fti: asset tracing in asia

TRANSCRIPT

Presentation for FraudNet

Asset Tracing Investigations in Asia -The Real DealThe Real Deal

David Holloway, Senior Managing DirectorCatherine Williams, Senior Managing Director

11 March 2011

Contents

I. Introduction

II. Asset Searching by Investigators

III. Asset Tracing by Forensic Accountants

IV. Case Study – Moulin Global Eyecare Holdings LimitedIV. Case Study – Moulin Global Eyecare Holdings Limited

V. Q & A

I. IntroductionI. Introduction

The Global Footprint of FTI Consulting

We deploy more than 3,500 professionals from every major financial center to every corner of the globe so that we can serve our clients wherever challenges arise.

North AmericaUnited StatesAnnapolisAtlantaBaltimoreBethesdaBostonBrentwoodCambridgeCharlotteChicagoClevelandDallasDenverDetroitHoustonIndianapolisKing of PrussiaLos AngelesMiamiMorristownNashville

Asia PacificAustraliaMelbournePerthSydney

ChinaBeijingGuangzhouShanghai

Hong Kong

IndiaMumbai

JapanTokyo

The PhilippinesManila

NashvilleNew YorkOaklandOrlandoOrange CountyPhiladelphiaPhoenixPittsburghRockvilleRoselandSaddle BrookSalt Lake CitySan FranciscoSeattleTucsonWalnut CreekWashington, DCWest Palm Beach

CanadaTorontoVancouver

MexicoMexico City

PanamaPanama City

Singapore

South AmericaArgentinaBuenos Aires

BrazilSão Paulo

ColombiaBogotá

Africa / Middle EastBahrainManama

United Arab EmiratesAbu DhabiDubai

South AfricaCape TownJohannesburg

●

Europe

BelgiumBrussels

FranceParis

GermanyFrankfurtMunich

IrelandDublin

RussiaMoscow

SpainMadrid

United KingdomEpsomLondonManchesterNorthamptonStirling

●

Forensic & Litigation Consulting Services in Asia

FTI is a leading independent provider of Forensic & Litigation Consulting services in Asia. As a specialist firm, we do not provide audit, taxation or compliance services and so we are free from conflict of interest issues.

We offer a broad range of specific skills – from expert witness services to the valuation of businesses and equity, legal technologies and reconstruction of accounting records.

Our team has been involved in many of the region’s most high profile and complex litigation, dispute resolution, forensic IT, financial and fraud investigations.

Our Services

• Expert Witness

• Economic Loss Quantification

• Valuations

• Financial Investigations

• Reconstruction and Analysis of Accounting

• Records

• Asset Tracing

• Forensic Data Analysis

• Independent Accounting Based Evidence

Forensic Accounting Litigation Support and Technology

Business Intelligence & Investigations

• Global Electronic Discovery

• Computer Forensics

• Forensic Data Analysis

• e-Discovery

• Expert Witness Testimony

• Fraud and Corporate Investigations

• International Asset Searches

• Investigative Due Diligence

• Pre IPO Investigative Due Diligence

• Corporate Governance

• Political Risk Assessment

• Crisis Management

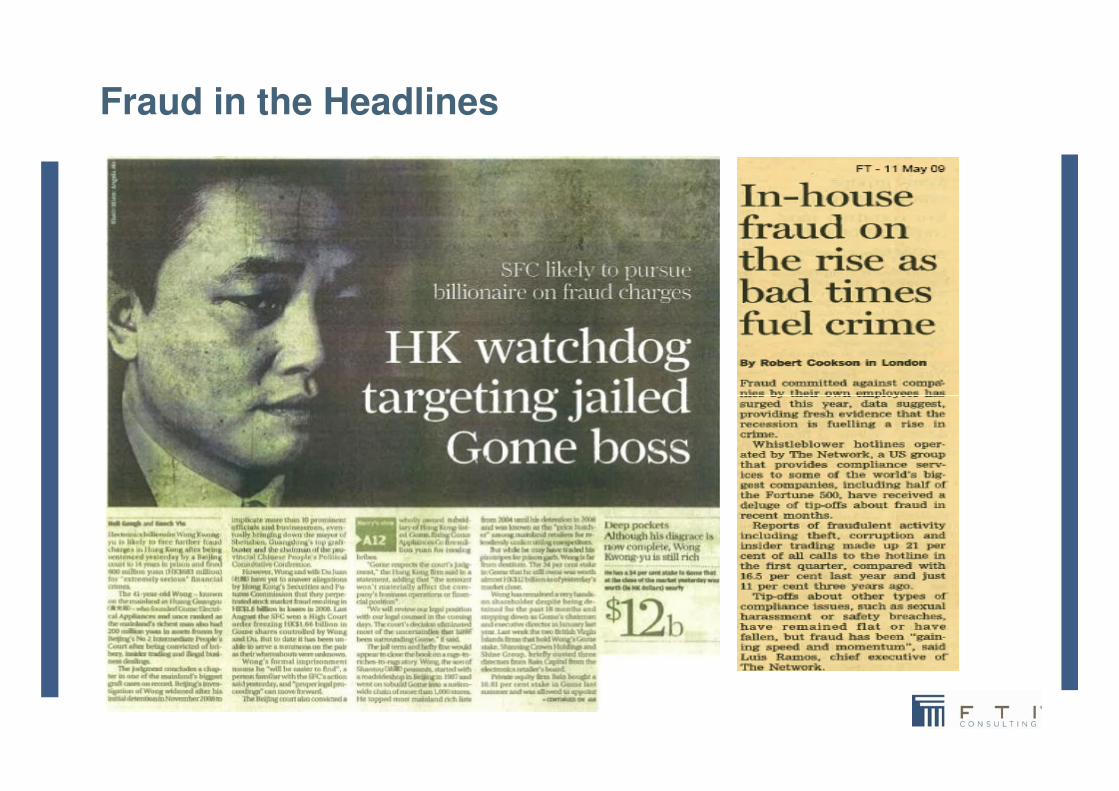

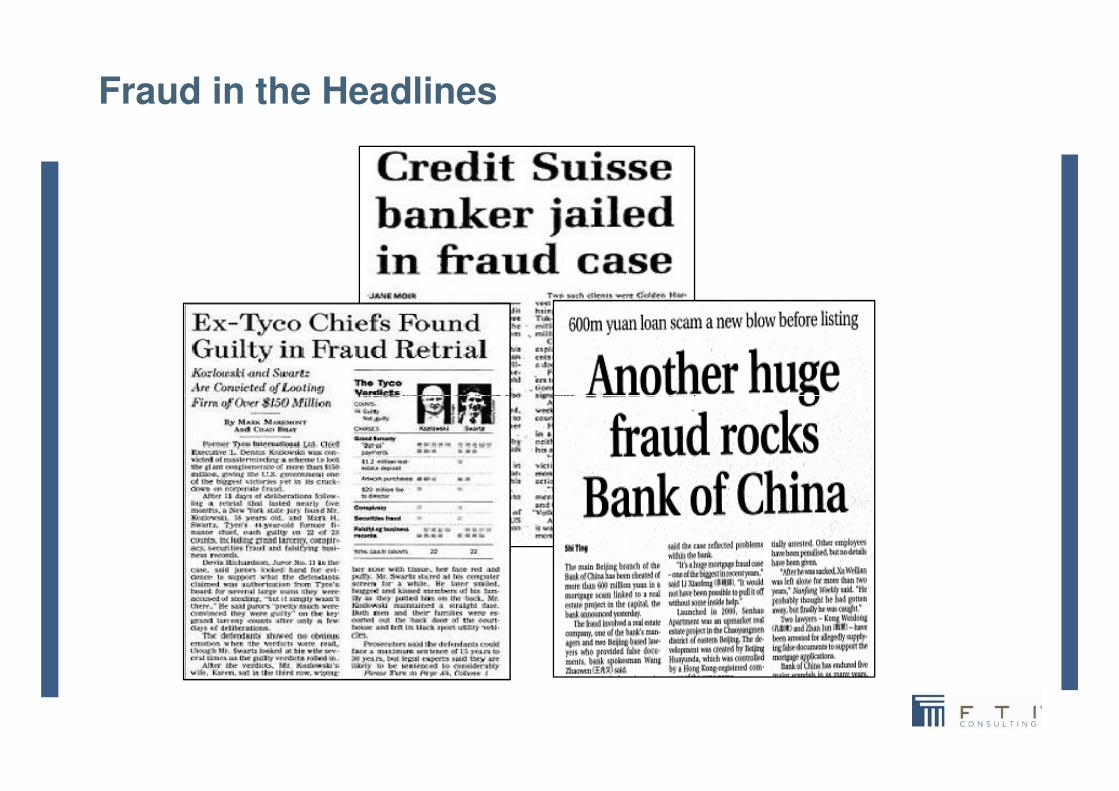

Fraud in the Headlines

Fraud in the Headlines

Fraud in the Headlines

•A - Thailand

•B - China

Fraud in Asia

Answer:

Where do the largest frauds occur in Asia ?

E - Japan•B - China

•C - Malaysia

•D - Indonesia

•E - Japan

E - Japan

• $$$ - impact to bottom line?

• Is the loss covered by insurance?

• Can we otherwise recover losses?

• Who is involved - management, staff?

• How did it occur & how can we stop further losses?

Key Management Concerns When Fraud is

Discovered

• How did it occur & how can we stop further losses?

• Is there a requirement to report to regulators?

• How to keep from media because of impact on corporate image?

• Should a report be made to police?

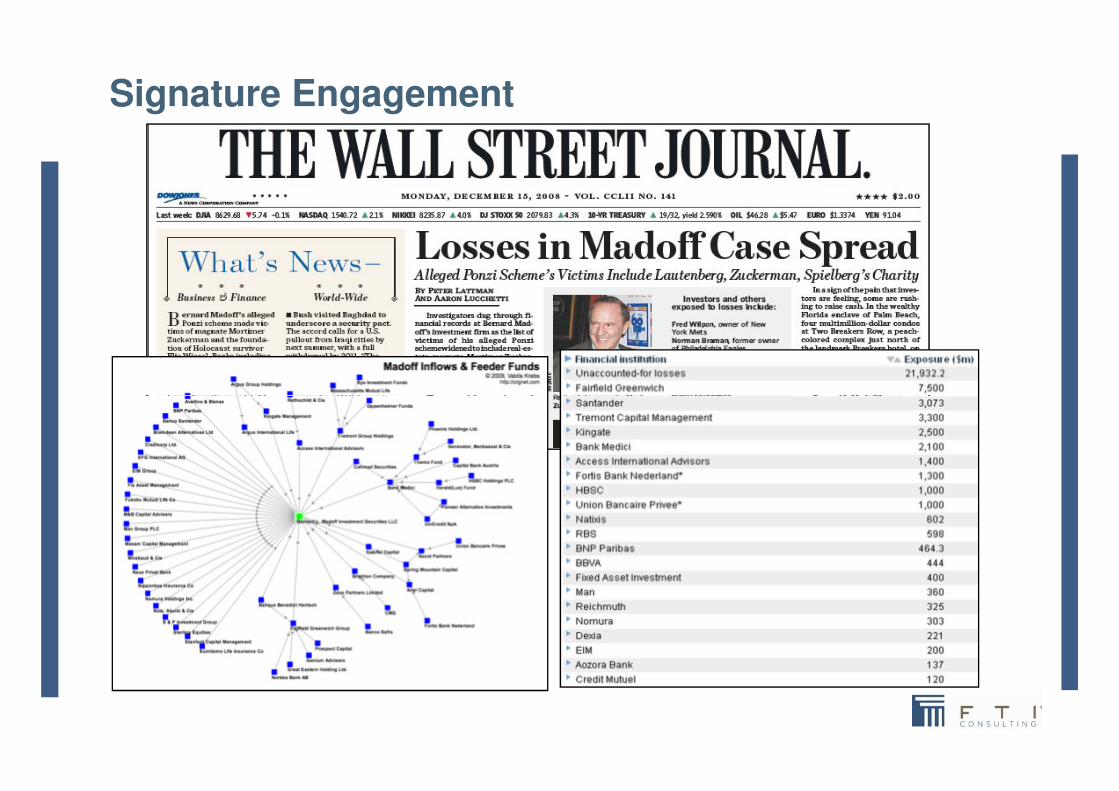

Signature Engagement

Signature Engagement

II. Asset Searching by Investigators

Types of Asset Searching

• Proceeds of fraudulent activities

• Pre litigation assessment of assets

• Post judgment assessment

• Financial worth inquires

Role of Investigators

• Identification of actual and potential assets: direct and beneficial ownership

• Evidence to support civil action/s and attachment of relevant assets

• Working with legal counsel as necessary to facilitate attachment and collection processattachment and collection process

• Assembly of evidential packages to support potential leveraged discussions

• To support criminal action, where it is considered necessary

Keys to Successful Asset Searching

• Speed: asset searching needs to be initiated almost as quickly as a fraud investigation commences - everyday that goes by adds to the difficulty of recovery

• Ring-fence any relevant insurance policies as soon as possible

• Think as the culprits• Think as the culprits

• Develop a chronology of events around key time frames –‘more footprints in the sand’ are likely before discovery of wrongdoing

• Local knowledge

Basic Methodology

Phase 1 – Review & Debrief

• Full debrief and securing of all available identifiers

• Establishing a base-line profile of the target/s from client knowledge

• Establishing a base-line of known or suspected assets• Establishing a base-line of known or suspected assets

• Identifying potential live sources

Basic Methodology

Phase 2 – Profiling Targets through Research & Public

Record Sources

• Comprehensive profiling of the target/s: initially through desktop investigative research

• Searching and analysis of public record sources• Searching and analysis of public record sources

• Requires full understanding of range of global research and public record sources throughout the world

Basic Methodology

Phase 3 – In-depth Field Inquiries

• Using information and intelligence obtained during debriefing and research, commence a series of discreet field inquiries

• These inquiries are focused on those aspects, • These inquiries are focused on those aspects, individuals or entities most likely to produce information and evidence as to the identification and verification of ownership and potential value of assets

• Use of link analysis tools to support findings

• Bank and securities accounts

Basic Methodology

Phase 4 – Recovery of Assets

• During this process, we will agree with the client as to the most effective recovery strategies and will support the client and their legal advisors in executing the agreed process

• In appropriate circumstances, FTI may suggest proactive dialogue with debtors to encourage early settlement –dialogue with debtors to encourage early settlement –leveraged negotiations

Some Recent Asia Case Examples

– Successful identification in the PRC and Hong Kong of concealed assets, primarily property/real estate estimated to be worth US$100M, of the chairman (guarantor) of a formerly listed PRC-based metals company

– Successful identification in India of significant land holdings and property of two promoters of a listed company owing and property of two promoters of a listed company owing US$40M to a leading Hong Kong bank – collateral for the debts being non-existent trade receivables

Some Recent Asia Case Examples

– Successful identification in Australia, PRC, Taiwan and Hong Kong (plus other jurisdictions in Asia Pacific) of land, property, investments, etc valued in excess of US$300M of a financial advisor to a mega-rich Middle-East family

– A successful investigation showing long-term fraud in Taiwan and various parts of the PRC and Hong Kong by a Taiwan and various parts of the PRC and Hong Kong by a seafood processing and exporting business and its principals (the loan guarantors) in relation to unpaid loans amounting to US$70M to a syndicate of 18 banks

III. Asset Tracing by Forensic Accountants

Direct

Method

Identifies assets through specific financial transactions:

• Accounting system – undisclosed ledgers

• Trial Balance – identifies all account ledgers

• General Ledger – all transactions / narrations

Asset Tracing

• General Ledger – all transactions / narrations

• Correspondence – emails, customer / supplier files

• Accounting vouchers

• Bank statements – unrecorded funds flow

• Tax returns

• Forensic imaging – emails, laptops, servers

Where the books and records are

available!

Indirect

Method

Identifies assets through financial analysis and publicly available information:

• Financial ratios – listed entities

• Searches – Internet, Factiva, Bloomberg, Company Registers, Property Title, Court records

Asset Tracing

• Net worth analysis

• Source & application of funds

• Reconstruction of accounts

• Credit agencies

Where there are partial or no books

and records!

IV. Case Study – Moulin Global Eyecare Holdings

Limited Limited

• Listed on the HKSE October 1993

• Suspension from trading on 18 April 2005 for delay in filing financial results

• Auditors resigned on 18 April 2005 (3rd change of auditors in 5 yrs)

• Accounting irregularities identified during review as IFA

Asset Tracing - Moulin

• Appointed PL on 23 June 2005; Liquidator on 28 August 2006

Issues encountered:

• Shredding of documents by employees

• Invoice templates for friendly suppliers located on employee’s computers

• Fictitious sales – North American customers

Asset Tracing - Moulin

• Fictitious sales – North American customers

• Related party transactions - loans

• Friendly suppliers - operated / controlled by management

• Window dressing of cash balances at interim and year end

• Trade finance fraud – provided cashflow

• Secret room of documents

• Fake chops/ falsification of documents

Delivering Documents – Hong Kong Style

Asset Tracing

The recovery

Draft Balance Sheet as at 31 December 2004

Assets

• Cash at Bank – HKD1.2 billion

- Including HKD265 million in PRC

• Trade Receivables – HKD679 million

• “Other” Receivables – HKD500 million

• Actual cash at bank on our appointment was about HKD9 million

• Trust Agreement signed supporting HKD310 million in the PRC but didn’t exist

• Window dressed bank accounts at

Moulin Balance Sheet

• Prepaid Board Space – HKD54 million

• Fixed Assets – HKD870 million

• Inventory – HKD465 million

• Due from Senior Mgmt – HKD93 million

Liabilities

• Bank Creditors – HKD1.7 billion

• Window dressed bank accounts at year end

• Irregular trade finance arrangement to provide cash flow

• “Round robin” transactions

• Group and “related” entities had over 350 bank accounts

Draft Balance Sheet as at 31 December 2004

Assets

• Cash at Bank – HKD1.2 billion

- Including HKD265 million in PRC

• Trade Receivables – HKD679 million

• “Other” Receivables – HKD500 million

• Prepaid Board Space – HKD54 million

• 4 biggest customers were in the US/Canada.

• Accounted for more than 37% of Group sales per year.

• Didn’t exist, customer addresses are all residential addresses. One was a

Moulin Balance Sheet

• Prepaid Board Space – HKD54 million

• Fixed Assets – HKD870 million

• Inventory – HKD465 million

• Due from Senior Mgmt – HKD93 million

Liabilities

• Bank Creditors – HKD1.7 billion

addresses. One was a Chinese Restaurant in McCook, Nebraska and another the CEO’s mother’s residence in Richmond Canada

• Moulin received significant trade finance against these debtors.

Locating overseas assets

We obtained title searches on all the North American Customers

Draft Balance Sheet as at 31 December 2004

Assets

• Cash at Bank – HKD1.2 billion

- Including HKD265 million in PRC

• Trade Receivables – HKD679 million

• “Other” Receivables – HKD500 million

• Subsidiary with Money Lending Licence.

• Supposedly lending funds to third parties.

• Executed loan agreements at 9% pa.

• Didn’t exist, questionable parties signing loan

Moulin Balance Sheet

• Prepaid Board Space – HKD54 million

• Fixed Assets – HKD870 million

• Inventory – HKD465 million

• Due from Senior Mgmt – HKD93 million

Liabilities

• Bank Creditors – HKD1.7 billion

parties signing loan agreements.

• Used Money Lending Business to explain significant fluctuations in cash and support large number of transactions going through bank accounts.

The PRC Credit Union where funds of HK$80 million were said to be deposited

Moulin Balance Sheet

Draft Balance Sheet as at 31 December 2004

Assets

• Cash at Bank – HKD1.2 billion

- Including HKD265 million in PRC

• Trade Receivables – HKD679 million

• “Other” Receivables – HKD500 million

• Prepaid Board Space – HKD54 million

• Prepaid Board Space –HKD54 million – didn’t exist

• Amount Due from Senior Management – HKD93 million – didn’t exist

• Fixed Assets – HKD870 million – Significantly

Moulin Balance Sheet

• Prepaid Board Space – HKD54 million

• Fixed Assets – HKD870 million

• Inventory – HKD465 million

• Due from Senior Mgmt – HKD93 million

Liabilities

• Bank Creditors – HKD1.7 billion

million – Significantly overstated

• Inventories – HKD465 million – Significantly overstated

Draft Balance Sheet as at 31 December 2004

Assets

• Cash at Bank – HKD1.2 billion

- Including HKD265 million in PRC

• Trade Receivables – HKD679 million

• “Other” Receivables – HKD500 million• Head office sold off

• Assets in China held on trust

Moulin Balance Sheet

• Prepaid Board Space – HKD54 million

• Fixed Assets – HKD870 million

• Inventory – HKD465 million

• Due from Senior Mgmt – HKD93 million

Liabilities

• Bank Creditors – HKD1.7 billion

• Assets in China held on trust

by relative

• No access to books and

records

• Some factory equipment

didn’t exist - leasing scam

• Freezing order on

equipment – Bank of China

Draft Balance Sheet as at 31 December 2004

Assets

• Cash at Bank – HKD1.2 billion

- Including HKD265 million in PRC

• Trade Receivables – HKD679 million

• “Other” Receivables – HKD500 million

Moulin Balance Sheet

• Prepaid Board Space – HKD54 million

• Fixed Assets – HKD870 million

• Inventory – HKD465 million

• Due from Senior Mgmt – HKD93 million

Liabilities

• Bank Creditors – HKD1.7 billion

• Approximately HKD1 billion

in “off balance” sheet

borrowings

• Simply didn’t report it

• Highly irregular trade finance

arrangements

• Business was burning cash

Storage of Documents - Hong Kong style

• Concealed by a cloak cupboard that swung outwards to reveal a hidden door

• The hidden door, once opened, revealed a room stacked with various accounting information and books and records.

Results

What we realised:-

• Promissory note US$3 million – negotiated settlement with US debtor US$2 million

• Sale of retail optical shops (Shanghai)

• Factory in the PRC (Zhongshan)

• Sale of retail outlets in USA know as Eyecare Centers of America –Moulin acquired in

2005 shortly prior to collapse2005 shortly prior to collapse

• Golf and country club memberships

• Asian distribution business

• Debtors from subsidiaries

• Chairman & CEO bankrupt

• Litigation – auditors & directors

Results

• Criminal Prosecutions

Jurisdictional issues

Issues where receivables are the major asset, especially if owed by

PRC entities:

• Local creditors have a commercial priority e.g. “jump in and freeze assets”.

• No effective recovery legislation i.e. recoveries work on “first in – first serve” basis.

• Any recoveries would be used to satisfy preferential creditors first – statutory debts • Any recoveries would be used to satisfy preferential creditors first – statutory debts

and employee entitlements.

• Workers and local authorities may cause significant issues.

• Offshore investors/creditors often receive little as local creditors strip assets before

they can be secured / realised

• Arbitration awards can be enforced by Chinese Courts however no transparency

• Chops and legal representatives - control business

Jurisdictional issues

Hong Kong Ordinance (Cap 32):

• Companies Ordinance:

S221 – Examination of directors and officers of the company

1. any officer of the company or person known or suspected to have in his

possession any property of the company or supposed to be indebted to the

company, orcompany, or

2. any person whom the court deems capable of giving information concerning the

promotion, formation, trade, dealings, affairs, or property of the company.

S211 – Power to recover company’s books and records

“.. to the liquidator any money, property, or books and papers in his hands to

which the company is prima facie entitled.”

• BVI Companies – joint appointment in both jurisdictions

45