for agent use only. this material may not be used with the public. mliny01311318035 10/13 insurance...

TRANSCRIPT

For agent use only. This material may not be used with the public.

MLINY01311318035 10/13

Insurance products are issued by: John Hancock Life Insurance Company (U.S.A.), Boston, MA 02116 (not licensed in New York) and John Hancock Life Insurance Company of New York, Valhalla, NY 10595 and securities offered through John Hancock Distributors LLC through other broker/dealers that have a selling agreement with John Hancock Distributors LLC, 197 Clarendon Street, Boston, MA 02116.

Accum

ulation

For agent use only. This material may not be used with the publicFor agent use only. This material may not be used with the public2 of 11

Advantages of Accumulation IUL

• Often the most competitive product for cash value accumulation in the industry

• Highly competitive 12% Current Cap (New York Rates)

• Competitive Fixed Account that provides safe and steady growth

• Cumulative guarantee ensures an average annualized rate of return of 2% over the life of the policy, upon surrender

Accum

ulation

For agent use only. This material may not be used with the publicFor agent use only. This material may not be used with the public

Life Insurance in Retirement Planning

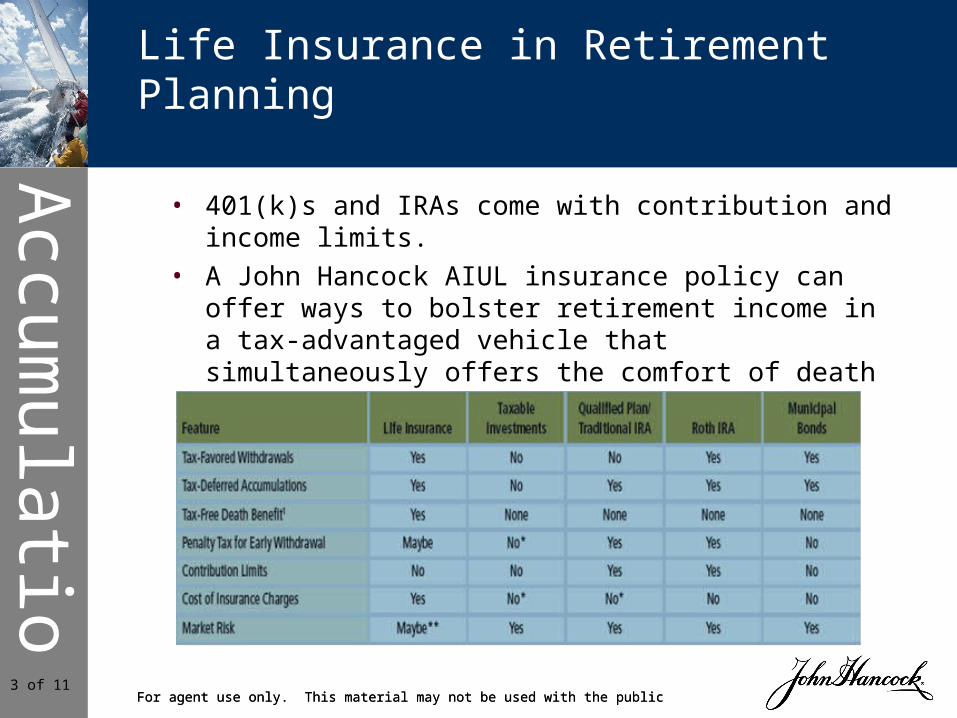

• 401(k)s and IRAs come with contribution and income limits.

• A John Hancock AIUL insurance policy can offer ways to bolster retirement income in a tax-advantaged vehicle that simultaneously offers the comfort of death benefit protection.

3 of 11

Accum

ulation

For agent use only. This material may not be used with the publicFor agent use only. This material may not be used with the public4 of 11

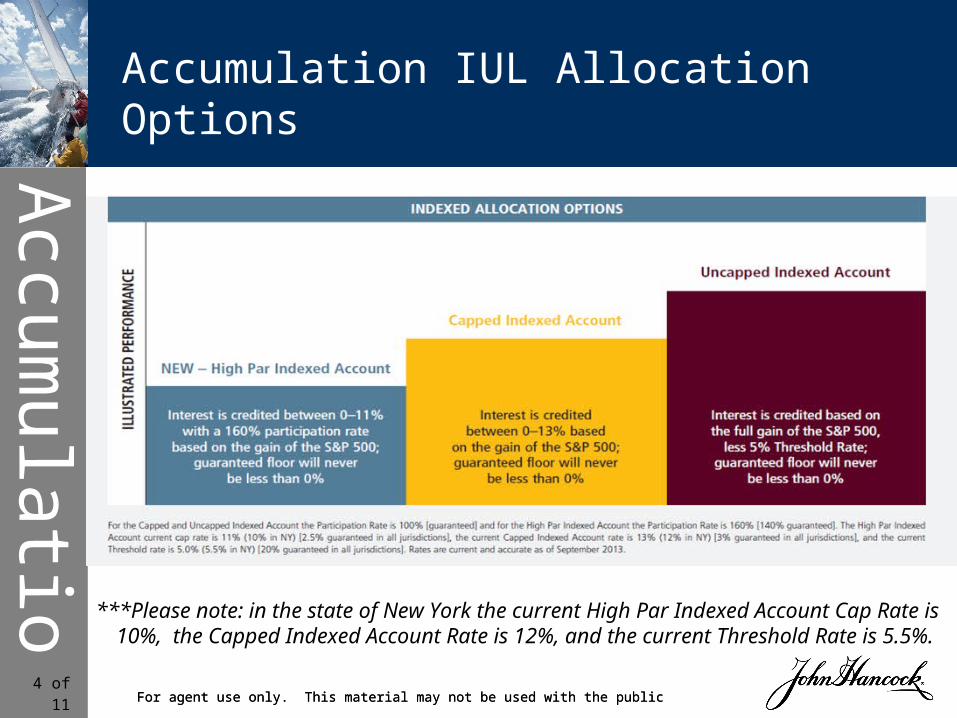

Accumulation IUL Allocation Options

***Please note: in the state of New York the current High Par Indexed Account Cap Rate is 10%, the Capped Indexed Account Rate is 12%, and the current Threshold Rate is 5.5%.

Accum

ulation

For agent use only. This material may not be used with the publicFor agent use only. This material may not be used with the public5 of 11

Product Features

• Qualified Long-Term Care (LTC) Rider2

– Typically lower cost & higher MMBA than competitors

• Two Loan Options– “Standard Loans” – Zero-net cost loan years 11+

– “Index Loans” – More risk & reward potential

• 4.55% Current Fixed Account Rate (New York Rates)

Accum

ulation

For agent use only. This material may not be used with the public6 of 11

LTC Rider

• Female, Age 60, Preferred Risk Class

• Plans to retire at age 70

• Pay $30,000 for 10 Years for a $500,000 Death Benefit

Income Target LTC Pool

Without LTC $31,922 $13,810 $0

With LTC* $31,236 $14,325 $500,000

Difference -2% +4% +$500,000

Assumes an 7% rate of return Distributions from Age 71-85, Targeting $50,000 at Lifetime. This is a supplemental illustration. Not all benefits and values are guaranteed. The assumptions on which the non-guaranteed elements are based are subject to change by the insurer. Actual results may be more or less favorable.

*2% LTC Rider

Accum

ulation

For agent use only. This material may not be used with the publicFor agent use only. This material may not be used with the public7 of 11

Additional Riders

• Return of Premium (ROP)– Increase death benefit by % of premiums paid (up to 100%)

• Disability of Specified Premium (DPSP)– Pays specified amount into policy in event of disability

• Accelerated Benefit – Pays portion of death benefit in case of terminal illness

Accum

ulation

For agent use only. This material may not be used with the public8 of 11

IUL Practices John Hancock Avoids

*John Hancock applies interest on the cash value throughout the year. **Due to crediting rates and or charges.

Competitor information is current and accurate to the best of our knowledge as of October 2013.

John John HancockHancock

Pac Pac LifeLife AXAAXA LincolnLincoln PennPenn Minn. Minn.

LifeLife AvivaAviva INGING

Multi-Year Segments X X X X X X

Applying interest credits to the lowest value* X X X

Holding Account rate lower than Fixed Account X

No partial interest on withdrawals X X X X

Weaker Fixed Account performance** X X X X X

Accum

ulation

For agent use only. This material may not be used with the publicFor agent use only. This material may not be used with the public9 of 11

John Hancock’s Accumulation IUL

Taking the helm with the right skills and performance

Accum

ulation

For agent use only. This material may not be used with the public10 of 11

Insurance policies and/or associated riders and features may not be available in all states.

Guaranteed product features are dependent upon minimum premium requirements and the claims-paying ability of the issuer.

Loans and withdrawals will reduce the death benefit and the cash surrender value, and may cause the policy to lapse. Lapse or surrender of a policy with a loan may cause the recognition of taxable income. Withdrawals in excess of the cost basis (premiums paid) will be subject to tax and certain withdrawals within the first 15 years may be subject to recapture tax. Additionally, policies classified as Modified Endowment Contracts may be subject to tax when a loan or withdrawal is made. A federal tax penalty of 10% may also apply if the loan or withdrawal is taken prior to age 59½. Cash value available for loans and withdrawals may be more or less than originally invested. Withdrawals are available after the first policy year.

1. Excluding dividends. Standard & Poor’s®, S&P®, S&P 500®, Standard & Poor’s 500 and 500 are trademarks of Standard & Poor’s Financial Services LLC, a subsidiary of The McGraw-Hill Companies, Inc. and have been licensed for use by John Hancock. The Product is not sponsored, sold, endorsed or promoted by Standard & Poor’s, and Standard & Poor’s makes no representation regarding the advisability of purchasing the Product. The S&P 500® Index is an index of 500 stocks that are generally representative of the performance of leading companies in leading industries within the U.S. You cannot invest directly in the S&P 500® Index.

2. The Long-Term Care (LTC) rider is an accelerated death benefit and may not be available in all states. Maximum face amount: $5 million with the LTC rider. The LTC rider is not considered long-term care insurance in some states. When the policy death benefit is accelerated for long-term care expenses, the death benefit is reduced dollar for dollar, and the cash value is reduced proportionately. There are additional costs associated with this rider. Please go to www.jhsalesnet.com for a complete list of up-to-date state approvals. For prospective policyholders in New York, this product is a life insurance policy that accelerates the death benefit for qualified long-term care services and is not a health insurance policy providing long-term care insurance subject to the minimum requirements of New York law, does not qualify for the New York State Partnership for Long-Term Care program and is not a Medicare supplement policy. This rider has exclusions and limitations, reductions of benefits, and terms under which the rider may be continued in force or discontinued. Consult the state specific Outline of Coverage for additional details.

Disclosures

Accum

ulation

For agent use only. This material may not be used with the public11 of 11

Disclosures Cont.

LIMITATIONS ON OR CONDITIONS FOR ELIGIBILITY FOR PAYMENT OF BENEFITSLimitations. We will not pay Accelerated Benefits for Qualified Long Term Care Services incurred during the Elimination Period, or for any care, treatment, or charges described in the Non-Duplication of Benefits or Exclusions provisions, below. We will not pay Accelerated Benefits in excess of the Maximum Monthly Benefit Amount for any Calendar Month during any Period of Care, and may modify coverage under this rider following reinstatement.Exclusions. Qualified Long Term Care Services does not include care or treatment:(a) for intentionally self-inflicted injury;(b) required as a result of alcoholism or drug abuse (unless drug abuse was a result of the administration of drugs as part of treatment by a Physician);(c) due to war (declared or undeclared) or any act of war, or service in any of the armed forces or auxiliary units;(d) due to participation in a felony, riot or insurrection;(e) for which no charge is normally made in the absence of insurance;(f) provided by a member of the Life Insured’s Immediate Family;(g) provided outside the fifty United States and the District of Columbia.Non-Duplication of Benefits. Qualified Long Term Care Services does not include charges covered under any of the following:(a) Medicare (including amounts that would be reimbursable but for the application of a deductible or coinsurance amounts);(b) any other governmental program (except Medicaid);(c) any state or federal workers’ compensation, employer’s liability or occupational disease law, or any motor vehicle no-fault law;(d) expenses for services or items available or paid under another long term care insurance or health insurance policy.

Some riders may have additional fees and expenses associated with them.

The Return of Premium Rider allows clients to select a percentage of the premiums paid to be returned to the beneficiaries in addition to the death benefit. There are costs associated with the ROP rider, as well as limitations on the cumulative amount that can be returned. Not available in conjunction with certain other riders.

Variable universal life insurance has annual fees and expenses associated with it in addition to life insurance related charges (which differ with the product chosen), including surrender charges and investment management fees. Variable universal life insurance products are long-term contracts and are sold by prospectus. They are subject to market risk due to the underlying sub-accounts, and are unsuitable as a short term savings vehicle. The primary purpose of variable universal life insurance is to provide lifetime protection against economic loss due to the death of the insured person. Cash values are not guaranteed if the client is invested in the investment accounts. There are risks associated with each investment option, and the policy may lose value.

Please contact 1-888-266-7498, option 2 to obtain product and fund prospectuses or if you are interested in obtaining a selling agreement with John Hancock Distributors LLC (for New York, contact 1-800-743-5542, option 5). The prospectuses contain complete details on investment objectives, risks, fees, charges and expenses as well as other information about the investment company. Please advise your clients to carefully read the prospectuses which contain this and other information on the product and the underlying portfolios, and consider these factors carefully before investing.