fringe benefits examples of fringes cash non-cash automobiles awards,prizes cellular phones...

TRANSCRIPT

FRINGEFRINGE BENEFITS BENEFITS

Examples of Fringes

CASH NON-CASH

• AUTOMOBILES• AWARDS,PRIZES • CELLULAR PHONES• EDUCATIONAL

REIMUBURSEMENTS• SAVINGS BONDS• ALLOWANCES• MEAL MONEY

(BASED ON HOURS WORKED)

• GROUP TERM LIFE• MOVING EXPENSES• PARKING• ER PROVIDED

LIVING QUARTERS• CLOTHING OTHER

THAN CERTAIN UNIFORMS

• SPOUSAL TRAVEL• SEASON TICKETS

EXAMPLES OF EXCLUDED FRINGES

• Accident and health plans

• achievement awards

• athletic facilities• de minims fringes• dependent care

asst. programs• educational assist• employee discounts

• Group-term life• lodging on

employer’s premises

• moving expenses reimbursements

• no-additional cost services

• tuition reduction• working condition

fringes

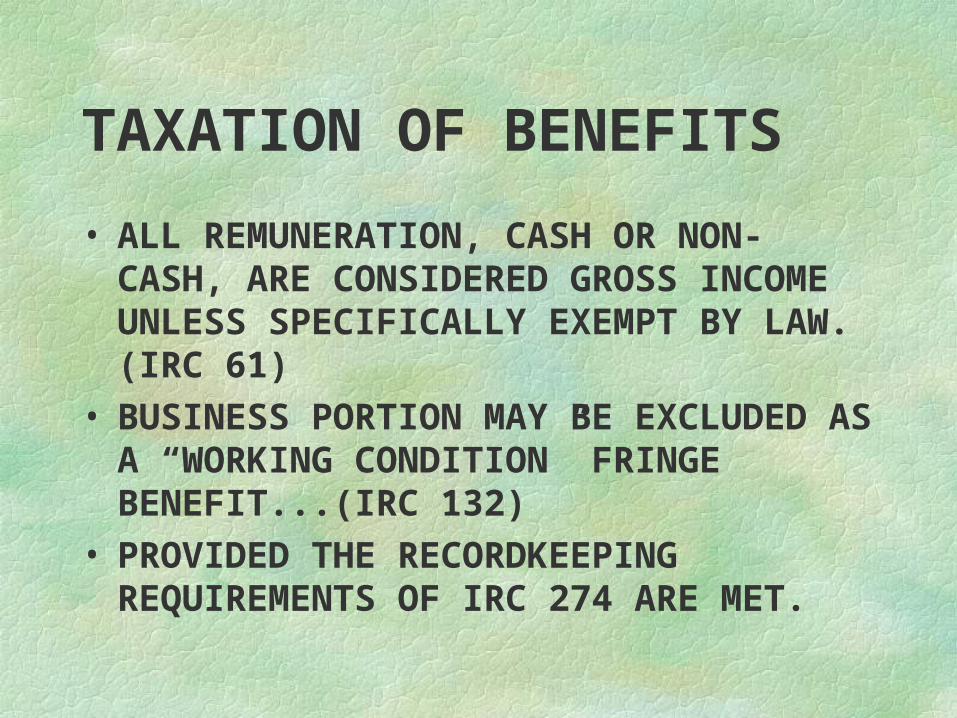

TAXATION OF BENEFITS

• ALL REMUNERATION, CASH OR NON- CASH, ARE CONSIDERED GROSS INCOME UNLESS SPECIFICALLY EXEMPT BY LAW. (IRC 61)

• BUSINESS PORTION MAY BE EXCLUDED AS A “WORKING CONDITION” FRINGE BENEFIT...(IRC 132)

• PROVIDED THE RECORDKEEPING REQUIREMENTS OF IRC 274 ARE MET.

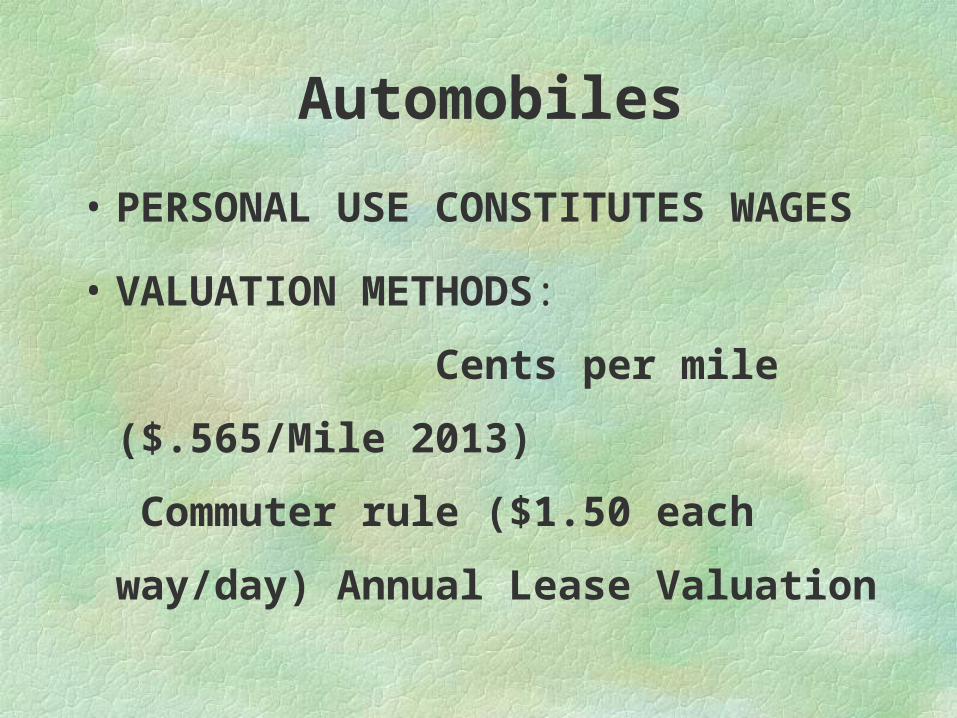

Automobiles

• PERSONAL USE CONSTITUTES

WAGES

• VALUATION METHODS:

Cents per mile ($.565/Mile

2013) Commuter rule

($1.50 each way/day) Annual

Lease Valuation

CENTS-PER-MILECENTS-PER-MILE

• FMV of auto must be less than $16,000 for automobile; $17,000 for truck - 2013

• At Least 50 Percent Of Annual Mileage Must Be For Business Use

• Must Be Actually Driven At Least 10,000 Miles Per Year (May Be All Personal Miles)

• Used During The Year Primarily By Employees.

COMMUTER RULECOMMUTER RULE

• Must own or lease vehicle and provide vehicle to one or more employees

• Auto must be provided for bona fide non-compensatory reasons – i.e., on-call

• Must have written policy that prohibits personal use other than commuting or de minims personal use.

• Cannot be used for Control employee • Government Control employee is any

elected official or employee whose salary exceeds $145,700 for 2011.

ANNUAL LEASE VALUATIONANNUAL LEASE VALUATION

• Annual Lease Value Table provides annual lease amount based on the fair market value of the automobile.

• Prorate annual lease amount based on percentage of personal use.

• Additional $.055 mile charged for each personal mile if employer provides fuel.

• Records must be maintained to show total miles and personal or business use.

• Employer may elect to tax 100% personal.

Exempt Vehicles

• Clearly Marked Police or Fire Vehicles

• Unmarked Police Cars *

• Ambulances or Hearses

• Large Trucks• School Buses

EMPLOYEE EXPENSE

REIMBURSEMENTPLANS:

Must have an “Accountable

Plan”

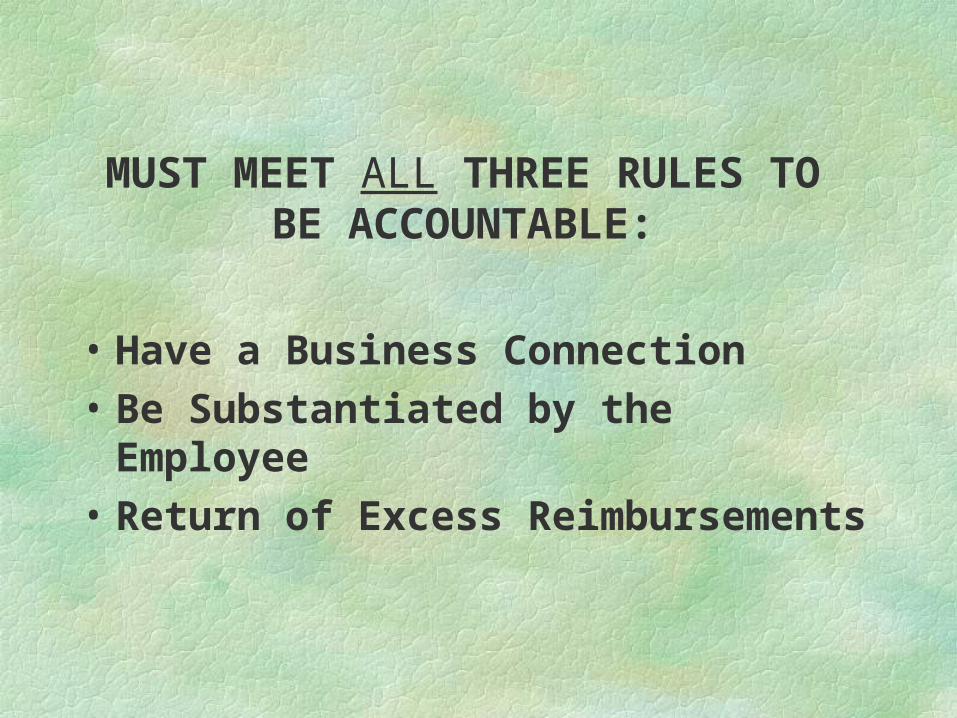

MUST MEET ALL THREE RULES TO BE ACCOUNTABLE:

• Have a Business Connection• Be Substantiated by the

Employee• Return of Excess

Reimbursements

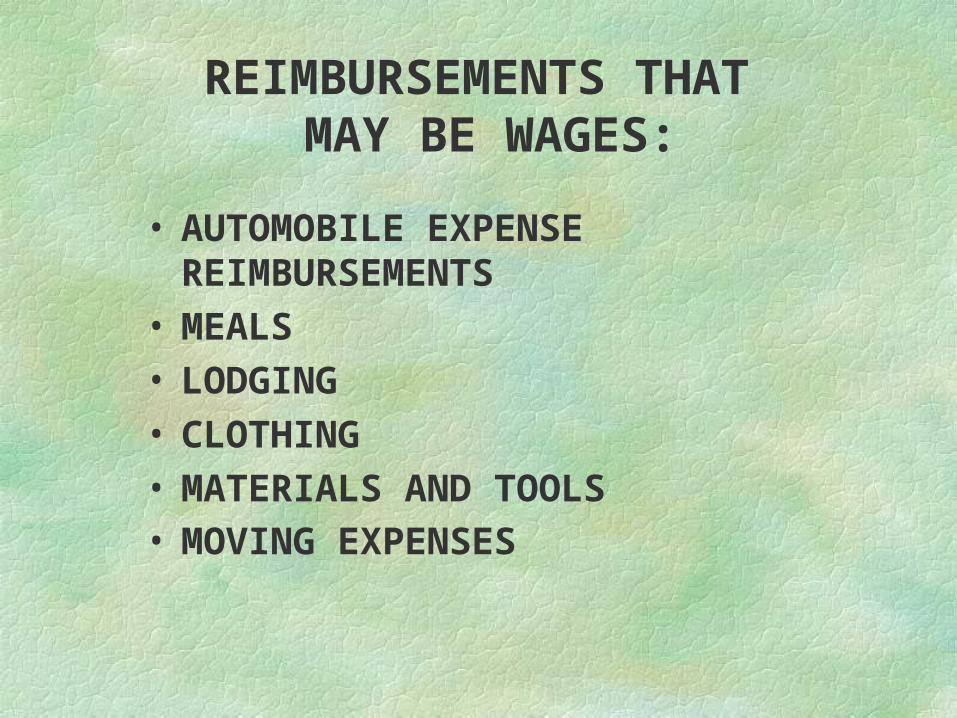

REIMBURSEMENTS THAT MAY BE WAGES:

• AUTOMOBILE EXPENSE REIMBURSEMENTS

• MEALS• LODGING• CLOTHING• MATERIALS AND TOOLS• MOVING EXPENSES

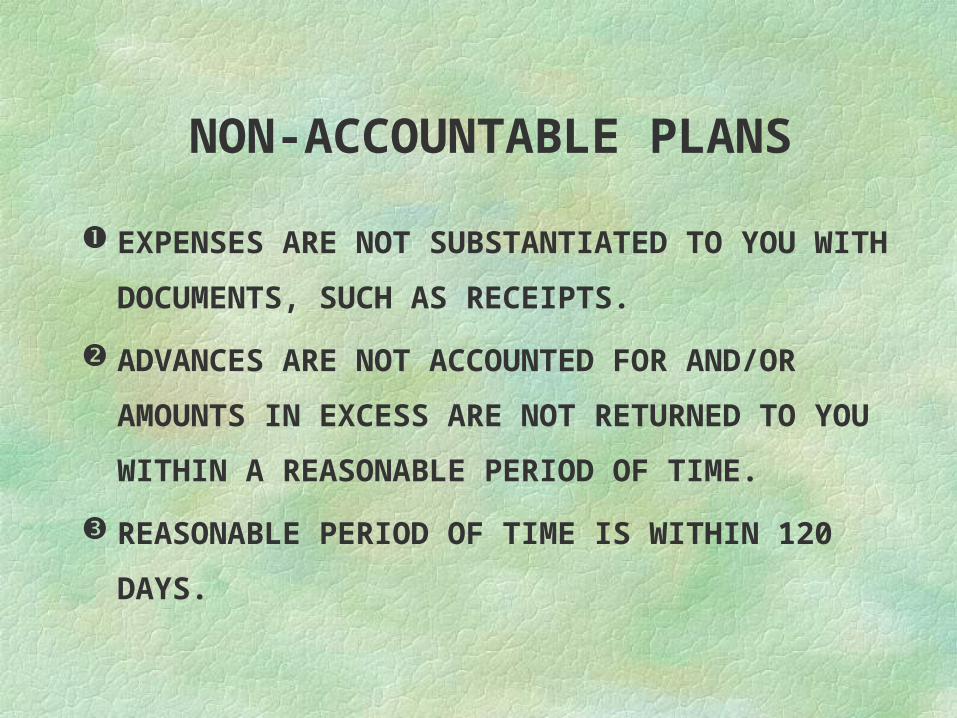

NON-ACCOUNTABLE PLANS

EXPENSES ARE NOT SUBSTANTIATED TO YOU

WITH DOCUMENTS, SUCH AS RECEIPTS.

ADVANCES ARE NOT ACCOUNTED FOR

AND/OR AMOUNTS IN EXCESS ARE NOT

RETURNED TO YOU WITHIN A REASONABLE

PERIOD OF TIME.

REASONABLE PERIOD OF TIME IS WITHIN 120

DAYS.

EMPLOYEE ALLOWANCES

Types of Allowances

• Car Allowance• Uniform Allowance• Moving Allowance• Travel Advance• Tool Allowance

Cell Phones and Computers

• Computers are considered “listed property”

• Must account for personal use• Personal use taxable wages • Wages subject to all employment

tax• NOTE: Cell phones are no longer

considered “listed property” – must be noncompensatory reasons

Supper Money

• Must be paid to enable employee to work overtime

• Based on hours worked - Taxable wages

• Subject to all employment taxes

Longevity Pay

• Report on Form W-2• Do NOT report on Form 1099-Misc• Subject to all employment taxes

Reimbursement Personal Expenses

• Payment for meals, not away overnight - Personal

• Uniforms must be qualified• Plain clothes detectives - reimbursed

for torn suit - Personal

Resources

• Publications 15, 15A, 15B• IRC Section 3121• Payroll Management Guides• NC 218 Coordinator• Internal Revenue Service

Idaho FSLG Specialist

• Chris Casteel• Phone: 208-363-8818• Fax: 208-387-2849• E-mail:

•[email protected]• Address:

•550 West Fort •Boise, ID 83724

• .