focused disciplined striving - e.on...focused disciplined striving european energy & utilities...

TRANSCRIPT

Focused Disciplined Striving

European Energy & Utilities Credit Conference 2016 Henryk Wuppermann, Head of Corporate Finance, E.ON SE London, 24 November 2016

1

Disclaimer (I/II)

This document and the presentation to which it relates contains information relating to E.ON SE ("E.ON") that must not be relied upon for any purpose and may not be redistributed, reproduced, published, or passed on to any other person or used in whole or in part for any other purpose. By accessing this document you agree to abide by the limitations set out in this document. This document is being presented solely for informational purposes and should not be treated as giving investment advice. The information contained in this presentation comprise financial and similar information (e.g. pro-forma financial results). This information is neither audited nor reviewed and should be considered preliminary and subject to change. In particular the presentation of pro-forma financial results may be different compared to the final presentation within the E.ON consolidated financial statements. Certain information in this presentation is based on management estimates. Such estimates have been made in good faith and represent the current beliefs of applicable members of management. Estimates may not be correct or complete. Accordingly, no representation or warranty (express or implied) is given that such estimates are correct or complete. We advise you that some of the information presented herein is based on statements by third parties, and that no representation or warranty, express or implied, is made as to, and no reliance should be placed on, the fairness, accuracy, completeness or correctness of this information or any other information or opinions contained herein, for any purpose whatsoever. Certain statements contained herein may be statements of future expectations and other forward-looking statements that are based on the E.ON’s current views and assumptions and involve known and unknown risks and uncertainties that may cause actual results, performance or events to differ materially from those expressed or implied in such statements. No one undertakes to publicly update or revise any such forward-looking statement. Neither E.ON or any of their respective officers, employees or affiliates nor any other person shall assume or accept any responsibility, obligation or liability whatsoever (in negligence or otherwise) for any loss howsoever arising from any use of this presentation or the statements contained herein as to third person statements, any statements of future expectations and other forward-looking statements, or the fairness, accuracy, completeness or correctness of statements contained herein. In giving this presentation, none of E.ON or their respective agents undertake any obligation to provide the recipient with access to any additional information or to update this presentation or any information or to correct any inaccuracies in any such information.

2

Disclaimer (II/II)

This presentation is not intended to provide the basis for any evaluation or any securities and should not be considered as a recommendation that any person should purchase any shares or other securities. This presentation contains certain financial measures (including forward-looking measures) that are not calculated in accordance with IFRS and are therefore considered as "Non-IFRS financial measures". The Management of E.ON believes that the Non-IFRS financial measures used by E.ON, when considered in conjunction with (but not in lieu of) other measures that are computed in accordance with IFRS, enhance an understanding of EON's results of operations, financial position or cash flows. A number of these Non-IFRS financial measures are also commonly used by securities analysts, credit rating agencies and investors to evaluate and compare the periodic and future operating performance and value of E.ON and other companies with which E.ON competes. These Non-IFRS financial measures should not be considered in isolation as a measure of E.ON's profitability or liquidity, and should be considered in addition to, rather than as a substitute for, net income and the other income or cash flow data prepared in accordance with IFRS. In particular, there are material limitations associated with our use of Non-IFRS financial measures, including the limitations inherent in our determination of each of the relevant adjustments. The Non-IFRS financial measures used by E.ON may differ from, and not be comparable to, similarly-titled measures used by other companies. Certain numerical data, financial information and market data (including percentages) in this presentation have been rounded according to established commercial standards. As a result, the aggregate amounts (sum totals or interim totals or differences or if numbers are put in relation) in this presentation may not correspond in all cases to the amounts contained in the underlying (unrounded) figures appearing in the consolidated financial statements. Furthermore, in tables and charts, these rounded figures may not add up exactly to the totals contained in the respective tables and charts.

3

Agenda

New E.ON and strategic update

Financial and operating update

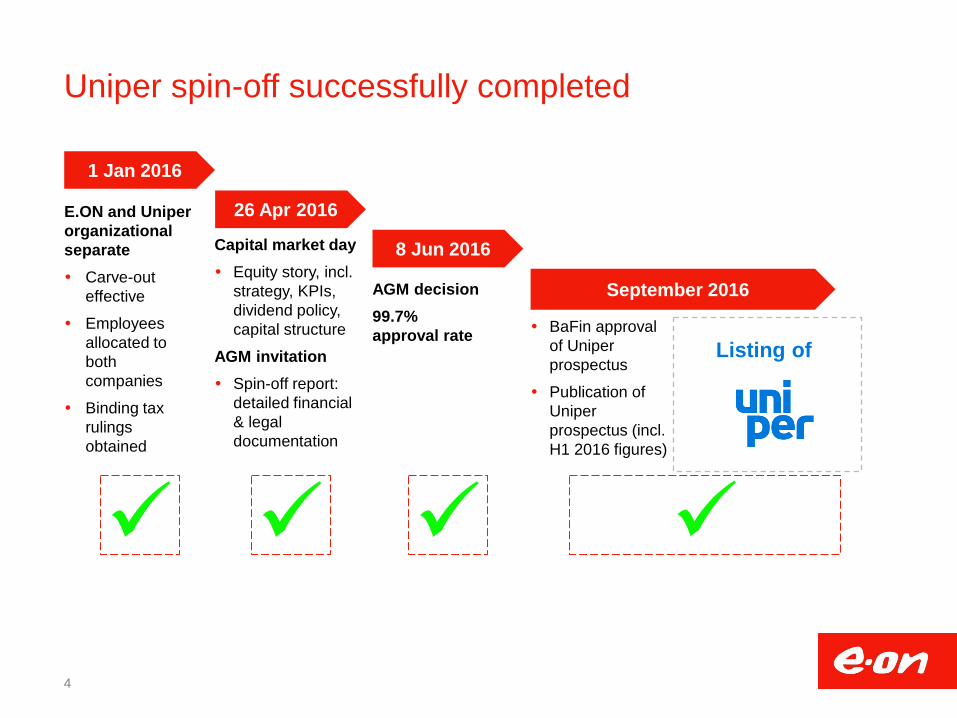

Uniper spin-off successfully completed

1 Jan 2016

E.ON and Uniper organizational separate Carve-out

effective

Employees allocated to both companies

Binding tax rulings obtained

26 Apr 2016

8 Jun 2016

September 2016 AGM decision 99.7% approval rate

Capital market day Equity story, incl.

strategy, KPIs, dividend policy, capital structure

AGM invitation Spin-off report:

detailed financial & legal documentation

4

Listing of BaFin approval

of Uniper prospectus

Publication of Uniper prospectus (incl. H1 2016 figures)

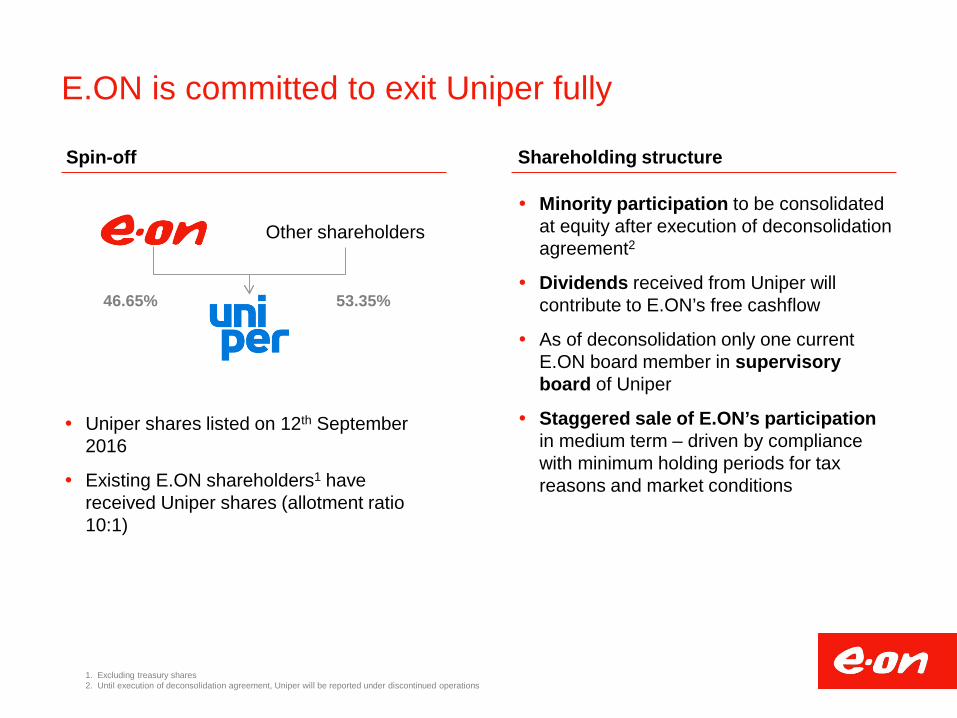

E.ON is committed to exit Uniper fully

Minority participation to be consolidated at equity after execution of deconsolidation agreement2

Dividends received from Uniper will contribute to E.ON’s free cashflow

As of deconsolidation only one current E.ON board member in supervisory board of Uniper

Staggered sale of E.ON’s participation in medium term – driven by compliance with minimum holding periods for tax reasons and market conditions

Other shareholders

46.65% 53.35%

Uniper shares listed on 12th September 2016

Existing E.ON shareholders1 have received Uniper shares (allotment ratio 10:1)

Spin-off Shareholding structure

1. Excluding treasury shares 2. Until execution of deconsolidation agreement, Uniper will be reported under discontinued operations

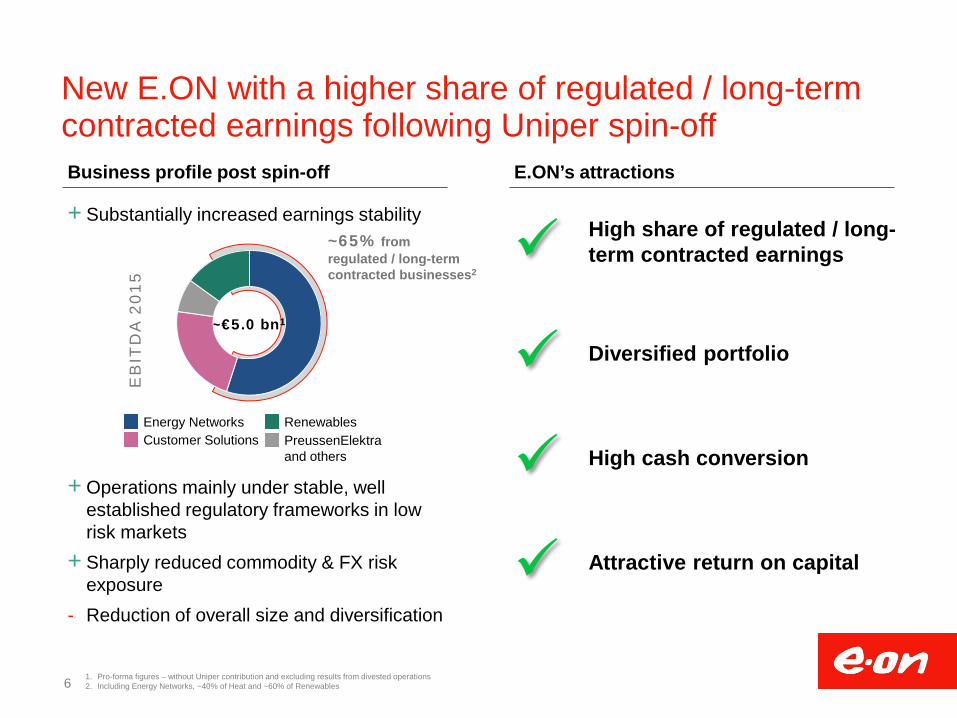

+ Substantially increased earnings stability

+ Operations mainly under stable, well

established regulatory frameworks in low risk markets

+ Sharply reduced commodity & FX risk exposure

- Reduction of overall size and diversification

New E.ON with a higher share of regulated / long-term contracted earnings following Uniper spin-off

High share of regulated / long-term contracted earnings

High cash conversion

Diversified portfolio

E.ON’s attractions

Attractive return on capital

Business profile post spin-off

1. Pro-forma figures – without Uniper contribution and excluding results from divested operations 2. Including Energy Networks, ~40% of Heat and ~60% of Renewables

EB

ITD

A 2

01

5

Renewables Customer Solutions

PreussenElektra and others

Energy Networks

~€5.0 bn1

~65% from regulated / long-term contracted businesses2

6

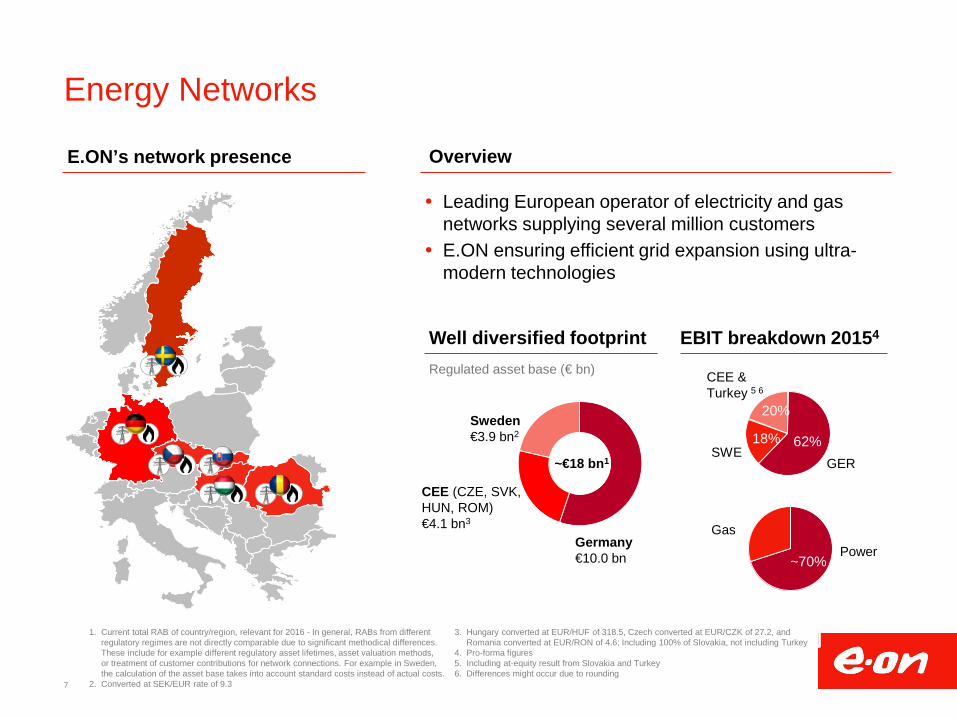

62% 18%

20%

7

Overview

EBIT breakdown 20154

Leading European operator of electricity and gas networks supplying several million customers E.ON ensuring efficient grid expansion using ultra-

modern technologies

Energy Networks

E.ON’s network presence

GER SWE

CEE & Turkey 5 6

Power Gas

1. Current total RAB of country/region, relevant for 2016 - In general, RABs from different regulatory regimes are not directly comparable due to significant methodical differences. These include for example different regulatory asset lifetimes, asset valuation methods, or treatment of customer contributions for network connections. For example in Sweden, the calculation of the asset base takes into account standard costs instead of actual costs.

2. Converted at SEK/EUR rate of 9.3

3. Hungary converted at EUR/HUF of 318.5, Czech converted at EUR/CZK of 27.2, and Romania converted at EUR/RON of 4.6; Including 100% of Slovakia, not including Turkey

4. Pro-forma figures 5. Including at-equity result from Slovakia and Turkey 6. Differences might occur due to rounding

~70%

Well diversified footprint

Regulated asset base (€ bn)

CEE (CZE, SVK, HUN, ROM)

€4.1 bn3

~€18 bn1

Germany €10.0 bn

Sweden €3.9 bn2

8

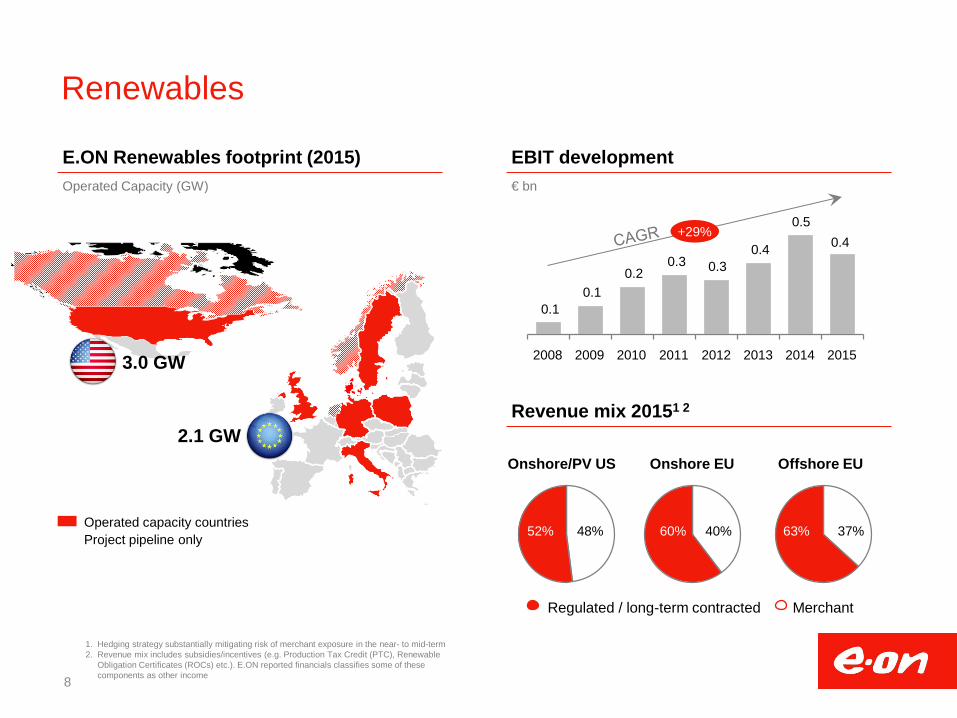

Renewables

Operated capacity countries Project pipeline only

1. Hedging strategy substantially mitigating risk of merchant exposure in the near- to mid-term 2. Revenue mix includes subsidies/incentives (e.g. Production Tax Credit (PTC), Renewable

Obligation Certificates (ROCs) etc.). E.ON reported financials classifies some of these components as other income

E.ON Renewables footprint (2015)

2.1 GW

3.0 GW

Operated Capacity (GW)

Onshore/PV US Onshore EU Offshore EU

Regulated / long-term contracted Merchant

0.1 0.1

0.2 0.3 0.3

0.4

0.5 +29%

2015

0.4

2014 2013 2012 2011 2010 2009 2008

52% 48% 60% 40% 63% 37%

Revenue mix 20151 2

EBIT development € bn

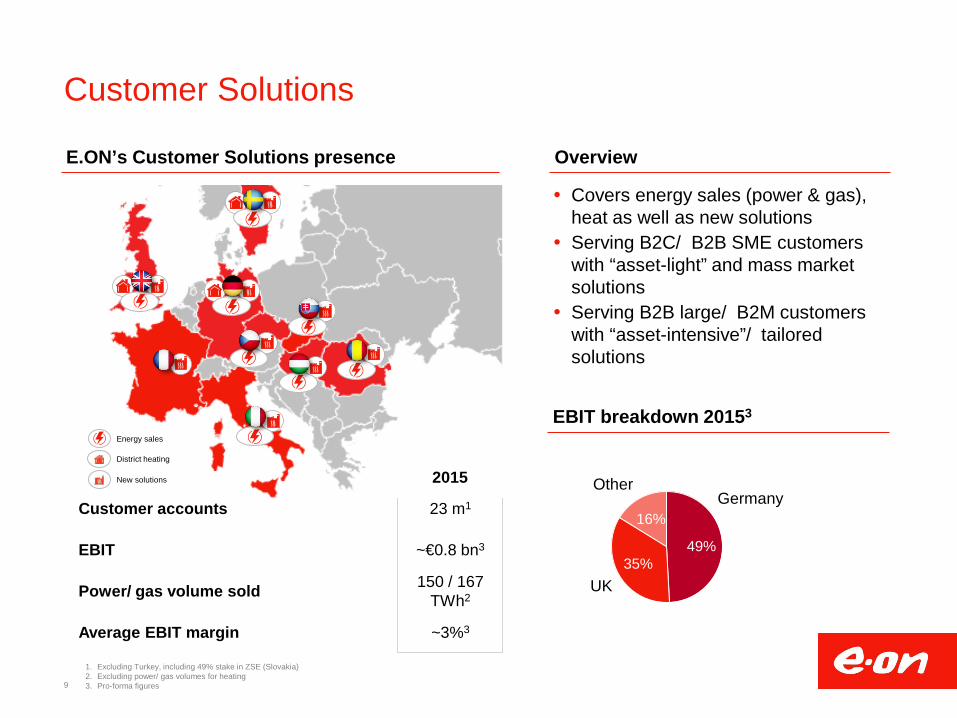

Customer Solutions

49% 35%

16% Germany

UK

Other

1. Excluding Turkey, including 49% stake in ZSE (Slovakia) 2. Excluding power/ gas volumes for heating 3. Pro-forma figures 9

EBIT

Power/ gas volume sold

Average EBIT margin

~€0.8 bn3

150 / 167 TWh2

~3%3

Customer accounts 23 m1

E.ON’s Customer Solutions presence

EBIT breakdown 20153

2015

Energy sales

District heating

New solutions

Covers energy sales (power & gas), heat as well as new solutions Serving B2C/ B2B SME customers

with “asset-light” and mass market solutions Serving B2B large/ B2M customers

with “asset-intensive”/ tailored solutions

Overview

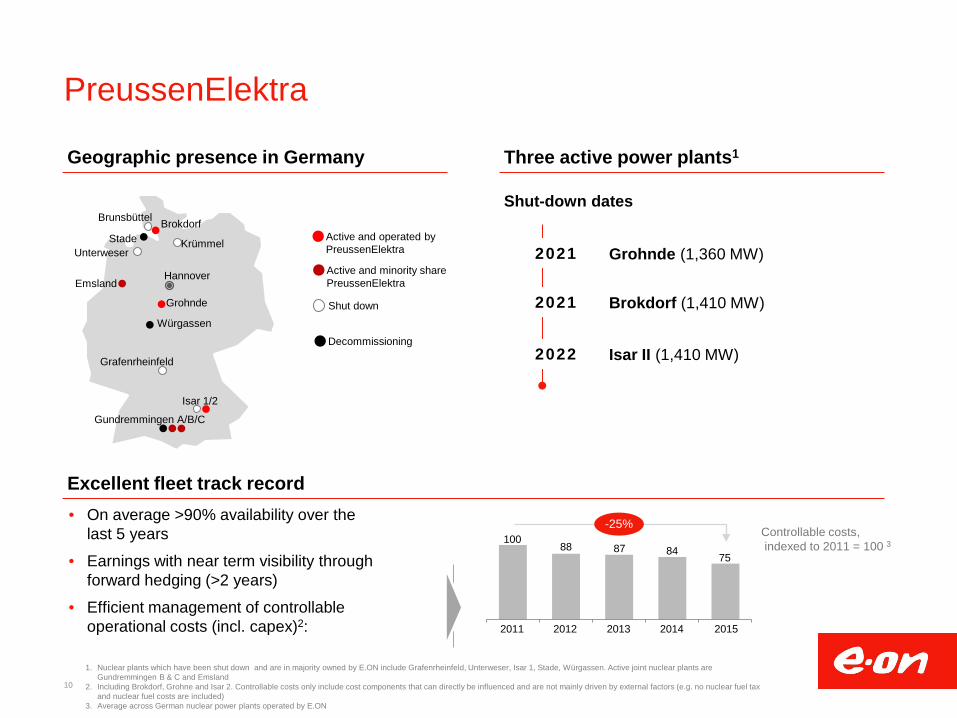

PreussenElektra

Decommissioning

Shut down

Active and operated by PreussenElektra

Active and minority share PreussenElektra

Brunsbüttel Brokdorf Stade

Unterweser Krümmel

Hannover Emsland

Grohnde

Würgassen

Grafenrheinfeld

Isar 1/2

Gundremmingen A/B/C

Geographic presence in Germany

10

Three active power plants1

Shut-down dates

Grohnde (1,360 MW) 2021

Brokdorf (1,410 MW) 2021

Isar II (1,410 MW) 2022

Excellent fleet track record • On average >90% availability over the

last 5 years

• Earnings with near term visibility through forward hedging (>2 years)

• Efficient management of controllable operational costs (incl. capex)2:

100 88 87 84 75

2015 2014 2013 2012 2011

Controllable costs, indexed to 2011 = 100 3

-25%

1. Nuclear plants which have been shut down and are in majority owned by E.ON include Grafenrheinfeld, Unterweser, Isar 1, Stade, Würgassen. Active joint nuclear plants are Gundremmingen B & C and Emsland

2. Including Brokdorf, Grohne and Isar 2. Controllable costs only include cost components that can directly be influenced and are not mainly driven by external factors (e.g. no nuclear fuel tax and nuclear fuel costs are included)

3. Average across German nuclear power plants operated by E.ON

11

Agenda

New E.ON and strategic update

Financial and operating update

12

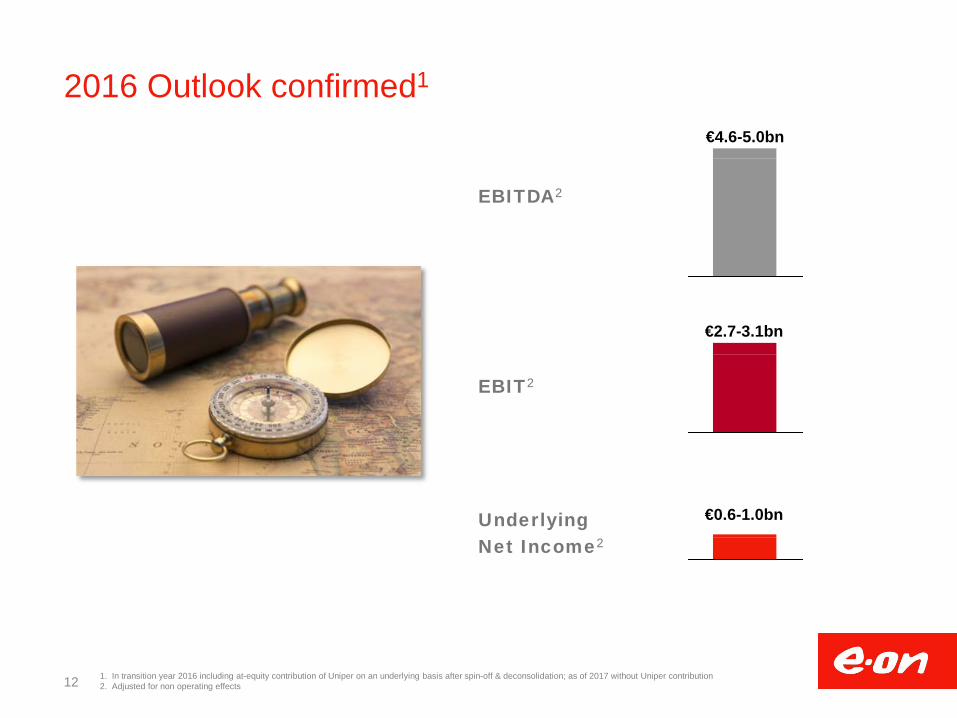

2016 Outlook confirmed1

€0.6-1.0bn

€4.6-5.0bn

EBITDA2

EBIT2

Underlying Net Income2

€2.7-3.1bn

1. In transition year 2016 including at-equity contribution of Uniper on an underlying basis after spin-off & deconsolidation; as of 2017 without Uniper contribution 2. Adjusted for non operating effects

13

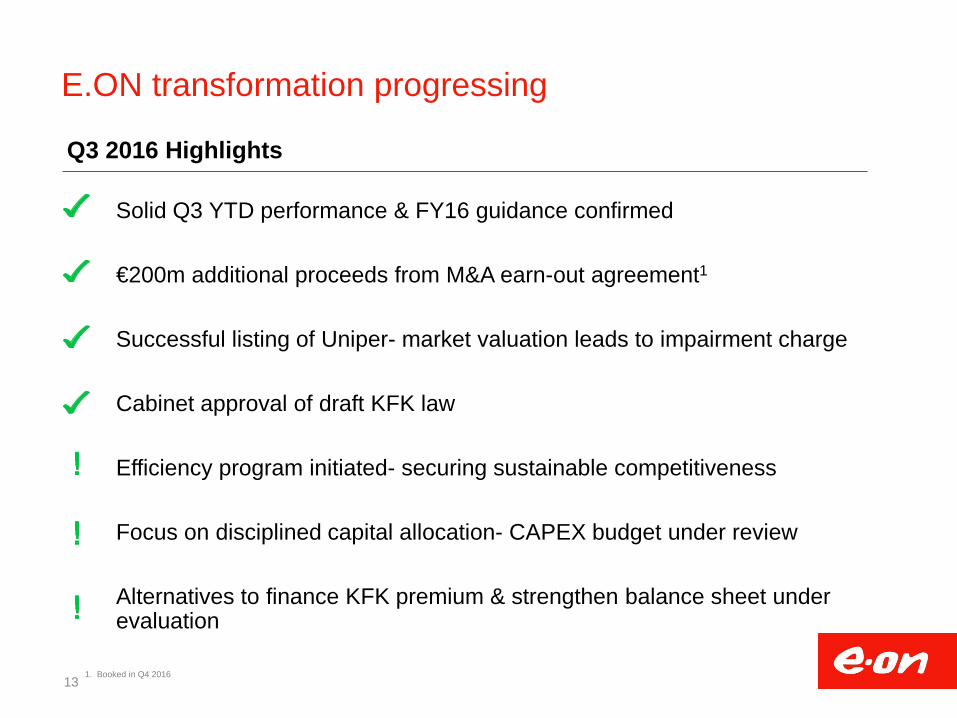

E.ON transformation progressing

Solid Q3 YTD performance & FY16 guidance confirmed

€200m additional proceeds from M&A earn-out agreement1

Successful listing of Uniper- market valuation leads to impairment charge

Cabinet approval of draft KFK law

Efficiency program initiated- securing sustainable competitiveness

Focus on disciplined capital allocation- CAPEX budget under review

Alternatives to finance KFK premium & strengthen balance sheet under evaluation

Q3 2016 Highlights

1. Booked in Q4 2016

14

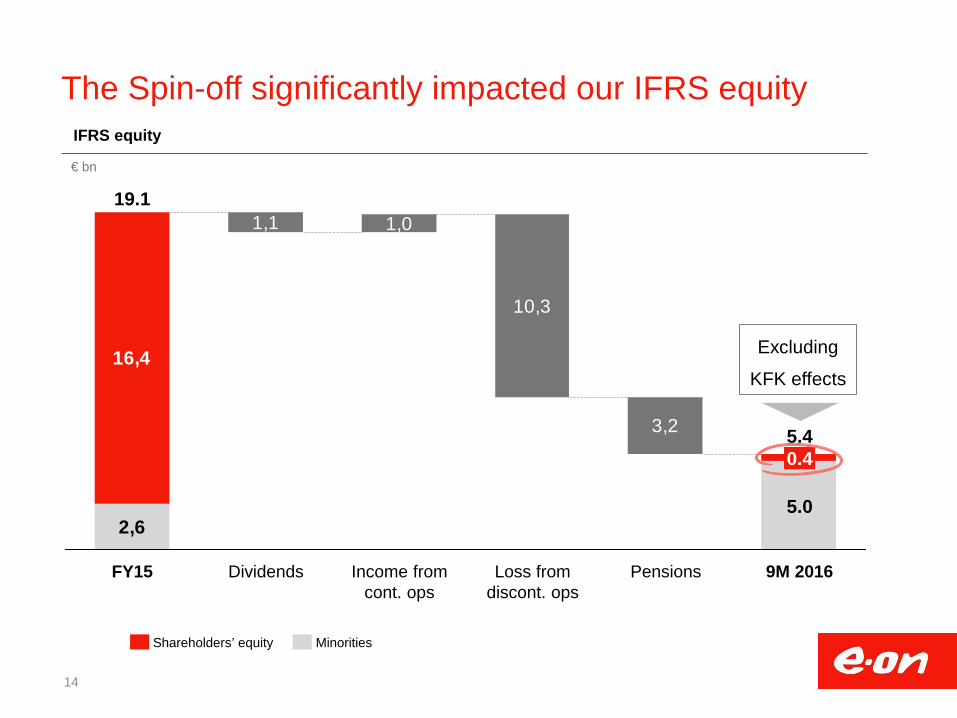

The Spin-off significantly impacted our IFRS equity

1,1 1,0

10,3

3,2

2,6

16,4

9M 2016

5.4

5.0

0.4

Pensions Loss from discont. ops

Income from cont. ops

Dividends FY15

19.1

IFRS equity

€ bn

Shareholders’ equity Minorities

Excluding

KFK effects

15

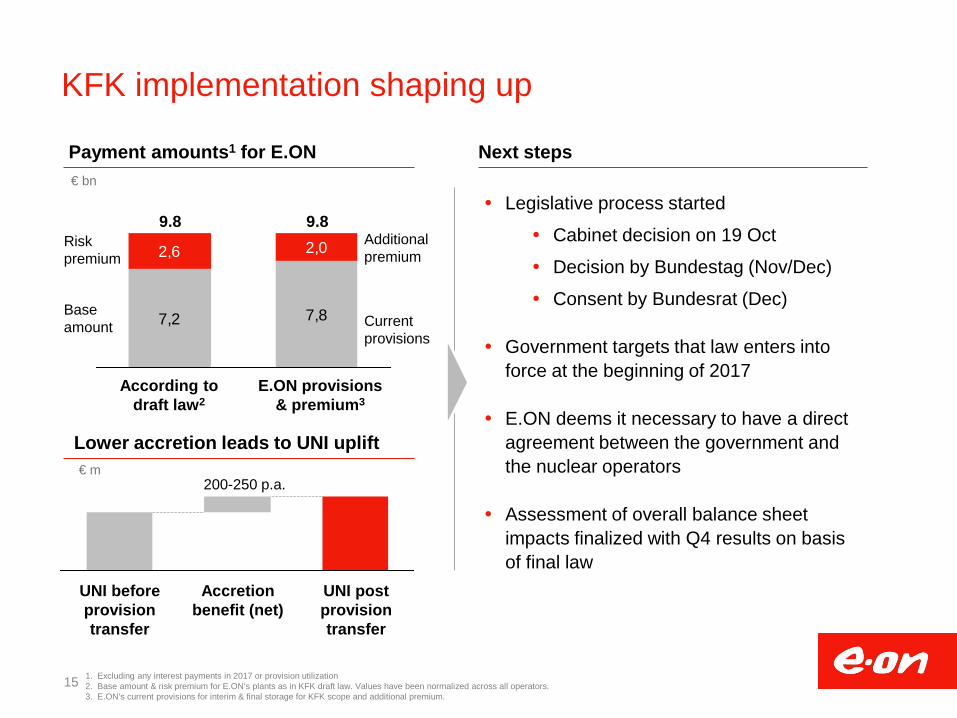

KFK implementation shaping up

Next steps Payment amounts1 for E.ON

1. Excluding any interest payments in 2017 or provision utilization 2. Base amount & risk premium for E.ON‘s plants as in KFK draft law. Values have been normalized across all operators. 3. E.ON’s current provisions for interim & final storage for KFK scope and additional premium.

€ bn

Legislative process started

Cabinet decision on 19 Oct

Decision by Bundestag (Nov/Dec)

Consent by Bundesrat (Dec)

Government targets that law enters into force at the beginning of 2017

E.ON deems it necessary to have a direct agreement between the government and the nuclear operators

Assessment of overall balance sheet impacts finalized with Q4 results on basis of final law

7,2 7,8

2,02,6

9.8 9.8

Lower accretion leads to UNI uplift

UNI post provision transfer

Accretion benefit (net)

UNI before provision transfer

€ m

200-250 p.a.

Base amount

Risk premium

Current provisions

Additional premium

According to draft law2

E.ON provisions & premium3

16

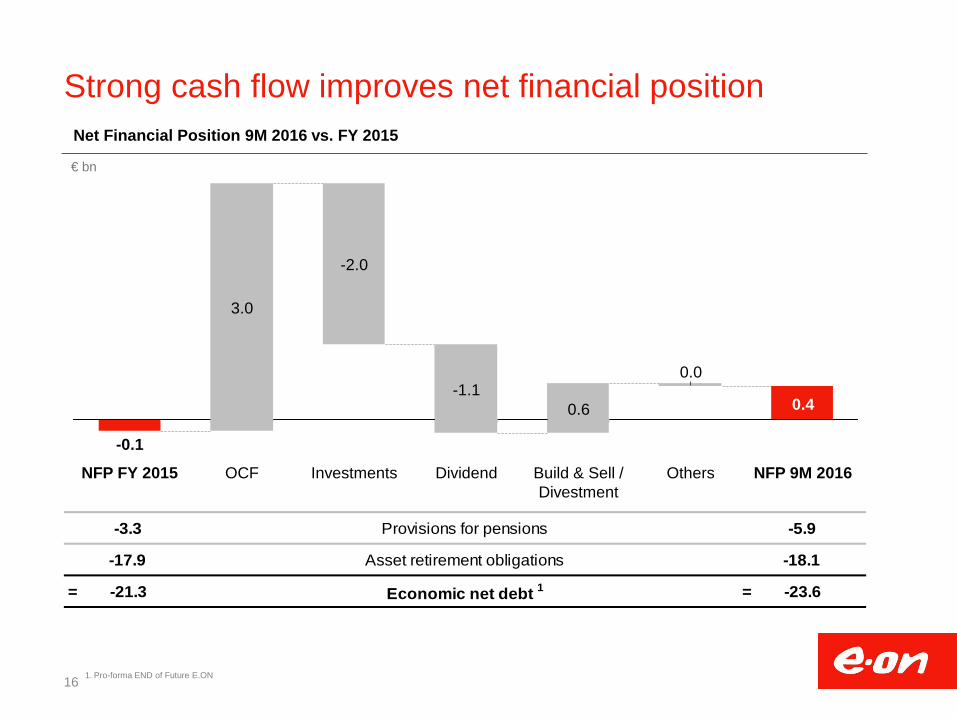

Strong cash flow improves net financial position

Others

0.4

NFP 9M 2016

0.0

Build & Sell / Divestment

0.6

Dividend

-1.1

Investments

-2.0

OCF

3.0

NFP FY 2015

-0.1

€ bn

Net Financial Position 9M 2016 vs. FY 2015

-3.3 -5.9

-17.9 -18.1

= -21.3 = -23.6Economic net debt 1Asset retirement obligations

Provisions for pensions

1. Pro-forma END of Future E.ON

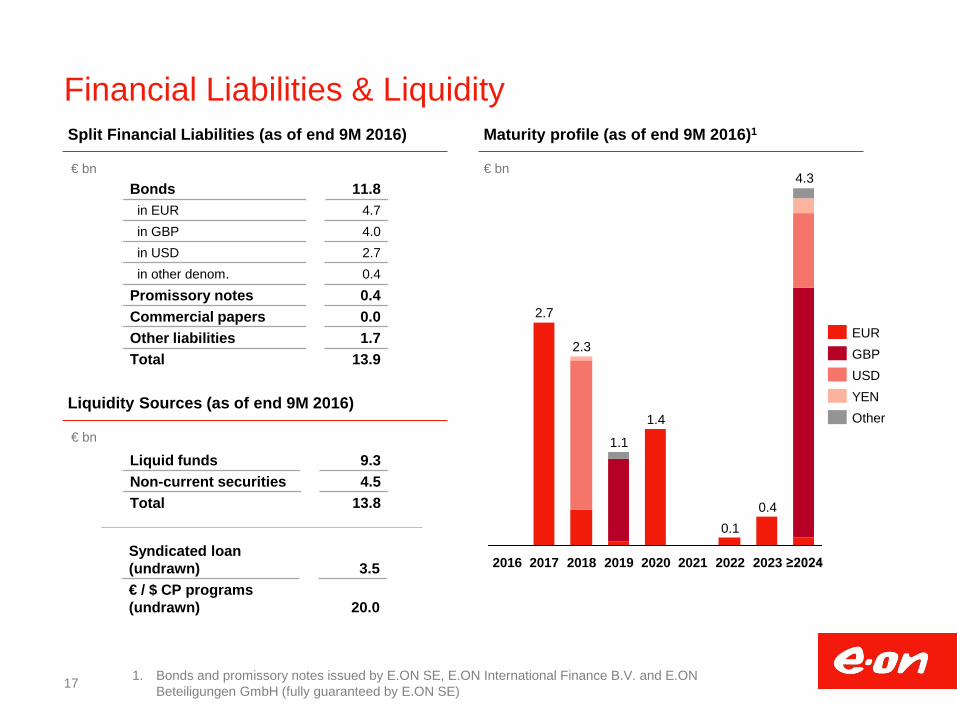

Financial Liabilities & Liquidity

17

Split Financial Liabilities (as of end 9M 2016) Maturity profile (as of end 9M 2016)1

1. Bonds and promissory notes issued by E.ON SE, E.ON International Finance B.V. and E.ON Beteiligungen GmbH (fully guaranteed by E.ON SE)

€ bn

2018

4.3

0.4

1.4

1.1

2.7

2017

0.1

2016 2020 2019 2021 2022 ≥2024 2023

2.3

€ bn

GBP USD

EUR

YEN Other

Bonds 11.8 in EUR 4.7 in GBP 4.0 in USD 2.7 in other denom. 0.4 Promissory notes 0.4 Commercial papers 0.0 Other liabilities 1.7 Total 13.9

Liquidity Sources (as of end 9M 2016)

€ bn

Liquid funds 9.3 Non-current securities 4.5 Total 13.8

Syndicated loan (undrawn) 3.5 € / $ CP programs (undrawn) 20.0

Backup

Financials

Economic net debt

Operations

Spin-off

Reporting calendar & Important links

18

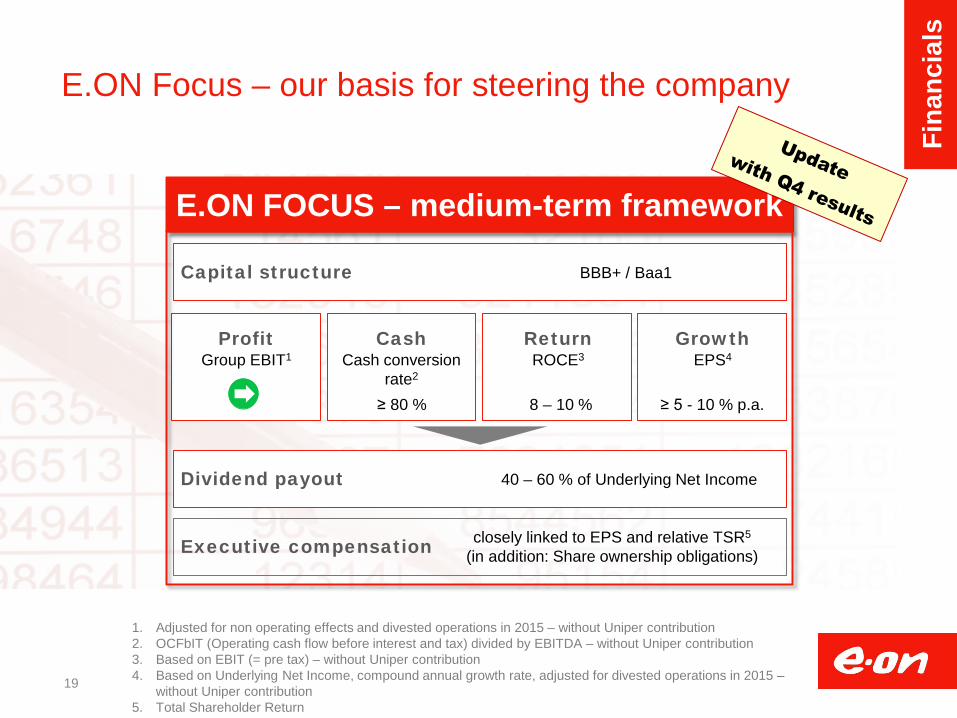

E.ON Focus – our basis for steering the company

Executive compensation

Profit Group EBIT1

Cash Cash conversion

rate2 ≥ 80 %

Return ROCE3

8 – 10 %

Growth EPS4

Capital structure BBB+ / Baa1

Dividend payout 40 – 60 % of Underlying Net Income

E.ON FOCUS – medium-term framework

closely linked to EPS and relative TSR5

(in addition: Share ownership obligations)

≥ 5 - 10 % p.a.

19

1. Adjusted for non operating effects and divested operations in 2015 – without Uniper contribution 2. OCFbIT (Operating cash flow before interest and tax) divided by EBITDA – without Uniper contribution 3. Based on EBIT (= pre tax) – without Uniper contribution 4. Based on Underlying Net Income, compound annual growth rate, adjusted for divested operations in 2015 –

without Uniper contribution 5. Total Shareholder Return

Fina

ncia

ls

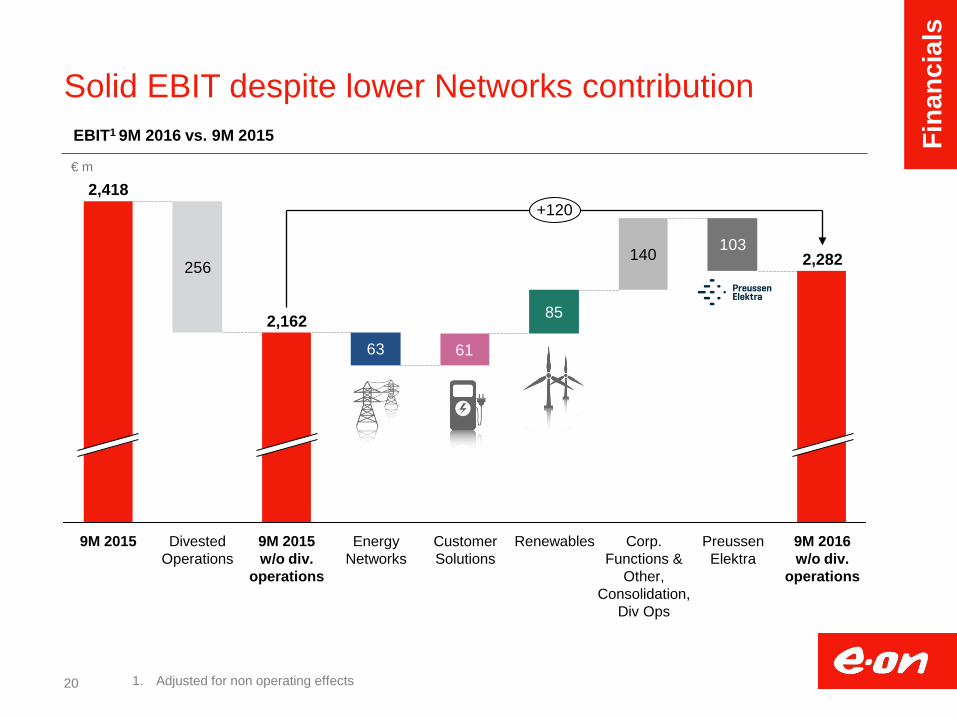

Solid EBIT despite lower Networks contribution

20 1. Adjusted for non operating effects

63 61

85

103140256

Preussen Elektra

2,282

9M 2016 w/o div.

operations

+120

Renewables Corp. Functions &

Other, Consolidation,

Div Ops

Customer Solutions

Energy Networks

9M 2015 w/o div.

operations

2,162

Divested Operations

9M 2015

2,418

EBIT1 9M 2016 vs. 9M 2015

€ m

Fina

ncia

ls

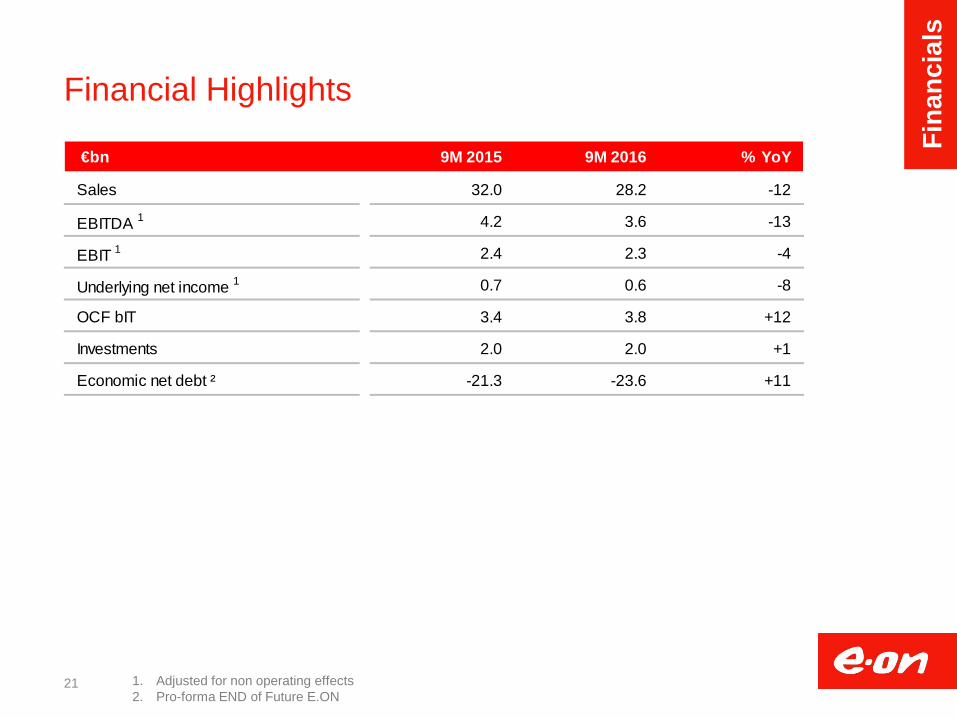

Financial Highlights

21 1. Adjusted for non operating effects 2. Pro-forma END of Future E.ON

€bn 9M 2015 9M 2016 % YoY

Sales 32.0 28.2 -12

EBITDA 1 4.2 3.6 -13

EBIT 1 2.4 2.3 -4

Underlying net income 1 0.7 0.6 -8

OCF bIT 3.4 3.8 +12

Investments 2.0 2.0 +1

Economic net debt ² -21.3 -23.6 +11

Fina

ncia

ls

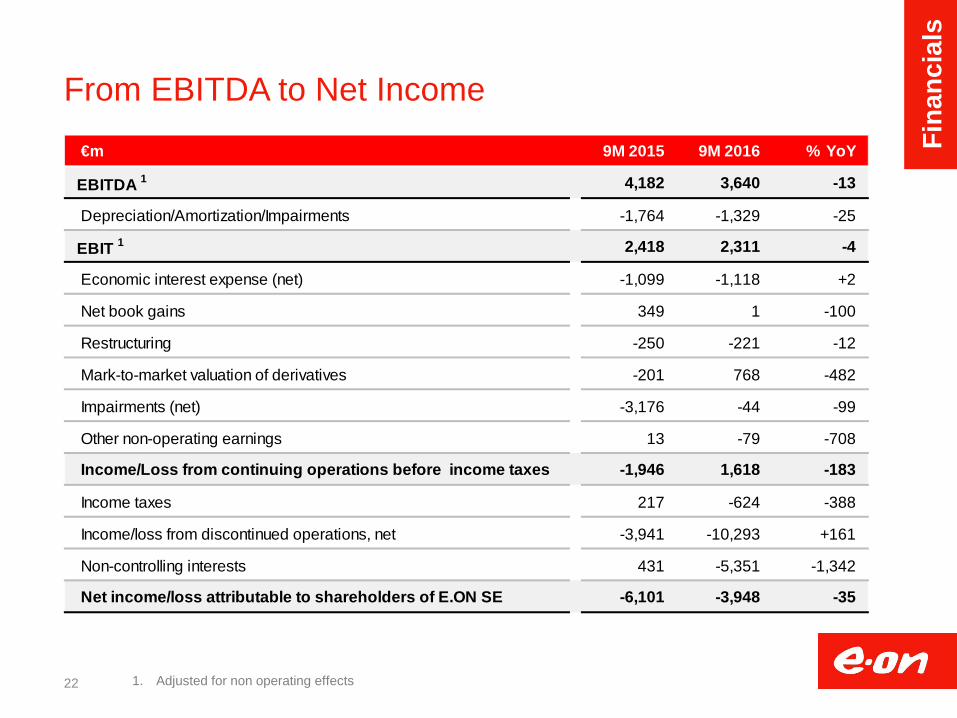

From EBITDA to Net Income

22 1. Adjusted for non operating effects

€m 9M 2015 9M 2016 % YoY

EBITDA 1 4,182 3,640 -13

Depreciation/Amortization/Impairments -1,764 -1,329 -25

EBIT 1 2,418 2,311 -4

Economic interest expense (net) -1,099 -1,118 +2

Net book gains 349 1 -100

Restructuring -250 -221 -12

Mark-to-market valuation of derivatives -201 768 -482

Impairments (net) -3,176 -44 -99

Other non-operating earnings 13 -79 -708

Income/Loss from continuing operations before income taxes -1,946 1,618 -183

Income taxes 217 -624 -388

Income/loss from discontinued operations, net -3,941 -10,293 +161

Non-controlling interests 431 -5,351 -1,342

Net income/loss attributable to shareholders of E.ON SE -6,101 -3,948 -35

Fina

ncia

ls

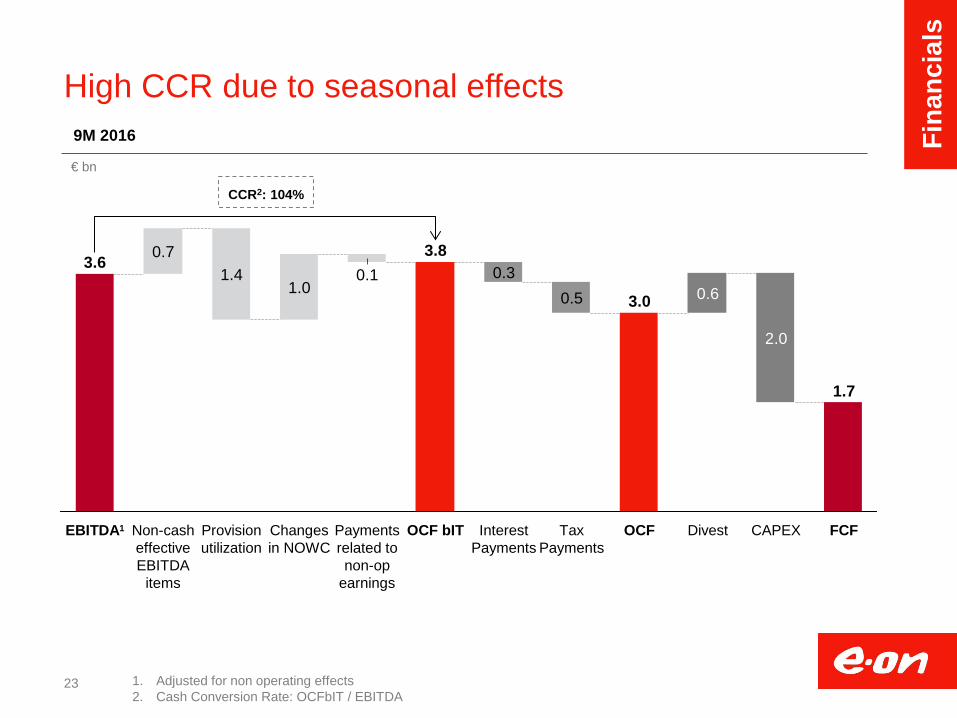

High CCR due to seasonal effects

23

9M 2016

€ bn

Payments related to non-op

earnings

Changes in NOWC

Non-cash effective EBITDA

items

EBITDA1

3.6

Provision utilization

0.7

FCF

2.0

1.7

OCF

3.0

Tax Payments

Interest Payments

OCF bIT

3.8 1.4

1.0 0.1

CAPEX

0.3

Divest

0.5 0.6

1. Adjusted for non operating effects 2. Cash Conversion Rate: OCFbIT / EBITDA

CCR2: 104%

Fina

ncia

ls

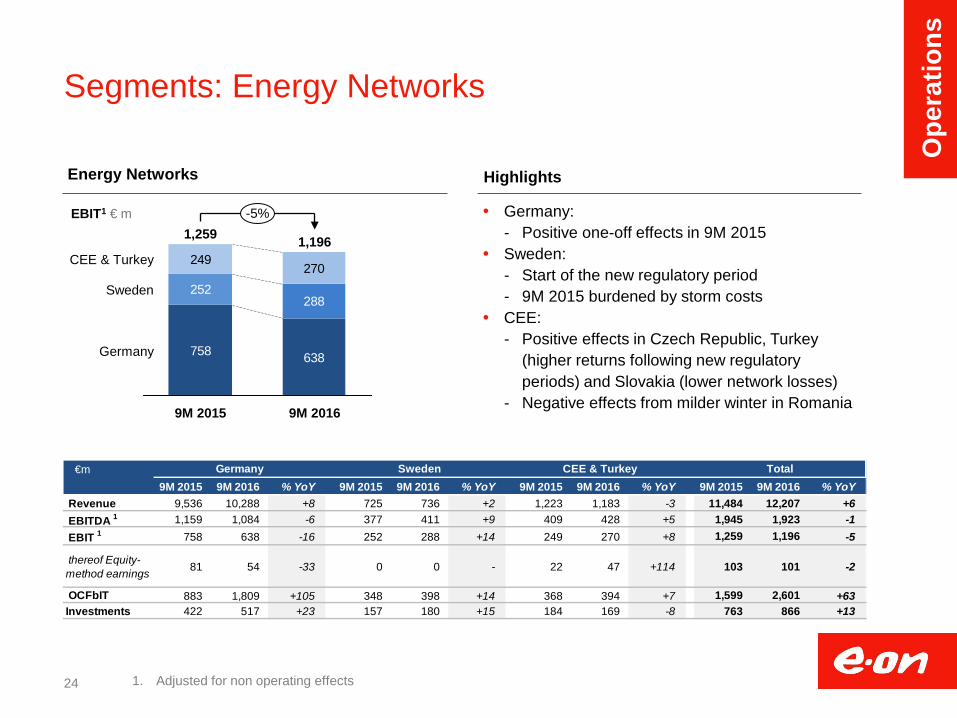

Segments: Energy Networks

Germany: - Positive one-off effects in 9M 2015

Sweden: - Start of the new regulatory period - 9M 2015 burdened by storm costs

CEE: - Positive effects in Czech Republic, Turkey

(higher returns following new regulatory periods) and Slovakia (lower network losses)

- Negative effects from milder winter in Romania

Energy Networks Highlights

EBIT1 € m

758 638

252288

249270

9M 2016 9M 2015

1,196

Germany

1,259 -5%

Sweden

CEE & Turkey

1. Adjusted for non operating effects 24

€m 9M 2015 9M 2016 % YoY 9M 2015 9M 2016 % YoY 9M 2015 9M 2016 % YoY 9M 2015 9M 2016 % YoY

Revenue 9,536 10,288 +8 725 736 +2 1,223 1,183 -3 11,484 12,207 +6 EBITDA 1 1,159 1,084 -6 377 411 +9 409 428 +5 1,945 1,923 -1 EBIT 1 758 638 -16 252 288 +14 249 270 +8 1,259 1,196 -5

thereof Equity-method earnings 81 54 -33 0 0 - 22 47 +114 103 101 -2

OCFbIT 883 1,809 +105 348 398 +14 368 394 +7 1,599 2,601 +63 Investments 422 517 +23 157 180 +15 184 169 -8 763 866 +13

Germany Sweden CEE & Turkey Total

Ope

ratio

ns

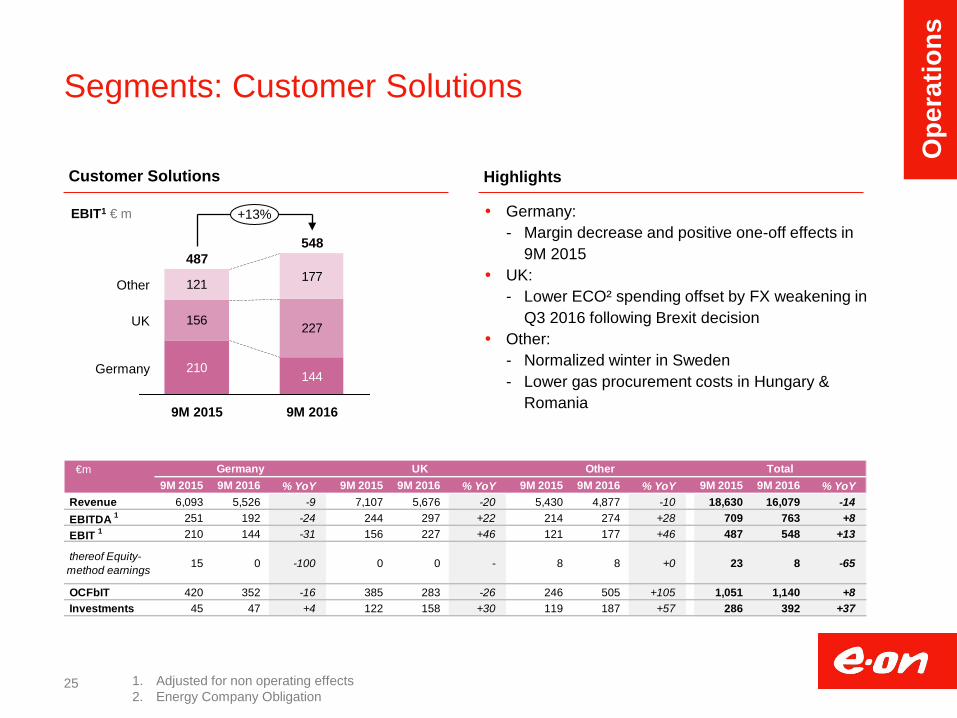

Segments: Customer Solutions

Customer Solutions Highlights

Germany: - Margin decrease and positive one-off effects in

9M 2015 UK:

- Lower ECO² spending offset by FX weakening in Q3 2016 following Brexit decision

Other: - Normalized winter in Sweden - Lower gas procurement costs in Hungary &

Romania

210144

156 227

121 177

UK

+13%

548

Other

Germany

9M 2016 9M 2015

487

1. Adjusted for non operating effects 2. Energy Company Obligation

25

€m 9M 2015 9M 2016 % YoY 9M 2015 9M 2016 % YoY 9M 2015 9M 2016 % YoY 9M 2015 9M 2016 % YoY

Revenue 6,093 5,526 -9 7,107 5,676 -20 5,430 4,877 -10 18,630 16,079 -14 EBITDA 1 251 192 -24 244 297 +22 214 274 +28 709 763 +8 EBIT 1 210 144 -31 156 227 +46 121 177 +46 487 548 +13

thereof Equity-method earnings 15 0 -100 0 0 - 8 8 +0 23 8 -65

OCFbIT 420 352 -16 385 283 -26 246 505 +105 1,051 1,140 +8 Investments 45 47 +4 122 158 +30 119 187 +57 286 392 +37

TotalUKGermany Other

EBIT1 € m

Ope

ratio

ns

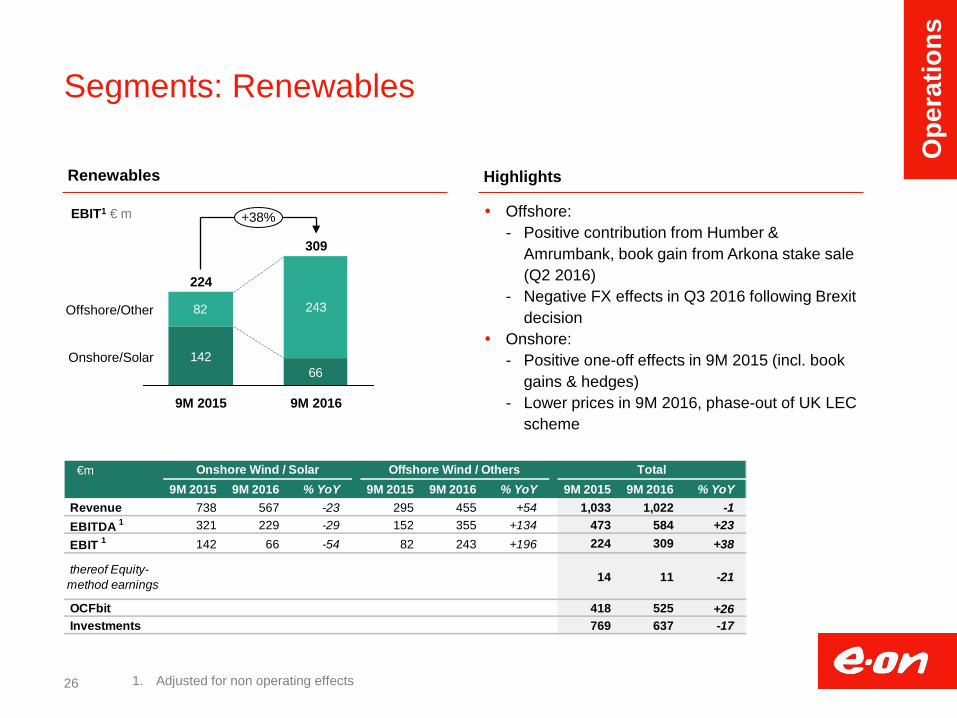

Segments: Renewables

Renewables Highlights

1. Adjusted for non operating effects

14266

82 243Offshore/Other

+38%

9M 2016

309

9M 2015

224

Onshore/Solar

Offshore: - Positive contribution from Humber &

Amrumbank, book gain from Arkona stake sale (Q2 2016)

- Negative FX effects in Q3 2016 following Brexit decision

Onshore: - Positive one-off effects in 9M 2015 (incl. book

gains & hedges) - Lower prices in 9M 2016, phase-out of UK LEC

scheme

26

€m 9M 2015 9M 2016 % YoY 9M 2015 9M 2016 % YoY 9M 2015 9M 2016 % YoY

Revenue 738 567 -23 295 455 +54 1,033 1,022 -1 EBITDA 1 321 229 -29 152 355 +134 473 584 +23 EBIT 1 142 66 -54 82 243 +196 224 309 +38

thereof Equity-method earnings 14 11 -21

OCFbit 418 525 +26 Investments 769 637 -17

Offshore Wind / Others TotalOnshore Wind / Solar

EBIT1 € m

Ope

ratio

ns

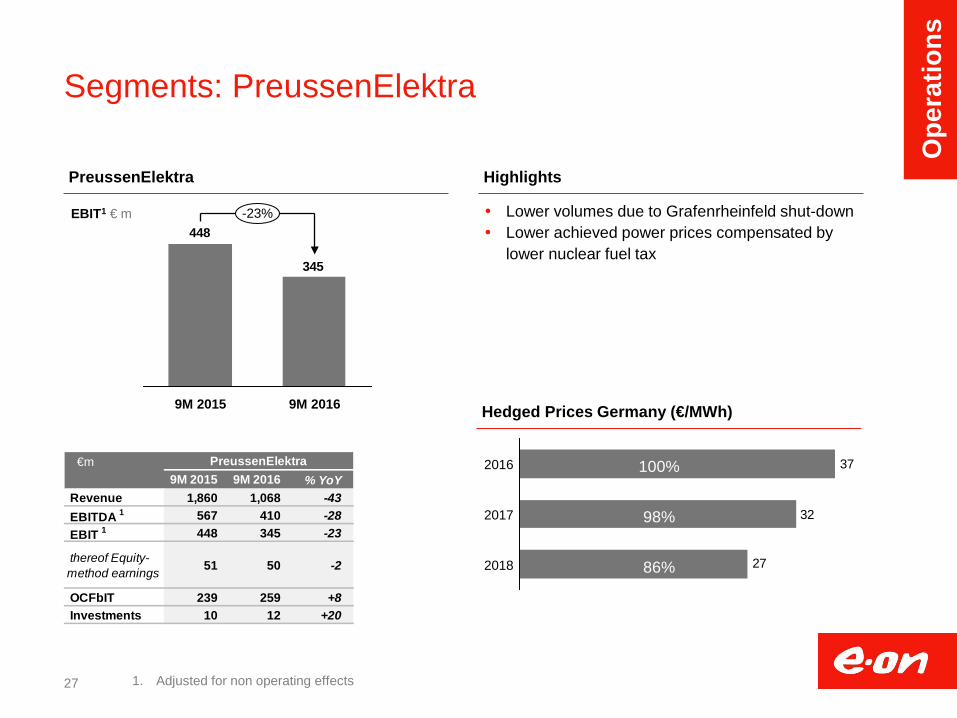

Segments: PreussenElektra

PreussenElektra Highlights

1. Adjusted for non operating effects

345

448-23%

9M 2016 9M 2015

Lower volumes due to Grafenrheinfeld shut-down Lower achieved power prices compensated by

lower nuclear fuel tax

27

€m 9M 2015 9M 2016 % YoY

Revenue 1,860 1,068 -43 EBITDA 1 567 410 -28 EBIT 1 448 345 -23

thereof Equity-method earnings 51 50 -2

OCFbIT 239 259 +8 Investments 10 12 +20

PreussenElektra

32

27

37

2018

2017

2016

Hedged Prices Germany (€/MWh)

100%

98%

86%

EBIT1 € m

Ope

ratio

ns

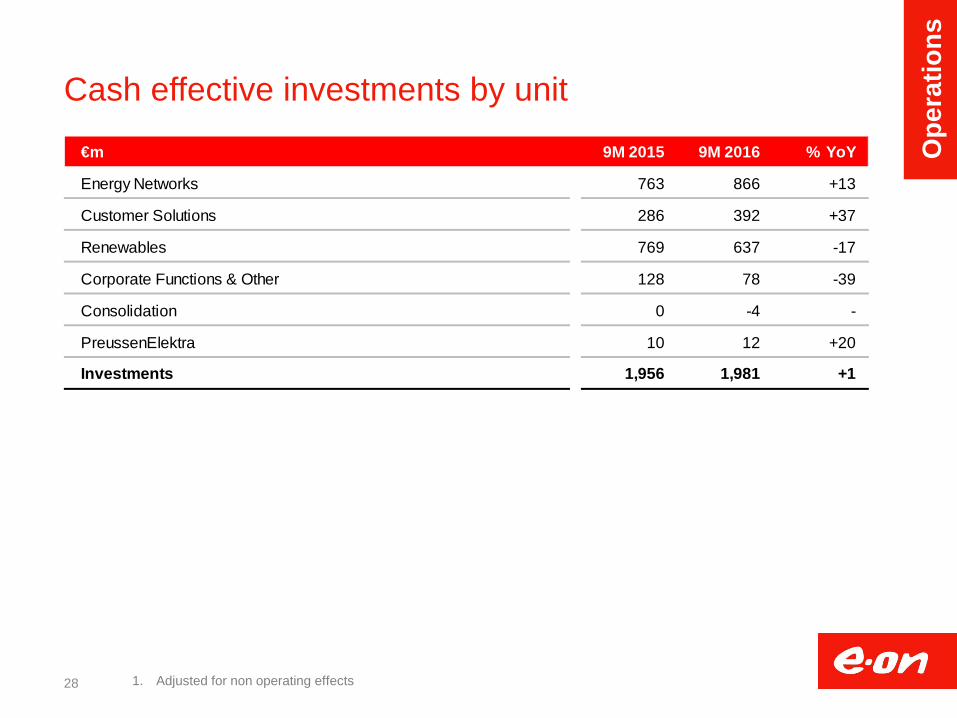

Cash effective investments by unit

28 1. Adjusted for non operating effects

€m 9M 2015 9M 2016 % YoY

Energy Networks 763 866 +13

Customer Solutions 286 392 +37

Renewables 769 637 -17

Corporate Functions & Other 128 78 -39

Consolidation 0 -4 -

PreussenElektra 10 12 +20

Investments 1,956 1,981 +1

Ope

ratio

ns

Economic Net Debt1

29 1. Pro-forma END of Future E.ON 2. Net figure; does not include transactions relating to our operating business or asset management 3. Net of profit and loss sharing agreements with Uniper

€m 31 Dec 2015 30 Sept 2016

Liquid funds 7,829 9,308

Non-current securities 4,536 4,540

Financial liabilities -15,790 -13,878

Adjustment FX hedging ² 218 452

Net Uniper Loan ³ 3,079 0

Net financial position -129 422

Provisions for pensions -3,281 -5,921

Asset retirement obligations -17,930 -18,124

Economic net debt -21,340 -23,623

Econ

omic

net

deb

t

30

1.1 1.6

-0.6

E.ONGroup

DeconsolidationUniper

NewE.ON

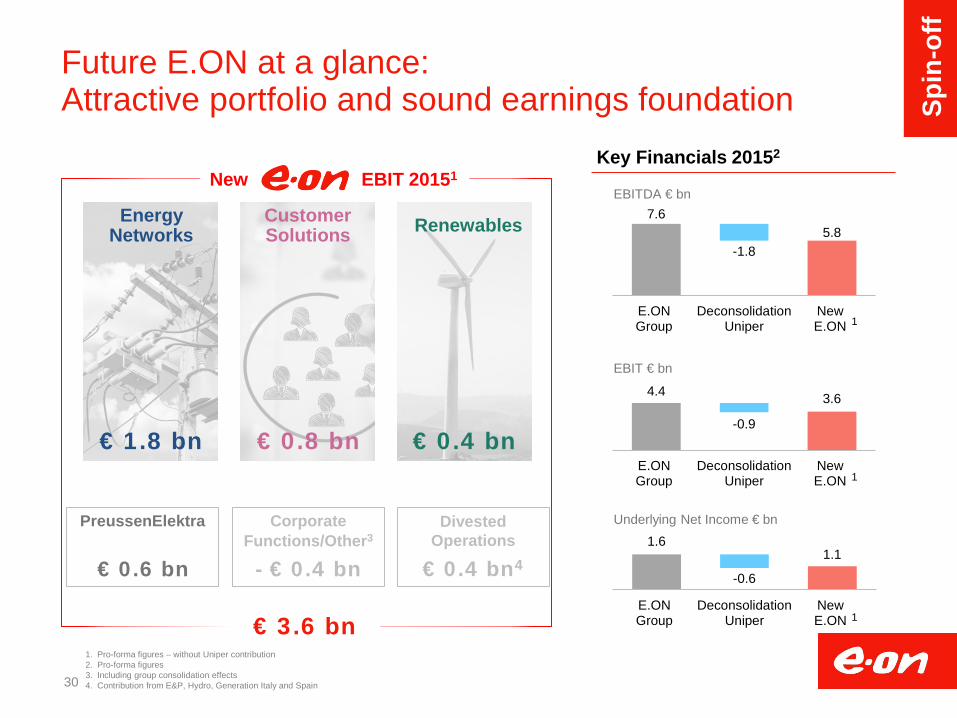

Future E.ON at a glance: Attractive portfolio and sound earnings foundation

Corporate Functions/Other3

PreussenElektra

Energy Networks

€ 1.8 bn € 0.4 bn

- € 0.4 bn € 0.6 bn

Renewables

Key Financials 20152

EBITDA € bn

EBIT € bn

Underlying Net Income € bn

5.8 7.6

-1.8

E.ONGroup

DeconsolidationUniper

NewE.ON

3.6 4.4

-0.9

E.ONGroup

DeconsolidationUniper

NewE.ON

Divested Operations

€ 0.4 bn4

1. Pro-forma figures – without Uniper contribution 2. Pro-forma figures 3. Including group consolidation effects 4. Contribution from E&P, Hydro, Generation Italy and Spain

€ 0.8 bn

Customer Solutions

1

1

1

New EBIT 20151

€ 3.6 bn

Spin

-off

31

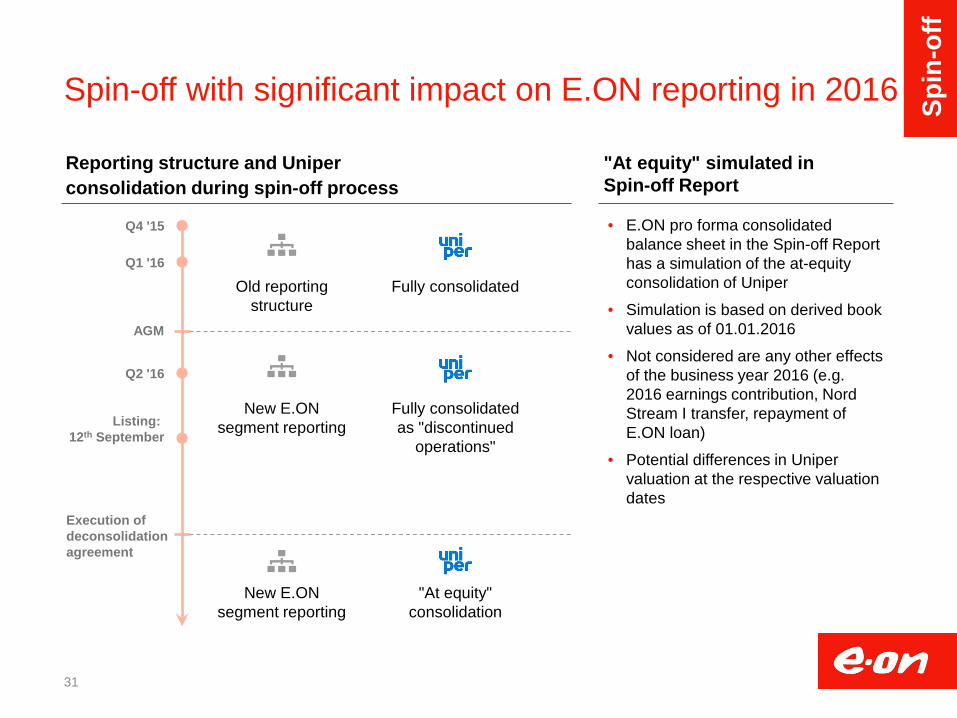

Spin-off with significant impact on E.ON reporting in 2016

AGM

Execution of deconsolidation agreement

Old reporting structure

New E.ON segment reporting

• E.ON pro forma consolidated balance sheet in the Spin-off Report has a simulation of the at-equity consolidation of Uniper

• Simulation is based on derived book values as of 01.01.2016

• Not considered are any other effects of the business year 2016 (e.g. 2016 earnings contribution, Nord Stream I transfer, repayment of E.ON loan)

• Potential differences in Uniper valuation at the respective valuation dates

Fully consolidated

New E.ON segment reporting

Fully consolidated as "discontinued

operations"

"At equity" consolidation

Q4 '15

Q1 '16

Q2 '16

Listing: 12th September

Reporting structure and Uniper consolidation during spin-off process

"At equity" simulated in Spin-off Report

Spin

-off

32

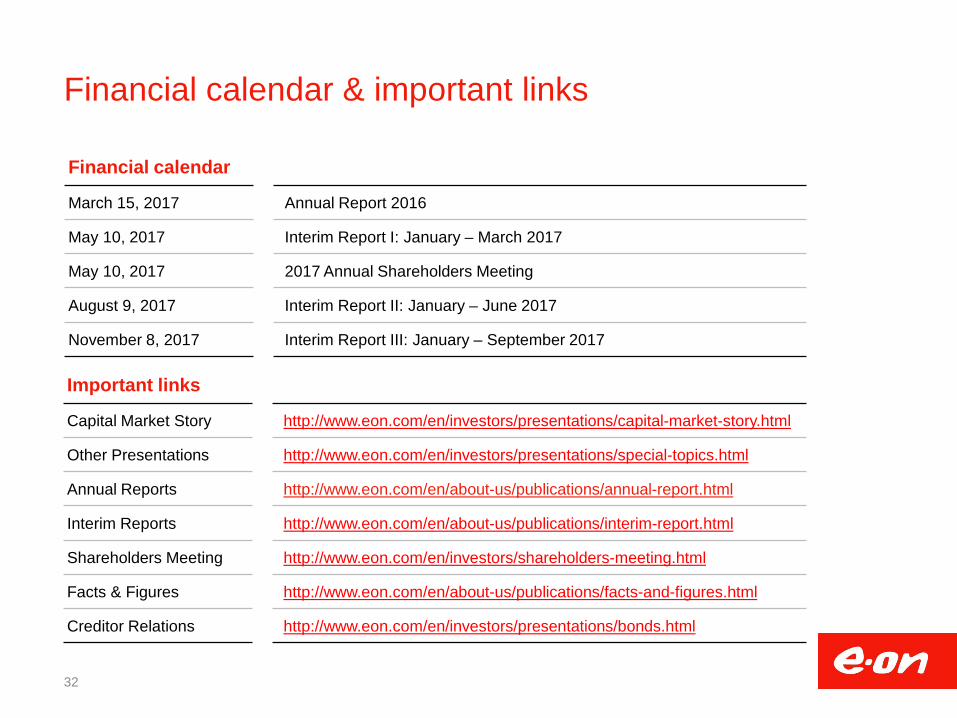

Financial calendar & important links

Important links

Capital Market Story http://www.eon.com/en/investors/presentations/capital-market-story.html

Other Presentations http://www.eon.com/en/investors/presentations/special-topics.html

Annual Reports http://www.eon.com/en/about-us/publications/annual-report.html

Interim Reports http://www.eon.com/en/about-us/publications/interim-report.html

Shareholders Meeting http://www.eon.com/en/investors/shareholders-meeting.html

Facts & Figures http://www.eon.com/en/about-us/publications/facts-and-figures.html

Creditor Relations http://www.eon.com/en/investors/presentations/bonds.html

Financial calendar

March 15, 2017 Annual Report 2016

May 10, 2017 Interim Report I: January – March 2017

May 10, 2017 2017 Annual Shareholders Meeting

August 9, 2017 Interim Report II: January – June 2017

November 8, 2017 Interim Report III: January – September 2017