e&o concerns in builders risk insurance - … · e&o concerns in builders risk insurance...

TRANSCRIPT

Education ProgramSEducation ProgramS

E&O Concerns in Builders Risk Insurance

sponsoredby

E&O Concerns in Builders Risk InsuranceAn Underwriter’s PerspectiveMAIA Annual Conference & Trade FairNovember 13, 2015

Rich SojaSenior Vice President, Inland MarineTokio Marine Management & Insurance Companies+1 212 297 [email protected]

Coordinated and made possible by the Inland Marine Underwriters Association (IMUA)

HIGHLY CONFIDENTIAL – DO NOT COPY 2

These opinions are mine and not necessarily the opinion of Tokio Marine Management

I am not a licensed agent

I am not an attorney

I am not offering any professional advice

Disclaimers

Let’s get on with the presentation!

Rich SojaSenior Vice President, Inland Marine

Tokio Marine Management & Insurance Companies

HIGHLY CONFIDENTIAL – DO NOT COPY 3

Here’s what I hope to cover with you this morning

General Industry Discussion

Today’s Agenda

Coverage Issues

Special Topics

Brief introduction to Builders Risk Insurance Who is Insured The Construction Contract

Hazards of Insuring Builder Risk Under a Property Policy Faulty Design and Workmanship Exclusions Common Additional Coverages and Extensions of Coverage Soft Costs, Loss of Rental Income, Delay in Start-Up, ALOP

Renovation Projects “Green Building” Implications Summary of Potential Pitfalls

HIGHLY CONFIDENTIAL – DO NOT COPY 4

Section 1: General Industry Background

HIGHLY CONFIDENTIAL – DO NOT COPY

Audience Survey

Is it Inland Marine or is it Property

What are We Covering?

When are We Covering It?

Project vs. Open Builders Risk Policies

Common Additional Coverages & Extensions

5

Know the BasicsBrief Introduction to Builders Risk Insurance

HIGHLY CONFIDENTIAL – DO NOT COPY

Owner

General Contractor

Sub-Contractors?

Sub-Sub Contractors of Every Tier

Architects & Engineers?

Material Suppliers?

6

We Are All In This TogetherWho Is Insured?

HIGHLY CONFIDENTIAL – DO NOT COPY

Driving principle behind a broad Named Insured Wording

Waiver of Subrogation Implications

Rights of a Named Insured vs. Additional Insured or Loss Payee

7

The ImplicationsWho Is Insured?

HIGHLY CONFIDENTIAL – DO NOT COPY 8

The Construction ContractUnderstanding Your Client’s Obligations

HIGHLY CONFIDENTIAL – DO NOT COPY

Who obtains the insurance

Type of Insurance (“Builders risk or equivalent”)

Extent of Coverage and It’s Implications

Named Insured

Waiver of Subrogation

The Broker’s Role in Reviewing Contracts

9

The Construction ContractMatching Coverage to Requirements

HIGHLY CONFIDENTIAL – DO NOT COPY 10

Section 2: Coverage Issues

HIGHLY CONFIDENTIAL – DO NOT COPY

Additions or Renovations may not be covered adequately or at all

Property Covered (Underground Property, Land Improvements, Off-Site, Transit)

Perils Excluded (Testing, Faulty Design/Workmanship, National Catastrophe)

Deductible, and its implication for subcontractors of every tier

Business Interruption/Extra Expense vs. Delay in Start-Up/Soft Costs

Named Insured Status/ Waiver of Subrogation

11

Hazards of Insuring Builders Risk via a Property PolicySquare Peg Round Hole

HIGHLY CONFIDENTIAL – DO NOT COPY

Premise behind the Design Exclusion: It’s a Professional Liability Coverage

Premise behind the Workmanship Exclusion: It’s a Business Risk

However….The Resulting Damage can be Addressed

“DE Wordings” and “LEG” Wordings –what an agent needs to know

12

Faulty Design / Workmanship ExclusionsResulting Damage Variations

HIGHLY CONFIDENTIAL – DO NOT COPY

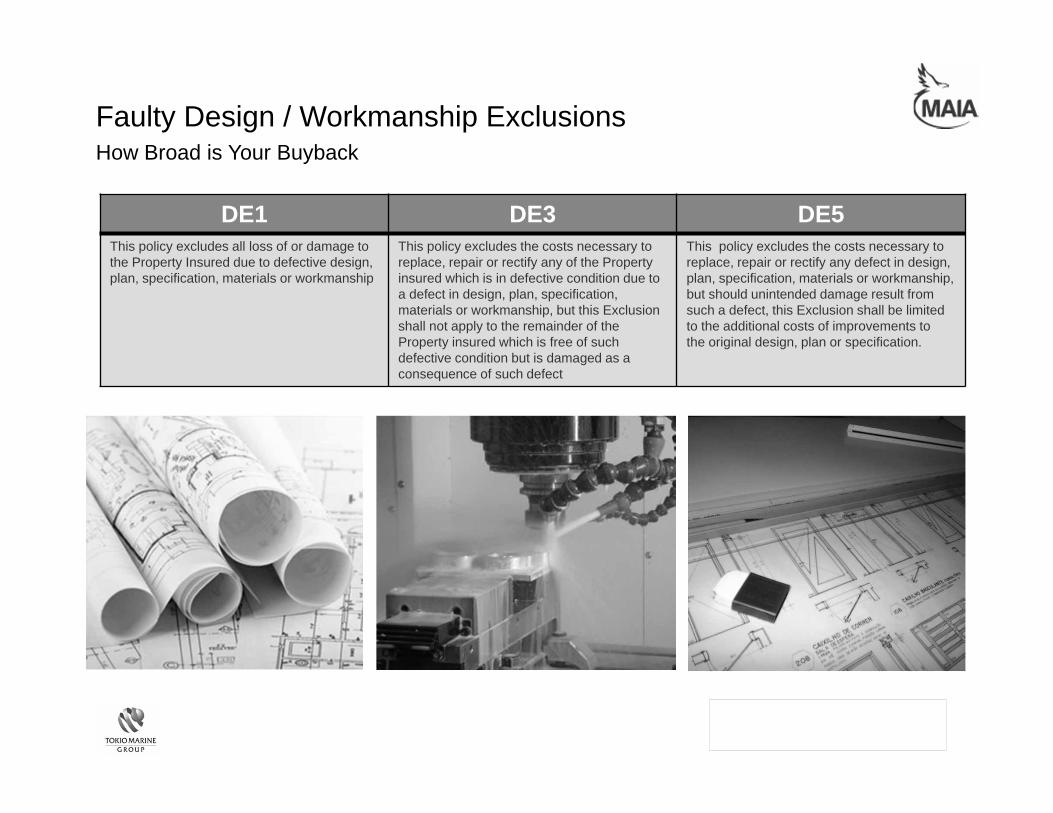

Faulty Design / Workmanship ExclusionsHow Broad is Your Buyback

DE1 DE3 DE5This policy excludes all loss of or damage to the Property Insured due to defective design, plan, specification, materials or workmanship

This policy excludes the costs necessary to replace, repair or rectify any of the Property insured which is in defective condition due to a defect in design, plan, specification, materials or workmanship, but this Exclusion shall not apply to the remainder of the Property insured which is free of such defective condition but is damaged as a consequence of such defect

This policy excludes the costs necessary to replace, repair or rectify any defect in design, plan, specification, materials or workmanship, but should unintended damage result from such a defect, this Exclusion shall be limited to the additional costs of improvements to the original design, plan or specification.

HIGHLY CONFIDENTIAL – DO NOT COPY

Temporary Works: Scaffolding, Formswork, Falsework

Off-Premises and In Transit: 4 Story Office Building vs. Hedge-Fund Data Center

Ordinance or Law

Hot Testing

Site Preparation (i.e., exception to the Land Exclusion)

Contractual Penalties

Business Interruption & Extra Expense Related Coverage

14

Common Additional Coverages & Extensions of CoverageExtensions Matter

HIGHLY CONFIDENTIAL – DO NOT COPY

Costs incurred after a covered loss related to other than labor or materials

A few examples:

15

Soft Costs / Loss of Rental Income / Delay in Start-Up / ALOPExtra Expense & Business Interruption

• Accounting Fees

• Advertising

• Architects & Engineering Fees

• Building Inspection Fees

• Construction Loan Fees

• Equipment Rental

• Feasibility Plan Studies

• Insurance Costs

• Legal Fees

• Permit Fees

• Surety Bond Premiums

• Etc.

HIGHLY CONFIDENTIAL – DO NOT COPY

SOFT COSTS

Useful Insights: How the Industry Works

16

Soft But Real

Not unusual to run 20-40% of the completed value

If construction contract and lending document do not require, some contractors may not request

If requested, detailed breakout of projected fees is useful – all may not qualify

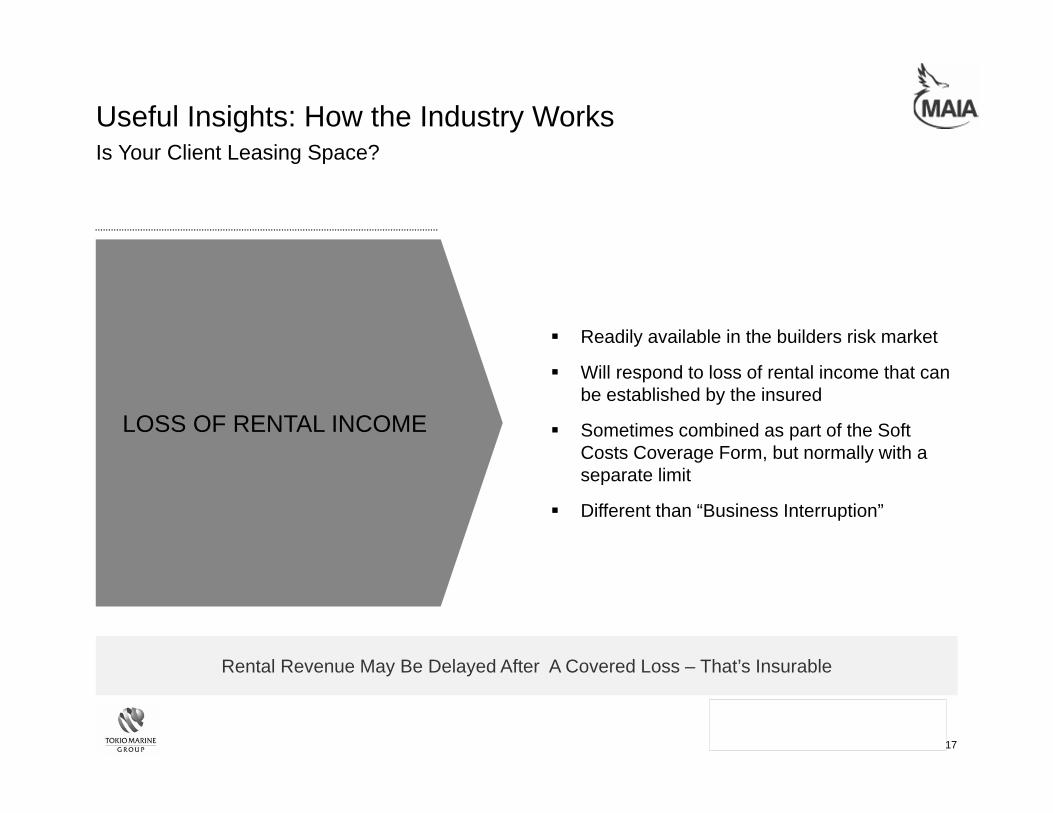

Loss of Rental Income may be a separate & distinct coverage from Soft Costs

Lendor’s May Not Require It, But You Should Ask For It!

HIGHLY CONFIDENTIAL – DO NOT COPY

LOSS OF RENTAL INCOME

Useful Insights: How the Industry Works

17

Is Your Client Leasing Space?

Rental Revenue May Be Delayed After A Covered Loss – That’s Insurable

Readily available in the builders risk market

Will respond to loss of rental income that can be established by the insured

Sometimes combined as part of the Soft Costs Coverage Form, but normally with a separate limit

Different than “Business Interruption”

HIGHLY CONFIDENTIAL – DO NOT COPY

DELAY IN START UP / ALOP

Useful Insights: How the Industry Works

18

Prove Your Loss

Set Proper Expectations With Your Client

Equivalent of Business Income Insurance for operational facility

Advanced Loss of Profits (ALOP) is a recoupment of anticipated profits from a covered loss that results in a delayed opening of the facility

Not a common request in the United States (unless JV partnership from Overseas)

Non-standardized forms

Example: Construction of a Home Depot store in a new location

Example: Construction of a start-up high-end fashion store in NYC

HIGHLY CONFIDENTIAL – DO NOT COPY 19

Section 3: Special Topics

HIGHLY CONFIDENTIAL – DO NOT COPY 20

THE DILEMMA:Where and how to insure the existing structuring

PROPERTY POLICY PROBLEM:Vacancy Provision

BUILDERS RISK POLICY PROBLEM:Exclusion for Existing Property

Renovation Projects

HIGHLY CONFIDENTIAL – DO NOT COPY

Costs to restore the property to its pre-established environmental compliance rating level after a covered construction loss

Fees for recertification

Loss of Income from Delay in Occupancy or Use

21

Green Building ConstructionGreen Can Be Expensive

Insurance Implications focus on:

HIGHLY CONFIDENTIAL – DO NOT COPY

Green Building Standards are variable (i.e., LEED) and may be required to be specified on the policy

Coverage Can Include:

– Restoration of indoor air quality

– Costs of Replacement Electricity to achieve certification

– Costs of Replacement Water to achieve certification

Cautionary Areas include:

– How to value the Project and the “Green Elements”

– Vegetative Roofs

– Rehabilitation and Renovation Risks where Green Elements applies to all

– Non-standardization of Forms or Endorsements

22

Green Building ConstructionThere Are Special Considerations

HIGHLY CONFIDENTIAL – DO NOT COPY

Understand the Construction Contract. Or at least, disclosure & transparency on where there is not compliance.

Sufficient limits and sub-limits for all coverages.

Identifying key coverage considerations in a non-standardized market.

Identifying and solving unique issues involved in Renovation Projects, Green Construction, and other areas.

23

Summary of Potential PitfallsBe A Superhero For Your Client

HIGHLY CONFIDENTIAL – DO NOT COPY 24

Construction Insurance, November 1999The Insurance Institute of London

Inland Marine Insurance, 2nd EditionAmerican Institute for Chartered Property Casualty UnderwritersArthur L. Flitner, CPCU, ARM, AICErin M. Gambeski

The Builders Risk Book, 2010International Risk Management Institute, Inc.Steven M. Coombs, CPCU, ARMDonald S. Malecki, CPCU

Credits and Q&A

HIGHLY CONFIDENTIAL – DO NOT COPY 25

Rich Soja is a noted industry expert in commercial inland marine insurance. Prior to joining TokioMarine, Rich was Executive Vice President and Chief Marine Underwriter, U.S. at Aspen Insurance. Before Aspen, Rich enjoyed a twenty two year career with Chubb & Son rising to the position of SVP and worldwide manager of Chubb Marine Underwriters. He was responsible for all marine operations for the company including strategy development, underwriting, profit & loss, training, treaty reinsurance and personnel.

Rich has been actively engaged in IMUA for over twenty years. He served as chairman of the IMUA Board of Directors and has presented numerous training and education classes for underwriters and brokers alike. He holds the Chartered Property & Casualty (CPCU) designation as well as the Associate in Marine Insurance Management (AMIM) and Associate in Reinsurance (ARe) degrees.

You can reached him at [email protected] or 212 297 6832

About the Speaker

About Tokio Marine

Tokio Marine Group was founded in 1879, has greater than $30 Billion in revenues, is the world’s 6th largest property & casualty insurer and conducts business in 40 countries. The US company is admitted in 50 states for all lines of insurance and is rated A++ XV by A.M. Best. Having acquired Philadelphia Insurance Companies in 2008, Tokio Marine Management is well poised to partner with Philadelphia’s distribution network, as well as its own, to provide outstanding service on a wide variety of inland marine products.