frost & sullivan asia pacific mega trends

TRANSCRIPT

1 <0000-00>

Global and Asia Pacific Mega Trends

Mega Trends to 2020

2 <0000-00>

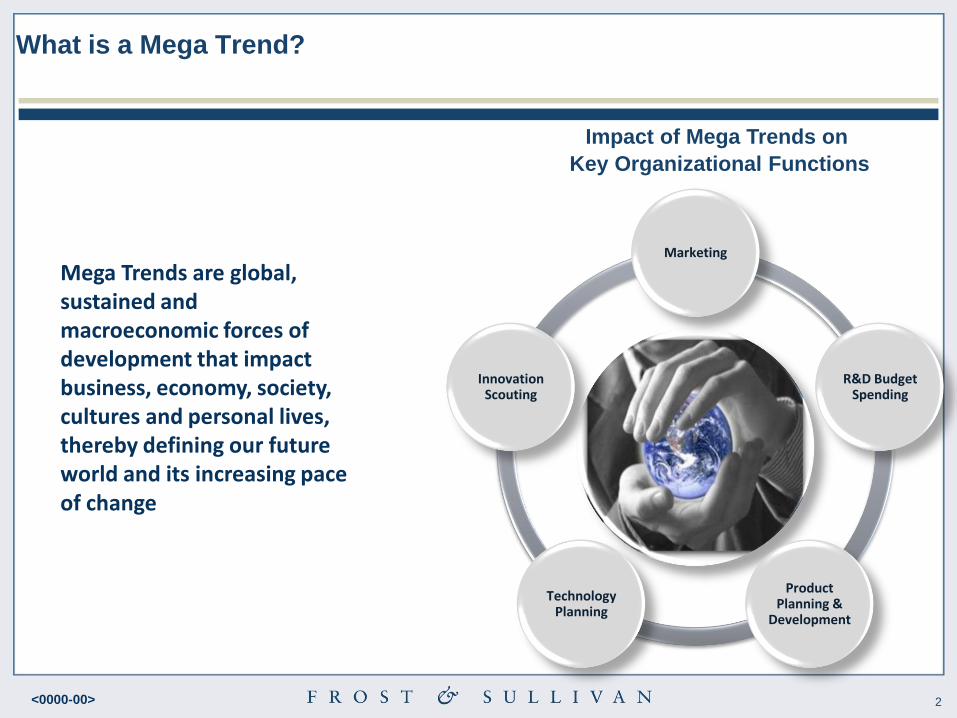

What is a Mega Trend?

Impact of Mega Trends on

Key Organizational Functions

Marketing

R&D Budget Spending

Product Planning &

Development

Technology Planning

Innovation Scouting

Mega Trends are global, sustained and macroeconomic forces of development that impact business, economy, society, cultures and personal lives, thereby defining our future world and its increasing pace of change

3 <0000-00>

Top Global Mega Trends

Urbanization

Smart is the New

Green

Innovating to Zero

Health, Wellness and

Ageing

E-Mobility

New Business Models

Infrastructure

Social Trends

4 <0000-00>

Rise of the “new” super economies in Asia

- Indonesia, Vietnam, The Philippines & Bangladesh

Indonesia, Vietnam, The Philippines and

Bangladesh are expected to be the ―new super

economies‖ driving the Asian growth story in 2020

5 <0000-00>

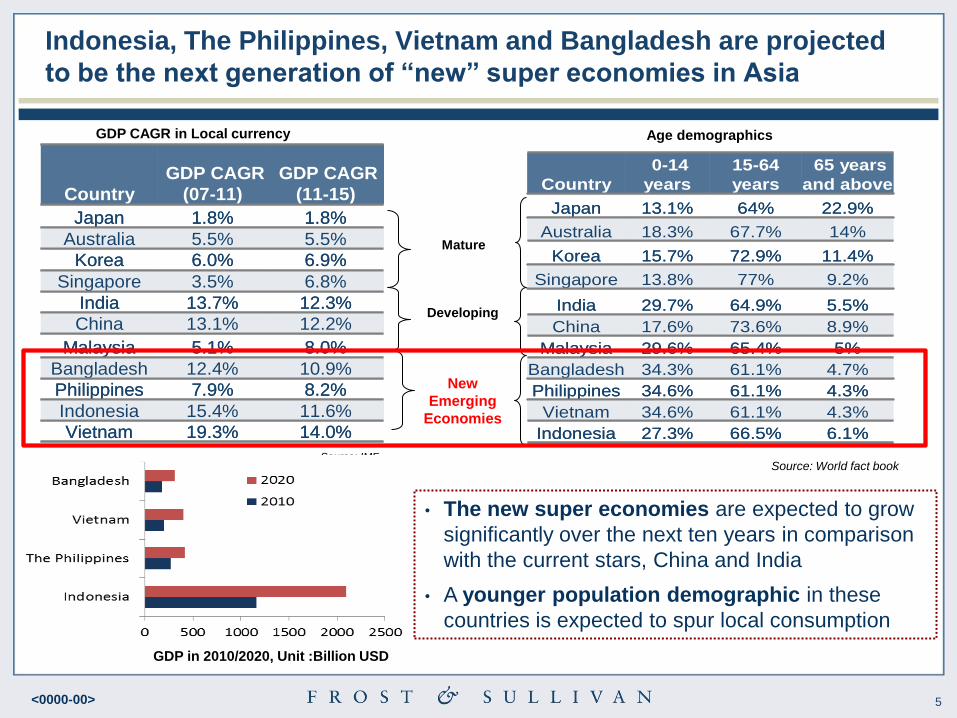

Indonesia, The Philippines, Vietnam and Bangladesh are projected

to be the next generation of “new” super economies in Asia

• The new super economies are expected to grow

significantly over the next ten years in comparison

with the current stars, China and India

• A younger population demographic in these

countries is expected to spur local consumption

Source: IMF

11.6%15.4%Indonesia

14.0%19.3%Vietnam

8.2%7.9%Philippines

10.9%12.4%Bangladesh

Country

GDP CAGR

(07-11)

GDP CAGR

(11-15)

Japan 1.8% 1.8%

Australia 5.5% 5.5%

Korea 6.0% 6.9%

Singapore 3.5% 6.8%

India 13.7% 12.3%

China 13.1% 12.2%

Malaysia 5.1% 8.0%

11.6%15.4%Indonesia

14.0%19.3%Vietnam

8.2%7.9%Philippines

10.9%12.4%Bangladesh

Country

GDP CAGR

(07-11)

GDP CAGR

(11-15)

Japan 1.8% 1.8%

Australia 5.5% 5.5%

Korea 6.0% 6.9%

Singapore 3.5% 6.8%

India 13.7% 12.3%

China 13.1% 12.2%

Malaysia 5.1% 8.0%

Mature

GDP CAGR in Local currency

Developing

4.7%61.1%34.3%Bangladesh

4.3%61.1%34.6%Philippines

5%65.4%29.6%Malaysia

14%67.7%18.3%Australia

11.4%72.9%15.7%Korea

22.9% 64%13.1% Japan

66.5%

61.1%

73.6%

64.9%

77%

15-64

years

4.3%34.6%Vietnam

6.1%27.3%Indonesia

Country

0-14

years

65 years

and above

Singapore 13.8% 9.2%

India 29.7% 5.5%

China 17.6% 8.9%

4.7%61.1%34.3%Bangladesh

4.3%61.1%34.6%Philippines

5%65.4%29.6%Malaysia

14%67.7%18.3%Australia

11.4%72.9%15.7%Korea

22.9% 64%13.1% Japan

66.5%

61.1%

73.6%

64.9%

77%

15-64

years

4.3%34.6%Vietnam

6.1%27.3%Indonesia

Country

0-14

years

65 years

and above

Singapore 13.8% 9.2%

India 29.7% 5.5%

China 17.6% 8.9%

Source: World fact book

Age demographics

New

Emerging

Economies

GDP in 2010/2020, Unit :Billion USD

6 <0000-00>

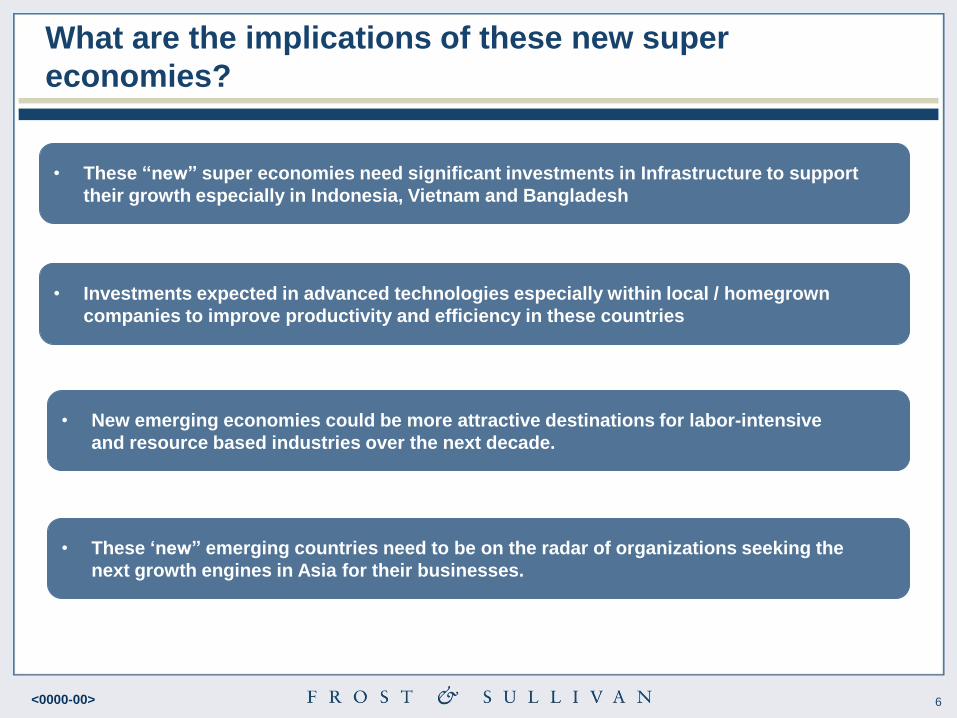

What are the implications of these new super

economies?

• These “new” super economies need significant investments in Infrastructure to support

their growth especially in Indonesia, Vietnam and Bangladesh

• Investments expected in advanced technologies especially within local / homegrown

companies to improve productivity and efficiency in these countries

• New emerging economies could be more attractive destinations for labor-intensive

and resource based industries over the next decade.

• These „new” emerging countries need to be on the radar of organizations seeking the

next growth engines in Asia for their businesses.

7 <0000-00>

The Aging of Asia

Asian populations will age significantly over the next decade

8 <0000-00>

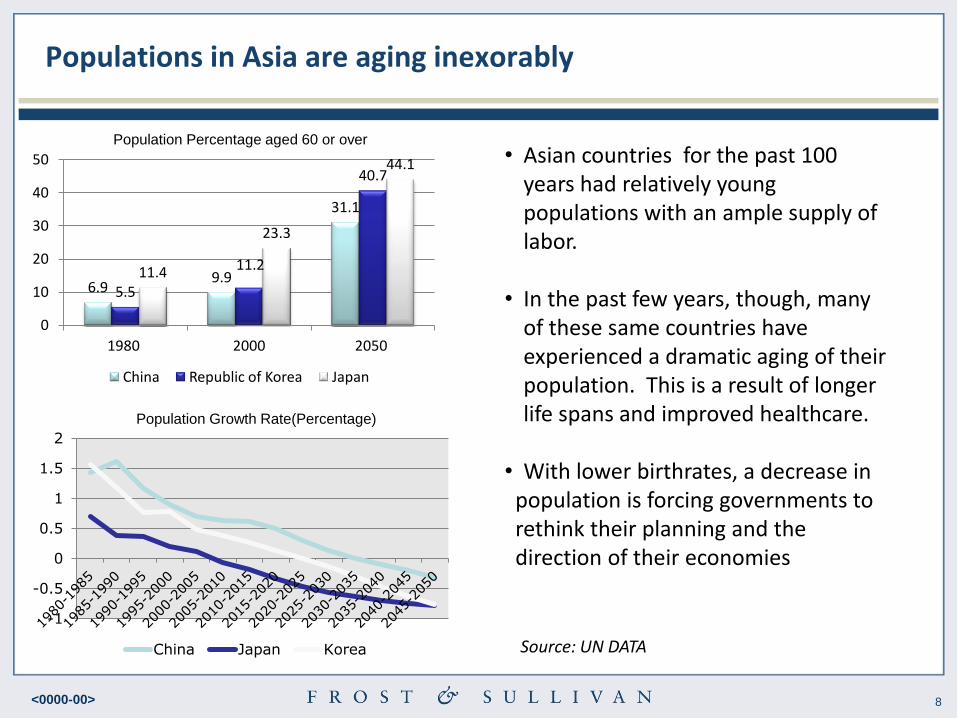

Populations in Asia are aging inexorably

6.9 9.9

31.1

5.5

11.2

40.7

11.4

23.3

44.1

0

10

20

30

40

50

1980 2000 2050

China Republic of Korea Japan

Population Percentage aged 60 or over

-1

-0.5

0

0.5

1

1.5

2

China Japan Korea

Population Growth Rate(Percentage)

• Asian countries for the past 100 years had relatively young populations with an ample supply of labor.

• In the past few years, though, many

of these same countries have experienced a dramatic aging of their population. This is a result of longer life spans and improved healthcare.

• With lower birthrates, a decrease in population is forcing governments to rethink their planning and the direction of their economies

Source: UN DATA

9 <0000-00>

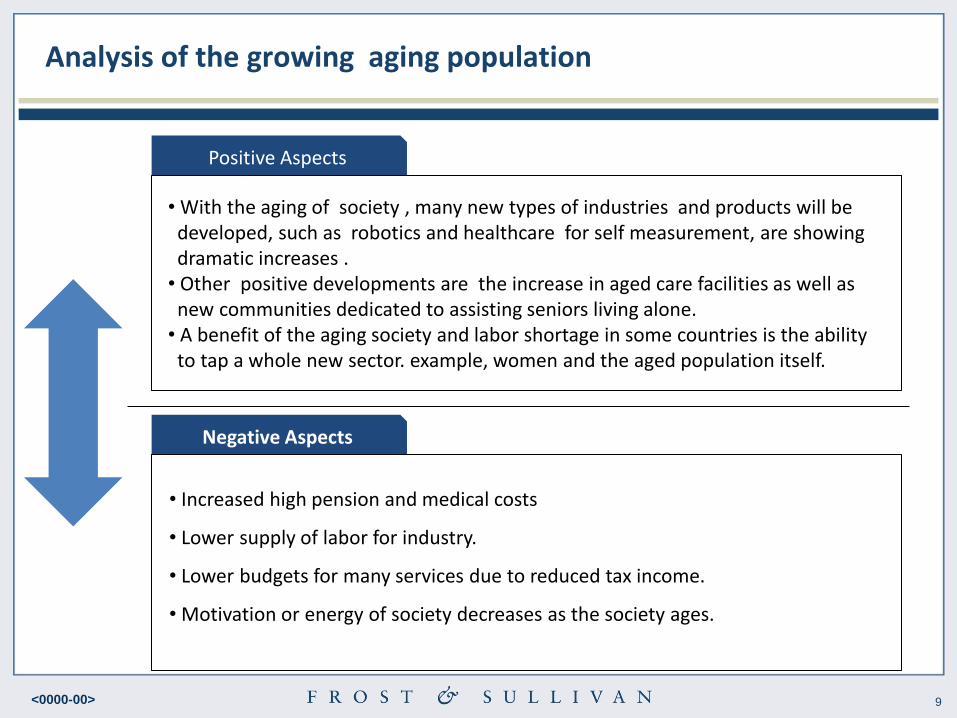

Analysis of the growing aging population

Positive Aspects

• With the aging of society , many new types of industries and products will be developed, such as robotics and healthcare for self measurement, are showing dramatic increases . • Other positive developments are the increase in aged care facilities as well as new communities dedicated to assisting seniors living alone. • A benefit of the aging society and labor shortage in some countries is the ability to tap a whole new sector. example, women and the aged population itself.

Negative Aspects

• Increased high pension and medical costs

• Lower supply of labor for industry.

• Lower budgets for many services due to reduced tax income.

• Motivation or energy of society decreases as the society ages.

10 <0000-00>

Investments in infrastructure to dominate

government spending in Asia

Government spending on infrastructure is expected to provide

significant growth opportunities for private sector participation

through PPP during the next ten years till 2020

11 <0000-00> USD billion

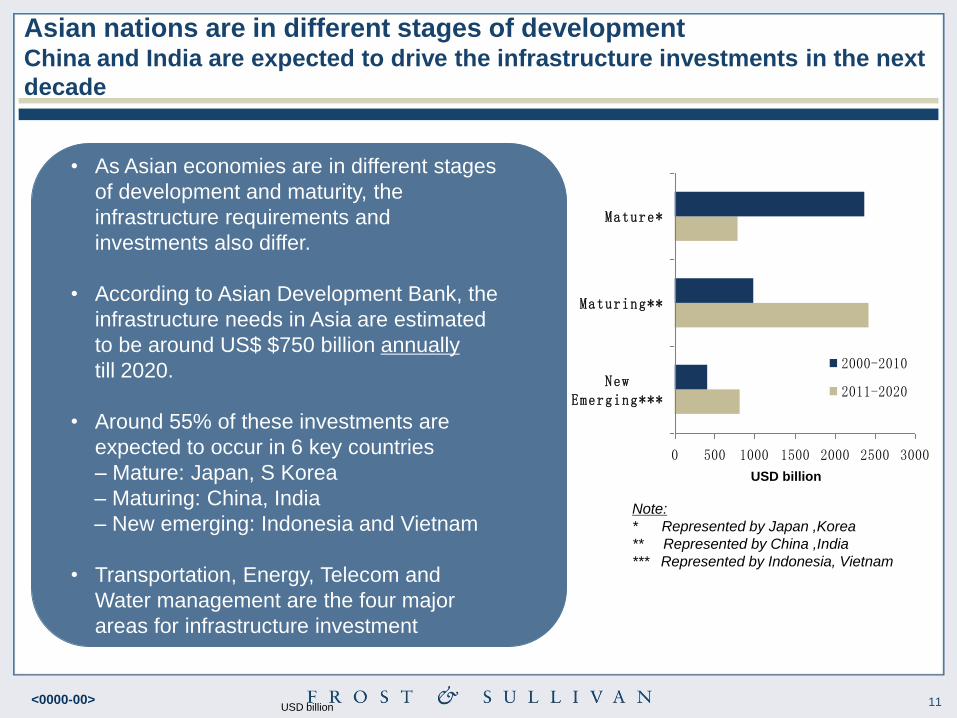

Asian nations are in different stages of development China and India are expected to drive the infrastructure investments in the next

decade

0 500 1000 1500 2000 2500 3000

NewEmerging***

Maturing**

Mature*

2000-2010

2011-2020

Note:

* Represented by Japan ,Korea

** Represented by China ,India

*** Represented by Indonesia, Vietnam

• As Asian economies are in different stages

of development and maturity, the

infrastructure requirements and

investments also differ.

• According to Asian Development Bank, the

infrastructure needs in Asia are estimated

to be around US$ $750 billion annually

till 2020.

• Around 55% of these investments are

expected to occur in 6 key countries

– Mature: Japan, S Korea

– Maturing: China, India

– New emerging: Indonesia and Vietnam

• Transportation, Energy, Telecom and

Water management are the four major

areas for infrastructure investment

USD billion

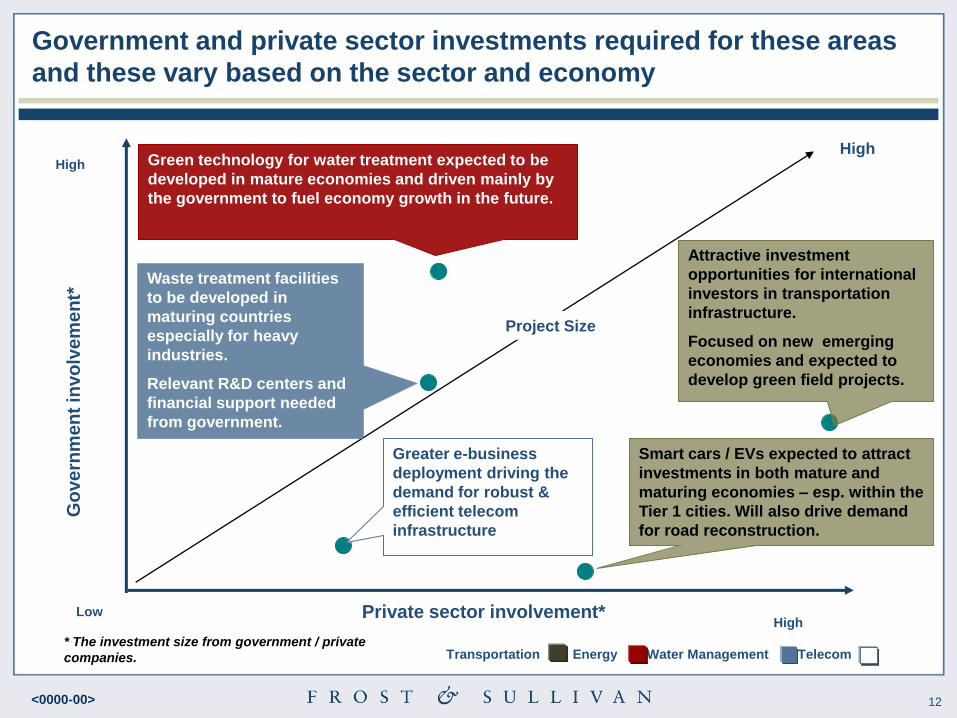

12 <0000-00>

Government and private sector investments required for these areas

and these vary based on the sector and economy G

ove

rnm

en

t in

vo

lve

me

nt*

Private sector involvement*

High

Low High

Project Size

High

Transportation Energy Water Management Telecom

Greater e-business

deployment driving the

demand for robust &

efficient telecom

infrastructure

Waste treatment facilities

to be developed in

maturing countries

especially for heavy

industries.

Relevant R&D centers and

financial support needed

from government.

Smart cars / EVs expected to attract

investments in both mature and

maturing economies – esp. within the

Tier 1 cities. Will also drive demand

for road reconstruction.

Green technology for water treatment expected to be

developed in mature economies and driven mainly by

the government to fuel economy growth in the future.

* The investment size from government / private

companies.

Attractive investment

opportunities for international

investors in transportation

infrastructure.

Focused on new emerging

economies and expected to

develop green field projects.

13 <0000-00>

Growth in Intra Asia Trade

Intra Asian Trade will grow exponentially over the next decade

14 <0000-00>

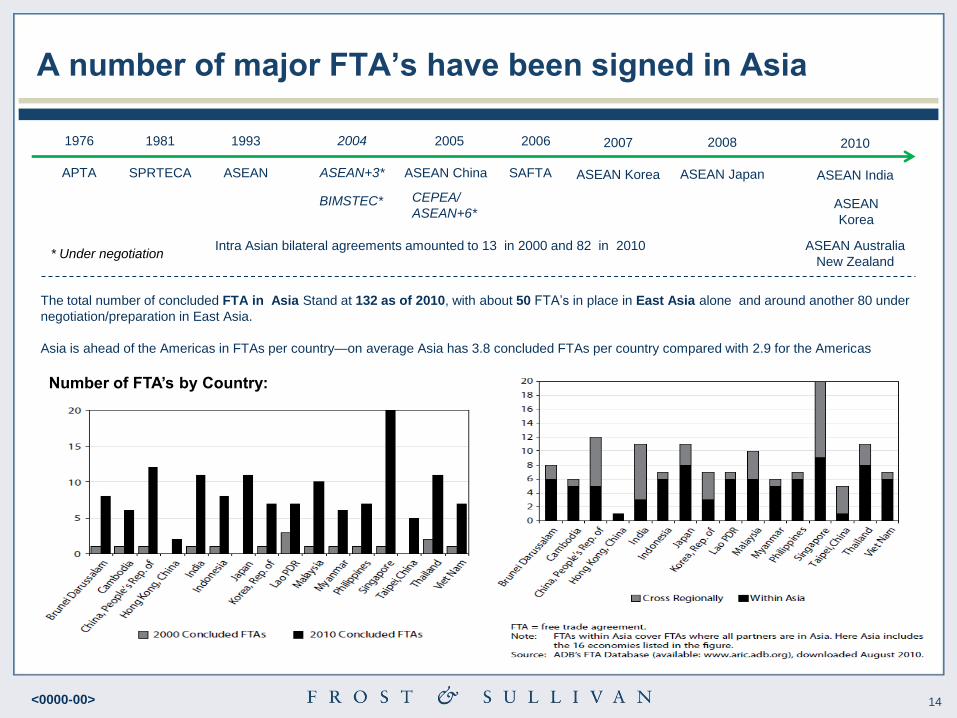

A number of major FTA‟s have been signed in Asia

1976

APTA

1993

ASEAN

2006

SAFTA

1981

SPRTECA

2010

ASEAN India

2008

ASEAN Japan

2007

ASEAN Korea

2005

ASEAN China

ASEAN Australia

New Zealand

BIMSTEC* CEPEA/

ASEAN+6*

2004

ASEAN+3*

ASEAN

Korea

Intra Asian bilateral agreements amounted to 13 in 2000 and 82 in 2010

The total number of concluded FTA in Asia Stand at 132 as of 2010, with about 50 FTA’s in place in East Asia alone and around another 80 under

negotiation/preparation in East Asia.

Asia is ahead of the Americas in FTAs per country—on average Asia has 3.8 concluded FTAs per country compared with 2.9 for the Americas

Number of FTA‟s by Country:

* Under negotiation

15 <0000-00>

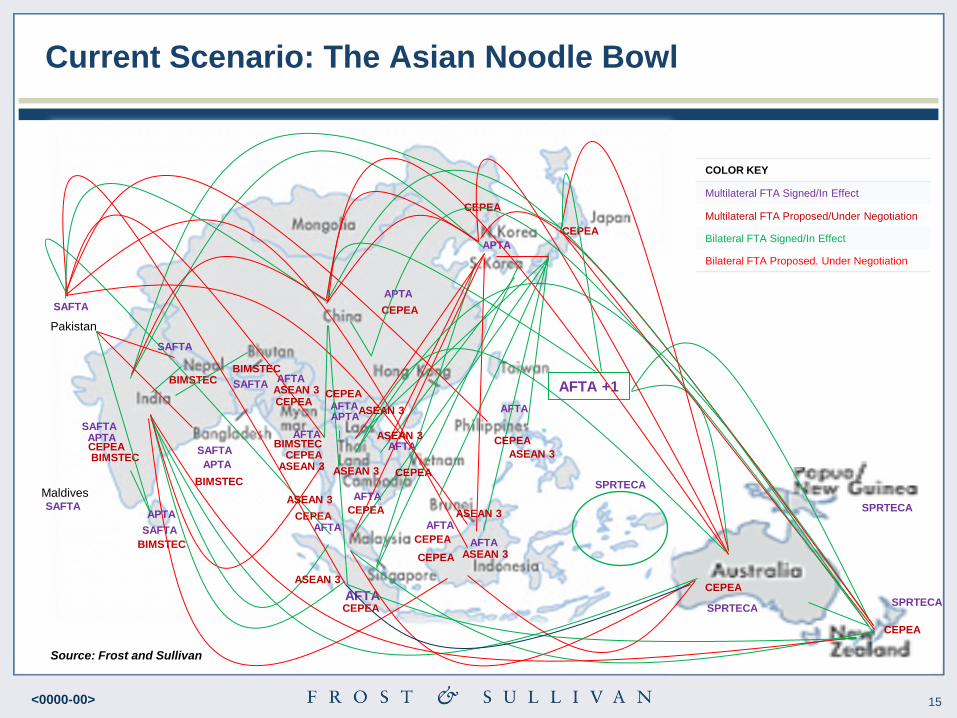

Current Scenario: The Asian Noodle Bowl

SPRTECA

APTA

AFTA

Pakistan

Maldives

SAFTA

SPRTECA SPRTECA

SPRTECA SAFTA

SAFTA

SAFTA

SAFTA

SAFTA

SAFTA

APTA

APTA

APTA

APTA

APTA

AFTA

AFTA

AFTA

AFTA

AFTA

AFTA

AFTA

AFTA

AFTA

BIMSTEC

BIMSTEC

BIMSTEC

BIMSTEC

BIMSTEC BIMSTEC

AFTA +1

Source: Frost and Sullivan

CEPEA

CEPEA

CEPEA

CEPEA

CEPEA

CEPEA

CEPEA

CEPEA

CEPEA

CEPEA

CEPEA

CEPEA

CEPEA

CEPEA

CEPEA

CEPEA

ASEAN 3

ASEAN 3

ASEAN 3

ASEAN 3

ASEAN 3

ASEAN 3

ASEAN 3

ASEAN 3 ASEAN 3

ASEAN 3

COLOR KEY

Multilateral FTA Signed/In Effect

Multilateral FTA Proposed/Under Negotiation

Bilateral FTA Signed/In Effect

Bilateral FTA Proposed. Under Negotiation

16 <0000-00>

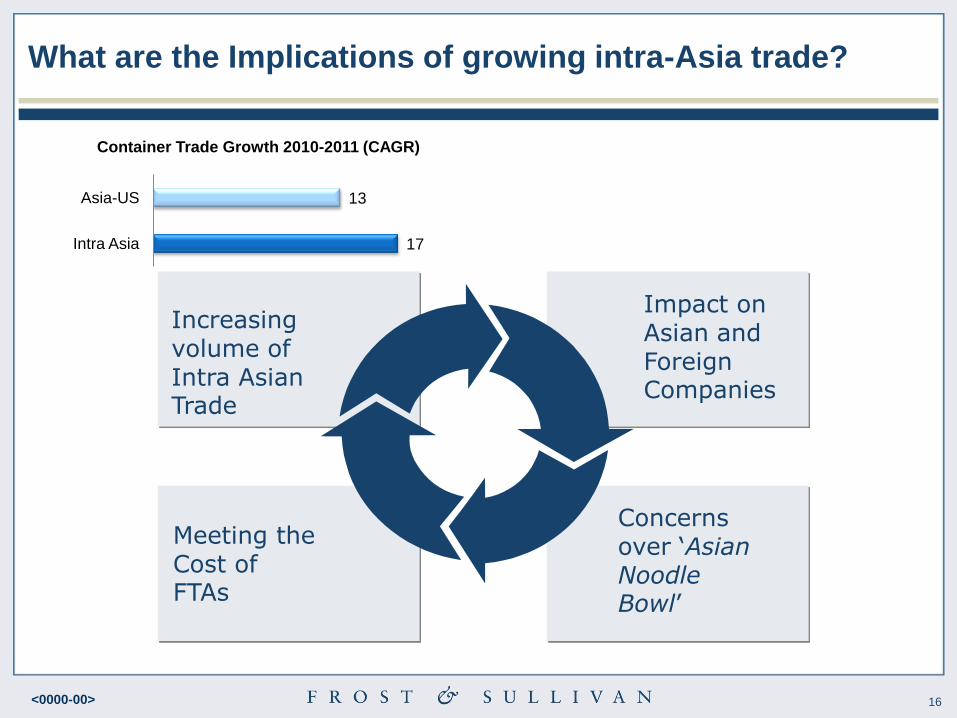

What are the Implications of growing intra-Asia trade?

17

13

Intra Asia

Asia-US

Container Trade Growth 2010-2011 (CAGR)

Increasing volume of Intra Asian Trade

Impact on Asian and Foreign Companies

Meeting the Cost of FTAs

Concerns over ‘Asian Noodle Bowl’

17 <0000-00>

Increased Urbanization and Emergence of Super

Cities

Asia will continue to urbanize with the emergence of more and

more ―super cities‖

18 <0000-00>

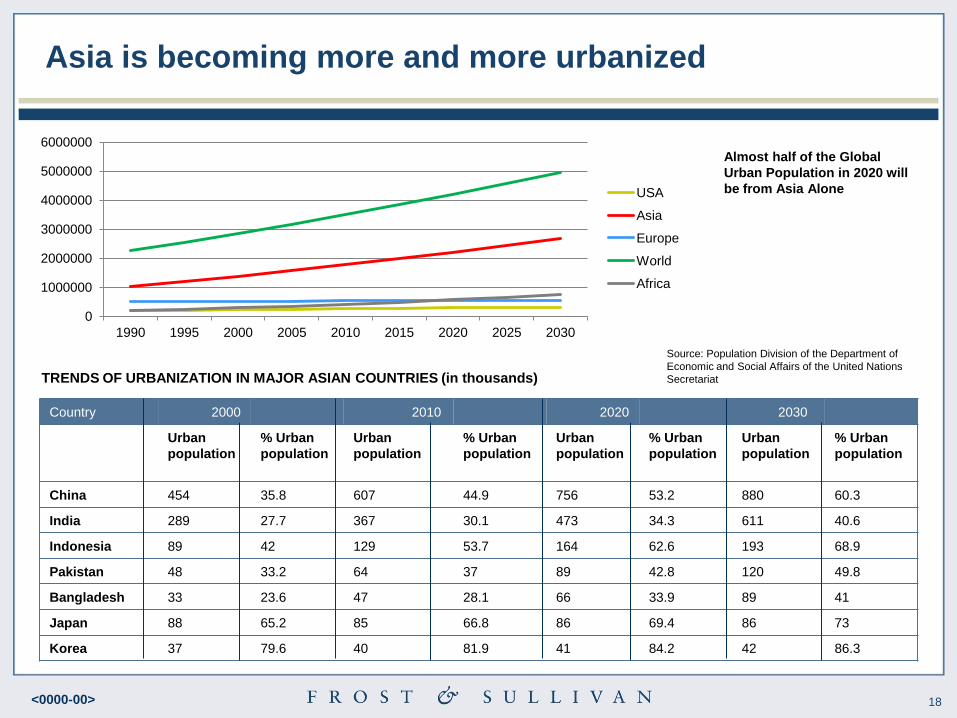

Asia is becoming more and more urbanized

0

1000000

2000000

3000000

4000000

5000000

6000000

1990 1995 2000 2005 2010 2015 2020 2025 2030

USA

Asia

Europe

World

Africa

Almost half of the Global

Urban Population in 2020 will

be from Asia Alone

Country 2000 2010 2020 2030

Urban

population

% Urban

population

Urban

population

% Urban

population

Urban

population

% Urban

population

Urban

population

% Urban

population

China 454 35.8 607 44.9 756 53.2 880 60.3

India 289 27.7 367 30.1 473 34.3 611 40.6

Indonesia 89 42 129 53.7 164 62.6 193 68.9

Pakistan 48 33.2 64 37 89 42.8 120 49.8

Bangladesh 33 23.6 47 28.1 66 33.9 89 41

Japan 88 65.2 85 66.8 86 69.4 86 73

Korea 37 79.6 40 81.9 41 84.2 42 86.3

Source: Population Division of the Department of

Economic and Social Affairs of the United Nations

Secretariat TRENDS OF URBANIZATION IN MAJOR ASIAN COUNTRIES (in thousands)

19 <0000-00>

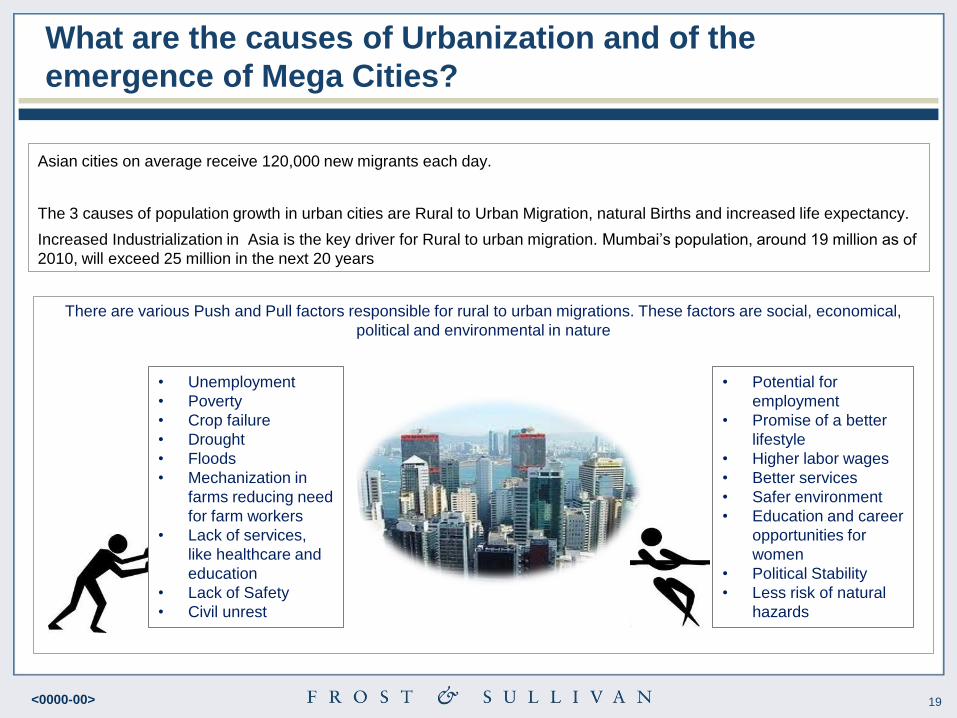

What are the causes of Urbanization and of the

emergence of Mega Cities?

Asian cities on average receive 120,000 new migrants each day.

The 3 causes of population growth in urban cities are Rural to Urban Migration, natural Births and increased life expectancy.

Increased Industrialization in Asia is the key driver for Rural to urban migration. Mumbai’s population, around 19 million as of

2010, will exceed 25 million in the next 20 years

There are various Push and Pull factors responsible for rural to urban migrations. These factors are social, economical,

political and environmental in nature

• Unemployment

• Poverty

• Crop failure

• Drought

• Floods

• Mechanization in

farms reducing need

for farm workers

• Lack of services,

like healthcare and

education

• Lack of Safety

• Civil unrest

• Potential for

employment

• Promise of a better

lifestyle

• Higher labor wages

• Better services

• Safer environment

• Education and career

opportunities for

women

• Political Stability

• Less risk of natural

hazards

20 <0000-00>

Huge Increase In Education Within Asia Pacific As

Governments and Businesses Are Moving Towards

Becoming Knowledge Based Economies

Huge Increase in Education

21 <0000-00>

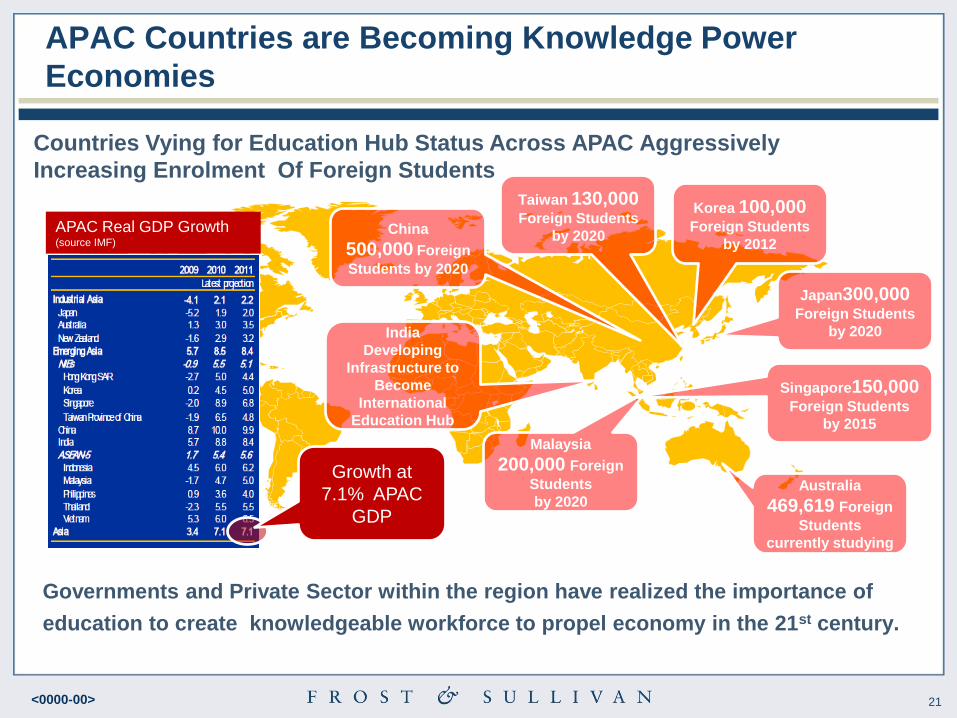

APAC Real GDP Growth (source IMF)

APAC Countries are Becoming Knowledge Power

Economies

Governments and Private Sector within the region have realized the importance of

education to create knowledgeable workforce to propel economy in the 21st century.

Countries Vying for Education Hub Status Across APAC Aggressively

Increasing Enrolment Of Foreign Students

Malaysia

200,000 Foreign

Students

by 2020

Singapore150,000 Foreign Students

by 2015

Australia

469,619 Foreign

Students

currently studying

Korea 100,000 Foreign Students

by 2012

India

Developing

Infrastructure to

Become

International

Education Hub

China

500,000 Foreign

Students by 2020

Japan300,000

Foreign Students

by 2020

Taiwan 130,000

Foreign Students

by 2020

Growth at

7.1% APAC

GDP

22 <0000-00>

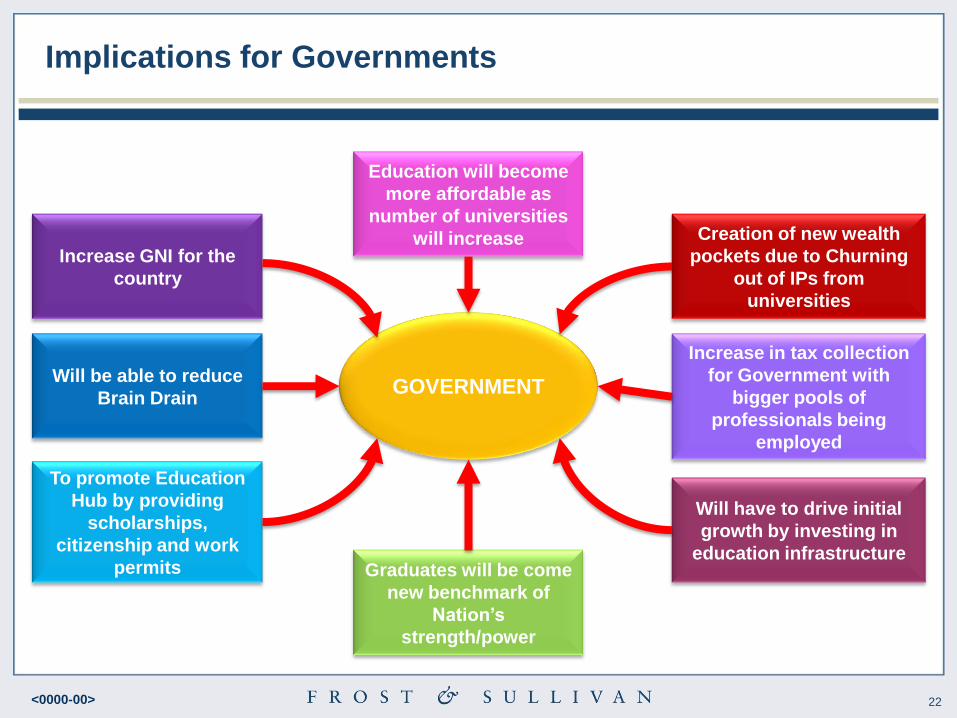

Implications for Governments

GOVERNMENT

Graduates will be come

new benchmark of

Nation‟s

strength/power

Creation of new wealth

pockets due to Churning

out of IPs from

universities

Increase in tax collection

for Government with

bigger pools of

professionals being

employed

To promote Education

Hub by providing

scholarships,

citizenship and work

permits

Will have to drive initial

growth by investing in

education infrastructure

Education will become

more affordable as

number of universities

will increase

Will be able to reduce

Brain Drain

Increase GNI for the

country

23 <0000-00>

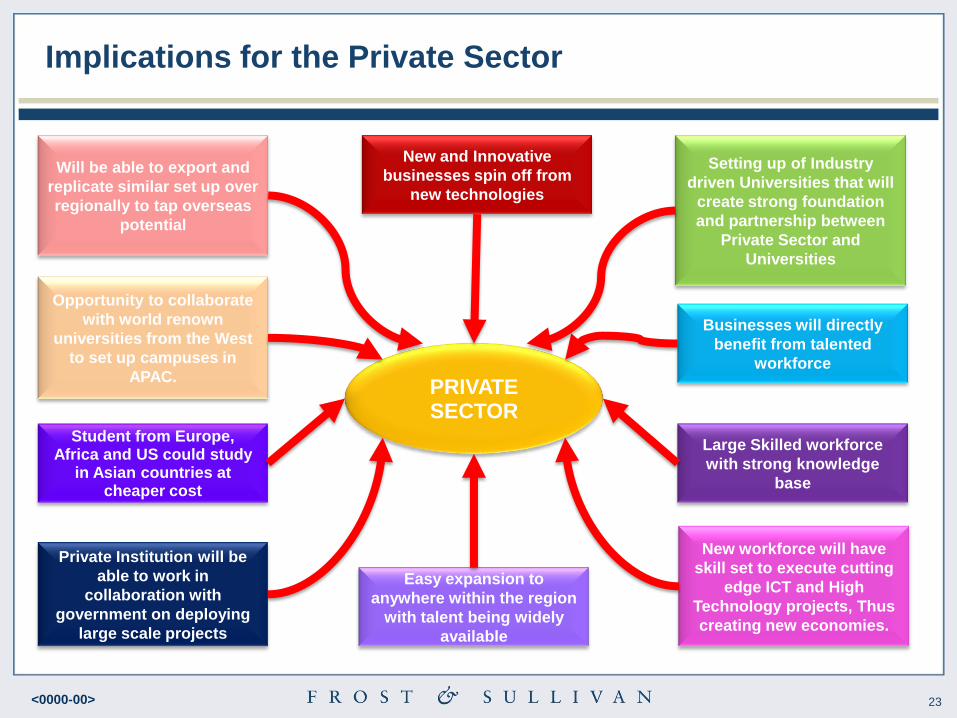

Implications for the Private Sector

PRIVATE SECTOR

Easy expansion to

anywhere within the region

with talent being widely

available

Businesses will directly

benefit from talented

workforce

Large Skilled workforce

with strong knowledge

base

Private Institution will be

able to work in

collaboration with

government on deploying

large scale projects

New workforce will have

skill set to execute cutting

edge ICT and High

Technology projects, Thus

creating new economies.

New and Innovative

businesses spin off from

new technologies

Student from Europe, Africa and US could study

in Asian countries at cheaper cost

Opportunity to collaborate

with world renown

universities from the West

to set up campuses in

APAC.

Setting up of Industry

driven Universities that will

create strong foundation

and partnership between

Private Sector and

Universities

Will be able to export and

replicate similar set up over

regionally to tap overseas

potential

24 <0000-00>

The Asia Pacific Mobile Broadband Revolution

Broadband internet connections will become

ubiquitous in Asia

25 <0000-00>

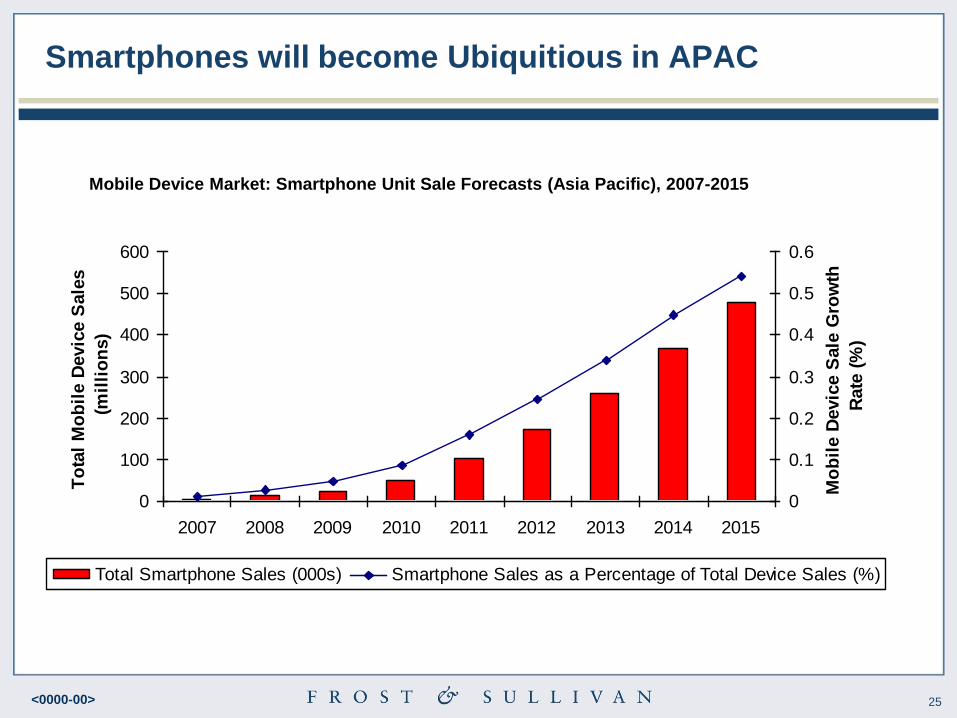

Smartphones will become Ubiquitious in APAC

0

100

200

300

400

500

600

2007 2008 2009 2010 2011 2012 2013 2014 2015

To

tal

Mo

bil

e D

evic

e S

ale

s

(mil

lio

ns)

0

0.1

0.2

0.3

0.4

0.5

0.6

Mo

bil

e D

evic

e S

ale

Gro

wth

Rate

(%

)

Total Smartphone Sales (000s) Smartphone Sales as a Percentage of Total Device Sales (%)

Mobile Device Market: Smartphone Unit Sale Forecasts (Asia Pacific), 2007-2015

26 <0000-00>

What are the implications of Mobile Broadband

Adoption?

• Smartphones are quickly becoming ubiquitous in the

region which is driving mobile Internet growth over

3G networks.

• Operators are also starting to offer prepaid mobile

Internet services in emerging markets and given that

over 80% of the region uses prepaid mobile access

this will allow more consumers to be connected.

• The region has already seen several LTE networks

deployed with many more planned over the coming

two years. These new 4G networks will offer

significantly faster browsing speeds.

• Faster networks in the region will enable new

services for operators such as mobile health, mobile

payments, machine-to-machine communications etc.

M-Health

Machine-to-Machine Communications

27 <0000-00>

Ageing and growing populations will drive a huge

increase in health expenditure in Asia

Huge Increase in Health Expenditure

28 <0000-00>

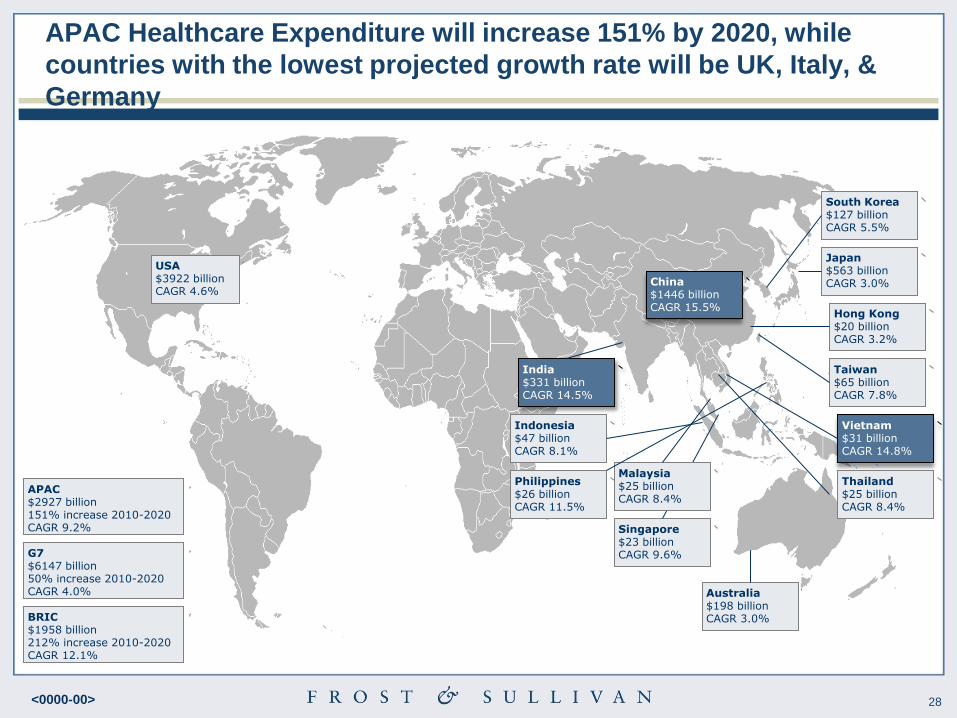

APAC Healthcare Expenditure will increase 151% by 2020, while

countries with the lowest projected growth rate will be UK, Italy, &

Germany

G7 $6147 billion 50% increase 2010-2020 CAGR 4.0%

APAC $2927 billion 151% increase 2010-2020 CAGR 9.2%

Australia $198 billion CAGR 3.0%

Japan $563 billion CAGR 3.0%

Hong Kong $20 billion CAGR 3.2%

South Korea $127 billion CAGR 5.5%

Singapore $23 billion CAGR 9.6%

Malaysia $25 billion CAGR 8.4%

Taiwan $65 billion CAGR 7.8%

India $331 billion CAGR 14.5%

China $1446 billion CAGR 15.5%

Indonesia $47 billion CAGR 8.1%

Vietnam $31 billion CAGR 14.8%

Philippines $26 billion CAGR 11.5%

Thailand $25 billion CAGR 8.4%

BRIC $1958 billion 212% increase 2010-2020 CAGR 12.1%

USA $3922 billion CAGR 4.6%

29 <0000-00>

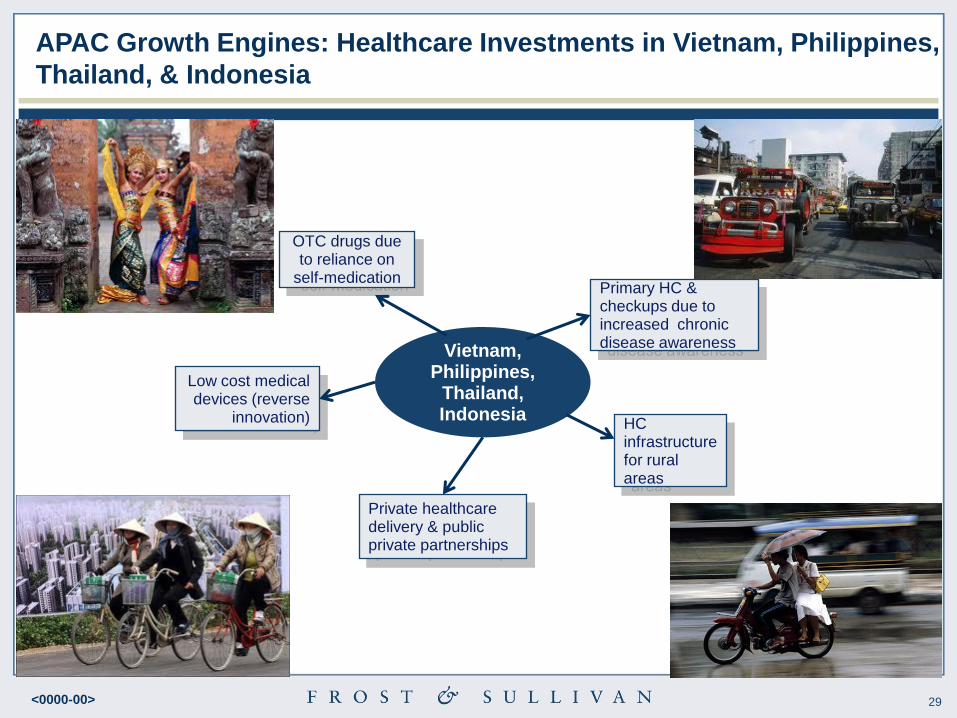

Vietnam, Philippines,

Thailand, Indonesia

Primary HC & checkups due to increased chronic disease awareness

OTC drugs due to reliance on

self-medication

HC infrastructure for rural areas

Low cost medical devices (reverse

innovation)

Private healthcare delivery & public private partnerships

APAC Growth Engines: Healthcare Investments in Vietnam, Philippines,

Thailand, & Indonesia

30 <0000-00>

Control Over Strategic Assets by China

The Chinese Government, either directly or through

SOEs, will increasingly seek to gain control over

strategic assets throughout Asia Pacific

31 <0000-00>

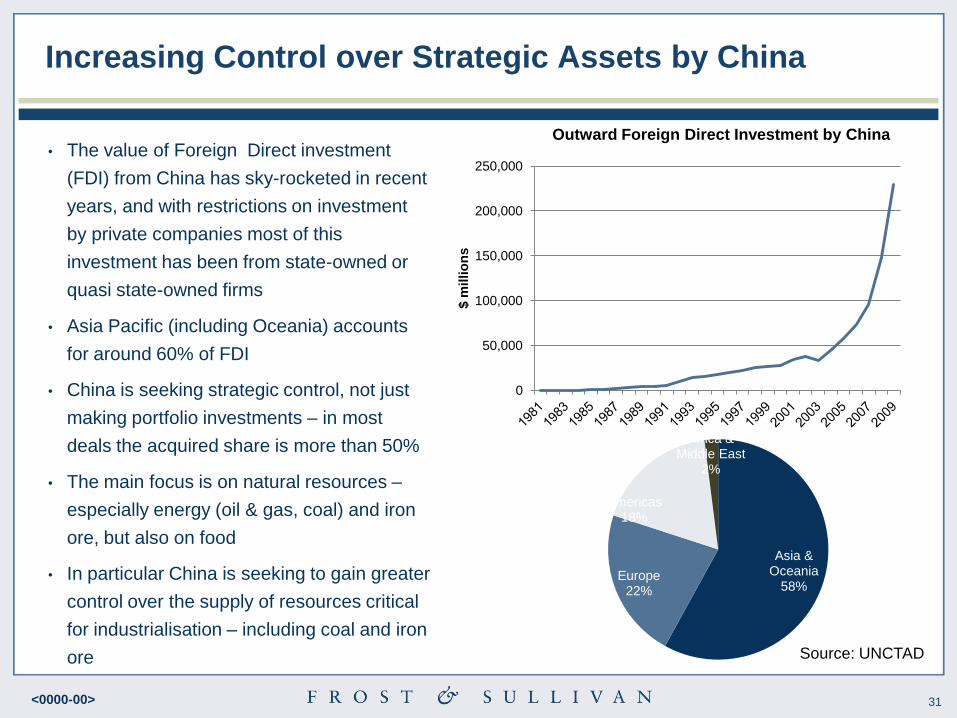

Increasing Control over Strategic Assets by China

• The value of Foreign Direct investment

(FDI) from China has sky-rocketed in recent

years, and with restrictions on investment

by private companies most of this

investment has been from state-owned or

quasi state-owned firms

• Asia Pacific (including Oceania) accounts

for around 60% of FDI

• China is seeking strategic control, not just

making portfolio investments – in most

deals the acquired share is more than 50%

• The main focus is on natural resources –

especially energy (oil & gas, coal) and iron

ore, but also on food

• In particular China is seeking to gain greater

control over the supply of resources critical

for industrialisation – including coal and iron

ore

0

50,000

100,000

150,000

200,000

250,000

$ m

illio

ns

Outward Foreign Direct Investment by China

Asia & Oceania

58% Europe

22%

Americas 18%

Africa & Middle East

2%

Source: UNCTAD

32 <0000-00>

What are the implications of Chinese control over

strategic assets?

• Increasing scrutiny of deals by Governments – in

response to political pressures at home,

governments are likely to closely scrutinise deals

and can be expected to reject some on ―national

interest‖ grounds

• As China gains more control over overseas assets

(mines, farms, etc) we can expect to see greater

sales of Chinese products and services required to

work the assets in Asia Pacific markets – such as

mining equipment, agricultural chemicals, steel tubes

for oilfield use, etc

• Much Chinese investment in resources involves

investment where the investor is also the buyer of

the resource, or is linked to the buyer of the resource

(iron ore, coal, etc). This is likely to have the effect of

stabilizing and perhaps moderating commodity price

increases

33 <0000-00>

Asia Pacific Leads Growth by Tapping New Wealth

Pockets In Renewables Energy Sectors Across

The Region

Huge Growth in Renewable Energy

34 <0000-00>

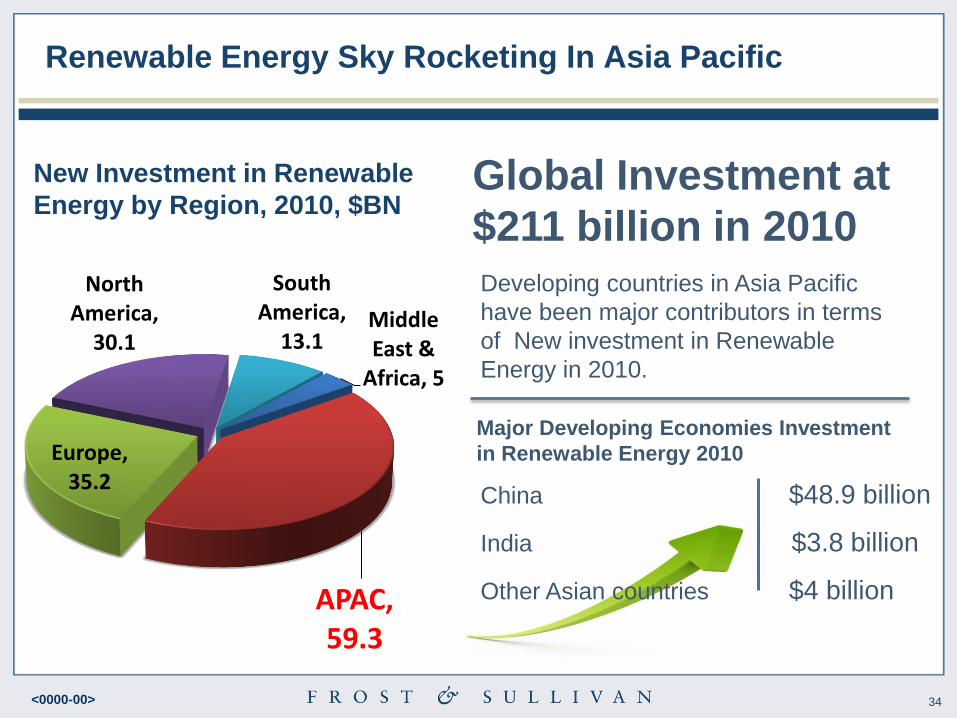

Middle East &

Africa, 5

APAC, 59.3

Europe, 35.2

North America,

30.1

South America,

13.1

Renewable Energy Sky Rocketing In Asia Pacific

Developing countries in Asia Pacific

have been major contributors in terms

of New investment in Renewable

Energy in 2010.

Global Investment at

$211 billion in 2010

Major Developing Economies Investment

in Renewable Energy 2010

China $48.9 billion

India $3.8 billion

Other Asian countries $4 billion

New Investment in Renewable

Energy by Region, 2010, $BN

35 <0000-00>

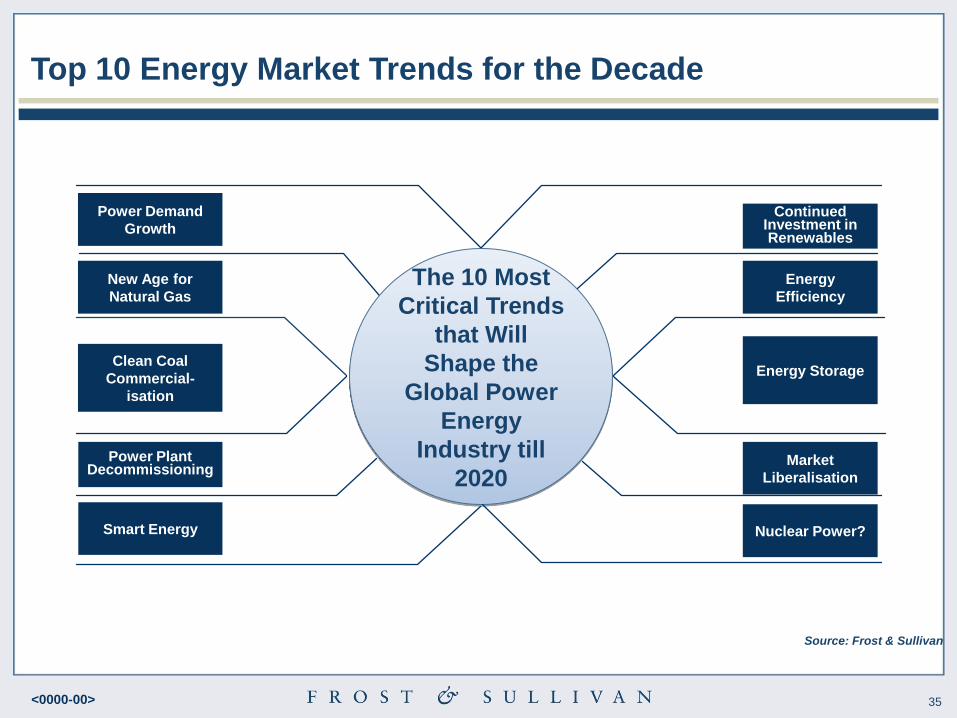

The 10 Most

Critical Trends

that Will

Shape the

Global Power

Energy

Industry till

2020

Source: Frost & Sullivan

Power Demand

Growth

New Age for

Natural Gas

Clean Coal

Commercial-

isation

Power Plant Decommissioning

Smart Energy Nuclear Power?

Energy

Efficiency

Energy Storage

Continued Investment in Renewables

Market

Liberalisation

Annual Power and Energy Outlook

Top 10 Energy Market Trends for the Decade

36 <0000-00>

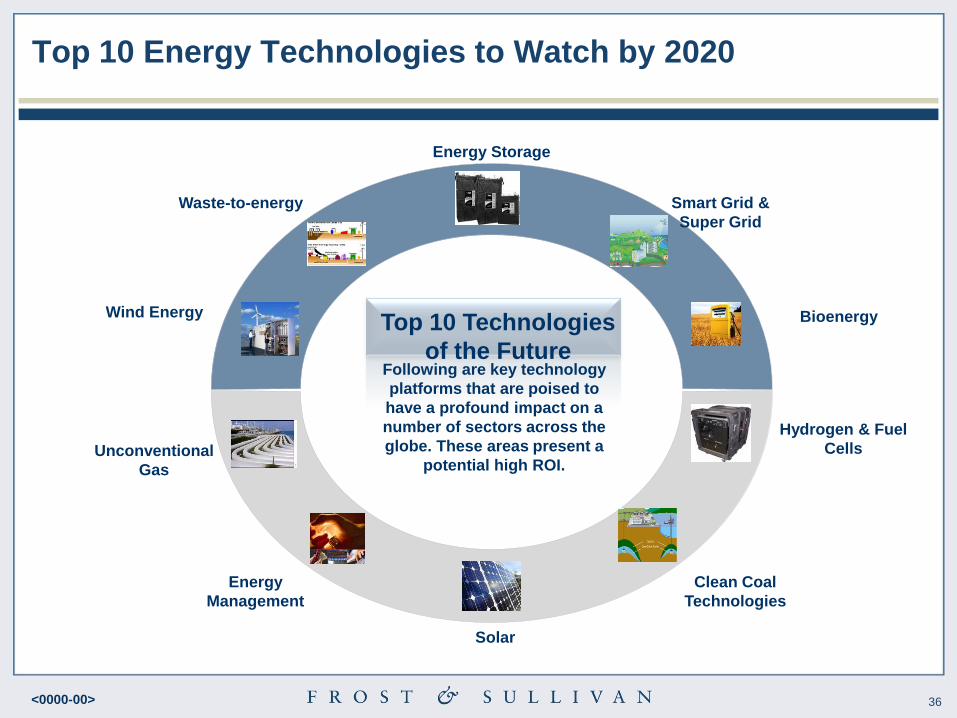

Top 10 Energy Technologies to Watch by 2020

Wind Energy

Waste-to-energy

Energy Storage

Smart Grid &

Super Grid

Bioenergy

Hydrogen & Fuel

Cells Unconventional

Gas

Energy

Management

Solar

Clean Coal

Technologies

Top 10 Technologies

of the Future Following are key technology

platforms that are poised to

have a profound impact on a

number of sectors across the

globe. These areas present a

potential high ROI.

37 <0000-00>

Key Strategic Conclusions

1. Mega trends are connected and inter-wined which suggests ―synergetic‖

opportunities between them

2. It is important to understand the eco-system of the mega-trend and the

elements of the value chain which have most profitability

3. All these trends are global and have global ramifications thereby offering

scalable opportunities

4. These forces are changing rapidly and bringing new competencies into play

at half the life-cycle speed of the past decade

5. Organisations’ need ―Mega Trend‖ champions and teams within their

organisation structure to best exploit the opportunity