florida housing finance agency · florida housing finance corporation credit underwriting report...

TRANSCRIPT

____________________________________________________

Florida Housing Finance Corporation

Credit Underwriting Report

MLF Towers

EHCL - #2003-003E

Section A Board Summary

Section B Loan Commitment Conditions

Section C Supporting Information and Schedules ____________________________________________________

Prepared by

Seltzer Management Group, Inc.

Final Review Report

January 8, 2004 ____________________________________________________

SMG ____________________________________________________

Section A

Board Summary

MLF Towers

EHCL PROGRAM CREDIT UNDERWRITING REPORT SMG ___________________________________________________ Executive Summary This is a Florida Housing Finance Corporation (“FHFC” or “Florida Housing”) Elderly Housing Community Loan (“EHCL”) Program credit underwriting report for the MLF Towers, an existing 14-story concrete and steel apartment building consisting of 146 units of affordable housing for the elderly, located at 540 2nd Avenue, South, St. Petersburg, Florida. MLF Towers offers features and amenities that are typical of other high-rise affordable housing developments built in the late 1970s and early 1980s, including a lobby area, elevators, community room, library, dining area, kitchen, game room and laundry facility. This development contains 146 one-bedroom units, and unit features include a fully equipped kitchen, emergency call system, carpeting, and central HVAC. Ownership Structure: The applicant, MLF Housing, Inc. (“MLF”), was organized as a not for profit organization, to acquire an interest in real estate property located in St. Petersburg, and to construct and operate thereon an apartment complex of 146 units under Section 202 of the National Housing Act. Construction was completed in 1981. Its purpose is to provide housing and services to low-income elderly and handicapped persons. Such projects are regulated by the U.S. Department of Housing and Urban Development (“HUD”). Rent subsidies under Section 8 are available to qualifying tenants. The subject’s two major programs are its Section 202 direct loan (discussed below) and Section 8 rent subsidies. An analysis of the credit-worthiness of the applicant was performed by Seltzer Management Group, Inc. (“SMG” or “Seltzer”). In addition, SMG verified the Applicant’s funds on deposit in an amount sufficient to provide the minimum 15% matching fund requirement of the EHCL Program. EHCL Loan: The applicant has applied to Florida Housing for EHCL funds, in the amount of $150,000, to finance the proposed upgrades, life-safety and building preservation (replacement of roof and existing chilling tower), at MLF Towers. The EHCL loan will be non-amortizing with a 15-year term and an interest rate of 1.25% comprised of a base rate of 1% plus servicing fees of .25%. This loan will be in a third mortgage position (see Additional Information – Existing Finance Structure discussion below). Both principal and accrued interest will be due at maturity, and loan services fees (.25%) are due annually. Note that, for HUD Section 202 accounting purposes, the debt service (principal and interest) on this loan should be funded annually as part of the operating budget, in order to justify the higher rent that is required to be in effect to pay this loan off. Therefore, SMG recommends that a reserve account be established in which the applicant be required to submit monthly principal and interest payments, to be held in escrow for future pay-off of this loan. For purposes of this analysis, SMG has incorporated an annual debt service on this loan, equal to a monthly principal and interest payment, amortized over a 15-year term, at an interest rate of 1.25% (inclusive of annual servicing fees). Other Financing Sources: Additional financing sources to fund the proposed improvements are provided by the applicant in the form of matching funds totaling $52,884.

MLF Towers PAGE A - 1

January 8, 2004

EHCL PROGRAM CREDIT UNDERWRITING REPORT SMG ___________________________________________________ The matching funds are proposed to be funded from an existing replacement reserve account. Audited financial statements indicate that this account totaled $243,147 for the year ended, April 30, 2003. Use of funds from the replacement reserve account is subject to HUD approval. The matching funds amount is equal to 35.26% of the requested loan amount, which meets the minimum 15% requirements set forth in FHFC Rule 67-32. Additional Information: 1. Historical Operating Results: Combined (see Existing Financing Structure discussion below)

debt service coverage is calculated at 1.03 for year ended April 30, 2003. It should be noted that Section 8 rental subsidies totaled $930,869 and $897,784 for the years ended April 30, 2003, and 2002, respectively. The Section 8 Contract expires September 24, 2006, and its renewal is uncertain at this time. The subject is economically dependent on the continuation of the Section 8 funding. Further, the subject operates in a regulated environment. The operations of the subject are subject to the administrative directives, rules and regulations of federal, state, and local regulatory agencies, including, but not limited to HUD. Such administrative directives, rules, and regulations are subject to change by an act of congress or an administrative change mandated by HUD. Such changes may occur with little notice or inadequate funding to pay for the related cost, including the additional administrative burden, to comply with the change.

2. Existing Financing Structure: The subject property is encumbered by a note payable, HUD held first mortgage. The current balance is approximately $5,115,000. The note requires monthly payments of $45,057 (or $540,684 annually), including interest at 8.5%. The mortgage (original balance $6,146,100) has a 40-year term and matures in August 2022. The applicant closed on another EHCL loan ($136,892) in March 2002 to finance the replacement of the fire alarm and emergency call systems. All improvements have been completed and the applicant is in compliance with all applicable loan obligations and conditions. This loan has a second mortgage position. In addition, the applicant has received funding from its sponsoring not for profit corporation, Gulfcoast Housing Foundation, Inc., to fund certain operating shortages related to the onsite meals program. The unsecured related party note accrues interest at 8.25% and is repaid only from residual receipts as defined by HUD. With accrued interest, the related party receivable totaled $127,919 at April 30, 2003.

3. HUD Approval: The first mortgage lender, HUD, will not approve the proposed ECHL loan until satisfactory review of all loan documents pertaining to the proposed transaction. Further, HUD must approve and review all bids and specifications for the proposed improvements.

4. Pro Forma NOI: As discussed earlier, the subject’s rental income is dependant upon continued Section 8 rental assistance. Section 8 rents are set by HUD at an amount to provide income sufficient to fund operating expenses, replacement reserve requirements and debt service payments. This recommendation assumes that Section 8 rents will continue to be set at an amount to provide income sufficient to fund operating expenses, replacement reserve requirements, and debt service payments, including amounts necessary to retire the EHCL loan and deferred interest.

Issues and Concerns:

MLF Towers PAGE A - 2

January 8, 2004

EHCL PROGRAM CREDIT UNDERWRITING REPORT SMG ___________________________________________________ None Recommendation: SMG recommends a EHCL Program loan, in the amount of $150,000 be awarded to this development. This recommendation is based upon the assumptions detailed in the Board Summary (Section A) and subject to the Loan Conditions outlined in the Loan Commitment Conditions (Section B). The reader is cautioned to refer to these sections for complete information. Prepared by:

Benjamin S. Johnson President

MLF Towers PAGE A - 3

January 8, 2004

EHCL PROGRAM CREDIT UNDERWRITING REPORT SMG ___________________________________________________

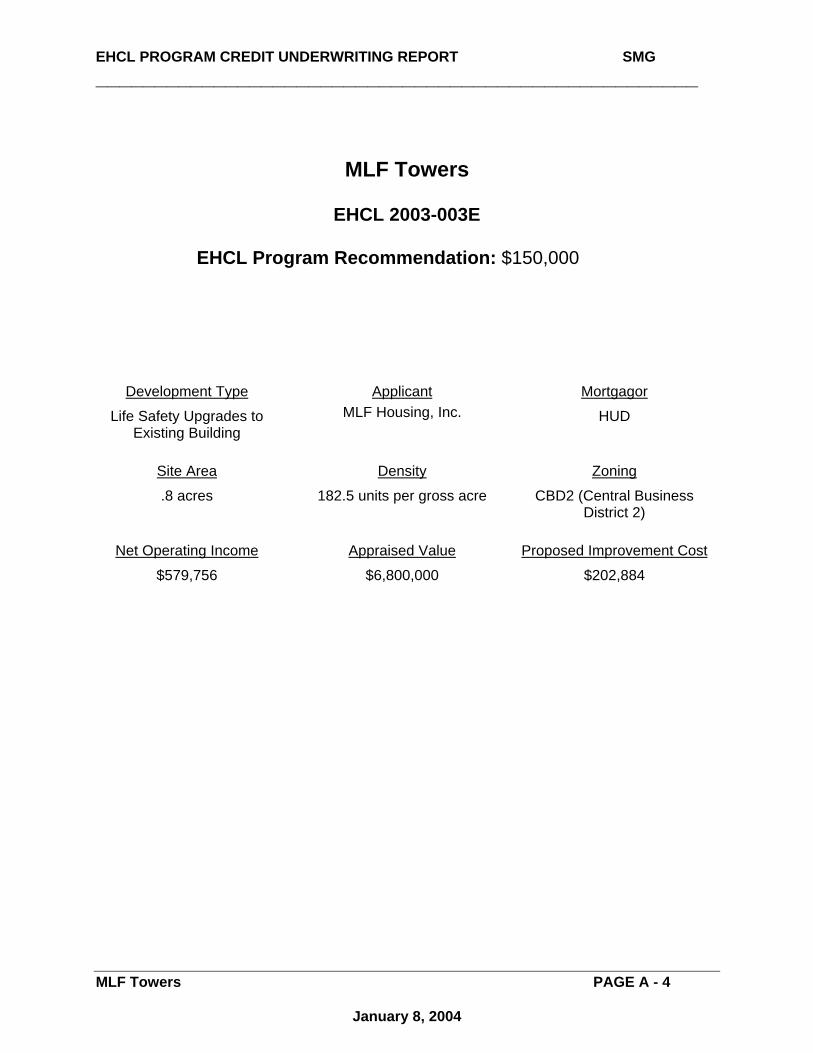

MLF Towers

EHCL 2003-003E

EHCL Program Recommendation: $150,000

Development Type Applicant Mortgagor Life Safety Upgrades to

Existing Building MLF Housing, Inc. HUD

Site Area Density Zoning .8 acres 182.5 units per gross acre CBD2 (Central Business

District 2)

Net Operating Income Appraised Value Proposed Improvement Cost $579,756 $6,800,000 $202,884

MLF Towers PAGE A - 4

January 8, 2004

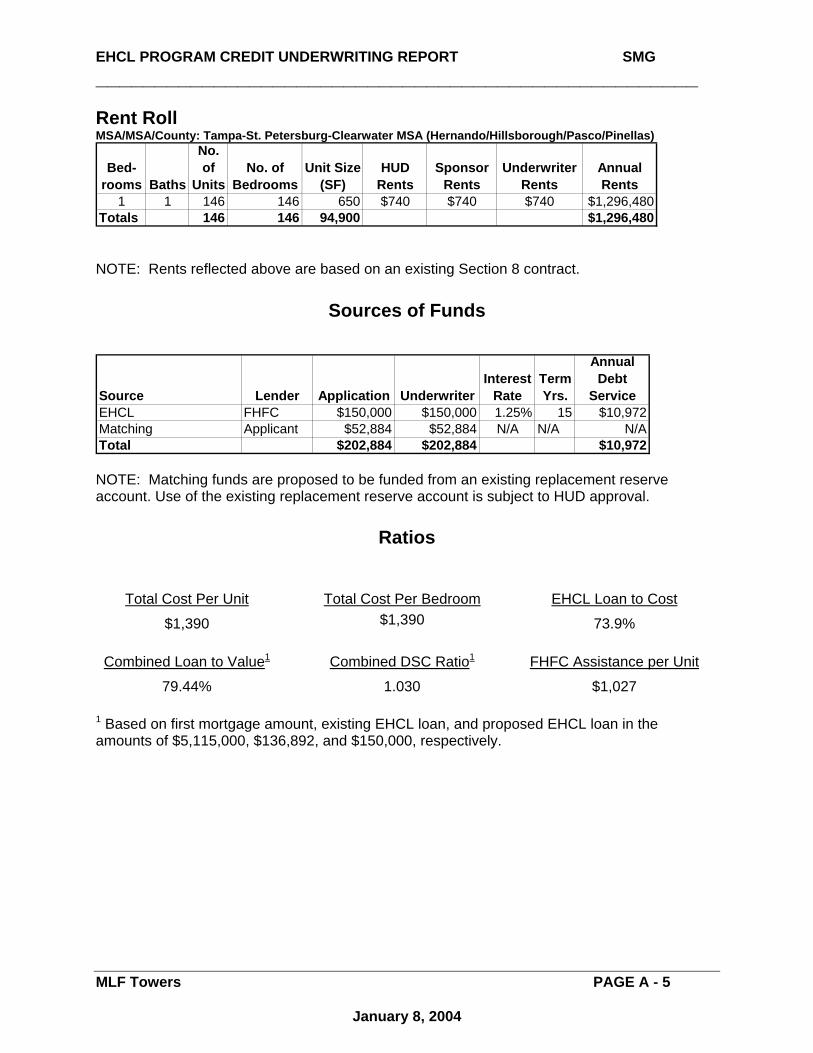

EHCL PROGRAM CREDIT UNDERWRITING REPORT SMG ___________________________________________________ Rent Roll MSA/MSA/County: Tampa-St. Petersburg-Clearwater MSA (Hernando/Hillsborough/Pasco/Pinellas)

Bed-rooms Baths

No. of

UnitsNo. of

BedroomsUnit Size

(SF)HUD

RentsSponsor

RentsUnderwriter

RentsAnnual Rents

1 1 146 146 650 $740 $740 $740 $1,296,480Totals 146 146 94,900 $1,296,480

NOTE: Rents reflected above are based on an existing Section 8 contract.

Sources of Funds

Source Lender Application UnderwriterInterest

RateTerm Yrs.

Annual Debt

ServiceEHCL FHFC $150,000 $150,000 1.25% 15 $10,972Matching Applicant $52,884 $52,884 N/A N/A N/ATotal $202,884 $202,884 $10,972 NOTE: Matching funds are proposed to be funded from an existing replacement reserve account. Use of the existing replacement reserve account is subject to HUD approval.

Ratios

Total Cost Per Unit Total Cost Per Bedroom EHCL Loan to Cost $1,390 $1,390 73.9%

Combined Loan to Value1 Combined DSC Ratio1 FHFC Assistance per Unit 79.44% 1.030 $1,027

1 Based on first mortgage amount, existing EHCL loan, and proposed EHCL loan in the amounts of $5,115,000, $136,892, and $150,000, respectively.

MLF Towers PAGE A - 5

January 8, 2004

EHCL PROGRAM CREDIT UNDERWRITING REPORT SMG ___________________________________________________

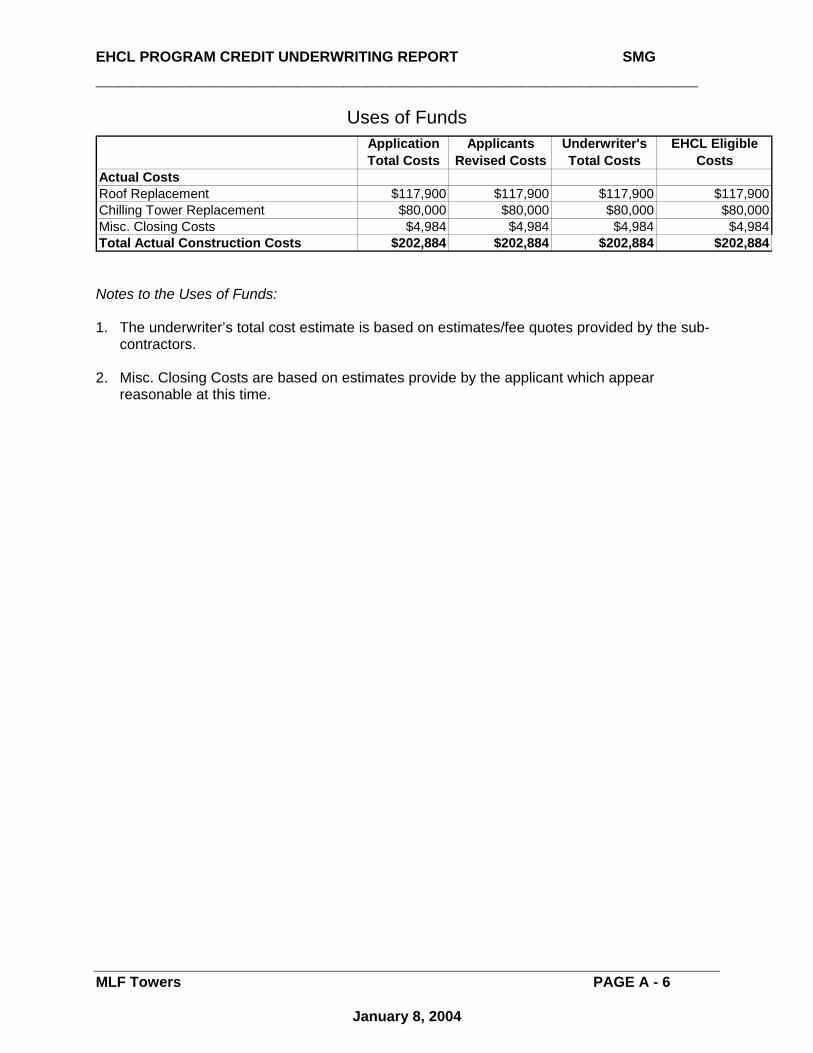

Uses of Funds Application Total Costs

Applicants Revised Costs

Underwriter's Total Costs

EHCL Eligible Costs

Actual CostsRoof Replacement $117,900 $117,900 $117,900 $117,900Chilling Tower Replacement $80,000 $80,000 $80,000 $80,000Misc. Closing Costs $4,984 $4,984 $4,984 $4,984Total Actual Construction Costs $202,884 $202,884 $202,884 $202,884 Notes to the Uses of Funds: 1. The underwriter’s total cost estimate is based on estimates/fee quotes provided by the sub-

contractors. 2. Misc. Closing Costs are based on estimates provide by the applicant which appear

reasonable at this time.

MLF Towers PAGE A - 6

January 8, 2004

EHCL PROGRAM CREDIT UNDERWRITING REPORT SMG ___________________________________________________ Operating – Pro Forma

ANNUAL PER UNIT

$1,333,633 $9,134

$9,000 $62Laundry Income $3,536 $24

$269,300 $1,845$12,356 $85

$1,627,825 $11,149

Vacancy Loss - 3.0% ($48,835) ($334)Collection Loss - 1.0% ($16,278) ($111)

$1,562,712 $10,704

$0 $0$72,373 $496

Management Fees $78,136 $535$41,425 $284

$250,328 $1,715$102,242 $700

$6,080 $42$112,845 $773

$0 $0$67,000 $459

$252,528 $1,730$0 $0

$982,957 $6,733

$579,756 $3,971

$540,684 $3,703$11,344 $78$10,972 $75

$563,000 $3,856

$16,756 $115

TaxesInsurance

Marketing and AdvertisingMaintenance and Repairs

Variable:

General and AdministrativePayroll ExpensesUtilities

DESCRIPTIONRevenue

Gross Potential Rental Revenue

Gross Potential Income

Other Income:Commercial

ServicesMiscellaneous Income

Less:

Total Effective Gross Revenue

ExpensesFixed:

Replacement ReserveOther: ServicesOther:

Grounds Maintenance and Landscaping

Total Expenses

Net Operating Income

Debt Service PaymentsFirst MortgageEHCL - existingEHCL - proposed

Total Debt Service Payments

Operating Income After Debt Service - Before Tax Cash Flow

MLF Towers PAGE A - 7

January 8, 2004

EHCL PROGRAM CREDIT UNDERWRITING REPORT SMG ___________________________________________________

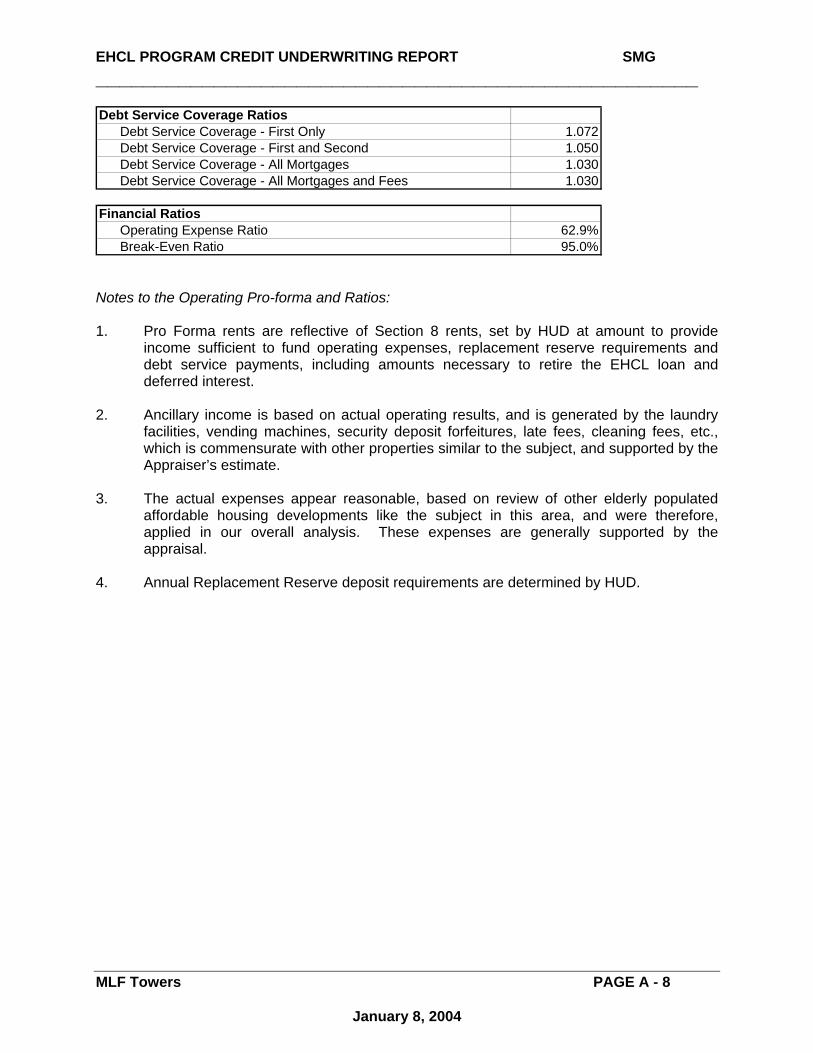

1.0721.0501.0301.030

62.9%95.0%

Debt Service Coverage RatiosDebt Service Coverage - First Only

Operating Expense RatioBreak-Even Ratio

Debt Service Coverage - First and SecondDebt Service Coverage - All MortgagesDebt Service Coverage - All Mortgages and Fees

Financial Ratios

Notes to the Operating Pro-forma and Ratios: 1. Pro Forma rents are reflective of Section 8 rents, set by HUD at amount to provide

income sufficient to fund operating expenses, replacement reserve requirements and debt service payments, including amounts necessary to retire the EHCL loan and deferred interest.

2. Ancillary income is based on actual operating results, and is generated by the laundry

facilities, vending machines, security deposit forfeitures, late fees, cleaning fees, etc., which is commensurate with other properties similar to the subject, and supported by the Appraiser’s estimate.

3. The actual expenses appear reasonable, based on review of other elderly populated

affordable housing developments like the subject in this area, and were therefore, applied in our overall analysis. These expenses are generally supported by the appraisal.

4. Annual Replacement Reserve deposit requirements are determined by HUD.

MLF Towers PAGE A - 8

January 8, 2004

SMG ____________________________________________________

Section B

Loan Commitment Conditions

January 8, 2004

EHCL PROGRAM CREDIT UNDERWRITING REPORT SMG ____________________________________________________ Elderly Housing Community Loan (EHCL) Program Recommendation

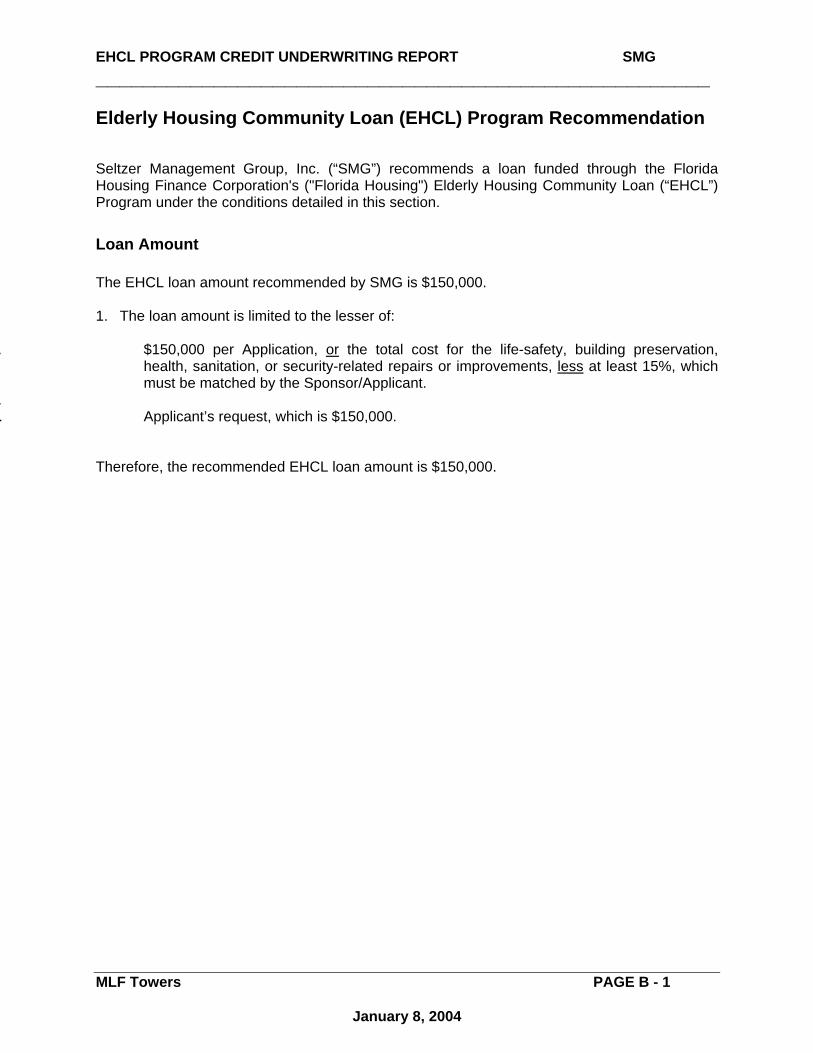

Seltzer Management Group, Inc. (“SMG”) recommends a loan funded through the Florida Housing Finance Corporation's ("Florida Housing") Elderly Housing Community Loan (“EHCL”) Program under the conditions detailed in this section.

Loan Amount The EHCL loan amount recommended by SMG is $150,000. 1. The loan amount is limited to the lesser of:

. $150,000 per Application, or the total cost for the life-safety, building preservation,

health, sanitation, or security-related repairs or improvements, less at least 15%, which must be matched by the Sponsor/Applicant.

.

. Applicant’s request, which is $150,000. Therefore, the recommended EHCL loan amount is $150,000.

MLF Towers PAGE B - 1

January 8, 2004

EHCL PROGRAM CREDIT UNDERWRITING REPORT SMG ____________________________________________________

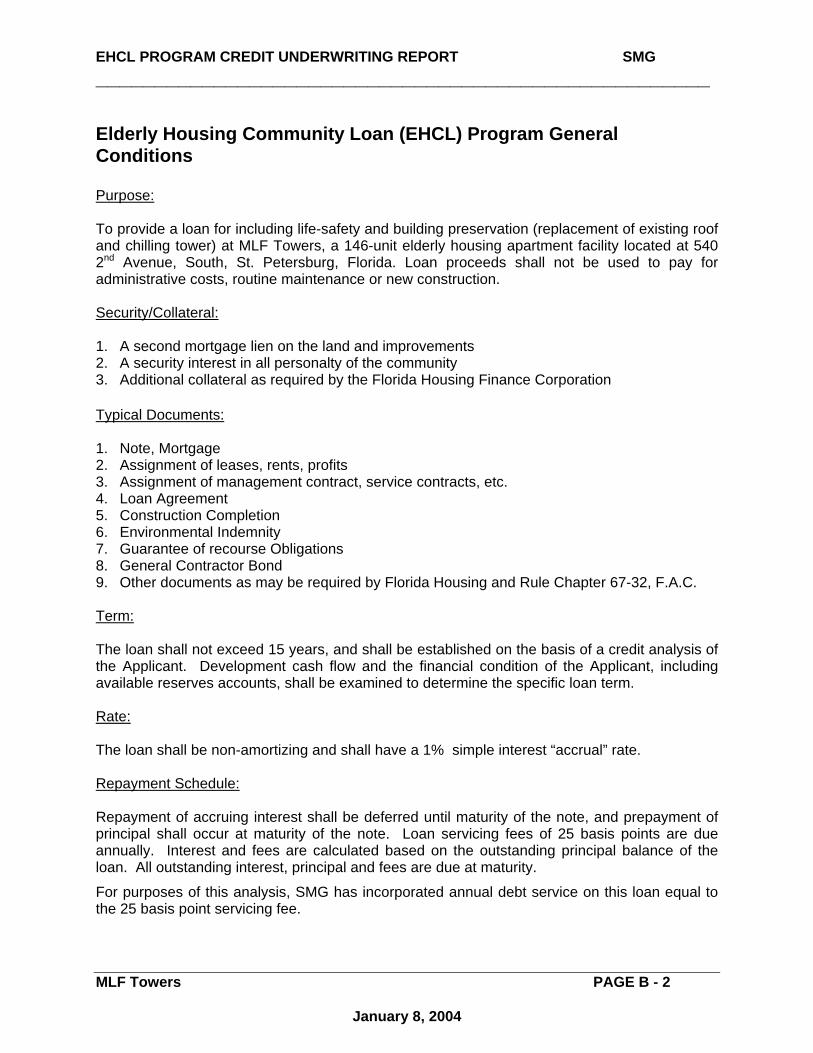

Elderly Housing Community Loan (EHCL) Program General Conditions Purpose: To provide a loan for including life-safety and building preservation (replacement of existing roof and chilling tower) at MLF Towers, a 146-unit elderly housing apartment facility located at 540 2nd Avenue, South, St. Petersburg, Florida. Loan proceeds shall not be used to pay for administrative costs, routine maintenance or new construction. Security/Collateral: 1. A second mortgage lien on the land and improvements 2. A security interest in all personalty of the community 3. Additional collateral as required by the Florida Housing Finance Corporation Typical Documents: 1. Note, Mortgage 2. Assignment of leases, rents, profits 3. Assignment of management contract, service contracts, etc. 4. Loan Agreement 5. Construction Completion 6. Environmental Indemnity 7. Guarantee of recourse Obligations 8. General Contractor Bond 9. Other documents as may be required by Florida Housing and Rule Chapter 67-32, F.A.C. Term: The loan shall not exceed 15 years, and shall be established on the basis of a credit analysis of the Applicant. Development cash flow and the financial condition of the Applicant, including available reserves accounts, shall be examined to determine the specific loan term. Rate: The loan shall be non-amortizing and shall have a 1% simple interest “accrual” rate. Repayment Schedule: Repayment of accruing interest shall be deferred until maturity of the note, and prepayment of principal shall occur at maturity of the note. Loan servicing fees of 25 basis points are due annually. Interest and fees are calculated based on the outstanding principal balance of the loan. All outstanding interest, principal and fees are due at maturity. For purposes of this analysis, SMG has incorporated annual debt service on this loan equal to the 25 basis point servicing fee.

MLF Towers PAGE B - 2

January 8, 2004

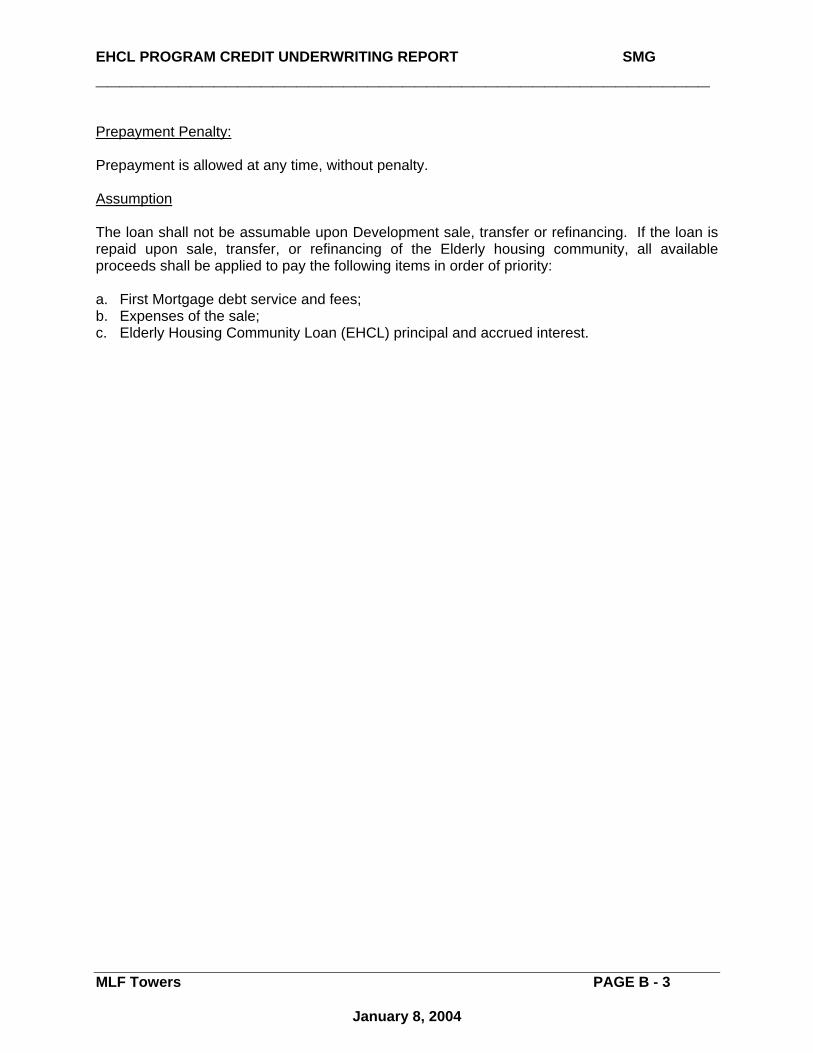

EHCL PROGRAM CREDIT UNDERWRITING REPORT SMG ____________________________________________________ Prepayment Penalty: Prepayment is allowed at any time, without penalty. Assumption The loan shall not be assumable upon Development sale, transfer or refinancing. If the loan is repaid upon sale, transfer, or refinancing of the Elderly housing community, all available proceeds shall be applied to pay the following items in order of priority: a. First Mortgage debt service and fees; b. Expenses of the sale; c. Elderly Housing Community Loan (EHCL) principal and accrued interest.

MLF Towers PAGE B - 3

January 8, 2004

EHCL PROGRAM CREDIT UNDERWRITING REPORT SMG ____________________________________________________ Conditions This recommendation is contingent upon the review and approval of the following items by SMG and Florida Housing at least two weeks prior to closing. Failure to submit these items within this time frame may result in postponement of the closing date. 1. Building permits and any other necessary approvals and permits required to implement

the improvements or a letter from the local permitting and/or approval authority stating that all necessary permits and approvals will be issued upon receipt of applicable fees. If a letter is provided, copies of all permits will be required as a condition to the first post-closing draw.

2. Final sources and uses of funds, itemized by source and line item, in a format and in amounts approved by the Servicer. A detailed calculation of the construction interest based on the final draw schedule (see below), documentation of the closing costs, and draft loan closing statement must also be provided. The final sources and uses of funds schedule will be attached to the Loan Agreement as the approved Development budget.

3. Final draw schedule to be approved prior to closing, itemized by line item, and showing the sources of funds for monthly draws. Loan funds must be disbursed pro rata with Borrower’s contribution and all other loan funds.

4. Evidence of general liability, flood (if applicable), builder’s risk and replacement cost hazard insurance reflecting Florida Housing as Loss Payee/ Mortgagee, in coverages, deductibles and amounts satisfactory to Florida Housing.

5. HUD approval of funding 15% match, if match will be funded from existing replacement reserve account.

6. If a reserve account is required, HUD approval to establish a reserve account into which the applicant submits monthly principal and interest payments, to be held in escrow for future pay-off of the Loan.

This recommendation is contingent upon the review and approval of the following items by Florida Housing and its legal counsel at least two weeks before closing. Failure to receive approval of these items within this time frame may result in postponement of the closing date.

1. Title insurance binder or commitment for title insurance with copies of all Schedule B exceptions in the amount of the Loan.

2. Evidence of general liability, flood (if applicable), builder’s risk and replacement cost hazard insurance reflecting Florida Housing as Loss Payee/ Mortgagee, in coverages, deductibles and amounts satisfactory to Florida Housing.

3. Receipt of a legal opinion from the Borrower's counsel acceptable to Florida Housing addressing the following matters:

a. The legal existence and good standing of the Borrower and of any partnership that is the general partner of the Borrower (the "GP") and of any corporation or partnership that is the managing general partner of the GP and of any corporate guarantor;

b. The due authorization, execution, and delivery by the Borrower and the guarantors, of all Loan documents;

MLF Towers PAGE B - 4

January 8, 2004

EHCL PROGRAM CREDIT UNDERWRITING REPORT SMG ____________________________________________________

c. The Loan documents being in full force and effect and enforceable in accordance with their terms, subject to bankruptcy and equitable principles only;

d. That the Borrower and the Development are in compliance with all laws and regulations applicable to the construction, development and operation of the Development, and that all permits required for construction, rehabilitation and operation of the Development and any improvements related thereto have been obtained and are in full force and effect;

e. The Borrower's and the corporate guarantor's execution, delivery and performance of the Loan documents shall not result in a violation of, or conflict with, any judgments, orders, contracts, mortgages, security agreements or leases to which the Borrower is a party or to which the Development is subject;

f. Such other matters as Florida Housing or its counsel may require. 4. Such other assignments, affidavits, certificates, financial statements, closing statements

and other documents as may be reasonably requested by Florida Housing or its counsel in form and substance acceptable to Florida Housing or its counsel, in connection with the Loan.

5. Documentation of the legal formation and current authority to transact business in Florida for the Borrower, the general partner/principal(s) of the Borrower, the guarantors, and any limited partners of the Borrower.

6. Building permits and any other necessary approvals and permits required to implement the improvements or a letter from the local permitting and/or approval authority stating that all necessary permits and approvals will be issued upon receipt of applicable fees. If a letter is provided, copies of all permits will be required as a condition to the first post-closing draw.

7. Construction contract or contracts pertaining to improvements to be made with the Loan. 8. Any other reasonable conditions established by Florida Housing and its counsel.

This recommendation is also contingent upon satisfaction of the following additional conditions. 1. Compliance with all provisions of Section 420.5087, Florida Statutes and Chapter 67-32,

Florida Administrative Code (the statute and rule governing the EHCL Program). 2. Satisfactory achievement or completion of all conditions and requirements of the credit

underwriting report. 3. Acceptance by the Borrower and execution of all documents evidencing and securing

the Loan in form and substance satisfactory to Florida Housing, including, but not limited to, the Promissory Note, the Loan Agreement, and the Mortgage and Security Agreement, setting forth the terms of this commitment letter.

4. At all times there will be undisbursed loan funds (collectively held by Florida Housing, the First Lender and any other sources) sufficient to complete the improvements. If at any time there are not sufficient funds (held by Florida Housing, First Lender and any other sources) to complete the improvements, the Borrower will be required to expend additional equity on the improvement costs or to deposit additional equity with Florida Housing which is sufficient (in Florida Housing's judgment) to complete the improvements before additional Loan funds are disbursed.

5. Construction Completion Guarantee from MLF Housing, Inc.

MLF Towers PAGE B - 5

January 8, 2004

EHCL PROGRAM CREDIT UNDERWRITING REPORT SMG ____________________________________________________

6. Environmental Indemnity from MLF Housing, Inc. 7. Consultech is to act as Florida Housing’s inspector during the construction period. 8. A mortgagee title insurance policy naming Florida Housing as the insured in the amount

of the Loan to be issued at closing. Any exceptions to the title insurance policy must be acceptable to Florida Housing.

9. Property tax and hazard insurance escrow to be established and maintained by the First Lender or the Servicer.

10. If applicable, a reserve account in which the Borrower will be required to submit monthly principal and interest payments, plus loan servicing fees to be held in escrow by the First Lender or the Servicer. Note for HUD Section 236 accounting purposes, the debt service (principal and interest) on this Loan should be funded annually in the budget, in order to justify the higher rent that is required to be in effect to pay off the Loan.

11. Draw requests subsequent to the first draw request require lien releases from all parties filing notices to owner, acknowledging receipt of all payments due as of the date of the prior draw.

12. Evidence of work in place and amounts due contractors for work completed (or amounts due to Borrower as reimbursement for prior payments to contractors for completed work) is required prior to disbursement of any EHCL funds.

13. Receipt of a draw request and any reasonably required supporting documentation in the format prescribed by the Servicer and Florida Housing. Supporting documentation may include lien releases, title insurance endorsements or other documentation.

14. EHCL funds to be disbursed pro rata with Borrower’s matching contribution funds. 15. A Replacement Reserve Fund shall be maintained by the first mortgagee or Florida

Housing, for the term of the Loan at a minimum amount of $462 per unit annually ($5,583 monthly), as required by the first mortgagee/HUD, and as approved by the Servicer.

16. The receipt by Florida Housing of annual audited financial and operating statements on subject Development and all guarantors.

17. Any other reasonable requirements of the Servicer, Florida Housing and its legal counsel.

MLF Towers PAGE B - 6

January 8, 2004

EHCL PROGRAM CREDIT UNDERWRITING REPORT SMG ____________________________________________________

Section C

Supporting Information and Schedules

____________________________________________________

EHCL PROGRAM CREDIT UNDERWRITING REPORT SMG

Development Information Location: 540 2nd Avenue, South, St. Petersburg, Florida 33701 County: Pinellas County MSA: Tampa-St.Petersburg-Clearwater

(Hernando/Hillsborough/Pasco/Pinellas) Acreage: .8 acres Zoning: CBD2 (Central Business District 2) Density: 182.5 units/ acre, which is typical in this high-rise market Flood Zone: C, no flood insurance required Site Control: Own Acquisition Method: Not Applicable Acquisition Details: Not Applicable Development Type: Life safety upgrades to existing building Year Built: Construction completion - 1981 Construction Type: 14-story high rise Units: 146 units Dwelling Buildings: One 14-Story High Rise Accessory Buildings: None Square Footage: Approximately 94,900

Improvements Description: This is an existing 14-story concrete and steel apartment building

consisting of a 146-unit affordable housing development for the elderly, located 540 2nd Avenue, South, St. Petersburg, Florida. MLF Towers offers features and amenities that are typical of other high-rise affordable housing developments built in the 1970s, including a lobby area, elevators, community room, library, dining area, kitchen, game room, and laundry facility. This development contains 146 one-bedroom units, and unit features include a fully equipped kitchen, emergency call system, carpeting, and central HVAC. Many of the units have newer appliances, although some of the original cabinets and build-out appeared to be somewhat dated. Overall, it is estimated that

MLF Towers PAGE C-1 January 8, 2004

EHCL PROGRAM CREDIT UNDERWRITING REPORT SMG

the subject’s effective age is 25 years, with a remaining economic life of 30 years.

Other than grab bars and emergency pull stings, the units have not been modified for handicapped accessibility. The Americans with Disability Act (ADA) is a non-enforceable Federal guideline.

Proposed Use of EHCL Funds: To provide life-safety and building preservation improvements of the

subject. Specifically, the replacement of existing roof and chilling tower.

Unit Mix: 146 One Bedroom/One Bath units Site Inspection: At the time of inspection, August 2003, the subject was considered in

average to good condition. The lobby and surrounding areas were in good condition and appeared to be well maintained. Subject is a short distance from several hospitals and many professional medical services offices are within walking distance. In addition, the subject is only a short distance from Al Lang stadium, the St. Petersburg Pier, and the waterfront. Shopping, church, and park facilities are also nearby.

. Surrounding sites have been developed with uses compatible with the subject zoning. Utilities available to the site include water, sewer, electric, telephone, and trash collection.

Appraised Value: A Limited Appraisal (Income Approach to Value Only) in Summary

Format was completed by Value Tech Realty Services, Inc. The resulting “as is” market value of the fee simple interest of the subject property, as restricted by the HUD 202 funding program utilizing a market capitalization rate is $6,800,000.

Market Study: SMG has performed an independent analysis of the subject market. SMG concludes that there is sufficient demand in the area for this type of development.

The subject’s average occupancy over the last three-year period has exceeded 98%. Currently, there is a waiting list. Strong occupancy is also indicative of comparable properties.

Property Conditions Report: SMG has relied upon a property condition report, dated September 29,

2003, performed by HUD. The property scored 95 points (total points available – 100). In addition, the report noted no health and safety violations. A site visit performed by SMG indicated no significant defects or deferred maintenance.

MLF Towers PAGE C-2 January 8, 2004

EHCL PROGRAM CREDIT UNDERWRITING REPORT SMG

Borrower Information Borrower Name: MLF Housing, Inc. Borrower Type: A Florida Not-For-Profit 501 (c)(3) Corporation. Ownership Structure: The applicant, MLF Housing, Inc. (“MLF”), was organized as a not for

profit organization, to acquire an interest in real estate property located in St. Petersburg, and to construct and operate thereon an apartment complex of 146 units under Section 202 of the National Housing Act. Construction was completed in 1981. Its purpose is to provide housing and services to low-income elderly and handicapped persons. Such projects are regulated by the U.S. Department of Housing and Urban Development (“HUD”). Rent subsidies under Section 8 are available to qualifying tenants. The subject’s two major programs are its Section 202 direct loan and Section 8 rent subsidies.

This non-profit entity is sponsored by the Gulfcoast Housing Foundation, Inc.

Contact Person(s): Judy Pennala (727) 578-1174 Applicant Address: 11300 4th Street North, Suite 200 St. Petersburg, Fl., 33716 Federal Employer ID: 59-1904656 Experience: MLF is a non-profit organization that has owned and operated this

facility for the past 20 years. Credit Evaluation: An analysis of the credit-worthiness of the Applicant was performed by

SMG. In addition, SMG has verified the applicant’s funds on deposit in an amount sufficient to provide the 15% matching fund requirement of the EHCL Program.

The business report by Dun & Bradstreet on MLF revealed an overall “Good” credit appraisal with no derogatory information.

Banking References: The applicant provided banking references, which revealed no

derogatory information. Financial Statements: The applicant provided financial statements for the past two years,

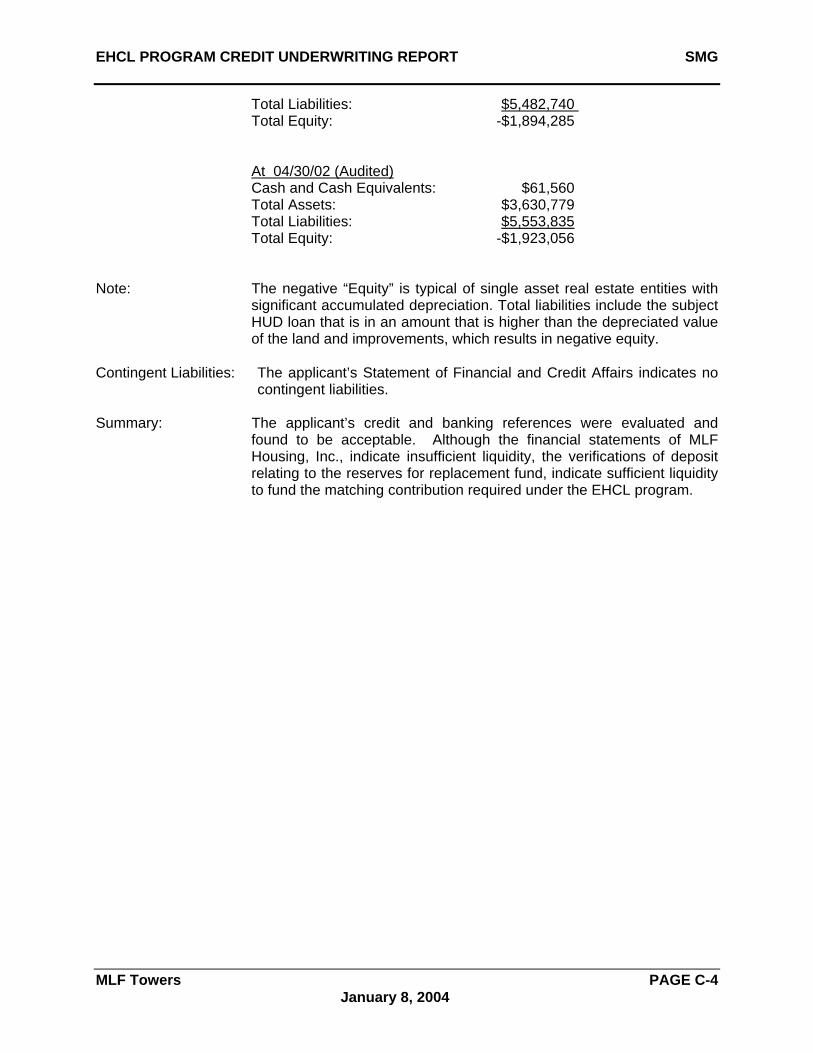

which are summarized as follows: At 4/30/03 (Audited) Cash and Cash Equivalents: $19,649 Total Assets: $3,588,455

MLF Towers PAGE C-3 January 8, 2004

EHCL PROGRAM CREDIT UNDERWRITING REPORT SMG

Total Liabilities: $5,482,740 Total Equity: -$1,894,285 At 04/30/02 (Audited) Cash and Cash Equivalents: $61,560 Total Assets: $3,630,779 Total Liabilities: $5,553,835 Total Equity: -$1,923,056 Note: The negative “Equity” is typical of single asset real estate entities with

significant accumulated depreciation. Total liabilities include the subject HUD loan that is in an amount that is higher than the depreciated value of the land and improvements, which results in negative equity.

Contingent Liabilities: The applicant’s Statement of Financial and Credit Affairs indicates no

contingent liabilities. Summary: The applicant’s credit and banking references were evaluated and

found to be acceptable. Although the financial statements of MLF Housing, Inc., indicate insufficient liquidity, the verifications of deposit relating to the reserves for replacement fund, indicate sufficient liquidity to fund the matching contribution required under the EHCL program.

MLF Towers PAGE C-4 January 8, 2004

EHCL PROGRAM CREDIT UNDERWRITING REPORT SMG

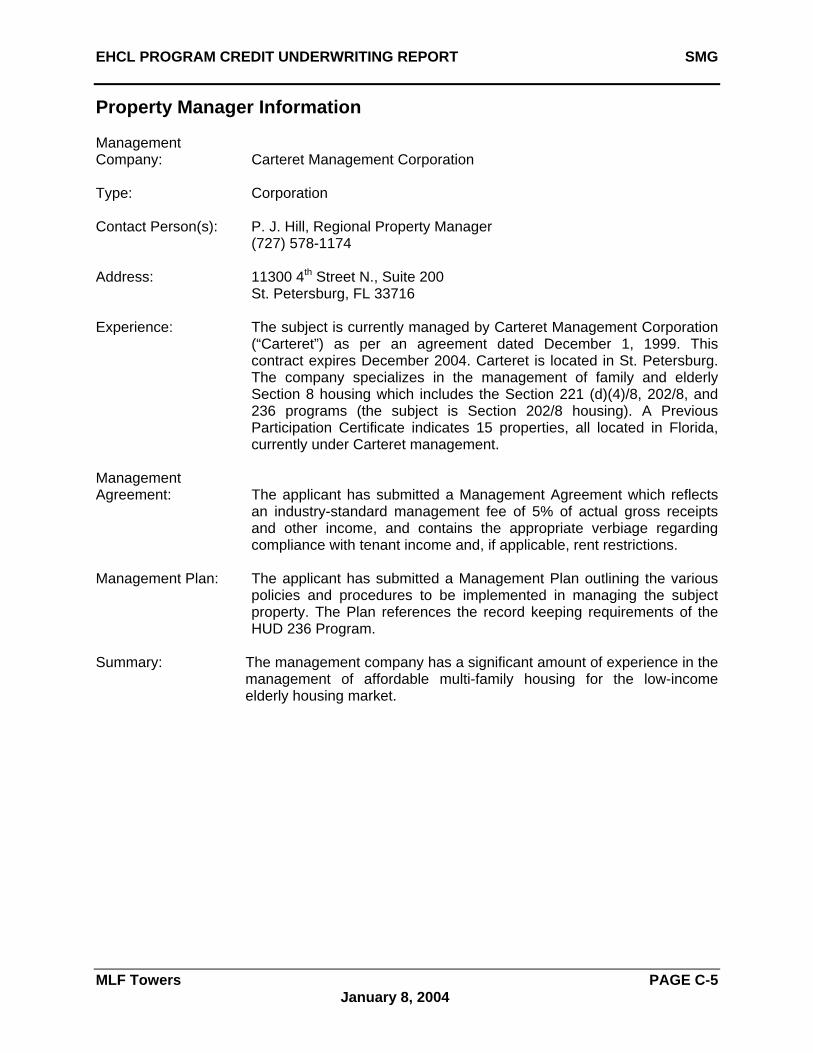

Property Manager Information Management Company: Carteret Management Corporation Type: Corporation Contact Person(s): P. J. Hill, Regional Property Manager (727) 578-1174 Address: 11300 4th Street N., Suite 200 St. Petersburg, FL 33716 Experience: The subject is currently managed by Carteret Management Corporation

(“Carteret”) as per an agreement dated December 1, 1999. This contract expires December 2004. Carteret is located in St. Petersburg. The company specializes in the management of family and elderly Section 8 housing which includes the Section 221 (d)(4)/8, 202/8, and 236 programs (the subject is Section 202/8 housing). A Previous Participation Certificate indicates 15 properties, all located in Florida, currently under Carteret management.

Management Agreement: The applicant has submitted a Management Agreement which reflects

an industry-standard management fee of 5% of actual gross receipts and other income, and contains the appropriate verbiage regarding compliance with tenant income and, if applicable, rent restrictions.

Management Plan: The applicant has submitted a Management Plan outlining the various

policies and procedures to be implemented in managing the subject property. The Plan references the record keeping requirements of the HUD 236 Program.

Summary: The management company has a significant amount of experience in the

management of affordable multi-family housing for the low-income elderly housing market.

MLF Towers PAGE C-5 January 8, 2004

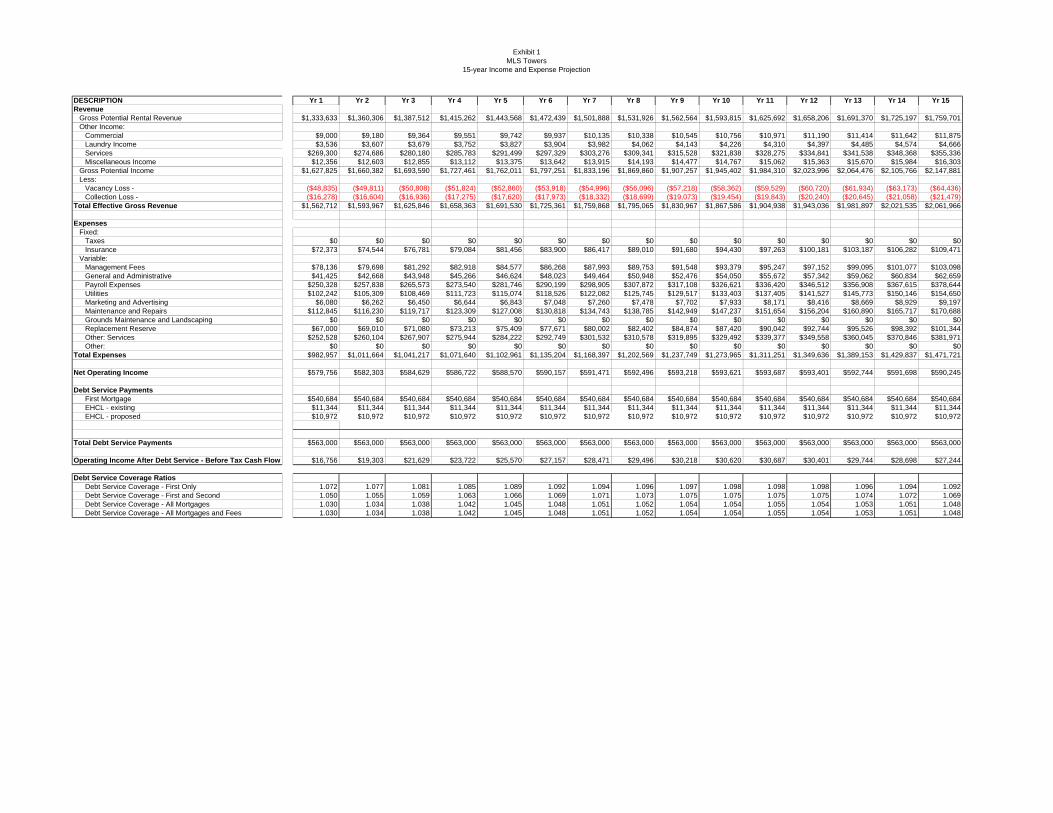

Exhibit 1MLS Towers

15-year Income and Expense Projection

Yr 1 Yr 2 Yr 3 Yr 4 Yr 5 Yr 6 Yr 7 Yr 8 Yr 9 Yr 10 Yr 11 Yr 12 Yr 13 Yr 14 Yr 15

$1,333,633 $1,360,306 $1,387,512 $1,415,262 $1,443,568 $1,472,439 $1,501,888 $1,531,926 $1,562,564 $1,593,815 $1,625,692 $1,658,206 $1,691,370 $1,725,197 $1,759,701

$9,000 $9,180 $9,364 $9,551 $9,742 $9,937 $10,135 $10,338 $10,545 $10,756 $10,971 $11,190 $11,414 $11,642 $11,875Laundry Income $3,536 $3,607 $3,679 $3,752 $3,827 $3,904 $3,982 $4,062 $4,143 $4,226 $4,310 $4,397 $4,485 $4,574 $4,666

$269,300 $274,686 $280,180 $285,783 $291,499 $297,329 $303,276 $309,341 $315,528 $321,838 $328,275 $334,841 $341,538 $348,368 $355,336$12,356 $12,603 $12,855 $13,112 $13,375 $13,642 $13,915 $14,193 $14,477 $14,767 $15,062 $15,363 $15,670 $15,984 $16,303

$1,627,825 $1,660,382 $1,693,590 $1,727,461 $1,762,011 $1,797,251 $1,833,196 $1,869,860 $1,907,257 $1,945,402 $1,984,310 $2,023,996 $2,064,476 $2,105,766 $2,147,881

Vacancy Loss - ($48,835) ($49,811) ($50,808) ($51,824) ($52,860) ($53,918) ($54,996) ($56,096) ($57,218) ($58,362) ($59,529) ($60,720) ($61,934) ($63,173) ($64,436)Collection Loss - ($16,278) ($16,604) ($16,936) ($17,275) ($17,620) ($17,973) ($18,332) ($18,699) ($19,073) ($19,454) ($19,843) ($20,240) ($20,645) ($21,058) ($21,479)

$1,562,712 $1,593,967 $1,625,846 $1,658,363 $1,691,530 $1,725,361 $1,759,868 $1,795,065 $1,830,967 $1,867,586 $1,904,938 $1,943,036 $1,981,897 $2,021,535 $2,061,966

$0 $0 $0 $0 $0 $0 $0 $0 $0 $0 $0 $0 $0 $0 $0$72,373 $74,544 $76,781 $79,084 $81,456 $83,900 $86,417 $89,010 $91,680 $94,430 $97,263 $100,181 $103,187 $106,282 $109,471

Management Fees $78,136 $79,698 $81,292 $82,918 $84,577 $86,268 $87,993 $89,753 $91,548 $93,379 $95,247 $97,152 $99,095 $101,077 $103,098$41,425 $42,668 $43,948 $45,266 $46,624 $48,023 $49,464 $50,948 $52,476 $54,050 $55,672 $57,342 $59,062 $60,834 $62,659

$250,328 $257,838 $265,573 $273,540 $281,746 $290,199 $298,905 $307,872 $317,108 $326,621 $336,420 $346,512 $356,908 $367,615 $378,644$102,242 $105,309 $108,469 $111,723 $115,074 $118,526 $122,082 $125,745 $129,517 $133,403 $137,405 $141,527 $145,773 $150,146 $154,650

$6,080 $6,262 $6,450 $6,644 $6,843 $7,048 $7,260 $7,478 $7,702 $7,933 $8,171 $8,416 $8,669 $8,929 $9,197$112,845 $116,230 $119,717 $123,309 $127,008 $130,818 $134,743 $138,785 $142,949 $147,237 $151,654 $156,204 $160,890 $165,717 $170,688

$0 $0 $0 $0 $0 $0 $0 $0 $0 $0 $0 $0 $0 $0 $0$67,000 $69,010 $71,080 $73,213 $75,409 $77,671 $80,002 $82,402 $84,874 $87,420 $90,042 $92,744 $95,526 $98,392 $101,344

$252,528 $260,104 $267,907 $275,944 $284,222 $292,749 $301,532 $310,578 $319,895 $329,492 $339,377 $349,558 $360,045 $370,846 $381,971$0 $0 $0 $0 $0 $0 $0 $0 $0 $0 $0 $0 $0 $0 $0

$982,957 $1,011,664 $1,041,217 $1,071,640 $1,102,961 $1,135,204 $1,168,397 $1,202,569 $1,237,749 $1,273,965 $1,311,251 $1,349,636 $1,389,153 $1,429,837 $1,471,721

$579,756 $582,303 $584,629 $586,722 $588,570 $590,157 $591,471 $592,496 $593,218 $593,621 $593,687 $593,401 $592,744 $591,698 $590,245

$540,684 $540,684 $540,684 $540,684 $540,684 $540,684 $540,684 $540,684 $540,684 $540,684 $540,684 $540,684 $540,684 $540,684 $540,684$11,344 $11,344 $11,344 $11,344 $11,344 $11,344 $11,344 $11,344 $11,344 $11,344 $11,344 $11,344 $11,344 $11,344 $11,344$10,972 $10,972 $10,972 $10,972 $10,972 $10,972 $10,972 $10,972 $10,972 $10,972 $10,972 $10,972 $10,972 $10,972 $10,972

$563,000 $563,000 $563,000 $563,000 $563,000 $563,000 $563,000 $563,000 $563,000 $563,000 $563,000 $563,000 $563,000 $563,000 $563,000

$16,756 $19,303 $21,629 $23,722 $25,570 $27,157 $28,471 $29,496 $30,218 $30,620 $30,687 $30,401 $29,744 $28,698 $27,244

1.072 1.077 1.081 1.085 1.089 1.092 1.094 1.096 1.097 1.098 1.098 1.098 1.096 1.094 1.0921.050 1.055 1.059 1.063 1.066 1.069 1.071 1.073 1.075 1.075 1.075 1.075 1.074 1.072 1.0691.030 1.034 1.038 1.042 1.045 1.048 1.051 1.052 1.054 1.054 1.055 1.054 1.053 1.051 1.0481.030 1.034 1.038 1.042 1.045 1.048 1.051 1.052 1.054 1.054 1.055 1.054 1.053 1.051 1.048

Debt Service Coverage - All MortgagesDebt Service Coverage - All Mortgages and Fees

Total Debt Service Payments

Operating Income After Debt Service - Before Tax Cash Flow

Debt Service Coverage RatiosDebt Service Coverage - First Only

EHCL - proposed

Debt Service Coverage - First and Second

Net Operating Income

Debt Service PaymentsFirst MortgageEHCL - existing

Replacement ReserveOther: ServicesOther:

Total Expenses

Total Effective Gross Revenue

ExpensesFixed:

Utilities

InsuranceTaxes

Marketing and AdvertisingMaintenance and RepairsGrounds Maintenance and Landscaping

Variable:

General and AdministrativePayroll Expenses

Less:

DESCRIPTIONRevenue

Gross Potential Rental Revenue

Gross Potential Income

Other Income:Commercial

ServicesMiscellaneous Income