funding and investment opportunities in current …. a k kinra.pdf · funding and investment...

TRANSCRIPT

Funding and Investment Opportunities Funding and Investment Opportunities in in

Current Economic EnvironmentCurrent Economic Environment

February 11, 2011

Presented By

A.K. KINRA

Finance Director

JK Tyre & Industries Ltd.

� Indian Economy Overview

� Economic Growth

� Interest Rate & Inflation

� Financial Markets Overview

� Financing Options

Contents

� Financing Options

� Potential Investment Oppurtunities

� 2011: Challenges

2

Indian Economy Overview

3

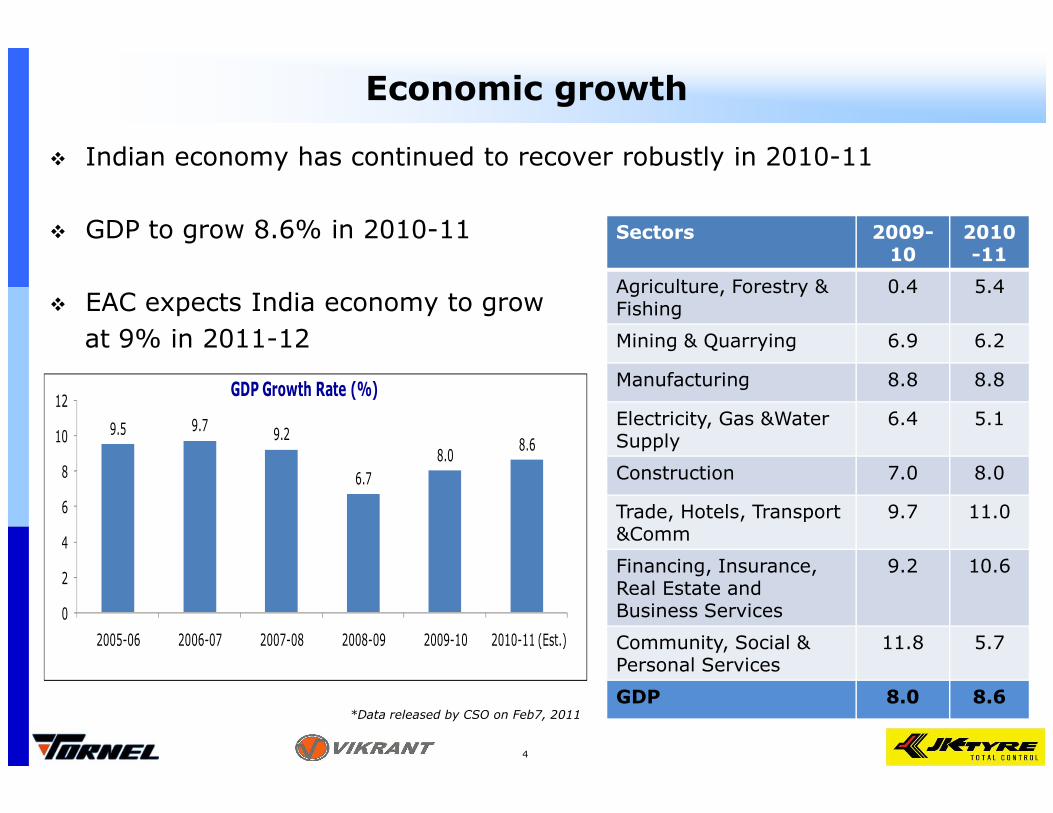

Economic growth

� Indian economy has continued to recover robustly in 2010-11

� GDP to grow 8.6% in 2010-11

� EAC expects India economy to grow

at 9% in 2011-12

12GDP Growth Rate (%)

Sectors 2009-10

2010-11

Agriculture, Forestry & Fishing

0.4 5.4

Mining & Quarrying 6.9 6.2

Manufacturing 8.8 8.8

Electricity, Gas &Water 6.4 5.19.5 9.7

9.2

6.7

8.08.6

0

2

4

6

8

10

12

2005-06 2006-07 2007-08 2008-09 2009-10 2010-11 (Est.)

4

Electricity, Gas &Water Supply

6.4 5.1

Construction 7.0 8.0

Trade, Hotels, Transport &Comm

9.7 11.0

Financing, Insurance, Real Estate and Business Services

9.2 10.6

Community, Social & Personal Services

11.8 5.7

GDP 8.0 8.6*Data released by CSO on Feb7, 2011

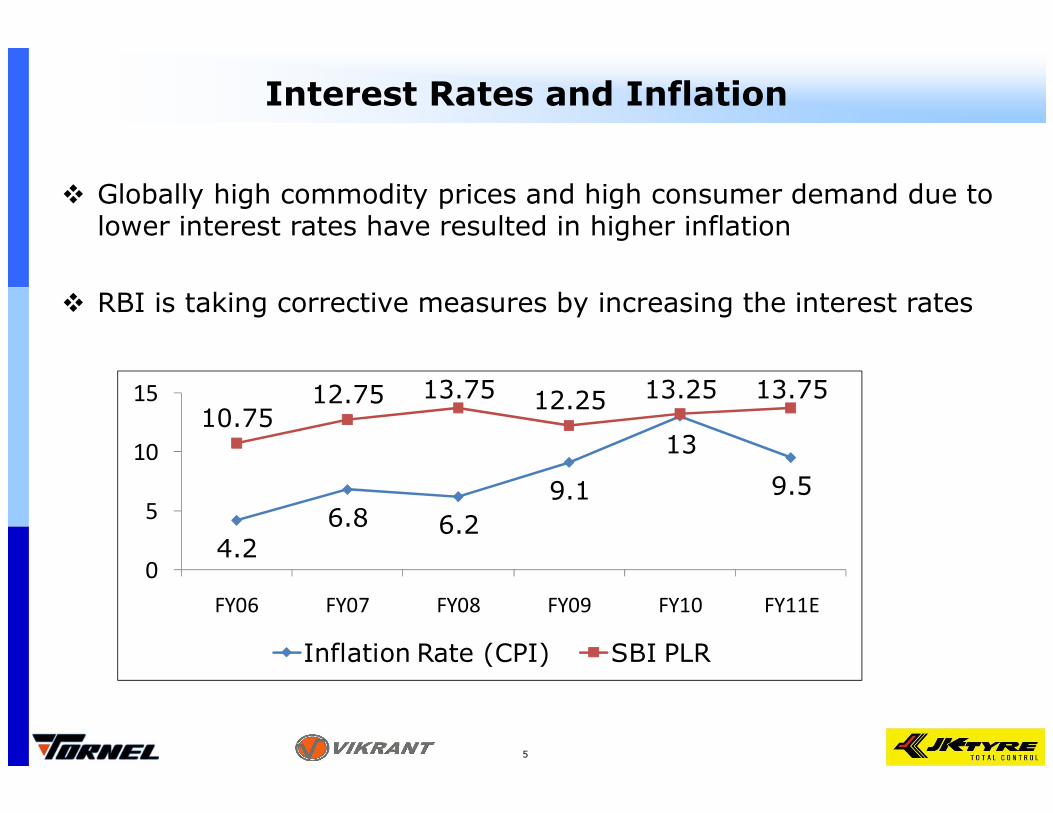

Interest Rates and Inflation

� Globally high commodity prices and high consumer demand due to lower interest rates have resulted in higher inflation

� RBI is taking corrective measures by increasing the interest rates

10.7512.75 13.75 12.25 13.25 13.7515

5

4.26.8 6.2

9.1

13

9.5

10.7512.75 12.25

0

5

10

FY06 FY07 FY08 FY09 FY10 FY11E

Inflation Rate (CPI) SBI PLR

Financial Market Overview

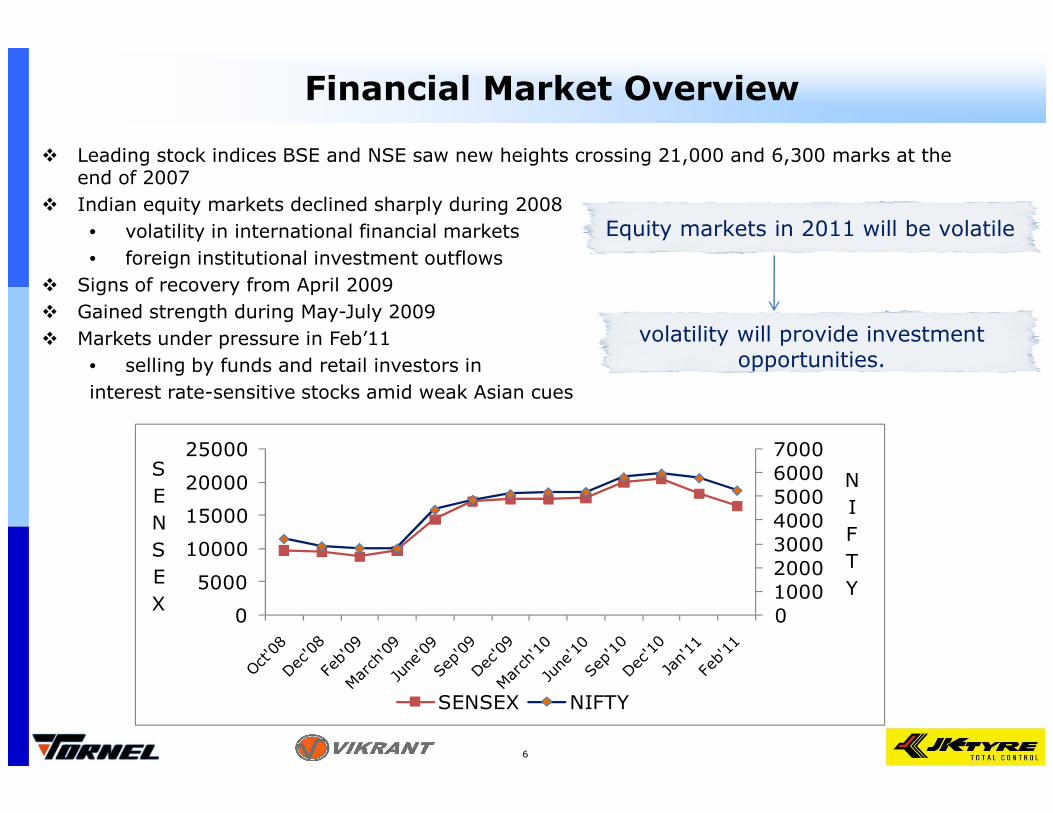

� Leading stock indices BSE and NSE saw new heights crossing 21,000 and 6,300 marks at the end of 2007

� Indian equity markets declined sharply during 2008

• volatility in international financial markets

• foreign institutional investment outflows

� Signs of recovery from April 2009

� Gained strength during May-July 2009

� Markets under pressure in Feb’11

• selling by funds and retail investors in

interest rate-sensitive stocks amid weak Asian cues

Equity markets in 2011 will be volatile

volatility will provide investment opportunities.

6

0

1000

2000

3000

4000

5000

6000

7000

0

5000

10000

15000

20000

25000

N

I

F

T

Y

S

E

N

S

E

X

SENSEX NIFTY

Overview of Indian Equity Capital Market

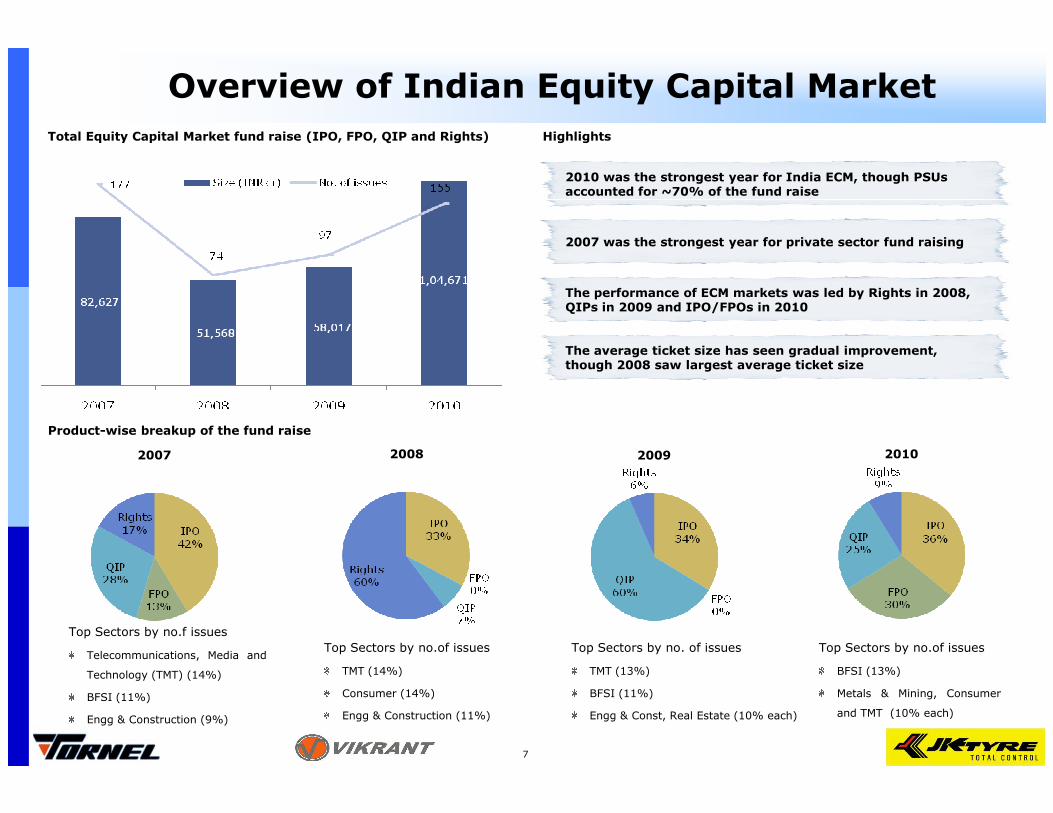

Total Equity Capital Market fund raise (IPO, FPO, QIP and Rights)

2010 was the strongest year for India ECM, though PSUs accounted for ~70% of the fund raise

2007 was the strongest year for private sector fund raising

The performance of ECM markets was led by Rights in 2008, QIPs in 2009 and IPO/FPOs in 2010

The average ticket size has seen gradual improvement, though 2008 saw largest average ticket size

Highlights

7

Product-wise breakup of the fund raise

2007 2008 2009 2010

Top Sectors by no.f issues

Telecommunications, Media and

Technology (TMT) (14%)

BFSI (11%)

Engg & Construction (9%)

Top Sectors by no.of issues

TMT (14%)

Consumer (14%)

Engg & Construction (11%)

Top Sectors by no. of issues

TMT (13%)

BFSI (11%)

Engg & Const, Real Estate (10% each)

Top Sectors by no.of issues

BFSI (13%)

Metals & Mining, Consumer

and TMT (10% each)

22,810

20,873

6,264

16,823

20

6

11

20

2007 2008 2009 2010

BFSI Power & Energy Metals & Mining Real Estate Engg & Construction

Size (INR cr) No. of issues

7,739

12,588

17,58920,277

7 7

8

11

2007 2008 2009 2010

10,131

5,354 3,138

27,840

11

6

4

16

2007 2008 2009 2010

16,351

10,525

6,092

12

0

10 10

2007 2008 2009 2010

2,850

558

4,378

5,648

16

8

10

14

2007 2008 2009 2010

Overall Decrease in Size Steady performance except in 2008

Appetite in 2010 Lower Compared to Improving Markets

Disinvestment Led Spurt in 2010

Consistent Growth

Sector Analysis

2007 2008 2009 2010

Other Infra Healthcare & Pharma TMT Consumer Miscellaneous

2007 2008 2009 2010 2007 2008 2009 2010 2007 2008 2009 2010

7,677

1,882 2,026

5,263

12

5

4

10

2007 2008 2009 2010

786

154

2,153

1,468

5

4

5

6

2007 2008 2009 2010

5,242

2,262

3,1722,782

24

10

13

15

2007 2008 2009 2010

2,651

1,223

4,139

3,333

14

109

15

2007 2008 2009 2010

6,389 6,6734,632

15,146

56

18

23

38

2007 2008 2009 2010

Sharp drop in # of deals in 2008-2009

Increasing growth in 2009 & 2010

Gradual increase starting 2008

Varying size movements

8

IPO/FPO Market has seen Strong Revival in 2010

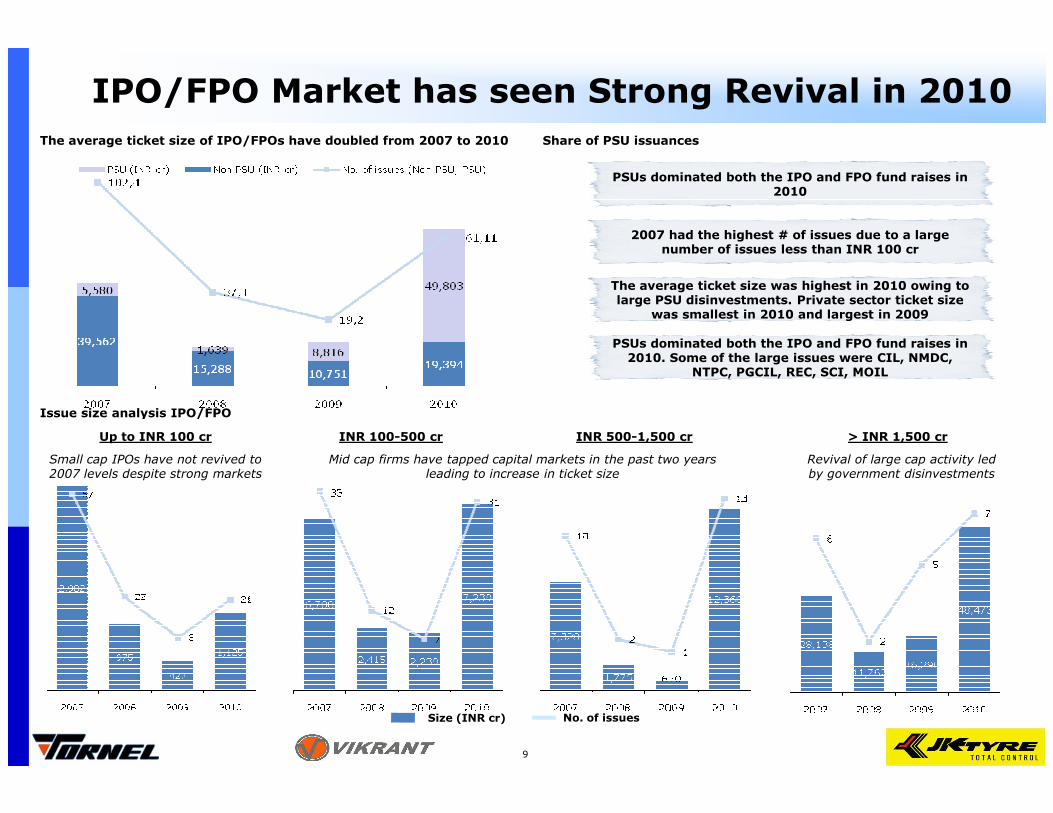

The average ticket size of IPO/FPOs have doubled from 2007 to 2010

Issue size analysis IPO/FPO

Share of PSU issuances

PSUs dominated both the IPO and FPO fund raises in 2010

2007 had the highest # of issues due to a large number of issues less than INR 100 cr

The average ticket size was highest in 2010 owing to large PSU disinvestments. Private sector ticket size

was smallest in 2010 and largest in 2009

PSUs dominated both the IPO and FPO fund raises in 2010. Some of the large issues were CIL, NMDC,

NTPC, PGCIL, REC, SCI, MOIL

9

Issue size analysis IPO/FPO

Up to INR 100 cr INR 100-500 cr INR 500-1,500 cr > INR 1,500 cr

Size (INR cr) No. of issues

Revival of large cap activity led by government disinvestments

Mid cap firms have tapped capital markets in the past two years leading to increase in ticket size

Small cap IPOs have not revived to 2007 levels despite strong markets

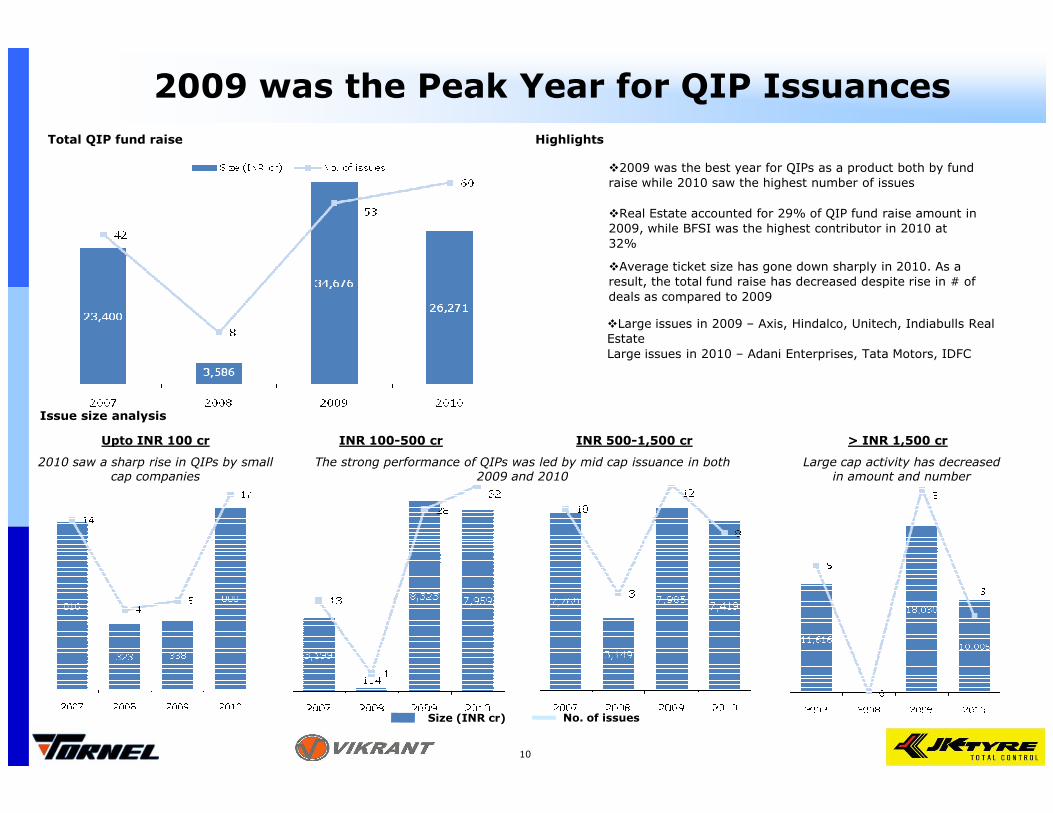

2009 was the Peak Year for QIP Issuances

Total QIP fund raise Highlights

�2009 was the best year for QIPs as a product both by fund

raise while 2010 saw the highest number of issues

�Real Estate accounted for 29% of QIP fund raise amount in

2009, while BFSI was the highest contributor in 2010 at

32%

�Average ticket size has gone down sharply in 2010. As a

result, the total fund raise has decreased despite rise in # of

deals as compared to 2009

�Large issues in 2009 – Axis, Hindalco, Unitech, Indiabulls Real

Estate

Large issues in 2010 – Adani Enterprises, Tata Motors, IDFC

10

Issue size analysis

Upto INR 100 cr INR 100-500 cr INR 500-1,500 cr > INR 1,500 cr

Size (INR cr) No. of issues

Large cap activity has decreased in amount and number

The strong performance of QIPs was led by mid cap issuance in both 2009 and 2010

2010 saw a sharp rise in QIPs by small cap companies

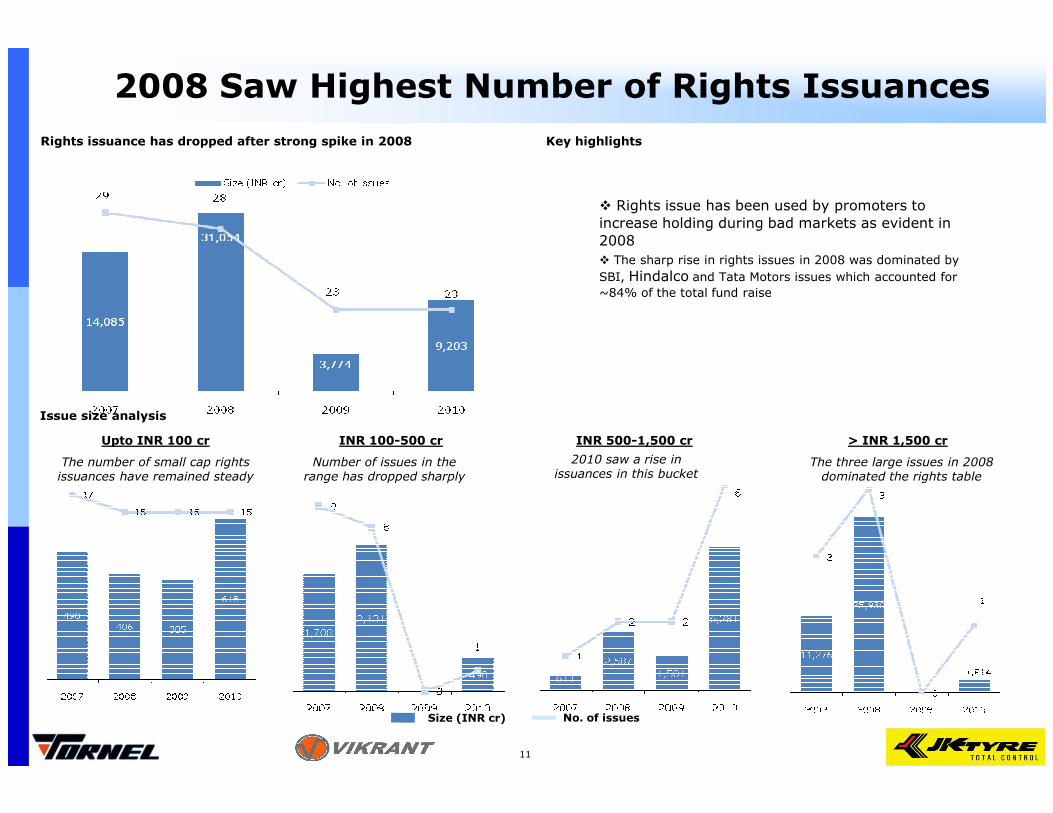

2008 Saw Highest Number of Rights Issuances

Rights issuance has dropped after strong spike in 2008

� Rights issue has been used by promoters to

increase holding during bad markets as evident in

2008

� The sharp rise in rights issues in 2008 was dominated by

SBI, Hindalco and Tata Motors issues which accounted for

~84% of the total fund raise

Key highlights

11

Issue size analysis

Upto INR 100 cr INR 100-500 cr INR 500-1,500 cr > INR 1,500 cr

Size (INR cr) No. of issues

The three large issues in 2008 dominated the rights table

Number of issues in the range has dropped sharply

The number of small cap rights issuances have remained steady

2010 saw a rise in issuances in this bucket

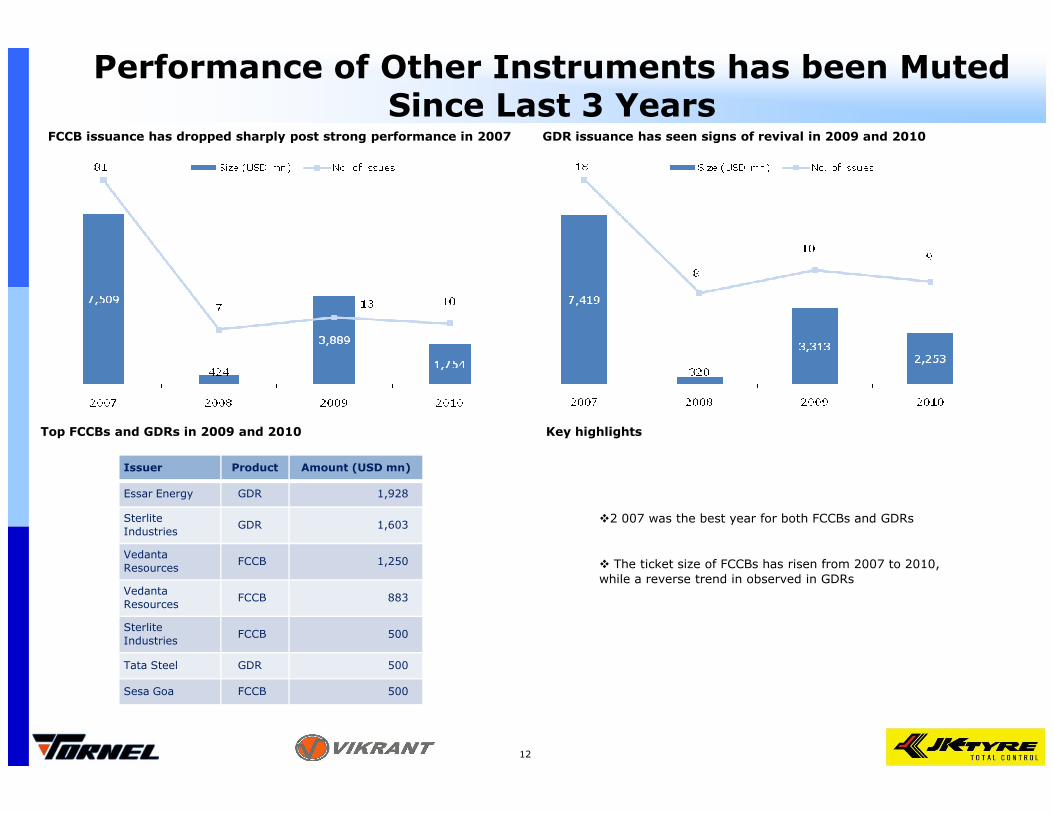

Performance of Other Instruments has been Muted Since Last 3 Years

GDR issuance has seen signs of revival in 2009 and 2010FCCB issuance has dropped sharply post strong performance in 2007

12

Top FCCBs and GDRs in 2009 and 2010

�2 007 was the best year for both FCCBs and GDRs

� The ticket size of FCCBs has risen from 2007 to 2010,

while a reverse trend in observed in GDRs

Key highlights

Issuer Product Amount (USD mn)

Essar Energy GDR 1,928

Sterlite

IndustriesGDR 1,603

Vedanta

ResourcesFCCB 1,250

Vedanta

ResourcesFCCB 883

Sterlite

IndustriesFCCB 500

Tata Steel GDR 500

Sesa Goa FCCB 500

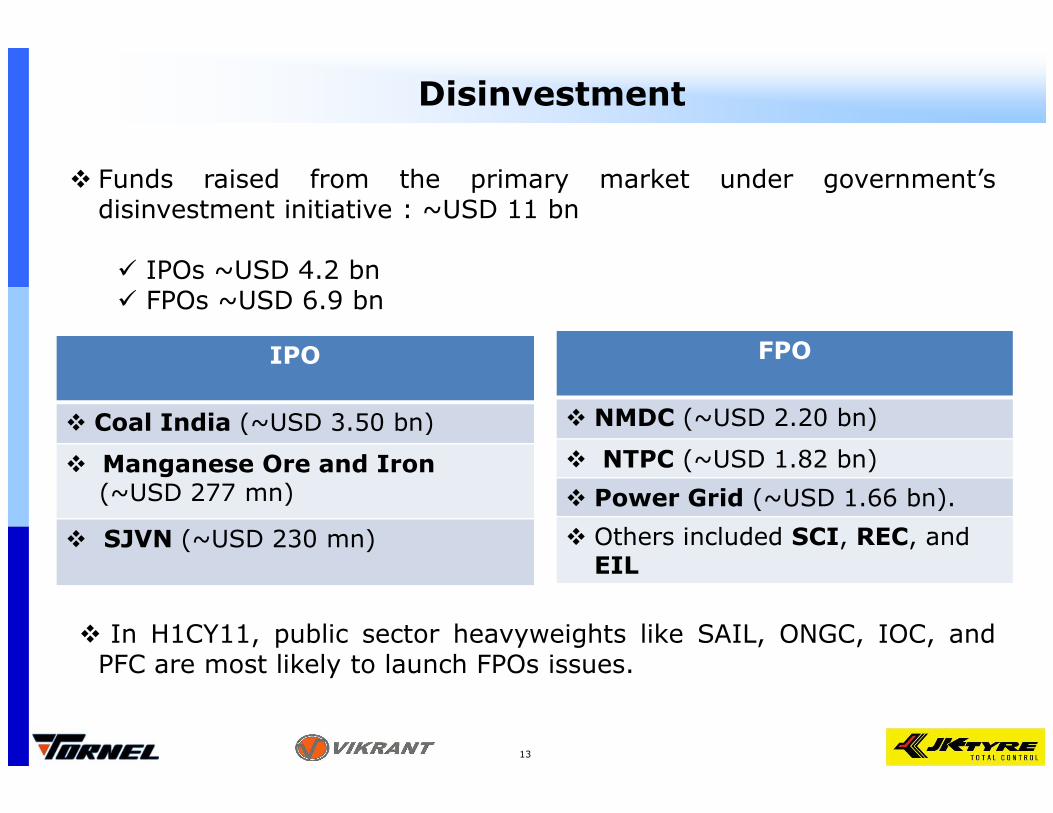

Disinvestment

� Funds raised from the primary market under government’sdisinvestment initiative : ~USD 11 bn

� IPOs ~USD 4.2 bn� FPOs ~USD 6.9 bn

FPO

� NMDC (~USD 2.20 bn)

IPO

Coal India (~USD 3.50 bn) � NMDC (~USD 2.20 bn)

� NTPC (~USD 1.82 bn)

� Power Grid (~USD 1.66 bn).

� Others included SCI, REC, and EIL

� Coal India (~USD 3.50 bn)

� Manganese Ore and Iron (~USD 277 mn)

� SJVN (~USD 230 mn)

� In H1CY11, public sector heavyweights like SAIL, ONGC, IOC, andPFC are most likely to launch FPOs issues.

13

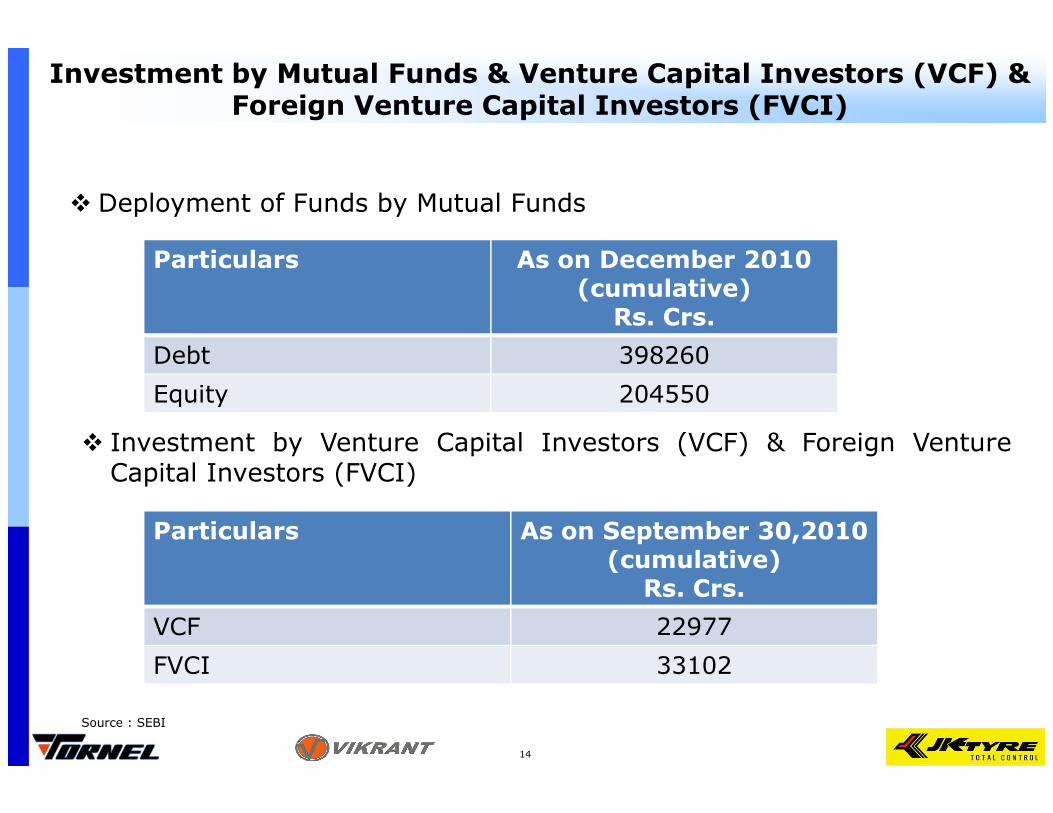

Investment by Mutual Funds & Venture Capital Investors (VCF) & Foreign Venture Capital Investors (FVCI)

� Deployment of Funds by Mutual Funds

Particulars As on December 2010 (cumulative)

Rs. Crs.

Debt 398260

Equity 204550

14

� Investment by Venture Capital Investors (VCF) & Foreign VentureCapital Investors (FVCI)

Equity 204550

Particulars As on September 30,2010 (cumulative)

Rs. Crs.

VCF 22977

FVCI 33102

Source : SEBI

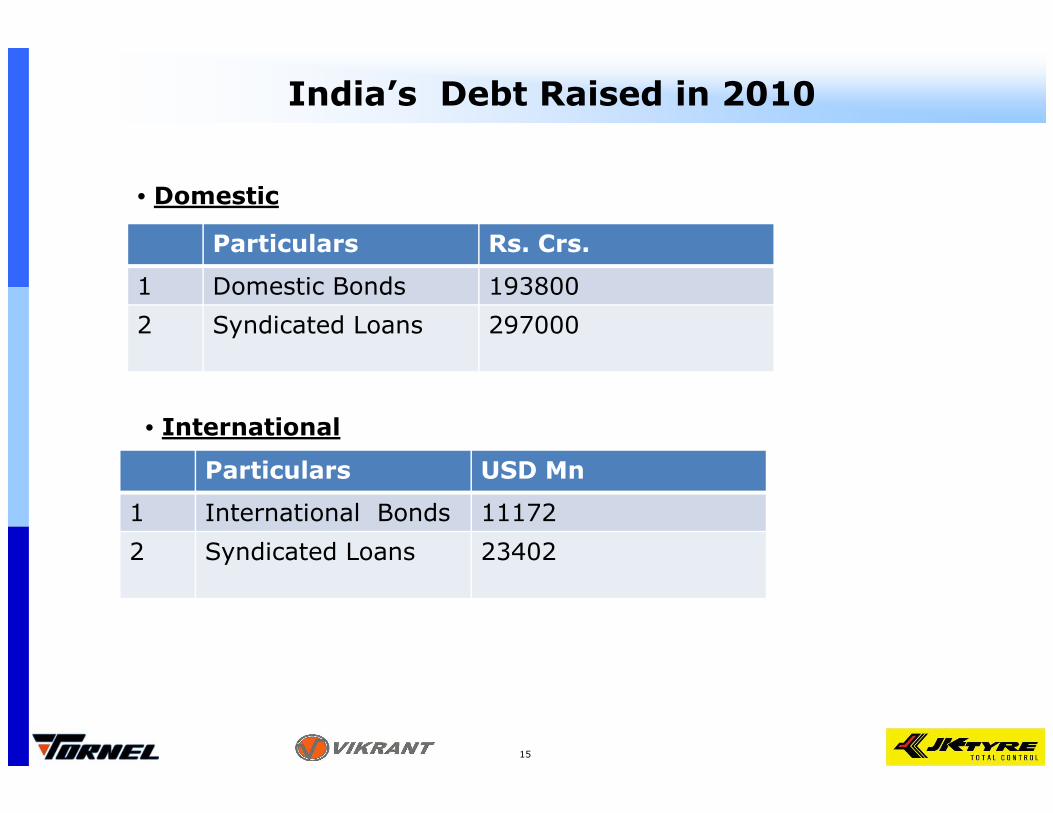

India’s Debt Raised in 2010

Particulars Rs. Crs.

1 Domestic Bonds 193800

2 Syndicated Loans 297000

• Domestic

15

Particulars USD Mn

1 International Bonds 11172

2 Syndicated Loans 23402

• International

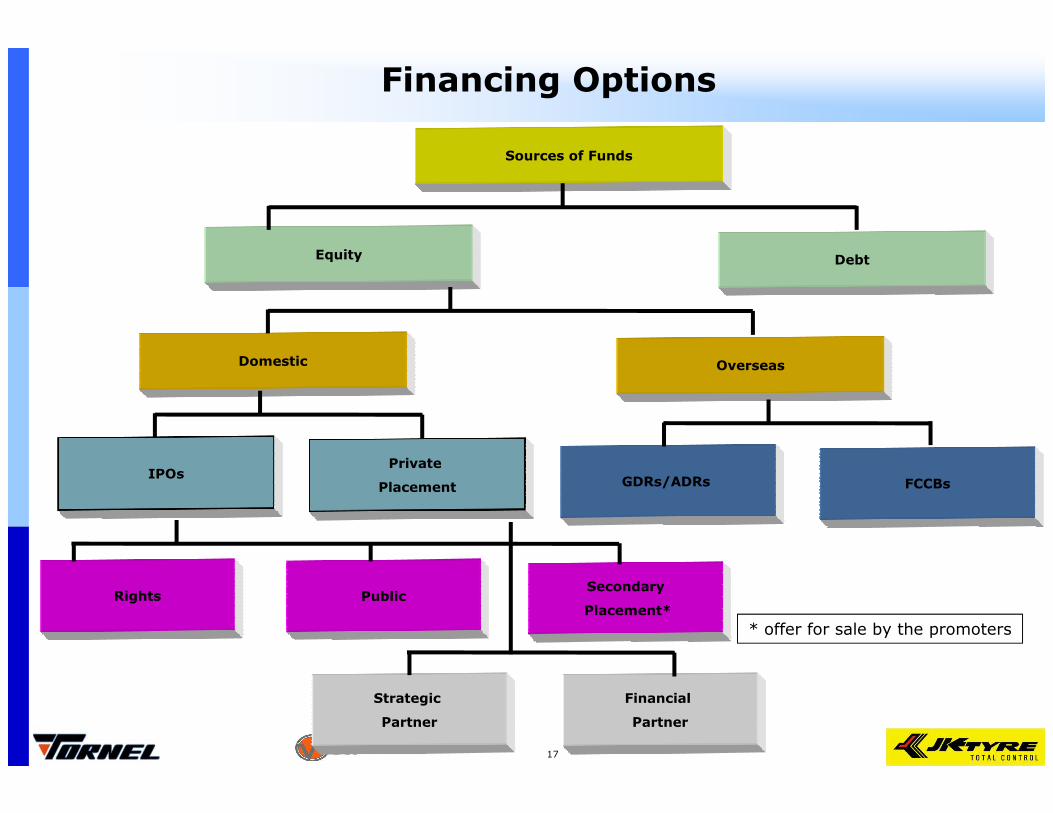

Financing Options

16

Equity

Sources of Funds

Financing Options

Domestic Overseas

Debt

Rights Public

Strategic

Partner

GDRs/ADRs

Private

PlacementIPOs

FCCBs

Financial

Partner

Secondary

Placement*

* offer for sale by the promoters

17

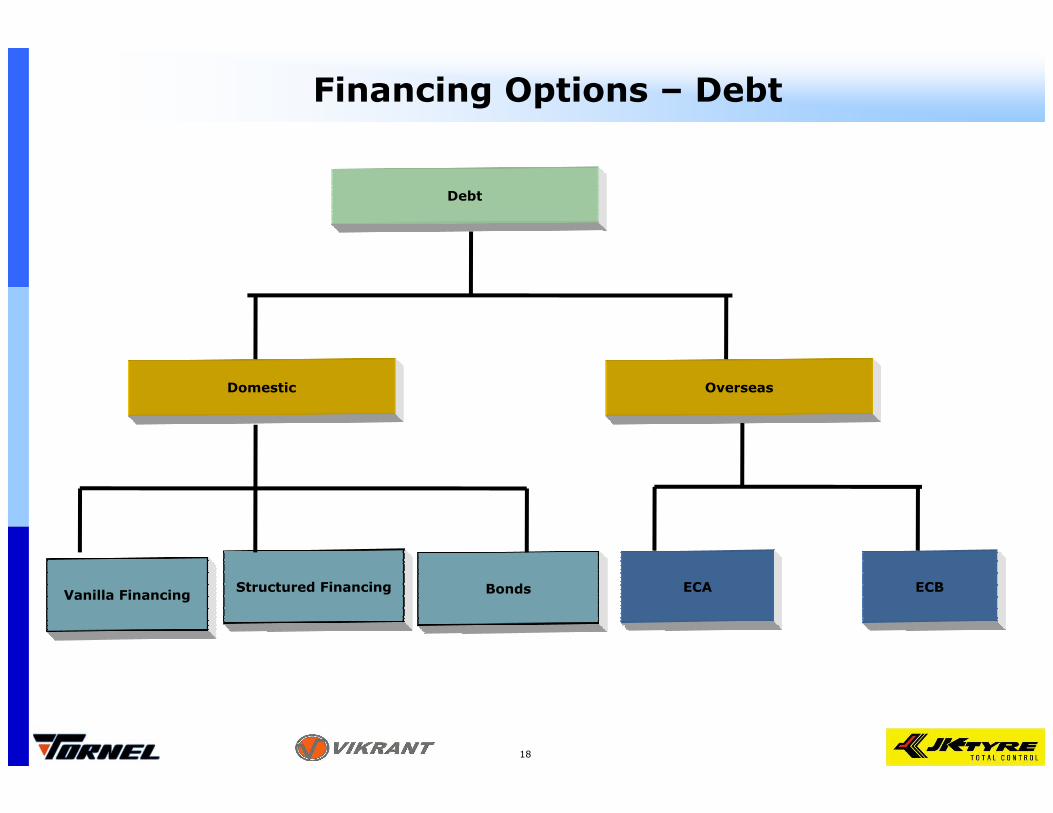

Financing Options – Debt

Domestic Overseas

Debt

ECAStructured FinancingVanilla Financing

18

ECBBonds

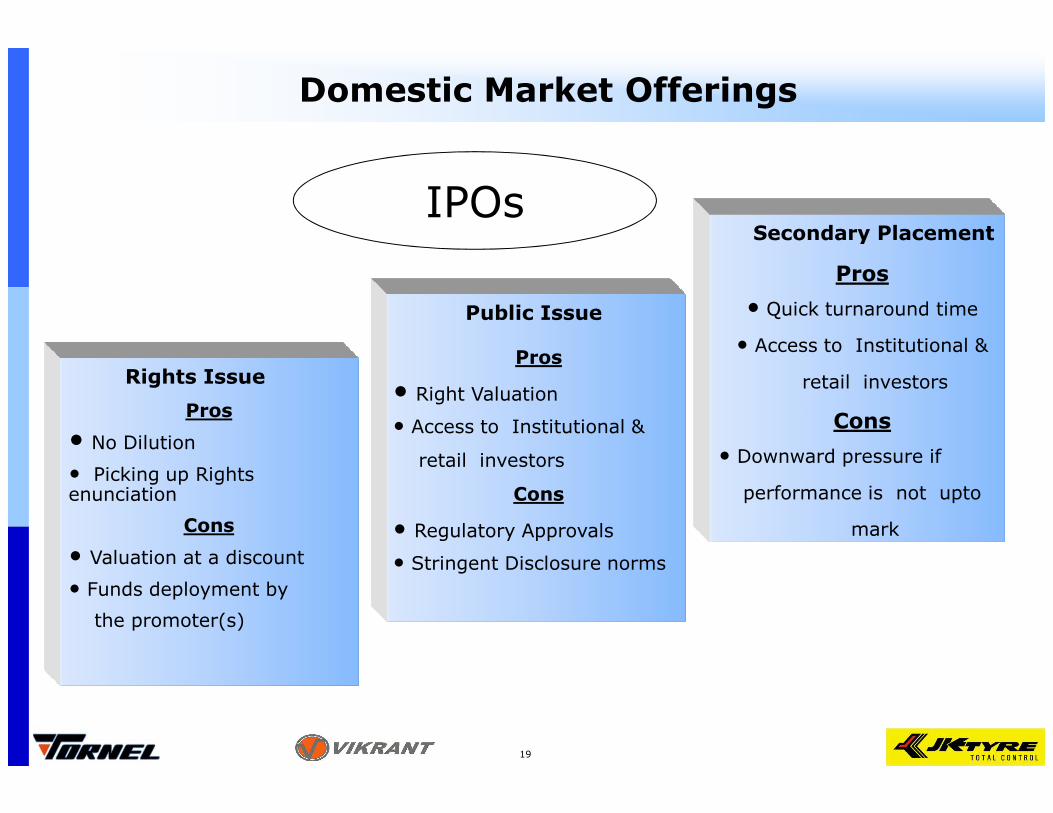

IPOs

Public Issue

Rights Issue

Pros

Pros

• Right Valuation

Pros

• Quick turnaround time

• Access to Institutional &

retail investors

Secondary Placement

Domestic Market Offerings

Pros

• No Dilution

• Picking up Rights enunciation

Cons

• Valuation at a discount

• Funds deployment by

the promoter(s)

• Access to Institutional &

retail investors

Cons

• Regulatory Approvals

• Stringent Disclosure norms

Cons

• Downward pressure if

performance is not upto

mark

19

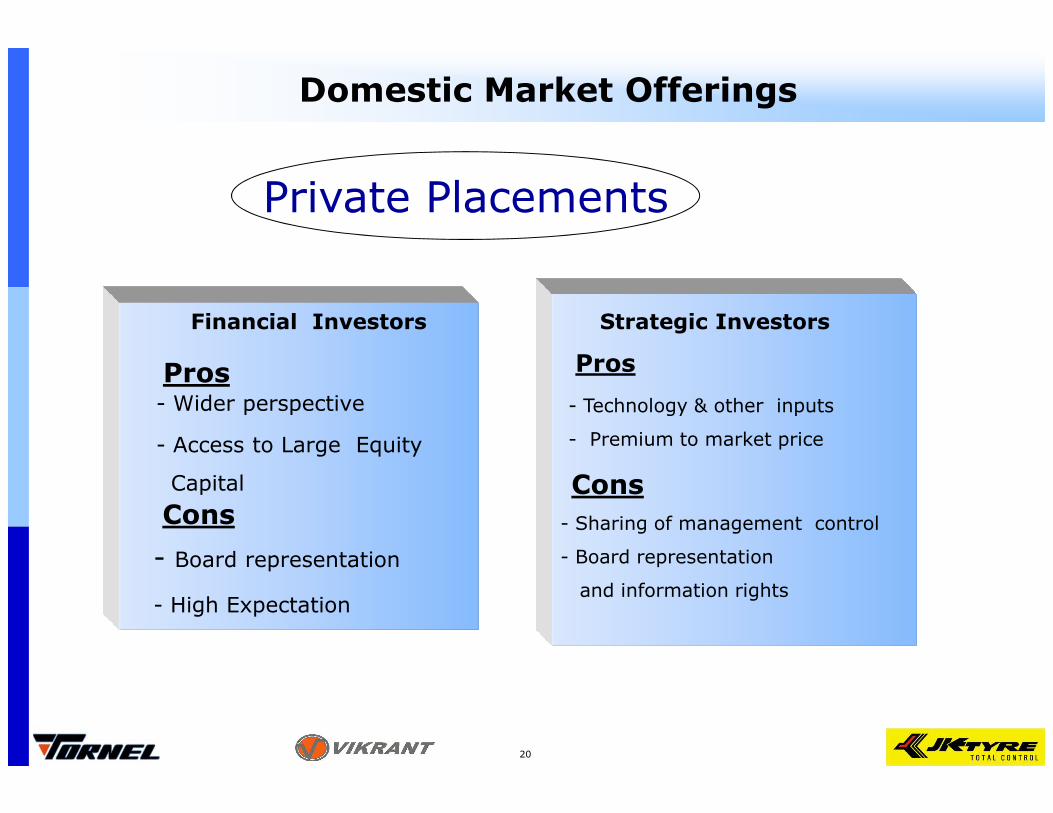

Private Placements

Financial Investors

Pros Pros

- Wider perspective - Technology & other inputs

Strategic Investors

Domestic Market Offerings

- Wider perspective

- Access to Large Equity

Capital

ConsCons

- Board representation

- High Expectation

- Technology & other inputs

- Premium to market price

- Sharing of management control

- Board representation

and information rights

20

Overseas Offerings

Overseas Offerings

GDRs/ADRs

Pros Pros• Premium to market price • Low rate of interest

FCCBs

• Premium to market price

• Access to Global Investors

Cons Cons

• Stringent Disclosure /

compliance requirement

• Uneconomical if size is less

than $ 30-50 mn

• Low rate of interest

• Access to large funds

• Board Representation*

• Not appropriate for highly

geared company

* if subscribed by foreign banks/ multilateral agencies

21

•Invest in emerging companies

specially unlisted stocks

•Desire active participation in

the company to run up the

price &liquidity in the market

PE Funds

Financial Partners

• Invest in high growth

Industries

• No minimum size of

HNI –Domestic/Overseas

•Invest to achieve the overall

objectives of the institution

•Not much participation in

re-rating of the stock but

gives good signal in the market

to have these kind of investors

Multilateral Agencies

price &liquidity in the market

•Usually want active

participation with at least 1

board seat as well

•Very high risk being couple

of Investors

22

•

Investment

• Good for diversification of

shareholding

to have these kind of investors

•Usually wants board seat &

updation of information on

time to time

•Good to have these kinds of

reputed investors in

shareholding specially for

lending through ECA etc.

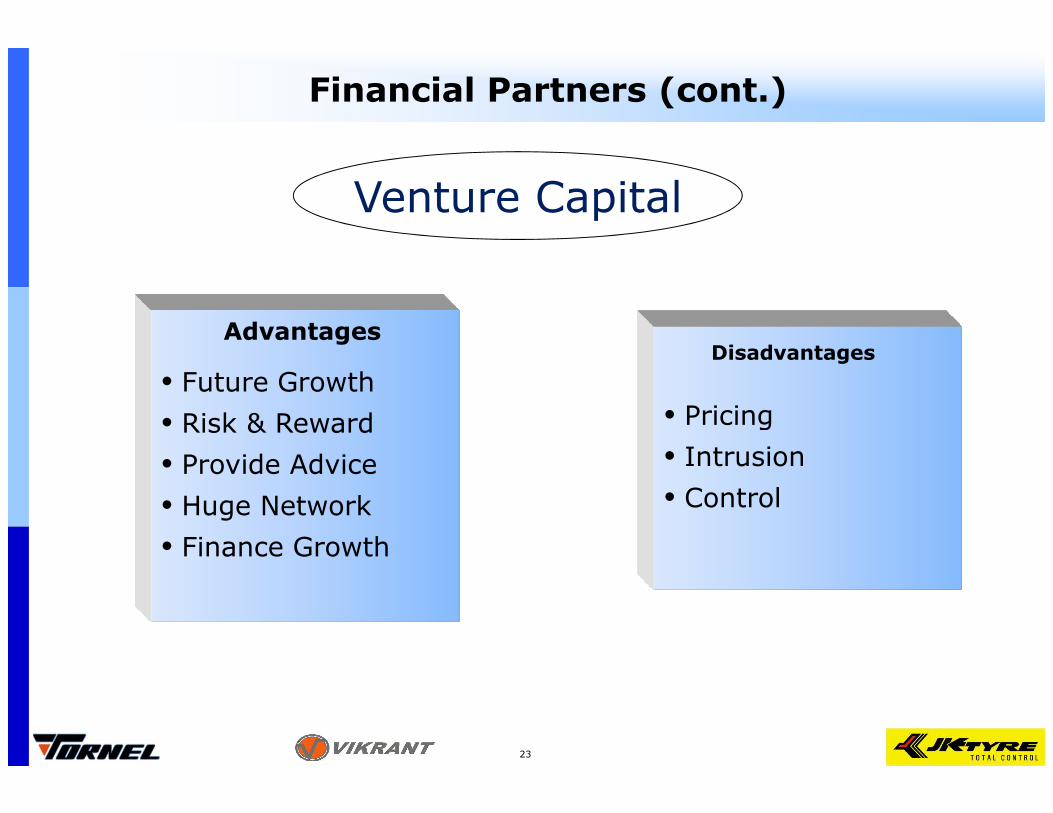

• Future Growth• Risk & Reward

Advantages

Financial Partners (cont.)

• Pricing

Disadvantages

Venture Capital

• Risk & Reward• Provide Advice• Huge Network• Finance Growth

23

• Pricing• Intrusion• Control

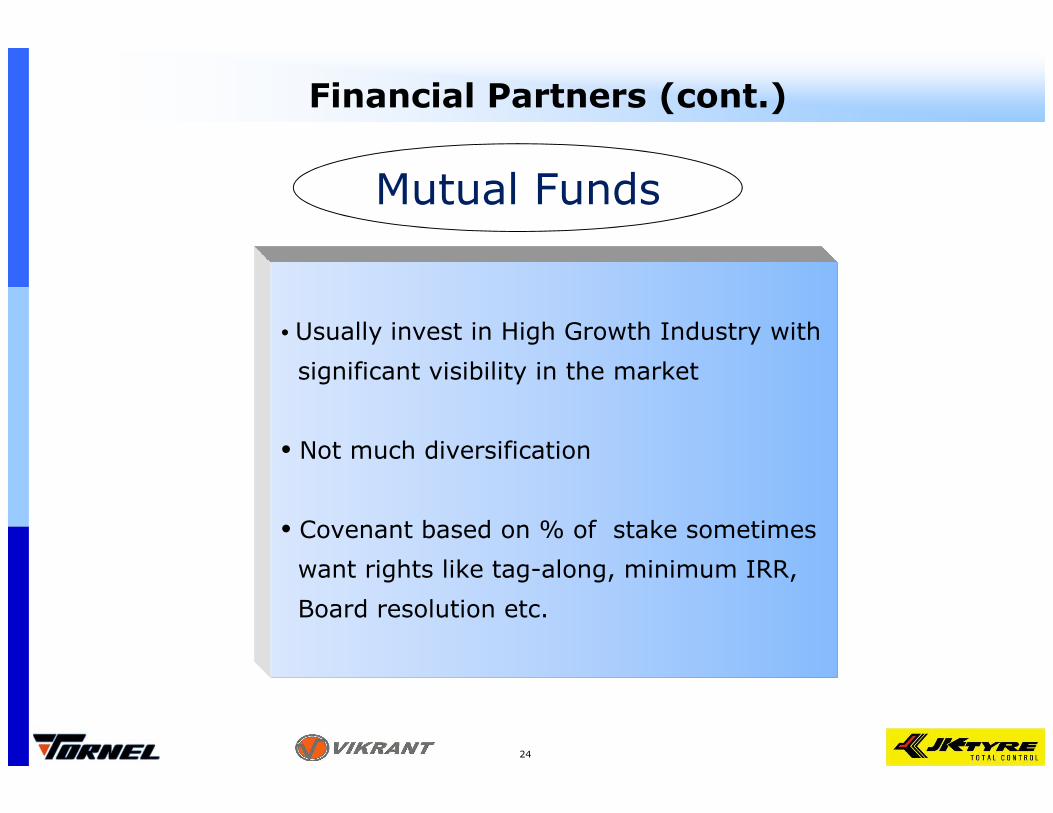

• Usually invest in High Growth Industry with

significant visibility in the market

Financial Partners (cont.)

Mutual Funds

• Not much diversification

• Covenant based on % of stake sometimes

want rights like tag-along, minimum IRR,

Board resolution etc.

24

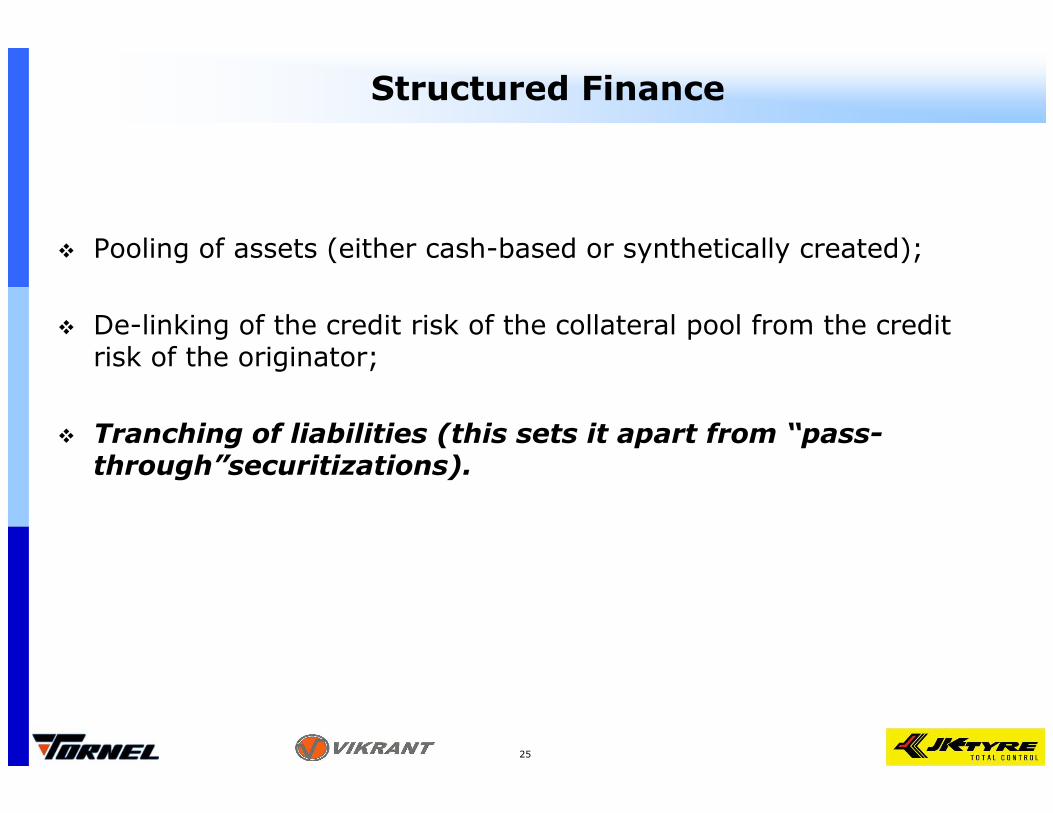

Structured Finance

� Pooling of assets (either cash-based or synthetically created);

� De-linking of the credit risk of the collateral pool from the credit risk of the originator;

� Tranching of liabilities (this sets it apart from “pass-through”securitizations).

25

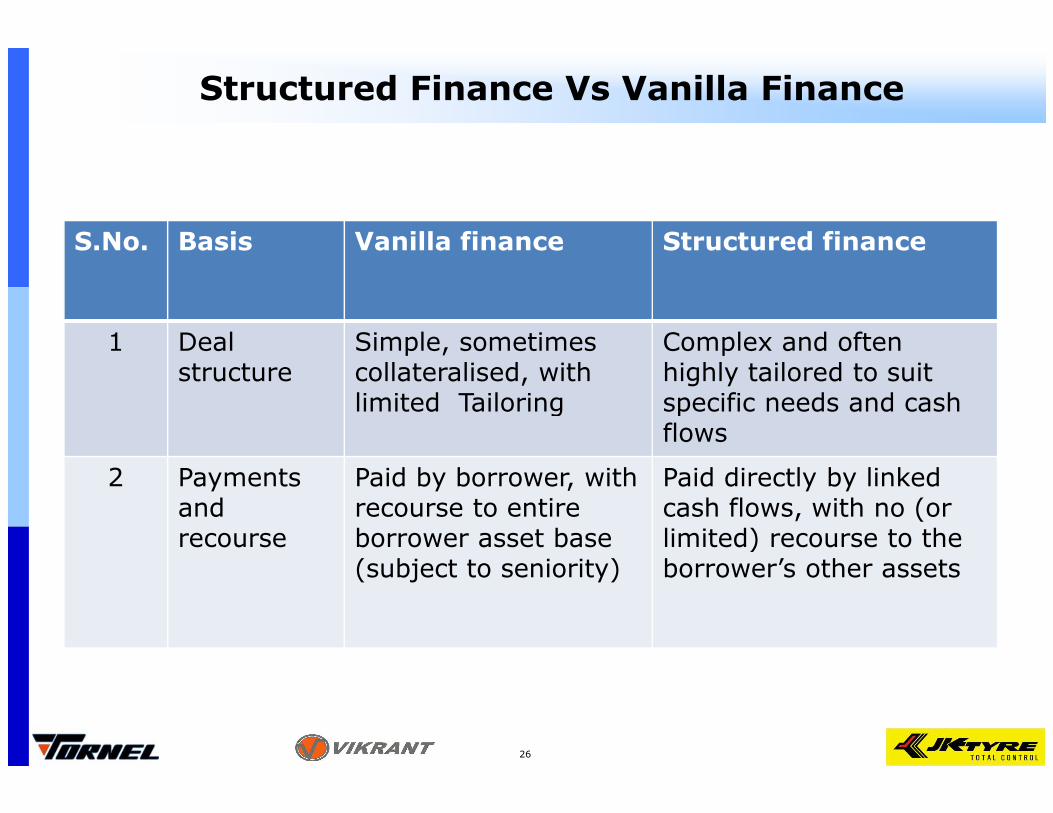

Structured Finance Vs Vanilla Finance

S.No. Basis Vanilla finance Structured finance

1 Deal structure

Simple, sometimes collateralised, with limited Tailoring

Complex and often highly tailored to suit specific needs and cash limited Tailoring specific needs and cash flows

2 Payments and recourse

Paid by borrower, with recourse to entire borrower asset base (subject to seniority)

Paid directly by linked cash flows, with no (or limited) recourse to the borrower’s other assets

26

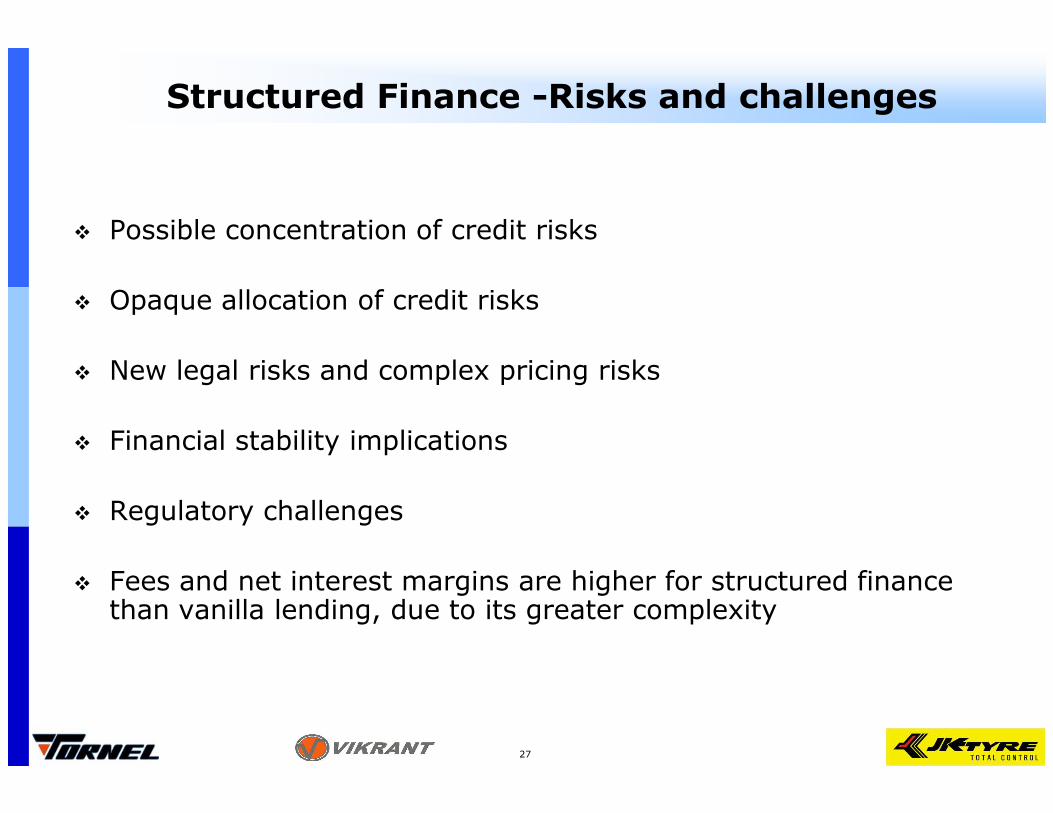

Structured Finance -Risks and challenges

� Possible concentration of credit risks

� Opaque allocation of credit risks

� New legal risks and complex pricing risks

� Financial stability implications

� Regulatory challenges

� Fees and net interest margins are higher for structured finance than vanilla lending, due to its greater complexity

27

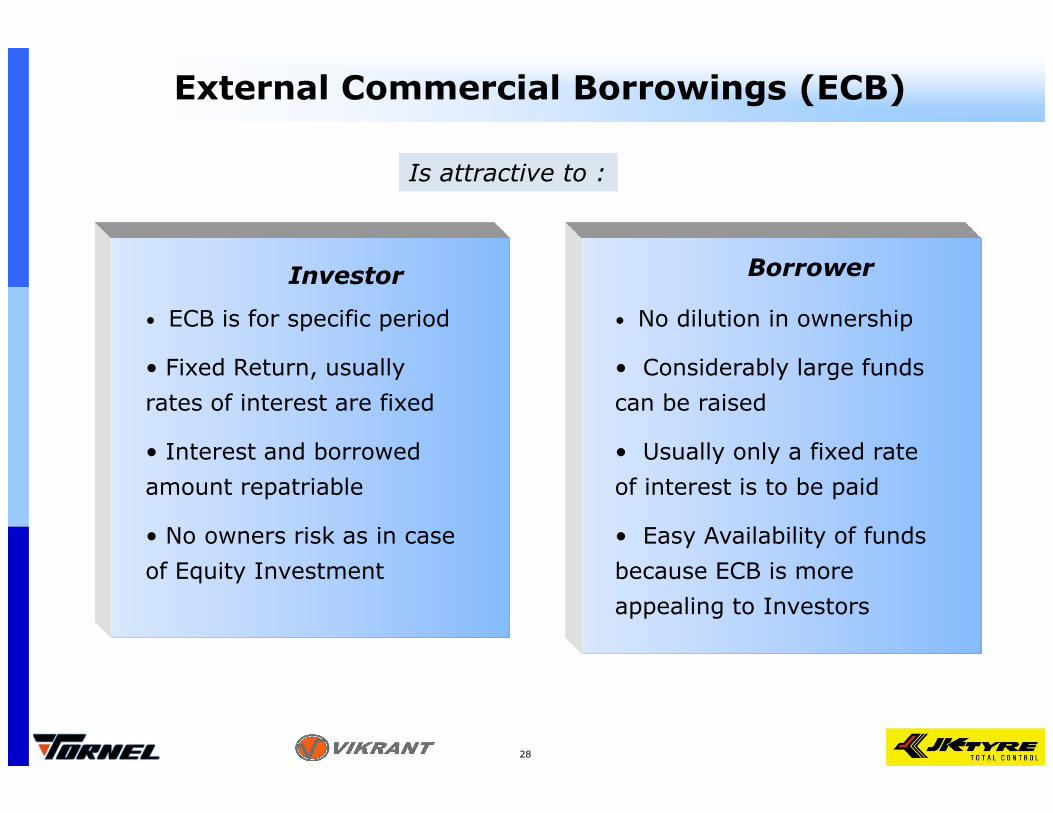

External Commercial Borrowings (ECB)

Investor

• ECB is for specific period

• Fixed Return, usually

rates of interest are fixed

Borrower

• No dilution in ownership

• Considerably large funds

can be raised

Is attractive to :

rates of interest are fixed

• Interest and borrowed

amount repatriable

• No owners risk as in case

of Equity Investment

can be raised

• Usually only a fixed rate

of interest is to be paid

• Easy Availability of funds

because ECB is more

appealing to Investors

28

Potential Investment Opportunities

29

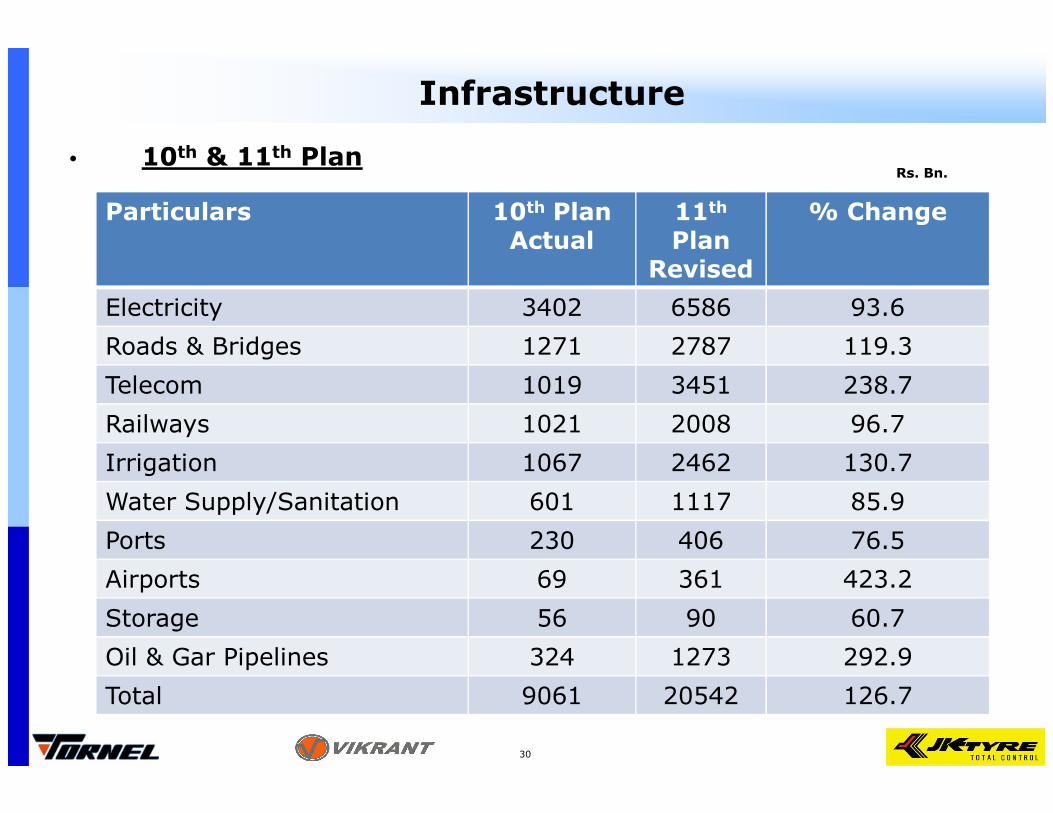

Infrastructure

• 10th & 11th Plan

Particulars 10th Plan Actual

11th

Plan Revised

% Change

Electricity 3402 6586 93.6

Roads & Bridges 1271 2787 119.3

Telecom 1019 3451 238.7

Rs. Bn.

30

Railways 1021 2008 96.7

Irrigation 1067 2462 130.7

Water Supply/Sanitation 601 1117 85.9

Ports 230 406 76.5

Airports 69 361 423.2

Storage 56 90 60.7

Oil & Gar Pipelines 324 1273 292.9

Total 9061 20542 126.7

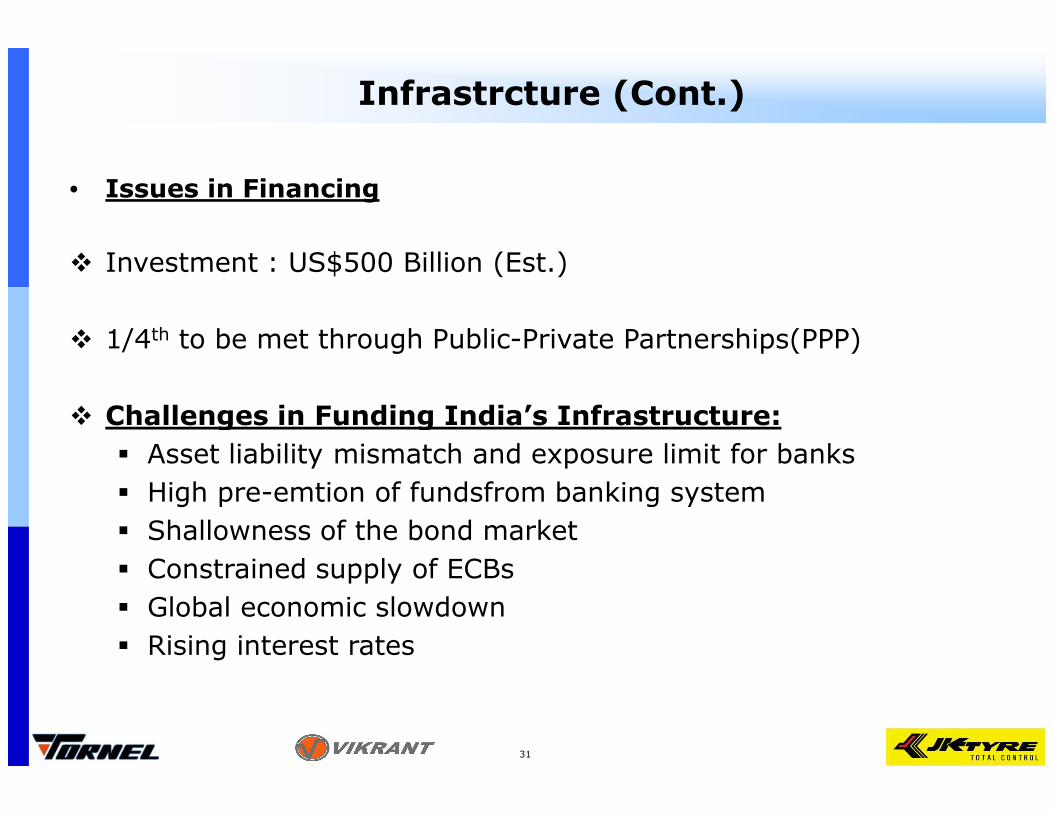

Infrastrcture (Cont.)

• Issues in Financing

� Investment : US$500 Billion (Est.)

� 1/4th to be met through Public-Private Partnerships(PPP)

� Challenges in Funding India’s Infrastructure:� Challenges in Funding India’s Infrastructure:

� Asset liability mismatch and exposure limit for banks

� High pre-emtion of fundsfrom banking system

� Shallowness of the bond market

� Constrained supply of ECBs

� Global economic slowdown

� Rising interest rates

31

Automobiles

� Investment up to US$ 17.12 billion in fresh capacity in the next 4 years

• Components industry : US$ 12 billion up to the end of the Automotive Mission Plan.

� Car manufacturing capacity set to rise to 5.7 million units by � Car manufacturing capacity set to rise to 5.7 million units by 2015

� India aims to become the small car hub of the world by dethroning Japan

32

Auto Components

� Ministry of Heavy Industries and Public Enterprises hasenvisaged Automotive Mission Plan 2006-2016. It targets to:

– Increase turnover to US$ 122 billion–US$ 159 billion by 2016from US$ 34 billion in 2006

– Increase export revenue to US$ 35 billion by 2016

– Provide employment to additional 25 million people by 2016

33

• Challenges

� Revamp distribution strategies

� Change the product design and agent commission structure

� Strong bancassurance

Insurance

� Strong bancassurance

� Lower cost overruns

� Established distribution networks

6-8 established players are likely to be better positioned to manage these challenges

34

• Growth Drivers

� High rates of growth

� Increased market liberalization

• Challenges

� Access to technology

� Raw material availability

Indian Aerospace Industry

The Indian aerospace industry has historically been dominated by large Public Sector Units (PSUs).

liberalization

� High domestic demand

� Cost advantages

� Talent base

� Leveraging IT competitiveness

� Access to funding

� Certification processes

� Skill availability

� Quality issues

35

• Investment Oppurtunities

� Investment opportunities in new aircraft and anddevelopment of airport infrastructure.

� Associated areas, such as MRO (Maintenance, Repair & Overhaul), offer high investment potential.

Indian Aerospace Industry (Cont.)

Overhaul), offer high investment potential.

� Increased Air cargo traffic

36

• Critical Issues - very important for the qualitative growth of the Indian banking

� Know Your Customer (KYC)

� Treating customers fairly (TCF)

� Capital and Liquidity risk management

Banking and Financial Sector

� Capital and Liquidity risk management

� Asset Quality

� Inclusive Growth: Financial Inclusion Leveraging Technology

� mass availability of products

� wide range of services to satisfy the financial and nonfinancial

� needs of all types of customers

� key enabling factor has been the adoption of technology

37

• Proposed Guidelines

� At least Rs 1,000 crore as the entry level capital

� New banks should be substantially large & well-capitalised,

� Ability to expand their operations swiftly after getting licences

Banking and Financial Sector (Cont.)

� Ability to expand their operations swiftly after getting licences

� New banks have to foster financial inclusion

� Resources sufficient enough to enable them expand the banking reach faster

38

� Emerging hub for contract research, Biotechnology, Clinical trials and Clinical data management.

� Licensing deals with MNCs for New Chemical Entities and New Drug Delivery Systems.

� Marketing alliances for MNC products in domestic and international markets.

Pharmaceutical Industry

� Marketing alliances for MNC products in domestic and international markets.

� Contract manufacturing arrangements with MNCs.

� Enormous potential for developing India as a centre for international clinical trials.

� Possibilities for expansion of Bio-similars and Bio-pharmaceuticals.

39

� In the knowledge process outsourcing, India is climbing theglobal value chain and is expected to add value to global KPO-valuation research, investment research, patent filing, insuranceclaims processing, online teaching and legal process outsourcing.

� Increased M&A driven by need for global service delivery

Information Technology Sector

� Increased M&A driven by need for global service delivery capabilities

� IT sector emerged as the preferred space for venture capital investments in India

40

� IIP growth slowing near term: Industrial growth in 1QCY11 is likely to slow to the 5% levels, thereby raising some question marks on the sustainability of growth.

� Rising inflation is biggest worry: After a softer headline inflationover this quarter, inflation is likely to pick up and could be in the 7-8%range late this year. More importantly, this will be driven by coreinflation rather than the agflation of 2010.

� Monetary tightening, rising interest rates: It is expectes that RBI

2011: Challenges

� Monetary tightening, rising interest rates: It is expectes that RBIwill increase policy rates by 100bp, the cash reserve ratio by 25bpand the statutory liquidity ratio by 50bp to contain inflationexpectations. Also banks too will hike rates by 100 bps over next 12-15 months.

� Earnings downgrades: On a bottom up basis, it is forecasted thatearnings to grow 31% in FY11 and 24% in FY12. It is seen thatearnings downgrades as margins disappoint led by (a) rising

commodity prices (b) rising wage costs and (c) higher interest costs.

Uncertainity of Demand Uncertainity of Forecasting

41

2011 – Hope for the Best

� 2010 has turned out to be one of the most range bound years in India in the last 20 years. Expert see 2011 an even more difficult year with markets

� Global quantitative easing is positive

� Strong GDP Growth~ 8.5%

• Industrial Growth around 8% in FY12• Industrial Growth around 8% in FY12

� Strong earning growth

� FII flows in Indian Market at $29 Bn. in 2010

• The global backdrop is encouraging for FII flows to all emerging markets including India

� Rural demand key driver in 2011

42

Just a word aboutJust a word aboutJust a word aboutJust a word about

43

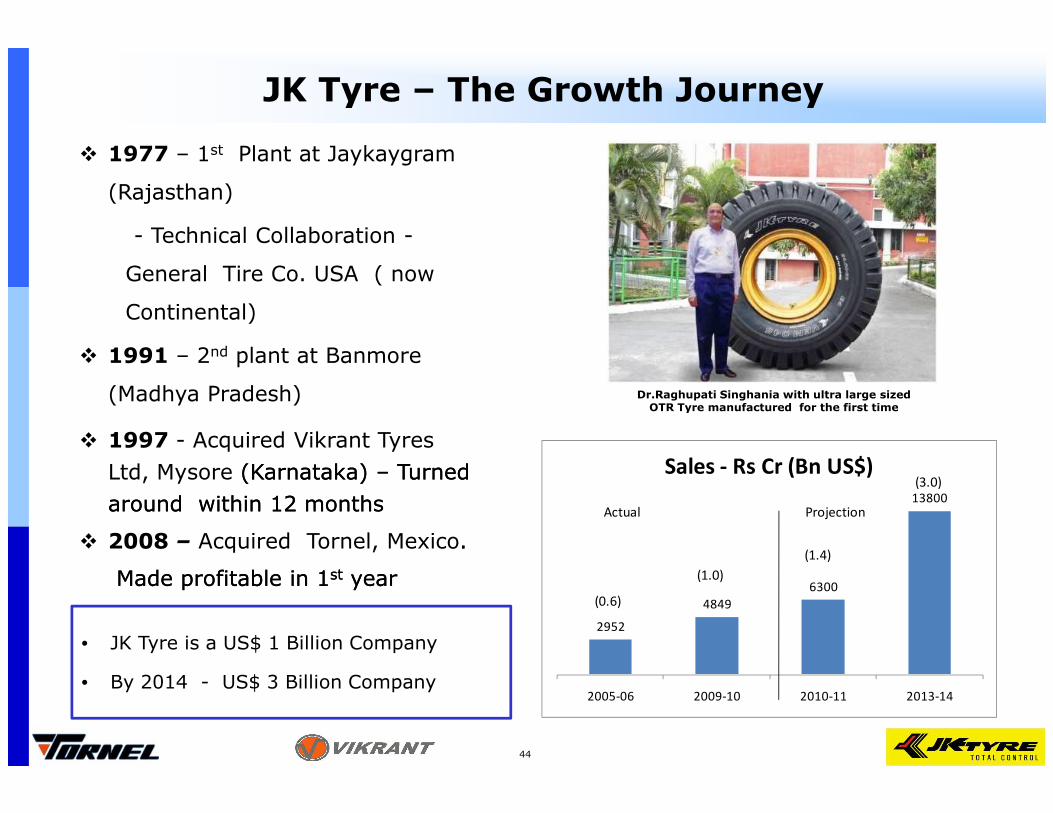

� 1977 – 1st Plant at Jaykaygram

(Rajasthan)

- Technical Collaboration -

General Tire Co. USA ( now

Continental)

� 1991 – 2nd plant at Banmore

(Madhya Pradesh)

JK Tyre – The Growth Journey

Dr.Raghupati Singhania with ultra large sized OTR Tyre manufactured for the first time

� 1997 - Acquired Vikrant Tyres

Ltd, Mysore (Karnataka) (Karnataka) –– Turned Turned

around within 12 monthsaround within 12 months

� 2008 – Acquired Tornel, Mexico..

Made profitable in 1Made profitable in 1stst yearyear

• JK Tyre is a US$ 1 Billion Company

• By 2014 - US$ 3 Billion Company 44

2952

4849

6300

13800

2005-06 2009-10 2010-11 2013-14

Sales - Rs Cr (Bn US$)

(0.6)

(1.0)

(1.4)

(3.0)

Actual Projection

OTR Tyre manufactured for the first time

44

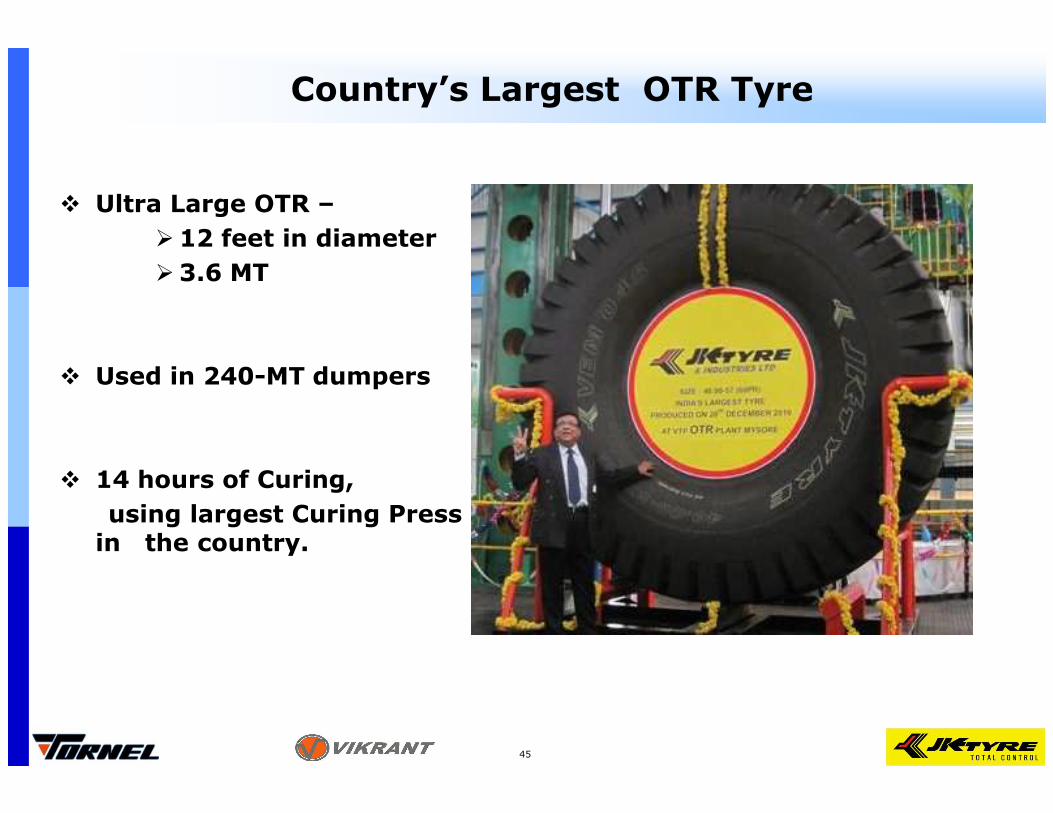

Country’s Largest OTR Tyre

� Ultra Large OTR –

�12 feet in diameter

�3.6 MT

� Used in 240-MT dumpers

� 14 hours of Curing,

using largest Curing Press in the country.

45

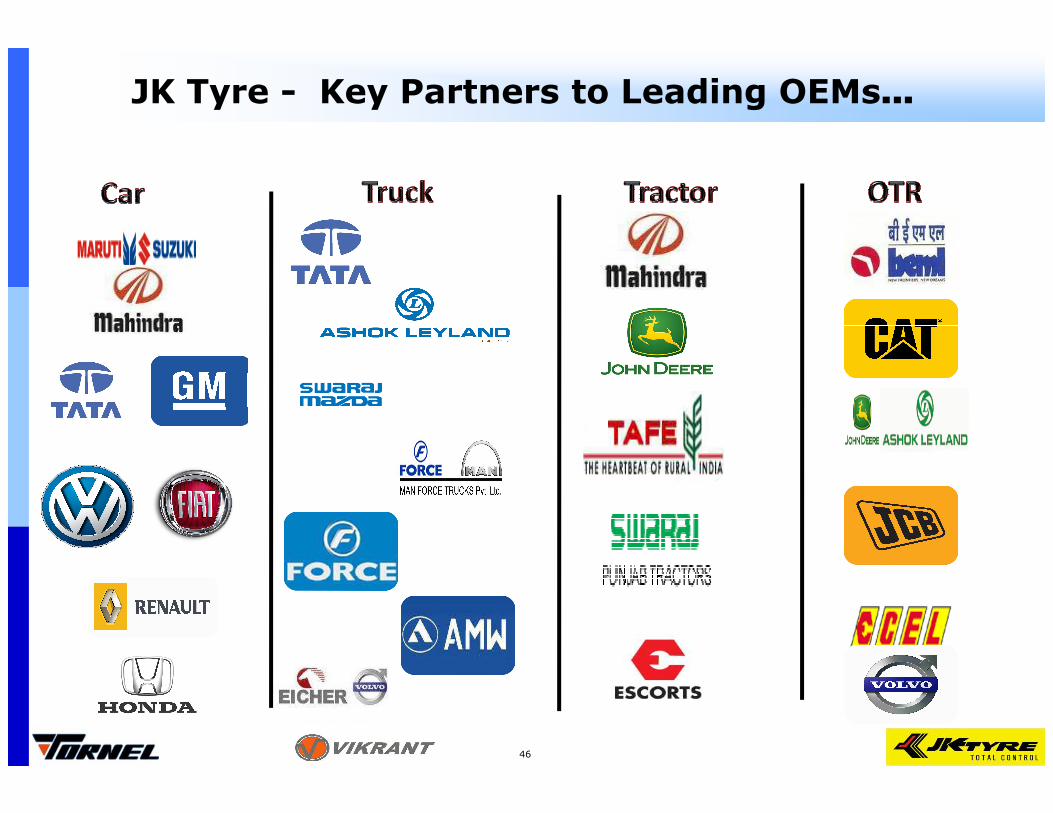

JK Tyre - Key Partners to Leading OEMs...

Maruti

Mahindra

x

x

X

X

x

x

x

46

Partnerships in Offing

47

JK Tyre – Leading Brand in India

Selected as a Super Brand -2009-10 & 2010-11 (Consumer Survey validated by the Super Brands Council)

� 75th amongst India’s 100 Most Valuable Brands 2010

48

� Export Excellence Award 2009, Federation of Karnataka Chambers of Commerce & Industry

Awards & Accolades – Recognition of efforts:

� Golden Peacock National Quality Award

� Golden Peacock Environment Award 2009

� Special Commendation for Golden Peacock Environment

Management Award – 2010 - Banmore Tyre Plant

�Annual Greentech Environment Excellence Award 2010�Annual Greentech Environment Excellence Award 2010

� National Energy Conservation Award – 2009 – KTP

� Rajasthan Energy Conservation Award – 2009 – KTP

� CII Energy Management Award – 2009 –KTP

� CII Water Management Award – 2009 –KTP

KTP – Kankroli Tyre Plant

49

Awards & Recognition (Cont.)

� India Manufacturing Excellence Gold Award 2010

� Talent Management Award from Employer Branding Institute, Mumbai

� 4th Employer Branding Award 2009 for Excellence in Training

� National CSR Award for Best Corporate Social Practices Instituted by Bombay Stock Exchange

50

50

THANKTHANKTHANKTHANK YOUYOUYOUYOUTHANKTHANKTHANKTHANK YOUYOUYOUYOU

51