experience clarity // cpas & advisors fraud trends and detection: an update shauna...

TRANSCRIPT

experience clarity //

CPAs & ADVISORS

FRAUD TRENDS AND DETECTION: AN UPDATEShauna Woody-Coussens, CFEManaging Director – Forensic & Valuation Services

COST OF INSURANCE FRAUD

Nearly $80 billion in fraudulent claims made in the US annually1

May be a conservative figure as much insurance fraud goes undetected and unreportedFraudulent claims estimated to increase the average household’s insurance costs by more than $300 per year

After narcotics trafficking, insurance fraud is the largest criminal enterprise in the US2

Insurance fraud is the 2nd most costly white-collar crime in US, behind tax evasion3

1 Coalition Against Insurance Fraud estimate2 Property Casualty 3603 National Insurance Crime Bureau

2 // experience clarity

DATA ANALYTICS AND THE INSURANCE INDUSTRY

Traditional and recent usesActuarial risk analysisBehavior-based credit scores as an enhancement to personal auto insurance underwritingPredictive and optimization models in business processes such as sales, marketing and service

3 // experience clarity

MY GOAL TODAY…

Convince you to use data analytics within your organization to help you prevent and detect occupational fraud

4 // experience clarity

OCCUPATIONAL FRAUD TRENDS

5 // experience clarity

ACFE 2014 REPORT TO THE NATIONS

Typical organization loses 5% of its annual revenue to fraud

Median loss was $145,000 for all companiesOne fifth of losses were over $1 million

Frauds lasted 18 months before being detected

58% of victim organizations recover nothing

6 // experience clarity

7 // experience clarity

8 // experience clarity

9 // experience clarity

10 // experience clarity

11 // experience clarity

12 // experience clarity

Answer questions through use of analytical softwareAs simple as Excel

Filter Sort

As complex as you want to make itACLIDEASQL

DATA ANALYTICS

13 // experience clarity

WHAT’S THE BIG DEAL?

“Big Data” nightmare – we need helpManual review is inefficientSuspicious activity is a 96.5% match to normal, so you are less likely to notice it through a manual reviewSampling does not reveal patterns & trendsSystem weaknesses lead to fraudSo… even if no fraud is evident, weaknesses are often uncovered that can be corrected to help mitigate fraud

14 // experience clarity

APPLICATIONS IN THE INSURANCE INDUSTRY

15 // experience clarity

CorruptionBillingExpense reimbursement

Non-cashPayroll

TOP OCCUPATIONAL FRAUD SCHEMES IN THE INSURANCE INDUSTRY

16 // experience clarity

17

Corruption

CORRUPTION

An employee misuses his or her influence in a business transaction in a way that violates his or her duty to the employer in order to gain a direct or indirect benefit In my experience, the most common form of corruption is the payment of kickbacks to related to purchases

18 // experience clarity

CORRUPTION EXAMPLE

Insurance agent colluded with an auto glass vendor to bill for OEM glass replacement when wrecking yard glass often used

Data mining pointed out unusual level of OEM glass pricing for that vendor Loss was $500,000

19 // experience clarity

RED FLAGS FOR CORRUPTION

Off-book fraud, so very hard to detectPayments often do not go through the organization’s accounting recordsPayments often paid in cash

Look for “behavioral” red flagsRapidly increasing purchases from one vendorExcessive purchases of goods and servicesToo close of a relationship with a vendor

20 // experience clarity

Compare order quantity to optimal reorder quantityCompare purchase volumes/prices from like vendorsCompare quantities ordered and receivedCheck for inferior goods (# of returns by vendor)Unstructured data review (read suspected fraudster’s email….)

DATA ANALYTICS FOR CORRUPTION

21 // experience clarity

22

Billing Schemes

Fraudster creates false support for a fraudulent purchase, causing the nonprofit to pay for goods or services that are nonexistent, overpriced or unnecessary

Invoicing via shell companyInvoicing via an existing vendor

False invoicing for non-accomplice vendorsPay-and-return schemes

Personal purchases with nonprofit’s funds

BILLING SCHEMES

23 // experience clarity

BILLING FRAUD EXAMPLE

Employee set up fictitious vendors to bill employer for purchases never made

Employee made repeated purchases in the amount of $24,950 when his sole authority was $25,000Loss was $2.2 million over a 2 year period

24 // experience clarity

Vendor anomaliesPayment anomaliesPurchasing anomalies

Accounts payable invoicesCredit card/p-card purchases

RED FLAGS FOR BILLING SCHEMES

25 // experience clarity

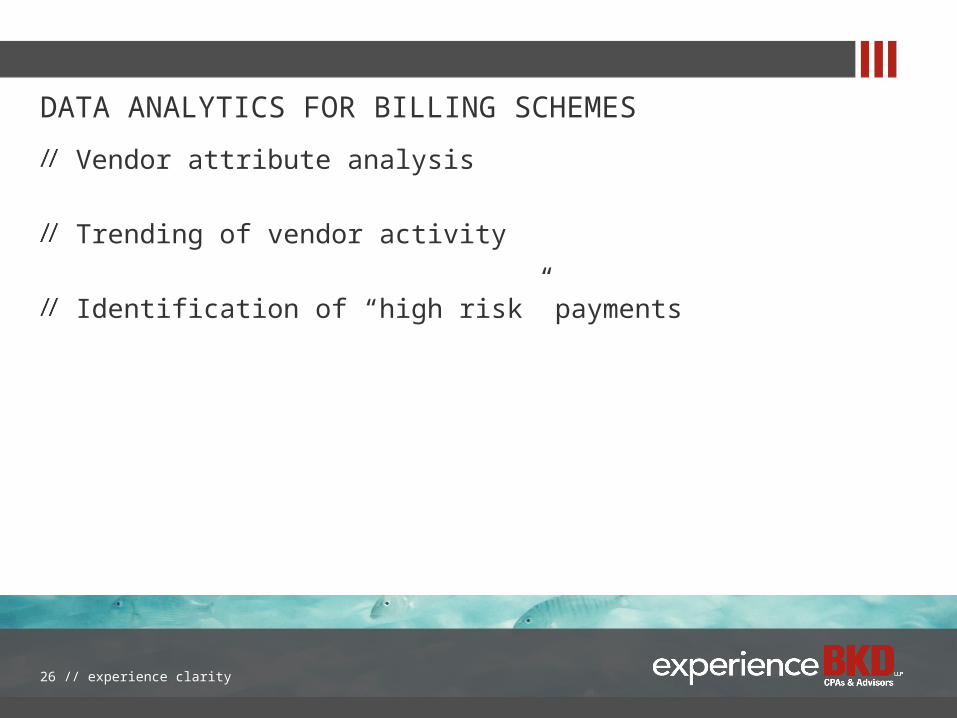

Vendor attribute analysis

Trending of vendor activity

Identification of “high risk” payments

DATA ANALYTICS FOR BILLING SCHEMES

26 // experience clarity

27

Expense Reimbursements & Purchasing Cards

EXPENSE REIMBURSEMENT/P-CARDS

Any scheme in which an employee makes a claim for reimbursement or fictitious or inflated business expenses

Employee files fraudulent expense report, claiming personal travel, nonexistent meals, etc. Employee purchases personal items and submits and invoice to employer for paymentEmployee purchases goods/services for inappropriate uses and charges to employer for payment

28 // experience clarity

RED FLAGS FOR EXPENSE REIMBURSEMENT /P-CARD SCHEMES

Expenses exceed what was budgeted or prior years totalsExpenses claimed on days employee did not workPurchases that do not appear to be business relatedMinimal or non existent support for requestsAltered receiptsUnusual or excessive reimbursements to one employeeSubmitted receipts are consecutively numberedExpenses in round dollar amountsExpenses just below receipt submission threshold

29 // experience clarity

Identify transactions on weekends, holidays or while employee is on vacationIdentify split transactions in which a large purchase are split into smaller transactions just under approval thresholdIdentify unusually high or frequent expense reimbursement/p-card usageIdentify expenses in round dollar amounts

DATA ANALYTICS FOR EXPENSE REIMBURSEMENT/P-CARD SCHEMES

30 // experience clarity

31

Non-Cash

NON-CASH FRAUD SCHEMES

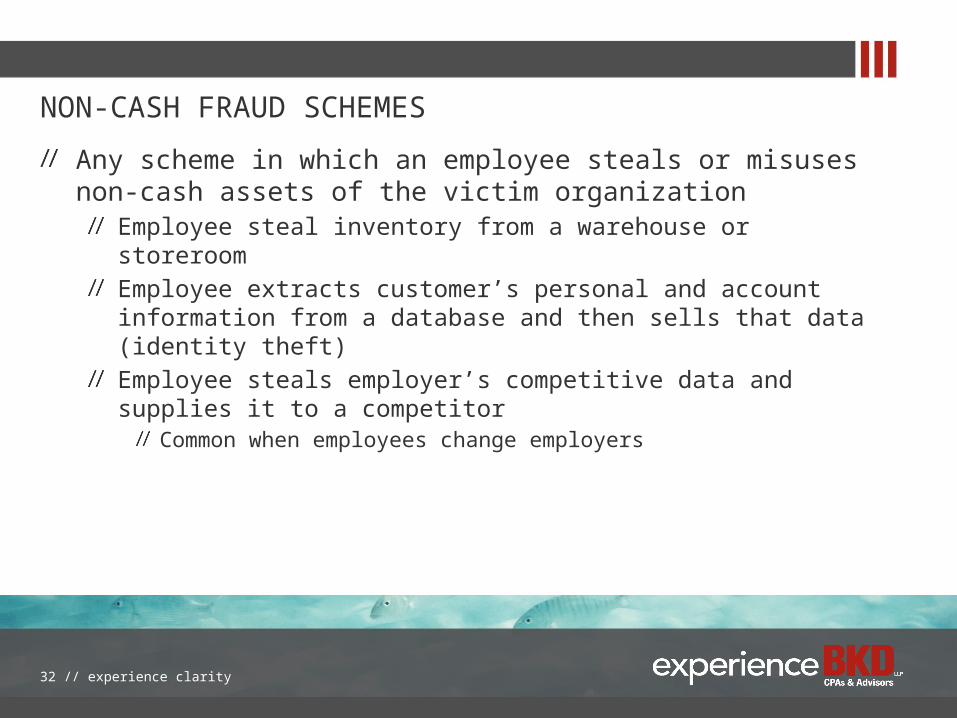

Any scheme in which an employee steals or misuses non-cash assets of the victim organization

Employee steal inventory from a warehouse or storeroomEmployee extracts customer’s personal and account information from a database and then sells that data (identity theft)Employee steals employer’s competitive data and supplies it to a competitor

Common when employees change employers

32 // experience clarity

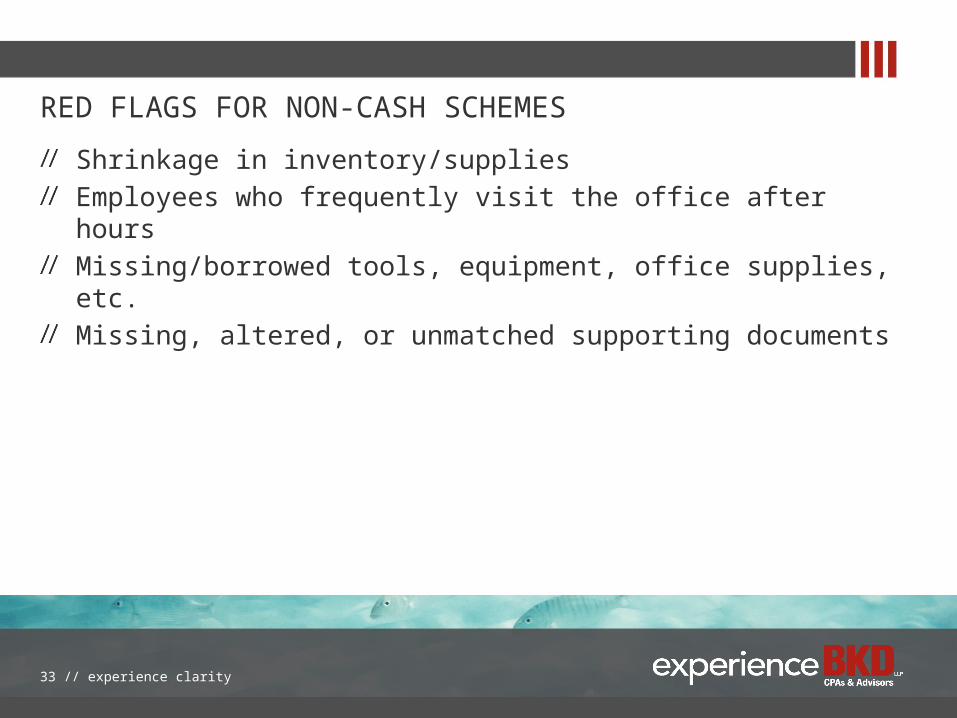

RED FLAGS FOR NON-CASH SCHEMES

Shrinkage in inventory/suppliesEmployees who frequently visit the office after hoursMissing/borrowed tools, equipment, office supplies, etc.Missing, altered, or unmatched supporting documents

33 // experience clarity

DATA ANALYTICS FOR NON-CASH SCHEMES

Automated monitoring of:Online transactions and inquiriesThe date, time and source of online access, especially if the system can be accessed from a WAN or the InternetReport generation and downloading, including operational and custom reports or queries, especially those containing customer/client account informationEmails sent and received and attachment sizes

34 // experience clarity

35

Payroll

Ghost employeesFictitious employees entered into payroll system

Terminated employeesTerminated employees remain on payroll system with direct deposit to a current employee’s account

Duplicate payrollOverpayment schemes

Higher pay rates, inflated hours, unauthorized bonuses

PAYROLL SCHEMES

36 // experience clarity

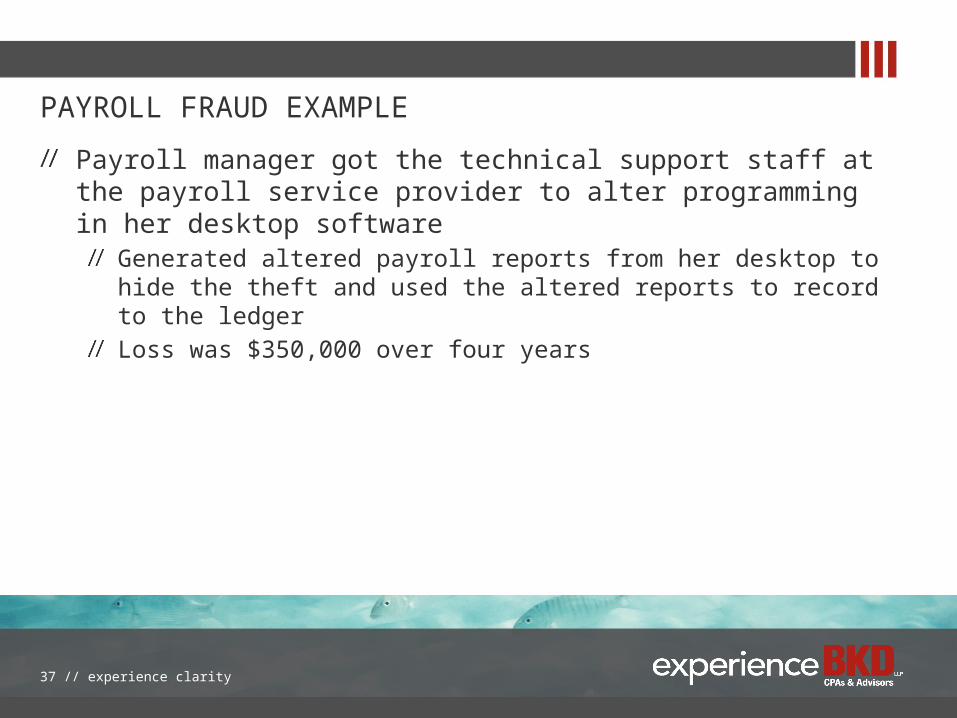

PAYROLL FRAUD EXAMPLE

Payroll manager got the technical support staff at the payroll service provider to alter programming in her desktop software

Generated altered payroll reports from her desktop to hide the theft and used the altered reports to record to the ledgerLoss was $350,000 over four years

37 // experience clarity

Look for lack of:Bank accounts for electronic paymentsHome addresses and phone numbersHoliday leave, vacation or sick leaveBenefit/tax deductions

Also look forDuplicate SSNsDuplicate bank account numbersDuplicate home addressesPO box addressesPayments after termination

RED FLAGS/DATA ANALYTICS FOR PAYROLL SCHEMES

38 // experience clarity

INNOVATIONS IN ADVANCED TECHNOLOGY TOOLS

39 // experience clarity

TYPES OF UNSTRUCTURED DATA

Email (corporate and personal)Network Files and ECM SystemsPhone records, cell phonesComputer hard drives (deleted activity)Internet history, social media, chat, Skype, IMBoard minutes, performance appraisals

40 // experience clarity

LEVERAGE DATA IN YOUR ORGANIZATION

41 // experience clarity

DATA ANALYTICS – A GUIDE TO APPLICATION

1. Build a profile of potential risks• What are your highest risk business processes?• What frauds could occur in those processes?• What would red flags for fraud look like in those business processes?

2. Identify data available to help test for potential fraud• Identify and define specific fraud risks to be tested• For each risk, identify and define data requirements, data access processes and

analysis logic

3. Develop procedures & analyze data• Start with relatively simple tests and then add more complex analysis building a

library of specific tests• This is not testing a sample, it is testing the POPULATION

42 // experience clarity

DATA ANALYTICS – A GUIDE TO APPLICATION

4. Make analysis results understandable• Try to answer one question at a time

5. Does analysis result address the identified fraud risk?• If not, go back to step #3 and refine• Are there additional tests that are needed

6. Perform investigation of anomalies or unexpected patterns, as appropriate

43 // experience clarity

QUESTIONS?

Contact Information

Shauna Woody-Coussens, CFEBKD, LLP

1201 Walnut, Ste. 1700Kansas City, MO 64106

44 // experience clarity

THANK YOU

FOR MORE INFORMATION // For a complete list of our offices and subsidiaries, visit bkd.com or contact:

Shauna Woody-Coussens, CFE // Managing [email protected] // 816.701.0150

45 // experience clarity