from risk assessment to analyzing data - key fraud tools to use

TRANSCRIPT

From Risk Assessment to Analyzing Data – Key

Fraud Tools to UseSouthern AZ IIA/AGA Joint Meeting

February 8, 2017

Karin M. Smith, MBA, SFO, CFE

Refresher – The Fraud Triangle

2

Fraud Risk Assessments

Fraud Risk Assessment

Employee

Physical Controls

SkimmingCheck

Tampering

Purchasing and Billing

Payroll Expenses

Conflict of Interest

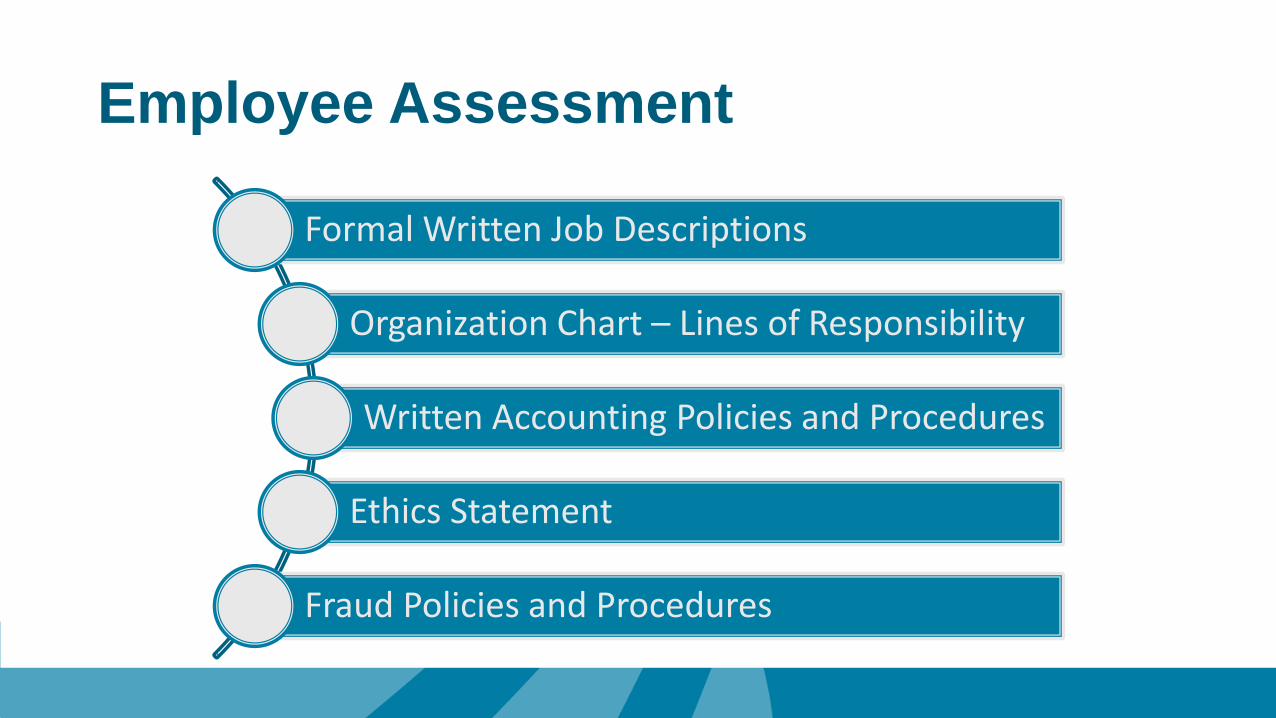

Employee Assessment

Formal Written Job Descriptions

Organization Chart – Lines of Responsibility

Written Accounting Policies and Procedures

Ethics Statement

Fraud Policies and Procedures

Physical Controls Assessment

Restrict Access

Video Recording

Random Audits

Background Checks

Investigate Accusations

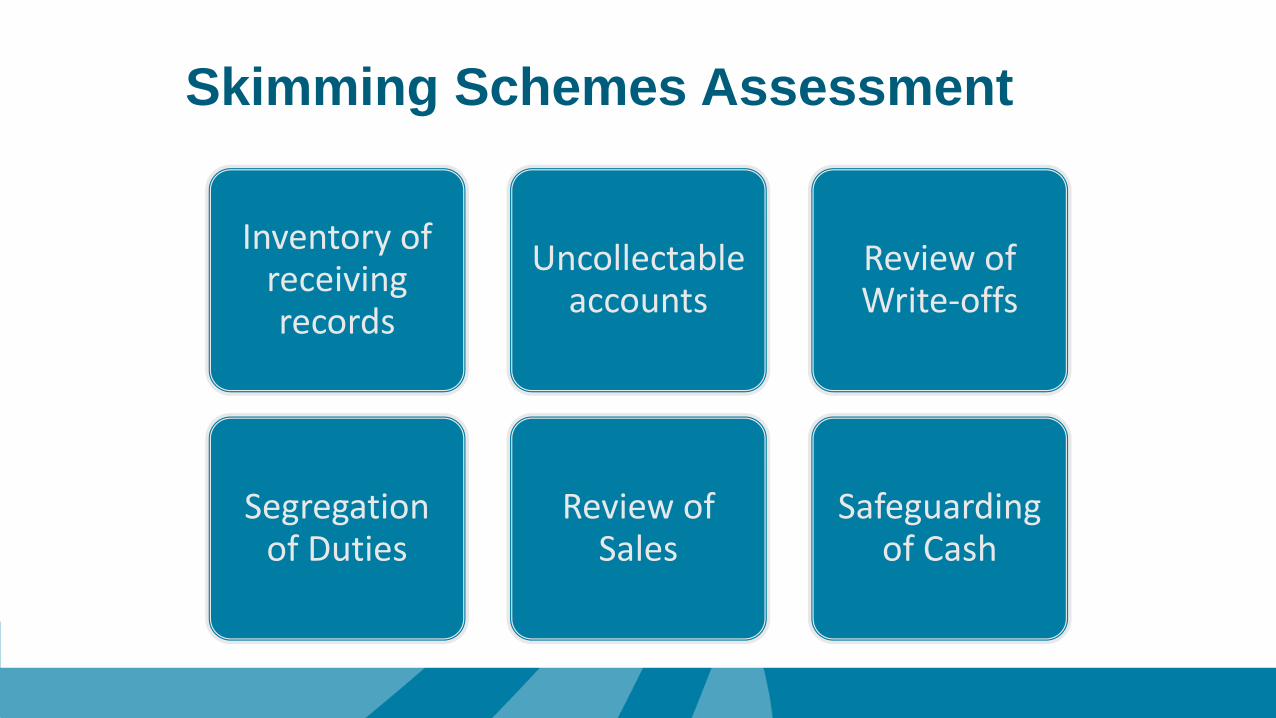

Skimming Schemes Assessment

Inventory of receiving records

Segregation of Duties

Uncollectable accounts

Review of Sales

Review of Write-offs

Safeguarding of Cash

Check Tampering Assessment

Unused Checks

Positive Pay

Check SignersBank

Reconciliations

Voided and Missing Checks

Purchasing and Billing Assessment

Organizational Structure

Vendor Information

ProcurementReceiving Reports

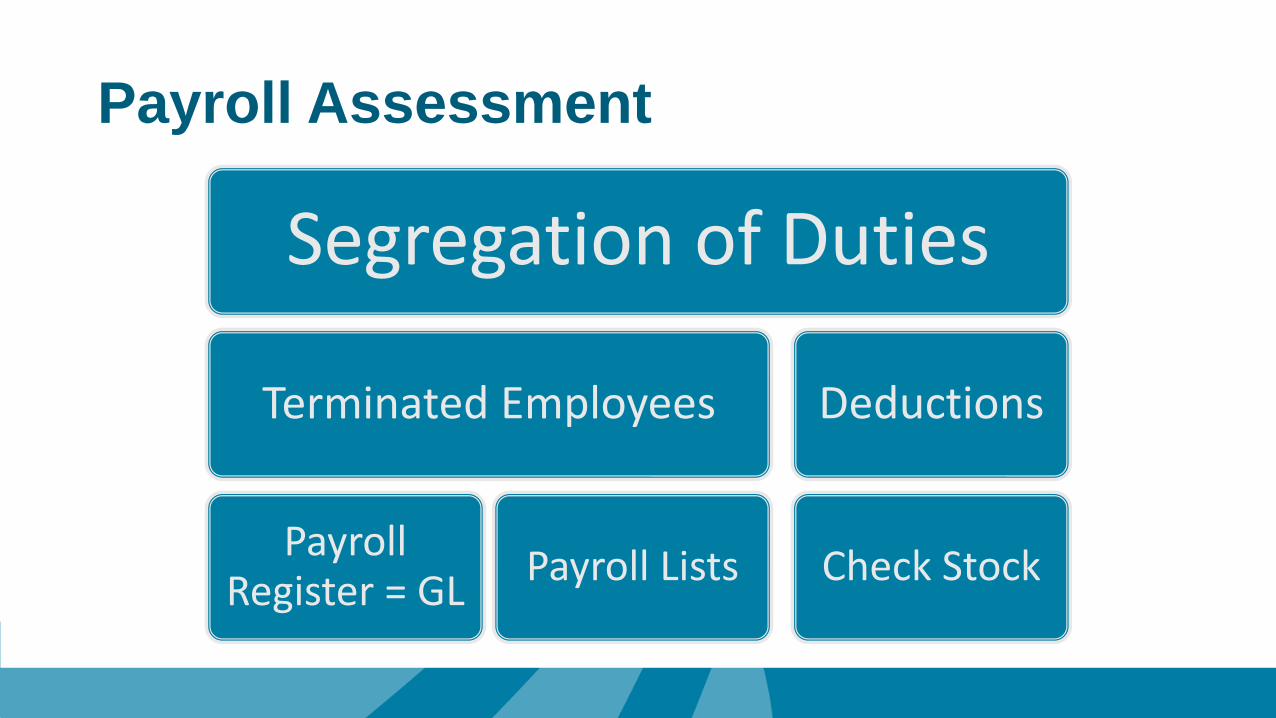

Payroll Assessment

Segregation of Duties

Terminated Employees

Payroll Register = GL

Payroll Lists

Deductions

Check Stock

Expenses Assessment

Expense Accounts

Employee Reimbursements

Receipts

Review

Conflict of Interest Assessment

Vendor vs Employee

Prior Employees

Disclosure

Vendor Agreement

Vendor Audits

Analyzing Data

Why Perform Data Analysis?

Convert the 7% By Accident to Not By Accident

Find It On Your Terms Not Someone Else's

All organizations should perform

comprehensive Data Analysis!

Why Perform Data Analysis?

Do you sign the year-end representation letter to the external auditors?

Key representations:

• Responsible for internal control environment

• No known significant deficiencies in the design of or operation of internal controls

• Acknowledge responsibility for the design and

implementation of programs and controls to prevent and detect fraud

• No known material instances of fraud

Fiduciary responsibility as a member of the executive management team

Why Perform Data Analysis?

Prevent Fraud

Prevent Misuse

Detect Errors

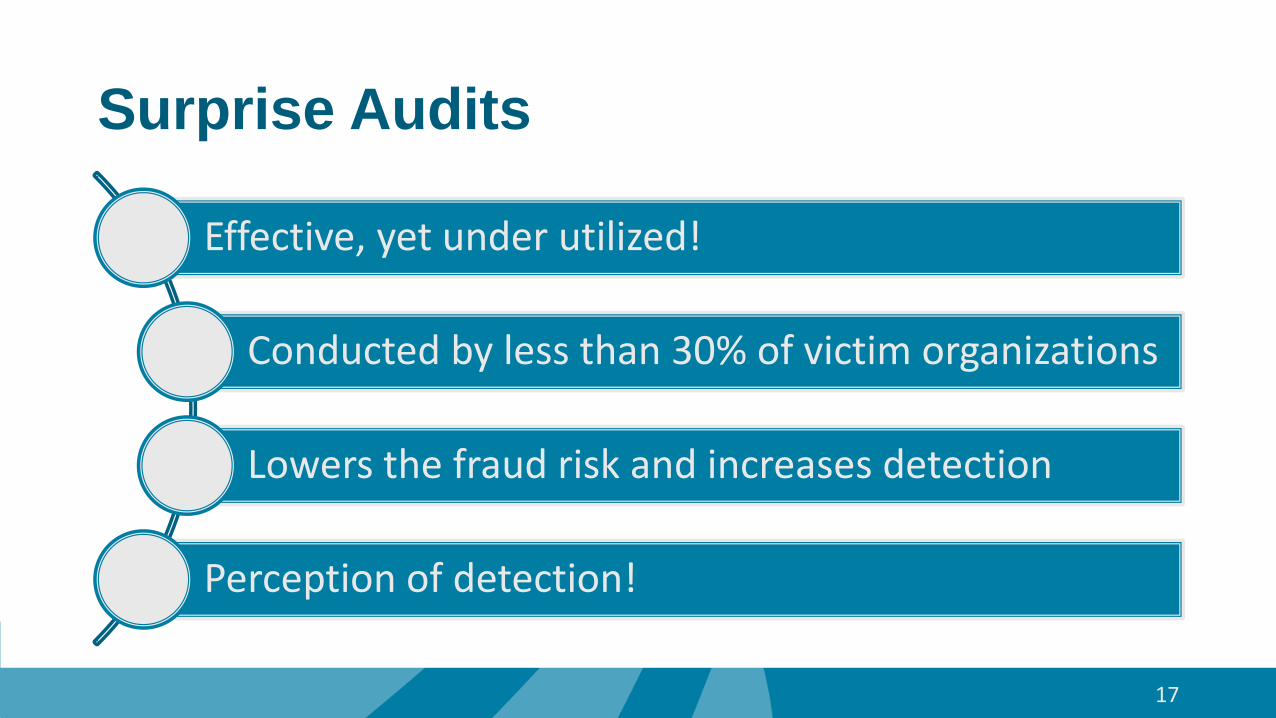

Surprise Audits

Effective, yet under utilized!

Conducted by less than 30% of victim organizations

Lowers the fraud risk and increases detection

Perception of detection!

17

Purchasing & Payables

Payroll

General Ledger

18

Attention Areas

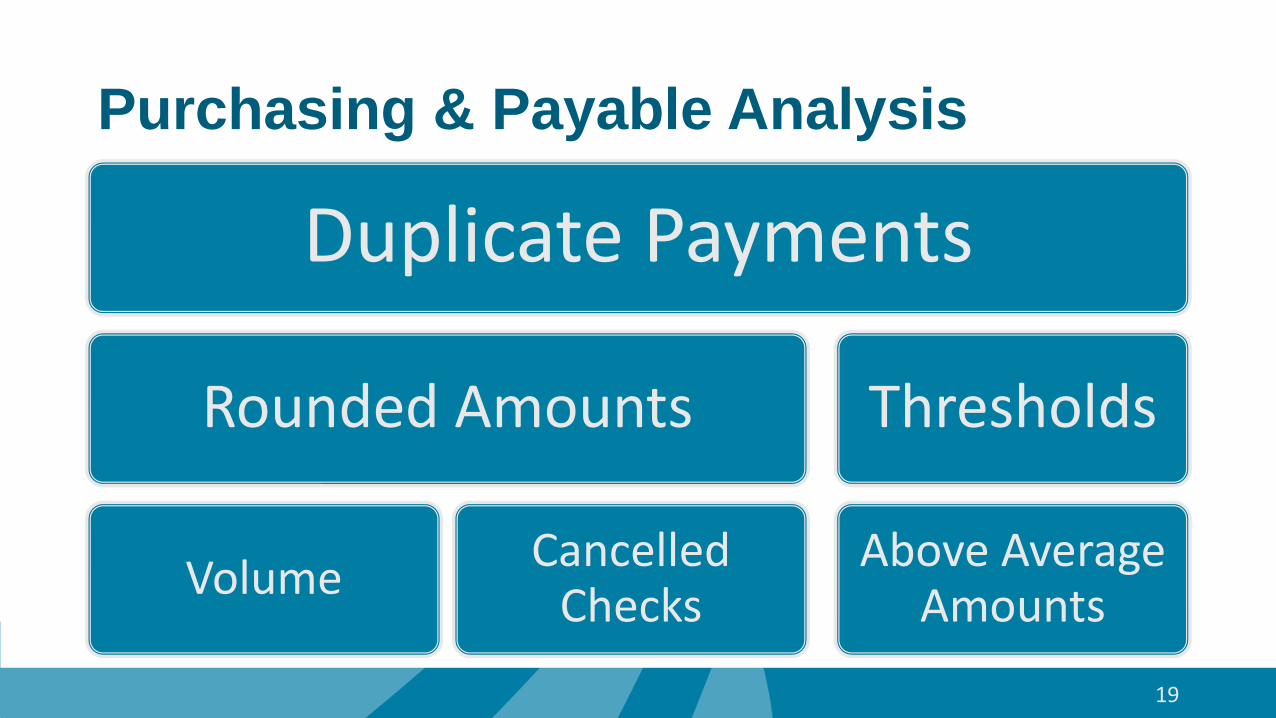

Purchasing & Payable Analysis

Duplicate Payments

Rounded Amounts

VolumeCancelled

Checks

Thresholds

Above Average Amounts

19

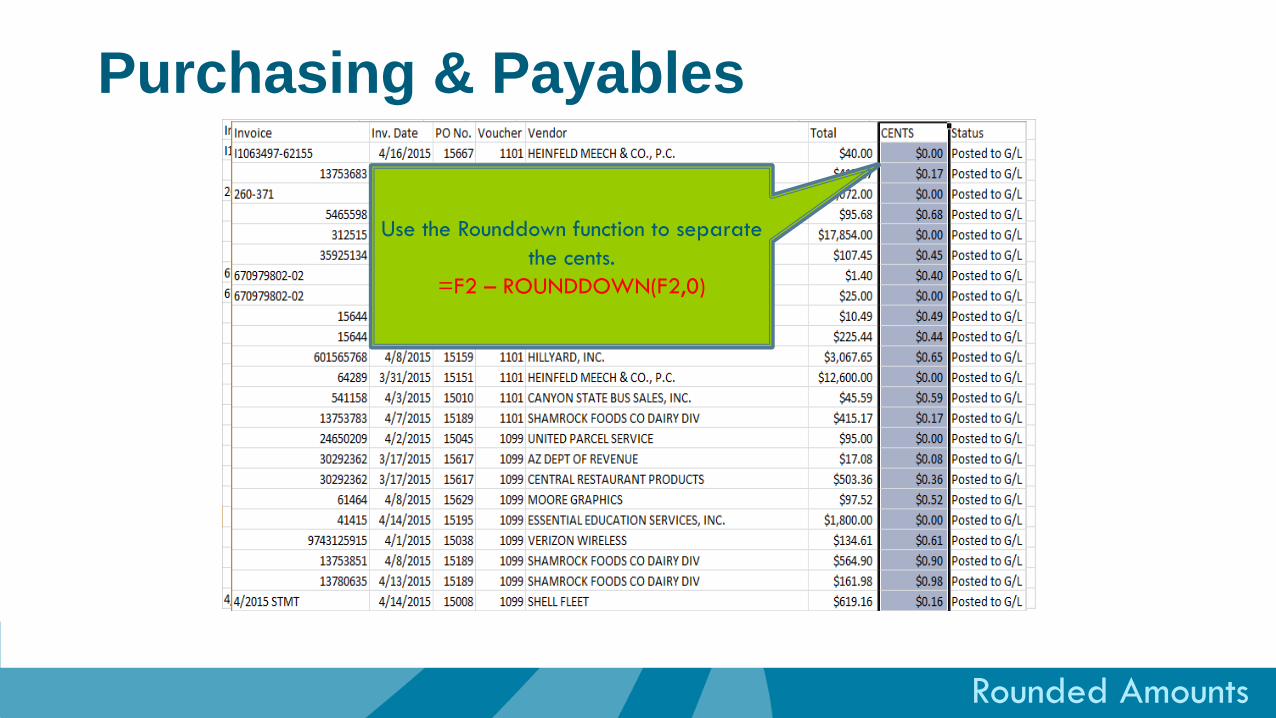

Rounded Amounts

Use the Rounddown function to separate

the cents.

=F2 – ROUNDDOWN(F2,0)

Purchasing & Payables

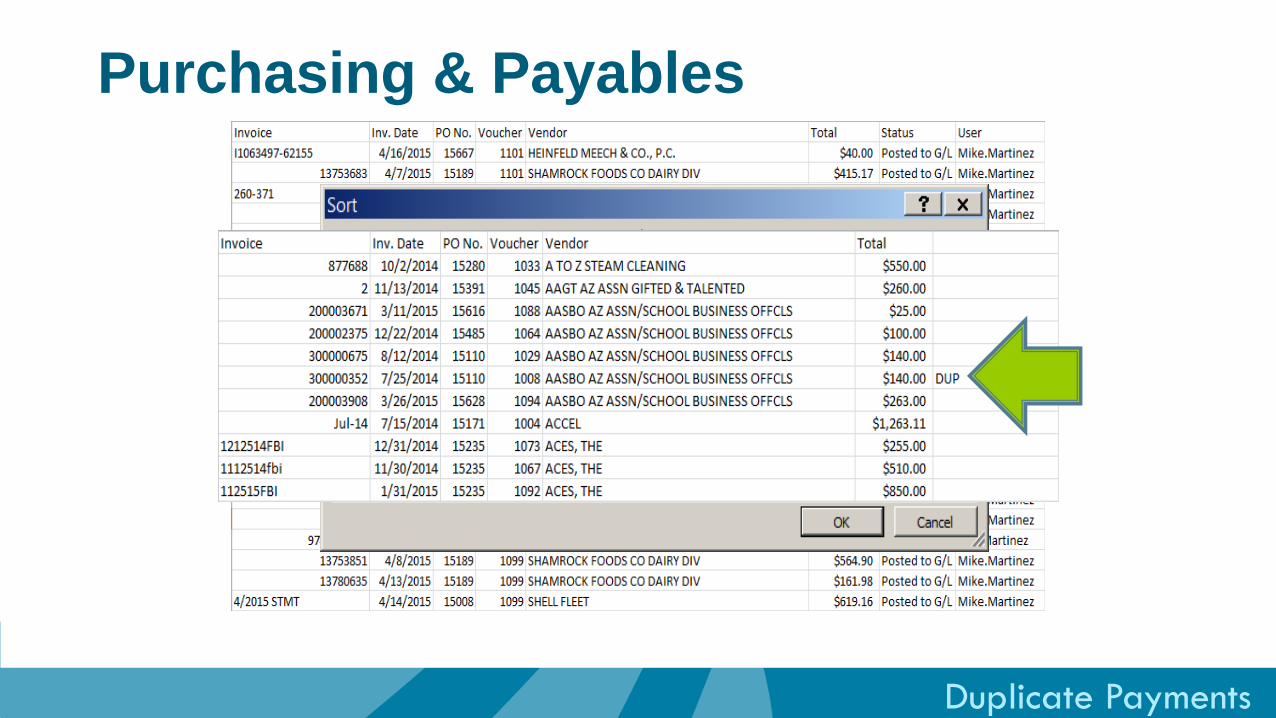

Duplicate Payments

Use the IF function to look for duplicates.

=IF(F2=F1,”DUP”,””)

Purchasing & Payables

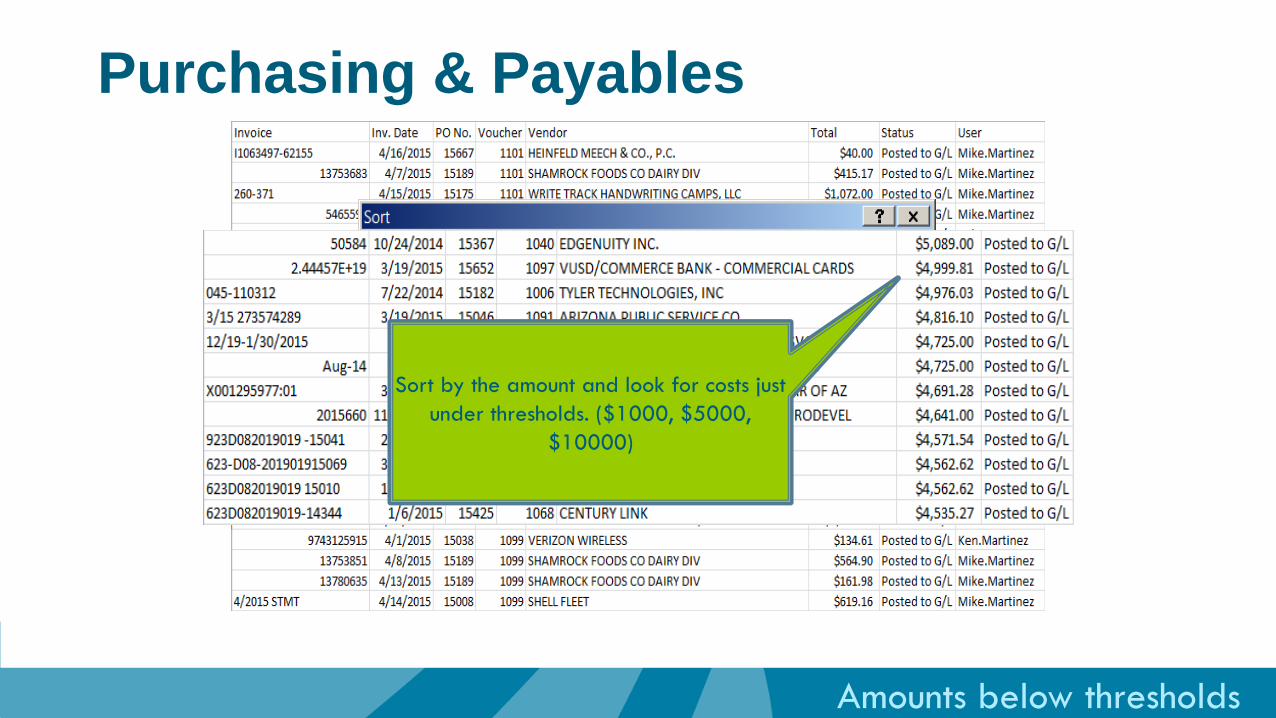

Amounts below thresholds

Sort by the amount and look for costs just

under thresholds. ($1000, $5000,

$10000)

Purchasing & Payables

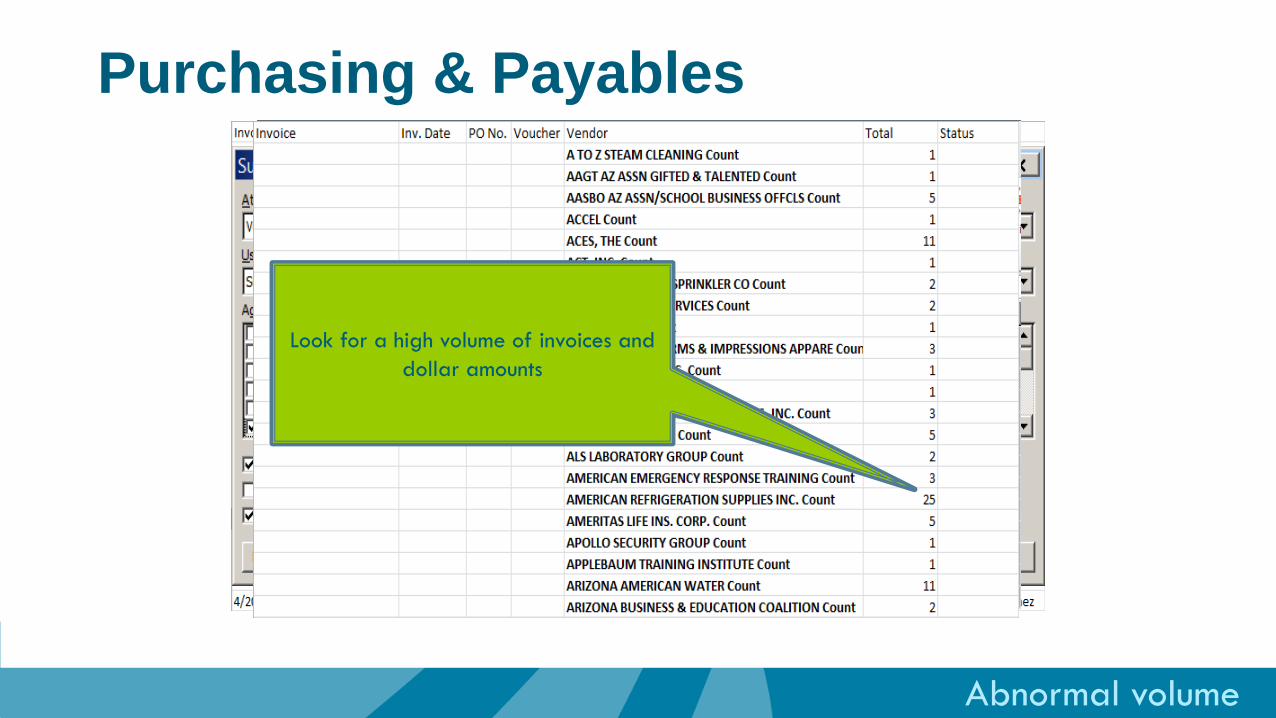

Abnormal volume

Use these options to roll up amounts

Look for a high volume of invoices and

dollar amounts

Purchasing & Payables

Purchasing & Payables

Employees as Vendors

Payment without a PO

Separation of Duties

User Roles

24

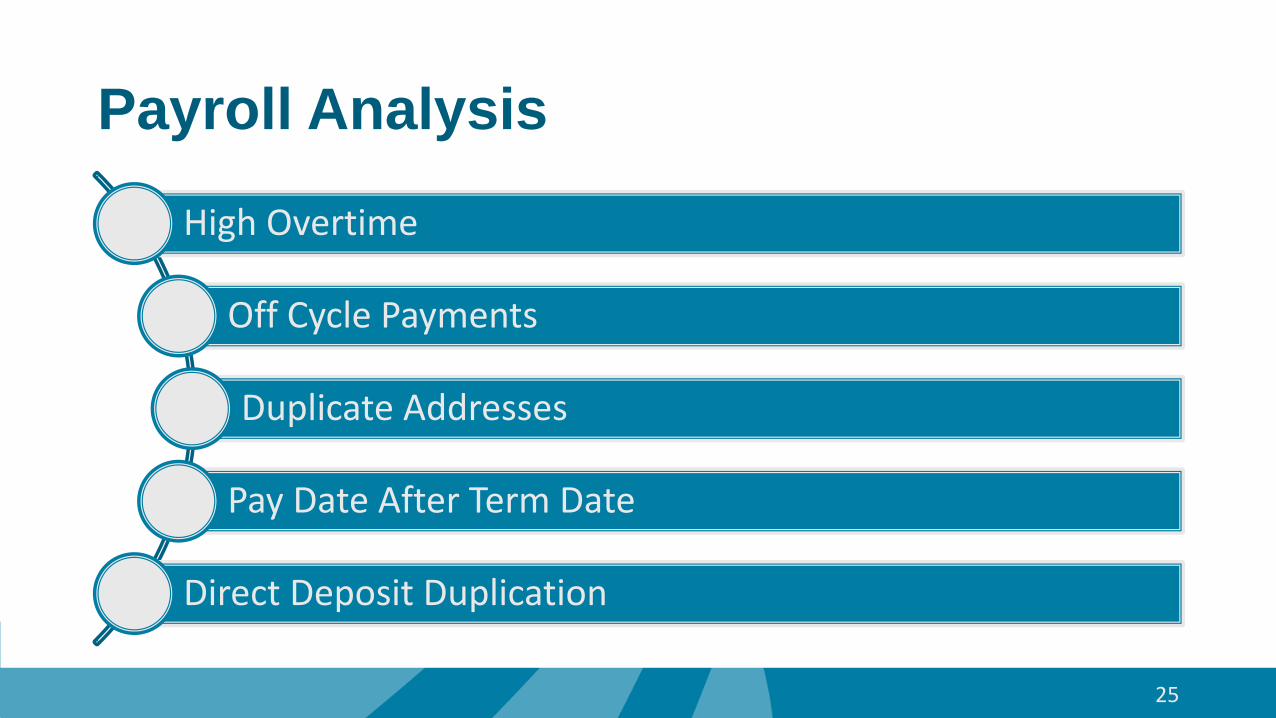

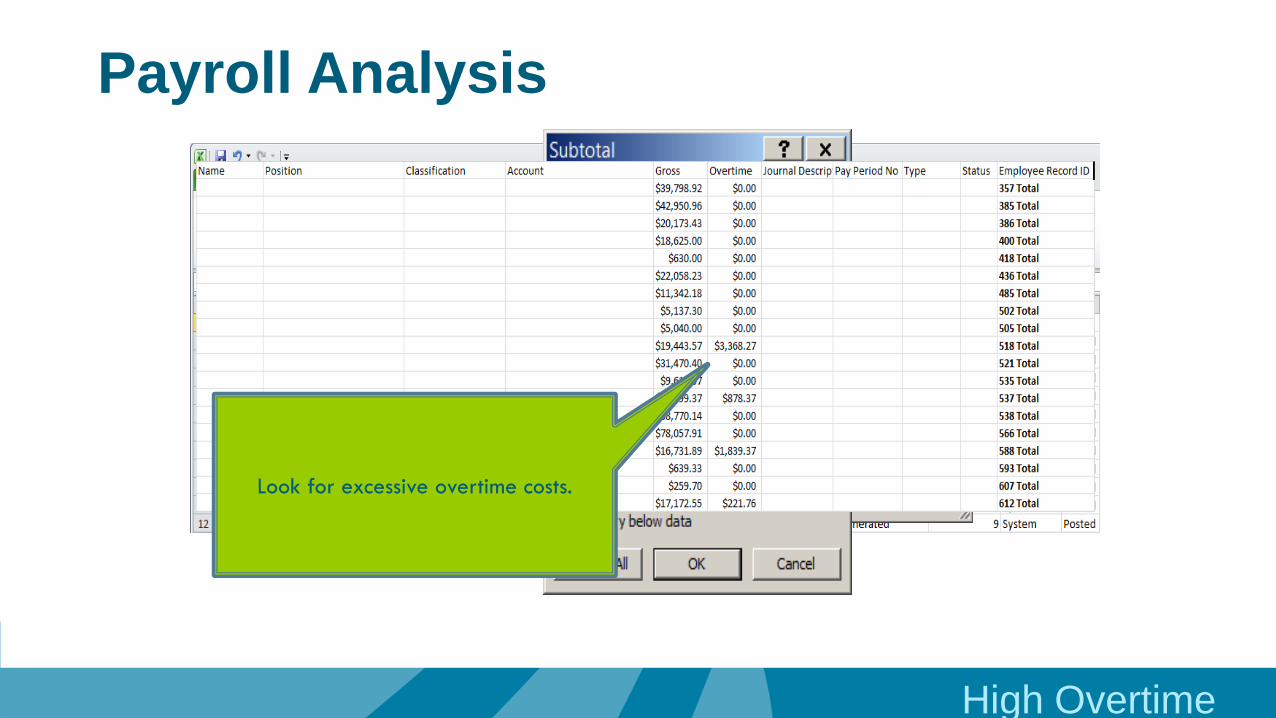

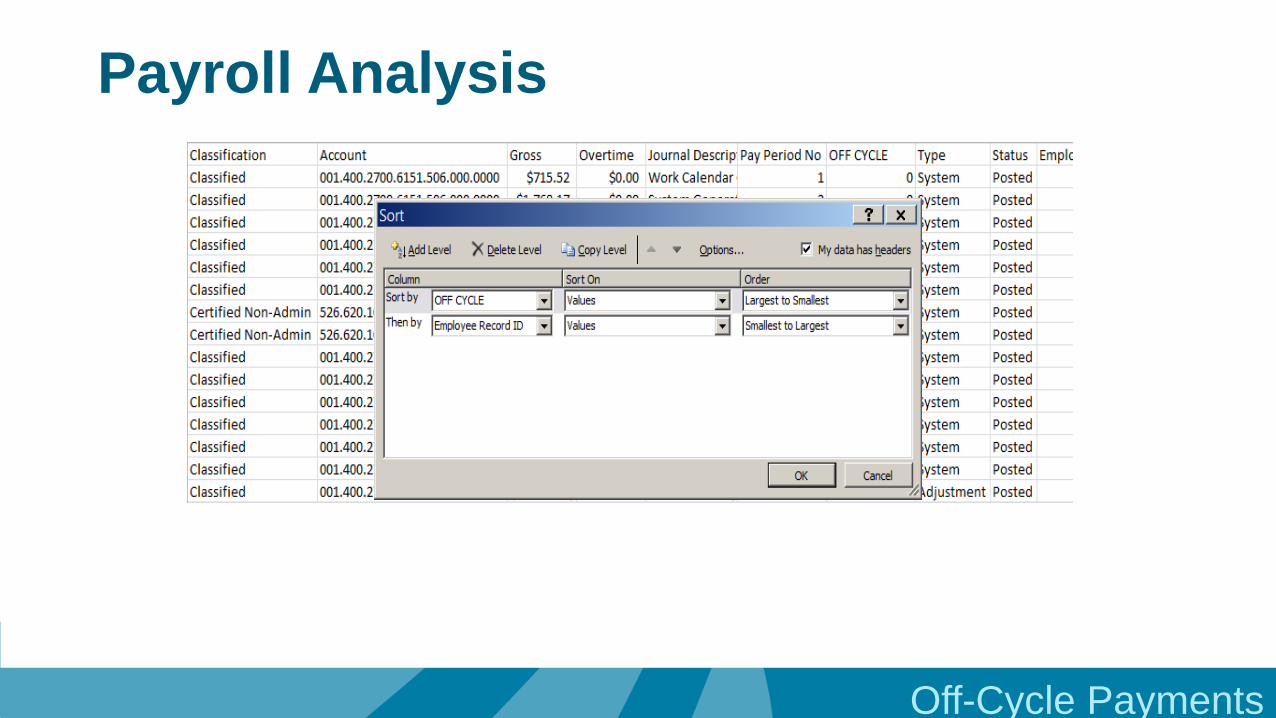

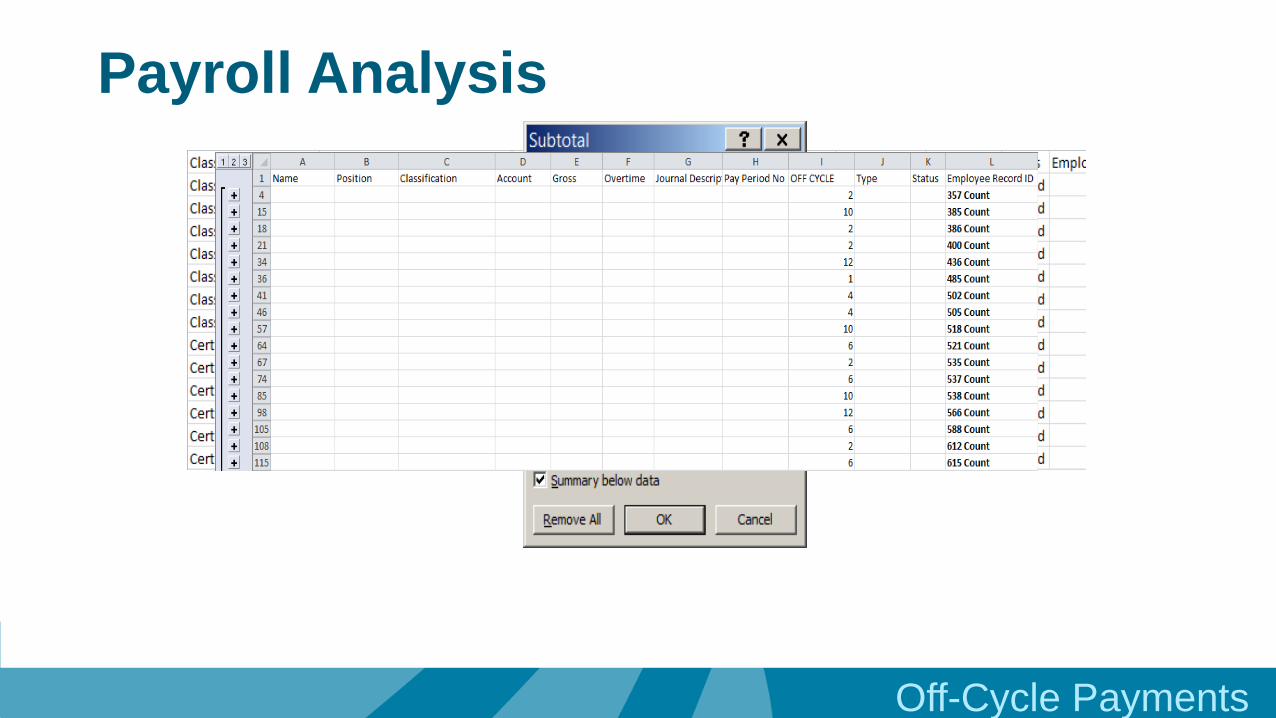

Payroll Analysis

High Overtime

Off Cycle Payments

Duplicate Addresses

Pay Date After Term Date

Direct Deposit Duplication

25

High Overtime

Look for excessive overtime costs.

Payroll Analysis

Off-Cycle Payments

Payroll Analysis

Off-Cycle Payments

Payroll Analysis

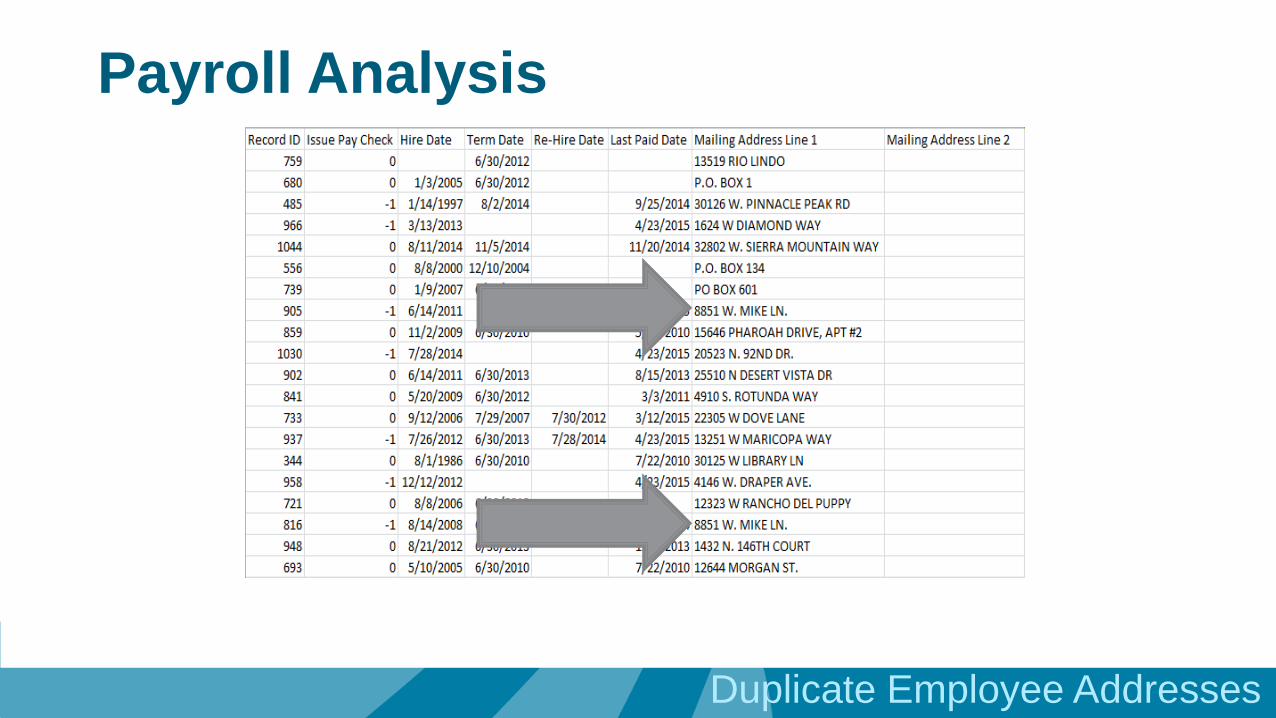

Duplicate Employee Addresses

Payroll Analysis

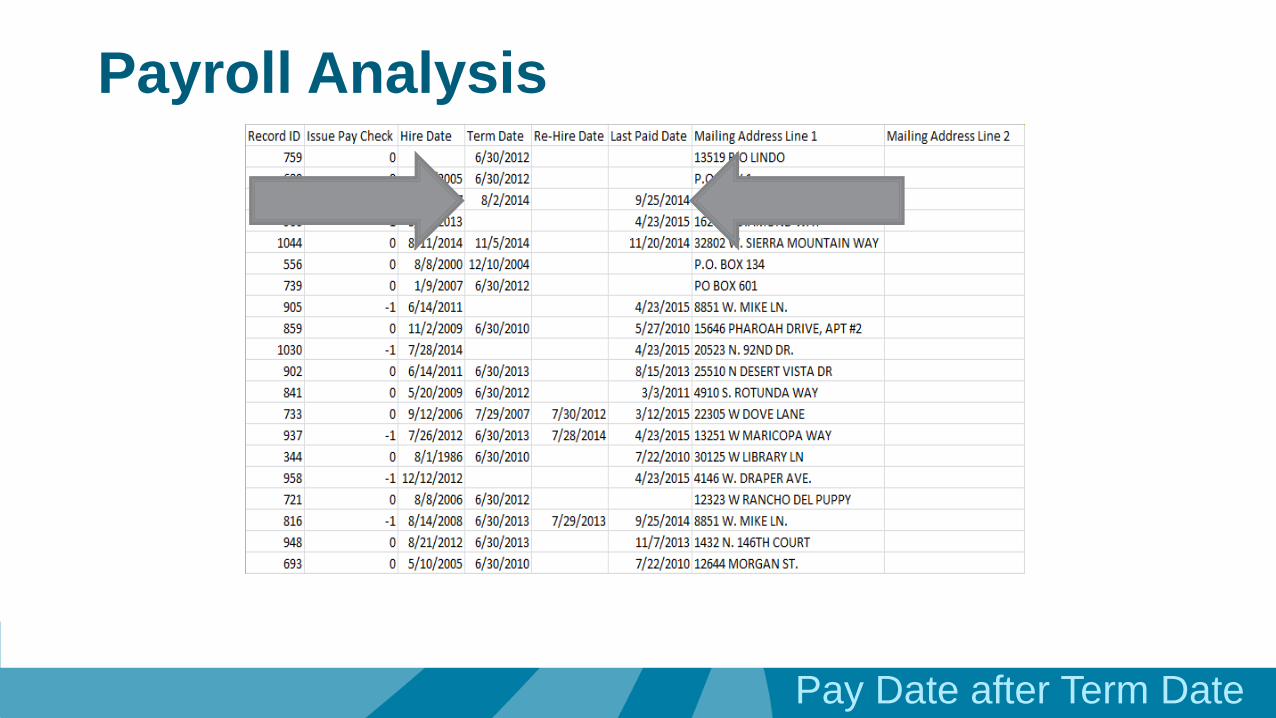

Pay Date after Term Date

Payroll Analysis

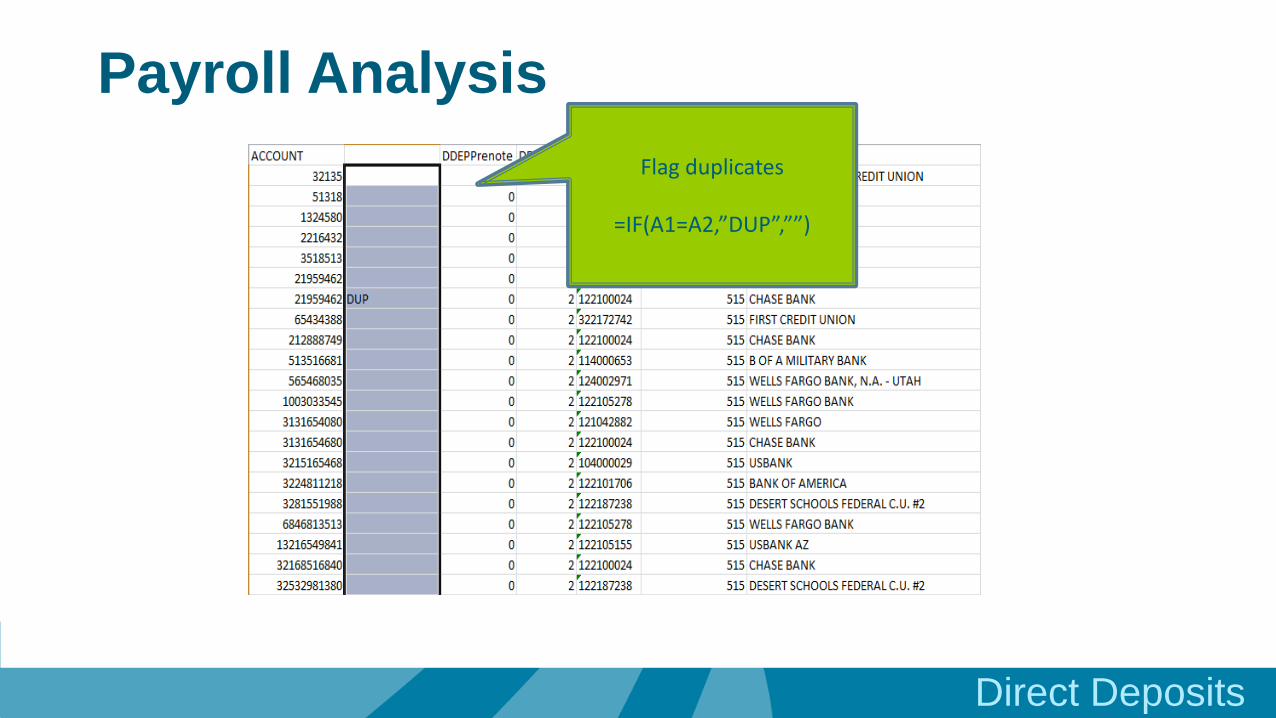

Direct Deposits

Flag duplicates

=IF(A1=A2,”DUP”,””)

Payroll Analysis

General Ledger Analysis

JE by Type

JE by User

JE by Month

32

JOURNAL USER Lines DEBIT_SUM CREDIT_SUM

Accounts Payable BWayne 10803 5,093,232.97 (5,086,485.10)Adjusting BWayne 14 4,079,311.89 (4,079,311.89)Deposits BWayne 1160 12,130,618.21 (12,130,618.21)Payroll BWayne 656 473,066.21 (473,066.21)Adjusting PParker 473 61,801.20 (61,801.20)Payroll PParker 3529 1,467,280.28 (1,467,280.28)Adjusting BBanner 40 11,851.86 (11,851.86)

Adjusting SRogers 7674 3,633,438.51 (3,633,438.51)Warehouse DLance 54 9,755.64 (9,755.64)

Adjusting MMurdock 218 488,395.54 (488,395.54)

Warehouse JHowlett 43 6,253.20 (6,253.20)

Adjusting DPrince 2370 16,652,036.65 (16,652,036.65)Adjusting JStorm 81 9,531.77 (9,531.77)Payroll JStorm 34760 17,550,658.85 (17,550,658.85)Accounts Payable CKent 3630 2,396,549.96 (2,396,549.96)

Adjusting BGrimm 24 3,321.76 (3,321.76)Adjusting TStark 6 2,092,940.91 (2,092,940.91)

Is it strange that TStark made so few adjusting entries totaling so much?

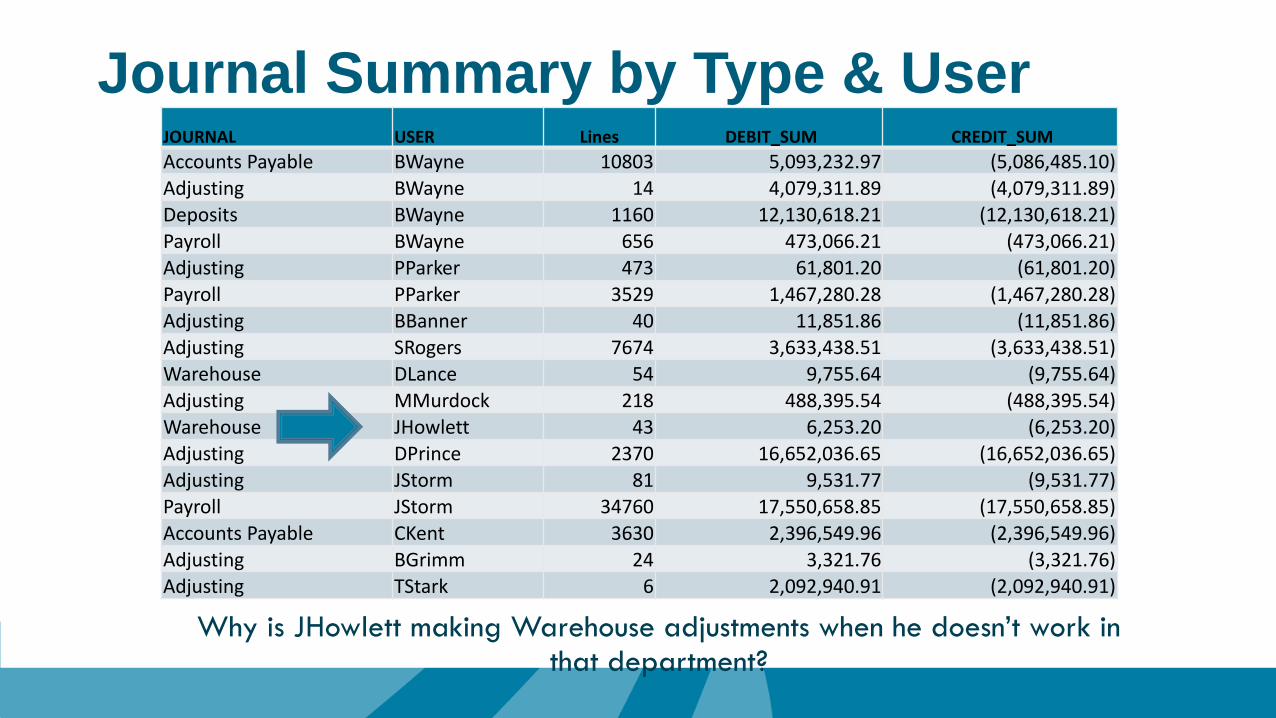

Journal Summary by Type & User

JOURNAL USER Lines DEBIT_SUM CREDIT_SUM

Accounts Payable BWayne 10803 5,093,232.97 (5,086,485.10)Adjusting BWayne 14 4,079,311.89 (4,079,311.89)Deposits BWayne 1160 12,130,618.21 (12,130,618.21)Payroll BWayne 656 473,066.21 (473,066.21)Adjusting PParker 473 61,801.20 (61,801.20)Payroll PParker 3529 1,467,280.28 (1,467,280.28)Adjusting BBanner 40 11,851.86 (11,851.86)

Adjusting SRogers 7674 3,633,438.51 (3,633,438.51)Warehouse DLance 54 9,755.64 (9,755.64)

Adjusting MMurdock 218 488,395.54 (488,395.54)

Warehouse JHowlett 43 6,253.20 (6,253.20)

Adjusting DPrince 2370 16,652,036.65 (16,652,036.65)Adjusting JStorm 81 9,531.77 (9,531.77)Payroll JStorm 34760 17,550,658.85 (17,550,658.85)Accounts Payable CKent 3630 2,396,549.96 (2,396,549.96)

Adjusting BGrimm 24 3,321.76 (3,321.76)Adjusting TStark 6 2,092,940.91 (2,092,940.91)

Why is JHowlett making Warehouse adjustments when he doesn’t work in that department?

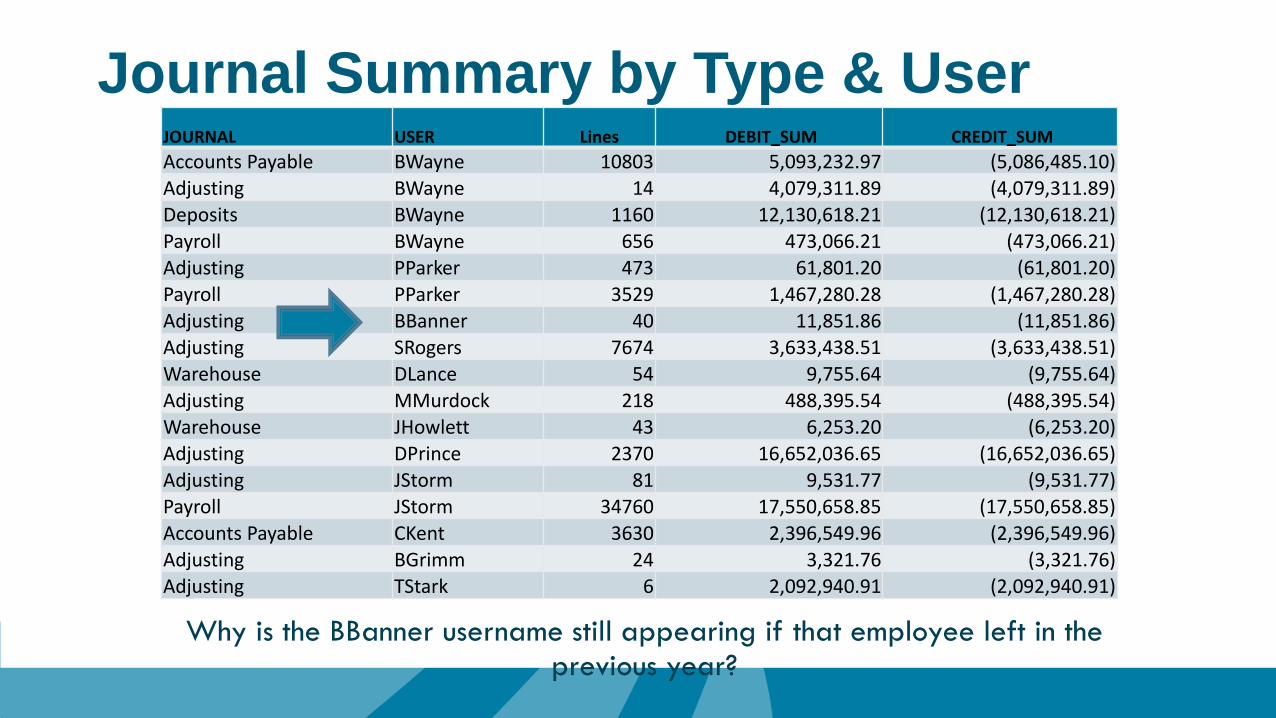

Journal Summary by Type & User

JOURNAL USER Lines DEBIT_SUM CREDIT_SUM

Accounts Payable BWayne 10803 5,093,232.97 (5,086,485.10)Adjusting BWayne 14 4,079,311.89 (4,079,311.89)Deposits BWayne 1160 12,130,618.21 (12,130,618.21)Payroll BWayne 656 473,066.21 (473,066.21)Adjusting PParker 473 61,801.20 (61,801.20)Payroll PParker 3529 1,467,280.28 (1,467,280.28)Adjusting BBanner 40 11,851.86 (11,851.86)

Adjusting SRogers 7674 3,633,438.51 (3,633,438.51)Warehouse DLance 54 9,755.64 (9,755.64)

Adjusting MMurdock 218 488,395.54 (488,395.54)

Warehouse JHowlett 43 6,253.20 (6,253.20)

Adjusting DPrince 2370 16,652,036.65 (16,652,036.65)Adjusting JStorm 81 9,531.77 (9,531.77)Payroll JStorm 34760 17,550,658.85 (17,550,658.85)Accounts Payable CKent 3630 2,396,549.96 (2,396,549.96)

Adjusting BGrimm 24 3,321.76 (3,321.76)Adjusting TStark 6 2,092,940.91 (2,092,940.91)

Why is the BBanner username still appearing if that employee left in the previous year?

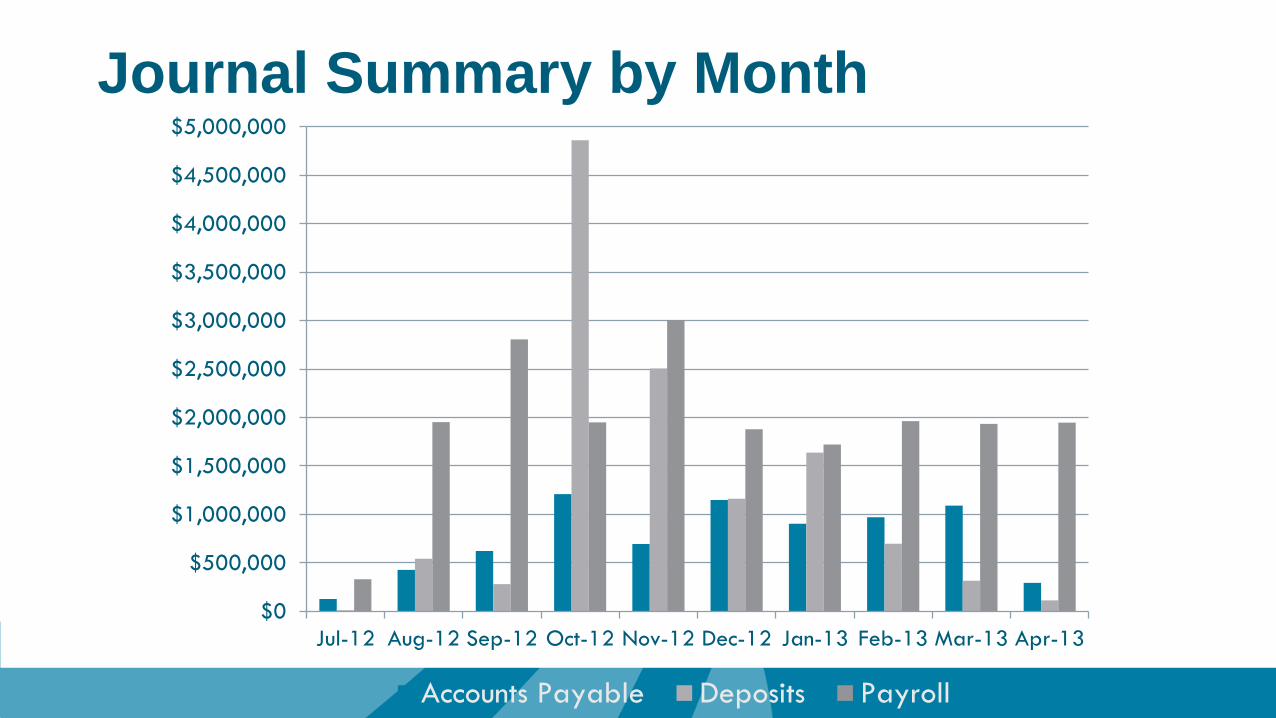

Journal Summary by Type & User

$0

$500,000

$1,000,000

$1,500,000

$2,000,000

$2,500,000

$3,000,000

$3,500,000

$4,000,000

$4,500,000

$5,000,000

Jul-12 Aug-12 Sep-12 Oct-12 Nov-12 Dec-12 Jan-13 Feb-13 Mar-13 Apr-13

Accounts Payable Deposits Payroll

Journal Summary by Month