end user’s perspective - platts automotive industry advantage india platts steel markets asia...

TRANSCRIPT

. . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . .

End User’s Perspective: Impact of Steel Prices on the Automotive and Machinery Industry.

Platts Steel Markets Asia Conference. 18th Nov.2016. Chandrashekhar Jagtap

1

Agenda

. . . . .

. . . . .

. . . . .

. . . . .

. . . . .

. . . . .

. . . . .

. . . . .

. . . . .

1 Overview: The Indian Automotive Industry

2 Supply and Demand Projections

3 Impact of Steel Trend and Prices on Automotive Industry

2

4 Challenges for buyers in Short and Long term.

5 Industry expectations from Steel Producers

Platts Steel Markets Asia Conference. 18th Nov.2016. Chandrashekhar Jagtap

Source: Tata Motors, Society of Indian Automobile Manufacturers (SIAM), TechSci Research

• Closed market

• Five players

• Long waiting

periods and

outdated

models

• Seller’s market

• Joint Venture (JV):

Indian government and

Suzuki formed Maruti

Udyog; commenced

production in 1983

• Component

manufacturers entered

the market via JV

• Buyer’s market

• Sector de-licensed in

1993

• Major Original

Equipment

Manufacturers (OEMs)

started assembly

operations in India

• Imports permitted from

April 2001

• Introduction of value -

added tax in 2005

• More than 35 market players

• Indian companies gaining

acceptance on a global scale

• Setting up of National

Automotive Board to act as

facilitator between the

government and industry

• Government has proposed

GST to support lower raw

material cost

• Launch of Automotive Mission

Plan 2016-26 in 2015

Evolution of the Indian Automotive Sector

Platts Steel Markets Asia Conference. 18th Nov.2016. Chandrashekhar Jagtap 9

0.4 million units

(1982)

0.6 million units

(1992)

11 million units

(2007)

21.5 million

units (FY14)

24 million units

(FY16)

Before 1982

1983–92

1993-2007 2008 onwards

3

Indian Automotive Industry

Indian Automotive Industry

Growth in the Indian Automobile Industry

Platts Steel Markets Asia Conference. 18th Nov.2016. Chandrashekhar Jagtap 4

1.3 1.3 1.6 1.8 2.4

3.0 3.1 3.2 3.1 3.2 3.4

0.4

0.5

0.6

0.4

0.6

0.8

0.9

0.8

0.7

0.7

0.8

0.4

0.6

0.5

0.5

0.6

0.8

0.9

0.8

0.8

0.9

0.9

7.6 8.5

8.0 8.4

10.5

13.4

15.4 15.7

16.9

18.5 18.8

FY06 FY07 FY08 FY09 FY10 FY11 FY12 FY13 FY14 FY15 FY16

Passenger Vehicle Commercial Vehicle Three Wheelers Two Wheelers

Production of automobiles increased at a CAGR of 9.4 per cent over FY06-16

Around 15% of total vehicles produced in India are exported

Total production of automobiles in India (million units)

Source: SIAM, TechSci Research

Indian Automotive Industry

Advantage India

Platts Steel Markets Asia Conference. 18th Nov.2016. Chandrashekhar Jagtap 5

FY15

Market size:

USD 74

billion

FY26E

Market size:

USD 260 to

300 billion

Advantage

India

•

Policy support

The government aims to develop India as a global manufacturing as well as R&D hub

• There has been a wide array of policy support in the form of sops, taxes and FDI encouragement

Innovation opportunities

• Tata Nano and the upcoming Pixel have opened up the potentially large ultra low- cost car segment

• Innovation is likely to intensify among engine technology and alternative fuels

• Strong growth in demand due to rising income, middle class, and a young population is likely to propel India among the world’s top five auto manufacturers by 2016

• Growth in export demand is set to accelerate

• Government takes Initiatives to set up manufacturing plants through Make in India

Rising investments

• India has significant cost advantages; auto firms save 10-25 per cent on operations vis-à-vis Europe and Latin America

• A large pool of skilled manpower and a growing technology base would induce greater investments

Growing Demand

Source: Automotive Mission Plan (2006–2026),

Make in India

The Automotive Mission Plan 2016-26 (AMP 2026) targets a fourfold growth in the automotive industry.

6 Platts Steel Markets Asia Conference. 18th Nov.2016. Chandrashekhar Jagtap

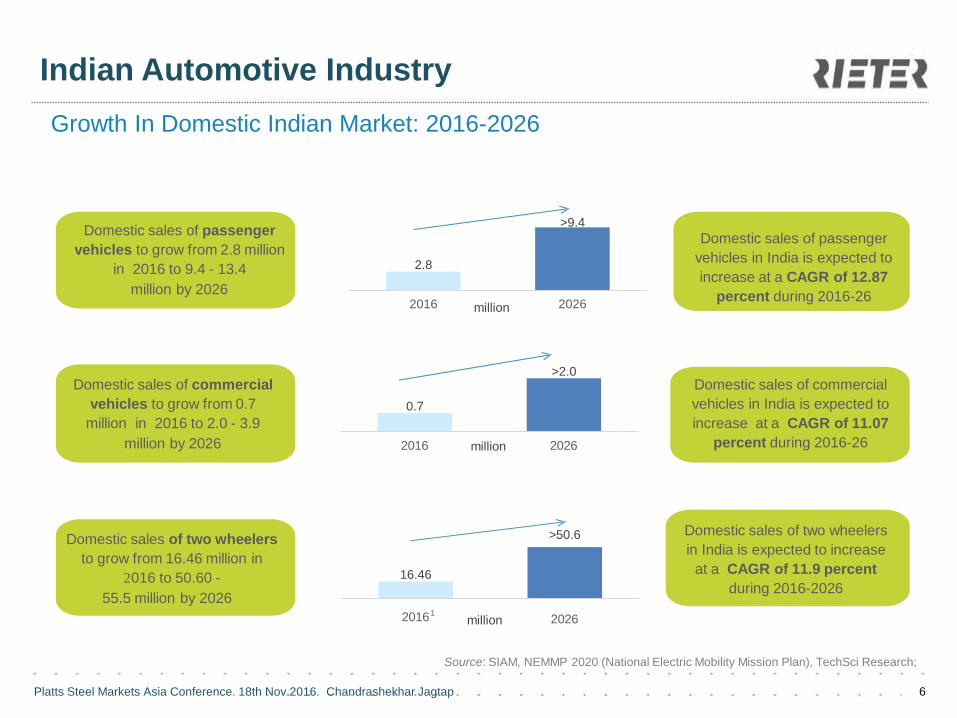

0.7

>2.0

2016 2026

2.8

>9.4

2016 2026

Domestic sales of passenger

vehicles in India is expected to

increase at a CAGR of 12.87

percent during 2016-26

Domestic sales of commercial

vehicles in India is expected to

increase at a CAGR of 11.07

percent during 2016-26

Domestic sales of passenger

vehicles to grow from 2.8 million

in 2016 to 9.4 - 13.4

million by 2026

Domestic sales of commercial

vehicles to grow from 0.7

million in 2016 to 2.0 - 3.9

million by 2026

million

million

16.46

>50.6

20161 2026

Domestic sales of two wheelers

in India is expected to increase

at a CAGR of 11.9 percent

during 2016-2026

Domestic sales of two wheelers

to grow from 16.46 million in

2016 to 50.60 -

55.5 million by 2026

million

Growth In Domestic Indian Market: 2016-2026

Indian Automotive Industry

Source: SIAM, NEMMP 2020 (National Electric Mobility Mission Plan), TechSci Research;

Indian Automotive Industry

Indian Automotive Industry – Competitive Advantage

Platts Steel Markets Asia Conference. 18th Nov.2016. Chandrashekhar Jagtap 7

Design and

engineering skills

Manufacturing

skills

Manpower

costs

Supplier

base

Raw

materials

East Asia Korea

China

Thailand

Indonesia

Vietnam

Central &

Eastern Europe

Czech Republic

Romania

Poland

Slovakia

Russia

Hungary

Turkey

Latin America Brazil

Mexico

Less competitive than India In competition with India Source: ACMA, TechSci Research

Agenda

. . . . .

. . . . .

. . . . .

. . . . .

. . . . .

. . . . .

. . . . .

. . . . .

. . . . .

1 Overview: The Indian Automotive Industry

2 Supply and Demand Projections

3 Impact of Steel Trend and Prices on Automotive Industry

8

4 Challenges for buyers in Short and Long term.

5 Industry expectations from Steel Producers

Platts Steel Markets Asia Conference. 18th Nov.2016. Chandrashekhar Jagtap

Automotive Industry: Key Consumer of Steel

Structure of Indian Steel Sector

Platts Steel Markets Asia Conference. 18th Nov.2016. Chandrashekhar Jagtap 9

Steel

End use

Structural steel

Construction steel

Rail steel

Form

Liquid steel Crude steel

Ingots

Semis

Finished steel

Flat

Non-flat

Composition

Non-alloy steel

Low carbon steel

Medium carbon steel

High carbon

steel

Alloy

Stainless

Silicon electrical

High speed

Source: Report on Indian steel industry by Competition Commission of India,

TechSci Research

Key Steel Consuming Sectors in India

Platts Steel Markets Asia Conference. 18th Nov.2016. Chandrashekhar Jagtap 10

35%

20% 12%

10%

8%

15%

Construction

Infrastructure

Automobiles

Pipes and Tubes

Capital Goods

Others

- In FY15, Crude Steel production in India was 88.98

million tonnes and Finished Steel production in India

was 92.17 million tonnes

Automotive Industry: Key Consumer of Steel

13.25 12.52 12.82 13.44 12.83 9.23

55.3

7

63.1

8

68.8

6

74.2

4

79.3

4

58.4

9

FY1

1

FY1

2

FY1

3

FY1

4

FY1

5

FY1

6H

1

Public Sector Private Sector

Finished steel production(million tonnes)

16.99 16.48 16.48 16.77 17.21 13.34

53.6

8

57.8

1

61.9

4

64.9

2

71.7

7

53.7

4

FY1

1

FY1

2

FY1

3

FY1

4

FY1

5

FY1

6H

1

Public Sector Private Sector

Crude steel production (million tonnes) Key Steel Consuming Sectors in India

- Automotive Industry is third largest consumer of Steel

In India and consume 12% of total Steel Produced in India

- The Automotive Industry is forecasted to grow in size by

USD 74 billion in 2015 to USD 260-300 billion by 2026

- With increasing capacity addition in the automotive

industry, demand for steel from the sector is expected to be

robust

Source:: Ministry of Steel Annual Report, TechSci Research

Agenda

. . . . .

. . . . .

. . . . .

. . . . .

. . . . .

. . . . .

. . . . .

. . . . .

. . . . .

1 Overview: The Indian Automotive Industry

2 Supply and Demand Projections

3 Impact of Steel Trend and Prices on Automotive Industry

11

4 Challenges for buyers in Short and Long term.

5 Industry expectations from Steel Producers

Platts Steel Markets Asia Conference. 18th Nov.2016. Chandrashekhar Jagtap

Metal Cost as % of Sales price for Auto OEMs

Platts Steel Markets Asia Conference. 18th Nov.2016. Chandrashekhar Jagtap 12

- Domestic steel prices have increased 10-12 % after

imposition of MIP (minimum Import Duty) by Union

Government.

- Steel cost accounts for 8% for Two Wheelers, 11% for

Passenger Vehicles and 15% for Commercial

vehicles sales price.

- A 10% increase in domestic steel prices would

require a price increase of 0.6% in two wheelers, 1%

in passenger vehicles and 1.6% in MHCV commercial

vehicles

Impact of Steel Prices on Automotive Industry

20%

8%

6% 2%

4%

60%

Two Wheelers

Metal/Castings

Steel

Aluminium

Copper

Other Metals

Polymers+Overhead +Profit

24%

15%

3% 3% 4%

52%

Commercial Vehicles

Metal/Castings

Steel

Aluminium

Copper

Other Metals

Polymers+Overhead+ Profit

19%

11%

3% 2%

3%

62%

Passenger Vehicle

Metal/Castings

Steel

Aluminium

Copper

Other Metals

Polymers+Overhead +Profit

Source:: Kotak Securities Research Report

Agenda

. . . . .

. . . . .

. . . . .

. . . . .

. . . . .

. . . . .

. . . . .

. . . . .

. . . . .

1 Overview: The Indian Automotive Industry

2 Supply and Demand Projections

3 Impact of Steel Trend and Prices on Automotive Industry

13

4 Challenges for buyers in Short and Long term

5 Industry expectations from Steel Producers

Platts Steel Markets Asia Conference. 18th Nov.2016. Chandrashekhar Jagtap

14 Platts Steel Markets Asia Conference. 18th Nov.2016. Chandrashekhar Jagtap

Challenges for buyers in Short and Long term

- MIP and Anti dumping duty

- Currency Fluctuation

- Monopolistic market in certain special steel grades

- Long process of new steel grade approval

- Low bargaining power of Buyers

- Steel availability in small MOQ resulted into high inventory level

Agenda

. . . . .

. . . . .

. . . . .

. . . . .

. . . . .

. . . . .

. . . . .

. . . . .

. . . . .

1 Overview: The Indian Automotive Industry

2 Supply and Demand Projections

3 Impact of Steel Trend and Prices on Automotive Industry

15

4 Challenges for buyers in Short and Long term

5 Industry expectations from Steel Producers

Platts Steel Markets Asia Conference. 18th Nov.2016. Chandrashekhar Jagtap

16 Platts Steel Markets Asia Conference. 18th Nov.2016. Chandrashekhar Jagtap

Industry expectations from Steel Producers

- Development of special grade alloy steels for small MOQ

- Payment credit extension to Tier 1 and Tier 2 suppliers

- Immediate response on Quality issues

- Reduce Minimum Order Quantity

- Carry safety stock of fast moving raw material

- Local warehouse in all major Industry Clusters

17 Platts Steel Markets Asia Conference. 18th Nov.2016. Chandrashekhar Jagtap

Thank You