fy 2015 corporate presentation - jk cement 2015 corporate presentation disclaimer safe harbor...

TRANSCRIPT

FY 2015

CORPORATE PRESENTATION

Disclaimer Safe Harbor Statement

This presentation is strictly confidential and may not be copied, published, distributed or transmitted. The information in this presentation is being provided by J. K. Cement Limited (also referred to as ‘JKC’ or ‘Company’). By attending the meeting where this presentation is being made or by reading the presentation materials, you agree to be bound by following limitations: The information in this presentation has been prepared for use in presentations by JKC for information purposes only and does not constitute, or should be regarded as, or form part of any offer, invitation, inducement or advertisement to sell or issue, or any solicitation or initiation of any offer to purchase or subscribe for, any securities of the Company in any jurisdiction, including the United States and India, nor shall it, or the fact of its distribution form the basis of, or be relied on in connection with, any investment decision or any contract or commitment to purchase or subscribe for any securities of the Company in any jurisdiction, including the United States and India. This presentation does not constitute a recommendation by the Company or any other party to sell or buy any securities of the Company. This presentation and its contents are not and should not be construed as a prospectus or an offer document, including as defined under the Companies Act, 2013, including the rules formulated thereunder (to the extent notified and in force) or an offer document under the Securities and Exchange Board of India (Issue of Capital and Disclosure Requirements) Regulations, 2009 as amended. This presentation and its contents are strictly confidential to the recipient and should not be further distributed, re-transmitted, published or reproduced, in whole or in part, or disclosed by recipients directly or indirectly to any other person or press, for any purposes. In particular, this presentation is not for publication or distribution or release in any country where such distribution may lead to a breach of any law or regulatory requirement. No person is authorized to give any information or to make any representation not contained in or inconsistent with this presentation or and if given or made, such information or representation must not be relied upon as having been authorized by us. Receipt of this presentation constitutes an express agreement to be bound by such confidentiality and the other terms set out herein. Any failure to comply with this restriction may constitute a violation of applicable securities laws. No representation or warranty, express or implied, is made as to, and no reliance should be placed on, the fairness, accuracy, completeness or correctness of the information or opinions contained in this presentation. Neither JKC nor any of its affiliates, advisors or representatives shall have any responsibility or liability whatsoever (for negligence or otherwise) for any loss howsoever arising from any use of this presentation or its contents or otherwise arising in connection with this presentation. The information set out herein may be subject to updating, completion, revision, verification and amendment and such information may change materially. This presentation is based on the economic, regulatory, market and other conditions as in effect on the date hereof. It should be understood that subsequent developments may affect the information contained in this presentation, which neither JKC nor its affiliates, advisors or representatives are under an obligation to update, revise or affirm. This presentation contains forward-looking statements based on the currently held beliefs and assumptions of the management of JKC, which are expressed in good faith and, in their opinion, reasonable. Forward-looking statements involve known and unknown risks, uncertainties and other factors, which may cause the actual results, financial condition, performance, or achievements of JKC or industry results, to differ materially from the results, financial condition, performance or achievements expressed or implied by such forward-looking statements. Unless otherwise indicated, the information contained herein is preliminary and indicative and is based on management information, current plans and estimates. Industry and market-related information is obtained or derived from industry publications and other sources and has not been independently verified by us. Given these risks, uncertainties and other factors, recipients of this document are cautioned not to place undue reliance on these forward-looking statements. JKC disclaims any obligation to update these forward-looking statements to reflect future events or developments. THIS PRESENTATION IS NOT AN OFFER FOR SALE OF SECURITIES IN INDIA, THE UNITED STATES OR ELSEWHERE

Corporate Presentation 2

General Introduction Company Overview Key Highlights Business Strategy Annexures

Strictly Private & Confidential

Contents

Corporate Presentation 3

General Introduction

1 Company Overview

4

Business Strategy 3

Key Highlights

Annexure

2

Company Overview Key Highlights Business Strategy Annexures

Strictly Private & Confidential

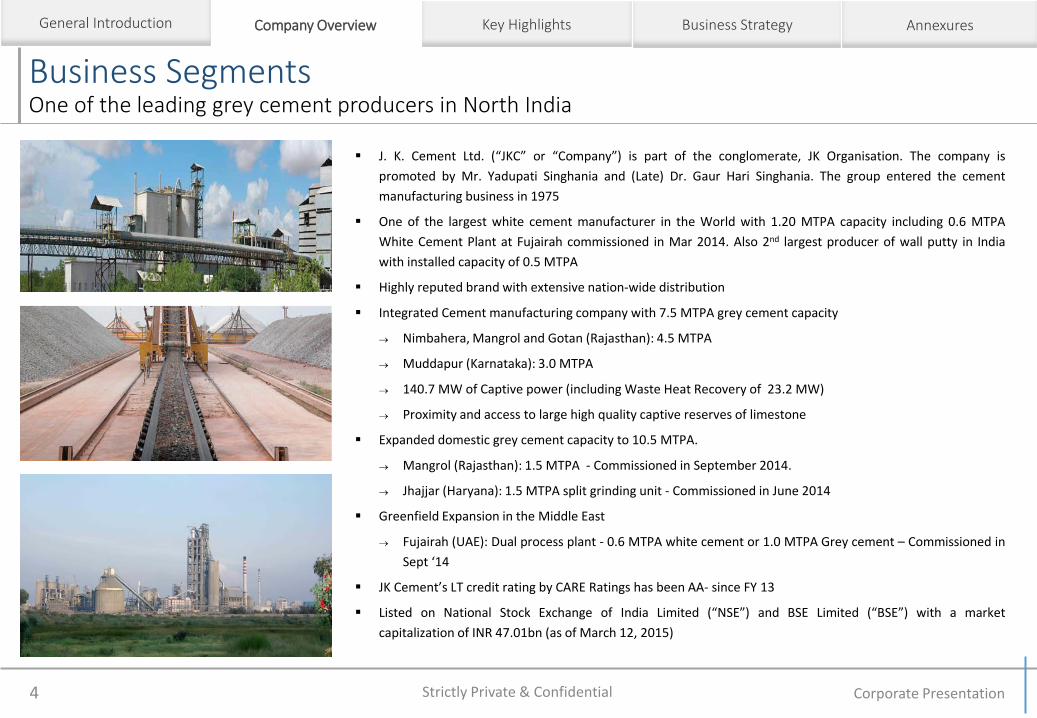

Business Segments One of the leading grey cement producers in North India

Corporate Presentation 4

Company Overview General Introduction Key Highlights Business Strategy Annexures

J. K. Cement Ltd. (“JKC” or “Company”) is part of the conglomerate, JK Organisation. The company is

promoted by Mr. Yadupati Singhania and (Late) Dr. Gaur Hari Singhania. The group entered the cement

manufacturing business in 1975

One of the largest white cement manufacturer in the World with 1.20 MTPA capacity including 0.6 MTPA

White Cement Plant at Fujairah commissioned in Mar 2014. Also 2nd largest producer of wall putty in India

with installed capacity of 0.5 MTPA

Highly reputed brand with extensive nation-wide distribution

Integrated Cement manufacturing company with 7.5 MTPA grey cement capacity

Nimbahera, Mangrol and Gotan (Rajasthan): 4.5 MTPA

Muddapur (Karnataka): 3.0 MTPA

140.7 MW of Captive power (including Waste Heat Recovery of 23.2 MW)

Proximity and access to large high quality captive reserves of limestone

Expanded domestic grey cement capacity to 10.5 MTPA.

Mangrol (Rajasthan): 1.5 MTPA - Commissioned in September 2014.

Jhajjar (Haryana): 1.5 MTPA split grinding unit - Commissioned in June 2014

Greenfield Expansion in the Middle East

Fujairah (UAE): Dual process plant - 0.6 MTPA white cement or 1.0 MTPA Grey cement – Commissioned in

Sept ‘14

JK Cement’s LT credit rating by CARE Ratings has been AA- since FY 13

Listed on National Stock Exchange of India Limited (“NSE”) and BSE Limited (“BSE”) with a market

capitalization of INR 47.01bn (as of March 12, 2015)

Strictly Private & Confidential

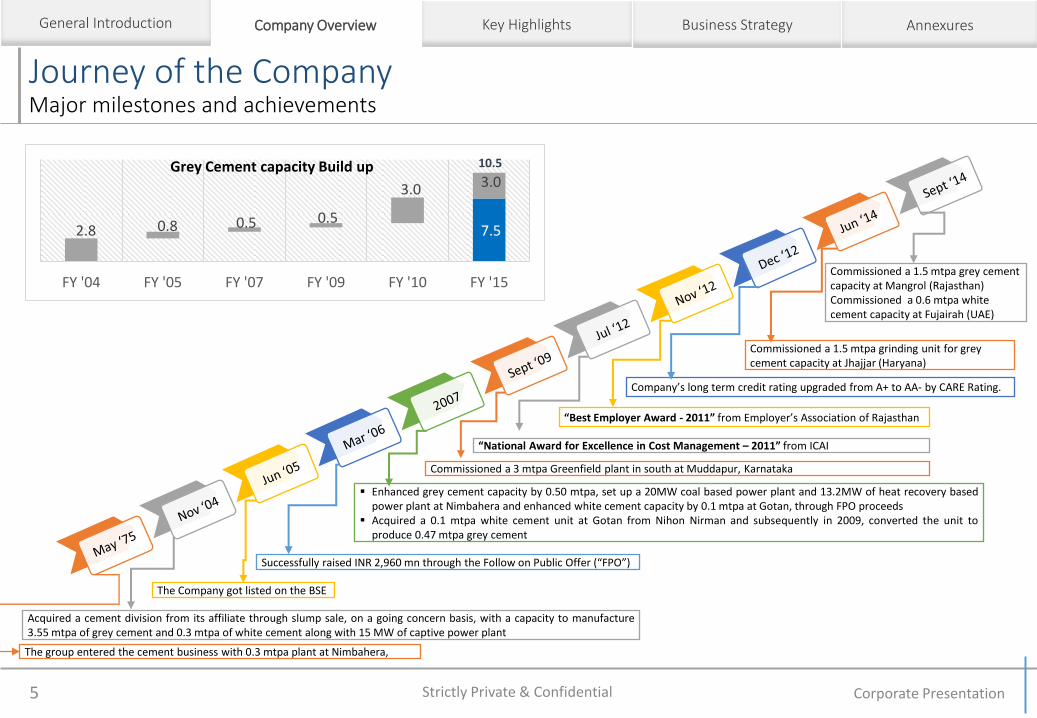

Journey of the Company Major milestones and achievements

Corporate Presentation 5

Company Overview General Introduction Key Highlights Business Strategy Annexures

The group entered the cement business with 0.3 mtpa plant at Nimbahera,

Acquired a cement division from its affiliate through slump sale, on a going concern basis, with a capacity to manufacture 3.55 mtpa of grey cement and 0.3 mtpa of white cement along with 15 MW of captive power plant

The Company got listed on the BSE

Successfully raised INR 2,960 mn through the Follow on Public Offer (“FPO”)

Commissioned a 3 mtpa Greenfield plant in south at Muddapur, Karnataka

Company’s long term credit rating upgraded from A+ to AA- by CARE Rating.

Enhanced grey cement capacity by 0.50 mtpa, set up a 20MW coal based power plant and 13.2MW of heat recovery based power plant at Nimbahera and enhanced white cement capacity by 0.1 mtpa at Gotan, through FPO proceeds

Acquired a 0.1 mtpa white cement unit at Gotan from Nihon Nirman and subsequently in 2009, converted the unit to produce 0.47 mtpa grey cement

“National Award for Excellence in Cost Management – 2011” from ICAI

“Best Employer Award - 2011” from Employer’s Association of Rajasthan

Commissioned a 1.5 mtpa grey cement capacity at Mangrol (Rajasthan) Commissioned a 0.6 mtpa white cement capacity at Fujairah (UAE)

Commissioned a 1.5 mtpa grinding unit for grey cement capacity at Jhajjar (Haryana)

7.5 2.8 0.8 0.5 0.5

3.0 3.0

FY '04 FY '05 FY '07 FY '09 FY '10 FY '15

10.5 Grey Cement capacity Build up

Strictly Private & Confidential

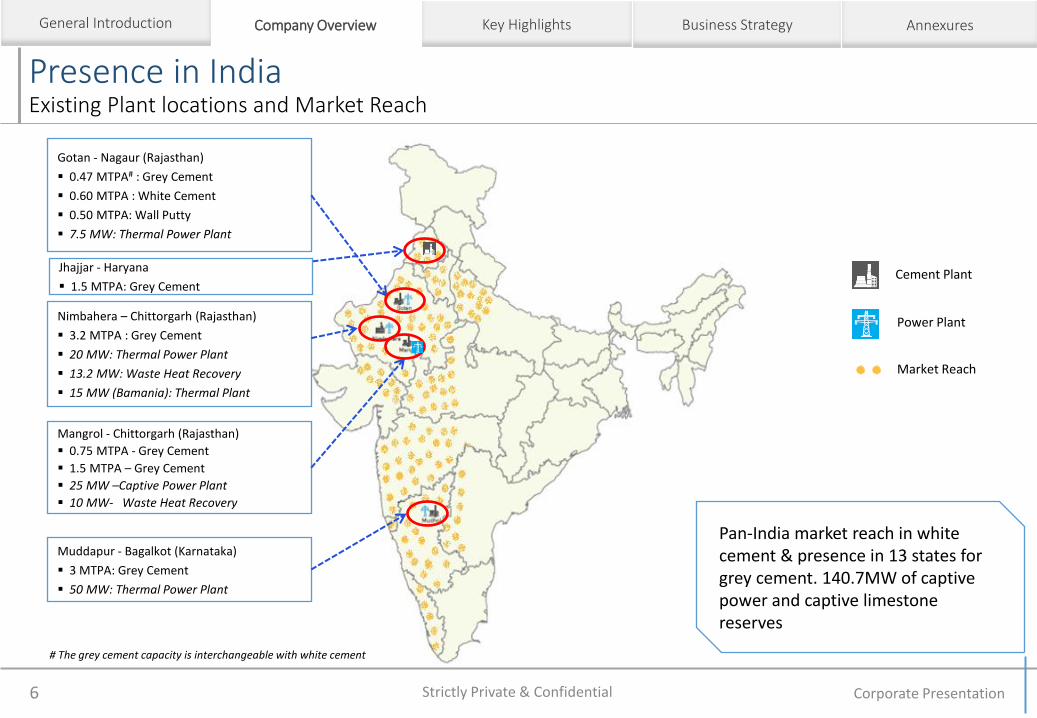

Presence in India Existing Plant locations and Market Reach

Corporate Presentation 6

Company Overview General Introduction Key Highlights Business Strategy Annexures

Cement Plant

Power Plant

Market Reach

Gotan - Nagaur (Rajasthan)

0.47 MTPA# : Grey Cement

0.60 MTPA : White Cement

0.50 MTPA: Wall Putty

7.5 MW: Thermal Power Plant

Nimbahera – Chittorgarh (Rajasthan)

3.2 MTPA : Grey Cement

20 MW: Thermal Power Plant

13.2 MW: Waste Heat Recovery

15 MW (Bamania): Thermal Plant

Mangrol - Chittorgarh (Rajasthan)

0.75 MTPA - Grey Cement

1.5 MTPA – Grey Cement

25 MW –Captive Power Plant

10 MW- Waste Heat Recovery

Muddapur - Bagalkot (Karnataka)

3 MTPA: Grey Cement

50 MW: Thermal Power Plant

Pan-India market reach in white cement & presence in 13 states for grey cement. 140.7MW of captive power and captive limestone reserves

# The grey cement capacity is interchangeable with white cement

Jhajjar - Haryana

1.5 MTPA: Grey Cement

Strictly Private & Confidential

Key Highlights One of the leading grey cement producers in North India

Corporate Presentation 7

Key Highlights General Introduction Company Overview Business Strategy Annexures

Cement Sector on Strong Foundation with Positive Future Outlook

Sustained demand coupled with slowdown in capacity addition resulting in higher capacity utilization

Improvement in profitability, backed by higher cement prices and operating margins

Integrated manufacturing facilities at multiple locations

Plants in North & South India enable the company to serve multiple regions

140.7 MW of captive power including waste heat recovery of 23.2 MW and large captive limestone reserves at close proximity

Presence in White cement business with strong growth and profitability

White cement & wall putty segments contribute consistently to profitability and provide healthy margins & stable cash flows

Increased White cement capacity to augment current market share of ~43% (Based on FY ’14 performance).

Wall putty capacity is 0.5 mtpa and plan to increase capacity by 0.2 mtpa by end of fiscal 2016.

Domestic expansion to consolidate leadership in North and improve operating efficiencies

Expansion plan to tap new markets, increase market share in North India and derive benefit from VAT incentives for entire production at Mangrol and Haryana

North based plants operated at 85%+ and newer plants will offer better operating efficiency

Increase in share from south plant, which serves higher realization markets, will improve margins

Dual process plant in UAE to grow internationally

Cater to white cement demand in Middle East & North Africa(MENA) and infrastructure development projects in Qatar

Unit in UAE provides logistical advantage to serve GCC and MENA countries and frees up current export quantity from India for domestic sale

Strictly Private & Confidential

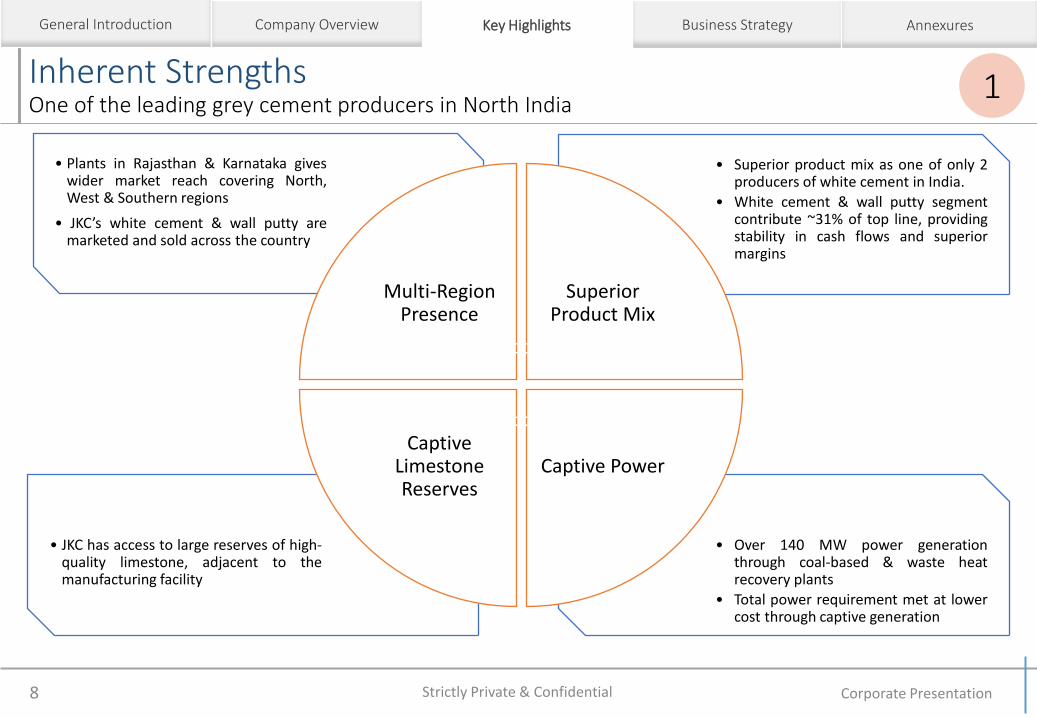

Inherent Strengths One of the leading grey cement producers in North India

Corporate Presentation 8

1

Key Highlights General Introduction Company Overview Business Strategy Annexures

• Over 140 MW power generation through coal-based & waste heat recovery plants

• Total power requirement met at lower cost through captive generation

• JKC has access to large reserves of high-quality limestone, adjacent to the manufacturing facility

• Superior product mix as one of only 2 producers of white cement in India.

• White cement & wall putty segment contribute ~31% of top line, providing stability in cash flows and superior margins

• Plants in Rajasthan & Karnataka gives wider market reach covering North, West & Southern regions

• JKC’s white cement & wall putty are marketed and sold across the country

Multi-Region Presence

Superior Product Mix

Captive Power Captive

Limestone Reserves

Strictly Private & Confidential

Established Brands Well established brands in all segments that the Company operates in

Corporate Presentation 9

Key Highlights General Introduction Company Overview Business Strategy Annexures

2

White Cement Value Added Products

J.K. White Cement is marketed and distributed across the country White cement based Wall Putty and Water Proofing Compound

Grey Cement

Ordinary Portland Cement (OPC) is sold under the J.K. Cement brand name, Sarvashaktiman

Portland Pozzolana Cement (PPC) and Portland Slag Cement (PSC) variants are sold under the J.K. Super Cement brand name

Strictly Private & Confidential

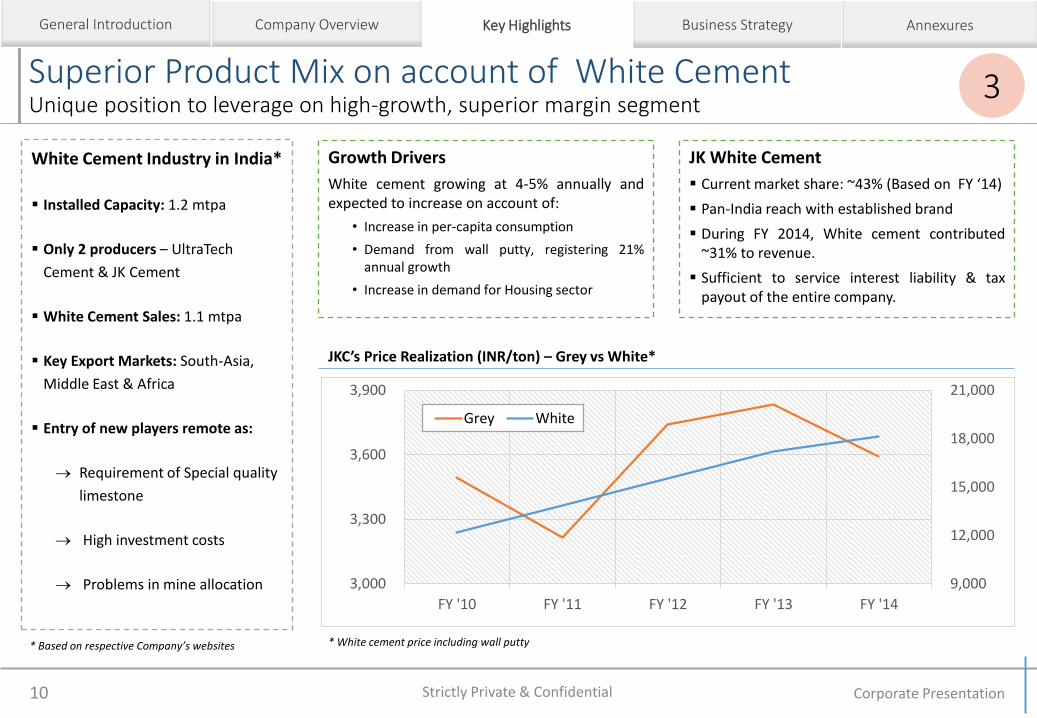

Superior Product Mix on account of White Cement Unique position to leverage on high-growth, superior margin segment

Corporate Presentation 10

Key Highlights General Introduction Company Overview Business Strategy Annexures

3

White Cement Industry in India*

Installed Capacity: 1.2 mtpa

Only 2 producers – UltraTech

Cement & JK Cement

White Cement Sales: 1.1 mtpa

Key Export Markets: South-Asia,

Middle East & Africa

Entry of new players remote as:

Requirement of Special quality

limestone

High investment costs

Problems in mine allocation

Growth Drivers

White cement growing at 4-5% annually and expected to increase on account of:

• Increase in per-capita consumption

• Demand from wall putty, registering 21% annual growth

• Increase in demand for Housing sector

JK White Cement

Current market share: ~43% (Based on FY ‘14)

Pan-India reach with established brand

During FY 2014, White cement contributed ~31% to revenue.

Sufficient to service interest liability & tax payout of the entire company.

9,000

12,000

15,000

18,000

21,000

3,000

3,300

3,600

3,900

FY '10 FY '11 FY '12 FY '13 FY '14

Grey White

* White cement price including wall putty

JKC’s Price Realization (INR/ton) – Grey vs White*

Strictly Private & Confidential

* Based on respective Company’s websites

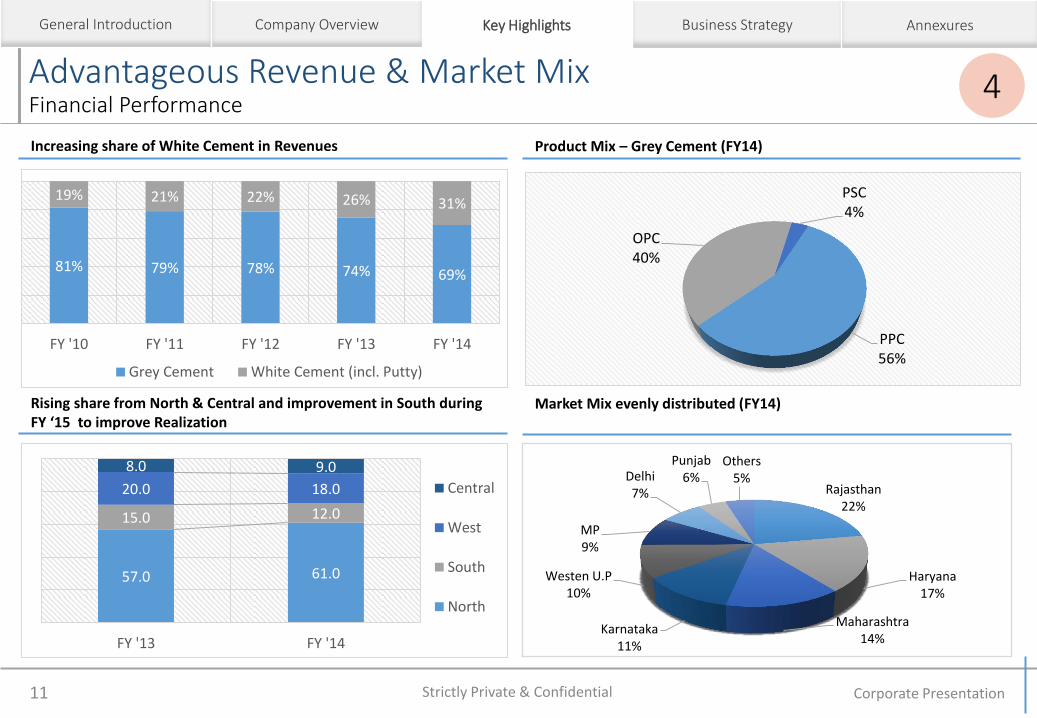

Advantageous Revenue & Market Mix Financial Performance

Corporate Presentation 11

Increasing share of White Cement in Revenues Product Mix – Grey Cement (FY14)

Rising share from North & Central and improvement in South during FY ‘15 to improve Realization

Market Mix evenly distributed (FY14)

Key Highlights General Introduction Company Overview Business Strategy Annexures

81% 79% 78% 74% 69%

19% 21% 22% 26% 31%

FY '10 FY '11 FY '12 FY '13 FY '14

Grey Cement White Cement (incl. Putty)

4

PPC 56%

OPC 40%

PSC 4%

57.0 61.0

15.0 12.0

20.0 18.0

8.0 9.0

FY '13 FY '14

Central

West

South

North

Rajasthan 22%

Haryana 17%

Maharashtra 14%

Karnataka 11%

Westen U.P 10%

MP 9%

Delhi 7%

Punjab 6%

Others 5%

Strictly Private & Confidential

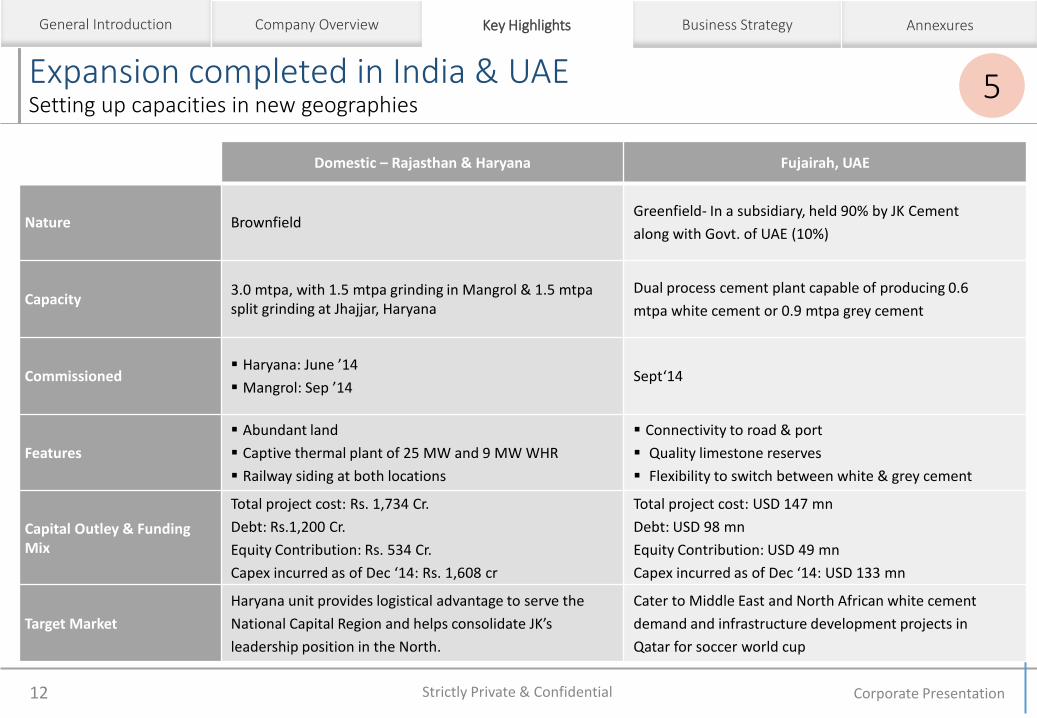

Expansion completed in India & UAE Setting up capacities in new geographies

Corporate Presentation 12

Key Highlights General Introduction Company Overview Business Strategy Annexures

Domestic – Rajasthan & Haryana Fujairah, UAE

Nature Brownfield Greenfield- In a subsidiary, held 90% by JK Cement

along with Govt. of UAE (10%)

Capacity 3.0 mtpa, with 1.5 mtpa grinding in Mangrol & 1.5 mtpa split grinding at Jhajjar, Haryana

Dual process cement plant capable of producing 0.6

mtpa white cement or 0.9 mtpa grey cement

Commissioned Haryana: June ’14

Mangrol: Sep ’14 Sept‘14

Features

Abundant land

Captive thermal plant of 25 MW and 9 MW WHR

Railway siding at both locations

Connectivity to road & port

Quality limestone reserves

Flexibility to switch between white & grey cement

Capital Outley & Funding Mix

Total project cost: Rs. 1,734 Cr.

Debt: Rs.1,200 Cr.

Equity Contribution: Rs. 534 Cr.

Capex incurred as of Dec ‘14: Rs. 1,608 cr

Total project cost: USD 147 mn

Debt: USD 98 mn

Equity Contribution: USD 49 mn

Capex incurred as of Dec ‘14: USD 133 mn

Target Market

Haryana unit provides logistical advantage to serve the

National Capital Region and helps consolidate JK’s

leadership position in the North.

Cater to Middle East and North African white cement

demand and infrastructure development projects in

Qatar for soccer world cup

5

Strictly Private & Confidential

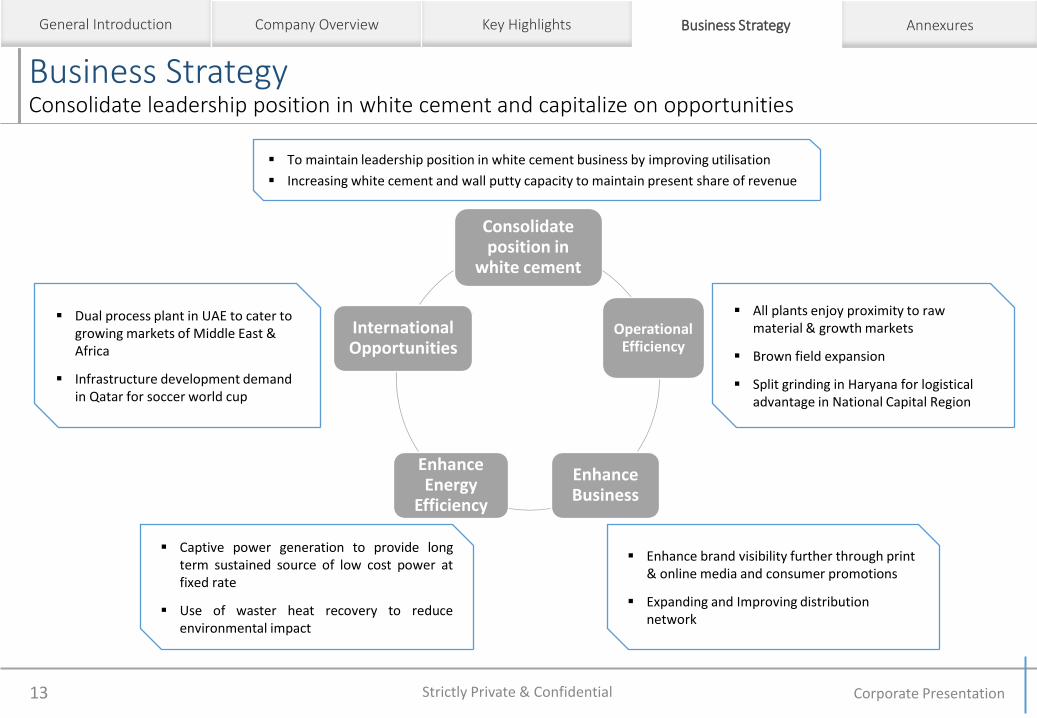

Business Strategy Consolidate leadership position in white cement and capitalize on opportunities

Corporate Presentation 13

Business Strategy General Introduction Company Overview Key Highlights Annexures

Consolidate position in

white cement

Operational Efficiency

Enhance Business

Enhance Energy

Efficiency

International Opportunities

To maintain leadership position in white cement business by improving utilisation

Increasing white cement and wall putty capacity to maintain present share of revenue

All plants enjoy proximity to raw material & growth markets

Brown field expansion

Split grinding in Haryana for logistical advantage in National Capital Region

Enhance brand visibility further through print & online media and consumer promotions

Expanding and Improving distribution network

Captive power generation to provide long term sustained source of low cost power at fixed rate

Use of waster heat recovery to reduce environmental impact

Dual process plant in UAE to cater to growing markets of Middle East & Africa

Infrastructure development demand in Qatar for soccer world cup

Strictly Private & Confidential

FY 2015

Thank you for your Interest

Annexures Follow

J.K. CEMENT LIMITED Kamla Tower, Kanpur-208001

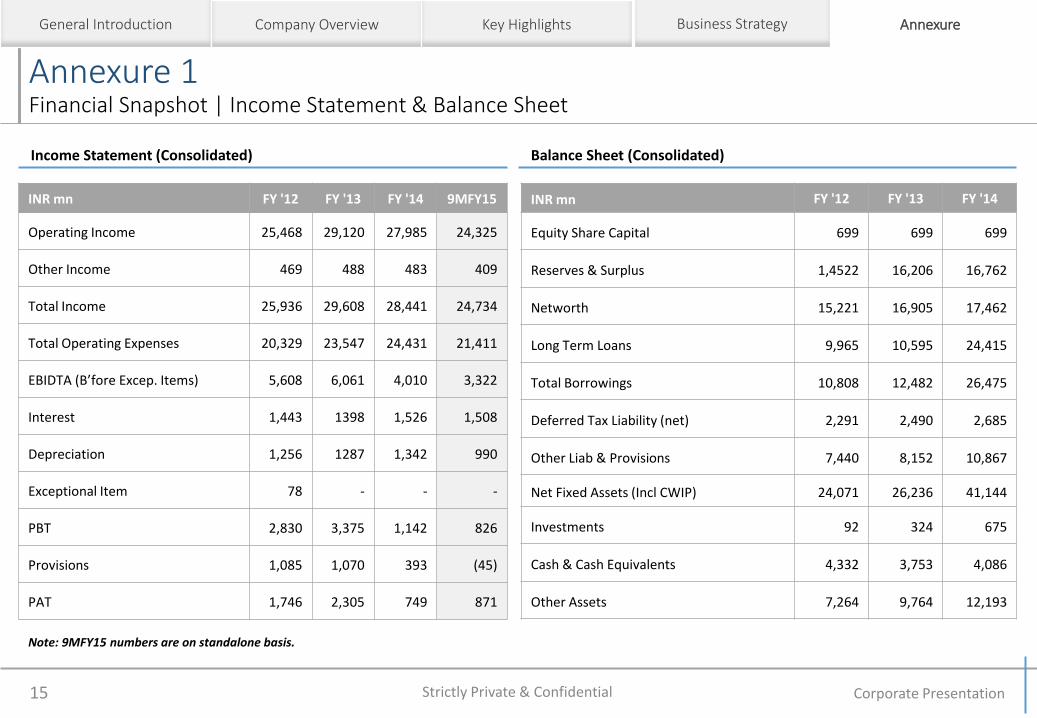

Annexure 1 Financial Snapshot | Income Statement & Balance Sheet

Corporate Presentation 15

Balance Sheet (Consolidated) Income Statement (Consolidated)

Annexure General Introduction Company Overview Key Highlights Business Strategy

INR mn FY '12 FY '13 FY '14 9MFY15

Operating Income 25,468 29,120 27,985 24,325

Other Income 469 488 483 409

Total Income 25,936 29,608 28,441 24,734

Total Operating Expenses 20,329 23,547 24,431 21,411

EBIDTA (B’fore Excep. Items) 5,608 6,061 4,010 3,322

Interest 1,443 1398 1,526 1,508

Depreciation 1,256 1287 1,342 990

Exceptional Item 78 - - -

PBT 2,830 3,375 1,142 826

Provisions 1,085 1,070 393 (45)

PAT 1,746 2,305 749 871

INR mn FY '12 FY '13 FY '14

Equity Share Capital 699 699 699

Reserves & Surplus 1,4522 16,206 16,762

Networth 15,221 16,905 17,462

Long Term Loans 9,965 10,595 24,415

Total Borrowings 10,808 12,482 26,475

Deferred Tax Liability (net) 2,291 2,490 2,685

Other Liab & Provisions 7,440 8,152 10,867

Net Fixed Assets (Incl CWIP) 24,071 26,236 41,144

Investments 92 324 675

Cash & Cash Equivalents 4,332 3,753 4,086

Other Assets 7,264 9,764 12,193

Note: 9MFY15 numbers are on standalone basis.

Strictly Private & Confidential

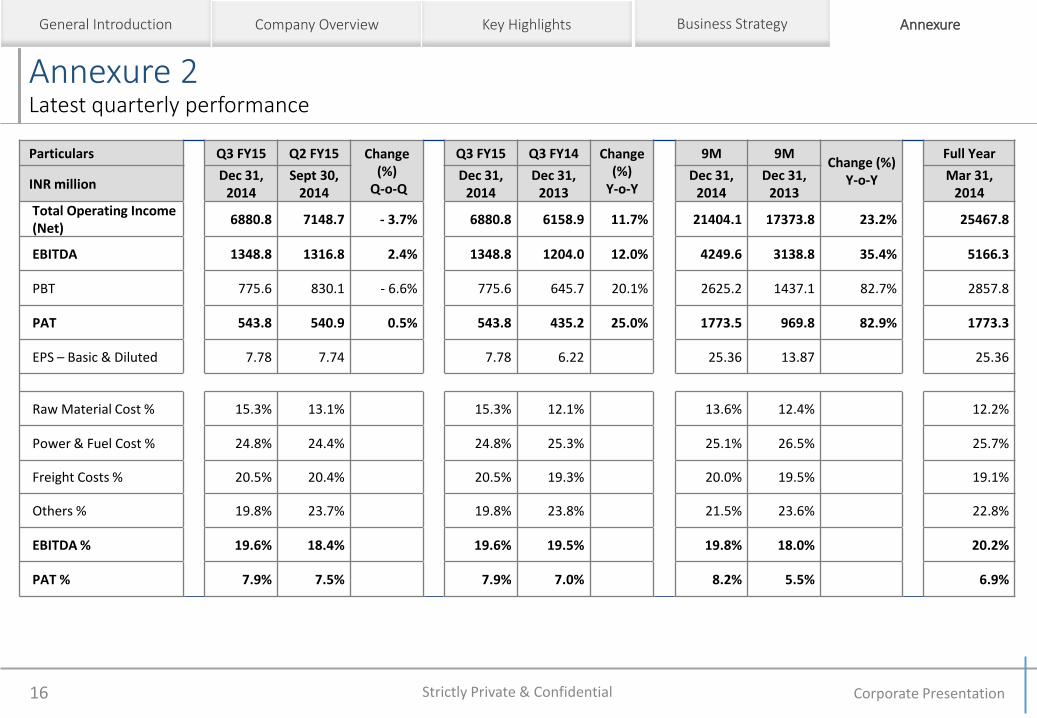

Annexure 2 Latest quarterly performance

Corporate Presentation 16

Annexure General Introduction Company Overview Key Highlights Business Strategy

Particulars Q3 FY15 Q2 FY15 Change (%)

Q-o-Q

Q3 FY15 Q3 FY14 Change (%)

Y-o-Y

9M 9M Change (%)

Y-o-Y

Full Year

INR million Dec 31,

2014 Sept 30,

2014 Dec 31,

2014 Dec 31,

2013 Dec 31,

2014 Dec 31,

2013 Mar 31,

2014 Total Operating Income

(Net) 6880.8 7148.7 - 3.7% 6880.8 6158.9 11.7% 21404.1 17373.8 23.2% 25467.8

EBITDA 1348.8 1316.8 2.4% 1348.8 1204.0 12.0% 4249.6 3138.8 35.4% 5166.3

PBT 775.6 830.1 - 6.6% 775.6 645.7 20.1% 2625.2 1437.1 82.7% 2857.8

PAT 543.8 540.9 0.5% 543.8 435.2 25.0% 1773.5 969.8 82.9% 1773.3

EPS – Basic & Diluted 7.78 7.74 7.78 6.22 25.36 13.87 25.36

Raw Material Cost % 15.3% 13.1% 15.3% 12.1% 13.6% 12.4% 12.2%

Power & Fuel Cost % 24.8% 24.4% 24.8% 25.3% 25.1% 26.5% 25.7%

Freight Costs % 20.5% 20.4% 20.5% 19.3% 20.0% 19.5% 19.1%

Others % 19.8% 23.7% 19.8% 23.8% 21.5% 23.6% 22.8%

EBITDA % 19.6% 18.4% 19.6% 19.5% 19.8% 18.0% 20.2%

PAT % 7.9% 7.5% 7.9% 7.0% 8.2% 5.5% 6.9%

Strictly Private & Confidential

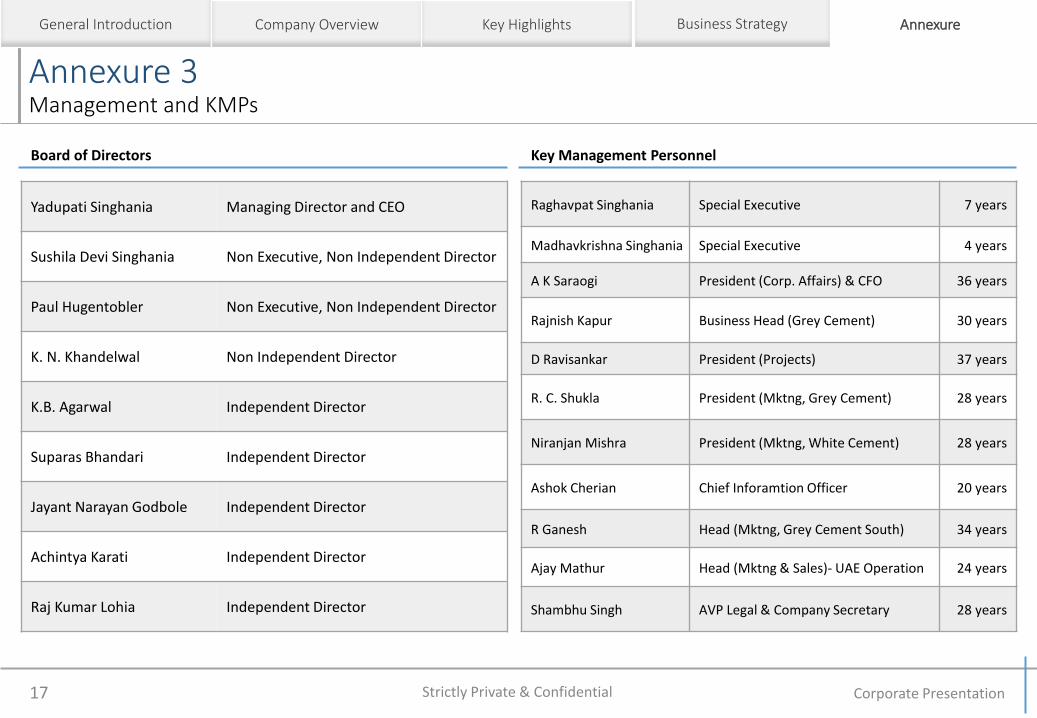

Annexure 3 Management and KMPs

Corporate Presentation 17

Annexure General Introduction Company Overview Key Highlights Business Strategy

Key Management Personnel Board of Directors

Yadupati Singhania Managing Director and CEO

Sushila Devi Singhania Non Executive, Non Independent Director

Paul Hugentobler Non Executive, Non Independent Director

K. N. Khandelwal Non Independent Director

K.B. Agarwal Independent Director

Suparas Bhandari Independent Director

Jayant Narayan Godbole Independent Director

Achintya Karati Independent Director

Raj Kumar Lohia Independent Director

Raghavpat Singhania Special Executive 7 years

Madhavkrishna Singhania Special Executive 4 years

A K Saraogi President (Corp. Affairs) & CFO 36 years

Rajnish Kapur Business Head (Grey Cement) 30 years

D Ravisankar President (Projects) 37 years

R. C. Shukla President (Mktng, Grey Cement) 28 years

Niranjan Mishra President (Mktng, White Cement) 28 years

Ashok Cherian Chief Inforamtion Officer 20 years

R Ganesh Head (Mktng, Grey Cement South) 34 years

Ajay Mathur Head (Mktng & Sales)- UAE Operation 24 years

Shambhu Singh AVP Legal & Company Secretary 28 years

Strictly Private & Confidential

Annexure 4 Awards & Recognitions

Corporate Presentation 18

Annexure General Introduction Company Overview Key Highlights Business Strategy

9th National Award for Excellence in Cost Management, 2011 (The Institute of Cost Accountants of India)

Commemorative Stamp in honor of the Founding Father

Productivity Excellence Award 2009-10 (Rajasthan State Productivity Council)

Over All Performance Award by Indian Bureau of Mines

Best Employer Award, 2011 Employers’ Association of Rajasthan

Strictly Private & Confidential

Best Employer Award in Northern Region, 2012 Employer’s Association of Northern India