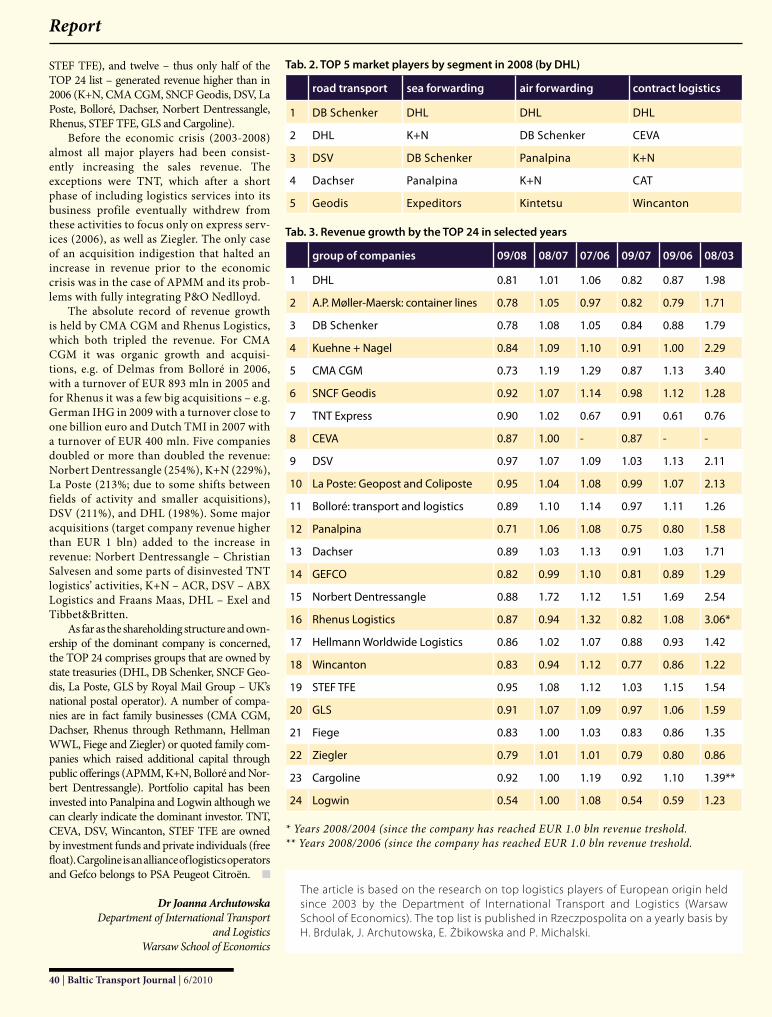

european logistics bsr's rail freight transport

TRANSCRIPT

Baltic TransportJournal IS

SN 1

733-

6732

€ 15/50 PLN (VAT 0%)

b i m o n t h l y - d a i l y c o m p a n i o n

№ 6/2010 (38), NOVEMBER/DECEMBER

Report

European logistics

Dredging & maritime construction

Baltic Transport Journal is an official media partner of:

Focus

BSR’s rail freight transport

The East West TC project has an important task: to be a testing ground for innovations, new technology, business models and improved transport management systems which will facilitate more sustainable transport solutions than those of today.

www.ewtc2.eu

– a testing ground for Innovations

The East West Transport Corridor

Lead partner

6/2010 | Baltic Transport Journal | �

Contents

Editorial ................................................................................................................................................ 4

EWTC Newsletter ................................................................................................... 5An innovative instrument for international cooperation

BTJ Calendar of partnership events 2010-2011 ...................................................................... 6

What’s new .......................................................................................................................................... 8

Happy ending – happy beginning .......................................................................................... 13The merger of APM Terminals & Cargo Service

The vision and the spirit .............................................................................................................. 14Stena Line’s historic shift of vessels lifts up Karlskrona-Gdynia route

Striving for stability ...................................................................................................................... 16Interview with Søren Poulsgaard Jensen, Scandlines

Economic cornerstones of the region .................................................................................... 18Investments in Bremen and Bremerhaven

Ships under a magnifier .............................................................................................................. 20New EU regulations to improve maritime safety

Implications of the PROBO Koala case on maritime shipping ...................................... 22Legal ambiguities on ship waste

Making the choice to thrive ....................................................................................................... 24Klaipėda port’s standpoint

A profitable junction .................................................................................................................... 25Investment opportunities in the Port of Gdańsk

Crossing the shoreline using HDD Technology .................................................................. 26Trenchless engineering for marine industry

BTJ Special: Dredging and maritime construction ........................................... 29An indispensable, unknown industryAiming at greater depths

Report: European logistics ................................................................................. 35Europe and the world The top players on the market Russian transport and logisticsA willingness to make changes

TransBaltic Newsletter ........................................................................................ 44Intermodal terminals of the futureEmergence and significance of dry portsNorth West Russia – an area in mobilization

Baltic Ports Organization Newsletter ............................................................... 48Finland has a new port

Focus: The BSR’s rail freight transport system ................................................. 51The place of Øresund BridgeGerman-Scandinavian railway servicesERTMS – from a concept to a mature signalling systemFirst step towards an intermodal terminals network in Poland

The future is still unwritten ........................................................................................................ 58European road freight analysis by Transport Intelligence

Size does matter ............................................................................................................................ 60Oversize transport strategy Mecklenburg-Western Pomerania

Events: Transport Week 2011 ....................................................................................................... 62

Collector’s corner ........................................................................................................................... 64

Transport miscellany .................................................................................................................... 65

Who’s who ........................................................................................................................................ 66

� | Baltic Transport Journal | 6/2010

Dear Readers,

Baltic TransportJournal

President of the Boardbogdan ołdakowski

Publishing Directorpiotr trusiewicz

Managing Editorlena lorenc

Contributing writersand update correspondents:algirdas šakalys, alison nissen,

martyna bildziukiewicz, marek błuś, jörg lattner, iven krämer, marek perzyński,

roland antonowicz, rada ebaltas, janusz kasprowicz, robert osikowicz,

rené kolman, halina brdulak, joanna archutowska, dominik buszta,

małgorzata nosorowska, violeta roso, evelina hansson malm, ernest czermański,

marcin wołek, hans e. boysen, emmanuel brutin, john manners-bell, kristina hunke

English Language Editorsalison nissen

Design and DTPmedon

Art Director&Graphic Designerdanuta sawicka

Publisherbaltic press sp. z o.o.

Address: 8 Pułaskiego Street81-368 Gdynia, Poland

[email protected]. +48 58 627 23 94, tel. +48 58 627 23 95

fax +48 58 621 69 66www.baltictransportjournal.com

Marketing & Sales (advertising, tradefairs, conferences)

piotr [email protected]

anna [email protected]

Printmedon

Address: Medon sp. j.ul. Kartuska 245, 80-125 Gdańsk, Poland

e-mail: [email protected]

Circulation: 2,500

Cover photo: Agnieszka Selig

(Port channel reconstruction in Gdynia)

Subscriptions can be orderedin Kolporter offices in Poland.

For more information call 0801-205-555 or visitwww.kolporter-spolka-akcyjna.com.pl/prenumerata.asp

Editorial

Company indexA.P. Møller-Maersk 13, 38, 39, 40; Abu Dhabi Transmission & Despatch Company 28; ABX Logistics 38, 40; ACR 38, 40; AGA 25; Ahlers International 66; Air Berlin Group 66; Air China 12; AirBaltic 12; Airbus 12; Älvsborg Ro/Ro 8; Amsterdam Container Terminals (ACT) 9; Anese 28; Apache Corporation 28; APM Terminals-Cargo Service 13; Apollo Management L.P. 38; ArcelorMittal 25; Autotransportlogistic 10; AXS Alphaliner 9; Baltic Ground Services 12; Baltic Port Service 25; Banverket 53; Bolloré Group 38, 39, 40; Bornholmstrafikken 66; Boskalis International 34; Boskalis Nordic 33; Brunnsviksholmen LNG Terminal 27; C. Ports 8; Capgemini 37, 58; Cargo Service 13; Cargoline Logistics 38, 39, 40; CAT Logistics Services 38, 39; CEVA Logistics 38, 39, 40; Chemiki 25; Chevron 28; China Petroleum & Chemical Corporation (Sinopec) 28; Christian Salvesen 38, 40; CMA CGM 38, 39, 40; Cobelfret 8; Coffee House Böhm 64; Conservice 34; Consorzio Venezia Nuova 28; Copelouzos Group 12; Copenhagen Kastrup Airport 53; Copenhagen Merchants 25; Copenhagen-Malmö Port (CMP) 51, 53; Dachser 38, 39, 40; Danske Færger 66; DB Schenker 35, 37, 38, 39, 40, 59; DB Schenker Rail Automotive 10; DB Schenker Rail Scandinavia 52; Deepwater Container Terminal Gdańsk (DCT) 25; Delmas 40; DFDS 8; DHL 36, 38, 39, 40, 59; Doraco 34; Dr Cordesmeyer 25; Dredging International 32,33; Drewry Shipping Consultants 9; DrillTec 26, 28; DSV 38, 39, 40; Duke Energy 28; Dutch Landscaping Contractors Association 30; EEW Special Pipe Constructions 61; EGL 38; Eimskip 47; Estonian Railways (Eesti Raudtee) 10; Europa Linien 66; Exel 38, 40; Expeditors 38, 39, 40; Falköping Port 45; Farstad Shipping 8; FIEGE 38, 39, 40; Finnair 12; Finnlines 14; First Container Terminal (FCT) 66; First Quantum Group 66; FlowTex 28; Fosfory 25; Frans Maas 38, 66; Fraport 12; Frost & Sullivan 41; Gaspol 25; Gazprom 28; Gdańsk Bulk Terminal 25; Gedser Ferry Port 16; GEFCO 38, 39, 40, 66; General Logistics Systems (GLS) 38, 39, 40; Geodis Logistics Poland 66; Global Terminal Network 13; Gottwald Port Technology 10; Hainan Airlines 12; Hamburg Port Authority 44; Hamburger Hafen und Logistik (HHLA) 10, 57; Hamina Kotka Ltd. 48, 49; Harwich International Port 14; Hays Logistics 38; HDI 28; Hector Rail 52; Hellmann Worldwide Logistics 39, 40; HNA Group 12; Hochtief 34; Hong Kong International Airport 30; Hook of Holland Port 14; Hutchison Port Holdings 9; Hydrobudowa 34; Hyundai Merchant Marine (HMM) 9; IHG Logistics 40; Iranian Offshore Oil Company 28; JDA Software Group 37; Josef MÖBIUS 32, 33; JV VIS-MOS 28; Kintetsu World Express 39, 40; Klaipėda LNG Terminal 27; Kodeco Energy Co. 28; Koltseva Holdings 12; Kuehne + Nagel 39, 40; La Poste 38, 39, 40; Lahti Regional Development Company 44; Lauda Air 66; LFV 12; Linde Gaz Polska 25; Linde Group 25; Lion Ferry Sweden 66; LLoyd Zigaretten 64; LMR Drilling 28; Logistika-Terminal 66; Logport 10; Logwin 38, 39, 40; London Luton Airport 12; Longbore 28; LOTOS 25; Lucas Group 28; Lufthansa 65; M&M Group 66; Maasvlakte 2,13; Macquarie Group 25; Malmö Sturup Airport 51; Malteurop Polska 25; Marine Current Turbines (MCT) 28; Martin Brinkmann 64; Mears Group 28; Mecklenburger Metallguss (MMG) 61; Mediterranean Shipping Company (MSC) 18, 24; Michels Directional Crossings 28; MIST 45; Nacap 28; Nakskov Skibsværft 65; National Container Company (NCC) 66; Neptun Werft 61; NIKI 66; Norbert Dentressangle 38, 39, 40; Nord Stream 27; Norddeutscher Lloyd 65; Nordsee Nassbagger und Tiefbau 33; North Cape Minerals 25; NSCC-DrillTec 28; Ogden 64; oneworld 66; Øresundsbro Konsortiet 51; P&O Nedlloyd 38, 40; Panalpina 38, 39, 40; PCC Intermodal 56; PerAarsleff 34; Petrolesport 42; PKP Cargo 7, 11; Polferries 16, 62; Port of Aarhus 13, 17; Port of Amsterdam 7, 22; Port of Antwerp 7, 18; Port of Arkhangelsk 46, 47; Port of Bathurst 65; Port Botany 45; Port of Bremerhaven 13, 18, 19; Port of Gdańsk 25, 62; Port of Gdańsk Cargo Logistics (Port Gdański Eksploatacja) 25; Port of Gdynia 14, 15, 34; Port of Gothenburg 6, 13, 14, 15, 45, 49; Port of Hamburg 13, 18, 44; Port of Hamina 42, 48, 49; Port of Helsinki 48; Port of Karlskrona 14, 15; Port of Kirkenes 47; Port of Klaipėda 5, 24, 27; Port of Koper 8; Port of Kotka 42, 48, 49; Port of Le Havre 28; Port of Liepaja 16, 68ł Port of Marseilles 8; Port of Murmansk 46, 47; Ports of Paldiski 10ł Port of Ponta Delgada 8; Port of Riga 16, 24; Port of Rostock 7, 16, 54, 60, 69; Port of Rotterdam 7, 18; Port of Sassnitz 54, 60; Port of Sillamäe 10; Port of St. Petersburg 16, 47, 48, 66; Port of Stralsund 60; Port of Tallinn 24, 62; Port of Trelleborg 51; Port of Ventspils 16, 24; Port of Vostochny 42; Port of Wismar 60; Port of Zeebrugge 9; Port Północny 25; Ports of Stockholm 62; Primorsk LNG Terminal 27; Puttgarden Ferry Port 16; Red Nacional de Ferrocarriles Españoles (RENFE) 55; Rethmann-Gruppe 40; Rhenus Logistics 38, 39, 40; Robert Osikowicz Engineering 28; Robin Hood Airport Doncaster Sheffield 12; Rødby Ferry Port 16; ROLF SCS 42; Rome Fiumicino Airport 12; Royal Mail 40; RWE DEA 40; RWE Innogy 19; RWE npower 28; SafeSeaNet (SSN) 21; SAS Scandinavian Airlines 12; Saudi Aramco 28; Scandlines 16, 66; Schenker Automotive RailNet 10; SEA-invest Group 25; Shell Exploration & Production 28; SHV Gas 25; Sibelco Nordic 25; Singapore Changi International Airport 30; SNCF Geodis 38, 39, 40, 66; St. Petersburg Pulkovo Airport 12; STEF-TFE 39; Stena Line 14, 15; Stockholm Skavsta Airport 12; Stockholm-Arlanda Airport 12; STX OSV Holdings 8; Süd-Chemie 25; Sun Hung Kai Properties 28; SustAccess 45; Swiss International Air Lines Ltd. 66; Sydfynske 66; Sydney Airport 30; Świnoujście LNG Terminal 27; Tallinn Airport 10, 12; Tatco Boring 28; Technip 28; Telstra 28; Terminal Investment 24; Terramare 33; The National Gas Company of Trinidad and Tobago 28; Thiel Logistik 38; Tibbet and Britten Group 38, 40; TMI Logistics 40; TNT Express 38, 39, 40; Tokyo Narita International Airport 30; TOTAL 28; Trafigura 22, 23; TransGas 28; Transporeon 28; Transport Intelligence 56; TransportForsk Föreningen 53; Travemünde Ferry Port 14, 16; Vilnius International Airport 12; Virginia Inland Port 45; Virginia Natural Gas 28; VTB Bank 12; Wallenius Wilhelmsen Logistics (WWL) 40, 42, 43, 66; Weissheimer Malz 25; Wincanton 38, 39, 40; Wizz Air 12; YRC Worldwide 59; ZIEGLER Group 38, 39, 40.

ISSN

173

3-67

32

€ 15/50 PLN (VAT 0%)

b i m o n t h l y - d a i l y c o m p a n i o n

№ 6/2010 (38), NOVEMBER/DECEMBER

Report

European logistics

Dredging & maritime construction

Baltic Transport Journal is an official media partner of:

Focus

BSR’s rail freight transport Tthe cover of this year’s last BTJ heralds a special section on dredging. We surely devote a lot of attention to engineering, its importance for the maritime industry and impact on countries’ economic development,

particularly in the text by Rene Kolman as well as the article “Aiming at greater depths” which tracks down major dredging-involved projects in the region. Furthermore, Rob-ert Osikowicz with his text on HDD technology provides you with substantial infor-mation on the little known specificity of trenchless engineering and its possible imple-mentation in the marine industry. See our “European logistics” report to get a view of the current situation on the logistics market and the sector’s most significant players. Go to Focus for information on the BSR’s railway cargo transport system and to find what Dariusz Stefański of PCC Intermodal tells about their new inland terminal and the future of intermodal market in Poland. I would also like to draw your attention to the interview with Kimmo Naski about the fusion of Kotka and Hamina ports. In a way, mutual cooperation is this issue’s recurring theme and in a difficult economy it often takes the form of mergers. Integration is surely a positive thing, but the striking number of such operations raises questions about the condition of the industry. With the hope you will enjoy your reading, on behalf of the editorial board, I wish you all a peaceful Christmas time, a Happy Channukah and a healthy, fulfilling new year.

Lena Lorenc

6/2010 | Baltic Transport Journal | �

EWTC newsletter

An innovative instrument for international cooperation

Growing competitiveness inspires us to create such forms of cooperation that enable effectively solving transnational transport problems. This summer European and Asian companies received a significant signal for prompting activity within interregional transportation and logistics areas.

The East-West Transport Corridor Association

It is difficult to fit the transport and lo-gistics sector, in a broad sense, into a specific geographic framework, since its development has been heavily affected by globalization trends, as compared to other segments of the economy. In

this context it becomes vitally important to develop and enhance horizontal collabora-tion among countries, notwithstanding their economic or political frameworks, with the aim to systematically eliminate procedural barriers, promoting interstate dialogue and matching national economic interests.

Constitutive conference of EWTCA

On June 29th the international East-West Transport Corridor Association was founded in Vilnius, the capital of Lithuania. The conference at-tracted nearly 100 participants from 14 countries. The newly established EWTCA consists of six business associations, four public administrative institutions, two universities and 14 companies.

First and foremost, the EWTC Association is expected to activate the cooperation of trans-port and logistics companies, intermodal trans-port operators, consignors and consignees, governmental bodies, academic and research institutions, and promote dialogue between the states embracing the corridor with the view of addressing emerging problems. The As-sociation, among its other tasks, will focus on identifying bottlenecks along the EWTC, sim-plification of documentation and procedures, development of innovations and intermodal

Algirdas Šakalys is the newly elected President of the International EWTC Association. In 1991-2000 as Vice Minister of Transport and Communica-tions of Lithuania, he was responsible for transport policy and foreign rela-tions, later as a consultant to the President of Lithuania for transport policy. Currently, he is also an Adviser to the Prime Minister of the Republic of Lithuania and holds the position of Director of the Competence Center of Intermodal Transport & Logistics at Vilnius Gediminas Technical University.

techniques, and naturally, on the representation of the common interests of EWTC partners in various international organizations.

The EWTC Association particularly aims at developing the East-West Transport Corri-dor which is expected in the short run to be-come an important and effective transport link in the global transportation and logistics chain in Europe and Asia. Moreover, the Associa-tion will assist in implementing the transport policy within the EU Baltic Sea Strategy, with special emphasis on environmentally-friendly transport development.

The initial steps

The concept of a ‘green corridor’ gives priority to rail as one of the most ecological modes of transport, as well as to the sustaina-ble integration of all the modes. In accordance with this strategic line, the Association is ori-entated towards promoting more intensive use of rail services, and enhanced railway interac-tions with road and sea transport. In order to identify the starting steps of activity, an in-quiry among EWTCA partners was executed.

According to survey data, initial key activities were determined. They are as follows:

– to form a strategy and Action Plan for im-plementing the EWTC;

– to introduce the EWTCA to international institutions, international businesses and governmental structures (the presenta-tion of EWTCA at EXPO 2010, at the Eu-ropean Commission, at the international conference in Fort Lauderdale (USA);

– to establish the Secretariat of the EWTCA (in Vilnius) and to solve the question of its official residence;

– to elaborate the concept of the green transport corridor;

– to form a common brokerage tool for communication and information ex-change among EWTCA partners;

– to develop partnership links of the asso-ciation in order to eliminate bottlenecks and to create the missing links across the global Asia-Europe land bridge.

Moreover, a regional business seminar of EWTCA partners took place on 8-9th of November, 2010 (Klaipėda-Karlshamn). The seminar attracted partners from Ukraine, Belarus, the Russian Federation (Kalinin-grad region), Sweden and Lithuania. The participants within the Baltic-Black Sea re-gional cooperation framework discussed the prolongation of the Klaipeda-Odessa route (Viking project) towards the North (Swe-den) as well as South (Turkey).

The EWTCA should make a significant contribution and generate added value in terms of handling and developing trade flows between Europe and Belarus, China, Kazakhstan, Rus-sia, Ukraine, and other Far Eastern countries. This shall be supported by the efficient co-operation between shippers, transportation, logistics companies, intermodal terminal op-erators, national, regional and domestic au-thorities and research institutions considering not only the BSR’s market needs, but also the global trade demands of Europe and Asia. �

Dr Algirdas Šakalys

� | Baltic Transport Journal | 6/2010

BTJ calendar of partnership events 2010-2011

BTJ 6/2010 (Nov.-Dec. edition) BTJ Special: Dredging and maritime constructionReport: European logistics

Focus: BSR’s railway freight transport systemIssue distributed at:

BPO Seminar: LNG in the Baltic and North Sea12 January 2011, SE/Gothenburgwww.bpoports.com

EuroRail 201122-24 February 2011, DE/Berlinwww.terrapinn.com/2011/eurorail

GreenPort Logistics 2011& Energy for GreenPorts 201123-24 February 2011, IT/Venicewww.portstrategy.com/greenportvenice

Port Centric Logistics Conference 20111-2 March 2011, UK/Birminghamwww.navigateevents.com

Baltic Ports Organization in cooperation with the Port of Gothenburg are jointly organizing the seminar “LNG in the Baltic and North Sea – Business opportunities or the cost factor for the ports”. Among the analyzed matters one should expect prospects for LNG fuel both from the ship-owner and the port perspective, as well as bunkering and distribution issues. The seminar is addressed towards ports, the shipping sector and other related businesses.

Now in its 14th year, EuroRail is the leading platform for rail market CEOs to meet and discuss how to overcome the challenges of today’s competitive environment, and how to capitalise on the opportunities created through rail’s strategic advantages in a market geared towards sustainability.

The event will examine practical, economically viable solutions, as well as applications and case studies in use for reducing carbon footprints and energy consumption management. The talks will have their follow-up at GreenPort’s Annual Congress, 14-15 September 2011 in Hamburg.

The 2nd Port Centric Logistics Conference will bring together relevant supply chain partners to debate on how effective port centric logistics solutions are changing current distribution systems and generating a competitive advantage. Experts from different branches will share their knowledge and experience on trends in maritime trade flows.

BTJ 1/2011 (Jan.-Feb. edition)Issue distributed at:

Transport Week 20111-3 March 2011, PL/Gdańskwww.actiaconferences.com

RORO Shipping Conference 20119-10 March 2011, DK/Copenhagenwww.informaglobalevents.com

Europort Istanbul 201123-26 March 2011, TR/Istanbulwww.europort-istanbul.com

SITL 201129-31 March 2011, FR/Pariswww.sitl.eu

TransRussia26-29 April 2011, RU/Moscowwww.transrussia.ru/eng

Actia Conferences and Baltic Transport Journal (as the main media partner) invite you to a joint event integrating three already well-established international conferences: the 5th Ro-Ro & Ferry Conference, the 5th Baltic Container Conference and the 4th RailPort. The event will be accompanied by a 3-day open trade fair, free seminars and discussion panels, and topped with an evening gala dinner. Integration (and competition) within transport sectors in the Baltic and CEE countries will be the main theme of the market discussions.

Informa’s RORO is becoming an annual event, introducing a new forum for ro-ro owners and operators. The 2011 event this time only includes a conference section, but promises to bring you up to speed on all recent developments in the sector and new challenges facing the industry. The 2012 edition in Gothenburg will traditionally feature both a conference and exhibition.

Europort Istanbul International Maritime Exhibition has proven to be the complete platform for the maritime industry in Turkey and is now moving full speed ahead to bring the international maritime sector to the exhibition and a wide range of conferences and workshops for 11th time. The previous 2009 edition gathered over 200 exhibitors and almost 8,000 visitors from 48 countries, 95% of whom expressed their intention to visit the event in 2011.

For more than 30 years SITL brings together all transportation and logistics communities and presents products and services dedicated to distribution and the supply chain of tomorrow. Last year’s show brought 500 exhibitors, 27 thou. attendees to the trade fair and a cycle of 30 conferences and workshops, and the organizers are heading towards another record breaking result.

The 16th edition of the largest international transport event in Russia and its neighbouring countries is a good opportunity to establish or enhance your company’s presence on the Russian market. Each year the show gathers representatives from all major transport sectors, including freight forwarders, logistics providers, shipping lines, ports, terminals, rail and road carriers, material handling equipment, etc.

Report: Baltic energy marketFocus: IT solutions for transport

BTJ 2/2011 (March-Apr. edition)Issue distributed at:

Transport Logistic 201110-13 May 2011, DE/Munichwww.transportlogistic.de/en

Nor-Shipping 201124-27 May 2011, NO/Oslowww.nor-shipping.com

TOC Europe 20117-9 June 2011, BE/Antwerpwww.tocevents-europe.com

SIL Barcelona 20117-10 June 2011, ES/Barcelonawww.silbcn.com

Since 1978 Transport Logistic has established itself as the most important trade fair for logistics, mobility, IT and supply-chain management in Europe. The 13th edition, once again co-organized with Air Cargo Europe, will provide an expert overview of new markets, trends and innovations in the international transport and logistics industry via its many accompanying conferences, seminars, workshops, presentations, etc.

Notwithstanding the downturn in the European shipbuilding/shiprepair market, 2009 Nor-Shipping was the largest in the history of this event, dating back to 1967. With more than 1,100 exhibitors and 33,000 attendees, the show featured 22 national and four thematic pavilions in six halls. This redesigned thematic exhibition layout plus selection of technical conferences and workshops turned out to be a success, so 2011 will follow a similar concept.

The Terminal Operations Conference & Exhibition traditionally gathers suppliers of container terminal services, handling equipment, systems and software. Hundreds of executives from the port, terminal and shipping sectors will meet to discuss the evolution of global maritime trade and how to improve the performance of shipping, port and hinterland services to support trade growth.

Over the last 13 years, International Logistics and Material Handling Exhibition in Barcelona, has become the reference point for all logistics sectors, as an effective and profitable tool for doing business and making contacts in a professional and friendly climate that is difficult to match. The event will be supported by the Mediterranean Logistics and Transport Forum, a number of technical conferences and dedicated business meetings.

Report: Breakbulk & project cargoFocus: Financing and insurance

6/2010 | Baltic Transport Journal | �

BTJ calendar of partnership events 2010-2011

BTJ 3/2011 (May-June edition)Issue distributed at:

European Shortsea Congress 201129-30 June 2011, DE/Hamburgwww.navigateevents.com

GreenPort Congress 201114-15 September 2011, DE/Hamburgwww.greenport.com

Held already twice in Dublin and once in Liverpool, the 4th European Shortsea Congress will first time take place on the continent, comprising a two-day conference catering to bulk and unitized shortsea supply chains. The event is guaranteed to bring numerous networking activities.

The 6th GreenPort Congress moves to Hamburg, the European Green Capital 2011, and will feature a 2-day technical conference, gala dinner, and a study tour of the main ports in the North European range: Hamburg, Bremen, Amsterdam, Rotterdam and Antwerp. The topics will include collective solutions for clean shipping, global regulations on CO

2 emissions, energy efficiency, sustainable

development of land and seaward access, etc. More info at: [email protected].

Report: Ro-ro & ferry marketFocus: Transport and ecology

BTJ 4/2011 (July-Aug. edition)Issue distributed at:

BALTEXPO 20116-8 September 2011, PL/Gdańskwww.baltexpo.com.pl

BPO Annual Conference 20118-9 September 2011, DE/Rostockwww.bpoports.com

Seatrade Europe 201127-29 September 2011, DE/Hamburgwww.seatrade-europe.com

Along with the Polish shipbuilding restructuring process, the private yards continue their production and new areas of their activities require modern machinery and investments. Baltexpo will target these topics during its 16th international exhibition and conference. In over 30 years, the event has always attracted thousands of professionals from the entire maritime sector: ship owners/operators, shipyards, ports, equipment manufacturers/suppliers, etc.

Baltic Ports Organization invites all executives interested in improving the competitiveness of maritime transport in the region, increasing the efficiency of ports/terminals, developing infrastructure and value added services, as well as extending both ashore and hinterland connections, to its annual conference, this year held at and co-organized by the Port of Rostock.

Seatrade Europe brings together key decision makers in the industry for a high-level conference, a major exhibition, travel agent training and an exceptional social programme. This event attracts senior purchasers, technical and hotel directors, itinerary planners and other major players from the world’s cruise and rivercruise market. A rare chance to accomplish months of business in a few days whilst your prime target group is gathered under one roof.

Report: Baltic maritime ranking 2011Focus: Baltic shipyards

BTJ 5/2011 (Sept.-Oct. edition)Issue distributed at:

TRAKO International Railway Fair12-14 October 2011, PL/Gdańskwww.mtgsa.com.pl/title,lang,2.html

Baltic Development Forum Summit 201124-27 October 2011, PL/Gdańskwww.bdforum.org

Europort Rotterdam 20118-11 November 2011, NL/Rotterdamwww.europort.nl

The most important rail meeting in Poland and one of the largest in CE Europe, giving the opportunity to promote agglomeration rail transport, freight forwarding and logistics, present the latest technology and hold business meetings. The exhibition is organized in partnership with Polish National Railways (PKP) together with a number of seminars, conferences and presentations.

For the first time Poland will host the annual BDF Summit. Baltic Development Forum will work closely together with the Polish government during its EU-presidency (second half of 2011) and the European Commission, and hopes that this show will be a good demonstration of how to combine top-down political guidance with bottom-up enthusiasm and entrepreneurship.

A bi-annual event gathering over 30,000 professionals from all segments of the shipbuilding/shiprepair industry, giving an overview of the latest technologies in the maritime industry. Construction of vessels, dredging, fishery, inland navigation, mega yachts, naval specials, offshore, sea shipping, workboats, and much more is waiting for you at the four-day exhibition and its assisting conferences.

Report: Baltic containerizationFocus: Railway transport

BTJ 6/2011 (Nov.-Dec. edition)Issue distributed at:

Intermodal Europe 201129 Nov.-1 Dec. 2011, DE/Hamburgwww.intermodal-events.com

After a 3-years break the Intermodal Europe exhibition and conference will again be hosted in Hamburg. The world’s leading event for all associated with the container and intermodal industries dates back to 1976 (at first named CTC – the Container Technology Conference). Intermodal Europe is organised by IIR Exhibition, a part of the Informa Group.

Report: Bulk transportFocus: Road traffic

� | Baltic Transport Journal | 6/2010

MaritimeSTX OSV Holdings Limited has secured new contracts with Farstad Shipping, an interna-tional supplier of large, modern offshore sup-port vessels. The contracts of approx. NOK 1.3 bln include a total of four Platform Supply Ves-sels for delivery 2012-13. Two of those vessels will be delivered from the group’s yards in Nor-way, the other two from the yard in Vietnam.

X-Press Container Line has started a new weekly feeder service linking Gothenburg, Antwerp and Southampton, which is the first direct container service between these ports. Meanwhile the company has cut Antwerp from the Gothenburg Express (AGX) and short-ened the service to a final call at Rotterdam.

Port of Hamburg reported a strong growth of 8% in seaborne cargo handlings with the result of 89.4 mln tonnes in the first nine months of this year. With a total of 5.9 mln TEU the container segment recorded double-digit growth of 10.7%.

Port of Klaipėda has been chosen as a tran-sit hub, through which the United States will send supplies for NATO’s International Security Assistance Force in Afghanistan. The cargo will later go via rail-freight across Russia. Lithuania is the last of the Baltic states chosen to serve as a shipping point for US cargo transit.

Danish ferry operator DFDS and C. Ports (a sister company to Cobelfret) will pay SEK 48 mln to acquire Älvsborg Ro/Ro company, which has been established by the Port of Gothenburg to operate ro-ro termi-nal for the next 25 years. The shares in joint venture of DFDS and C. Ports will be 65% and 35%, respectively. The terminal has seven ro-ro berths and a total area of 463,000 m2. The background of the deal is a decision from February 2010 to devide the port into a mu-nicipal Port Austhority and three separate terminal operating companies. Gothenburg port’s responsibilities will include maintaining

DFDS and C. Ports will own a ro-ro terminal in Gothenburg

What’s new?

Phot

o: P

ort o

f Aar

hus

the harbour and quay’s infra-structure, while Älvsborg Ro/Ro will be responsible for the surface of the terminal area. This operation will open up new opportunities for port employees and the port itself, creating a secure and long-term revenue flow. As Port of Gothenburg’s Chief Execu-tive Magnus Kårestedt states, “DFDS and C. PORTS share our visions with regard to the port, they have sector knowl-edge which is second to none

and they have a long-term strategy. This was a key requirement for agreeing to this long-term deal.” Chairman of the Port of Gothen-burg Sven Hulterström adds, “It feels ex-tremely positive that two of the port’s largest customers have joined forces to run the Ro-Ro Terminal.” The agreement with the Port of Gothenburg will come into effect in January 2011, making DFDS and C. Ports in charge of the terminal company, 320 employees and all customer contracts. Ro-Ro is the first of three terminals in the hands of the private operator. Operations on the container and car terminal in Gothenburg will be transferred next year. �

COMPETENCETAKES YOU THEREwww.upm.comwww.upmseaways.com

COMPETENCETAKES YOU THEREwww.upm.comwww.upmseaways.com

COMPETENCETAKES YOU THEREwww.upm.comwww.upmseaways.com

Phot

o: Th

e Por

t of G

othe

nbur

g

6/2010 | Baltic Transport Journal | �

MaritimeMalteurop Polska and Copenhagen Merchants will jointly develop Gdańsk Bulk Terminal. GBT, with warehouse capac-ities of 35 thou. tonnes, is due to launch its operation in autumn 2011.

Extra-slow-steaming (ESS) programmes have increased this winter. According to the analyst AXS Alphaliner, ESS, ena-bling carriers to burn less fuel and absorb excess capacity, is currently adopted on 93% of Far East-North Europe loops and 80% of Far East-Mediterranean loops.

NORDEN’s 2010 Q3 operating profit (EBIT-DA) was USD 22 mln compared to USD 28 mln for the same period in 2009. The total operating profit for the first 9 months increased by 178% to USD 201 mln against USD 72 mln for the same period in 2009.

Maersk Line is the most reliable ship-ping line according to Schedule Reli-ability Insight report Q3 2010 on the 20 largest carriers, issued by Drewry Ship-ping Consultants. Maersk’s schedule reli-ability performance in Q2 2010 reached 78.9%. The second place in the rating belongs to Hyundai Merchant Marine with an on-time rate of 78%, followed by APL (73.8%) and United Arab Shipping Company (67.9%).

The European Commission has launched “blue belt”, a one-year pilot project designed to reduce complex ad-ministrative procedures in shipping as well as ensuring free vessels operations within the internal EU market. Work on the “blue belt” will be carried out by the European Maritime Safety Agency.

What’s new?

The analysts’ view on the crisis in shipping

According to research by the Centre for Mar-itime Studies of the University of Turku, Finland, total cargo volumes decreased by 10% in Baltic seaports in 2009, comparing to the year before. A dramatic fall in all cargo types was noted, but handling of containers decreased the most (by nearly one quarter). Between 2006 and 2009, the total amount of cargo handled in Baltic ports declined by 6%. Measured by total handlings, Russia became the leading country in the BSR, with a share of 23% in 2009, closely followed by

the former leader, Sweden. The prospects for the container shipping market are now looking con-siderably better. A report produced by Hackett Associates and the Bremen Institute of Shipping Economics and Logistics (ISL) shows that in Sep-tember 2010 container volumes at six of Europe’s top ports (Hamburg, Zeebrugge, Rotterdam, Bremerhaven, Le Havre and Antwerp) grew by an average of 12.6%, year on year. The authors of the report predict continuous growth in 2011, but note that it might be slower than this year. �

Phot

o: N

CC

Rough times for European container businessAmsterdam Container Terminals (ACT),

an owned subsidiary of Hutchison Port Hold-ings, will reorganize due to the insufficient market demand. The increasing capacity that characterizes container handling in north-western Europe touches ACT directly, as the company is not able to receive the largest

container vessels. ACT will maintain enough capacity to be able to handle deep-sea cargo, functioning from now on as a smaller, but full deep-sea terminal. This operation will include selling a portion of its equipment and result in job losses for 70 employees, for whom a social plan will be provided. �

10 | Baltic Transport Journal | 6/2010

Promoting Estonian ports’ in the Far East

What’s new?

New merger within Schenker

DB Schenker-owned vehicle logistics compa-nies, Autotransportlogistic and Schenker Auto-motive RailNet are merging “in a response to the industry’s greater demand for integrated network solutions for components, as well as finished vehi-cles from a single source,” as it was stated by board member Karsten Sachsenröder. The new com-pany, DB Schenker Rail Automotive is to start operating in Q1 of 2011 and will comprise four di-visions, with separate sales and dispatch structures for finished vehicles. The new structure is aimed at ensuring business neutrality through third-party forwarders for the finished vehicle business. �Ph

oto:

DB

Sche

nker

POLZUG Intermodal GmbHContainer Terminal Burchardkai, HamburgTel.: + 49 40 - 74 11 45-0E-Mail: [email protected]

POLZUG Intermodal POLSKA Sp. z o.o.ul. Ks. l. Skorupki 5, WarszawaTel.: + 48 22 - 336 34 00E-Mail: [email protected]

POLZUG_BTJ_184x118_6.indd 1 03.11.10 15:07

LogisticsThe German Logistics Association (BVL) awarded Nord Stream AG with the 2010 German Logistics Award in recognition of its project “Logistics for the Pipeline”, that is, the gas pipeline through the Baltic Sea from Vyborg, Russia, to Lubmin near Greifswald, Germany, connecting natural gas reserves in Russia with the European gas grid.

Kuehne + Nagel has begun the construc-tion of a new distribution centre in Duisburg’s harbour area, Germany, which will enlarge the company’s warehousing facilities in Duisburg Logport by app. 28,000 m2. The new distribu-tion centre for customers from the consumer healthcare industry will open in May 2011.

HHLA together with Gottwald Port Tech-nology, the Institute for Vehicle Technology at RWTH Aachen University and the Institute for Energy- and Environmental Research Hei-delberg, are involved in a research project, aimed at lowering CO

2 emissions through the

use of battery-powered container transport-ers. If the test project results in a success, HHLA will place electrically-powered containers at its Altenwerder terminal in Hamburg.

Estonian Logistics Cluster (EAC), cooperat-ing with the Ministry of Economic Affairs and Communications, the Foreign Ministry and Enterprise Estonia, is promoting the country’s logistical location and competitive advantages in several cities in China and Vietnam. EAC, 70% financed by the EU Regional Development Fund, aims at increasing the potential of the country’s logistics sector on various target markets and to increase export turnover. A number of meet-ings with companies operating on the Asian and Northwest Russian course as well as state

organizations have already taken place. In addi-tion, Enterprise Estonia, which distributes EU structural funds in the country has recently de-cided to provide EEK 12.8 mln (EUR 818 thou.) for the development of the cluster, which involves 18 partners, incl. ports of Tallinn, Sillamäe, Pald-iski, Estonian Railways, Tallinn Airport and the Tallinn University of Technology. The EAC project commenced in June 2010 and will last until December 2012. As a result of its activ-ity, the export turnover of the members should increase by at least 30% within five years. �

6/2010 | Baltic Transport Journal | 11

OverlandRussian Railways signed an agreement with Siemens AG on 18 November to set up an engineering centre which will produce multiple-unit trains for coun-tries with 1,520 mm gauge rail tracks, along with their components, fittings, parts, and details. The parties intend to establish long-term scientific-technical cooperation focused on developing, building, and testing new projects.

The privatisation of PKP Cargo, Eu-rope’s second largest rail freight opera-tor, is scheduled for 2011. The company is to be sold off for approx. PLN 3 bln (EUR 765 mln) to corporate investors or other companies operating in the in-dustry sector.

VR Cargo and Transpoint, two impor-tant Finnish rail logistics operators, have merged and adopted a new name of VR Transpoint, which has therefore be-come Finland’s largest logistics group. The company offers expertise in railway, groupage (LTL), mass goods (FTL) and international logistics.

What’s new?

After 3 years of operation and funding by the European Commission, the LABEL project has resulted in a truck parking area (TPA) label-ling scheme for Europe. The International Road Transport Union (IRU) and International Trans-port Forum (ITF) have become the implement-ing bodies of the results. LABEL’s objectives were to validate existing international draft standards for adequate facilities for professional drivers as well as to establish at least 70 TPA sites certified in Member States. IRU and ITF will now jointly operate, maintain and further develop LABEL

IRU and ITF to implement truck parking labelling scheme

through the TRANSPark web-based platform developed by the two organizations to provide online information on TPA availability, loca-tion and parking site facilities in 40 countries. TRANSPark, beyond its present e-registration and search tools, will host new facilities such as the labelling scheme. IRU Head of Goods Transport and Facilitation, Peter Krausz, stated that this cooperation will increase driver, vehi-cle and cargo security and improve basic con-ditions for observing strict social rules on driv-ing and rest times for professional truckers. �

Single-wagon rail freight services endangeredThe problem of cutting and collapse of single-

wagon rail freight services was touched upon at the Rail Freight Seminar organized by the European Shippers’ Council. According to ESC, many ship-pers dependent on this service will be forced to ei-ther put their goods on lorries again or be left with no alternative, which may result in factories being shut down. Henk Schaafstal, Chairman of the ESC have stated, that it is important for the ship-pers to remain positive and confirm to the single

wagon-load service providers their willingness to look at any solutions to keep such services go-ing. “There isn’t much time to find solutions; but I have to hope there is still light at the end of the tunnel”, Schaafstal said. Among proposed solu-tions there are e.g. rail freight operators combining their operations for international single-wagon services, or customers joining to offer the neces-sary volumes for a logistics company to manage and contract the necessary rail freight services. �

12 | Baltic Transport Journal | 6/2010

What’s new?

AviationVilnius International Airport (VIA) has decided to entrust technical maintenance of engineering facilities to the private company UAB Baltic Ground Services. The operation is aimed at reducing the airport’s operating costs and improving the quality of services. VIA signed a one year contract with the company and has set a half-year transitional period.

Negotiations on creating a direct connection between China and Estonia have been held by Hainan Airlines and Air China with Tallinn Airport. HNA Group’s subsidiary Hainan Air-lines has recently begun expansion into Eu-rope. In September the company showed its interest in buying 48% of Latvian airBaltic.

From March 2011, Finnair will start a daily connection between Helsinki and Gdańsk, the company’s third destination in Poland in addition to Kraków and Warsaw. The service to Helsinki is to open fast connections to Asia via Finland’s capital to residents of Gdańsk and the the airport’s catchment area.

Stockholm-Arlanda Airport, Swedish air navigation services LFV and SAS Scandi-navian Airlines are jointly involved in a major EU project (SESAR JU) aimed at cre-ating a single European airspace and elimi-nating unnecessarily long routes, for better punctuality, lower fuel consumption and cutting CO

2 emissions by 10% by 2020.

From April 2011 Lufthansa is going to be using biofuel on commercial flights. The “burnFAIR” project, dedicated to the test-ing of biofuel, is backed by the German government within the framework of its aviation research programme aimed at un-derpinning the sustainability of air traffic.

According to the International Air Trans-port Association, European airlines saw a 12.1% year-on-year demand increase in Oc-tober. The last month has also seen growth of 14.4% y-o-y in international air cargo traf-fic. Until then, overall freight volumes had been declining each month since May.

Construction of a new international pas-senger terminal at St. Petersburg Pulk-ovo Airport (LED), Russia’s fourth largest aviation gateway, has been launched by Fraport and its partners in the Northern Capital Gateway consortium (VTB Bank, Cypriot investor Koltseva Holdings, Cope-louzos Group of Greece).

The largest low cost airline servicing Eu-rope, Wizz Air, has announced the opening of its 14th operational base in Vilnius, Lithuania. With this movement, scheduled for April 16, 2011, the company will launch eight new routes from Vilnius to London-Luton, Robin Hood Airport Doncaster Sheffield, Cork, Eindhoven, Stockholm-Skavsta, Milan-Bergamo, Rome Fiumicino and Barcelona. Services to London and Doncaster Sheffield will be in operation five times and twice a week, respectively. Flights

Wizz Air’s new base in the capital of Lithuania

from the company’s facilities in Vilnius will ini-tially be handled by new Airbus A320. As Wizz Air’s chief executive officer József Váradi states, the airline is extremely content on this expan-sion. “Beyond further enhancing the travel op-portunities in the Lithuanian market, we will create hundreds of local jobs and significant revenue uplift for the local tourism industry,” he adds. In addition, Wizz Air also launches direct flights to Brno, the Czech Republic’s second-largest city, from London-Luton. �

Phot

o: W

izz

Air

The EU has increased security on air cargoThe European Union has set out a series of

recommendations concerning air cargo secu-rity in response to the security alert on October 30th, when explosive devices were found in cargo shipments from Yemen at airports in Germany and the UK. The terrorist plan failed, nonethe-less it resulted in delays and vast financial losses. EU proposals are focused on three key areas: strengthening cargo security controls, better coordination of actions and information within

the EU as well as joint action at the international level. New legislative steps will concern cargo originating from outside the EU, the first ones will be to define criteria for identifying freight representing a risk and to establish mechanisms allowing for the evaluation of security standards at non-EU airports. The number of EU inspec-tions will be increased. Moreover, further in-vestment in research is planned to improve the performance of current detection technologies. �

LC: six new aircraft by 2015

Lufthansa Cargo will add the equivalent of six MD-11 widebodies, in response to forecasted 5% annual increase in its airfreight traffic from 2012

to 2015, driven by Asian demand. Ac-cording to the company’s executive board member of Product and Sales Andreas Otto, Lufthansa Cargo will begin think-ing about a fleet replacement in five years and the final decision are to be made by 2020. “We have an excellent system in fine-tuning our loads and to generate the best yield,” Otto noted, and mentioned the company’s investment plans – Lufthansa Cargo, in reaction on increasing demand

for medical shipments, will create a hub for phar-maceuticals transport in Hyderabad as well as a warehouse for cooling freight at Frankfurt hub. �

Phot

o: W

ikim

edia

Com

mon

s

6/2010 | Baltic Transport Journal | 1�

Maritime

Happy ending – happy beginningThe merger of APM Terminals & Cargo Service

Once upon a time in the Port of Aarhus, there was a cargo handling company, operating next to a container services giant. One September day in 2010 both entities decided to start working together and merge. Will they live happily ever after?

As they announced August 31st, APM Terminals and Cargo Service set up a joint venture called APM Terminals-Cargo Service; the process of merging is to be concluded by the end of

2010. The new, combined offer comprises one 15-metre deepwater berth, one set of truck gates and on-dock container repair facilities with both standard and refrigerated containers.

“We have decided to join forces and merge the two container terminals to create a larg-er, more efficient and competitive container operation. Together we have a much better chance to position ourselves in the interna-tional container market,” explains Lars Krabbe, Managing Director of Cargo Service Holding A/S. Logically, the main goal of the merger is a higher competitive advantage on the Baltic market as well as a wider scope of services. Among other aims the two parties mention in-ter alia reduced environmental costs.

As far as efficiency and cost effectiveness are concerned, the operation may be well worth a mass. According to Bjarne Mathiesen, Direc-tor, Port of Aarhus, the former two operators were both below the critical volume needed to run viable operations. Hence, bringing the vol-umes together would reduce both capital costs and the running costs per unit handled.

Who’s who

APM Terminals is an independent com-pany, yet associated with the A.P. Møller Mae-rsk Group and a part of the Global Terminal Network. The latter consists of 50 operating container facilities in 34 countries on five continents. In the first three quarters of 2010, GTN reached a container throughput of 23.5 mln TEU and USD 3.14 bln in revenue. The company is developing consistently and has for the time being seven new terminal devel-opment projects underway. However, apart from new investments inter alia in German Wilhelmshaven and Dutch Maasvlakte 2, the company’s activities concentrate on the Asia-Pacific and African regions. This is easily ex-plained by numbers: as APM Terminals’ CFO underlined during the Port Finance Confer-ence in London, the biggest business now lies in emerging economies (South America, sub-Saharan Africa, India), where 2/3 of global container throughput is handled.

Going back to Europe and the Baltic Sea re-gion – the other half of the newlyweds, Cargo Service, is operating in three sectors: project, multi-terminal and warehousing. The main ac-tivity within the project division is the handling and loading of wind turbines. “Every year we load on average 80 vessels with wind turbines,

of about 120,000 metric tonnes each,” says Lars Krabbe. The project division also handles any other heavy duty and out of gage cargo. The lat-ter is to remain the key activity of the company, independent of the merger. Cargo Service op-erates in Denmark exclusively, employing ap-prox. 65 people. Until this year, it was handling 5 divisions. However, due to the merger, it has transferred all container related activities and assets (container terminal, repair and EMR) to the joint venture with APM Terminals.

Beneficiaries

The new company will certainly stimulate some thoughts to its competitors, among them other Danish ports, as well as Gothenburg, Bremerhaven or Hamburg. Aarhus is one of the most important ports of the Baltic Sea. The port is ambitious both regionally and locally. Not only is it striving to become a hub for the Baltic (see BTJ 2/2010), but it is also developing local and regional connections. For example, in June 2009, thanks to the efforts of APM Ter-minals, an innovative rail service was opened, allowing quick service to Copenhagen.

It is certainly too early to foresee a success or a failure of the undertaking; however, there seems to be a few benefits and beneficiaries of the merger. According to Bjarne Mathiesen, Port of Aarhus will be one of them, since there is no longer the same need for internal competition in the port itself. By combining forces, the port would gain a more focused image, concentrating on container services as well as, hopefully, bigger cargo volumes.

More mergers ahead?

The Baltic Sea region has been witness-ing numerous fusions recently (port opera-tors, ports themselves) and it seems that this may even be the case more often in the future. Rationalizing operations and consolidating volumes will probably be continued – not only due to the economic downturn. “The up-coming restrictive limits for emissions in the Baltic Sea will probably result in a closer co-operation between shipping lines and ports,” says Mathiesen. This will not necessarily lead to fewer actors, but the roles of the different entities may shift. In the long run the number of market players may therefore decrease. �

Martyna Bildziukiewicz

Phot

o: C

argo

Ser

vice

1� | Baltic Transport Journal | 6/2010

Maritime

The vision and the spiritStena Line’s historic shift of vessels lifts up Karlskrona-Gdynia route

Introduction of two new superferries to the Hook of Holland-Harwich service has started a domino effect in Stena Line’s Baltic fleet. Karlskrona-Gdynia has recently received the first one of the thoroughly converted ferries intended for this service.

It is the most significant ship transfer in the company’s history. Two sister giant ferries have been introduced to the Netherlands-UK route. Each one is 240 metres long and comes with a capacity of 1,200 passengers, 230 cars

and 300 freight vehicles. The new vessels have taken over the names of their predecessors and operate as Stena Hollandica and Stena Britan-nica. In the meantime, the ‘old’ Hollandica and Britannica have been moved from the North Sea to the Sweden-Germany service, where they replaced four vessels that formerly sailed between Gothenburg and two German ports – Kiel and Travemünde. Hence, pure freight service to Travemünde has been terminated and the total traffic now goes only on the re-ferred two ro-paxes via the Port of Kiel. Cor-respondingly the ships have been renamed to Stena Germanica and Stena Scandinavica (so the names on the Gothenburg-Kiel route are also kept the same). Finally, the ‘previous’ Ger-manica and Scandinavica are to run between Karlskrona and Gdynia. The first ship has undergone serious conversions and already

entered the line in early November under the new name of Stena Vision. The second unit, af-ter its similar reconstruction, will join in April next year as Stena Spirit.

Good times, bad times

Established 15 years ago, Karlskrona- Gdynia has always been primarily a cargo route, even though it naturally serves people’s trans-fer between Scandinavia and the continent. The service has been developing very well, of-ten with annual double digit growth in both cargo volumes and the number of passengers. It reached its peak of almost 94,000 ro-ro units and over 430,000 pax in 2007. Yet, the route has gone through some tough times within the last two years, reacting extremely fast to the fi-nancial depression already in November 2008. Freight volumes fell to 86,000 in 2008 and then further down to only 66,000 last year. Mean-while the passenger traffic firstly declined to the annual level 375,000 and then to 350,000 in 2009. An important factor was however that the company withdrew one ship from service,

leaving only two vessels on the line. Appar-ently, today there has been a particularly quick recovery seen as well. The first three quarters of 2010 brought 57,000 units which stands for 15% y-o-y improvement. Within the same pe-riod, the route has also carried around 300,000 people, which – even though the peak summer days are over – can be a nice prognosis for to-tal 15-20% annual growth. According to Stena Line executives, freight traffic on this route is well balanced both ways, but as the service was previously provided by one ferry and one char-tered freighter vessel, the company could not make full use of its potential due to the differ-ences in ships. A well equipped Stena Baltica is surely much more attractive to cruise travel-lers than cargo customers. It can facilitate 1,200 people in its hotel section, several restaurants, bars, a night club and wellness centre. On the other hand, the ship can fit max. 80 trucks on its 1,590 lane metres. Adversely, Finnarrow is able to carry up to 120 lorries (2,400 lm), but it is designated for 200 people only and offers prac-tically no leisure opportunities onboard. These, together with the usual problem of filling up day departures (contrary to often fully booked evenings), has caused a number of difficulties in proper line utilisation. Nevertheless, the average freight load rate on one ship in service in Sep-tember 2010 was already at the level of 69%. To-day cargo stands for more than half of the line’s income mix, with the rest shared by passenger tickets and onboard services.

New ferries in service

Running two practically equal ships will be a big change to the Swedish-Polish route. The charter agreement with Finnlines has just come to an end, and Stena Vision has stepped into Finnarow’s place, offering 2,200 lm and accommodation for 1,300 passengers at basic, possible to improve even up to 1,700 people at maximum peak times. As one might notice, today’s cargo space is a bit down, but imple-menting the second sister vessel will raise the overall freight potential by 20% and more than double passenger capacity. This is indeed a huge upgrade in Stena Line’s travel offer, with nicely renovated cabins, a good choice of restaurants and bars, a night-club, modern conference rooms, luxury SPA, a 400 m2 shop-ping centre, sundeck and an open-space living room with a glass wall giving everyone an at-tractive view of the sea. “With two departures

Phot

o: S

tena

Lin

e

6/2010 | Baltic Transport Journal | 1�

Maritime

per ship daily, we are talking about even 7,000 people travelling on this route every day, and we can facilitate everybody with all needs, in-cluding organizing conferences or even con-gresses,” says Niclas Mårtensson, Karlskrona-Gdynia route director. Stimulating passenger traffic is surely the main expected outcome, but modern facilities should not go without attention from the trucking sector. Ferry market observations show that whenever one introduces a modern ship, the line usually also experiences an increase in freight traffic. Of course, cargo will most likely continue as Karlskrona-Gdynia’s bread and butter from Monday to Thursday, just supported with an extra add up of leisure and holiday during the weekends. “Truckers are actually among the best customers of our onboard service, mak-ing wide use of shopping and entertainment,” states Marek Kiersnowski, Stena Line Pol-ska’s managing director. “Many drivers spend a significant part of their lives onboard ships, and we pay particular attention to the quality of their service,” tells Kiersnowski. Thus, there are modern truckers’ lounges at terminals in both ports. Each of the new ferries also has a dedicated restaurant and a truckers lounge room open 24/7. Each one of drivers cabins is equipped with a TV set and an Internet hot spot. The company also runs a special loy-alty programme for drivers that – besides the usual rewards – allows for a free leisure trip to take together with an accompanying guest. Stena Line also distinctly cares for the qual-ity of food service both for the usual passen-gers and the truckers, with the latter having each day a different menu that cannot repeat within a 10-day period. This allows people to drive to/from Scandinavia and back without repeating the same meal.

With the introduction of the first new unit right now, the route management will keep the same timetable and aims at resigning from two different schedules (the peak summer season and low winter season) after the implementa-tion of the second unit. A little exception to this rule will be short Christmas and Eastern holidays. “We trust that one full year sailing will be well appreciated by both passengers and freight customers,” finalizes Kiersnowski.

Boosting Sweden-Poland traffic

As Niclas Mårtensson puts it, the two new ships have the chance to create a unique com-bination of freight/passenger services on the Baltic – quite different to the ones in e.g. the Stockholm area, where you have many lines to numerous destinations, but all the ships (even those with space for 2-3,000 guests) offer max. 800 lm for cargo. Conversion works of the two units cost about EUR 32 mln, and a significant

part of this goes to creating an extra 400 lane metres of freight capacity to each ships. All formerly existing car decks are now dedicated exclusively to cargo, and a new passenger car deck was built in place of the removed 150 cab-ins. “The reason why we have undertaken this huge investment programme is that we still believe in the market, even though we do not expect a further freight boost on this route as we experienced this year,” reveals Mårtensson, at the same time expressing his belief in con-tinued growth of 6-10% in coming years. Any-way, this might be still more than the projected outcome of Danish or German markets (2-3% annual increase). His optimism refers much to the infrastructure improvements currently go-ing on in Poland. “The A1 highway in Poland that should be finished within 1.5 years will be-come an aorta for cargo flows from the Czech Republic, Slovakia and Hungary, and it will go directly up to our terminal in Gdynia,” he says. Meanwhile the new road should also be widely used in transit down to the Mediterranean and the Balkans by Swedish holiday makers. “We will be offering the quickest and most enter-taining way down to the continent, however, we see changing the Swedish travel habits as a real challenge,” Mårtensson points out. Defi-nitely, with the previously used vessels, the company didn’t have the right tools to grow on the Swedish tourist market. The most attrac-tive departures from Sweden were carried out by a cargo ship, which finally resulted in 70% of the passengers being Polish. Due to the lack of proper facilities, there have also been very few coach groups and cruising passengers. Mårtensson also believes in the rising share of unaccompanied trailers. It is still a very small percentage (currently four per cent of total volumes), but Stena Line expects a further

change in the freight pattern due to the visible trend of just-in-time deliveries and more trail-ers coming by rail to Karlskrona from main-land Sweden.

The new vessels are of maximum size that can call at Helskie Quay in Gdynia, so they are perfectly matched to today’s infrastruc-ture. However, even if the ferry terminal can serve 1,700 customers at once, getting to/from the city may soon become a bottleneck, not-withstanding if the city adds extra shuttle bus services or not. Before the crisis, the company was involved in serious talks with the port au-thority to build a new terminal, but the project has been postponed due to the fall in traffic. “It naturally depends on the market, but it’s likely that we will be in need of putting larger ships of 240 m on this route within the next five years,” comments Polish subsidiary managing director. Supposing things go well, this issue can soon step back on the agenda.

The company is also very serious about developing services in the central part of the Baltic. They purchased a majority of shares in Port of Karlskrona this year, and being so far its only customer – it also takes the burden of all the operating costs. Therefore, Stena Line wants to build up the critical mass in Karlskrona by strengthening its connection to Poland, and by starting up new services either themselves, or together with another operator. “Apart from our ships staying in the port, there are still 19 hours a day to fill up traffic and to help us transform Karlskrona into a transport and logistics centre for both freight and passengers,” invites Mårtensson, pointing to the East as the most interesting direction for potential network expansion. �

Piotr Trusiewicz

Stena Vision during its conversion from Stena Germanica in Gothenburg shipyard (October 2010)

Phot

o: P

iotr

Tru

siew

icz

1� | Baltic Transport Journal | 6/2010

Maritime

Striving for stabilityInterview with Søren Poulsgaard Jensen, COO Freight Based Network, Scandlines

Scandlines, one of Europe’s largest ferry companies, operates 17 vessels on nine of its own routes among 12 ports in the Baltic Sea. About the company’s plans and investments, we talk with a mem-ber of the management board of Scandlines Deutschland.

� You have been responsible for Scandlines’ freight services for one year now. What has changed in this area at the company during this time?

I think the crisis hit Scandlines in a very simi-lar way as occurred in other companies offer-ing transport solutions. The customers simply stopped trading with each other and we, as many others, saw a sharp drop in the volumes. We entered crisis management mode with savings rounds, etc., and are very happy that most economists do not believe in a double dip, so we can now concentrate on catching up. Generally, this year our focus has primarily been on creating route stability following a difficult and challenging 2009. Nevertheless, we have managed to launch a new route be-tween Travemünde and Ventspils/Liepaja in this period as well.

� And how is this line doing? Are you content with the volumes onboard?

Certainly, we are happy with the develop-ment. The transport to and from the Baltics is a market with a lot of competition and a hinterland that can be used for various op-tions. On this basis we are very content to see that our customers have received our ini-tiative well. During the crisis we saw the vol-umes on some of our Baltic routes drop by 50% within one year. This year we have seen it come back with 25-30%. In other words,

Phot

o: S

cand

lines

a great improvement measured on the huge loss of the year before. However, this devel-opment describes the BSR’s situation well – the market is not stable yet and the fluc-tuations are dramatic.

� Can you tell about your new investments in Rostock, Germany and Gedser, Denmark?

Scandlines is investing a total of EUR 230 mln in the expansion of the ports in Ros-tock and Gedser and two newbuildings. In Rostock a new berth will be rebuilt accord-ing to Scandlines’ specifications to be ready for the arrival of new ships in 2012. The cur-rent berth will be used as a backup, so that Scandlines will be ready for 4-ship opera-tion, if necessary. In Gedser harbour owned by Scandlines, we will invest EUR 43 mln in its expansion. A new terminal, check-in and marshalling area will be created there, amongst others.

� How do you think the Fehmarn Belt Fixed Link will affect your route net-work? Are there any plans for further modernization of the fleet, besides the Rostock-Gedser service?

We do not expect the bridge to be ready sooner than 2018, so it is 8-9 years from now, a lot can happen during this time. We are considering the continuation of our services on Puttgarden-Rødby, even when the fixed link is ready. We will of course have to adjust our business model to the circumstances, but there may actually still be demand for a ferry business parallel to the link. Our ships on the route will be amortized by 2018, so we will be able to operate at low costs. Nevertheless, we are preparing for a shift in our business, and the newbuildings we just ordered are a sign of that. The Eastern Corridor is becoming more and more important and we will be focusing a lot on developing Gedser-Ros-tock. We are hoping to have hourly depar-tures on this route, we might even operate with four ships in the future.

� Does Scandlines have any plans to add new ro-ro services towards Russia? Do you consider this country a promising market for these services? What do you think about the privatization of Polfer-ries (PŻB)?

We have no current plans towards Russia, but there is no doubt that any Baltic op-erator will always have to keep the Russian market in mind. There has been a huge im-provement over the last decade in Russian ports when it comes to container handling. I worked in Moscow from 2000 to 2004 and when I started there, Riga was by far the most important container hub for Rus-sia. Within two years the traffic migrated to St. Petersburg because that was the strategy from the political side, and business as well as the authorities responded to the call. The entire nature of the ro-ro segment is to get the vessels in turning as quickly as possible, allowing a fast cargo flow. The procedures in Russia today have not yet reached the level that calls for this traffic to find a natu-ral way directly into the Russian market. That will, however, change at some point and all Baltic operators need to keep an eye on Russia when that happens. Regarding Polferries, I can only say that, in general, competing in ferry shipping with state-sup-ported companies as a private operator is unhealthy.

� Today, there are 15 ferry and seven ro-ro operators with regular open freight services on the Baltic (not mentioning car carriers and dedicated industrial shipping that are opening up in the mar-ket). Do you think that the network is already dense enough?

It is hard to say. One can argue that the cur-rent threatening legislation on sulphur emis-sion may potentially create a disturbance in the availability of ferry services, so I hope our politicians are keeping a keen eye on that. �

Lena Lorenc, Marek Błuś

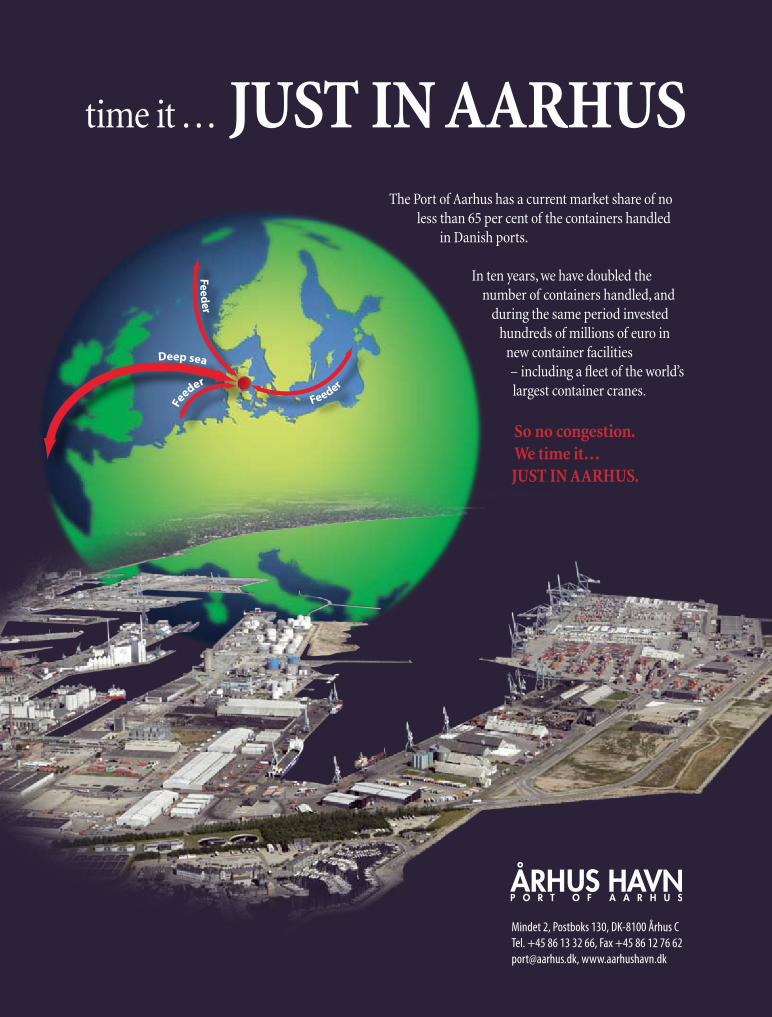

time it . . . JUST IN AARHUSThe Port of Aarhus has a current market share of no

less than 65 per cent of the containers handled in Danish ports.

In ten years, we have doubled the number of containers handled, and

during the same period invested hundreds of millions of euro in

new container facilities – including a fleet of the world’s largest container cranes.

So no congestion. We time it… JUST IN AARHUS.

Mindet 2, Postboks 130, DK-8100 Århus CTel. +45 86 13 32 66, Fax +45 86 12 76 [email protected], www.aarhushavn.dk

Deep sea

Feeder

Feeder

Fe

eder

1� | Baltic Transport Journal | 6/2010

Maritime

Economic cornerstones of the regionInvestments in Bremen and Bremerhaven

The ports of Bremen and Bremerhaven play a major role in the local and national economy of Germany. Today about 86,000 jobs are directly or indirectly related to them.

Ports and foreign trade have estab-lished the economic base of the Free Hanseatic City of Bremen since the 9th century. The con-stitution of the State of Bremen, therefore, includes provisions

prescribing the construction and maintenance of modern ports and the pursuit and ongoing development of shipping and trade, for the ben-efit of Bremen, Germany and Europe.

The Ports of Bremen nowadays consist of two port complexes located at the river Weser: the City-port of Bremen and the Port of Bremer-haven. The key feature of the twin ports is their universal function and their distinctive division of labour. While Bremerhaven, located only 32 nautical miles from the open sea, specialises in handling container vessels, car carriers and fruit reefer ships, the terminals in Bremen, located 60 km further to the south, concentrate on bulk, general and heavy-lift cargo.

Containers have been the major driving force of growth for the Ports of Bremen over the last 40 years. The quay beside the river We-ser at Container Terminal “Wilhelm Kaisen” is the backbone of the port and can accommodate the world’s largest container ships. Since its early beginning in 1968, Container Terminal Bremer-haven has passed through a continuous process of expansion and upgrading. With the comple-tion of Container Terminal 4 at the end of 2008,

Map

: Bre

men

port

s

Bremerhaven offers a total quay length of almost five kilometres including 14 purpose-built berths for mega-container vessels and more than 300 hectares of operating area and storage space. Three independent companies, NTB, Eurogate and MSC-Gate, operate the terminal facilities.

Organization

The remit of the harbour master, such as ship-ping traffic control and other sovereign tasks, is the responsibility of the public port authority “Hansestadt Bremisches Hafenamt”. In 2002 the responsibility for construction work, maintenance, operational management and marketing of the ports was transferred to Bremenports, a company founded under private law. Bremenports, a private company whose prime responsibilities are port construction and port expansion projects. The city is the owner of the infrastructure and hence responsible for building and maintenance costs. The superstructure, however, is owned and main-tained by private companies. On behalf of the Free Hanseatic City of Bremen, Bremenports leases out operation areas to private companies.

The driving forces

The Ports of Bremen and Bremerhaven are one of Europe’s most important centres for cargo handling, transportation and logistics, playing an

important role especially for the Baltic Sea and Scandinavia. Ranked behind Rotterdam, Ant-werp and Hamburg, Bremerhaven is the fourth largest container port in Europe. As one of the world’s most important automobile transhipment locations, Bremerhaven can accommodate almost 125,000 vehicles. Nearly half of the parking ca-pacity is protected in high-bay warehouses. Cur-rently, there are 12 berths available for loading and discharging vessels specialised in the transport of automobiles and other rolling cargo. The technical centres, covering 300,000 m2 and called “Europe’s biggest car workshop”, offer a wide range of pre-delivery services, like depreservation and car-wash plants, finishing booths and numerous car lifts.

Bremen is also the birthplace of cargo vil-lages – GVZ Bremen was established already in 1985 and is now a recognized leader within the league of cargo villages. It offers 496 hectares of intermodular, highly synergized solutions for all requirements of logistics services and production. 150 companies with a total workforce of 8,000 are located in the cargo village of Bremen.

Infrastructure and future investments

In competition with other European seaports, a strong position in the automobile handling and logistics sector can be secured only by continu-ously adapting the port infra- and superstructure. Having evaluated various scenarios, the Senate of

6/2010 | Baltic Transport Journal | 1�

Maritime

Bremen decided to improve seaward access by building a new lock replacing the old Kaiser-Lock, a permanent bottleneck since 1897. Its insufficient dimensions as well as increasingly frequent dis-ruptions and repairs have disturbed traffic. Con-struction works began in November 2007 and the new lock will be inaugurated in April 2011.

The seaward approach to Bremerhaven from the North Sea is the so-called Outer Weser. In order to improve accessibility for large container vessels, the Free Hanseatic City of Bremen ad-vocates the deepening of the Outer Weser navi-gation channel. The river itself is classified as a federal tidal waterway and is not yet navigable by fully loaded Ultra-Large Container Ships (ULCS) independent of tides. The aim of the projected adjustment of the Outer Weser is to provide non-tidal access to Container Terminal Bremerhaven for ULCSs with a maximum loaded draught of 13.5 m. This is equivalent to a future load factor of 93% of a design draught of 14.5 m in S-Class ships. Dredging works are expected in 2011 and will be accompanied by another project expand-ing Lower Weser. Both projects represent de-mand-driven adjustments of the river and prom-ise a significant improvement in the seaward accessibility of Bremerhaven and Bremen.

In view of future container turnover and the growing size of container vessels in leaps and bounds, the Senate of Bremen decided to