export taxes, industrial policy and the value chain in ... · export taxes, industrial policy and...

TRANSCRIPT

Export Taxes, Industrial Policy and the Value

Chain in China After WTO

Jason GarredLondon School of Economics

January 2014

FOR GEP POSTGRADUATE CONFERENCE APPLICATIONPRELIMINARY - PLEASE DO NOT CIRCULATE OR CITE

Abstract

Well-known results in international trade theory suggest that govern-ments may achieve equivalent improvements in their terms of trade viamore than one set of policy instruments. So it is puzzling that importtariffs are usually seen as the main instrument of trade policy worldwide,and that the decline in trade restrictiveness associated with GATT andWTO has not, as far as we know, been followed by substitution towardsother policy instruments not covered by those agreements. In this paper,I carefully document changes in China’s export policies over a ten-yearperiod after its accession to WTO, and find that China’s average exporttax rates increased significantly during this time. This occurred mainlyvia decreases in rates of VAT refunds for exporters, a policy not coveredby WTO rules. However, I find little evidence that the sectoral distri-bution of China’s post-WTO export tax rises is consistent with terms-of-trade concerns. Instead, both empirical evidence and statements frompolicymakers suggest the presence of ongoing industrial policy favouringdownstream industries: China’s export tax increases are concentrated inindustries where its WTO-induced import tariff cuts were smallest, and asubstantial part of this relationship is explained by relatively larger cutsto tariffs on processed goods being followed by relatively larger rises inexport taxes on raw materials. I thus suggest a simple theory of unilateraltrade policy in the context of a two-stage value chain in which policymak-ers’ aim is to move domestic factors into downstream sectors at minimumshort-run cost to real income. In this model, an import tariff on processedgoods is the preferred policy, while an export tax on raw materials, if fea-sible, may achieve the same goal but with inferior terms-of-trade effects.

1 Introduction

It is a longstanding result in the theory of international trade that a given out-come desired by a government may be achieved through more than one set of

1

policy instruments. Textbooks often introduce students to the theory of tradepolicy by showing that either a unilateral import tariff or a unilateral export taxmay improve domestic welfare by raising the world price of a country’s exportsrelative to its imports. Yet it is import tariffs rather than export taxes thatare generally acknowledged to be the key instruments of real-world trade policy.Moreover, although the international negotiations associated with the GeneralAgreement on Tariffs and Trade (GATT) and the World Trade Organization(WTO) are credited with decreasing the restrictiveness of trade policy world-wide, mainly via large reductions in average import tariffs, these agreementsdo not cover all possible instruments of trade policy. If these agreements leaveroom for such policies to be continued via other instruments, is there a reasonwhy governments do not substitute towards these, or have we simply failed toobserve such substitution in practice?

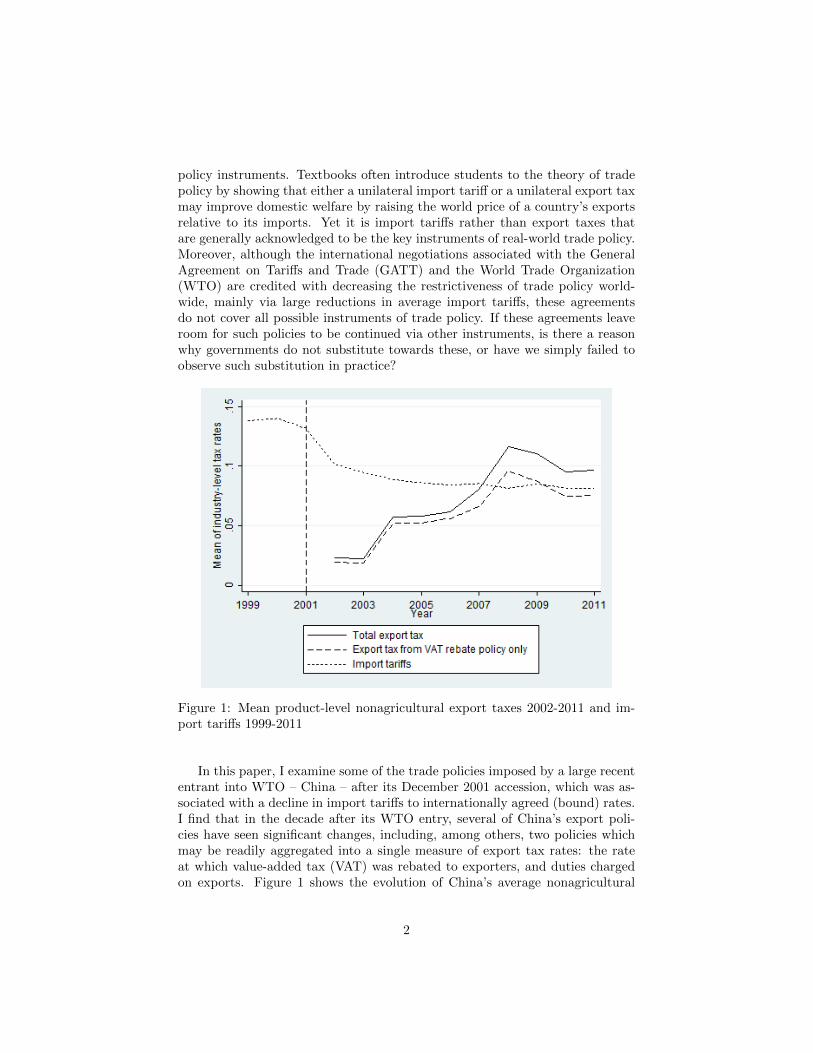

Figure 1: Mean product-level nonagricultural export taxes 2002-2011 and im-port tariffs 1999-2011

In this paper, I examine some of the trade policies imposed by a large recententrant into WTO – China – after its December 2001 accession, which was as-sociated with a decline in import tariffs to internationally agreed (bound) rates.I find that in the decade after its WTO entry, several of China’s export poli-cies have seen significant changes, including, among others, two policies whichmay be readily aggregated into a single measure of export tax rates: the rateat which value-added tax (VAT) was rebated to exporters, and duties chargedon exports. Figure 1 shows the evolution of China’s average nonagricultural

2

export taxes across industries by this measure starting in 2002: while importtariffs fell towards their bound levels, export taxes rose by an average of 7%across industries between 2002 and 2011. This was mostly due to changes inVAT rebate policy, an instrument not covered by GATT/WTO.1

The imposition of export taxes after import tariffs are removed appears con-sistent with theoretical results in the optimal trade policy literature. In a recentcontribution, Costinot et al. (2013) have characterized the set of unilateral op-timal trade policies in a two-country, multi-sector Ricardian framework, findingthat domestic real income may be maximized with, among other policies, a uni-form positive tariff accompanied by export subsidies or a set of export taxesalong with zero barriers to imports.2 The emergence of export taxes thus seemsto be a natural response to the cuts in import tariffs and prohibition of exportsubsidies required as a condition of WTO accession, due to these terms-of-tradeconsiderations.

However, statements from policymakers about China’s post-WTO exportpolicies do not appear to focus on their effects on the terms of trade. They in-stead tend to suggest that these policies were set with industrial policy in mind,and in particular by a desire to ‘move up the value chain’ – i.e. to stimulateprocessed goods industries using export restrictions on their raw materials:3

China’s industrial strategy is to leverage and exploit the differencesin the international and domestic markets for raw materials anddownstream, processed products, using restraints on exports as thelinchpin. – US government submission to China - raw materialsWTO dispute (WTO 2011)

Resource-rich regions all want to expand into the more-profitabledownstream processing sectors instead of just supplying the rawmaterials, said a government official with Baotou city in the InnerMongolia Autonomous Region, one of China’s major mining centers.– Wall Street Journal, August 2010

We are certainly not focusing on the short-term benefits of raisingthe rare earth price. Our wish is for Baotou in Inner Mongolia tobecome the world’s ‘Rare Earths Valley’, the world’s rare earths in-dustrial base. – Zhao Shuanglian, Vice Chairman of Inner Mongolia,September 2009 (china.com.cn 2009)

Below, I attempt to understand the determinants of the post-WTO growthin China’s export taxes by testing both the terms-of-trade and industrial policy

1China has argued that its export duties are also consistent with its GATT/WTO commit-ments, but this has been challenged by the US and EU using the WTO’s dispute settlementmechanism; see Section 2.1 below for a full discussion.

2Lerner (1936) demonstrates the symmetry between an import tariff and an export tax ina two-sector model.

3While this characterization emphasizes the intended encouragement of a particular set ofindustries, the policies are also often portrayed using an alternative industry-level rationale:the discouragement of ‘highly polluting, energy-intensive’ industries.

3

hypotheses using variation in export tax growth across products and industries.First, while standard models of optimal trade policy would suggest that China’sexport tax rates should increase in China’s market power, I find little evidencethat rises in export taxes between 2002 and 2011 were correlated with either oftwo product-level proxies of market power: the market share of Chinese goodsin total world trade and the import demand elasticities of its largest tradingpartner during the period, the United States.

However, the data does provide evidence for the claim that China’s tradepolicy has been driven by ongoing industrial policy preferences, as I find thatgrowth in export taxes after WTO accession was significantly larger in indus-tries that experienced smaller WTO-induced decreases in import tariffs. Inother words, the largest increases in support via trade policy (in the form ofsmaller export taxes, and thus relatively larger export subsidies) were affordedto industries that had experienced the largest falls in such support due to thetariff cuts associated with WTO accession.

Using several different definitions of ‘raw materials’, I also confirm that in-creases in export taxes in China have been significantly larger for raw materialsindustries than for industries producing processed goods. I then show that thisrelationship accounts for a large part of the correlation between rises in exporttaxes and WTO-induced declines in import tariffs. Thus, while the extent of‘tariff escalation’ – larger tariffs on processed goods than on raw materials –in China’s tariff schedule declined as a result of WTO accession, this has sincebeen replaced with rising gaps between export taxes on these two stages ofproduction.

Having established these stylized facts about China’s policies, I suggest asimple theory of unilateral trade policy when industrial policy preferences fordownstream goods are the primary motivation for conducting trade policy. Inparticular, I model a two-stage value chain in which the aim of policymakers isto move a fixed proportion of domestic factors into downstream sectors, but thepolicy by which this is accomplished is chosen according to a standard staticreal income maximization problem. Of the four simple trade policies considered– an import tariff or export subsidy on downstream sectors, or an export taxor import subsidy on raw materials – I show that in a two-country symmetricframework, an import tariff on downstream goods is strictly preferred. This isbecause although the import tariff is one of two policies that improve domesticterms-of-trade, the other such policy – the export tax on raw materials – has twokey disadvantages: its effects on raw materials prices are partly passed throughto domestic consumers via imports of foreign goods, and it leads to inefficientchanges in the global allocation of factors across the two stages of production.

I then briefly explore the relevance of this theory for trade policy outsideChina, noting that the observed import tariff and export tax policies of othercountries are also consistent with a preference for downstream sectors. However,few countries share the land endowments and capital stock that have madeChina a leading producer of a wide range of raw materials, suggesting a possibleexplanation for the apparent rarity of export taxes in practice: an unwillingnessto shift production away from desirable downstream sectors, along with the

4

inability of many countries to use taxes on exports of raw materials in order tostimulate them.

This paper contributes to the wider trade policy literature on several dimen-sions. First, it forms part of an active empirical literature on the determinants oftrade policy. Some of this literature has focused on the compatibility of observedtrade policies with theories in which welfare gains occur via improvements incountries’ terms of trade. These studies have used data on such policy instru-ments as noncooperative tariffs (Broda, Limao and Weinstein 2008), cooperativetariffs (Bagwell and Staiger 2011) and antidumping tariffs (Bown and Crowley2013); one innovation of this paper is to conduct such a test using variation inexport taxes rather than import policies. The paper also informs another branchof this literature that considers the relative importance of terms-of-trade con-siderations and industry-level determinants, usually political-economy factors,in trade policymaking (e.g. Goldberg and Maggi 1999).

The paper also relates to the literature exploring the symmetry betweendifferent trade policy instruments. Lerner’s (1936) two-sector study of symmetrybetween export taxes and import tariffs has been extended to various morecomplex contexts; like this paper, McKinnon (1966) explores the topic in amodel with intermediate goods. Few papers have attempted to reconcile thissymmetry with the relative rarity with which export taxes are observed, thoughEthier (2004, 2007) has twice made theoretical contributions to this question.

Empirical studies of export taxes are relatively rare, partly because of thescarcity of export tax data; both the dataset and the empirics in this paper thusserve as contributions to the trade policy literature in this sense. An importantrecent dataset has been compiled by Solleder (2013), who identifies 111 countriesimposing export taxes and compiles product-level panel data on export tax ratesfrom twenty of these. Although Solleder’s dataset of tax rates includes China, itincorporates only China’s export duties and not its VAT rebate or other exportpolicies. The OECD has also recently collected data on export restrictions; seeKim (2010) and Fliess and Mard (2012).

As I will discuss below, many researchers have commented on the existenceof ‘tariff escalation’, higher tariffs on processed goods as compared to raw ma-terials. Like this paper, a subset of these studies also discuss the relative exporttax rates of these two stages of production, including Golub and Finger (1979)and Latina, Piermartini and Ruta (2011). Dixit and Grossman (1982) studyoptimal trade policy in the context of multistage production.

Finally, the paper adds to a growing literature on trade policy in China,which has mostly focused on the effects of its recent policy changes rather thantheir determinants. Chandra and Long (2013) calculate the elasticity of Chineseexports to VAT rebate rates, using firm-level data on VAT payments. Khandel-wal, Schott and Wei (2013) examine the impact of the local institutional reformassociated with the removal of externally imposed export quotas on textiles andapparel after the end of the Multifiber Arrangement. Chen and Ravallion (2004)and Brandt et al. (2012) consider the effects of the tariff cuts associated withWTO accession, at the household and firm level respectively.

The remainder of the paper is laid out as follows. Section 2 introduces the

5

two export policies (export VAT rebates and export duties) that will be thepaper’s primary focus, conducts an empirical analysis of their determinants andthen checks whether these two policies have been complemented or offset bychanges in China’s other export policies during this period. Section 3 presentsthe theoretical framework. Section 4 then discusses the real-world relevance ofthe paper’s theoretical findings and draws conclusions.

2 Export taxes in China after WTO

2.1 China’s export tax policies

This section will discuss two types of export policies that have been substantiallyamended in China since 2002: rebates of VAT for exporters and export duties.Both policies vary at the product level; lists of products subject to export dutiesand the corresponding rates are published by China annually along with itsschedule of import tariffs, while the calculation of VAT for exporting firmsdepends on the VAT rebate rates for which their exported products are eligible,which are updated and disseminated on an ad hoc basis. Since the officialrebate rates for many products are lower than the rate of VAT, the latter policyis effectively also an export tax; as noted by Feldstein and Krugman (1990), in asystem where countries charge VAT on imports (as do China and other countrieswith value-added taxes), the nondistortionary policy is for countries to also fullyrebate VAT on exports, so that the total VAT charged on domestically producedand imported goods is equalized within each country.

Although the WTO’s Trade Policy Reviews of China agree that China’s less-than full VAT rebates constitute a “levy on exports” (WTO 2008), such a policydoes not contravene WTO rules. Members of the WTO are restricted fromimposing quantitative restrictions on exports or export subsidies, but neitherVAT rebate policy nor export duties are ruled out by the articles of GATT orWTO agreements. However, use of export duties is in principle restricted forChina, which agreed in its WTO accession agreement to “eliminate all taxesand charges applied to exports” with exceptions only allowed for a set of 84eight-digit goods for which maximum export duty rates were explicitly agreed.When some of China’s export duties were challenged on this basis by the US,EU and Mexico via the WTO’s dispute settlement mechanism, China arguedthat its export duties were covered by Article XX of the GATT, which allowsfor exceptions from GATT rules for measures “relating to the conservation ofexhaustible natural resources” or “necessary to protect human, animal or plantlife or health”.4 The WTO panel for the case rejected this argument in 2011,ruling that the language in China’s accession agreement did not allow for theapplication of GATT Article XX to its export duties.5

4While these were the two exceptions called upon by China in its defense in the China -raw materials dispute, Article XX also allows for several other possible exceptions; see GATT(1947, 1994).

5This aspect of the panel’s ruling was upheld on appeal in 2012. The ruling in a subsequentcase addressing China’s export policies (China - rare earths) had not been publicly released

6

The analysis below will examine the changes in China’s export policies fromthe beginning of 2002, the year following its December 2001 WTO accession,to the beginning of 2011, the year of the WTO panel ruling clarifying China’sineligibility to impose export duties via GATT Article XX. Because both the listof products (and their maximum duties) included in its accession agreement andthe potential for the justification of additional export duties under GATT ArticleXX may have affected the products on which China chose to impose exportduties, I consider both the export taxes jointly implied by both incompleteVAT rebates and export duties, and the export tax equivalent of China’s VATrebate policy alone.

In particular, product-level data on export taxes is generated by using infor-mation on both policies to calculate a single rate of export tax for each product(with and without export duties), using the principle that a product affordeda full VAT rebate and not subject to an export tax has a total export tax rateof zero.6 Product-level data on export duties is sourced directly from the rele-vant official annual notices, while product-level data on VAT rates and exportrebate rates is based on the archive of official export VAT refund schedules pub-licly available at www.taxrefund.com.cn (a privately run web site), and checkedagainst information from ad hoc official notices.

The raw data uses a ten-digit (or sometimes eight-digit) Chinese productclassification based on the international six-digit Harmonized System (HS) clas-sification. I create a panel dataset at the six-digit level by taking simple averagesof these taxes, first at the eight-digit and then at the six-digit level, and thenusing correlation tables available from the United Nations Statistics Divisionweb site to concord products across the various versions of the HS classification.I then define taxes at the annual level using the rates effective on January 1 ofeach year. Finally, for many applications, I average these six-digit taxes at thelevel of the four-digit industry as defined by the Chinese industrial classification.The analysis is conducted only for nonagricultural sectors, where the distinc-tion between ‘raw materials’ and ‘processed goods’ is clearest, as I will discussin section 2.2.3 below.7 After concordances of industry and product definitionsand omission of agricultural goods, 239 four-digit industries and 3831 six-digitproducts remain.

Figure 1 (in the introduction) summarizes how China’s nonagricultural ex-port taxes, averaged across four-digit industries, changed from 2002 to 2011.Much of the growth in export taxes during this time was driven by falls in VATrebate rates, the first major reform of which took effect at the beginning of2004. Several subsequent reforms to VAT rebates steadily increased the averageeffective export tax rate, with a short-run peak in the late 2000s. The number

as of this writing.6A full explanation of this calculation may be found in Appendix 1.7In particular, I omit all goods covered by the WTO’s agreement on agriculture, which

includes both primary agricultural products and processed agricultural goods such as food,beverages and tobacco products. I also omit fisheries and their products, which are mostlyfound within the food and beverages sectors, as well as key inputs to agriculture (fertilizersand pesticides).

7

of four-digit nonagricultural industries (six-digit products) with an export taxequivalent via VAT rebate policy of 5% of more rose from 7 (65) in 2002 to121 (1542) in 2011. The maximum export tax achieved using incomplete VATrebates is 17%, China’s standard industrial VAT rate; as of 2011, 693 productsacross 82 industries were subject to this maximum export tax, including 40industries for which all products fell in this category.

China’s export duties have affected a relatively narrower set of products andindustries, with only 188 six-digit products across 44 industries subject to anonzero export duty in 2011. The incidence of export duties rose quickly from2005 to 2008; while export duties applied to only 24 six-digit nonagriculturalproducts across 11 industries in 2005, this had grown to 229 products in 45industries as of the beginning of 2008.8 From 2008 to 2011, export duties wereimposed only on goods that were also assigned VAT rebate rates of zero, andthus had already reached the maximum export tax possible via VAT rebatepolicy.

2.2 Determinants of China’s export taxes

In this section, three stylized facts are presented about the export taxes adoptedin China between 2002 and 2011. First, I find little evidence that rises inexport taxes over this period are related to Chinese market power, as definedby either its world share in export markets or the import demand elasticity ofits largest trading partner, the United States. Second, growth in export taxes issignificantly larger in industries which experienced smaller tariff cuts associatedwith WTO accession. Third, rises in export taxes are systematically larger forraw materials industries as compared to industries producing processed goods.I show that this third phenomenon accounts for a large part of the second:much of the correlation between rises in export taxes and falls in import tariffsis due to shrinking gaps in tariffs between raw materials and processed goodsbeing replaced with rising gaps between export taxes on these two stages ofproduction.

2.2.1 Terms-of-trade and export taxes

I first test the hypothesis that China’s export taxes are set in line with terms-of-trade incentives. In its simplest form, this hypothesis is based on a monopolyargument: if there are multiple Chinese firms competing in a given sector, Chinabenefits from raising the price of these firms’ exports to the level that wouldbe set by those firms if they could successfully form a cartel. The textbooktwo-country partial-equilibrium treatment of export taxes under assumptions ofperfect competition thus suggests that in a sector for which import demand forChina’s goods is less than infinitely elastic, China gains from imposing an exporttax, and that the optimal export tax is an inverse function of its trading partner’s

8As noted above, this analysis does not include agricultural goods and their inputs, someof which were also subject to export duties during this period; many of the highest rates wereapplied to fertilizers.

8

import demand elasticity. In a recent paper, Costinot et al. (2013) extendthis standard result to multiple sectors within a Ricardian general-equilibriumframework, and find that optimal export taxes should weakly increase with acountry’s comparative advantage, with the optimal average level of taxes (orsubsidies) depending on the level of import tariffs. Again, the key finding isthat optimal export taxes are higher in sectors in which the country’s marketpower is larger.

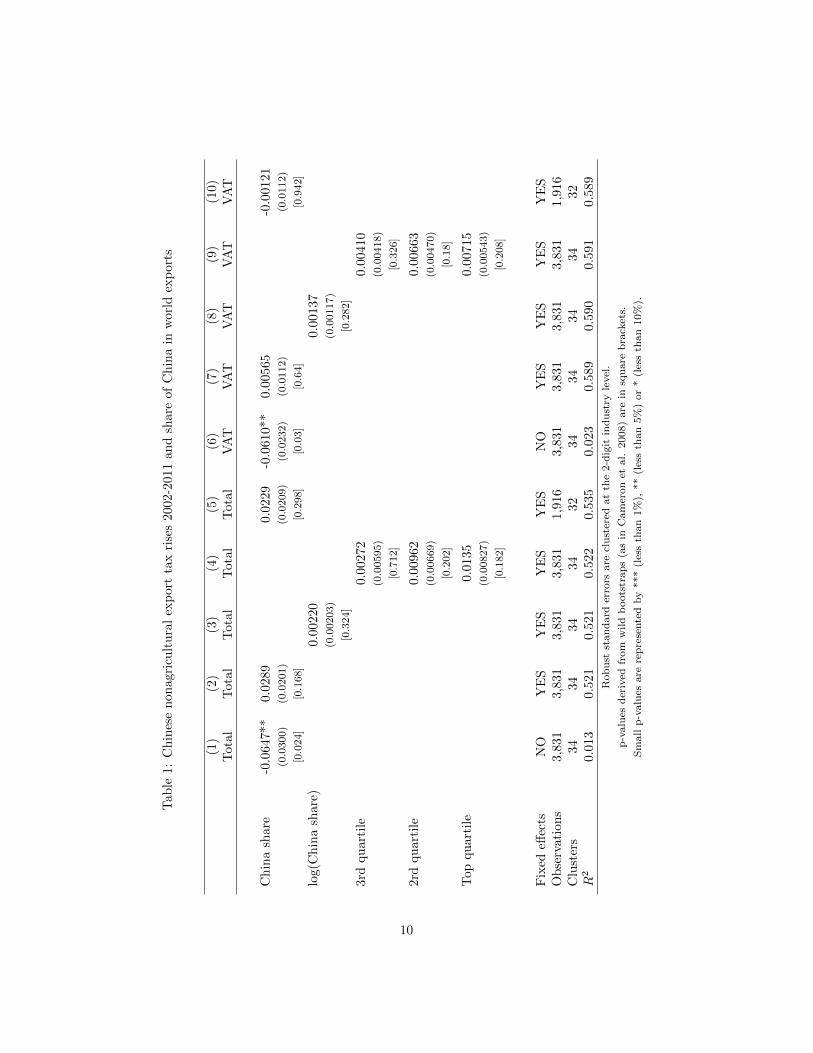

Two measures of market power are used here. I first use world trade data for2002 and 2003 – i.e. after China joined the WTO but before the first increasein its export taxes – to calculate the average market share of Chinese exportsin world trade. In particular, for each year, the value of Chinese exports ineach product category is calculated and divided by the total value of worldtrade in that product, and the resulting shares are then averaged across the twoyears.9 This measure makes clear that China is a large country in the worldtrading system: across six-digit HS products, the value of the 25th, 50th and75th percentile of the share of Chinese exports in world trade is 1.4%, 4.6% and14.2% respectively.

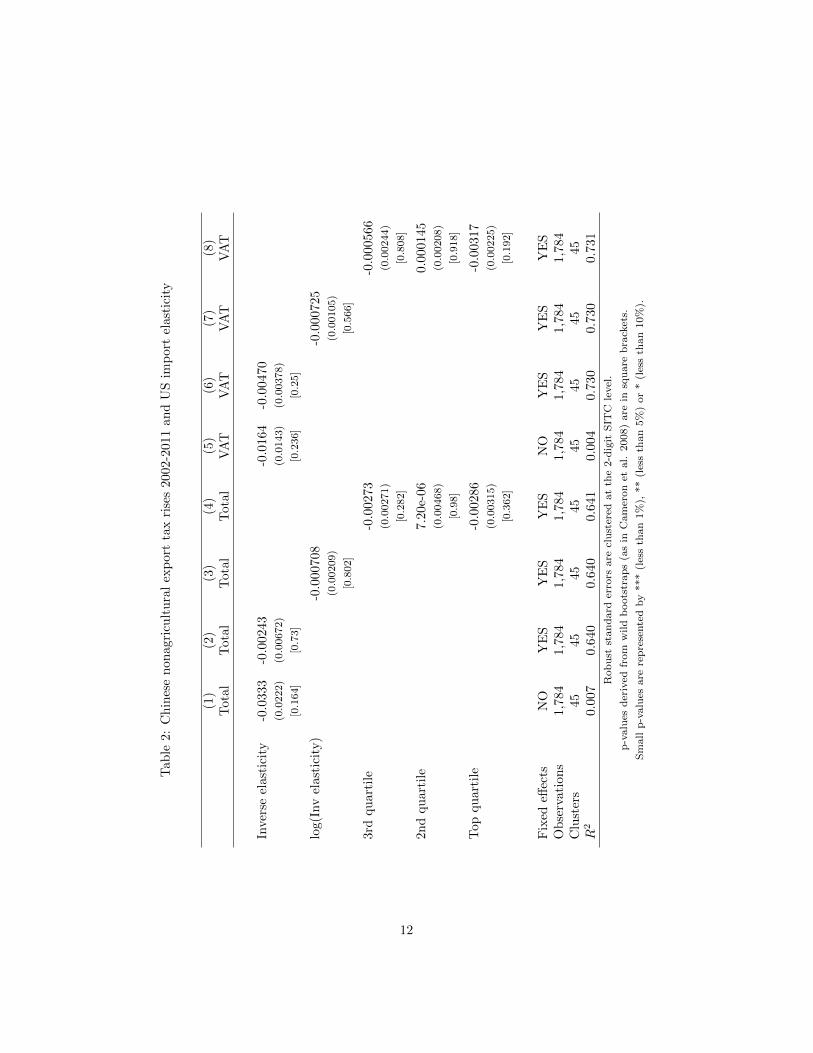

A second measure is provided by a product-level dataset of estimated tradeelasticities for the United States, the largest importer of Chinese goods dur-ing this period, from Broda and Weinstein (2006). Their paper uses a Krugman(1980) framework, assuming a constant elasticity of substitution across varietiesof each traded product, where varieties are defined at the product-country level.Within the theory, lower product-level elasticities imply less willingness by USconsumers to substitute away from Chinese varieties to those from other coun-tries, and thus, other things equal, higher Chinese market power. Using data onUS imports from 1990 to 2001, Broda and Weinstein calculate these elasticitiesat several different levels of aggregation; I use data at the five-digit level of theSITC classification, which provides the closest match in level of aggregation tosix-digit HS product codes.10

Tables 1 and 2 summarize the results of product-level regressions of changesin Chinese export taxes from 2002 to 2011 (i.e. tax2011 − tax2002) on each ofthese two variables separately. The simple regression in column (1) of Table 1suggests that the rise in export taxes was significantly higher in products forwhich China had a smaller average market share in 2002-03, and that the cor-relation between the two variables is very small (R2 of 0.01). When two-digitindustry fixed effects are included in column (2), the estimated coefficient onChina’s market share switches to the expected sign, but loses statistical signifi-cance, and again has limited explanatory power; the associated beta coefficientis just 0.05. Alternative specifications for the right-hand side similar to thosein Broda, Limao and Weinstein (2008) – log market share in column (3) andquartile dummies in column (4) – remain statistically insignificant and econom-ically small. Column (4) suggests that export tax increases on products in thetop quartile of market share were only 1 percentage point higher on average

9This data is sourced from UN COMTRADE via the CEPII BACI dataset.10I also drop the top 1% and bottom 1% of their elasticity estimates to avoid results that

are driven by outliers.

9

Tab

le1:

Ch

ines

en

onagr

icu

ltu

ral

exp

ort

tax

rise

s2002-2

011

an

dsh

are

of

Ch

ina

inw

orl

dex

port

s

(1)

(2)

(3)

(4)

(5)

(6)

(7)

(8)

(9)

(10)

Tot

alT

otal

Tot

al

Tota

lT

ota

lV

AT

VA

TV

AT

VA

TV

AT

Ch

ina

shar

e-0

.064

7**

0.02

890.0

229

-0.0

610**

0.0

0565

-0.0

0121

(0.0

300)

(0.0

201)

(0.0

209)

(0.0

232)

(0.0

112)

(0.0

112)

[0.0

24]

[0.1

68]

[0.2

98]

[0.0

3]

[0.6

4]

[0.9

42]

log(

Ch

ina

shar

e)0.

00220

0.0

0137

(0.0

0203)

(0.0

0117)

[0.3

24]

[0.2

82]

3rd

qu

arti

le0.0

0272

0.0

0410

(0.0

0595)

(0.0

0418)

[0.7

12]

[0.3

26]

2rd

qu

arti

le0.0

0962

0.0

0663

(0.0

0669)

(0.0

0470)

[0.2

02]

[0.1

8]

Top

qu

arti

le0.0

135

0.0

0715

(0.0

0827)

(0.0

0543)

[0.1

82]

[0.2

08]

Fix

edeff

ects

NO

YE

SY

ES

YE

SY

ES

NO

YE

SY

ES

YE

SY

ES

Ob

serv

atio

ns

3,83

13,

831

3,83

13,8

31

1,9

16

3,8

31

3,8

31

3,8

31

3,8

31

1,9

16

Clu

ster

s34

3434

34

32

34

34

34

34

32

R2

0.01

30.

521

0.52

10.5

22

0.5

35

0.0

23

0.5

89

0.5

90

0.5

91

0.5

89

Rob

ust

stan

dard

erro

rsare

clu

ster

edat

the

2-d

igit

ind

ust

ryle

vel

.

p-v

alu

esd

eriv

edfr

om

wild

boots

trap

s(a

sin

Cam

eron

etal.

2008)

are

insq

uare

bra

cket

s.

Sm

all

p-v

alu

esare

rep

rese

nte

dby

***

(les

sth

an

1%

),**

(les

sth

an

5%

)or

*(l

ess

than

10%

).

10

than those in the bottom quartile, and that this difference is not statisticallysignificant.

If the Ricardian model inspiring this specification is taken seriously, thecorrect approach is to study taxes only on net export products, since only exporttaxes on these goods will be effective in practice. Column (5) thus drops allsix-digit goods for which China’s trade balance was negative in either 2002 or2003, but this results in little change in the estimated coefficient. Also, asdiscussed above, although China imposed export duties in this period that wentbeyond those allowed by its accession agreement, its flexibility in doing so mighthave been constrained by its perceived ability to defend these taxes within theGATT/WTO rules. I thus run the regressions in columns (1) through (5) againusing only the export taxes implied by variation across products in VAT exportrebates; the results are similar to those in columns (1) to (5).

In Table 2, tax changes are regressed on the US elasticities of substitutionfrom Broda and Weinstein (2006) at the five-digit SITC level. Column (1) showsthat export taxes increased by more on products with lower inverse elasticities,again the opposite sign from that implied by the terms-of-trade hypothesis,though the result is not statistically significant. This time, however, addingfixed effects (now at the two-digit SITC product level) does not reverse the signof the estimated coefficient, nor do the alternative specifications in columns (3)and (4) or limitation to VAT policy in columns (5) through (8).

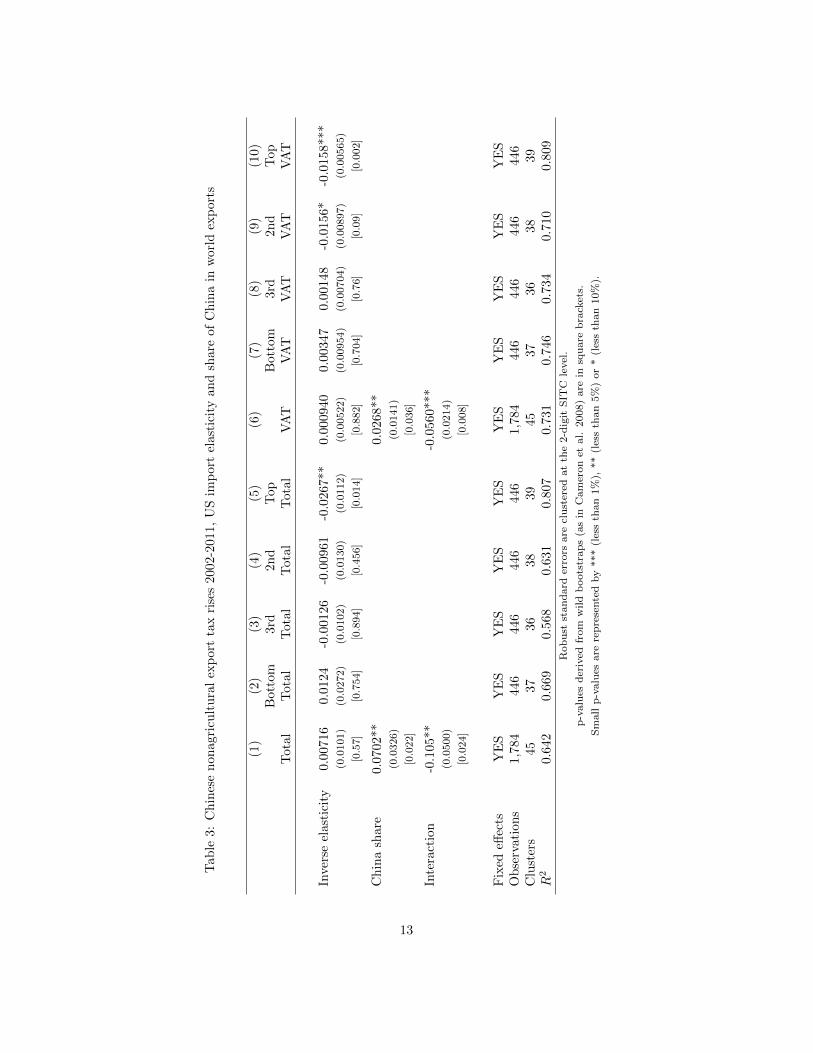

Columns (1) and (6) of Table 3 display the results of a regression with aninteraction of the two variables, again with two-digit SITC product fixed ef-fects. This shows that export tax rises actually do increase in China’s share ofworld trade for goods perceived by US consumers as relatively homogeneous,but that this relationship declines as substitutability between varieties becomeslower. This might be because increases in export taxes are relatively high forall differentiated goods within a given industry (in which even a small countrymay wield market power; see Gros (1987) for the case of optimal import tariffs)but only for homogeneous goods in which China has a large market share. Theregression in column (2) of Table 2 is thus rerun for each quartile of the distri-bution of Chinese market share across products, in columns (2) to (5) for totalexport taxes and (7) to (10) for export taxes via VAT policy only. These resultsinstead suggest that the finding in columns (1) and (6) is driven by the top endof the distribution of products by market share; among products in which Chinahad a large market share in 2002 and 2003, more homogeneous products (fromthe perspective of US consumers) experienced relatively larger increases in ex-port taxes between 2002 and 2011 than more differentiated products. Whilethis result may appear puzzling from the perspective of the terms-of-trade hy-pothesis, it will be discussed further in Section 4 in light of the other stylizedfacts presented below.

2.2.2 Import tariff cuts and export taxes

The quotes in the introduction, emphasizing the support for particular industriesprovided by China’s export policies rather than their effects on terms of trade,

11

Tab

le2:

Ch

ines

en

onag

ricu

ltu

ral

exp

ort

tax

rise

s2002-2

011

an

dU

Sim

port

elast

icit

y

(1)

(2)

(3)

(4)

(5)

(6)

(7)

(8)

Tot

alT

otal

Tota

lT

ota

lV

AT

VA

TV

AT

VA

T

Inve

rse

elas

tici

ty-0

.033

3-0

.002

43-0

.0164

-0.0

0470

(0.0

222)

(0.0

0672)

(0.0

143)

(0.0

0378)

[0.1

64]

[0.7

3]

[0.2

36]

[0.2

5]

log(

Inv

elas

tici

ty)

-0.0

00708

-0.0

00725

(0.0

0209)

(0.0

0105)

[0.8

02]

[0.5

66]

3rd

qu

arti

le-0

.00273

-0.0

00566

(0.0

0271)

(0.0

0244)

[0.2

82]

[0.8

08]

2nd

qu

arti

le7.2

0e-

06

0.0

00145

(0.0

0468)

(0.0

0208)

[0.9

8]

[0.9

18]

Top

qu

arti

le-0

.00286

-0.0

0317

(0.0

0315)

(0.0

0225)

[0.3

62]

[0.1

92]

Fix

edeff

ects

NO

YE

SY

ES

YE

SN

OY

ES

YE

SY

ES

Ob

serv

atio

ns

1,78

41,

784

1,7

84

1,7

84

1,7

84

1,7

84

1,7

84

1,7

84

Clu

ster

s45

4545

45

45

45

45

45

R2

0.00

70.

640

0.6

40

0.6

41

0.0

04

0.7

30

0.7

30

0.7

31

Rob

ust

stan

dard

erro

rsare

clu

ster

edat

the

2-d

igit

SIT

Cle

vel

.

p-v

alu

esd

eriv

edfr

om

wild

boots

trap

s(a

sin

Cam

eron

etal.

2008)

are

insq

uare

bra

cket

s.

Sm

all

p-v

alu

esare

rep

rese

nte

dby

***

(les

sth

an

1%

),**

(les

sth

an

5%

)or

*(l

ess

than

10%

).

12

Tab

le3:

Ch

ines

en

onag

ricu

ltu

ral

exp

ort

tax

rise

s2002-2

011,

US

imp

ort

elast

icit

yan

dsh

are

of

Ch

ina

inw

orl

dex

port

s

(1)

(2)

(3)

(4)

(5)

(6)

(7)

(8)

(9)

(10)

Bot

tom

3rd

2n

dT

op

Bott

om

3rd

2n

dT

op

Tot

alT

otal

Tot

al

Tota

lT

ota

lV

AT

VA

TV

AT

VA

TV

AT

Inve

rse

elas

tici

ty0.

0071

60.

0124

-0.0

0126

-0.0

0961

-0.0

267**

0.0

00940

0.00347

0.0

0148

-0.0

156*

-0.0

158***

(0.0

101)

(0.0

272)

(0.0

102)

(0.0

130)

(0.0

112)

(0.0

0522)

(0.0

0954)

(0.0

0704)

(0.0

0897)

(0.0

0565)

[0.5

7]

[0.7

54]

[0.8

94]

[0.4

56]

[0.0

14]

[0.8

82]

[0.7

04]

[0.7

6]

[0.0

9]

[0.0

02]

Ch

ina

shar

e0.

0702

**0.0

268**

(0.0

326)

(0.0

141)

[0.0

22]

[0.0

36]

Inte

ract

ion

-0.1

05**

-0.0

560***

(0.0

500)

(0.0

214)

[0.0

24]

[0.0

08]

Fix

edeff

ects

YE

SY

ES

YE

SY

ES

YE

SY

ES

YE

SY

ES

YE

SY

ES

Ob

serv

atio

ns

1,78

444

644

6446

446

1,7

84

446

446

446

446

Clu

ster

s45

3736

38

39

45

37

36

38

39

R2

0.64

20.

669

0.56

80.6

31

0.8

07

0.7

31

0.7

46

0.7

34

0.7

10

0.8

09

Rob

ust

stan

dard

erro

rsare

clu

ster

edat

the

2-d

igit

SIT

Cle

vel

.

p-v

alu

esd

eriv

edfr

om

wild

boots

trap

s(a

sin

Cam

eron

etal.

2008)

are

insq

uare

bra

cket

s.

Sm

all

p-v

alu

esare

rep

rese

nte

dby

***

(les

sth

an

1%

),**

(les

sth

an

5%

)or

*(l

ess

than

10%

).

13

imply that the post-WTO growth in Chinese export taxes may instead haveresulted from the desire to use trade policy to stimulate a chosen subset ofindustries. Indeed, much of the variation in export tax growth during thisperiod occurred at the industry level; a regression of tax changes on a full setof four-digit industry dummies results in an adjusted R2 of 0.73. This suggestsa testable hypothesis: if the Chinese government intended its trade policy tosupport the same set of industries after its WTO entry as before, then one wouldexpect that the industries whose protection via import tariffs saw the largestdecline due to WTO entry would be those with the largest relative rise in ratesof export subsidy (i.e. the smallest rise in export taxes) afterwards.

This hypothesis is examined in Table 3, again with the change in exporttaxes from 2002 to 2011 as the dependent variable. On the right-hand side,the variable max{tar1999− tarbound, 0}, where tar1999− tarbound, the differencebetween China’s 1999 applied tariffs and its bound (negotiated) tariffs, is usedas a proxy for the tariff cuts due to China’s WTO entry.11 Because the agreedschedule for implementation of China’s bound tariffs extended from 2000 to 2010(with most tariffs to be reduced to their bound rates by 2005), 1999 representsa year in which China’s tariffs were in principle unconstrained by its WTOagreements, while all of its tariffs should have been reduced to bound levelsbefore 2011.12 Indeed, this variable corresponds almost exactly to the actualdifference between 1999 and 2011 applied tariffs, with a correlation coefficientof 0.97 between the two variables at the six-digit product level.

Table 4 provides evidence in favour of the hypothesis that China’s exporttaxes have been driven by ongoing industrial policy. Column (1) shows thatsix-digit products whose tariffs were reduced by one additional percentage pointfrom their 1999 levels due to WTO accession saw a 0.4 percentage point smallerincrease in export taxes from 2002 to 2011; that is, export tax increases werelarger for products whose tariffs fell by less. When the analysis is conducted atthe industry level by taking simple averages of tariff cuts and tax rises withineach four-digit industry, the estimated coefficient rises in absolute value to al-most 0.9. When only VAT policy is taken into account, the size of each of theseeffects becomes smaller, but the explanatory power of the regression remainsapproximately the same; the values of R2 for these regressions suggest that ap-proximately 20% of variation in changes in export taxes (by either definition)across industries is explained by the tariff cuts associated with WTO accession.

I also consider whether this result is robust to considering export taxes onlyon goods of which China was a net exporter in both 2002 and 2003, and importtariffs only on products for which China was a net importer in each of these

11Product-level panel data on China’s applied tariffs, along with its schedule of boundtariffs, is sourced from WTO Tariff Analysis Online and UNCTAD TRAINS at the eight-digitlevel and averaged at the six-digit level.

12In practice, however, according to Branstetter and Lardy (2008), China’s 1999 tariffswere already an outcome of the process of WTO accession, as China unilaterally liberalizedtariffs starting in the early 1990s “to gain credibility with its negotiating partners that it wasseriously committed to opening up its economy”. Nonetheless, Branstetter and Lardy alsoreport that China agreed to additional commitments in 1999 with the United States thatformed part of its actual WTO accession agreement.

14

Tab

le4:

Ch

ines

en

onag

ricu

ltu

ral

exp

ort

tax

rise

s2002-2

011

an

dta

riff

cuts

ass

oci

ate

dw

ith

WT

Oacc

essi

on

(1)

(2)

(3)

(4)

(5)

(6)

Tot

alT

ota

lT

ota

lV

AT

VA

TV

AT

Tar

iffcu

t-0

.413

***

-0.8

90***

-0.6

01**

-0.3

28**

-0.5

71***

-0.4

65**

(0.1

03)

(0.2

54)

(0.1

88)

(0.0

828)

(0.1

36)

(0.1

41)

[0.0

04]

[0.0

08]

[0.0

22]

[0.0

16]

[0.0

04]

[0.0

16]

Un

itP

rod

uct

Ind

ust

ryIn

du

stry

Pro

du

ctIn

du

stry

Ind

ust

ryO

bse

rvat

ion

s3,

827

239

149

3,8

27

239

149

Clu

ster

s34

34

31

34

34

31

R2

0.13

20.2

16

0.1

82

0.1

64

0.2

30

0.2

17

Rob

ust

stan

dard

erro

rsare

clu

ster

edat

the

two-d

igit

ind

ust

ryle

vel

.

p-v

alu

esd

eriv

edfr

om

wild

boots

trap

s(a

sin

Cam

eron

etal.

2008)

are

insq

uare

bra

cket

s.

Sm

all

p-v

alu

esare

rep

rese

nte

dby

***

(les

sth

an

1%

),**

(les

sth

an

5%

)or

*(l

ess

than

10%

).

15

two years. This still allows for a comparison of the two policies at the industrylevel, but the regression’s two industry-level variables are now generated by twononintersecting sets of six-digit products. As shown in columns (3) and (6) ofTable 4, the results remain statistically significant.

2.2.3 Raw materials and export taxes

A second suggestion provided by the quotes in the introduction about the na-ture of China’s post-WTO trade policy is that it reflects the aim to stimulateindustries producing processed goods via restrictions on exports of raw materi-als. The two recent WTO dispute settlement cases relating to China’s exportrestrictions have both focused entirely on products usually described as ‘rawmaterials’; indeed, the first case was titled “China – Measures Related to theExportation of Various Raw Materials”.13 In this section, I examine the ex-tent to which China’s export taxes were raised on raw materials industries ascompared to industries producing processed goods, and then relate this to therelationship between tax rises and tariff cuts discussed above.

Before conducting an empirical analysis, it is necessary to clearly definewhich industries produce ‘raw materials’ and which industries produce ‘pro-cessed goods’. This amounts to determining a dividing line somewhere in theindustrial value chain turning products of the extractive industries (e.g. logs,ores, or crude oil) into goods for final consumption (e.g. envelopes, machines, orplastic toys). While it might initially seem natural to draw this line immediatelyafter the extractive stage, some manufacturing industries are also producers ofgoods often considered as raw materials (e.g. paper pulp, pig iron, or polymers).Indeed, coke, a manufactured product of coal, was one of the products includedin the China - raw materials WTO dispute. I thus use three perspectives onthe concept of ‘raw materials’ in order to define them below: that they tend tobe homogeneous; used as intermediates by industry; but not yet describable as‘articles’ or their ‘parts’.

The primary definition that will be used in the empirical analysis belowis based mainly on the last of these three perspectives, as embedded in theHarmonized System (HS) classification of traded goods. The headings of manymajor categories of the HS system (e.g. “Plastics and articles thereof”, “Woodand articles of wood”; “Textiles and textile articles”) imply a progression froma particular raw material to articles made from this material, which is thenreflected in the order in which the six-digit HS products are numbered. TheHS-based definition of raw materials used here is thus based on the dividing linebetween the raw material and “articles thereof” within each such section of theHS classification, with other sections classified as entirely constituted of eitherraw materials (e.g. “Ores, slag and ash”) or processed goods (e.g. “Clocks andwatches and parts thereof”).

A second definition is based on the United Nations Broad Economic Cat-egories classification, which categorizes six-digit HS products as consumption

13The other case is titled “China – Measures Related to the Exportation of Rare Earths,Tungsten and Molybdenum”.

16

goods, capital goods or intermediate goods according to the System of NationalAccounts. I define raw materials products as all intermediate products withthe exception of two categories described as “parts and accessories”. As a thirdalternative, I also use the ‘liberal’ measure of homogeneous goods provided byRauch (1999), who identifies a set of SITC products that are either sold on orga-nized exchanges or reference-priced; if a good is in either of these two categories,I classify it as a raw material.

In each case, I define a four-digit industry as a ‘raw materials industry’ ifmore than half of the products associated with that industry fall under the rel-evant definition above. Reassuringly, the three measures are highly correlated:the three correlation coefficients range from 0.58 to 0.70 at the product leveland from 0.60 to 0.73 at the industry level. This means that in line with in-tuition about the industrial value chain, homogeneous goods according to theoften-used classification of Rauch (1999) tend to be intermediates (according toBEC) but not ‘articles’ or their ‘parts’ (according to HS).14

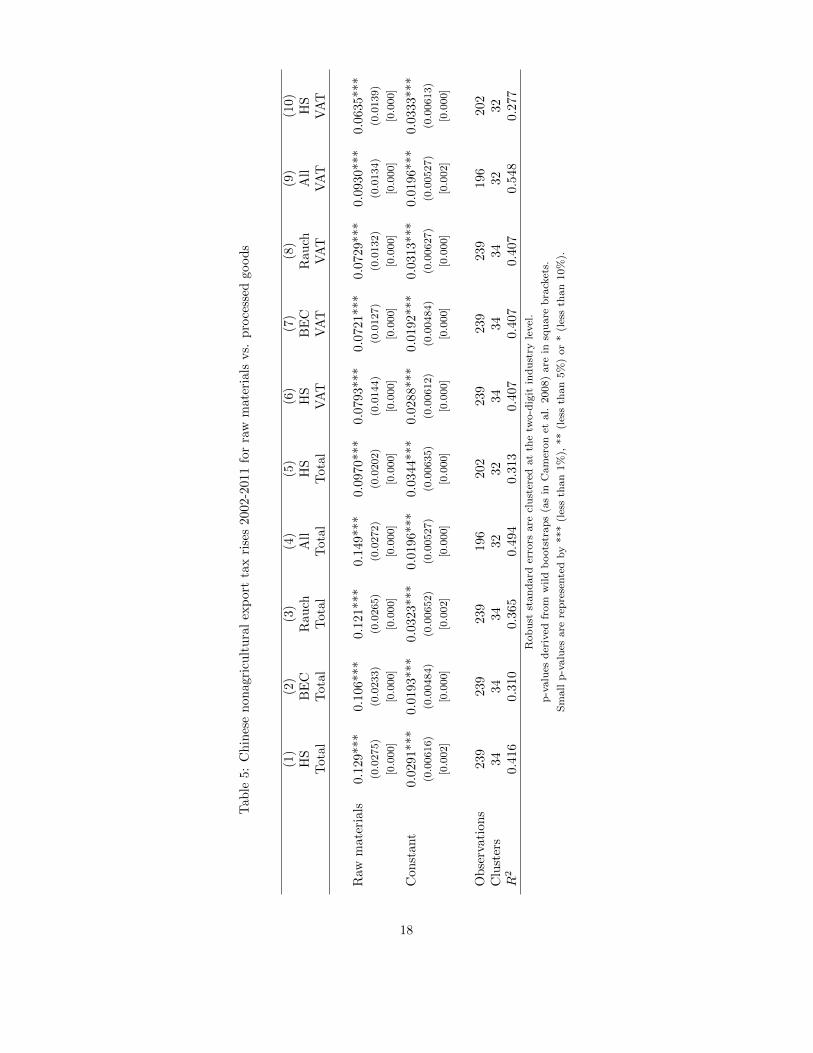

Columns (1) to (3) of Table 5 display the results of regressing averageindustry-level changes in export taxes from 2002 to 2011 on each of the threedummy variables defined above. The results show that the average rise in taxeson processed goods industries was relatively small – around 2 to 3 percentagepoints – while average increases in export taxes on raw materials sectors weresignificantly higher, by at least 10 percentage points. The values of R2 for theseregressions should also be noted; for example, the variable using the HS defini-tion of raw materials accounts for 42% of variation in average export tax risesacross industries.

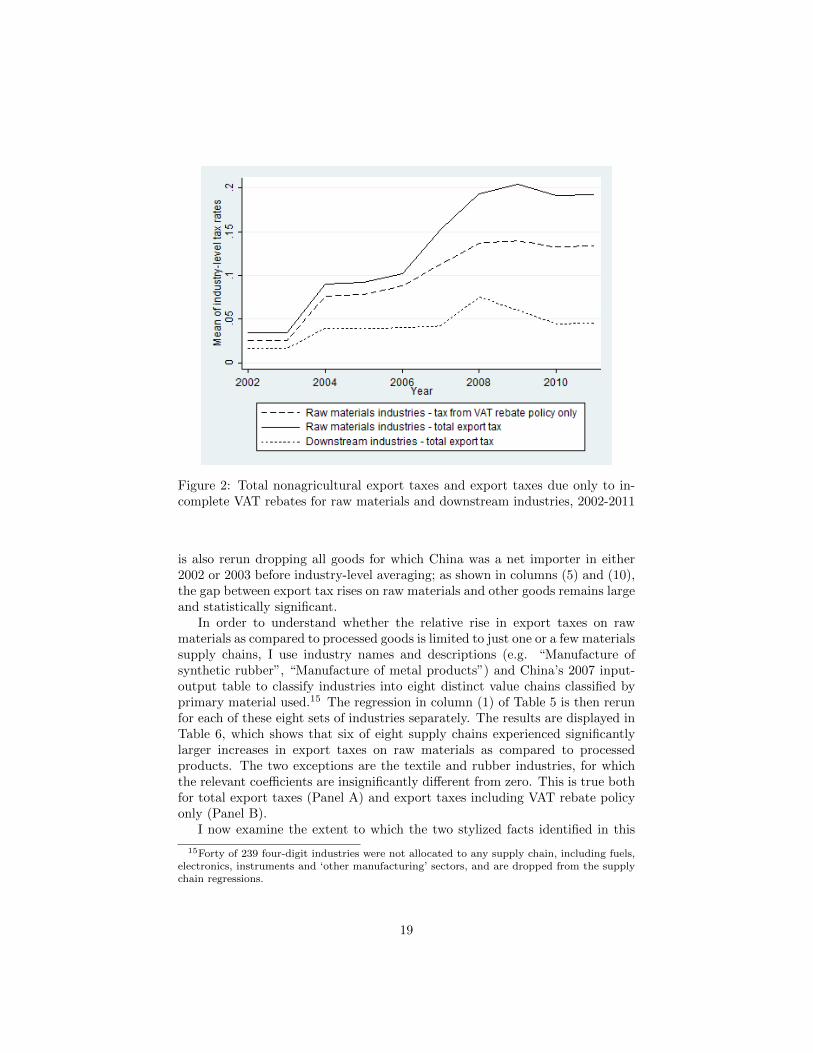

As discussed in section 2.1, one possible reason for this variation in exporttaxes across sectors is that China may have been constrained in its imposition ofexport duties by its accession agreement and the perceived potential to defendits measures through exceptions in Article XX of the GATT (e.g. “conservationof exhaustible natural resources”). However, identical regressions using onlyvariation in VAT rebate policy, whose results are displayed in columns (6) to(8), produce qualitatively similar results. Figure 2 displays a time series ofChina’s average export taxes across industries with and without export duties,using the HS definition of raw materials.

I also run identical regressions in which all products for which the threedefinitions do not all agree are dropped before taxes are averaged at the industrylevel. As shown in columns (4) and (9), including only these ‘unambiguous’observations boosts both the magnitude of the effect – now 15 percentage pointsfor total export taxes and 9 percentage points for VAT policy only – and theregressions’ explanatory power. The baseline regression using the HS definition

14This relationship is much weaker for agricultural products. This is especially true forfood and beverage sectors, in which the ‘raw materials’-‘processed goods’ dichotomy is alsoless intuitively clear: many products of primary industries, such as fruits, vegetables, eggs andmilk, are also often consumed as final goods, and much processing is done in service industries(e.g. restaurants) or as home production. Therefore, as discussed in footnote 7 above, I havenot included agricultural goods in the analysis in this paper. Note that no agricultural goodswere included in the two WTO dispute settlement cases discussed above.

17

Tab

le5:

Ch

ines

en

onag

ricu

ltu

ral

exp

ort

tax

rise

s2002-2

011

for

raw

mate

rials

vs.

pro

cess

edgood

s

(1)

(2)

(3)

(4)

(5)

(6)

(7)

(8)

(9)

(10)

HS

BE

CR

au

chA

llH

SH

SB

EC

Rau

chA

llH

ST

otal

Tot

al

Tota

lT

ota

lT

ota

lV

AT

VA

TV

AT

VA

TV

AT

Raw

mat

eria

ls0.

129*

**0.

106*

**0.

121***

0.1

49***

0.0

970***

0.0

793***

0.0

721***

0.0

729***

0.0

930***

0.0

635***

(0.0

275)

(0.0

233)

(0.0

265)

(0.0

272)

(0.0

202)

(0.0

144)

(0.0

127)

(0.0

132)

(0.0

134)

(0.0

139)

[0.0

00]

[0.0

00]

[0.0

00]

[0.0

00]

[0.0

00]

[0.0

00]

[0.0

00]

[0.0

00]

[0.0

00]

[0.0

00]

Con

stan

t0.

0291

***

0.01

93**

*0.

0323***

0.0

196***

0.0

344***

0.0

288***

0.0

192***

0.0

313***

0.0

196***

0.0

333***

(0.0

0616)

(0.0

0484)

(0.0

0652)

(0.0

0527)

(0.0

0635)

(0.0

0612)

(0.0

0484)

(0.0

0627)

(0.0

0527)

(0.0

0613)

[0.0

02]

[0.0

00]

[0.0

02]

[0.0

00]

[0.0

00]

[0.0

00]

[0.0

00]

[0.0

00]

[0.0

02]

[0.0

00]

Ob

serv

atio

ns

239

239

239

196

202

239

239

239

196

202

Clu

ster

s34

3434

32

32

34

34

34

32

32

R2

0.41

60.

310

0.365

0.4

94

0.3

13

0.4

07

0.4

07

0.4

07

0.5

48

0.2

77

Rob

ust

stan

dard

erro

rsare

clu

ster

edat

the

two-d

igit

ind

ust

ryle

vel

.

p-v

alu

esd

eriv

edfr

om

wild

boots

trap

s(a

sin

Cam

eron

etal.

2008)

are

insq

uare

bra

cket

s.

Sm

all

p-v

alu

esare

rep

rese

nte

dby

***

(les

sth

an

1%

),**

(les

sth

an

5%

)or

*(l

ess

than

10%

).

18

Figure 2: Total nonagricultural export taxes and export taxes due only to in-complete VAT rebates for raw materials and downstream industries, 2002-2011

is also rerun dropping all goods for which China was a net importer in either2002 or 2003 before industry-level averaging; as shown in columns (5) and (10),the gap between export tax rises on raw materials and other goods remains largeand statistically significant.

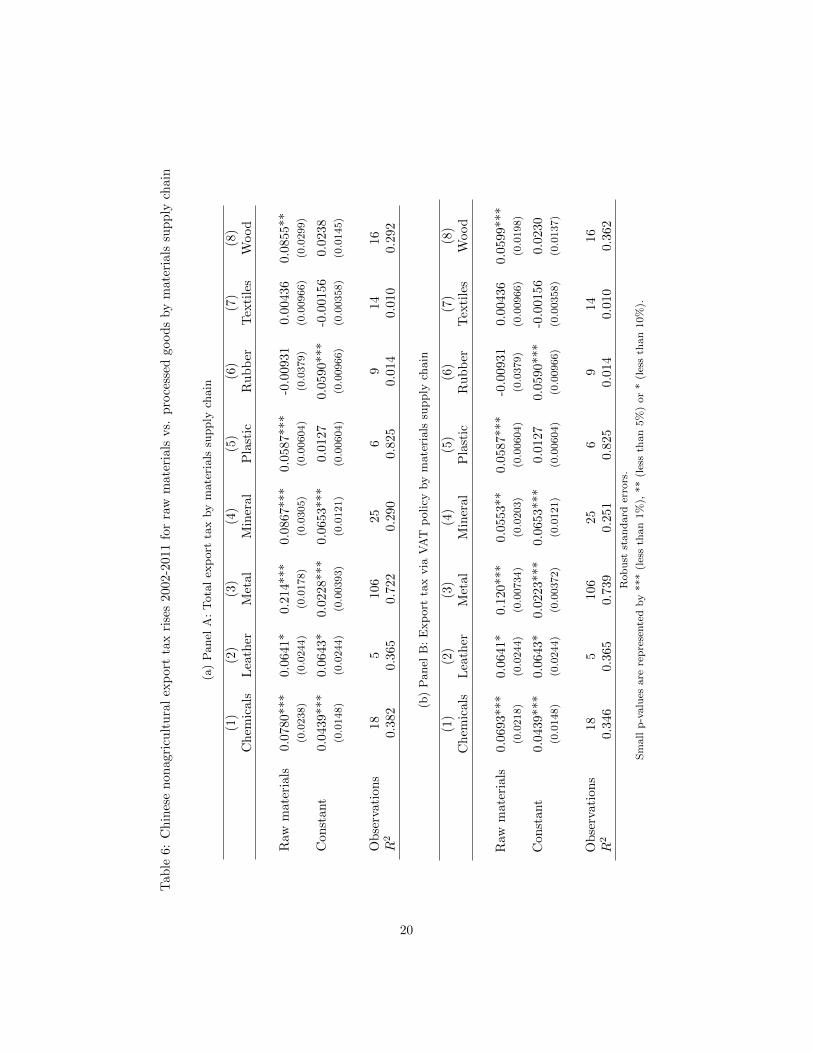

In order to understand whether the relative rise in export taxes on rawmaterials as compared to processed goods is limited to just one or a few materialssupply chains, I use industry names and descriptions (e.g. “Manufacture ofsynthetic rubber”, “Manufacture of metal products”) and China’s 2007 input-output table to classify industries into eight distinct value chains classified byprimary material used.15 The regression in column (1) of Table 5 is then rerunfor each of these eight sets of industries separately. The results are displayed inTable 6, which shows that six of eight supply chains experienced significantlylarger increases in export taxes on raw materials as compared to processedproducts. The two exceptions are the textile and rubber industries, for whichthe relevant coefficients are insignificantly different from zero. This is true bothfor total export taxes (Panel A) and export taxes including VAT rebate policyonly (Panel B).

I now examine the extent to which the two stylized facts identified in this

15Forty of 239 four-digit industries were not allocated to any supply chain, including fuels,electronics, instruments and ‘other manufacturing’ sectors, and are dropped from the supplychain regressions.

19

Tab

le6:

Ch

ines

en

onag

ricu

ltu

ral

exp

ort

tax

rise

s2002-2

011

for

raw

mate

rials

vs.

pro

cess

edgoods

by

mate

rials

sup

ply

chain

(a)

Panel

A:

Tota

lex

port

tax

by

mate

rials

supply

chain

(1)

(2)

(3)

(4)

(5)

(6)

(7)

(8)

Ch

emic

als

Lea

ther

Met

al

Min

eral

Pla

stic

Ru

bb

erT

exti

les

Wood

Raw

mat

eria

ls0.

0780

***

0.06

41*

0.2

14***

0.0

867***

0.0

587***

-0.0

0931

0.0

0436

0.0

855**

(0.0

238)

(0.0

244)

(0.0

178)

(0.0

305)

(0.0

0604)

(0.0

379)

(0.0

0966)

(0.0

299)

Con

stan

t0.

0439

***

0.06

43*

0.0

228***

0.0

653***

0.0

127

0.0

590

***

-0.0

0156

0.0

238

(0.0

148)

(0.0

244)

(0.0

0393)

(0.0

121)

(0.0

0604)

(0.0

0966)

(0.0

0358)

(0.0

145)

Ob

serv

atio

ns

185

106

25

69

14

16

R2

0.38

20.

365

0.7

22

0.2

90

0.8

25

0.0

14

0.0

10

0.2

92

(b)

Panel

B:

Exp

ort

tax

via

VA

Tp

olicy

by

mate

rials

supply

chain

(1)

(2)

(3)

(4)

(5)

(6)

(7)

(8)

Ch

emic

als

Lea

ther

Met

al

Min

eral

Pla

stic

Ru

bb

erT

exti

les

Wood

Raw

mat

eria

ls0.

0693

***

0.06

41*

0.1

20***

0.0

553**

0.0

587***

-0.0

0931

0.0

0436

0.0

599***

(0.0

218)

(0.0

244)

(0.0

0734)

(0.0

203)

(0.0

0604)

(0.0

379)

(0.0

0966)

(0.0

198)

Con

stan

t0.

0439

***

0.06

43*

0.0

223***

0.0

653***

0.0

127

0.0

590***

-0.0

0156

0.0

230

(0.0

148)

(0.0

244)

(0.0

0372)

(0.0

121)

(0.0

0604)

(0.0

0966)

(0.0

0358)

(0.0

137)

Ob

serv

atio

ns

185

106

25

69

14

16

R2

0.34

60.

365

0.7

39

0.2

51

0.8

25

0.0

14

0.0

10

0.3

62

Rob

ust

stan

dard

erro

rs.

Sm

all

p-v

alu

esare

rep

rese

nte

dby

***

(les

sth

an

1%

),**

(les

sth

an

5%

)or

*(l

ess

than

10%

).

20

Tab

le7:

Ch

ines

en

onag

ricu

ltu

ral

imp

ort

tari

ffs

1999

an

dd

iffer

ence

sw

ith

bou

nd

tari

ffs

for

raw

mate

rials

vs.

pro

cess

edgood

s

(a)

Panel

A:

1999

tari

ffs

(1)

(2)

(3)

(4)

(5)

(6)

(7)

(8)

(9)

All

Ch

emic

als

Lea

ther

Met

al

Min

eral

Pla

stic

Ru

bb

erT

exti

les

Wood

Raw

mat

eria

ls-0

.096

5***

-0.0

774*

**-0

.110***

-0.1

34***

-0.1

22***

-0.0

235**

-0.0

326

-0.0

882***

-0.0

708

(0.0

182)

(0.0

252)

(0.0

0479)

(0.0

123)

(0.0

225)

(0.0

0785)

(0.0

493)

(0.0

239)

(0.0

511)

[0.0

02]

Con

stan

t0.

171*

**0.

161*

**0.

246***

0.1

61***

0.1

77***

0.1

81***

0.1

89***

0.2

87***

0.1

59***

(0.0

102)

(0.0

238)

(0.0

0479)

(0.0

101)

(0.0

196)

(0.0

0785)

(0.0

279)

(0.0

124)

(0.0

422)

[0.0

00]

Ob

serv

atio

ns

239

185

106

25

69

14

16

R2

0.24

80.

237

0.9

78

0.3

93

0.5

27

0.3

10

0.0

59

0.4

98

0.1

46

(b)

Panel

B:

Diff

eren

ces

bet

wee

n1999

tari

ffs

and

bound

tari

ffs

(1)

(2)

(3)

(4)

(5)

(6)

(7)

(8)

(9)

All

Ch

emic

als

Lea

ther

Met

al

Min

eral

Pla

stic

Ru

bb

erT

exti

les

Wood

Raw

mat

eria

ls-0

.033

3***

-0.0

465*

*-0

.0947**

-0.0

456***

-0.0

465***

-0.0

0197

-0.0

00591

-0.0

164

-0.0

616

(0.0

0986)

(0.0

180)

(0.0

260)

(0.0

0642)

(0.0

124)

(0.0

0432)

(0.0

216)

(0.0

278)

(0.0

398)

[0.0

04]

Con

stan

t0.

0632

***

0.07

62**

*0.

107**

0.0

551***

0.0

503***

0.0

880***

0.0

426**

0.1

33***

0.1

09***

(0.0

0531)

(0.0

169)

(0.0

260)

(0.0

0551)

(0.0

118)

(0.0

0432)

(0.0

162)

(0.0

206)

(0.0

337)

[0.0

00]

Ob

serv

atio

ns

239

185

106

25

69

14

16

R2

0.09

50.

181

0.524

0.2

05

0.3

51

0.0

10

0.0

00

0.0

32

0.1

81

Rob

ust

stan

dard

erro

rs;

thes

eare

clu

ster

edat

2-d

igit

ind

ust

ryle

vel

inco

lum

n(1

)in

both

pan

els.

p-v

alu

esd

eriv

edfr

om

wild

boots

trap

s(a

sin

Cam

eron

etal.

2008)

are

insq

uare

bra

cket

s.

Sm

all

p-v

alu

esare

rep

rese

nte

dby

***

(les

sth

an

1%

),**

(les

sth

an

5%

)or

*(l

ess

than

10%

).

21

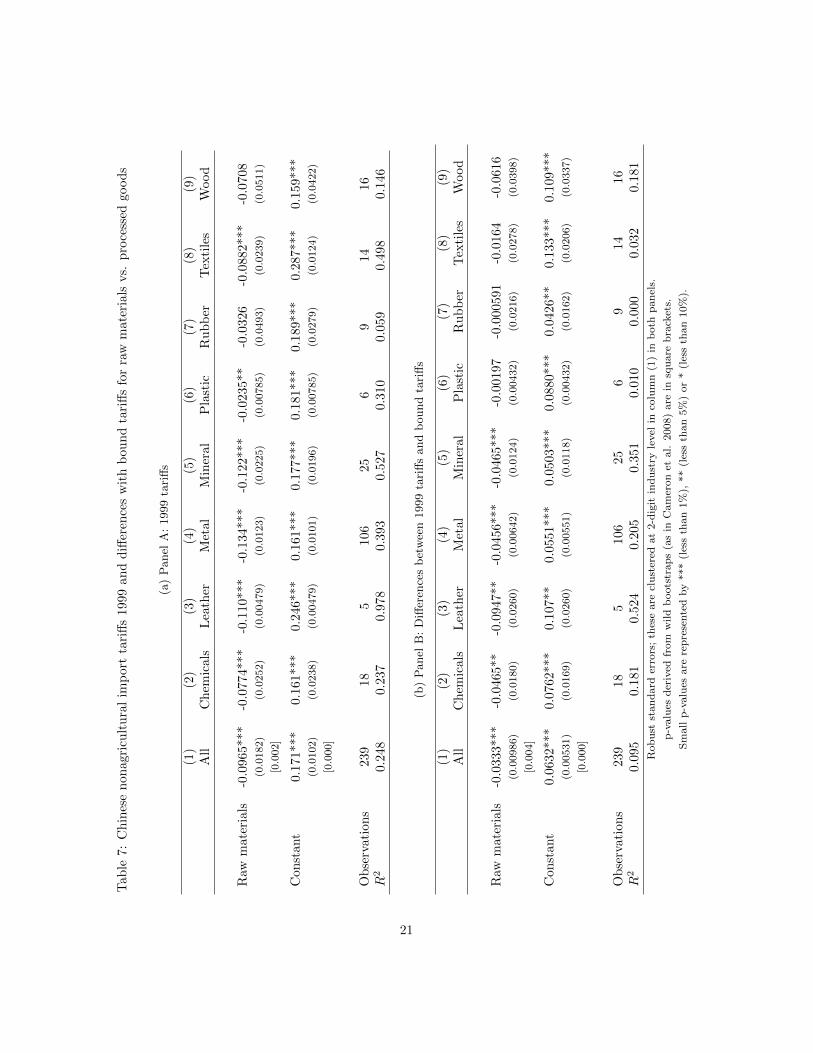

section and the previous one are linked: to what extent is the finding in theprevious section driven by relatively higher tariff cuts for processed goods beingreplaced by relatively higher export tax increases for raw materials? I firstobserve that China’s pre-WTO tariff schedule was characterized by systematictariff escalation; i.e. higher tariffs on processed goods as compared to rawmaterials. Using the HS definition of raw materials, Panel A of Table 7 showsthat China’s applied tariffs in 1999 were higher on processed goods than rawmaterials overall (column (1)) and within each of the eight raw materials supplychains (columns (2) through (9)), with this result being statistically significantfor six of eight supply chains.

Unsurprisingly, China’s WTO accession involved import tariff cuts that werehigher on goods whose initial tariffs were already high (Brandt et al. 2013).Using the tariff cut variable from section 2.2.2 (i.e. max{tar1999− tarbound, 0}),Panel B of Table 7 shows that this involved an overall decline in tariff escalation(column (1)): average tariffs on processed goods industries declined by twice asmuch as average tariffs on raw materials due to WTO accession, a statisticallysignificant difference. Columns (2) to (9) also show that tariff escalation wassignificantly reduced in four of eight supply chains, with a fifth (wood) seeinglarger declines in average processed goods tariffs by 6 percentage points, thoughwith a relatively large standard error. Notably, the three supply chains forwhich the extent of tariff escalation does not appear to have fallen include bothof those which did not experience relatively higher rises in export taxes on rawmaterials (textiles and rubber).

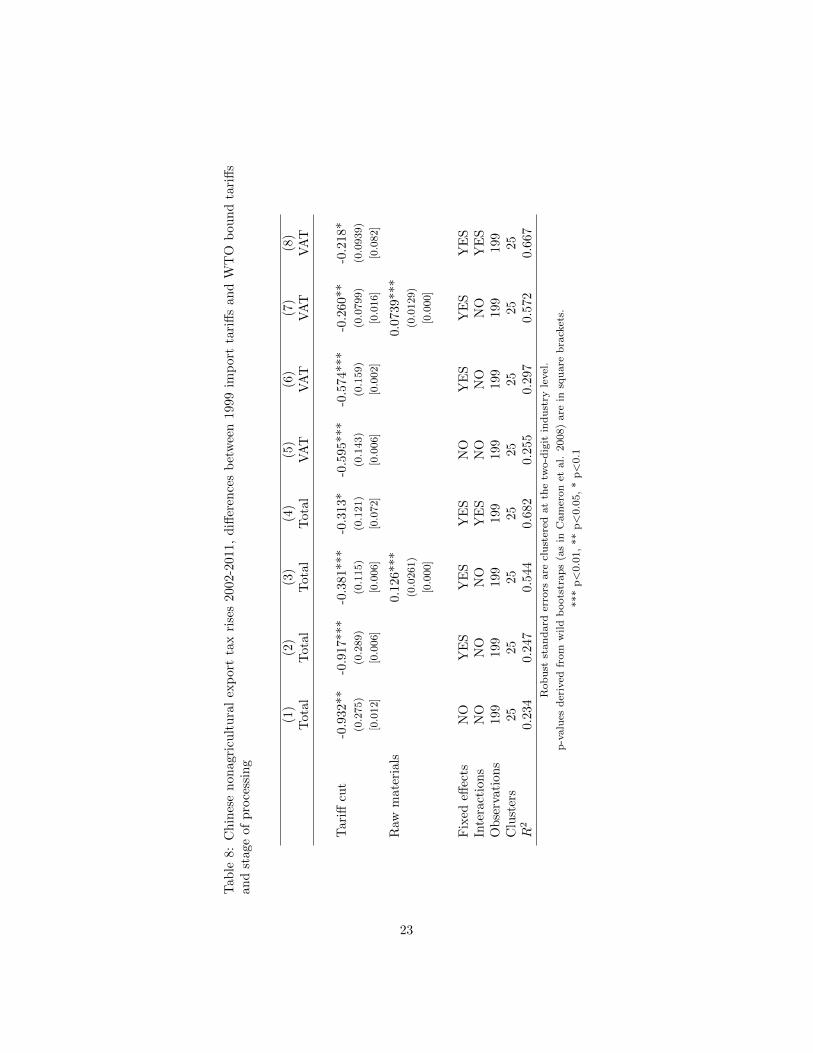

The connection between rises in raw materials export taxes, reductions intariff escalation and the results in section 2.2.2 are tested more directly in Table8. Column (1) of Table 8 reproduces the results of column (2) of Table 4 –i.e. a regression of tax rises on WTO-induced tariff cuts at the industry level– but including only the 199 industries that have been categorized into supplychains. The resulting estimated coefficient on tariff cuts is very similar to thatin column (2) of Table 4. This regression is then rerun with supply chain fixedeffects, which has little effect on the estimated relationship between tax increasesand tariff reductions, as shown in column (2) of Table 8. In order to assess theextent to which this relationship is attenuated by controlling for the largerrises in raw materials export taxes, the raw materials dummy variable is thenadded to the regression. The answer is substantially although not completely,as the coefficient on tariff cuts declines in absolute value from -0.92 to -0.38, butremains statistically significant (Column (3)). When the coefficient on the rawmaterials variable is allowed to vary by supply chain through the inclusion ofa full set of interactions between the raw materials and supply chain dummiesin Column (4), the size of the relationship between tax rises and tariff cuts isreduced to -0.31, approximately a third of its level in Column (2). Running theseregressions for VAT-rebate-only export taxes yields similar results (Columns (5)to (8)): the coefficient of interest is reduced in absolute value from -0.57 to -0.22after accounting for differences in tax rises between raw materials and processedgoods.

22

Tab

le8:

Ch

ines

en

onag

ricu

ltu

ral

exp

ort

tax

rise

s2002-2

011,

diff

eren

ces

bet

wee

n1999

imp

ort

tari

ffs

an

dW

TO

bou

nd

tari

ffs

and

stag

eof

pro

cess

ing

(1)

(2)

(3)

(4)

(5)

(6)

(7)

(8)

Tot

alT

otal

Tota

lT

ota

lV

AT

VA

TV

AT

VA

T

Tar

iffcu

t-0

.932

**-0

.917

***

-0.3

81***

-0.3

13*

-0.5

95***

-0.5

74***

-0.2

60**

-0.2

18*

(0.2

75)

(0.2

89)

(0.1

15)

(0.1

21)

(0.1

43)

(0.1

59)

(0.0

799)

(0.0

939)

[0.0

12]

[0.0

06]

[0.0

06]

[0.0

72]

[0.0

06]

[0.0

02]

[0.0

16]

[0.0

82]

Raw

mat

eria

ls0.1

26***

0.0

739***

(0.0

261)

(0.0

129)

[0.0

00]

[0.0

00]

Fix

edeff

ects

NO

YE

SY

ES

YE

SN

OY

ES

YE

SY

ES

Inte

ract

ion

sN

ON

ON

OY

ES

NO

NO

NO

YE

SO

bse

rvat

ion

s19

919

9199

199

199

199

199

199

Clu

ster

s25

2525

25

25

25

25

25

R2

0.23

40.

247

0.5

44

0.6

82

0.2

55

0.2

970.5

72

0.6

67

Rob

ust

stan

dard

erro

rsare

clu

ster

edat

the

two-d

igit

ind

ust

ryle

vel

.

p-v

alu

esd

eriv

edfr

om

wild

boots

trap

s(a

sin

Cam

eron

etal.

2008)

are

insq

uare

bra

cket

s.

***

p<

0.0

1,

**

p<

0.0

5,

*p<

0.1

23

2.3 Other export policies

A potential problem with the export tax measures used in the empirical analysisabove is that they only take account of two instruments that are readily quan-tified and aggregated – export duties and VAT rebates – but ignore changes inChina’s other export policies. For example, it is possible that there was substi-tution between export instruments during the period of interest: rising exportduties and VAT rebates might have acted as replacements for other export poli-cies of declining restrictiveness. In this case, the inferences about substitutionbetween import and export policies reached in the sections above might beinvalid because of the bias induced by other policies omitted in the relevantregressions.

I have thus collected data on all other product-level measures identified as‘policies affecting exports’ in the four WTO Trade Policy Reviews of China(WTO 2006, 2008, 2010, 2012): prohibition of exports via processing trade;export licensing; export quotas; state trading requirements; and export prohibi-tions.16 In all cases, data is sourced from official policy notices: annual schedulesof products subject to export licenses, quotas and state trading requirements,and ad hoc announcements of changes in policy regarding prohibition of exports(via processing trade or otherwise).

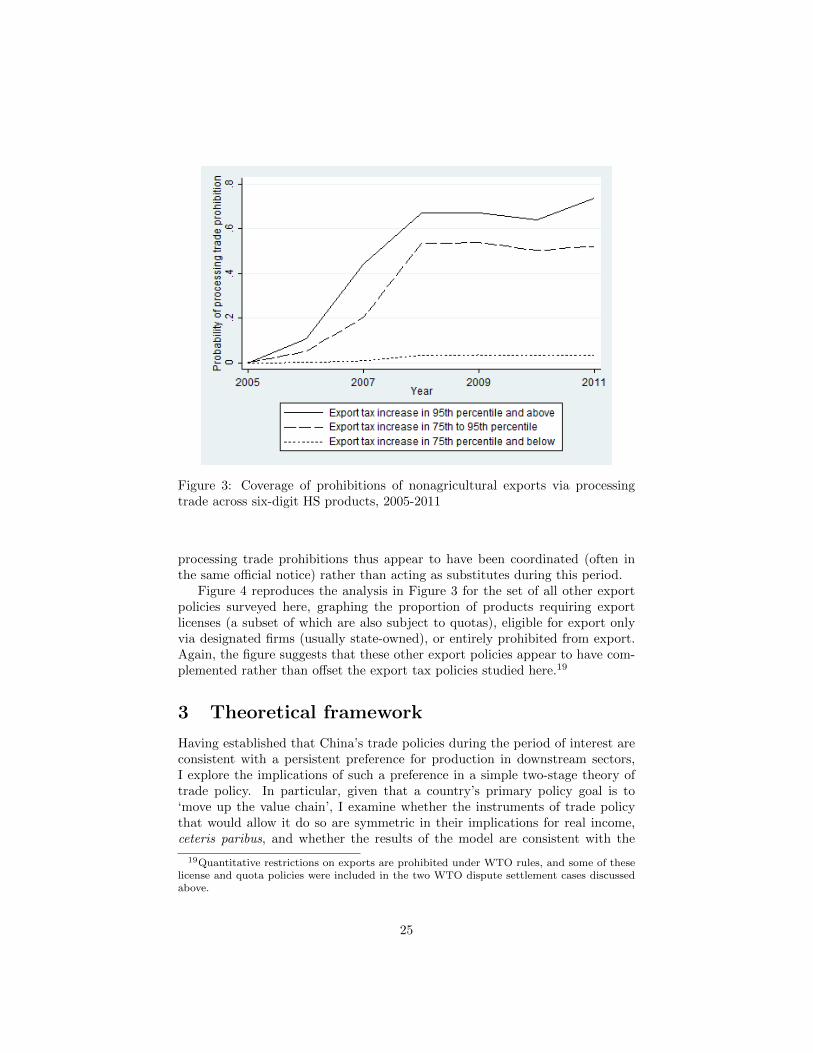

Among these instruments, the largest change in policy after China’s WTOaccession was to the list of products for which export via processing trade is pro-hibited. Processing trade accounted for approximately half of Chinese exportsthroughout the period of interest, and its existence is particularly important tothe analysis of this paper because exports via processing trade are duty-free,implying the possibility of tax-induced substitution between the ‘ordinary trade’and ‘processing trade’ regimes.

The data I record on prohibitions of export via processing trade begins withan official notice from 2004 declaring that “[a]djustments and updates will bemade annually to the list of prohibited processing trade goods ... in accordancewith the country’s economic development and industrial policies.”17 As shownin Figure 3, from 2005 (the first full year after the list of goods in this noticebecame effective) to 2011, the list of products banned from export via processingtrade expanded greatly.18 Moreover, the products prohibited from export viaprocessing trade corresponded very closely to the products on which export taxesincreased during the period. Among goods whose total export tax increase (asdefined in section 2.1 above) between 2002 and 2011 was among the top 5%across products, 73% were included on the prohibited list for processing tradein 2011. This was also true of 43% of other products in the top quartile ofexport tax rises, but only 3% of other products. Increases in export taxes and

16Some policies that are identified in the WTO reviews but that do not vary primarily atthe product level, such as tax concessions to foreign-invested enterprises, are not consideredhere.

17See Shangwubu, haiguanzongshu, guojiahuanjingbaohuzongju gonggao (2004) no. 55.18Note that I classify a six-digit product as being prohibited from export via processing trade

if I observe at least one eight-digit or ten-digit good within that six-digit product category onthe list of prohibited goods at the beginning of a given year.

24

Figure 3: Coverage of prohibitions of nonagricultural exports via processingtrade across six-digit HS products, 2005-2011

processing trade prohibitions thus appear to have been coordinated (often inthe same official notice) rather than acting as substitutes during this period.

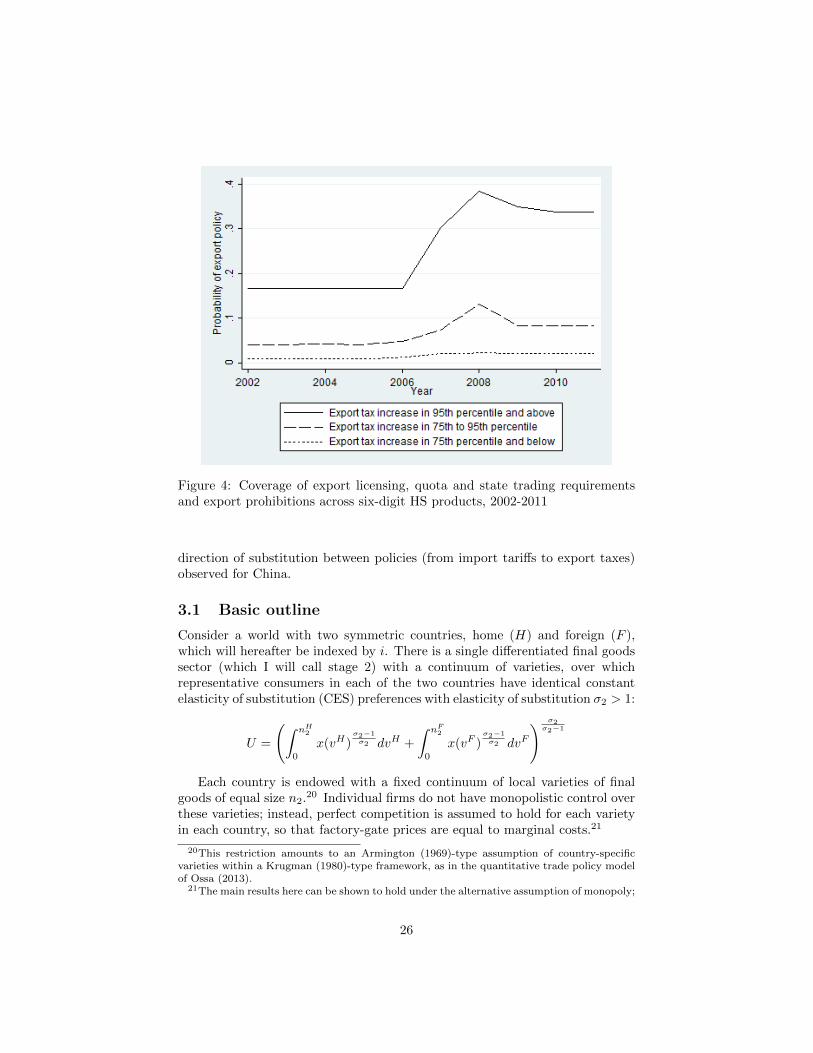

Figure 4 reproduces the analysis in Figure 3 for the set of all other exportpolicies surveyed here, graphing the proportion of products requiring exportlicenses (a subset of which are also subject to quotas), eligible for export onlyvia designated firms (usually state-owned), or entirely prohibited from export.Again, the figure suggests that these other export policies appear to have com-plemented rather than offset the export tax policies studied here.19

3 Theoretical framework

Having established that China’s trade policies during the period of interest areconsistent with a persistent preference for production in downstream sectors,I explore the implications of such a preference in a simple two-stage theory oftrade policy. In particular, given that a country’s primary policy goal is to‘move up the value chain’, I examine whether the instruments of trade policythat would allow it do so are symmetric in their implications for real income,ceteris paribus, and whether the results of the model are consistent with the

19Quantitative restrictions on exports are prohibited under WTO rules, and some of theselicense and quota policies were included in the two WTO dispute settlement cases discussedabove.

25

Figure 4: Coverage of export licensing, quota and state trading requirementsand export prohibitions across six-digit HS products, 2002-2011

direction of substitution between policies (from import tariffs to export taxes)observed for China.

3.1 Basic outline

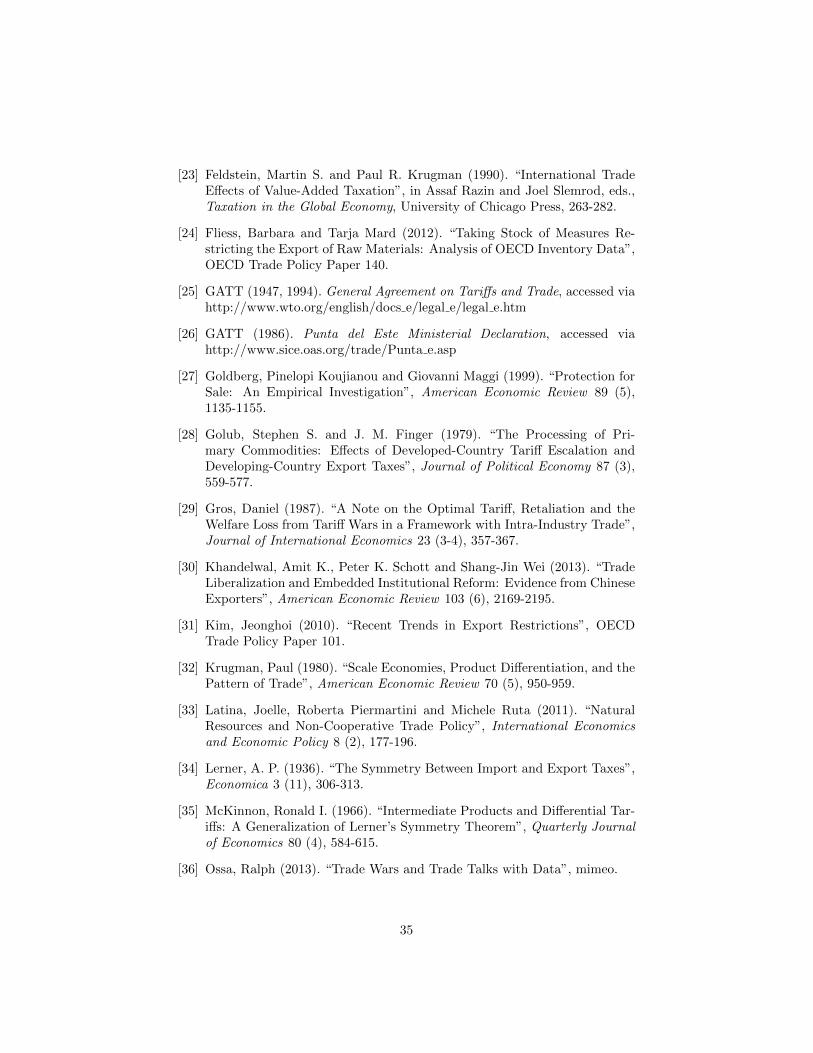

Consider a world with two symmetric countries, home (H) and foreign (F ),which will hereafter be indexed by i. There is a single differentiated final goodssector (which I will call stage 2) with a continuum of varieties, over whichrepresentative consumers in each of the two countries have identical constantelasticity of substitution (CES) preferences with elasticity of substitution σ2 > 1:

U =

(∫ nH2

0

x(vH)σ2−1σ2 dvH +

∫ nF2

0

x(vF )σ2−1σ2 dvF

) σ2σ2−1

Each country is endowed with a fixed continuum of local varieties of finalgoods of equal size n2.20 Individual firms do not have monopolistic control overthese varieties; instead, perfect competition is assumed to hold for each varietyin each country, so that factory-gate prices are equal to marginal costs.21

20This restriction amounts to an Armington (1969)-type assumption of country-specificvarieties within a Krugman (1980)-type framework, as in the quantitative trade policy modelof Ossa (2013).

21The main results here can be shown to hold under the alternative assumption of monopoly;

26

Production of stage 2 goods requires a combination of labour, of which eachcountry has an endowment L that is inelastically supplied to firms, and a contin-uum of imperfectly substitutable raw materials, with elasticity of substitutionacross materials inputs of σ1 > 1.22 Raw materials and labour have Cobb-Douglas shares β and 1− β in the sector 2 production function, which may bewritten as:

q(vi2) = z2

(∫ nH1

0

mi2(vH1 )

σ1−1σ1 dvH1 +

∫ nF1

0

mi2(vF1 )

σ1−1σ1 dvF1

) σ1σ1−1β

l(vi2)1−β

These raw materials are also spread across the two countries symmetrically,in the sense that each country produces a nonintersecting continuum of n1distinct raw materials. Firms specializing in raw materials production (stage1) are also assumed to be perfectly competitive. Production of raw materialsrequires only labour: q(vi1) = z1l(v

i).The two countries are able to trade without cost unless trade taxes are

charged by one of the countries; I assume that trade taxes may be imposedonly by H without retaliation from F . Given the model’s symmetry assump-tions, under free trade, a share 1− β of each country’s labour force engages inproduction of stage 2 goods; i.e. LH2 = LF2 = (1− β)L if there is free trade.

Now say that the government of H sets the policy goal of ‘moving up thevalue chain’, which I characterize as a shift of a small proportion of the labourforce from stage 1 production into stage 2.23 In particular, say H targetsdLH2 /L = k > 0. Also say that rather than considering the full spectrumof possible policies with which it might achieve this goal, the government ofH instead chooses among a limited set of simple instruments: a single uni-form trade tax (import tariff or export tax) or trade subsidy (import subsidyor export subsidy) on one of the two stages of production. The question to beinvestigated below is which of these policies accomplish the goal at minimumcost (i.e. maximum gain) to local real income.24

Given the goal of moving a small amount of H labour into stage 2, fourpossible policies will be under consideration: a small import tariff on stage 2,a small export tax on stage 1, a small export subsidy on stage 2 and a small