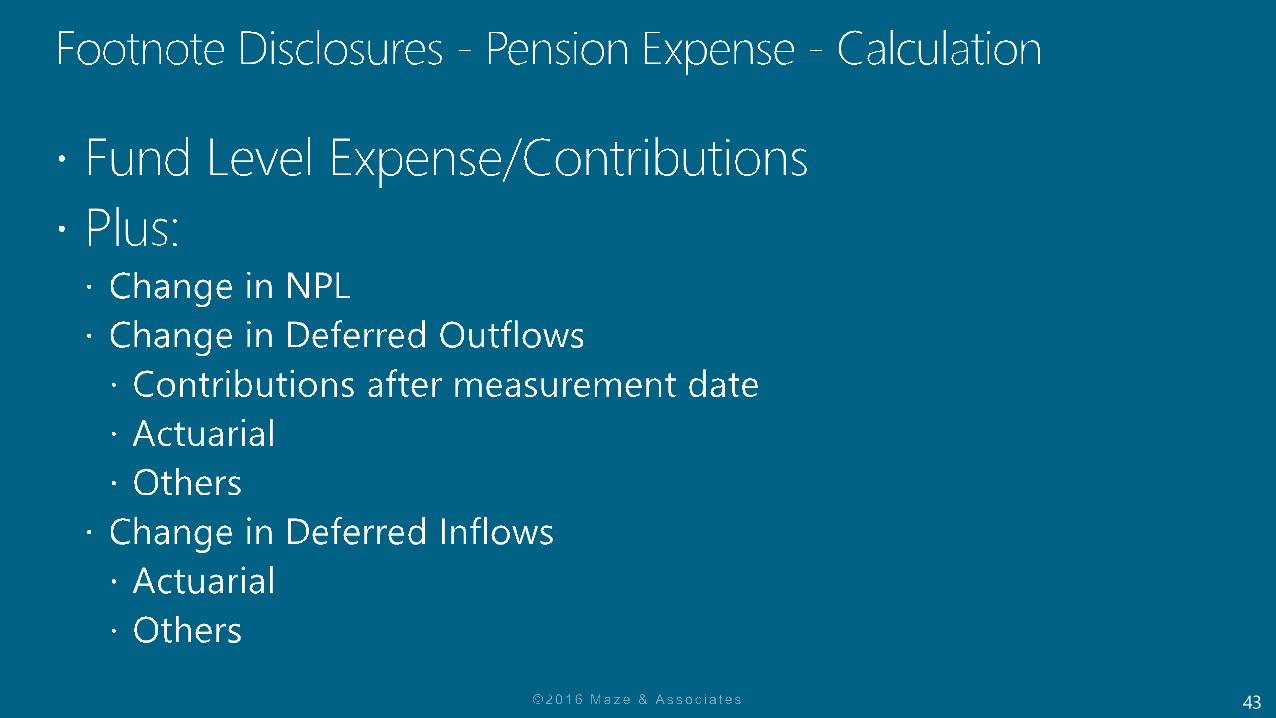

Proportionate Share of Contributions

34

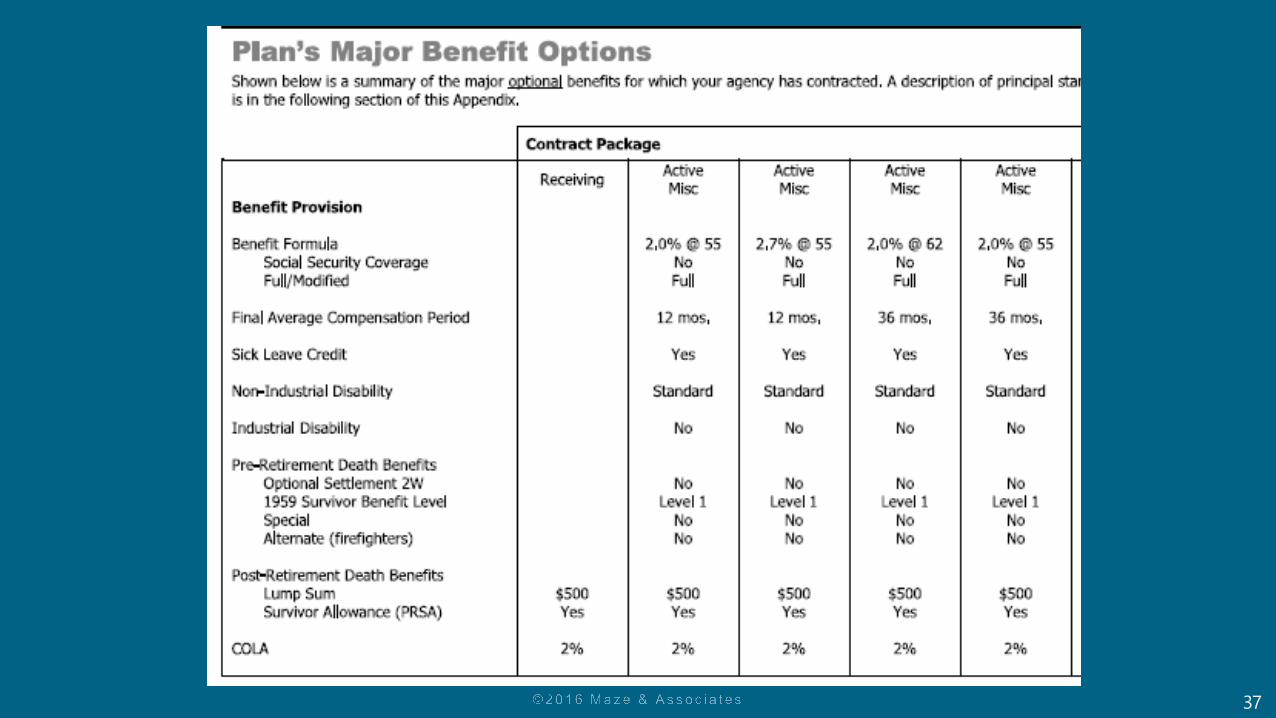

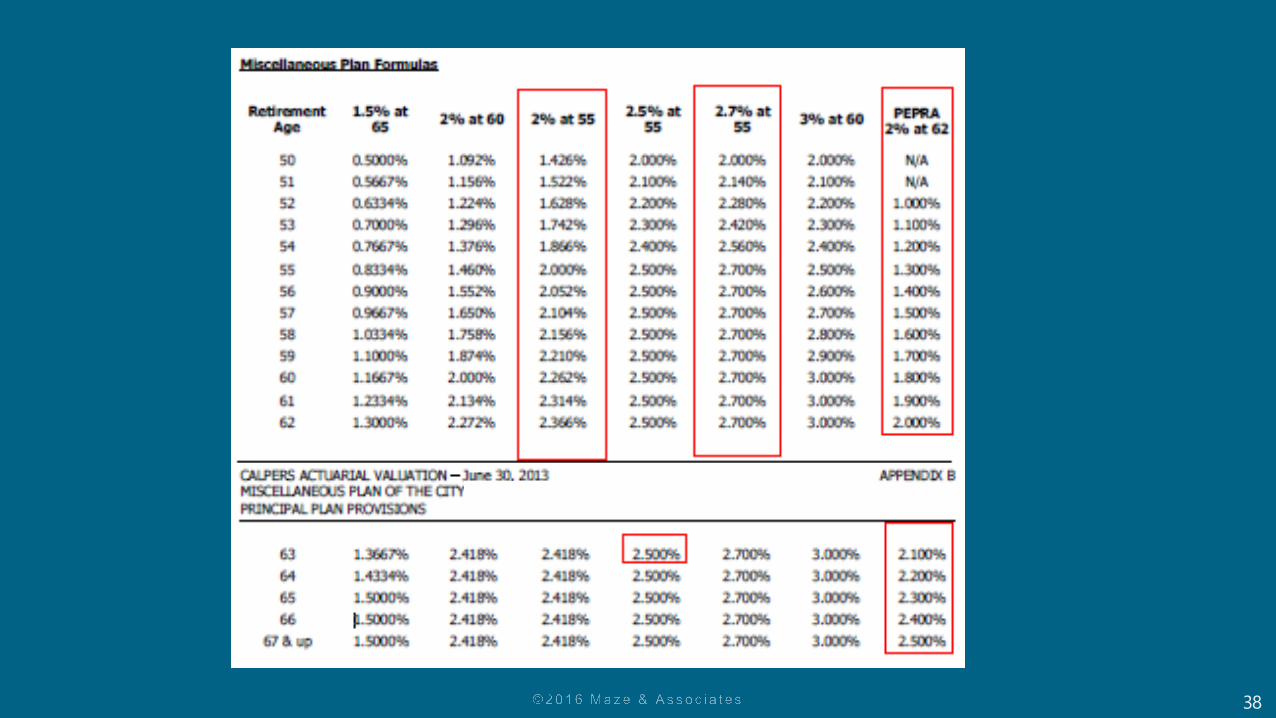

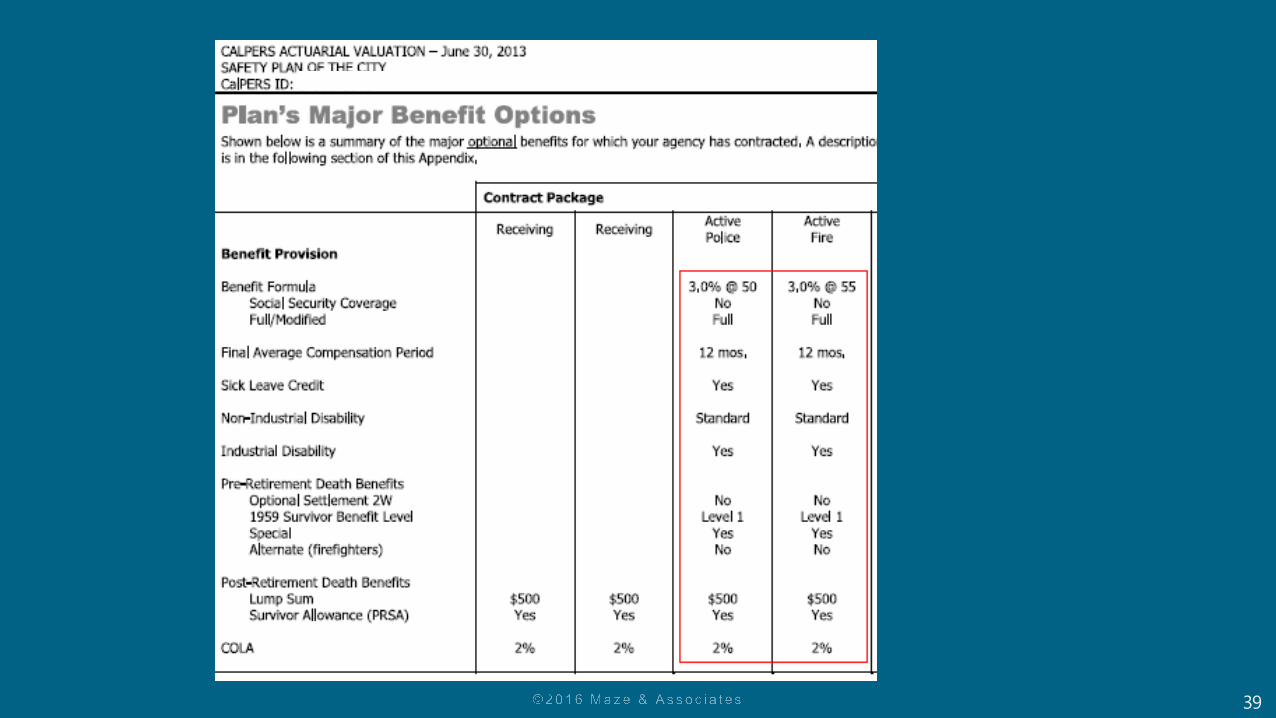

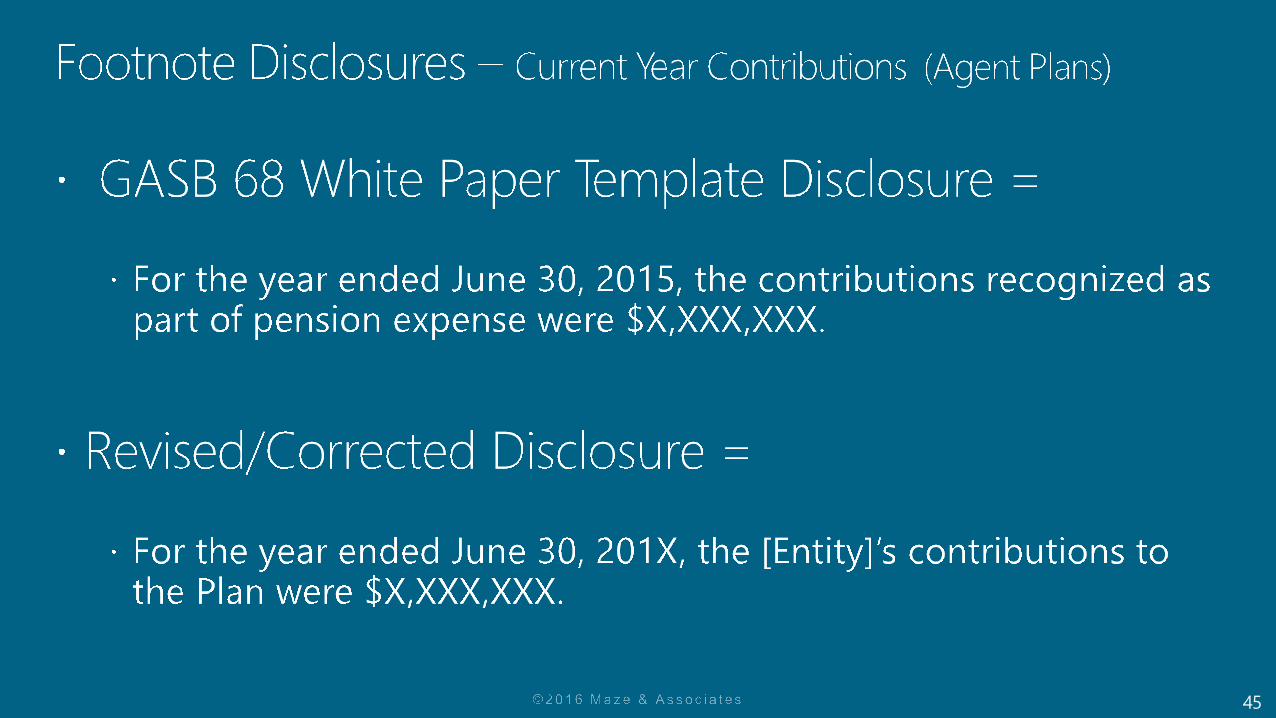

Disclosure Sources

35

36

37

38

39

40

41

Clarifications

42

43

44

45

46

47

48

49

50

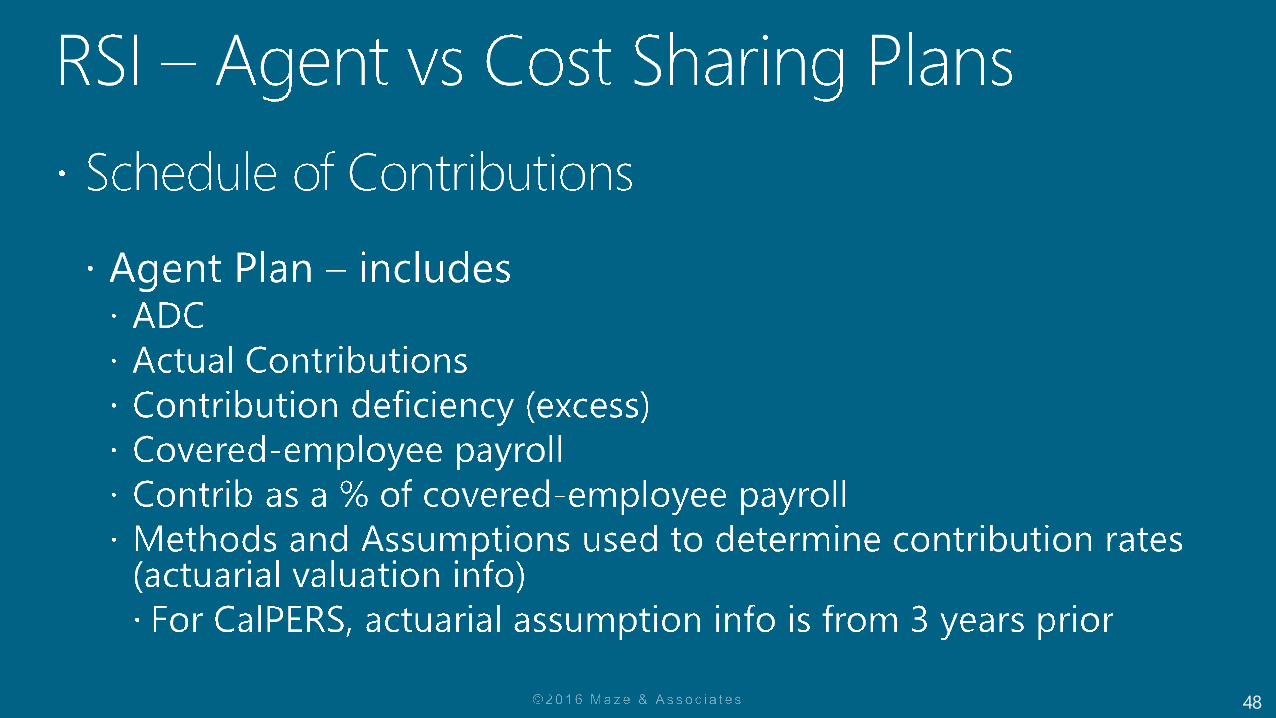

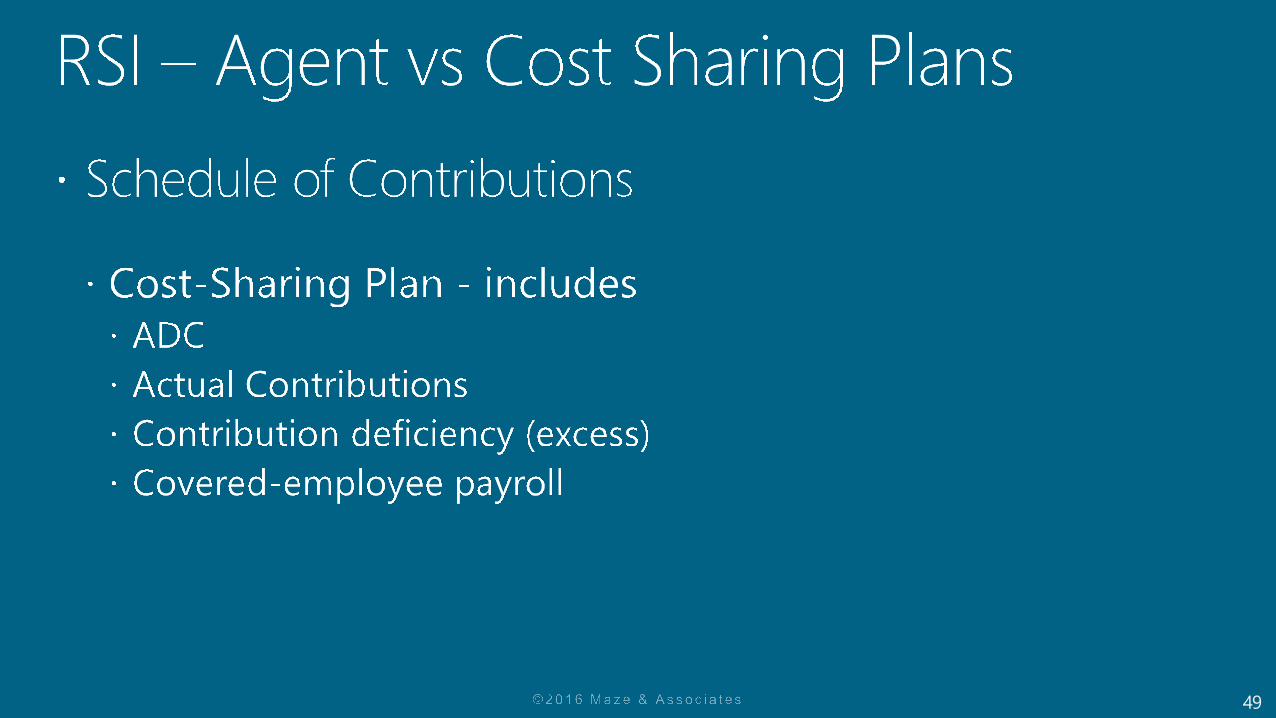

CEP = The total payroll of employees that are provided with pensions through the pension plan, including pensionable and non-pensionable amounts.

51

52

53

54

55

56

57

58

59

http://www.gasb.org/jsp/GASB/Page/GASBSectionPage&cid=1176160042391#gasbs75

https://www.calpers.ca.gov/page/employers/actuarial-services/gasb

60

https://www.calpers.ca.gov/docs/gasb-68-cost-sharing-guide.pdf

CCMA White Paper – Implementing GASB No. 68 Accounting and Financial Reporting for Pensions: http://www.calcpa.org/members/technical-resources/gaa-white-papers

61

62