financial stability report 2015 - · pdf file7 introduction financial stability report 2015...

TRANSCRIPT

Podgorica, 2016

FINANCIAL STABILITY REPORT 2015

PUBLISHED BY: Central Bank of Montenegro Bulevar Svetog Petra Cetinjskog 6 81000 Podgorica Telephone: +382 20 664 997, 664 269 Fax: +382 20 664 576

WEB SITE: http://www.cbcg.me

CENTRAL BANK COUNCIL: Milojica Dakić, MS, Governor Nikola Fabris, PhD, Vice-Governor Asim Telaćević Milivoje Radović, PhD Milorad Jovović, PhD Srđa Božović, PhD

DESIGNED BY: Andrijana Vujović Nikola Nikolić

TRANSLATED BY: Translation Services Division

PRINTED BY: Studio Branko d.o.o. Podgorica

PRINTED IN: 100 copies

Users of this publication are requested to make reference to the source of information whenever they use data from the Report.

ABBREVIATIONS

ARIMA model Autoregressive integrated moving average modelAED Dirham, currency of the United Arab EmiratesGDP Gross Domestic ProductCBCG Central Bank of MontenegroCDS Credit default swap CHF Swiss Franc DNS Deferred net settlement EBRD European Bank for Reconstruction and Development ECB European Central Bank EIB European Investment BankEMU Economic and Monetary Union EONIA Euro overnight index average EPCG Electric Power Company of Montenegro EU European UnionEUR Euro EURIBOR Euro interbank offered rateFED Federal ReservesFOMC Federal Open Market CommitteeGBP Pound Sterling (H)CPI (Harmonised) Consumer Prices Index JPY Japanese YenKAP Aluminium Plant Podgorica KfW Kreditanstalt für Wiederaufbau LIBOR London interbank offered rate MF Ministry of Finance MFI Micro-credit financial institutions IMF International Monetary Fund MSCI Morgan Stanley Capital International NOK Norwegian Kroner VAT Value added tax PPP Purchasing power parity RESET Regression equation specification error test ROAA Return on Average Assets ROAE Return On Average EquityRTGS Real Time Gross SettlementUSA United States of AmericaFDI Foreign Direct Investments OF MN OGM Official Gazette of Montenegro UK United KingdomUSD United States Dollar VIF Variance inflation factor WIIW Wiener Institut für Internationale Wirtschaftsvergleiche ZZZ Employment Agency

CONTENTS

INTRODUCTION 7

1. INTERNATIONAL ENVIRONMENT 9

1.1. Overview of Macroeconomic Developments 9

2. MACROECONOMIC DEVELOPMENTS IN THE COUNTRY 23

2.1. Economic Activity Developments 232.2. Inflation 302.3. Fiscal Deficit/Surplus 352.4. Public Debt 382.5. Balance of Payments 392.6. Real Estate Market 40

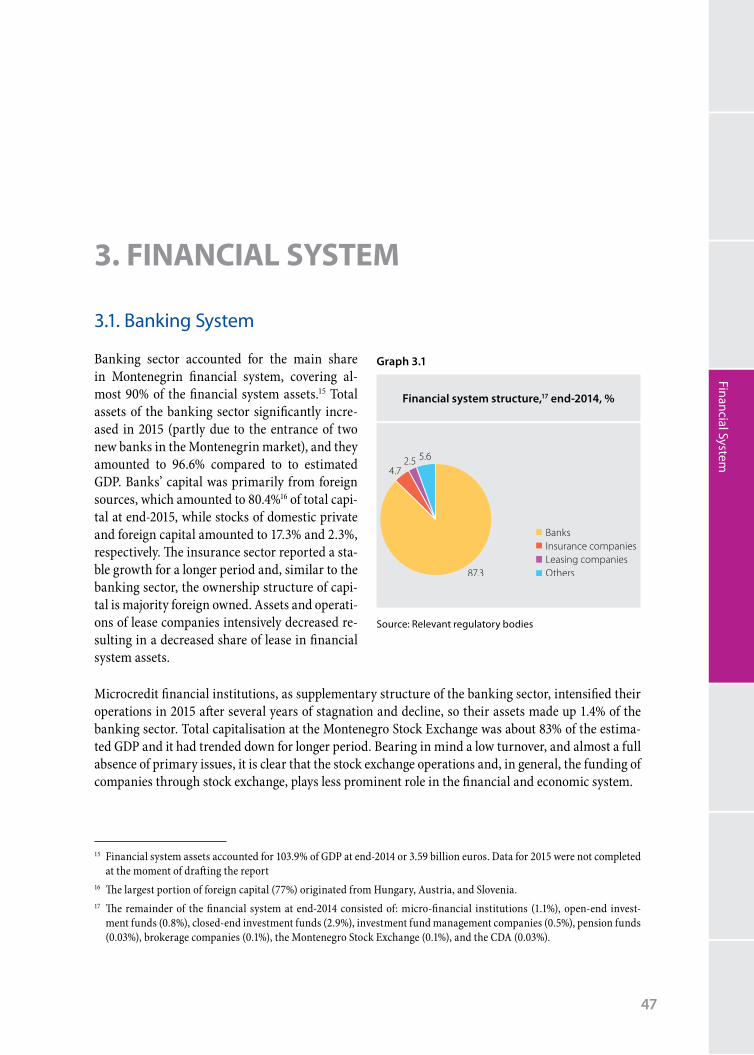

3. FINANCIAL SYSTEM 47

3.1. Banking System 473.1.1. Capital 483.1.2. Banking Sector Profitability 503.1.3. Total Assets and Liabilities Structure 523.1.4. Credit Risk 573.1.5. Liquidity Risk 603.1.6. Market risks 623.1.7. Interest rates 66

3.2. Micro-credit financial institutions 693.3. Capital Market 703.4. Insurance Sector 72

4. FINANCIAL INFRASTRUCTURE 73

4.1. Payment System 734.2. Credit Registry 75

5. CONCLUDING REMARKS 77

5.1. Policies for preservation of financial stability 81

7

Introduction Financial Stability Report 2015

INTRODUCTION

Financial stability is the fundamental prerequisite for economic development. Essentially, financial stability approach means that monetary policy creators analyse and prevent the occurrence of all tho-se events that may pose threat to financial stability via monetary and economic policy measures. This approach generally implies two dimensions of financial stability: micro-dimension that addresses ri-sks from the aspect of individual financial institutions and macro dimension that observes risks from the aspect of the overall financial system. The objective of such a two-dimensional approach is to pro-perly assess systemic risk, i.e. the risk of spilling illiquidity or insolvency problem from an individual institution over to the entire system. The financial stability approach that is also applied by the CBCG may be presented through the following scheme:

Schematic 1 – Framework for maintaining financial stability

Source: Schinasi, G., 2005, „Preserving Financial Stability“

With a view to achieving financial stability, it would be necessary to identify potential risks before they appear and result in a crisis or problems in the financial market functioning. This means implemen-ting preventive and timely well-dimensioned policies. Of course, the objective cannot be to prevent all potential problems in the financial market because it is impossible to manage all risks and uncertain-ties, and there is also no market that has not undergone fluctuations or turbulences. Therefore, efforts should be put on minimizing the biggest risks and ensuring system vitality in case of a crisis. Thus,

8

Central Bank of Montenegro Financial Stability Report 2015

the very objectives of the Financial System Stability Report as well as activities of the CBCG in this area are preventive actions and identification of the most important risks before their materialisation.

9

International Environment

1. INTERNATIONAL ENVIRONMENT

1.1. Overview of Macroeconomic Developments

In 2015, the global economy grew at a rate lower than in 2014. Estimated growth rate amounted to 3.1%,1 which has been revised 0.4 percentage points downwards since 2015. Advanced economies grew at the rate of 1.9%, while the growth rates for the emerging/developing countries was 4.0%.

Table 1.1

Overview of main global indicators, y-o-y, %

Indicator 2014 2015Forecast

Differences from October 2015 projections,

percentage points

2016 2017 2016 2017

GDP growthWorld 3,4 3,1 3,4 3,6 -0,2 -0,2

Advanced economies 1,8 1,9 2,1 2,1 -0,1 -0,1

Emerging and Developing economies 4,6 4,0 4,3 4,7 -0,2 -0,2

USA 2,4 2,5 2,6 2,6 -0,2 -0,2

Euro area 0,9 1,5 1,7 1,7 0,1 0,0

Germany 1,6 1,5 1,7 1,7 0,1 0,2

France 0,2 1,1 1,3 1,5 -0,2 -0,1

Italy -0,4 0,8 1,3 1,2 0,0 0,0

Spain 1,4 3,2 2,7 2,3 0,2 0,1

Japan 0,0 0,6 1,0 0,3 0,0 -0,1

UK 2,9 2,2 2,2 2,2 0,0 0,0

Canada 2,5 1,2 1,7 2,1 0,0 -0,3

Advanced economies outside G7 and euro area 2,8 2,1 2,4 2,8 -0,3 -0,1

Emerging and Developing economies 2,8 3,4 3,1 3,4 0,1 0,0

Russia 0,6 -3,7 -1,0 1,0 -0,4 0,0

China 7,3 6,9 6,3 6,0 0,0 0,0

India 7,3 7,3 7,5 7,5 0,0 0,0

Latin America and the Caribbean 1,3 -0,3 -0,3 1,6 -1,1 -0,7

Middle East, North Africa, Afghanistan, and Pakistan 2,8 2,5 3,6 3,6 -0,3 -0,5

Sub-Saharan Africa 5,0 3,5 4,0 4,7 -0,3 -0,2

Volume of global trade (goods and services) 3,4 2,6 3,4 4,1 -0,7 -0,5

Consumer pricesAdvanced economies 1,4 0,3 1,1 1,7 -0,1 0,0

Emerging and Developing economies 5,1 5,5 5,6 5,9 0,5 1,0

Source: World Economic Outlook (WEO) Update, IMF, January 2016

1 According to the IMF’s World Economic Outlook Report, updated in January 2016

10

Central Bank of Montenegro Financial Stability Report 2015

Lower growth rates primarily resulted from lower growth rates of emerging/developing countries, which weight for the calculation of global growth rate was higher compared to the advanced econo-mies. Contrary to that, although moderate and uneven, economic growth of developing countries was higher than in 2014. The volume of global trade substantially declined year-on-year.

Main risks that marked 2015 will largely influence the global economic activity in 2016 as well, invol-ving a further decline in the prices of energy generated products and commodities, an increase in the FED interest rates, a deceleration and budget review of Chinese economy, and geopolitical risks.

A decline in oil prices was more evident in H2 2015 mostly due to a higher supply as a result of strate-gic policies of main oil producers. Surely, oil and other commodity prices influence inflation outlooks and thus expectations concerning monetary policy developments. Globally speaking, a positive effect should be evident through available profit and corporate revenues instigating private consumption and investments in countries importing energy generated products. On the other hand, such price in the exporting countries usually slows down or delays new investments in energy sector. Currencies of these countries are more or less dependant on oil price developments. In addition, strengthening of the U.S. dollar would increase pressure on the commodities prices.

According to the IMF, low commodities prices could lower growth rate in commodities of exporting countries up to 1% in the period 2015-2017 as compared to 2012-2014, whereby a decline in growth rate of energy generated products of exporting countries could be even up to 2.25%.

The aluminium price declined 21.6% y-o-y and it amounted to USD 1,497.2 per tonne.

2 HIPC for the euro area countries, IPC for the USA

Commodities prices (2005 = 100), 2014-2015

Graph 1.1

Source: IMF

Consumer price indices of selected countries2, %, 2014-2015

Graph 1.2

Source: Eurostat, U.S. Bureau of Labor Statistics

11

International Environment

Develped countries continued recording low inflation rates and deflation in 2015, primarily under the influence of a decline in the prices of energy generated products. The annual inflation rate in H2 2015 increased both in the euro area and the USA although these are inflation rates that are still far away from the medium-term objective of the Eurosystem’s and the FED’s monetary policies. The purchase of government securities in the secondary market, the so-called „quantitative easing“ was introduced in the euro area, and the rate on overnight deposits of banks held with the Eurosystem declined from -0.2% to -0.3% in December 2015.

However, this programme was completed in the USA due to better economic results and inflation projections in the medium-term. The FED passed a decision on increasing the reference interest rate by 0.25 percentage points at end-2015, which was the first increase in this rate since December 2008.

China s economy recorded a further slowdown in 2015, while the estimated growth rate amounted to 6.9% which was the lowest rate in the last 25 years, while the IMF forecasts pointed to further dece-leration in 2016 and 2017. Generally speaking, China s economy grew at the expected rates, whereas exports and particularly imports dropped substantially and indicated weaker investments and in-dustrial output. China’s economic slowdown undoubtedly affected the global growth and its major trading partners (EU, USA and Japan) through trading channels, as well as the commodities prices, thereby affecting the countries whose main sources of revenues are commodities.

The transformation process of the Chinese economy from an export-driven into a consumer-driven economy was partially successful. The consumption was rather high during 2015, as compared to the investments and industrial output. The Chinese authorities had been trying to actively shape econo-mic developments for a long period using numerous stimulation measures that did not always yield desirable results. Enormous FX reserves were used to defend the exchange rate appreciations, which divided the opinions of analysts. A substantial USD debt of the economy could, with the depreciation of the local currency, result in serious repercu-ssions both in the real sector and banks where the level of non-performing loans have been alre-ady posing a concern. In this situation, a further increase in the reference interest rate in the USA poses a high risk (China is not the only emer-ging/developing country exposed to this type of risk). On the other hand, a significant amount of FX reserves was spent to maintain the exchange rate in 2015. In addition, there was a high capital outflow that could continue in 2016.

The euro area and its largest economies repor-ted better results during 2015 when compared to 2014. The growth was based on higher private spending and exports in some countries which was positively affected by low oil prices, a weaker Euro exchange rate, and favourable borrowing possibilities. The European Commission estima-ted a rate of growth of 1.6% for 2015, while the continuance of economic recovery in the euro

GDP growth rates of selected countries, Q/Q-4, %, 2014-2015

Graph 1.3

Source: Eurostat, US Bureau of Economic Analysis

12

Central Bank of Montenegro Financial Stability Report 2015

area is expected in 2016 and 2017, with a mode-rate growth rates of 1.7% and 1.9%, respectively. The U.S. economy continued to grow in 2015 with rather high rates and it managed to maintain momentum from the previous years. Economies of the regional countries with which Montenegro has significant trade reported positive growth ra-tes and the prospects for 2016 and 2017 are rela-tively good.

Box 1.1 - Current positions of some economies compared to the Great Recession

The Great Recession (at the time of occurrence called the Global economic crisis) is a period from the end of the first decade of the 21st century, which was characterised by a fall in economic activity of developed economies and a slowdown of growth in emerging and developing economies. The Great Recession corresponds with the Global financial crisis, i.e. the U.S. subprime mortgage crisis which were essentially the triggers of the Great Recession.

The Great Recession did not start simultaneously nor did it last equally in all countries. The leading global economies, the USA and the UK were hit first, followed by Italy and Japan, which reported nega-tive growth rates already in 2008, but developed countries, as a group, recorded a positive growth rate of 0.2%. The recession deepened in these countries in 2009 and emerged in almost all other developed economies. Growth rates of the emerging and developing economies, although declining, compensat-ed for the negative growth of developed economies, thus the global growth rate in 2009 was slightly above zero which was, however, the worst growth rate in the world after World War II.

The rate of growth of European emerging and developing countries amounted to -3% in 2009, whereas the growth rate of the Montenegrin economy was -5.7%. With regard to this group of countries, only Poland, as well as Albania and Kosovo (two countries with the lowest convergence level compared to developed countries), reported positive growth rates in this year.

In 2015, various countries are on different positions compared to 2008 as the year preceding the 2009 crisis year. The U.S. economy reached in 2011 the GDP level from 2008 (measured by constant prices), while the estimates showed that the euro area reached this level not before in 2015. Montenegro`s economy reached the 2008 real GDP level in 2013.

GDP growth rates of regional countries, Q/Q-4, %, 2014-2015

Graph 1.4

Source: National Statistical Offices

13

International Environment

If the analysis included the number of citizens, i.e. real GDP per capita, the situation would be some-what different and countries that recorded declines in the number of citizens over the same period reported better per capita results and vice versa.

Table 1

GDP change in constant prices, 2015/2008, %

Country GDP GDP per capita

Albania 18.5 25.6

Bosnia and Herzegovina 3.4 4.7

Bulgaria 2.4 8.7

Montenegro 5.3 3.8

France 3.2 -0.1

Greece -27.1 -25.5

Croatia -11.8 -10.2

India 64.9 48.2

Italy -7.2 -10.

Japan 2.3 3.4

China 75.9 69.9

Kosovo 25.9 -

Macedonia 15.3 14.0

Germany 6.1 6.5

Romania 3.0 7.0

Russia 1.8 -0.7

USA 10.4 4.7

Slovenia -4.7 -7.1

Spain -3.1 -4.0

Serbia -1.0 1.6

UK 7.1 1.3

World 25.3 -

Euro area 0.2 -

European Union 2.6 -

Source: IMF, CBCG calculations

In 2015, almost all euro area countries reported a decline in unemployment.3 The unemployment rates declined in four largest economies of the euro area (Germany, France, Italy and Spain), whereby the unemployment rate in Germany (4.5% at end-2015) indicated high competitiveness of the German economy at the global level. On the other hand, Spain had an extremely high rate of 20.8% with a decli-

3 The latest available monthly data were taken for December 2015 unemployment rates for drafting this report.

14

Central Bank of Montenegro Financial Stability Report 2015

ne of 2.8 percentage points annually. Unemployment was still high in Greece (24.6% in November), Croatia (16.6%), Cyprus (15.7%), and Portugal (12.2%).

Unemployment declined in the USA also in 2015 (down to 5%), thus continuing a gradual down-trend from Q4 2009 when it reached 10%. The unemployment rate is one of the main monetary policy indicators of the FED. Although the cu-rrent level of unemployment indicates the dyna-mic economic activity, analysts have certain di-sagreements concerning the adequacy of such in-dicators and potential differences from the actual position of the labour market - fewer new em-ployees in manufacturing industry, a low labour force-to-working age ratio, a high so-called „U6“ unemployment rate4 and the like. The unem-ployment rate also dropped in Japan, by 0.1 per-centage points and it amounted to 3.3% although it should be pointed out that the unemployment rate is not the primary problem of the Japanese economy but rather deflation risk and weak eco-nomic growth (which is, rather atypically, achie-ved together with low unemployment rates).

In 2015, the current account deficit in most euro area countries declined, while surpluses increa-sed. Of the largest euro area countries, only Fran-ce reported a deficit, which was trending down. Greece, which had an enormous current account deficit, substantially improved its position. Such a situation in the euro area resulted from lower commodity prices and higher competitiveness of export products considering weaker Euro.

Positive developments in state finance continued also in 2015 not only with leading economies but also with the periphery countries. Graphs 1.7 and 1.8 below show a summary of state finance de-velopments in the euro area countries. It is clear that the process of fiscal consolidation continued and fiscal deficits are currently substantially lower. In addition, lower deficits bring about lower borrowings, so there is a slowdown of growth and, in certain cases, government debt declines. Howe-

4 A wider concept of the `unemployment rate definition which also covers a group of the so-called marginally attached employees, like those "discouraged" to look for a job, and also part-time employees.

Unemployment rates of selected countries, 2008-2015,%

Current account deficit of the euro area selected countries, % of GDP

(2011-2016; 2016 presented in grey)

Graph 1.5

Graph 1.6

Source: Eurostat, U.S. Bureau of Labor Statistics

Source: European Commission - Winter Forecast 2016 (February 2016)

15

International Environment

ver, even stronger consolidation is required in most countries, since the levels of government debt of some countries are extremely high. On the other hand, growth in public sector debt, which was higher than government debt in many of the euro area countries generally stopped or slightly declined.

Box 1.2 - Public finances and current account balances in economies in the region5

Public finances of the regional countries - Albania, Montenegro, Macedonia, and Serbia as candidate countries, and Croatia and Slovenia as EU member states - are not satisfactory.

All of the mentioned countries recorded fiscal deficits, whereas a declining trend in the following two years is expected. Observed through public debt, perhaps as a better structural indicator of soundness of the public finances, Macedonia is the only country better than Montenegro for which the European Commission estimates the public debt to GDP ratio of 61.4% in 2015, with an uptrend in the following two years. On the other hand, Croatia, Slovenia, and Serbia are already in a „danger zone“ of close to or above 80%. Both EU and euro area have already exceeded the Maastricht Criteria of 60% and they are currently close to or beyond 90%.

Large number of analysts believe that poor situation in the public finances results basically from the external non-competitiveness of European countries, while, in their opinion, recapitalisations/nation-alisations of banks in the crisis period were in a certain way also the result of external non-competi-tiveness. Aggregately, the EU or euro area countries currently have positive current account balances, whereby core countries (Germany, Austria, the Netherlands) are still better compared to the periphery

5 The analysis in this box is given on the basis of the European Commission’s data, which in the case of Montenegro do not correspond completely with the data of the official domestic institutions. As this is probably the case also with the data from other countries, the European Commission’s data are fully kept due to the consistency of the source for all observed countries.

Fiscal deficit of selected countries in the euro area, % of GDP (2011-2016;

2016 presented in grey)

Government debt of the euro area selected countries, % of GDP (2007-2016;

2016 presented in grey)

Graph 1.7 Graph 1.8

Source: European Commission - Winter Forecast 2016 (February 2016)

Source: European Commission - Winter Forecast 2016 (February 2016)

16

Central Bank of Montenegro Financial Stability Report 2015

countries (Greece, Italy, Spain and Portugal). In that respect, the situation in countries in the region, as well as in the entire EU an the euro area is much better than in the pre-crisis period (as the period of extremely high consumption) although their economic growth is smaller relative to the above men-tioned period. With regard to the regional countries, Montenegro has the most obvious current ac-count deficit. As for larger economies, Serbia had the largest deficit, that in Macedonia is slightly above zero, while Croatia and Slovenia in particular, report significant surpluses in their current accounts.

Table 1

Public finances and current account balances in the regional economies, % of GDP

CountryBudget balance Gross public debt Current account balance

2015 2016 2017 2015 2016 2017 2015 2016 2017

Albania -3,5 -2,3 -1,8 72,3 71,6 69,9 -10,9 -11,9 -12,3

Montenegro -7,0 -6,6 -6,1 61,4 65,8 68,9 -12,9 -13,4 -13,9

Croatia -4,2 -3,9 -3,2 86,0 87,0 87,4 4,2 3,1 3,2

Macedonia -3,8 -3,5 -3,1 39,6 40,8 41,6 0,2 0,2 0,1

Slovenia -2,9 -2,4 -1,9 83,5 79,8 79,5 6,9 7,2 6,9

Serbia -3,8 -3,7 -3,5 76,2 79,9 81,8 -5,1 -4,9 -4,9

EU -2,5 -2,1 -1,7 87,2 86,9 85,7 2,1 2,1 2,0

euro area -2,2 -1,9 -1,6 93,5 92,7 91,3 3,7 3,6 3,4

2015 - estimate, 2016-2017 - forecast

Source: European Commission - Winter 2016 European Economic Forecast

Financial Markets and Monetary Policy

Developments in the global economy during 2015 showed still strong influence of the largest central banks, which decisions are important for both national and global markets.

With the aim of achieving targeted inflation in medium-term, the European Central Bank passed a decision at the beginning of December 2015 to cut the interest rate on overnight deposits (deposit fa-cility) by 0.1 percentage points to -0.3%. The main reference interest rate remained the same. It was decided to continue with the quantitative easing programme until 2017, i.e. until the Governing Coun-cil of the ECB deems it necessary. In addition, a decision was passed to expand the spectrum of public sector instruments qualifying for the Public Sector Purchase Programme to include market debt of regional and local governments. On the other hand, at its meeting held in the middle of December 2015, in accordance with market expectations and previous announcements, the Fed s FOMC passed a decision to increase the reference interest rate by 0.25 percentage points to range from 0.25% to 0.5%, which represented the first increase of the reference interest rate since December 2008. Taking into consideration certain „shifts“ in domestic and international markets, the FOMC explained that its decision resulted from the significant progress in the labour market and expectations concerning inflation growth up to a targeted level in the medium-term. The central banks of England and Japan continued to keep their reference interest rates at extremely low levels of 0.5% and 0-0.1%, since March 2009 and December 2008, respectively.

17

International Environment

Reference interbank rates moved pursuant to the monetary policy directions. The EONIA and the EURIBOR were at their record low levels - the EONIA ranged from 0.09% to -0.24%, while the 3M EU-RIBOR ranged between 0.08% and -0.13%.

The six-month USD LIBOR grew over the year, particularly in the last quarter, which resulted in market expectations and finally an increase in the Fed s reference interest rate. The six-month LIBOR ranged from 0.35% to 0.85%.

The connectivity and influence of the Chinese economy on the global economy was particularly evident in the financial markets in 2015. The failure of Chinese SSE composite index, which occurred in the middle of June 2015, has had swift and big reflection in global capital market. The American market, as the market with greater depth and reliability, showed a relatively strong resilience to the initial failure of the Shanghai in-dex. However, at end-August, influenced by seve-ral simultaneous factors (lower commodities pri-ces, low inflation, lower values of most Asian cu-rrencies against the USD, uncertainties regarding the monetary policy in the USA), the U.S. capital market recorded an enormous three-day decline.

Reference interest rates of central banks,%, 2014-2015 Reference market interest rates, %, 2014-2015

MSCI global indices, 2014-2015

Graph 1.9 Graph 1.10

Graph 1.11

Source: Bloomberg Source: Bloomberg

Source: Bloomberg

18

Central Bank of Montenegro Financial Stability Report 2015

Soon afterwards indices recovered but they were still below the average values for the first two qu-arters of 2015, which was particularly evident in the European markets. Volatility also gradu-ally declined until changes in the FED s and the ECB s interest rates. At end-December 2015 and in early 2016, a new large fall of leading indices occurredand the majority of indices came close to their levels back in 2013.

During 2015, Euro depreciated in nominal terms against the leading global currencies, the USD, JPY, GBP, and CHF by 10.2% (from 1.2098 to 1.0857 USD against 1 EUR), 9.9%, 9.5%, and 5.1%, respectively. The variance ratio against above mentioned currencies amounted to 2.6%, 2.5%, 3.3% and 2.5%, respectively. Somewhat higher variance was noted in the Euro exchange rate against Swiss Franc, primarily due to trading af-ter the announcement of the Swiss National Bank that it would no longer ban the strengthening of Swiss Franc against Euro starting from the midd-le of January 2015.

Indicators of volatility/stress at the financial markets, 2014-2015

Graph 1.12

Source: Bloomberg

Euro against other currencies, 2014-2015, 1 January 2014=100 (growth/decline shows

strengthening/weakening of Euro)

Yields on 10-year government bonds, %, 2014-2015

Graph 1.13 Graph 1.14

Source: Bloomberg, CBCG calculations Source: Bloomberg

19

International Environment

Yields on 10-year bonds of majority of the euro area countries dropped during 2015. The U.S. 10-year government bonds yield amounted to 2.2% at end-2015, which represented an attractive risk premium to investors on equivalent German and Swiss bonds that yielded 0.27% and -0.06% at end of the year, respectively. This could influence further strengthening of the U.S. dollar or weakening of the Euro. The price of gold amounted to 1,061.1 U.S. dollar per fine ounce at end-2015.

Box 1.3 – The ECB`s monetary policy and Euro interest rates

The European Central Bank maintained the policy of record low interest rates in 2015, whereby the main refinancing operations rate remained at 0.05% throughout the year, while the rate on overnight deposits of banks held with the Eurosystem dropped in December from -0.2% to -0.3%. This directly reflected on market interest rates, thus the EONIA and the 3-month EURIBOR were at their record low levels; the EONIA stood at 0.14% at the beginning of the year and -0.13% at the end of the year, while the EURIBOR was 0.08% at the beginning and -0.13% at the end of the year. Thus the ECB influenced a decline in Euro interest rates on deposits held with banks in the European market, while interest rates on deposits of individual banks were formed depending on the maturity of individual types of deposits and credit ratings of banks.

In addition to the interest rates policy, and af-ter further weak outlooks for the price levels and economic activity in the euro area, the ECB started with the quantitative easing pro-gramme in 2015, i.e. the purchase of govern-ment securities in the secondary market. This programme started on 21 March as an upgrade of another two asset purchase programmes, the Third Covered Bond Purchase Programme and Asset-Backed Securities Purchase Pro-gramme that started in October and November 2014, respectively. Asset purchase will last at least until March 2017 and maybe even longer, depending on the economic situation. Monthly purchase was about 60 billion euros, and asset purchase through these programmes amount-ed to about 650 billion euros at end-2015. This mostly resulted in an increase in total assets of Eurosystem from 2.2 trillion euros to 2.8 trillion euros during 2015.

The ECB intended to cut further the level of lending interest rates through quantitative eas-ing and boost investments and private sector spending through better financing conditions, simultaneously cutting deposit interest rates, which generally discourages savings. The ECB evaluated that the programme currently meets the expecta-tions. However, one gets the impression that such quantitative easing policy, together with the current policy of low reference interest rates, additionally distorts market of Euro interest rates on government securities, i.e. it unnaturally cuts the level of interest rates in nominal terms. For instance, interest rates

Source: Bloomberg

Graph 1ECB reference interest rates in the market and yields on bonds of selected countries, %, and Eurosystem’s assets, in EUR billion, 2006-2015

20

Central Bank of Montenegro Financial Stability Report 2015

on three-month debt of majority euro area countries were negative at end-2015, including periphery countries, except Greece. Interest rates on two-year debt of Italy, Spain and Portugal were around zero, while they were negative on German and French debts. Finally, interest rates on the ten-year debt of Germany, France, Italy, Spain and Portugal were only -0.3%, 1%, 1.6%, 1.8% and 2.5%, respectively, which was extremely low, taking into consideration the public debt levels of majority of these coun-tries and overall economic situation and expectations. Simultaneously, compared to the debt crisis in the euro area, a significant convergence between interest rates is currently evident, without major differences between core and periphery countries.

Expectations for 2016 and potential effects of international environment on Montenegro

The IMF forecasted growth of the global economy at higher rates in the period 2016 – 2017, whereby these growth forecasts have been already declined. The global economy growth forecast amounted to 3.4% for 2016 and also for the volume of global trade.

Advanced economies will grow at a rate of 2.1%. in 2016. As for the largest euro area economies, only the forecast for Spain is lower compared 2015. Emerging/developing economies will grow at a rate of 4.3%, according to the IMF forecast, which 0.3 percentage points more compared to 2015. With regard to the BRIC countries, the Chinese economy will slow down, while the Russian economy will experience a substantially smaller decline and it should have a positive growth rate in 2017. As for European emerging and developing economies, the IMF forecasted growth of this region of 3.1% (0.3 percentage points lower than in 2015), which represents a relatively modest growth rate. Forecasts for economies in Montenegro’s immediate environment, which should achieve relatively good results in the following two years, are encouraging.

The most important impact of international environment on Montenegro is capital flows, whether these are foreign direct investment or other forms of foreign investments - portfolio and other inves-tments, since the growth of Montenegrin economy is still primarily caused by the inflow of foreign investments. Based on this criteria, the most important economic partners are Russia and EU/euro area. To that end, still relatively weak growth of the EU/euro area countries (in relation to, for exam-ple, USA), and instabilities in Russia (the IMF expects a decline in economic activity of 3.7% in 2015) pose relative threat. In particular, geopolitical tensions and situation in Ukraine should be mentioned here as well. However, there were no negative developments in 2015 in this area, and net FDI inflow increased 75% y-o-y. FDIs from Russia declined by 43.8% after a decline of 10% in 2014 compared to 2013, and Russia ranked third in 2015 among investor countries in Montenegro. However, the largest amount of investments in real estates came from Russia in 2015, closely to 54 million euros. As for portfolio investments, 500 million euros was gathered based on the issue of Government Eurobonds in 2015 (with the lowest interest rate in relation to all previous issues of Eurobonds), and a net inflow of foreign portfolio investments was 32.8% higher than in 2014.

Ukraine crisis did not have much effect on tourist overnights and arrivals, since arrivals of both Russi-an and Ukraine tourists declined y-o-y (-6.3% and -10.6%, respectively), while overnights of Russian tourists increased and that of Ukraine tourists slightly declined (6.3% and -0.3%, respectively). With

21

International Environment

regard to the number of tourists from Serbia, an extraordinary growth of both arrivals (29.7%) and overnights (39%) was reported over the one-year period partially due to the low base effect.

As for the exchange rates, the most important for Montenegrin economy are the Euro-U.S. dollar and partially (specifically) the Euro-Swiss Franc exchange rates. A stronger Euro against the U.S. dollar enables a decline in fuel prices while, on the other hand, it brings lower revenues to aluminium indu-stry. With regard to the banks’ balance sheets, the U.S. dollar is the most represented second foreign currency compared to Euro both on the assets and liabilities and the capital side, amounting to some 155 million euros at end-2015. However, the positions are well balanced and funds in U.S. dollars were mostly placed at deposit accounts abroad, thus no danger should be present in this area for Montene-grin banks. In addition, the effect of the EUR-USD exchange rate was a relatively important factor for the Government debt and guarantees to the extent in which the hedging against exchange rate was not contracted. The share of debt in other foreign currencies (including SDR and not excluding the SDR portion in euros) in total Government debt was 12% at end-September 2015, of which the largest porti-on referred to USD, and there was a significant portion of dollar loans guaranteed by the Government (almost 90 million euros at end-September 2015). Weakening of Euro compared to U.S. dollar in this context would have a negative effect on public finances. Finally, with regard to the EUR-CHF currency pair, one bank had exposure in CHF in the amount of about 21 million euros at end-2015, mostly in lo-ans to citizens - residents. Although this bank hedged against foreign exchange rate risk by balancing the position on the liabilities and capital side, it could not avoid credit risk and it had/has significant problems in collecting these loans. Any weakening of EUR against CHF exerts a pressure on debtors, i.e. bank’s exposures and the situation particularly worsened when the Swiss National Bank announ-ced abandoning the ceiling of already strong Franc in mid-January 2015. The situation in Montenegro changed somehow with the adoption of the Law on the Conversion of Swiss Franc (CHF)-denomina-ted loans into Euro (EUR)-denominated loans at end-July 2015 aimed at protecting the debtors of this bank. The Law envisages the conversion of debt into EUR the day when the loan agreement was made and a new calculation of loans by applying a flat interest rate of 8.2%. (Simultaneously, the imple-mentation of the Law will not lead to a decline in the solvency ratio of this bank below the regulatory minimum).6

With regard to the Greek crisis, it is difficult to say at this moment what the situation will be and what would be the effects of potential new negative developments. Concerning direct impacts on Montene-gro, they should not be significant, since there are no Greek banks in Montenegro’s market, our banks are not connected with Greek banks and they are not exposed to other Greek entities, the import in Greece is small as is FDI inflow from Greece. However, potential indirect effects are possible throu-gh the crisis effect on overall situation in the euro area/EU, i.e. in global financial markets. There is a potential increase in return on government debt of the euro area periphery countries, which could result in expensive borrowing of Montenegro in the following period. Generally speaking, risk premi-um could increase with regard to any type of foreign investments to Montenegro. Also, certain Euro depreciation against U.S. dollar is possible (and other global currencies), which could not seriously jeopardise the Montenegrin economy since EUR is the most represented currency in all important segments of the economy both in its flows and conditions. Finally, certain transfer of foreign tourists from Greece to Montenegro is likely to happen, if deepening of the crisis would result in social unrest in Greece and other difficulties (fuel and/or food and other groceries shortages, lack of cash in banks, worsening of the refugees situation, and the like) that would be substantially strong so that tourists

6 OGM 46/2015

22

Central Bank of Montenegro Financial Stability Report 2015

perceive Greece as an unstable country. Currently, negative indirect effects of the Greek crisis practi-cally are not felt by the Montenegrin economy.

It is very important to mention the ECB monetary policy, which additionally cut its interest rates to historically minimum levels. The ECB Governing Council decided, at its meeting held at the beginning of December 2015, to additionally lower interest rate on overnight deposits of banks held with the Eu-rosystem from -0.2% to -0.3%, while the interest rate on overnight loans of the Eurosystem to banks and the interest rate on main refinancing operations remained at 0.3% and 0.05%, respectively. Also, this has been an ongoing trend of lowering the ECB interest rates, which started at the end of 2008.

This represents the possibility for Montenegro and also a danger for further accumulation of certain risks. With regard to foreign borrowings of banks (from parent/related or other banks), it had a decli-ning trend in the previous years. Although borrowings were stable in 2015, relatively speaking, it sli-ghtly declined in 2015 as well, making up only 7.5% of total banks’ liabilities and capital at the end of the year. This ongoing decline was a result of several factors: 1) deleveraging strategy, i.e. a decline in exposure of parent banks to its subsidiaries due to problems faced by parent banks in parent markets, 2) stabilisation and growth in deposit base of domestic banks and the related change in the approach of domestic banks to finance more through domestic deposits and less through foreign borrowings, and 3) the losing of momentum in the Montenegrin economy and the related loss of attractive inves-tment possibilities for domestic banks, together with a decline in demand for loans with certain enti-ties. Moreover, as for the banks’ borrowings, risks are currently under control.

On the other hand, government foreign borrowing remains a concern. It increased in the post-crisis period as a result of several factors, thus external debt at end-September 2015 amounted to 54.9% of GDP. With regard to the structure, Eurobonds accounted for the main share, based on which debt increased by 966.6 million euros (26.9% of GDP), which is almost half of the amount of external debt, while the remaining portion of the external debt referred to bilateral credit arrangements. In addition, the increase in debt based on Eurobonds resulted in growth in total government external debt. Higher borrowing was possible since foreign central banks (primarily the ECB but also the FED) maintained expansive monetary policy and created a substantial amount of additional liquidity which the banks did not want to transfer to the private sector, and on the other hand, Montenegro s indebtedness at the beginning of this period was relatively low. However, currently, indebtedness has grown increasingly while fiscal deficits in the post-crisis period remain a structural problem since the economy has solid growth, and certain fiscal deficits are still being recorded. On the other hand, it is unreasonable to expect that the euro interest rates would soon return to normal levels, which is attractive for indebted-ness.

Positive side of extremely low Euro interest rates reflected in the possibility of refinancing of the exi-sting debt (Eurobonds and the remaining portion of external debt) at low interest rates, which would influence the decline of interest expenditures in future, thereby indirectly influencing the space for decline in the balance (principal) of debt. However, new borrowings which would not be used just for refinancing, but which would additionally increase the balance (principal) of debt, would represent a dangerous accumulation of risks and extreme vulnerability in the situation when euro interest rates start returning to their normal levels.

23

Macroeconom

ic Developm

ents in the Country

2. MACROECONOMIC DEVELOPMENTS IN THE COUNTRY

2.1. Economic Activity Developments

Economic growth in Montenegro showed stronger signs of recovery in 2015 compared to the previous period. Almost all indicators measuring economic activity in the country recorded relatively strong annual growths, thereby contributing to a positive rate of total real growth of 3.2%7. Manufacturing industry, tourism, and construction sectors affected positively such estimated growth rate. The decline in output reported in the electricity, gas and steam supply sector of 5.9% and that in the mining and quarrying sector of 8.1% had a negative impact.

Table 2.1

Selected industries’ trend, 2015/2014, %

Retail trade, turnover (constant prices) 2,2

Tourism

Number of arrivals 12,9

Number of overnights 15,7

Manufacturing industry, physical volume 19,9

Construction

Value of completed works 5,8

Effective working hours 4,7

Electricity, gas and steam supply -5,9

Mining and quarrying, physical volume -8,1

Forestry, physical volume (index weighted) 17,6

Source: Monstat

Monstat s final data showed real growth in Montenegro’s GDP of 1.8% in 2014, while the preliminary data for Q1, Q2, Q3 and Q4 2015 showed real growth of 3%, 3.7%, 4.2%, and 1.4%, respectively.

7 Monstat preliminary data.

24

Central Bank of Montenegro Financial Stability Report 2015

Labour market developments did not have a consistent trend. The reporting year was characterised by growth both in the number of employed (1.2%) and registered unemployed persons (3.9%). A sli-ght increase in gross and net wages and salaries was recorded in 2015 of 0.27% and 0.6% respectively, which was still not sufficient for stronger recovery of aggregate demand. However, simultaneously reduced pressure of labour factors contributed to the preservation of the corporate sector s competi-tiveness.

The unemployment rate was still very high. According to the Employment Agency data, the unem-ployment rate in December amounted to 17.24% and it increased 2.29 percentage point y-o-y. Accor-ding to the Monstat s Labour Force Survey, the unemployment rate amounted to 17.6% in 2015.

As compared to the neighbouring countries which also faced high unemployment, Montenegro has a medium score, which certainly does not diminish the need to undertake activities to reduce unem-ployment rate and resolve structural problems in the economy.

Table 2.2

Basic labour market indicators (annual average)

2014 2015 Change (2015/2014), %

Employed 173,595 175,617 1.2

Unemployed 33,284 34,587 3.9

Wages, gross, EUR 723 725 0.27

Wages, net, EUR 477 480 0.6

Sources: Monstat, Employment Agency

Table 2.3

Unemployment in the regional countries, Labour Force Survey, %

Country Unemployment rates, 2015

Slovenia 9,0

Croatia 16,6

Serbia 17,0

Montenegro 17,6

Macedonia 27,0

Bosnia and Herzegovina 27,7

Source: WIIW, March 2016; for Montenegro - Monstat

Reduced liquidity and insufficient recovery of the real sector were still present in 2015. The enforced collection indicators pointed to the problem of the corporate sector liquidity. As at 31.12.2015, 14,870 debtors had their accounts frozen, which was the y-o-y increase of 5%. As for the value of these acco-unts, the total amount of debt based on which the accounts were frozen amounted to 548,021,273.62 euros, which was a y-o-y increase of 10.5%. On the other hand, the share of persons whose accounts were frozen declined and stood at 19.3%, i.e. 2.5 percentage points less than at end-2014.

25

Macroeconom

ic Developm

ents in the Country

It is worth mentioning that debt concentration was relatively high at the year-end. Thus, 10 largest debtors or 0.07% of total number of recorded debtors accounted for 12.25% in the total amount of fro-zen funds, which means that the amount of their frozen funds was 67,159,234.05 euros.

Fifty largest debtors comprising 0.34% of total recorded debtors accounted for 35.36% in total amount of frozen funds, which means that the amount of their frozen funds was 193,804,256.39 euros.

Table 2.4

Basic statistics of enforced collection, end of the period

2014 2015 Change, %

Number of persons with frozen accounts 14,160 14,870 5.0

As % of total number of persons 21.8 19.3 (percentage points) -2.5

entities with uninterruptedly frozen accounts up to one year, EUR 58,394,100.19 38,756,790.53 -33.6

entities with uninterruptedly frozen accounts over one year, EUR 437,717,022.82 509,264,483.09 16.3

Total, EUR 496,111,123.01 548,021,273.62 10.5

Source: CBCG

Forecast of GDP trends in 2016 and impact on financial stability

Real growth in 2016 will depend on a number of factors influencing the intensity and level of recovery. The most important variables that are expected to affect a high inflow of foreign capital are the conti-nuance of work on a large number of initiated investment projects in tourism, energy sector and public sector (highway construction) and the dynamic for realisation of the announced investment projects in 2016. Capital inflow was the main driver of the economy in the last several years. The level of FDI inflows in developing countries and Montenegro will depend on the situation in the international market and the willingness of foreign investors to invest (to lend money).

The highway construction has a dual impact on the situation of economic activity and the level of ri-sks in Montenegro. This capital and one-off investment will affect growth of economic activity whilst affecting an increase in the public debt and pressures in the fiscal sector. When implementing such important infrastructure projects, it is very important that the development component enables public debt sustainability.

When it comes to the contribution of the banking sector to GDP growth, it should be borne in mind still present problems of high interest rates and a relatively high level of non-performing loans alt-hough both indicators trended down during 2015. Banks are still cautious when granting new loans. However, an increasing trend in new loans indicated the improvement of the situation and change in banks’ expectations regarding the situation in the economy from the position of new risk taking. Further decline in non-performing loans is expected as is a gradual decline in interest rates which would positively affect a further decline in new loans and a sound financing of the real recovery. The entrance of new banks in the market and higher competition should encourage such trends.

26

Central Bank of Montenegro Financial Stability Report 2015

According to the foreign institutions’ forecasts shown in Table 2.5, the growth rate is expected of 3.75% (the rate is obtained as a simple average of forecasts of GDP growth by international institutions from the same Table).

Table 2.5

Forecasts of international institutions on Montenegro’s GDP trending in 2016 (in %)

Institution Estimated growth rate for 2016

IMF 4.7*

EBRD 4.0

UN Department for Economic and Social Affairs 3.3

European Commission 4.0

Vienna Institute 2.8

World Bank 3.7

* IMF, World Economic Outlook Database April 2016 Source: Web sites of individual institutions

Box 2.1 - GDP per capita and actual individual spending according to the purchasing power parity

Noticeable differences in GDP per capita and actual individual spending at purchasing power parity (PPP) have been present among the EU member states and EU candidate countries.

GDP per capita at PPP is an indicator that eliminates differences in prices between peer countries and it is more realistic indicator of differences regarding the degree of economic development compared to GDP per capita in terms of current prices. Ac-cording to Eurostat and peer coun-tries, the value of index for Montene-gro is 41. This means that the living standard in Montenegro is more than half the EU average. However, the liv-ing standard in Montenegro is only 14 points below the average of the former Yugoslav countries and only Slovenia and Croatia are in front of Montenegro as EU member states.

Table 1

GDP per capita at PPP, EU 28 = 100, 2014

Country Index

Albania 30

Bosnia and Herzegovina 29

Bulgaria 47

Montenegro 41

France 107

Greece 73

Croatia 59

Italy 96

Macedonia 37

Germany 124

Romania 55

Slovenia 83

Spain 91

Serbia 37

UK 109

EX YU 48

USA 148

Japan 100

Source: Eurostat, CBCG calculations

27

Macroeconom

ic Developm

ents in the Country

The IMF data, which were calculated compared to the U.S. economy as the benchmark economy, showed that the position of all major economies was worse than that of the USA in terms of GDP per capita at PPP. Meas-ured by this indicator, even besides strong convergence that occurred in the last several years and decades, the living standard in China and India is currently four and nine times lower than in the USA, respectively. German economy is closest to the USA, and German GDP per capita at PPP was 16 points lower than the American. Based on the same data, the living standard in Montenegro was three and a half times lower than in the USA or some-what below the average standard of the former Yugoslav countries.

However, it is considered that the ac-tual individual consumption is even better indicator of the living standard of households than GDP per capita. Actual individual consumption indi-cates actual consumption of goods and services by households, including situations when such a consumption is funded by the state or non-profit or-ganisations, which varies by the coun-try, particularly in the case of health services or education services. The Eurostat data (EU 28 = 100) showed 52 points for Montenegro, which is much better compared to to the GDP per capita. Simultaneously, Montenegro is at the average level of the former Yu-goslav countries, based on the actual individual consumption.

Table 2

GDP per capita at PPP, USA = 100, 2015 (estimate)

Country Index

Albania 21

Bosnia and Herzegovina 18

Bulgaria 33

Montenegro 28France 74

Greece 46

Croatia 38

India 11

Italy 64

Japan 68

China 25

Macedonia 25

Germany 84

Romania 37

Russia 42

Slovenia 55

Spain 63

Serbia 24

UK 73

EX YU 31

Source: IMF, CBCG calculations

Table 3

Actual individual consumption per capita at PPP, EU 28 = 100, 2014

Country Index

Albania 37

Bosnia and Herzegovina 38

Bulgaria 51

Montenegro 52France 112

Greece 83

Croatia 60

Italy 98

Macedonia 40

Germany 123

Romania 57

Slovenia 75

Spain 88

Serbia 47

UK 115

EX YU 52

Source: Eurostat, CBCG calculations

28

Central Bank of Montenegro Financial Stability Report 2015

Table 2.6

Montenegro: Selected economic indicators, 2010-2016 (Forecasts with assumption of current economic policies also applying in the future period)

Real economy 2011 2012 2013 20142015 2016

estimate forecast

Nominal GDP (in million euros) 3.265 3.181 3.362 3.458 3.641 3.840

Gross national savings (as percentage of GDP) 1,8 2,1 5,1 4,6 14,6 10,0

Gross investments (as percentage of GDP) 19,3 20,6 19,6 19,8 28,0 28,6

Change in percentages

Real GDP 3,2 -2,7 3,5 1,8 4,1 4,6

Industrial output -10,3 -7,1 10,6 -11,5 13,7 ...

Tourism

Arrivals 8,7 4,8 3,7 1,7 12,7 ...

Overnights 10,2 4,3 2,8 1,5 15,6 ...

CPI (annual average) 3,1 3,6 2,2 -0,7 1,6 0,9

CPI (period end) 2,8 5,1 0,3 -0,3 1,4 1,4

GDP deflator 1,2 0,2 2,1 1,0 1,2 0,8

Average net salary (12 month average)1 1,0 0,7 -1,7 -0,5 0,4 ...

Cash and loans (period end, change in %)

Loans to private sector2 -13,0 -3,1 2,1 -0,4 2,3 2,7

Corporates -20,3 -4,9 0,4 -2,8 2,2 ...

Households -3,2 -1,1 3,7 1,7 2,7 ...

Private sector deposits 1,2 7,2 1,3 6,1 9,0 ...

General Government finances, based on accrual accounting3 as percentage of GDP

Revenues and grants 38,5 39,9 41,3 43,5 40,6 42,2

Expenditures 45,3 45,7 47,6 46,1 48,0 51,4

Deficit/surplus -6,7 -5,8 -6,3 -2,6 -7,4 -9,2

Primary deficit/surplus -5,3 -4,0 -4,2 -0,3 -4,9 -6,8

Domestic financing (net) 2,5 -0,6 1,4 -0,6 -1,8 1,8

Privatisation proceeds 0,2 0,2 0,8 0,3 0,3 0,1

Gross General Government debt 45,6 53,4 55,2 59,9 66,5 70,5

General Government debt and issued guarantees 57,2 65,4 64,2 69,0 80,8 84,1

Balance of payments

Current account balance -17,6 -18,5 -14,5 -15,2 -13,3 -18,6

Foreign direct investments 11,9 14,5 9,6 10,2 15,7 12,0

External debt (stock at end of period) 145,0 155,9 151,5 154,8 152,1 154,8

Of which: private sector4 112,4 115,2 111,3 109,6 94,8 93,3

Real effective exchange rate (based on CPI; average % change)

(minus refers to depreciations) -3, 2 3,2 0,8 -2,0 ... ...

Additionally:

Nominal GDP growth (in percentages) 4,5 -2,6 5,7 2,8 5,3 5,5

Deficit/surplus without highway construction project (as percentage of GDP) -6,7 -5,8 -6,3 -2,6 -2,9 -1,2

Aluminium price (in euro per tonne) 1.822 1.542 1.348 1.514 1.549 1.391

1 Including a change in the MONSTAT methodology, starting from 1 January 2010;2 Changes in classification of off-balance sheet items created a break in structure in 2012; annual change in credit growth

in 2013 cannot be compared due to the change in methodology;3 Data includes state funds and municipalities, but not the state owned companies;4 Assessments, because private debt statistics is not published;

Source: Taken from the IMF Mission Report within the consultations pursuant to Article IV of the IMF Articles of Agreement, March 2016 (Original source: MF, CBCG, Monstat, Employment Agency, IMF’s forecasts and assessments)

29

Macroeconom

ic Developm

ents in the Country

Table 2.7

Montenegro: Selected economic indicators, 2014-2017

Indicator 20142015 2016 2017

Forecasts

Real GDP growth 1,8 3,9 4,0 4,1

Unemployment rate (as % of total labour force) 18,2 17,6 17,2 16,8

Consumer prices index, % -0,5 1,5 1,9 2,2

Current account deficit (% of GDP) -15,2 -12,9 -13,4 -13,9

Fiscal deficit (% of GDP) -2,8 -7,0 -6,6 -6,1

Public debt (% of GDP) 54,8 61,4 65,8 68,9

Source: European Commission - Winter Forecast 2015 (February 2016)

Table 2.8

Real growth of GDP, EBRD projections, %

Country/Region 2014Projection, November 2015 Projection, May 2015

2015 2016 2016 Change May - Nov

Central Europe and Baltic Countries

Croatia -0,4 0,9 0,5 0,5 0,0

Estonia 2,9 2,0 2,8 3,0 -0,2

Hungary 3,7 2,9 2,1 2,3 -0,2

Latvia 2,4 2,3 3,1 3,1 0,0

Lithuania 3,0 1,7 3,0 3,2 -0,2

Poland 3,3 3,4 3,3 3,4 -0,1

Slovakia 2,5 3,1 3,2 3,3 -0,1

Slovenia 3,0 2,3 2,0 2,3 -0,3

Average 3,1 3,0 2,9 3,0 -0,1

South-eastern Europe

Albania 2,2 2,3 3,3 3,0 0,3

Bosnia and Herzegovina 1,0 2,8 3,0 3,0 0,0

Bulgaria 1,5 1,8 2,0 1,5 0,5

Cyprus -2,5 1,0 1,7 1,5 0,2

Macedonia 3,5 3,5 3,5 3,7 -0,2

Greece 0,7 -1,5 -2,4 2,0 -4,4

Kosovo 0,9 2,0 3,0 3,5 -0,5

Montenegro 1,8 3,0 4,0 3,7 0,3

Romania 2,8 3,5 3,7 3,2 0,5

Serbia -1,8 0,5 1,8 1,8 0,0

Average 1,4 1,6 1,6 2,5 -0,5

30

Central Bank of Montenegro Financial Stability Report 2015

According to the model-based CBCG projections in 2016, GDP growth will range from 3.8% to 4.2%, with the central projection of about 4%. For testing the central projection of GDP, a GDP estimate using the expenditure method was also done. Starting assumptions for the calculation using the ex-penditure method include:

• Growth of the household spending of 2.7% due to an increase in wages and salaries and certain new employment, caused by the strengthening of investment activity, increase in pensions, and increase in lending activity of banks, mild decline in lending interest rates due to larger market pressures;

• Government spending growth up to 2.5% as a result of the announced increase in wages and salaries in the public sector and pensions;

• Growth in investments in fixed assets of 15.5% as a result of capital investments in the con-struction of the Smokovac-Mateševo highway section and foreign direct investments in the area of tourism (Portonovi, Luštica, bay of Pržno near Tivat and Mamula) and energy (con-struction of submarine cable between Italy and Montenegro and wind power plant at Možura);

• Export of goods and services will grow at a rate of 1%, as a consequence of projected lower con-sumption by foreign tourists compared to the record 2015, and also weak external demand for goods, particularly for metals;

• Imports will show growth of 3.5% because of investors’ need to import equipment, constructi-on material, and labour force, especially for the highway construction, and the substitution of the import of food by domestic production will have a negative effect on imports growth.

According to the expenditure method, GDP will grow at a rate of 4% in 2016, which indicates the vali-dity of the central projection of the GDP growth.

Simple average of the real GDP growth estimates by international institutions shows that the Monte-negrin GDP growth in 2016 should be at the level of 3.75% (Table 2.5).

2.2. Inflation

Monthly inflation rate in December 2015 amou-nted to -0.3%, while the consumer prices increa-sed by 1.4% y-o-y. The average annual CPI inflati-on amounted to 1.5% which was higher than the average annual inflation in EU (0.0%).

The largest inflation drivers in 2015 was growth in the prices under food and non-alcoholic beve-rages (2.4%), housing, water, electricity, gas and other fuels (1.6%), clothing and footwear (5.0%), health care (1.6%), alcoholic beverages and to-bacco (3.3%) and hotels and restaurants(3.4%) ca-tegories.

Consumer prices, annual growth rate (%) 2014-2015

Graph 2.1

Source: Monstat

31

Macroeconom

ic Developm

ents in the Country

Table 2.9

Share of trends of individual categories of products in total inflation

Weight Growth rate XII 15/XII 14

Share, percentage points

TOTAL 1.000 1.4 1.4

Food and non-alcoholic beverages 386.4 2.4 0.93

Alcoholic beverages and tobacco 37.9 3.3 0.13

Clothing and footwear 70.7 5.0 0.35

Housing, water, electricity gas and other fuels, 153.1 1.6 0.24

Furnishing, household equipment and routine household maintenance 46.9 1.1 0.05

Health care 38.2 1.6 0.06

Transport 101.0 -4.6 -0.46

Communications 57.1 0.1 0.01

Recreation and culture 27.2 0.5 0.01

Education 15.7 0.0 0.0

Hotels and restaurants 23.0 3.4 0.08

Other products and services 42.8 0.5 0.02

Source: Monstat and CBCG calculations

According to the harmonised consumer prices index (HCPI) (methodological standard in the EU/euro area, which differs somewhat from the consumer prices index (CPI)), the annual inflation rate in Mon-tenegro amounted to 1.7% in December 2015. The average annual growth rate according to the HCPI amounted to 1.4%.8

Table 2.10

CPI (HCPI) of the selected countries, %8

XII 12/XII 11 XII 13/XII 12 XII 14/XII 13 III 15/III 14 VI 15/VI 14 IX 15/IX 14 XII 15/XII 14

Albania 2.4 1.9 0.7 2.2 1.4 2.2 2.0

BiH 1.8 -1.2 -0.4 -0.2 -0.5 -1.8 -1.3

Montenegro 5.1 0.3 -0.3 1.6 1.9 1.7 1.4

EMU 2.2 0.8 -0.2 -0.1 0.2 -0.1 0.2

EU 2.3 1.0 -0.1 -0.1 0.1 -0.1 0.2

Croatia 4.4 0.5 -0.1 0.0 0.1 -0.5 -0.3

Macedonia 4.7 1.4 -0.5 -0.3 0.5 -0.2 -0.3

Slovenia 3.1 0.9 -0.1 -0.4 -0.9 -1.0 -0.6

Source: Statistical offices of the selected countries, Eurostat

8 CPI for non-EU countries (Albania, Bosnia and Herzegovina, Montenegro and Macedonia), i.e. HCPI for the EU member states.

32

Central Bank of Montenegro Financial Stability Report 2015

In addition to the quantitative easing measures and maintaining stimulative monetary policy, the inflation in euro area and the EU remained low and at 0.2%. With a view to achieving targe-ted level of inflation below but close to 2%, quan-titative easing measures are still carried out.

Weights of 38.6% for CPI and 31.7% for HCPI make the food the most important category/factor in the total inflation in Montenegro. In the euro area, in accordance with the average household spending and its spending for food and non-alcoholic beve-rages, the same weight amounted to 15.6%, which indicated to substantially lower effect of global changes in food prices on general inflation relative to to the situation in Montenegro.

The IMF estimates show a further decline in the prices of oil and other energy generated products also in 2016.

Based on the last projections for the IMF Mission Report within the consultations pursuant to Article IV of the IMF Articles of Agreement, the IMF estimated that the inflation rates in Montenegro would be positive in the following medium-term period. Annual inflation in the period 2016-2020 will amo-unt to 1.4%, 1.4%, 1.6%, 1.7%, and 1.8%, respectively.

General inflation trend and trend of food commodities inflation in Montenegro and the

euro area; HIPC, %, annual rate, 2014-2015

Graph 2.2

Source: Monstat, Eurostat

CPI projections of Montenegro for 2016

Graph 2.3

Source: CBCG, 2016

33

Macroeconom

ic Developm

ents in the Country

Inflation fan chart of Montenegro, based on the ARIMA model assessment for 2016, shows 90% proba-bility of inflation measured by the consumer prices index, depending on the month, which will range in the interval from 0.7% to 2.8%, whereas the projected inflation for end-2016 will vary from 1.9% to 2.8%. Namely, as the time span for forecasting increases, uncertainty increases, as does the forecast span. The central projection of the fan chart (which refers to the darkest part of growth) shows the probability span of 10%. The central projection of the model shows that an average inflation in 2016 will be 1.6%.

Starting assumptions for the inflation forecast for 2016 include:

1. Growth in investments and more intensive economic activity in 2016;2. A 5% increase of electricity price (planned increase of prices in August 2016 included);3. Real wages and salaries will increase in 2016 as compared to 2015;4. Real estate prices stagnation5. Mild decline in oil and natural gas prices;6. Unfavourable weather in the country and the region could result in a more pronounced

growth in the food commodities prices.

Any deviation in some of the said assumptions would require correction of the forecast.

Box 2.2 - Prices and consumption disparities

Significant price disparities exist among the EU member states and candidate countries. Generally, in accordance with the economic development level and nominal wages and salaries, prices are higher in developed countries relative to less developed countries. Observed by groups of products, the con-vergence is higher with tradable commodities and lower with less tradable commodities and services. According to the Eurostat statistics, goods and services in Montenegro are half the prices compared to the EU average; to be more precise, 45% of the EU average prices, which is, generally observed, at the level of the average of the former Yugoslav countries (except Kosovo). According to the group of products, clothing in Montenegro is only 7% cheaper, equipment for personal transport by 14%, and household appliances by 18%, while electronic devices and footwear were more expensive than in the EU, by 1% and 7%, respectively.

34

Central Bank of Montenegro Financial Stability Report 2015

Table 1

Prices of individual groups of products by countries, EU 28 = 100, 2014

Group of products AL BiH BU MN FR GR CRO IT HU GER RUS SL ES SRB UK EX YU

Food and non-alcoholic beverages 69 76 70 76 110 103 92 110 59 104 68 96 93 70 104 78

Alcoholic beverages and tobacco 50 47 57 58 106 91 71 96 37 93 70 81 87 50 166 57

Clothing 66 85 80 93 102 89 86 104 76 101 86 94 85 92 103 88

Footwear 74 81 73 107 104 93 83 108 80 105 96 87 91 92 95 88

Electricity, gas and other fuels 60 47 51 54 94 100 67 119 48 121 55 88 111 42 96 58

Furniture and furnishings 53 58 51 66 95 101 76 113 61 94 69 79 103 65 118 68

Household appliances 82 67 67 82 106 89 90 103 62 99 77 94 99 79 113 79

Electronic devices 112 98 95 101 100 100 106 97 89 96 108 103 95 93 109 98

Personal transport equipment 79 83 82 86 102 91 87 98 85 97 85 87 102 83 103 85

Transport services 34 69 48 53 106 76 78 71 40 118 47 95 81 56 134 65

Communications 52 80 69 72 97 139 72 118 61 103 56 90 107 54 125 72

Restaurants and hotels 42 57 44 60 109 81 76 109 42 98 52 85 88 50 114 62

Total 48 52 48 55 108 85 66 103 47 101 53 82 92 50 121 59

Source: Eurostat, CBCG calculations

Disparities are very pronounced in specific groups of products and services in total households con-sumption. In general, households in developed countries spend more on furniture and services (in percentage terms) and less on food, as opposed to less developed countries. As for the EU countries compared to the candidate countries (except Turkey), households spend more from their budgets on housing, water and electricity (24.4% compared to 18.9%), transport (13% compared to 9.6%), recrea-tion and culture (8.6% compared to 6.4%) and in particular on restaurants and hotels (8.2% compared to only 2.9%). On the other hand, households in the candidate countries spend on food and non-al-coholic beverages 32.9% of their budgets as compared to the EU where they spend only 12.3%. Com-pared to the candidate countries’ average, households in Montenegro, spend more on clothing and footwear (8.3% compared to 5% of the budget), and less on recreation and culture or housing, water and electricity (3.6% compared to 6.4% or 14.5% compared to 18.9% of the budget, respectively).

35

Macroeconom

ic Developm

ents in the Country

Table 2

Households’ consumption by countries and groups of products, %, 2014

Group of products AL BU MN FR GR IT HU GER RUS SL ES SRB UK EU (28)

EU candidate

Food and non-alcoholic beverages 39.0 18.7 34.2 13.4 16.8 14.2 32.8 10.2 29.7 15.0 13.0 25.7 8.6 12.3 32.9

Alcoholic beverages and tobacco 3.1 6.7 3.8 3.5 4.9 4.2 5.6 3.3 5.4 5.6 4.0 6.9 4.0 4.0 4.9

Clothing and footwear 4.1 3.1 8.3 4.2 3.4 6.1 4.3 4.9 3.4 5.2 4.4 3.3 5.7 5.0 5.0

Housing, water, electricity 13.0 18.8 14.5 26.7 21.1 24.4 25.8 24.3 21.4 18.6 23.8 22.1 24.3 24.4 18.9

Furniture, furnishings and household maintenance 6.1 6.4 4.0 5.3 3.3 6.1 3.0 6.7 4.4 5.3 4.1 3.8 4.7 5.4 4.2

Health 4.9 4.9 3.9 4.3 4.1 3.3 1.5 5.4 6.0 4.0 4.2 4.2 1.8 3.9 3.6

Transport 5.4 15.4 11.5 13.0 13.6 12.0 8.9 14.2 11.3 16.2 11.5 12.6 14.1 13.0 9.6

Communications 1.9 5.6 4.9 2.6 3.5 2.3 3.9 2.7 4.2 3.3 2.6 4.6 2.0 2.5 3.8

Recreation and culture 12.8 7.0 3.6 8.2 4.9 6.6 3.0 9.5 6.1 8.6 6.8 6.2 10.0 8.6 6.4

Education 2.9 0.9 2.8 0.9 2.3 1.0 1.4 0.8 2.1 1.3 1.8 1.3 1.8 1.2 2.1

Restaurants and hotels 2.8 7.0 3.0 6.5 14.5 9.7 3.4 5.3 2.1 7.0 14.5 2.2 9.6 8.2 2.9

Other goods and services 4.1 5.6 5.5 11.5 7.6 10.0 6.4 12.8 4.0 9.9 9.3 7.1 13.3 11.5 5.8

Albania, France, Macedonia - 2013, Romania - 2012

Source: Eurostat, CBCG calculations

2.3. Fiscal Deficit/Surplus

Fiscal consolidation remained the priority of Montenegro s fiscal policy in 2015. However, budget pro-jections were not met in the volume and according to the dynamics as it was planned. Thus, a down-trend in negative balance of the budget continued also in 2015. Montenegrin budget recorded a level of deficit higher than that planned, primarily due to the repayment of obligations from the previous period and capital expenditure in the current budget.

Table 2.11

Fiscal deficit/surplus trend - latest data

Description/ Period 2011 2012 2013 2014 Assessment2015

Projection2016

Source revenues, in million euros 1.133,2 1.126,1 1.243,4 1.353,6 1.326,7 1.458,5

Expenditures, in million euros 1.318,8 1.333,9 1.459,2 1.460,7 1.618,0 1.732,4

Deficit/surplus, in million euros -185,7 -207,8 -215,8 -107,1 -291,3 -273,9

Deficit/surplus, as % of share in GDP -5,6 -6,5 -6,4 -3,1 -8,1 -7,2

Source: 2011-2014 – laws on budget execution, 2015-2016 - MF (GDDS tables)

36

Central Bank of Montenegro Financial Stability Report 2015

Source revenues of the budget amounted to 1.33 billion euros or 36.9% of the estimated GDP9. The-se revenues declined by 0.2% compared to the plan. The decline in revenues resulted from the lower collection of taxes than planned mostly due to lower collection of VAT revenues (-23.1 million euros or 4.8%), corporate income tax (-4.5% million euros or 9.6%) and personal income tax (-3.2 million euros or 2.9%). Source revenues declined by 2% compared to 2014.

The most important year-on-year increase in revenues was recorded in the collection of excise duties that amounted to 170 million euros, which represented a growth of 8.7% or 13.5 million euros. Incre-ase in these revenues resulted from the increase in excise duties on tobacco pursuant to the „excise calendar“, which was in the function of harmonisation of domestic regulation with the EU regulations.

The Ministry of Finance estimated that total budget proceeds (source revenues and additional fun-ding) in 2015 amounted to 2.17 billion euros or 60.3% of the estimated GDP.

Table 2.12

Budget revenues in 2015 and comparison with 2014

Type of revenueOutturn Plan

Difference relative to the plan

2014Difference relative

to 2014

mil. € mil. € mil. € % mil. € mil. € %

BUDGET REVENUES 1,326.7 1,329.2 -2.5 -0.2 1.353.7 -27.0 -2.0

Taxes 805.5 832.7 -27.1 -3.3 833.2 -27.7 -3.3

Personal income tax 104.8 107.9 -3.1 -2.9 104.4 0.4 0.3

corporate income tax 42.2 46.6 -4.4 -9.4 45.0 -2.9 -6.4

Tax on immovable property transactions 1.5 1.6 -0.1 -6.3 1.5 0.0 0.5

Value added tax 457.1 480.2 -23.1 -4.8 497.6 -40.5 -8.1

excise duties 170.0 167.7 2.3 1.4 156.5 13.5 8.7

Tax on international trade and transactions 22.9 22.9 0.0 0.0 22.3 0.6 2.8

Other taxes of the Republic 7.1 5.7 1.4 24.6 6.0 1.2 19.2

Contributions 437.3 417.5 19.8 4.7 444.3 -7.0 -1.6

Contributions for pension and disability insurance 264.1 246.4 17.7 7.2 270.1 -6.0 -2.2

Contributions for health insurance 150.3 145.5 4.8 3.3 151.0 -0.7 -0.5

Contributions for unemployment insurance 12.1 12.7 -0.6 -4.7 12.2 -0.1 -0.4

Other contributions 10.8 12.9 -2.1 -16.3 11.0 -0.2 -2.0

Duties 13.2 16.9 -3.7 -21.9 15.0 -1.9 -12.5

Fees 29.6 13.5 16.1 119.3 17.3 12.3 70.9

Other revenues 26.6 37.0 -10.4 -28.1 29.7 -3.1 -10.6

Proceeds from loan repayments and funds carried forward from the previous year

7.9 5.1 2.8 54.9 8.5 -0.6 -6.9

Donations 6.6 6.6 0.0 0.0 5.6 1.0 18.8

ADDITIONAL FINANCING

Borrowings and loans from domestic sources 175,2 0,0 175,2 ... 244,9 -69,69 -28,5

Borrowings and loans from foreign sources 657,5 634,1 23,5 3,7 290,8 366,73 -91,9

Proceeds from sale of property 7,8 0,0 7,8 ... 6,7 1,15 17,2

Increase/decrease in deposits -7,6 0,0 -7,6 -0,2 -5,4 -2,28 42,6

Source: Ministry of Finance

9 Estimated GDP for 2015 amounted to 3.6 billion euros.

37

Macroeconom

ic Developm

ents in the Country

Budget expenditures of the budget amounted to 1.62 billion euros or 45% of the estimated GDP. The exenditures recorded an increase of 10.8% compared to 2014. If compared to the plan, expenditures increased by 3.4% (by 53 million euros) where the difference was mainly a result of growth recorded in the repayment of liabilities from the previous years, capital expenditures, expenditures for services, and transfers to institutions, individuals, non-governmental and public sectors.

Table 2.13

Budget expenditures in 2015 and comparison with 2014

Type of expendituresOutturn Plan

Difference relative to the

plan2014 Difference

relative to 2014

mil. € mil. € mil. € % mil. € mil. € %

BUDGET EXPENDITURES 1.618,0 1.565,0 53.0 3.4 1.460,8 157.2 10.8

CURRENT EXPENDITURES 1,390.0 1,280.3 109.7 8.6 1.393.1 -3.1 -0.2

Current budget expenditures 669.7 631.8 37.8 6.0 635.0 34.6 5.5

Gross salaries and contributions charged to the employer

382.2 379.4 2.8 0.7 387.3 -5.2 -1.3

Other personal earnings 14.7 11.6 3.1 26.9 12.0 2.8 23.3

Expenditures for material 25.6 29.4 -3.8 -13 28.6 -3.0 -10.4

Expenditures for services 58.5 41.5 16.9 40.8 54.1 4.4 8.1

Expenditures for current maintenance 20.1 20.8 -0.7 -3.3 21.3 -1.2 -5.4

Interests 81.8 75.8 6.0 8.0 75.5 6.3 8.3

Lease 7.9 8.3 -0.4 -4.9 8.0 -0.1 -1.4

Subsidies 19.6 21.3 -1.6 -7.7 18.4 1.2 6.5

Other expenditures 30.7 29.9 0.9 2.8 29.8 0.9 3.2

Capital expenditures in current budget 28.5 13.8 14.6 105.7 66.2 -37.8 -57.0

Transfers for social welfare 487.0 504.9 -17.8 -3.5 492.2 -5.1 -1.0

Social welfare related benefits 60.8 60.5 0.3 0.5 61.9 -1.0 -1.7

Funds for technological redundancies 16.7 19.4 -2.8 -14.3 22.6 -5.9 -26.3

Pension and disability insurance related benefits 387.0 402.5 -15.4 -3.8 384.4 2.7 0.7

Other healthcare related benefits 14.5 15.0 -0.6 -3.7 15.2 -0.8 -5.0

Other health insurance related benefits 8.1 7.4 0.6 8.6 8.1 0.0 -0.3

Transfer to institutions, individuals, non-governmental and public sector

136.2 128.3 7.9 6.2 99.0 37.2 37.5

Transfer to institutions, individuals, non-governmental and public sector

135.8 127.9 7.9 6.2 96.9 38.9 40.2

Other transfers 0.5 0.4 0.0 6.4 2.2 -1.7 -79.2

CAPITAL BUDGET 228.0 284.7 -56.7 -19.9 67.7 160.3 236.7

Borrowings and loans 3.0 2.3 0.7 32.3 2.5 0.5 19.8

Reserves 16.6 13.1 3.6 27.5 13.5 3.1 23.0

Repayment of guarantees 0.0 0.0 0.0 ... 15.3 -15.3 -100.0

Repayment of liabilities from the previous years 77.4 0.0 77.4 ... 65.2 12.2 18.7

Net increase in liabilities 0.0 0.0 0.0 ... 4.1 -4.1 -100.0

DEBT REPAYMENT 541.7 398.3 143.5 36.0 434.1 107.7 -67.0

Repayment of securities and loans to residents 221.7 46.7 175.0 374.7 239.0 -17.3 -26.8

Repayment of securities and loans to non-residents 320.0 317.8 2.3 0.7 195.1 125.0 -98.8

Repayment of liabilities from the previous years 0.0 33.8 0.0 ...

Source: Ministry of Finance

38

Central Bank of Montenegro Financial Stability Report 2015

According to the Ministry of Finance estimates, the Budget of Montenegro generated deficit of 291.3 million euros or 8.1% of GDP in 2015, which is 184.1 million euros more than in 2014. This was the se-venth consecutive year of the budget deficit, which indicates still present pressure of this vulnerability on fiscal and overall financial stability of the system. Additionally, debt repayment amounted to 541.7 million euros (the amount that is not included in the deficit).

The implementation of the biggest infrastructure project in Montenegro - the construction of the part of the „Bar - Boljare“ highway, section „Smokovac - Mateševo“ started in 2015, which is funded from the capital budget and the funds were provided from the credit arrangement signed with the Exim Bank.

With regard to the public finances consolidation at the local level, the Government approved resche-duling of tax debt based on taxes and contributions for employees wages and salaries in the amount of 89.07 million euros.