ft 001 presentation%20findings final

DESCRIPTION

http://www.unityfour.eu/images/erevna/FT-001_presentation%20findings_final.pdfTRANSCRIPT

1

Economic Climate and Expectations in Greece

Research Results:

For 2016

2

Enterprise size

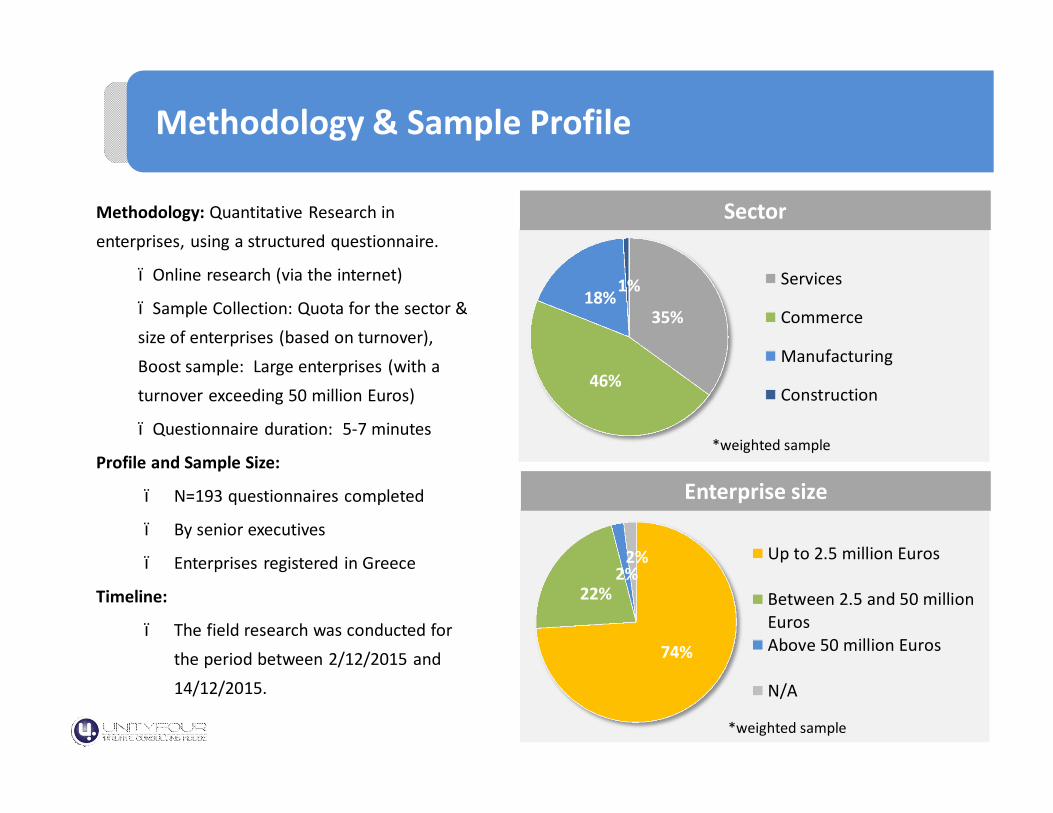

Methodology & Sample Profile

Methodology: Quantitative Research in enterprises, using a structured questionnaire.

– Online research (via the internet)

– Sample Collection: Quota for the sector & size of enterprises (based on turnover), Boost sample: Large enterprises (with a turnover exceeding 50 million Euros)

– Questionnaire duration: 5-7 minutes

Profile and Sample Size:

– Ν=193 questionnaires completed

– By senior executives

– Enterprises registered in Greece

Timeline:

– The field research was conducted for the period between 2/12/2015 and 14/12/2015.

35%

46%

18%1% Services

Commerce

Manufacturing

Construction

Sector

74%

22%2%

2% Up to 2.5 million Euros

Between 2.5 and 50 millionEurosAbove 50 million Euros

N/A

Sector

*weighted sample

*weighted sample

3

Definitions

• The classification of enterprises in terms of size was based on the turnover declared. Where:

Small Up to 2.5 million Euros

Medium Between 2.5 million and 50 million Euros

Large Exceeding 50 million Euros

• The term “business executives” refers to the following: General managers, owners, financial directors, commercial directors, etc. Specifically, the rate is noted in the following table:

Ν=193 %

Owners 72 37%

Managing Director

26 13%

Head of Accounting

24 12%

Finance Manager

22 11%

Ν=193 %General

Manager17 9%

HR Manager 5 3%

Sales Director 5 3%

Other 16 8%

4

Key findings

5

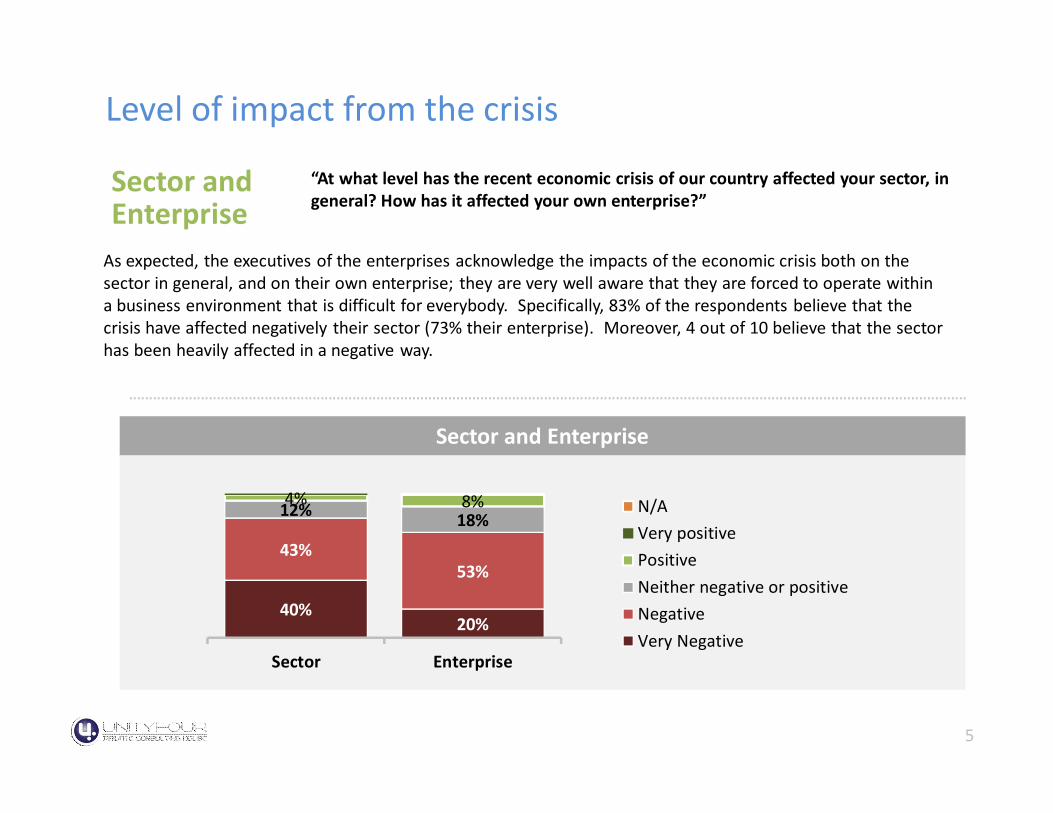

TurnoverLevel of impact from the crisis

Sector and Enterprise

“At what level has the recent economic crisis of our country affected your sector, in general? How has it affected your own enterprise?”

As expected, the executives of the enterprises acknowledge the impacts of the economic crisis both on the sector in general, and on their own enterprise; they are very well aware that they are forced to operate within a business environment that is difficult for everybody. Specifically, 83% of the respondents believe that the crisis have affected negatively their sector (73% their enterprise). Moreover, 4 out of 10 believe that the sector has been heavily affected in a negative way.

Sector and Enterprise

40%20%

43%53%

12% 18%4% 8%

Sector Enterprise

N/AVery positivePositiveNeither negative or positiveNegativeVery Negative

6

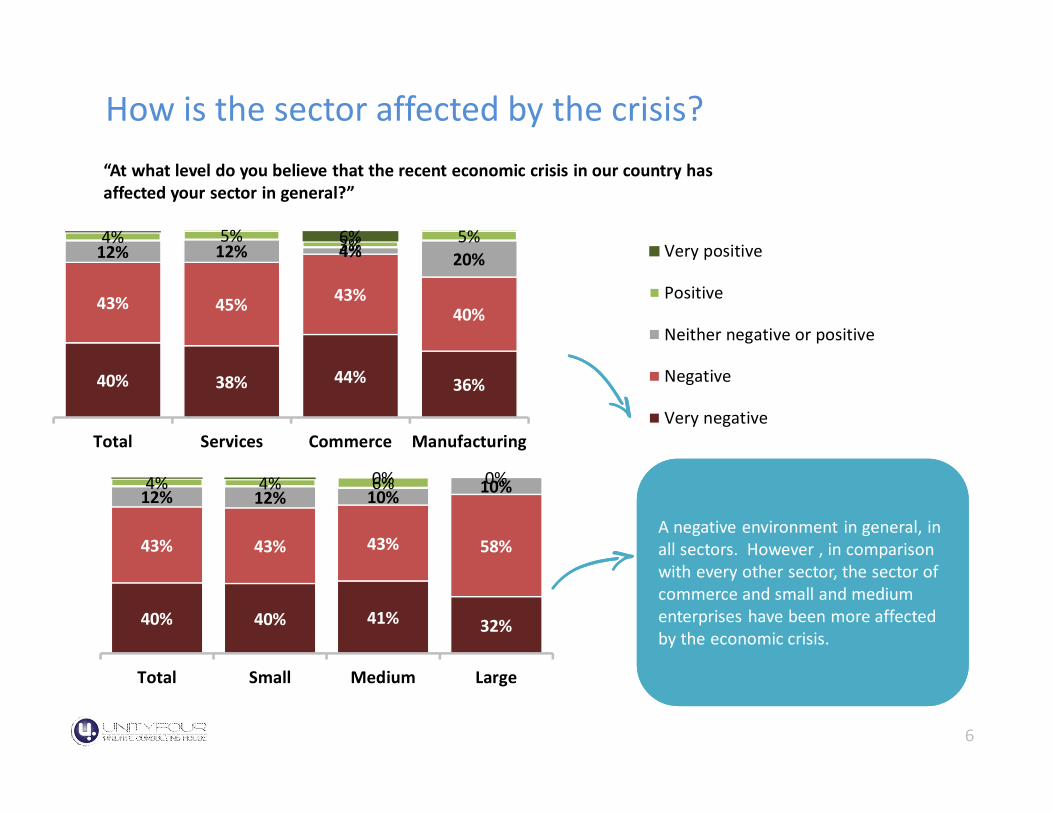

TurnoverHow is the sector affected by the crisis?“At what level do you believe that the recent economic crisis in our country has affected your sector in general?”

40% 38% 44% 36%

43% 45% 43%40%

12% 12% 4% 20%4% 5% 3% 5%6%

Total Services Commerce Manufacturing

Very positive

Positive

Neither negative or positive

Negative

Very negative

40% 40% 41% 32%

43% 43% 43% 58%

12% 12% 10% 10%4% 4% 6% 0%0%

Total Small Medium Large

A negative environment in general, in all sectors. However , in comparison with every other sector, the sector of commerce and small and medium enterprises have been more affected by the economic crisis.

7

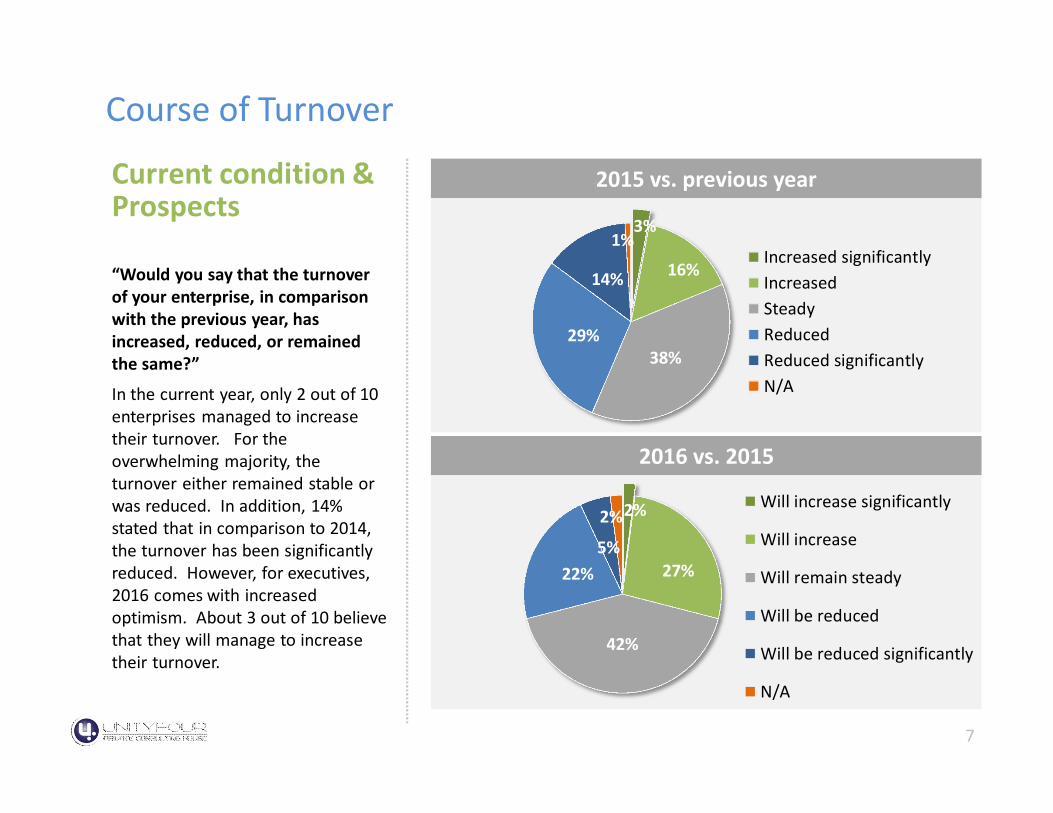

TurnoverCourse of Turnover

Current condition & Prospects

“Would you say that the turnover of your enterprise, in comparison with the previous year, has increased, reduced, or remained the same?”

In the current year, only 2 out of 10 enterprises managed to increase their turnover. For the overwhelming majority, the turnover either remained stable or was reduced. In addition, 14% stated that in comparison to 2014, the turnover has been significantly reduced. However, for executives, 2016 comes with increased optimism. About 3 out of 10 believe that they will manage to increase their turnover.

2015 vs. previous year

2016 vs. 2015

2%

27%

42%

22%5%

2%Will increase significantly

Will increase

Will remain steady

Will be reduced

Will be reduced significantly

N/A

3%

16%

38%29%

14%

1%Increased significantlyIncreasedSteadyReducedReduced significantlyN/A

8

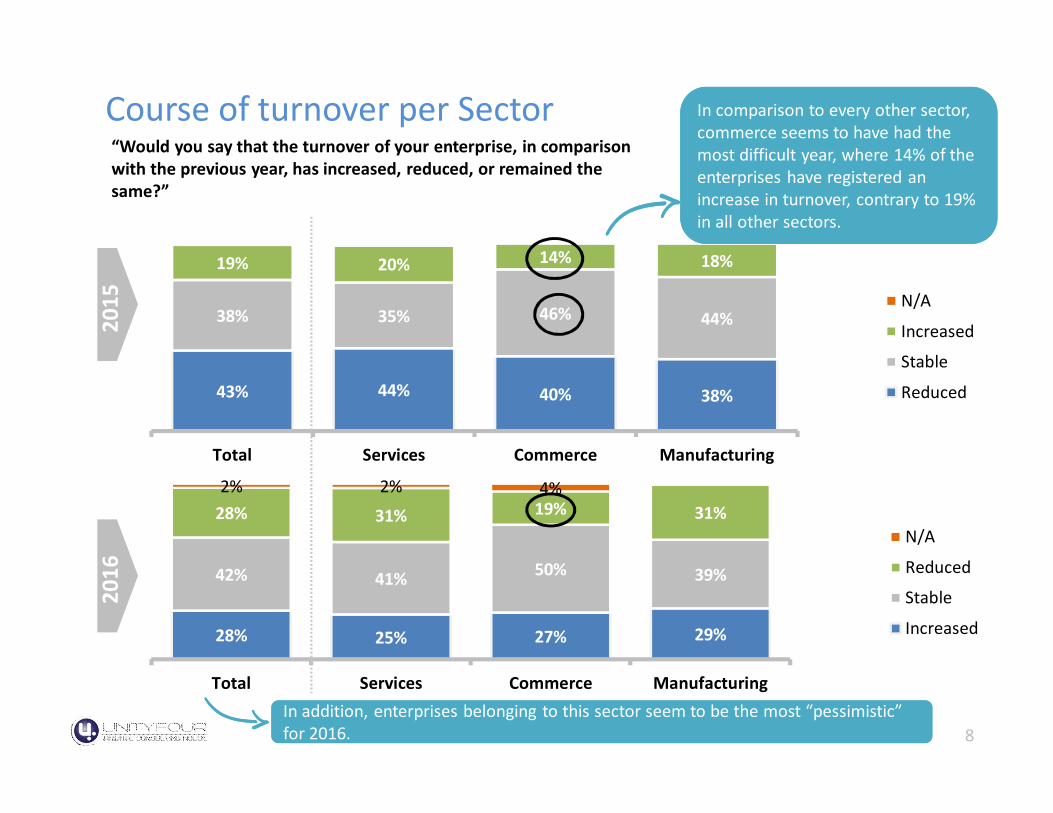

TurnoverCourse of turnover per Sector“Would you say that the turnover of your enterprise, in comparison with the previous year, has increased, reduced, or remained the same?”

43% 44% 40% 38%

38% 35% 46% 44%

19% 20% 14% 18%

Total Services Commerce Manufacturing

N/A

Increased

Stable

Reduced

28% 25% 27% 29%

42% 41% 50% 39%

28% 31% 19% 31%2% 2% 4%

Total Services Commerce Manufacturing

N/A

Reduced

Stable

Increased

2015

2016

In comparison to every other sector, commerce seems to have had the most difficult year, where 14% of the enterprises have registered an increase in turnover, contrary to 19% in all other sectors.

In addition, enterprises belonging to this sector seem to be the most “pessimistic” for 2016.

9

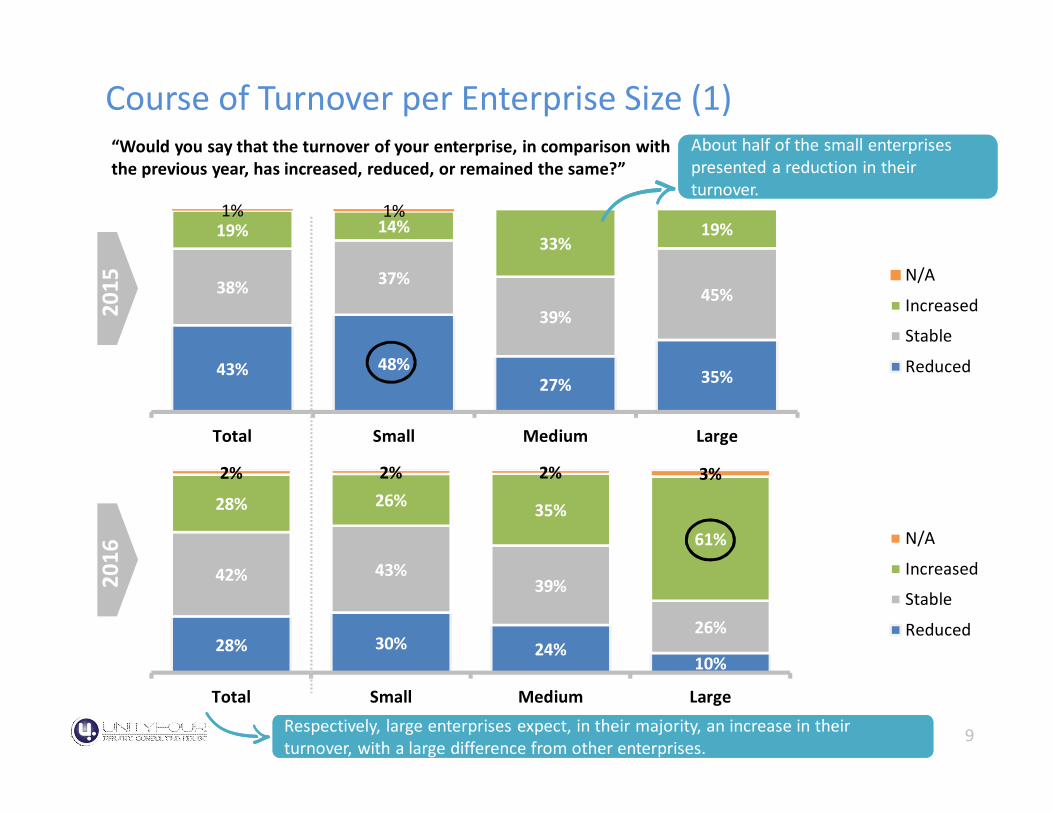

TurnoverCourse of Turnover per Enterprise Size (1)“Would you say that the turnover of your enterprise, in comparison with the previous year, has increased, reduced, or remained the same?”

43% 48%27% 35%

38% 37%

39%45%

19% 14%33%

19%1% 1%

Total Small Medium Large

N/A

Increased

Stable

Reduced

28% 30% 24%10%

42% 43%39%

26%

28% 26% 35%61%

2% 2% 2% 3%

Total Small Medium Large

N/A

Increased

Stable

Reduced

2015

2016

Respectively, large enterprises expect, in their majority, an increase in their turnover, with a large difference from other enterprises.

About half of the small enterprises presented a reduction in their turnover.

10

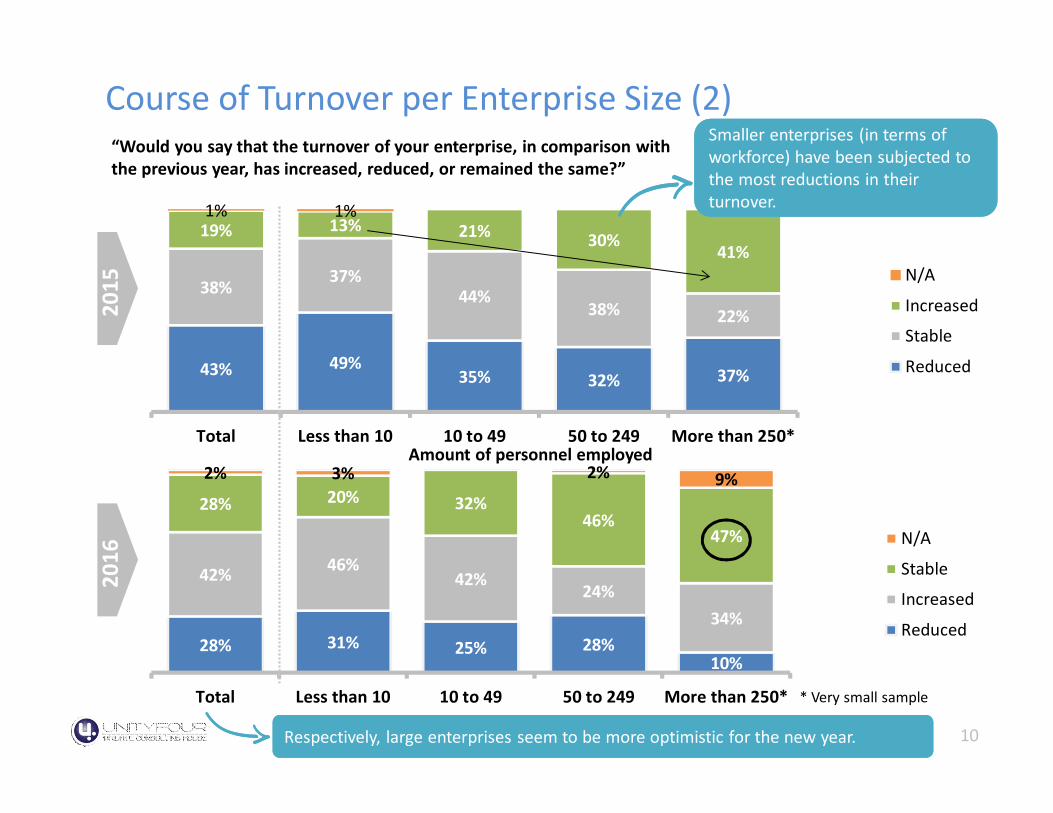

TurnoverCourse of Turnover per Enterprise Size (2)“Would you say that the turnover of your enterprise, in comparison with the previous year, has increased, reduced, or remained the same?”

43% 49%35% 32% 37%

38% 37%44%

38% 22%

19% 13% 21% 30% 41%

1% 1%

Total Less than 10 10 to 49 50 to 249 More than 250*

N/A

Increased

Stable

Reduced

28% 31% 25% 28%10%

42% 46%42%

24%34%

28% 20% 32%46%

47%

2% 3% 2% 9%

Total Less than 10 10 to 49 50 to 249 More than 250*

N/A

Stable

Increased

Reduced

2015

2016

Respectively, large enterprises seem to be more optimistic for the new year.

Smaller enterprises (in terms of workforce) have been subjected to the most reductions in their turnover.

Amount of personnel employed

* Very small sample

11

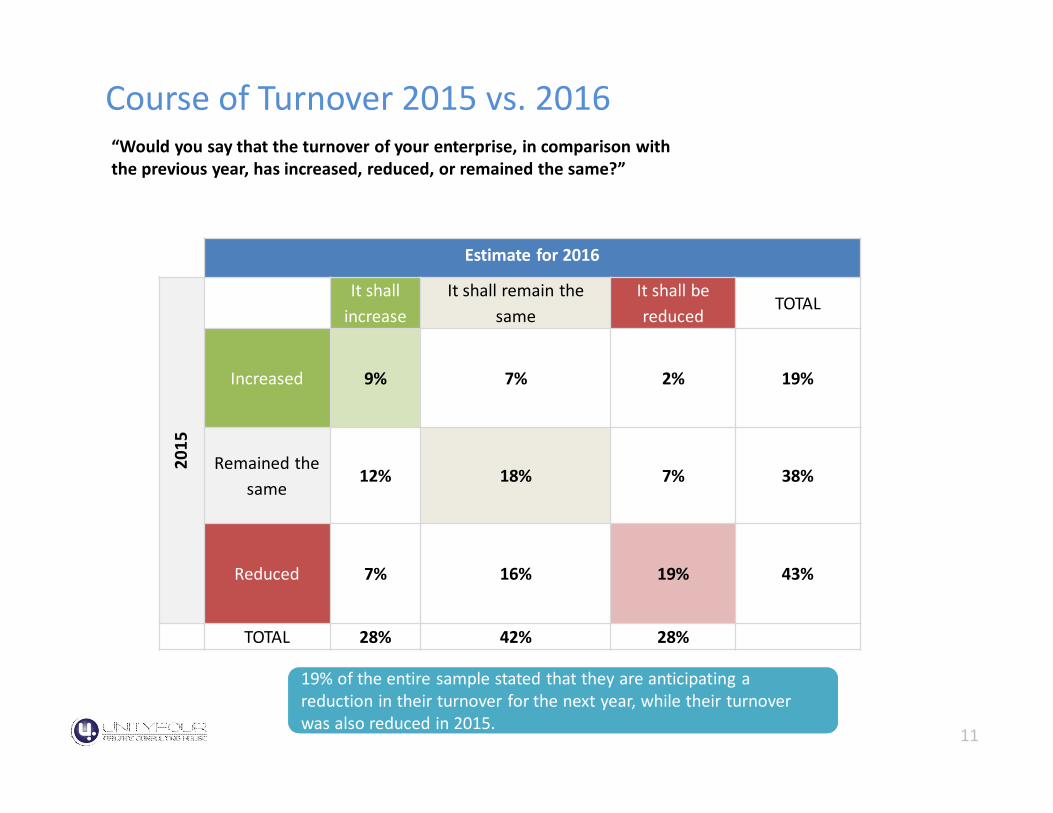

TurnoverCourse of Turnover 2015 vs. 2016“Would you say that the turnover of your enterprise, in comparison with the previous year, has increased, reduced, or remained the same?”

Estimate for 2016

2015

It shall increase

It shall remain the same

It shall be reduced

TOTAL

Increased 9% 7% 2% 19%

Remained the same

12% 18% 7% 38%

Reduced 7% 16% 19% 43%

TOTAL 28% 42% 28%

19% of the entire sample stated that they are anticipating a reduction in their turnover for the next year, while their turnover was also reduced in 2015.

12

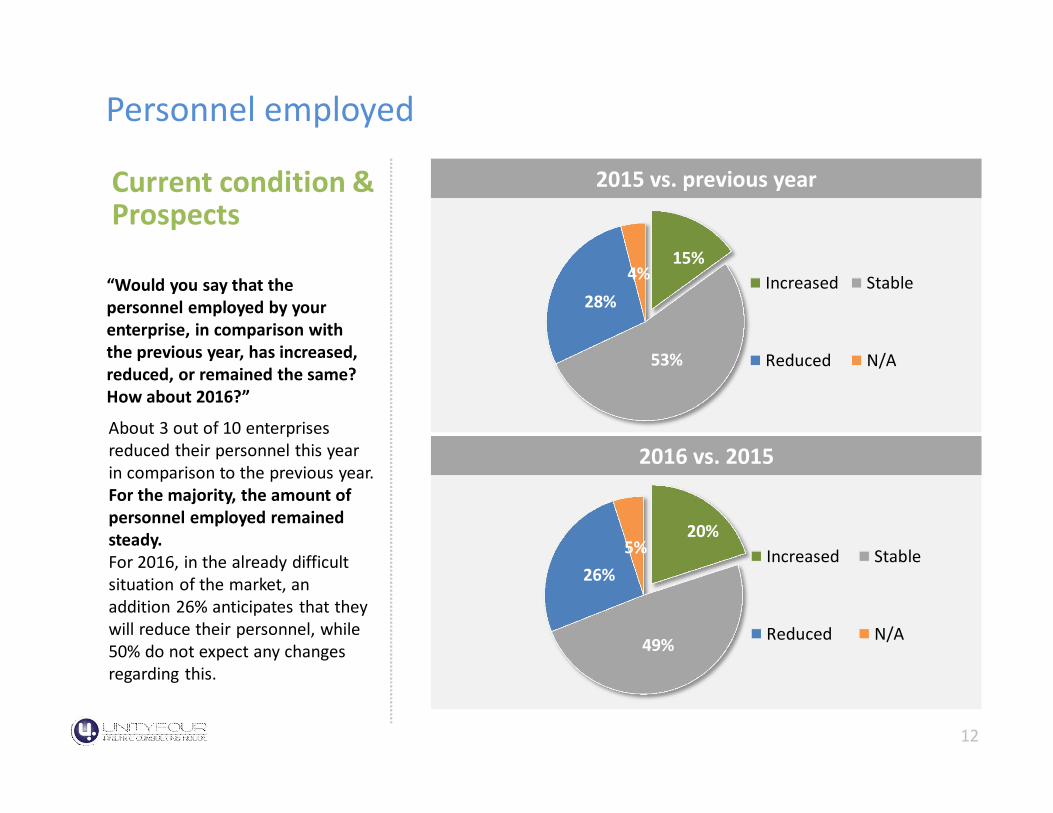

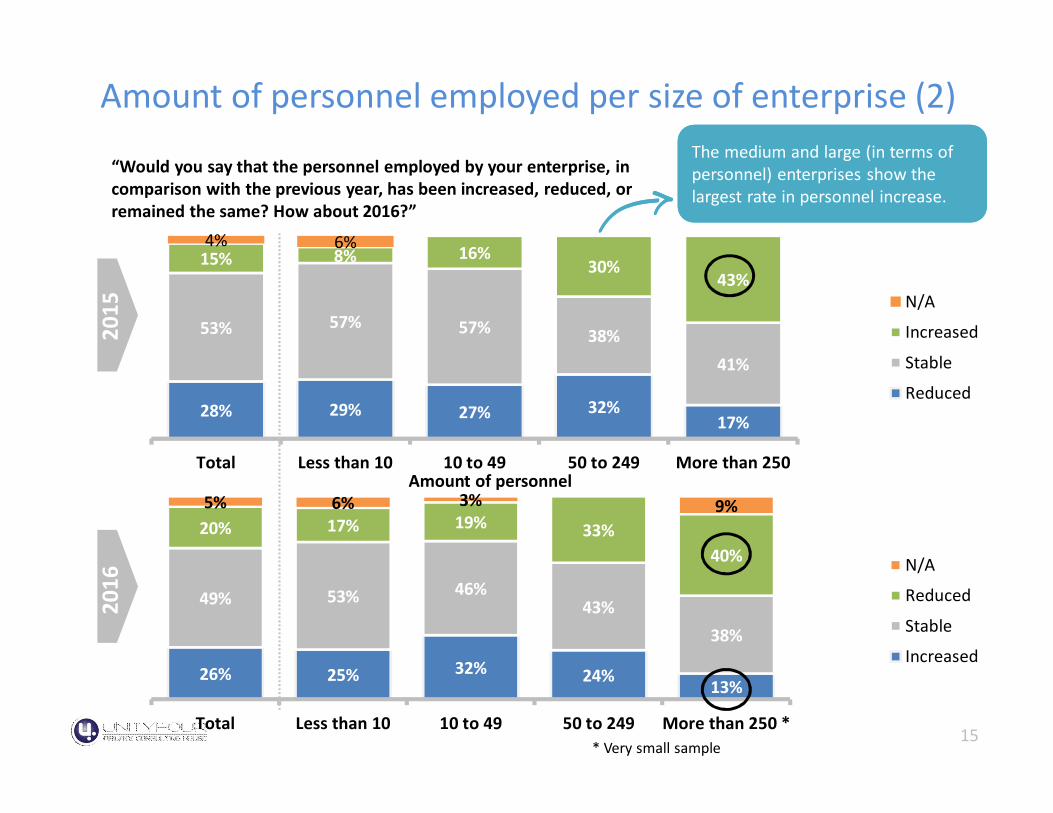

TurnoverPersonnel employed

Current condition & Prospects

“Would you say that the personnel employed by your enterprise, in comparison with the previous year, has increased, reduced, or remained the same? How about 2016?”

About 3 out of 10 enterprises reduced their personnel this year in comparison to the previous year. For the majority, the amount of personnel employed remained steady. For 2016, in the already difficult situation of the market, an addition 26% anticipates that they will reduce their personnel, while 50% do not expect any changes regarding this.

2015 vs. previous year

2016 vs. 2015

20%

49%

26%5% Increased Stable

Reduced N/A

15%

53%

28%4% Increased Stable

Reduced N/A

13

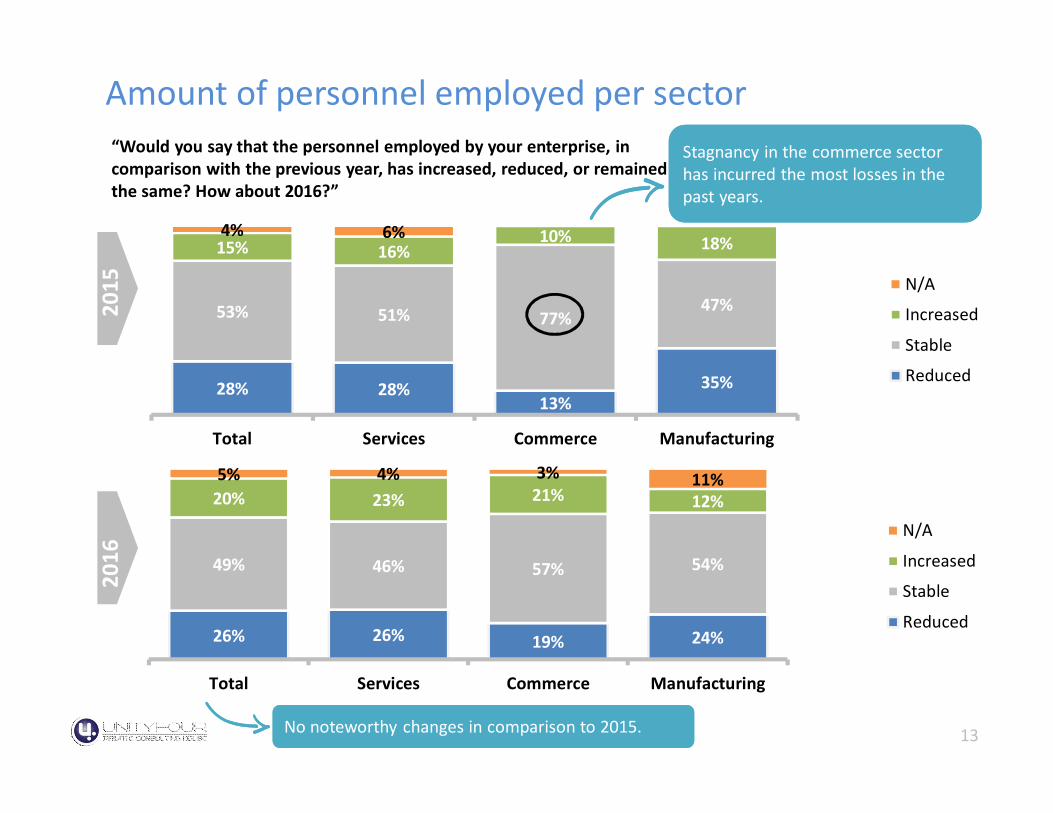

TurnoverAmount of personnel employed per sector“Would you say that the personnel employed by your enterprise, in comparison with the previous year, has increased, reduced, or remained the same? How about 2016?”

28% 28%13%

35%

53% 51% 77%47%

15% 16%10% 18%

4% 6%

Total Services Commerce Manufacturing

N/A

Increased

Stable

Reduced

26% 26% 19% 24%

49% 46% 57% 54%

20% 23% 21% 12%5% 4% 3% 11%

Total Services Commerce Manufacturing

N/A

Increased

Stable

Reduced

2015

2016

Stagnancy in the commerce sector has incurred the most losses in the past years.

No noteworthy changes in comparison to 2015.

14

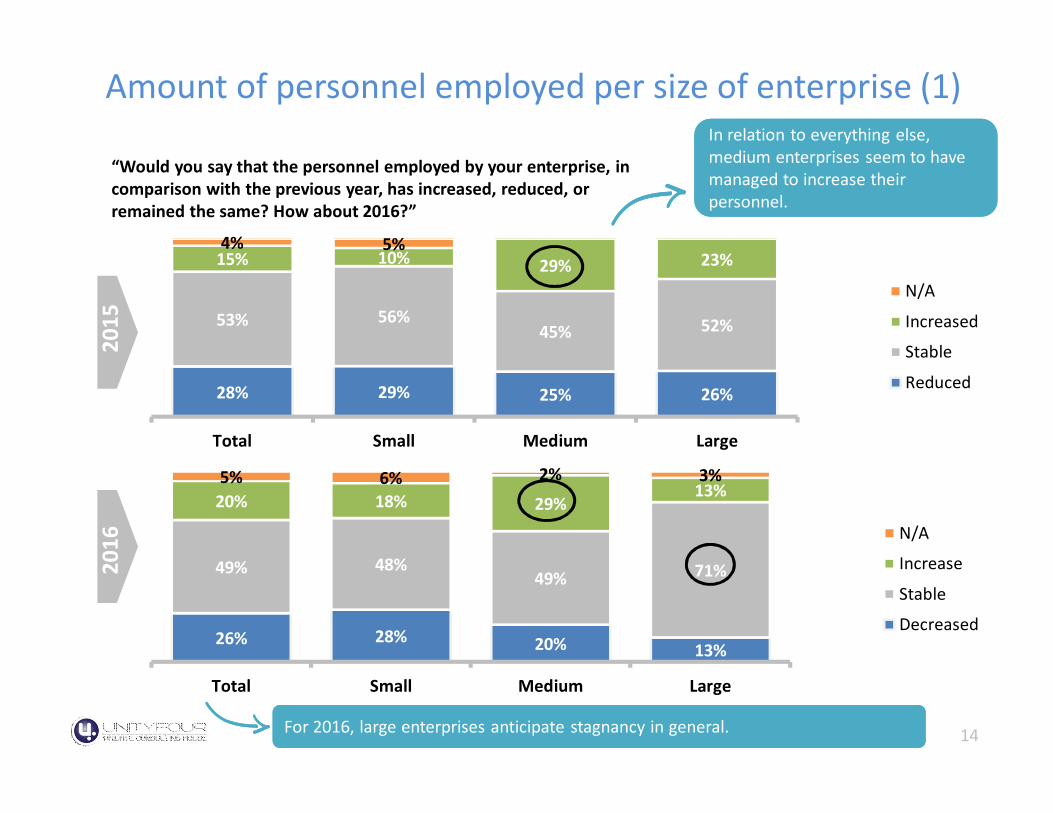

TurnoverAmount of personnel employed per size of enterprise (1)

28% 29% 25% 26%

53% 56%45% 52%

15% 10% 29% 23%4% 5%

Total Small Medium Large

N/A

Increased

Stable

Reduced

26% 28% 20% 13%

49% 48%49% 71%

20% 18% 29%13%

5% 6% 2% 3%

Total Small Medium Large

N/A

Increase

Stable

Decreased

2015

2016

“Would you say that the personnel employed by your enterprise, in comparison with the previous year, has increased, reduced, or remained the same? How about 2016?”

In relation to everything else, medium enterprises seem to have managed to increase their personnel.

For 2016, large enterprises anticipate stagnancy in general.

15

TurnoverAmount of personnel employed per size of enterprise (2)

2015

2016

“Would you say that the personnel employed by your enterprise, in comparison with the previous year, has been increased, reduced, or remained the same? How about 2016?”

28% 29% 27% 32%17%

53% 57% 57% 38%41%

15% 8% 16%30%

43%

4% 6%

Total Less than 10 10 to 49 50 to 249 More than 250

N/A

Increased

Stable

Reduced

26% 25% 32% 24% 13%

49% 53% 46%43%

38%

20% 17% 19% 33%40%

5% 6% 3% 9%

Total Less than 10 10 to 49 50 to 249 More than 250 *

N/A

Reduced

Stable

Increased

2015

2016

Amount of personnel

The medium and large (in terms of personnel) enterprises show the largest rate in personnel increase.

* Very small sample

16

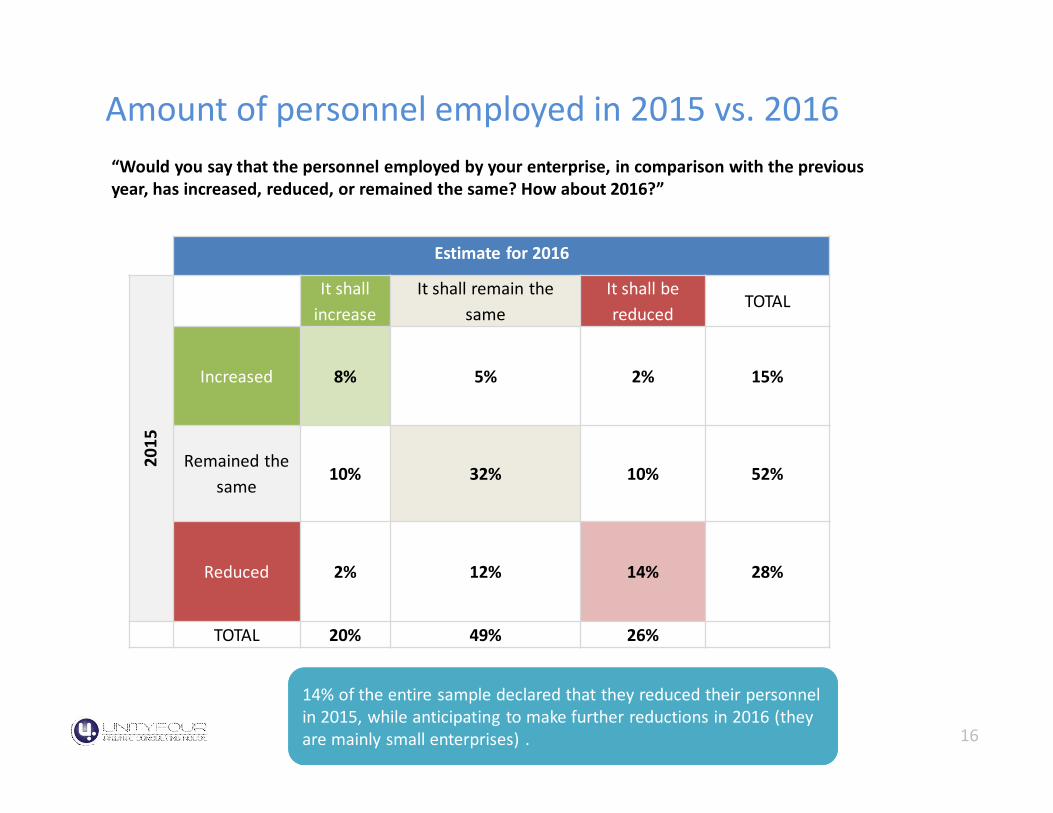

TurnoverAmount of personnel employed in 2015 vs. 201620

15

“Would you say that the personnel employed by your enterprise, in comparison with the previous year, has increased, reduced, or remained the same? How about 2016?”

Estimate for 2016

2015

It shall increase

It shall remain the same

It shall be reduced

TOTAL

Increased 8% 5% 2% 15%

Remained the same

10% 32% 10% 52%

Reduced 2% 12% 14% 28%

TOTAL 20% 49% 26%

14% of the entire sample declared that they reduced their personnel in 2015, while anticipating to make further reductions in 2016 (they are mainly small enterprises) .

17

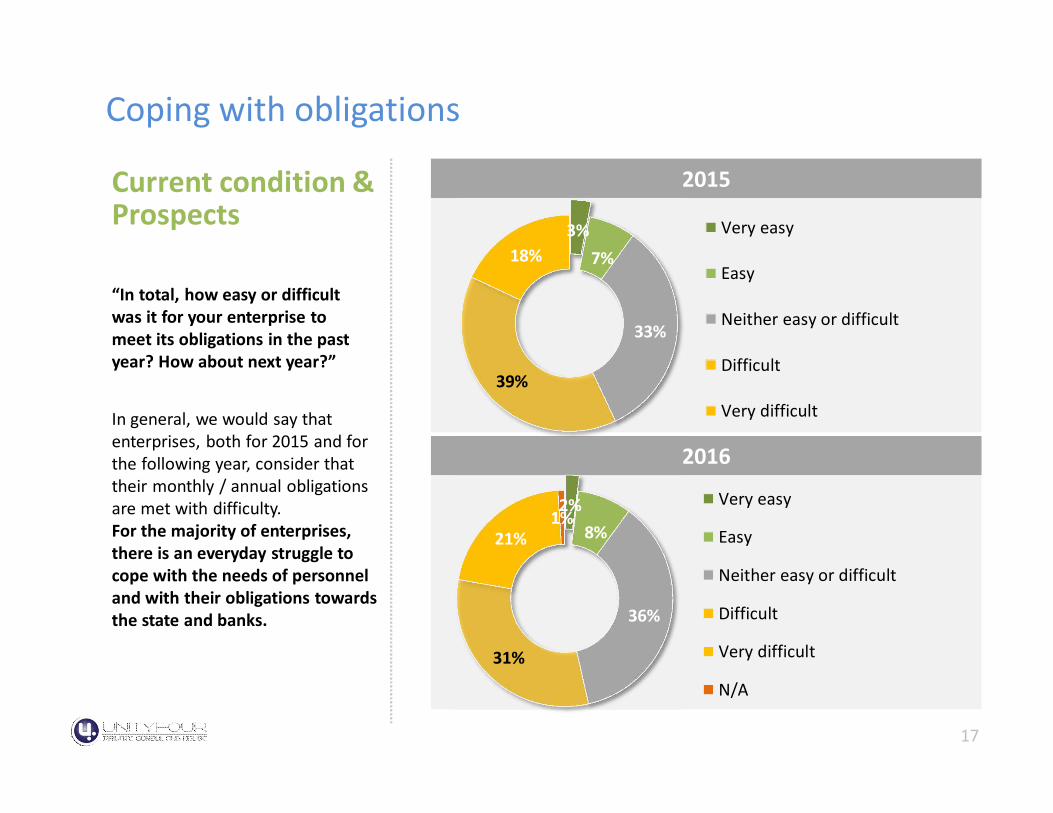

TurnoverCoping with obligations

Current condition & Prospects

“In total, how easy or difficult was it for your enterprise to meet its obligations in the past year? How about next year?”

In general, we would say that enterprises, both for 2015 and for the following year, consider that their monthly / annual obligations are met with difficulty. For the majority of enterprises, there is an everyday struggle to cope with the needs of personnel and with their obligations towards the state and banks.

2015

2016

3%7%

33%

39%

18%Very easy

Easy

Neither easy or difficult

Difficult

Very difficult

2%8%

36%

31%

21%1%

Very easy

Easy

Neither easy or difficult

Difficult

Very difficult

N/A

18

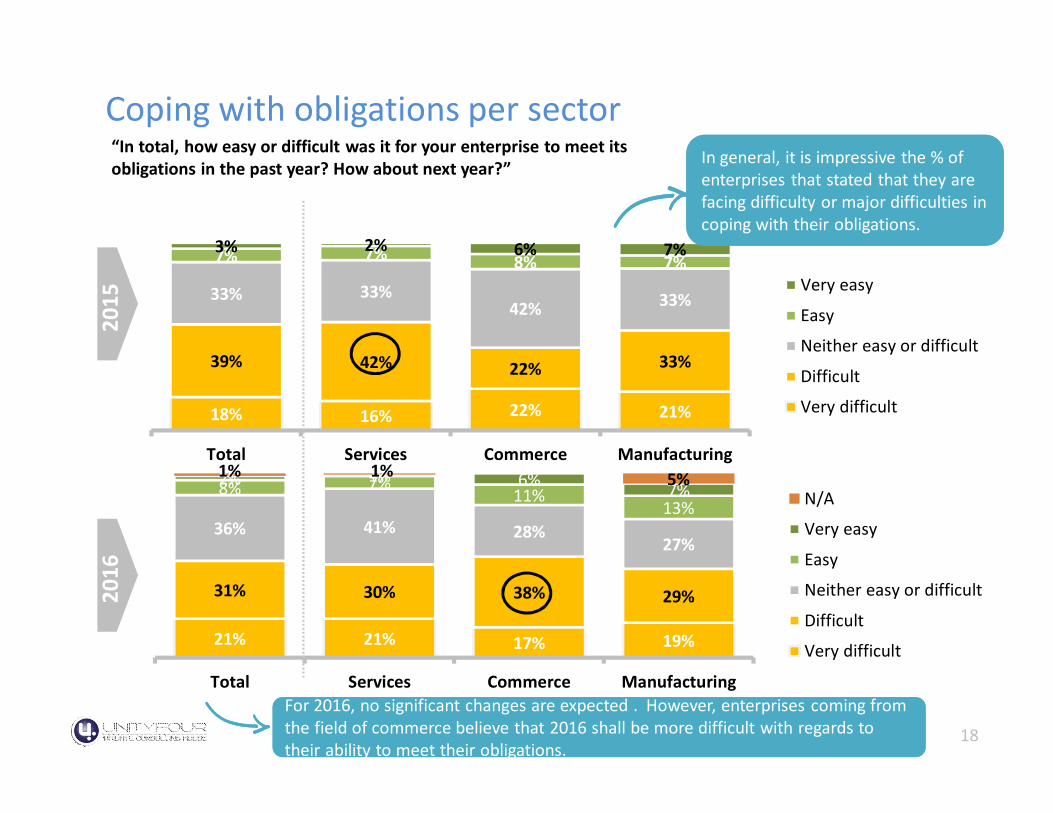

TurnoverCoping with obligations per sector“In total, how easy or difficult was it for your enterprise to meet its obligations in the past year? How about next year?”

18% 16% 22% 21%

39% 42% 22% 33%

33% 33%42% 33%

7% 7% 8% 7%3% 2% 6% 7%

Total Services Commerce Manufacturing

Very easy

Easy

Neither easy or difficult

Difficult

Very difficult

2015

2016

21% 21% 17% 19%

31% 30% 38% 29%

36% 41% 28%27%

8% 7%11%

13%2% 1% 6% 7%1% 1% 5%

Total Services Commerce Manufacturing

N/A

Very easy

Easy

Neither easy or difficult

Difficult

Very difficult

In general, it is impressive the % of enterprises that stated that they are facing difficulty or major difficulties in coping with their obligations.

For 2016, no significant changes are expected . However, enterprises coming from the field of commerce believe that 2016 shall be more difficult with regards to their ability to meet their obligations.

19

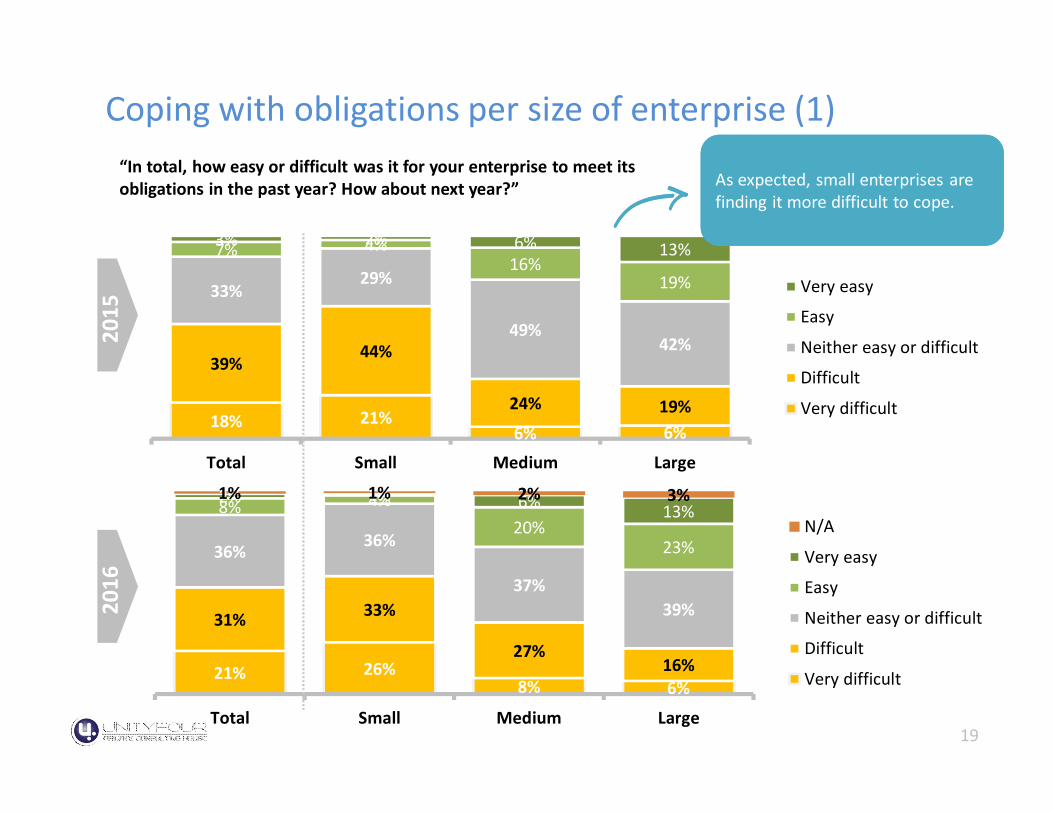

TurnoverCoping with obligations per size of enterprise (1)

18% 21%6% 6%

39%44%

24% 19%

33%29%

49%42%

7% 4%16%

19%

3% 2% 6% 13%

Total Small Medium Large

Very easy

Easy

Neither easy or difficult

Difficult

Very difficult

2015

2016

21% 26%8% 6%

31% 33%

27%16%

36% 36%

37%39%

8% 4%20%

23%

2% 1% 6% 13%1% 1% 2% 3%

Total Small Medium Large

N/A

Very easy

Easy

Neither easy or difficult

Difficult

Very difficult

“In total, how easy or difficult was it for your enterprise to meet its obligations in the past year? How about next year?” As expected, small enterprises are

finding it more difficult to cope.

20

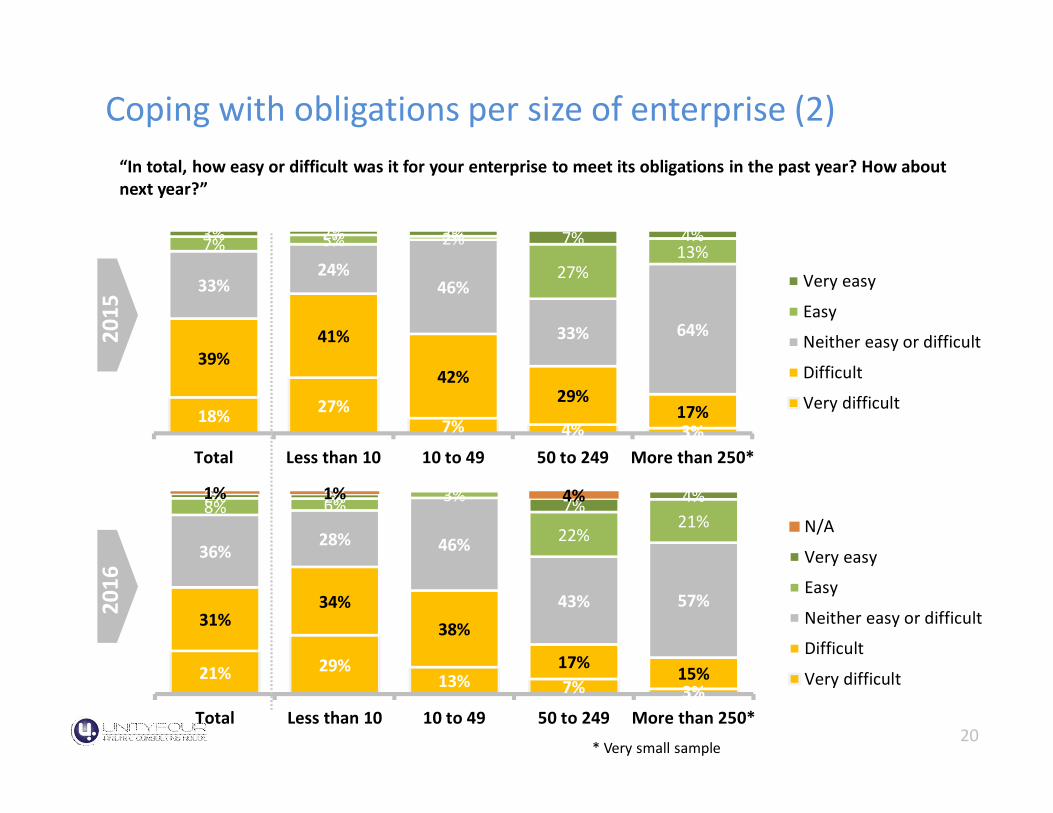

TurnoverCoping with obligations per size of enterprise (2)

18% 27%7% 4% 3%

39%41%

42%29%

17%

33%24%

46%

33% 64%

7% 5% 2%

27%13%

3% 2% 3% 7% 4%

Total Less than 10 10 to 49 50 to 249 More than 250*

Very easy

Easy

Neither easy or difficult

Difficult

Very difficult

2015

2016

21% 29%13% 7% 3%

31%34%

38%

17% 15%

36%28% 46%

43% 57%

8% 6% 3%

22%21%

2% 2% 7% 4%1% 1% 4%

Total Less than 10 10 to 49 50 to 249 More than 250*

N/A

Very easy

Easy

Neither easy or difficult

Difficult

Very difficult

“In total, how easy or difficult was it for your enterprise to meet its obligations in the past year? How about next year?”

* Very small sample

21

TurnoverObstacles for growth

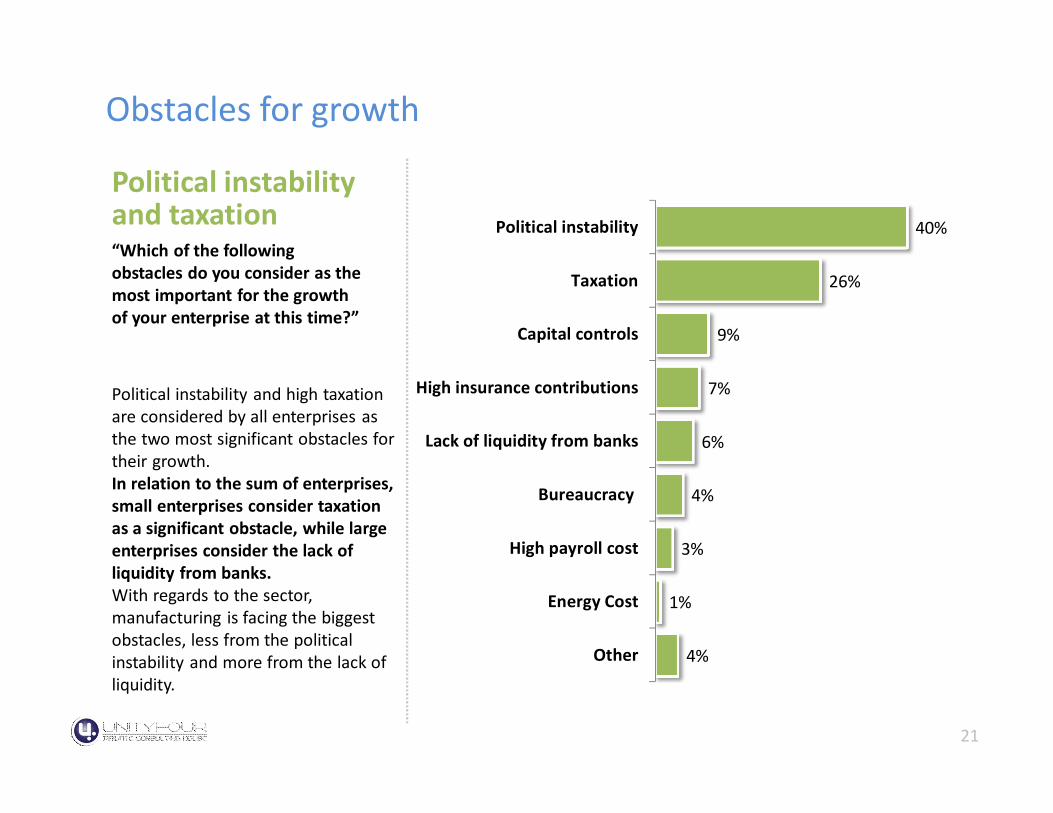

Political instability and taxation “Which of the following obstacles do you consider as the most important for the growth of your enterprise at this time?”

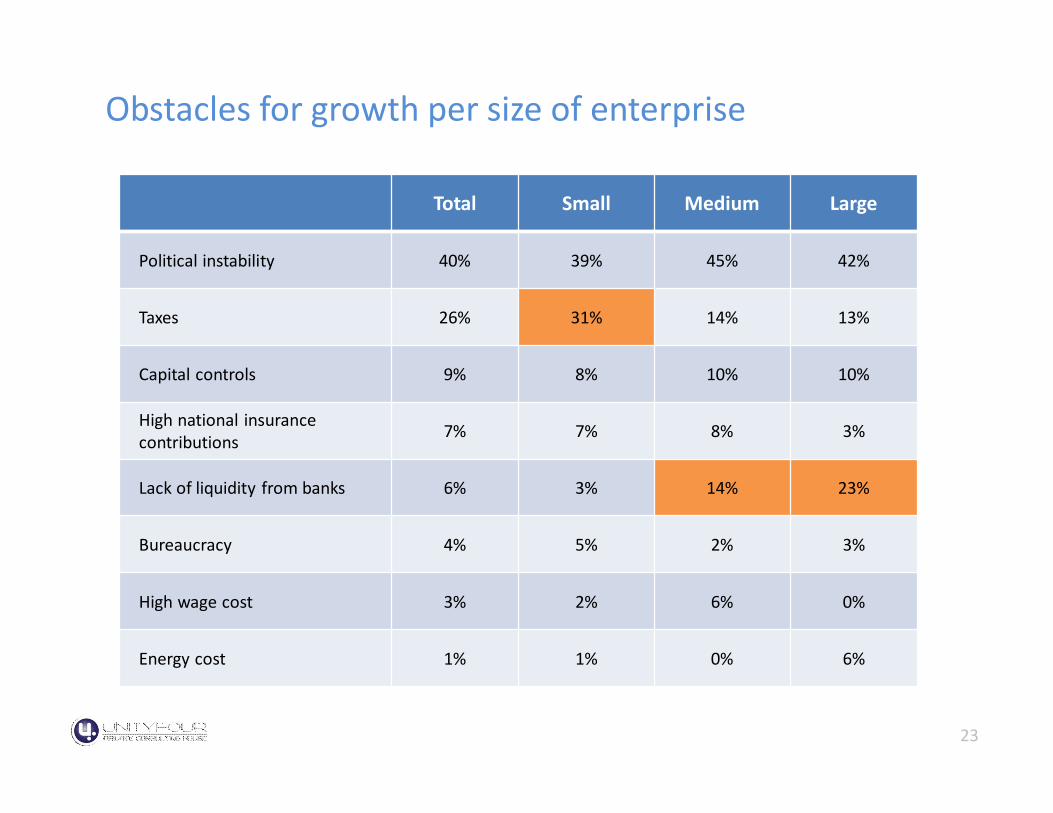

Political instability and high taxation are considered by all enterprises as the two most significant obstacles for their growth. In relation to the sum of enterprises, small enterprises consider taxation as a significant obstacle, while large enterprises consider the lack of liquidity from banks. With regards to the sector, manufacturing is facing the biggest obstacles, less from the political instability and more from the lack of liquidity.

40%

26%

9%

7%

6%

4%

3%

1%

4%

Political instability

Taxation

Capital controls

High insurance contributions

Lack of liquidity from banks

Bureaucracy

High payroll cost

Energy Cost

Other

22

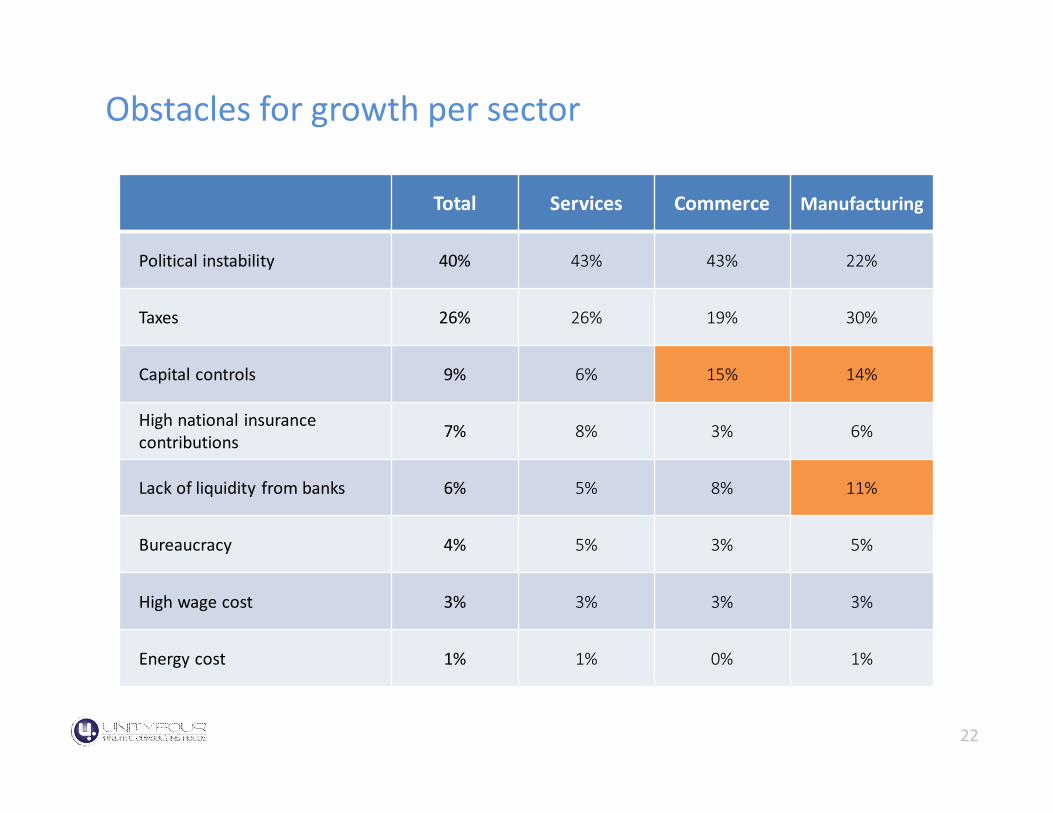

TurnoverObstacles for growth per sector

Total Services Commerce Manufacturing

Political instability 40% 43% 43% 22%

Taxes 26% 26% 19% 30%

Capital controls 9% 6% 15% 14%

High national insurance contributions 7% 8% 3% 6%

Lack of liquidity from banks 6% 5% 8% 11%

Bureaucracy 4% 5% 3% 5%

High wage cost 3% 3% 3% 3%

Energy cost 1% 1% 0% 1%

23

TurnoverObstacles for growth per size of enterprise

Total Small Medium Large

Political instability 40% 39% 45% 42%

Taxes 26% 31% 14% 13%

Capital controls 9% 8% 10% 10%

High national insurance contributions 7% 7% 8% 3%

Lack of liquidity from banks 6% 3% 14% 23%

Bureaucracy 4% 5% 2% 3%

High wage cost 3% 2% 6% 0%

Energy cost 1% 1% 0% 6%

24

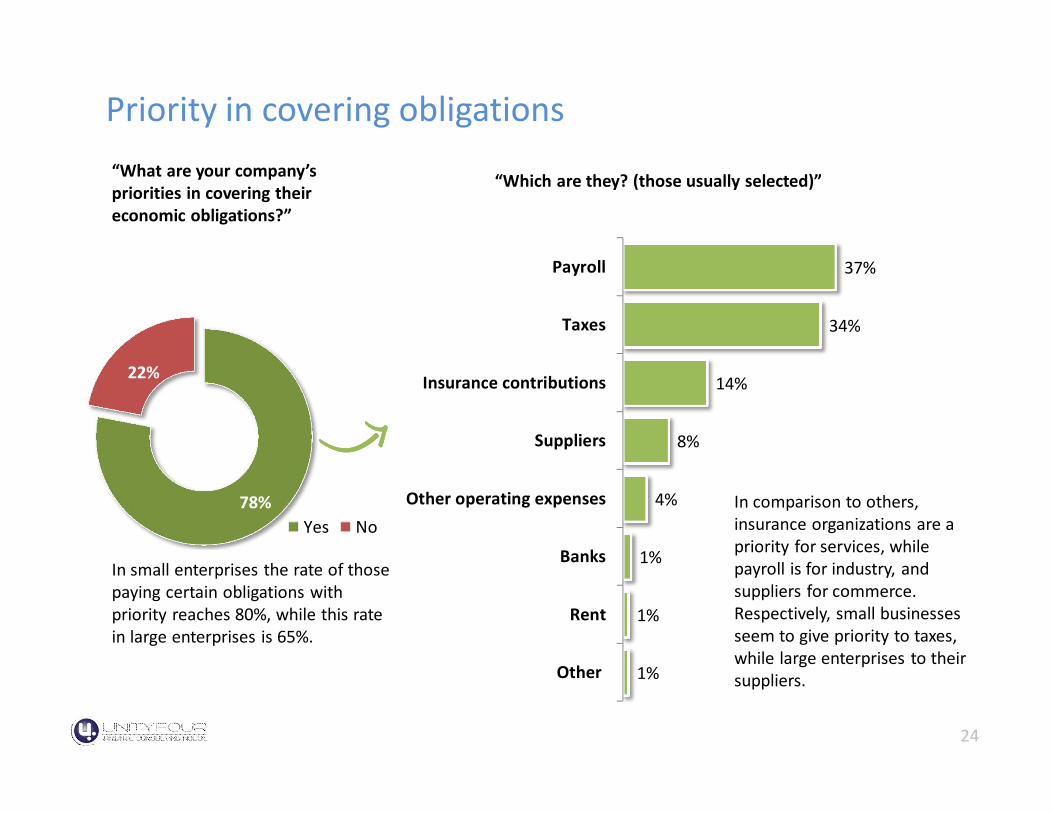

TurnoverPriority in covering obligations“What are your company’s priorities in covering their economic obligations?”

37%

34%

14%

8%

4%

1%

1%

1%

Payroll

Taxes

Insurance contributions

Suppliers

Other operating expenses

Banks

Rent

Other

78%

22%

Yes No

“Which are they? (those usually selected)”

In small enterprises the rate of those paying certain obligations with priority reaches 80%, while this rate in large enterprises is 65%.

In comparison to others, insurance organizations are a priority for services, while payroll is for industry, and suppliers for commerce. Respectively, small businesses seem to give priority to taxes, while large enterprises to their suppliers.

25

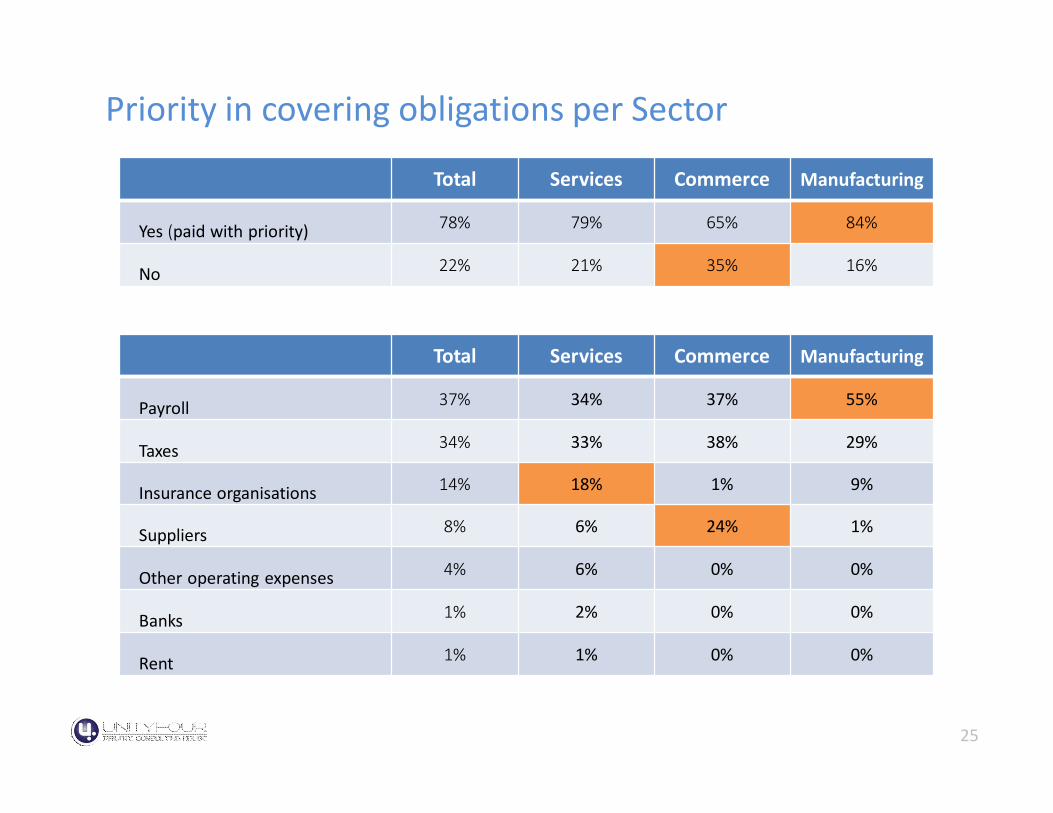

TurnoverPriority in covering obligations per Sector

Total Services Commerce Manufacturing

Payroll 37% 34% 37% 55%

Taxes 34% 33% 38% 29%

Insurance organisations 14% 18% 1% 9%

Suppliers 8% 6% 24% 1%

Other operating expenses 4% 6% 0% 0%

Banks 1% 2% 0% 0%

Rent 1% 1% 0% 0%

Total Services Commerce Manufacturing

Yes (paid with priority) 78% 79% 65% 84%

No 22% 21% 35% 16%

26

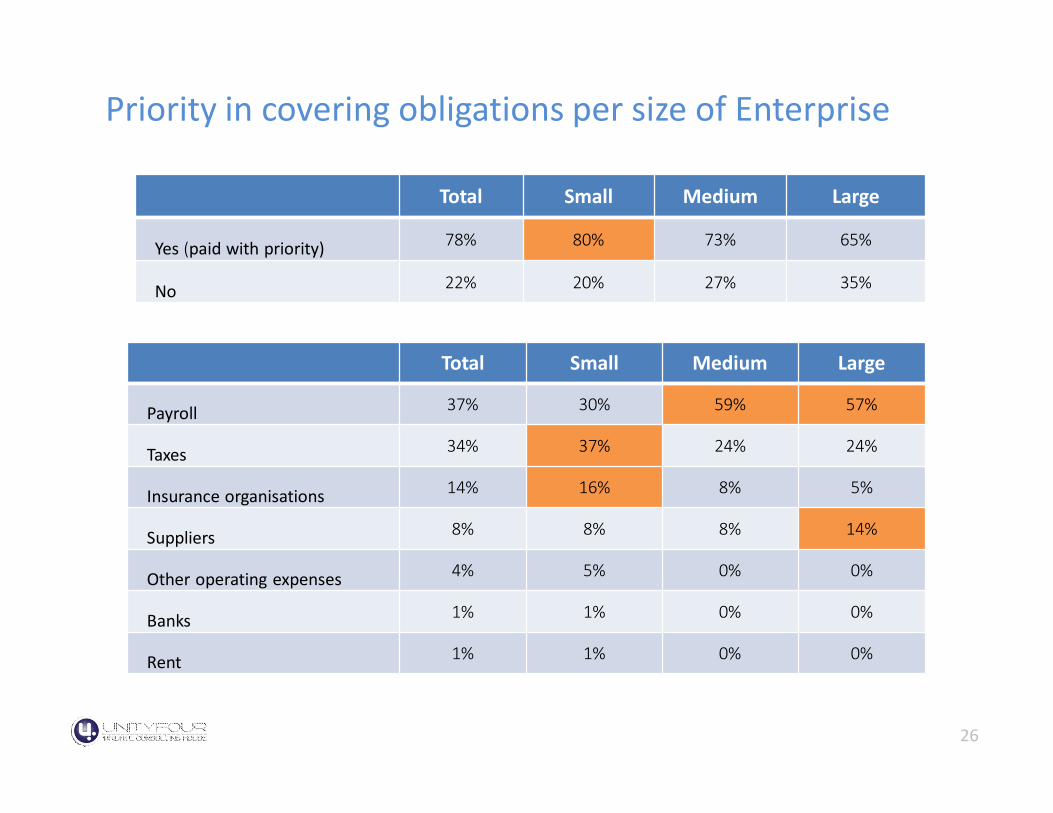

TurnoverPriority in covering obligations per size of Enterprise

Total Small Medium Large

Payroll 37% 30% 59% 57%

Taxes 34% 37% 24% 24%

Insurance organisations 14% 16% 8% 5%

Suppliers 8% 8% 8% 14%

Other operating expenses 4% 5% 0% 0%

Banks 1% 1% 0% 0%

Rent 1% 1% 0% 0%

Total Small Medium Large

Yes (paid with priority) 78% 80% 73% 65%

No 22% 20% 27% 35%

27

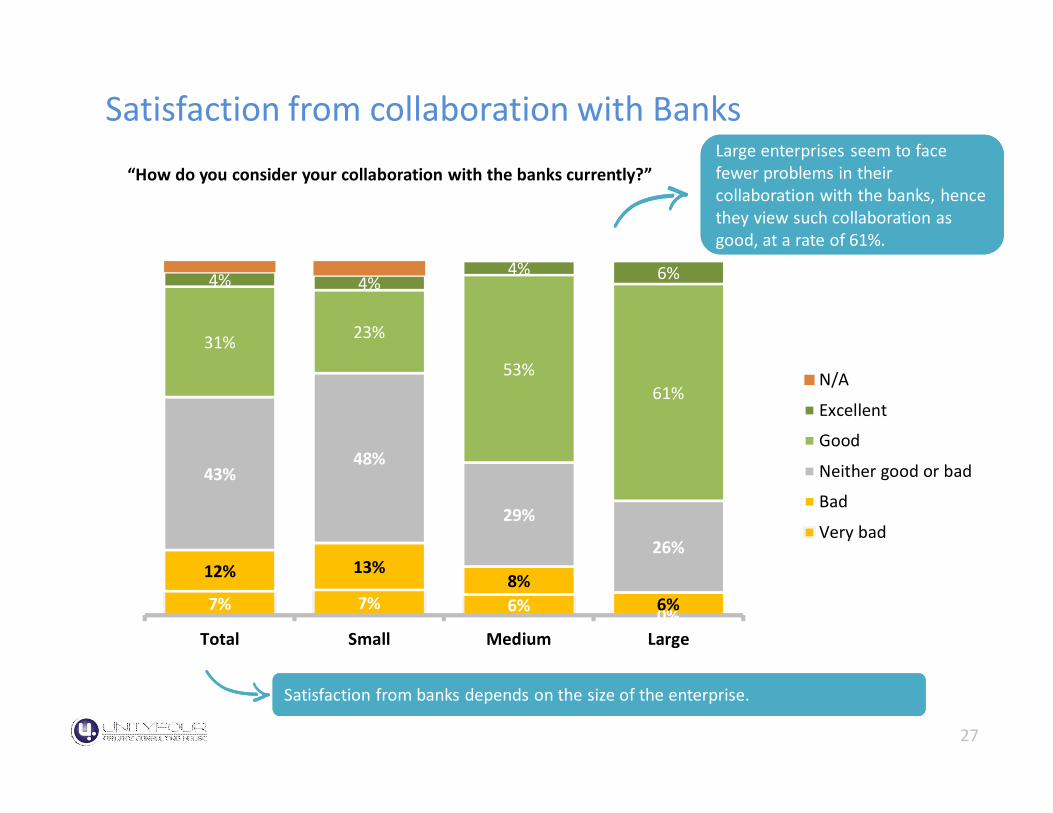

TurnoverSatisfaction from collaboration with Banks

7% 7% 6% 0%

12% 13%8%

6%

43%48%

29%

26%

31% 23%

53%61%

4% 4%4% 6%

Total Small Medium Large

N/A

Excellent

Good

Neither good or bad

Bad

Very bad

“How do you consider your collaboration with the banks currently?”Large enterprises seem to face fewer problems in their collaboration with the banks, hence they view such collaboration as good, at a rate of 61%.

Satisfaction from banks depends on the size of the enterprise.

28

Summary

29

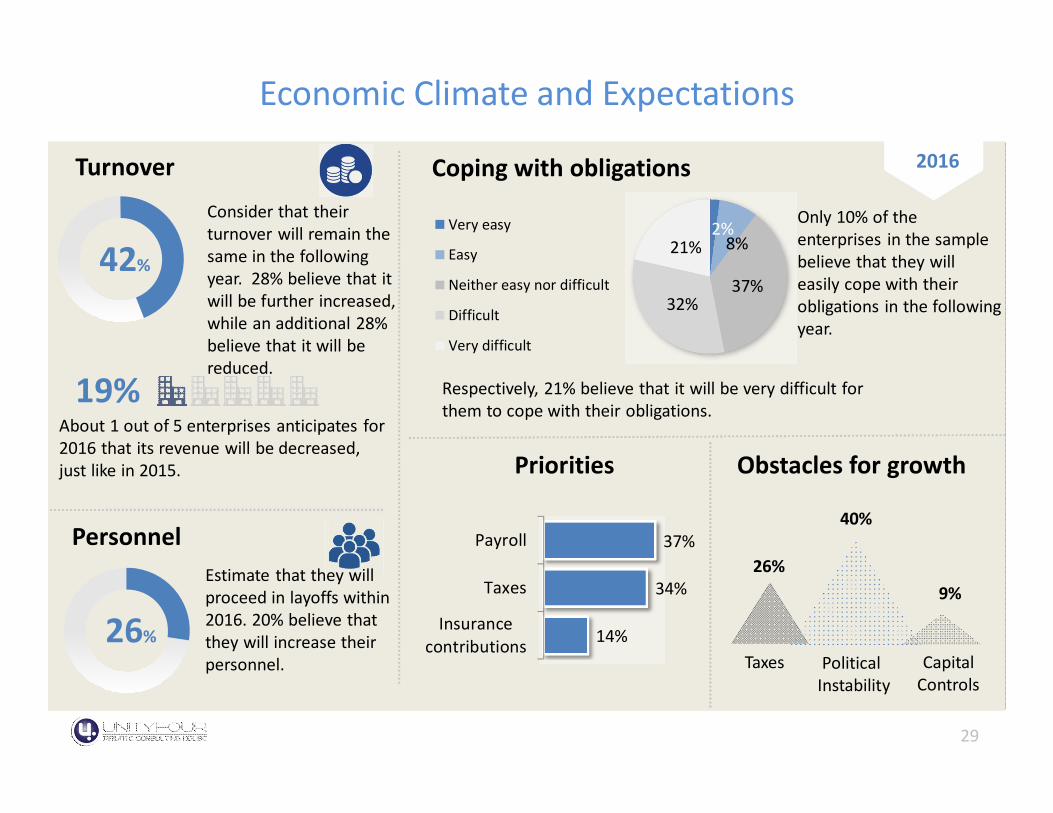

TurnoverEconomic Climate and Expectations

2016

42%

Consider that their turnover will remain the same in the following year. 28% believe that it will be further increased, while an additional 28% believe that it will be reduced.

Turnover

Personnel

26%

Estimate that they will proceed in layoffs within 2016. 20% believe that they will increase their personnel. Taxes

26%

CapitalControls

9%

Political Instability

40%

Obstacles for growth

19%About 1 out of 5 enterprises anticipates for 2016 that its revenue will be decreased, just like in 2015.

2%8%

37%32%

21%Very easy

Easy

Neither easy nor difficult

Difficult

Very difficult

Coping with obligations

Only 10% of the enterprises in the sample believe that they will easily cope with their obligations in the following year.

Respectively, 21% believe that it will be very difficult for them to cope with their obligations.

Priorities

37%

34%

14%

Payroll

Taxes

Insurancecontributions

30

TurnoverConclusions (1)It is a fact that in the recent years, the country has been enduring an extensive period of recession, mainlycharacterized by high unemployment, reduction of investments, and an increased feeling of uncertainty andinstability. The economic crisis has left and continues to leave its mark on almost every sector of the financialactivity. Demand for products and services has been significantly reduced, along with numerous enterprises,which despite all efforts did not manage to survive.

As expected, the crisis first affected the weakest, who exited the game and left the smaller pie to the strongeror better prepared.

The results of this research confirm the above, since enterprises believe that their sector has endured theheaviest losses. 4 out of 10 executives believe that their sector has been heavily affected in a negative way.Commerce and generally small and medium-sized enterprises have paid the biggest toll.

In an already aggravated commercial environment, businesses must fight even more to survive.

Based on the above, the key obstacles that must be surpassed are political instability (40%), taxation (26%) andthe capital controls, which are noted as the key obstacle by 9% of the samples.

31

TurnoverConclusions (2)As long as these obstacles continue to exist and become even more difficult, it is true that enterprises willcontinue to struggle to cope with their obligations. For 2016, 52% of the respondents consider that they willhave great difficulty and difficulty in coping with their obligations. Commercial enteprises, and generally smallenterprises, will face the biggest hardship.

Already, numerous enterprises (mainly the smaller ones) pay some of their obligations with priority. For most ofthem, payroll (37%), taxes (34%) and insurance organizations (14%) come first in the list of obligations. Inaddition, suppliers are the most important obligation for commercial and large enterprises.

With regards to personnel, according to business executives, the new year is not expected to be significantlydifferent from the previous one. The key characteristic is stagnancy. This becomes all the more important afterconsidering that some of the enterprises are already in their limits in terms of personnel. However, 28% areoptimistic, considering that their personnel will increase within 2016, thus balancing somewhat the loss ofemployment.

32

TurnoverConclusions (3)Finally, with regards to the turnover of enterprises, the forecasts by executives for 2016 appear to be slightlymore optimistic.

2015 will close with 2 out of 10 enterprises having an increase in their turnover, in relation to 2014, while for2016, 3 out of 10 executives believe that they will manage to increase their turnover. Optimism depends on thesize of the enterprise, i.e. the larger the company, the bigger the expectation for growth, and vice versa.

With regards to the majority (42%), 2016 will not bring any major changes to their turnover.