exponential smoothing

TRANSCRIPT

1. ¿Qué significa la palabra ‘exponencial’ en esta técnica de modelado?

2. El modelo se creó en 1960. ¿Por qué crees que siga siendo popular después de 50 años?

3. ¿Qué tipos de tendencia considera esta técnica?

4. ¿Qué tipos de estacionalidad considera esta técnica?

5. El modelo holt winters tiene por lo menos tres puntos débiles que se han intenadoresolver desde su creación. ¿Cuáles son?

Use the historical data to forecast the future

Let different parts of the history have different impact on the forecasts

Forecast model is not developed from any statistical theory

weight

today

Decreasing weight given

to older observations

0 1

( )

( )

( )

1

1

1

2

3

Simple exponential smoothing

Double exponential smoothing

Triple exponential smoothing

Exponential smoothing works well with data that is “moving sideways” (stationary) ( simple smoothing)

Must be adapted for data series which exhibit a definite trend (double exponential smoothing)

Must be further adapted for data series which exhibit trend and seasonal patterns (triple exponential smoothing)

It’s important to get familiar with this notation

Further on we’ll introduce the trend and seasonal components

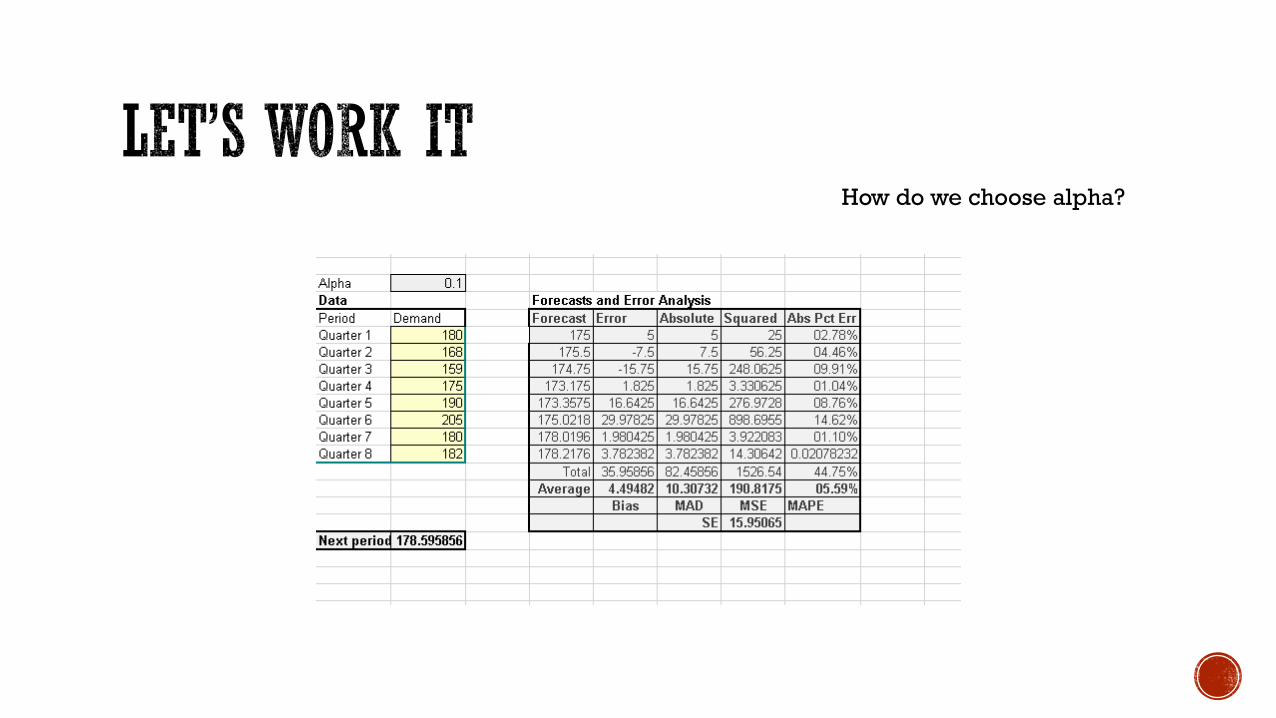

Mean Forecast Error (MFE or Bias): Measures average deviation of forecast from actual.

Mean Absolute Deviation (MAD): Measures average absolute deviation of forecast from actual.

Mean Absolute Percentage Error (MAPE):Measures absolute error as a percentage of the forecast.

Standard Squared Error (MSE): Measures variance of forecast error

Tracking Signal (TS): Measures the shift/drift of the forecasting model to consistently overestimate or underestimate demand

SEASONAL

• None

SEASONAL

• Additive

SEASONAL

•

Multiplicative

DOUBLE EXP SMOOTHING TRIPLE EXP SMOOTHING (WINTERS’ METHOD)

More complex ES models (double ES and Winters’ method), have been

developed to accommodate time series with trend and seasonal components.

The general idea here is that forecasts are not only computed from consecutive

previous observations (as in SES), but an independent (smoothed) trend and

seasonal component can be added.