eu 11 r egular e conomic r eport m acroeconomic r eport : f ocus on c roatia

TRANSCRIPT

EU11 REGULAR ECONOMIC

REPORT

MACROECONOMIC REPORT:

FOCUS ON CROATIA

Entering the fifth year of recession

Croatia: Quarterly GDP growth, y/y

EU 11 and EU15: GDP growth, y/y

Source: Eurostat, CROSTAT, World Bank staff calculations

Deteriorating Labor Market Conditions

Sour labor market developments, Croatia, in % Less opportunities (or incentives) even in the informal sector

Source: CROSTAT, World Bank staff calculations

External Debt (% of GDP) CAD and Net FDI (% of GDP)

External Position Slightly Improved External debt although high, shrank slightly due

to bank deleveraging – some 20 pp of GDP above EU11

CAD turned positive in Q4 2012 while net FDI inflow improved

Source: CNB, CROSTAT, World Bank staff calculations

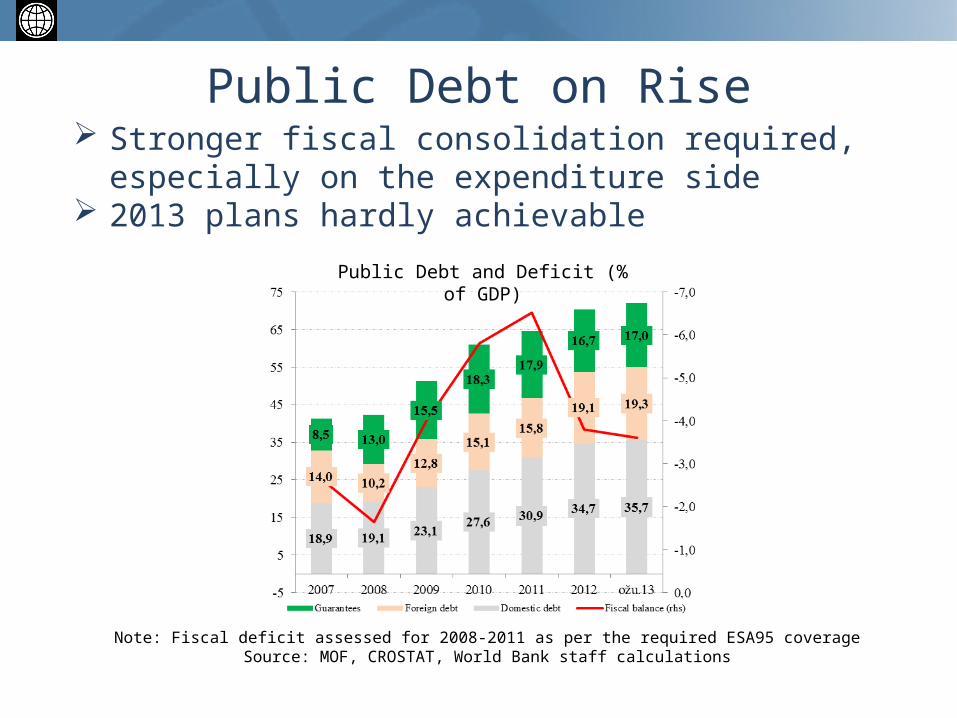

Public Debt and Deficit (% of GDP)

Public Debt on Rise Stronger fiscal consolidation required,

especially on the expenditure side 2013 plans hardly achievable

Note: Fiscal deficit assessed for 2008-2011 as per the required ESA95 coverageSource: MOF, CROSTAT, World Bank staff calculations

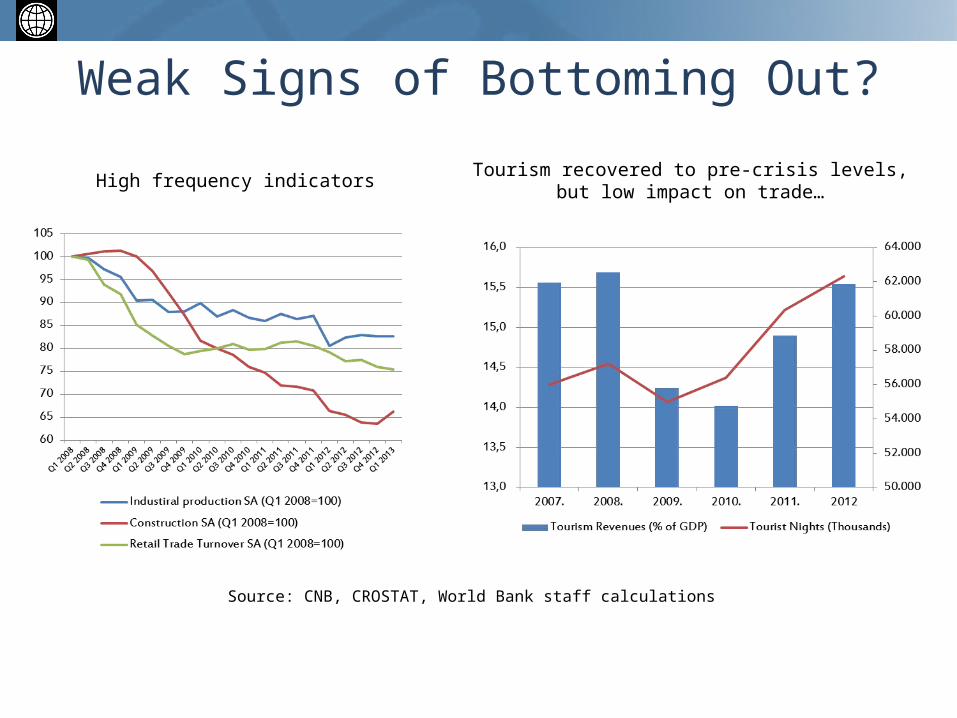

Weak Signs of Bottoming Out?

Tourism recovered to pre-crisis levels, but low impact on trade…

High frequency indicators

Source: CNB, CROSTAT, World Bank staff calculations

Some Softening of the Labor Market

Source: CROSTAT, HZZ, World Bank staff calculations

However, Structural Problems Deepened

Labor market entry for youth particularly constrained

Source: CROSTAT, HZZ, World Bank staff calculations

Job destruction in industry continued; public sector employment dominated

Reform agenda – seizing opportunities

84th in the World Bank’s Doing Business rankings or 81st on the Global Competitiveness rankings

Challenging competition after July 1 with many of the world’s best nations for doing business.

What To Do – Fiscal Consolidation

10

Need to regain the investment credit rating before the capital market deteriorates (again) Interest payments at 3% of GDP already at the

capital spending level Expenditure-based consolidation remains a priority

– public spending at around 45% of GDP as opposed to 40% of GDP of EU10

Fiscal space exists in the area of the wage bill, subsidies and consumption

Social spending requires redistribution from categorical to targeted social programs and a separation from contribution-based benefits from categorical benefits

Capital spending needs to be EU-funded and to take into consideration future maintenance cost

What To Do – Investment Climate

11Disclosure

Time/Cost

• Strengthen the business environment in the areas of: insolvency proceedings; issuance of construction permits; registering property; and transparency of related-party transactions.

• Open up the network industries such as energy, railways, postal services and telecoms to competition to deliver better services at better prices for business and citizens.

• Deepen the governance reform in the areas of: e-governance, performance-based public sector pay; territorial reorganization; review business necessity of quasi-fiscal institutions

Source: World Bank

What To Do – Labor Market and Social Sectors

12

Demand and supply side issues, no quick wins: EPL still highly rigid in stimulating employment and

accelerating restructuring Skill mismatches Low labor participationWhich reforms:

Increasing hiring flexibility (a good set of proposals submitted by the government)

Reducing rigidity of collective firing Improving VET education and providing incentives for LLL Reducing incentives for early retirement, consolidating social

benefits and improving their targeting

What To Do - EU Funds

13

• July 1, 2013 Croatia Becomes 28th EU Member State• EU Structural Funds:

– 1.2% of GDP available for absorption in 2013 or 0.8% of GDP in payments.

– Around 3.5% of GDP per year over the next programming period in commitments

– Ease the external balance position and improve debt sustainability

What needs to be done? Create fiscal space in the order of 1 percent of GDP per year as

counterpart funds and for pre-financing Develop sector and regional development strategies linked to

sustainable fiscal frameworks

Thank you

www.worldbank.hr

14