ethics for the tennessee cpa mark h. crocker, cpa, cgma executive director, tennessee state board of...

TRANSCRIPT

Ethics for the Tennessee CPA

• Mark H. Crocker, CPA, CGMAExecutive Director, Tennessee State Board of Accountancy

• Don Mills, CPA, CFETNSBA Investigator

• Ray Butler, CPATNSBA Investigator

20 Questions

• Where did these 20 questions come from?• Attendees at our previous seminars• Calls from our licensees• Problem areas in compliance

What is “the Board”?

• Eleven Members – Appointed by Governor• Serve Terms of 3 Years• Nine are CPAs• One is Attorney• One is Public Member• Meets Quarterly- usually in January, May, July

and October

Current Members of the Board

• Trey Watkins, CPA, Chairman – Memphis

• Casey Stuart, CPA, Vice Chair – Chattanooga

• William Blaufuss, CPA, Sec. – Nashville

• Henry Hoss, CPA – Chattanooga• Stephen Eldridge, CPA – Jackson• Vic Alexander, CPA - Nashville

• Troy Brewer, CPA – Nashville• Stan Sawyer, CPA – Memphis• Don Royston, CPA – Kingsport• Jennifer Brundige, JD –

Nashville, Public Member• John Roberts, Attorney-at-Law –

Nashville, Attorney Member

Administrative Support Staff

• Executive Director – Mark H. Crocker, CPA, CGMA • Investigator – Don Mills, CPA, CFE• Investigator – Ray Butler, CPA• Advisory Attorney – Chris Whittaker, Esq.• Education Coordinator – Kathy Riggs, Ph.D.• Licensing Coordinator – Brenda Demastus• Disciplinary Coordinator – Karen Condon• Office Manager – Patricia Turner• Admin. Assistant – Sandy Cooper

Function of Administrative Office

• Initial Licensing (testing and reciprocity)• Renewing Licenses• Updating Files• Assisting Licensees & Public• Investigation of Complaints• Education• Provide Assistance to Board Members

How many CPAs are there in Tennessee?

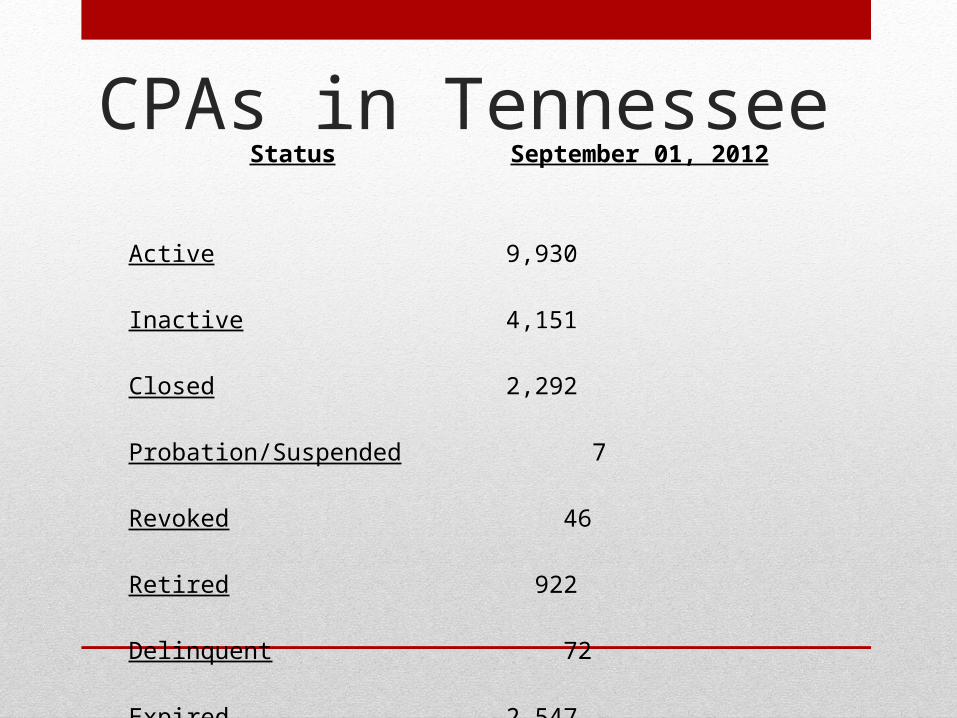

CPAs in Tennessee Status September 01, 2012

Active 9,930

Inactive 4,151

Closed 2,292

Probation/Suspended 7

Revoked 46

Retired 922

Delinquent 72

Expired 2,547

Deceased 2,478

Other 434

Total Licenses 22,879

Tennessee State Board of Accountancy

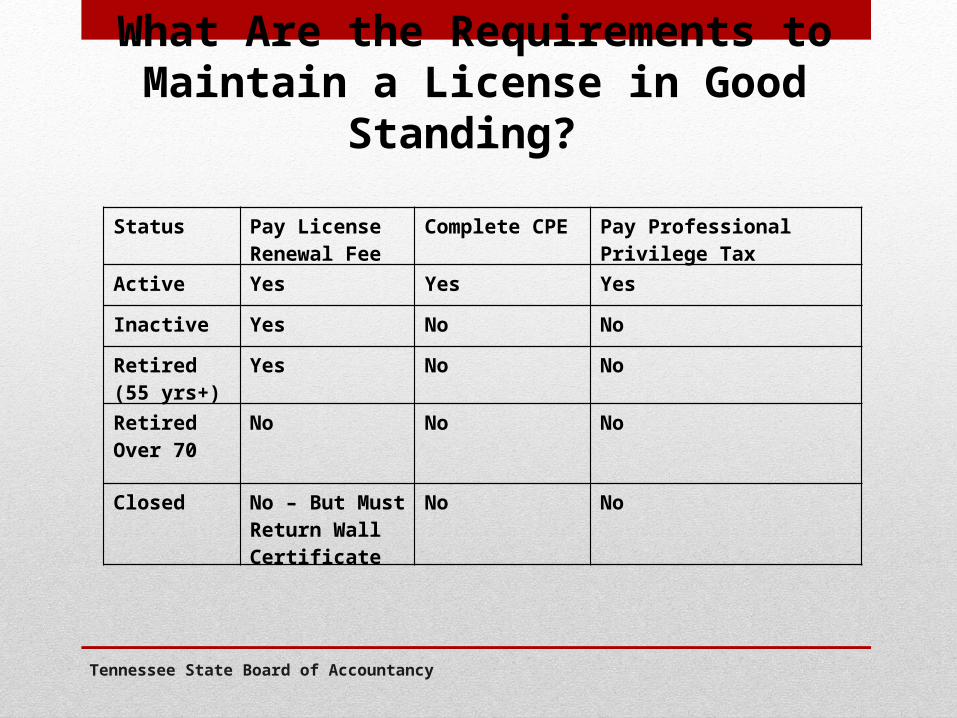

What Are the Requirements to Maintain a License in Good Standing?

Status Pay License Renewal Fee

Complete CPE Pay Professional Privilege Tax

Active Yes Yes Yes

Inactive Yes No No

Retired(55 yrs+)

Yes No No

Retired Over 70

No No No

Closed No – But Must Return Wall Certificate

No No

Tennessee State Board of Accountancy

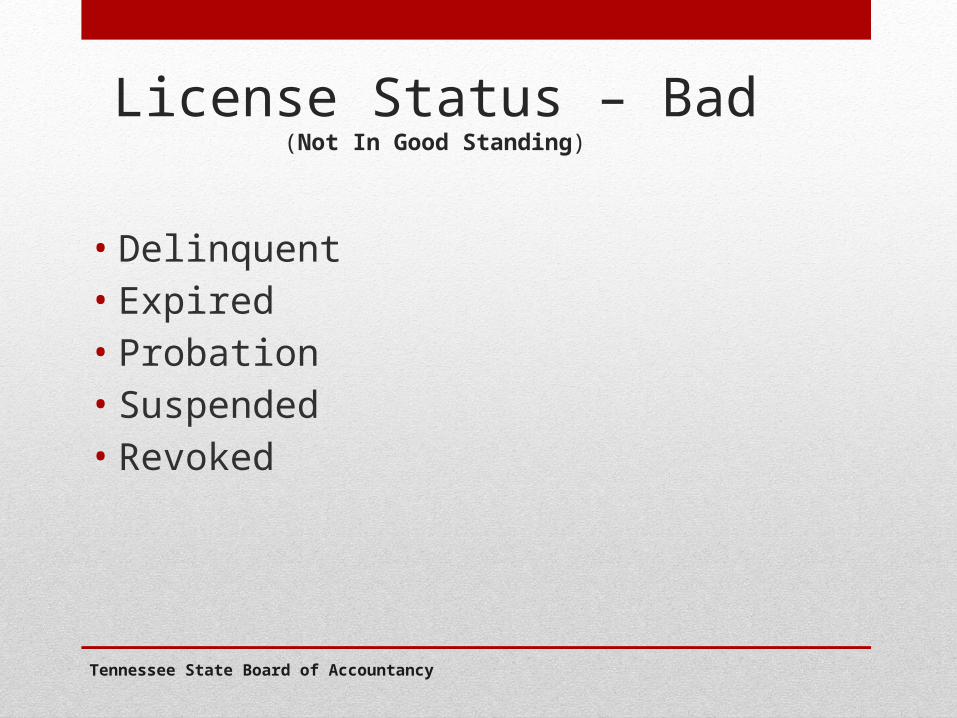

License Status – Bad(Not In Good Standing)

• Delinquent• Expired• Probation• Suspended• Revoked

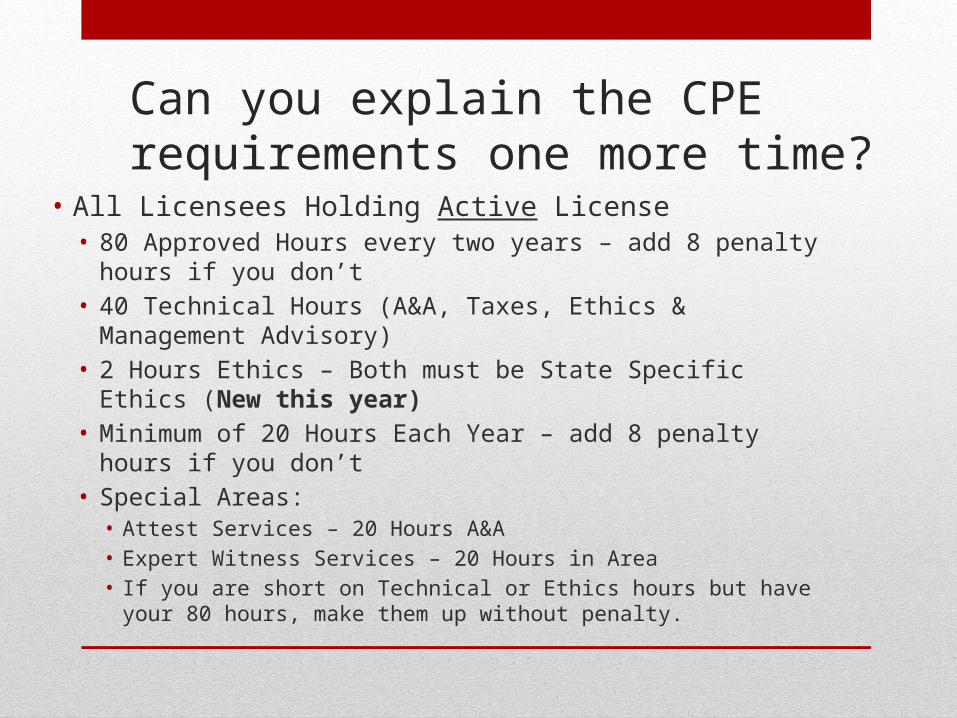

Can you explain the CPE requirements one more time?

• All Licensees Holding Active License• 80 Approved Hours every two years – add 8 penalty hours if you

don’t• 40 Technical Hours (A&A, Taxes, Ethics & Management Advisory)• 2 Hours Ethics – Both must be State Specific Ethics (New this

year)• Minimum of 20 Hours Each Year – add 8 penalty hours if you don’t• Special Areas:

• Attest Services – 20 Hours A&A• Expert Witness Services – 20 Hours in Area• If you are short on Technical or Ethics hours but have your 80 hours, make

them up without penalty.

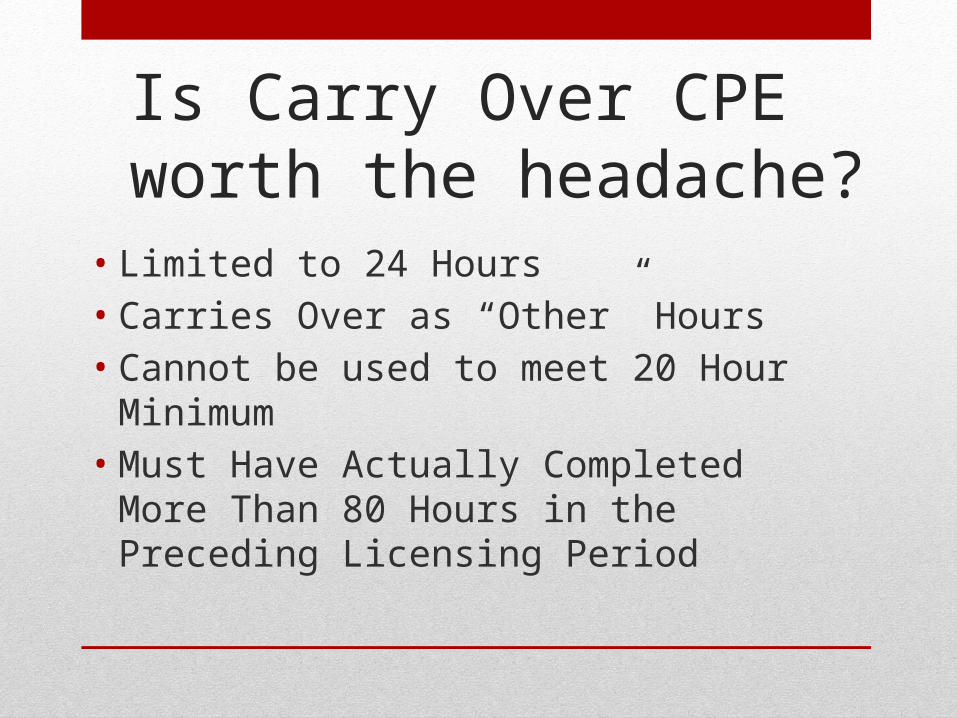

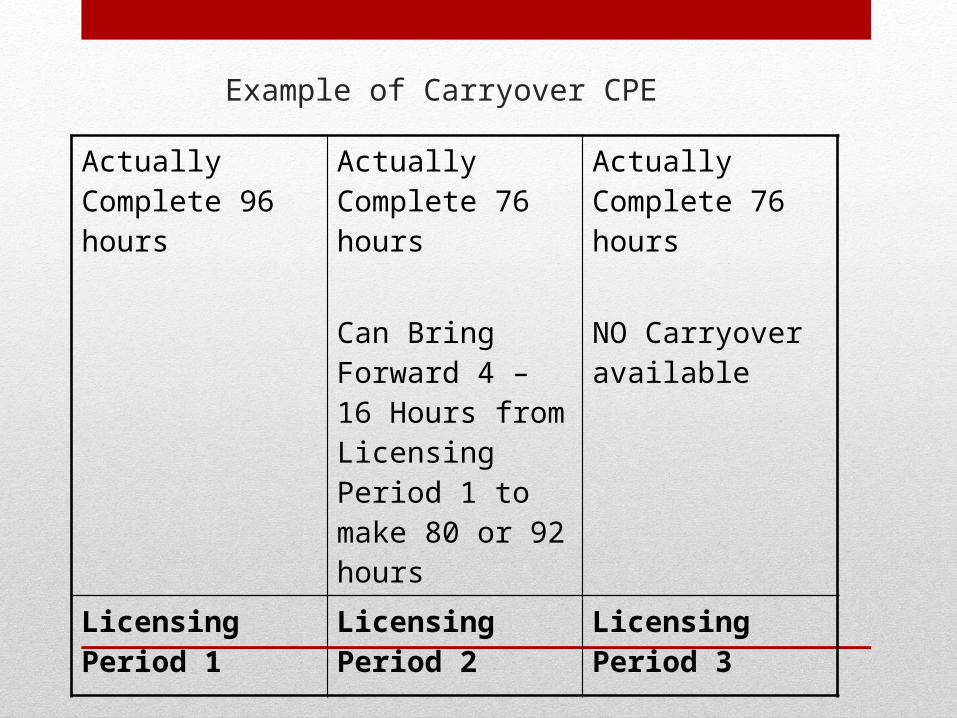

Is Carry Over CPE worth the headache?

• Limited to 24 Hours• Carries Over as “Other” Hours• Cannot be used to meet 20 Hour Minimum• Must Have Actually Completed More Than 80

Hours in the Preceding Licensing Period

Example of Carryover CPE

Actually Complete 96 hours

Actually Complete 76 hours

Can Bring Forward 4 – 16 Hours from Licensing Period 1 to make 80 or 92 hours

Actually Complete 76 hours

NO Carryover available

Licensing Period 1

Licensing Period 2

Licensing Period 3

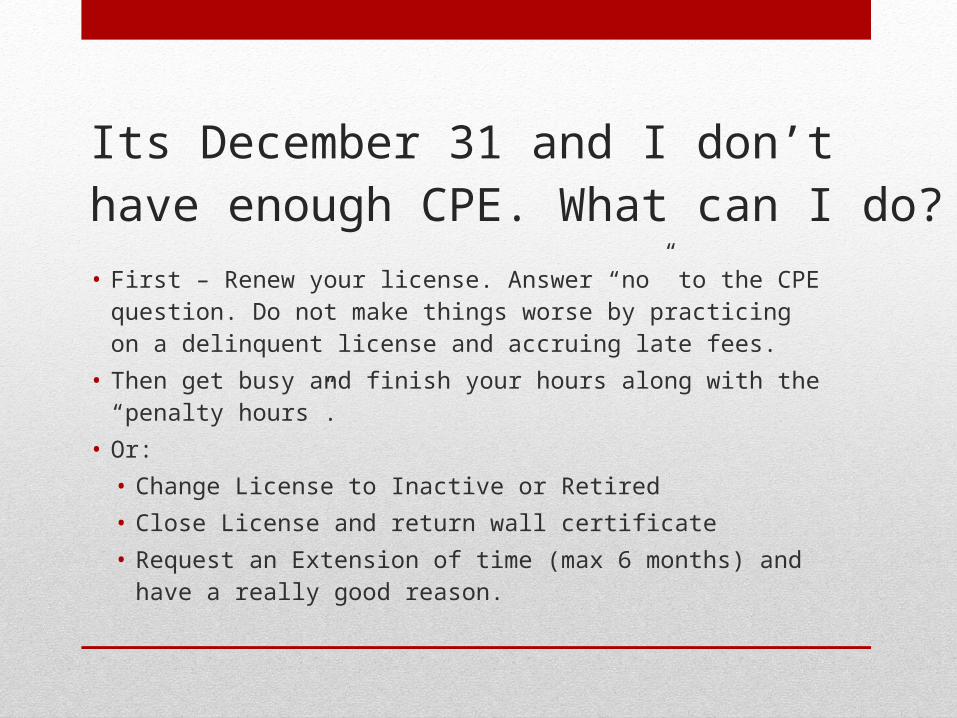

Its December 31 and I don’t have enough CPE. What can I do?• First – Renew your license. Answer “no” to the CPE

question. Do not make things worse by practicing on a delinquent license and accruing late fees.

• Then get busy and finish your hours along with the “penalty hours”.

• Or:• Change License to Inactive or Retired• Close License and return wall certificate• Request an Extension of time (max 6 months) and have

a really good reason.

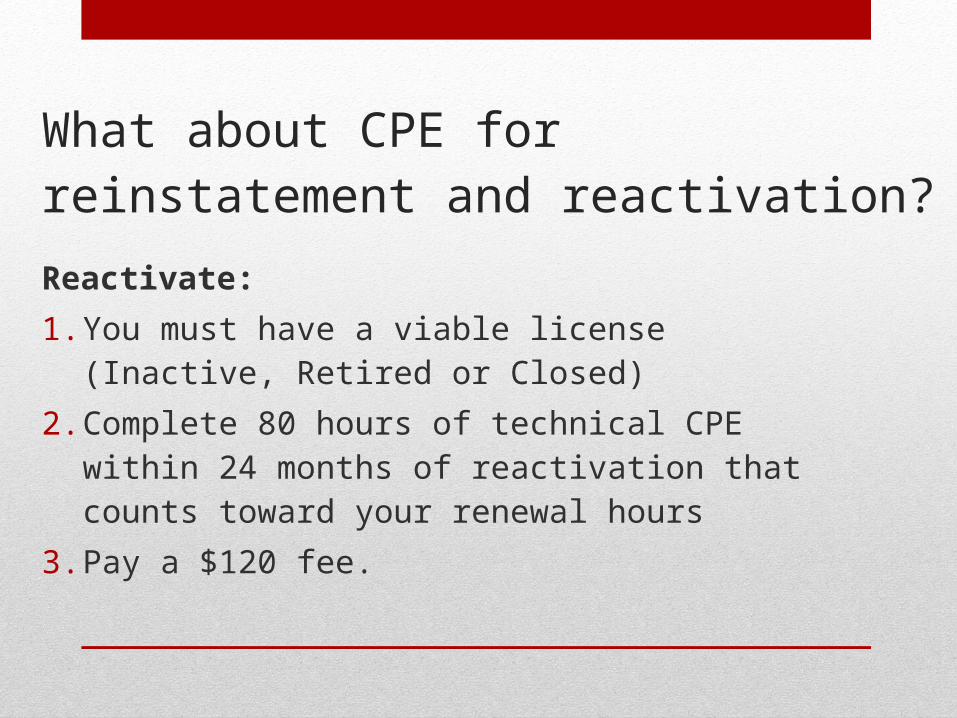

What about CPE for reinstatement and reactivation?Reactivate:

1. You must have a viable license (Inactive, Retired or Closed)

2. Complete 80 hours of technical CPE within 24 months of reactivation that counts toward your renewal hours

3. Pay a $120 fee.

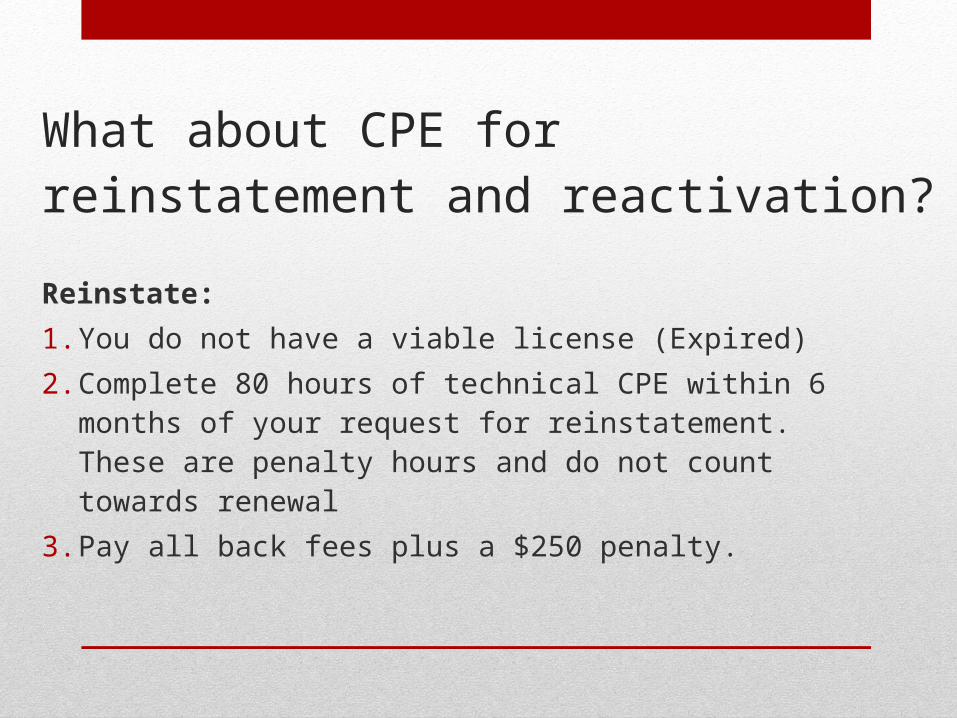

What about CPE for reinstatement and reactivation?Reinstate:

1. You do not have a viable license (Expired)

2. Complete 80 hours of technical CPE within 6 months of your request for reinstatement. These are penalty hours and do not count towards renewal

3. Pay all back fees plus a $250 penalty.

Any other rule changes I need to know about?1. Penalty for Late Renewal of License – Changed from two

$50 penalties applied in February and April to one $100 penalty applied in February.

2. Address Change – New rule requires notification to the Board of any changes in email address within 30 days.

3. Education- If you were not approved to sit for the exam on 6/24/12, you must now complete 30 semester hours accounting education and 24 of those hours must be in upper division accounting courses.

I have a large client…

who calls and asks if I know anything about a CPA from Nevada who has applied for a position with the corporation. Is there any way I can help?

Go online to CPAverify.org, maintained by the NASBA. It contains licensee information from 31 states and Puerto Rico. It will tell you if the individual is properly licensed and, in some cases, if that person has been disciplined by their respective board.

Now call your client and earn some brownie points.

How Long Must I Keep My Working Papers?

A firm issues an audit report on an entity for the fiscal year ended June 30, 2009. The auditors’ report is dated October 15, 2009. The Board requires that working papers be kept for five years after the period in which the report is issued.

How Long Must I Keep My Working Papers?

Answer: In this case, the period in which the audit report was issued is June 30, 2010. The working papers must be retained until July 1, 2015.

I have this friend…

who works for a private corporation and does a few tax returns on the side. Does he have to open a firm?

“YES”

• If you are a licensed CPA in the state and you provide accounting services – you must be affiliated with a CPA firm.

• Definition of accounting services:• Tax return preparation• Attest services• Any other services in which you hold out as a CPA

I work in private industry but volunteer my time …

at a nonprofit agency where I perform basic bookkeeping services. I do not prepare financial statements. Do I need a firm permit?

No – as long as the licensee does not make management decisions for the agency.

I work at home and only do bookkeeping for a limited number of clients. Do I need a firm permit?

1. Do your bookkeeping services consist of more than:• Recording transactions to the client’s

general ledger which have been coded by management.

• Posting client approved entries to the trial balance.

• Preparation of reconciliations for bank accounts, accounts receivable, etc.

2. Do your clients know that you are a CPA?

If you answered “yes” to these questions – you need a firm permit.

$50

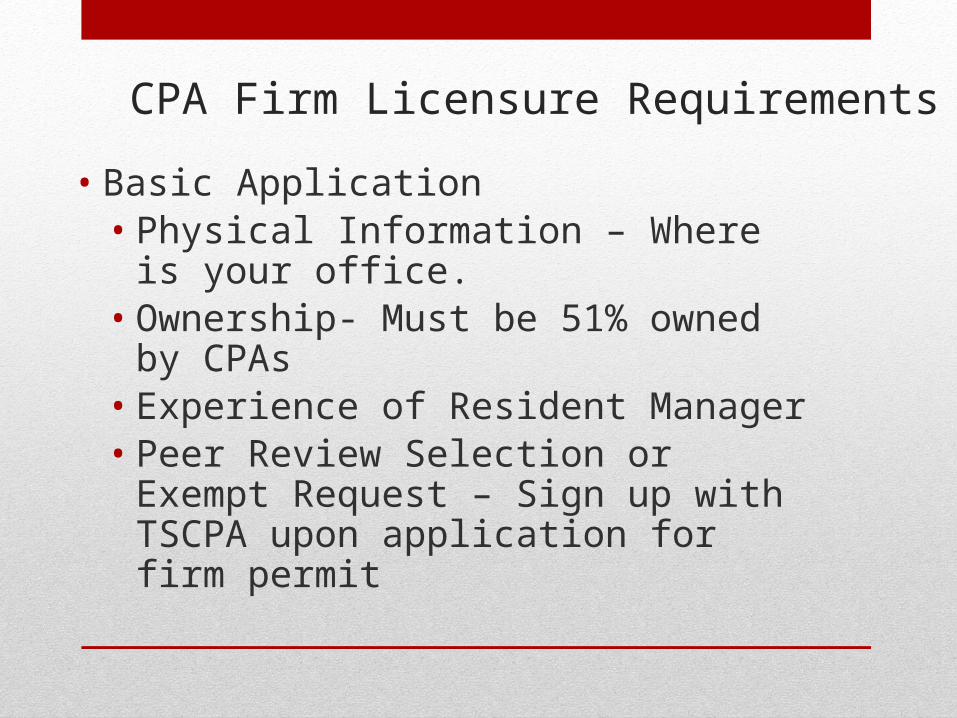

CPA Firm Licensure Requirements

• Basic Application• Physical Information – Where is your office.• Ownership- Must be 51% owned by CPAs• Experience of Resident Manager• Peer Review Selection or Exempt Request –

Sign up with TSCPA upon application for firm permit

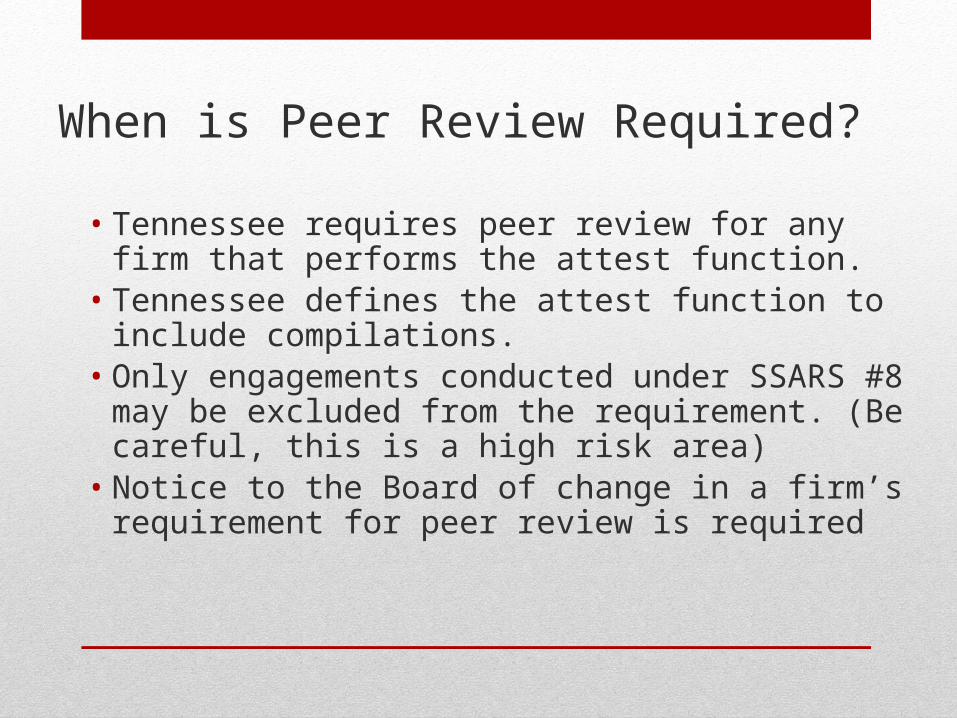

When is Peer Review Required?

• Tennessee requires peer review for any firm that performs the attest function.

• Tennessee defines the attest function to include compilations.

• Only engagements conducted under SSARS #8 may be excluded from the requirement. (Be careful, this is a high risk area)

• Notice to the Board of change in a firm’s requirement for peer review is required

If I prepare “management-use-only” financial statements for my clients:

1. What kind of report do I put on it?2. Can I avoid peer review?

1. A management-use-only compilation is issued without a report when a CPA does not reasonably expect the financial statements to be used by a third party. Instead, document an understanding with the entity through the use of an engagement letter, preferably signed by management.

2. Since financial statements compiled for management’s use only do not include a report, they are theoretically outside the purview of peer review.

How many complaints does the Board receive in a year?

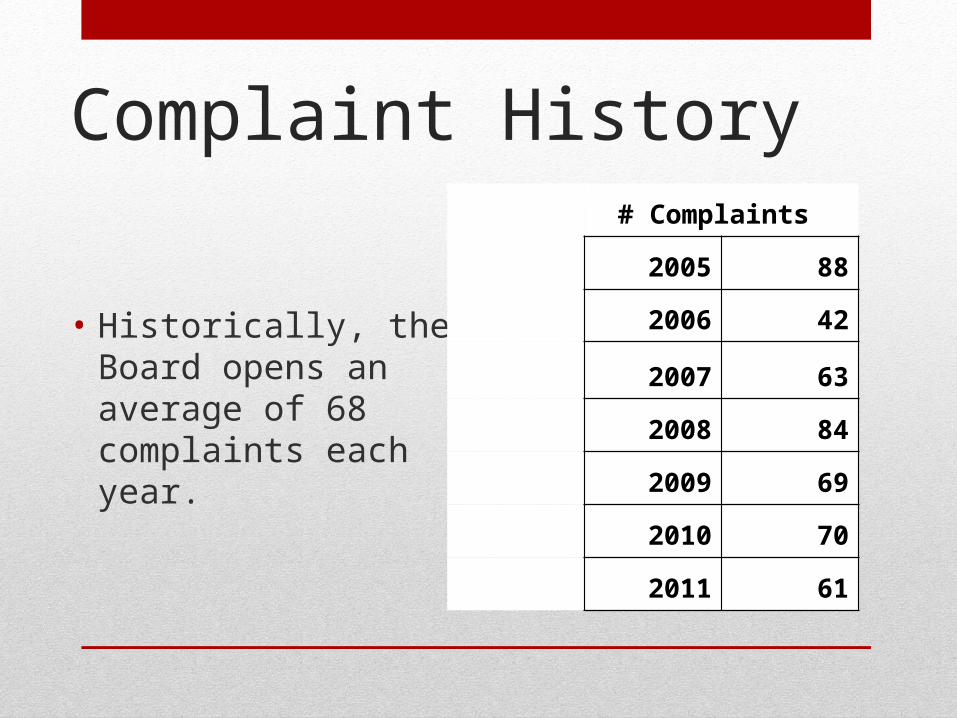

Complaint History

• Historically, the Board opens an average of 68 complaints each year.

# Complaints

2005 88

2006 42

2007 63

2008 84

2009 69

2010 70

2011 61

Who files a complaint?

• Licensees • Your (former) clients• The Board• State and Federal Agencies

As a Licensee, am I required to notify the Board of others who may be violating the law and rules of our profession?

Rule 0020-4-.03 (2)(d) states in part:Conduct reflecting adversely upon the licensee’s fitness to perform services includes…concealment of information regarding violations by other licensees of the Act or the Rules….

What is the #1 question asked by CPAs during a complaint investigation?

Are you going to make me take the exam again?

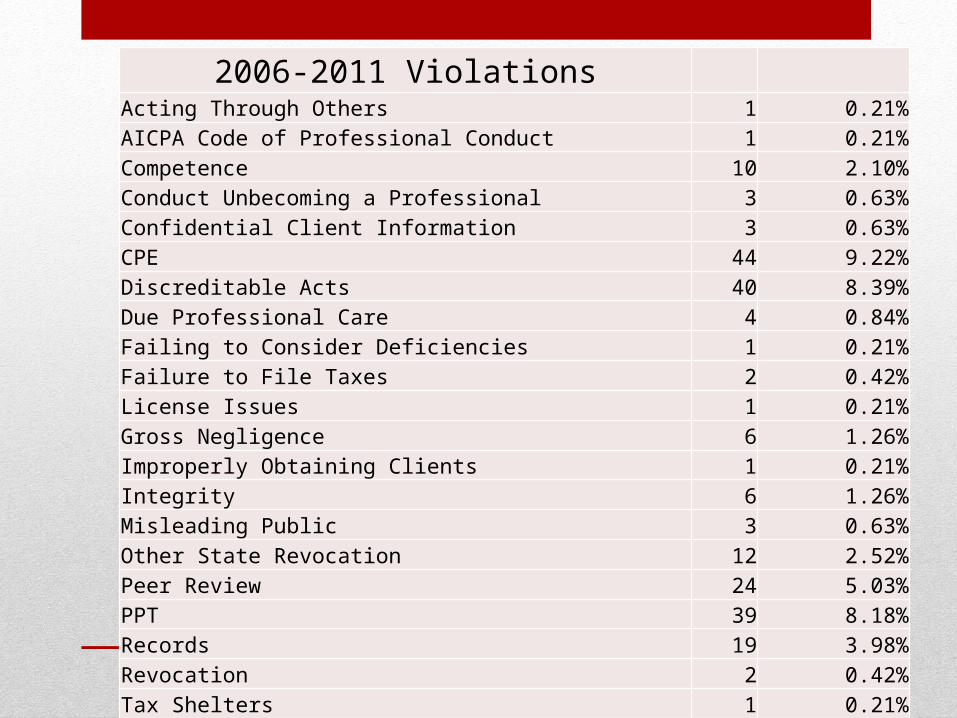

What are the most common complaints received by the Board?

2006-2011 Violations Acting Through Others 1 0.21%AICPA Code of Professional Conduct 1 0.21%Competence 10 2.10%Conduct Unbecoming a Professional 3 0.63%Confidential Client Information 3 0.63%CPE 44 9.22%Discreditable Acts 40 8.39%Due Professional Care 4 0.84%Failing to Consider Deficiencies 1 0.21%Failure to File Taxes 2 0.42%License Issues 1 0.21%Gross Negligence 6 1.26%Improperly Obtaining Clients 1 0.21%Integrity 6 1.26%Misleading Public 3 0.63%Other State Revocation 12 2.52%Peer Review 24 5.03%PPT 39 8.18%Records 19 3.98%Revocation 2 0.42%Tax Shelters 1 0.21%Unlicensed Practice 162 33.96%Violation of Consent Order 4 0.84%

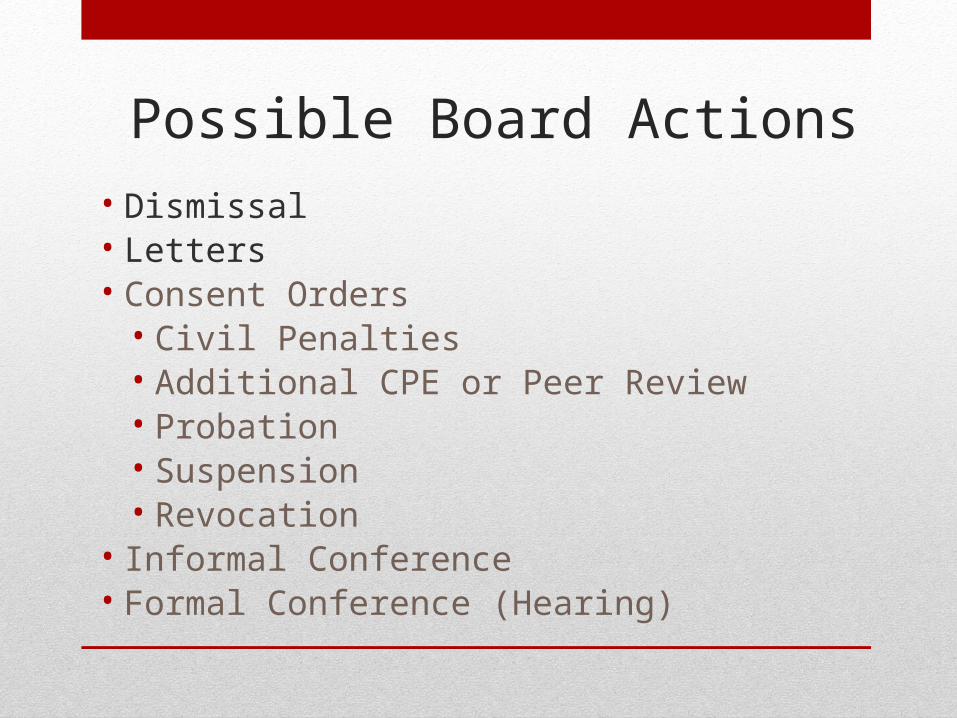

What actions can the Board take concerning a complaint?

Possible Board Actions • Dismissal• Letters• Consent Orders

• Civil Penalties• Additional CPE or Peer Review• Probation • Suspension• Revocation

• Informal Conference• Formal Conference (Hearing)

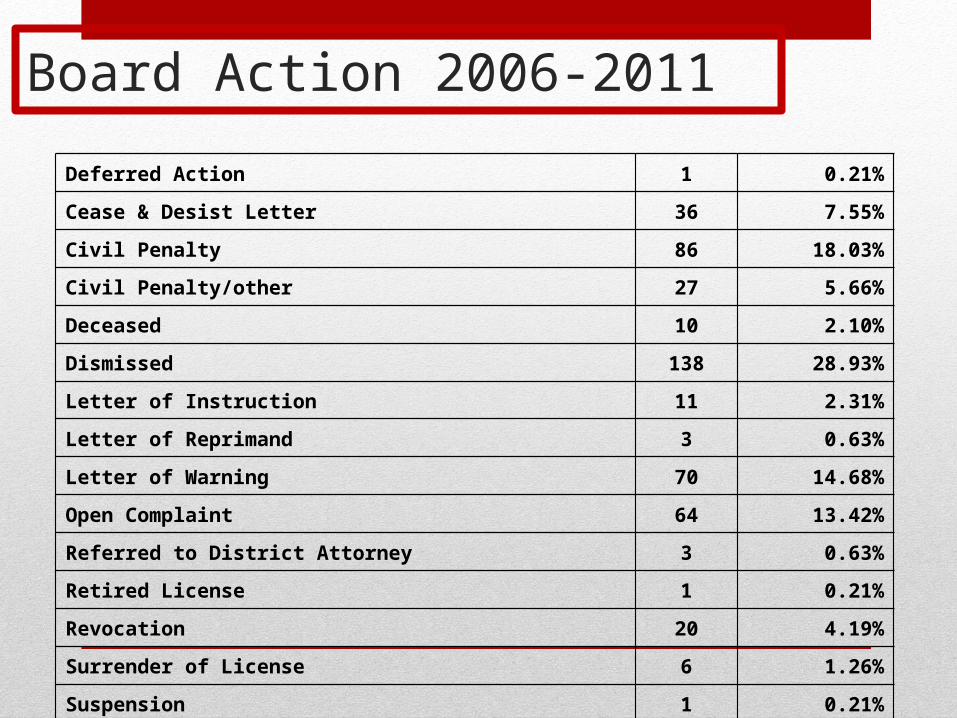

Board Action 2006-2011

Deferred Action 1 0.21%

Cease & Desist Letter 36 7.55%

Civil Penalty 86 18.03%

Civil Penalty/other 27 5.66%

Deceased 10 2.10%

Dismissed 138 28.93%

Letter of Instruction 11 2.31%

Letter of Reprimand 3 0.63%

Letter of Warning 70 14.68%

Open Complaint 64 13.42%

Referred to District Attorney 3 0.63%

Retired License 1 0.21%

Revocation 20 4.19%

Surrender of License 6 1.26%

Suspension 1 0.21%

What is the difference between tax avoidance and tax evasion?

JAIL

Can you explain mobility?

Case Study:A firm is contracted to perform the independent audit of a Tennessee municipality. The firm is licensed in good standing with the State of Mississippi, but not in Tennessee. A review of the audit reveals apparent failures to meet the fieldwork standards required by the “Yellow Book” and a complaint against the firm is initiated by the Tennessee Board.

Mobility-doing bad work in TennesseeCase Study:

In its response to the complaint, the firm asserts that the Tennessee Board has no jurisdiction to impose disciplinary action on a Mississippi firm and that any action against the firm must be taken by the Mississippi Board of Accountancy.

Mobility-doing bad work in Tennessee

Tennessee Code Annotated, Section 62-1-117 allows an individual from another state with a valid license to practice in Tennessee with no notice to the Board; however, it requires that:

“An individual licensee of another state exercising the privilege under this chapter shall consent to the personal and subject matter jurisdiction and disciplinary authority of the board….”

Mobility-doing bad work in Tennessee

Disposition:The Board’s investigation revealed a failure to follow professional standards. The complaint was settled via Consent Order signed by the firm acknowledging the failure and agreeing to a probationary period of two years and a civil penalty of $2,000.

In addition, the Tennessee Board notified the Mississippi Board of the action taken.

Mobility-firm previously licensed in Tennessee

Case Study #2:A North Carolina firm is hired to perform the independent audit of a Knoxville nonprofit agency. The firm was previously licensed in Tennessee, but closed that firm permit prior to beginning the audit. A Tennessee firm filed a complaint against the firm, alleging that the Carolina firm could not practice in Tennessee.

Mobility-firm previously licensed in Tennessee

Disposition:The North Carolina firm met the requirements to practice in Tennessee and the complaint was dismissed.

Mobility-firm previously licensed in Tennessee

What if?The North Carolina firm hired to perform the audit had an expired firm permit in Tennessee?

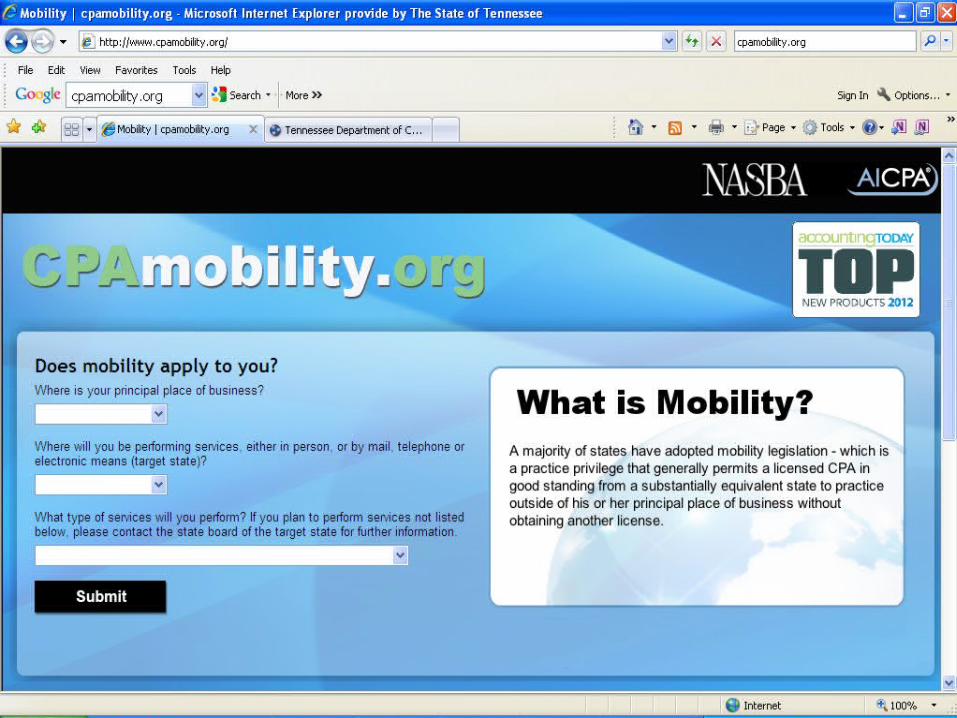

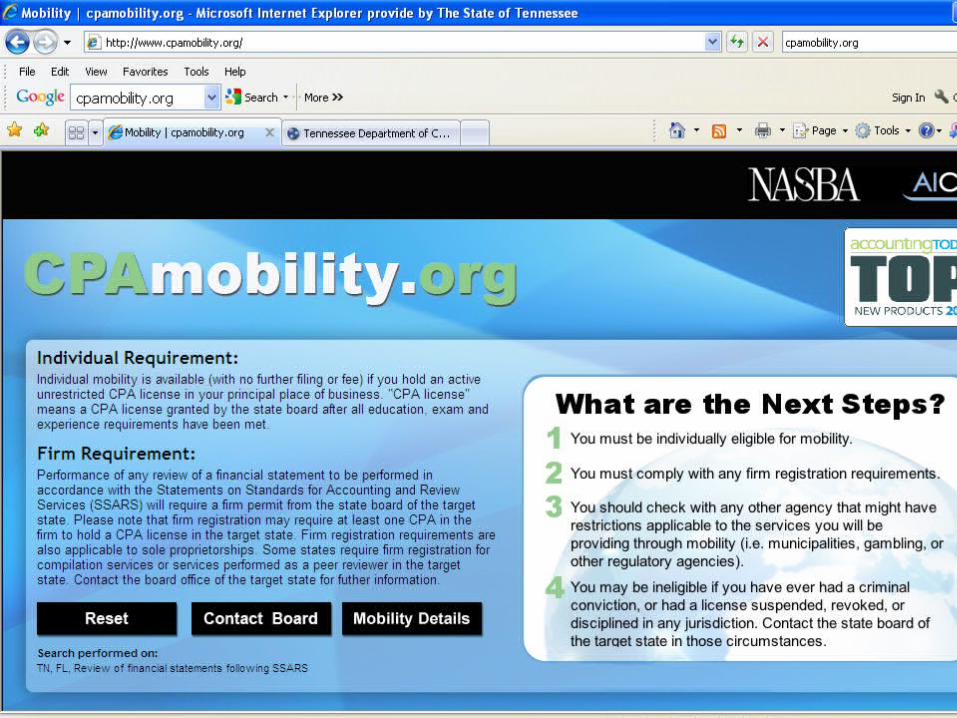

What about Mobility from Tennessee to another state?

The newest tool in mobility can be found at:• CPAmobility.org

Lets see how easy it is.

Can we have more case studies?

Yes – And today you get to be the Board.

Client Records

Case Study:An employee of a firm discards the extra W-2’s while preparing a client’s tax return. Placed in a dumpster by the custodial staff, the W-2 somehow blows onto a nearby sidewalk. A citizen finds the W-2 and mails it to the client. The client files a complaint with the Board, alleging that the firm released confidential client information.

Client Records

Disposition:You are the Board – What action should be taken?

1. Dismiss.2. Letter of warning.3. Civil penalty of $500 and probation for one

year.4. Other?

Professional StandardsCase Study:

A licensee’s client requests that his Federal tax return status be shown as “Married-Filing Separately” and the licensee does so.

When the client’s spouse becomes aware of the change in status, she files a complaint with the Board. She alleges that the licensee had no right to change the status of a tax return without her approval, especially since the clients had filed a joint return in the past.

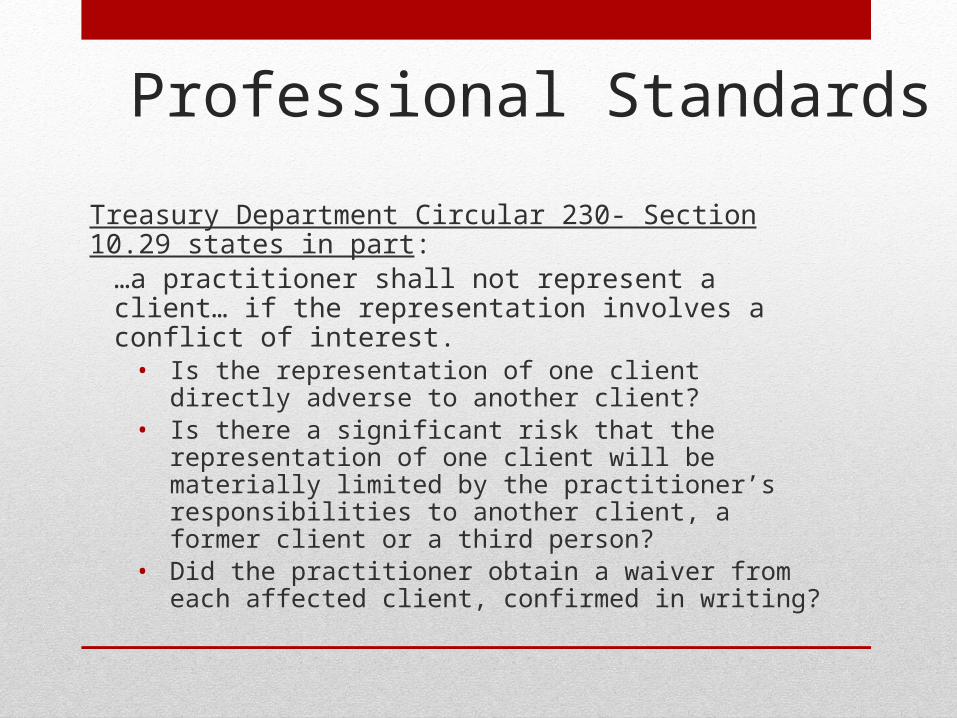

Professional StandardsTreasury Department Circular 230- Section 10.29 states in part:

…a practitioner shall not represent a client… if the representation involves a conflict of interest.

• Is the representation of one client directly adverse to another client?

• Is there a significant risk that the representation of one client will be materially limited by the practitioner’s responsibilities to another client, a former client or a third person?

• Did the practitioner obtain a waiver from each affected client, confirmed in writing?

Professional Standards

Disposition:You are the Board – What action should be taken?

1. Dismiss.2. Letter of warning.3. Civil penalty of $500 and probation for one

year.4. Consent Order, Civil Penalty, and notice to

the Internal Revenue Service?

Unlicensed PracticeCase Study:

A complaint is opened against a non-licensed firm for advertising “accounting services” and using the word “accounting” throughout its website.The Board’s investigation revealed that the firm used the “CPA” designation and engaged in conduct that constitutes the practice of accountancy under Tennessee law. In addition, the firm employed three licensees who failed to report the fact that they were working in an unregistered firm.

Unlicensed PracticeHearing:

In an informal hearing, the firm’s owner was given the opportunity to obtain licensure through the formation of a new firm that contained at least a 51% ownership interest with any or all of the licensees he currently employed.Alternatively, the licensees could close their CPA licenses and the firm could continue to operate with no reference to “accounting” or the use of the “CPA” designation.The owner refused to act and the matter went to a Formal Hearing.

Unlicensed Practice

Disposition:You are the Board – What action should be taken?

1. Dismiss.2. Binding Letter of Instruction.3. Consent Order with a Civil penalty of

$5,000.4. Suspension of the three CPA licenses until

the firm is compliant5. Other?

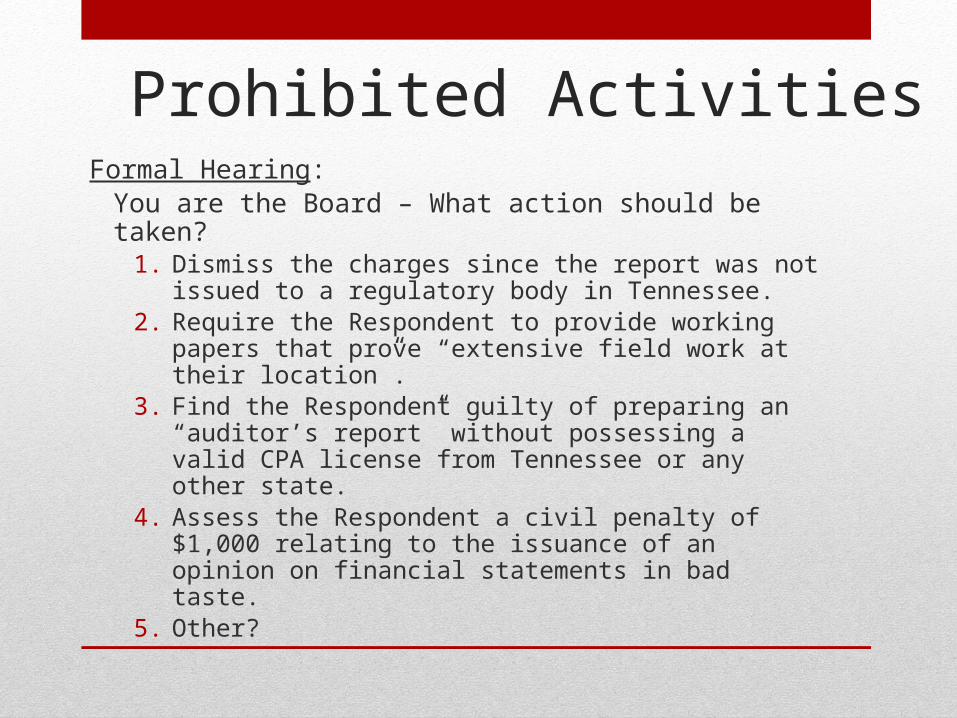

Prohibited Activities

Case Study:A regulatory board in another state submitted the following “opinion” after they were unable to find the individual’s CPA license.

How many discrepancies can you spot?

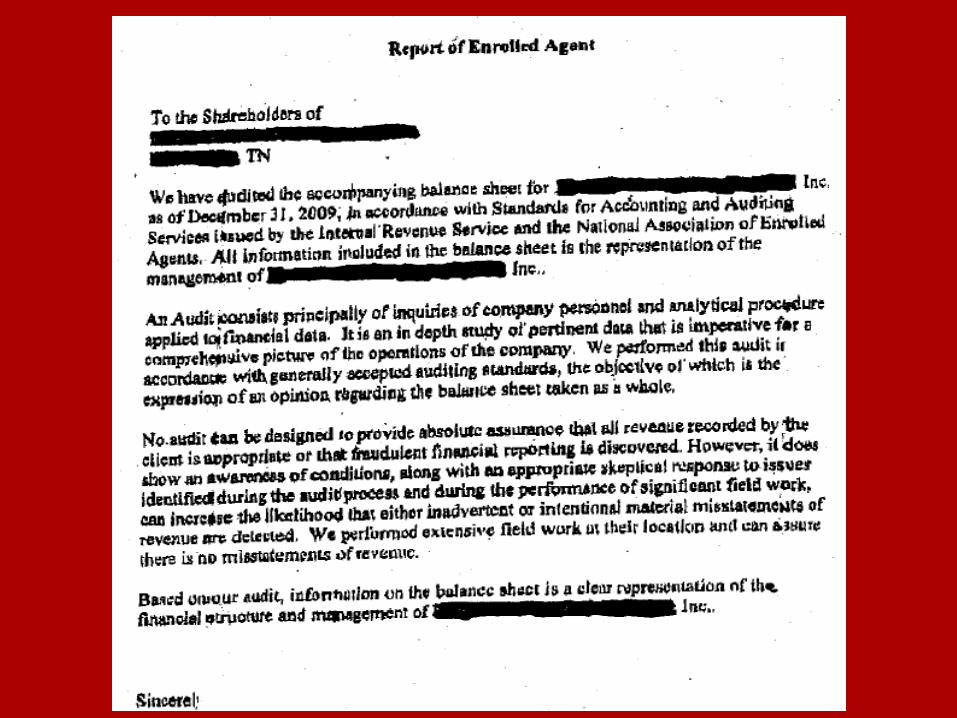

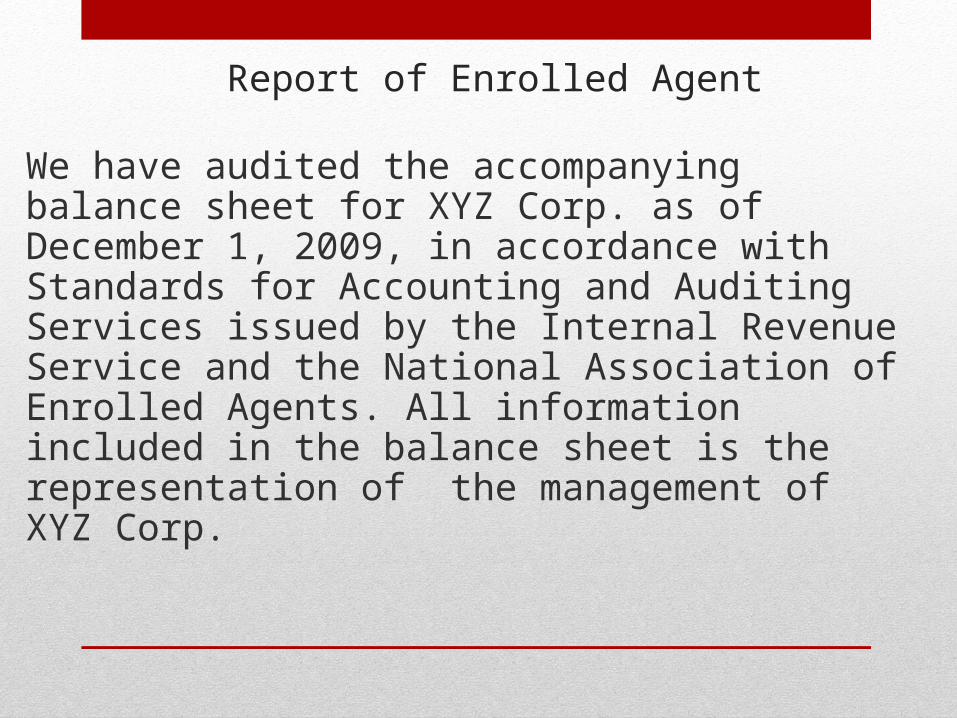

Report of Enrolled Agent

We have audited the accompanying balance sheet for XYZ Corp. as of December 1, 2009, in accordance with Standards for Accounting and Auditing Services issued by the Internal Revenue Service and the National Association of Enrolled Agents. All information included in the balance sheet is the representation of the management of XYZ Corp.

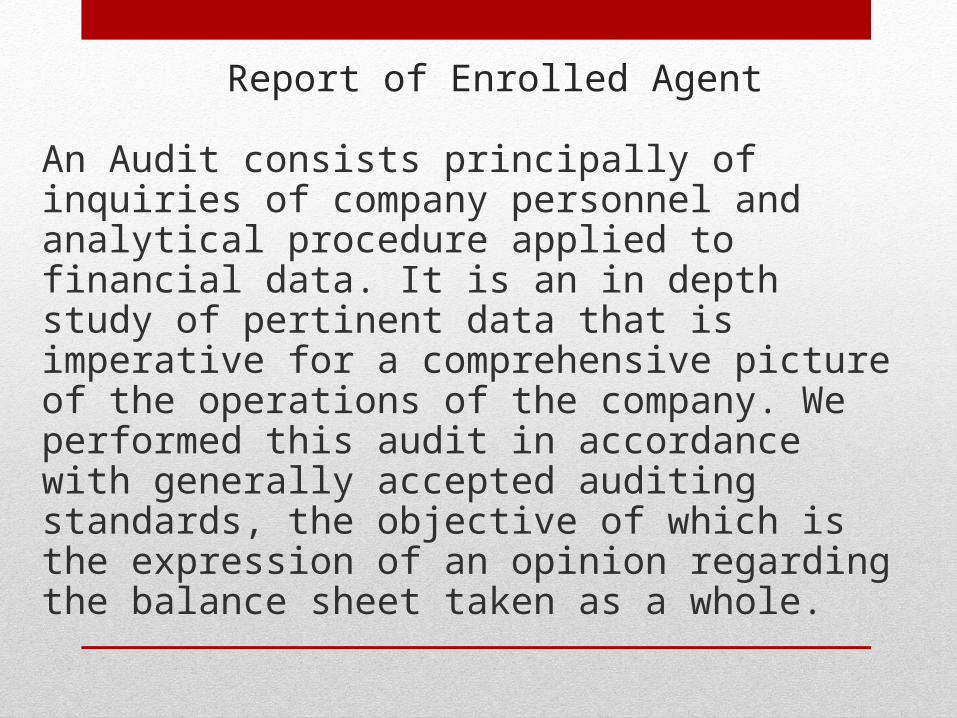

Report of Enrolled Agent

An Audit consists principally of inquiries of company personnel and analytical procedure applied to financial data. It is an in depth study of pertinent data that is imperative for a comprehensive picture of the operations of the company. We performed this audit in accordance with generally accepted auditing standards, the objective of which is the expression of an opinion regarding the balance sheet taken as a whole.

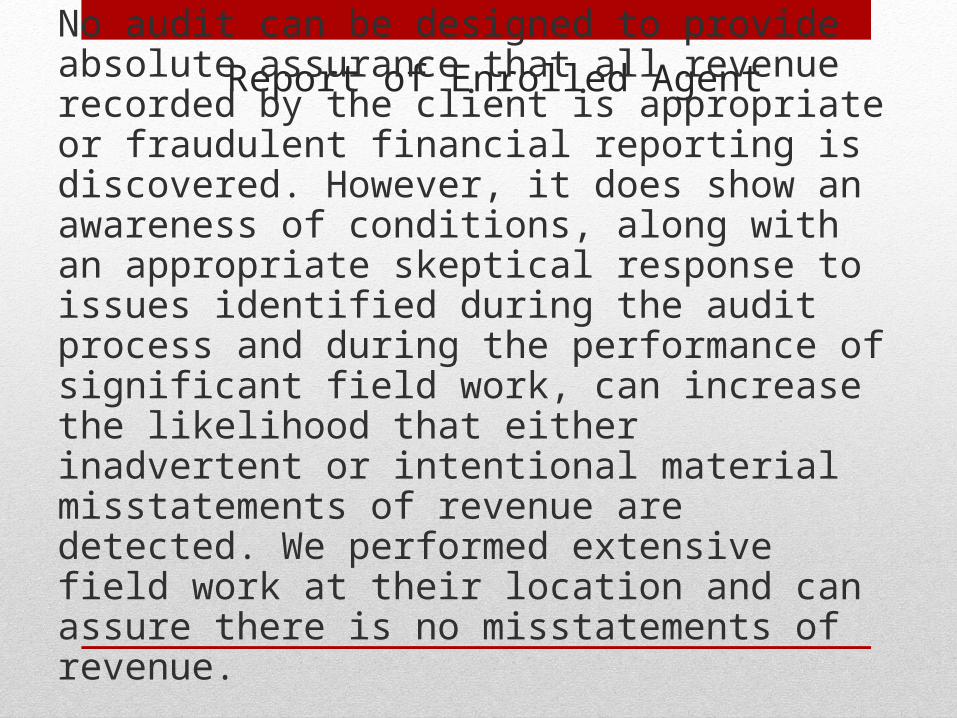

Report of Enrolled Agent

No audit can be designed to provide absolute assurance that all revenue recorded by the client is appropriate or fraudulent financial reporting is discovered. However, it does show an awareness of conditions, along with an appropriate skeptical response to issues identified during the audit process and during the performance of significant field work, can increase the likelihood that either inadvertent or intentional material misstatements of revenue are detected. We performed extensive field work at their location and can assure there is no misstatements of revenue.

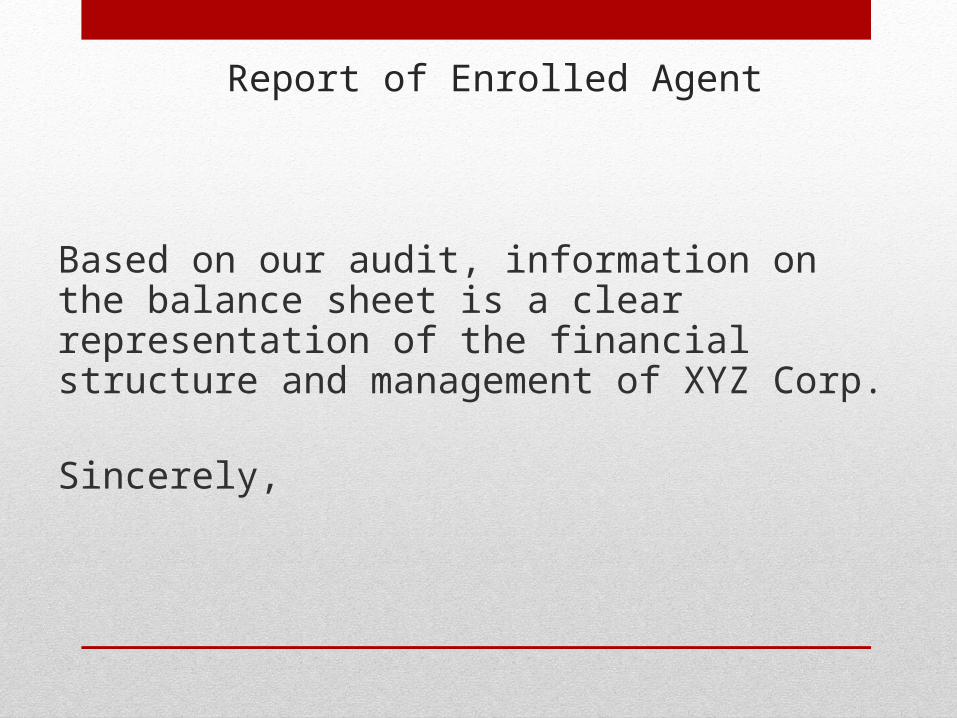

Report of Enrolled Agent

Based on our audit, information on the balance sheet is a clear representation of the financial structure and management of XYZ Corp.

Sincerely,

Prohibited ActivitiesFormal Hearing:

You are the Board – What action should be taken?1. Dismiss the charges since the report was not

issued to a regulatory body in Tennessee.2. Require the Respondent to provide working

papers that prove “extensive field work at their location”.

3. Find the Respondent guilty of preparing an “auditor’s report” without possessing a valid CPA license from Tennessee or any other state.

4. Assess the Respondent a civil penalty of $1,000 relating to the issuance of an opinion on financial statements in bad taste.

5. Other?

Final Question - What can we do for you?

• How can we best serve the public interest?

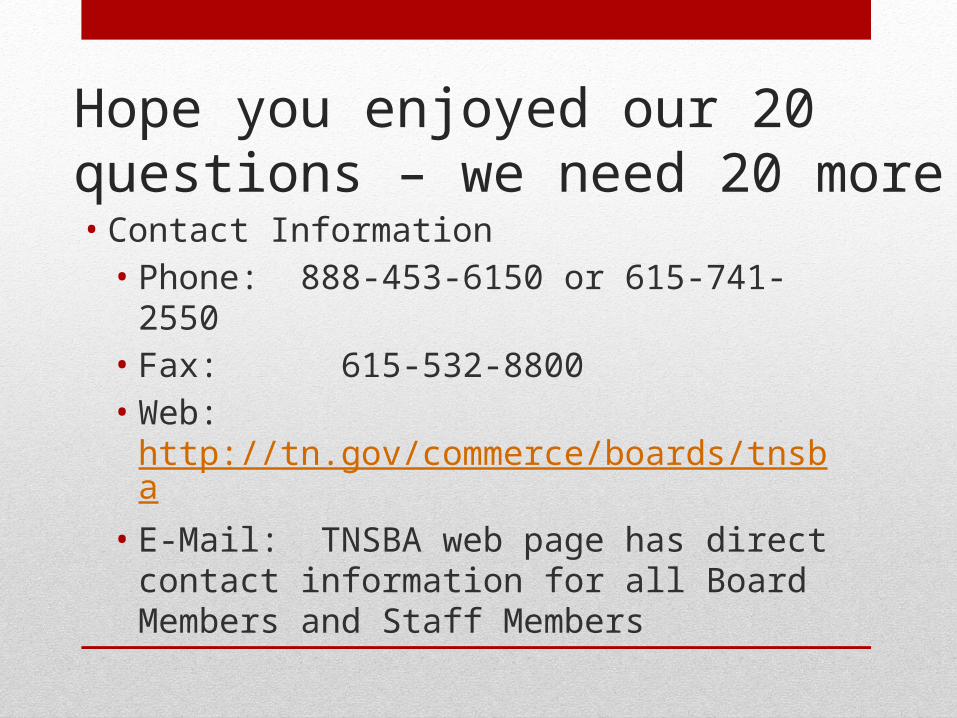

Hope you enjoyed our 20 questions – we need 20 more• Contact Information

• Phone: 888-453-6150 or 615-741-2550• Fax: 615-532-8800• Web: http://tn.gov/commerce/boards/tnsba• E-Mail: TNSBA web page has direct contact

information for all Board Members and Staff Members