fa assignment

TRANSCRIPT

1 | P a g e

Faculty of Business

Submission of Group Assignments: Cover Sheet

Date of Assignment: 08.2016 Due Date: 08.2016

Date of Submission: 08.2016

1. Course: Bachelor of Business Administration

2. Year: 1 3.Semester: 1 4.Module Code: BM111

5. Module Name: Fundamentals of Accounting

6. Lecturer-in-charge: Ms. Shashitha Jayakody

7. Title of assignment: Sources of Finance

8. Supervisor:

Declaration:

We certify that:

• This assignment is my/our own work, based on my/our personal study and/or research.

• I/We have duly acknowledged all material and sources used in the preparation of this assignment.

• Neither the assignment, nor a substantial part of it, has been previously submitted for assessment in SLIIT

or any other institution.

• I/We have not copied in part, or in whole, or otherwise plagiarized the work of other students. I/We are

fully aware of the rules and regulations of SLIIT regarding plagiarism and exam malpractices. I/We

understand that I am/all of us are liable to bear the consequences of (anyone involved in) plagiarism.

• The use of any material in this assignment does not infringe the intellectual property/copyright of a third

party.

• All resources documents/reference materials are attached to this document.

Student ID Student Name Signature Contribution %

BM16432376 Nadishan G.S.W.Y. 20%

BM16428034 Samaratunga Y.A.M.S. 20%

BM16429024 Nawarathna N.M.D. 20%

BM16430532 Wijesooriya W.A.D.I. 20%

BM14406386 Galigomuwe N.G.J. 20%

2 | P a g e

TABLE OF CONTENTS

1. Abstracts……………………………………………………………….....3

2. Acknowledgement………………………………………………………..4

3. Introduction……………………………………………………………….5

4. What is source of finance………………………………………………....6

5. Internal financial sources of Lucky Lanka PLC…………………………..7

a. Own capital………………………………………………..8

b. Working capital…………………………………………..10

c. Sales of assets…………………………………………….11

d. Provision of depreciation…………………………………12

e. Retained profit……………………………………………13

6. External financial sources of Lucky Lanka PLC…………………………14

a. Share issuance……………………………………………15

b. Bank loans………………………………………………..18

c. Bank overdrafts…………………………………………..20

d. Leasing…………………………………………………...21

e. Hire purchasing…………………………………………...23

7. Conclusion………………………………………………………………...24

8. Recommendation………………………………………………………… 25

9. References………………………………………………………………...26

3 | P a g e

1. Abstracts

This report was furnished to describe the various financial sources of Lucky Lanka Milk

Processing PLC to their day to day activities in order to grow and change over time.

Lucky Lanka Milk Processing PLC is one of the leading Sri Lankan brand names which

earned fame of bringing Sri Lanka’s name to global level. Lucky Lanka Milk Processing PLC

is very popular among Sri Lankans. Because of it is ingeniousness and it helps to consolidate

Sri Lankan farmers. Lucky Lanka Milk Processing PLC is recently listed in Colombo Stock

Exchange also.

Lucky Lanka Milk Processing has to raise funds through various sources in order to execute

their day to day operations as well as company’s growth. This report discuss about Lucky

Lanka Milk Processing PLC financial sources.

4 | P a g e

2. Acknowledgement

We as a group of student of SLIIT would like to express our profound gratitude to Ms.

Shashitha Jayakodi for her constant encouragement throughout this assignment in order to

make this task fulfill.

Secondly we would like to thank Mr. G.S.W. Hareendra who is the regional marketing

manager of Lucky Lanka Milk Processing PLC supported us by providing these valuable

information in prompt manner to achieve this task.

Last but not least we would like to express our thanks to the staff of Lucky Lanka Milk

Processing PLC for their co-operation during this assignment.

5 | P a g e

3. Introduction

This report is furnished to explain how Lucky Lanka Milk Processing PLC fulfills their

financial requirements through various resources to execute their day to day activities as well

as business growth. Lucky Lanka Milk Processing PLC was established in 1991 and that time

it was quite a small scale business and now it has expanded to vast level through past 2 & ½

decades and they have registered under Companies Act No. 7 of 2007 and recently listed in

Colombo Stock Exchange also. This company privileges Sri Lankan indigenous milk farmers

to uplift their businesses as well as to consolidate Sri Lanka’s rural economy. In this report

we discuss about how this company satisfy their financial requirements.

Basically we have recognized some financial resources of the company we have categorized

two main headings; ‘Internal Financial Resources’ and ‘External Financial Resources’. Under

internal financial resources we can recognize own capital, working capital, sales of assets,

provision of depreciation and retained profit. External resources are share issuances (voting

and non-voting), bank loans, over drafts, leasing, hire purchasing.

In this assignment we are going to explain each resource which we have mentioned in the

above paragraph thoroughly. Furthermore we hope to discuss about the situations where the

company uses those financial resources as well as advantages and disadvantages of them.

6 | P a g e

4. What is source of finance?

Finance is a compulsory segment for every business from the beginning to throughout its

entire life time. Basically we can see day to day finance requirement for any business in the

need world as well as there are some finance requirement can be generated in the long run

when the business organization wants to improve or expand their business. Finance is not

only a require to carry out their day to day activities but also this is very critical when some

important factors come to play such as expansion of business, increase the product range,

acquiring another business and etc.

Finance resources can be easily introduced as how particular business organization raise their

funds for different activities. Finance resources are very critical when considering the

liquidity of a business organization. At a given time business organizations have various

ways to raise their funds and each organization chooses and appropriate option by

considering their stability, easiness (readiness), accessibility and etc. Business organization

can basically raise their funds in two main ways; internal resources and external resourses.

7 | P a g e

5. Internal financial sources of Lucky Lanka PLC

In this chapter we are going to discuss about internal financial sources and how they effect on

company’s financial requirements as well as advantages and disadvantages of each source.

We are going to explain about some internal financial source which we have recognized in

Lucky Lanka Milk Processing PLC as follow.

1. Own Capital

2. Working Capital

3. Sales of Assets

4. Provision of Depreciation

5. Retained Profit

8 | P a g e

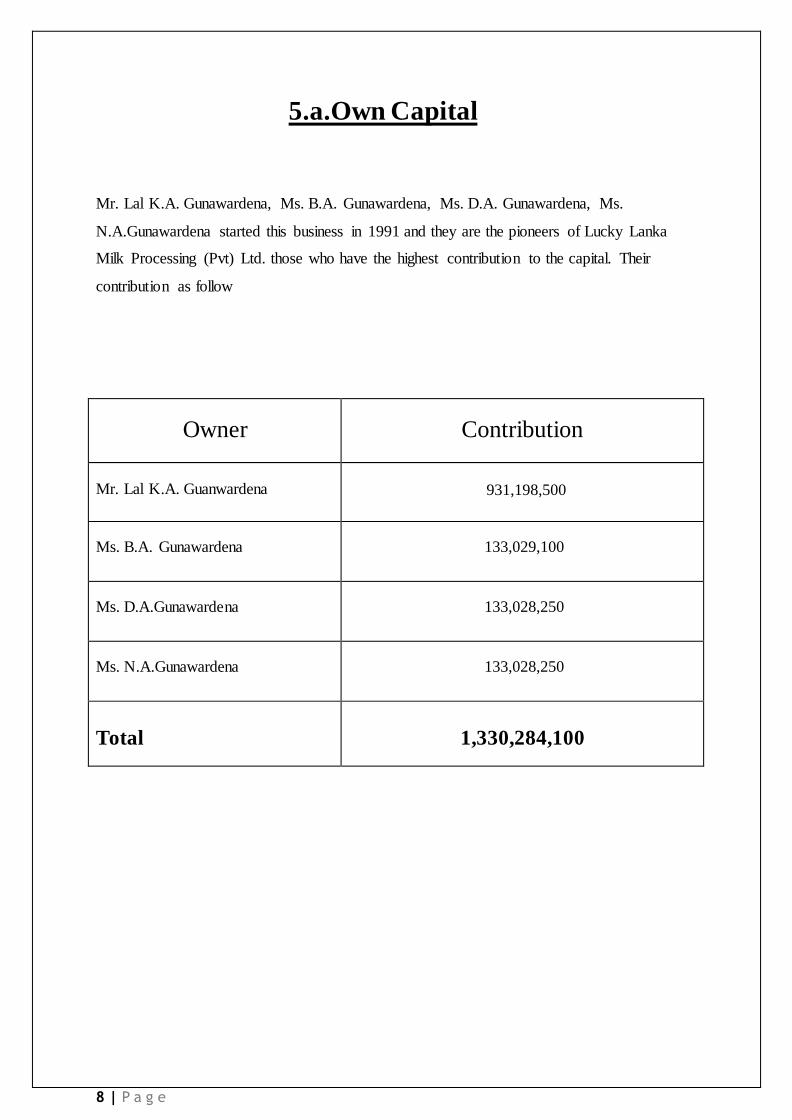

5.a.Own Capital

Mr. Lal K.A. Gunawardena, Ms. B.A. Gunawardena, Ms. D.A. Gunawardena, Ms.

N.A.Gunawardena started this business in 1991 and they are the pioneers of Lucky Lanka

Milk Processing (Pvt) Ltd. those who have the highest contribution to the capital. Their

contribution as follow

Owner

Contribution

Mr. Lal K.A. Guanwardena

931,198,500

Ms. B.A. Gunawardena

133,029,100

Ms. D.A.Gunawardena

133,028,250

Ms. N.A.Gunawardena

133,028,250

Total

1,330,284,100

9 | P a g e

Advantages of Own Capital

1. Generated among owners, therefore no need to pay fixed pay back outside party.

2. Provided by the owners and it motivates them to improve and growth the business.

3. In case of profit loss or bankrupt this has lenient payback procedures.

Disadvantages of Own Capital

1. Government taxes are applied.

10 | P a g e

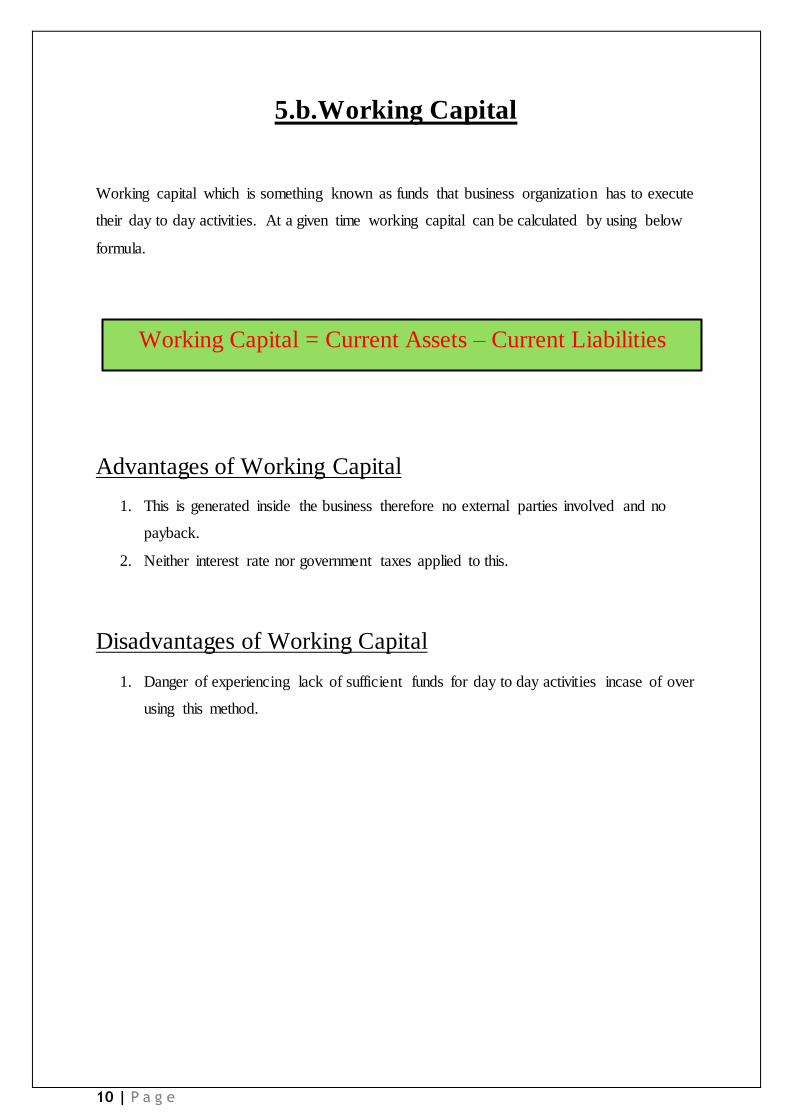

Working Capital = Current Assets – Current Liabilities

5.b.Working Capital

Working capital which is something known as funds that business organization has to execute

their day to day activities. At a given time working capital can be calculated by using below

formula.

Advantages of Working Capital

1. This is generated inside the business therefore no external parties involved and no

payback.

2. Neither interest rate nor government taxes applied to this.

Disadvantages of Working Capital

1. Danger of experiencing lack of sufficient funds for day to day activities incase of over

using this method.

11 | P a g e

5.c.Sales of Assets

This is another internal source of raising funds by selling business’s own assets. By this

method company can generate money for its capital needs. This source falls under short or

long term finance depending on what kind of assets are sold. By selling something like a

motor vehicle they can cater their short term small financial requirements. If they sell land or

building they can cater to long term and bigger finance needs.

Advantages of Sales of Assets

1. Sold to raise cash.

2. Makes sense to dispose of underused assets.

3. Finance development without extra borrowing.

4. They can sale and lease it back.

5. Loses assets but has the use of the cash.

Disadvantages of Sales of Assets

1. Time taken to sell the assets.

2. Advertising and other expenses (Stamp fee)

3. Lose of an asset.

12 | P a g e

5.d.Provision of Depreciation

Some assets as machineries, vehicles etc. have used full life time and expenses are allocated

certain amount of money based of particular method (Straight-line method and Reducing

Balance method) to reestablish the certain asset after its useful life time. This is another

internal finance resource of Lucky Lanka Milk Processing PLC because they have lot of

machineries involved in their business.

Advantages of Provision Depreciation

1. No government taxes apply.

2. Nil cost involved (except calculation cost)

3. Long term basis and comparatively very low amount is allocated certain time period

hence company generated necessary funds gradually.

Disadvantages of Provision Depreciation

1. Difficult to make predictions of life time and end value therefore accuracy is reduced.

2. More assets show significant expenses.

13 | P a g e

Retained profit = Net profit - Dividends

5.e.Retained Profit

Retained profit is something known as the sum of the profit which remains after paying

dividends to shareholders. This source falls under long term financial source for the company

and this does not have many fixed day of maturity like debentures. After certain period of

time companies issues ordinary shares in order to raise their stated capital as well as to attract

new investors to the business. This source of finance is only available for a business which

has been trading for more than one year.

Advantages of Retained Profit

1. Doesn’t have to be repaid.

2. No interest is payable.

3. No government taxes apply.

4. Can attract new investors.

Disadvantages of Retained Profit

1. Not available to a new business.

2. Demoralizing investors due reduce dividends (earnings)

3. Does not generate any income to the company for the period that their holding it.

14 | P a g e

6. External financial sources of Lucky Lanka PLC

External financial resources are the methods of raising funds with outside parties involvement

Lucky Lanka Milk Processing PLC as a company with huge operations as well as a listed

company they have vast range of external financial resources, some of them as follow.

1. Share issuances

2. Bank loans

3. Bank overdrafts

4. Leasing

5. Hire Purchasing

In this chapter we are going to discuss about external financial sources and how they effect

on company’s financial requirements as well as advantages and disadvantages of each source.

15 | P a g e

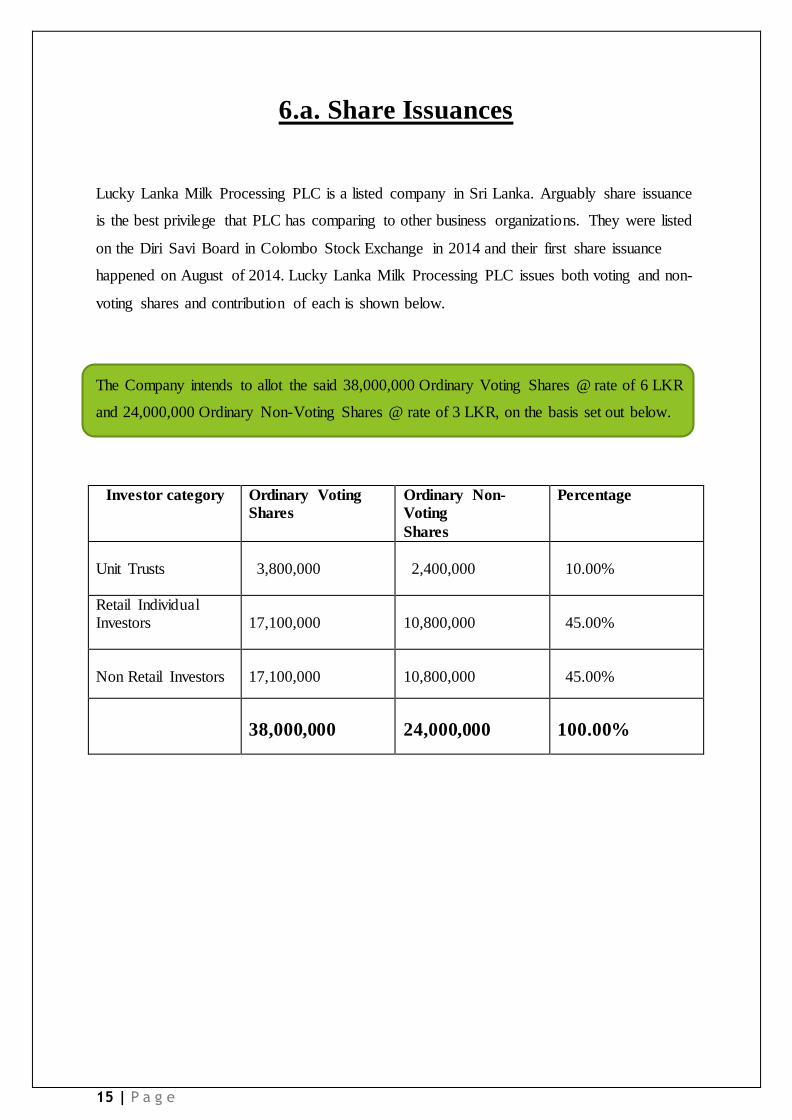

6.a. Share Issuances

Lucky Lanka Milk Processing PLC is a listed company in Sri Lanka. Arguably share issuance

is the best privilege that PLC has comparing to other business organizations. They were listed

on the Diri Savi Board in Colombo Stock Exchange in 2014 and their first share issuance

happened on August of 2014. Lucky Lanka Milk Processing PLC issues both voting and non-

voting shares and contribution of each is shown below.

The Company intends to allot the said 38,000,000 Ordinary Voting Shares @ rate of 6 LKR

and 24,000,000 Ordinary Non-Voting Shares @ rate of 3 LKR, on the basis set out below.

Investor category Ordinary Voting

Shares Ordinary Non-

Voting

Shares

Percentage

Unit Trusts

3,800,000

2,400,000

10.00%

Retail Individual Investors

17,100,000

10,800,000

45.00%

Non Retail Investors

17,100,000

10,800,000

45.00%

38,000,000

24,000,000

100.00%

16 | P a g e

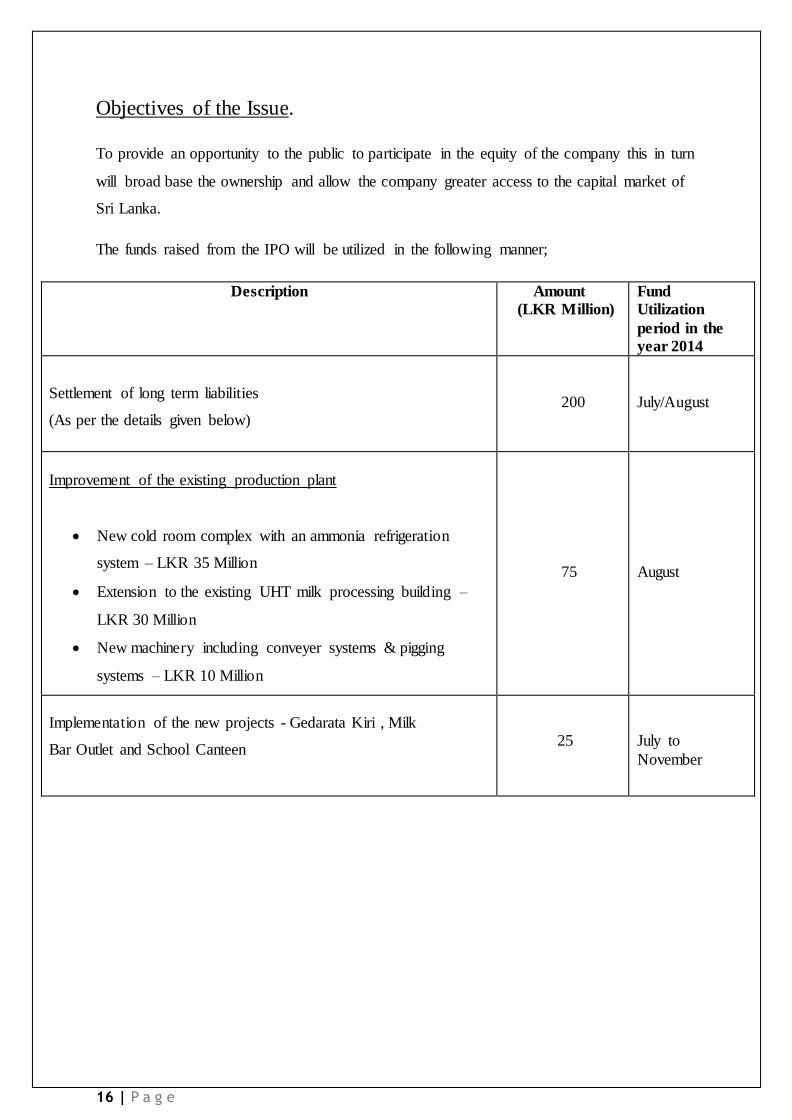

Objectives of the Issue.

To provide an opportunity to the public to participate in the equity of the company this in turn

will broad base the ownership and allow the company greater access to the capital market of

Sri Lanka.

The funds raised from the IPO will be utilized in the following manner;

Description Amount

(LKR Million) Fund

Utilization

period in the

year 2014

Settlement of long term liabilities

(As per the details given below)

200

July/August

Improvement of the existing production plant

New cold room complex with an ammonia refrigeration

system – LKR 35 Million

Extension to the existing UHT milk processing building –

LKR 30 Million

New machinery including conveyer systems & pigging

systems – LKR 10 Million

75

August

Implementation of the new projects - Gedarata Kiri , Milk

Bar Outlet and School Canteen

25

July to

November

17 | P a g e

Advantages of Share Issuances

1. Dividend is variable with profit as well as not to be paid in case of lose.

2. Assets are not subjected to reduce when issuing.

3. In case of bankrupt or any other unexpected condition shares have least propriety to

pay back.

4. This is a privilege of PLC which helps to raise huge amount of funds as well as

contribute many investors.

5. Permanent source. (when required can issue)

Disadvantages of Share Issuances

1. Can result loss of control from its initiator.

2. Have to share company’s profit.

3. Issuance cost.

18 | P a g e

6.b. Bank Loans

Lucky Lanka Milk Processing PLC has taken loans of 164,698,318 LKR to consolidate

company’s infrastructure .These loans were taken from various financial institutions such as

licensed commercial banks and registered finance companies. Below table shows the

contribution of loans to Lucky Lanka Milk Processing PLC financial flow.

Name of Registered Finance

Companies

Type of the Loan Amount outstanding as at

31-03-2014 (LKR)

Mercantile Investment

Term Loan

7,114,960

Asia Assets Finance PLC

Term Loan

2,356,266

Name of Licensed Commercial

Banks

Type of the Loan Amount outstanding as at

31-03-2014 (LKR)

Union Bank PLC

Term Loan

110,751,718

Commercial Bank PLC

Term Loan

9,301,821

NDB Bank PLC

Term Loan

35,173,553

19 | P a g e

Advantages of Bank Loans

1. Set repayments are spread over a period of time which is good for budgeting.

2. Can raise significant amount of funds.

Disadvantages of Bank Loans

1. Can be expensive due to interest payments.

2. Bank may require security on the loan.

3. Time taken is quite high.

20 | P a g e

6.C. Bank Overdrafts

This is a facility of current account holders to manage their instance financial requirements.

This facility is known as the privilege to draw (issue) cheques than the remaining balance of

the account. This is very easy method but interest rate is very high. Commercial banks issue

two types of overdrafts which are known as ‘permanent overdraft’ and ‘temporary overdraft’.

Lucky Lanka Milk Processing PLC uses both types of overdrafts to fulfill their temporary

financial requirements.

Advantages of Bank Overdrafts

1. Easy to use this facility.

2. Almost no paper works involved.

3. Can access easily as when company need.

Disadvantages of Bank Overdrafts

1. Very high interest rate to be paid.

2. Amount that can be raised through this method is comparatively low.

21 | P a g e

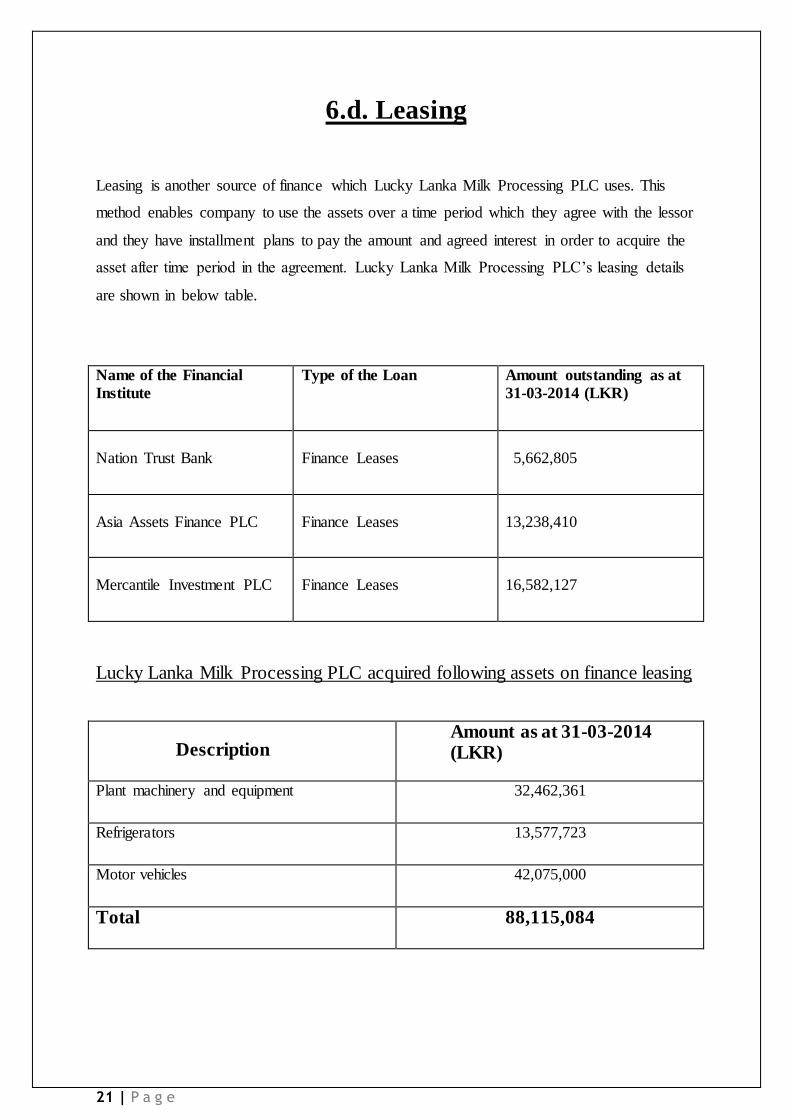

6.d. Leasing

Leasing is another source of finance which Lucky Lanka Milk Processing PLC uses. This

method enables company to use the assets over a time period which they agree with the lessor

and they have installment plans to pay the amount and agreed interest in order to acquire the

asset after time period in the agreement. Lucky Lanka Milk Processing PLC’s leasing details

are shown in below table.

Lucky Lanka Milk Processing PLC acquired following assets on finance leasing

Name of the Financial

Institute Type of the Loan Amount outstanding as at

31-03-2014 (LKR)

Nation Trust Bank

Finance Leases

5,662,805

Asia Assets Finance PLC

Finance Leases

13,238,410

Mercantile Investment PLC

Finance Leases

16,582,127

Description Amount as at 31-03-2014 (LKR)

Plant machinery and equipment 32,462,361

Refrigerators 13,577,723

Motor vehicles 42,075,000

Total 88,115,084

22 | P a g e

Advantages of Leasing

1. No need to pay entire price of an asset to use it.

2. Payments are made as installments hence gradually funds are going away from the

company and simultaneously they can use the asset as well.

3. Time taken for the process is comparatively low. (Paper work)

Disadvantages of Leasing

1. Fixed interest to be paid.(high cost)

2. In case of failure to pay installments according to agreement may lose the asset as

well the payments made.

23 | P a g e

6.e. Hire Purchasing

This is an agreement of owner of asset let the company use the asset on hire where hirer

(Lucky Lanka Milk Processing PLC) has to pay regular installment, by the time hirer made

all payments hire is allegeable to purchase the asset. These periodic payments are also

included an interest other than the price of the asset.

Advantages of Hire Purchasing

1. Immediate without making the full payment company is eligible to use the

asset.(obtain benefits by using the asset)

2. Expensive assets can be utilized as the payment is spread over a period of time.

3. Easy to access as well as no guarantee to be shown in order to obtain privileges of

hire purchasing.

4. Fixed rental payments make budgeting easier as all the expenditures are known in

advance.

5. Possibility of granting the ownership of the asset after the agreed time.

Disadvantages of Hire Purchasing

1. Company has to pay an interest other than the price of the asset.

2. To obtain the legal authority over the asset have to make the entire payment which

interest included.

3. Company’s funds are going away for a longer period.

4. In case of changing company strategy or any other condition which resulting the

asset unessential company is subject to penalty.

24 | P a g e

7. Conclusion

Lucky Lanka Milk Processing PLC is Sri Lankan leading dairies production supplier and

throughout this assignment we have recognized various sources of finance which are used by

the company. We as a group of students following business management degree understood

pros and cons of each source further more we have learnt that financial sources can be

categorized in various methods such as internal and external, short time period and long time

period and etc. In this study we have realized that Lucky Lanka Milk Processing PLC uses

more external sources to raise their funds and they are obtaining the privileges of PLC as

well. Choosing the most appropriate alternate among the available methods to raise funds is

very crucial to any business organization.

25 | P a g e

8. Recommendation

We would like to recommend Lucky Lanka Milk Processing PLC to issue ‘debentures’ as

well because of various reasons such as

1. More preferred by investors.

Investors would like to invest on debentures because safety of the investment hence

company can raise more funds.

2. Management is not subject to change.

No voting rights granted by the investors those who invest on debentures.

3. Company can invest on long time framed projects.

This is a reliable source and company has clear idea about the funds raised by

debentures.

4. Can obtain tax relief because debentures are recognizing as loans.

Income tax relief for the interest paid to debentures hence debentures are recognize as

loan.

5. When inflation existing in the economy it is an advantage to the

company.

When inflation occurs in the economy the exact interest paid is less.

6. Less Costly.

No need to pay dividends only fixed amount of interest paid.

26 | P a g e

9.References

1. http://www.cse.lk/company_info.do

2. http://colombostockwatch.com/company/lucky- lanka-milk-processing-company- llmp-

n0000/

3. http://www.luckylanka.lk/

4. https://www.cse.lk/cmt/upload_report_file/1365_1441970985492.pdf

5. http://www.luckylanka.com/images/Lucky-Lanka-Initial-Public-Offering-

Prospectus.pdf

6. http://www.businessdictionary.com/

7. http://www.investopedia.com/