finding the right path - ashburton's perspective jan 2012

DESCRIPTION

With many uncertainties of 2011 still unresolved, we are positioned to take advantage of tactical opportunities managing risks. Ashburton's quarterly magazine - providing the latest maket insights and topical investment news.TRANSCRIPT

January 2012

PerspectiveWELCOME

Phew! What a year...

Ashburton’s Managing Director, Peter Bourne, shares his views on what to expect for the year ahead.

| OUTLOOK

Interesting times ahead

We gather global and regional insights from our investment team.

| GLOBAL EQUITIES

Capital and income

Introducing a new investment offering for long-term capital appreciation.

| MULTI ASSET

A new concept?

Pioneering the multi asset investment philosophy for 30 years.

| NEWS

Latest news

We welcome a new member to the Asset Allocation team and raise some money for charity.

| PERFORMANCE

Our latest fund performance figures as at 31 December 2011.

www.ashburton.comA member of the FirstRand Group

Finding the right pathWith many of the uncertainties of 2011 still unresolved, we are positioned to take advantage of tactical opportunities while managing risk.

Contents

Contributors

Tristan Hanson

Tristan is Ashburton’s Head of Asset Allocation, with responsibility for Ashburton’s Multi Asset Funds, Total Return Bond Funds and related research. He holds a Masters in Public Administration in International Development (MPA/ID) from Harvard University’s Kennedy School of Government and the Securities and Investments Diploma.

Derry Pickford

Derry joined Ashburton’s Asset Allocation team in December 2011 and has 12 years experience in the investment industry. Derry hold a BA(Hons) and MA(Hons) in Economics from the University of Cambridge (Clare College). He also holds the Investment Management Certificate (IMC).

Nicholas Lee

Nicholas is Ashburton’s Director of Investment and Fund Management. He has direct responsibility for the core strategies of Asset Management, Cash and Fixed Income and Equities. Nick joined Ashburton in 1988 and has 30 years experience in the investment industry. Nick is a member of the Securities Institute.

Veronika Pechlaner

Veronika is Ashburton’s Investment Manager responsible for Global Equities. She joined Ashburton’s European Equities team in 2008 from Goldman Sachs in London where she contributed as Executive Director to the pan European equity research product. Veronika has been a CFA charterholder since 2005 and holds a Master degree in Finance and International Management from the University of Innsbruck (Austria, E.U).

Tom Zambon

Tom is Ashburton’s Regional Sales Manager for the offshore islands, with responsibility for business development and building relationships with intermediaries who use Ashburton’s investment solutions for their clients. Tom joined Ashburton in 2004 after gaining 20 years offshore financial experience as an Independent Financial Adviser and is FPC qualified.

WelcomeAshburton’s Managing Director, Peter Bourne, recaps the major events of 2011 and looks forward to opportunities for the year ahead.

Outlook for 2012May You Live in Interesting Times 04 By Tristan Hanson & Derry Pickford While we do not expect 2012 to be easy, our aim will be to manage portfolios to take advantage of both short and longer-term opportunities, while protecting as best we can against downside risk.

Global equities

Diversification for Uncertain Times 07 By Nicholas Lee & Veronika Pechlaner To suit these uncertain times, Ashburton offers a unique way to get exposure to a focused list of leading global companies through the Ashburton Global Equity Portfolio solution.

Multi Asset

Multi Asset Investing 08 By Tom Zambon The diversification offered by a true multi asset fund may offer the investor a better chance of a consistent return without the worrying volatility usually associated with investing into ‘risk assets’.

NewsWe welcome a new member to the Asset Allocation team. 10 Plus, our Investment Director parts with his 40 year old moustache for a charity fundraiser.

PerformanceOur latest fund performance figures as at 31 December 2011. 11ContactsDetails for our contacts in Jersey, South Africa and the UK. 12

While this can quickly get a little depressing, I

should highlight that the prospect of negative

outcomes can quickly reverse to become the

reality of positive surprises. Markets have been

dealing with these implications for some time

now and we are a year further through the

necessary and long term rehabilitation of the

global financial system that triggered in 2008.

We do believe there will continue to be tactical

opportunities in select areas that we will be able

to take advantage of. Our extensive and proven

experience in multi asset investment stands us

in good stead to accomplish this.

Emerging markets remain a key focus area for

Ashburton as the balance of economic power

continues to shift away from developed nations.

As part of a leading African Financial Services

Group, we are particularly alert to opportunities

opening up in that continent, the Indian sub-

continent and beyond.

2012 promises to be an exciting year for

Ashburton. I trust that this Olympic year will be

rewarding and enjoyable for you as well!

Regards

Welcome

WELCOME | OUTLOOK | GLOBAL EQUITIES | MULTI ASSET | NEWS | PERFORMANCE | 2 | 3 |

Phew! What a year...

2011 was a tumultuous year. In twelve short months, the world was reshaped by a dramatic series of events. From floods to devastating earthquakes, from the economic decay of fiscal imbalances to the dithering inability of European leaders to address their own debt crisis, from the brutal dispatch of despot Gaddafi and Al-Qaeda leader Bin Laden and the death of Kim Jong-Il to the untimely loss of tech icon Steve Jobs, from riots in London and Moscow to the Arab Spring which set North Africa and the Middle East on an uneven path towards democracy, enabled in part for the first time by social media and technology, the sheer pace of these events set markets on an unrelenting rollercoaster ride for much of the year.

Peter BourneManaging Director

Looking forward as we do annually in this

edition of Perspective, it remains very difficult, if

not impossible, to predict an end to the volatility

that plagues investors. The Eurozone crisis

hangs over us like the Sword of Damocles, with

the absence of a clear path towards resolution

suggesting that it could get worse before it gets

better.

Elsewhere, there are signs of stabilisation in

other economies but not to the extent that will

yet excite markets. China remains a focal point

in terms of concerns over emerging market

growth even as the authorities move towards a

more accommodative policy stance, perhaps

ahead of the key leadership change scheduled

for this year.

And as democracy still struggles to take root

in the Arab Spring region, key presidential

elections in another three world powers, the

United States, Russia and France, will also

shape market direction and stability during the

year.

...the prospect of negative outcomes can quickly reverse to become the reality of positive surprises.

Emerging markets remain a key focus area for Ashburton as the balance of economic power continues to shift away from developed nations.

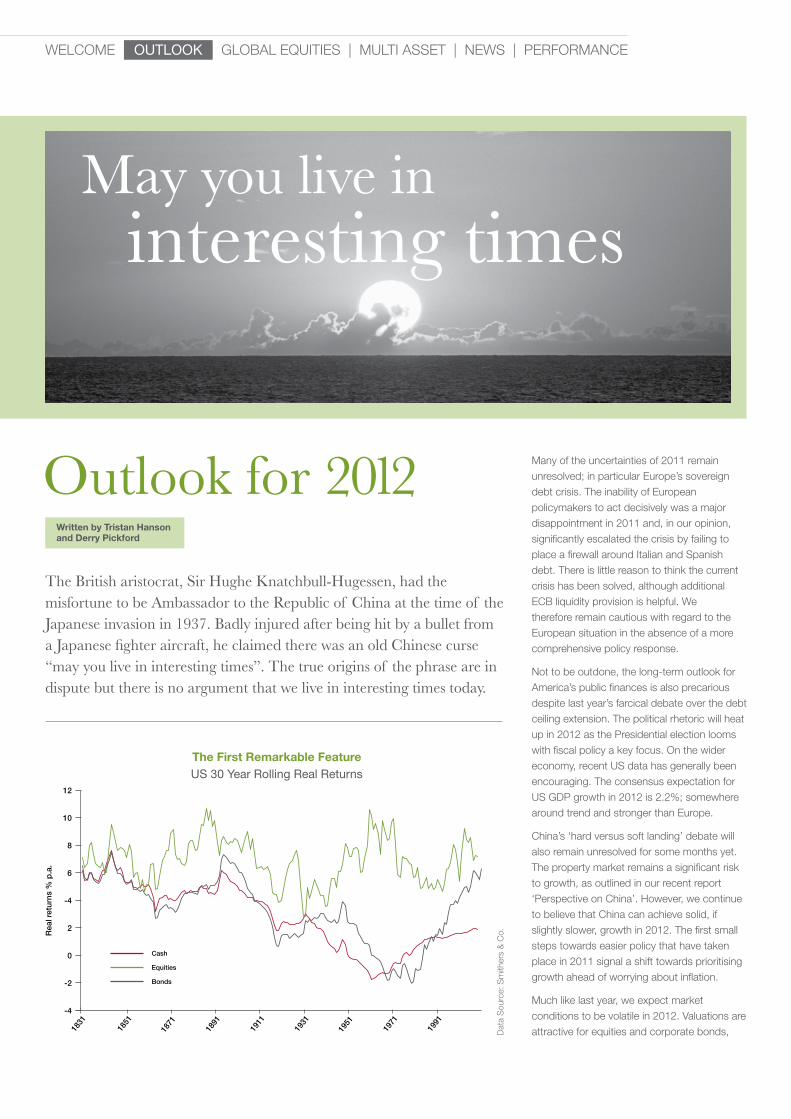

The First Remarkable FeatureUS 30 Year Rolling Real Returns

-4

-2

0

2

4

6

8

10

12

1831 1851 1871 1891 1911 1931 1951 1971 1991

Rea

l ret

urns

% p

.a.

Data Sources: Siegel 1801 - 1899 and DMS 1899 - 2010.

Dat

a S

ourc

e: S

mith

ers

& C

o.

10

12

-4

-2

0

2

-4

6

8

Rea

l ret

urns

% p

.a.

1851

1871

1891

1911

1931

1951

1971

1991

Cash

Equities

Bonds

1831

WELCOME | OUTLOOK | GLOBAL EQUITIES | MULTI ASSET | NEWS | PERFORMANCE

The British aristocrat, Sir Hughe Knatchbull-Hugessen, had the misfortune to be Ambassador to the Republic of China at the time of the Japanese invasion in 1937. Badly injured after being hit by a bullet from a Japanese fighter aircraft, he claimed there was an old Chinese curse “may you live in interesting times”. The true origins of the phrase are in dispute but there is no argument that we live in interesting times today.

Many of the uncertainties of 2011 remain unresolved; in particular Europe’s sovereign debt crisis. The inability of European policymakers to act decisively was a major disappointment in 2011 and, in our opinion, significantly escalated the crisis by failing to place a firewall around Italian and Spanish debt. There is little reason to think the current crisis has been solved, although additional ECB liquidity provision is helpful. We therefore remain cautious with regard to the European situation in the absence of a more comprehensive policy response.

Not to be outdone, the long-term outlook for America’s public finances is also precarious despite last year’s farcical debate over the debt ceiling extension. The political rhetoric will heat up in 2012 as the Presidential election looms with fiscal policy a key focus. On the wider economy, recent US data has generally been encouraging. The consensus expectation for US GDP growth in 2012 is 2.2%; somewhere around trend and stronger than Europe.

China’s ‘hard versus soft landing’ debate will also remain unresolved for some months yet. The property market remains a significant risk to growth, as outlined in our recent report ‘Perspective on China’. However, we continue to believe that China can achieve solid, if slightly slower, growth in 2012. The first small steps towards easier policy that have taken place in 2011 signal a shift towards prioritising growth ahead of worrying about inflation.

Much like last year, we expect market conditions to be volatile in 2012. Valuations are attractive for equities and corporate bonds,

Outlook for 2012Written by Tristan Hanson and Derry Pickford

May you live in interesting times

| 4 | 5 |

Given what is happening in Europe at the moment, is there a reason to be invested?

I agree with the sentiment that the situation we face is full of uncertainty, but that is why we are focusing on European companies that make their earnings abroad. In times of austerity, when consumers are spending less, we also prefer companies that have an ‘efficiency angle to them’ (without increasing prices, one way of improving margins is by reducing the unit cost of production). German industry, for example, has been at the forefront of productivity augmentation for years (having initially entered the euro at too strong a rate).

How is this ‘economic headwind’ affecting the content of your portfolio?

Calling the ‘market turn’ is exceptionally tough in the current environment, so our focus is on structural themes that may require a medium-term outlook. An example of such a theme is oil services:

Today the world uses approximately 88m barrels of oil per day (bpd). Assuming 4% global GDP growth until 2020, the world requires some 105m bpd; 17m bpd of additional demand. However, depletion of ageing fields means that 40m bpd needs to be replaced. Therefore 70%

We asked our lead fund managers for their views and insights on the outlook for their specific investment regions in 2012.

Regional Outlooks

of our investment rationale for oil services is independent of global growth.

The disaster in the Gulf of Mexico has also led to the urgent replacement of old, defunct equipment. Norwegian oil service companies are particular benefactors from this movement.

Do you have a favourite area, and if so, what is it?

Yes, Liquid Natural Gas (LNG) and in particular the shippers of LNG. In an age where traditional hydrocarbons are perceived as too dirty, renewables too reliant on (heavily indebted) government funding and nuclear as too dangerous (Fukishima), we are evidently turning to a cleaner carbon fuel; gas. The ability to transport the gas (super-cooled and in liquid form) moves the gas from being a ‘stranded’ resource to one that can be traded on an international market. Some markets are significantly over supplied (due to new techniques of production, called ‘fraccing’) and have low gas prices (e.g. US - $3Btu), whilst others are shifting their energy portfolios away from nuclear and towards gas (e.g. Japan and Germany) and are undersupplied, paying high prices (up to $17Btu). These vast regional price differentials provide an obvious incentive to transport and sell gas on the higher priced market.

European Equities, Richard Robinson

Q A&In times of austerity, when consumers are spending less, we prefer companies that have an ‘efficiency angle to them’...

although expectations for growth in corporate profits might be challenged by a difficult global economic backdrop. We see little value in developed market government bonds. US Treasuries have acted as a good hedge against the deteriorating economic environment but valuations are now stretched and we would need Japanese style deflation to get further upside in Treasuries on a medium-term horizon. We feel that the Federal Reserve has sufficient tools and determination to prevent this and the upside in bonds is now limited. For the first time in 180 years, the 30 year compound return on Treasuries has overtaken that on equities. This does not bode well for future returns from bonds. On our models we expect real returns from US Treasuries to be negative over the next 10 years.

Against this backdrop, maintaining the flexibility to take advantage of tactical opportunities and manage risks will be paramount. While we do not expect 2012 to be easy, our aim will be to manage portfolios to take advantage of both short and longer-term opportunities, while protecting as best we can against downside risk. With time we are confident that this approach will deliver the steady positive returns over the cycle, as has been the case for nearly three decades in our Asset Management portfolios and funds.

Much like last year, we expect market conditions to be volatile in 2012.

While we do not expect 2012 to be easy, our aim will be to manage portfolios to take advantage of both short and longer-term opportunities, while protecting as best we can against downside risk.

WELCOME | OUTLOOK | GLOBAL EQUITIES | MULTI ASSET | NEWS | PERFORMANCE

As US housing was at the epicentre of the US crisis in 2008, do you see any likelihood of a turnaround next year?

There are a number of reasons to be increasingly optimistic regarding the outlook for US housing. Affordability has improved, driven by lower prices and record low mortgage rates. The labour market is slowly improving and the US has generally favourable demographics while construction is at unsustainably low levels currently.

Will rising Chinese labour costs make US/ Mexican manufacturing supply chains more competitive?

Boston Consulting Group (BCG) estimate that by 2015 Chinese labour costs will be 25% more than in Mexico. Mexico benefits from duty-free access through NAFTA and much quicker transportation than the 21 days it takes to ship from China to the US West Coast. With improvement in border delays and Mexican infrastructure, there could be a real chance of developing a world beating supply chain.

US markets seem have been something of a safe haven in the past year; do you expect this to continue to be the case?

While there are a multitude of issues seething under the surface, and we have seen glimpses of them in the bitter fiscal negotiations between the Democrats and Republicans, the supporting factors for the US remain in place. These include a well regulated and efficient market offering investors liquidity, access to hungry world beating businesses plus indirect exposure to emerging markets. The dollar has gained from its safe haven status away from more unpredictable overseas currencies, whilst businesses have been recording quarter on quarter growth in earnings since 2009. On a final note, this year is the fourth year in the Presidential electoral cycle which is generally supportive of market sentiment.

How is Japan placed to take advantage of

the structural Asian growth story?

Japan has been geographically surrounded

by growth since 1999, yet has stagnated

itself. However, Japanese companies are now

not only out-sourcing production to Asia but

increasingly focusing on Asian markets for

their products. There are the obvious themes

in production automation, capital goods and

autos but under-recognised is the opportunity

Japanese banks have to grow in the region

as European and US banks retreat. Japan

may also join the Trans-Pacific Partnership, an

Asia-Pacific free trade alliance, which should

improve economic integration.

Japan is closing a year to forget with the

triple disaster in March 2011, what can we

expect in 2012 as Japan rebuilds itself?

Whilst companies and people have worked

hard to return to their pre-crisis lives, the

government has procrastinated. There are lots

of interesting reconstruction themes; with LNG

being a particularly interesting one given the

concerns about nuclear energy’s viability.

On some measures Japan’s fiscal

situation is worse than parts of the

Euro-zone. Does this concern you at all?

With government debt exceeding 200% of

GDP, and public finances stretched in the face

of declining tax revenues, one could easily get

worried about this. However, low economic

growth and stringent financial regulation

actually builds the appetite for JGBs. Since

JGBs are largely held domestically we don’t

see any immediate blow-up.

Emerging markets underperformed the major indices in 2011. Is the outlook really that bleak?

The short answer is no. Whilst emerging markets have not been immune from a slowdown, in the main they have the advantage of strong balance sheets, flexibility in taxation and labour laws and strong underlying demand. Perhaps the most important differentiator is that public debt in EM economies is substantially lower (38% of GDP) than industrialised nations. And whilst rising inflation, fuel and food prices have (rightly) given investors plenty of sleepless nights, inflationary pressures are easing and many EM central banks have already begun a process of marginal easing.

Where are valuations?

As an example let’s take China. MSCI China is trading at a 8.2x forward P/E multiple; over one standard deviation below its long term average. At these levels the market is pricing in a second wave global financial crisis scenario, unjustified in our view because the economy is actually doing reasonably well despite Beijing’s heavy-handed attempts to achieve a sharp slowdown in key areas. Indicators such as freight traffic, power production and retail sales all remain fairly buoyant. Thus we would argue that value is emerging for the genuine long-term investor.

Can we expect any surprises on the political front?

2012 is a key political year for many Asian economies. There is the issue of the Chinese Party leadership transition, Presidential and Legislative Yuan elections in Taiwan and several key state elections in India. We are less worried about the China situation, given that incoming leaders (Xi Jinping is likely to be President and Li Keqiang Vice Premier) have been part of a small decision making group responsible for orchestrating policy for years now. Taiwan elections are upon us in January and are delicately poised, although the Kuomintang Party has recently gained ground in the polls, following incumbent President Ma’s disastrous run of bad publicity. An opposition Demographic Progressive Party victory would

US Equities, Nick Skiming

Japan Equities, Simon Finch

Chindia Equities, Craig Farley

Q A&

Q A&

Q A&The dollar has gained from its safe haven status away from more unpredictable overseas currencies...

likely result in stricter measures to control property prices and a cooler cross-straits relationship with China, damaging sentiment. As for India, Prime Minister Singh’s latest U-turn to disallow foreign investment into the retail sector could not have been more poorly timed, given the decision making paralysis that has crippled government in 2011. India’s new generation are voting with their feet and have no issue dismissing governments that are not delivering on their mandate.

The Importance of Reinvested Dividends

56$

76$

86$

996$

9:6$

956$

976$

986$

;96$

;669

$

;66;$

;66;$

;66:$

;66:$

;66:$

;66<$

;66<$

;665

$

;665

$

;66=$

;66=$

;66=$

;667

$

;667

$

;66>$

;66>$

;66>$

;668

$

;668

$

;696

$

;696

$

;699

$

;699

$

;699

$

170

210

50

70

90

110

150

190

130

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

MSCI World Capital Return $ MSCI World Total Return $

WELCOME | OUTLOOK | GLOBAL EQUITIES | MULTI ASSET | NEWS | PERFORMANCE | 6 | 7 |

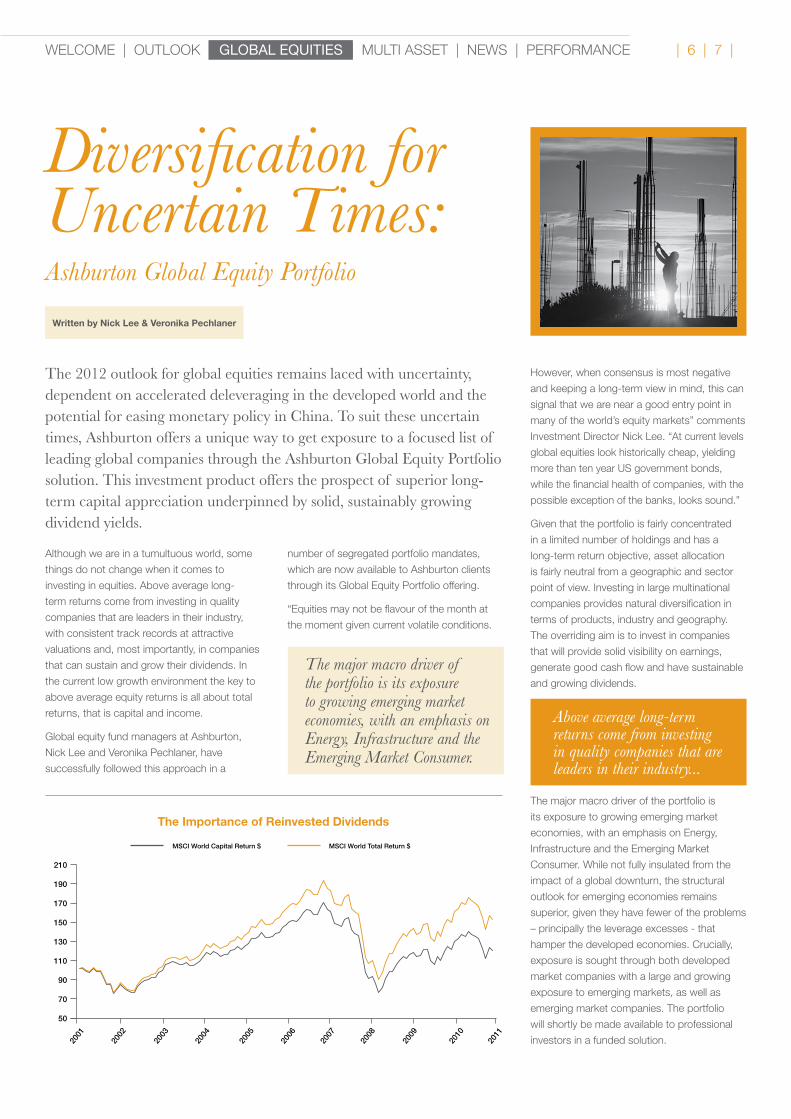

The 2012 outlook for global equities remains laced with uncertainty, dependent on accelerated deleveraging in the developed world and the potential for easing monetary policy in China. To suit these uncertain times, Ashburton offers a unique way to get exposure to a focused list of leading global companies through the Ashburton Global Equity Portfolio solution. This investment product offers the prospect of superior long-term capital appreciation underpinned by solid, sustainably growing dividend yields.

Although we are in a tumultuous world, some

things do not change when it comes to

investing in equities. Above average long-

term returns come from investing in quality

companies that are leaders in their industry,

with consistent track records at attractive

valuations and, most importantly, in companies

that can sustain and grow their dividends. In

the current low growth environment the key to

above average equity returns is all about total

returns, that is capital and income.

Global equity fund managers at Ashburton,

Nick Lee and Veronika Pechlaner, have

successfully followed this approach in a

number of segregated portfolio mandates,

which are now available to Ashburton clients

through its Global Equity Portfolio offering.

“Equities may not be flavour of the month at

the moment given current volatile conditions.

However, when consensus is most negative

and keeping a long-term view in mind, this can

signal that we are near a good entry point in

many of the world’s equity markets” comments

Investment Director Nick Lee. “At current levels

global equities look historically cheap, yielding

more than ten year US government bonds,

while the financial health of companies, with the

possible exception of the banks, looks sound.”

Given that the portfolio is fairly concentrated

in a limited number of holdings and has a

long-term return objective, asset allocation

is fairly neutral from a geographic and sector

point of view. Investing in large multinational

companies provides natural diversification in

terms of products, industry and geography.

The overriding aim is to invest in companies

that will provide solid visibility on earnings,

generate good cash flow and have sustainable

and growing dividends.

The major macro driver of the portfolio is

its exposure to growing emerging market

economies, with an emphasis on Energy,

Infrastructure and the Emerging Market

Consumer. While not fully insulated from the

impact of a global downturn, the structural

outlook for emerging economies remains

superior, given they have fewer of the problems

– principally the leverage excesses - that

hamper the developed economies. Crucially,

exposure is sought through both developed

market companies with a large and growing

exposure to emerging markets, as well as

emerging market companies. The portfolio

will shortly be made available to professional

investors in a funded solution.

Diversification for Uncertain Times: Ashburton Global Equity Portfolio

The major macro driver of the portfolio is its exposure to growing emerging market economies, with an emphasis on Energy, Infrastructure and the Emerging Market Consumer.

Above average long-term returns come from investing in quality companies that are leaders in their industry...

Written by Nick Lee & Veronika Pechlaner

The so-called “new” concept of Multi Asset Investment has been somewhat of a buzz phrase around the investment community in recent times. But is it really new, and what indeed does this offer the investor?

The definition that describes a Multi Asset fund will vary, but Ashburton’s view is that a true Multi Asset fund will offer a high level of diversification between different asset classes and across different geographical regions. In essence, the Ashburton approach would see an investor’s money being spread between assets such as equities; government bonds, corporate bonds, foreign exchange, commodities, Hedge Funds, property, and cash, to mitigate risk.

Ashburton is one of the few investment managers who utilise cash as an investment asset in its own right, and many investors are comforted to see that we are not afraid to

increase cash levels in our Funds during times of market stress. This overall strategy results in the portfolio having an inbuilt natural hedge against a potential downturn in one particular asset class.

Ashburton clients have had the benefit of this holistic style of investment management for over 30 years; and our first unitised Multi Asset Fund, the Ashburton Replica Asset Management Fund, was launched in 1992. Since then, the Fund has delivered an impressive 6.24% annual compound to investors, over a period which has witnessed both highs and lows for investment markets. The Asset Management

Funds have the simple but highly effective ethos of actively allocating between four main asset classes: equities, bonds, cash and foreign currency. The Funds are able to rebalance between these core assets in ways that many managed funds cannot; to take advantage of the upside and preserve against the downside.

More recently, we have enhanced the range of funds available under the Multi Asset banner by adding three Multi Asset Funds which are structured on a sliding scale of risk - cautious, balanced and aggressive. This allows investors to choose a fund suited to their investment objective and tolerance to risk, plus it offers the

Written by Tom ZambonRegional Sales Manager

Multi Asset Investing

Average Sterling Asset Management Personal Portfolio Replica Sterling Asset Management Fund

0

200

400

600

800

1000

1200

1400

2008 Lehmans Bros Collapse

1987 Black Monday

1990 Recession

1994 Bond Crisis

1997 Asian Crisis

1998 LTCM Collapse

1999 Technological Bubble

2001 9/11

2005 Global Credit Bubble

2007 Global

Liquidity Crunch

2010European sovereign

debt crisis

Jan 8

1Ja

n 82Ja

n 83Ja

n 84Ja

n 85Ja

n 86Ja

n 87Ja

n 88Ja

n 89Ja

n 90Ja

n 91Ja

n 92Ja

n 93Ja

n 94Ja

n 95Ja

n 96Ja

n 97Ja

n 98Ja

n 99Ja

n 00Ja

n 01Ja

n 02Ja

n 03Ja

n 04Ja

n 05Ja

n 06Ja

n 07Ja

n 08Ja

n 09Ja

n 10Ja

n 11

China overtakes Japanas No.2 Economy

1992 UK leaves ERM

2003Iraq War II

Ashburton Sterling Asset Managementa 30 year track record

Ashburton’s Asset Management Service, which encapsulates our investment philosophy, has experienced the highs and lows of booms and recessions, high and low inflation, high and low interest rates, and its performance over the years speaks for itself.

% GrowthS

ourc

e: L

ippe

r as

at 3

1/12

/201

0

WELCOME | OUTLOOK | GLOBAL EQUITIES | MULTI ASSET | NEWS | PERFORMANCE

| 8 | 9 |

flexibility of switching up or down this scale if these change. As well as utilising the traditional asset classes used in the Asset Management Funds, these new Multi Asset Funds can use commodities, hedge funds and alternative assets such as property to add diversity to portfolios.

So what does this mean for investors, and why should they be considering a Multi Asset approach? The answer could lie in the view that the diversification offered by a true multi asset fund may offer the investor a better chance of a consistent return without as much of the worrying volatility usually associated with investing into ‘risk assets.’ This view is highlighted by the profound changes we have seen in the world’s economy. Some believe that the investment world may never be quite the same again following the events we have all witnessed over the last five years or so. Investors who have traditionally taken directional bets on single assets such as equities may now look on with incredulity as the financial world lurches between crisis and meltdown. As a result, the word ‘volatility’ has now become part of everyday language for investors and it may remain that way for some time to come.

The Ashburton investment process embedded within the Multi Asset Funds is aimed at delivering long-term growth with reduced volatility. All of the funds take a global view; whereby the investment manager can seek out opportunities worldwide rather than concentrating risk within one geographical region.

Each of the Funds also has clearly defined parameters when it comes to risk taking. For instance, the Cautious Fund can never hold more than a 30% exposure to equities, whereas the Balanced Fund may increase this exposure up to 60%. We can also make use of efficient portfolio methods such as using derivatives to quickly and inexpensively reduce or increase exposure to risk assets when we see opportunities arise. The efficiency with which the funds can allocate between different asset classes, particularly in such volatile times as we have witnessed, is vital to the long-term success of the Funds.

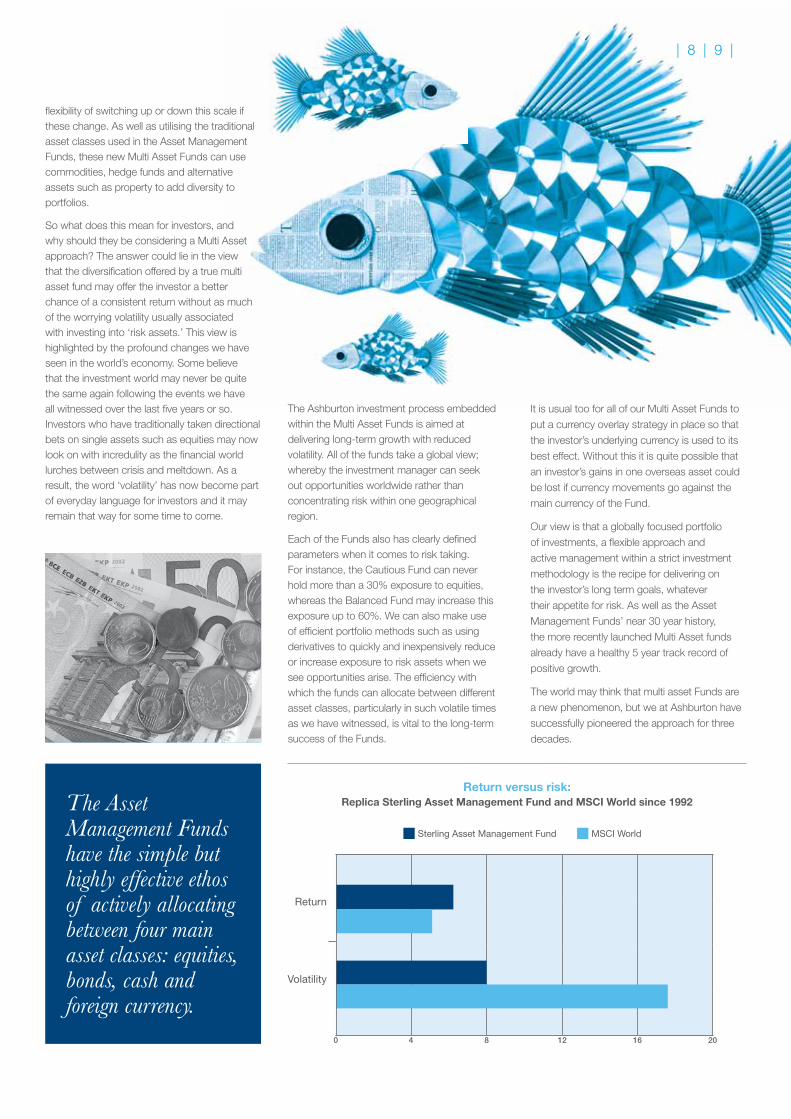

The Asset Management Funds have the simple but highly effective ethos of actively allocating between four main asset classes: equities, bonds, cash and foreign currency.

Return versus risk: Replica Sterling Asset Management Fund and MSCI World since 1992

It is usual too for all of our Multi Asset Funds to

put a currency overlay strategy in place so that

the investor’s underlying currency is used to its

best effect. Without this it is quite possible that

an investor’s gains in one overseas asset could

be lost if currency movements go against the

main currency of the Fund.

Our view is that a globally focused portfolio

of investments, a flexible approach and

active management within a strict investment

methodology is the recipe for delivering on

the investor’s long term goals, whatever

their appetite for risk. As well as the Asset

Management Funds’ near 30 year history,

the more recently launched Multi Asset funds

already have a healthy 5 year track record of

positive growth.

The world may think that multi asset Funds are

a new phenomenon, but we at Ashburton have

successfully pioneered the approach for three

decades.

Return

Volatility

Sterling Asset Management Fund MSCI World

0 4 8 12 16 20

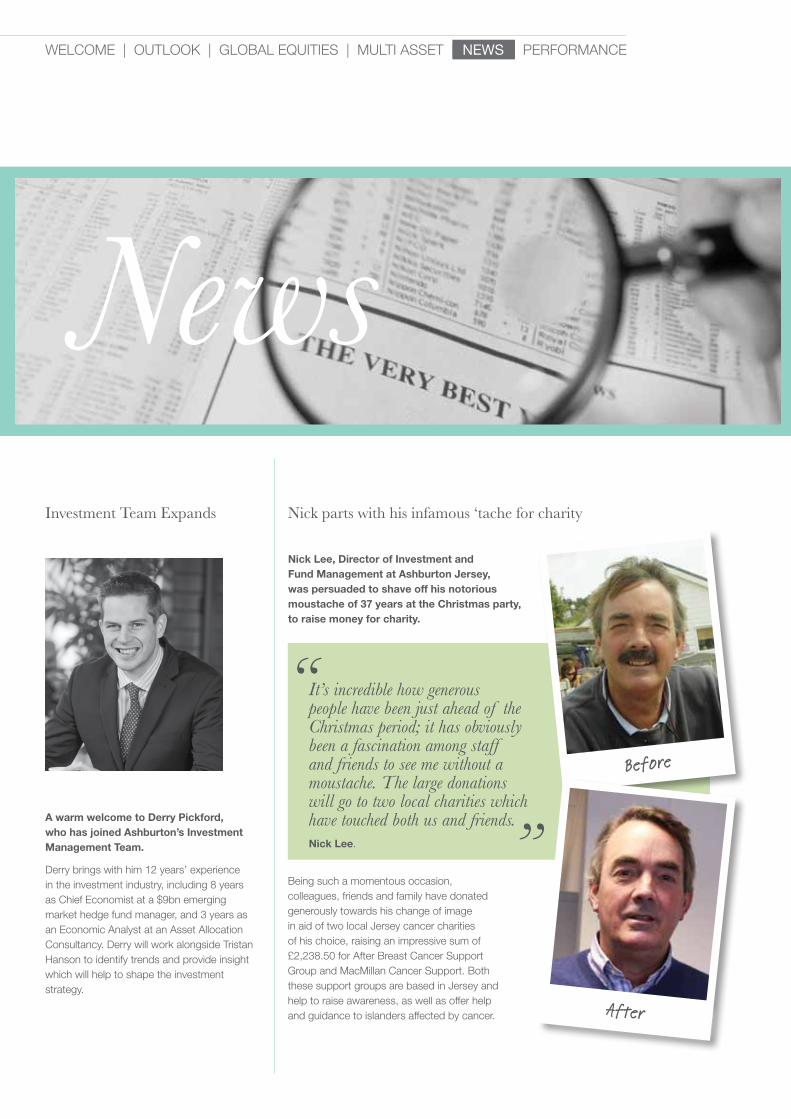

Being such a momentous occasion, colleagues, friends and family have donated generously towards his change of image in aid of two local Jersey cancer charities of his choice, raising an impressive sum of £2,238.50 for After Breast Cancer Support Group and MacMillan Cancer Support. Both these support groups are based in Jersey and help to raise awareness, as well as offer help and guidance to islanders affected by cancer.

NewsInvestment Team Expands Nick parts with his infamous ‘tache for charity

It’s incredible how generous people have been just ahead of the Christmas period; it has obviously been a fascination among staff and friends to see me without a moustache. The large donations will go to two local charities which have touched both us and friends.A warm welcome to Derry Pickford,

who has joined Ashburton’s Investment Management Team.

Derry brings with him 12 years’ experience in the investment industry, including 8 years as Chief Economist at a $9bn emerging market hedge fund manager, and 3 years as an Economic Analyst at an Asset Allocation Consultancy. Derry will work alongside Tristan Hanson to identify trends and provide insight which will help to shape the investment strategy.

WELCOME | OUTLOOK | GLOBAL EQUITIES | MULTI ASSET | NEWS | PERFORMANCE

Before

After

“

”Nick Lee.

Nick Lee, Director of Investment and Fund Management at Ashburton Jersey, was persuaded to shave off his notorious moustache of 37 years at the Christmas party, to raise money for charity.

| 10 | 11 |WELCOME | OUTLOOK | GLOBAL EQUITIES | MULTI ASSET | NEWS | PERFORMANCE

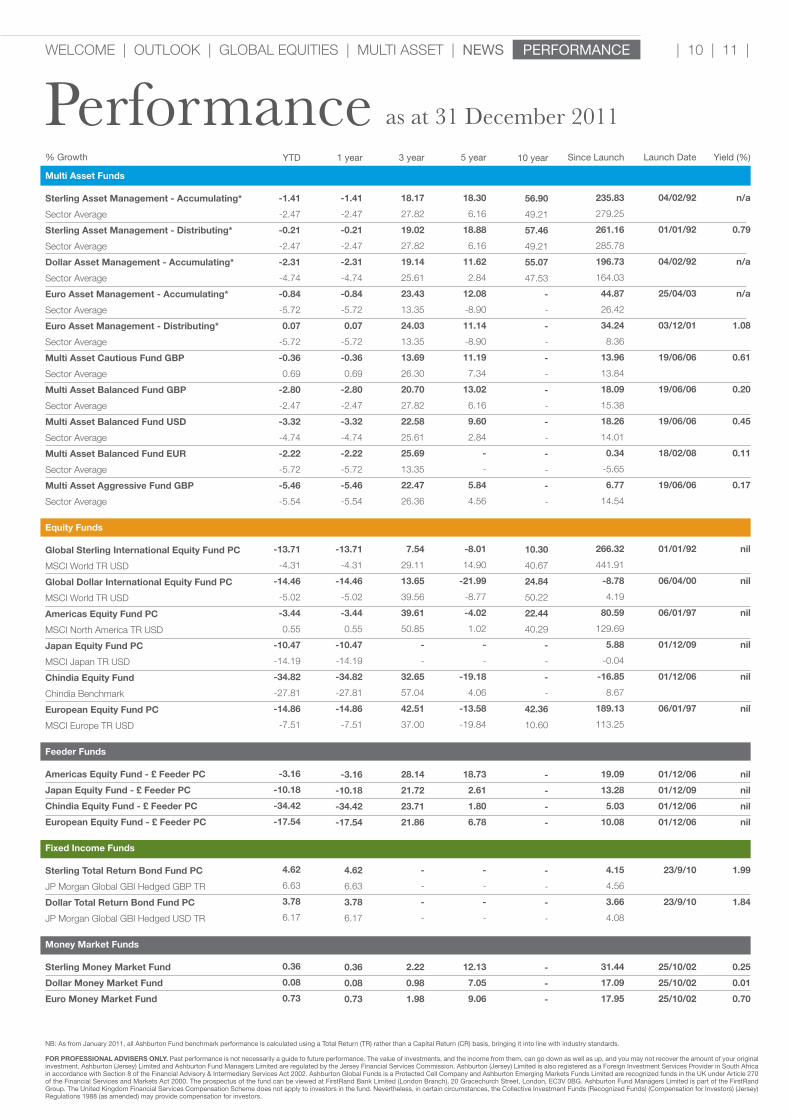

Performance as at 31 December 2011

NB: As from January 2011, all Ashburton Fund benchmark performance is calculated using a Total Return (TR) rather than a Capital Return (CR) basis, bringing it into line with industry standards.

FOR PROFESSIONAL ADVISERS ONLY. Past performance is not necessarily a guide to future performance. The value of investments, and the income from them, can go down as well as up, and you may not recover the amount of your original investment. Ashburton (Jersey) Limited and Ashburton Fund Managers Limited are regulated by the Jersey Financial Services Commission. Ashburton (Jersey) Limited is also registered as a Foreign Investment Services Provider in South Africa in accordance with Section 8 of the Financial Advisory & Intermediary Services Act 2002. Ashburton Global Funds is a Protected Cell Company and Ashburton Emerging Markets Funds Limited are recognized funds in the UK under Article 270 of the Financial Services and Markets Act 2000. The prospectus of the fund can be viewed at FirstRand Bank Limited (London Branch), 20 Gracechurch Street, London, EC3V 0BG. Ashburton Fund Managers Limited is part of the FirstRand Group. The United Kingdom Financial Services Compensation Scheme does not apply to investors in the fund. Nevertheless, in certain circumstances, the Collective Investment Funds (Recognized Funds) (Compensation for Investors) (Jersey) Regulations 1988 (as amended) may provide compensation for investors.

10 year

56.90

49.21

57.46

49.21

55.07

47.53

-

-

-

-

-

-

-

-

-

-

-

-

-

-

10.30

40.67

24.84

50.22

22.44

40.29

-

-

-

-

42.36

10.60

-

-

-

-

-

-

-

-

-

-

-

Multi Asset Funds

Sterling Asset Management - Accumulating*

Sector Average

Sterling Asset Management - Distributing*

Sector Average

Dollar Asset Management - Accumulating*

Sector Average

Euro Asset Management - Accumulating*

Sector Average

Euro Asset Management - Distributing*

Sector Average

Multi Asset Cautious Fund GBP

Sector Average

Multi Asset Balanced Fund GBP

Sector Average

Multi Asset Balanced Fund USD

Sector Average

Multi Asset Balanced Fund EUR

Sector Average

Multi Asset Aggressive Fund GBP

Sector Average

Equity Funds

Global Sterling International Equity Fund PC

MSCI World TR USD

Global Dollar International Equity Fund PC

MSCI World TR USD

Americas Equity Fund PC

MSCI North America TR USD

Japan Equity Fund PC

MSCI Japan TR USD

Chindia Equity Fund

Chindia Benchmark

European Equity Fund PC

MSCI Europe TR USD

Feeder Funds

Americas Equity Fund - £ Feeder PC

Japan Equity Fund - £ Feeder PC

Chindia Equity Fund - £ Feeder PC

European Equity Fund - £ Feeder PC

Fixed Income Funds

Sterling Total Return Bond Fund PC

JP Morgan Global GBI Hedged GBP TR

Dollar Total Return Bond Fund PC

JP Morgan Global GBI Hedged USD TR

Money Market Funds

Sterling Money Market Fund

Dollar Money Market Fund

Euro Money Market Fund

YTD

-1.41

-2.47

-0.21

-2.47

-2.31

-4.74

-0.84

-5.72

0.07

-5.72

-0.36

0.69

-2.80

-2.47

-3.32

-4.74

-2.22

-5.72

-5.46

-5.54

-13.71

-4.31

-14.46

-5.02

-3.44

0.55

-10.47

-14.19

-34.82

-27.81

-14.86

-7.51

-3.16

-10.18

-34.42

-17.54

4.62

6.63

3.78

6.17

0.36

0.08

0.73

1 year

-1.41

-2.47

-0.21

-2.47

-2.31

-4.74

-0.84

-5.72

0.07

-5.72

-0.36

0.69

-2.80

-2.47

-3.32

-4.74

-2.22

-5.72

-5.46

-5.54

-13.71

-4.31

-14.46

-5.02

-3.44

0.55

-10.47

-14.19

-34.82

-27.81

-14.86

-7.51

-3.16

-10.18

-34.42

-17.54

4.62

6.63

3.78

6.17

0.36

0.08

0.73

% Growth 3 year

18.17

27.82

19.02

27.82

19.14

25.61

23.43

13.35

24.03

13.35

13.69

26.30

20.70

27.82

22.58

25.61

25.69

13.35

22.47

26.36

7.54

29.11

13.65

39.56

39.61

50.85

-

-

32.65

57.04

42.51

37.00

28.14

21.72

23.71

21.86

-

-

-

-

2.22

0.98

1.98

5 year

18.30

6.16

18.88

6.16

11.62

2.84

12.08

-8.90

11.14

-8.90

11.19

7.34

13.02

6.16

9.60

2.84

-

-

5.84

4.56

-8.01

14.90

-21.99

-8.77

-4.02

1.02

-

-

-19.18

4.06

-13.58

-19.84

18.73

2.61

1.80

6.78

-

-

-

-

12.13

7.05

9.06

Since Launch

235.83

279.25

261.16

285.78

196.73

164.03

44.87

26.42

34.24

8.36

13.96

13.84

18.09

15.38

18.26

14.01

0.34

-5.65

6.77

14.54

266.32

441.91

-8.78

4.19

80.59

129.69

5.88

-0.04

-16.85

8.67

189.13

113.25

19.09

13.28

5.03

10.08

4.15

4.56

3.66

4.08

31.44

17.09

17.95

Launch Date

04/02/92

01/01/92

04/02/92

25/04/03

03/12/01

19/06/06

19/06/06

19/06/06

18/02/08

19/06/06

01/01/92

06/04/00

06/01/97

01/12/09

01/12/06

06/01/97

01/12/06

01/12/09

01/12/06

01/12/06

23/9/10

23/9/10

25/10/02

25/10/02

25/10/02

Yield (%)

n/a

0.79

n/a

n/a

1.08

0.61

0.20

0.45

0.11

0.17

nil

nil

nil

nil

nil

nil

nil

nil

nil

nil

1.99

1.84

0.25

0.01

0.70

JERSEY

Ashburton (Jersey) LimitedPO Box 23917 Hilary StreetSt HelierJerseyJE4 8SJ

Tom ZambonDirect dial: +44 (0)1534 512010Email: [email protected]

Kellie ChristianDirect dial: +44 (0)1534 512118Email: [email protected]

UK

London5th floor20 Gracechurch StreetLondon EC3V 0BGUnited Kingdom

Gavin FraserDirect dial: +44 (0)1534 512234Email: [email protected]

Terry JamesDirect dial: +44 (0)207 939 1803Email: [email protected]

SOUTH AFRICA

JohannesburgGround Floor5 Merchant Place9 Fredman DriveSandton2146South Africa

David ChristieDirect dial: +27 (0)11 245 5039Email: [email protected]

Claire DaviesDirect dial: +27 (0)11 245 5057Email: [email protected]

Eloise TrewinDirect dial: +27 (0)11 245 5040Email: [email protected]

Cape TownThe Pavilion155 Campground RoadNewlands7700South Africa

Adam BenzimraDirect dial: +27 (0)21 673 3502Email: [email protected]

DurbanBlock CTorino Court4 Crooked LaneHillcrest3610South Africa

Debbie MiskinDirect dial: +27 (0)31 560 7860Email: [email protected]

Global Contacts

The average investment results include the returns for all clients who were clients for the whole of each calendar year and are adjusted for money added or withdrawn. Figures for funds are calculated on a bid to bid price basis, ignoring any initial charge, with gross income re-invested. Personal portfolios are calculated at a mid-market basis. All figures are calculated as at 31 December 2011 on a rolling basis. The comparative index used in each case is that deemed to be most appropriate for each fund. The views expressed in Ashburton’s Perspective represent the collective views of the Ashburton investment team and the Ashburton external advisers, which will change with altering market conditions and may not necessarily be reflected in the composition of managed portfolios. Past performance is not necessarily a guide to future performance. The value of investments, and the income from them, can go down as well as up, and you may not recover the amount of your original investment. Ashburton (Jersey) Limited and Ashburton Fund Managers Limited are regulated by the Jersey Financial Services Commission. Ashburton (Jersey) Limited is also registered as a Foreign Investment Services Provider in South Africa in accordance with Section 8 of the Financial Advisory & Intermediary Services Act 2002. Ashburton Global Funds is a Protected Cell Company and a recognised fund in the UK under Article 270 of the Financial Services and Markets Act 2000. The prospectus of the fund can be viewed at FirstRand Bank Limited (London Branch), 20 Gracechurch Street, London, EC3V 0BG. Ashburton Fund Managers Limited is part of the First Rand Group. The United Kingdom Financial Services Compensation Scheme does not apply to investors in the fund. Nevertheless, in certain circumstances, the Collective Investment Funds (Recognised Funds) (Compensation for Investors) (Jersey) Regulations 1988 (as amended) may provide compensation for investors.