fgmc seller guide - fgmc correspondent correspondent seller guide.… · 7.2.11 underwriting...

TRANSCRIPT

Correspondent Lending

Seller Guide

Effective Date: 12/10/2015

Last Updated: 6/1/2018

First Guaranty Mortgage Corporation ®

Version 1.9 Correspondent Lending Seller Guide 2 CONFIDENTIAL DOCUMENT First Guaranty Mortgage Corporation must give prior written permission for this work, or any part thereof, to be used, reproduced, or transmitted in any form or by any means, by or to any party outside of First Guaranty Mortgage Corporation, its regulators and investors.

Document is Not Legal or Compliance Advice This document should not be construed as legal or compliance advice. FGMC encourages Correspondents to consult with their legal and/or compliance counsel for any legal or compliance matters.

Document Version Matrix Version Changes Date

1.0 Initial Version Finalized 12/21/2015 1.1 Update 01/19/2016 1.2 Update 04/15/2016 1.3 Update 07/28/2016 1.4 Update 10/25/2016 1.5 Update 01/30/2017 1.6 Update 05/10/2017 1.7 Update 07/31/2017 1.8 Update 08/30/2017 1.9 Update 02/27/2018 2.0 Update 05/01/2018 2.1 Update 06/01/2018

First Guaranty Mortgage Corporation ®

Version 1.9 Correspondent Lending Seller Guide 3 CONFIDENTIAL DOCUMENT First Guaranty Mortgage Corporation must give prior written permission for this work, or any part thereof, to be used, reproduced, or transmitted in any form or by any means, by or to any party outside of First Guaranty Mortgage Corporation, its regulators and investors.

1 INTRODUCTION ............................................................................................................... 8

1.1 Purpose............................................................................................................................. 8 1.2 Applicability ...................................................................................................................... 8 1.3 Correspondent Lending .................................................................................................... 8 1.4 Correspondent Loan Process ........................................................................................... 8

2 GETTING STARTED ........................................................................................................... 8

2.1 Overview .......................................................................................................................... 8 2.2 Approval ........................................................................................................................... 8 2.3 Setup .............................................................................................................................. 10

2.3.1 Resources ................................................................................................................ 10 2.3.1.1 FGMC Correspondent Website ........................................................................... 10 2.3.1.2 Portal Training ..................................................................................................... 10 2.3.1.3 Loan Submission .................................................................................................. 10 2.3.1.4 Submitting Files for Underwriting ....................................................................... 11 2.3.1.5 General Information ............................................................................................ 11 2.3.1.6 Pricing .................................................................................................................. 12 2.3.1.7 Original Collateral/Notes ..................................................................................... 12 2.3.1.8 Final Documents .................................................................................................. 12 2.3.1.9 Compliance .......................................................................................................... 12 2.3.1.10 Important Addresses ........................................................................................... 12

3 CORRESPONDENT ELIGIBILITY ........................................................................................ 13

3.1 Overview ........................................................................................................................ 13 3.2 Eligibility ......................................................................................................................... 13

3.2.1 Requirements .......................................................................................................... 13 3.3 Approval Levels .............................................................................................................. 14

3.3.1 Loan Purchase Eligibility ......................................................................................... 14 3.3.2 FHA Loan Purchase Eligibility .................................................................................. 14

3.4 Maintaining Eligibility ..................................................................................................... 15 3.4.1 Notification of Significant Changes ......................................................................... 15 3.4.2 Changes to Corporate Authority and Banking Relationships ................................. 15 3.4.3 Compliance Reporting Requirements ..................................................................... 15 3.4.4 Periodic Reviews ..................................................................................................... 16 3.4.5 Early Payoff Remedies ............................................................................................ 16 3.4.6 Audits ...................................................................................................................... 16 3.4.7 Correspondent Annual Recertification ................................................................... 16 3.4.8 Financial Statement Delivery Requirements .......................................................... 17

3.5 Loan Defects ................................................................................................................... 17 3.5.1 Early Payment Default ............................................................................................ 17 3.5.2 Loan Defects Detected ............................................................................................ 17

4 CREDIT PARAMETERS .................................................................................................... 17

4.1 Overview ........................................................................................................................ 17 4.2 Product Options ............................................................................................................. 17 4.3 Exclusionary Lists ............................................................................................................ 17

First Guaranty Mortgage Corporation ®

Version 1.9 Correspondent Lending Seller Guide 4 CONFIDENTIAL DOCUMENT First Guaranty Mortgage Corporation must give prior written permission for this work, or any part thereof, to be used, reproduced, or transmitted in any form or by any means, by or to any party outside of First Guaranty Mortgage Corporation, its regulators and investors.

5 APPRAISAL REQUIREMENTS .......................................................................................... 18

5.1 Overview ........................................................................................................................ 18 5.2 Correspondent Certification........................................................................................... 18 5.3 Appraisal Requirements ................................................................................................. 18 5.4 Enhanced Appraisal Requirements ................................................................................ 19

6 COMMITMENT POLICY/LOAN LOCKS ............................................................................. 19

6.1 Overview ........................................................................................................................ 19 6.2 Best Efforts/Mandatory Locks ........................................................................................ 20

6.2.1 Best Efforts Definition ............................................................................................. 20 6.2.2 Mandatory Lock Definition ..................................................................................... 20 6.2.3 Service Release Premium ........................................................................................ 20 6.2.4 Loan Registration .................................................................................................... 20

6.2.4.1 Lock Confirmations .............................................................................................. 20 6.2.4.2 Off-Sheet Pricing Request ................................................................................... 21 6.2.4.3 Duplicate Locks .................................................................................................... 21 6.2.4.4 Fallout .................................................................................................................. 21 6.2.4.5 Lock Periods ........................................................................................................ 21 6.2.4.6 Lock Expiration Date............................................................................................ 22 6.2.4.7 Lock Extensions ................................................................................................... 22 6.2.4.8 Relocks ................................................................................................................. 22 6.2.4.9 Renegotiations .................................................................................................... 23 6.2.4.10 Pair-Offs via Mandatory Rate Sheet Locks .......................................................... 23 6.2.4.11 Canceling Mandatory Locks via Rate Sheet ........................................................ 23 6.2.4.12 Swaps on Mandatory Locks via Rate Sheet ......................................................... 24 6.2.4.13 FGMC Mandatory Trade Desk ............................................................................. 24 6.2.4.14 Trade Confirmations ............................................................................................ 24 6.2.4.15 Delivery Timeframes ........................................................................................... 24 6.2.4.16 Delivery Tolerance ............................................................................................... 24

6.2.5 Settlement Dates .................................................................................................... 24 6.2.6 Roll/Extension Fees ................................................................................................. 25 6.2.7 Roll/Extension Periods ............................................................................................ 25 6.2.8 Pair Offs Calculations .............................................................................................. 25

7 DELIVERY PROCEDURES ................................................................................................. 26

7.1 Overview ........................................................................................................................ 27 7.1.1 Document Upload ................................................................................................... 27 7.1.2 Purchasable Form ................................................................................................... 28 7.1.3 Collateral Package ................................................................................................... 28 7.1.4 Uniform Closing Dataset (UCD) Requirements ....................................................... 29

7.2 Closed Loan Documentation .......................................................................................... 29 7.2.1 Ability to Repay and Qualified Mortgage Rule ....................................................... 29 7.2.2 Required Forms and Reference Data ...................................................................... 30 7.2.3 Bailee Specifications ............................................................................................... 30 7.2.4 General Closing Specifications ................................................................................ 30 7.2.5 Note Endorsement .................................................................................................. 31

First Guaranty Mortgage Corporation ®

Version 1.9 Correspondent Lending Seller Guide 5 CONFIDENTIAL DOCUMENT First Guaranty Mortgage Corporation must give prior written permission for this work, or any part thereof, to be used, reproduced, or transmitted in any form or by any means, by or to any party outside of First Guaranty Mortgage Corporation, its regulators and investors.

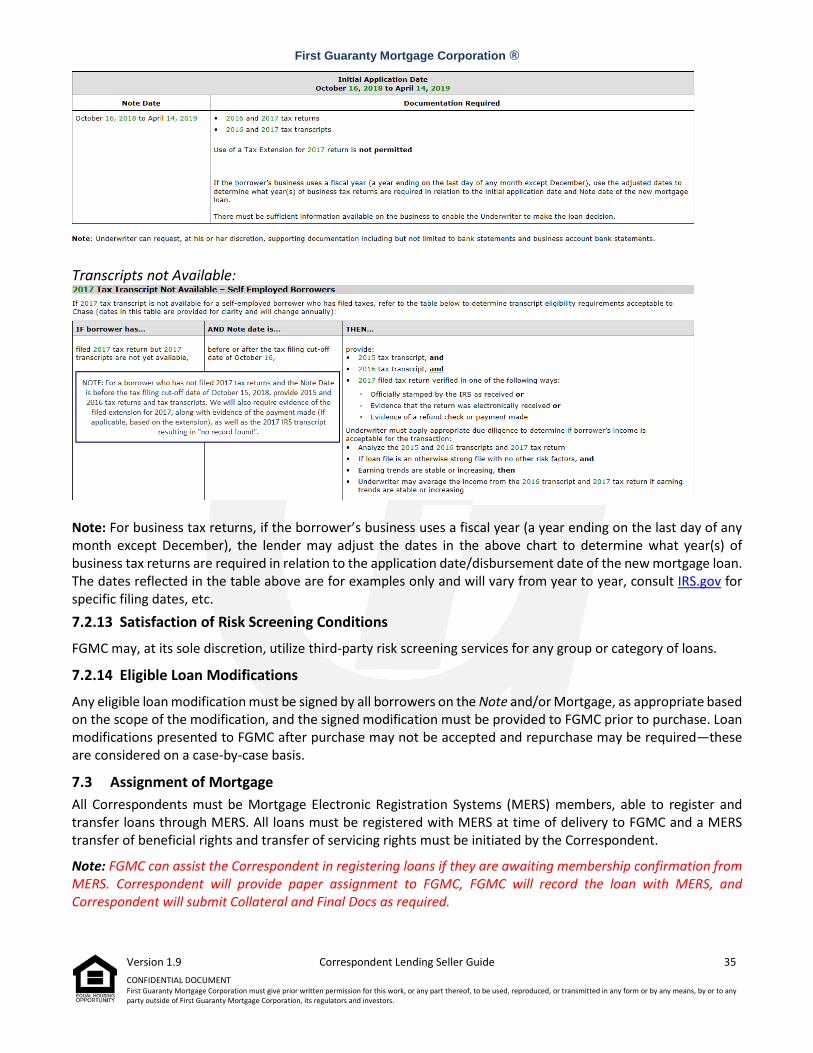

7.2.6 Due-On Sale Clause ................................................................................................. 31 7.2.7 Initial Application Date ........................................................................................... 31 7.2.8 Late Charge ............................................................................................................. 31 7.2.9 Mortgagee Clause ................................................................................................... 31 7.2.10 HUD-1 Settlement Statement/Closing Disclosure .................................................. 32 7.2.11 Underwriting Conditions ......................................................................................... 32 7.2.12 Tax Requirements ................................................................................................... 32 7.2.13 Satisfaction of Risk Screening Conditions ............................................................... 35 7.2.14 Eligible Loan Modifications ..................................................................................... 35

7.3 Assignment of Mortgage ................................................................................................ 35 7.4 Mortgage Loan Purchase ............................................................................................... 36

7.4.1 Calculation of Purchase Proceeds ........................................................................... 36 7.4.2 Decline to Purchase ................................................................................................ 37 7.4.3 Principal Balance Purchased ................................................................................... 37 7.4.4 Accrued Interest ...................................................................................................... 37 7.4.5 Interest Credits at Closing ....................................................................................... 37 7.4.6 Escrow Waiver Fees ................................................................................................ 37 7.4.7 Power of Attorney (POA) ........................................................................................ 38 7.4.8 Trust Review Guidelines ......................................................................................... 38 7.4.9 Signature Specifications .......................................................................................... 39 7.4.10 New York Consolidation, Extension & Modification Agreement (NY CEMA) ......... 40

7.5 Title Insurance Specifications ......................................................................................... 40 7.6 Private Mortgage Insurance ........................................................................................... 41 7.7 Hazard Insurance ............................................................................................................ 42

7.7.1 Hazard Insurance General Specifications ............................................................... 42 7.7.2 Types of Hazard Insurance Coverage ...................................................................... 42 7.7.3 Amount of Hazard Insurance Coverage .................................................................. 43 7.7.4 Hazard Insurance Deductible .................................................................................. 43 7.7.5 Additional Hazard Insurance Coverage ................................................................... 43 7.7.6 Special Endorsements ............................................................................................. 44

7.8 Flood Insurance .............................................................................................................. 45 7.8.1 Non-Participating Communities.............................................................................. 45 7.8.2 Flood Determination Certification .......................................................................... 45 7.8.3 Required Documentation ....................................................................................... 45 7.8.4 Elevation Certificate ................................................................................................ 46 7.8.5 Required Coverage .................................................................................................. 46 7.8.6 Deductible Amount ................................................................................................. 46

7.9 Disaster Policy ................................................................................................................ 47 7.9.1 Determining Affected Areas ................................................................................... 47 7.9.2 Valuation Requirements for Property in Affected Areas ........................................ 47 7.9.3 Valuation and Inspection Requirements ................................................................ 47 7.9.4 Current Disaster Updates........................................................................................ 48

7.10 Real Estate Taxes ............................................................................................................ 48 7.11 Escrow/Impound Accounts ............................................................................................ 48

7.11.1 Escrow Waiver ........................................................................................................ 49

First Guaranty Mortgage Corporation ®

Version 1.9 Correspondent Lending Seller Guide 6 CONFIDENTIAL DOCUMENT First Guaranty Mortgage Corporation must give prior written permission for this work, or any part thereof, to be used, reproduced, or transmitted in any form or by any means, by or to any party outside of First Guaranty Mortgage Corporation, its regulators and investors.

7.12 Loan Sale Notification .................................................................................................... 49 7.12.1 Due Dates ................................................................................................................ 49 7.12.2 Borrower Notification ............................................................................................. 49 7.12.3 Servicing Information .............................................................................................. 50 7.12.4 Vendor Notifications ............................................................................................... 50 7.12.5 Payment Processing Requirements ........................................................................ 51 7.12.6 Non-Sufficient Funds ............................................................................................... 51 7.12.7 Corporate Advances/Invoice Requirements ........................................................... 51 7.12.8 Wire Instructions..................................................................................................... 51 7.12.9 MERS/Transfer of Mortgage Instructions ............................................................... 52 7.12.10 Hazard Insurance .................................................................................................... 52 7.12.11 Tax Instructions ....................................................................................................... 52 7.12.12 PMI & MIP Instructions ........................................................................................... 53 7.12.13 Escrows ................................................................................................................... 53

7.13 Final Documents ............................................................................................................. 54 7.13.1 Delivery ................................................................................................................... 54 7.13.2 Shipping Procedures ............................................................................................... 55 7.13.3 Recovery .................................................................................................................. 55 7.13.4 Government Insuring Documents........................................................................... 55 7.13.5 Government Insuring Delivery ................................................................................ 56 7.13.6 Final Title Policy Delivery ........................................................................................ 56 7.13.7 Billing ....................................................................................................................... 57

7.14 Reporting ........................................................................................................................ 57 7.15 Responsible Lending ....................................................................................................... 57 7.16 Funding Fees................................................................................................................... 57 7.17 Non-Delegated Loan Delivery ........................................................................................ 57

7.17.1 Non-Delegated Setup .............................................................................................. 58 7.17.2 Loan Package........................................................................................................... 58 7.17.3 Loan Programs ........................................................................................................ 58 7.17.4 Package Review ....................................................................................................... 60 7.17.5 Credit Denials .......................................................................................................... 60 7.17.6 Clear to Close .......................................................................................................... 61

7.18 Renovation and Construction Loan Programs ............................................................... 62 7.19 Property Value for Loans Sold More than Four Months from Note Date ..................... 62

8 Appendix ...................................................................................................................... 63

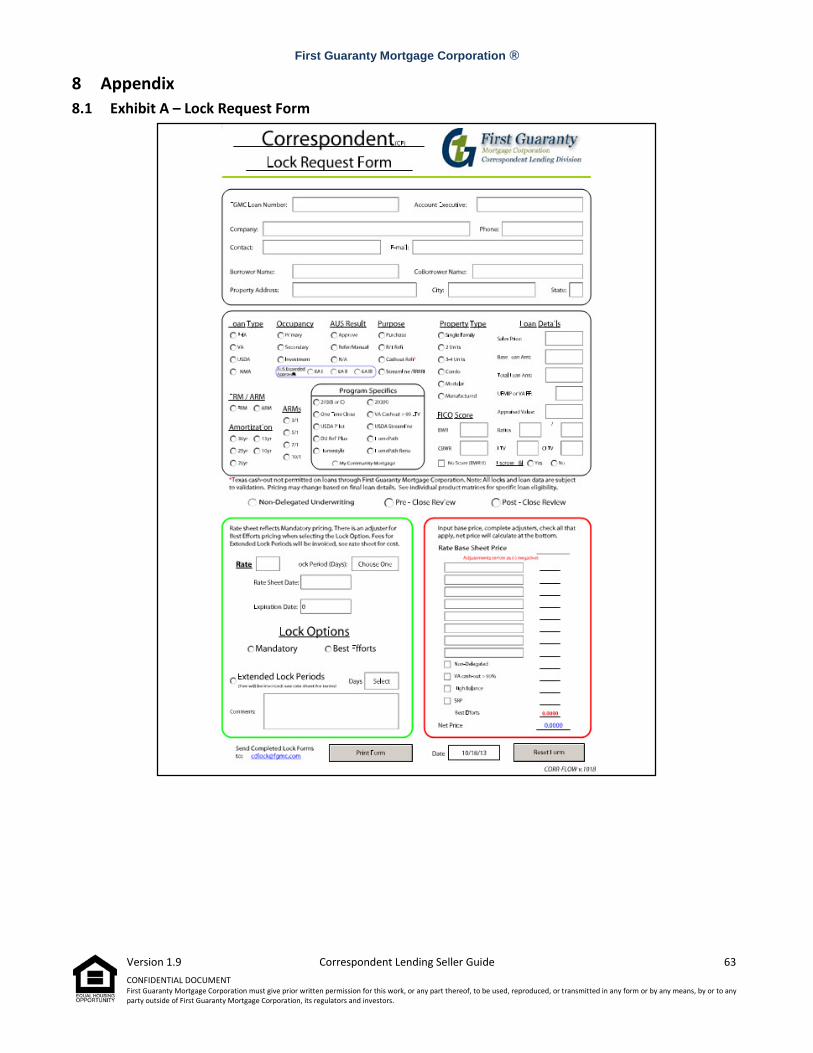

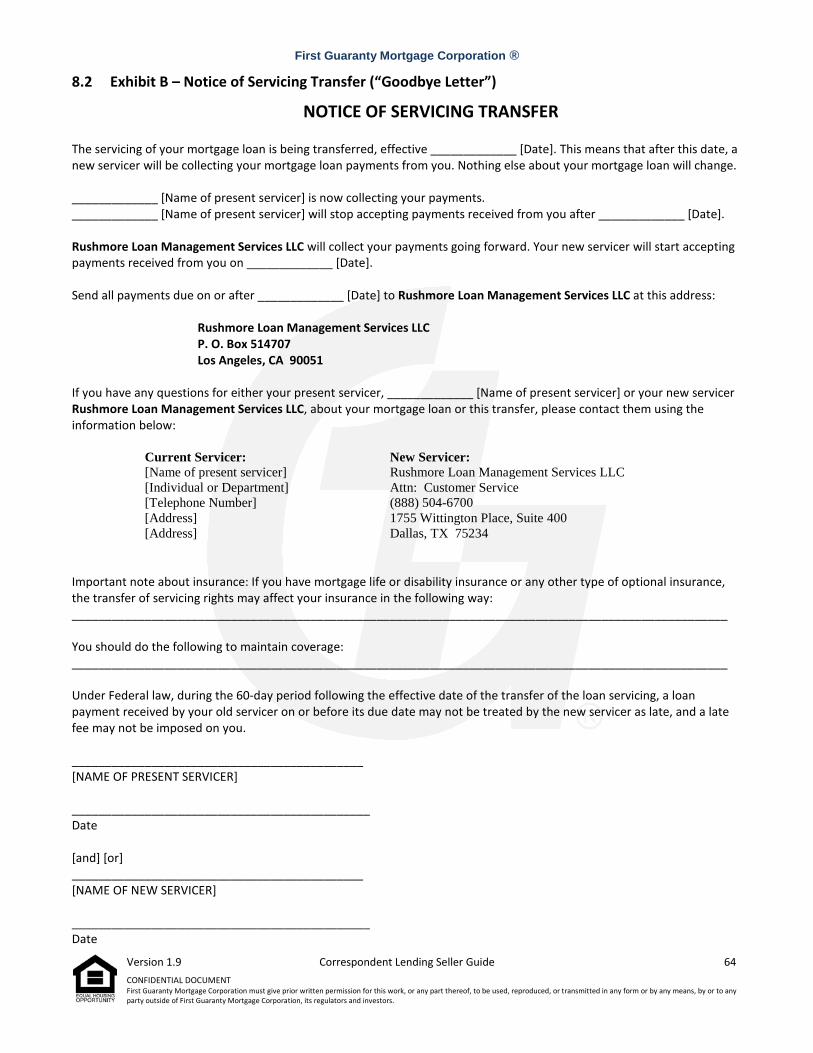

8.1 Exhibit A – Lock Request Form ....................................................................................... 63 8.2 Exhibit B – Notice of Servicing Transfer (“Goodbye Letter”) ......................................... 64 8.3 Exhibit C – Final Documents Transmittal ....................................................................... 65 8.4 Exhibit D – Non-Delegated Correspondent Checklists/Stacking Orders ........................ 66

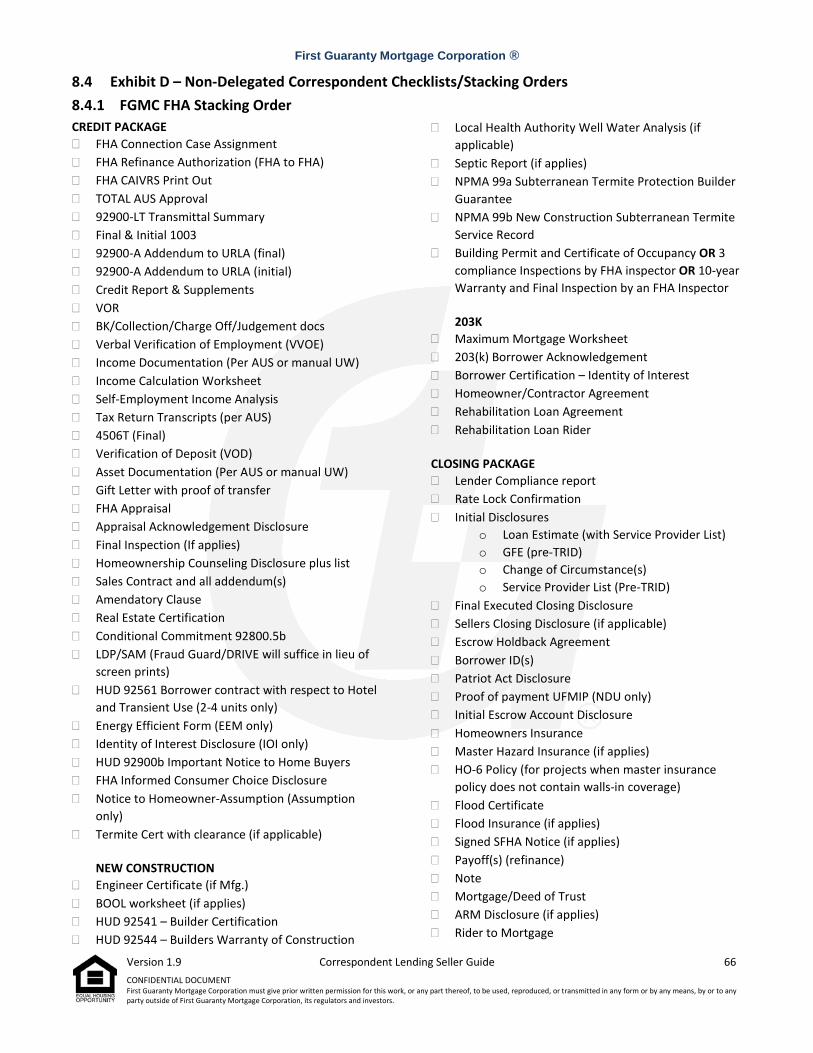

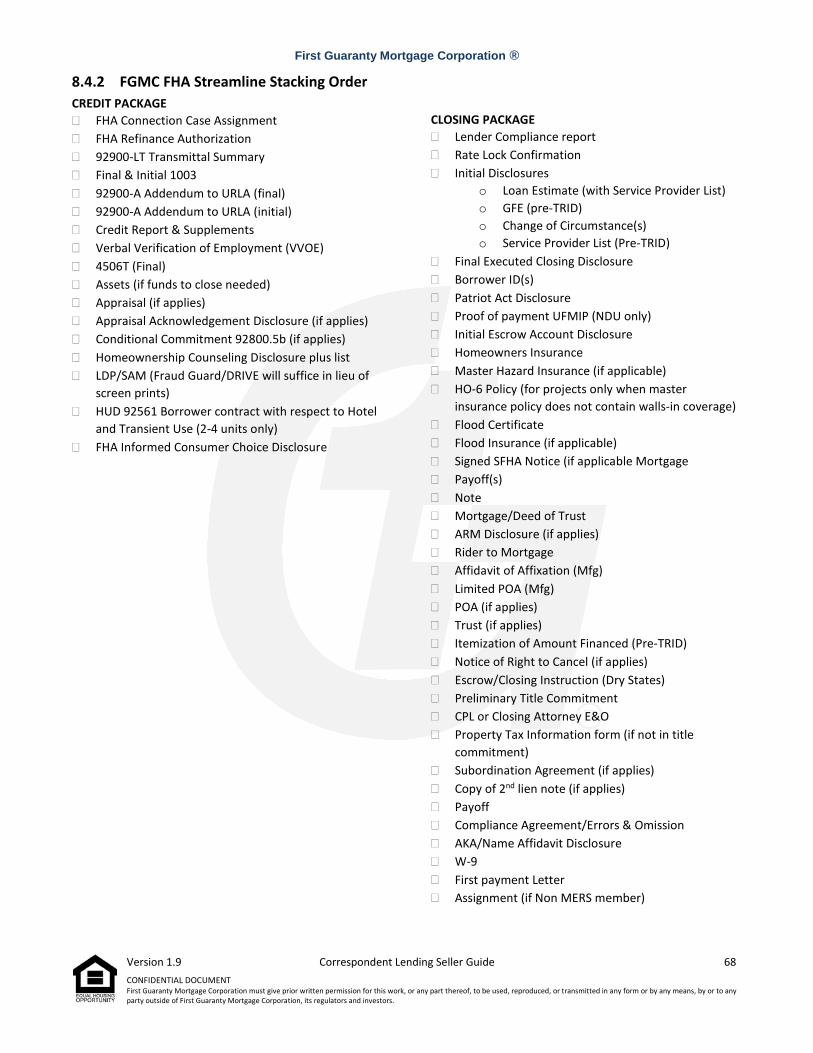

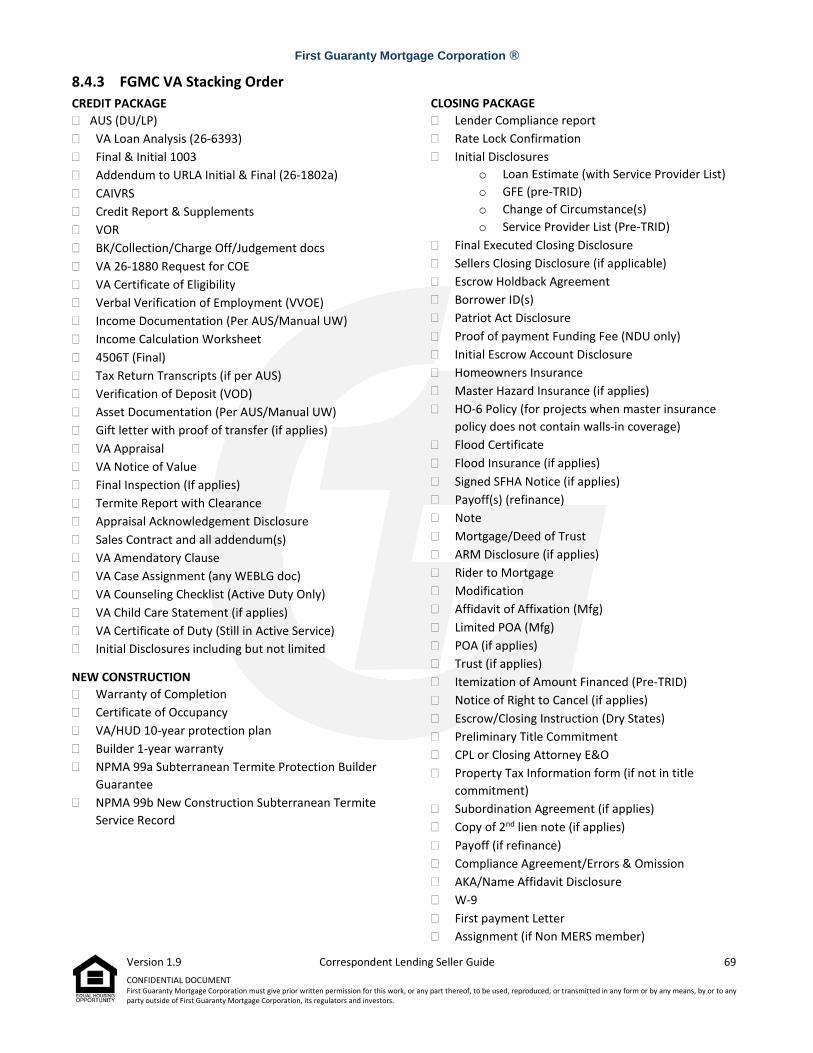

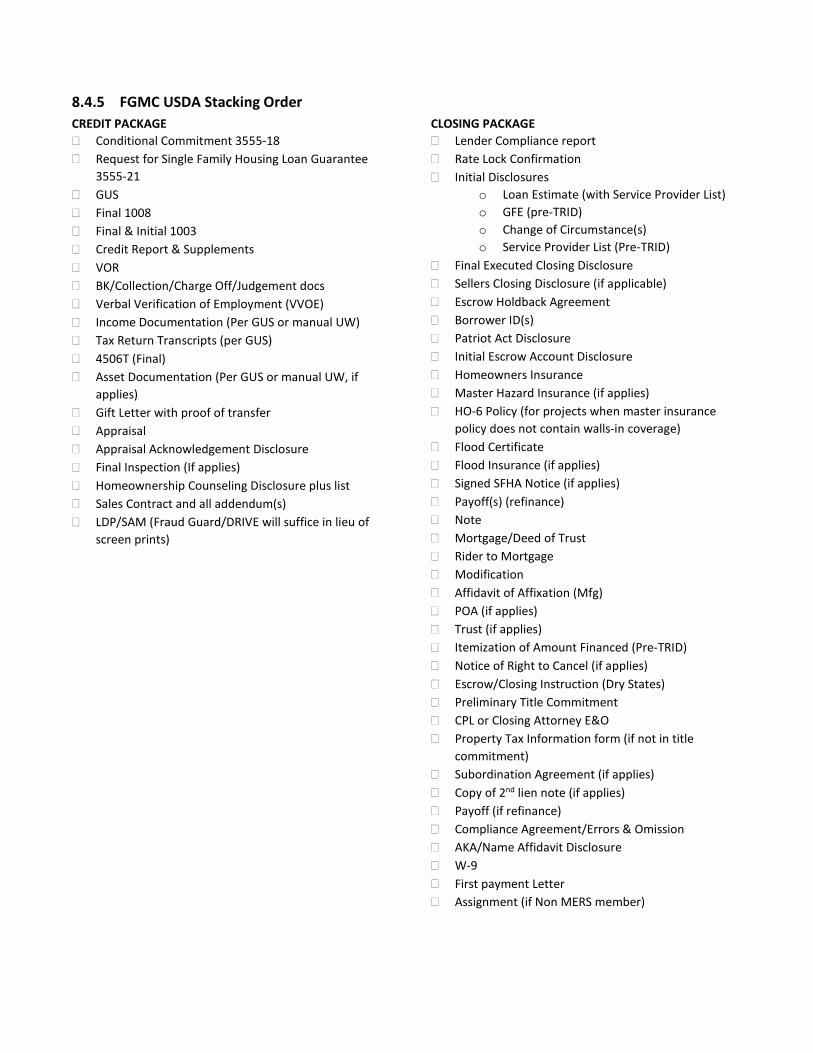

8.4.1 FGMC FHA Stacking Order ...................................................................................... 66 8.4.2 FGMC FHA Streamline Stacking Order .................................................................... 68 8.4.3 FGMC VA Stacking Order ........................................................................................ 69 8.4.4 FGMC VA IRRRL Stacking Order .............................................................................. 70 8.4.5 FGMC USDA Stacking Order .................................................................................... 71

First Guaranty Mortgage Corporation ®

Version 1.9 Correspondent Lending Seller Guide 7 CONFIDENTIAL DOCUMENT First Guaranty Mortgage Corporation must give prior written permission for this work, or any part thereof, to be used, reproduced, or transmitted in any form or by any means, by or to any party outside of First Guaranty Mortgage Corporation, its regulators and investors.

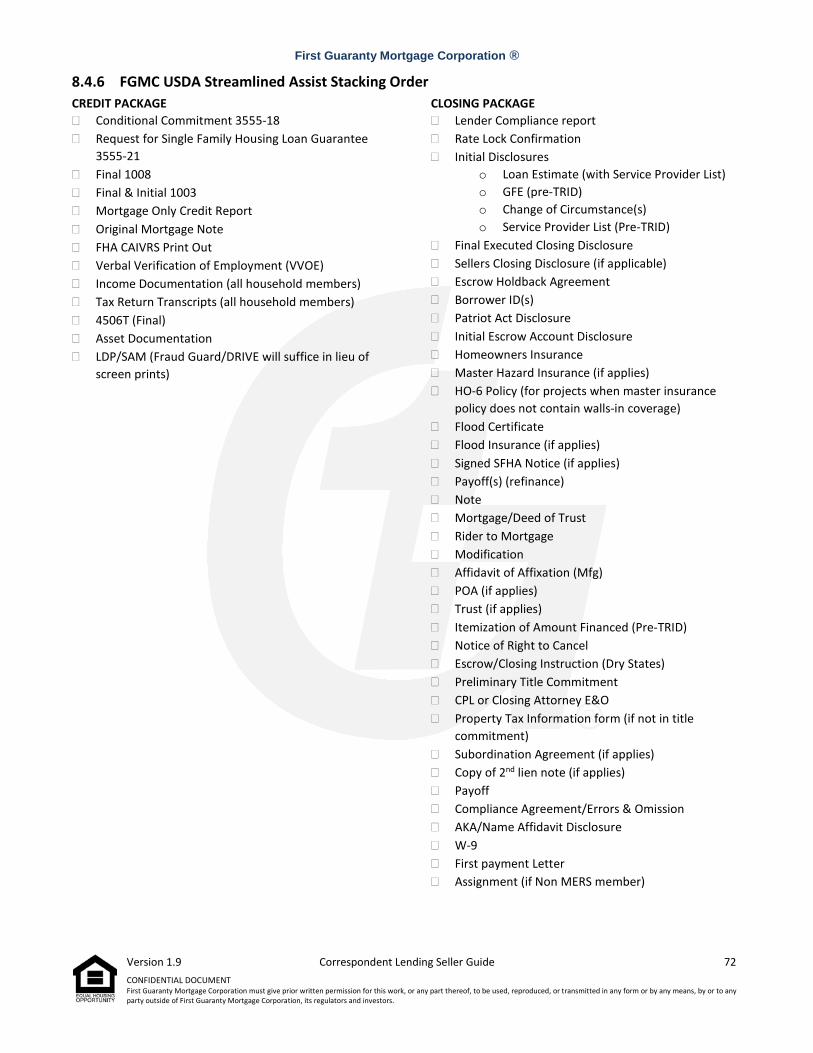

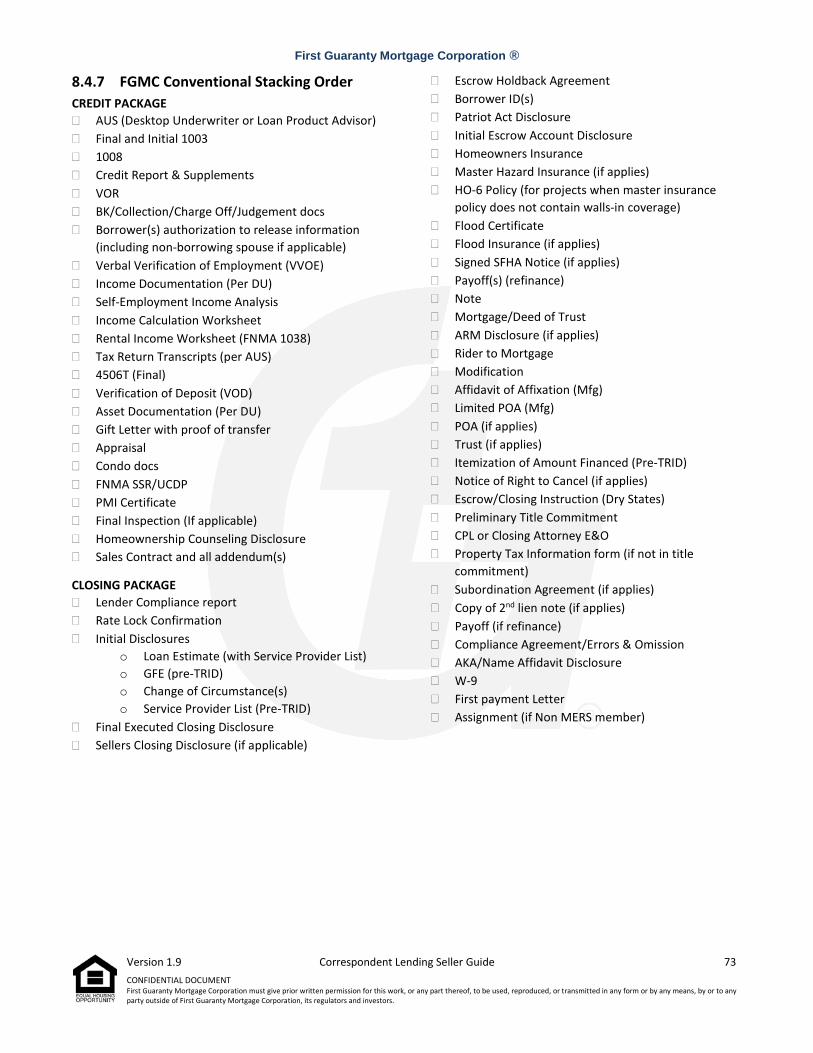

8.4.6 FGMC USDA Streamlined Assist Stacking Order ..................................................... 72 8.4.7 FGMC Conventional Stacking Order ....................................................................... 73

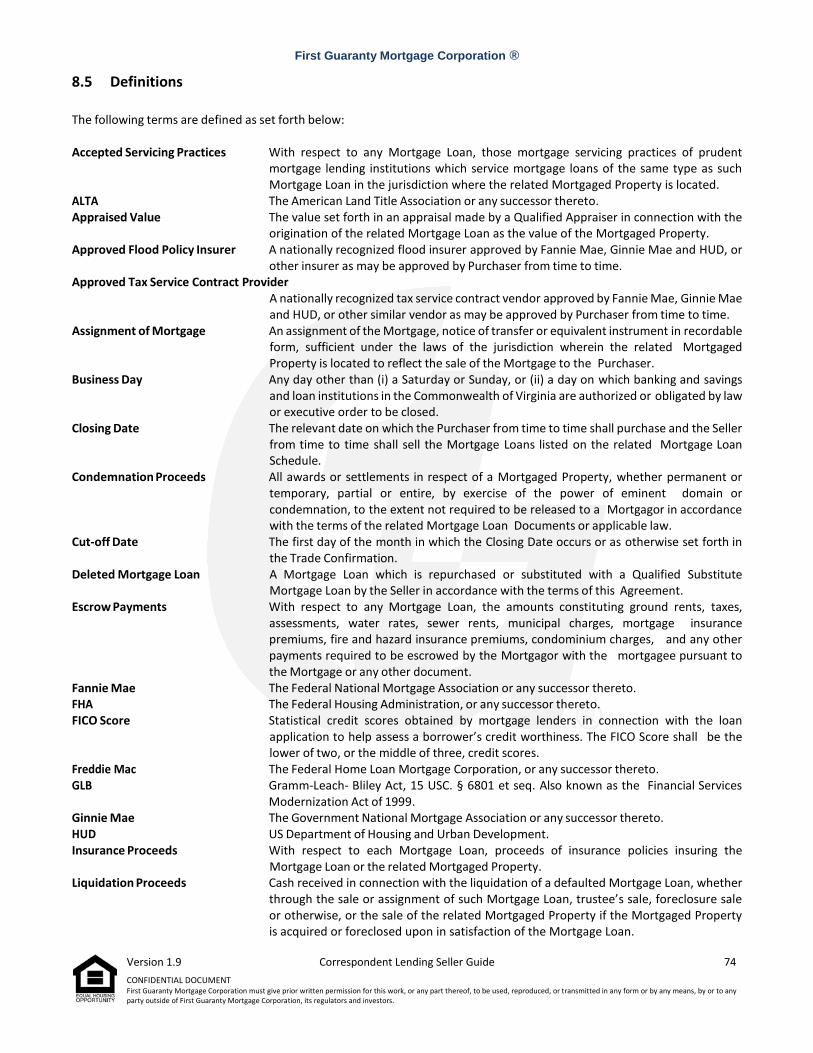

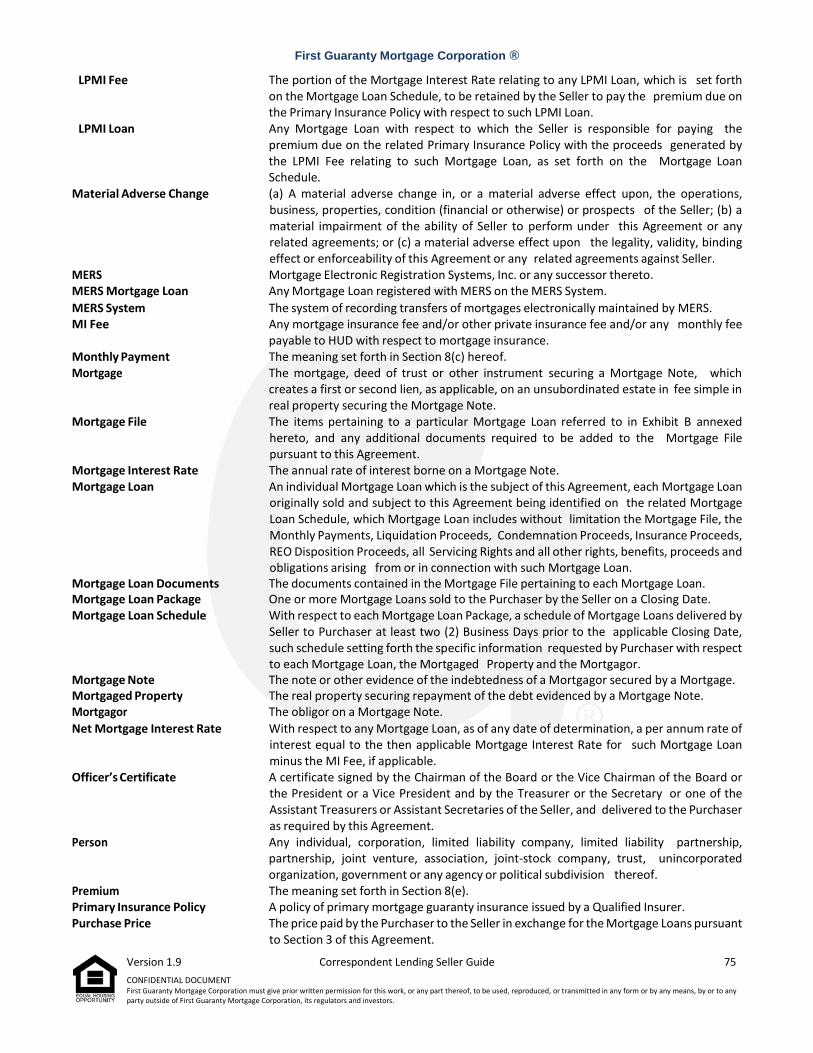

8.5 Definitions ...................................................................................................................... 74 8.6 Contents of each Mortgage File ..................................................................................... 77

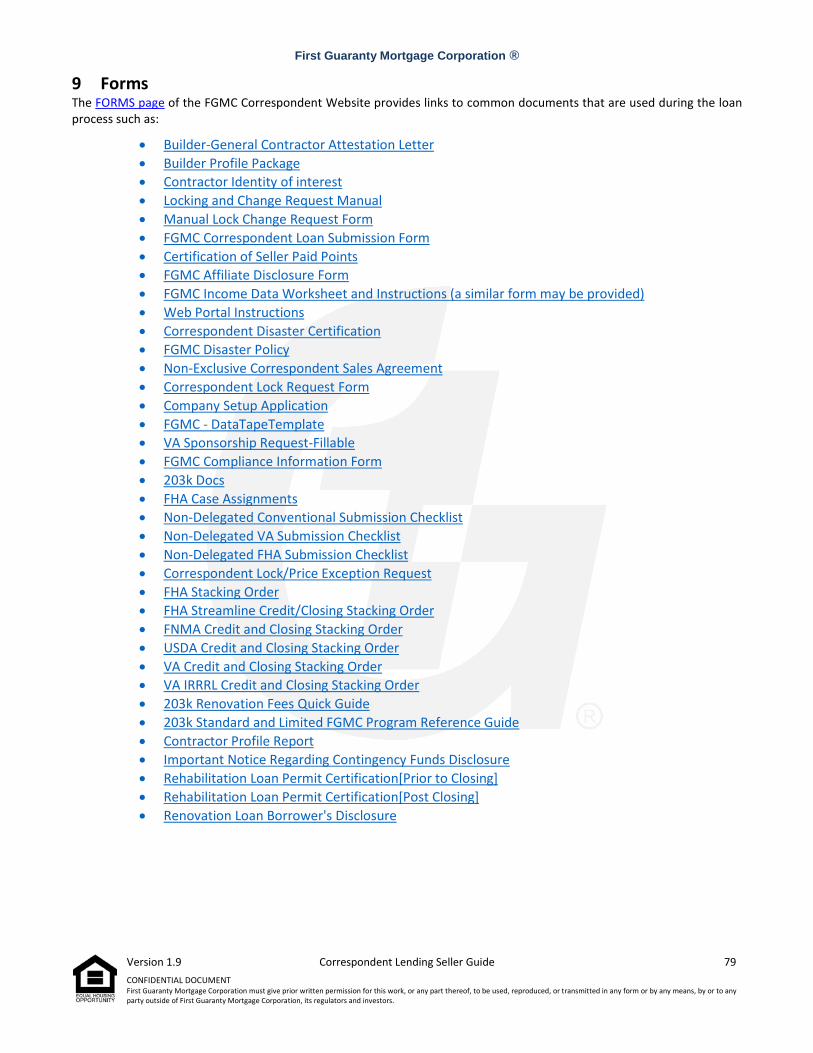

9 Forms ............................................................................................................................ 79

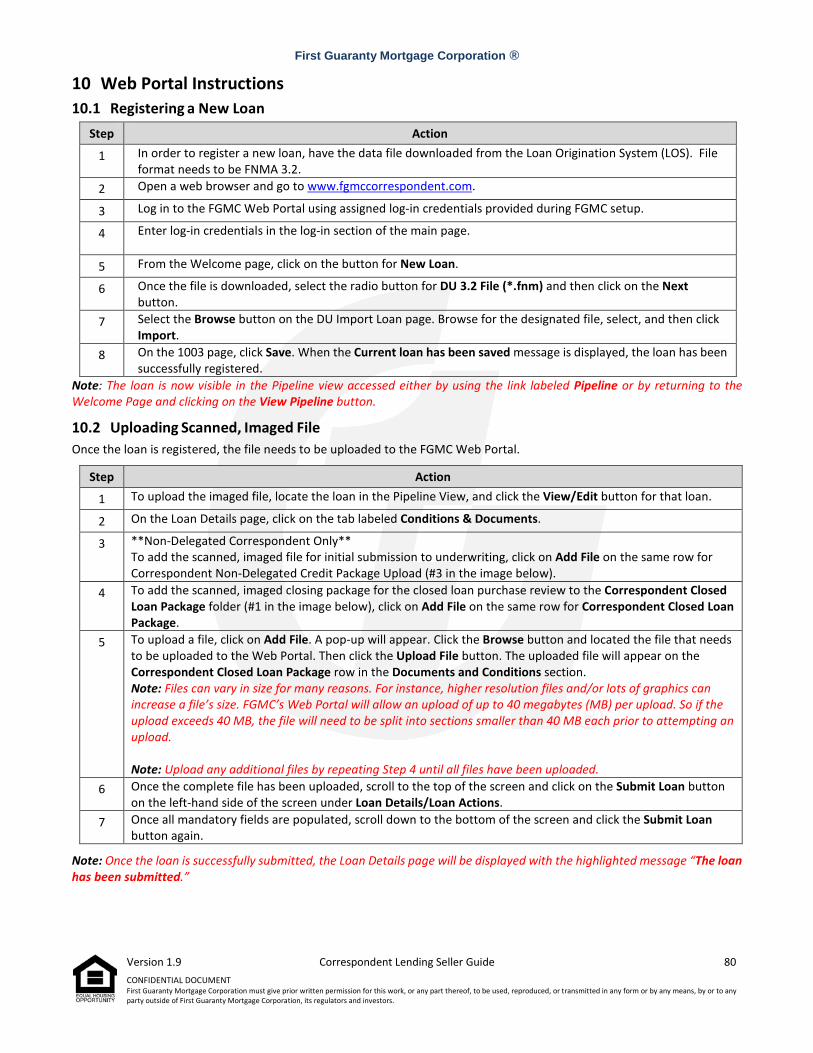

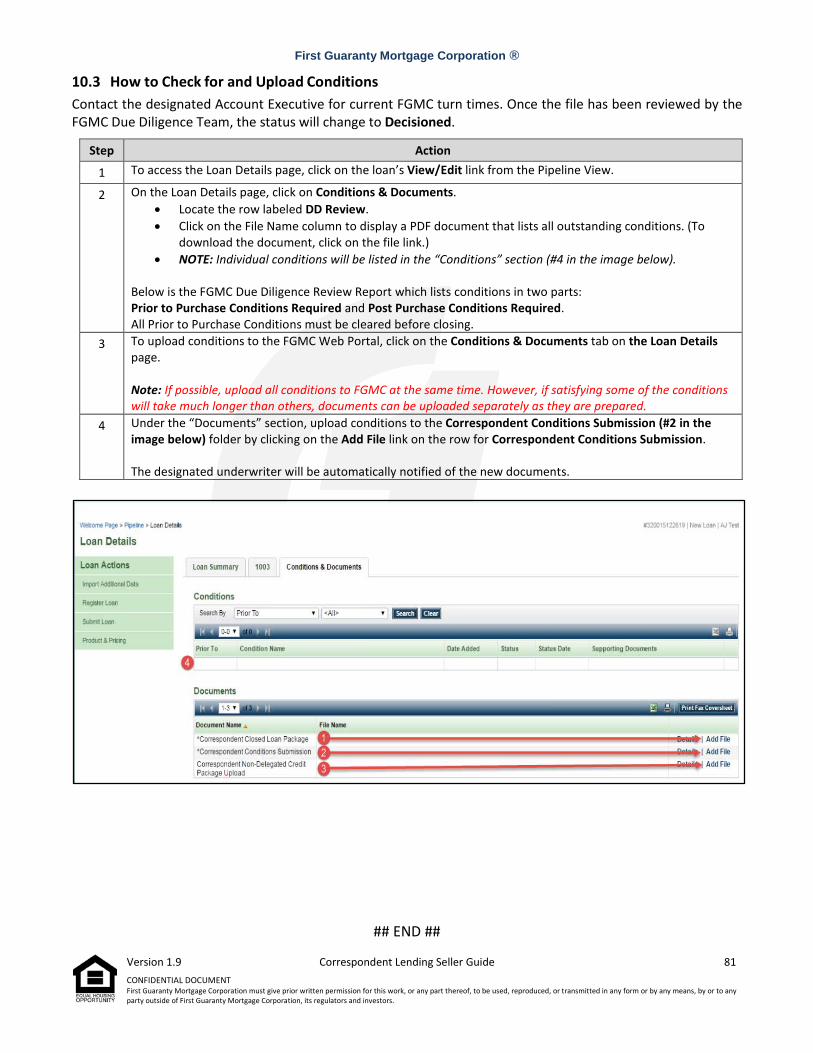

10 Web Portal Instructions ................................................................................................. 80

10.1 Registering a New Loan .................................................................................................. 80 10.2 Uploading Scanned, Imaged File .................................................................................... 80 10.3 How to Check for and Upload Conditions ...................................................................... 81

First Guaranty Mortgage Corporation ®

Version 1.9 Correspondent Lending Seller Guide 8 CONFIDENTIAL DOCUMENT First Guaranty Mortgage Corporation must give prior written permission for this work, or any part thereof, to be used, reproduced, or transmitted in any form or by any means, by or to any party outside of First Guaranty Mortgage Corporation, its regulators and investors.

1 INTRODUCTION 1.1 Purpose The Correspondent Lending Division of First Guaranty Mortgage Corporation (FGMC) purchases loans from approved sellers. This Correspondent Lending Seller Guide details the terms and conditions that govern Correspondent participation in the FGMC Correspondent Lending Program. Occasionally, FGMC communicates updates and revisions to this Guide through email communications and online bulletins located on the FGMC Correspondent website. Each bulletin will indicate its effective date. The basic terms and conditions of the Mortgage Loan Purchase and Sale Agreement (MLPSA) have been incorporated into this Guide, however in the event of a conflict with this document the MLPSA will govern.

1.2 Applicability This Guide shall apply to FGMC in its entirety including all divisions, departments, subsidiaries, and affiliates.

1.3 Correspondent Lending A Correspondent, as defined by FGMC, is an FGMC-approved mortgage lender that originates, funds, and closes mortgages in their name. The Correspondent then submits the loan to FGMC for review (and/or underwriting), purchase, and funding. 1.4 Correspondent Loan Process All Correspondents should use this Guide to ensure that loans are prepared in accordance with FGMC requirements, thus increasing the chance of acceptance, purchase, and funding. After Correspondents create the loan, the loan package will proceed through the pipeline as follows:

• Started – Loan has either been registered or submitted through the FGMC Correspondent website and is in an active folder at FGMC.

• Processing – Once document upload is complete, loan processing begins. Correspondent sends required (

• Collateral Package) documentation for review. • Submitted – Awaiting a list of requirements from FGMC Underwriter or File Reviewer. • Decisioned – Loan has been conditioned and FGMC is waiting for suspense or condition uploads

to clear. • Resubmitted – Cleared loan is ready for submission. • Approved – Loan is ready for purchase. FGMC must receive either reverse Bailee letters or original

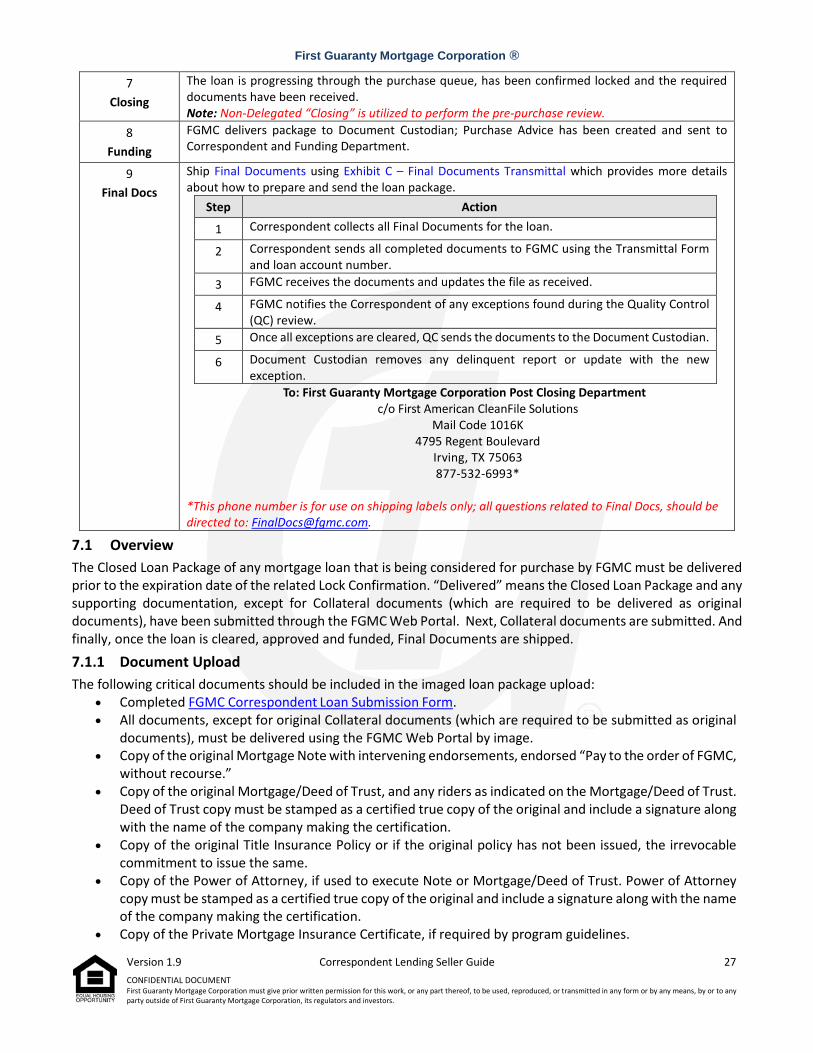

documents prior to purchase. • Closing – The loan is progressing through the purchase queue, has been confirmed locked, and

the required documents received. • Funding – FGMC delivers package to Document Custodian; Purchase Advice has been created and

sent to Correspondent and Funding Department. • Final Docs – Correspondent ships Final Documents as required.

2 GETTING STARTED 2.1 Overview First Guaranty Mortgage Corporation (FGMC) is in the business of providing the best possible service to its clients and customers. To begin a relationship as an FGMC Correspondent, Sellers can visit the Comergence Compliance LLC website. There, a Seller can log in or create a new account to get started.

2.2 Approval The following is an overview of documents necessary for Correspondent approval. These will be requested and maintained by Comergence as part of the approval process.

First Guaranty Mortgage Corporation ®

Version 1.9 Correspondent Lending Seller Guide 9 CONFIDENTIAL DOCUMENT First Guaranty Mortgage Corporation must give prior written permission for this work, or any part thereof, to be used, reproduced, or transmitted in any form or by any means, by or to any party outside of First Guaranty Mortgage Corporation, its regulators and investors.

• Two (2) most recent years audited financial statements • Interim financial statements (most recent available) • Resumes of Key Management (all applicable):

o Chief Executive Officer o Chief Financial Officer o Head of Secondary Marketing o Head of Operations o Head of Production o Head of Compliance o Underwriting Manager(s) o Closing Manager o Funding Manager o Post-Closing Manager

• Resumes of Underwriters (CHUMS Numbers required, if applicable) • Appraiser Independence Requirements (AIR) Certification of Compliance • Anti-Money Laundering (AML) Bulletin • AML Certification • Company Formation/Corporate By-laws • Corporate Resolutions • FACT Act Compliance (Red Flag Policy) • FGMC Mortgage Loan Purchase and Sale Agreement • Investor Scorecards for most recent quarter for all investors providing scorecards • IRS Form W-9 • Letter of Reference from Primary Warehouse Bank • Quality Control Policy and Procedure Documents • Surety/Fidelity Bond insurance ($300,000 minimum) • Copies of all of the following that are available:

o Appraisal Management Policy o Compliance Management Program o Credit Policy o Complaint Management Program o Fraud Management Policy

Comergence will conduct a background and licensing check consisting of the following steps: • Background check of ownership • Office of Foreign Assets Control (OFAC) check • HUD Limited Denial List check • Licensing review • Federal criminal/civil records check • Secretary of State check • Regulatory sanctions check • Review for bankruptcy, foreclosures, or liens/judgments • State/local criminal records check

Next, FGMC will perform the following due diligence: • Financial review • Quality Control review • Comprehensive Risk Assessment (Business, Operations, Compliance) • Consumer and Social Media review

First Guaranty Mortgage Corporation ®

Version 1.9 Correspondent Lending Seller Guide 10 CONFIDENTIAL DOCUMENT First Guaranty Mortgage Corporation must give prior written permission for this work, or any part thereof, to be used, reproduced, or transmitted in any form or by any means, by or to any party outside of First Guaranty Mortgage Corporation, its regulators and investors.

• HUD Neighborhood Watch review - Minimum requirements for all approvals (except Non-Delegated Approval) is current and trailing 3-month average Compare Ratio < 150

In addition, the following requirements will be necessary for FGMC risk review: • All Approval Requests (Non-Delegated, Delegated, Mandatory, Third Party Origination (TPO)):

o FGMC Business Questionnaire o FGMC Unfair, Deceptive, or Abusive Acts and Practices (UDAAP) Questionnaire o FGMC Information Security Questionnaire

• Mandatory Approval Requests Only: o Hedging Policy o Pricing Policy o Copy of hedging vendor agreement o Full set of most recent month’s hedging reports

• Third Party Origination Approval Requests Only: o Copy of TPO Approval and Monitoring Program o FGMC TPO Questionnaire

2.3 Setup Once FGMC has sent approval, the Correspondent needs to fill out the Company Setup Application and email the completed form to [email protected]. This is the first step in getting properly setup on the FGMC Web Portal. The FGMC Help Desk will set up individual users once the completed form has been received.

The Correspondent will be assigned an Account Executive (AE) as the main point of contact. The Correspondent will also be classified as Delegated or Non-Delegated based on FGMC-established requirements. The Delegated Correspondent performs the loan underwriting while the 7.17 Non-Delegated Loan Delivery requires loans to be underwritten by FGMC and follows a slightly different process.

2.3.1 Resources These important resources will provide Correspondents with learning opportunities in order to quickly establish a working relationship with FGMC.

2.3.1.1 FGMC Correspondent Website www.fgmccorrespondent.com

Resources Learning Center

• Bulletins • Forms • Correspondent Checklist • NMLS Consumer Access

• Product Option Guides • Loan Submission • Delivery Information • TRID Resource Center

2.3.1.2 Portal Training Live FGMC Web Portal training is provided every Thursday at 2:00 PM ET. The session usually lasts 45 minutes and will help Correspondents better understand how to register, submit, and lock loans and upload conditions. The webinar is an online meeting available to all clients. Correspondents can contact their Account Executive (AE) for details and a training schedule. If a Correspondent encounters an issue or error when submitting a file, uploading conditions, or locking, the FGMC Help Desk is available for assistance by emailing [email protected].

2.3.1.3 Loan Submission Submission and Condition instructions and Loan Submission Form:

First Guaranty Mortgage Corporation ®

Version 1.9 Correspondent Lending Seller Guide 11 CONFIDENTIAL DOCUMENT First Guaranty Mortgage Corporation must give prior written permission for this work, or any part thereof, to be used, reproduced, or transmitted in any form or by any means, by or to any party outside of First Guaranty Mortgage Corporation, its regulators and investors.

• Instructions for submitting loans and uploading conditions to FGMC can be found here: o See Delivery Procedures o If at any time there is an issue or error submitting a file, uploading conditions, or

locking a loan, the FGMC Help Desk is available for assistance by emailing [email protected].

• Be sure to include the FGMC Correspondent Loan Submission Form on all loan submissions.

2.3.1.4 Submitting Files for Underwriting Correspondents are advised to provide a full, complete file at the time of submission; however, if some items are not available at the time of submission, packages will be accepted with the minimum docs required below. Please refer to the minimum requirements for each submitted file. These items may not be applicable to all files, but this provides Correspondents with a basic list of documents needed to proceed.

• FGMC Submission Form • Automated Underwriting System (AUS) Findings – FNMA Desktop Underwriter (DU) only,

FHA/VA DU or Loan Prospector (LP) • 1003 Loan Application (unsigned OK) • Assets / Income • Sales Contract, if applicable

NOTE: If a submission form is not provided clearly identifying the correct channel, the FGMC Input Department will hold the file until received (status/milestone will show as PROCESSING). FGMC will accept a TBD file for review for purchase transactions only. Be aware that the less documentation provided upfront for initial Underwriter review, the more conditions will be added to the loan approval.

2.3.1.5 General Information The FHA Case Assignments document provides information related to FHA Connection. FGMC ID Numbers:

• FHA ID number is 7516800469 • VA ID Number is 6852450000 • MERS ID is 1000314 • NMLS Number is 2917 • Rushmore Servicer ID is 30941

Once a loan is fully submitted into the FGMC pipeline, the loan will be routed to the Input Department. The system milestone will show as STARTED. Once the file is reviewed, the system is updated as necessary and the Correspondent is notified of any missing items. If the loan is put on hold for any reason, the milestone will show as PROCESSING. Once the loan has moved through input, it will then be put into the reviewer’s queue. At this time the milestone will show as SUBMITTAL.

Pre Purchase Review and Conditions Once in the SUBMITTAL stage, the loan is in queue for underwriting/review on a first-in/first-out basis. Turn times (posted at www.fgmccorrespondent.com) begin the day AFTER the loan was fully submitted to FGMC to account for one (1) full business day.

Closed Loans Once the loan is decisioned, the review/approval will be uploaded to the FGMC Web Portal for retrieval any time. The milestone will show as DECISIONED.

NOTE: Once the conditions have been uploaded, the Correspondent must click the SUBMIT FOR REVIEW button located above the Conditions section on the upload screen. This is the only way the Underwriter is notified that conditions have been submitted for review.

First Guaranty Mortgage Corporation ®

Version 1.9 Correspondent Lending Seller Guide 12 CONFIDENTIAL DOCUMENT First Guaranty Mortgage Corporation must give prior written permission for this work, or any part thereof, to be used, reproduced, or transmitted in any form or by any means, by or to any party outside of First Guaranty Mortgage Corporation, its regulators and investors.

2.3.1.6 Pricing Correspondents should contact their Account Executive for all pricing questions and issues. Locking/Pricing is completed through the FGMC Web Portal. Correspondents can contact [email protected] for the associated lock/pricing username or other assistance. See COMMITMENT POLICY/LOAN LOCKS for more details.

2.3.1.7 Original Collateral/Notes FGMC requires the original final Collateral Documents on all Conforming Mortgage Loans and on Government Mortgage Loans when applicable. The Collateral Package must be shipped to the FGMC custodian no later than the same day that the Loan Package is delivered (via the FGMC Web Portal) to FGMC. For more information, see Collateral Package.

2.3.1.8 Final Documents For complete details about the procedure for shipping documents, see DELIVERY PROCEDURES and Final Documents.

2.3.1.9 Compliance FGMC strictly adheres to federal, state, and agency laws and regulations. It is the Lender’s responsibility for Delegated and Non-Delegated loans to adhere to all applicable federal, state, and agency laws and regulations prior to closing the loans. Note: Correspondents are responsible for ensuring all loans sold to FGMC are originated and closed in accordance with all federal, state, city, county, and agency high-cost/predatory lending regulations. FGMC will not purchase any loan (Agency, Non-Agency, FHA, VA, or USDA) that meets the definition of a “subprime loan” under New York State Law.

2.3.1.10 Important Addresses The submission process for documents (Imaged, Collateral, and Final/Trailing) is covered in detail in the DELIVERY PROCEDURES section. For quick reference, applicable addresses are as follows: Collateral Documents: Final Documents:

Deutsche Bank National Trust Company First Guaranty Mortgage Corporation Post Closing Dept Attn: Team FGMC/Correspondent c/o First American CleanFile Solutions 1761 East St. Andrews Place Mail Code 1016K Santa Ana, CA 92705 4795 Regent Boulevard Irving, TX 75063

Compliance Actions: Borrower’s First Payment: First Guaranty Mortgage Corporation Rushmore Loan Management Services LLC Attn: Client Administration PO Box 514707 1900 Gallows Road, Suite 800 Los Angeles, CA 90051-4707 Tysons Corner, VA 22182 Overnight Payments may be sent to:

Rushmore Loan Management Services LLC 15480 Laguna Canyon Road, Suite 100 Irvine, CA 92618 Vendor Notification: Borrower’s General Correspondence:

First Guaranty Mortgage Corporation Rushmore Loan Management Services LLC Attn: Servicing Dept. Attn: Customer Service 5280 Corporate Drive B200 1755 Wittington Place, Suite 400, Frederick, MD 21703 Dallas, TX 75234

3 CORRESPONDENT ELIGIBILITY 3.1 Overview With respect to loans sold to FGMC and in addition to the Mortgage Loan Purchase and Sale Agreement and other legal agreements between FGMC and the Correspondent, each Correspondent is bound by the provisions of this Guide. 3.2 Eligibility

The requirements stated below, unless waived by FGMC at its sole and absolute discretion, must be met by Lenders in order to be eligible for participation in the FGMC Correspondent Program. FGMC reserves the right, in its sole discretion, to determine whether a prospective Correspondent meets these eligibility requirements. Once approved, Correspondents are required to maintain the eligibility requirements. If a Correspondent fails to maintain one or more of the eligibility requirements, FGMC may suspend purchasing mortgage loans from the Correspondent and/or terminate its business relationship with the Correspondent.

3.2.1 Requirements Correspondents must follow the requirements listed below.

Experience The Correspondent must have been an active originator of first lien, investment-quality residential mortgage loans using Fannie Mae’s Desktop Underwriter (DU) or Freddie Mac’s Loan Product Advisor Automated Underwriting System (AUS) engine during the previous two years. Facilities The Correspondent must have adequate facilities with which to originate first lien residential mortgage loans.

Selling Standards • The Correspondent must follow generally accepted mortgage lending practices with respect to its

mortgage loan origination activities. • The Correspondent’s company must be an organization which is committed to, and engages in,

responsible lending practices.

Capital Requirements The Correspondent and the Correspondent’s parent corporation, if any, must meet the capital requirements of each state and federal regulatory agency with jurisdiction over any of the Correspondent’s or parent corporation’s activities, as applicable. Minimum requirements are:

• Delegated Loans: $500,000 net worth (NW) and 20% NW in cash. • Non-Delegated Loans: $150,000 NW and $50,000 in cash. • Mandatory Locks: $1,000,000 NW and 20% of NW in cash. • Delivery of Third-Party Originated (TPO) Loans: $1,000,000 NW and 20% of NW in cash.

Legal Standing • The Correspondent must be duly organized, validly existing, and in good standing under the laws of the

jurisdiction of its organization and qualified to transact business and properly licensed in each jurisdiction where it originates or services mortgage loans.

• The Correspondent must be in good standing with all applicable regulatory authorities and not subject to any extraordinary supervision of its operations.

• The Correspondent must have the power and authority to enter into the FGMC Correspondent Mortgage Loan Purchase and Sale Agreement.

• The Correspondent’s compliance with the terms and conditions of the agreement, including the terms and conditions of this Guide, must not violate any of the provisions of its articles of incorporation, charter

First Guaranty Mortgage Corporation ®

Version 1.9 Correspondent Lending Seller Guide 14 CONFIDENTIAL DOCUMENT First Guaranty Mortgage Corporation must give prior written permission for this work, or any part thereof, to be used, reproduced, or transmitted in any form or by any means, by or to any party outside of First Guaranty Mortgage Corporation, its regulators and investors.

or bylaws or any other instrument relating to the conduct of the Correspondent’s business, the ownership of its property or any other agreement to which it is a party or by which it is bound.

Licensing The Correspondent must possess and maintain all required licenses necessary to conduct its activities in each jurisdiction in which any mortgaged property is located or otherwise be exempt from such requirements.

Insurance Correspondents that are not federally insured must maintain a blanket fidelity bond and errors and omissions insurance coverage in the amount of $300,000 each. The deductible may not exceed the greater of $100,000 or 5% of the face amount of the bond.

3.3 Approval Levels 3.3.1 Loan Purchase Eligibility

• Delegated Correspondents must underwrite and close all loans delivered to FGMC for purchase. • Loans must meet FGMC and Investor guidelines. • AUS decision required in accordance with the following:

o Conventional: Desktop Underwriter (DU) approval. o FHA: DU or LP TOTAL Scorecard approval. Streamline transactions do not require a TOTAL Scorecard

approval. o VA: DU approval, LP approval, or manual underwrite per Product Profile. Interest Rate Reduction

Refinance Loans (IRRRL) transactions do not require an AUS approval. o Rural: USDA Guaranteed Underwriting System (GUS) approval or manual underwrite per Product

Profile.

Loans underwritten by a nationally recognized Mortgage Insurance (MI) contract underwriting company that meet the above criteria are eligible for purchase.

Correspondents must be aware of the following when utilizing MI contract underwriting: • The Correspondent must establish and utilize its own contract underwriting agreement with the MI

Company. FGMC will not be a party to these agreements. • The Correspondent is responsible for all representations and warranties to FGMC for underwriting

decisions. • The Correspondent must perform normal due diligence in processing and underwriting the loan prior to

submitting the loan to the contract underwriter. • Even though the MI Company will be underwriting as an agent of the Correspondent, Correspondents are

still responsible for all origination activities. • Correspondents are responsible for complying with federal and state reporting requirements, including

but not limited to, reporting under the Home Mortgage Disclosure Act (HMDA) and Nationwide Licensing System Mortgage (NLSM) call reports and financial statements.

• A contract underwriting decision issued by the MI Company on behalf of the Correspondent will not impact or change the Correspondent’s responsibility and obligation to sell FGMC loans that are in full compliance with the Guide and the Mortgage Loan Purchase and Sale Agreement.

3.3.2 FHA Loan Purchase Eligibility

In addition to the Purchase Eligibility requirements for FHA Loans, Correspondents must: • Meet all other eligibility requirements, as applicable. • Meet HUD’s loan insurance requirements. • Realize any government loan not insured within 60 days of loan closing may be subject to repurchase or

collection of an uninsured loan fee. • Be HUD approved and have a DE Underwriter on staff. • Provide a copy of their HUD approval letter.

First Guaranty Mortgage Corporation ®

Version 1.9 Correspondent Lending Seller Guide 15 CONFIDENTIAL DOCUMENT First Guaranty Mortgage Corporation must give prior written permission for this work, or any part thereof, to be used, reproduced, or transmitted in any form or by any means, by or to any party outside of First Guaranty Mortgage Corporation, its regulators and investors.

• Be in good standing with HUD and other applicable agencies.

3.4 Maintaining Eligibility

Any Correspondent approved for participation in the FGMC Correspondent Program must continue to meet the eligibility requirements herein to maintain its eligibility and approval to participate.

3.4.1 Notification of Significant Changes The Correspondent must send FGMC written notice of any contemplated major changes in its organization, including its notice copies of any filings with, or approvals from, its regulators. FGMC requires notice of, among other things, the following significant changes relating to the Correspondent:

• Any mergers, consolidations, or reorganizations. • Any direct or indirect material change in ownership. An “indirect change in ownership” includes any

change in the ownership of the Correspondent’s parent, any owner of the parent, or any beneficial owner of the Correspondent that does not own a direct interest in the Correspondent.

• Any change in corporate name. • Any change from a federal charter to a state charter (or vice versa) if the Correspondent is a savings and

loan association or a bank. • Material changes in financial condition.

3.4.2 Changes to Corporate Authority and Banking Relationships In the event that there is any change in corporate authority, the lender must immediately deliver to FGMC a replacement Corporate Resolution, which accurately reflects the corporate authorizations granted by the lender, or a Funding Instructions Notification which accurately describes the banking relationships in effect, as applicable.

FGMC will not recognize any changes in the Correspondent’s corporate authorizations or funding instructions until the replacement Corporate Resolution, or Funding Instructions Notification, as applicable, is received by FGMC.

3.4.3 Compliance Reporting Requirements If the Correspondent is subject to the jurisdiction of any governmental agency or quasi-governmental agency, including but not limited to, state regulatory entities, the Consumer Financial Protection Bureau (CFPB), Fannie Mae, Freddie Mac, Department of Housing and Urban Development (HUD) or Federal Deposit Insurance Corporation (FDIC), FGMC may request copies of any audit reports issued by such agencies.

If any disciplinary action is taken by any such agency, including suspension or termination of the Correspondent’s selling or servicing rights, the Correspondent must notify FGMC within three (3) business days of such action. Any reports or notices to be delivered to FGMC pursuant to this section of the Guide must be delivered to the following address:

First Guaranty Mortgage Corporation Attn: Client Administration

1900 Gallows Road, Suite 800 Tysons Corner, VA 22182

First Guaranty Mortgage Corporation ®

Version 1.9 Correspondent Lending Seller Guide 16 CONFIDENTIAL DOCUMENT First Guaranty Mortgage Corporation must give prior written permission for this work, or any part thereof, to be used, reproduced, or transmitted in any form or by any means, by or to any party outside of First Guaranty Mortgage Corporation, its regulators and investors.

3.4.4 Periodic Reviews FGMC will routinely review each Correspondent’s book of business to monitor performance. The reviews may include, but are not limited to, the following:

• Product mix • Best-effort commitment pull through rate • Mark-to-market (MTM) exposure • Delinquency data • HUD compare ratios • Repurchase activity • Defective delivery rate • Number of Early Payment Default (EPD) loans • Number of Early Payoffs (EPO) and overall portfolio turnover

3.4.5 Early Payoff Remedies Consistent with the prepayment review process of the Agencies, FGMC routinely reviews each Correspondent’s portfolio of loans to monitor levels of prepayments. If such analysis identifies unusual prepayment behavior (as defined by one or more of the Agencies) by an FGMC Correspondent, the originating broker or loan officer, FGMC may seek additional protections, including an extended EPO period on future loan purchases or disallowing loans to be submitted from identified brokers or loan officers prior to purchasing any additional mortgage loans from a Correspondent. Further, if FGMC receives invoices from an investor due to unusual prepayment speeds, the cost (which may include an EPO recapture of all amounts paid in excess of the loan amount) will be passed on to and borne by the Correspondent.

See the FGMC Mortgage Loan Purchase and Sale Agreement regarding solicitation, Government-Sponsored Enterprise (GSE) eligible loans, and the GSE’s policy regarding prepayment behavior.

3.4.6 Audits FGMC may audit the Correspondent’s mortgage loan origination operations and examine the books and records relating to any mortgage loan sold by the Correspondent to FGMC. The Correspondent will facilitate such audits and provide FGMC and its agents with access to the Correspondent’s offices, books and records at reasonable times during the Correspondent’s normal business hours.

3.4.7 Correspondent Annual Recertification Within 30 days of their yearly initial approval date, all Correspondents will be advised to complete the Correspondent Annual Recertification form as part of the Correspondent Annual Recertification Process. In addition, Correspondents are required to provide the following:

• Most recent years audited financial statements • Interim financial statements (most recent available) • Resumes of key management (revised or additional) that differ from those previously provided to FGMC • Resumes of current Underwriters (CHUMS Numbers required, if applicable) • Anti-Money Laundering (AML) Bulletin • AML Certification • Corporate Resolutions • Corporate Formation/Corporate Bylaws • FGMC Mortgage Loan Purchase and Sale Agreement (previous version can remain unchanged) • Letter of Reference from Primary Warehouse Bank • QC reports with management responses for most recent quarter • Surety/Fidelity Bond insurance ($300,000 minimum) • Fair and Accurate Credit Transactions (FACT) Act Compliance (Red Flag Policy)

First Guaranty Mortgage Corporation ®

Version 1.9 Correspondent Lending Seller Guide 17 CONFIDENTIAL DOCUMENT First Guaranty Mortgage Corporation must give prior written permission for this work, or any part thereof, to be used, reproduced, or transmitted in any form or by any means, by or to any party outside of First Guaranty Mortgage Corporation, its regulators and investors.

• Copies of any policies, procedures or programs (revised or additional) that differ from those previously provided to FGMC

Comergence will work with FGMC to perform the required background checks and verifications, including past performance with FGMC, and then provide Correspondent with the results. 3.4.8 Financial Statement Delivery Requirements All Correspondents are required to provide audited financials within 120 days of fiscal year end.

3.5 Loan Defects 3.5.1 Early Payment Default If, at any time, within the first six (6) months following purchase of the Loan, any scheduled Monthly Payment on such Mortgage Loan is or becomes ninety (90) days delinquent with respect to a monthly payment, Seller shall be obligated to repurchase the affected Mortgage Loan upon the occurrence of one or more of the following circumstances (each, a “Repurchase Obligation”) affecting a Mortgage Loan:

Where an Early Payment Default has occurred with respect to the Mortgage Loan;

The Purchaser (FGMC) reserves the right to, in lieu of repurchase, recapture the Service Release Premium (SRP), an administrative fee of $3,000 and any estimated associated loss in respect to the Mortgage Loan.

3.5.2 Loan Defects Detected For all loans acquired by Purchaser that are determined to have eligibility violations, the Purchaser will inform the Seller, in writing, and provide a response time in accordance to the Mortgage Loan Purchase and Sale Agreement.

If a Seller provides a response within the allotted time in accordance to the Mortgage Loan Purchase and Sale Agreement and both the Purchaser and/or Purchaser’s investor agree with the provided rebuttal, the repurchase demand will be rescinded.

If a Seller cannot cure the eligibility violation but is able to refinance the existing mortgage loan, the Purchaser reserves the right to recapture the Service Release Premium (SRP) paid in respect to such mortgage loan, if the eligibility violation is detected within three (3) years of the Funding Date. Additional holding fees may be applicable if the refinance extends beyond the Agency repurchase due date.

If the eligibility violation cannot be cured, an effective repurchase due date will be set. The repurchase due date will be the greater of the investor repurchase date or 30 days from initial repurchase notification. If funds are not remitted by the repurchase due date, the Purchaser reserves the right to charge the Seller a daily or monthly holding fee until the full Repurchase Price is remitted.

4 CREDIT PARAMETERS 4.1 Overview As outlined in the Mortgage Loan Purchase and Sale Agreement, loans sold to FGMC by the Correspondent are bound by the provisions in this Guide.

4.2 Product Options • Refer to Product Option Guides for details on each FGMC product. • For Non-Delegated loans, see Non-Delegated Loan Delivery.

4.3 Exclusionary Lists Correspondents are required to adhere to all applicable agency requirements, including those requiring lenders to check loan participants against exclusionary lists. Individuals or entities confirmed to be on an exclusionary list may not be a party to a loan sold to FGMC. Agency exclusionary lists include, but may not be limited to:

First Guaranty Mortgage Corporation ®

Version 1.9 Correspondent Lending Seller Guide 18 CONFIDENTIAL DOCUMENT First Guaranty Mortgage Corporation must give prior written permission for this work, or any part thereof, to be used, reproduced, or transmitted in any form or by any means, by or to any party outside of First Guaranty Mortgage Corporation, its regulators and investors.

• U.S. General Services Administration (GSA) Excluded Party List (EPL) available through GSA’s System of Award Management (SAM) website;

• HUD’s Limited Denial of Participation List (LDP); • Federal Housing Finance Agency’s (FHFA) Suspended Counterparty Program (SCP); and • Freddie Mac’s Exclusionary List.

5 APPRAISAL REQUIREMENTS 5.1 Overview FGMC allows Correspondent Sellers to order appraisal reports following their own internal appraisal management policies. Each appraisal report submitted to FGMC requires the individual appraiser to fully comply with all Uniform Standards of Professional Appraisal Practice (USPAP), Financial Institutions Reform Recovery and Enforcement Act (FIRREA) appraisal regulatory standards, and the Federal Housing Finance Agency (FHFA) which issued the Appraiser Independence Requirements (AIR). Additionally, all reports must meet all minimum appraisal requirements as set forth by the secondary market, including Government-Sponsored Enterprises (GSEs), Federal Housing Administration (FHA) and Department of Veterans Affairs (VA).

Correspondent Sellers must comply with FGMC standards for meeting AIR. They must have documented internal appraisal procedures, including, but not limited to, if they utilize Appraisal Management Companies (AMCs) and/or a panel of approved appraisers as outlined under FGMC Policy – Requirements for Correspondent Use of Appraisal Management Companies (AMCs) and/or Proprietary Panel of Approved Appraiser. FGMC will review Correspondent Seller policies and procedures for meeting AIR, to determine if the Correspondent’s documented internal appraisal procedures utilize AMCs and/or a panel of approved appraisers, and if they meet all standards outlined in the FGMC Policy. 5.2 Correspondent Certification With every appraisal report submitted to FGMC, the Correspondent certifies:

• The appraisal has been conducted by a licensed or certified appraiser. Correspondent certifies that it has adequate controls to ensure the appraiser is in good standing and licenses/certifications are current.

• The Correspondent has thoroughly reviewed the report and has concluded that the property is adequate collateral to support the loan.

• The report complies with FGMC, Uniform Standards of Professional Appraisal Practice (USPAP) and agency standards.

• Any information known to the Correspondent that could adversely affect value or marketability was disclosed to the appraiser.

• The appraiser has adequately supported any assumptions, data, analysis, rationale, and conclusions made or used to determine value and marketability.

• The information on the report is accurate, consistent, clearly written, and sufficiently documented. • Appraiser comments addressing declining property value (if any) are acted upon appropriately. • By delivering loans to FGMC, the Correspondent represents and warrants that their appraisal process and

appraisal reports are in compliance with all agency and HUD requirements, as well as all applicable state or federal statutes in all aspects of ordering, evaluating, disclosures and processing appraisals. Appraisals provided by a third party, such as a mortgage or real estate broker, are not acceptable.

5.3 Appraisal Requirements • Determined by AUS Findings. Property Inspection Waivers are permitted by FGMC when offered by

Desktop Underwriter (DU). • A Market Conditions Addendum (Fannie Mae Form 1004MC/Freddie Mac Form 71) is required for all loans

delivered with appraisals of one to four unit properties. It must be included with appraisal Forms 1004/70, 1025/72, 1073/465, 1075/466, 2055/2075.

First Guaranty Mortgage Corporation ®

Version 1.9 Correspondent Lending Seller Guide 19 CONFIDENTIAL DOCUMENT First Guaranty Mortgage Corporation must give prior written permission for this work, or any part thereof, to be used, reproduced, or transmitted in any form or by any means, by or to any party outside of First Guaranty Mortgage Corporation, its regulators and investors.

• A full appraisal is required, regardless of AUS findings, if any of the following conditions exist: o Purchase transactions of REO properties and all purchases of properties whose most recent

transaction was a foreclosure sale. o Apparent adverse physical deficiencies or conditions. o Apparent adverse environmental conditions. o The subject property does not conform to the neighborhood.

• First generation PDF of the Appraisal Report. • Summary Submissions Report (SSR) if submitted to Fannie Mae Uniform Collateral Data Portal (UCDP) or

FHA/Department of Housing and Urban Development (HUD) Electronic Appraisal Delivery (EAD) Portal (effective June 27, 2016). (Note: The SSR document must have a status of “Successful” to be acceptable.)

• The VA Form (26-1805) must have the Client/Broker listed as the Originating Lender and FGMC listed as the Sponsor for Non-Delegated Correspondent loans.

5.4 Enhanced Appraisal Requirements With every appraisal report submitted to FGMC, the Correspondent certifies:

• The appraisal has been conducted by a licensed or certified appraiser. Correspondent certifies that it has adequate controls to ensure the appraiser is in good standing and licenses/certifications are current.

• The Correspondent has thoroughly reviewed the report and has concluded that the property is adequate collateral to support the loan.

• The report complies with FGMC, USPAP, and agency standards. • Any information known to the Correspondent that could adversely affect value or marketability was

disclosed to the appraiser. • The appraiser has adequately supported any assumptions, data, analysis, rationale, and conclusions made

or used to determine value and marketability. • The information on the report is accurate, consistent, clearly written, and sufficiently documented. • Appraiser comments addressing declining property value (if any) are acted upon appropriately. • By delivering loans to FGMC, the Correspondent represents and warrants that their appraisal process and

appraisal reports are in compliance with the all agency and HUD requirements as well as all applicable state or federal statutes in all aspects of ordering, evaluating, disclosures and processing appraisals. Appraisals provided by a third party, such as a mortgage or real estate broker, are not acceptable.

6 COMMITMENT POLICY/LOAN LOCKS All loans are required to be locked with the lock desk at FGMC prior to authorization to clear a loan for purchase. Loan files that are not locked and/or have a lock expired at the time of review will receive a condition indicating the loan must be locked. This condition must be satisfied before FGMC will clear the loan for purchase. 6.1 Overview All Correspondents have the ability to submit locks, extensions, and change requests. For detailed instructions, Correspondents can reference the Locking and Change Request Manual or contact their Account Executive. Assistance with the online portal or the locking process can also be obtained by emailing [email protected].

The FGMC Lock Desk is open until 9:00 PM ET for all products. New locks and extension requests received through the correspondent website will be processed the same day with exception of FHA 203k, VA and all High Balance products. All online profile changes, emails, relocks and manual lock requests submitted between 7:00 PM – 9:00 PM ET will be processed the next business day. Manual lock requests and relocks received after 9:00 PM ET will be processed the following business day once pricing is made available. Pricing is made available every morning once Rate Sheets have been updated and sent. Pricing is updated between 9:45 AM and 10:30 AM ET every business day. Pricing may also be updated throughout the day as needed and new Rate Sheets will be sent out. FGMC does not offer overnight price protection.

First Guaranty Mortgage Corporation ®

Version 1.9 Correspondent Lending Seller Guide 20 CONFIDENTIAL DOCUMENT First Guaranty Mortgage Corporation must give prior written permission for this work, or any part thereof, to be used, reproduced, or transmitted in any form or by any means, by or to any party outside of First Guaranty Mortgage Corporation, its regulators and investors.

Note: Correspondents may access historical pricing via the FGMC online locking system if available, but it is the responsibility of the Correspondent to keep historical records of FGMC rate sheets and lock confirmations. Off-sheet pricing requests, transactions requiring a manual lock request, or locks done via FGMC extended lock option need to be submitted using Exhibit A – Lock Request Form and emailing to [email protected].. Currently transactions that require a manual lock request are:

• GNMA High Balance loans collateralized by a manufactured home, • GNMA ARM loans collateralized by a manufactured home, • Fannie Mae Loans with non-traditional credit, • Any loan product to be locked at an interest rate not published on the rate sheet, or • Fannie Mae DU Refi Plus with credit scores below 620.

6.2 Best Efforts/Mandatory Locks FGMC offers Correspondents two options for selling mortgage loans—Best Efforts and Mandatory, each with its own benefits. An explanation of the two types of locks can be found below. Note that loans cannot be switched from Best Efforts to Mandatory option (or from Mandatory to Best Efforts) after a loan has been locked.

6.2.1 Best Efforts Definition A Best Efforts Lock is an agreement between FGMC and the Correspondent for the purchase and sale of a specified, eligible mortgage loan by a specific date and for a specific price. Correspondents commit to providing their best effort to sell this loan to FGMC. A Best Efforts Lock is borrower and property specific. Choosing this option means that the Correspondent will not incur borrower-driven fallout risk prior to the loan closing. Things to remember:

• For loans that do not close, Correspondents may cancel the lock without incurring a pair-off fee. • For Re-Locks, Correspondents are obligated to perform within the Re-Lock terms of this policy.

Notes: • A loan may not be switched from Best Efforts to Mandatory after a loan has been locked. • A pair-off fee is a fee assessed when the aggregate principal balance of a mortgage funded or purchased

under a delivery commitment falls below the tolerance specified. (See Error! Reference source not found..) 6.2.2 Mandatory Lock Definition A Mandatory Lock is an agreement between FGMC and the Correspondent for the purchase and sale of a specified, eligible mortgage loan by a specific date and for a specific price. The Correspondent commits to sell the loan(s) to FGMC and failure to do so may result in a pair-off fee.

Note: A loan may not be switched from Mandatory to Best Efforts after the loan has been locked.

6.2.3 Service Release Premium FGMC pays the Correspondent a Service Release Premium (SRP) on each loan based on specific loan criteria. The SRP is included in the GNMA (FHA, VA, USDA loans) and Fannie Mae TPO base pricing.

6.2.4 Loan Registration All loans must be registered prior to requesting a lock. All bulk registrations must be completed within 48 hours of commitment. For instructions on how to register a loan, refer to the Web Portal Instructions located on the FGMC Correspondent website under Forms or go to the Registering a New Loan section of this Guide.

6.2.4.1 Lock Confirmations Lock confirmations are sent automatically via email to the Correspondent upon FGMC confirming a lock was requested via FGMC’s online locking system. All lock confirmations will be sent to the email assigned to the User during the online Web Portal setup. If a lock confirmation is not received upon locking a loan online, the Correspondent should email [email protected] to ensure that FGMC has the most recent contact email on file.

In addition, all lock confirmations for loans that are locked online may be retrieved after a loan is locked by the

First Guaranty Mortgage Corporation ®

Version 1.9 Correspondent Lending Seller Guide 21 CONFIDENTIAL DOCUMENT First Guaranty Mortgage Corporation must give prior written permission for this work, or any part thereof, to be used, reproduced, or transmitted in any form or by any means, by or to any party outside of First Guaranty Mortgage Corporation, its regulators and investors.

Correspondent, at any time. For instructions on how to retrieve lock confirmations online, refer to the Locking and Change Request Manual located on the FGMC Correspondent website under “Resources/Forms” or contact the assigned Account Executive.

Lock confirmations for all manual requests will be sent via email by the FGMC Lock Desk within 24 hours of request.

6.2.4.2 Off-Sheet Pricing Request Requests for off-sheet pricing must be submitted to: [email protected] no later than 4:00 PM ET and confirmed with FGMC no later than 5:00 PM ET. In addition, off-sheet pricing is only available as a mandatory delivery.

6.2.4.3 Duplicate Locks Correspondents must monitor their pipeline to prevent duplicate loans and double locks (same borrower, same property address, etc.). A lock commitment is associated with one specific physical address. If a property address changes, a new lock is required and will not be considered a duplicate lock. In the event that the Correspondent locks a loan with the same property address more than once, the following procedures will apply:

If two loans are registered and locked with same borrower/ property address and…

Then the...

Both loans have locks that are active, Original loan will remain active and FGMC will apply worst case pricing between the two locks. The second loan will be canceled and will count against the Correspondent’s fallout percentage.

The original loan is canceled and a new loan, with the same property address, is locked ≤ 30 days from the cancellation date,

Worst case pricing and applicable relock fee will apply, in addition to all previous relock and extension fees. The second loan will be canceled and will count against the Correspondent’s fallout percentage.

Note: In the event that the Correspondent locks a loan Mandatory with the same property address more than once and both locks are active, the second loan will be canceled and subject to a pair-off fee and count towards the Correspondent’s fallout percentage.

6.2.4.4 Fallout FGMC will monitor the Correspondent’s fallout percentages. FGMC will contact any Correspondent with excessive fallout percentages (typically over 20%) to determine the origin.

6.2.4.5 Lock Periods The standard lock periods include 15, 30, 45, and 60 days, however extended locks are available. Remember that before a lock can be tracked and confirmed from FGMC’s system, the loan must be registered in the portal. Additionally:

• Loans must be in Approval status prior to lock expiration (i.e. cleared for purchase) o The closed loan package must be received, AND o Loan has been reviewed and cleared by FGMC Due Diligence for all prior-to-purchase (suspense)

conditions. • Closed loan packages delivered to FGMC by 5 p.m. ET on the day of lock expiration, will receive a free,

automatic 10-day extension. The 10-day free extension will provide additional time to clear prior-to-purchase suspense conditions.

• If the loan has not been cleared for purchase after the free 10 days, automatic extensions will be charged per the rate sheet in increments of 15 days.

• After 45 days of automatic extensions at a charge, the lock will expire and is subject to re-lock or pair-off fees per this policy.

Note: Lock Periods section of this policy DO NOT apply to Mandatory Trade Desk loans. Loans must be delivered to FGMC in fundable condition (credit and closed loan package) before 5:00 PM ET on day of lock expiration. If

First Guaranty Mortgage Corporation ®

Version 1.9 Correspondent Lending Seller Guide 22 CONFIDENTIAL DOCUMENT First Guaranty Mortgage Corporation must give prior written permission for this work, or any part thereof, to be used, reproduced, or transmitted in any form or by any means, by or to any party outside of First Guaranty Mortgage Corporation, its regulators and investors.

FGMC detects a deficiency during the funding review process, suspense conditions will be issued via the online portal for the Correspondent to access or through direct email contact with the Correspondent. It is the Correspondent’s responsibility to review and clear these suspense items quickly in order to avoid extension charges.

6.2.4.6 Lock Expiration Date When the initial lock expiration date falls on a weekend or holiday, the lock expiration date is automatically moved to the next business day.

Loans must be delivered in fundable condition (credit and closed loan package) on or before 5:00 PM ET on the day of lock expiration date. Loans delivered after the lock expiration date will be subject to FGMC re-lock policies. A free 10-day extension will provide additional time to clear any prior-to-purchase suspense conditions, if applicable.

6.2.4.7 Lock Extensions (Only applies to lock extensions done prior to delivery of loan to FGMC. Otherwise, charged Auto Extensions apply as listed in “Lock Periods” section of this policy.) Correspondent Sellers may request an extension on or before the lock expiration date. If a lock is expired an extension may not be requested and the loan must be relocked. When requesting an extension before the lock expiration date, the request may only be submitted and will only be granted by FGMC when the loan is within 15 days of lock expiration. For example, if a loan is locked on the 1st of the month for 30 days then an extension can be submitted any day after the 16th of that same month. The number of days selected for extension will be added to the expiration date. Lock extension days are available in 7, 15, or 30 day increments at the extension price listed on the FGMC Correspondent Rate Sheet. See below for the maximum number of extensions and the total maximum of extension days.

Conforming Max extension requests 3

Max extension days 45

Extension Days Extension Cost 7 Days (.125) 15 Days (.250) 30 Days (.500)

All extension requests done prior to delivery of loan to FGMC must be submitted online. FGMC will only accept email extension request for loans that were originally locked manually.

6.2.4.8 Relocks Relocks may only be submitted on expired locks. If a loan has been expired for at least 30 days, then it is considered a new lock and pricing will be based on current market. Loans that have been expired for less than 30 can be relocked for 15 or 30 days (Correspondent Rate Sheet). Relocks for loans expired for less than 30 are subject to worse case pricing plus the applicable relock fee, and all previous extension/relock fees. Relock fees can be found on the table below. Loans may only be relocked one time.

Relock Days Relock Fee 15 Days (.250) 30 Days (.500)

Note: Relock fee applied to FGMC Delegated and Non-Delegated Rate Sheets only. If at the time of Relock the rate has increased, the worst of pricing between existing price and current price on the new rate lock will apply. If at the time of Relock the product is changed, the worst of pricing between the existing price on the original

First Guaranty Mortgage Corporation ®

Version 1.9 Correspondent Lending Seller Guide 23 CONFIDENTIAL DOCUMENT First Guaranty Mortgage Corporation must give prior written permission for this work, or any part thereof, to be used, reproduced, or transmitted in any form or by any means, by or to any party outside of First Guaranty Mortgage Corporation, its regulators and investors.

product and the current price on the new product will apply. The price may not improve regardless of product change.

6.2.4.9 Renegotiations Correspondents may submit a Renegotiation Request from the time the first Rate Sheet is generated until 4:00 PM ET to [email protected]. Correspondents are responsible for calculating the renegotiated gross price using the Renegotiated Price Calculation below. The renegotiation price is based on the FGMC Correspondent Rate Sheet that is in effect when the request is received. Requests received after 4:00 PM ET will not be processed and a new request must be submitted the next business day within the renegotiation hours listed in this policy.