financial year-end closing of 2012 module #1 part 2 /3

DESCRIPTION

„ESTIMATES: PROVISION FOR DOUBTFUL DEBT, INVENTORY PROVISIONS, PROVISIONS FOR LIABILITIES” SELF-CHECK OF ACCOUNTING CALCULATIONS 24EasyAudit is an additional tool to traditional consulting in the financial and tax reporting and in many instances it can replace such consulting. See what kind of services are available in 24EasyAudit! The 24EasyAudit service is not focused on presenting technical aspects, regulations, interpretations, jurisdiction, etc. but places stress on solving accounting and reporting problems. The 24EasyAudit service is not focused on presenting technical aspects, regulations, interpretations, jurisdiction, etc. but places stress on solving accounting and reporting problems. The support provided to users by 24EasyAudit results from an innovative web application combining a number of financial audit techniques and methods with an expanded systems of tooltips and help. How to calculate cash flow? How to calculate deferred tax? How to calculate inventory provision? How to calculate provision for debtors? Find us: https://24easyaudit.com/ facebook.com/24EasyAudit linkedin.com/company/24easyaudit slideshare.net/24EasyAudit twitter.com/24EasyAudit SAMODZIELNE SPRAWDZANIE KSIĘGOWYCH KALKULACJI 24EasyAudit to uzupełnienie tradycyjnego doradztwa w sprawozdawczości finansowej i podatkowej, a w wielu przypadkach takie doradztwo zastępuje. Zapoznaj się z usługami wbudowanymi w 24EasyAudit ! Serwis 24EasyAudit nie skupia się na prezentowaniu suchych treści merytorycznych, przepisów, interpretacji, orzecznictwa itp., lecz kładzie nacisk na praktyczne rozwiązywanie problemów księgowych i sprawozdawczych. Serwis 24EasyAudit to pakiet usług elektronicznych z zakresu rachunkowości i podatków dostarczanych on-line przez stronę www, który adresowany jest głównie do księgowych i dyrektorów finansowych, działów sprawozdawczości, biur rachunkowych, kontrolerów finansowych, audytorów wewnętrznych, biegłych rewidentów i doradców podatkowych, pracujących dla lub obsługujących małe, średnie i duże firmy prowadzące pełną księgowość, a także do kierownictwa, organów nadzorczych i właścicieli takich podmiotów. Jak liczyć przepływy pieniężne? Jak liczyć podatek odroczony? Jak liczyć odpis na zapasy? Jak liczyć odpis na należności? Znajdź nas: https://24easyaudit.pl/ facebook.com/24EasyAudit linkedin.com/company/24easyaudit slideshare.net/24EasyAudit twitter.com/24EasyAuditTRANSCRIPT

.

Financial year-end closing of 2012 Module #1 Part 2 /3

„ESTIMATES: PROVISION FOR DOUBTFUL DEBT, INVENTORY PROVISIONS, PROVISIONS FOR

LIABILITIES”

Training on accounting and income tax aspects related to financial year-end closing of 2012. Common errors and fast remedies.

© 2012 EASYAUDIT Sp. z o.o. with its registered office in Gdynia. All rights reserved. December 2012 https://24easyaudit.com.

• Module 1: Estimates: provision for doubtful debt, inventory provisions, provisions for

liabilities

• Module 2: Fixed assets: impairment testing of fixed assets, depreciation, accounting for

financial leasing

• Module 3: Cash flow statement

• Module 4: Corporate income tax, recognition of income and expenses – Deferred tax and

Corporation tax

• 24EasyAudit: Information on the Web application supporting accounting at balance sheet

closing for 2012

Content of the training

.

© 2012 EASYAUDIT Sp. z o.o. with its registered office in Gdynia. All rights reserved. December 2012 https://24easyaudit.com.

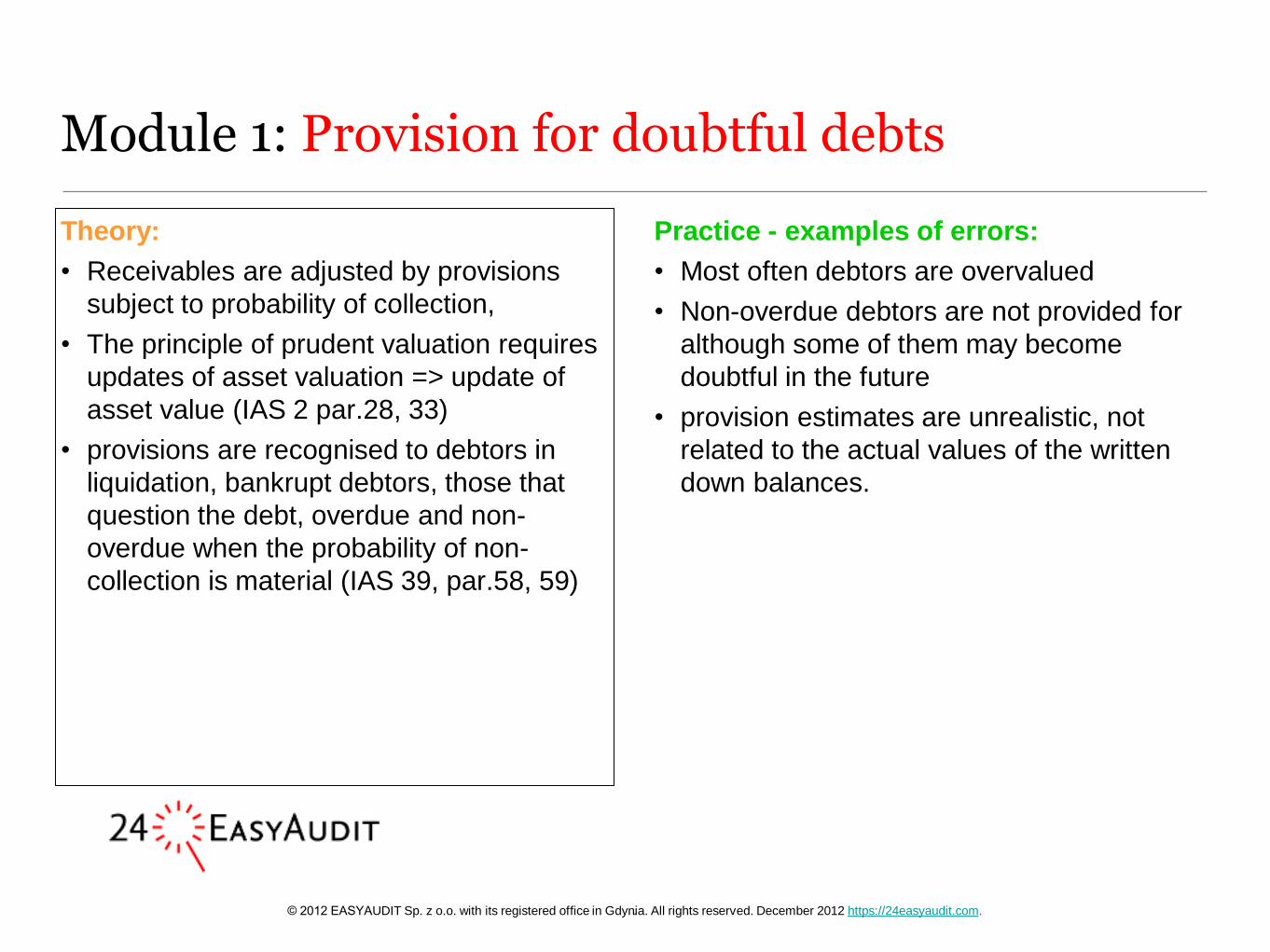

Module 1: Provision for doubtful debts

.

Do you know that …?

An assumption is often made that there is no

problem with current debtors and no analysis

is made of collection records.

However, provision for debtors should also

apply to debtors that are not overdue since

most probably a portion of them will become

uncollectible in the future. An appropriate

analysis will determine the potentially

uncollectible portion.

© 2012 EASYAUDIT Sp. z o.o. with its registered office in Gdynia. All rights reserved. December 2012 https://24easyaudit.com.

Module 1: Provision for doubtful debts

Theory:

• Receivables are adjusted by provisions

subject to probability of collection,

• The principle of prudent valuation requires

updates of asset valuation => update of

asset value (IAS 2 par.28, 33)

• provisions are recognised to debtors in

liquidation, bankrupt debtors, those that

question the debt, overdue and non-

overdue when the probability of non-

collection is material (IAS 39, par.58, 59)

.

Practice - examples of errors:

• Most often debtors are overvalued

• Non-overdue debtors are not provided for

although some of them may become

doubtful in the future

• provision estimates are unrealistic, not

related to the actual values of the written

down balances.

© 2012 EASYAUDIT Sp. z o.o. with its registered office in Gdynia. All rights reserved. December 2012 https://24easyaudit.com.

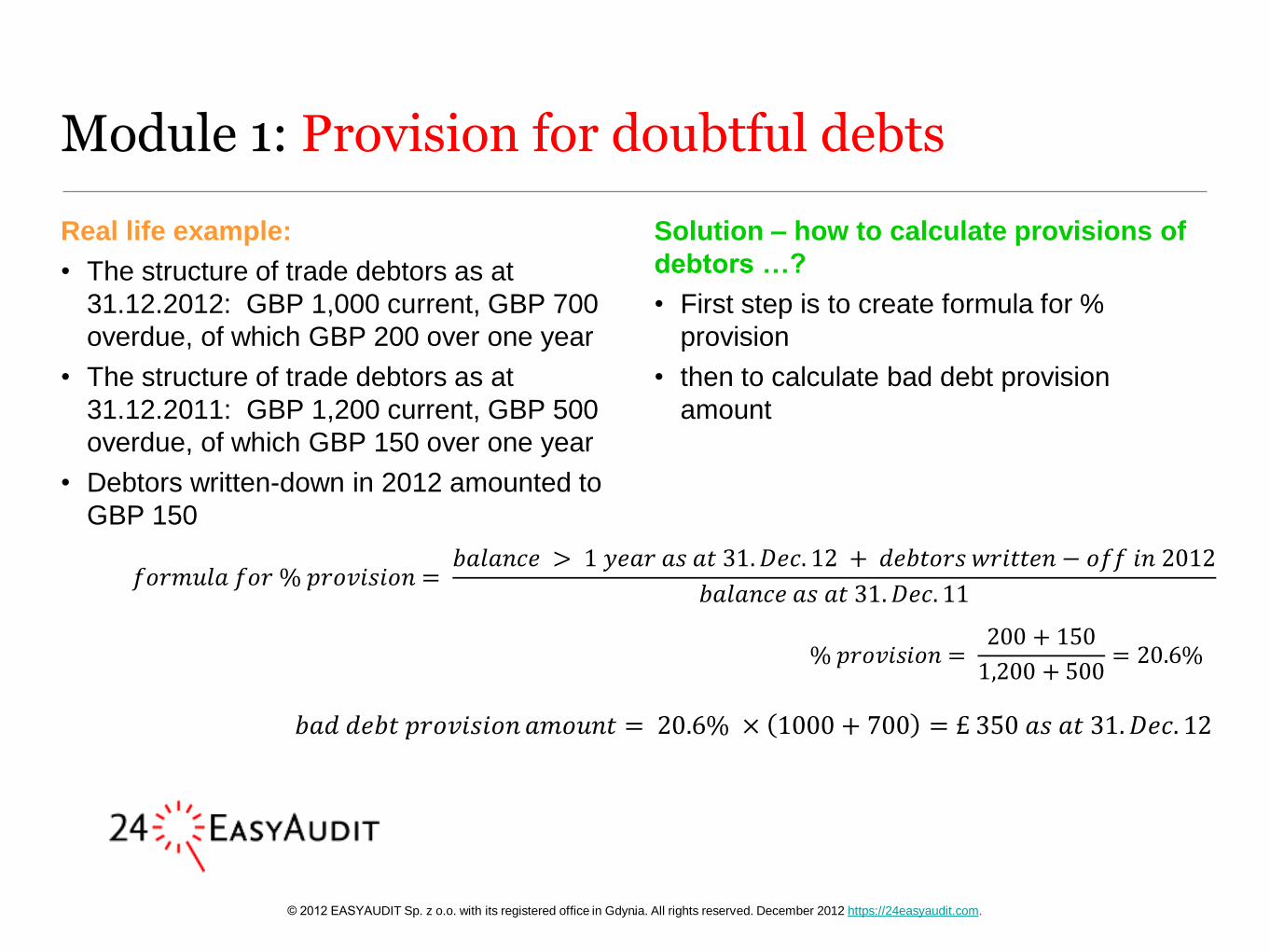

Module 1: Provision for doubtful debts

Real life example:

• The structure of trade debtors as at

31.12.2012: GBP 1,000 current, GBP 700

overdue, of which GBP 200 over one year

• The structure of trade debtors as at

31.12.2011: GBP 1,200 current, GBP 500

overdue, of which GBP 150 over one year

• Debtors written-down in 2012 amounted to

GBP 150

.

Solution – how to calculate provisions of

debtors …?

• First step is to create formula for %

provision

• then to calculate bad debt provision

amount

% 𝑝𝑟𝑜𝑣𝑖𝑠𝑖𝑜𝑛 = 200 + 150

1,200 + 500= 20.6%

𝑓𝑜𝑟𝑚𝑢𝑙𝑎 𝑓𝑜𝑟 % 𝑝𝑟𝑜𝑣𝑖𝑠𝑖𝑜𝑛 = 𝑏𝑎𝑙𝑎𝑛𝑐𝑒 > 1 𝑦𝑒𝑎𝑟 𝑎𝑠 𝑎𝑡 31. 𝐷𝑒𝑐. 12 + 𝑑𝑒𝑏𝑡𝑜𝑟𝑠 𝑤𝑟𝑖𝑡𝑡𝑒𝑛 − 𝑜𝑓𝑓 𝑖𝑛 2012

𝑏𝑎𝑙𝑎𝑛𝑐𝑒 𝑎𝑠 𝑎𝑡 31. 𝐷𝑒𝑐. 11

𝑏𝑎𝑑 𝑑𝑒𝑏𝑡 𝑝𝑟𝑜𝑣𝑖𝑠𝑖𝑜𝑛 𝑎𝑚𝑜𝑢𝑛𝑡 = 20.6% × 1000 + 700 = £ 350 𝑎𝑠 𝑎𝑡 31. 𝐷𝑒𝑐. 12

© 2012 EASYAUDIT Sp. z o.o. with its registered office in Gdynia. All rights reserved. December 2012 https://24easyaudit.com.

Module 1: Provision for doubtful debts

Errors can arise when:

• You have no precise idea how to calculate

provisions for debtors

• You do not refer your calculation of the

provision to what happened to the debtors

in the past (aging analysis, written-off

balances, etc.)

• You have scarce information and this is

the only thing you can rely on in calculating

the provisions for debtors

• You have no opportunity for an

independent verification of your

calculations

.

Support provided by the 24EasyAudit

provision calculator …?

• With 24EasyAudit you will assess if the

provisions for debtors are reasonable or

your will calculate the provisions.

• With tested auditing techniques underlying

24EasyAudit, you will calculate the bad

debt provision in no time or you will check

if the applied rules are reasonable.

ATTENTION: : With 24easyaudit and in built

modul you can quickly calculate provision for

doubtful accounts- click here to find out more

information about calculation of doubtful

accounts provisions with support of

24EasyAudit.

© 2012 EASYAUDIT Sp. z o.o. with its registered office in Gdynia. All rights reserved. December 2012 https://24easyaudit.com.

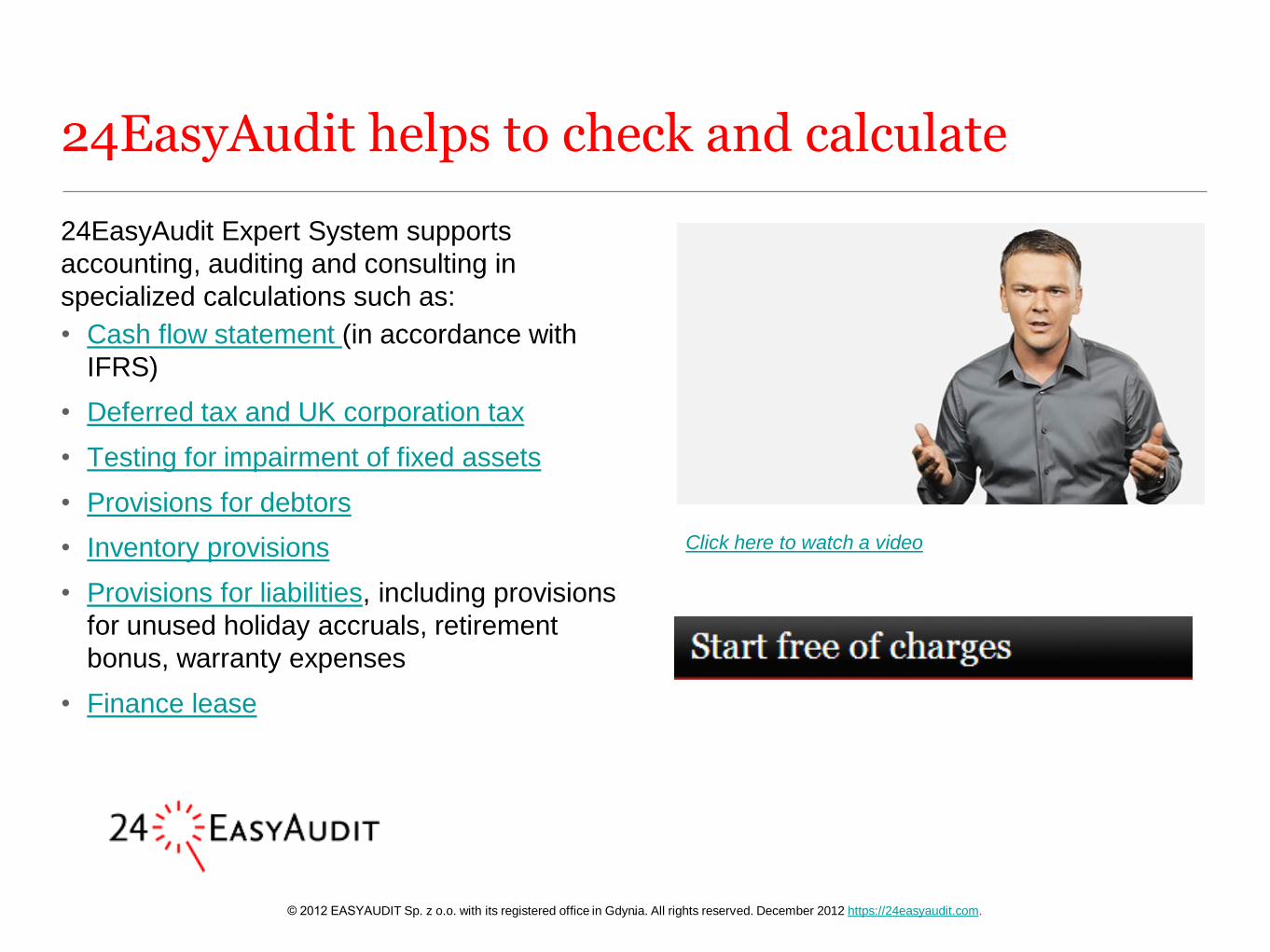

24EasyAudit helps to check and calculate

24EasyAudit Expert System supports

accounting, auditing and consulting in

specialized calculations such as:

• Cash flow statement (in accordance with

IFRS)

• Deferred tax and UK corporation tax

• Testing for impairment of fixed assets

• Provisions for debtors

• Inventory provisions

• Provisions for liabilities, including provisions

for unused holiday accruals, retirement

bonus, warranty expenses

• Finance lease

.

Click here to watch a video

© 2012 EASYAUDIT Sp. z o.o. with its registered office in Gdynia. All rights reserved. December 2012 https://24easyaudit.com.

Intellectual property of 24EasyAudit

• The 24EeasyAudit service, including the graphic and works marks of the Service names

(logo), software of the Service as well as all materials and content provided in the Service,

graphic solution and all other solutions are subject to copyright in accordance with

international law.

• The appearance, operating principles and concept of the Service constitute a protected

industrial design and are subject to protection in compliance with the Act on industrial

property – both for 24EasyAudit and 24 SamAudytuj.

© 2012 EASYAUDIT Sp. z o.o. with its registered office in Gdynia. All rights reserved. December 2012 https://24easyaudit.com.

Contact with 24EasyAudit

Iwona Ekman, President of the Management Board, [email protected], Tel. +48 660

484 064, direct line +48 58 746 30 42

Sławomir Ekman, Proxy, Originator and developer of the 24EasyAudit website, ACCA

Qualified Member, Polish PCA, [email protected], Tel. +48 600 094 919, Direct line

+48 58 746 30 41

Registration data: 24EasyAudit Sp. z o.o., ul. Msciwoja 9 lok. 10a, 81-361 Gdynia, KRS 0000374259, NIP 586-226-29-76, REGON

221152658. 24EasyAudit Spółka z ograniczona odpowiedzialnoscia S.K.A. ul. Msciwoja 9 lok. 10a, 81-361 Gdynia, KRS

0000428240, NIP 586-227-79-89, REGON 221715185 Share capital PLN 50,000, fully paid-up.