ex-post correction factor to apply in the calculation of ... · ex-post correction factor to apply...

TRANSCRIPT

Ex-post Correction Factor to apply in the calculation of the Public Service Obligation Levy

DOCUMENT TYPE:

Proposed Decision Paper

REFERENCE:

CER/08/170

DATE PUBLISHED:

17 September 2008

QUERIES TO: Jamie Burke [email protected]

The Commission for Energy Regulation, The Exchange,

Belgard Square North, Tallaght,

Dublin 24.

www.cer.ie

Ex-post correction factor in PSO Levy – CER/08/170 17 September 2008

2

CER – Information Page Abstract: Section 39 of the Electricity Regulation Act 1999 sets out the legal basis for the Public Service Obligation (the PSO) levy in Ireland. Statutory Instrument No. 217 of 2002 made under Section 39 requires that the Commission for Energy Regulation (the Commission) review the costs associated with the PSO and set the associated levy for the required period. This proposed decision paper focuses on the ex-post calculation of the correction factor to apply in calculating the costs incurred by all parties complying with their obligations in relation to the PSO in the SEM; Target Audience: Electricity generators and suppliers, including those participating in the Renewable Energy Feed in Tariff, and electricity customers. Related Documents:

• Electricity Regulation Act 1999

• S.I. No. 217 of 2002 - Electricity Regulation Act 1999 (Public Service Obligations) Order 2002 as amended

• S.I. No. 284 of 2008 - Amending S.I. No. 217 of 2002 for the REFIT

• Arrangements for the Public Service Obligation Levy, CER 08/153 http://www.cer.ie/en/renewables-current-consultations.aspx?article=39ce537a-1620-486d-b93e-bc70ab5934ca&mode=author

• Consultation on the Arrangements for the Public Service Obligation Levy, CER 08/093 http://www.cer.ie/en/renewables-current-consultations.aspx?article=39ce537a-1620-486d-b93e-bc70ab5934ca

• PSO Benchmark Price Setting Methodology AIP-SEM-07-431 PSO

Decision Paper : Published July 31st 2007 • Proposed Approach to Setting the PSO benchmark Price in SEM AIP-

SEM-07-240 PSO Consultation Paper: Published June 1st 2007

Ex-post correction factor in PSO Levy – CER/08/170 17 September 2008

3

• PSO Levy 2008/2009 Decision CER 08/129

http://www.cer.ie/en/renewables-current-consultations.aspx?article=d96d9b61-b24f-414e-b93e-abe0f4ce561e&mode=author

• Previous PSO Decision papers

http://www.cer.ie/en/renewables-decision-documents.aspx#PSODecisions

• PSO Invoicing and Collection Procedures, CER 03/013, 27th January 2003

• REFIT Terms and Conditions/Clarifications For further information on this proposed decision paper, please contact Jamie Burke ([email protected]) Analyst - Environment, at the Commission.

Ex-post correction factor in PSO Levy – CER/08/170 17 September 2008

4

Executive Summary Section 39 of the Electricity Regulation Act 1999 sets out the legal basis for the Public Service Obligation (the PSO) levy in Ireland. Statutory Instrument No. 217 of 2002 made under Section 39 requires that the Commission review the costs associated with the PSO and set the associated levy for the required period. In June of 2007 the Commission and NIAUR consulted on and determined the methodology for setting the PSO ex-ante benchmark price in the SEM. This proposed decision paper examines the methodology for the calculation of the ex-post correction factor - the ‘R-factor’ – for all relevant parties in the context of that decision. The approach is set out in Section 2 of this paper for both the Renewable Energy Feed in Tariff (REFIT) and other mechanisms supported by the PSO. At a high level it is being proposed that the ex-post correction factor be calculated based on the difference between total revenues and total costs, in accordance with the REFIT Terms and Conditions. For energy traded bilaterally outside the pool, revenues will be calculated based on cost to suppliers, again, in accordance with the REFIT Terms and Conditions and what it would have cost suppliers to purchase the equivalent volume of energy from the pool.

Ex-post correction factor in PSO Levy – CER/08/170 17 September 2008

5

Table of Contents Executive Summary .............................................................................................. 4 1.0 Introduction ..................................................................................................... 6

1.1 The Commission for Energy Regulation ...................................................... 6 1.2 Purpose of this paper ................................................................................... 6 1.3 Comments Received ................................................................................... 6 1.4 Background Information ............................................................................... 7 1.5 Structure of this paper ................................................................................. 8 1.6 Other Relevant Information .......................................................................... 8

2.0 The Ex-Post Calculation of the PSO Correction Factor in the SEM ................ 9 2.1 Introduction .................................................................................................. 9 2.2 Overview of Responses to the Ex-Post Calculation of the PSO Correction Factor in the SEM ............................................................................................ 10

2.2.1 Commissions Proposed Decision and Reasoning ............................... 11 2.3 Summary ................................................................................................... 19

3.0 Conclusions and Next Steps ..................................................................... 21 3.1 Summary ............................................................................................... 21 3.2 Next Steps ................................................................................................. 21

3.2.1 Summary of Next Steps ....................................................................... 21 3.2.2 Timetable of Implementation ............................................................... 21

Appendix A – Glossary of Terms ........................................................................ 22 Appendix B – REFIT Calculations ................................................................... 24 Appendix C – R-Factor Calculations ............................................................... 26

Ex-post correction factor in PSO Levy – CER/08/170 17 September 2008

6

1.0 Introduction

1.1 The Commission for Energy Regulation The Commission for Energy Regulation (‘the Commission’) is the independent body responsible for overseeing the regulation of Ireland's electricity and gas sector’s. The Commission was initially established and granted regulatory powers over the electricity market under the Electricity Regulation Act, 1999. The enactment of the Gas (Interim) (Regulation) Act, 2002 expanded the Commission’s jurisdiction to include regulation of the natural gas market, while the Energy (Miscellaneous Provisions) Act 2006 granted the Commission additional powers in relation to gas and electricity safety. The Electricity Regulation Amendment (SEM) Act 2007 outlined the Commission’s functions in relation to the Single Electricity Market (SEM) for the island of Ireland. This market is regulated by the Commission and the Northern Ireland Authority for Utility Regulation (NIAUR). The Commission is working to ensure that consumers benefit from regulation and the introduction of competition in the energy sector.

1.2 Purpose of this paper The purpose of this paper is to outline and describe the Commission’s proposed decision with regard to:

• the methodology to be applied to the ex-post calculation of correction factors to apply in calculating the costs incurred by all parties in complying with their obligations in relation to the PSO;

The Commission has carried out a public consultation on this topic, with a proposed decision regarding the Arrangements for the Public Service Obligation Levy (CER 08/093) being published on the Commission’s website on the 16th of June 2008, and has considered fully the comments and submissions received. Issues raised throughout the consultation process are addressed in this proposed decision paper.

1.3 Comments Received The Commission received nine submissions to the consultation paper (CER 08/093). Submissions were received from the following organisations or individuals:

• Viridian Power and Energy Limited • Hibernian Wind Power

Ex-post correction factor in PSO Levy – CER/08/170 17 September 2008

7

• Airtricity • Eirgrid • ESBIE • Irish Wind Energy Association • SWS • Meitheal na Gaoithe • Bord Gais Energy Supply

The Commission has published each of the responses received from the parties listed above with this proposed decision paper.

1.4 Background Information Under Section 39 of the Electricity Regulation Act 19991 the Commission is responsible for the imposition of public service obligations on the Board, licence holders and holders of permits under section 37 of the Principal Act. S.I. No. 217 of 20022 was made by the Minister under Section 39 which sets out more detail in relation to the above matters. S.I. No. 217 of 2002 provides, inter alia, for the calculation of the PSO to provide for the recovery of costs by relevant parties in accordance with the notifications to the EU regarding the various mechanisms supported by the PSO. Under SI 217 of 2002, the Commission is obliged to approve ESB’s estimated additional costs to be incurred in complying with the PSO imposed on ESB. These include additional costs related to the contracting of ESB with generating stations which use as their primary energy fuel source peat and generating stations chosen as a result of a competitive process which use as their primary fuel source such renewable, sustainable or alternative forms of energy. The REFIT was introduced by the Government as a support mechanism for certain types of renewable generation with the stated purpose of achievement of Ireland’s 2010 renewables target. The REFIT replaces the Alternative Energy Requirement (AER) mechanism. The REFIT was announced on May 1st 2006 and the Terms and Conditions of the scheme published.3 The Government applied to the EU for state aid clearance in August 2006 in accordance with Article 88(3) of the Treaty and this was received in September 2007 (N571/2006 and C (2007) 4317 final respectively).4 The REFIT differs from AER in that it is open to all suppliers, not just ESB Customer Supply. The supplier agrees to purchase all of the output from the generator under contract for 15 years and 1 http://acts.oireachtas.ie/en.act.1999.0023.7.html#partvi-sec39 2 http://www.irishstatutebook.ie/2002/en/si/0217.html 3 http://www.dcmnr.gov.ie/Energy/Sustainable+and+Renewable+Energy+Division/Sustainable+and+Renewable+Energy+Division.htm 4 http://ec.europa.eu/community_law/state_aids/comp-2006/n571-06.pdf

Ex-post correction factor in PSO Levy – CER/08/170 17 September 2008

8

under the REFIT there are three elements of compensation – a 15% balancing payment intended to cover balancing costs associated with contracting with undispatchable generators, a technology difference payment to promote diversity in renewable generation and an opportunity cost payment. The DCENR has recently made the necessary amendments to SI. No. 217 of 2002, under SI. No. 284 of 2008, to provide a statutory basis for the inclusion of the REFIT costs in the PSO levy.

1.5 Structure of this paper

• Sections 2 outlines the detail of the substantive issues which the

Commission sought views on and is now making its proposed decision on;

• Section 3 contains an overall summary of the proposed decision being made in this paper and the Commission’s conclusions in this area;

• Section 3.2 outlines the Commission’s next steps with regard to the

arrangements going forward for the PSO and the timetable regarding the proposed decision taken in this paper.

1.6 Other Relevant Information Any responses to the proposed decision as set out in this document regarding the arrangements for the Public Service Obligation Levy should be directed to the following, preferably in electronic format: Jamie Burke Analyst - Environment Commission for Energy Regulation The Exchange Tallaght Dublin 24 E-Mail: [email protected] Tel: 00 353 1 4000800 Fax: 00 353 1 4000850 Responses to this paper must be received by the close of business (17:00 hours), Tuesday 14 October 2008.

Ex-post correction factor in PSO Levy – CER/08/170 17 September 2008

9

2.0 The Ex-Post Calculation of the PSO Correction Factor in the SEM

2.1 Introduction The calculation of the PSO levy requires an ex-ante estimate of the monies to be recovered in a given levy period followed by the calculation of the monies that should have in fact been recovered by relevant parties two PSO periods ago. For example, the Commission has recently published its decision on the PSO monies5 to be recovered in the next PSO levy period (1 October 2008 – 30 September 2009). Following this period, parties will be required to submit auditors’ reports regarding the actual monies that should have been recovered by them under the PSO for 1 October 2008 – 30 September 2009. These differences will then be included in the PSO levy period 1 October 2010 -30 September 2011 in the ‘R factor’ and interest applied in accordance with the Notification of 2000.6 Prior to the introduction of the SEM the R-factor was necessary to account for differences between factors such as estimated versus actual plant output, customer demand etc. The Best New Entrant (BNE) was a theoretical price which did not change from the figure set ex-ante. This BNE price was used as a benchmark price pre-SEM with respect to the cost of a best new entrant generator in the Irish market. The advent of the SEM resulted in actual ex-post prices being available; therefore differences in ex-ante and ex-post values can now be taken account of. The RA’s decision paper (AIP/SEM/07/240) regarding the methodology for the setting of the ex-ante PSO benchmark price in the SEM did not explicitly address the methodology for the calculation of the ex-post correction factors. Therefore, the Commission is now putting forward a proposed decision on its preferred approach to this matter in relation to all PSO supported mechanisms, including the REFIT scheme. As stated in the Commission’s consultation paper CER 08/093, the Commission considers that the proposed approach is in line with the methodology employed in Northern Ireland regarding the calculation of the ex-post PSO correction factor.

5 CER 08/129, Public Service Obligation (PSO) Levy 2008/2009 Charges 6 Ref: Paragraphs 5.35 and 5.36 of the 2000 Notification of Public Service Obligations

Ex-post correction factor in PSO Levy – CER/08/170 17 September 2008

10

2.2 Overview of Responses to the Ex-Post Calculation of the PSO Correction Factor in the SEM One of the respondents to the consultation paper stated that the thinking applied by the Commission to the calculation of the ex-post factor “is consistent with the intent of the REFIT scheme. Use of actual revenues earned by individual’s projects is consistent with the principle of providing a fixed price floor to developers”. This respondent argued that the effect of schemes such as Capacity Payments, Ancillary Services, TLAF’s and TUoS should be included or excluded in the estimate of total revenues. “Adjusting income estimates for some of these factors and not others is arbitrary”. The respondent went on to request that the principle behind the ex-post correction factor be given more clarity and that the treatment of constrained energy needs to be considered by the Commission. Finally, this respondent requested that the “ex-post correction should probably provide for the case where excess payments were made to participants based on the ex-ante estimate” and, that the proposed decision paper “should explicitly confirm that all calculations are on an individual PPA basis rather than a supplier basis”. A second respondent also requested clarity on the REFIT correction factor and the term ‘Total Allowable Costs’ in section 2.2 of the consultation paper CER 08/093. Further to this, the respondent asked that the Commission “give detail as to whether these Total Allowable Costs, are based on ex-ante forecasts or on real ex-post figures” and that in the case of energy sold outside of the SEM that the Commission “provide more detail as to what happens in the situation that the actual revenue recovered is greater than that which would have been recovered if it had been sold through the pool”. Another respondent also requested that the terms ‘allowable costs’ be given further clarity by the Commission in its proposed decision. This respondent noted that it had three main concerns with the Commission’s proposal in the consultation paper. (i) “The R-Factor should be explicitly defined as a reconciliation payment arrangement, versus advance payments; the collector(s) must always be able to claw back over-payment”. (ii) a “possible over-payment to suppliers” and (iii) “non-payment of amounts defined in REFIT Terms and Conditions”. This respondent called for clarification on how constraint of generator output would be treated with regard to the REFIT payments and noted that these payments should be on the basis of metered generation as opposed to traded generation. The respondent also argued that “to minimise the difference between ex-ante payments and ex-post corrections, the ex-ante benchmark components should be as close a match as possible to those used in calculation of outturn”.

Ex-post correction factor in PSO Levy – CER/08/170 17 September 2008

11

A fourth respondent stated that it has was happy with the proposal in the consultation paper and “the idea of estimating revenue up front, drawing down during the PSO period and then reconciling against actual after the event is in line with the spirit of how REFIT should work”. This respondent requested that the definitions of A, B and C, as per Section 2.2 of CER 08/093, are extended to show the ex-ante calculation, the ex-post calculation and the ensuing reconciliation. The respondent went on to note that TLAF’s and TUoS “should be treated in the same way as capacity payments and ancillary service payments, and included in the calculation of Total Net Market Revenue”. All of these questions raised by the respondents above will be addressed in the next section of the paper, Section 2.2.1.

2.2.1 Commissions Proposed Decision and Reasoning It should be noted by all parties that in reaching this proposed decision the Commission has adhered to the principles and policies outlined in the relevant PSO and REFIT governing legislation, including SI 217 of 2002 as amended, SI 284 of 2008, the PSO Notifications to the EU, the relevant State Aid decisions and the REFIT Terms and Conditions, as published by the Department of Communications, Energy and Natural Resources (DCENR). (1) Non-REFIT: In Section 2.2 of the consultation paper CER 08/093, the Commission consulted on the treatment of costs and revenues associated with contracts and plants supported under the PSO, other than under the REFIT scheme. The Commission received no responses to this matter and is therefore proposing to proceed with the approach taken in CER 08/093. Revenues and costs associated with non-REFIT parties used in the calculation of the ex-post correction factor will be based on the individual contracts. (2) REFIT: As stated earlier in the paper under the REFIT scheme there are three forms of compensation streams accruing to suppliers, the 15% balancing payment, the technology difference payment for generators others than Large Wind, as defined in the Terms and Conditions of the REFIT, and the third is the opportunity cost payment. All suppliers contracting with a REFIT supported project are entitled to these three forms of compensation. Part (D) of Section 2.2.1 deals with the ex-post calculation of the first two compensation streams, i.e. the 15% balancing payment and the technology payment, while part (E) deals with the ex-post calculation of the opportunity cost. At the request of a number of respondents to the PSO Arrangements consultation paper CER 08/093, the Commission has decided to clarify a number of key issues that arose post publication of CER 08/093 in relation to the ex-post calculations of in-market REFIT supported contracts.

Ex-post correction factor in PSO Levy – CER/08/170 17 September 2008

12

(2A) REFIT PSO calculations on REFIT Power Purchase Agreement (PPA) Basis

Calculations of the monies recoverable under the PSO in relation to PPA’s supported by the REFIT will be made on an individual REFIT PPA basis as set out in the Schedule 3 of SI. 284 of 2008. These calculations on an individual PPA basis will be made for both the ex-ante setting of the PSO levy and the ex-post R-Factor calculation. The Commission notes that both SI. 284 and the REFIT Terms and Conditions clearly envisage that the REFIT calculations are made on a per REFIT PPA basis between an individual generator and supplier, and not on an individual supplier basis.

Article 6D of SI. 284 2008 states that (emphasis added): “(1) There shall be imposed by the Commission on each supplier specified in column (3) of Schedule 3 a requirement that pursuant to the REFIT power purchase agreement specified at that reference number, such supplier have available to it and purchase the electricity generated by the generation plant specified at that reference number in column (5), by the generator specified at that reference number in column (4), which electricity shall be generated from the energy source specified at that reference number in column (6) and which electricity is the subject of the REFIT power purchase agreement concerned”. Paragraph 3.1 of the REFIT Terms and Conditions states that “any licensed electricity supplier...in return for entering into a PPA to purchase the output from the proposed renewable energy powered plant, for 15 years, the supplier will, when these terms and conditions provide for it, be entitled to receive a REFIT payment, calculated in accordance with these terms and conditions”. It is the onus of the supplier to firstly set out on an individual PPA basis the ex-ante REFIT estimates of the relevant generators it has entered into PPA’s with, and who are listed in Schedule 3 of SI. 284, for submission to the Commission. In addition, the supplier will aggregate those estimates. The supplier is also required to calculate the relevant PSO monies ex-post, on a REFIT PPA basis and submit an aggregate figure.

(2B) Calculation of Interest accruing to over and under recoveries The interest rate to apply to both under and over recoveries of REFIT monies under the PSO will be that as set out in the PSO Notification of 2000. Section 5.36 of that document states that the applicable rate is “the actual annual interest rate at Euribor compounded over an average period outstanding of 2 years”. As noted earlier in the paper, the PSO Levy period has changed from being an annual period of 1 January to 31 December to covering the period 1 October to 30 September of the following year. As a result of this change and in keeping with the spirit of the original Notification, the Commission deems it appropriate to

Ex-post correction factor in PSO Levy – CER/08/170 17 September 2008

13

use the 12 month Euribor average interest rate, ranging from 1 October to 30 September of the following year, as the interest rate to be employed in calculating interest accruing to over and under recoveries of PSO monies. Therefore, the interest rate to apply for a possible over or under recovery of 2008/2009 REFIT monies in the 2010/2011 PSO period will be the 12 month Euribor average interest rate, ranging from 1 October 2008 to 30 September 2009 and the 12 month Euribor average interest rate, ranging from 1 October 2009 to 30 September 2010, compounded.

(2C) 15% Balancing Payment and Technology Difference Payment compensations streams

(i) Metered Generation: The basis for these two forms of compensation streams for REFIT contracts supported by the PSO accruing to suppliers will be calculated on metered generation (MG) of the REFIT supported generating plant. Market Scheduled Quantities (MSQ’s) will not be used in the calculation of these two forms of compensation.

The Commission is of the view that contracts between suppliers and generators that provide for purchase of output at the gate or at the trading point of the generator are both covered under the Terms and Conditions of the REFIT. Therefore, the Commission considers it appropriate to allow for the 15% Balancing Payments and the Technology Difference Payment accruing to suppliers to be calculated on metered generation either at the gate of the generation plant or at the Trading Point, in accordance with what is provided for in the individual contracts agreed between suppliers and generators under the REFIT.

It is important to clarify the definitions of metered generation at the gate and metered generation at the trading point with regard to the REFIT supported generators;

• Output at Gate: Metered Generation (MG) - Active Power7 produced at the Export Point (being the nominal commercial point of entry to the Transmission System of the Active Power generated at a Transmission Connected or Distribution Connected Site).

• At Trading Point: Loss Adjusted Metered Generation (MGLF) – Metered

Generation adjusted to reflect transmission losses and (where applicable) distribution losses (DLAF’s and TLAF’s) at the Trading Boundary8.

These actual metered generation figures will be calculated in the ex-post correction factor of the relevant period as outlined in Section 2.1 of this paper, i.e. 7 Refer to Trading and Settlement Code for definition 8 Ibid

Ex-post correction factor in PSO Levy – CER/08/170 17 September 2008

14

PSO period + 2 PSO periods. Further explanation of the use of actual metered generation (MG or MGLF as applicable), as opposed to MSQ’s, is provided in part (2D) of Section 2.2.1.

(ii) Independent compensation streams: It is also important to clarify that the 15% balancing payment and the technology difference payment are ring-fenced from each other and also from the other compensation stream, the opportunity cost payment, accruing to suppliers under the REFIT. The Commission is of the opinion that if one form of compensation was allowed to ‘net-off’ another form of compensation, i.e. for example if the 15% Balancing Payment were to be treated as a revenue in the calculation of the ex-post opportunity cost, it would be inconsistent with the design of the REFIT mechanism as laid out in the REFIT legislation and Terms and Conditions. To repeat, the 15% balancing payment and the technology difference payment accruing to suppliers under the REFIT are wholly independent of each other and the third compensation stream, the opportunity cost payment. (iii) R-Factor for 15% Balancing Payment and Technology Difference Payment: Although the 15% balancing payment and technology difference payment are independent of each other and the opportunity cost payment, these two forms of compensation will be the subject of an ex-post calculation and reconciliation process. Suppliers will be paid both the 15% balancing payment and technology difference payment (where the technology payment arises) based on their ex-ante estimates of generator output (MG or MGLF as discussed above). An ex-post reconciliation will take place on these two forms of compensation in the relevant PSO period, i.e. PSO period + 2 PSO periods. 9 For example, a supplier could provide the Commission with ex-ante technology difference payment associated with a REFIT supported generator. This positive ex-ante technology difference payment is included in the PSO levy for that particular PSO period. However, the Commission then carries out an ex-post reconciliation two PSO period’s later and finds, as per an audited supplier submission, that the supplier over-estimated the technology difference payment for that particular generator. This over-payment is taken into account in the calculation of the R-Factor and can result in a negative R-Factor, where PSO monies need to be paid back to the PSO levy by that supplier. In other cases, the R-Factor may be a positive figure or zero. Essentially, these two forms of payments will be reconciled for changes in quantities of energy output (MG or MGLF) by the REFIT supported generators, between ex-ante estimates of energy output (MG or MGLF) provided by suppliers and actual energy output figures calculated. A table outlining the 9 The ex-post calculation of the third compensation stream accruing to suppliers, the opportunity cost payment, is dealt with in point (2D) of this section.

Ex-post correction factor in PSO Levy – CER/08/170 17 September 2008

15

calculation of the net R-Factor for the 15% balancing payment and technology difference payment is provided in Appendix B of this paper.

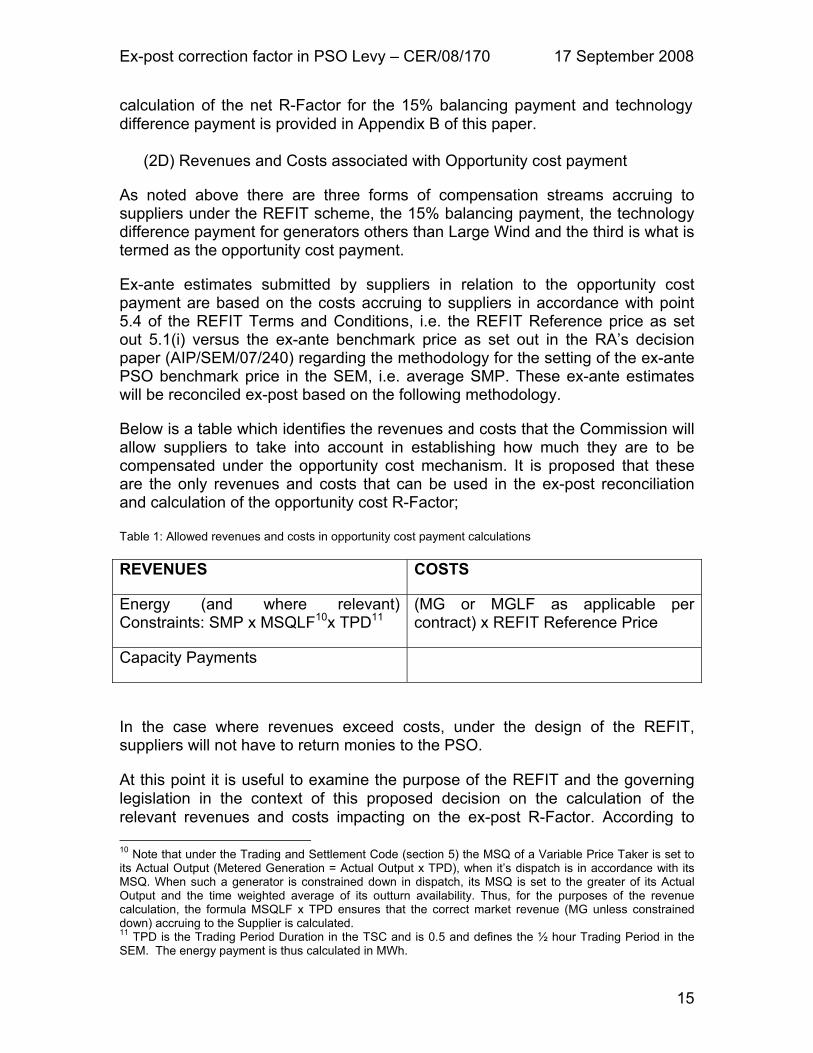

(2D) Revenues and Costs associated with Opportunity cost payment

As noted above there are three forms of compensation streams accruing to suppliers under the REFIT scheme, the 15% balancing payment, the technology difference payment for generators others than Large Wind and the third is what is termed as the opportunity cost payment.

Ex-ante estimates submitted by suppliers in relation to the opportunity cost payment are based on the costs accruing to suppliers in accordance with point 5.4 of the REFIT Terms and Conditions, i.e. the REFIT Reference price as set out 5.1(i) versus the ex-ante benchmark price as set out in the RA’s decision paper (AIP/SEM/07/240) regarding the methodology for the setting of the ex-ante PSO benchmark price in the SEM, i.e. average SMP. These ex-ante estimates will be reconciled ex-post based on the following methodology.

Below is a table which identifies the revenues and costs that the Commission will allow suppliers to take into account in establishing how much they are to be compensated under the opportunity cost mechanism. It is proposed that these are the only revenues and costs that can be used in the ex-post reconciliation and calculation of the opportunity cost R-Factor;

Table 1: Allowed revenues and costs in opportunity cost payment calculations

REVENUES COSTS

Energy (and where relevant) Constraints: SMP x MSQLF10x TPD11

(MG or MGLF as applicable per contract) x REFIT Reference Price

Capacity Payments

In the case where revenues exceed costs, under the design of the REFIT, suppliers will not have to return monies to the PSO.

At this point it is useful to examine the purpose of the REFIT and the governing legislation in the context of this proposed decision on the calculation of the relevant revenues and costs impacting on the ex-post R-Factor. According to 10 Note that under the Trading and Settlement Code (section 5) the MSQ of a Variable Price Taker is set to its Actual Output (Metered Generation = Actual Output x TPD), when it’s dispatch is in accordance with its MSQ. When such a generator is constrained down in dispatch, its MSQ is set to the greater of its Actual Output and the time weighted average of its outturn availability. Thus, for the purposes of the revenue calculation, the formula MSQLF x TPD ensures that the correct market revenue (MG unless constrained down) accruing to the Supplier is calculated. 11 TPD is the Trading Period Duration in the TSC and is 0.5 and defines the ½ hour Trading Period in the SEM. The energy payment is thus calculated in MWh.

Ex-post correction factor in PSO Levy – CER/08/170 17 September 2008

16

State Aid N/571/2006, the REFIT is aimed at protecting the environment and saving fossil fuel energy by increasing the contribution of renewable and sustainable energy to total electricity consumption in Ireland. To this end, the programme is allocated up to a quantitative capacity limit of 1450MW’s. The REFIT Terms and Conditions document states that the Minister has initiated a competition to “allocate support for the construction of 400MW’s in the period to 2010 of new electricity generation plant powered by biomass, hydropower or wind energy under the Renewable Energy Feed in Tariff programme (REFIT)”. In addition that document contains the following statements which are of relevance to the Commission’s proposed decision (emphasis added):

“eligible domestic electricity’ means electricity produced from renewable energy by new electricity generating plant in the State …..”

“Power Purchase Agreement’…..means….a contractual agreement between an electricity generator and a licensed supplier obliging the latter to purchase the output from a new renewable energy powered electricity generation plant ….”

It is also noted that the REFIT Terms and Conditions document refers to ‘KWh’ in relation to the reference prices, the calculation of the 15% balancing payment, the technology difference and the opportunity cost payments.12 Given the above, it seems that the basis for all three compensation streams, including the opportunity cost payment under the REFIT should be actual metered generation, as opposed to Market Scheduled Quantities (MSQ’s), and that this is consistent with the objective of meeting the 2010 target as laid out in the 2006 State Aid decision.

It was noted earlier in the paper that there is no pro forma contract for the REFIT and that different contracts between suppliers and generators may cover different costs and revenues or be related to either Market Scheduled Quantities (MSQ’s) or tradable quantities. The definition of a PPA is set out in the Terms and Conditions of the REFIT, as detailed above. Also, ‘KWh’s purchased’ are referred to throughout Paragraph’s 5.1 to 5.6 of the Terms and Conditions of the REFIT, which addresses the three compensation streams, including the opportunity cost payment.

In the absence of a pro forma contract, suppliers and generators are free to negotiate the precise terms and conditions of their PPA. Therefore, the contract between a supplier and a generator could:

• be based on MSQs rather than generated output. This would result in payment by the supplier to the generator for MSQs under the contract. These MSQs could differ from metered generation;

12 Paragraph 5.3 of the REFIT Terms and Conditions document refers.

Ex-post correction factor in PSO Levy – CER/08/170 17 September 2008

17

• provide that the supplier captures capacity payments, ancillary services payments and constraint payments. However, the contract may also provide that these payments go to the generator;

• provide for purchase, which may be either MSQ or metered output, at the trading point or at the gate of the generator, and

• contain conditions regarding Use of System charges.

As stated previously in this paper, the Commission in coming to this proposed decision has adhered to the principles and policies outlined in the relevant PSO and REFIT governing legislation, the PSO Notifications to the EU, the relevant State Aid decisions and the REFIT Terms and Conditions, as published by the DCENR. The purpose of the REFIT and the possible varying contractual arrangements between suppliers and generators has also been taken into consideration by the Commission.

In the interests of all parties involved in the REFIT and the PSO, including the final customer, it is necessary to examine those revenues and costs included and excluded from the calculation on an individual basis. (2E) (i) Revenues: It is important to note that revenue calculations will ordinarily be based on metered generation but in the case where the REFIT supported project, subject to a PPA, is constrained in the market then revenues will be based on Market Schedule Quantities (MSQs) as laid in table 1 above. The treatment of constraint payments is discussed further below.

All suppliers contracting with a REFIT supported project in the market will receive, as a source of revenue from the market, the System Marginal Price (SMP) multiplied by the metered generation that it has supplied to the market. Therefore, energy payments accruing to suppliers selling energy to the pool must be included as a source of revenue for the supplier in the table 1. For the purposes of the calculation of the ex-post opportunity cost payment, the Commission considers that it is appropriate to consider that the PPA price, agreed between a generator and a supplier, is effectively an ‘all-in’ price. It is deemed that this price covers the cost of the generator supplying energy to the supplier in the context of the REFIT, which includes energy and capacity. In the current market arrangements the supplier receives two payments, one for energy and one for capacity. However, under the PPA the supplier is only making one payment out to the generator, that which is agreed under the one PPA. Were the Commission not to include capacity payments to suppliers in the ex-post calculations as a revenue this would potentially increase the PSO levy for final customers.

Ex-post correction factor in PSO Levy – CER/08/170 17 September 2008

18

The Commission is aware that certain REFIT supported generators may in some instances be constrained down. In this situation whilst the market may compensate the generator for constrained generation, the supplier, under the REFIT Terms and Conditions is only deemed to face the cost as calculated based on the reference price in the REFIT Terms and Conditions. It is being proposed that such constraint payments be treated as a revenue accruing to suppliers, were the market will pay for such constraints. The calculation of these constraint payments is laid in table 1 above. Under the current market arrangements suppliers do not receive ancillary services payments and therefore these payments should not be included as a category of revenue accruing to the supplier. With regard to these arrangements, the generator contracts directly with the System Operator for the provision of ancillary services and therefore it is inappropriate to include them as a revenue accruing to suppliers.

(2E) (ii) Costs:

The Commission considers that the costs that should be taken into account in the calculation of the ex-post opportunity compensation stream are those set out in 5.4 of the REFIT Terms and Condition, i.e. the REFIT Reference price in 5.1(i), multiplied by the metered generation as defined in Section 2.2.1 of this paper. As discussed above, the Commission is of the view that contracts between suppliers and generators that provide for purchase of output at the gate or at the trading point of the generator are both covered under the Terms and Conditions of the REFIT (definitions in (2C) of Section 2.2.1).

The Commission has confirmed with the DCENR that use of system charges, such as TUoS and DUoS are included as inputs into the REFIT reference price and therefore the Commission is of the view that use of system charges should not be treated as separate costs borne by suppliers in contracting with REFIT supported generators. Consequently, TUoS and DUoS charges will not be treated as separate costs under the ex-post opportunity cost payment calculation.

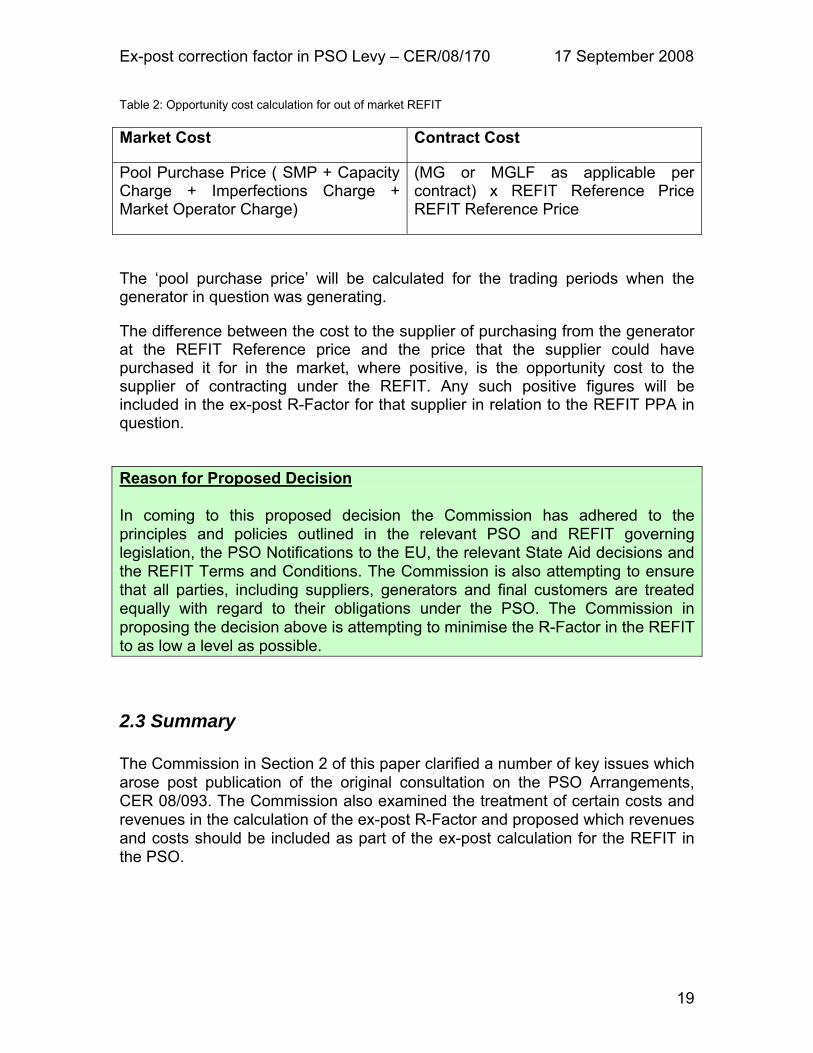

(3) Out of Market REFIT: At a high level, the purpose of the opportunity cost payment is to compensate suppliers for the additional cost of contracting with REFIT supported generators, relative to the PPA price paid. For out-of-market REFIT generators, the Commission considers that it is appropriate to determine any monies owing to suppliers buying directly from generators who they have entered into PPA’s with, by calculating the difference between the cost to suppliers at the REFIT Reference price and what it would have cost them to buy the equivalent volumes from the market. Table 2 sets out the calculation of the above.

Ex-post correction factor in PSO Levy – CER/08/170 17 September 2008

19

Table 2: Opportunity cost calculation for out of market REFIT

Market Cost Contract Cost

Pool Purchase Price ( SMP + Capacity Charge + Imperfections Charge + Market Operator Charge)

(MG or MGLF as applicable per contract) x REFIT Reference Price REFIT Reference Price

The ‘pool purchase price’ will be calculated for the trading periods when the generator in question was generating.

The difference between the cost to the supplier of purchasing from the generator at the REFIT Reference price and the price that the supplier could have purchased it for in the market, where positive, is the opportunity cost to the supplier of contracting under the REFIT. Any such positive figures will be included in the ex-post R-Factor for that supplier in relation to the REFIT PPA in question.

Reason for Proposed Decision In coming to this proposed decision the Commission has adhered to the principles and policies outlined in the relevant PSO and REFIT governing legislation, the PSO Notifications to the EU, the relevant State Aid decisions and the REFIT Terms and Conditions. The Commission is also attempting to ensure that all parties, including suppliers, generators and final customers are treated equally with regard to their obligations under the PSO. The Commission in proposing the decision above is attempting to minimise the R-Factor in the REFIT to as low a level as possible.

2.3 Summary The Commission in Section 2 of this paper clarified a number of key issues which arose post publication of the original consultation on the PSO Arrangements, CER 08/093. The Commission also examined the treatment of certain costs and revenues in the calculation of the ex-post R-Factor and proposed which revenues and costs should be included as part of the ex-post calculation for the REFIT in the PSO.

Ex-post correction factor in PSO Levy – CER/08/170 17 September 2008

20

Summary of Proposed Decisions taken in this paper:

- Revenues and costs associated with non-REFIT parties used in the calculation of the ex-post correction factor will be based on the individual contracts.

- Calculations of the monies recoverable under the PSO in relation to PPA’s supported by the REFIT will be made on an individual REFIT PPA basis.

- The 12 month Euribor average interest rate, ranging from 1 October to 30

September of the following year, will be used as interest rate in calculating interest accruing to over and under recoveries of PSO monies.

- The 15% Balancing Payment and Technology Difference Payment compensations streams will be calculated on metered generation of the generating plant, either at the gate of the generation plant or at the Trading Point.

- The 15% Balancing payment and the Technology Difference payment are ring-fenced from each other and also from the other compensation stream, the opportunity cost payment, accruing to suppliers under the REFIT.

- Although the 15% Balancing Payment and Technology Difference payment are independent of each other and the opportunity cost payment, these two forms of compensation will be the subject of an ex-post calculation and reconciliation process.

- For in market, revenues and costs accruing to supplier in the ex-post REFIT calculation of the Opportunity Cost compensation stream for in market REFIT are laid out in table 1 of Section 2.2.1 of the paper.

- For out of market REFIT PPA’s, the difference between the cost to the supplier of purchasing from the generator at the REFIT Reference price and the price that the supplier could have purchased it for, where positive, is the opportunity cost to the supplier of contracting under the REFIT.

Ex-post correction factor in PSO Levy – CER/08/170 17 September 2008

21

3.0 Conclusions and Next Steps

3.1 Summary The purpose of this paper was to outline and describe the Commission’s proposed decision with regard to the methodology to be applied to the ex-post calculation of correction factors to apply in calculating the costs, at the REFIT Reference price in accordance with the REFIT Terms and Conditions, incurred by all parties in complying with their obligations in relation to the PSO.

3.2 Next Steps

3.2.1 Summary of Next Steps

• The Commission will publish its final decision on the ex-post correction factor to apply for the REFIT upon reviewing responses to this paper.

• Publication of paper to reflect the updated PSO invoicing and collection

procedures as outlined in CER 08/153 with the necessary revisions to CER 03/013.

3.2.2 Timetable of Implementation

• Comments to this proposed decision paper due to be received by close of business Tuesday 14 October 2008, with the final decision on the matter to be published by the Commission in November.

Ex-post correction factor in PSO Levy – CER/08/170 17 September 2008

22

Appendix A – Glossary of Terms AER Alternative Energy Requirement Commission Commission for Energy Regulation CPI Consumer Price Index DCENR Department for Communications, Energy and

Natural Resources DLAF Distribution Loss Adjustment Factor DUoS Distribution Use of System Large Wind Wind based generators above installed capacity

of 5 Megawatts MG Metered Generation MGLF Metered Generation adjusted to reflect

transmission losses and (where applicable) distribution losses (DLAF’s and TLAF’s) at the Trading Boundary.

MSQ Market Scheduled Quantity NIAUR Northern Ireland Authority for Utility Regulation PPA Power Purchase Agreement PSO Public Service Obligation RAs Regulatory Authorities, being the Commission for

Energy Regulation and the Northern Ireland Authority for Utility Regulation

REFIT Renewable Energy Feed in Tariff SEM Single Electricity Market SI Statutory Instrument SMP System Marginal Price

Ex-post correction factor in PSO Levy – CER/08/170 17 September 2008

23

TPD The ½ hour Trading Period in the SEM TSO Transmission System Operator TLAF Transmission Loss Adjustment Factor TUoS Transmission Use of System

Ex-post correction factor in PSO Levy – CER/08/170 17 September 2008

24

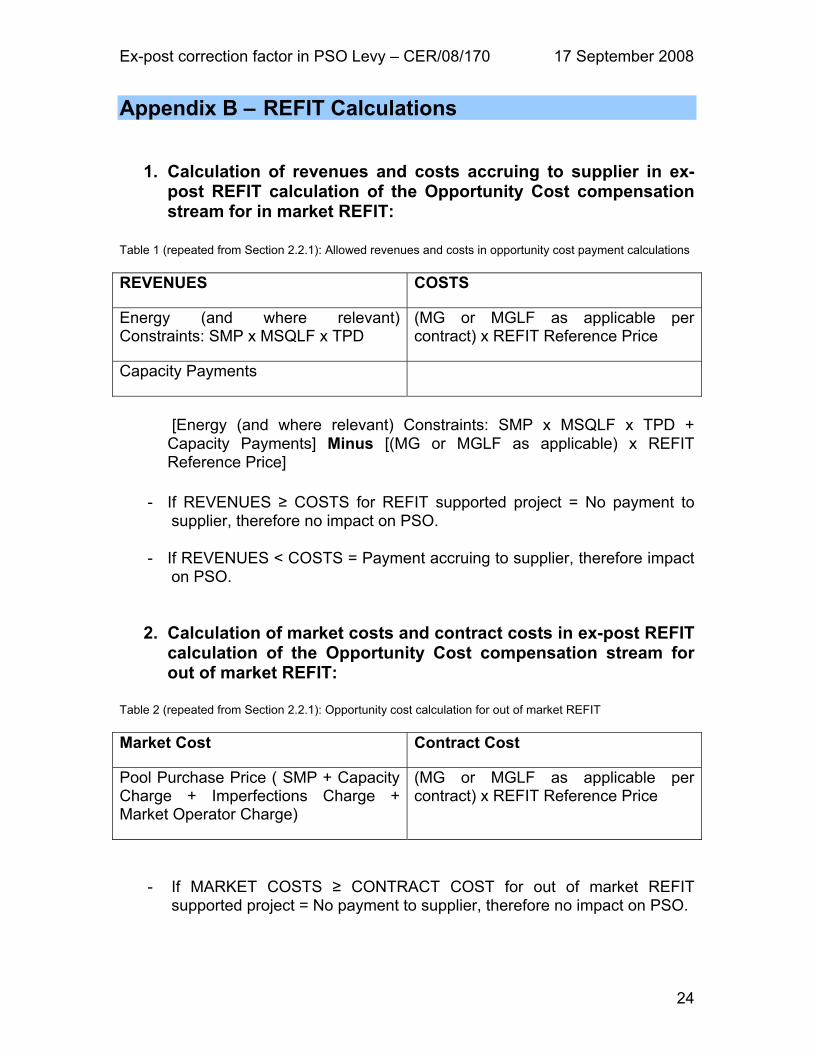

Appendix B – REFIT Calculations

1. Calculation of revenues and costs accruing to supplier in ex-post REFIT calculation of the Opportunity Cost compensation stream for in market REFIT:

Table 1 (repeated from Section 2.2.1): Allowed revenues and costs in opportunity cost payment calculations

REVENUES COSTS

Energy (and where relevant) Constraints: SMP x MSQLF x TPD

(MG or MGLF as applicable per contract) x REFIT Reference Price

Capacity Payments

[Energy (and where relevant) Constraints: SMP x MSQLF x TPD + Capacity Payments] Minus [(MG or MGLF as applicable) x REFIT Reference Price]

- If REVENUES ≥ COSTS for REFIT supported project = No payment to

supplier, therefore no impact on PSO. - If REVENUES < COSTS = Payment accruing to supplier, therefore impact

on PSO.

2. Calculation of market costs and contract costs in ex-post REFIT

calculation of the Opportunity Cost compensation stream for out of market REFIT:

Table 2 (repeated from Section 2.2.1): Opportunity cost calculation for out of market REFIT

Market Cost Contract Cost

Pool Purchase Price ( SMP + Capacity Charge + Imperfections Charge + Market Operator Charge)

(MG or MGLF as applicable per contract) x REFIT Reference Price

- If MARKET COSTS ≥ CONTRACT COST for out of market REFIT supported project = No payment to supplier, therefore no impact on PSO.

Ex-post correction factor in PSO Levy – CER/08/170 17 September 2008

25

- If MARKET COSTS < CONTRACT COST = Payment accruing to supplier, therefore impact on PSO.

Ex-post correction factor in PSO Levy – CER/08/170 17 September 2008

26

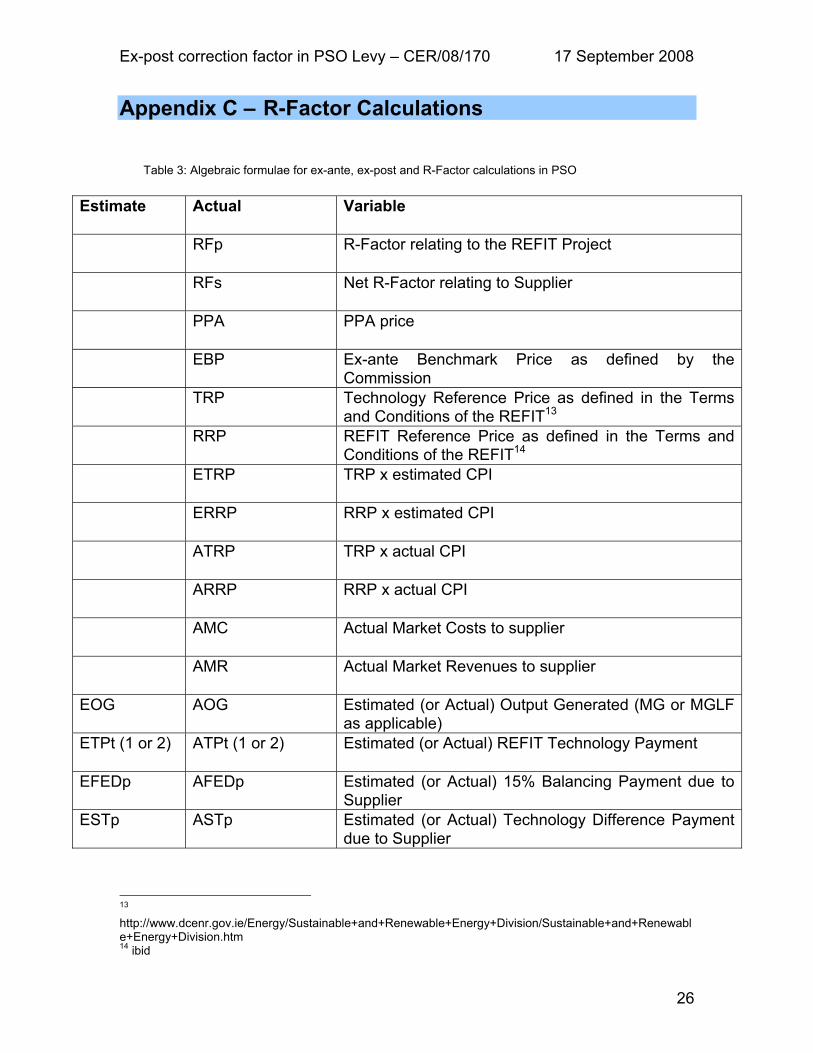

Appendix C – R-Factor Calculations

Table 3: Algebraic formulae for ex-ante, ex-post and R-Factor calculations in PSO

Estimate Actual Variable

RFp R-Factor relating to the REFIT Project

RFs Net R-Factor relating to Supplier

PPA PPA price

EBP Ex-ante Benchmark Price as defined by the Commission

TRP Technology Reference Price as defined in the Terms and Conditions of the REFIT13

RRP REFIT Reference Price as defined in the Terms and Conditions of the REFIT14

ETRP TRP x estimated CPI

ERRP RRP x estimated CPI

ATRP TRP x actual CPI

ARRP RRP x actual CPI

AMC Actual Market Costs to supplier

AMR Actual Market Revenues to supplier

EOG AOG Estimated (or Actual) Output Generated (MG or MGLF as applicable)

ETPt (1 or 2) ATPt (1 or 2) Estimated (or Actual) REFIT Technology Payment

EFEDp AFEDp Estimated (or Actual) 15% Balancing Payment due to Supplier

ESTp ASTp Estimated (or Actual) Technology Difference Payment due to Supplier

13 http://www.dcenr.gov.ie/Energy/Sustainable+and+Renewable+Energy+Division/Sustainable+and+Renewable+Energy+Division.htm 14 ibid

Ex-post correction factor in PSO Levy – CER/08/170 17 September 2008

27

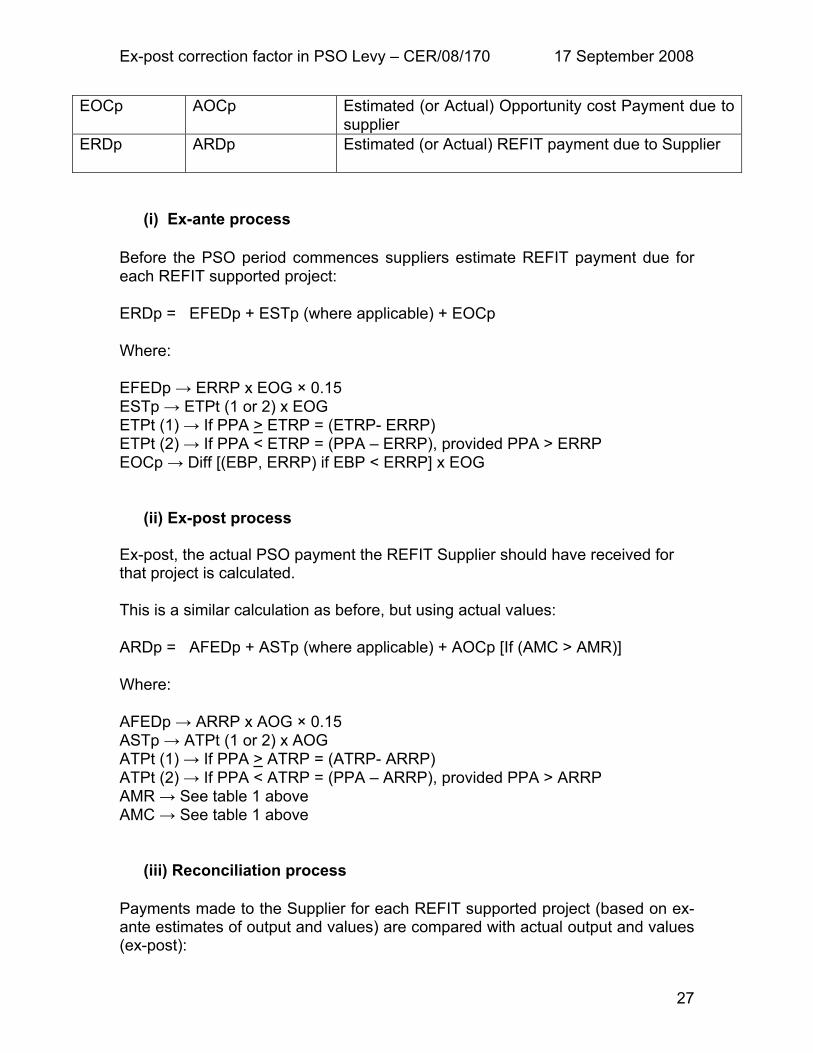

EOCp AOCp Estimated (or Actual) Opportunity cost Payment due to supplier

ERDp ARDp Estimated (or Actual) REFIT payment due to Supplier

(i) Ex-ante process

Before the PSO period commences suppliers estimate REFIT payment due for each REFIT supported project: ERDp = EFEDp + ESTp (where applicable) + EOCp Where: EFEDp → ERRP x EOG × 0.15 ESTp → ETPt (1 or 2) x EOG ETPt (1) → If PPA > ETRP = (ETRP- ERRP) ETPt (2) → If PPA < ETRP = (PPA – ERRP), provided PPA > ERRP EOCp → Diff [(EBP, ERRP) if EBP < ERRP] x EOG

(ii) Ex-post process

Ex-post, the actual PSO payment the REFIT Supplier should have received for that project is calculated. This is a similar calculation as before, but using actual values: ARDp = AFEDp + ASTp (where applicable) + AOCp [If (AMC > AMR)] Where: AFEDp → ARRP x AOG × 0.15 ASTp → ATPt (1 or 2) x AOG ATPt (1) → If PPA > ATRP = (ATRP- ARRP) ATPt (2) → If PPA < ATRP = (PPA – ARRP), provided PPA > ARRP AMR → See table 1 above AMC → See table 1 above

(iii) Reconciliation process

Payments made to the Supplier for each REFIT supported project (based on ex-ante estimates of output and values) are compared with actual output and values (ex-post):

Ex-post correction factor in PSO Levy – CER/08/170 17 September 2008

28

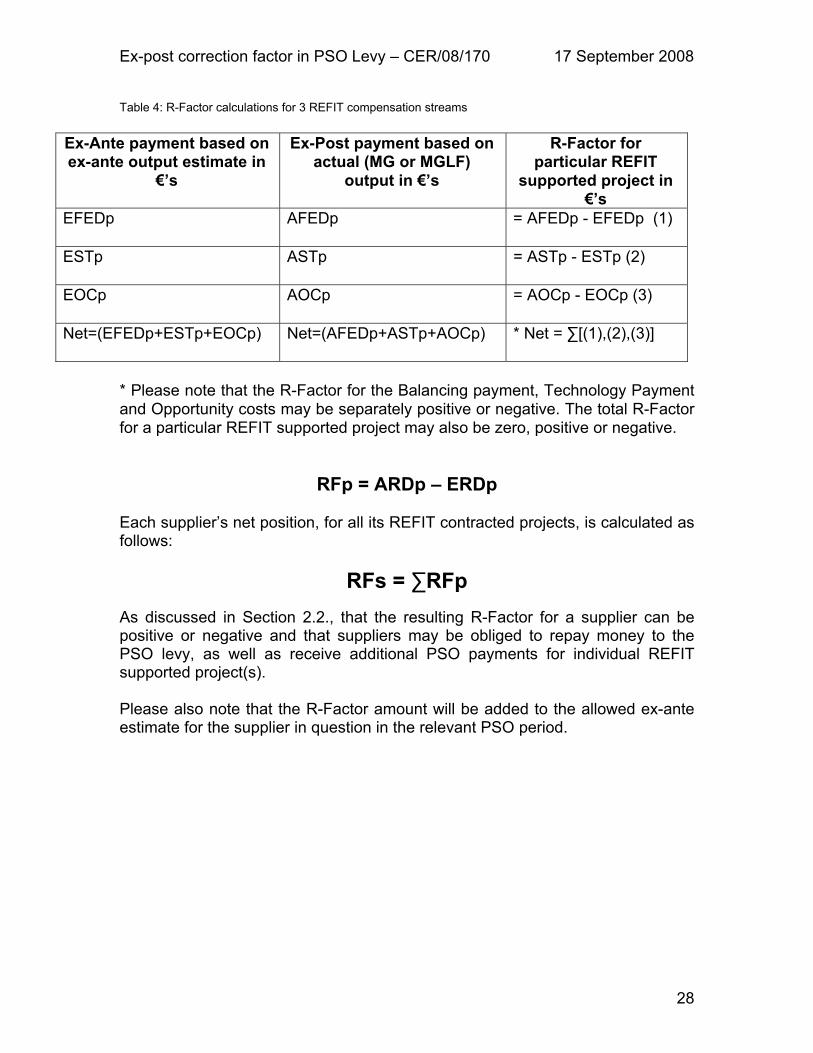

Table 4: R-Factor calculations for 3 REFIT compensation streams

Ex-Ante payment based on ex-ante output estimate in

€’s

Ex-Post payment based on actual (MG or MGLF)

output in €’s

R-Factor for particular REFIT

supported project in €’s

EFEDp AFEDp = AFEDp - EFEDp (1)

ESTp ASTp = ASTp - ESTp (2)

EOCp AOCp = AOCp - EOCp (3)

Net=(EFEDp+ESTp+EOCp) Net=(AFEDp+ASTp+AOCp) * Net = ∑[(1),(2),(3)]

* Please note that the R-Factor for the Balancing payment, Technology Payment and Opportunity costs may be separately positive or negative. The total R-Factor for a particular REFIT supported project may also be zero, positive or negative.

RFp = ARDp – ERDp Each supplier’s net position, for all its REFIT contracted projects, is calculated as follows:

RFs = ∑RFp As discussed in Section 2.2., that the resulting R-Factor for a supplier can be positive or negative and that suppliers may be obliged to repay money to the PSO levy, as well as receive additional PSO payments for individual REFIT supported project(s). Please also note that the R-Factor amount will be added to the allowed ex-ante estimate for the supplier in question in the relevant PSO period.