expectations islamic microfinance: fulfilling social … microfinance: fulfilling social and...

TRANSCRIPT

Islamic Microfinance: Fulfilling Social and Developmental Expectations 1 of 7www.qfinance.com

Islamic Microfinance: Fulfilling Social and DevelopmentalExpectationsby Mehmet Asutay

Executive Summary

Islamic banking and finance (IBF) is a value-oriented ethical proposition; the principles of IBF can be locatedin the principles and norms of Islamic moral economy (IME), which aims at human-centered economicdevelopment as opposed to the financialization of the economy.Social responsibility is an essential part of IBF; however, IBF institutions have been criticized for their socialfailure.Microfinance is a novel method for human-oriented economic development and a capacity-building tool,which easily fits into the IBF paradigm through social responsibility.The financial instruments of IBF and IME institutions can provide an important base for the development andprogress of Islamic microfinance (IMF), which fulfills the aspirations of developing communities in an Islamicway.A number of IBF institutions have demonstrated success in IMF, particularly by overcoming the burden ofinterest on the poor and expanding the asset base.

Rationalizing Islamic Microfinance through Essentializing the Islamic MoralEconomy

Islamic banking and finance (IBF) has become a mainstream financing method utilized by Islamic, as well asconventional, banking and financial institutions all over the world. Recently, however, IBF has been criticizedfor its social failure, in the sense that its operations are not different from the existing conventional toolsminus the interest. An essential nature of this criticism is related to the foundational axioms and principlesof IME which, as a worldview, is based on the authentic principles of Islam. Thus, IME is an authenticresponse to the failure of economic developmentalism in the Muslim world in constructing a human-centereddevelopment. In this attempt, IBF was considered as the financing and operational tool of the new paradigm,and consequently it is expected to fulfill the expectations and aspirational paradigm of IME.

The foundational principles and axioms of IME aimed at revealing the principles behind IBF through anethical worldview are:

vertical ethicality in terms of individuals as the creature of God being equal (tawhid);social justice and beneficence (adalah and ihsan) in terms of horizontal ethicality;growth in harmony (tazkiyah);allowing the social (individual and society) and natural environment to reach to and sustain its perfection(rububiyah);voluntary action but also compulsory action (fard) in serving the social interest;individuals, being the vicegerent of God on Earth (khalifah), are expected to fulfill and act according to theseprinciples in their economic and financial behavior.

These foundational principles are justified by a particular methodological understanding; the maqasid al-shariah (objectives of shariah) are interpreted as human well-being, which, in this context, is achievedthrough a socially operating moral economy in an Islamic framework that is expected to produce a sociallyand economic-financially optimum solution in overcoming the socioeconomic problems of a society.

Ethical Objective Functions of Islamic Finance

As part of this ethical economic paradigm, IBF is expected to operate within such an objective functionand framework to establish the optimality between financial operations and social objectives (as a morallyidentified objective function). To operationalize the ethical objective in IBF, further principles are developed

Islamic Microfinance: Fulfilling Social and Developmental Expectations 2 of 7www.qfinance.com

through the ontological sources of Islam. These principles, which aim to promote an ethical and sociallyoriented way of “doing finance,” are as follows.

Prohibition of interest (or riba) with the objective of providing a stable and socially efficient economicenvironment.Prohibition of fixed return on nominal transactions, with the objective of creating productive economic activityor asset-based financing over the debt-based system.In this moral economy, money does not have any inherent value in itself and therefore it cannot be createdthrough the credit system.The principle of profit and loss sharing, and hence risk sharing, is the essential axis around which economicand business activity takes place. This prevents the capital owner from shifting the entire risk on to theborrower, and hence it aims to establish a just balance between effort and return, and between effort andcapital. This axiom identifies the essential nature of Islamic microfinance.An important consequence of the profit/loss sharing principle is the participatory nature of economic andbusiness activity, as IBF instruments, capital, and labor merge to establish partnerships through theirindividual contributions which, as a principle, constitutes the fundamental nature of microfinance.By essentializing productive economic and business activity, uncertainty, speculation, and gambling are alsoprohibited, with the same rationale of emphasizing asset-based productive economic activity.

As can be seen, each of these principles, together with the above-mentioned axioms, provide rationale as towhy microfinancing is an essential part of IME and, hence, IBF. The following description of IBF in terms ofinstitutional and operational features provides further rationale as to why microfinance is inherently Islamic inits nature (Khan, 2007).

It is a form of community banking aiming at serving communities, not markets;It offers responsible finance, as it runs systematic checks on finance providers and restrains consumerindebtedness; it also offers ethical investments and corporate social responsibility (CSR) initiatives;It represents an alternative paradigm in terms of stability by linking financial services to the productive, realeconomy; it provides a moral compass for capitalism;It fulfills aspirations in the sense that it widens the ownership base of society and offers success withauthenticity.

As these principles indicate, IBF should serve social interests (for example, through microfinance) inestablishing its financial optimality such that it offers ethical and social solutions to development in Muslimand developing countries.

While IBF has been criticized for not fulfilling these principles in its current practice due to its adoption of acommercial banking structure, it can be seen that it has the potential to respond to the social objective, whichis an inherent function of Islamic finance.

In helping IBF to demonstrate its original ethical and social nature, new methods of financing can bedeveloped to appeal to their commercial nature as well. Since, by definition, IBF institutions are neverthelessexpected to contribute to social development, they have to move to the third institutionalization stage (thefirst stage was social banking in the 1960s, followed by commercial banking as the second institutionalphase from the mid-1970s until now), in which society and capacity building-oriented institutions, such asmicrofinancing and social banking, should run alongside the commercial banks. This fulfills the social andethical expectations as identified by IME, but also responds to the development needs of the societies inwhich they are operating.

Islamic Microfinance

Microfinance has become a critical tool in tackling poverty and aiding development through building thecapacity for the poor to enjoy greater self-sufficiency and sustainability, granting them access to financialservices and conceptualizing the poor individual as someone with innate entrepreneurial abilities who cangenerate jobs, income, and wealth if given access to credit. Through microfinance, the poor are given theopportunity to become stakeholders in the economy; therefore, enabled and functioning individuals will bethe outcome. Due to this objective function of microfinance, as a development tool it has enjoyed somesuccess. Consequently, a number of conventional financial institutions and banks now offer microfinance insupporting business ideas from small projects to housing projects.

Islamic Microfinance: Fulfilling Social and Developmental Expectations 3 of 7www.qfinance.com

Despite its success, microfinance has been criticized from an Islamic perspective for getting people into debtdue to its fixed interest charges. If a project does not yield the expected returns in conventional financing,difficulties can ensue for the borrower. IBF, thus, offers a more viable solution as a value-oriented financialproposition as part of the IME. Thus, typical IBF instruments, such as musharakah and mudarabah (basedon profit/loss sharing), or institutions such as IBF, but also waqfs (pious foundations), are rather appropriateas providers of microfinance. IMF fits into the asset-based economic paradigm and equity objective of IMEas well as fulfilling all other expectations. Thus, there is compatibility and complementarity between theobjectives and operational mechanism of microfinance and of IBF.

Despite having similar objectives, IBFs have not fully appreciated microfinance, which is also a commerciallyviable undertaking. However, in recent years there has been movement in this direction, as the successfulimplementation of IMF has shown in countries such as Bangladesh, Indonesia, Yemen, and Syria. InBangladesh, however, the direct involvement and success of the Bangladeshi Islamic Bank as a bankinginstitution is an important experiment.

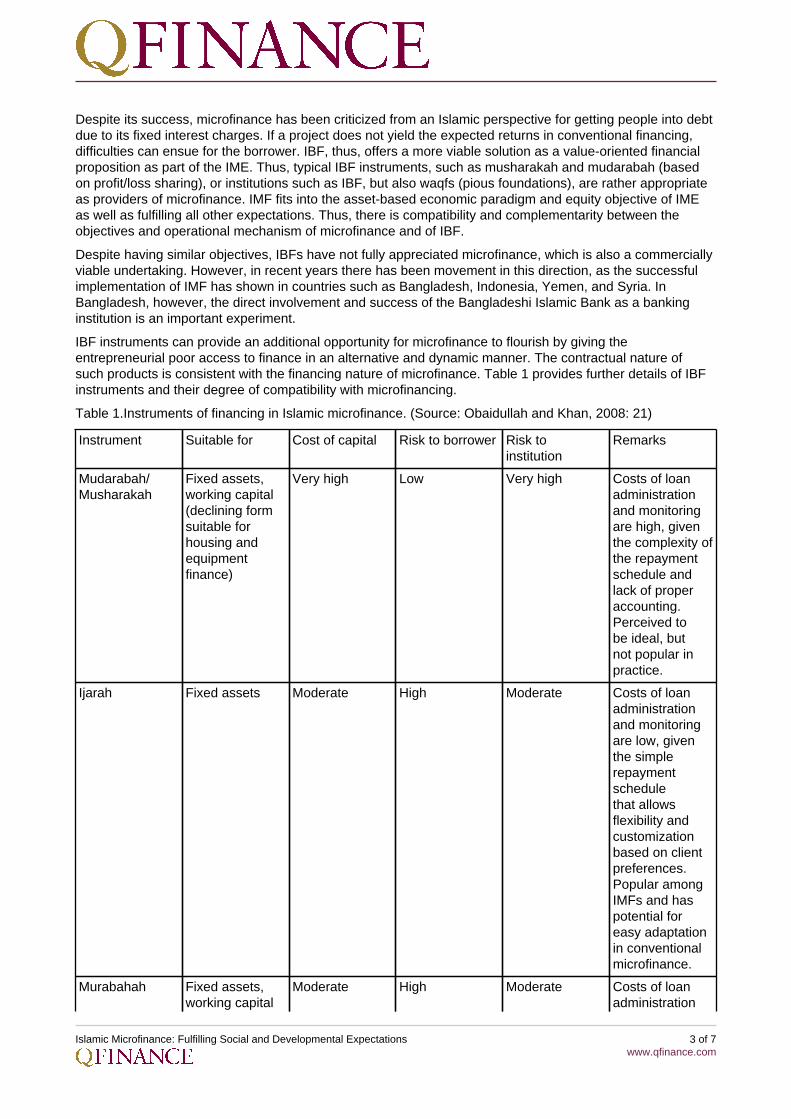

IBF instruments can provide an additional opportunity for microfinance to flourish by giving theentrepreneurial poor access to finance in an alternative and dynamic manner. The contractual nature ofsuch products is consistent with the financing nature of microfinance. Table 1 provides further details of IBFinstruments and their degree of compatibility with microfinancing.

Table 1.Instruments of financing in Islamic microfinance. (Source: Obaidullah and Khan, 2008: 21)

Instrument Suitable for Cost of capital Risk to borrower Risk toinstitution

Remarks

Mudarabah/Musharakah

Fixed assets,working capital(declining formsuitable forhousing andequipmentfinance)

Very high Low Very high Costs of loanadministrationand monitoringare high, giventhe complexity ofthe repaymentschedule andlack of properaccounting.Perceived tobe ideal, butnot popular inpractice.

Ijarah Fixed assets Moderate High Moderate Costs of loanadministrationand monitoringare low, giventhe simplerepaymentschedulethat allowsflexibility andcustomizationbased on clientpreferences.Popular amongIMFs and haspotential foreasy adaptationin conventionalmicrofinance.

Murabahah Fixed assets,working capital

Moderate High Moderate Costs of loanadministration

Islamic Microfinance: Fulfilling Social and Developmental Expectations 4 of 7www.qfinance.com

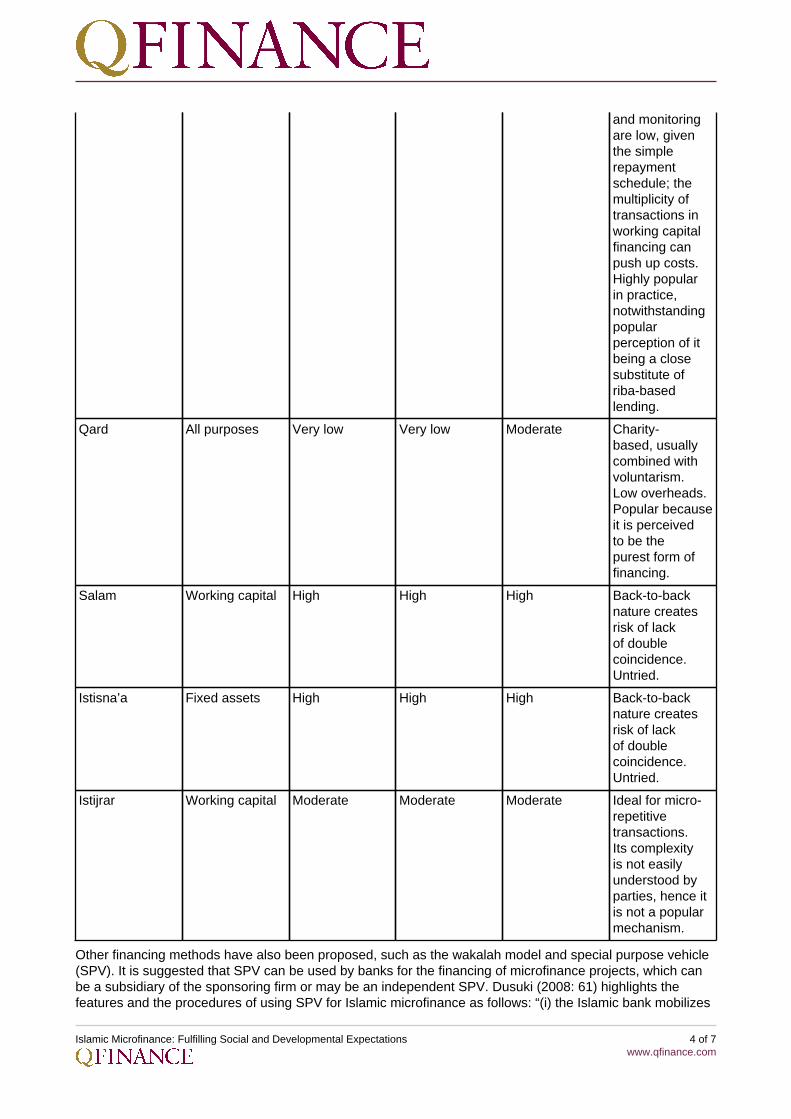

and monitoringare low, giventhe simplerepaymentschedule; themultiplicity oftransactions inworking capitalfinancing canpush up costs.Highly popularin practice,notwithstandingpopularperception of itbeing a closesubstitute ofriba-basedlending.

Qard All purposes Very low Very low Moderate Charity-based, usuallycombined withvoluntarism.Low overheads.Popular becauseit is perceivedto be thepurest form offinancing.

Salam Working capital High High High Back-to-backnature createsrisk of lackof doublecoincidence.Untried.

Istisna’a Fixed assets High High High Back-to-backnature createsrisk of lackof doublecoincidence.Untried.

Istijrar Working capital Moderate Moderate Moderate Ideal for micro-repetitivetransactions.Its complexityis not easilyunderstood byparties, hence itis not a popularmechanism.

Other financing methods have also been proposed, such as the wakalah model and special purpose vehicle(SPV). It is suggested that SPV can be used by banks for the financing of microfinance projects, which canbe a subsidiary of the sponsoring firm or may be an independent SPV. Dusuki (2008: 61) highlights thefeatures and the procedures of using SPV for Islamic microfinance as follows: “(i) the Islamic bank mobilizes

Islamic Microfinance: Fulfilling Social and Developmental Expectations 5 of 7www.qfinance.com

various sources of funds with specific microfinance objectives; (ii) the Islamic bank creates a bankruptcy-remote SPV; (iii) the bank allocates a certain amount of funds and passes it to the SPV; (iv) the funds arethen channeled to various clients depending on needs and demand. For example, zakah funds may onlybe allocated to poor clients for consumption purposes and capacity-building initiatives, while other types offunds can be used to finance their productive economic activities.” The selective nature of expenditures andinvestments, for instance from zakah funds, under such an arrangement, can overcome the fundamentalproblems of microfinance, as this would render financial accessibility for the poor for their consumption butalso help them to engage in capacity-building projects with the objective of productive economic activity andjob creation.

In addition to mainly commercial microfinance instruments, Wilson (2007) proposes that nonbankinginstitutions conduct microfinancing by using the wakalah model through the collection of zakah (compulsoryalms giving for those whose wealth is beyond the established threshold) and waqf (religious charitablefoundation) funds. The wakalah agency model combines certain features of a credit union through financialmanagement with the capital provided by a donor agency; in this case it can be a zakah fund or a waqf.The use of a zakah fund or waqf under such an arrangement would work in the same manner as describedabove.

It should be noted that waqf, as private nonbanking institutions, were used extensively throughout Muslimhistory to provide welfare services to the poor. Therefore, there is clear justification for their revitalizationin modern times to fund microfinance projects aimed at self-sufficiency and a sustainable economic life forthe poor. Furthermore, zakah have great potential in creating funds for development purposes. However,due to the absence of clear and transparent management structures in most Muslim societies, zakah fundsare disbursed to individual causes with no questioning of their wider sustainability and social objectives.Thus, IMF can be an excellent solution for the collection and management of zakah funds for the alleviationof poverty. Other forms of private charitable giving such as sadaqah (voluntary alms), hiba (donations),and tabarru (financial contributions), can form additional funding opportunities for IMF through nonbankingmicrofinance institutions.

In addition to these instruments for raising funds for IMF, deposit-type banking instruments such as wadiah,qard al-hasan, and mudarabah, in the form of savings, current, and time deposits, respectively, can be usedto raise funds for Islamic microfinance institutions. In deciding on the appropriate instrument to deploy, IMFprograms have to consider the relevant costs, benefits, trade-offs, and nature of the instruments, as set outin Table 1.

In addition to the implicit administration costs of IMF projects, potential risk areas have to be taken intoaccount by both the program and the borrower(s). The instrument selection process is dependent on thenature of the client and the project proposed. For instance, if the client is already in business and has aprogressive attitude and good business record, then the musharakah, mudarabah, and murabahah modelsof financial instruments, which involve various degrees of profit/loss sharing, would be appropriate. Inaddition, new clients who do not have any credit or track record could be financed by the qard al-hasan typeof soft loans, which do not have any financing or risk implications.

In the banking-oriented IMF, management of risk by the institution also becomes an important aspectof the process—based on the guarantee (or kafalah) and collateral (daman). The former is used as analternative risk management tool for default and delinquency in the case of financing individual microfinancearrangements, while mutual kafalah is commonly used by IMF institutions in the case of group financing. Itshould be noted that daman in terms of physical assets as collateral is not extensively used in managing riskby IMF institutions.

Another aspect of risk management is the protection of borrowers against potential risks, for whichmicro-takaful (in the form of mutual guarantee) is proposed as a solution, though this has yet to bedeveloped as a fully fledged instrument. In reality, however, largely informal methods are used for theprotection of borrowers or members. These often take the form of short-term emergency funds in the caseof hardship and difficulties. In some cases IMF institutions have managed to raise insurance funds fromcontributions to cover clients against any form of adversity they may face.

As regards Islamic microfinance providers, in addition to formal IMF institutions large numbers of informalmicrofinance institutions, member-based organizations, and nongovernmental organizations are active indelivering IMF-related services in different parts of the developing world.

Islamic Microfinance: Fulfilling Social and Developmental Expectations 6 of 7www.qfinance.com

Conclusion

A financial system should be able to provide financing to different segments of a given society such that,in addition to financial and economic objectives, social objectives may be served. Since social objectivesare an essential part of the IME, it is imperative for IBF to fulfill such objectives alongside their businessinterests. As a social and moral method of financing, IBF, therefore, should contribute directly to economicand social development. This can become possible through social banking and microfinance, though itshould be recalled that the initial experience of IBF in the early 1960s in Egypt was a social bank that wasmicrofinancing-oriented.

Due to the complementarity between IBF and microfinance, there is a need to see further and proactiveinvolvement of IBF and nonbanking Islamic institutions to provide IMF.

By using the essential methods and instruments outlined here, authentic models of IMF can be developedthat will ensure the proactive development and efficient running of microfinancing, so that self-sustaining andhuman-centered development, aimed at helping poor individuals and entrepreneurs who are excluded fromeconomic and financial life, can be achieved as expected by IME by also creating social capital.

More Info

Book:

• Ayub, Muhammad. Understanding Islamic Finance. Chichester, UK: Wiley, 2007.

Articles:

• Ahmed, Habib. “Financing microenterprises: An analytical study of Islamic microfinance institutions.”Islamic Economic Studies 9:2 (March 2002): 27–64. Online at: tinyurl.com/5t7ttsr [PDF].

• Dusuki, Asyraf Wadji. “Banking for the poor: The role of Islamic banking in microfinance initiatives.”Humanomics 24:1 (2008): 49–66. Online at: dx.doi.org/10.1108/08288660810851469

• Wilson, Rodney. “Making development assistance sustainable through Islamic microfinance.”IIUM Journal of Economics and Management 15:2 (2007): 197–217. Online at: www.iium.edu.my/enmjournal/152art3.pdf

Reports:

• Dhumale, Rahul, and Amela Sapcanin. “An application of Islamic banking principles to microfinance:Technical note.” World Bank and UN Development Programme working paper no. 23073. World Bank,1999.

• Khan, Iqbal. “Islamic finance: Relevance and growth in the modern financial age.” Presentation tothe Islamic Finance Seminar organized by the Harvard Islamic Finance Project, London School ofEconomics, UK, February 1, 2007.

• Obaidullah, Mohammed. “Role of microfinance in poverty alleviation: Lessons from experiences inselected IDB member countries.” Islamic Research and Training Institute, 2008. Online at: ssrn.com/abstract=1506077

• Obaidullah, Mohammed, and Tariqullah Khan. “Islamic microfinance development: Challenges andinitiatives.” Policy Dialogue Paper no. 2. Islamic Research and Training Institute, 2008. Online at:ssrn.com/abstract=1506073

See Also

Best Practice

• Rigidity in Microfinancing: Can One Size Fit All?• A Silent Revolution Not to Be Silenced: An Overview of the Microfinance Sector and Its Impact in

PakistanViewpoints

• The Financial Crisis and the World’s Poor

Islamic Microfinance: Fulfilling Social and Developmental Expectations 7 of 7www.qfinance.com

• Microfinancing• Why the World Needs a Green New Deal

Checklists

• Islamic Microfinance

To see this article on-line, please visithttp://www.qfinance.com/financing-best-practice/islamic-microfinance-fulfilling-social-and-developmental-expectations?full