fifteenth annual report(english)

TRANSCRIPT

4 Introduction

6 Chairman’s Message

8 Board of Directors

9 Board of Director’s Report for 15th AGM

22 ACEO’s Message

24 Management Team

27 Product Review

30 CSR Activities & SME Financing

33 Auditor’s Report

35 Schedules

76 Significant Accounting Policies

79 Notes to Account

93 Disclosure as per Basel II

97 ATM Locations

98 Branches

CONTENTS

| Kumari Bank | Annual Report 2015-20164

4

INTRODUCTION

Kumari Bank Limited, came into existence as the fifteenth commercial bank of Nepal by starting its banking operations from Chaitra 21, 2057 B.S (April 03, 2001) with an objective of providing competitive and modern banking services in the Nepalese financial market. The bank has paid up capital of NPR 2,699,166,532 of which 51% is contributed from pro-moters and remaining from public.

Kumari Bank Ltd has been providing wide - range of modern banking services through 38 points of representations located in various urban and semi urban part of the country, 36 branches outside and inside the valley; and 2 extension counters. The bank is pioneer in providing some of the latest / lucrative banking services like E-Banking and SMS Banking services in Nepal. The bank always focus on building sound technology driven internal system to cater the changing needs of the customers that enhance high comfort and value. The adoption of modern Globus Software, developed by Temenos NV, Switzerland and arrangement of centralized data base system enables customer to make highly secured transactions in any branch regardless of having account with

particular branch. Similarly the bank has been providing 365 days banking facilities, extended banking hours till 7 PM in the evening, Utility Bill Payment Services, Inward and Outward Remittance services, Online remit Services and various other banking services.

Visa Electron Debit Card, which is accessible in entire VISA linked ATMs (including 46 own ATMs) and POS (Point of Sale) terminals both in Nepal and India, has also added convenience to the customers. The bank has been able to get recogni-tion as an innovative and fast growing institution striving to enhance customer value and satisfaction by backing transparent business practice, professional management, corporate governance and total quality management as the organizational mission.

The key focus of the bank is always center on serving unful-filled needs of all classes of customers located in various parts of the country by offering modern and competitive banking products and services in their door step. The bank always prioritizes the priorities of the valued customer.

Kumari Teller Counter at Durbarmarg Branch

Kumari Bank | Annual Report 2015-2016 | 5

MISSIONOur mission is to deliver innovative products and services to our customers, use these inno-vative products to achieve financial inclusion, and do so by exemplifying good corporate gov-ernance, proactive risk management practices, and superior corporate social responsibility.

VISIONOur vision is to be the preferred financial partner to our customers, a center of career growth to our employees, and to maximize our sharehold-ers’ value, while contributing to our nation’s financial sector and to its economic welfare.

| Kumari Bank | Annual Report 2015-20166

6

Kumari Bank | Annual Report 2015-2016 | 7

CHAIRMAN’S MESSAGE

Dear Shareholders,

It gives me immense pleasure to place before you the highlights of your Bank’s performance during the financial year 2014-15. Details of the achievements and initiatives taken by your Bank are provided in the enclosed Annual Report for the year 2014-15.

I take this opportunity to impart you that the bank has announced 11% bonus share and 0.58% cash dividend for tax purpose, as proposed by the Board of Directors.

In the review period, the Bank has achieved growth in deposits and loans by 21.19% and 18.69% respectively to NPR 33.42 billion and NPR 27.07 billion respectively as compared to the previous fiscal year. In this period, bank’s net profit has increased by 15.55%. With past experiences, teamwork and taking up right strategies by the management, the Bank shall strive to perform better in the days to come.

In the current fiscal year, the Bank has targeted to increase its loan and investment to NPR 32 billion and NPR 5.78 billion respectively. Likewise, the deposit amount is targeted at NPR 38.50 billion. In the fiscal year 2015-16, the bank has a target of achieving operating profit of NPR 895.60 million and net profit of NPR 550 million. The operating expense in the running fiscal year is expected to be NPR 643.50 million. Currently, the Bank has 25 branches outside valley and 11 branches inside valley, altogether 36 branches, 2 extension counters and 46 ATMs. By the end of FY 2071/72, paid up capital of the bank has reached NPR 2.69 billion (including bonus share).

During the review period, the bank provided continuity on product innovation and automation

of services by operating Kumari Swastha Jeevan Bachat Khata, Kumari Remit Bachat Khata and Personal Loans and advances. Moving forward, we anticipate your continued support and patronage to encourage us to accomplish in order to become one of the leading financial service providers in the country.

The 14th Annual General Meeting of the Bank has proposed its plan for merger with Banks and Financial Institutions in order to raise the paid up capital to NPR 8 billion in line with the Central Bank requirement. Consequently, banks including Nepal Credit and Commerce Bank Ltd., Infrastructure Development Bank Ltd., Apex Development Bank Ltd., Supreme Development Bank Ltd. and International Development Bank Ltd. signed an MOU for merger on Poush 29, 2072 and Letter of Interest has already been obtained from NRB. Charter Accountant Firm P.Y.C. and Associates have been appointed for the Due Diligence Audit to decide on the swap ratio.

Finally, I wish to thank the bank’s management and staff members for considering the bank’s progress to be their own by providing dedicated services. I would like to express my gratitude and deep appreciation to Nepal Rastra Bank, Office of Company Registrar, Nepal Securities Board, Nepal Stock Exchange Ltd., shareholders, customers, partners-in-progress and all our well-wishers for their continued support, encouragement and guidance in making possible for us to complete yet another successful year.

With best wishes!Santosh Kumar Lama

Chairman

| Kumari Bank | Annual Report 2015-20168

8

BOARD OFDIRECTORS

Kumari Bank | Annual Report 2015-2016 | 9

BOARD OF DIRECTORS’ REPORTFOR FIFTEENTH ANNUAL GENERAL MEETING

Respected Shareholders,

On behalf of the Board of Directors, we would like to extend warm welcome to all the shareholders to the fifteenth Annual General Meeting of Kumari Bank Ltd.

We would like to express our heartfelt condolences to the departed souls due to the massive earthquake on April 26, 2015. Let us stand together, and pray to give courage to all those bereaved family members who have lost their loved ones. Also, we pray for the speedy recovery of those who have been injured due to this natural disaster.

We are delighted to present you this bank’s financial status of the fiscal year 2071/72, its achievement and future prospects in this fifteenth Annual General Meeting. Learning lessons

from our past experiences and facing utmost challenges in the banking sector, we have completed glorious 15 years of services. From its inception, this bank has been achieving continuous progress through modern banking technology and practices with its core objectives to provide excellent customer services, maximum return to our investors, maintain good corporate governance and moral values; and adhere to the rules and regulations set forth by the government. In days to come, with techno-savvy service delivery we shall continuously put our effort for the optimum quality of banking solutions. We take your suggestions as our course of action so that the bank can be more successful and sustained. We take your permission to present you with the achievements attained in the fiscal year 2071/72.

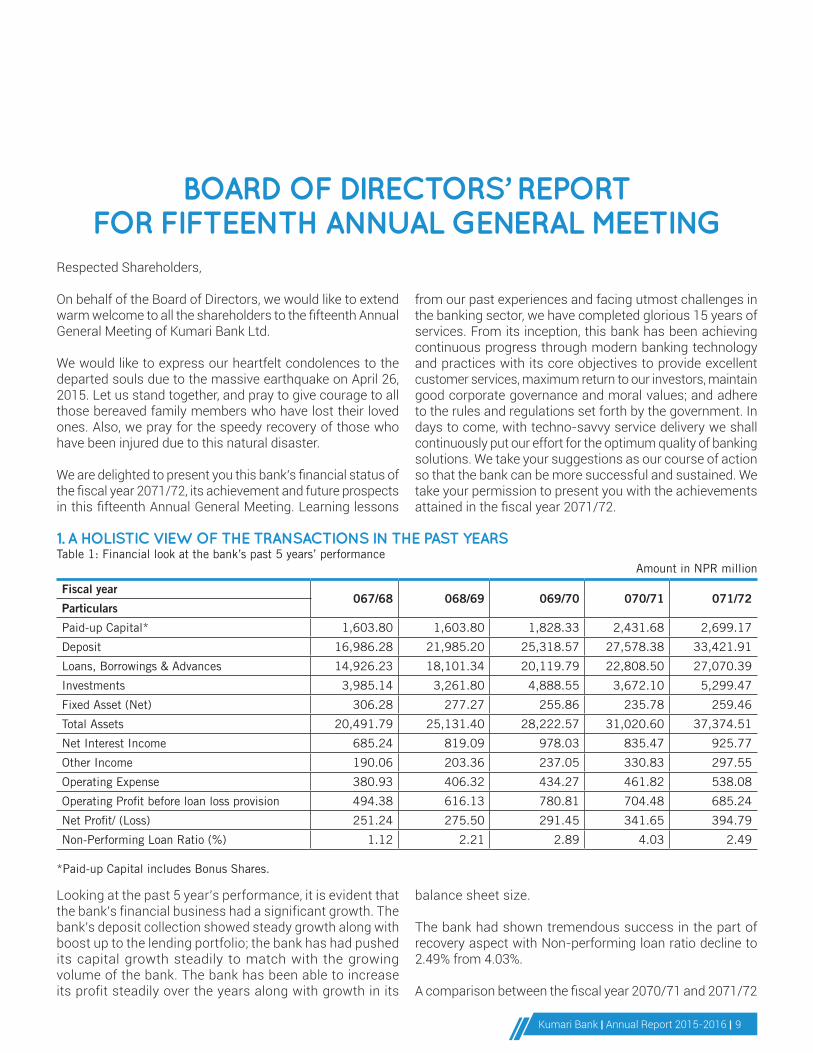

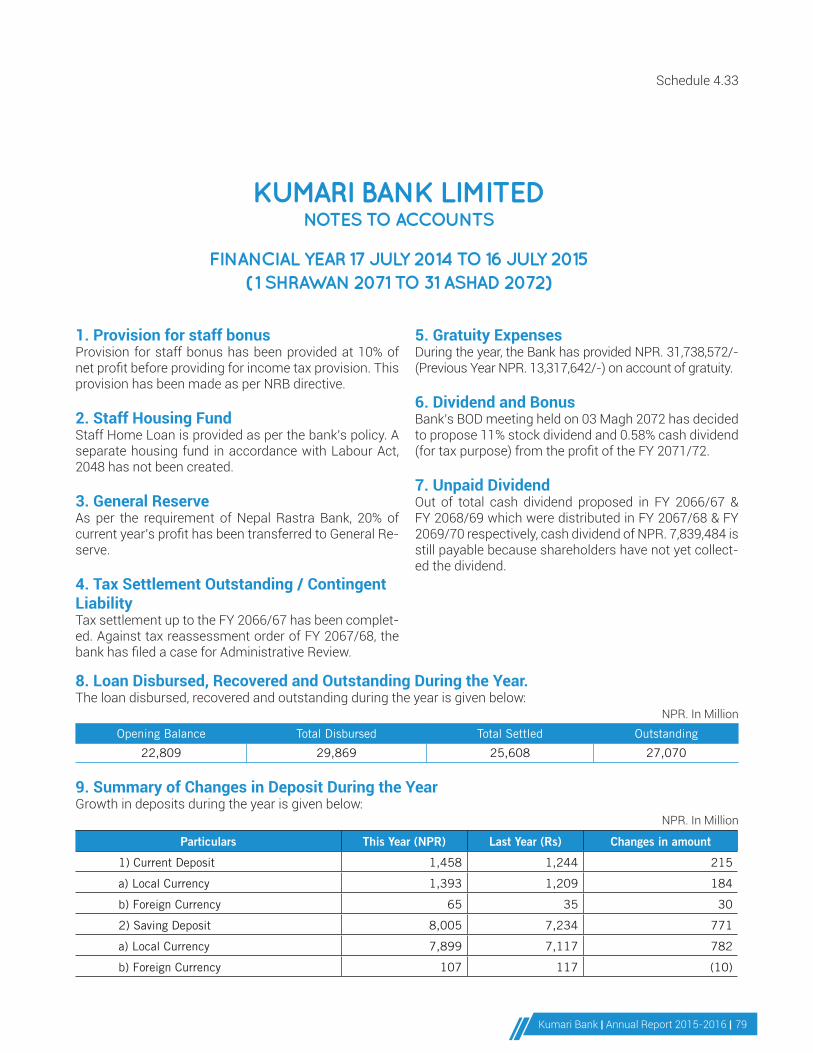

1. A HOLISTIC VIEW OF THE TRANSACTIONS IN THE PAST YEARSTable 1: Financial look at the bank’s past 5 years’ performance Amount in NPR million

Fiscal year 067/68 068/69 069/70 070/71 071/72

Particulars

Paid-up Capital* 1,603.80 1,603.80 1,828.33 2,431.68 2,699.17

Deposit 16,986.28 21,985.20 25,318.57 27,578.38 33,421.91

Loans, Borrowings & Advances 14,926.23 18,101.34 20,119.79 22,808.50 27,070.39

Investments 3,985.14 3,261.80 4,888.55 3,672.10 5,299.47

Fixed Asset (Net) 306.28 277.27 255.86 235.78 259.46

Total Assets 20,491.79 25,131.40 28,222.57 31,020.60 37,374.51

Net Interest Income 685.24 819.09 978.03 835.47 925.77

Other Income 190.06 203.36 237.05 330.83 297.55

Operating Expense 380.93 406.32 434.27 461.82 538.08

Operating Profit before loan loss provision 494.38 616.13 780.81 704.48 685.24

Net Profit/ (Loss) 251.24 275.50 291.45 341.65 394.79

Non-Performing Loan Ratio (%) 1.12 2.21 2.89 4.03 2.49

*Paid-up Capital includes Bonus Shares.

Looking at the past 5 year’s performance, it is evident that the bank’s financial business had a significant growth. The bank’s deposit collection showed steady growth along with boost up to the lending portfolio; the bank has had pushed its capital growth steadily to match with the growing volume of the bank. The bank has been able to increase its profit steadily over the years along with growth in its

balance sheet size.

The bank had shown tremendous success in the part of recovery aspect with Non-performing loan ratio decline to 2.49% from 4.03%.

A comparison between the fiscal year 2070/71 and 2071/72

| Kumari Bank | Annual Report 2015-201610

10

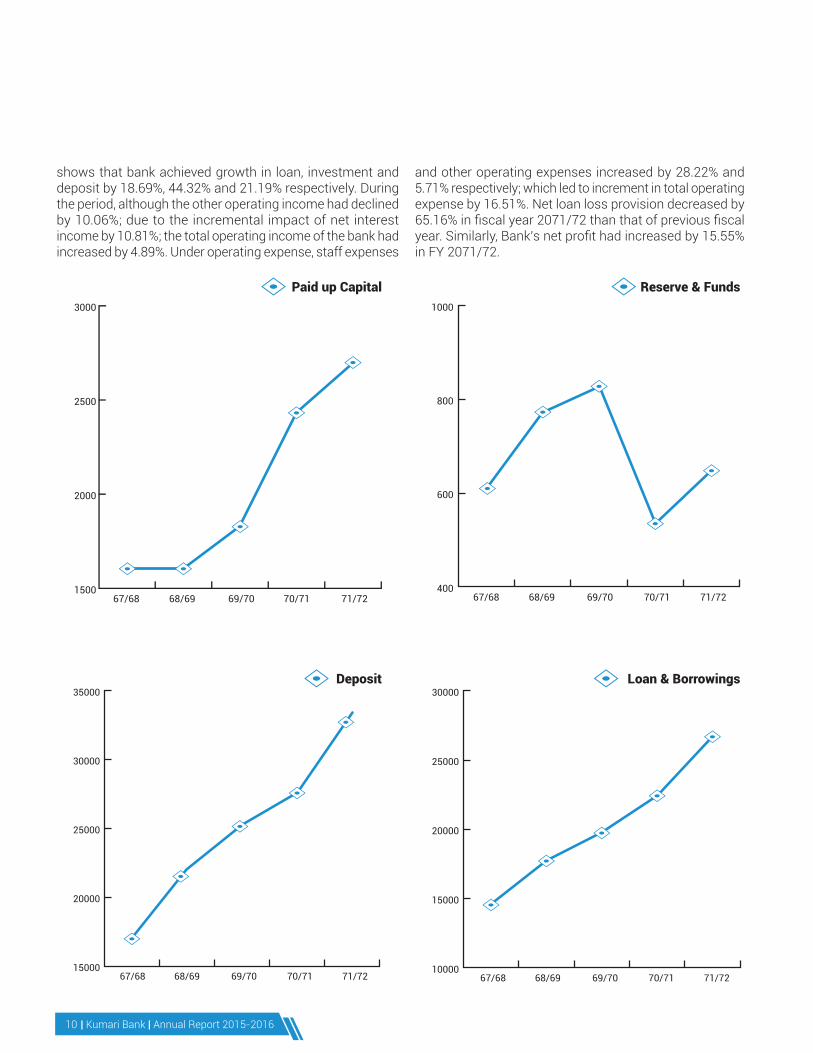

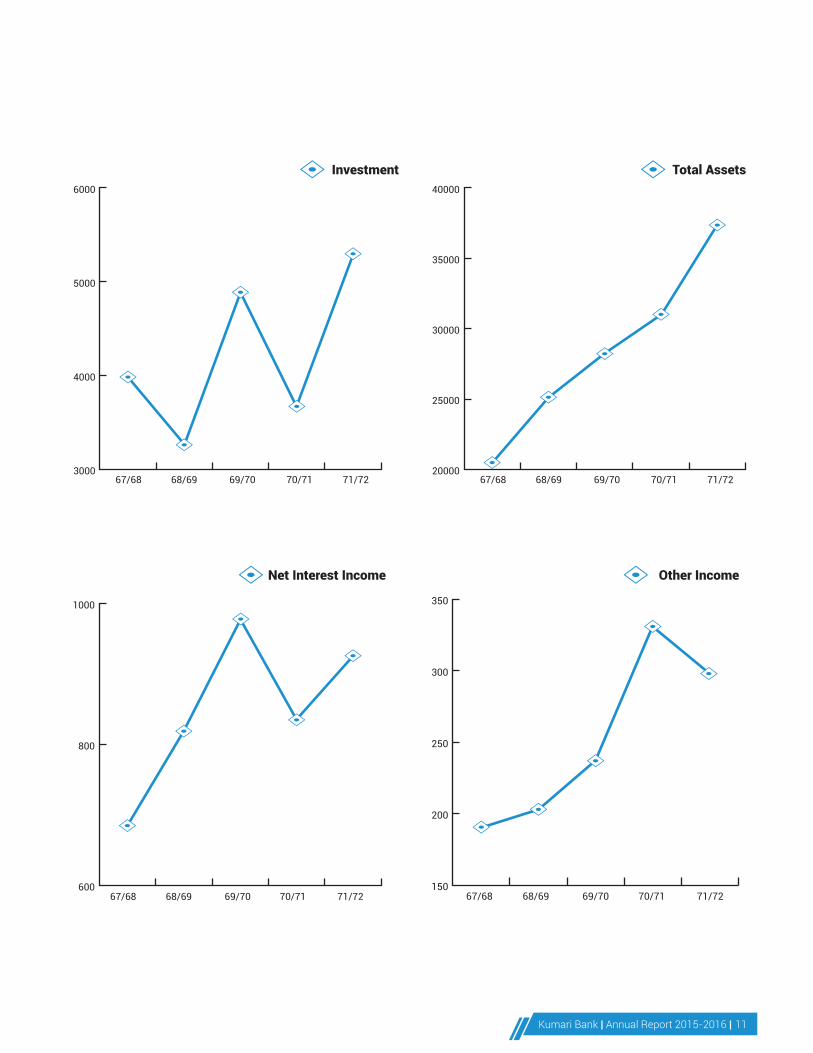

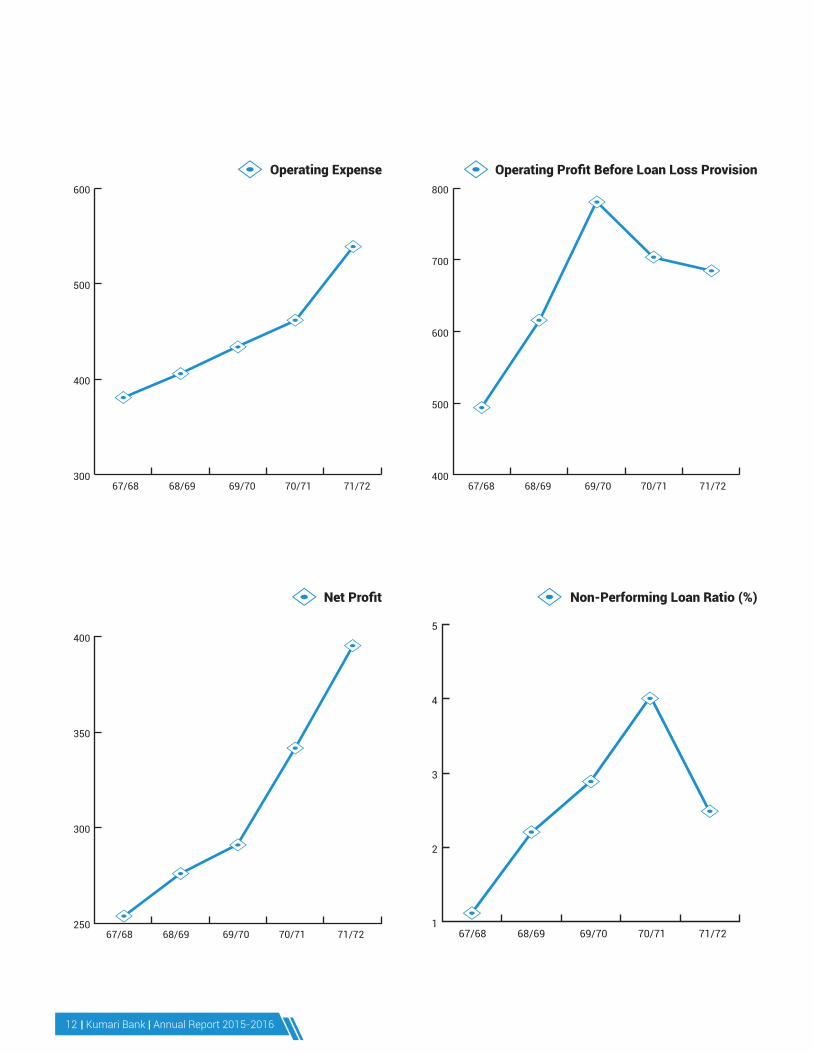

shows that bank achieved growth in loan, investment and deposit by 18.69%, 44.32% and 21.19% respectively. During the period, although the other operating income had declined by 10.06%; due to the incremental impact of net interest income by 10.81%; the total operating income of the bank had increased by 4.89%. Under operating expense, staff expenses

and other operating expenses increased by 28.22% and 5.71% respectively; which led to increment in total operating expense by 16.51%. Net loan loss provision decreased by 65.16% in fiscal year 2071/72 than that of previous fiscal year. Similarly, Bank’s net profit had increased by 15.55% in FY 2071/72.

67/68 68/69 69/70 70/71 71/721500

2000

2500

3000

67/68 68/69 69/70 70/71 71/72400

600

800

1000

67/68 68/69 69/70 70/71 71/7215000

20000

25000

30000

35000

67/68 68/69 69/70 70/71 71/7210000

15000

20000

25000

30000

Paid up Capital

Deposit

Reserve & Funds

Loan & Borrowings

Kumari Bank | Annual Report 2015-2016 | 11

67/68 68/69 69/70 70/71 71/723000

4000

5000

6000

67/68 68/69 69/70 70/71 71/7220000

25000

30000

35000

40000

67/68 68/69 69/70 70/71 71/72600

800

1000

67/68 68/69 69/70 70/71 71/72150

200

250

300

350

Investment

Net Interest Income Other Income

Total Assets

| Kumari Bank | Annual Report 2015-201612

12

67/68 68/69 69/70 70/71 71/72300

400

500

600

67/68 68/69 69/70 70/71 71/72400

500

600

700

800

67/68 68/69 69/70 70/71 71/72250

300

350

400

67/68 68/69 69/70 70/71 71/721

2

3

4

5

Operating Expense

Net Profit

Operating Profit Before Loan Loss Provision

Non-Performing Loan Ratio (%)

Kumari Bank | Annual Report 2015-2016 | 13

REVIEWING NATIONAL/ INTERNATIONAL ECONOMY:InternationalDuring the year 2015, the economic growth of developed countries is projected to improve and that of emerging and developing countries are expected to diminish. As per the World Economic Outlook published by International Monetary Fund as of July 2015; world’s economic growth is estimated to be 3.3% in 2015 whereas that on 2014 was 3.4%. The economic growth of United States of America for the year 2014 was 2.4% whereas that on the year 2015 is expected to be 2.5%. Similarly, economy of European countries and Japan in the year 2015 is expected to grow by 1.5% and 0.8% respectively. During the year 2014, the economy of European country increased by 0.8% and that of Japan declined by 0.1%. According to International Monetary Fund, the economy of emerging and developing countries in 2014 extended by 4.6% and is expected to grow by 4.2%. Similarly, in the year 2015, the economic growth of countries with minimum income level is expected to decline. The economic growth of such countries in 2014 was 6.0% and is expected to be 5.1% in 2015. The economic growth of neighboring countries India and China in 2015 is expected to be 7.5% and 6.8%. In 2014, the economic growth of such countries was 7.3% and 7.4% respectively. The world trade in the year 2014 increased by 3.2%; was expected to grow by 4.1% in 2015. Due to the decline in price of petroleum products and with decrease in the internal demand of petroleum products in the developed countries, the inflation of the developed countries is expected to decrease. In 2014, the inflation rate of such countries was maintained at 1.4% whereas it is expected to be 0% in 2015. In 2014, the inflation of emerging and developing countries was 5.1% and that in 2015 it is expected to be 5.5%. As per the estimation of International Monetary Fund on April 2015; the inflation rate of neighboring countries India and China is expected to be 6.1% and 1.2% respectively. (Source: Nepal Rastra Bank, Monetary Policy of Fiscal Year 2072/73).

NationalAccording to the primary estimation by Central Bureau of Statistics, for the fiscal year 2071/72, the Real Gross Domestic Product (GDP) rate based on actual base rate is expected to be 3.0% which was 5.1% in the previous fiscal year. Similarly, GDP in production price was 5.4% previous year and is expected to be 3.4% in the review period. In the review period, the economy was affected negatively and the growth rate remained minimum due to late monsoon, and devastating earthquake on Baisakh 12, 2072 and its aftershocks. According to the National Planning Commission, the earthquake had affected the economy adversely by NPR 706 billion approximately. Out of the total, it is estimated that 57.8% of the damage by earthquake is

sustained in social sector, 25.2% in productive sector, 9.5% in infrastructure sector and remaining 7.5% in other sectors. The total damage by earthquake comes around one-third of GDP for the fiscal year 2071/72. Loss on GDP is estimated to be NPR 36 billion, which subsequently effected in decline in the overall economic growth rate by 1.6%. In the review period, the agriculture sector which shares 33% of the total GDP; is expected to grow by 1.9% and that of non-agriculture sector by 3.6%. In the previous year the agriculture sector growth rate was 2.9% and that of non-agriculture sector rate was 6.3%. Due to the late monsoon, the main agriculture crops; wheat and maize production declined; and also due to the earthquake, which had impact on the loss of live stocks and crop production resulted in the low growth of the agriculture sector in the review period. In the review period, the growth rate of industrial sector is expected to be 2.6% which was 6.2% in previous year. Damage caused by earthquake directly to the fixed assets and production capacity of the industries; also induced scarcity of labor, their temporary management and low demand in the industrial produce had impacted adversely on the growth of industrial sector in the review period. The earthquake affected fixed assets and production capacity of industries by NPR 19 billion; almost 20% of the major road network had been damaged and affected 25% of the electricity production capacity which lead to adverse impact in industrial sector. The growth rate of service sector in the review period is expected to be 3.9% whereas that of previous year was 6.3%. Though there have been some improvements regarding industrial labor, peace security and other infrastructural problems; the major factor for decline in growth rate of service sector are due to effects of devastating earthquake and its aftershocks on hospitality business, real estate business, rental, wholesale and consumer business.

In the fiscal year 2071/72, the annual average inflation rate as per Consumer Price Index (CPI) is 7.2% and that in previous year was 9.1%.

In the fiscal year 2071/72, low export and increase imports had resulted in deficit in foreign trade. Due to the earthquake, due to low volume of imports at the end of the review period had resulted in the low rate of trade deficit. In the review period, total export decreased by 7.3% to NPR 85.32 billion whereas that in previous year was NPR 91.99 billion, which was a growth of 19.60% in comparison to its corresponding previous year. In the same review period, total import increased by 8.4% to NPR 774.68 billion whereas that in previous year was NPR714.37 billion, which was a growth of 28.3% in comparison to its corresponding previous year. Although there was decline in export and increase in import, but the export-import rate decreased to 11% in the review period which was 12.9% in previous year.

| Kumari Bank | Annual Report 2015-201614

14

The remittance inflow increased by 25% in the previous year and 13.6% in the review period which reached to NPR 617.28 billion.

In the fiscal year 2071/72, the Balance of Payment reached the highest i.e. NPR 144.85 billion which was NPR 127.13 billion last year.

In the fiscal year 2071/72, the total government expenditure under cash basis increased by 19.8% and reached NPR 499.96 billion and that in previous year increased by 16.3% i.e. to NPR 417.47 billion. In the review period, the capital expenditure based on cash basis increased by 26.6% and reached NPR 77.67 billion which was increased by 19.8% in previous year. In the review period the capital expenditure was 66.5% of the budget estimated for the period. In the previous year, the government expenditure increased in hefty due to the constituent assembly election; and due to the same the increment in the current year is seen minimal in comparison to the last year’s increment.

The deposit of Bank and Financial Institutions in the review period increased by 20.1% (NPR 282.6 billion) whereas that of previous year increased by 18.4% (NPR 218.68 billion). In the fiscal year 2071/72, the loan and investment of Bank and Financial Institutions increased by 17.5% (NPR 229.30 billion) whereas that in previous year increased by 14.4% (NPR 165.48 billion). In the review period, the private sectors by the Banks and Financial Institutions had extended loans in highest amount to production, construction and retail business portfolio. The loan to industrial production sector has increased by NPR 32.89 billion (14.8%) in the review period whereas that in previous year was increased by NPR 32.10 billion (16.8%). In the review period, loan to construction sector increased by Rs 33.31 billion (27.9%); retail business increased by NPR 53.23 billion (21.8%); transportation, communication and public service sector increased by NPR 12.75 billion (27%); which was NPR 23.49 billion (24.5%), NPR 45.94 billion (23.2%), NPR 3.45 billion (7.9%) respectively in previous fiscal year. Likewise, loan in agricultural sector in previous year increased by NPR 11.13 billion (28%) and that in the review period increased by NPR 14.25 billion (25%).

In the fiscal year 2071/72, the liquidity was retained through frequent deposit collection of NPR 155 billion, reverse repo NPR 315.80 billion and outright sale NPR 6 billion. Similarly, in the previous year, the liquidity was retained through reverse repo by NPR 602.50 billion and outright sale by NPR 8.50 billion. The weighted average interest rate of 91 days Treasury bill

in Asadh 2071 is 0.02% whereas it remained 0.1739% in Asadh 2072. Similarly, weighted average interbank interest rate among commercial banks in Asadh 2071 was 0.16% whereas that in Asadh 2072 is 1.01%. The weighted average interest rate for inter-bank transactions of other financial institutions for Asadh 2071 was 2.4% whereas that in Asadh 2072 is 3.89%.

In Asadh 2072, weighted average interest rate spread for commercial banks is 4.61% and was 5.21% in Asadh 2071. Similarly, the average base rate of commercial banks in Asadh 2071 was 8.36% and that in Asadh 2072 is 7.88%.

The overall Non-Performing loan ratio of Banks and Financial Institutions in Asadh 2072 is 3.33% and that in Asadh 2071 is 3.76%.

The NEPSE Index’s annual basis points diminished by 7.2% and reached to 961.2 points in Asadh 2072. The index was increased by 99.9% up to 1036.1 points in Asadh 2071.

Considering the overall economic situation of the fiscal year 2071/72, economic situation seems to be strong enough although economic structural framework seemed to be fragile. Even though country had an exceptional balance of payment situation, sufficient level of foreign exchange reserves and a mere single digit inflation indicating satisfactory level of economic stability, but inability to pace up the overall economic activities of the country is viewed as alarming factor inducing low rate of economic growth. Also, due to the earthquake in the last quarter of the review period had impact on the economic growth. (Source: Nepal Rastra Bank, Country’s Current Economic Status of Fiscal Year 2071/72).

3. REVIEW OF THE BANK’S OPERATIONS IN FY 2071/72:Analysis of the financial statement of review period clearly depicts the growth in banking transaction, asset and profit. Such increment led in increment of balance sheet size by 20.48%, which is NPR 37.37 billion in fiscal year 2071/72.

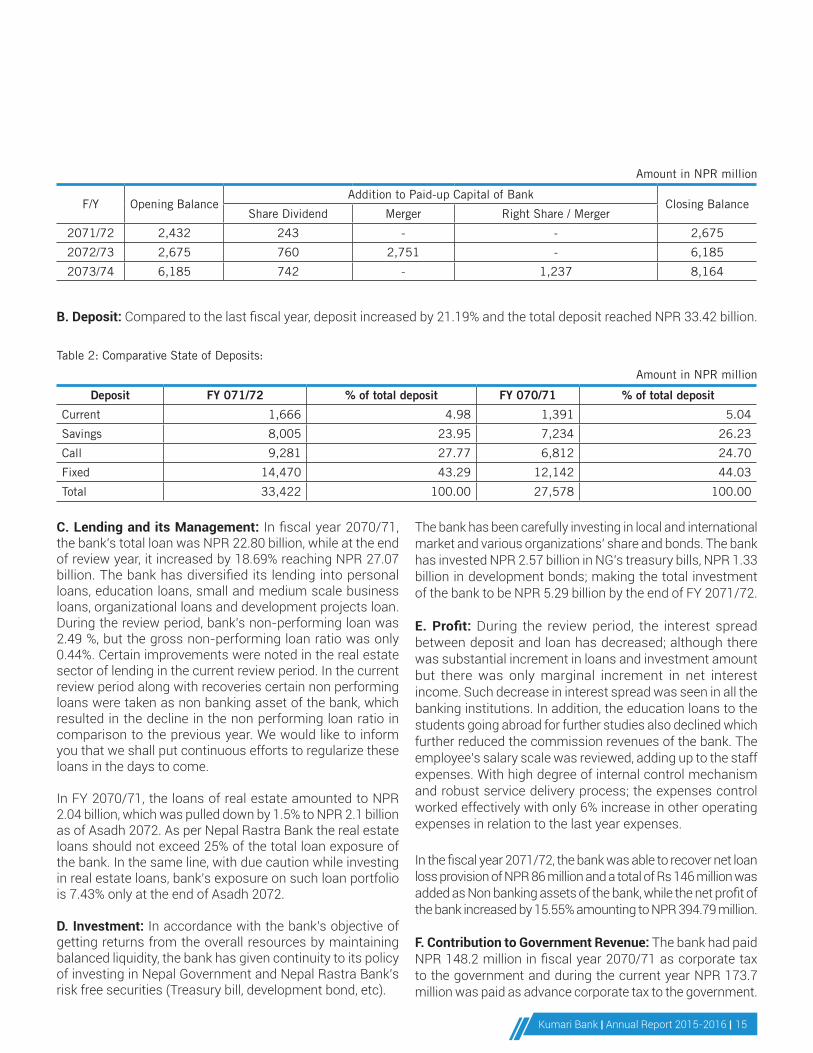

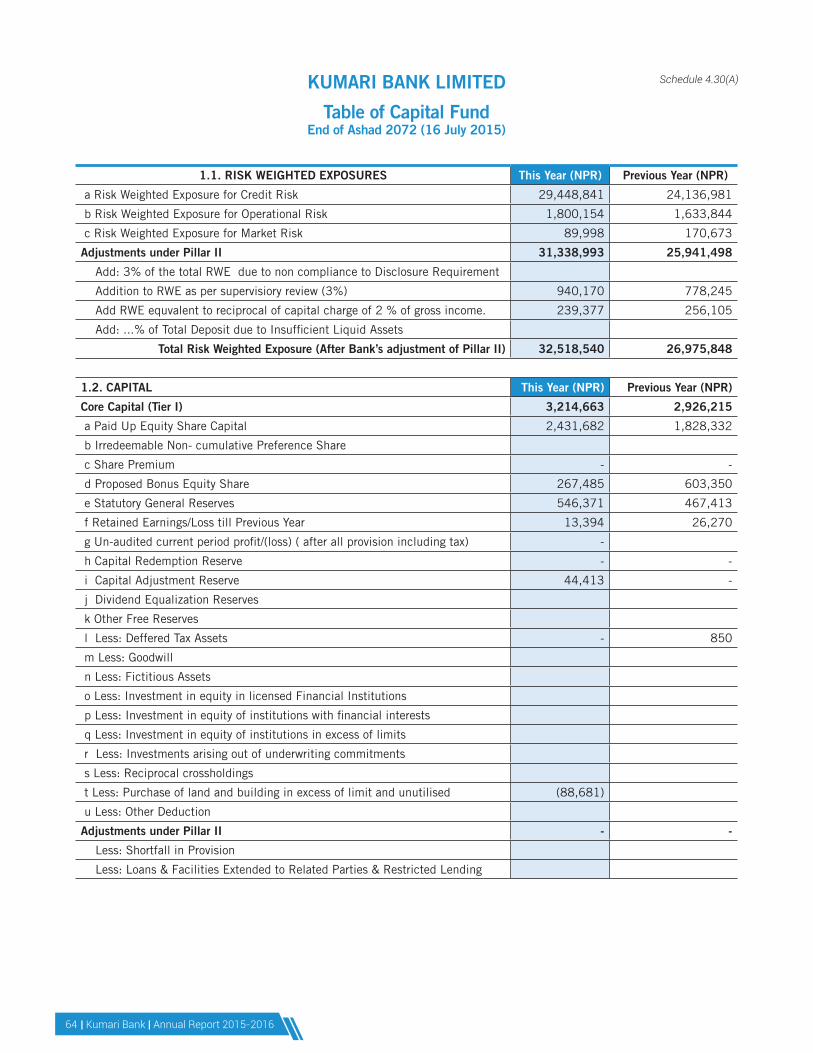

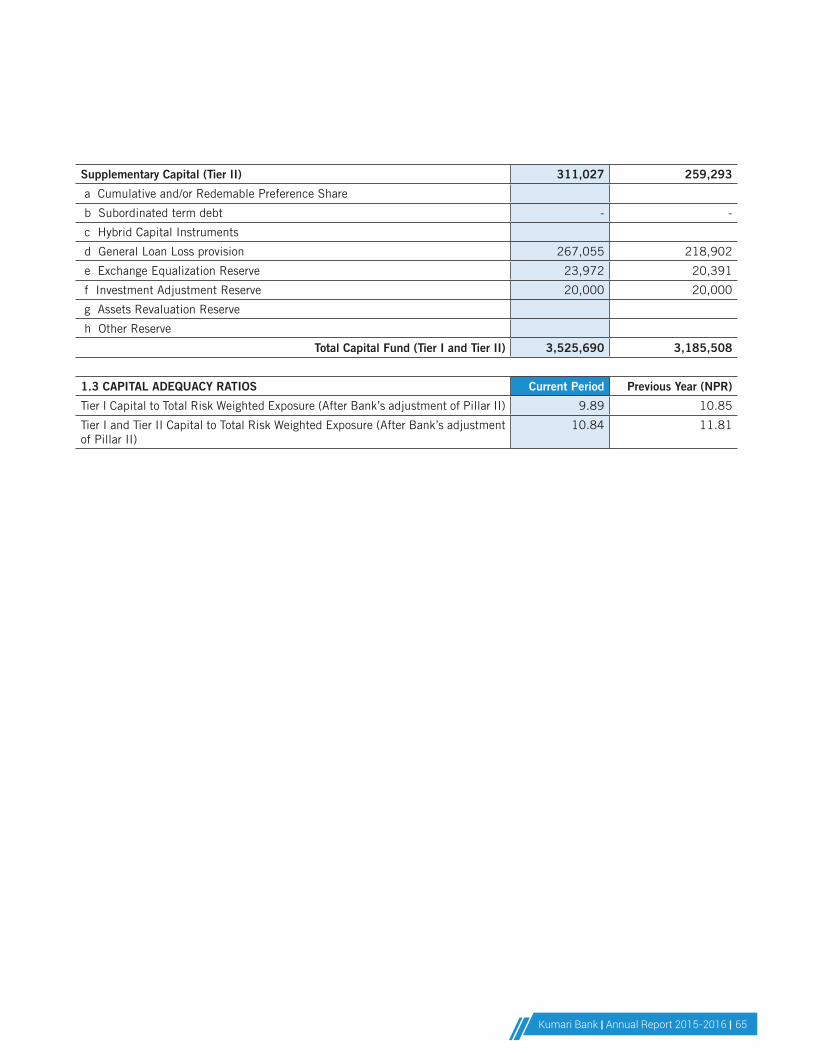

A. Capital management: By the end of 2071/72, paid up capital of the bank has reached to NPR 2.69 billion (including proposed bonus share). Also the capital adequacy ratio has to be minimum 10%, of which by the end of review period, the total capital adequacy is 10.84%. As per the Nepal Rastra Bank’s Capital requirement, bank had formulated following capital plan to adhere with the requirement of the Central Bank obligations.

Kumari Bank | Annual Report 2015-2016 | 15

Amount in NPR million

F/Y Opening BalanceAddition to Paid-up Capital of Bank

Closing BalanceShare Dividend Merger Right Share / Merger

2071/72 2,432 243 - - 2,675

2072/73 2,675 760 2,751 - 6,185

2073/74 6,185 742 - 1,237 8,164

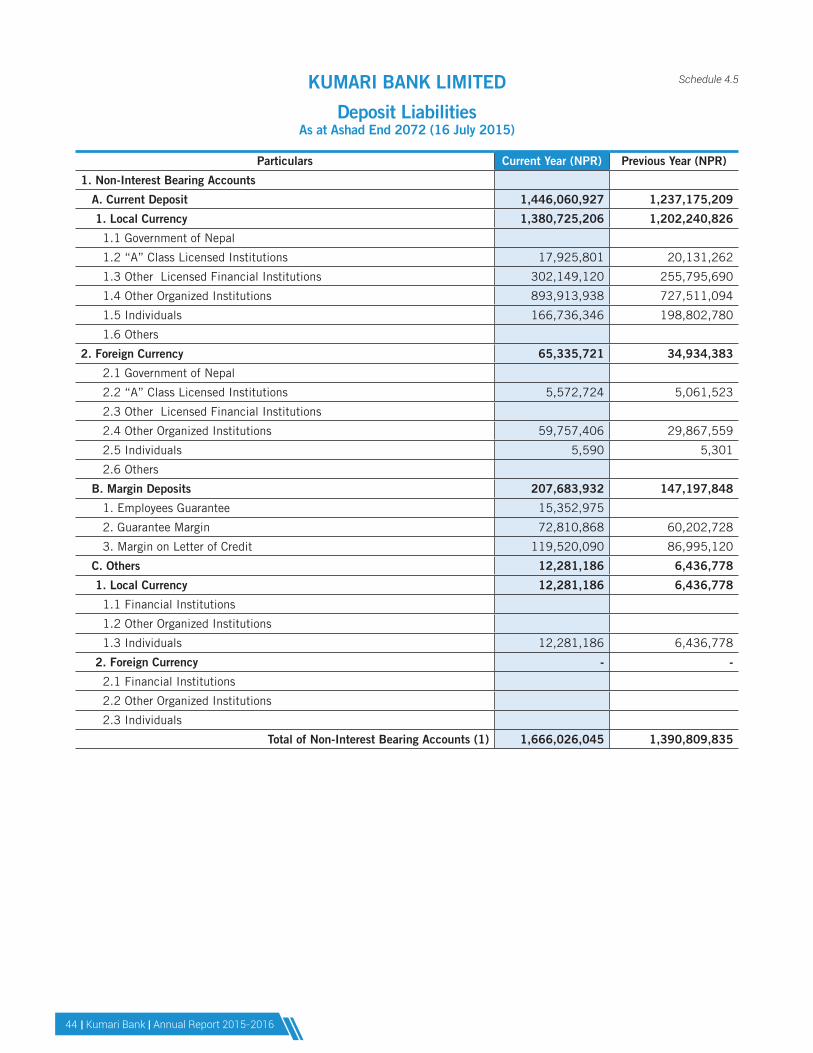

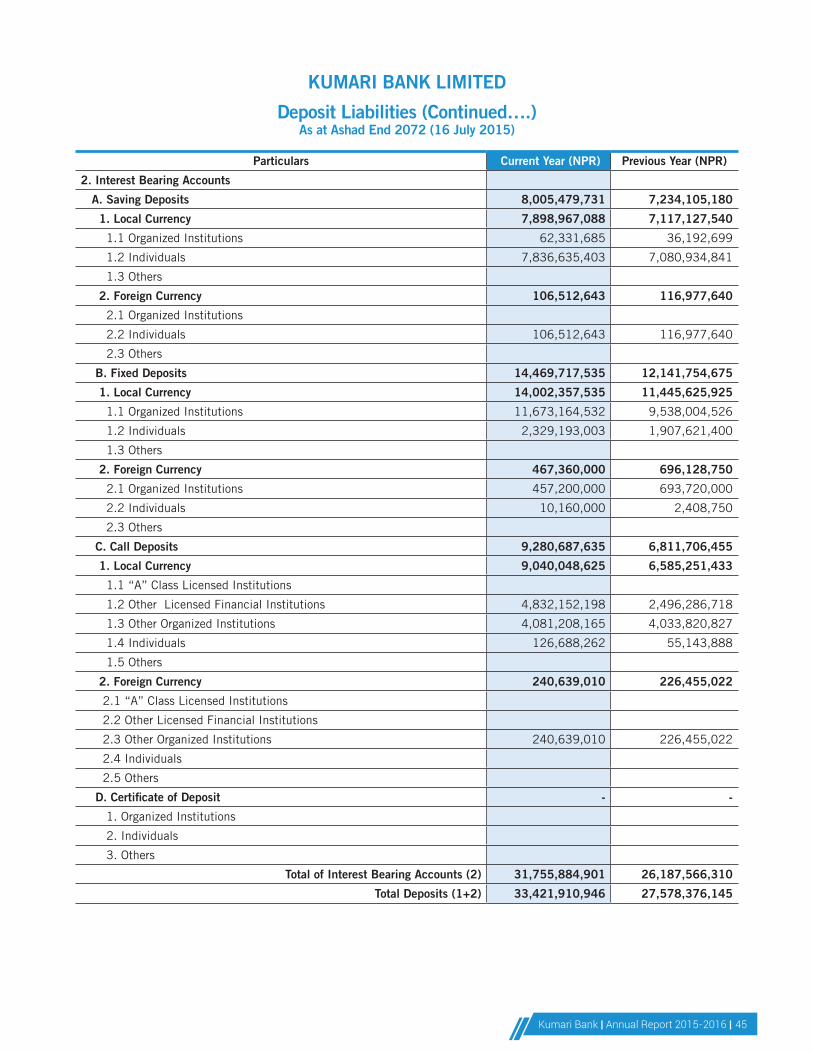

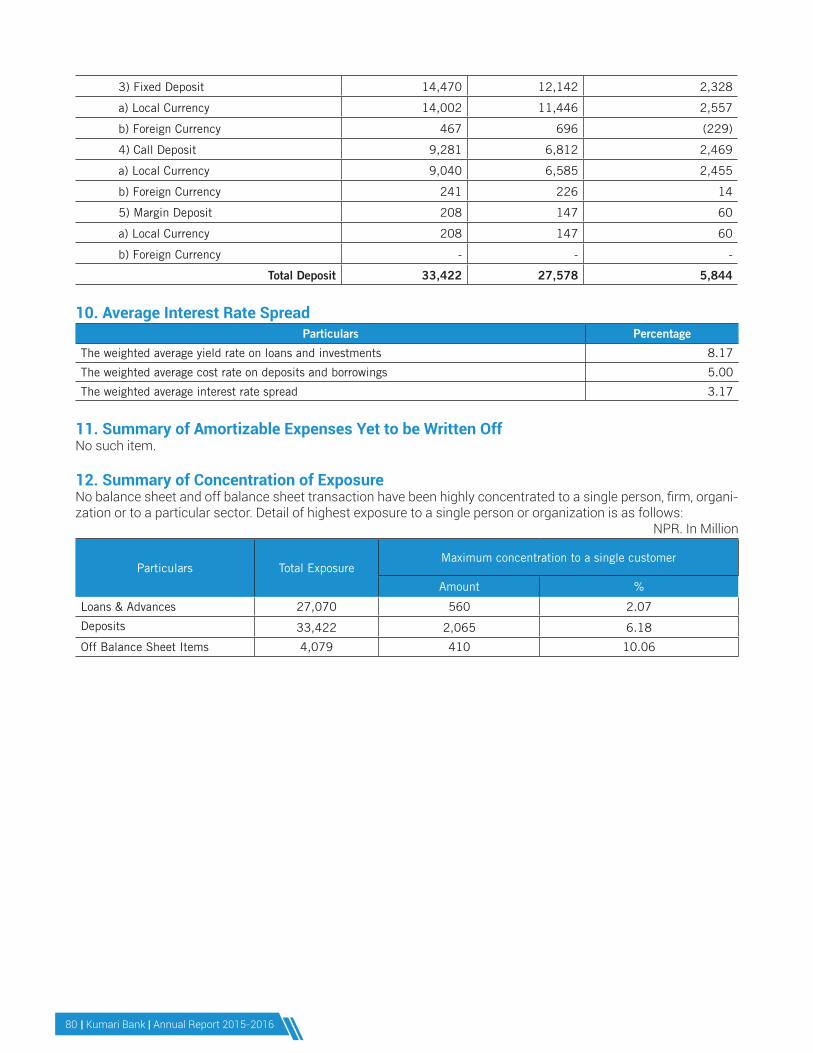

B. Deposit: Compared to the last fiscal year, deposit increased by 21.19% and the total deposit reached NPR 33.42 billion.

Table 2: Comparative State of Deposits:

Amount in NPR million

Deposit FY 071/72 % of total deposit FY 070/71 % of total deposit

Current 1,666 4.98 1,391 5.04

Savings 8,005 23.95 7,234 26.23

Call 9,281 27.77 6,812 24.70

Fixed 14,470 43.29 12,142 44.03

Total 33,422 100.00 27,578 100.00

C. Lending and its Management: In fiscal year 2070/71, the bank’s total loan was NPR 22.80 billion, while at the end of review year, it increased by 18.69% reaching NPR 27.07 billion. The bank has diversified its lending into personal loans, education loans, small and medium scale business loans, organizational loans and development projects loan. During the review period, bank’s non-performing loan was 2.49 %, but the gross non-performing loan ratio was only 0.44%. Certain improvements were noted in the real estate sector of lending in the current review period. In the current review period along with recoveries certain non performing loans were taken as non banking asset of the bank, which resulted in the decline in the non performing loan ratio in comparison to the previous year. We would like to inform you that we shall put continuous efforts to regularize these loans in the days to come.

In FY 2070/71, the loans of real estate amounted to NPR 2.04 billion, which was pulled down by 1.5% to NPR 2.1 billion as of Asadh 2072. As per Nepal Rastra Bank the real estate loans should not exceed 25% of the total loan exposure of the bank. In the same line, with due caution while investing in real estate loans, bank’s exposure on such loan portfolio is 7.43% only at the end of Asadh 2072.

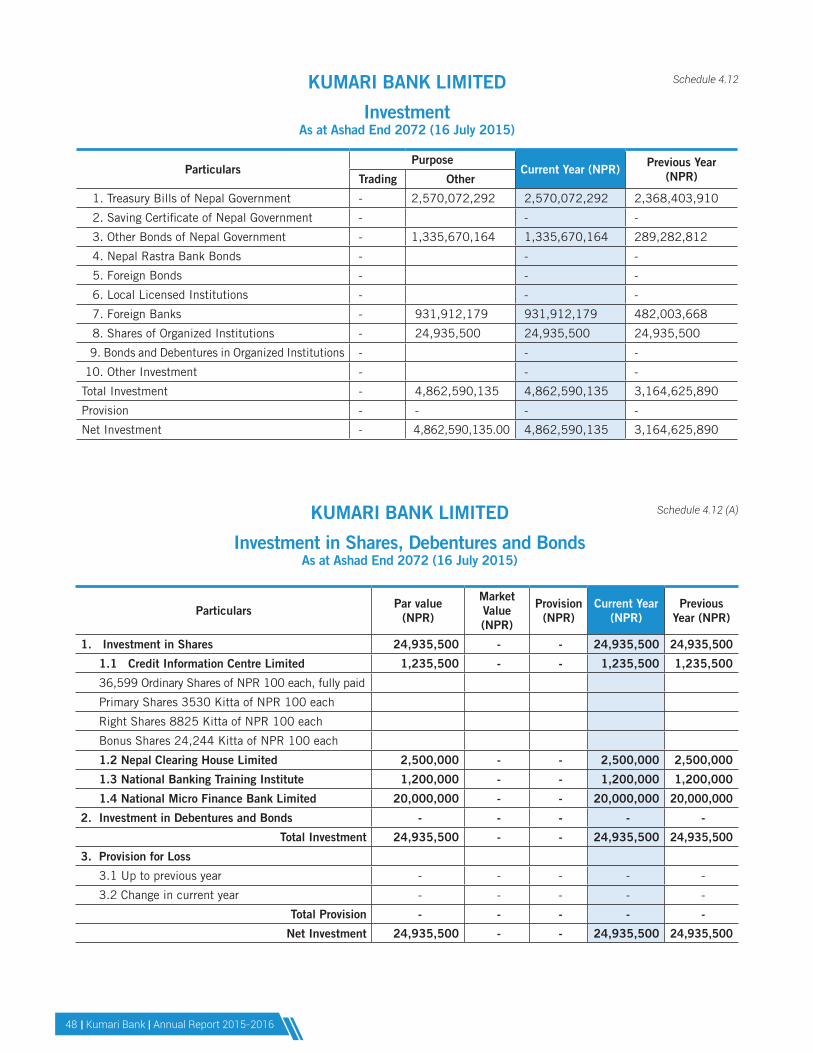

D. Investment: In accordance with the bank’s objective of getting returns from the overall resources by maintaining balanced liquidity, the bank has given continuity to its policy of investing in Nepal Government and Nepal Rastra Bank’s risk free securities (Treasury bill, development bond, etc).

The bank has been carefully investing in local and international market and various organizations’ share and bonds. The bank has invested NPR 2.57 billion in NG’s treasury bills, NPR 1.33 billion in development bonds; making the total investment of the bank to be NPR 5.29 billion by the end of FY 2071/72.

E. Profit: During the review period, the interest spread between deposit and loan has decreased; although there was substantial increment in loans and investment amount but there was only marginal increment in net interest income. Such decrease in interest spread was seen in all the banking institutions. In addition, the education loans to the students going abroad for further studies also declined which further reduced the commission revenues of the bank. The employee’s salary scale was reviewed, adding up to the staff expenses. With high degree of internal control mechanism and robust service delivery process; the expenses control worked effectively with only 6% increase in other operating expenses in relation to the last year expenses.

In the fiscal year 2071/72, the bank was able to recover net loan loss provision of NPR 86 million and a total of Rs 146 million was added as Non banking assets of the bank, while the net profit of the bank increased by 15.55% amounting to NPR 394.79 million.

F. Contribution to Government Revenue: The bank had paid NPR 148.2 million in fiscal year 2070/71 as corporate tax to the government and during the current year NPR 173.7 million was paid as advance corporate tax to the government.

| Kumari Bank | Annual Report 2015-201616

16

G. Products and Services: Kumari bank has launched differentiated products Kumari Swastha Jeevan Bachat Khata, Kumari Remit Bachat Khata and Personal Term Loans. Kumari Swastha Jeevan Bachat Khata has been introduced to promote savings and for improvement of quality of healthy lifestyle. The account holders of this new and peculiar product can avail discounts in the treatment cost incurred at Medanta Hospital, New Delhi. Customers are offered with co-branded ATM card used to get 5% discount with privileged services in pre-appointment, admission, consultation and follow-ups. Depositors under this scheme can also avail medical insurance facility of NPR 10,000.00 free of cost and heavy discounts are provided for the various types of services that the bank provides. Keeping in purview of providing service for transfer of fund within country and outside country the bank has been providing quality services via Kumari Remit Bachat Khata. The saving account scheme holders can also avail numerous discounts on varied services provided by the bank. In order to serve our valued customers Kumari bank has come up with various schemes under personal lending in simple and robust manner.

The Bank has been always been a techno-savvy service provider offering SMS Banking, Internet Banking and Kumari Mobile banking to its valued customers. The customers availing such services can make payments for mobile bills, telephone bills, credit card payments and other utility payments through internet portals. Similarly, the e-services of the bank can be linked with e-sewa, which could be used for interbank fund transfer, payment of air ticket, electricity bills and many other payment solutions. For smooth and easy remittance services, the Bank has introduced Kumari Remit software. Along with it, bank had made service level agreements with other remittance service providers to enhance further reach to the market in niche level. The Bank has been providing remittance services through more than 1000 remit agents throughout the country. The Bank has also signed agreement with 7 international remit companies.

The bank is even more resilient to bring newer services and added features for easier access of the products to the customers. We are continually in the process to provide market competitive privileged products and services to our valued customers. Electronic Banking since its inception, Kumari Bank has been providing varied innovative products and has made distinct market position in the industry. Visa Electron, Dollar Debit cards can be accessed via VISA network in Nepal, India and any other part of the world.

H. Branch and Network Expansion: The bank has extended 2 new branches inside the Kathmandu valley in this fiscal year. Currently, the bank has 25 branches outside valley and 11 branches inside valley, altogether 36 branches, 2 extension counters and 46 ATMs.

I. Corporate Governance: Banks and financial institutions are public organizations not only operated with shareholders’ funds but also through institutional and public deposit. This means that good corporate governance and moral character are two extremely sensitive issues that the bank takes into account. Being aware that the good corporate governance is the guiding path of the bank’s operations, the board of directors is consistently giving effort to conduct its activities according to the same, and to develop strong and transparent good corporate governance also in other activities of the bank.

J. Risk Management: A separate risk management sub-committee has been established to identify, monitor and protect the bank from potential risks associated with different activities of the bank. Policies and regulations have also been formed and implemented to manage the numerous risks associated with banking activities as well as other potential risks. The bank has taken the policy to make the internal control system more effective and efficient by properly managing the bank’s loans, operations, market and other risks.

The bank has executive management that formulates required policies, regulations, and documentation related to loan management, customer recognition, stress test and daily transactions activities.

i. Loan Risk Management: To identify and manage loan risks, bank has set up a separate department. The department assesses the risks associated before making any loan disbursements by the bank keeping in mind of the possible risks assessed with the predefined standards and policies set by the Nepal Rastra Bank as well as bank’s internal policy to hedge risks. The bank has taken up policy to determine loan risk segments and invest in the least risky segments by studying current scenario and expected future possible risk factors. Depending upon the changed market scenario bank adhere amendment of policies, reformulation of the loan portfolios, and determination of the level of risk and loan sectors. Also, the bank has priority set to reduce the concentration risks.

ii. Operating Risk Management: All the banking activities directed towards the operation of the bank is driven by given policies and guidelines with clearly defined work ethics, proper implementation and hedging of operational risk of the bank. To cope with the operational risk, the bank has set up a separate operation risk management department. It works as an identifier of risk associated with internal workflows and procedures, human resources related risks and provides suggestive solutions for such risk minimization. Because of this, we are confident that operating risks are being managed well.

Kumari Bank | Annual Report 2015-2016 | 17

iii. Liquidity Risk Management: Considering the scenario of excess liquidity and liquidity crunch on time from previous years, and impacts of the same on the profitability of the bank, various financial source and investment areas are determined and utilized in order to maintain optimum balance of liquidity. In order to cope and balance the liquidity scenarios and profitability match, ALCO/ Pricing Committee is formed.

iv. Market Risk Management: Bank is always alert regarding factors related to market risks and analyses those factors to prepare plan for the same. The bank has made policies and devised working methods to monitor the foreign exchange situation to minimize risks associated with fluctuations in foreign currency exchange rates. Similarly, arrangements have also been made for formulating the necessary policies and regulation by regular monitoring market interest rates. The ALCO/ Pricing Committee is formulated and entrusted to control such risks.

K. Corporate Social Responsibility: The bank is aware of its social responsibilities along with this professional intent as well. Kumari Bank, an eminent participant in CSR activities, had made its mark to support devastating earthquake victims. The bank had provided galvanized sheets worth of NPR 4.6 million towards those who lost their houses in the calamity. The bank had also extended helping hands to renovate ‘Kumari Ghar’ of Kathmandu by providing NPR 0.5 million; which in total comes to NPR 5.1 millions worth in cash value as support to earthquake victims. The bank has been providing scholarship to children via HOPAD Child and Women Promotion Society (NGO) as part of its regular CSR activities to support child welfare. The bank has provided free health camp service in Sindhupalchowk area through Indrawatee Community Service Centre as an initiative taken by bank towards promotion of healthy community. Cultural and social harmony is our responsibility; the bank has established ‘Kumari Education Fund’ in order to support Goddess Kumari for her higher studies. Every year NPR 50,000.00 is deposited in the fund. As part of cultural preservation initiative, the bank has been supporting Kumari Puja and Indra Jatra festival every year through various activities and financial support. For social welfare, the bank has distributed food to elderly citizens at Nisahaya sadan old age homes. In order to create awareness regarding possible diseases due to mosquitoes in Terai Region; Kumari Bank, Nijgadh branch distributed mosquito nets to Community Hospital of Nijgadh. The bank also organized tree plantation program in Dhanusa, Mahendranagar for creating environmental awareness. Besides, the bank also made its presence in various socio-cultural programs as blood donation program, school and colleges’ development programs, financial literacy programs and support to various clubs working for social development on regular basis.

L. Committees and sub-committees appointed by Board of Directors: According to popular law and the policies made under bank’s authority, the following committees and sub-committees are in place:

i. Audit committee: In accordance with Section 164 of the Company Act, an audit committee was in place comprising of director Naresh Dugar and bank’s internal audit head as member secretary under the convenorship of non-executive director Rasendra Bahadur Malla. Since, both directors Rasendra Bahadur Malla and Naresh Dugar have been staying abroad, their responsibilities are handed over to director Er. Binod Dawadi and director Dr. Shobha Kant Dhakal for the time being. The bank’s internal audit division reports directly to this committee.

ii. Human resource sub-committee: In order to guide management in selection of capable employees, recruitment, appointments, skill development and related services/ facilities, and other such matters, a human resource sub-committee comprising of head of human resource department under the convener ship of director Dr. Shobha Kant Dhakal is in place.

iii. Risk management sub-committee: In order to correctly identify and eradicate the risks of the bank, a committee comprising director Rasendra Bahadur Malla, director Puna Ram Bhandari and head from the concerned department under the convener ship of director Uttam Prasad Bhatarai is in place that formulates policies, regulations for the same.

Such committees and sub-committees appointed by the board of directors have been conducting their activities within the premises set by the Board, Company Act 2063 and in accordance to the Nepal Rastra Bank’s directives. This committees and sub-committees’ work, duties and authority and the conveners and member of the stated committees and sub-committees have not been provided with any additional reimbursements and facilities except for meeting allowances.

iv. Other management level committees: Besides the above mentioned committees and sub-committees appointed by the Board of Directors, the following have also been conducting their activities under convener ship of the CEO in order to implement the bank’s activities more effectively: management committee, pricing committee / asset and liability management committee, labor relations, HR committee, discipline and performance review committee, procurement committee and bad loans recovery committee. The members of these committees are not provided any allowances or any additional facilities.

| Kumari Bank | Annual Report 2015-201618

18

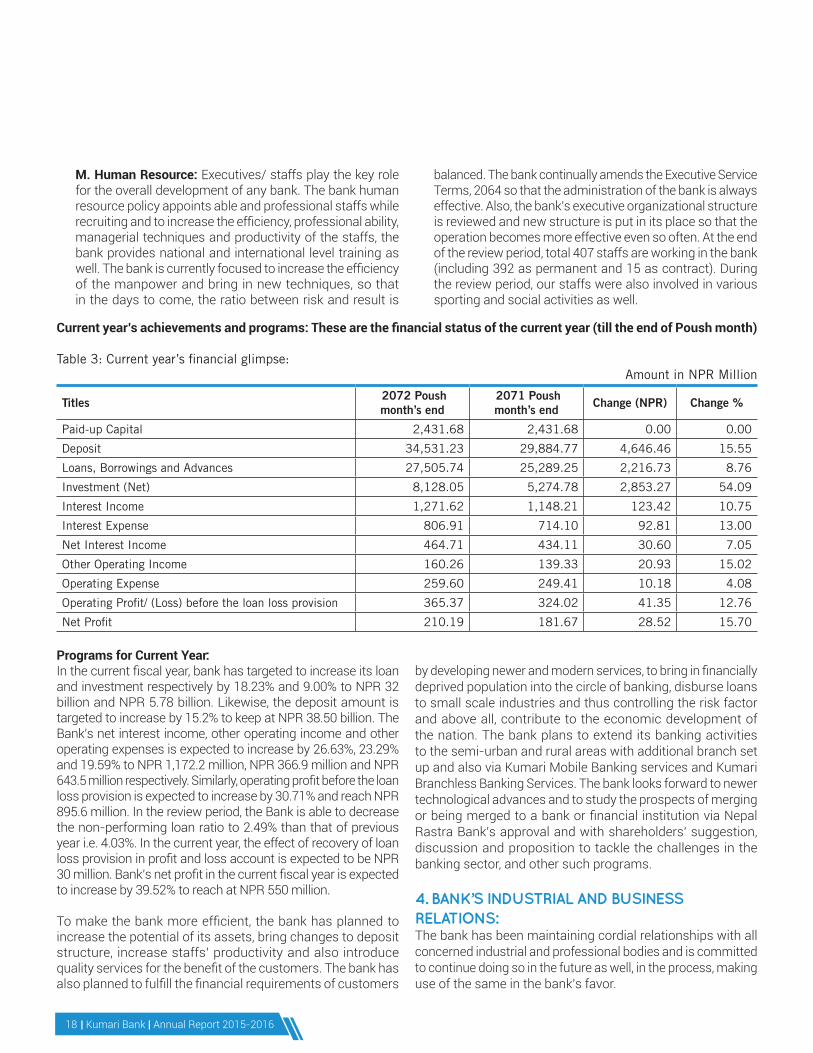

M. Human Resource: Executives/ staffs play the key role for the overall development of any bank. The bank human resource policy appoints able and professional staffs while recruiting and to increase the efficiency, professional ability, managerial techniques and productivity of the staffs, the bank provides national and international level training as well. The bank is currently focused to increase the efficiency of the manpower and bring in new techniques, so that in the days to come, the ratio between risk and result is

balanced. The bank continually amends the Executive Service Terms, 2064 so that the administration of the bank is always effective. Also, the bank’s executive organizational structure is reviewed and new structure is put in its place so that the operation becomes more effective even so often. At the end of the review period, total 407 staffs are working in the bank (including 392 as permanent and 15 as contract). During the review period, our staffs were also involved in various sporting and social activities as well.

Current year’s achievements and programs: These are the financial status of the current year (till the end of Poush month) Table 3: Current year’s financial glimpse: Amount in NPR Million

Titles 2072 Poush month’s end

2071 Poush month’s end Change (NPR) Change %

Paid-up Capital 2,431.68 2,431.68 0.00 0.00

Deposit 34,531.23 29,884.77 4,646.46 15.55

Loans, Borrowings and Advances 27,505.74 25,289.25 2,216.73 8.76

Investment (Net) 8,128.05 5,274.78 2,853.27 54.09

Interest Income 1,271.62 1,148.21 123.42 10.75

Interest Expense 806.91 714.10 92.81 13.00

Net Interest Income 464.71 434.11 30.60 7.05

Other Operating Income 160.26 139.33 20.93 15.02

Operating Expense 259.60 249.41 10.18 4.08

Operating Profit/ (Loss) before the loan loss provision 365.37 324.02 41.35 12.76

Net Profit 210.19 181.67 28.52 15.70

Programs for Current Year:In the current fiscal year, bank has targeted to increase its loan and investment respectively by 18.23% and 9.00% to NPR 32 billion and NPR 5.78 billion. Likewise, the deposit amount is targeted to increase by 15.2% to keep at NPR 38.50 billion. The Bank’s net interest income, other operating income and other operating expenses is expected to increase by 26.63%, 23.29% and 19.59% to NPR 1,172.2 million, NPR 366.9 million and NPR 643.5 million respectively. Similarly, operating profit before the loan loss provision is expected to increase by 30.71% and reach NPR 895.6 million. In the review period, the Bank is able to decrease the non-performing loan ratio to 2.49% than that of previous year i.e. 4.03%. In the current year, the effect of recovery of loan loss provision in profit and loss account is expected to be NPR 30 million. Bank’s net profit in the current fiscal year is expected to increase by 39.52% to reach at NPR 550 million.

To make the bank more efficient, the bank has planned to increase the potential of its assets, bring changes to deposit structure, increase staffs’ productivity and also introduce quality services for the benefit of the customers. The bank has also planned to fulfill the financial requirements of customers

by developing newer and modern services, to bring in financially deprived population into the circle of banking, disburse loans to small scale industries and thus controlling the risk factor and above all, contribute to the economic development of the nation. The bank plans to extend its banking activities to the semi-urban and rural areas with additional branch set up and also via Kumari Mobile Banking services and Kumari Branchless Banking Services. The bank looks forward to newer technological advances and to study the prospects of merging or being merged to a bank or financial institution via Nepal Rastra Bank’s approval and with shareholders’ suggestion, discussion and proposition to tackle the challenges in the banking sector, and other such programs.

4. BANK’S INDUSTRIAL AND BUSINESS RELATIONS: The bank has been maintaining cordial relationships with all concerned industrial and professional bodies and is committed to continue doing so in the future as well, in the process, making use of the same in the bank’s favor.

Kumari Bank | Annual Report 2015-2016 | 19

5. CHANGES IN BOARD OF DIRECTORS AND THE REASONS:Bank’s former Chairman, Mr. Noor Pratap J.B. Rana resigned from his position on Poush 21, 2072 on his self interest, which was accepted by the board meeting, held on Poush 23, 2072 effective from Poush 21, 2072.

Professor Dr. Rajan Bahadur Poudel resigned from the position on Chaitra 26, 2071 on personal grounds which was accepted by the board meeting.

We would like to thank them for their hard work and dedicated service towards the bank.

The board meeting held on Poush 27, 2072 appointed promoter shareholder Er. Binod Dawadi in place of Mr. Rana.

Similarly, the board meeting held on Magh 28, 2072 appointed Mr. Santosh Kumar Lama, promoter shareholder as Chairman which remained vacant after the resignation by Mr. Rana. 6. MAJOR ISSUES AFFECTING BUSINESS:The devastating earthquake that shook the country on Baisakh 12, 2072 and its aftershocks had its impact on the industrial and business activities. Apart from which, after the promulgation of the constitution of Nepal, the unstable political situation, border blockade, energy crisis and labor crisis had affected adversely to the bank. Country’s industrial and business sector need to develop in order to develop banking sector. Currently, industrial and business activities of the country are experiencing abnormal conditions, due to which the capacity of borrowers to repay loan and interest amount has diminished. Moreover, excess liquidity situation prevailed in the financial market; in the absence of justifiable and profitable investment opportunities. Hence, due to these factors banks are not in position to run its business activities in normal conditions and possibilities of negative impact on the bank’s profitability as well.

7. BOARD OF DIRECTORS’ RESPONSES TO THE AUDITOR’S REPORTExcept for normal comments concerning the bank’s regular business, no especially negative comments have been observed in the audit report. Instructions have also been given to the management to implement the suggestions and advice of the audit report. The financial statements of fiscal year 2071/72 were accepted by Nepal Rastra Bank on Magh 20, 2072; the comments and instructions have been included in the annual report. Bank has already given direction to its management team for implementation of received comments and instructions.

8. DIVIDEND DECLARATION:Kumari Bank announces 11% bonus share from its paid-up capital i.e. NPR 267.4 million and NPR 14.0 million cash dividend for tax purpose on bonus share as proposed by the board of directors; i.e. total of 11.58% which makes total amount of NPR 281.5 million as total dividend.

9. FORFEITED SHARESIn the reported year, no shares have been forfeited.

10. PROGRESS OF THE BANK AND ITS SUBSIDIARY COMPANIESThe progress of the bank has been presented under various headings in this report. The bank does not have any subsidiary companies.

11. MAJOR BUSINESSES CONDUCTED BY THE BANK AND ITS SUBSIDIARY COMPANIES IN FY 2071/72 AND ANY IMPORTANT CHANGES IN BUSINESS ACTIVITIESThe bank does not have any subsidiary companies and there are no major changes other than mentioned in this Annual Report.

12. IMPORTANT INFORMATION PROVIDED BY VALUED SHAREHOLDERNone.

13. DETAILS OF SHARE HOLDING BY THE COMPANY’S DIRECTORS AND OFFICE BEARERS IN THE PREVIOUS FY AND INFORMATION PROVIDED BY THEM ABOUT THEIR INVOLVEMENT IN THE TRADING OF COMPANY SHARES, IF ANYNo information as such.

14. INFORMATION ABOUT ANY AGREEMENTS CONCERNING THE BANK THAT SERVICE THE SELF INTEREST OF ANY DIRECTOR OR PEOPLE CLOSE TO THEMNone.

15. DETAILS ABOUT RE-PURCHASE OF SHARESNone.

16. DETAILS ABOUT INTERNAL CONTROL SYSTEM:There is a separate department to maintain the bank’s internal control systems. This department is always active to minimize

| Kumari Bank | Annual Report 2015-201620

20

risks associated with the Bank’s loans, operations and market risks. Monitoring of the effectiveness of the internal control systems is done on a regular basis by the Audit Department while conducting its regular audit.

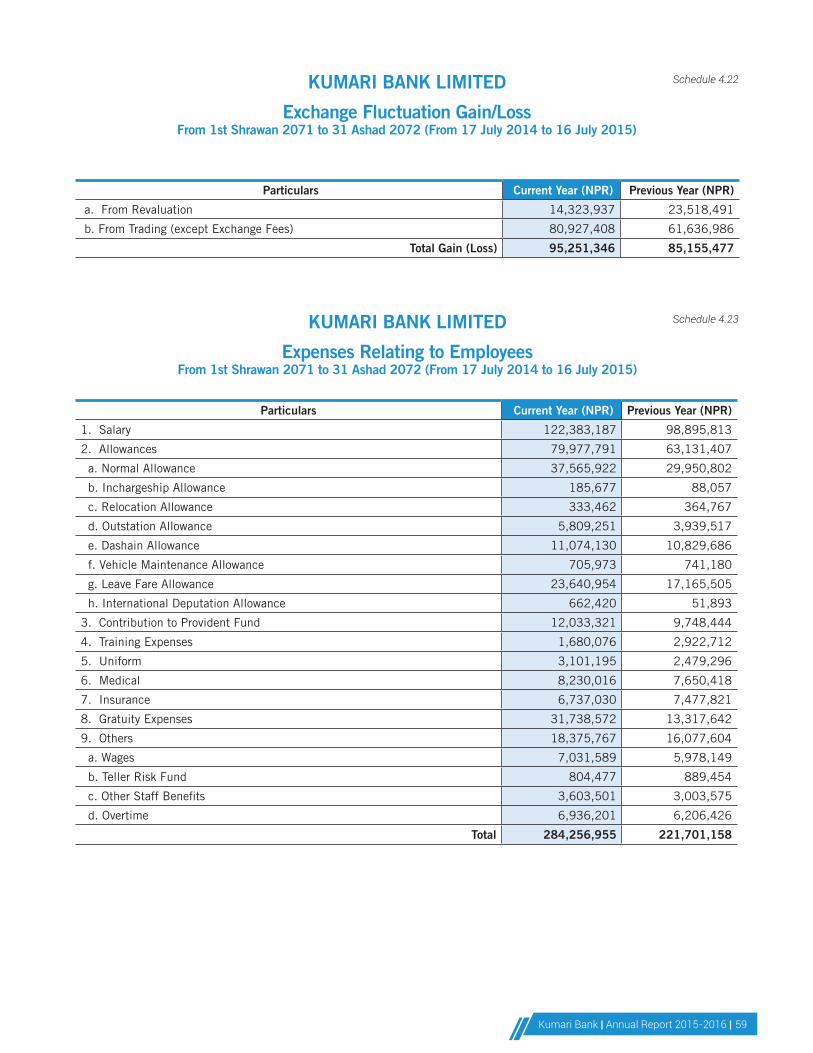

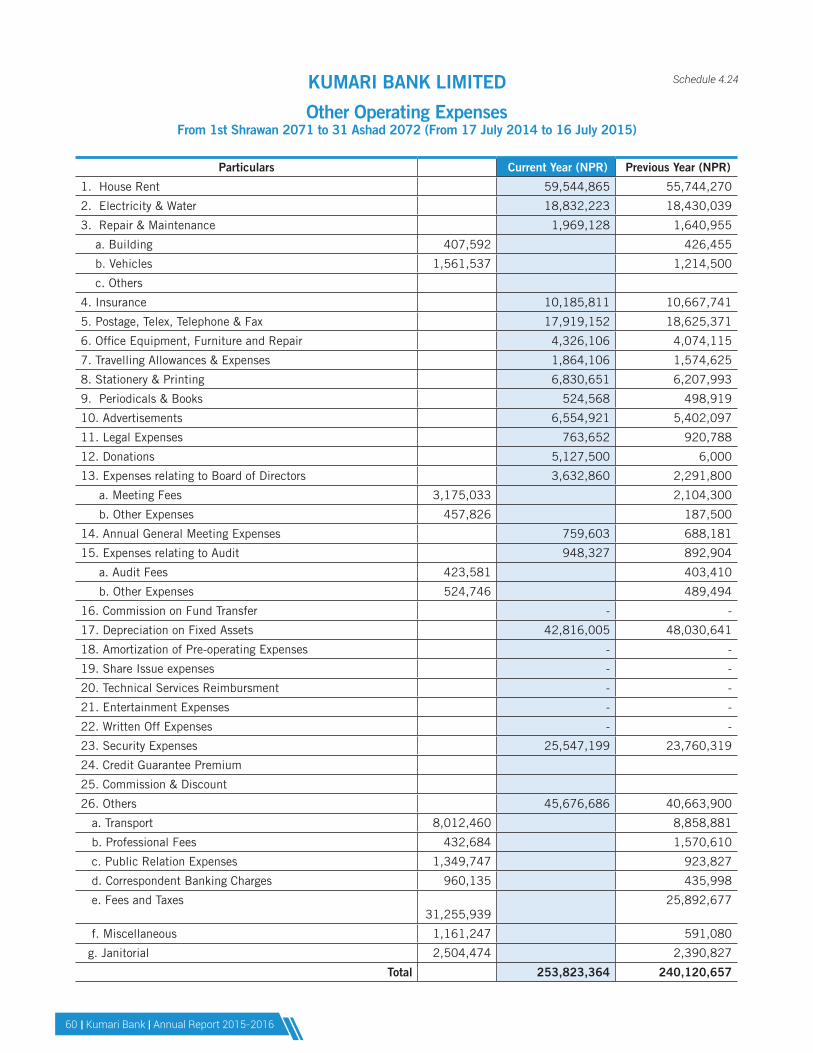

17. DETAILS OF THE BANK’S TOTAL OPERATING COSTSThe Bank’s operating costs in FY 2071/72 were as follows:

Staff expenses: NPR 284,256,955Other operating costs: NPR 253,823,364

Detailed description of the bank’s total operating costs has been stated in Annexure 4.23 and 4.24 of the Annual Report.

18. INFORMATION ABOUT AUDIT COMMITTEEAccording to the Company Act, Section 164, the audit committee is comprised of directors Naresh Dugar and bank’s internal audit department head, Ganesh Kumar K.C., as member secretary under the convener ship of non-executive director Rasendra Bahadur Malla (Mr. Malla and Mr. Dugar have been staying abroad so director Er. Binod Dawadi and director Dr. Shobha Kant Dhakal are given responsibility temporarily). Bank’s internal audit department reports directly to this committee. This committee has had 10 sittings in FY 2071/72. Member of this committee have been provided with meeting allowance at par with other board members. This committee’s activities are conducted in accordance with Nepal Rastra Bank‘s directives and Company Act regulations. No serious remarks on the bank’s operations have been observed in the

internal audit report. The audit committee has been conducting regular monitoring of the internal control systems and regularly providing suggestions concerning implementation to the management besides providing information on the same to the board of directors. The management of the bank has been improving its daily activities regularly as per the suggestion provided by audit committee.

19. INFORMATION ABOUT ANY CASH BALANCE TO BE PAID TO THE BANK BY DIRECTOR, MANAGING DIRECTOR, CHIEF EXECUTIVE OFFICER, BANK’S PROMOTERS OR THEIR CLOSE RELATIVES OR FIRM ASSOCIATED WITH THEM, COMPANY OR ORGANIZATIONNone.

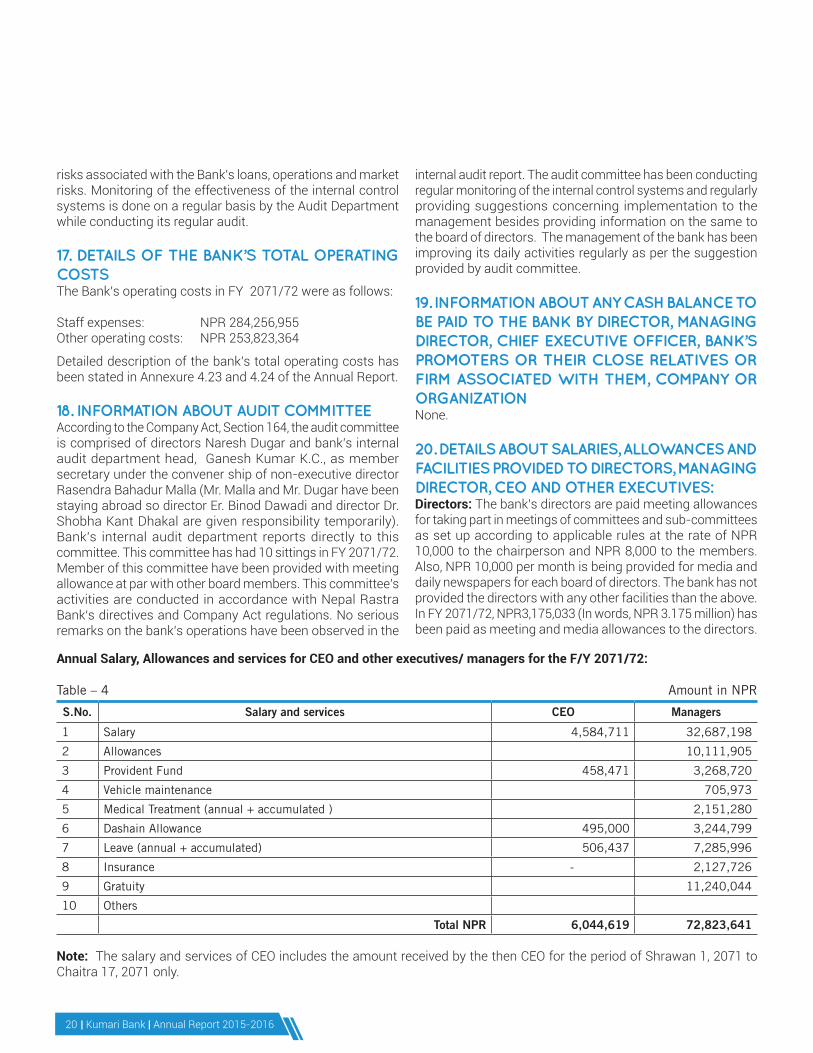

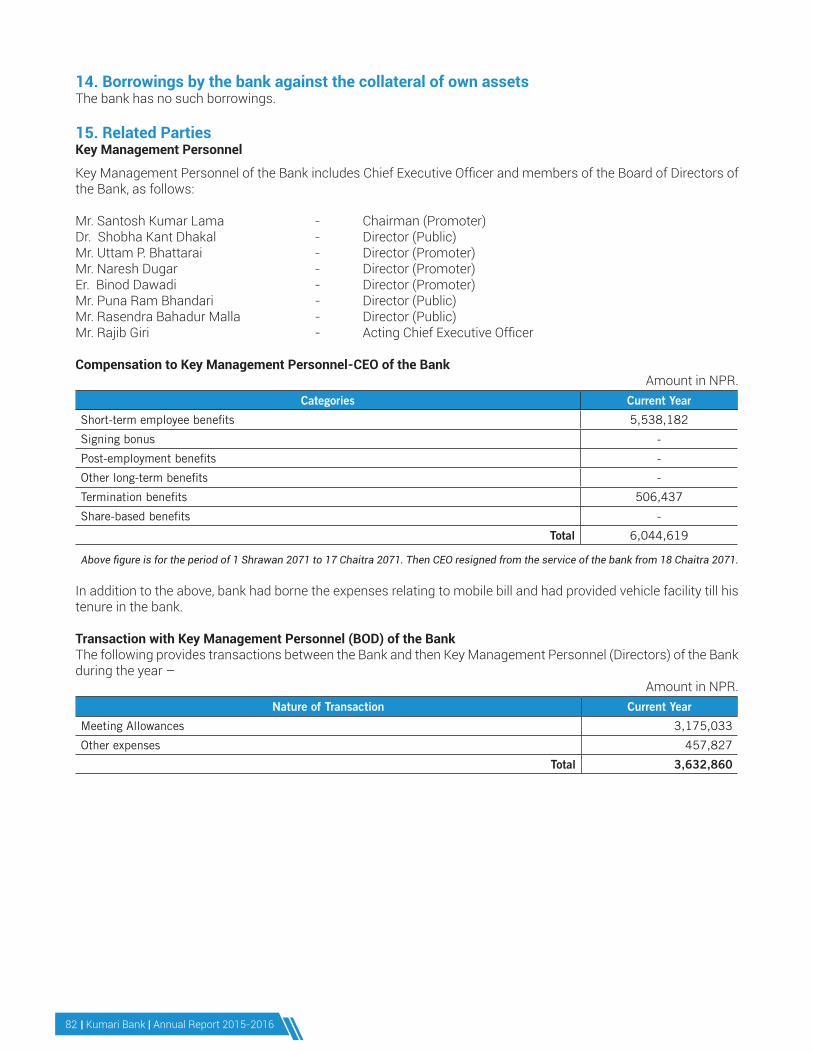

20. DETAILS ABOUT SALARIES, ALLOWANCES AND FACILITIES PROVIDED TO DIRECTORS, MANAGING DIRECTOR, CEO AND OTHER EXECUTIVES:Directors: The bank’s directors are paid meeting allowances for taking part in meetings of committees and sub-committees as set up according to applicable rules at the rate of NPR 10,000 to the chairperson and NPR 8,000 to the members. Also, NPR 10,000 per month is being provided for media and daily newspapers for each board of directors. The bank has not provided the directors with any other facilities than the above. In FY 2071/72, NPR3,175,033 (In words, NPR 3.175 million) has been paid as meeting and media allowances to the directors.

Annual Salary, Allowances and services for CEO and other executives/ managers for the F/Y 2071/72:

Table – 4 Amount in NPR

S.No. Salary and services CEO Managers

1 Salary 4,584,711 32,687,198

2 Allowances 10,111,905

3 Provident Fund 458,471 3,268,720

4 Vehicle maintenance 705,973

5 Medical Treatment (annual + accumulated ) 2,151,280

6 Dashain Allowance 495,000 3,244,799

7 Leave (annual + accumulated) 506,437 7,285,996

8 Insurance - 2,127,726

9 Gratuity 11,240,044

10 Others

Total NPR 6,044,619 72,823,641 Note: The salary and services of CEO includes the amount received by the then CEO for the period of Shrawan 1, 2071 to Chaitra 17, 2071 only.

Kumari Bank | Annual Report 2015-2016 | 21

Other than above mentioned salary and allowances, other managers are also provided with following services:

1. Vehicle along with driver to the CEO; vehicle loan, driver, fuel, and repair and maintenance to ACEO and AGM ;and vehicle loan, fuel and repair expenses according to the bank’s policy on transportation vehicles to other management office bearers.

2. Home and real estate loans/ personal loans to all permanent office bearers as per the bank’s staff service regulations.

3. Journals, telephone and mobile facilities as per the bank’s human resource policy.

21. DIVIDEND YET TO BE TAKEN BY SHAREHOLDERS: Out of 12% cash dividend distributed in FY 2066/67 and 7% cash dividend distributed in FY 2068/69; the shareholders are yet to collect the remaining amount of NPR 7,839,484 (in words NPR 7.83 million) from the distributed cash dividend till Asadh end 2072.

22. DETAILS OF ASSET SALES AND PURCHASES AS PER SECTION 141 OF THE COMPANY ACT, 2063: None.

23. DETAILS OF BUSINESS WITH ASSOCIATED COMPANIES AS PER SECTION 175 OF THE COMPANY ACT, 2063:None.

24. ANY OTHER INFORMATION NECESSARY TO BE REVEALED IN THE DIRECTORS REPORT AS PER THE COMPANY ACT, 2063, AND APPLICABLE LAWS: None.

25. OTHER INFORMATION: The bank’s board of directors accepted the resignation of CEO, Udaya Krishna Upadhyay effective from date Chaitra 18, 2071.

Information regarding Merger:14th Annual General Meeting of the Bank had entrusted authority to the bank’s board of directors to seek for appropriate banks and financial institutions for merger and/or acquisition and proceed for merger and/or acquire by appointing auditor for the purpose of due diligence audit. In the same spirit, the bank had reached agreement for merger process with Nepal Credit and Commerce Bank Ltd, Infrastructure Development Bank Ltd, Apex Development Bank Ltd., Supreme Development Bank and International Development Bank Ltd. on Poush 29, 2072 and

had presented the same to Nepal Rastra Bank for principle approval. Chartered accountant firm P.Y.C. and associates is appointed as due diligence auditor for the valuation of the merging banks and financial institutions. Currently, the appointed audit firm is carrying its activities and had set forth target to accomplish the DDA process by the end of Asadh 2072.

Vote of Thanks:We would like to extend our heartfelt gratitude to respected shareholders, customers, executives from Nepal Rastra Bank, Office of Company Registrar, Nepal Securities Board, Nepal Stock Exchange Ltd., CDS & Clearing Ltd., general public and all other concerned who have continuously provided their support, encouragement and guidance. We would also like to thank our statutory auditor M/s Dev Associates for conducting the audit on time and providing the bank with realistic professional advice. In addition, we wish to thank the bank’s management and staff members for considering the bank’s progress to be their own by providing dedicated services. Finally, by incorporating as its main principle the fact that bank and its customers are two sides of the same coin, and that it is due to our customers’ affection and trust that the bank has succeeded in reaching its present position. We offer our heartfelt gratitude to them with the promise to be still more committed to increase our strong relationship with our customers in the future.

Thank You,On behalf of the Board of Directors

…….............…………………………Dr. Shobha Kant Dhakal

(Director)

…….............…………………………Santosh Kumar Lama

(Chairman)

Date: Falgun 3, 2072

| Kumari Bank | Annual Report 2015-201622

22

Kumari Bank | Annual Report 2015-2016 | 23

ACTING CHIEF EXECUTIVEOFFICER’S MESSAGEI am privileged to be leading Kumari Bank at this juncture on your behalf. I am fully aware of the responsibilities and the trust that you have bestowed upon me and the management team to lead the bank. I can assure you that our prime focus shall be in delivering the best results and taking the bank to newer heights.

Here, I would like to mention that your bank has been able to increase its deposit base by 21.19% totaling NPR 33.42 billion and loan amount by 18.69% totaling NPR 27.07 billion in the fiscal year 2071/72. The net profit has increased by 15.55% as compared to last FY. Other financial indicators have witnessed a marked improvement including Non-Performing Loan (NPL) ratio by virtue of our tenacity and concerted efforts in the recovery process. We have continuously tried to introduce norms to establish the robust risk management process in the bank.

During the review period, the bank provided continuity on product innovation and automation of services by focusing on Kumari Swastha Jeevan Bachat Khata, Kumari Remit Bachat Khata and Personal Loans and advances. In the review period, we have been able to increase our business through Kumari Remit and tie-ups with several renowned national and international companies. Presently, we are providing quality services through 38 points of representations and 46 ATMs throughout the country.

Kumari Bank has remained committed to strengthen Corporate Social Responsibility (CSR) whereby we have been providing sponsorships to under privileged children from rural parts of Nepal. The bank has also provided financial support of NPR 50,000.00 for education to Ms. Matina Shakya, Living Goddess Kumari every

year. While in the health sector, we are conducting health camps in those areas which are deprived of good medical facilities. The bank is also contributing to number of CSR activities related to education, health and environment. Moreover, the bank has supported the earthquake victims by distributing Galvanized sheets of value NPR 5,100,000.00 in Gorkha, Dhading, Sindhupalchowk and Nawalparasi. The bank has also provided financial support to Kumari Ghar, Basantapur, Kathmandu for NPR 500,000.00 only to repair of Kumari Ghar against damage caused due to devastating earthquake dated Baisakh 12, 2072.

As in the past years, we shall continue to elevate the bank’s stature through expertise and dedication of our staff members, constant guidance and support from the board, encouragement from our shareholders and support from the regulators and our valued customers.

I would also like to mention here that recently Mr. Santosh Kumar Lama has been positioned as Chairman of the bank; who had been shouldering the bank’s responsibilities as Director for a long time.

Finally, I take this opportunity to thank our valued shareholders, regulatory bodies, NRB, customers, employees and well-wishers for their continued trust and support.

With warm regards,Rajib Giri

Acting Chief Executive Officer

| Kumari Bank | Annual Report 2015-201624

24

Kumari Bank | Annual Report 2015-2016 | 25

MANAGEMENT TEAMSitting, CenterMr. Rajib Giri, Acting Chief Executive Officer

Standing in First Row (Left to Right)Mr. Binod N. Shrestha, Head - Central LogisticsMr. Rajesh Shrestha, Chief Marketing OfficerMr. Rameshwar Sharma Aryal, Chief Operating OfficerMr. Angir Man Singh, Chief Risk OfficerMr. Narayan P. Ghimire, Head – Information Technology

Standing in Second Row (Left to Right)Mr. Narendra P. Chhatkuli, Head – Legal, Compliance and Company SecretaryMr. Ajit P. Bhattarai, Branch Manager, New RoadMr. Bikas Khanal, Head – Corporate CreditMr. Ganesh Kumar K.C., Head – Internal AuditMr. Rohit Singh, Head – Human Resources

| Kumari Bank | Annual Report 2015-201626

26

More Responsible to Services

Kumari Bank | Annual Report 2015-2016 | 27

PRODUCT REVIEW

Kumari Big Savings KhataKumari Big Savings Khata as the name suggests, provides higher rate of interest amongst the saving category product & additional banking benefits. It is the premium saving account which provides higher rate of return and value added banking services to the saving accountholders.

Kumari Smart Bachat KhataKumari Smart Bachat Khata offers account opening facility at zero balance. We believe in providing banking access to all hence, this is a very suitable account for everyone. Besides the facility to open account in zero balance, the accountholders are offered various banking facilities.

Kumari SavingsKumari Savings account is a special saving account that beholds the corporate name after “Living Goddess Kumari”. The customers can avail various value added banking services in this account.

50 Plus SavingsAs the name suggests, this saving account is targeted to all the individuals of 50 years and above. Interest rate is calculated on daily balance and provided on quarterly basis. There are attractive features associated with this account like 25% discount on locker, ATM debit card, Internet/ Mobile banking facilities, etc.

Subha Laxmi SavingsThis saving account is especially designed for the women of 16 years and above. Attractive interest rate on daily balance is provided to encourage saving habit. Besides, other features like 50% discount in locker, ATM debit card, accidental death insurance and internet/ mobile banking facilities are also offered to the customers.

| Kumari Bank | Annual Report 2015-201628

28

PRODUCT REVIEW

Kumari Remit Bachat KhataKumari Remit Bachat Khata is a saving deposit product targeted to the migrant workers and their relatives. It is a service via which the account holders can send their hard earned money in a safe and secured way in their account and also send payment request to the bank for the payment of fund to the beneficiary (his/ her relative) against ID details.

Twinkle Star SavingsTwinkle Star Savings is a saving account targeted to the children 16 years and below. This is an ideal account for children to instill saving habit from a very young age. Account holders are offered interest on daily balance. Children receive special gifts at the time of account opening with Kumari Bank and are eligible for special discounts on education loan as per the bank’s rule.

Kumari Flexi-Fix SchemeKumari Flexi-Fix Scheme is specially designed based on hybrid concept of flexi-fix mechanism to attract retail deposits. The customer will be able to receive facilities of a saving deposit type and earn interest similar to that of fixed deposit type. The scheme is based on “standing order” whereby a condition is applied for those applying for the scheme. The product carries special features such as:

a. Maximum Returns – As soon as the balance in saving account exceeds NPR 100,000.00, the excess sum amount, in multiples of NPR 10,000.00 will be transferred automatically to a higher interest earning non-operative account (FD).

b. Maximum Liquidity - The money parked in non-operative account (FD) as a result of the sweep from saving account can be easily accessed by issuing a cheque or through ATM etc. The amount is reversed swept from non- operative account (FD) to saving whenever the balance in saving falls short of required available balance to be maintained at all time.

c. Auto renewal facility – The Flexibility to maintain fund in non-operative account (FD) at a higher rate, can be renewed for period of 1 year and above 1 year i.e. 2 years.

Kumari Bank | Annual Report 2015-2016 | 29

PRODUCT REVIEW

Kumari Swastha Jeevan Bachat Khata Kumari Swastha Jeevan Bachat Khata (KSJBK) is a saving deposit product being introduced to promote ‘saving habit’ and ‘good health’ amongst the people. This product is being introduced with value addition of medical benefits along with modern banking services for a differentiation.

The accountholders of this product will be provided a “co-branded VISA Debit card” with privileged services and discounts in Medanta, Medicity- New Delhi, India; Norvic Hospital, Grande Hospital, Vayodha Hospital and Chirayu National Hospital based in Kathmandu, Nepal. These partner hospitals have offered discounts from 5% to 20% to KSJBK account holders on several of its services when payment is made by co-branded debit card.

In addition, the account holders of KSJBK will also receive hospitalization insurance up to a sum of NPR. 10,000 per year for free. And they also receive internet banking, ABBS without any charges as well. While the minimum balance to open KSJBK is NPR. 5,000 which provides attractive interest rates.

KBL Recurring Deposit SchemeKBL Recurring Deposit Scheme is a deposit product specifically designed to meet the saving requirement of individual customers with regular income source for specific term period of 2 to 5 years. The customers can deposit specific sum of fund on regular basis for pre-determined time period or open ended terms (in case of Institutions’ Provident Fund Deposit scheme). Major attraction of this product is the interest rate and implementation of planned or forced saving habit.

Kumari Salary Saving AccountKumari Salary Saving Account (KSSA) is a saving product specially designed for individuals with regular income (salaried people). The product focuses on making the product hassle free, easy, affordable and yet benefiting individual KSS accountholder NPR High interest rate and attractive banking service package are the key benefits provided in this product.

| Kumari Bank | Annual Report 2015-201630

30

CSR ACTIVITIES &SME FINANCING

Celebrating Global Money Week 2015

Scholarship program for ‘living goddess Kumari’ of Kathmandu on the occasion of its 14th anniversary, in order to give continuity to her further education. The amount of NPR 50,000.00 will be deposited every year in her saving account and upon her retirement, a lump sum amount will be granted to her for education purpose.

Jasta pata distribution in Dhading to support earthquake victims

Jasta pata distribution in Gorkha to support earthquake victims Jasta pata distribution in Nawalparasi to support earthquake victims

Kumari Bank | Annual Report 2015-2016 | 31

Krishi Sahakari Sangh Limited, Nawalparasi – Financed by Kumari Bank Ltd. Support to Kumari Ghar of NPR 500,000.00 only to renovate Kumari Ghar for destruction caused due to devastating earthquake & NPR 5,100,000.00 only for earthquake victims.

Jasta pata distribution in Sindhupalchowk to support earthquake victims Health Camp conduction in association with Indrawatee Community Service Centre (ICSC).

Kumari Bank Employees Union organized “Blood Donation Program” on the occasion of Bank’s 15th anniversary.

Kumari Bank Limited conducted ‘Financial LiteracyTraining’ in coordination with Nepal Banking Institute (NBI) as a part of its CSR activity in Budhanilkantha.Around 55 people were benefited from the training including staffs from various cooperatives and other local people of Budhanilkantha area.

More Responsible Via Network

| Kumari Bank | Annual Report 2015-201634

34

More Responsible in Technology

Kumari Bank | Annual Report 2015-2016 | 35

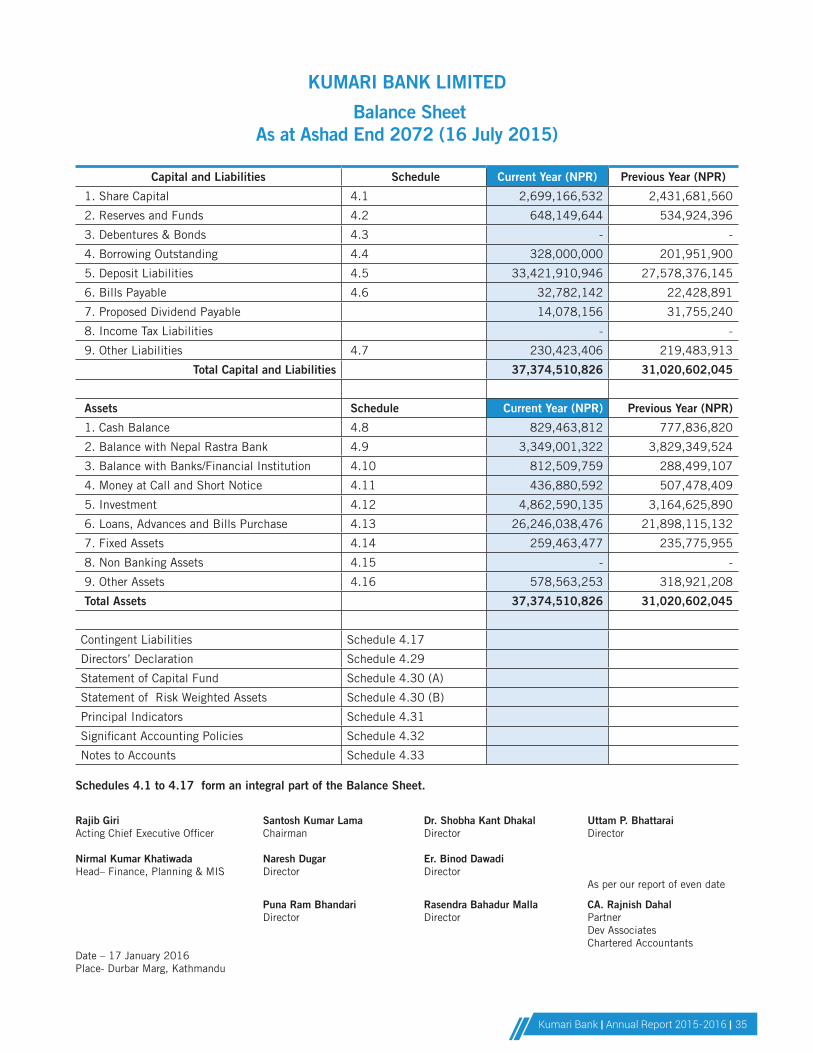

Capital and Liabilities Schedule Current Year (NPR) Previous Year (NPR)

1. Share Capital 4.1 2,699,166,532 2,431,681,560

2. Reserves and Funds 4.2 648,149,644 534,924,396

3. Debentures & Bonds 4.3 - -

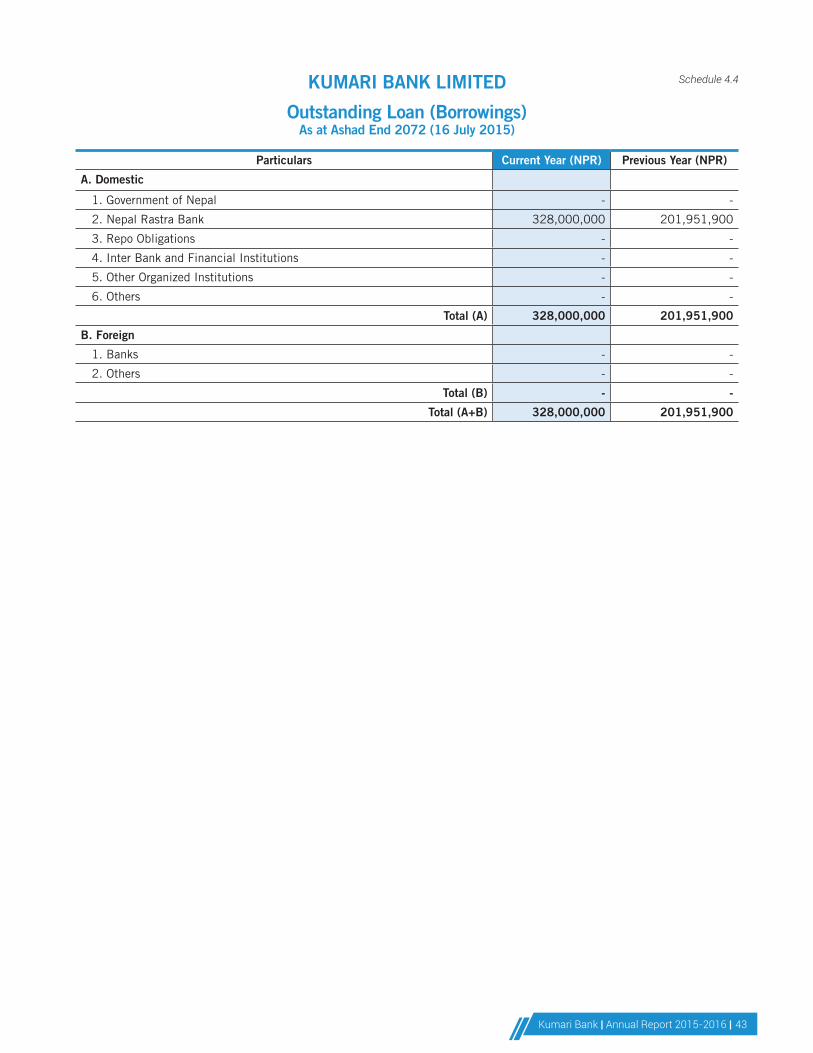

4. Borrowing Outstanding 4.4 328,000,000 201,951,900

5. Deposit Liabilities 4.5 33,421,910,946 27,578,376,145

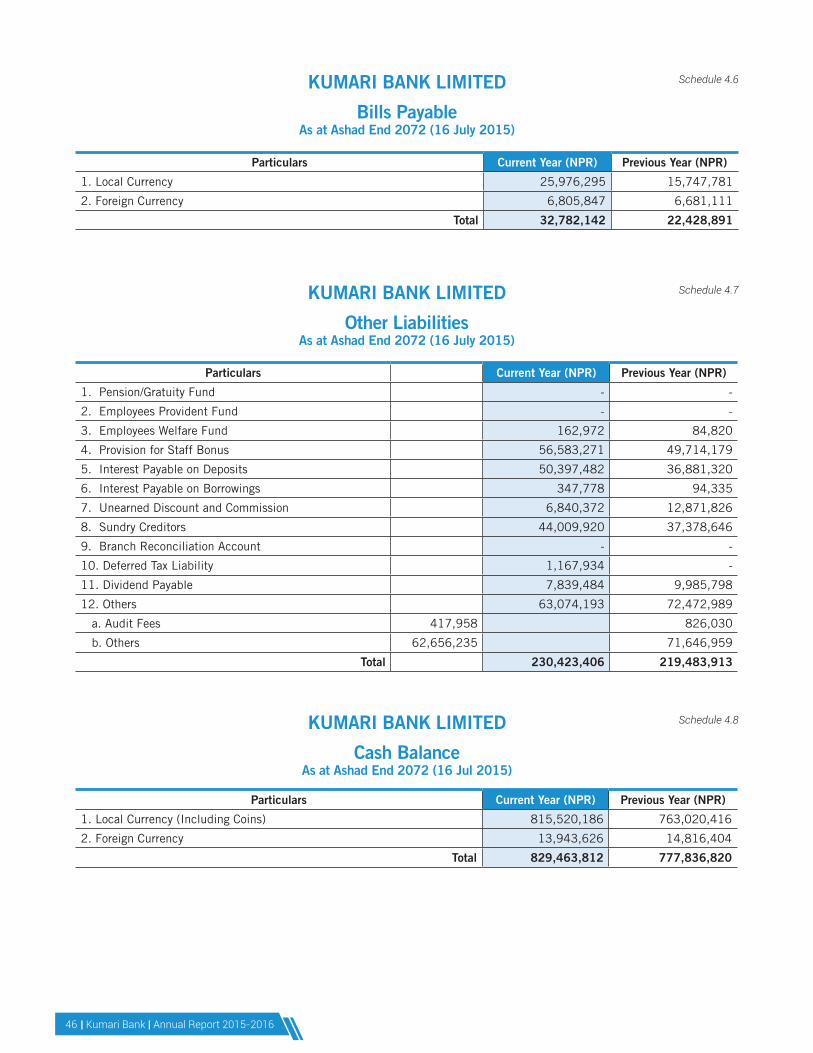

6. Bills Payable 4.6 32,782,142 22,428,891

7. Proposed Dividend Payable 14,078,156 31,755,240

8. Income Tax Liabilities - -

9. Other Liabilities 4.7 230,423,406 219,483,913

Total Capital and Liabilities 37,374,510,826 31,020,602,045

Assets Schedule Current Year (NPR) Previous Year (NPR)

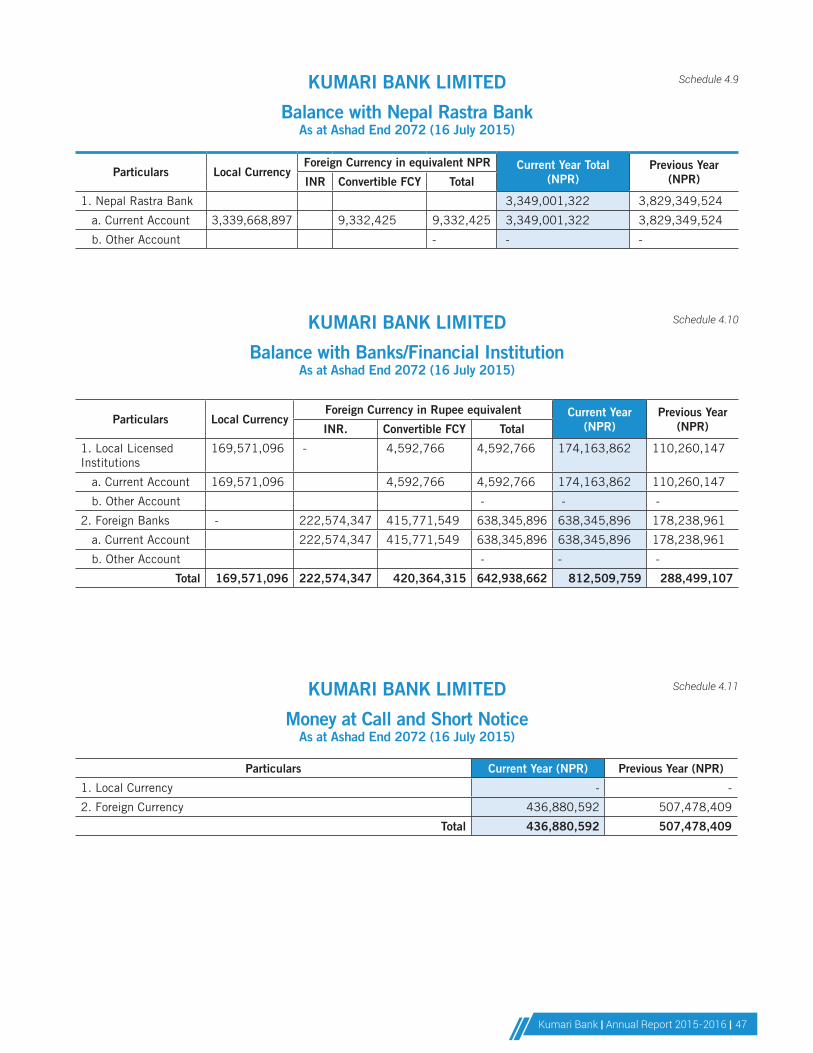

1. Cash Balance 4.8 829,463,812 777,836,820

2. Balance with Nepal Rastra Bank 4.9 3,349,001,322 3,829,349,524

3. Balance with Banks/Financial Institution 4.10 812,509,759 288,499,107

4. Money at Call and Short Notice 4.11 436,880,592 507,478,409

5. Investment 4.12 4,862,590,135 3,164,625,890

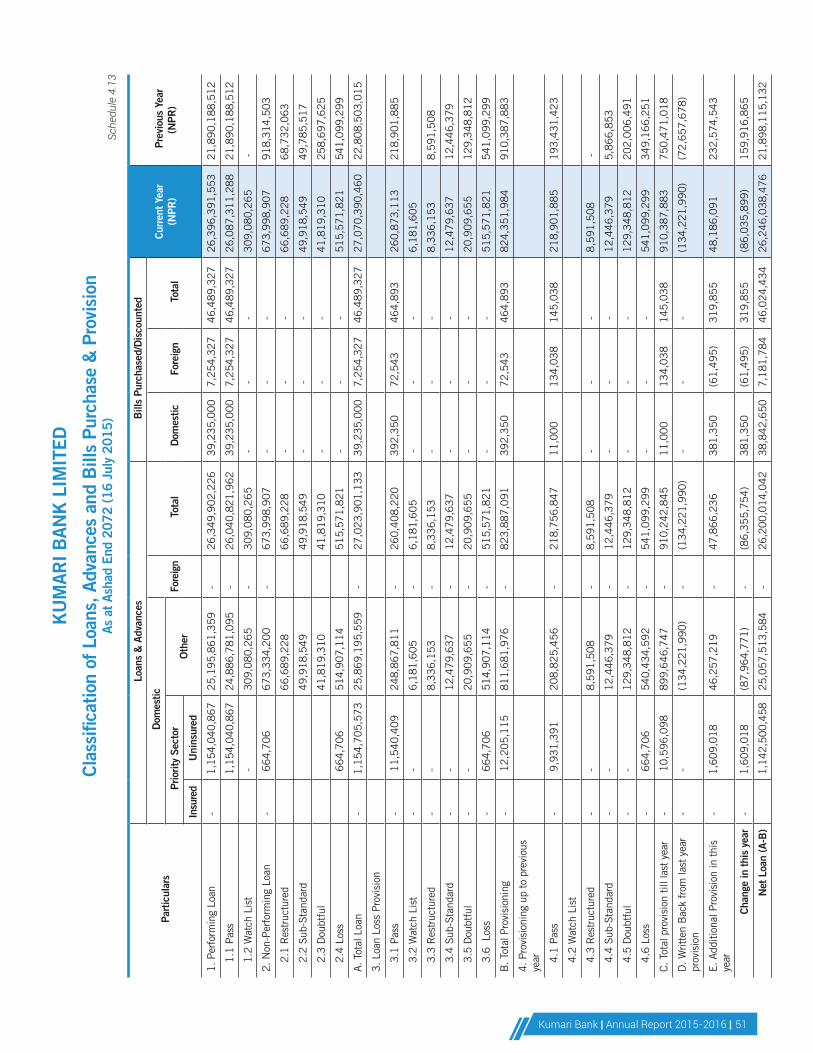

6. Loans, Advances and Bills Purchase 4.13 26,246,038,476 21,898,115,132

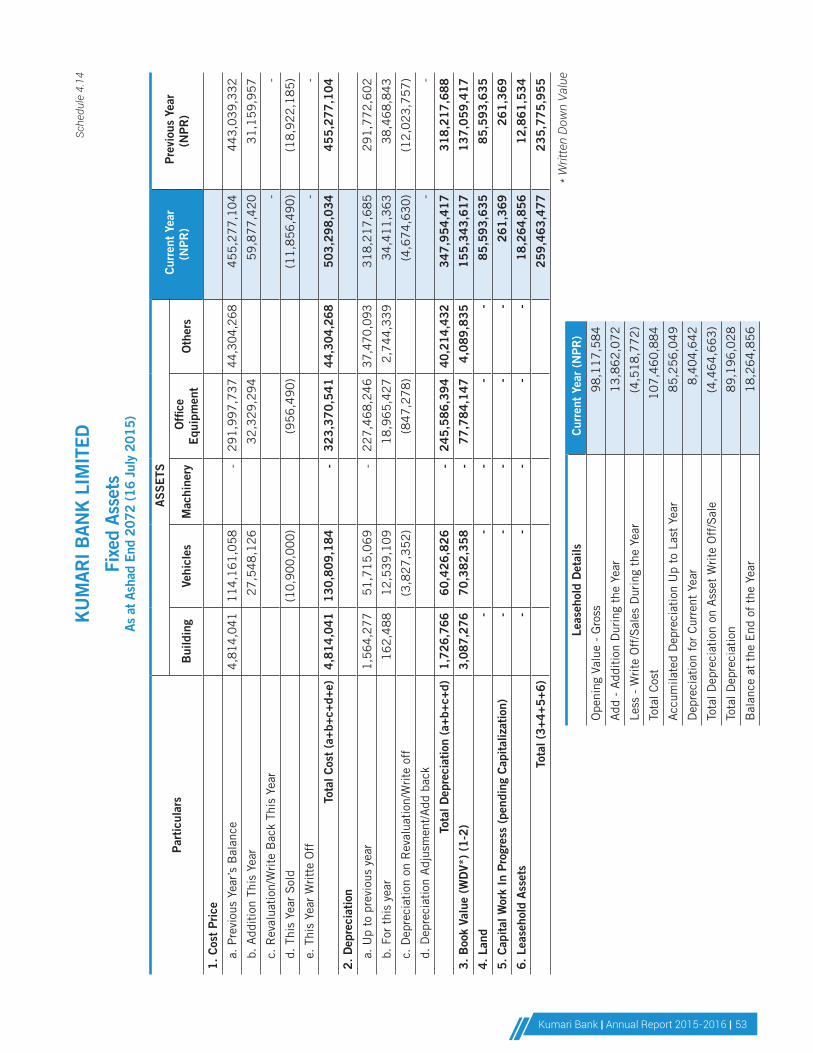

7. Fixed Assets 4.14 259,463,477 235,775,955

8. Non Banking Assets 4.15 - -

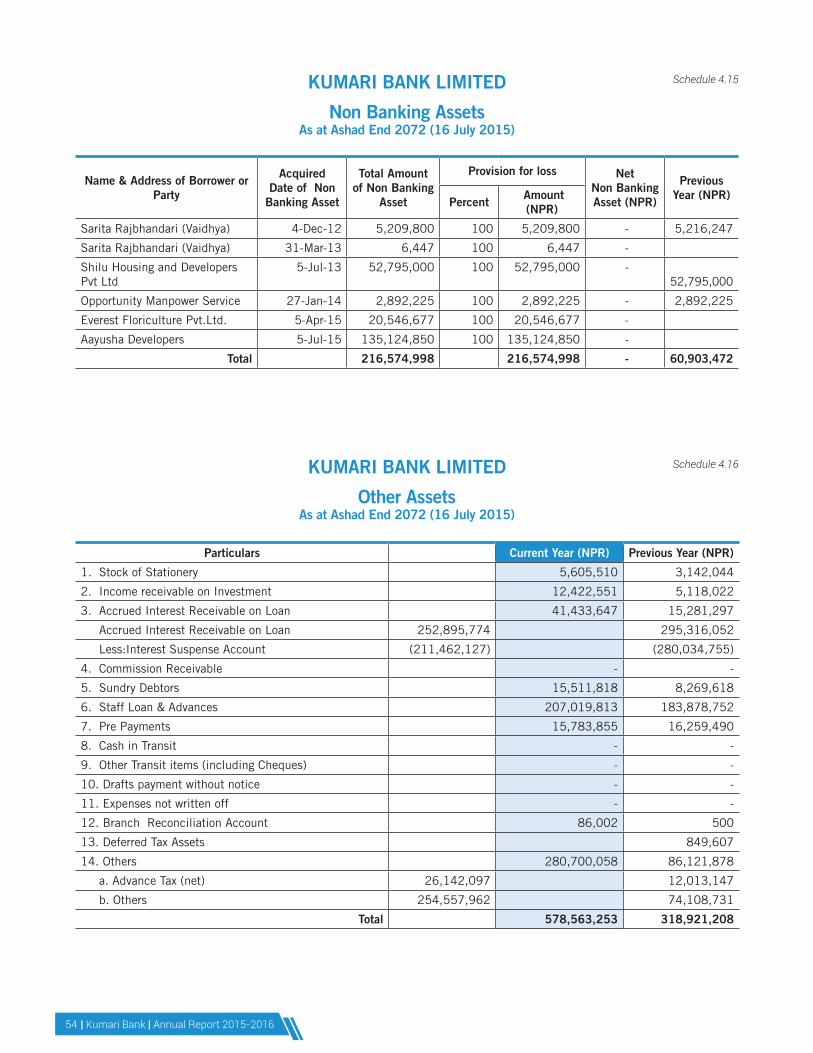

9. Other Assets 4.16 578,563,253 318,921,208

Total Assets 37,374,510,826 31,020,602,045

Contingent Liabilities Schedule 4.17

Directors’ Declaration Schedule 4.29

Statement of Capital Fund Schedule 4.30 (A)

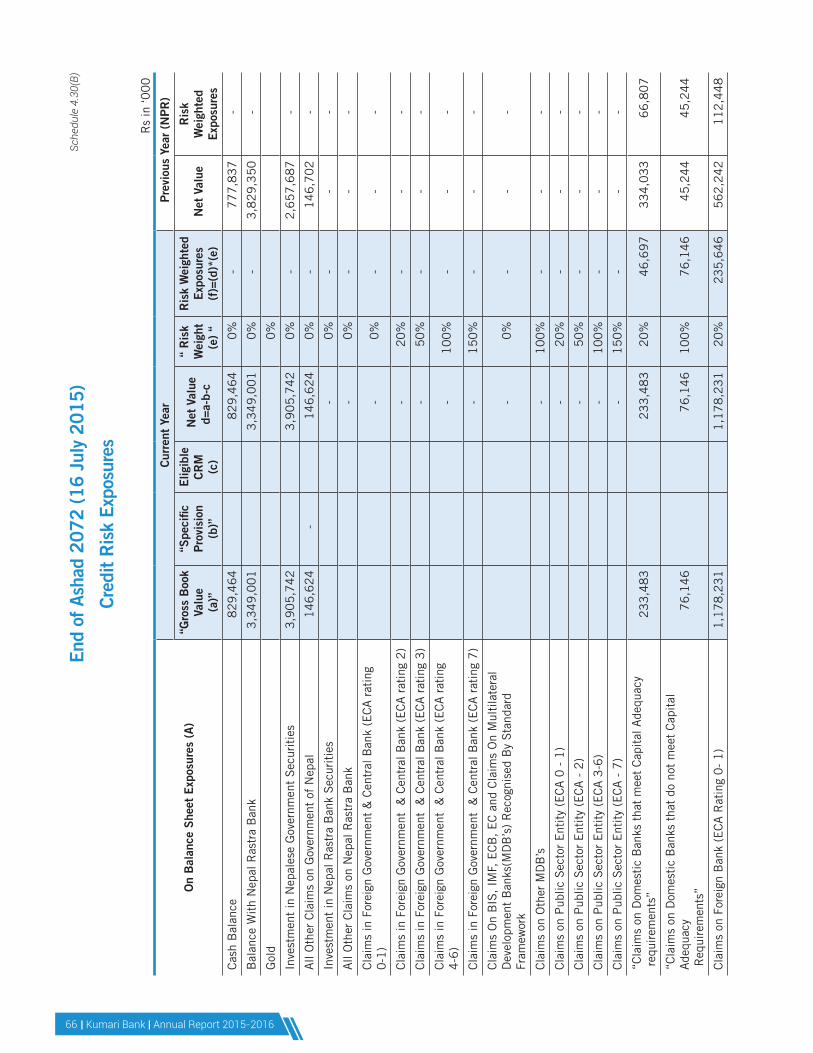

Statement of Risk Weighted Assets Schedule 4.30 (B)

Principal Indicators Schedule 4.31

Significant Accounting Policies Schedule 4.32

Notes to Accounts Schedule 4.33

KUMARI BANK LIMITED

Balance Sheet As at Ashad End 2072 (16 July 2015)

Schedules 4.1 to 4.17 form an integral part of the Balance Sheet.

Rajib Giri Santosh Kumar Lama Dr. Shobha Kant Dhakal Uttam P. Bhattarai Acting Chief Executive Officer Chairman Director Director

Nirmal Kumar Khatiwada Naresh Dugar Er. Binod DawadiHead– Finance, Planning & MIS Director Director As per our report of even date

Puna Ram Bhandari Rasendra Bahadur Malla CA. Rajnish Dahal Director Director Partner Dev Associates Chartered Accountants Date – 17 January 2016Place- Durbar Marg, Kathmandu

| Kumari Bank | Annual Report 2015-201636

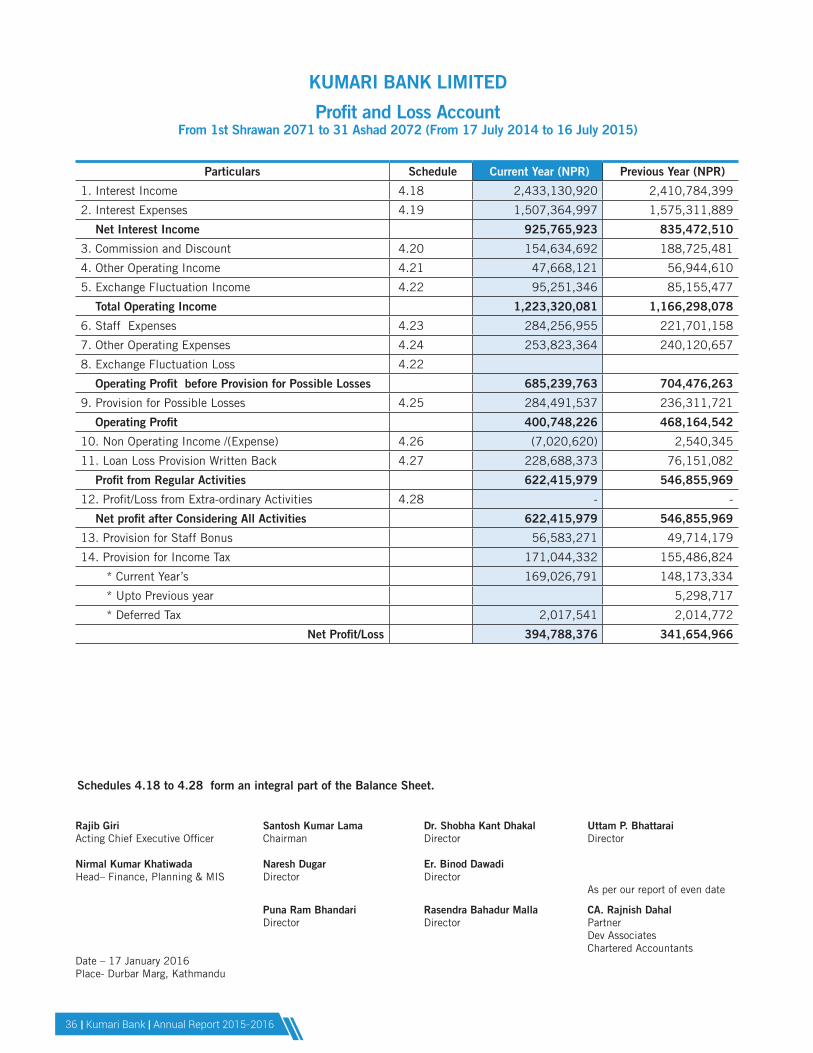

Particulars Schedule Current Year (NPR) Previous Year (NPR)

1. Interest Income 4.18 2,433,130,920 2,410,784,399

2. Interest Expenses 4.19 1,507,364,997 1,575,311,889

Net Interest Income 925,765,923 835,472,510

3. Commission and Discount 4.20 154,634,692 188,725,481

4. Other Operating Income 4.21 47,668,121 56,944,610

5. Exchange Fluctuation Income 4.22 95,251,346 85,155,477

Total Operating Income 1,223,320,081 1,166,298,078

6. Staff Expenses 4.23 284,256,955 221,701,158

7. Other Operating Expenses 4.24 253,823,364 240,120,657

8. Exchange Fluctuation Loss 4.22

Operating Profit before Provision for Possible Losses 685,239,763 704,476,263

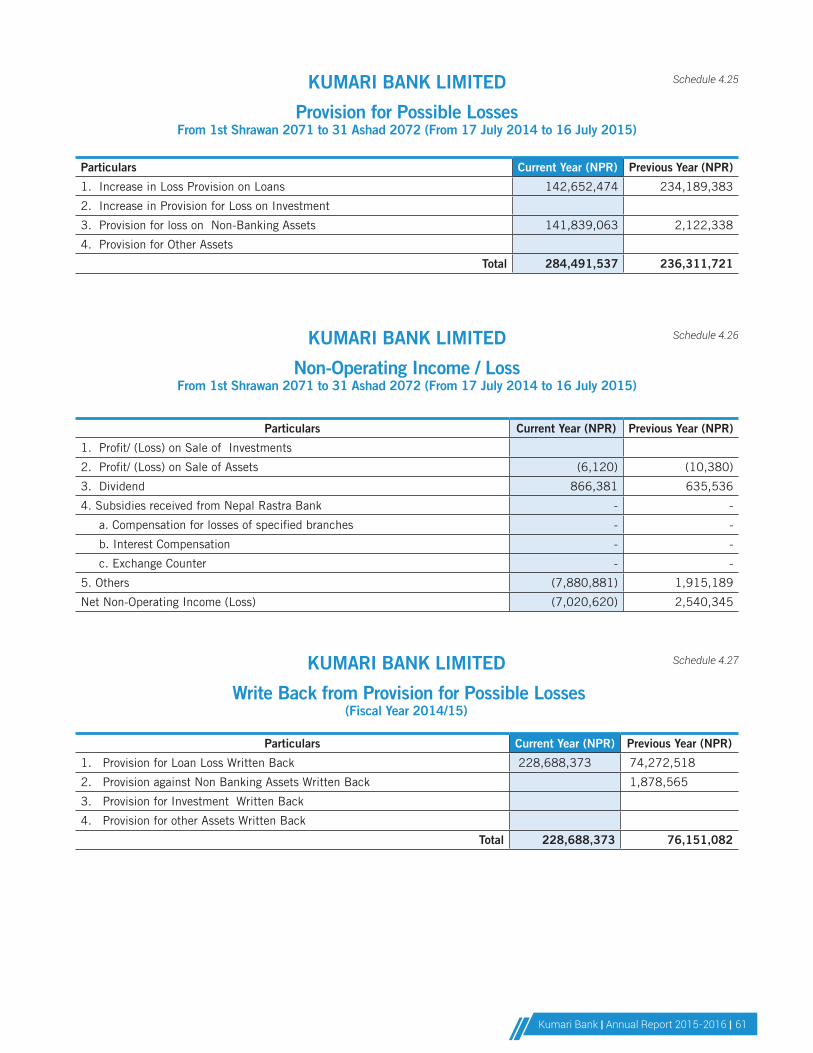

9. Provision for Possible Losses 4.25 284,491,537 236,311,721

Operating Profit 400,748,226 468,164,542

10. Non Operating Income /(Expense) 4.26 (7,020,620) 2,540,345

11. Loan Loss Provision Written Back 4.27 228,688,373 76,151,082

Profit from Regular Activities 622,415,979 546,855,969

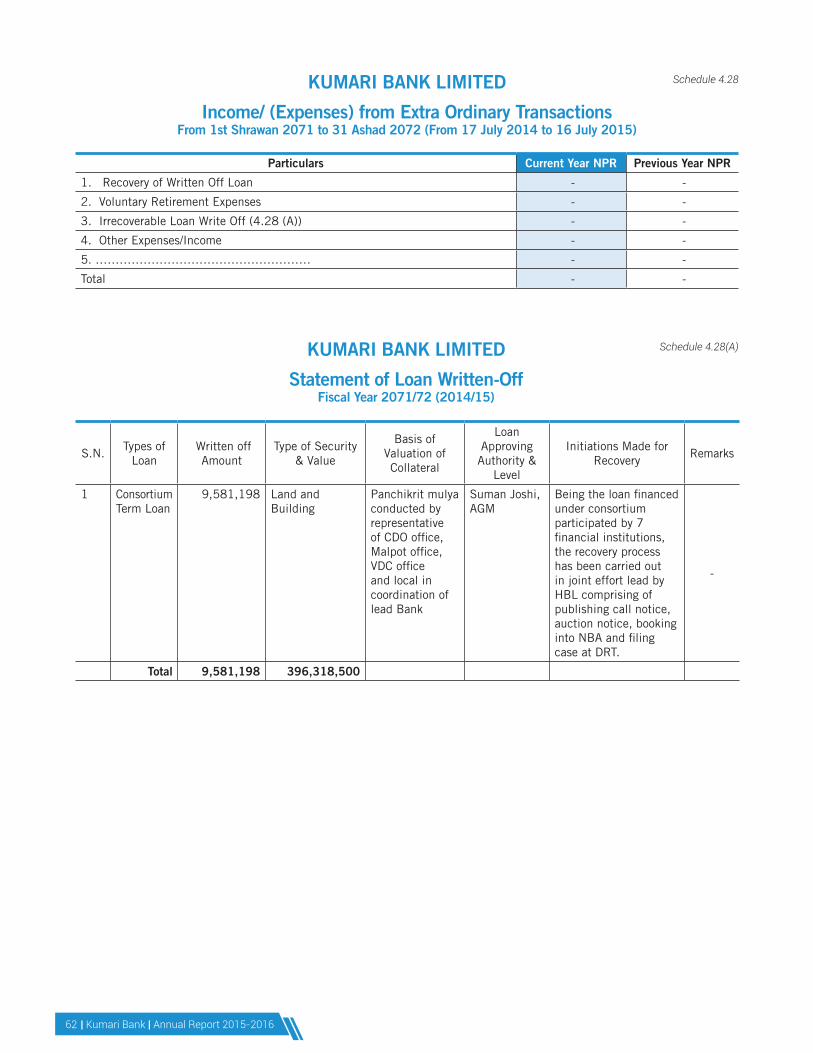

12. Profit/Loss from Extra-ordinary Activities 4.28 - -

Net profit after Considering All Activities 622,415,979 546,855,969

13. Provision for Staff Bonus 56,583,271 49,714,179

14. Provision for Income Tax 171,044,332 155,486,824

* Current Year’s 169,026,791 148,173,334

* Upto Previous year 5,298,717

* Deferred Tax 2,017,541 2,014,772

Net Profit/Loss 394,788,376 341,654,966

KUMARI BANK LIMITED

Profit and Loss AccountFrom 1st Shrawan 2071 to 31 Ashad 2072 (From 17 July 2014 to 16 July 2015)

Schedules 4.18 to 4.28 form an integral part of the Balance Sheet.

Rajib Giri Santosh Kumar Lama Dr. Shobha Kant Dhakal Uttam P. Bhattarai Acting Chief Executive Officer Chairman Director Director

Nirmal Kumar Khatiwada Naresh Dugar Er. Binod DawadiHead– Finance, Planning & MIS Director Director As per our report of even date

Puna Ram Bhandari Rasendra Bahadur Malla CA. Rajnish Dahal Director Director Partner Dev Associates Chartered Accountants Date – 17 January 2016Place- Durbar Marg, Kathmandu

Kumari Bank | Annual Report 2015-2016 | 37

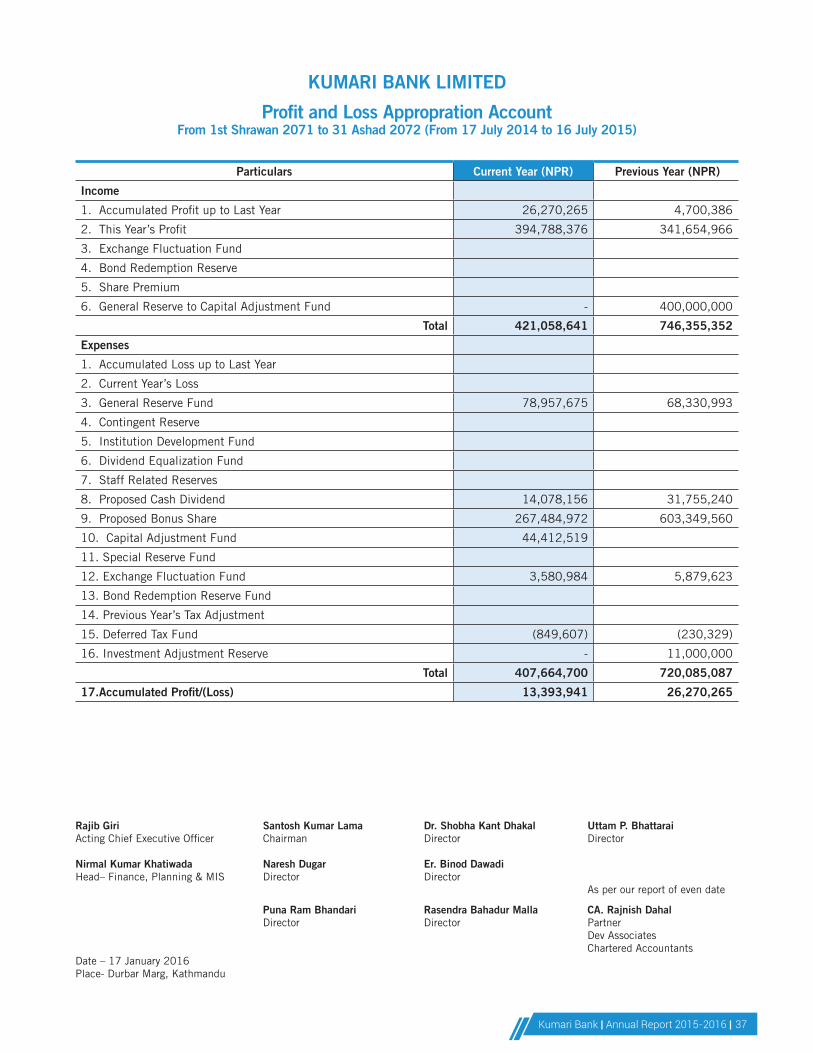

KUMARI BANK LIMITED

Profit and Loss Appropration AccountFrom 1st Shrawan 2071 to 31 Ashad 2072 (From 17 July 2014 to 16 July 2015)

Particulars Current Year (NPR) Previous Year (NPR)

Income

1. Accumulated Profit up to Last Year 26,270,265 4,700,386

2. This Year’s Profit 394,788,376 341,654,966

3. Exchange Fluctuation Fund

4. Bond Redemption Reserve

5. Share Premium

6. General Reserve to Capital Adjustment Fund - 400,000,000

Total 421,058,641 746,355,352

Expenses

1. Accumulated Loss up to Last Year

2. Current Year’s Loss

3. General Reserve Fund 78,957,675 68,330,993

4. Contingent Reserve

5. Institution Development Fund

6. Dividend Equalization Fund

7. Staff Related Reserves

8. Proposed Cash Dividend 14,078,156 31,755,240

9. Proposed Bonus Share 267,484,972 603,349,560

10. Capital Adjustment Fund 44,412,519

11. Special Reserve Fund

12. Exchange Fluctuation Fund 3,580,984 5,879,623

13. Bond Redemption Reserve Fund

14. Previous Year’s Tax Adjustment

15. Deferred Tax Fund (849,607) (230,329)

16. Investment Adjustment Reserve - 11,000,000

Total 407,664,700 720,085,087

17.Accumulated Profit/(Loss) 13,393,941 26,270,265

Rajib Giri Santosh Kumar Lama Dr. Shobha Kant Dhakal Uttam P. Bhattarai Acting Chief Executive Officer Chairman Director Director

Nirmal Kumar Khatiwada Naresh Dugar Er. Binod DawadiHead– Finance, Planning & MIS Director Director As per our report of even date

Puna Ram Bhandari Rasendra Bahadur Malla CA. Rajnish Dahal Director Director Partner Dev Associates Chartered Accountants Date – 17 January 2016Place- Durbar Marg, Kathmandu

| Kumari Bank | Annual Report 2015-201638

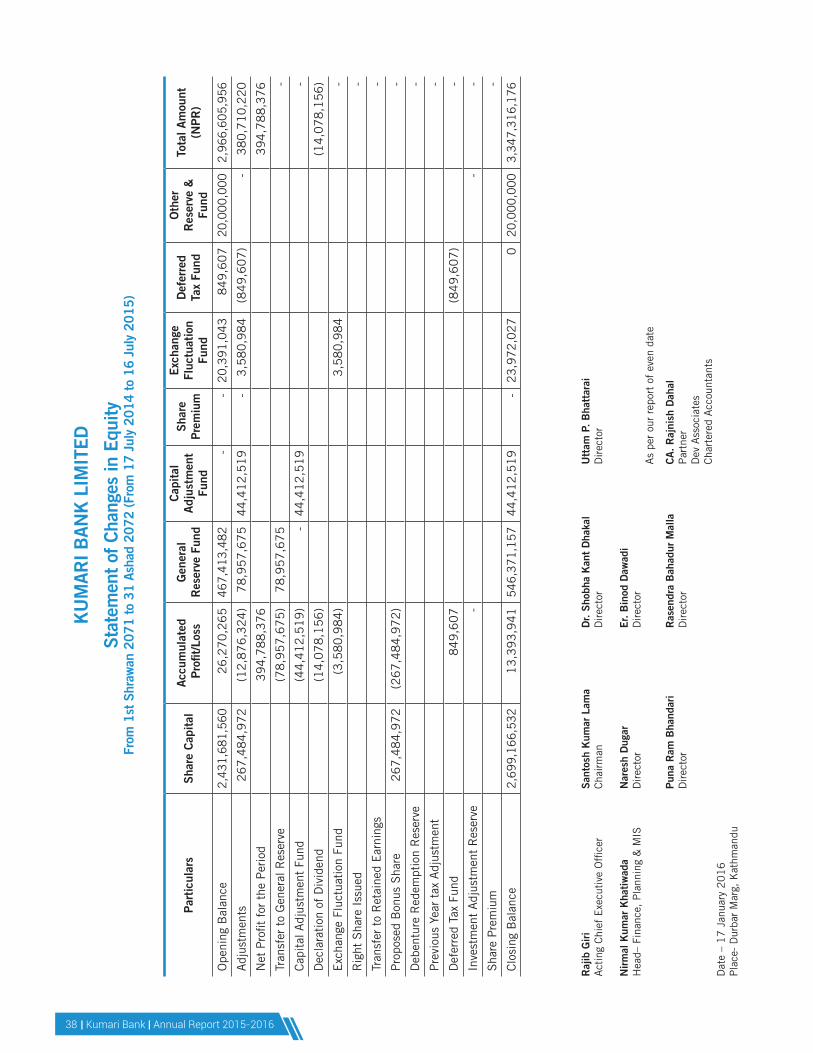

KU

MAR

I BAN

K L

IMIT

ED

Stat

emen

t of C

hang

es in

Equ

ityFr

om 1

st S

hraw

an 2

071

to 3

1 As

had

2072

(Fro

m 1

7 Ju

ly 2

014

to 1

6 Ju

ly 2

015)

Par

ticu

lars

S

hare

Cap

ital

A

ccum

ulat

ed

Pro

fit/L

oss

Gen

eral

R

eser

ve F

und

Cap

ital

A

djus

tmen

t Fu

nd

Sha

re

Prem

ium

Exc

hang

e

Fluc

tuat

ion

Fund

Def

erre

d Ta

x Fu

nd

Oth

er

Res

erve

&

Fund

Tota

l Am

ount

(N

PR

)

Ope

ning

Bal

ance

2,

431,

681,

560

2

6,2

70

,26

5

467,

413,

482

-

-

20,3

91,0

43

8

49

,60

7

20,0

00,0

00

2,96

6,60

5,95

6

Adj

ustm

ents

2

67

,48

4,9

72

(

12

,87

6,3

24

)7

8,9

57

,67

5

44

,41

2,5

19

-

3

,58

0,9

84

(

84

9,6

07

) -

3

80

,71

0,2

20

Net

Pro

fit f

or t

he P

erio

d 3

94

,78

8,3

76

3

94

,78

8,3

76

Tran

sfer

to

Gen

eral

Res

erve

(

78

,95

7,6

75

)7

8,9

57

,67

5

-

Cap

ital

Adj

ustm

ent

Fund

(

44

,41

2,5

19

) -

4

4,4

12

,51

9

-

Dec

lara

tion

of

Div

iden

d (

14

,07

8,1

56

)(1

4,0

78

,15

6)

Exc

hang

e Fl

uctu

atio

n Fu

nd

(3

,58

0,9

84

)3

,58

0,9

84

-

Rig

ht S

hare

Iss

ued

-

Tran

sfer

to

Ret

aine

d E

arni

ngs

-

Pro

pose

d B

onus

Sha

re

26

7,4

84

,97

2

(2

67

,48

4,9

72

) -

Deb

entu

re R

edem

ptio

n R

eser

ve

-

Pre

viou

s Ye

ar t

ax A

djus

tmen

t -

Def

erre

d Ta

x Fu

nd

84

9,6

07

(8

49

,60

7)

-

Inve

stm

ent

Adj

ustm

ent

Res

erve

-

-

-

Sha

re P

rem

ium

-

Clo

sing

Bal

ance

2,

699,

166,

532

1

3,3

93

,94

1

546,

371,

157

4

4,4

12

,51

9

-

23,9

72,0

27

0

20

,000

,000

3,

347,

316,

176

Raj

ib G

iri

San

tosh

Kum

ar L

ama

Dr.

Sho

bha

Kan

t D

haka

l U

ttam

P.

Bha

ttar

ai

Act

ing

Chi

ef E

xecu

tive

Offi

cer

Cha

irm

an

Dir

ecto

r D

irec

tor

Nir

mal

Kum

ar K

hati

wad

a

Nar

esh

Dug

ar

Er.

Bin

od D

awad

iH

ead–

Fin

ance

, P

lann

ing

& M

IS

Dir

ecto

r

Dir

ecto

r

As

per

our

repo

rt o

f ev

en d

ate

P

una

Ram

Bha

ndar

i R

asen

dra

Bah

adur

Mal

la

CA

. R

ajni

sh D

ahal

Dir

ecto

r D

irec

tor

Par

tner

Dev

Ass

ocia

tes

C

hart

ered

Acc

ount

ants

D

ate

– 1

7 J

anua

ry 2

01

6P

lace

- D

urba

r M

arg,

Kat

hman

du

Kumari Bank | Annual Report 2015-2016 | 39

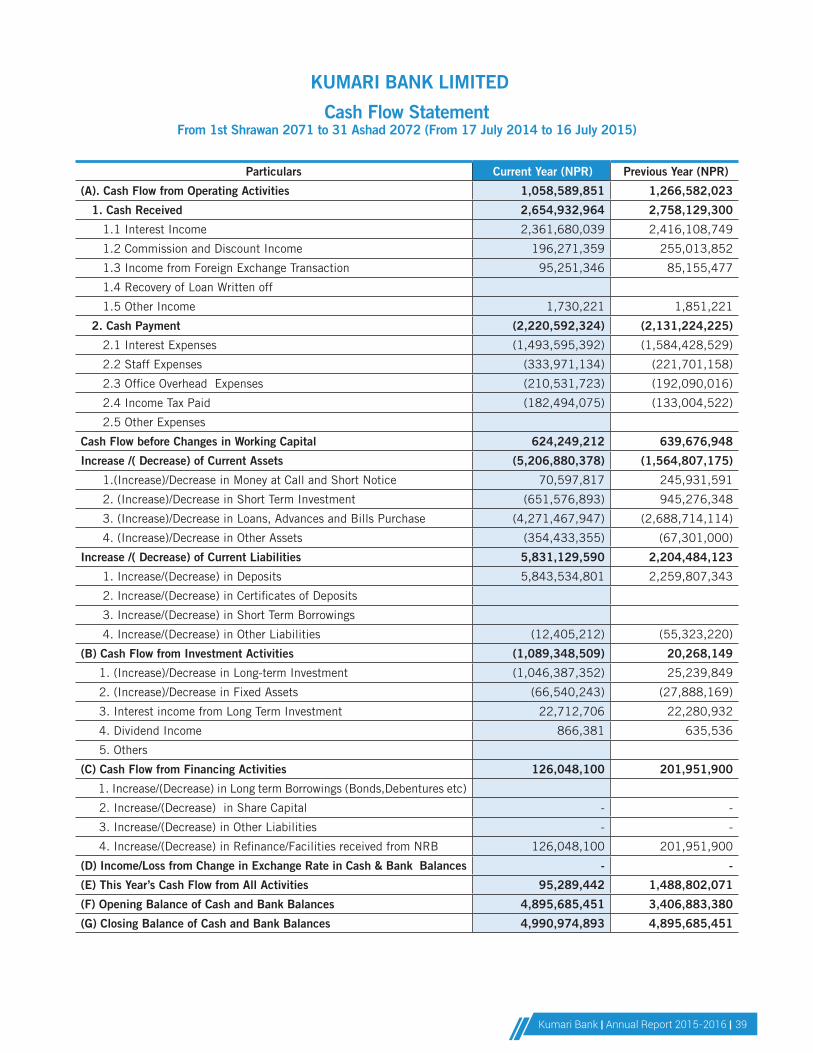

Particulars Current Year (NPR) Previous Year (NPR)

(A). Cash Flow from Operating Activities 1,058,589,851 1,266,582,023

1. Cash Received 2,654,932,964 2,758,129,300

1.1 Interest Income 2,361,680,039 2,416,108,749

1.2 Commission and Discount Income 196,271,359 255,013,852

1.3 Income from Foreign Exchange Transaction 95,251,346 85,155,477

1.4 Recovery of Loan Written off

1.5 Other Income 1,730,221 1,851,221

2. Cash Payment (2,220,592,324) (2,131,224,225)

2.1 Interest Expenses (1,493,595,392) (1,584,428,529)

2.2 Staff Expenses (333,971,134) (221,701,158)

2.3 Office Overhead Expenses (210,531,723) (192,090,016)

2.4 Income Tax Paid (182,494,075) (133,004,522)

2.5 Other Expenses

Cash Flow before Changes in Working Capital 624,249,212 639,676,948

Increase /( Decrease) of Current Assets (5,206,880,378) (1,564,807,175)

1.(Increase)/Decrease in Money at Call and Short Notice 70,597,817 245,931,591

2. (Increase)/Decrease in Short Term Investment (651,576,893) 945,276,348

3. (Increase)/Decrease in Loans, Advances and Bills Purchase (4,271,467,947) (2,688,714,114)

4. (Increase)/Decrease in Other Assets (354,433,355) (67,301,000)

Increase /( Decrease) of Current Liabilities 5,831,129,590 2,204,484,123

1. Increase/(Decrease) in Deposits 5,843,534,801 2,259,807,343

2. Increase/(Decrease) in Certificates of Deposits

3. Increase/(Decrease) in Short Term Borrowings

4. Increase/(Decrease) in Other Liabilities (12,405,212) (55,323,220)

(B) Cash Flow from Investment Activities (1,089,348,509) 20,268,149

1. (Increase)/Decrease in Long-term Investment (1,046,387,352) 25,239,849

2. (Increase)/Decrease in Fixed Assets (66,540,243) (27,888,169)

3. Interest income from Long Term Investment 22,712,706 22,280,932

4. Dividend Income 866,381 635,536

5. Others

(C) Cash Flow from Financing Activities 126,048,100 201,951,900

1. Increase/(Decrease) in Long term Borrowings (Bonds,Debentures etc)

2. Increase/(Decrease) in Share Capital - -

3. Increase/(Decrease) in Other Liabilities - -

4. Increase/(Decrease) in Refinance/Facilities received from NRB 126,048,100 201,951,900

(D) Income/Loss from Change in Exchange Rate in Cash & Bank Balances - -

(E) This Year’s Cash Flow from All Activities 95,289,442 1,488,802,071

(F) Opening Balance of Cash and Bank Balances 4,895,685,451 3,406,883,380

(G) Closing Balance of Cash and Bank Balances 4,990,974,893 4,895,685,451

KUMARI BANK LIMITED

Cash Flow StatementFrom 1st Shrawan 2071 to 31 Ashad 2072 (From 17 July 2014 to 16 July 2015)

| Kumari Bank | Annual Report 2015-201640

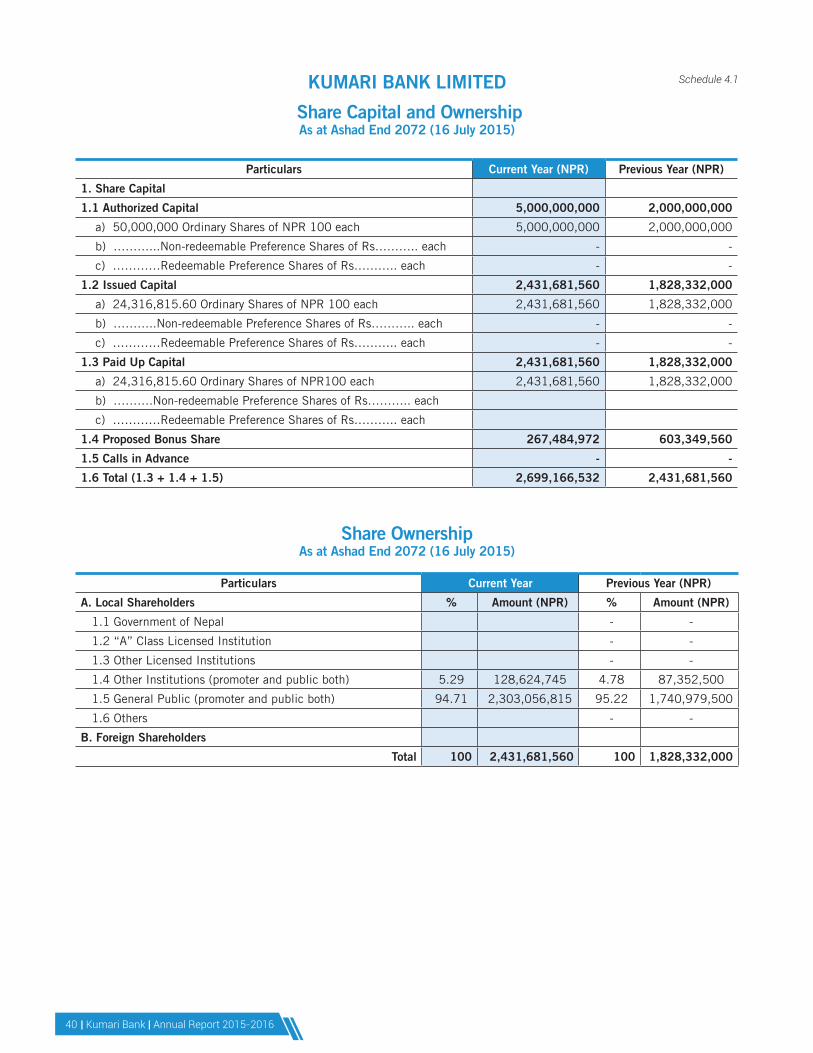

Particulars Current Year (NPR) Previous Year (NPR)

1. Share Capital

1.1 Authorized Capital 5,000,000,000 2,000,000,000

a) 50,000,000 Ordinary Shares of NPR 100 each 5,000,000,000 2,000,000,000

b) ………...Non-redeemable Preference Shares of Rs……….. each - -

c) …………Redeemable Preference Shares of Rs……….. each - -

1.2 Issued Capital 2,431,681,560 1,828,332,000

a) 24,316,815.60 Ordinary Shares of NPR 100 each 2,431,681,560 1,828,332,000

b) ………..Non-redeemable Preference Shares of Rs……….. each - -

c) …………Redeemable Preference Shares of Rs……….. each - -

1.3 Paid Up Capital 2,431,681,560 1,828,332,000

a) 24,316,815.60 Ordinary Shares of NPR100 each 2,431,681,560 1,828,332,000

b) ……….Non-redeemable Preference Shares of Rs……….. each

c) …………Redeemable Preference Shares of Rs……….. each

1.4 Proposed Bonus Share 267,484,972 603,349,560

1.5 Calls in Advance - -

1.6 Total (1.3 + 1.4 + 1.5) 2,699,166,532 2,431,681,560

KUMARI BANK LIMITED

Share Capital and OwnershipAs at Ashad End 2072 (16 July 2015)

Schedule 4.1

Particulars Current Year Previous Year (NPR)