finnish technologyindustryjanuary2015

TRANSCRIPT

Technology Industry /

Finnish Economic

Situation and Outlook

January 2015

13.1.2015 2

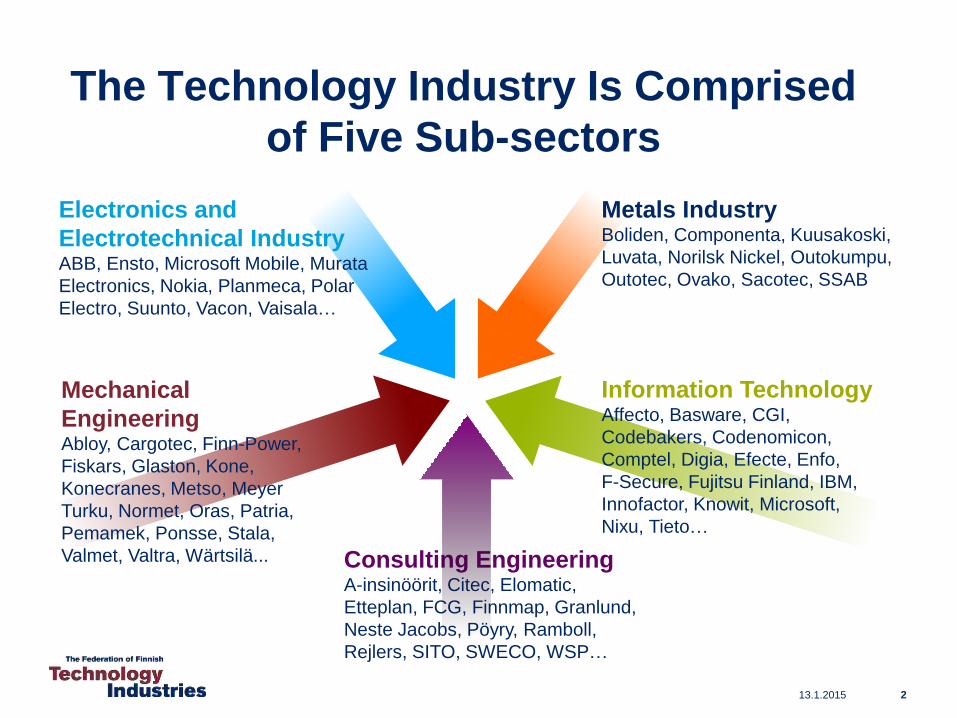

The Technology Industry Is Comprised

of Five Sub-sectors

Metals IndustryBoliden, Componenta, Kuusakoski,

Luvata, Norilsk Nickel, Outokumpu,

Outotec, Ovako, Sacotec, SSAB

Mechanical

EngineeringAbloy, Cargotec, Finn-Power,

Fiskars, Glaston, Kone,

Konecranes, Metso, Meyer

Turku, Normet, Oras, Patria,

Pemamek, Ponsse, Stala,

Valmet, Valtra, Wärtsilä...

Electronics and

Electrotechnical IndustryABB, Ensto, Microsoft Mobile, Murata

Electronics, Nokia, Planmeca, Polar

Electro, Suunto, Vacon, Vaisala…

Information TechnologyAffecto, Basware, CGI,

Codebakers, Codenomicon,

Comptel, Digia, Efecte, Enfo,

F-Secure, Fujitsu Finland, IBM,

Innofactor, Knowit, Microsoft,

Nixu, Tieto…

Consulting EngineeringA-insinöörit, Citec, Elomatic,

Etteplan, FCG, Finnmap, Granlund,

Neste Jacobs, Pöyry, Ramboll,

Rejlers, SITO, SWECO, WSP…

3

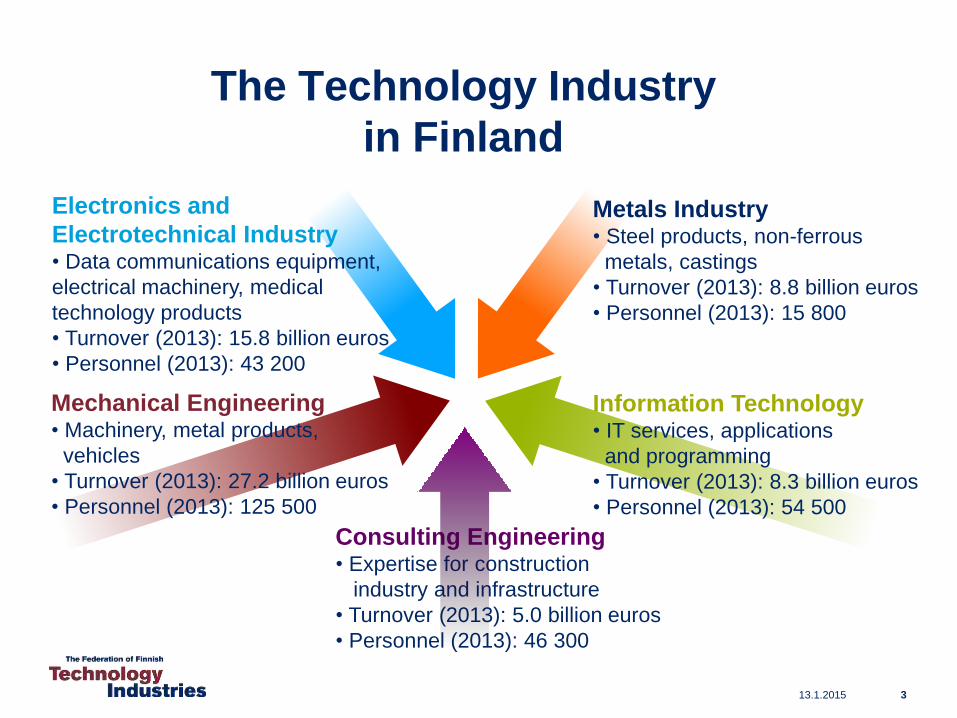

The Technology Industry

in Finland

Mechanical Engineering• Machinery, metal products,

vehicles

• Turnover (2013): 27.2 billion euros

• Personnel (2013): 125 500

Electronics and

Electrotechnical Industry• Data communications equipment,

electrical machinery, medical

technology products

• Turnover (2013): 15.8 billion euros

• Personnel (2013): 43 200

Information Technology• IT services, applications

and programming

• Turnover (2013): 8.3 billion euros

• Personnel (2013): 54 500

Metals Industry• Steel products, non-ferrous

metals, castings

• Turnover (2013): 8.8 billion euros

• Personnel (2013): 15 800

Consulting Engineering• Expertise for construction

industry and infrastructure

• Turnover (2013): 5.0 billion euros

• Personnel (2013): 46 300

13.1.2015

• 50 % of total Finnish exports.

• 75 % of private-sector R&D investment.

• Almost 280,000 employed directly in the sector, 700,000employed in total, equalling about 30% of the entire Finnish labour force.

• The Federation of Finnish Technology Industries has over 1,600 member companies.

13.1.2015 4

The Technology Industry –

the Most Important Sector in Finland

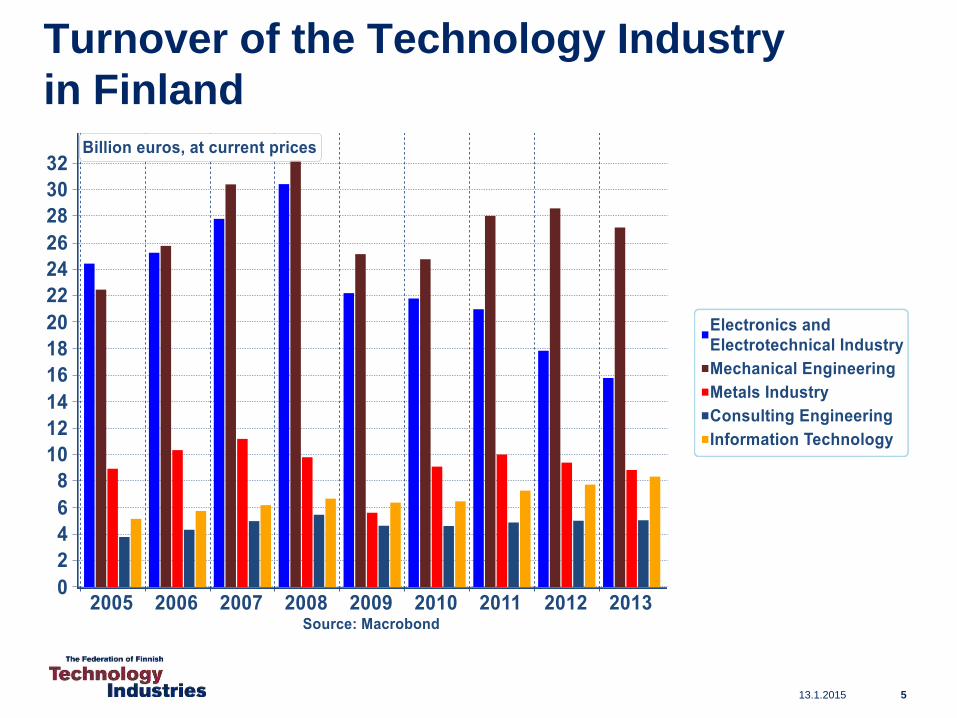

Turnover of the Technology Industry

in Finland

13.1.2015 5

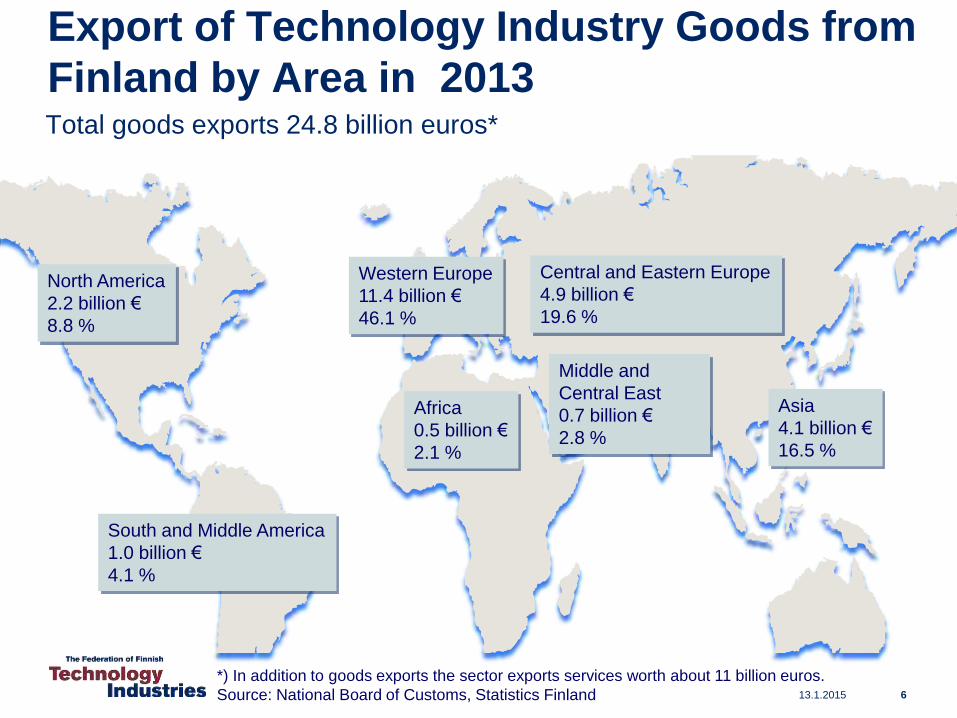

Export of Technology Industry Goods from

Finland by Area in 2013

13.1.2015 6

Total goods exports 24.8 billion euros*

North America

2.2 billion €

8.8 %

Western Europe

11.4 billion €

46.1 %

Middle and

Central East

0.7 billion €

2.8 %

Asia

4.1 billion €

16.5 %

Africa

0.5 billion €

2.1 %

South and Middle America

1.0 billion €

4.1 %

Central and Eastern Europe

4.9 billion €

19.6 %

*) In addition to goods exports the sector exports services worth about 11 billion euros.

Source: National Board of Customs, Statistics Finland

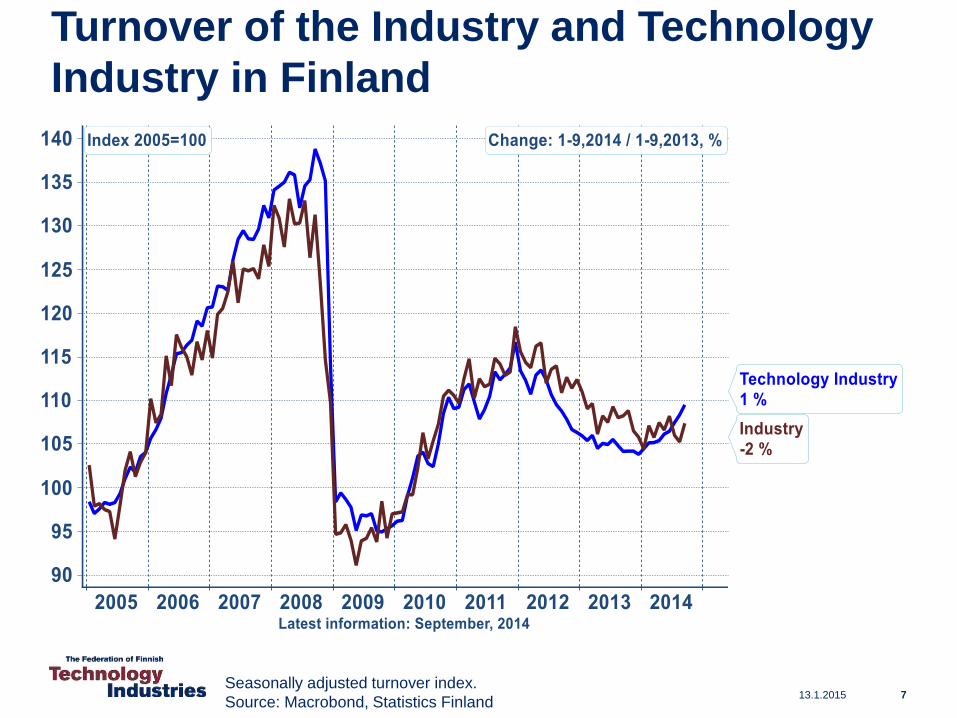

Turnover of the Industry and Technology

Industry in Finland

13.1.2015 7Seasonally adjusted turnover index.

Source: Macrobond, Statistics Finland

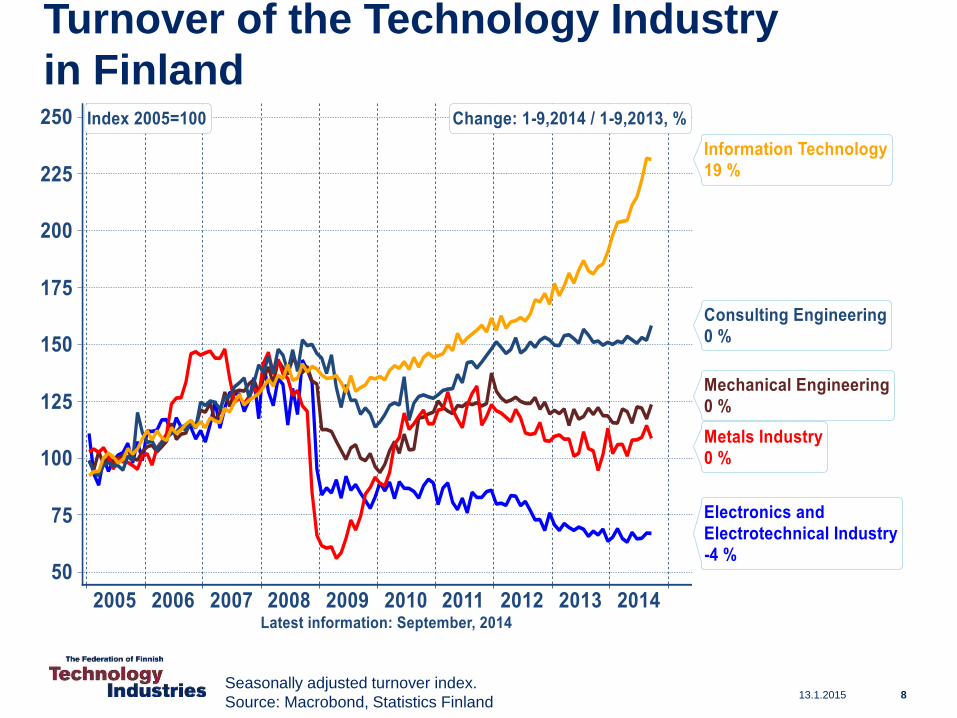

Turnover of the Technology Industry

in Finland

13.1.2015 8Seasonally adjusted turnover index.

Source: Macrobond, Statistics Finland

13.1.2015

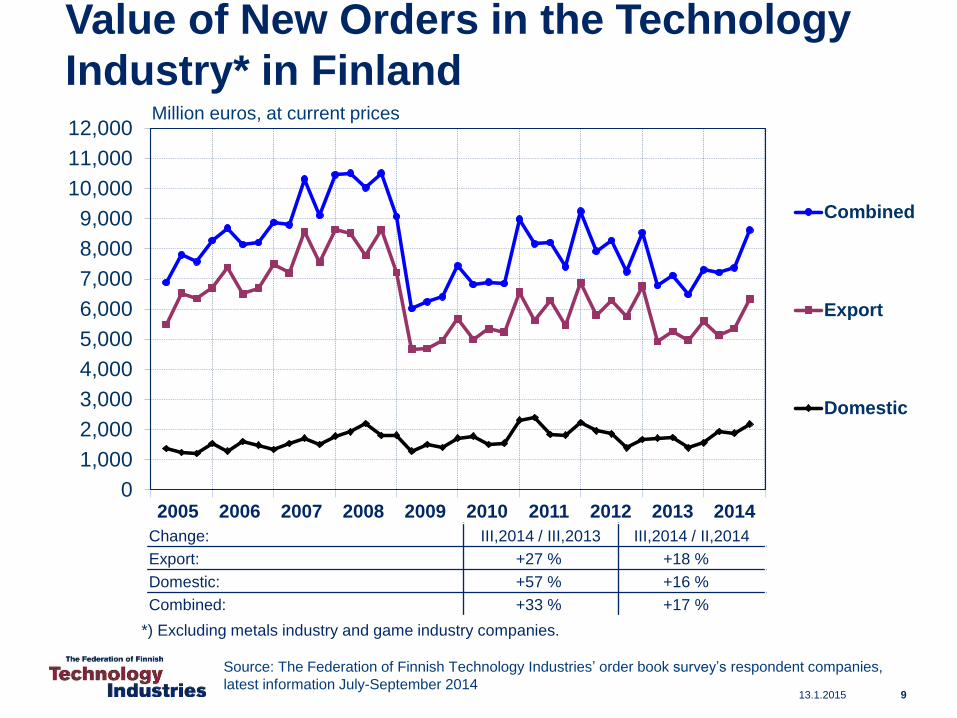

Value of New Orders in the Technology

Industry* in Finland

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

11,000

12,000

Combined

Export

Domestic

Million euros, at current prices

Source: The Federation of Finnish Technology Industries’ order book survey’s respondent companies,

latest information July-September 2014

*) Excluding metals industry and game industry companies.

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Change: III,2014 / III,2013 III,2014 / II,2014

Export: +27 % +18 %

Domestic: +57 % +16 %

Combined: +33 % +17 %

9

13.1.2015

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

20,000

22,000

24,000

Export

Domestic

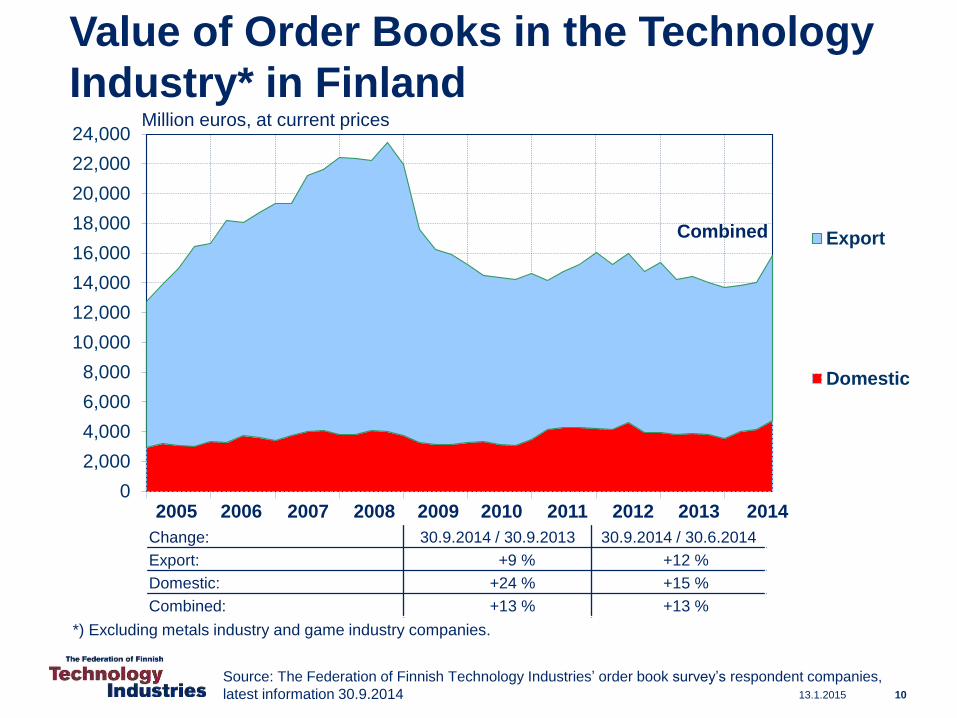

Value of Order Books in the Technology

Industry* in FinlandMillion euros, at current prices

Source: The Federation of Finnish Technology Industries’ order book survey’s respondent companies,

latest information 30.9.2014

*) Excluding metals industry and game industry companies.

Combined

Change: 30.9.2014 / 30.9.2013 30.9.2014 / 30.6.2014

Export: +9 % +12 %

Domestic: +24 % +15 %

Combined: +13 % +13 %

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

10

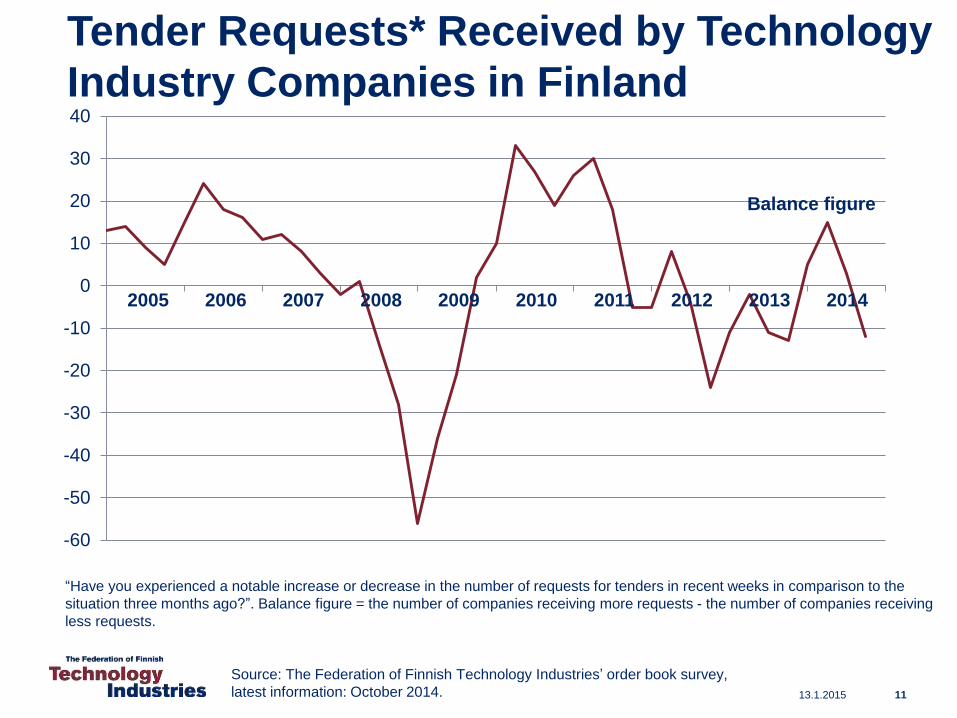

Tender Requests* Received by Technology

Industry Companies in Finland

Source: The Federation of Finnish Technology Industries’ order book survey,

latest information: October 2014.

“Have you experienced a notable increase or decrease in the number of requests for tenders in recent weeks in comparison to the

situation three months ago?”. Balance figure = the number of companies receiving more requests - the number of companies receiving

less requests.

-60

-50

-40

-30

-20

-10

0

10

20

30

40

Balance figure

1113.1.2015

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

13.1.2015

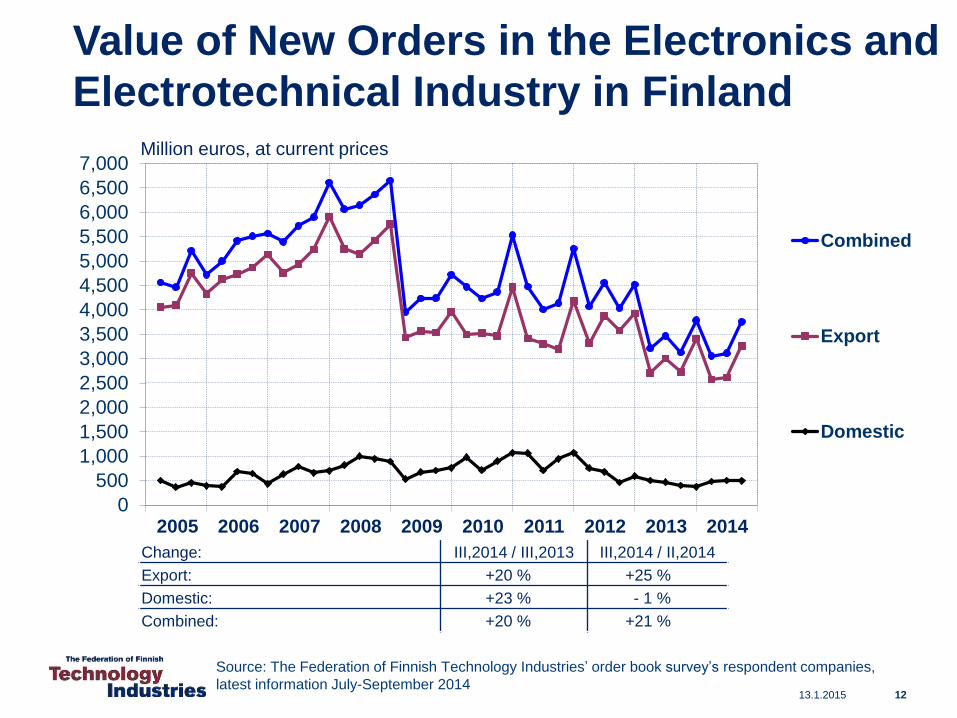

Value of New Orders in the Electronics and

Electrotechnical Industry in Finland

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

5,000

5,500

6,000

6,500

7,000

Combined

Export

Domestic

Million euros, at current prices

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Change: III,2014 / III,2013 III,2014 / II,2014

Export: +20 % +25 %

Domestic: +23 % - 1 %

Combined: +20 % +21 %

Source: The Federation of Finnish Technology Industries’ order book survey’s respondent companies,

latest information July-September 201412

13.1.2015

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

5,000

5,500

6,000

6,500

7,000

7,500

8,000

Export

Domestic

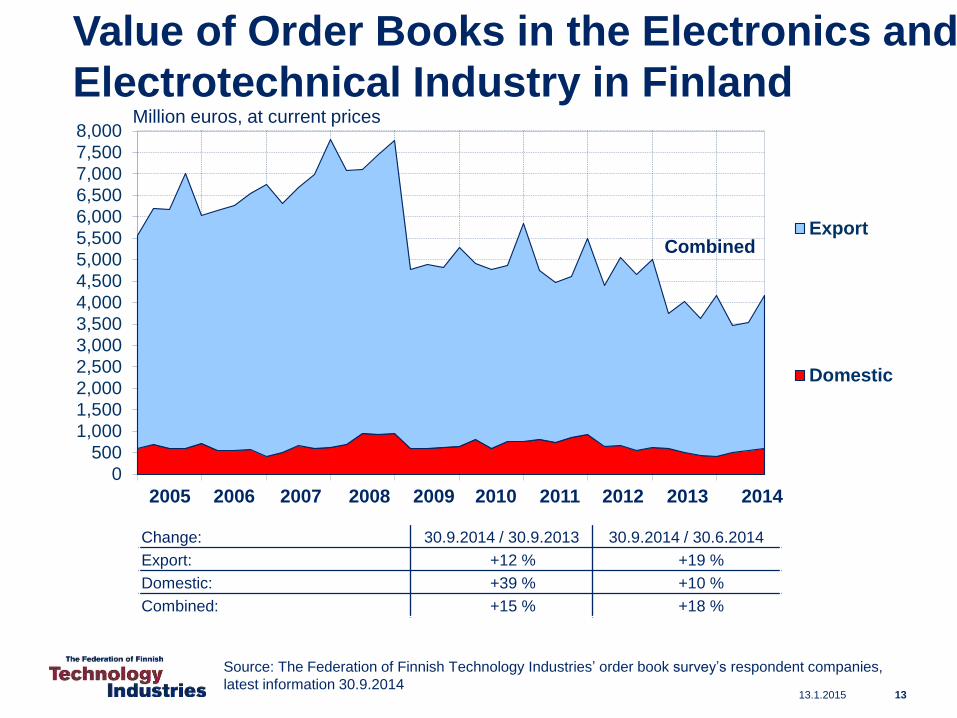

Value of Order Books in the Electronics and

Electrotechnical Industry in Finland

Combined

Million euros, at current prices

Change: 30.9.2014 / 30.9.2013 30.9.2014 / 30.6.2014

Export: +12 % +19 %

Domestic: +39 % +10 %

Combined: +15 % +18 %

Source: The Federation of Finnish Technology Industries’ order book survey’s respondent companies,

latest information 30.9.2014 13

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

13.1.2015

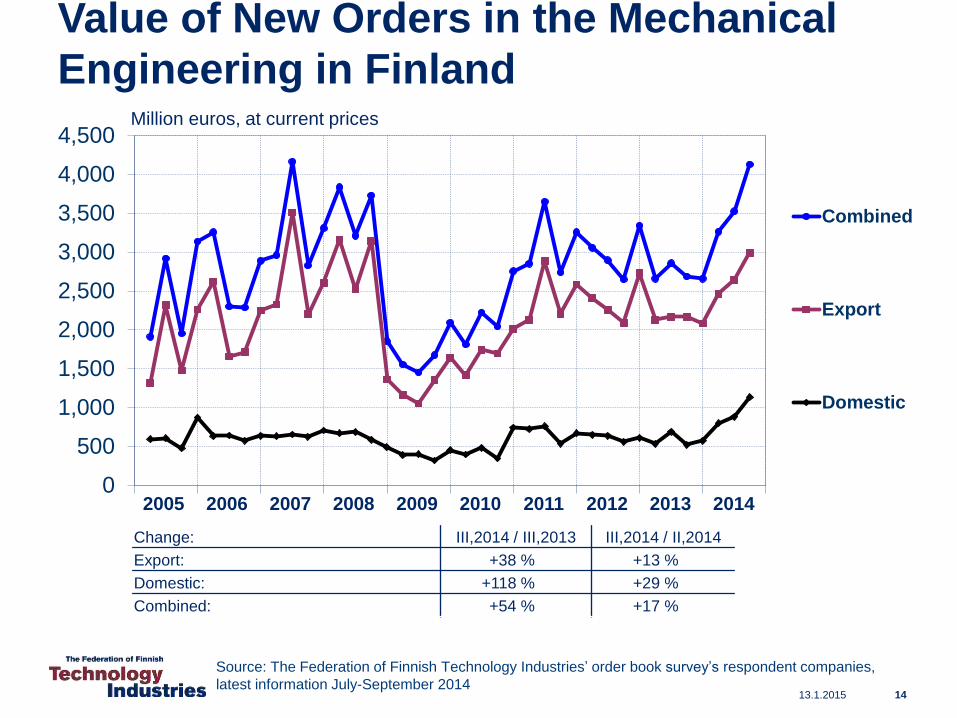

Value of New Orders in the Mechanical

Engineering in Finland

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

Combined

Export

Domestic

Million euros, at current prices

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Change: III,2014 / III,2013 III,2014 / II,2014

Export: +38 % +13 %

Domestic: +118 % +29 %

Combined: +54 % +17 %

Source: The Federation of Finnish Technology Industries’ order book survey’s respondent companies,

latest information July-September 201414

13.1.2015

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

11,000

12,000

13,000

14,000

15,000

Export

Domestic

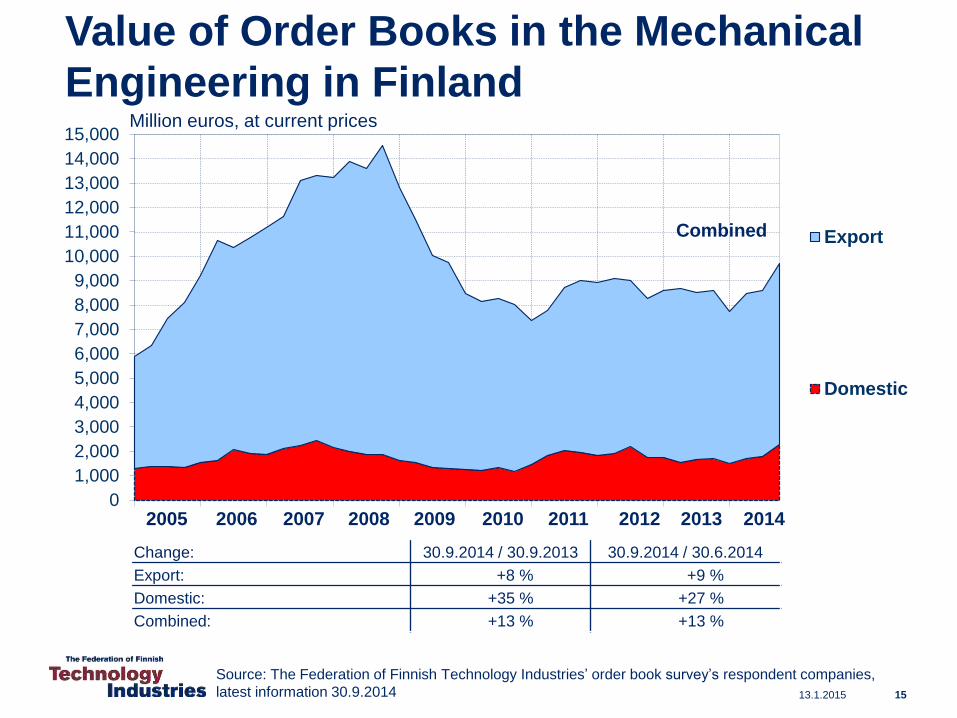

Value of Order Books in the Mechanical

Engineering in Finland

Combined

Million euros, at current prices

Change: 30.9.2014 / 30.9.2013 30.9.2014 / 30.6.2014

Export: +8 % +9 %

Domestic: +35 % +27 %

Combined: +13 % +13 %

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Source: The Federation of Finnish Technology Industries’ order book survey’s respondent companies,

latest information 30.9.2014 15

13.1.2015

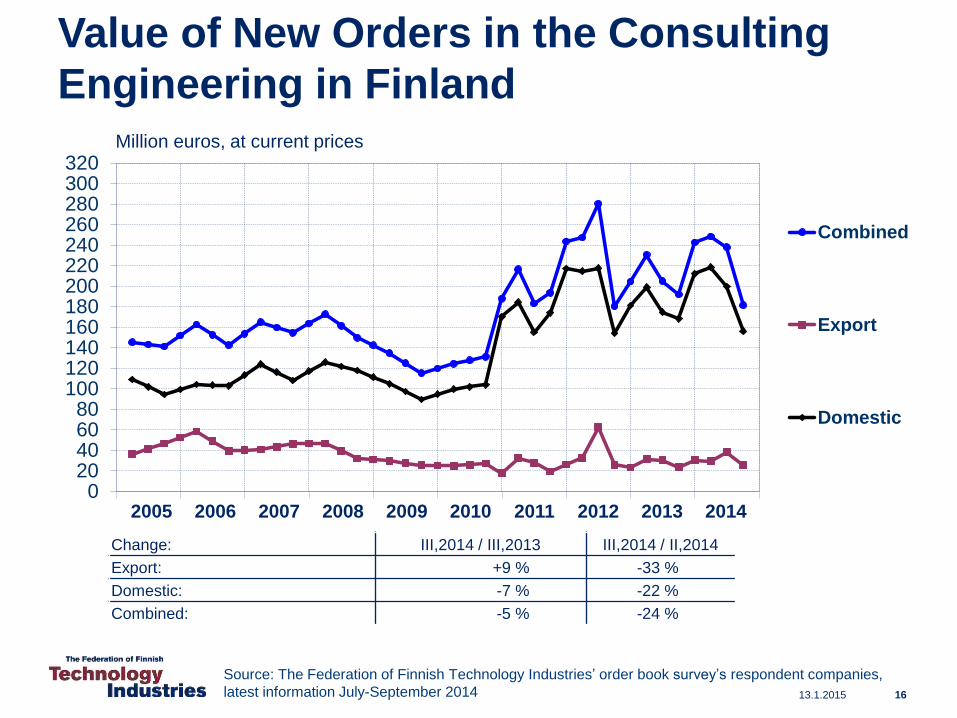

Value of New Orders in the Consulting

Engineering in Finland

020406080

100120140160180200220240260280300320

Combined

Export

Domestic

Million euros, at current prices

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Change: III,2014 / III,2013 III,2014 / II,2014

Export: +9 % -33 %

Domestic: -7 % -22 %

Combined: -5 % -24 %

Source: The Federation of Finnish Technology Industries’ order book survey’s respondent companies,

latest information July-September 2014 16

13.1.2015

0

50

100

150

200

250

300

350

400

450

500

550

Export

Domestic

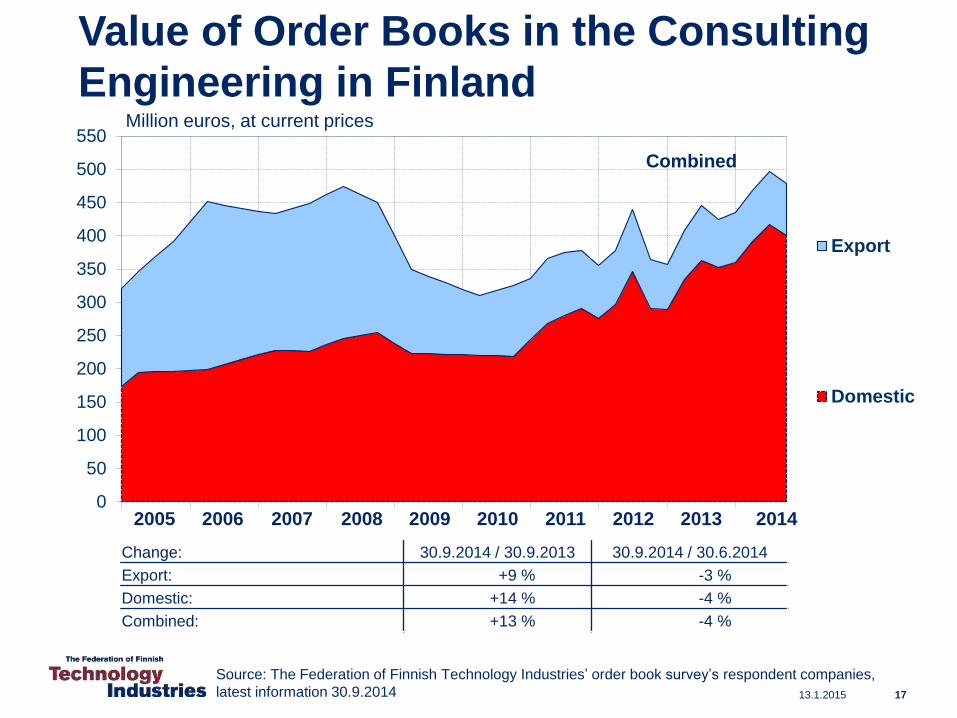

Value of Order Books in the Consulting

Engineering in Finland

Combined

Million euros, at current prices

Source: The Federation of Finnish Technology Industries’ order book survey’s respondent companies,

latest information 30.9.2014

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Change: 30.9.2014 / 30.9.2013 30.9.2014 / 30.6.2014

Export: +9 % -3 %

Domestic: +14 % -4 %

Combined: +13 % -4 %

17

13.1.2015

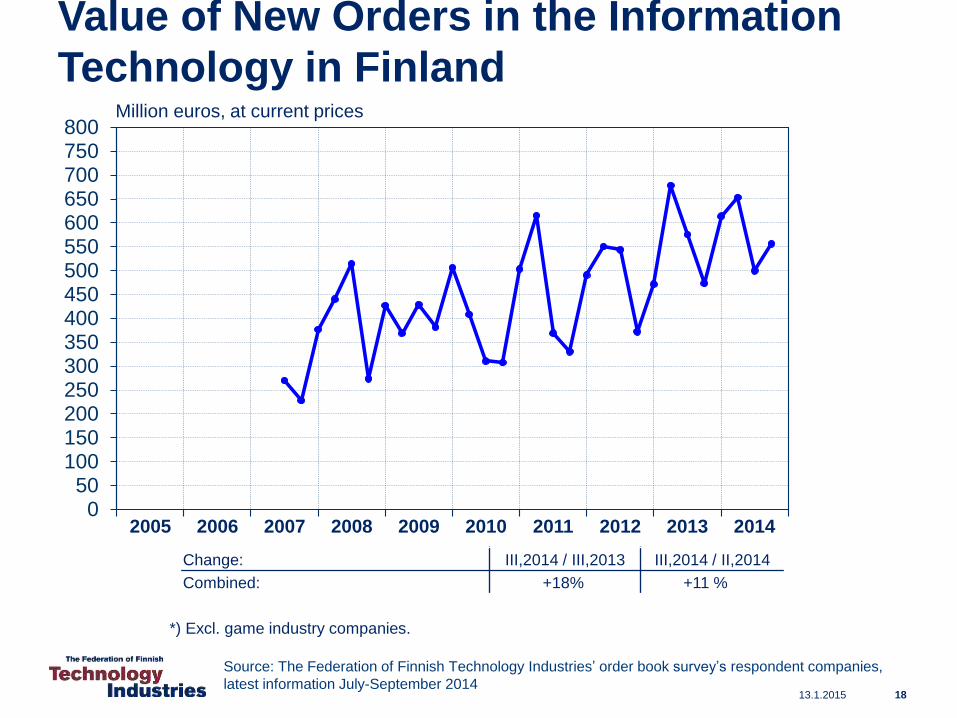

Value of New Orders in the Information

Technology in Finland

050

100150200250300350400450500550600650700750800

Million euros, at current prices

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Change: III,2014 / III,2013 III,2014 / II,2014

Combined: +18% +11 %

Source: The Federation of Finnish Technology Industries’ order book survey’s respondent companies,

latest information July-September 201418

*) Excl. game industry companies.

13.1.2015

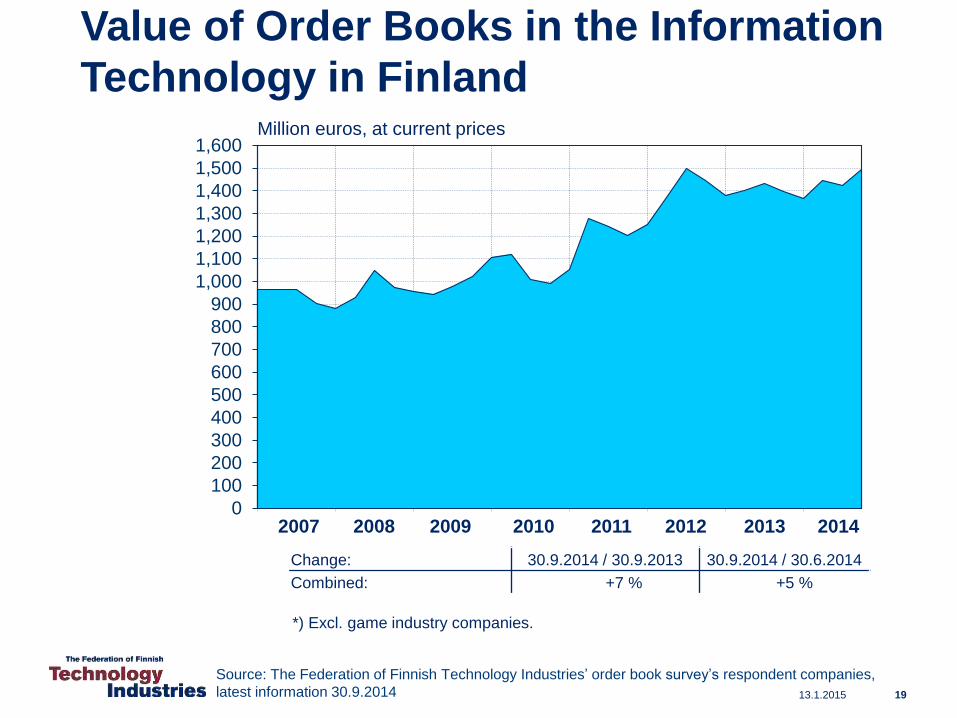

Value of Order Books in the Information

Technology in Finland

0

100

200

300

400

500

600

700

800

900

1,000

1,100

1,200

1,300

1,400

1,500

1,600Million euros, at current prices

2007 2008 2009 2010 2011 2012 2013 2014

Change: 30.9.2014 / 30.9.2013 30.9.2014 / 30.6.2014

Combined: +7 % +5 %

Source: The Federation of Finnish Technology Industries’ order book survey’s respondent companies,

latest information 30.9.2014 19

*) Excl. game industry companies.

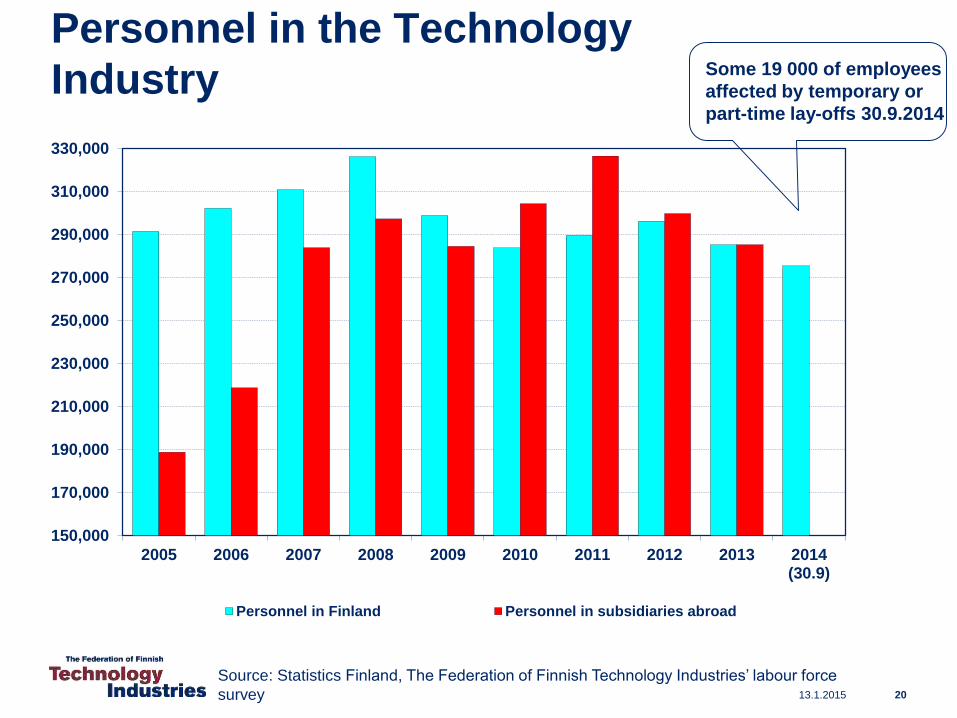

Personnel in the Technology

Industry

150,000

170,000

190,000

210,000

230,000

250,000

270,000

290,000

310,000

330,000

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014(30.9)

Personnel in Finland Personnel in subsidiaries abroad

Source: Statistics Finland, The Federation of Finnish Technology Industries’ labour force

survey

Some 19 000 of employees

affected by temporary or

part-time lay-offs 30.9.2014

13.1.2015 20

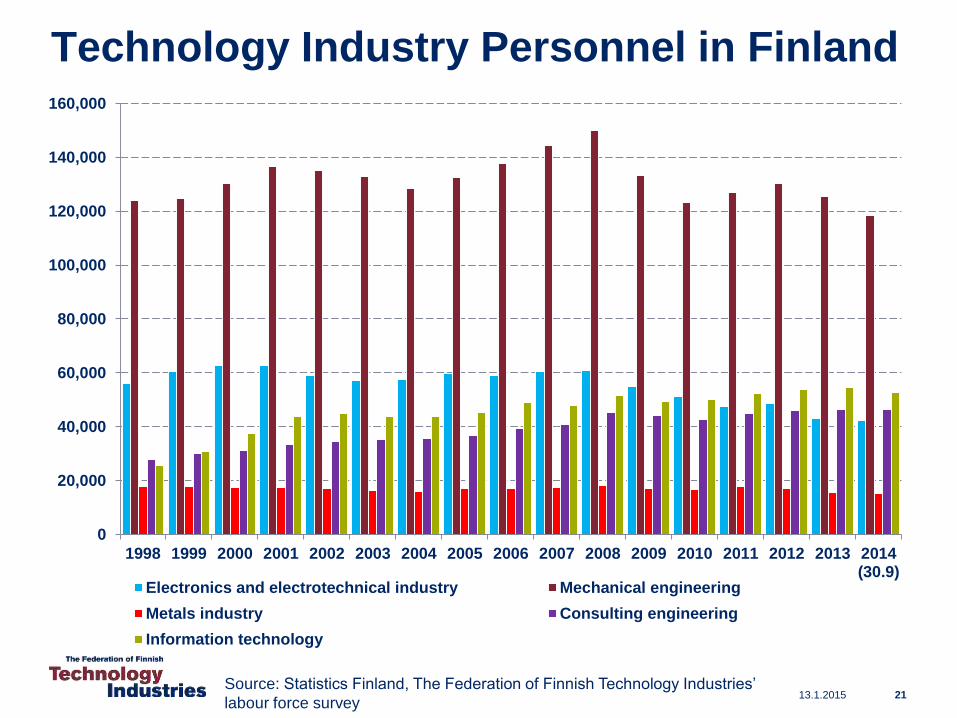

Technology Industry Personnel in Finland

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014(30.9)

Electronics and electrotechnical industry Mechanical engineering

Metals industry Consulting engineering

Information technology

Source: Statistics Finland, The Federation of Finnish Technology Industries’

labour force survey13.1.2015 21

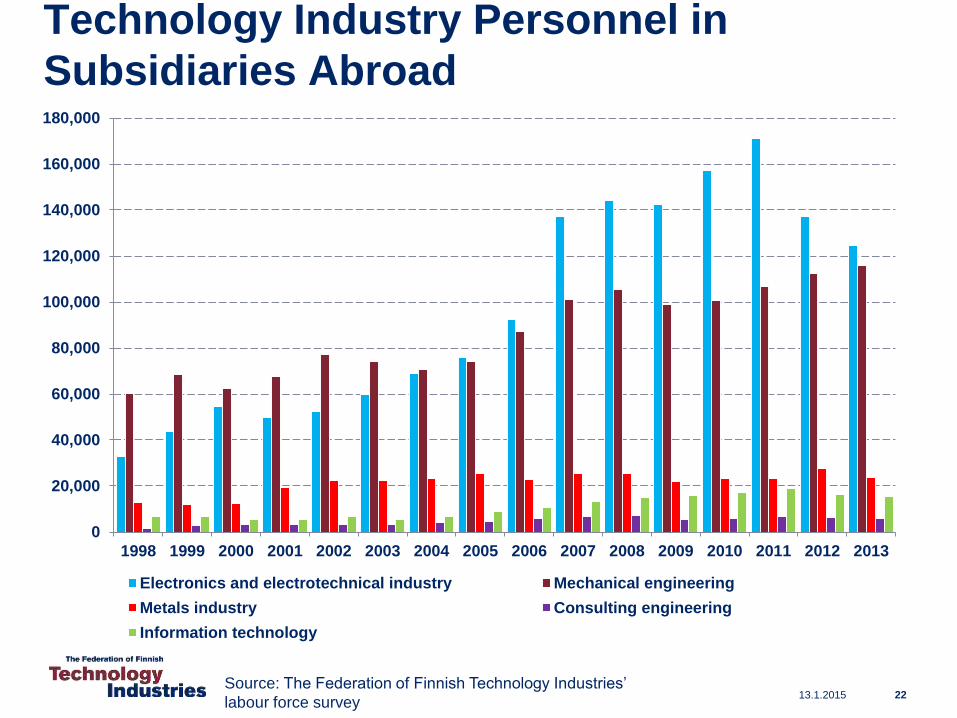

Technology Industry Personnel in

Subsidiaries Abroad

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

180,000

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Electronics and electrotechnical industry Mechanical engineering

Metals industry Consulting engineering

Information technology

Source: The Federation of Finnish Technology Industries’

labour force survey13.1.2015 22

13.1.2015 23

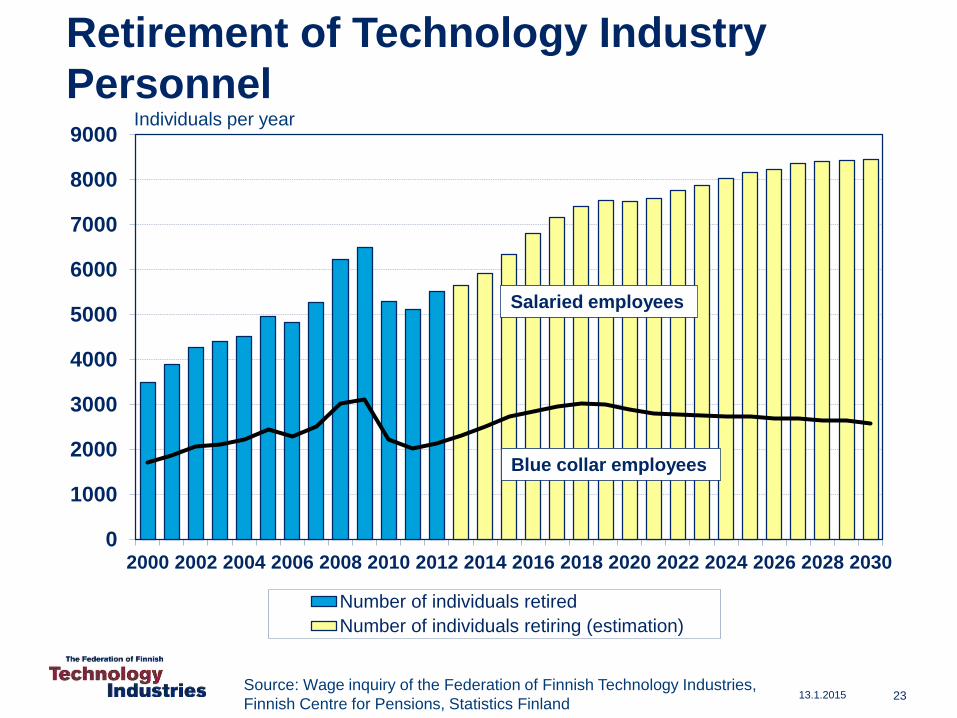

Retirement of Technology Industry

Personnel

0

1000

2000

3000

4000

5000

6000

7000

8000

9000

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 2020 2022 2024 2026 2028 2030

Number of individuals retired

Number of individuals retiring (estimation)

Source: Wage inquiry of the Federation of Finnish Technology Industries,

Finnish Centre for Pensions, Statistics Finland

Individuals per year

Salaried employees

Blue collar employees

13.1.2015 24

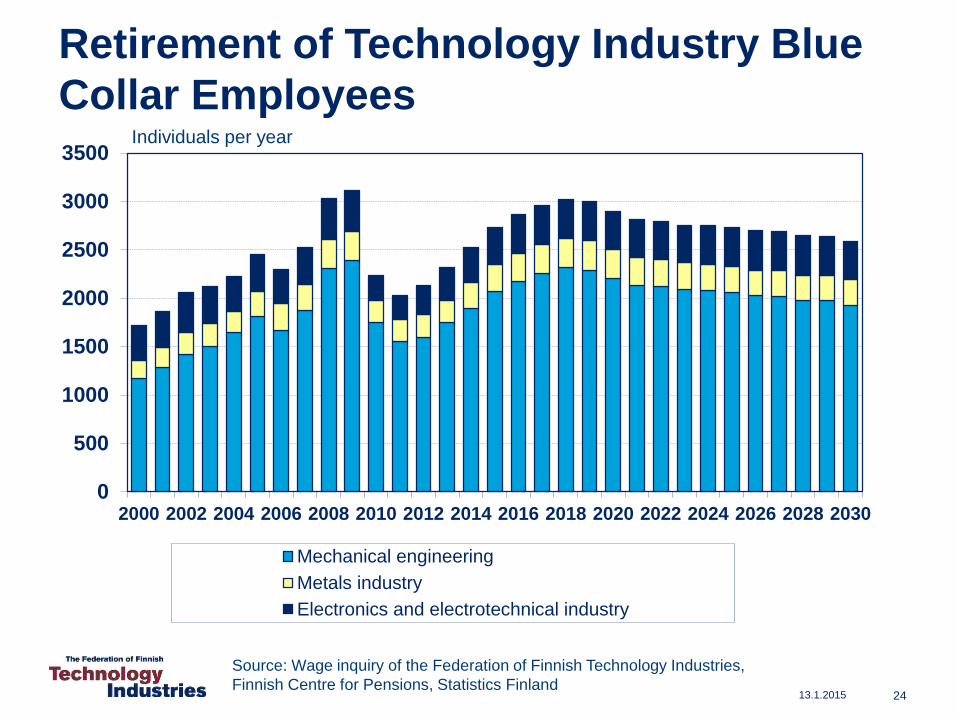

Retirement of Technology Industry Blue

Collar Employees

0

500

1000

1500

2000

2500

3000

3500

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 2020 2022 2024 2026 2028 2030

Mechanical engineering

Metals industry

Electronics and electrotechnical industry

Source: Wage inquiry of the Federation of Finnish Technology Industries,

Finnish Centre for Pensions, Statistics Finland

Individuals per year

Situational Overview and Outlook

• - Finland is in the grip of structural change. Development remains

uneven between companies.

• - Turnover in Finland in 2013 was some EUR 65 billion. In 2014 turnover

increased slightly compared to 2013. Turnover in the pre-crisis year

2008 was EUR 86 billion.

• - The monetary value of new orders reported between July-September

2014 was 33 % higher than in the corresponding period in 2013, and 17

% higher than in the preceding quarter.

• - At the end of September, the value of order books was 13 % higher

year-on-year, and 13 % above the value reported at the end of June.

• - The turnover of technology industry companies in the beginning of

2015 is expected to be higher than in the corresponding period year

earlier.

• - Since 2008, personnel numbers in Finland have shrunk by 50,000

employees, totalling 276,000 at the end of September 2014.

13.1.2015 25

13.1.2015 26

Increased Uncertainty in

the Global Economy

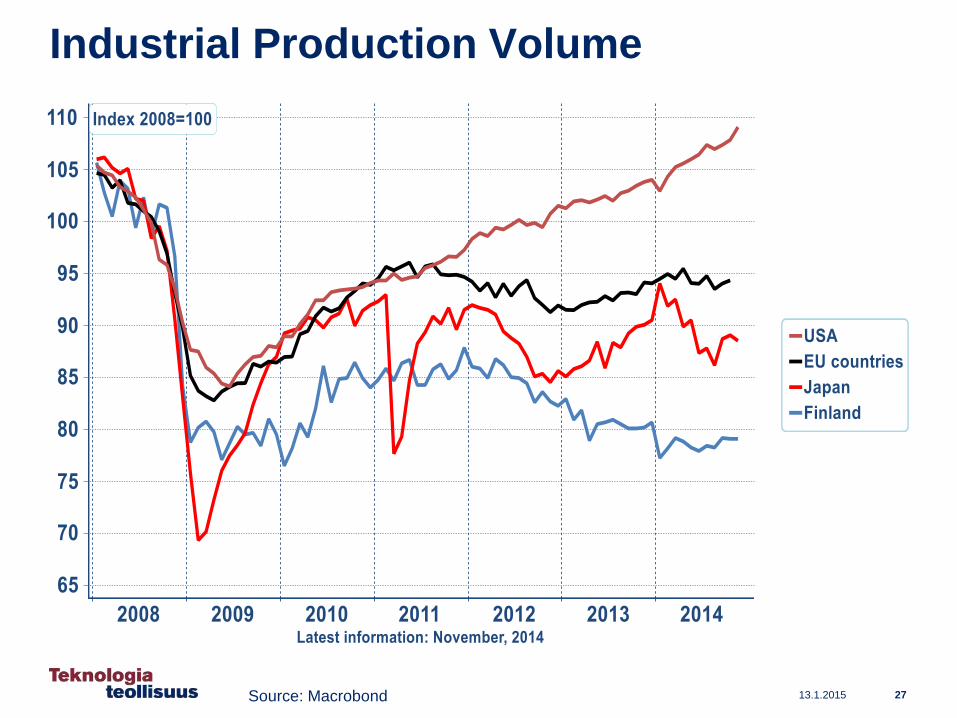

Industrial Production Volume

13.1.2015 27Source: Macrobond

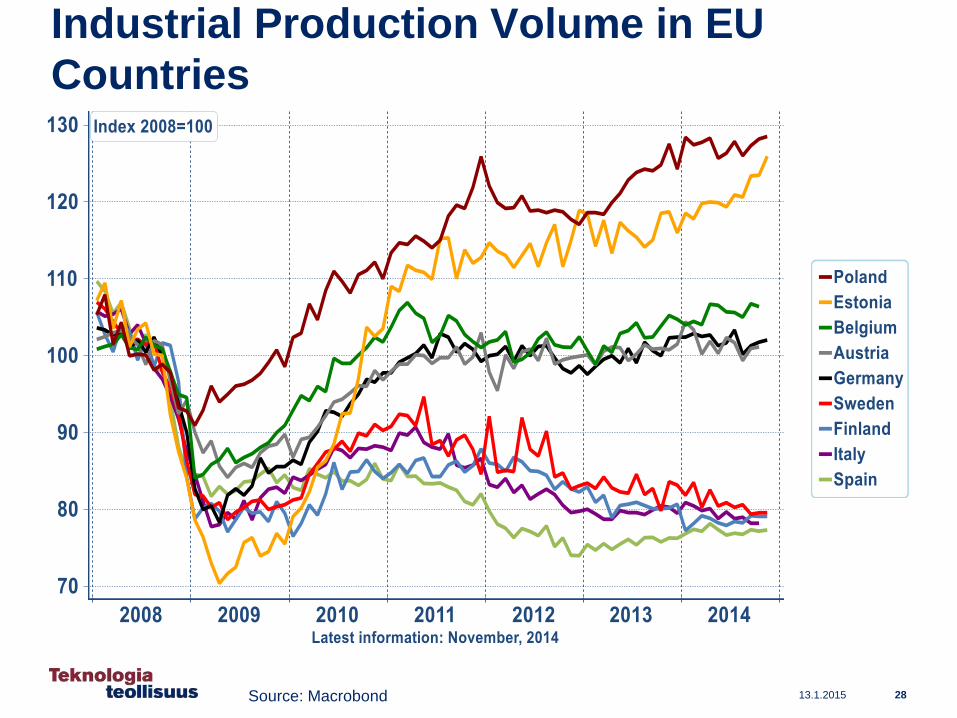

Industrial Production Volume in EU

Countries

13.1.2015 28Source: Macrobond

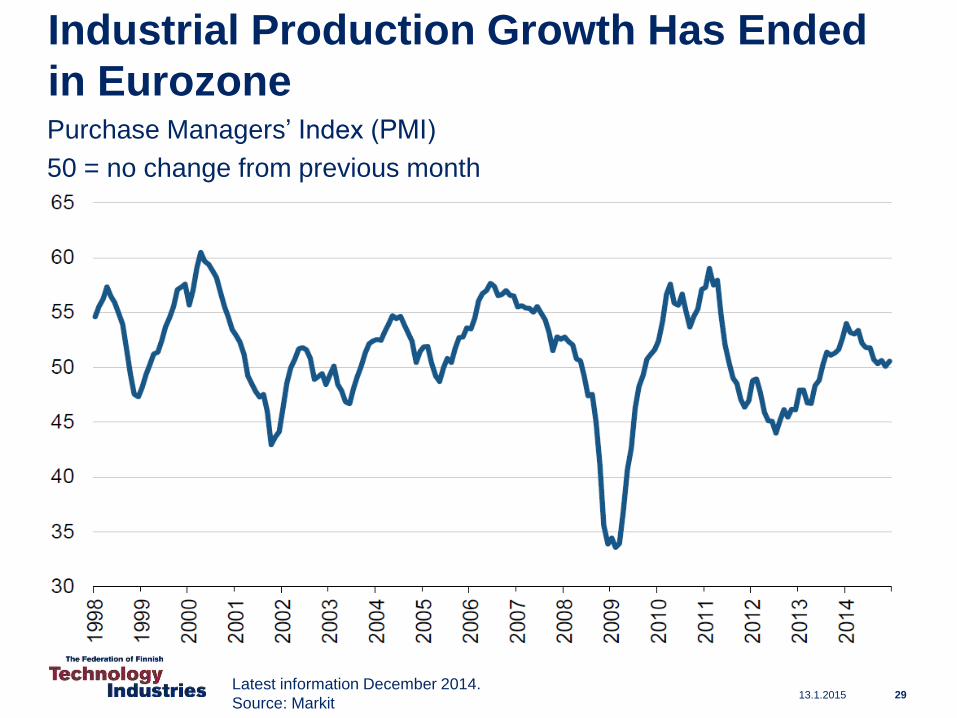

Industrial Production Growth Has Ended

in EurozonePurchase Managers’ Index (PMI)

50 = no change from previous month

13.1.2015 29Latest information December 2014.

Source: Markit

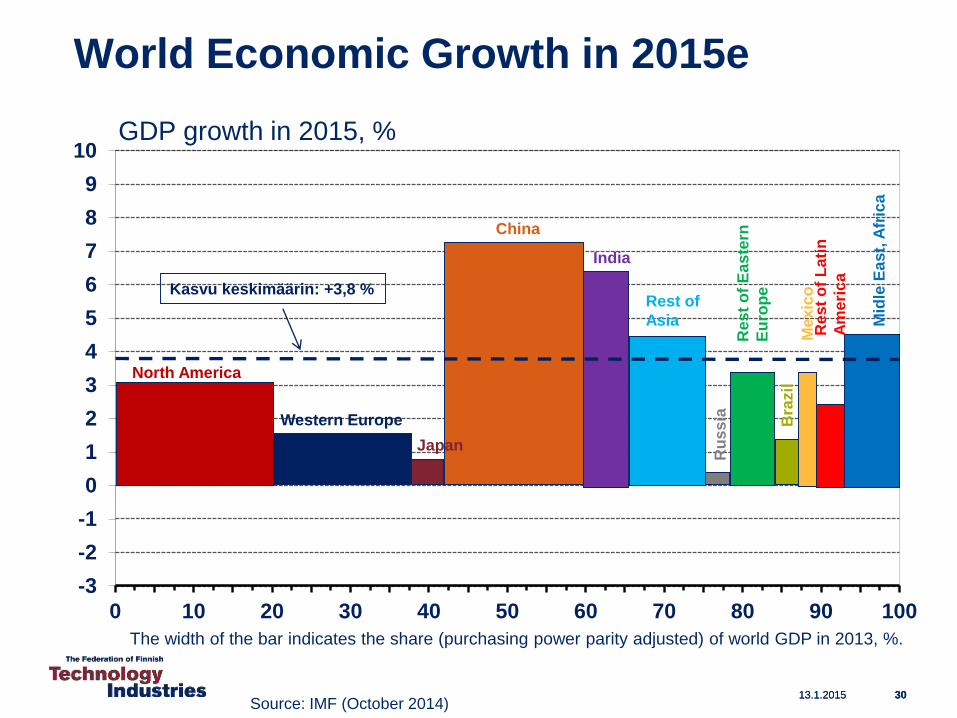

World Economic Growth in 2015e

13.1.2015 30Source: IMF (October 2014)

-3

-2

-1

0

1

2

3

4

5

6

7

8

9

10

0 10 20 30 40 50 60 70 80 90 100

North America

Western Europe

Japan

China

India

Rest of

Asia

Res

to

f E

as

tern

Eu

rop

e

Ru

ss

ia Bra

zil

Me

xic

oR

es

to

f L

ati

n

Am

eri

ca

Mid

leE

as

t, A

fric

a

The width of the bar indicates the share (purchasing power parity adjusted) of world GDP in 2013, %.

Kasvu keskimäärin: +3,8 %

13.1.2015 30

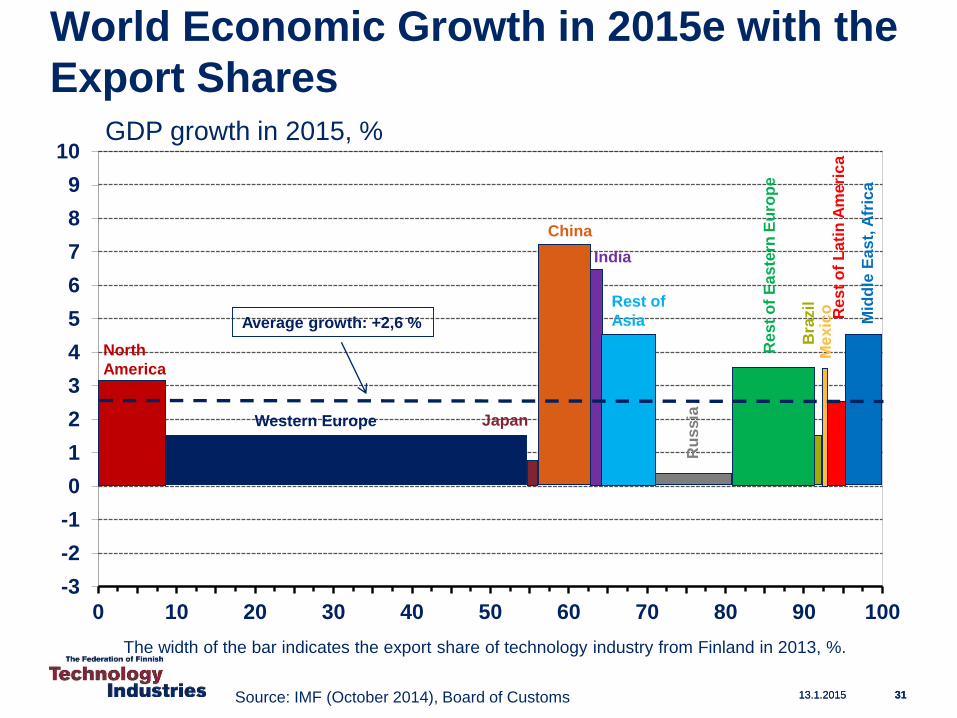

GDP growth in 2015, %

World Economic Growth in 2015e with the

Export Shares

13.1.2015 31

GDP growth in 2015, %

Source: IMF (October 2014), Board of Customs

-3

-2

-1

0

1

2

3

4

5

6

7

8

9

10

0 10 20 30 40 50 60 70 80 90 100

North

America

Western Europe Japan

China

India

Rest of

Asia

Re

st

of

Ea

ste

rn E

uro

pe

Ru

ss

ia

Bra

zil

Me

xic

o Re

st

of

La

tin

Am

eri

ca

Mid

dle

Ea

st,

Afr

ica

The width of the bar indicates the export share of technology industry from Finland in 2013, %.

Average growth: +2,6 %

13.1.2015 31

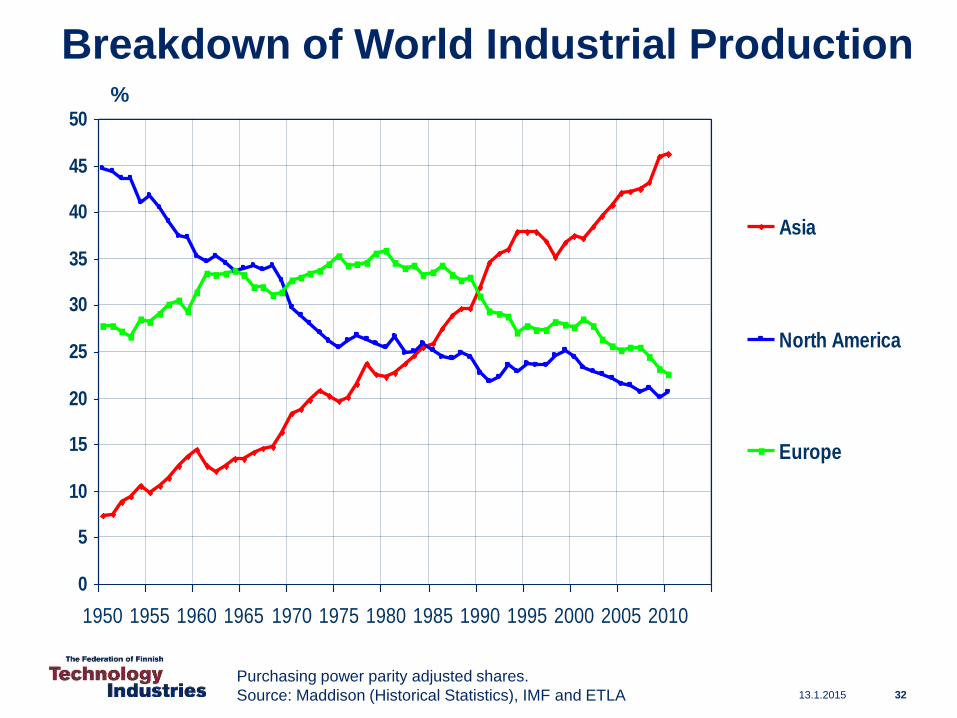

13.1.2015 32

Breakdown of World Industrial Production

0

5

10

15

20

25

30

35

40

45

50

1950 1955 1960 1965 1970 1975 1980 1985 1990 1995 2000 2005 2010

Asia

North America

Europe

Purchasing power parity adjusted shares.

Source: Maddison (Historical Statistics), IMF and ETLA

%

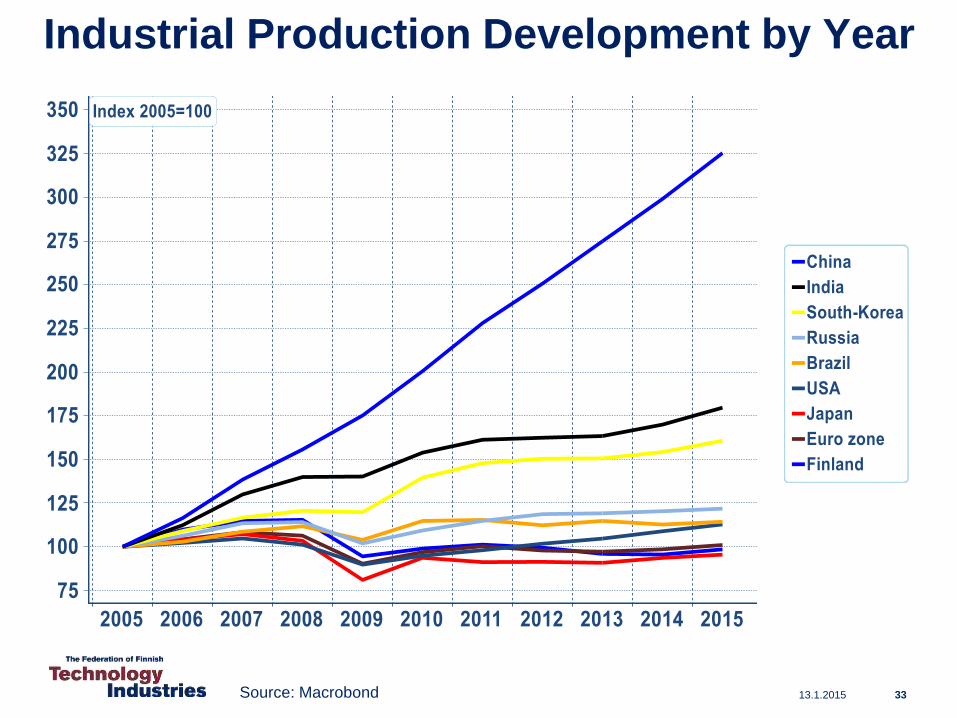

Industrial Production Development by Year

13.1.2015 33Source: Macrobond

13.1.2015 34

The Big Challenge for

Finland after 2008

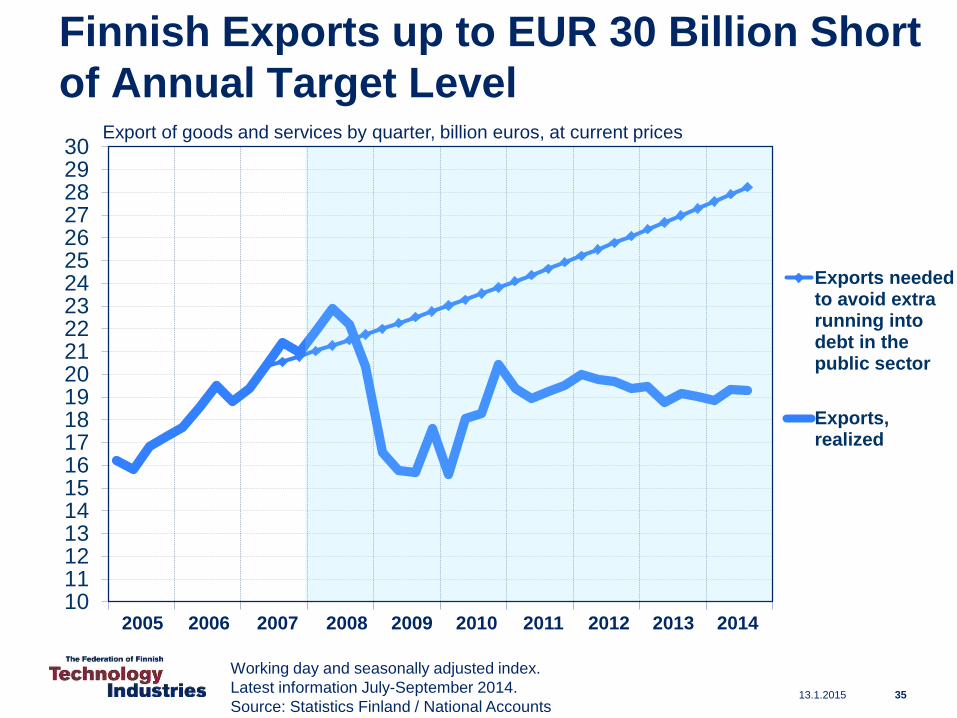

13.1.2015

Finnish Exports up to EUR 30 Billion Short

of Annual Target Level

101112131415161718192021222324252627282930

Exports neededto avoid extrarunning intodebt in thepublic sector

Exports,realized

Working day and seasonally adjusted index.

Latest information July-September 2014.

Source: Statistics Finland / National Accounts

Export of goods and services by quarter, billion euros, at current prices

35

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

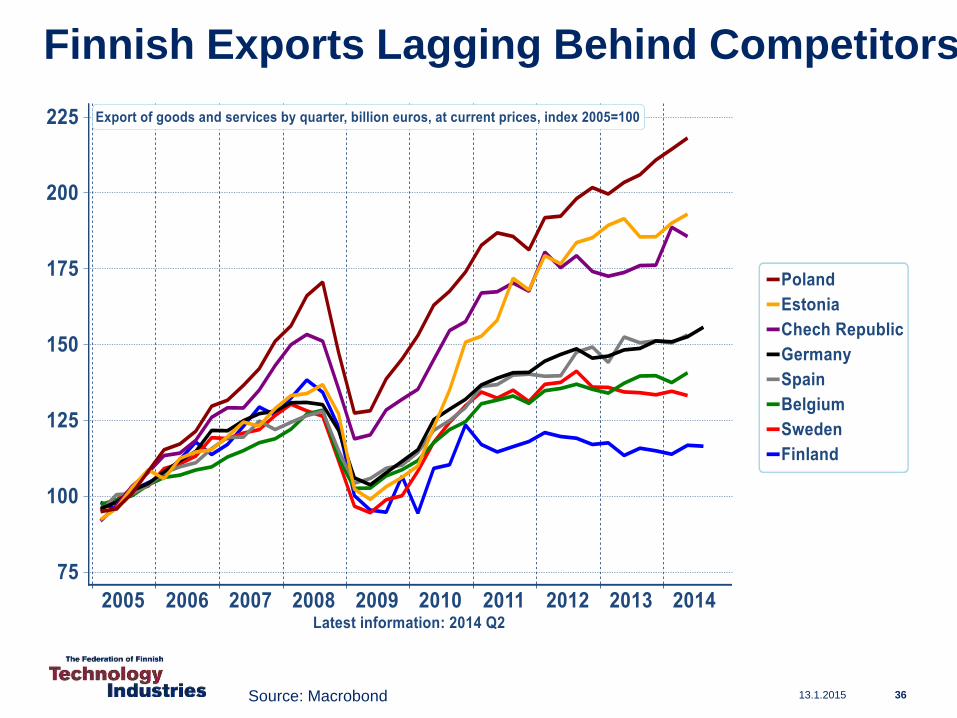

Finnish Exports Lagging Behind Competitors

13.1.2015 36Source: Macrobond

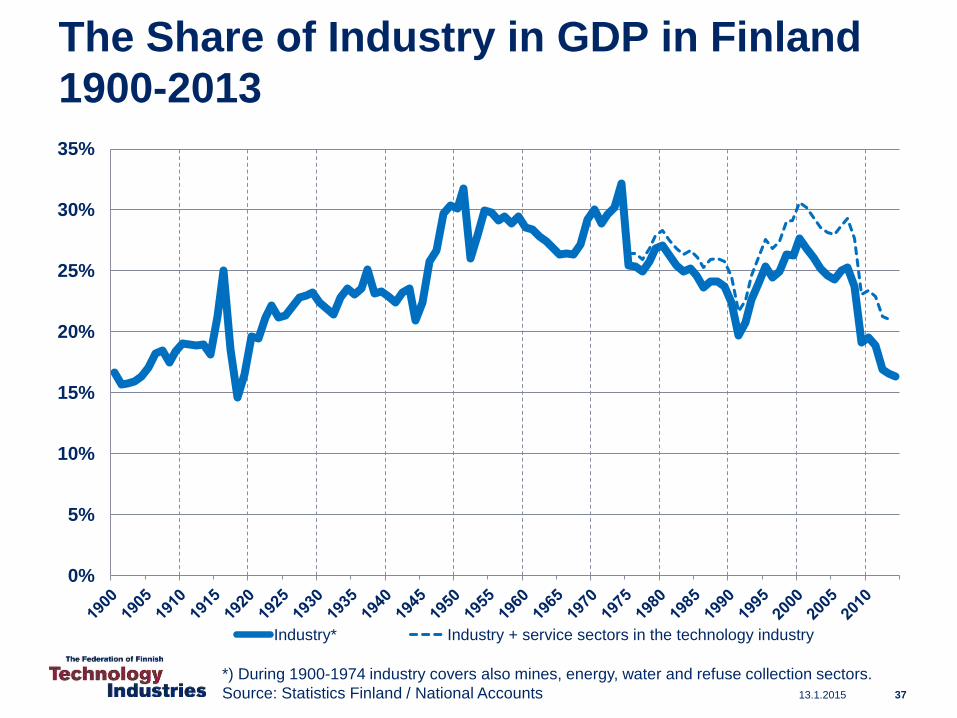

The Share of Industry in GDP in Finland

1900-2013

0%

5%

10%

15%

20%

25%

30%

35%

Industry* Industry + service sectors in the technology industry

*) During 1900-1974 industry covers also mines, energy, water and refuse collection sectors.

Source: Statistics Finland / National Accounts 13.1.2015 37

13.1.2015

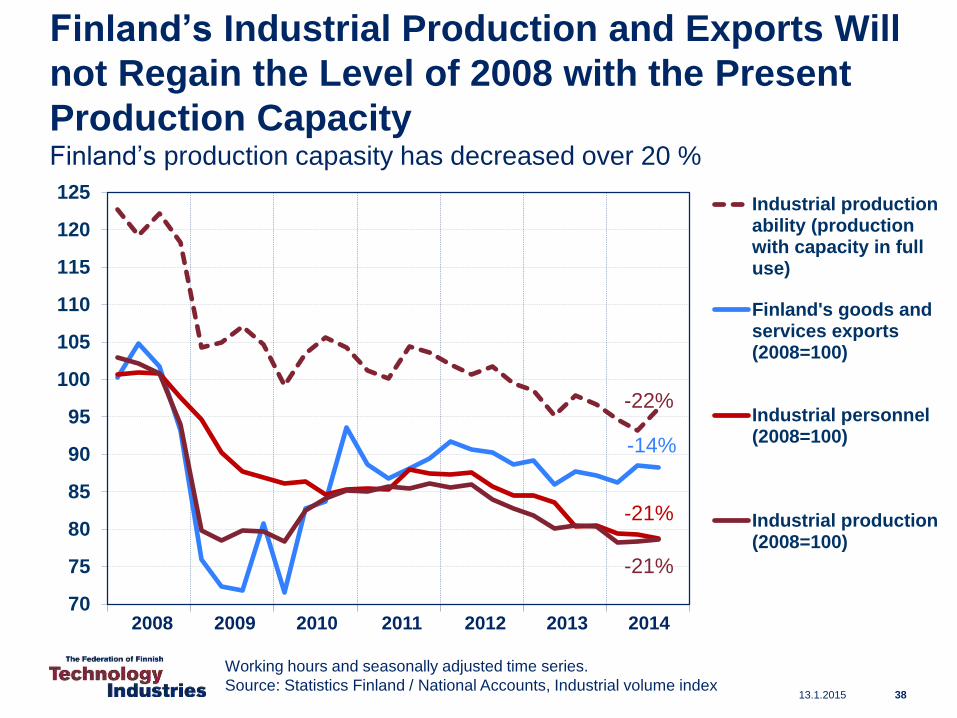

Finland’s Industrial Production and Exports Will

not Regain the Level of 2008 with the Present

Production CapacityFinland’s production capasity has decreased over 20 %

70

75

80

85

90

95

100

105

110

115

120

125Industrial productionability (productionwith capacity in fulluse)

Finland's goods andservices exports(2008=100)

Industrial personnel(2008=100)

Industrial production(2008=100)

-21%

-21%

-14%

Working hours and seasonally adjusted time series.

Source: Statistics Finland / National Accounts, Industrial volume index38

2008 2009 2010 2011 2012 2013 2014

-22%

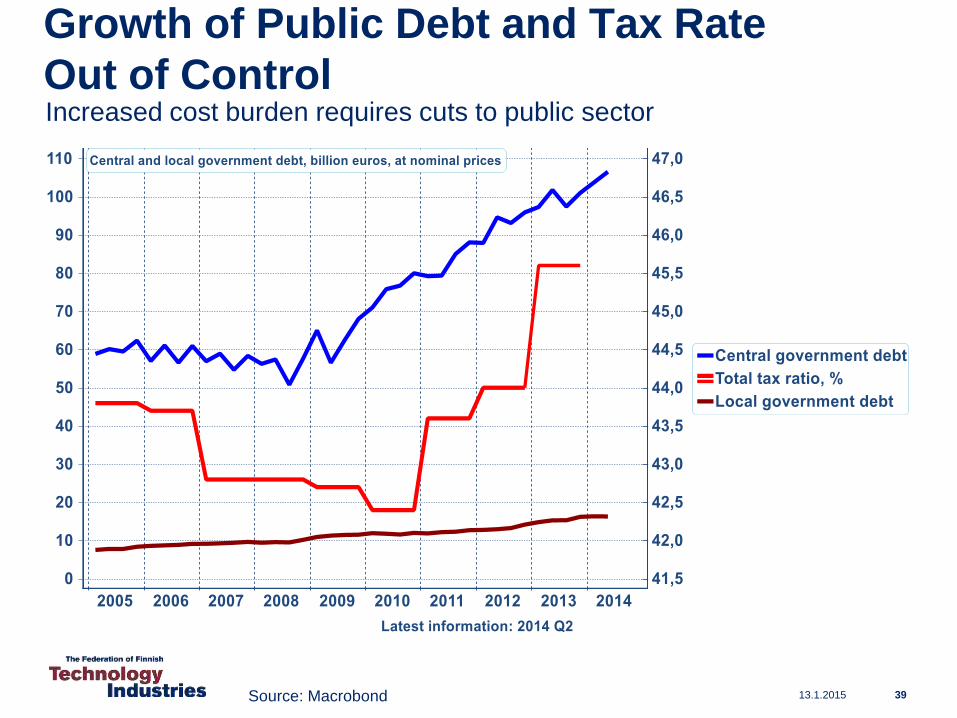

Growth of Public Debt and Tax Rate

Out of Control

13.1.2015 39

Increased cost burden requires cuts to public sector

Source: Macrobond

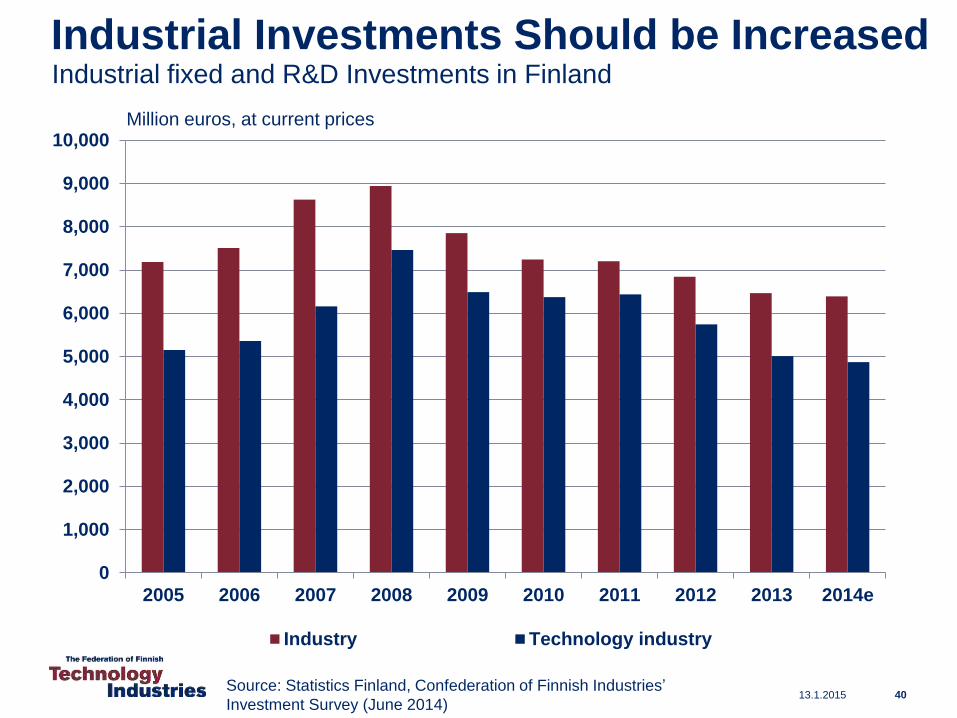

Industrial Investments Should be Increased

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014e

Industry Technology industry

Industrial fixed and R&D Investments in Finland

Source: Statistics Finland, Confederation of Finnish Industries’

Investment Survey (June 2014)13.1.2015 40

Million euros, at current prices

13.1.2015 41

80

85

90

95

100

105

110

115

120

125

130

135

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014e 2015e

USA

TheNetherlands

Switzerland

Sweden

Germany

Finland

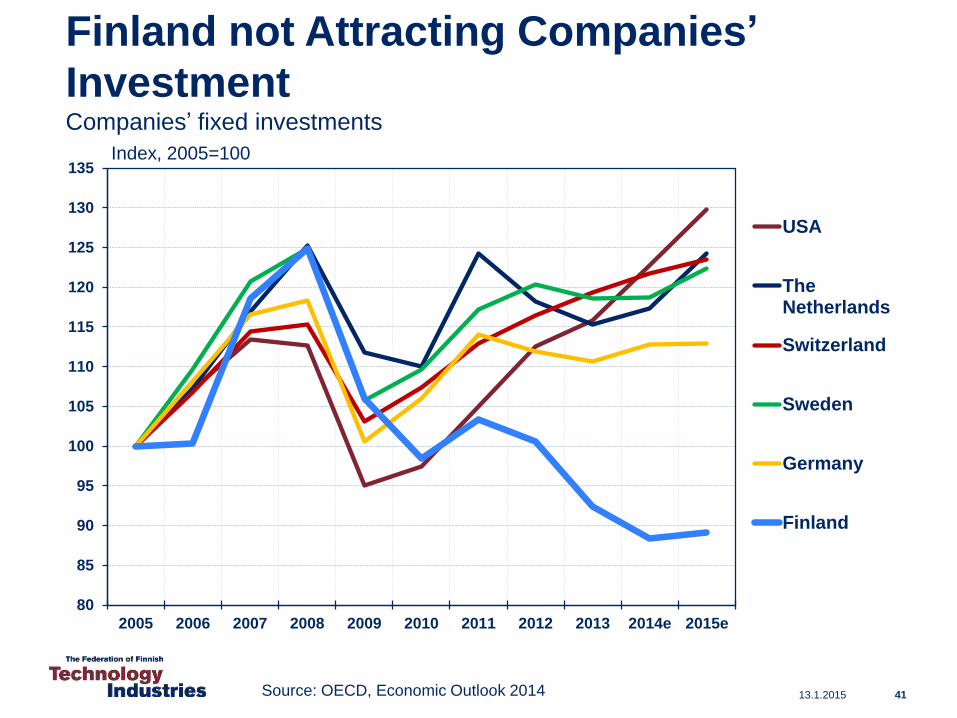

Finland not Attracting Companies’

InvestmentCompanies’ fixed investments

Source: OECD, Economic Outlook 2014

Index, 2005=100

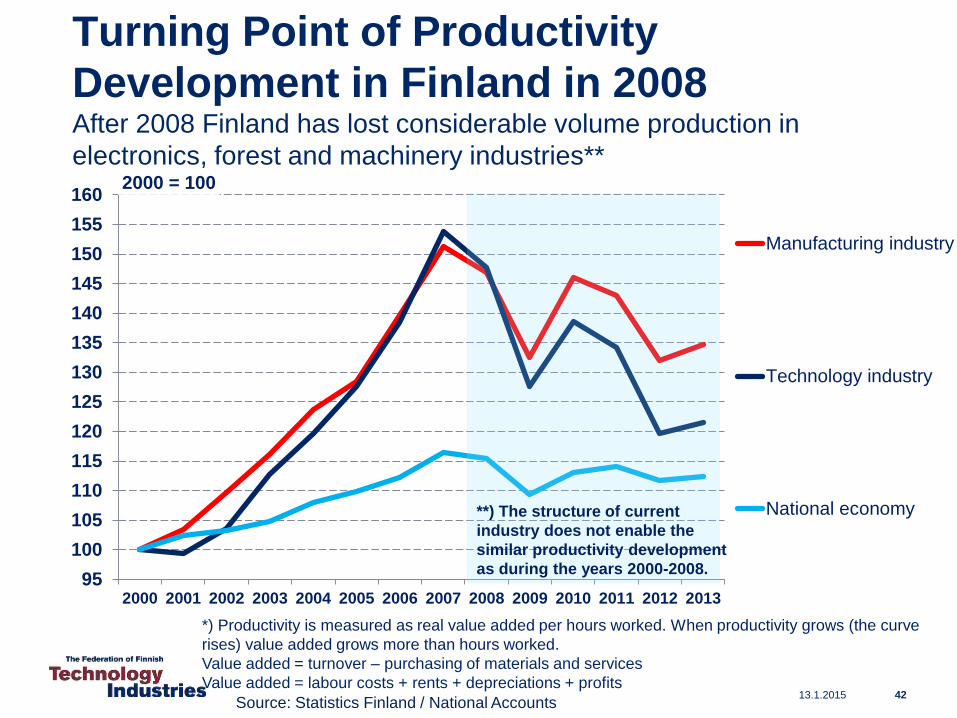

Turning Point of Productivity

Development in Finland in 2008After 2008 Finland has lost considerable volume production in

electronics, forest and machinery industries**

95

100

105

110

115

120

125

130

135

140

145

150

155

160

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

2000 = 100

Manufacturing industry

Technology industry

National economy

Source: Statistics Finland / National Accounts

*) Productivity is measured as real value added per hours worked. When productivity grows (the curve

rises) value added grows more than hours worked.

Value added = turnover – purchasing of materials and services

Value added = labour costs + rents + depreciations + profits13.1.2015 42

**) The structure of current

industry does not enable the

similar productivity development

as during the years 2000-2008.

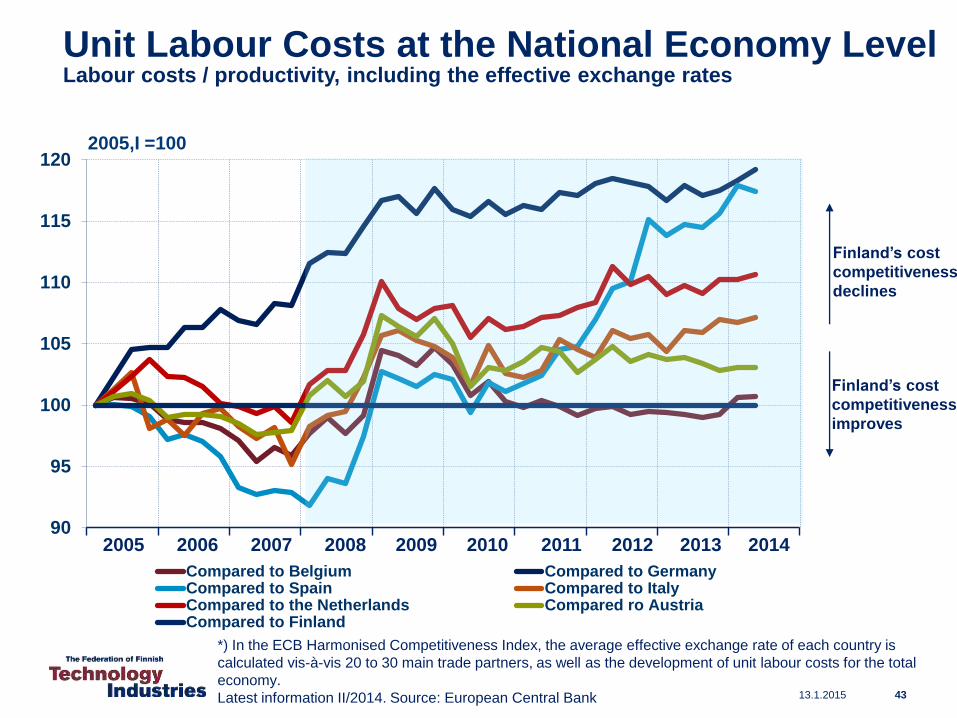

Unit Labour Costs at the National Economy Level Labour costs / productivity, including the effective exchange rates

90

95

100

105

110

115

120

Compared to Belgium Compared to GermanyCompared to Spain Compared to ItalyCompared to the Netherlands Compared ro AustriaCompared to Finland

*) In the ECB Harmonised Competitiveness Index, the average effective exchange rate of each country is

calculated vis-à-vis 20 to 30 main trade partners, as well as the development of unit labour costs for the total

economy.

Latest information II/2014. Source: European Central Bank

Finland’s cost

competitiveness

declines

2005,I =100

Finland’s cost

competitiveness

improves

13.1.2015 43

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

44

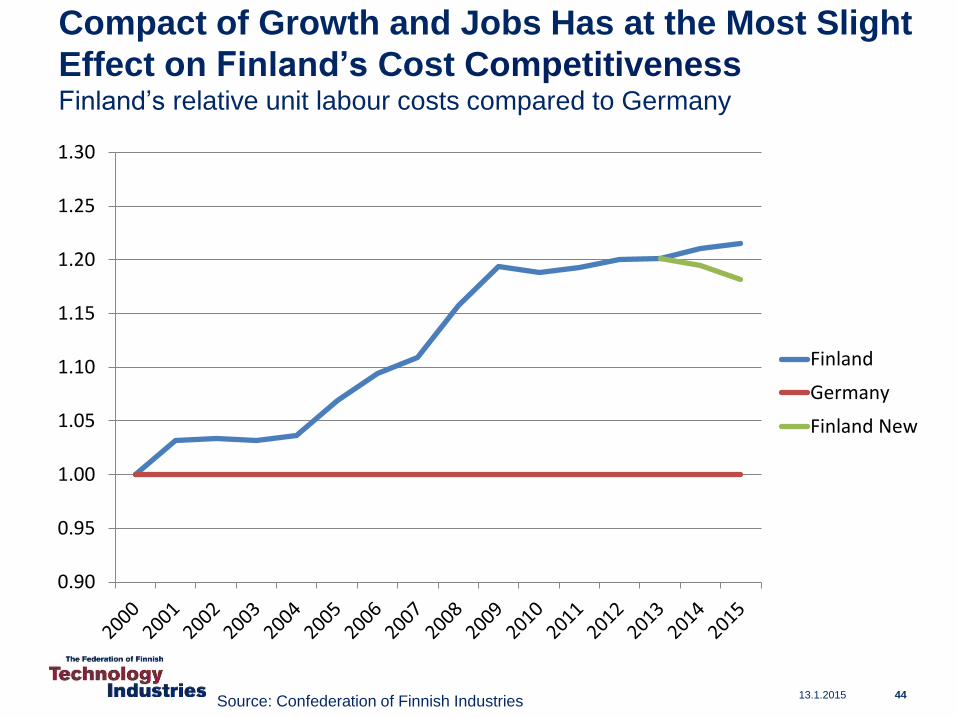

Compact of Growth and Jobs Has at the Most Slight

Effect on Finland’s Cost CompetitivenessFinland’s relative unit labour costs compared to Germany

0.90

0.95

1.00

1.05

1.10

1.15

1.20

1.25

1.30

Finland

Germany

Finland New

Source: Confederation of Finnish Industries13.1.2015

What should be done?

• Support the renewal of the industry

• Taxes should support growth and investment in Finland

• Support decision making in companies related to

compensation and working time

• No new European nor national burdens on companies,

which are deteriorating the competitiveness

13.1.2015 45

Long-Term Outlook and Challenges

• Global Structural Change Set to Continue Apace

– Industrial production and services will relocate to rapidly developing

economic areas

– Strong growth, large markets, cheap labour and increasing expertise will

increase the attractiveness of these regions.

• Competition over Skills and Raw Materials Set to Increase

– Due to an increase in retirement, the sector’s annual recruitment need in

Finland will rise considerably in the coming years.

– The availability of reasonably-priced energy also threatens to become an

investment bottleneck in Finland

• Combating Climate Change

– A challenge as costs are set to grow faster than in competitor countries

– An opportunity for new environmental and energy technologies

13.1.2015 46

The Federation of

Finnish Technology

Industries

13.1.2015 47

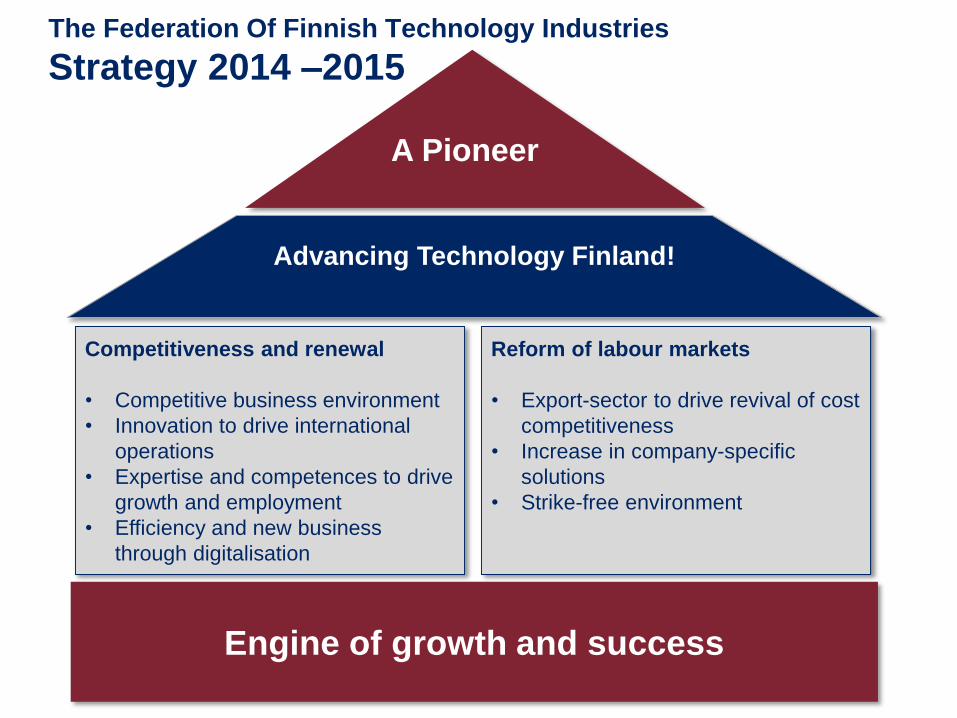

The Federation Of Finnish Technology Industries

Strategy 2014 –2015

Engine of growth and success

Advancing Technology Finland!

A Pioneer

Competitiveness and renewal

• Competitive business environment

• Innovation to drive international

operations

• Expertise and competences to drive

growth and employment

• Efficiency and new business

through digitalisation

Reform of labour markets

• Export-sector to drive revival of cost

competitiveness

• Increase in company-specific

solutions

• Strike-free environment

Technology Industries of Finland Centennial

Foundation

Laura Juvonen

Communications

Nora Elers

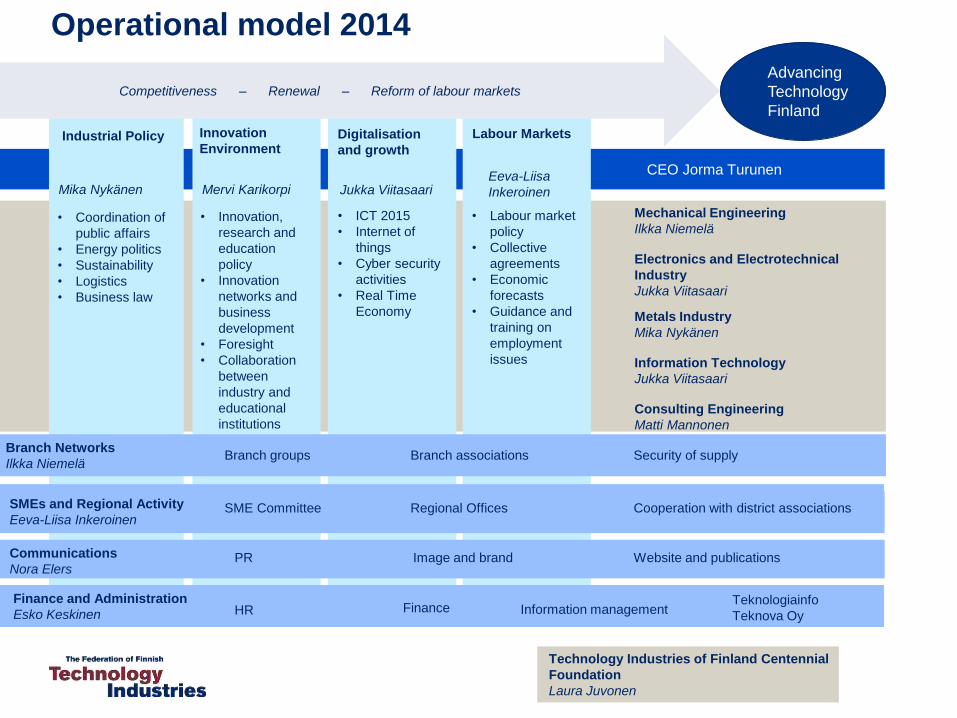

Operational model 2014

Industrial Policy

• Coordination of

public affairs

• Energy politics

• Sustainability

• Logistics

• Business law

Innovation

Environment

• Innovation,

research and

education

policy

• Innovation

networks and

business

development

• Foresight

• Collaboration

between

industry and

educational

institutions

Communications

Nora Elers

AluetoimistotYrittäjävaliokunta Piiriyhdistysyhteistyö

PR Image and brand

Mechanical Engineering

Ilkka Niemelä

Electronics and Electrotechnical

Industry

Jukka Viitasaari

Metals Industry

Mika Nykänen

Information Technology

Jukka Viitasaari

Consulting Engineering

Matti Mannonen

CEO Jorma Turunen

Advancing

Technology

Finland

Labour Markets

Website and publications

• Labour market

policy

• Collective

agreements

• Economic

forecasts

• Guidance and

training on

employment

issues

Digitalisation

and growth

• ICT 2015

• Internet of

things

• Cyber security

activities

• Real Time

Economy

Competitiveness – Renewal – Reform of labour markets

Eeva-Liisa

InkeroinenJukka ViitasaariMervi KarikorpiMika Nykänen

Regional Activity and Services

Eeva-Liisa Inkeroinen

SMEs and Regional Activity

Eeva-Liisa InkeroinenSME Committee Regional Offices Cooperation with district associations

Finance and Administration

Esko Keskinen HR Finance Information managementTeknologiainfo

Teknova Oy

Branch Networks

Ilkka NiemeläBranch groups Branch associations Security of supply

13.1.2015 50

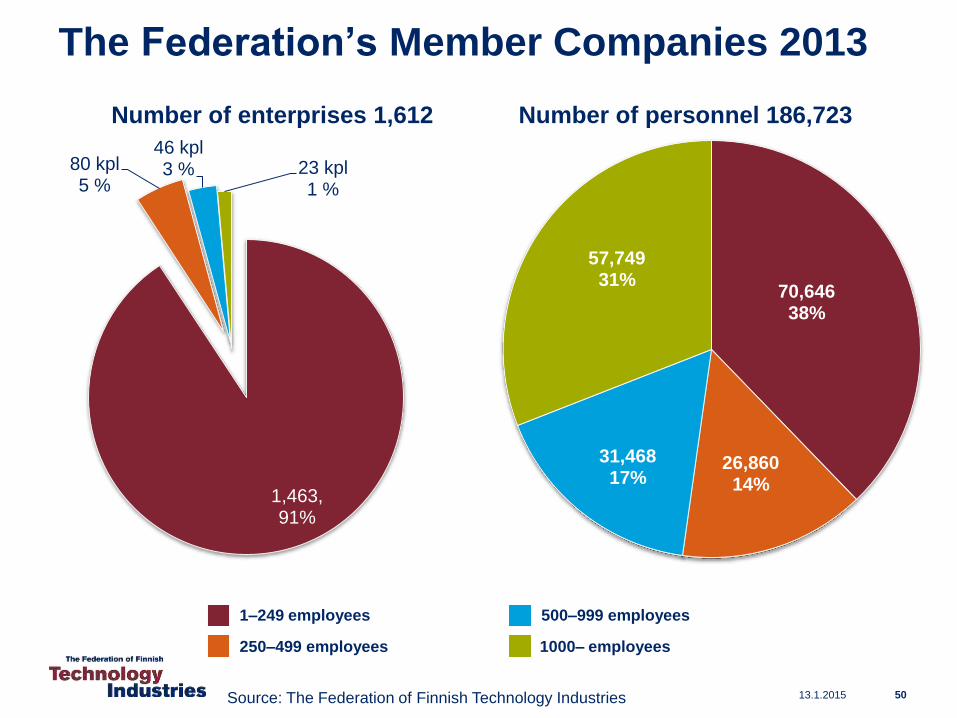

The Federation’s Member Companies 2013

1,463, 91%

80 kpl5 %

46 kpl3 % 23 kpl

1 %

Source: The Federation of Finnish Technology Industries

Number of enterprises 1,612 Number of personnel 186,723

1–249 employees

250–499 employees

500–999 employees

1000– employees

70,64638%

26,86014%

31,46817%

57,74931%

13.1.2015 51

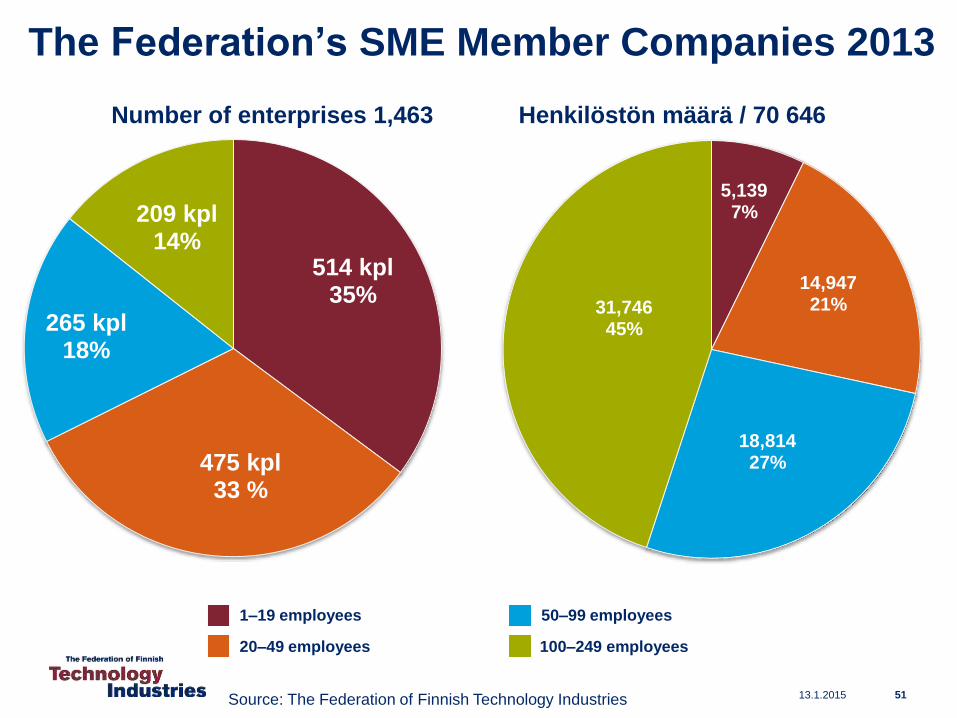

The Federation’s SME Member Companies 2013

514 kpl 35%

475 kpl33 %

265 kpl 18%

209 kpl 14%

Source: The Federation of Finnish Technology Industries

Number of enterprises 1,463 Henkilöstön määrä / 70 646

1–19 employees

20–49 employees

50–99 employees

100–249 employees

5,1397%

14,94721%

18,81427%

31,74645%

13.1.2015 52

Technology Is Everywhere

13.1.2015 53

The Technology Industry is also about Services

13.1.2015 54

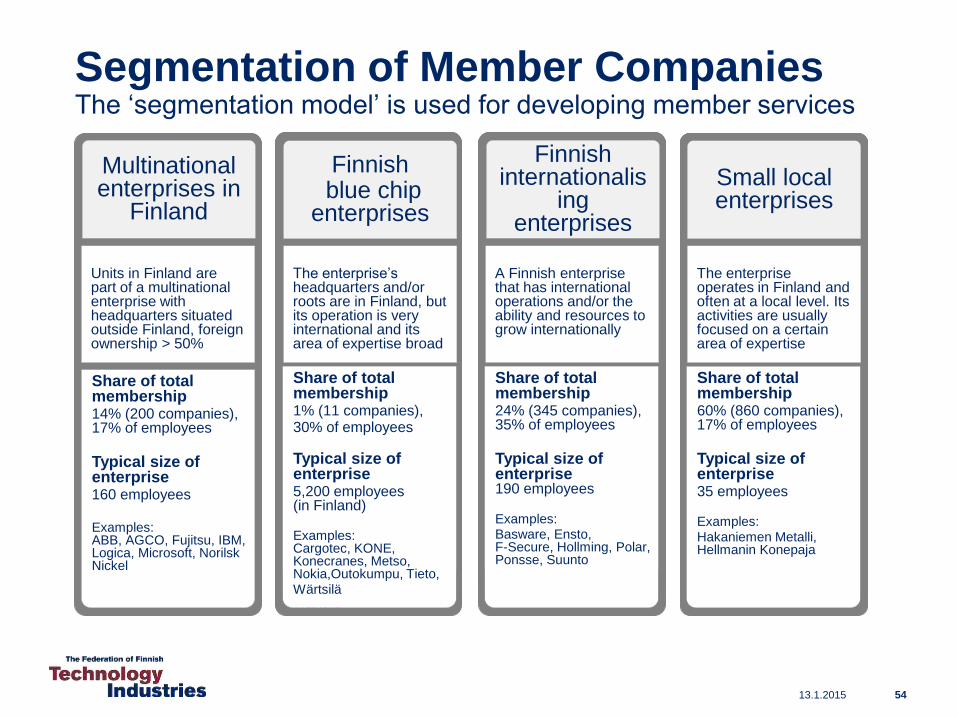

Segmentation of Member CompaniesThe ‘segmentation model’ is used for developing member services

Multinational enterprises in

Finland

Units in Finland are part of a multinational enterprise with headquarters situated outside Finland, foreign ownership > 50%

Share of totalmembership14% (200 companies), 17% of employees

Typical size of enterprise160 employees

Examples: ABB, AGCO, Fujitsu, IBM, Logica, Microsoft, NorilskNickel

Finnishblue chip

enterprises

The enterprise’s headquarters and/or roots are in Finland, but its operation is very international and its area of expertise broad

Share of total membership1 % (11 companies), 30 % of employees

Typical size of enterprise5 200 employees (in

Finland)

Examples: Cargotec, KONE, Konecranes, Metso, Nokia,Outokumpu, Rautaruukki, Tieto, Wärtsilä

Finnishinternationalis

ing enterprises

A Finnish enterprise that has international operations and/or the ability and resources to grow internationally

Share of total membership24 % (345 companies), 35 % of employees

Typical size of enterprise190 employees

Examples:Basware, Ensto, F-Secure, Hollming, Polar, Ponsse, Suunto

Small local enterprises

The enterprise operates in Finland and often at a local level. Its activities are usually focused on a certain area of expertise

Share of totalmembership60% (860 companies), 17% of employees

Typical size of enterprise35 employees

Examples:Hakaniemen Metalli, Hellmanin Konepaja

Share of totalmembership1% (11 companies), 30% of employees

Typical size of enterprise5,200 employees(in Finland)

Examples: Cargotec, KONE, Konecranes, Metso, Nokia,Outokumpu, Tieto, Wärtsilä

Share of totalmembership24% (345 companies), 35% of employees

Typical size of enterprise190 employees

Examples:Basware, Ensto, F-Secure, Hollming, Polar, Ponsse, Suunto

• The Federation - creating a

competitive business environment

– Promotes the interests of SMEs

– Supports expansion abroad

– Influences legislation

– Influences trade and industrial policy

– Promotes a competitive tax system

• Sub-sector and specialist groups

– Manage sub-sector specific

questions

13.1.2015 55

The Federation Promotes Entrepreneurship

13.1.2015 56

Working to Improve the Attractiveness of

the Sector

The Federation

• Provides information on jobs

and training within the sector for

teachers, parents and young

people

• Promotes collaboration between

companies and schools and

universities

• Works to enhance the image of

the sector.

13.1.2015 57

The Federation Is Here to Serve

• Provides labour market services and strives

to reshape working life:

– Guidance on employment issues

– Training and coaching

– Collective bargaining

– Improving productivity

– Influencing EU decision-making

• Publishes professional literature,

economic forecasts and statistics and

arranges seminars

• Provides legal services

Sub-sectors

13.1.2015 58

• 55 per cent of personnel employed

in Finland

• 70-80 per cent of sales from the

EU and neighbouring areas

• Urbanisation, and expansion in the

rapidly developing economies the

motor for growth

• Company presence in these areas

to continue to increase

• Increased R&D investment and

higher automation in production

required to improve

competitiveness

• High skilled and educated

personnel needed to replace

retiring employees

13.1.2015 59

Mechanical Engineering

fixed-investment products: machinery,

metal products,

vehicles

• Strong commitment to R&D

– in many fields over 10 per cent

of turnover

• Exports account for over 80 per

cent of sales

• Industry plays a vital role in the

development of the internet of

things (sensors collecting data)

• Competitiveness of enterprises

in Finland dependent upon:

– availability of university-level

experts

– effective commercial

exploitation of research

– finding the right niche

13.1.2015 60

Electronics and the Electro-technical

Industry

data and communications

equipment, electrical devices,

and instruments

• Rapidly growing economies

maintaining high demand for metals

and metal-based solutions.

• Exports account for 80 per cent of

sales

• Competitiveness of enterprises in

Finland dependent upon:

– the availability of a sufficiently skilled

workforce

– keeping up research of a high

standard

– reasonably-priced energy

– a competitive business environment

in the EU, especially regarding

climate and environmental policy

– reliable and reasonably-priced

logistics

13.1.2015 61

The Metals Industry

Steel products, non-ferrous metals, metal

based solutions, castings

• Thanks to digitalisation, demand for IT solutions is growing in all sectors of society

• IT solutions are needed for example in gaming industry, clean tech and health technology

• Finnish IT sector’s clients predominantly Finnish

• Growth of the sector in Finland requires

– a new customer-oriented approach from the sector’s enterprises

– education of the existing customer base

– new customers

– growth in the size of enterprises

– strong internationalisation

– skilled workforce

13.1.2015 62

Information Technology

IT solutions and services

• Companies are experts and designers in investment and development for industry, society and construction

• Competitiveness in Europe is good, global markets require new approaches

• Consulting engineering services are an important part of industrial company networks

• Over 60 percent of the employees have university degree education

• Competitiveness of the sector require– education and expert knowledge

– international expertise and networking

– investments and innovative solutions

– procurement emphasis on expertiseand quality

13.1.2015 63

Consulting Engineering

Knowledge intensive services for industry, society and construction