ft group investments pvt. ltd. group... · please see for further details. 6 grant thornton...

TRANSCRIPT

FT GROUP INVESTMENTS PVT. LTD.

J

J J

J .J ]

]

:J

J

!J

:J

j

J .J

J J J J ,. J J .l

~~ .· ;~

FT GROUP INVESTMENTS PVT. L'fD

FINANCIAL STATEMENTS

YEAR ENDED 31 MARCH 2017

FT Group Investments Pvt. Ltd

Contents Pages

Corporate data 2

Commentary of the directors 3

Certificate from the secretary 4

fndependent auditors' report S -9

Consolidated statement of fmancial position 10

Consolidated statement of comprehensive income 11

Consolidaled statement of changes in equity 12- 13

Consolidated statement of cash flows 14

Notes to the consolidated financial statements 15-46

Fr Group Investments Pvt. ltd

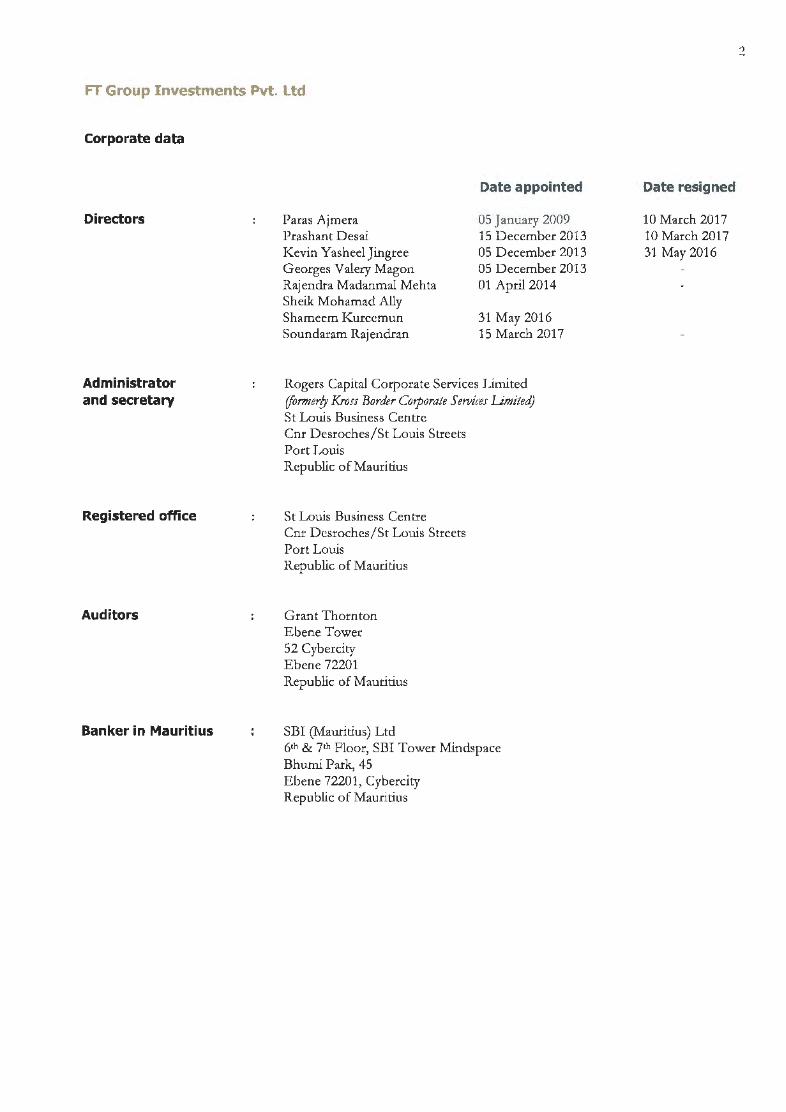

Corporate data

Directors

Administrator and secretary

Registered office

Auditors

Banker in Mauritius

Paras Ajmera Prashant Desai Kevin YasheelJingree Georges Valery Magon Rajendra Madanmal Mehta Sheik Mohamad Ally Shameem Kurccmun Soundaram Rajendran

Date appointed

OS January 2009 15 December 2013 05 December 2013 OS December 2013 01 April2014

31 May 2016 15 March 2017

Rogers Capital Corporate Services J.imited (former!J Kross Border Corporate S ervit'eJ Limited) StLouis Business Centre Cnr Desroches/St Louis Streets Port Louis Republic of Mauritius

StLouis Business Centre Cnr Dcsrochcs/St Louis Streets Port Louis Republic of Mauritius

Grant Thornton Ebene Tower 52 Cybercity Ebene 72201 Republic of Mauritius

SBI (Mauritius) Ltd 6•h & 7•h Floor, SBI Tower Minds pace Bhumi Park, 45 Ebene 72201, Cybercity Republic of Mauritius

Date resigned

10 March 2017 10 March 2017 31 May 2016

2

3

FT Group Investments Pvt. ltd

Commentary of the directors

'1 bt directors have the pleasure in submitting their report together with the audited consolidated financial statements of f<T (1roup Investments Pvt. Ltd, the "Compan)'", for the year ended 31 March 2017. The Company and its subsidiaries a.re collectively referred to as the "Group".

Principal activities

The principal activities of the Group are:

(i) to establish/acquit·e/hold investments globally in auromated electronic market places and/or software companies and/ or knowledge-based companies;

(ii) to operate spot and/or derivative Multi-Assets Class Exchanges; and (iii) to own and operate exchange markets and clearing and settlement corporations.

Results and dividends

The results for the year are as shown on page 11.

The directors did not recommend the payment of any dividend for the year under rc\riew (2016: Nil).

Directors

The present membership of the Board is set out on page 2.

Statement of directors' responsibilities in respect of the consolidated financial statements

Company law requires the directors to prepare consolidated financial statements for each financial year, which present fairly the financial position, financial performance and cash flows of the Group and the Company. In preparing those consolidated financial statements, the directors are required to:

• Select suitable accounting policies and then apply them consistently;

• Make judgements and estimates that are reasonable and prudent;

• State whether applicable accounting standards have been followed, subject to any material departures disclosed and explained in the consolidated financial statements; and

• Prepare the consolidated fmancial statements on the going concern basis unless it is inappropriate to presume tl1at the Group will continue in business.

The directors confirm that they have complied with the above requirements in preparing the consolidated financial statements.

Auditors

The auditors, Grant Thornton, have indicated their willingness to continue in office and a resolution concerning their re-appointment will be proposed at the Annual Meeting.

4

FT Group Investments Pvt. Ltd

Certificate from the Secretary to the member of FT Group Investments Pvt. Ltd

We certify, to the best of our knowledge and belief, that we have filed with the Registrar of Companies all such returns as are required of FI' Group Investments Pvt. Ltd under the Mauritius Companies Act 2001, during the financial year ended 31 March 2017.

for Rogers ~D.!!:!!Ll..&JCJ.l'l>Efrt·e Services Limited Secretary

Registered office:

St Louis Business Centre Cnr Des.roches/St Louis Streets Port Louis Republic of Mauritius

Date: 1 g HAY 20111

5

Grant Thornton Independent auditors' report To the member of FT Group Investments Pvt. Ltd

Report on the Audit of the Consolidated Financial Statements

Qualified Opinion

We have audited the consolidated fmancial statements of FT Group Investments Pvt. Ltd, the "Company", and its subsidiaries, together referred to as the "Group", which comprise the consolidated statement of financial position as at 31 March 2017, and the consolidated statement of comprehensive income, consolidated statement of changes in equity and consolidated statement of cash flows for the year then ended, and notes to the consolidated fmancial statements, including a summary of significant accounting policies.

In our opinion, except for the effects of the matters described in the Basis for Qualified Opinion section of our report, the accompanying consolidated fmancial statements on pages 10 to 46 give a true and fait view of the financial position of the Group and the Company as at 31 March 2017, and of their fmancial performance and their cash flows fo r the year then ended in accordance 'With International Financial Reporting Standards and the requirements of the Mauritius Companies Act 2001.

Basis for Qualified Opinion

Financial Support

Since incorporation, the Group relies on the fmancial support of the holding company as its level of activity docs not generate sufficient cash to support its operations and to meet capital expenditure. At 31 March 2017, the Group had a negative shareholder's fund of USD 81,854,417, which indicate that the Group is still heavily dependent on the holding company to remain in business.

However, the holding company is still faced 'With a number of legal cases for which the outcome is still unknown. In our opinion, any failure to secure the continuous financial support from the holding company will deeply impact the going conccxn of the Group.

Fair value of investment

The Company's subsidiary, Bourse Africa T .imjted (BAL), holds a Securities Exchange Licence issued by the Pinancial Services Commission (FSC) to operate as an Exchange.

Further to issues affecting the holding company, a company incorporated in India, since the financial year 2014/2015, the FSC had requested the latter to dispose of its stake in BAL. As at the date of this report, the disposal has not yet taken place. I Iowever, the holding company being an Indian entity, the completion of the stake sale could be subject to certain regulatory/ judicial approvals in India.

Grant Thornton Mauritius is a member firm of Grant Thornton International Ltd (GTIL). GTIL and the member firms are not a worldwide partnership. Services are delivered by the member firms. GTIL and its member firms are not agents of, and do not obligate, one another and are not liable for one another's acts or omissions.

Please see www.gtmu.com for further details.

6

Grant Thornton Independent auditors' report (Contd) To the member of FT Group Investments Pvt. Ltd

Report on the Audit of the Consolidated Financial Statements (Contd)

Basis for Qualified Opinion {Contd)

Fair value of investment (Contd)

In the meantime BAL had entered into negotiation with a potential buyer to acquire the holding company's stake in BAL. However, due to some procedural reasons at the level of the acquirer, the transaction is still not yet completed as at the date of this report.

The FSC is kept informed on the progress of the negotiation and to that effect BAL has requested the FSC to maintain its licence valid until the positive completion of the transaction.

Because of the significance of the licence for BAL, we believe that any failure to maintain the validity of the licence will deeply affect the very reason for existence of BAL in its capacity to act as a Multi-Asset Class Exchange and this ultimately will affect investment's carrying value of USD 8 million.

We conducted our audit in accordance with International Standards on Auditing. Our responsibilities under those standards are further described in the Auditors' Responsibilities for the Audit of the Consolidated f-iinancial Statements section of our report. We are independent of the Group in accordance with the ethical requirements that arc relevant to our audit of the consolidated financial statements, and we have fulfilled our other ethical responsibilities in accordance with these requirements. \XIe believe that the audit evidence we have obtained 1s sufficient and appropriate to provide a basis for our qualified opinion.

Information Other than the Consolidated Financial Statements and Auditors' Report Thereon ("Other Information")

Management is responsible for the Other Information. T11e Other Infonnation comprises the information included under the Corporate Data and Commentary of the Directors sections, but does not include the consolidated financial statements and our auditors' report thereon.

Our opinion on the consolidated financial statements docs not cover the Other Information and we do not express any form of assurance conclusion thereon.

In connection with our audit of the consolidated financial statements, our responsibility is to read the Other Information and, in doing so, consider whether the Other Information is materially inconsistent with the consolidated fmancial statements or our knowledge obtained in the audit or otherwise appears to be materially misstated. If, based on the work we have performed, we conclude that there is a material misstatement of this Other Information, we are required to report that fact. \X'e have nothing to report in this regard.

Grant Thornton Mauritius is a member firm ol Grant Thornton International ltd (GTILl. GTIL and the member firms are not a worldwide partnership. Services are delivered by the member firms. GTlL and its member firms are not agents of, and do not obligate, one another and are not liable for one another's acts or omissions.

Please see www.gtmu.com for further details.

7

Grant Thornton Independent auditors' report (Contd) To the member of FT Group Investments Pvt. Ltd

Report on the Audit of the Consolidated financial Statements {Contd)

Responsibilities of Management and Those Charged with Governance for the Consolidated financial Statements

Management is responsible for the preparation of the consolidated financial statements in accordance with International Financial Reporting Standards and the requirements of the Mauritius Companies Act 2001 and for such internal control as management determines is necessary to enable the preparation of the consolidated financial statements that arc free from material misstatement, whether due to fraud or error.

In preparing the consolidated financial statements, management is responsible for assessing the Group's ability to continue as a going concern, disclosing, as applicable, matters related to going concern and using the going concern basis of accounting unless management either intends to liquidate the Group or to cease operations, or have no realistic alternative but to do so.

Those charged with governance are responsible for overseeing the Group's financial reporting process.

Auditors' Responsibilities for the Audit of the Consolidated Financial Statements

Our objectives are to obtain reasonable assurance about whether the consolidated financial statements as a whole are free from material misstatement, whether due to fraud or error, and to issue an auditors' report that includes our opinion. Reasonable assurance is a high level of assurance, but is not a guarantee that an audit conducted in accordance with International Standards of Auditing will always detect a material misstatement when it exists. Misstatements can arise from fraud or error and are considered material if, individually or in the aggregate, they could reasonably be expected to influence the economic decisions of users taken on the basis of these consolidated financial statements.

As part of an audit in accordance with International Standards of Auditing, we exercise professional judgment and maintain professional skepticism throughout the audit. We also:

• Identify and assess the risks of material misstatement of the consolidated financial statements, whether due to fraud or error, design and perform audit procedures responsive to those risks, and obtain audit evidence that is sufficient and appropriate to provide a basis for our opinion. The risk of not detecting a material misstatement resulting from fraud is higher than for one resulting from error, as fraud may involve collusion, forgery, intentional omissions, misrepresentations, or the override of internal control.

• Obtain an understanding of internal control relevant to the audit in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the Company's internal control.

• Evaluate the appropriateness of accounting policies used and the reasonableness of accounting estimates and related disclosures made by management.

Grant Thornton Mauritius is a member firm of Grant Thornton International Ltd tGTIL). GTIL and the member firms are not a worldwide partnership. Services are delivered by the member firms. GTIL and its member ~rms are not agents of, and do not obligate, one another and are not liable for one another's acts or omissions.

Please see www.gtmu.com for further details.

8

Grant Thornton Independent auditors' report (Contd) To the member of FT Group Investments Pvt. Ltd

Report on the Audit of the Consolidated Financial Statements (Contd)

Auditors' Responsibilities for the Audit of the Consolidated Financial Statements ( Contd)

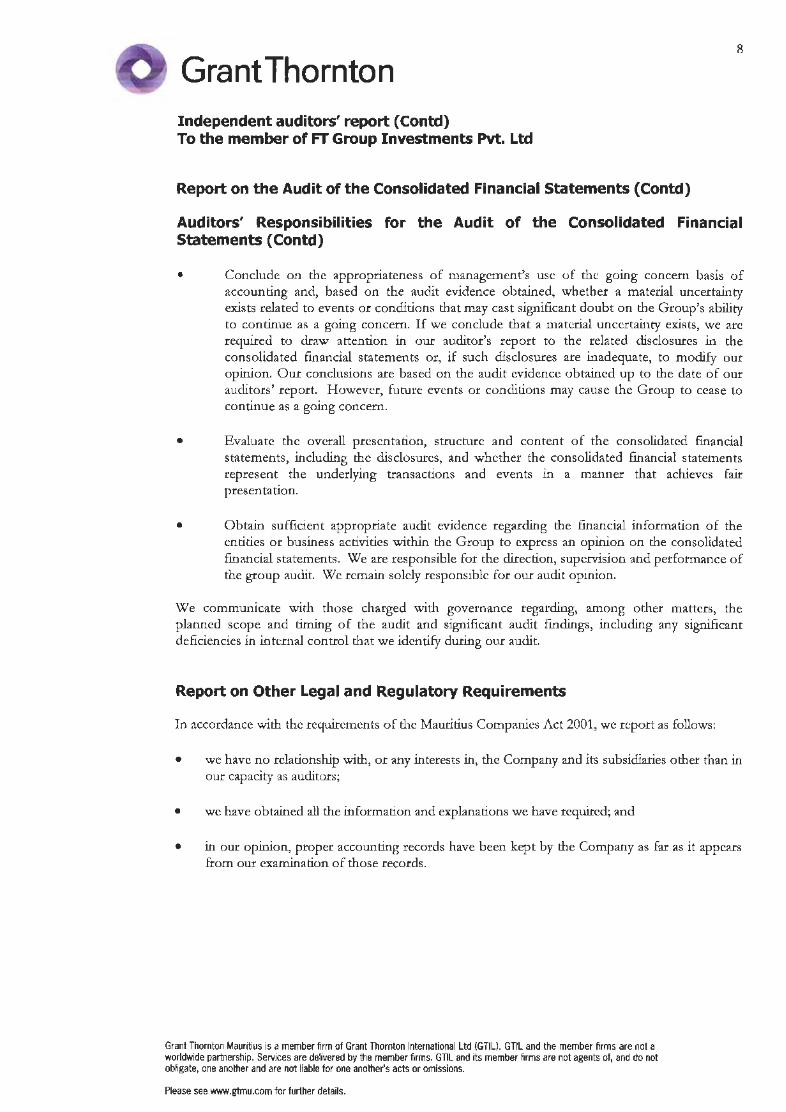

• Conclude on the appropriateness of management's usc of the going concern basis of accounting and, based on the audit evidence obtained, whether a material uncertainty exists related to events or conditions that may cast significant doubt on the Group's ability to continue as a going concern. If we conclude that a material uncertainty exists, we arc required to draw attention in our auditor's report to the related disclosures in the consolidated financial statements or, if such disclosures are inadequate, to modify our opinion. Our conclusions are based on the audit evidence obtained up to the date of our auditors' report. However, future events or conditions may cause Lhe Group to cease Lo continue as a going concern.

• Evaluate the overall presentation, structure and content of the consolidated financial statements, including the disclosures, and whether the consolidated financial statements represent the underlying transactions and events in a manner that achieves fair presentadon.

• Obtain sufficient appropriate audit evidence regarding the financial information of the entities or business activities within the Group to express an opinion on the consolidated financial statements. We are responsible for the direction, supervision and perfot·mance of the group audit. We remain solely responsible for our audit opinion.

We communicate with those charged with governance regat·ding, among other. matters, the planned scope and timing of the audit and significant audit fmdings, including any significant deficiencies in internal control that we identify during our audit.

Report on Other Legal and Regulatory Requirements

In accordance with the requirements of the Mauritius Companies Act 2001, we report as follows:

• we have no relationship with, or any interests in, the Company and its subsidiaries other than in our capacity as auditors;

• we have obtained all the information and explanations we have :required; and

• in our opinion, proper accounting records have been kept by the Company as far as it appears from our examination of those records.

Grant Thornton Mauritius is a member ~rm of Grant Thornton International Ltd (GTIL). GTIL and the member firms are not a worldwide partnership. Services are delivered by the member firms. Glll and its member firms are not agents of, and do not obligate, one another and are not liable for one another's acts or omissions.

Please see www.gtmu.com for further details.

Grant Thornton Independent auditors' report ( Contd} To the member of FT Group Investments Pvt. Ltd

Report on Other Legal and Regulatory Requirements (Contd)

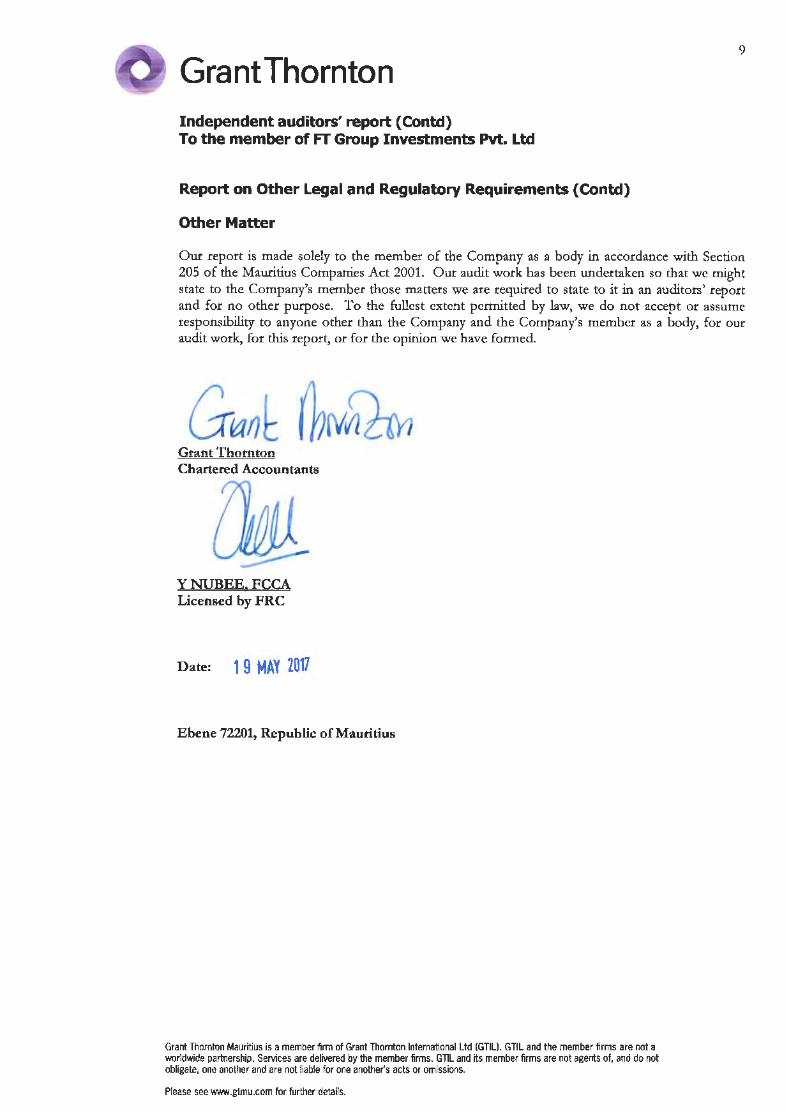

Other Matter

9

Our report is made solely to the member of the Company as a body in accordance with Section 205 of the Mauritius Companies Act 2001. Our audit work has been Wtdertaken so that we might state to the Company's member those matters we are required to state to it in an auditors' report and for no other purpose. To the fullest extent pennitted by law, we do not accept or assume responsibility to anyone other than the Company and the Company's member as a body, for our audit work, for this report, or for the opinion we have formed.

Grant Thornton Chartered Accountants

Y NUBEEt FCCA Licensed by FRC

Date: 19 MAY 2017

Ebene 72201, Republic of Mauritius

Grant Thornton Mauritius is a member finn of Grant Thornton International Ltd {GTILI. GTIL and the member firms are not a worldwide partnership. Services are delivered by the member firms. GllL and its member firms are not agents of, and do not obligate, one another and are not liable for one another's acts or omissions.

Please see WWN.gtmu.com for further details.

10

FT Group Investments Pvt. ltd

Consolidated of financial ..

statement pos1t1on as at 31 March

The Group The Company

Notes 2017 2016 2017 2016

USD USD uso USD

Assets

Non-current

Intangible assets 7 1 293,333

Property, plant and equipment 8 167,649 297,196

Investments in subsidiaries 9 8,000,000 8,000,000

Non-current assets 167,650 590,529 8,000,000 8,000,000

Current

Trade and other receivables 11 1,075,120 1,073,428 573,554 137,578

cash and cash equivalents 12 2,963,165 5,812,428 1!441,633 3,857,730

Current assets 4,038,285 6,885,856 2,015,187 3,995,308

Total assets 4,205,935 7,476,385 10,015,187 11,995,308

Equity and liabilities

Equity

Stated capital 13 124,060,002 124,060,002 124,060,002 124,060,002

Accumulated losses (205,006,707) (198,581,465) (199,227 ,908) ( 194,046,932)

Translation reserves (907,712) (904,618)

Total equity (81,854,417) (75,426,081) (75,167,906} (69,986,930)

Liabilities

Non-current

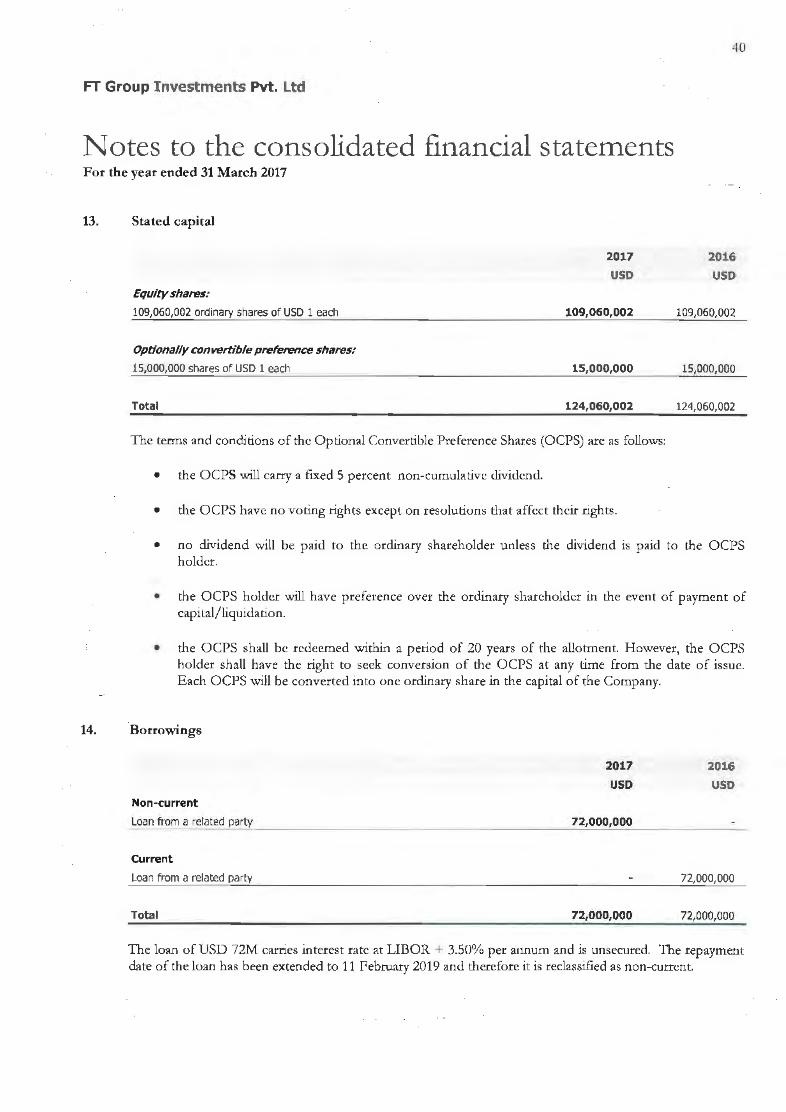

BorTowings 14 72,000,000 72,000,000

Provision for employees benefits 95,967 61,214

Non-current liabilities 72,095,967 61,214 72,000,000

Current

BorTowings 14 72,000,000 72,000,000

Payables 15 13,885,619 10,782,751 13,183,093 9,982,238

Deferred income 16 78,766 58,501

Current liabilities 13,964,385 82,841,252 13,183,093 81,982,238

Total liabilities 86,063,352 82,902,466 85,183,093 81,982,238

Total equity and liabilities 4,205,935 7,476,385 10,015,187 11,995,308

Apptov;w:.: __ l..:....._9_ H_AY __ 2G_l_7_. ___ and signed on its bc-=-h-al-f -by-:--\:.'--AJ- -4------

Dir.ector Director

The notes on pages 15 to 46 form an integral part of these consolidated financial statements.

11

FT Group Investments Pvt. ltd

Consolidated statement of comprehensive 1ncome for the year ended 31 March

The Group Notes 2017 2016

USD USD

4,892 6,793 324,130

Income Interest Other income

~----------------------------------~~~~ 407,622

Expenditure

Salaries and other benefits Legal and professional fees Interest expense Bank commissions and charges Travelling expenses Rental fees Other expenses IT expenses Audit fees Depredation and amortisation Net foreign exchange losses Loss on disposal of available-for-sale ftnandal assets Business development costs Bad debts written off Impairment of loans and interest Direct costs Impairment losses on investments in subsidiaries Impairment of goodwill Impairment losses on available-for-sale financial assets

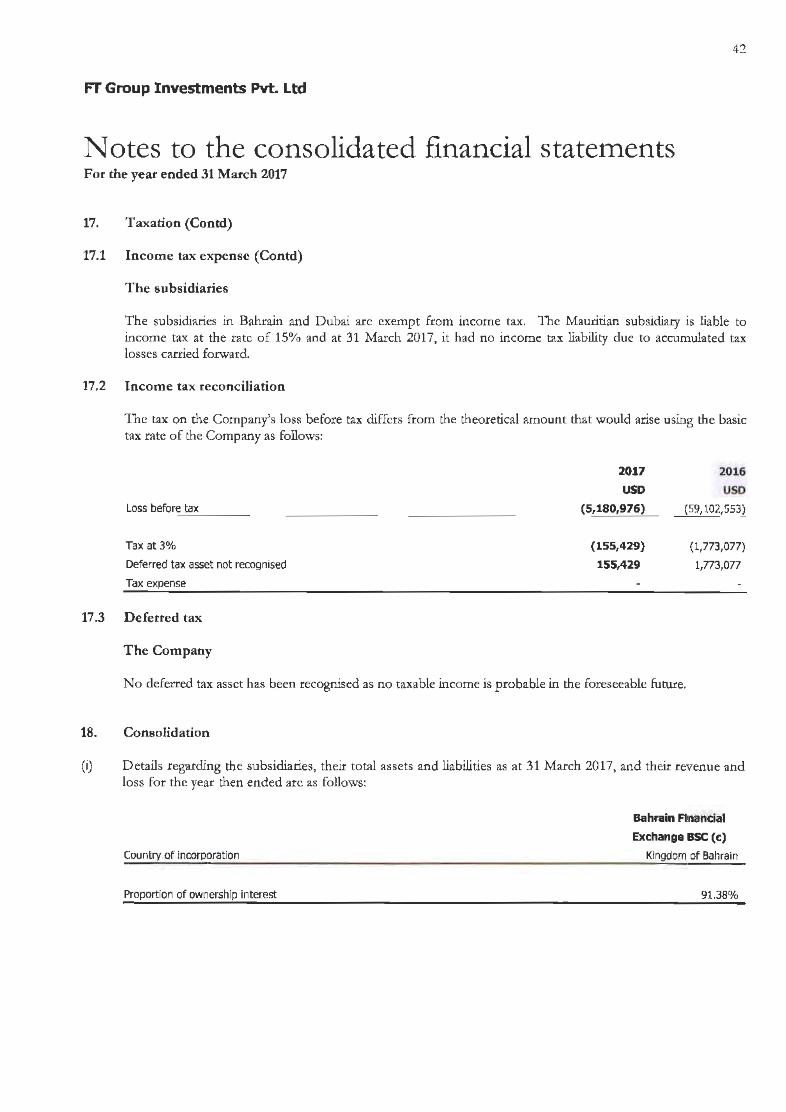

loss before tax

Tax expense

Loss for the year

Other comprehensive income for the year, net of tax: Items that will not be reclassified subsequently to profit or loss

Items that will be reclassified subsequently to profit or loss

Exchange differences on translation of foreign operations

Total comprehensive income for the year

7&8

10

11

9 6

10

17

329,022

1,785,623 207,189

3,203,153 4,416 6,781

108,588 528,725 258,794

26,880 422,879

21,401

7,357

32,543 139,935

6,754,264

(6,425,242)

(6,425,242)

(3,094}

(6,428,336)

414,415

1,743,736

333,745

2,866,608

6,052

11,302

102,377 550,264

241,323

27,422

4,016,604

20,727

4,184,253

104,247

8,059 273,221

192,707

29,401,781

999,190

45,083,618

(44,669,203)

(44,669,203)

(1,123,778)

The Company 2017 USD

434,623

434,623

74,395 3,203,349

2,312

18,000

1,517,543

800,000

5,615,599

(5,180,976)

(5,180,976)

(5,180,976}

2016 USD

297,032

297 032

56,800

2,864,783

2,602

18,500

4,184,253

44,975,001

10,000

59,399,585

(59,102,553)

(59,102,553)

The notes on page:; 15 to 46 form an integral part of these consolidated financial statements.

12

FT Group Investments Pvt. Ltd

Consolidated of changes .

for statement 1n eqmty the year ended 31 March The Group

Total

attributable to

stated Accumulated Translation owner of

capital losses reserves parent Total

USD USD USD USD USD At 01 April 2016 124,060,002 ( 198,581,465) (904,618) (75,426,081) (75,426,081)

Loss for tl1e year (6,425,242) (6,425,242) (6,425,242)

Otl1er comprehensive inrome for the year (3,094) (3,094) (3,094)

Total comprehensive income for the year (6,425,242) (3,094) (6,428,336) (6,428,336)

At 31 March 2017 124,060,002 (205,006,707) (907,712} (81,854,411) (81,854,417)

At 01 April 2015 124,060,002 (155,316,544) 219,160 (31,037,382) (31,037,382)

Movement in equity on de-recognition of a

subsidiary 1,404,282 1,404,282 1,404,282

Loss for the year (44,669,203) (44,669,203) (44,669,203)

Otl1er romprehenslve Income for the year (1,123,778) (1,123,778) (1,123,778)

Total comprehensive Income for the year (43,264,921) (1,123,778) (44,388,699) (44,388,699)

At 31 March 2016 124,060,002 (198,581,465) (904,618) (75,426,081) (75,426,081)

The notes on pages 15 to 46 form an integral part of the$(~ consolidated financial statements.

13

FT Group Investments Pvt. Ltd

Consolidated statement of changes in equity for the year ended 31 March (Contd) The Company

At 01 April 2016

Loss for the year

Other comprehensive income for the year

Total comprehensive income for the year

At 31 March 2017

At 01 April2015

Loss for the year

Other comprehensive income for the year

Total comprehensive income for the year

At 31 March 2016

stated

capital

USD 124,060,002

124,060,002

124,060,002

124,060,002

Accumulated

losses

USD (194,046,932}

(5,180,976}

(5,180,976)

{199,227,908}

(134,944,379)

(59,102,553)

(59,102,553)

(194,046,932)

The notes on pages 15 to 46 form an integral part of these consolidated financial statements.

Total

USD (69,986,930)

{5,180,976)

(5,180,976)

{75,167,906)

{10,884,377)

(59,102,553)

(59,102,553)

(69,986,930)

14

FT Group Investments Pvt. ltd

Consolidated statement of cash flows for the year ended 31 March

Operating activities Loss before tax

Adjustments for:

Depreciation and amortisation

Loss on disposal on available-for-sale financial assets Interest income

Interest expense

Impairment losses on investments in subsidiaries

Impairment losses on available-for-sale financial assets Movement in employees benefits Interest and loans written off Impairment of goodwill

Total adjustments

Cl1anges in working capital:

Change in trade and other receivables

Change in other payables and accruals Change in deferred income

----------------------~----

Total changes in working capital

Net cash used in operating activities

Investing activities Interest received Loan advanced

The Group 2017 2016 USD

(6,425,242)

422,879

(4,892)

3,203,153

34,405

32,543

3,688,088

(1,692} (101,666)

20,265

(83,093}

(2,820,247)

USD

(44,669,203)

4,016,604 4,184,253

(6,793) 2,866,608

999,190

(63,341) 273,221

29,401,781

41,671,523

90,278 (1,300,540)

(14,639)

(1,224,901)

The Company 2017 2016 USD

(5,180,976)

(434,623)

3,203,349 800,000

1,517,543

5,086,269

(4,016)

(2,494)

(6,510)

(101,217)

USD

(59,102,553)

4,184,253 (297,032) 2,864,783

44,975,001

10,000

7,287,645

59,024,651

1,985 7,026

9,011

(68,891)

4,892 (32,543)

6,270 2,662 23,919 (137,140) (2,317,542) (3,828,270)

Proceeds from disposal of available· for-sale financial assets Net cash flow used in investing activities

_________________ 4.cr'-=-19:...:6:.c:,5:..:5..:.5 __________________ ...c4ct.:,l:.=.95,319

Financing activities Proceeds from b~rrowings Net cash flow from financing activities

Net change in cash and cash equivalents Exchange differences on cash and cash equivalents cash and cash equivalents at the beginning of the year Cash derecognised on derecognition of subsidiary Cash and cash equivalents at the end of the year

cash and cash equivalents made up of: cash at bank and in hand (Note 12)

(27,651)

(2,847,898) (1,365)

5,812,428

2,963,165

4,065,686 (2,314,880) 390,968

2,000,000 2,000,000

1,843,105 295,850

3,701,740 (28,267)

5,812,428

5,812,428

1,441,633

1,441,633

2,000,000 2,000,000

2,322,077

1,535,653

3,857,730

3,857,730

The notes on pages 15 to 46 form an integral part of these consolidated financial statements.

15

FT Group Investments Pvt. ltd

Notes to the consolidated financial statements For the year ended 31 March 2017

1. General information and statement of compliance with the International Financial Reporting Standards

FT Group Investments Pvt. Ltd, the "Company", was incorporated in the Republic of Mauritius under the Mauritius Companies Act 2001 on 28 March 2007 as a private company with liability limited by shares. 111c Company holds a Category 1 Global Business Licence issued by the Financial Services Commission. The Company's registered office is c/o Rogers Capital Corporate Services Limited, St Louis Business Centre, Cnr Desroches/St J .ouis Streets, Port Louis, Republic of Mauritius.

The Company and its subsidiaries are collectively referred to as the "Group".

1l1c principal activities of the Group are:

• to establish/ ac<)tlirc/hold investments globally in an automated electronic market places and/ or software companies and/or knowledge-based companies;

• to operate spot and/or derivative Multi-Asset Class Exchanges; and • to own and operate exchange markets and clearing and settlement corporations.

1l1e consolidated financial statements of the Group have been prepared in accordance with International Financial Reporting Standards ("IPRS") as issued by International Accounting Standards Board (IASB).

2. Application of new and revised !FRS

2.1 New and revised standards that are effective for the year beginning on 01 April2016

In the current year, the following new and revised standards issued by the International Accounting Standards Board ("IASB'') became mandatory for the first time adoption for the financial year beginning on 01 April2016:

lAS 16 and lAS 38 L\S 16 and lAS 41 lAS 27 !FRS 11 IFRS 14 IFRS 10, IFRS 12 and lAS 28 lAS 1

Clarification of Acceptable Methods of Depreciation and Amortisation (Amendments to lAS 16 and lAS 38)

Agriculture: Bearer Plants (Amendments to lAS 16 and lAS 41) Equity Method in Separate Financial Statements (1\mendments to L\S 27) Accounting of Acquisitions of Interests in Joint Operations (Amendments to IfRS 11) Regulatory Deferral Accounts Investment Entities: Applying the Consolidation Exception (Amendments to IFRS 10, IFRS 12 and lAS 28) Disclosure Initiative (Amendments to LI\S 1 Presentation of Pinancial Statements)

'lhe directors have assessed the impact of the new and revised standards and concluded that only lAS 1, Disdosun Initiative (/lmendmenls to IA.5' 1) has impact on the disclosures of these consolidated financial statements.

16

FT Group Investments Pvt. ltd

Notes to the consolidated financial statements For the year ended 31 March 2017

2. Application of new and revised IFRS (Contd)

2.2 Standards, amendments to existing standards and interpretations that are not yet effective and have not been adopted early by the Group

At the date of authorisation of these fmancial slatements, certain new standards and amc.:ndments to existing standards and one interpretation have been published by the lASE but not yet effective, and have not been adopted early by the Group.

Management anticipates that all of the relevant pronouncements as applicable to the Group's activity will be adopted in the G roup's accounting policies for the first period beginning after the effective date of the pronouncements. Information on the new standards, amendments to existing s tandards and intL-rprctation is provided below.

lAS 12 lAS 7 IFRS 1S IrRS 9 IFRS 4 IFRS 2 IAS40 TrRS 16 lFRTC 22

Recognition of Deferred Tax Assets for Unrealised Losses (Amendments to lAS 12) Disclosw:e Initiative (Amendments to lAS 7) Revenue from Contracts with Customers rinancial ins truments (2014-) Applying IFRS 9 Pinancial Ins truments with IFRS 4 Insurance Contracts (Amendments to IFRS 4) Classification and Measurement of Share-based Payment T ransactions (Amendments to TFRS 2) Transfer of Investment Property (Amendments to Ii\.S 40) Lease~

Porcign Currency Transactions and i\dvance Consideration

Management has yet to assess the impact of the above standards, amendments and interpretation on the Group's consolidated financial statements.

3. Summary of accounting policies

3.1 Overall considerations

'lbc consolidated financial statements have been prepared usmg the significant accounting policies and measurement bases summarised below.

3.2 Basis of consolidation

The Group consolidated financial statements consolidate those of the Company and all of its subsidiaries. 'l'he parent controls a subsidiary if it is exposed, or has rights, to variable returns from its involvement with the subsidiary and has the ability to affect those rerurns through its power over the subsidiary. 1\ll subsidiaries have a reporting date of 31 March.

All transactions and balances between Group companies arc eliminated on consolidation, including unrcalised gains and losses on transactions between Group companies. Where unrealised losses on intra-group asset sales arc reversed on consolidation, the w1derlying asset is also tested for impairment from a group perspective. Amounts reported in the consolidated financial statements of subsidiaries have been adjusted where necessary to ensure consistency with the accounting policies adopted by the Group.

Profit or loss and other comprehensive income of subsidiaries acquired or disposed of during the year arc recognised from the effective date of acquisition, or up to the effective date of disposal, as 11pplicable. Results of subsidiaries which have been placed under liquidation procedures at the reporting date arc also not consolidated.

17

FT Group Investments Pvt. Ltd

Notes to the consolidated financial statements For the year ended 31 March 2017

3. Summary of accounting policies (Contd)

3.3 Busine11s combinations

The Group applies the acquisition method in accounting for business combinations. The consideration transfcrr<xl by the Group to obtain wntrol of a subsidiary is calculated as the sum of the acquisition-date fair values of assets transferred, liabilities incurred and the equity int~rcsts issued by the Group, which includes the fair value of any asset or liability arising from a contingent consideration arrangement. 1\cquisition costs arc expcnscd as incurred.

The Group recognises identifiable assets acquired and liabilities assumed in a business combination regardless of whcthcr they have been previously recognised in the acquirce's financial statements prior to the acquisition. Assets acquired and liabilities assumed are generally measured at thcir acquisition-date fair values.

Goodwill is stated after separate recognition of identifiable intangible assets. lt is calculated as th~ c.;"<:ccss of the sum of a) fair value of consideration transferred, b) the recognised amount of any non-cont.rolling interest in the acquiree and c) aC(Juisition-date fair value of any ex.isting equit}' interest in the acquiree, over the acquisition-date fair values of identifiable net assets. If the fair values of identifiable net assets exceed the sum calculated above, the excess amount (le gain on a bargain purchase) i.~ recogiused in profit or loss immediately.

3.4 Investment in subsidiaries

A subsidiary is an entity over which the Company has control. The Company controls an entity when it iR exposed to, or has rights to, variable returns from its involvement with the entity and has ability to affect those returns through its power over the entity. Subsidiaries are fully consolidated from the date on which control is transferred to the Company. They arc dcconsolidated from the date that control ceases.

Investment in subsidiary is stared at cost. \'\'here an indication of impairment exists, the recoverable amount of the investment is assessed. Where the carrying amount of the investment is greater than its estimated recoverable amount, it is written down immediately to its recoverable amount and the difference is charged to statement of profit or loss. On disposal of the investment, the difference between the net disposal proceeds and the carrying amount is charged or credited to consolidated sratcment of compt·ehensive income.

The valuation of investments may not necessarily represent the amounts that may eventually be realised from sales or other dispositions.

3.5 Goodwill

Goodwill represents the future economic benefits artsmg from a business combination that are not individually idenlified and separately recognised. See Note 3.3 for information on how goodwill is initially determined. GoodwiU is carried at cost less accumulated impairment losses, if any. Refer to Note 3.11 for a description of impairment testing procedures.

3.6 Foreign currency

Functional and presentation currency

'l'hc consolidated financial statements arc presented in currency USD, which is also the functional currency of the Group.

18

FT Group Investments Pvt. ltd

Notes to the consolidated financial statements For the year ended 31 March 2017

3. Summary of accounting policies (Contd)

3.6 Foreign currency (Contd)

Foreign currency transactions and balances

Porcign currency transactions are translated into the functional cunency o f the Group, using the exchange rates prevailing at the tlatcs of the transactions (spot exchange rate). Foreign exchange gains and losses resulting from the settlement of such transactions and from the re-measurement of monetary items denominated in foreign currency al year-end exchange rates are recognised in the statement of comprehensive mcome.

Non-monetary items are not retranslated at year end anti arc measured at historical cost (translated using the exchange rates at the transaction date), except for non-monetary items measured at fair value which arc translated using the exchange rates at the date when fair value was delermined.

Foreign operations

In the Group's financial statements, all assets, liabilities and transactions of the Group enttues with a functional currency other than the USD are translated into USD upon consolidation. The functional currency of the entities in the Group has remained unchanged during the reporting period.

On consolidation, assets and liabilities have been translated into t;SD at the closing rate at the reporting date. Goodwill and fair value adjustments arising on the acquisition of a foreign entity have been treated as assets and liabilities of the foreign entity and translated into USD at the closing rate. Income and expenditure have been translated into USD at the average rate over the reporting rate.

Exchange differences are charged/ credited to other comprehensive income and recognised in the currency translation reserve in equity. On disposal of a foreign operation, the related cumulative translation differences recognised in equity are rcclassifted to profit or loss and arc recognised as part of the gain or loss on disposal.

The average exchange rates for the year ended 31 March 2017 were as follows:

BHD/USD

AED/USD

3.7 Revenue recognition

Dividend income is recognised when the right to receive payment is established.

USD 2.64158

0.27228

Interest income is recognised on the accrual basis using the effective interest method, unless collectibility is in doubt

Trading commission fees are recognised on the date of transaction .in tl1e market.

Admission fees collected from prospective members prior to joining the exchange arc recognised as advances from members. Advances against membership application are only recognised as income when the application has been approved.

Invoices for annual fees are raised on a half yearly basis and is recorded on an accmal basis.

19

FT Group Investments Pvt. Ltd

Notes to the consolidated financial statements For the year ended 31 March 2017

3. Summary of accounting policies (Contd)

3.8 Operating expenses

Operating expenses are recognised in profit or loss upon utilisation of the service or at the date of their origin.

3. 9 Borrowing costs

Borrowings costs directly attt1butable to the acquisition, consttuction or production of a qualifying asset arc capitalised during the period of time that is necessary to complete and prepare the asset for its intended use or sale. Orher borrowings costs arc cxpcnscd in thc period in which they are incurred and reported in finance costs.

3.10 Property, plant and equipment

Property, plant and equipment arc initially recognised at acquisition cost or manufacturing cost, including any costs directly attt1butable to bringing the assets to the location and condition necessary for it to be capable of operating in the manner intended by management. Property, plant and equipment are subsequently measured using the cost model, cost less subsequent depreciation and impainnent losses.

Depreciation is recognised on a straight-line basis to write down the cost less estimated residual values of property, plant and equipment. The following useful lives :u·e applied:

I'urniturc and fittings Office equipment Motor vehicles Improvement to leasehold building

3- 10 years 3- 10 years 4- 10 years 3 years

No depreciation is charged on items of property, plant and equipment which are not yet in use and also on items not yet received and for which payments have already been made. In the case of leasehold property, expected useful lives are determined by reference to comparable owned assets or over the term of the lease, if shorter.

\Vhere the carrying amount of an asset is greater than its estimated recoverable amount, it is written down immediately to its recoverable amount. Gains and losses on disposal of property, plant and equipment are determined by reference to their carrying amount and are taken into account in determining operating profit. On disposal of an asset, the difference between the carrying value of the asset and sale consideration taken to the statement of comprehensive income.

Material residual value estimates and estimates of useful life are updated as reguired, but at least annually. Repairs and maintenance cost~ are expensed as incUI'red.

3.11 Impairment testing of goodwill and other intangible assets

I'or impainnent assessment purposes, assets are grouped at the lowest levels for which there are largely independent cash inflows (cash-generating units). As a result, some assets are tested individually for impairment and some are tested at cash-generating unit level. Goodwill is allocated to those cashgenerating units that are expected to benefit from synergies of the related business combination and represent the lowest level within the Group at which management monitors goodwill.

20

FT Group Investments Pvt. ltd

Notes to the consolidated financial statements For the year ended 31 March 2017

3. Summary of accounting policies (Contd)

3.11 Impairment testing of goodwill and other intangible assets (Contd)

Cash-generating units to which goodwill has been allocated (determined by management as equivalent to its operaling segments) are lested for .impairment at least annually. i\11 other individual assets o.r cashgenerating units arc tested for impairtn\:nt whenever events or c.:hangc; in circumstances indicate that the carrying amounr may not be recoverable.

i\n impairment loss is recognised for the amount by which the asset's or cash-generating unit's canying amount exceeds its recoverable amount, which is the higher of fair value less cost of disposal and vahle-inuse. To determine the value-in-usc, management estimates expected future cash flows from each cashgenerating unit and determines a suitable interest rate in order to calculate the present value of those cash flows. The data used for impairment testing procedures are directly linked to the Group's latest approved budget, adjusted as necessary to exclude lhe effects of funtre reorganisations and asset enhancements. Discount factors are determined for each cash-generating unit and reflect management's assessment of respective risk proftlcs, such as market and asset-specific risks factors.

Impairment losses for cash-generating units reduce first the carrying amount of any goodwill allocated to that cash-generating unit. Any remaining impairment loss is charged pro rata to the other assets in the cash-generating unit. With the excep tion of goodwill, all assets are subsequently reassessed for indications that an impairment loss previously recognised may no longer exist. An impairment loss is reversed if the asset's or cash-generating unit's recoverable amount exceeds its carrying amount.

3.12 Intangible assets

Intangible assets represent software licences for the Trading, Matching and Clearing Mechanism of the MultiAsset Class Exchange (the "Exchange") and are amortised over their estimated useful lives of five years.

Residual values and useful lives are reviewed at each reporting date. In addition, all intangible assets are subject to impairmenllesting.

Acquired computet softwares are capitalised on the basis of the costs incurred to acquire and bring to use d1e specific soflwares.

Costs associated with maintaining computer software programmes ate expensed as incurred.

3.13 Impairment of assets

At each reporting date, the Group reviews the carrying amounts of its assets to determine whether there is any indication that those assets have suffered an impairment loss. When an indication of an impairment loss exists, the carrying amount of the asset is assessed and is written down to its recoverable amount.

3.14 Financial instruments

Recognition, initial measurement and derecognition

Financial assets and financial liabilities are recognised when the Group becomes a party to the contractual provisions of the financial instrument and ate measured initially at fair value adjusted by transactions costs, except for those carried at fair value through profit or loss which are measured initially at fair value. Subsequent measurement of fmancial assets and fmancialliabilitics are described below.

21

FT Group Investments Pvt. Ltd

Notes to the consolidated financial statements For the year ended 31 March 2017

3. Summar:y of accoun ting policies (Contd)

3.14 Financial instruments (Contd)

Recognition, initial measurement and derecognition (Contd)

Financial assets are derecogniscd when the contractual rights to the cash flows from the financial asset expice, or when the financial asset and all substantial risks and rewards ar.e transferred. A financial liability is dcrccognised when it is extinguished, discharged, cancelled or expires.

Classification and subsequent measurement of financial assets

For the purpose of subsequent measurement, fmancial assets, other than those designated and effective as hedging instruments, are classified into available-for-sale financial assets, and loans and receivables.

All financial assets except for those at fair value through profit or loss arc subject to review for impairment at least at each reporting date to identify whether there is any objective eviden<.:e that a financial asset or a group of financial assets is impaired. Different criteria to determine impairment arc applied for each category of financial assets.

The ca tegor:y determines subscgucnt measurement and whether any resulting income and expense IS

recognised io profit or loss or in other comprehensive income.

All income and c::xpcnses relating lo financial assets thal are recognised in the consolidated statement of comprehensive income arc presented within fmance income, finance costs or other financial items, excc::pt for impairment of receivables which is presented within administrative expenses.

Atlailablefor-Jale jinamial aJJcls

Available-for-sale fmancial assets arc non-derivative [mancial assets that do not qualify for inclusion in any of the other categories of financial assets. The Group's available-for-sale financial assets consist of investments as disclosed in Note 10 to these consolida ted fm ancial statements.

Available-for-sale financial assets consist of investments in equity shares that arc not quoted in an active market. The best estimate of fair value is the transa<.:lion price on initial recugtulion ur l11e value al which a share transaction has been contracted.

Available-for-sale financial assets whose fair value cannot be measured reliably are carried at cost less impairment.

'l'he valuation of financial assets may not necessarily represen t the amounts that may eventually be realised from sales or othe.r dlsposicions.

Loan.r and m·eivable.r

Loans and receivables arc non-derivative financial assets with fixed or determinable payments that are not quoted in an active market. After initial recognition these arc measured at amortised cost using the effective interest method, less provision for impairment. Any change in their value is recognised in profit or loss. Discounting, however, is omitted where the effect of discounting is immaterial. TI1e Group's cash and cash equivalents and most receivables fall into dus category of financial i.tlsLrumeut:;.

22

FT Group Investments Pvt. Ltd

Notes to the consolidated financial statements For the year ended 31 Match 2017

3. Summary of accounting policies (Contd)

3.14 Financial instruments (Contd)

Classification and subsequent measurement of financial assets (Contd)

LoanJ' and m·et'vables (Contd)

An allowance for credit losses is established if there is objective <:vidence that the Group will be unable to collect all amounts due.

Individually significant receivables are considered for impairment when they arc past due or when other objective evidence is received that a specific counterparty will default. Receivables that are not considered to be individually impaired are reviewed for impairment in groups, whjch are determined by reference to the industry and region of a counterparty and other shared credit risk characteristics. The impairment loss estimate is chen based on rccmt hjstorical counte1.parly default rates for each identified group.

Classification and subsequent m easurement of financial liab ilities

The Group's fmancialliabilities include payables and botTowings.

Fi.nancial liabililies art: measured subseguently at amortised cost using the effective interest method.

All interest-related charges on financial liabilities are included '>Vithin finance costs or finance income.

O ffsetting financial instruments

Financial assets and liabilities arc offset and the net amount reported in the consolidated statement of financial position when there is a legally enforceable right to offset the recognised amounts and there is an intention to settle on a net basis or realise the asset and settle the liability simultaneously.

3.15 Cas h and cash equivalents

Cash and cash equivalents comprise cash at bank. Cash equivalents are short term, hjghly liquid investments maturing within 90 days from the da te of act}uisicion thar are readily convertible to known amounts of cash and whjch arc subject to an insignificant risk of change in value.

Bank overdrafts are shown within borrowings in current liabilities.

3.16 E quity and reserves

Stated capital is determined using the nominal values of shares that have been issued.

Translation reserve comprises of forcign currency translation <liffcrenccs arising from the translation in USD of the fmancial statements of the Group's forcign entities.

Accumulated losses include all current and prior years' results.

All transactions with owner of the parent are recorded separately within equity.

23

FT Group Investments Pvt. Ltd

Notes to the consolidated financial statements For the year ended 31 March 2017

3. Summary of acco unting policies (Contd)

3.17 T axation

Tax expense recognised in profit or loss comprises the sum of deferred tax and current tax not recognised in other comprehensive income or directly in equity.

Current income tax assets and/ or liabilities comprise those obligations to, or claims from, fiscal authorities relating to the current or prior reporting periods, that are unpaid at the reporting date. Current tax is payable on taxable profit, which differs from profit or loss in the f111ancial statements. Calculation of current tax is based on tax rates and tax laws rhat have bct'll enacted or substantively enacted by the end of the reporting period in the respective jurisdictions where each entity is incorporated.

'l1le subsicliary, Bourse Africa J .imited, is also subject to Corporate Social Responsibility Fund (CSRF) and the contribution is at a rate of 2% on the chargeable income of the preceding financial year.

However, effective as from 01 January 2017, further to changt: in the income tax legislation, a resident company is required to contribute at least 50% of its CSR money to the National CSR Foundation through the Mauritius Revenue Authority. The remaining 50% of the CSR can be used in accordance with the entity's own CSR Fund. The rate of contribution wiU further change to 75% in the following year.

Deferred income ta~cs arc calculated using the liability method on temporary differences between the carrying amounts of assets and liabilities and their tax bases.

D eferred tax assets and liabilit.ies arc calculated, without discounting, at tax rates that are expected to apply to their respective period of realisation, provided they are enacted or substantively enacted by the end of the reporting period.

Deferred tax assets are recognised to the extent that it is probable that they will be able to be utilised against future Laxablc income, based on the Group's forecast of fuLure operating results which is adjusted for significant non-taxable income and expenses and specific limits to the use of any unused tax loss or credit. Deferred tax liabilities arc always provided for in full.

Deferred tax assets and liabilities arc offset only when the Group has a right and intention to set off current tax assets and liabilities from the same taxation authority.

Changes in defer.red tax assets or liabilities ar.e recognised as a component of tax income or expense in profit or loss, except where they relate to items that are recognised in other comprehensive income or directly in equity, in which case the related deferred tax is also recognised in o ther comprehensive income or equity, respectively.

3.18 Leased assets

Operating leases

Where the Group is a lessee, payments on operating lease agreements arc recognised as an expense on a straight-line basis over the lease term. Associated costs, such as maintenance and insurance, are expensed as incurred. Any contingent rents are expensed in the period they are incurred.

24

FT Group Investments Pvt. ltd

Notes to the consolidated financial statements For the year ended 31 March 2017

3. Summary of accounting policies (Contd)

3.19 Related parties

A related party is a person or company where that person or company has control or joint control of the r.eporting company; has significanl influence over d1e reporting company; or is a member of the key management personnel of the reporting company or o f a parent of rlle reporting company.

3.20 Provisions

Provisions are recognised when the Group has a present legal or constmctive obligation as a result of past events, it is probable that an outflow o f resources embodying economic benefits will be required to settle rlle obligation, and a reliable estimate of the amount can be made. At time of effective p ayment, the provision is deducted from the corresponding expenses. All known risks at the reporting date are reviewed in detail and provision is made where nccessa1y.

3.21 Employee Benefits

Employees' end of service benefits

Pensions rights (and oilier social benefits) for the Bahraini employees arc covered by Social Insurance Organisation Scheme to which employees and employers contribute monthly on a fixed-percentage-of-salaries basis. "lbe Group's share of contributions to the scheme, which is a defined contribution scheme under lAS 19- Employee Benefits, is recognised as expense in the consolidated statement of comprehensive income.

Expatriate employees are entitled to leaving indemnities payable under the Babxaini I .abour Law, based on length of service and final remuneration. Provision for this, which is unfunded, and which represents a dcfmed benefit plan under lAS 19 - Employee Benefits, has been made by calculating the notional liability had all employees left at the reporting date. The provision is classified as a non-current liability in the consolidated statement of financial position.

Provision is made for end of service benefits due to employees of Financial Technologies Middle East DMCC in accordance with the relevant U.A.E labour legislation for rlleir period of service upto rlle end of the reporting period and disclosed in rlle accompanying consolidated financial statements as non-current liability.

Short-term employee benefits

The cost of short-tern employee benefits, (those payable 'Within 12 months after the service is rendered, such as paid vacation leave and sick leave, bonuses, and non-monetary benefits such as medical care), are recognised in the period in which the service is rendered and are not discounted.

Contributions to the National Pension Scheme and Medical Aid Scheme are expensed in the period in which they fall due.

3.22 Trade receivables

Trade receivables are amounts due from customers for services performed in the ordinary course of business and are classified as current assets if settlement is expected 'Within one year.

'l'rade receivables are recognised initially at fair value and subsequently measured at amortised cost using the effective interest method, less provision fo r impairment.

25

FT Group Investments Pvt. ltd

Notes to the consolidated financial statements For the year ended 31 March 2017

3. Summary of accounting policies (Contd)

3.23 Trade payables

Trade payablcs are obligations to pay for goods or services that have been acquired in the ordinary course of business from suppliers and are classifled as current liabilities if payment is due within one year.

Trade payables are recognised initially at fair value and subsequently measured at amortised cost using the effective interest method.

3.24 Comparatives

'W'here necessary, the comparatives have been adjusted to conform with changes in presentation in the current year.

3.25 Significant management judgement in applying accounting policies and estimation uncertainty

\'Vhen preparing the consolidated financial statements, management undertakes a number of judgements, estimates and assumptions about d1e recognition and measurement of assets, liabilities, income and expenses.

Significant management judgement

'l11e follow1ng are significant management judgements in applying the accounting policies of the Group that have the most significant effect on the consolidated financial statements is sel out below.

Determination offom:tional mmnry

The determination of the functional currency of the Group is critical since recording of transactions and exchange differences at:ising therefrom arc dependent on the functional currency selected. The directors have considered those factors and have determined that d1c functional currency of the Group is the USD.

Retvgnition ofdifemd tax aJJetJ

The extent to which the deferred tax assets can be recognised is based on an assessment of the probability of the Group's fun1rc taxable income against which d1e deferred tax assets c:m be utilised. Tn addition, significant judgement is required in assessing the impact of any legal or economic limits or uncertainties in various tax jurisdictions.

Contingent liabilities

.M".anagement applies its judgement to facts and advice it receives from its attomc.1rs, advocates and other advisors in assessing if an obligation is probable, more likely than not or remote. Tbis judgement application is used to determine if d1e obligation is recognised as a liability or disclosed as a contingent liability .

./J.vaihblefor-.rale investmmts

The Group follows the guidance of lAS 39 on determining when an investment is other than temporarily impaired. This determination requires significant judgement. In making this judgement, the Group evaluates, among other factors, the duration and extent to which the fair value of an investment is less ilian its cost and the financial health and near-term business outlook for the investee, including factors such as industry and sector performance, changes in technology and operational and financing cash flow.

26

FT Group Investments Pvt. Ltd

Notes to the consolidated financial statements For the year ended 31 March 2017

3. Summary of accounting policies (Contd)

3.25 Significant management judgement in applying accounting policies and estimation uncertainty (Contd)

Significant management judgement (Contd)

Goin.g fona;m a.rmmption

"l he directors have exercised judgement in assessing that the preparation of these consolidated financial statements on a going concern basis is appropriate. ln making this assessment, the directors have considered the Group's future business projects, future cash flows and future profitability and financial support from related parties.

Estimation uncertainties

Information about cstimares and assumptions that have the most significant effect on recogntllon and measurement of assets, liabilities, income and expenses is provided below. 1\ ctual results may be substantially different.

Businm wmbinations

On initial recognition, the assets and liabilities of the ac4uircd business and the consideration paid for them arc included in the consolidated financial statements at their fair values. ln measuring fair value, the directors usc estimates of future cash flows and discount rates.

Any subsequent change in these estimates would affect the amount of goodwill if the change qualifies as a measurement period adjustment. Any other change would be recognised in pro fit or loss in the subsequent period.

Urefitl lim of depmiable as.retJ·

:tvfanagement reviews the useful lives of depreciable assets at each reporting date. At the reporting date, management assesses that the useful lives represent the expected utility of the assets to the Group. The carrying amounts arc 21nalyscd in "!'\otcs 7 and 8. Actual results, hO\vcvcr, may \ar) due lo lechlli(;ai obsolescence, particularly rdati.ng to software and IT equipment.

·Fair value e.rtimr.ttion

The carrying values less impainncnt provision of rradc and other receivables are assumed to approximate their fair values. 'lbc fair value of fmancialliabilities for disclosure purposes is estimated by discounting the future contractual cash flows at the current market interest rate that is available for similar financial instruments.

Impairment testing

The recoverable amounts of cash-generating units and individual assets have been determined based on the higher of value-in-use calculations and fair values less costs to sell. These calculations require the use of escimates and assumprions. It is reasonably possible that the useful life assumption may change which may then impact the estimations and may then require a material adjustment to tJte carrying value of goodwill and tangible assets.

27

FT Group Investments Pvt. ltd

Notes to the consolidated financial statements For the year ended 31 March 2017

3. Summary of accounting policies (Contd)

3.25 Significant management judgement in applying accounting policies and estimation uncertainty (Contd)

Estimation uncertainties (Contd)

Impairment te.rtin._R, (Contd)

'lbe Group reviews and tests the carrying value of assets when events or changes in circumstances suggest that the carrying amount may not be recov<.:rable. Assets are grouped at the lowest kvcl for which identifiable cash flows are largely independent of cash flows of other assets and liabilities. Tf there are indications that impairment may have occurred, estimates are prepared of expected future cash flows for each group of assets. Expected future cash flows used to determine the value in use of assets are inhc.rcntly uncertain and could materially change over time. They are significantly affected by a number of factors including production estimates, supply and demand, together with economic factors such as exchange rates, inflation and interest.

.l7alr va/He measurement

Management uses valuation techniques to determine the fair value of financial instruments (where active market quotes arc not available) and non-financial assets. This involves developing estimates and assumptions consistent with how market participants would price the instrument. Management bases its assumptions on observable data as far as possible but tlus is not always available. In that case management uses the best information available. Estimated fair values may vary from the actual prices that would be achieved in an arm's length transaction at the reporting date.

u anJ" and refeivabfes

The Group assesses its loans and receivables for impairment at the end of each reporting period. In determining whether an impairment loss should be recorded in profit or loss, the Group makes judgements as to whether there is observable data indicating a measurable decrease in the estimated funue cash flows from a fmancial asset.

The impairment for loans and receivables is calculated on a portfolio basis, based on historical loss ratiog, adjusted for national and industry-specific economic conditions and other inJicators presem aL the reporting date that correlate with defaults on the portfolio.

Taxation

Judgement is required in determining the provision for income taxes due to the complexity of legislation. There are many transactions and calculation for which the ultimate tax determination is uncertain during the ordinary course of business. The Group recognises liabilities for anticipated issues based on estimate of whether additional taxes will be due. Where the fmal tax outcome of these matters is different from the amounts that were initially recorded, such differences will impact the income tax and deferred tax provisions in the period in which such determination is made.

28

FT Group Investments Pvt. Ltd

Notes to the consolidated financial statements For the year ended 31 March 2017

4. Financial instrument risk

Risk management objectives and policies

'lbc Company is exposed to various risks in relation to financial instruments. The Company's financial assets and liabilities by category are summarised below.

The Group The Company

2017 2016 2017 2016

USD USD USD USD Financial assets

loans and receivables:

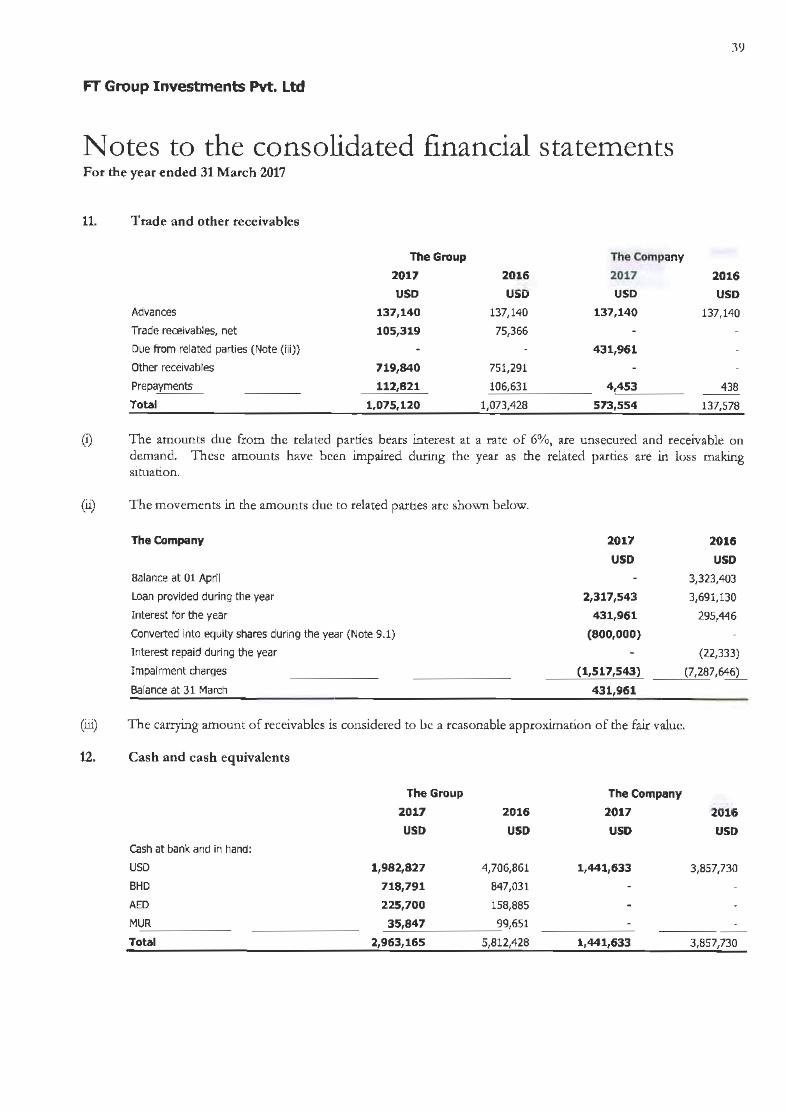

Trade and other receivables* 177,714 217,754

Due from related parties 431,961

Cash and cash equivalents 2,963,165 5,812,428 1,441,633 3,857,730

Total financial assets 3,140,879 6,030,182 1,873,594 3,857,730

The Group The Company

2017 2016 2017 2016

USD USD USD USD Financial liabilities

FinancialliabJYities measured at amortised cost: Non current

Borrowings 72,000,000 72,000,000

Current

Borrowings 72,000,000 72,000,000

Payables 13,885,619 10!782,751 13,183,093 9,982,238

13,885,619 82,782,751 13,183,093 81,982,238

Total financial liabilities 85,885,619 82,782,751 85,183,093 81,982,238

"Trade and other receivable: t'Omidered aJjinantial assetJ cxduduprepayments and advanceJ.

The Group's activities expose it to a variety of financial risks: market risk (including currency risk and interest rate risk), credit risk, concentration risk and liquidity risk. The Group's risk management policies are designed to identify and analyse these risks, to set up appropriate risk limits and controls, and to monitor the risks and adherence to limits by means of reliable and up-to-date information systems.

fusks arc managed by different levds o f management and committees. The latters arc responsible for overseeing the establishment and implementation of effective risk management systems and the monitoring of internal compliance and controls.

The most significant financial risks to which the Group is exposed arc described below.

29

FT Group Investments Pvt. ltd

Notes to the consolidated financial statements For the year ended 31 March 2017

4. Financial instrument risk (Contd)

Risk management objectives and policies (Contd)

Financial assets and financial liabilities (Contd)

4.1 Market risk analysis

Foreign currency sensitivity

The Group is not exposed to major foreign exchange risk as most of its assets and liabilities are denominated in the United States Dollar (USD), United Arab Emirates Dirhams (AED) and Bahrain Dinars (BHD). 'lbe percentage change on the BHD/USD and AED/USD exchange rate for the year ended 31 March 2017 was less than 1 1Yo and this would have impacted marginally on the Group's result. This percentage has been detennined based on the average market volatility in exchange rates in the previous 12 months.

The currency profile of the Group's financial assets and liabilities is as follows:-

31 March 2017

United States Dollar (USD)

Botswana Pula (BWP)

Mauritian Rupee (MUR)

Arab Emirates Dirham (AED)

Bahraini Dinars (BHD)

31 March 2016

United States Dollar (USD)

Botswana Pula (BWP)

Mauritian Rupee (MUR)

Arab Emirates Dirham (AED)

Bahraini Dinars (BHD)

Interest rate sensitivity

The Group

Financial Financial

assets liabilities

USD uso 2,014,587 85,502,874

2,451

35,847 125,314

347,963 35,281

740,031 222,150

3,140,879 85,885,619

The Group

Financial Financial

assets liabilities

USD USD 4,738,545 82,272,905

33,555

157,064 115,725

234,252 113,401

866,766 280,720

6,030,182 82,782.751

The Company

Financial

assets

USD 1,605,331

129,271

138,992

1,873,594

Financial

liabilities

USD 85,183,093

85,183,093

The Company

Financial

assets

USD 3,857,730

3,857,730

Financjal

liabilities

USD 81,982,238

81,982,238

lbc Group has an interest bearing financial liabilities in the form of a loan from a related party. The loan from the related party is indexed to the LIBOR + 3.5% per annum.

The Group has interest bearing financial assets in the form of cash and cash equivalents. The impact of changes in interest rate on the interest income derived from these cash and cash equivalents is not significant.

30

FT Group Investments Pvt. ltd

Notes to the consolidated financial statements For the year ended 31 March 2017

4. Financial instrument risk (Contd)

Risk management objectives and policies (Contd)

4.1 Market risk analysis (Contd)

Interest rate sensitivity (Contd)

The sensitivity analysis below has been determined based on the exposure to interest rates at the reporting date. The analysis is prepared assuming that the amount of liability outstanding at the reporting date was as such outstanding for the whole year.

If interest rate had been 25 basis points higher, the effect on loss would have been as follows:

Loss

The Group

2017 USD

(180,000)

2016

USD (180,000)

The Company

2017 USD

(180,000)

2016

USD (180,000)

If interest rate had been 25 basis points lower, the effect on loss would have been the opposite.

4.2 Credit risk analysis

Credit risk refers to the risk that counterparty will default on its contractual obligations resulting in financial loss to the Group. The Group has policies in place to deal with creditworthy counterparties as a means of mitigating the risk of financial loss &om defaults. The Group uses publicly available financial information and its own trading records to rate its major customers.

The Group's maximum exposure to credit risk is limited to the carrying amount of financial assets recognised at the reporting date, as summarised below:

The Group

2017

USD Current assets

Trade and other receivables 177,714

Due from related parties

cash and cash equivalents 2,963,165

Total 3,140,879

2016

USD

217,754

5,812,428

6,030,182

The Company

2017 2016

USO USD

431,961

1,441,633

1,873,594

3,857,730

3,857,730

The Company has given loans to group companies. The directors have assessed the recoverable amount of these loans and concluded that these loans were impaired by USD 1,517,543 at the reporting date.

Trade receivables consist of a limited number of customers. The qualiLy of individual credit or credit class is monitored on an ongoing basis and impairment losses are recognised as appropriate. Ongoing credit evaluation of the financial position of customers is performed and provision for doubtful debts is made where appropriate.

31

FT Group Investments Pvt. Ltd

Notes to the consolidated financial statements For the year ended 31 March 2017

4. Financial instrument risk (Contd)

Risk management objectives and policies (Contd)

4.2 Credit risk analysis (Contd)

The credit risk for the bank balances is considered negligible, since the counterparties are reputable banks with high quality external credit ratings.

None of the above fmancial assets are secured by collaterals or other credit enhancements.

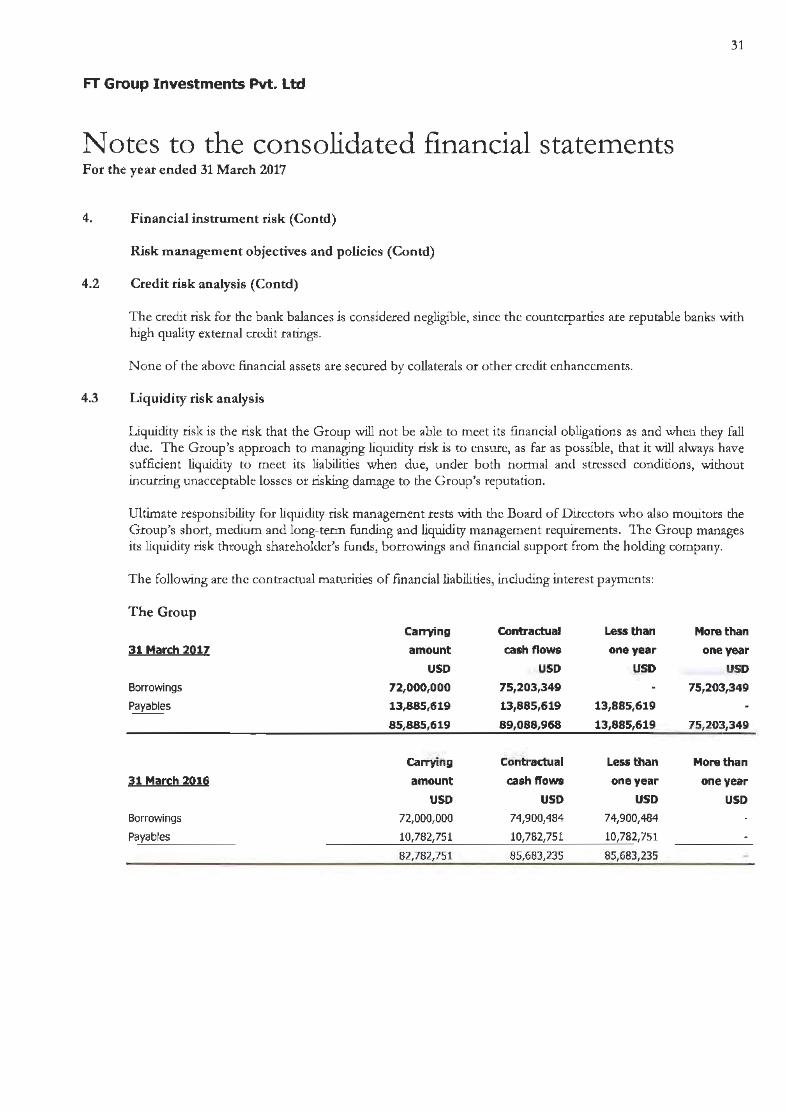

4.3 Liquidity risk analysis

Liquidity risk is the risk that the Group will not be able to meet its financial obligations as and when they fall due. The Group's approach to managing liquidity risk is to t:nsurc, as far as possible, that it will always have sufficient liquidity to meet its liabili ties when due, under both normal and stressed conditions, without incurring unacceptable losses or risking damage to the Group's reputation.

Ultimate responsibility for liquidity risk management rests with the Board of Directors who also monitors the Group's short, medium and long-tenn funding and liquidity management requirements. 1be Group manages its liquidity risk through shareholder's funds, borrowings and fmancial support from the holding company.

The following arc the contractual maturities of financial liabilities, including interest payments:

The Group

31 March 2017

Borrowings

Payables

31 March 2016

Borrowings

Payables

Carrying

amount

USD 72,000,000

13,885,619

85,885,619

canying

amount

USD 72,000,000

10,782,751

82,782,751

Contractual Less than

cash flows one year

USD USD 75,203,349

13,885,619 13,885,619

89,088,968 13,885,619

Contractual Less than

cath nows one year

USD USD 74,900,484 74,900,484

10,782,751 10,782,751

85,683,235 85,683,235

More than

one year

USD 75,203,349

75,203,349

More than

onevear

USD

32

FT Group Investments Pvt. Ltd

Notes to the consolidated financial statements For the year ended 31 March 2017

4. Financial instrument risk (Contd)

Risk management objectives and policies (Contd)

4.3 Liquidity risk analysis (Contd)

The Company Carrying Contractual Less than More than

31 March 2017 amount cash flows one year one year

USD uso uso USD Borrowings 72,000,000 75,203,349 75,203,349

Payables 13,183,093 13,183,093 13,183,093

85,183,093 88,386,442 13,183,093 75,203,349

Carrying Contractual Less than More than

31 March 2016 amount cash flows one year one year

USD USD USD USD Borrowings 72,000,000 74,900,484 74,900,484

Payables 9,982,238 9,982,238 9,982,238

81,982,238 84,882,722 84,882,722

5. Capital management policies and procedures

'I he Group's capital management objective~ are:

• to ensure its ability to continue as a going concern; and

• to provide an adequate return to the shareholder and other stakeholders

by pricing services commensurately with the level of risk.

The Group monitors capital on the basis of the carrying amount of equity less cash and cash equivalents as presented on the face of the consolidated statement of financial position.

The Group sets the amount of capital in proportion to its overall financing structure, that is, equity and fmancial liabilities. T he Group manages the capital structure and makes adjustments to it in the light of changes in economic conditions and the risk characteris tics of the underlying assets. In order to maintain or adjust the capital structure, the Group may adjust the amount of dividends paid, reduce capital, issue new shares, or sell assets to reduce debts.

FT Group Investments Pvt. ltd

Notes to the consolidated financial statements For the year ended 31 March 2017

5. Capital management policies and procedures (Contd)

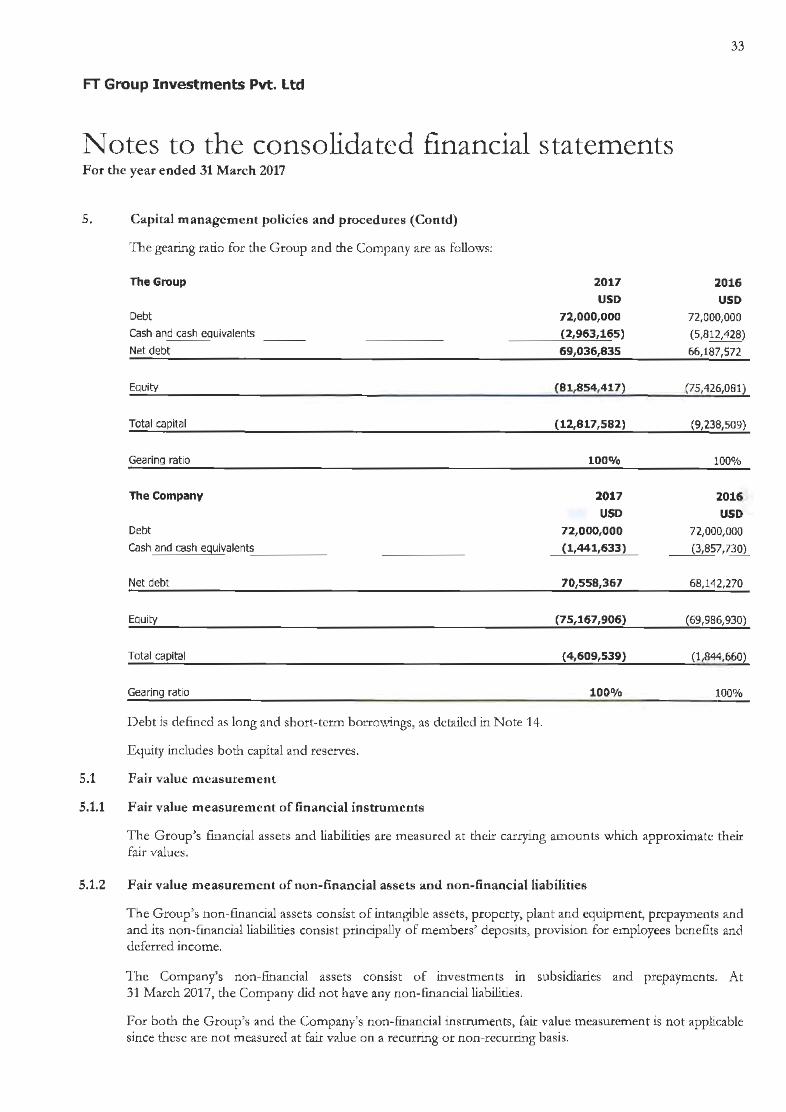

The gearing ratio for the Group and the Company are as follows:

The Group

Debt

Cash and cash eguivalents

Net debt

Equity

Total capital

Gearing ratio

The Company

Debt

Cash and cash equivalents

Net debt

Equity

Total capital

Gearing ratio

Debt is defmcd as long and short-term borrowings, as detailed in Note 14.

Equity includes both capital and reserves.

5.1 Fair value measurement

5.1.1 Fair value measurement of financial instruments

2017

USD 72,000,000

(2,963,165)

69,036,835

(81,854,417)

(12,817,582)

100%

2017

USD 72,000,000

(1,441,633)

70,558,367

(75,167,906}

(4,609,539)

100%

33

2016

USD 72,000,000

(5,812,428)

66,187,572

(75,426,081)

(9,238,509)

100%

2016

USD 72,000,000

(3,857,730)

68,142,270

(69,986,930}

(1,844,660)

100%

The Group's financial assets and liabilities are measured at their carrying amounts which approximate their fair values.

5.1.2 Fair value measurement of non-financial a.ssets and non-financial liabilities

The Group's non-fmandal assets consist of intangible assets, property, plant and equipment, prepayments and and its non-fmancialliabilities consist principally of members' deposits, provision for employees benefits and deferred income.

The Company's non-fmancial assets consist of investments in subsidiaries and prepayments. At 31 March 2017, the Company did not have any non- fmancialliabilities.

For both the Group's and the Company's non-financial instruments, fair value measurement is not applicable since these are not measured at fair value on a recurring or non-recurring basis.

FT Group Investments Pvt. Ltd

Notes to the consolidated financial statements For the year ended 31 Match 2017

6. Goodwill

At 01 April

Impainnent loss

At 31 March

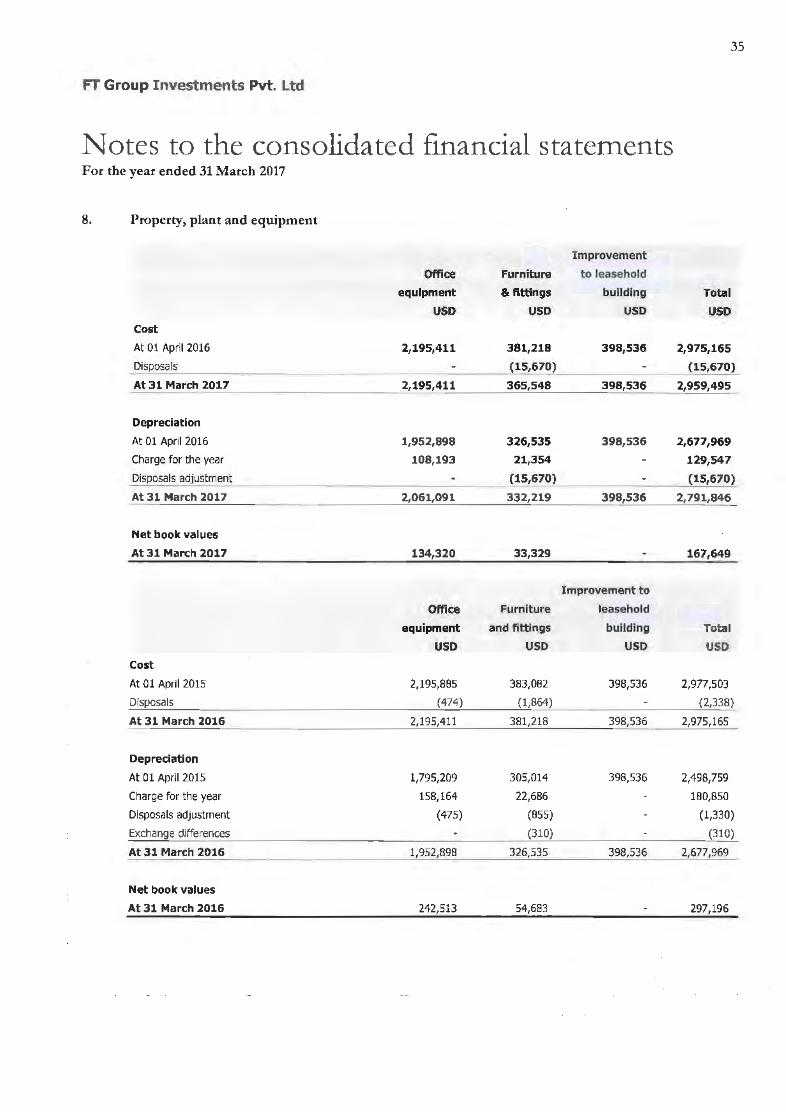

7. Intangible assets

Cost