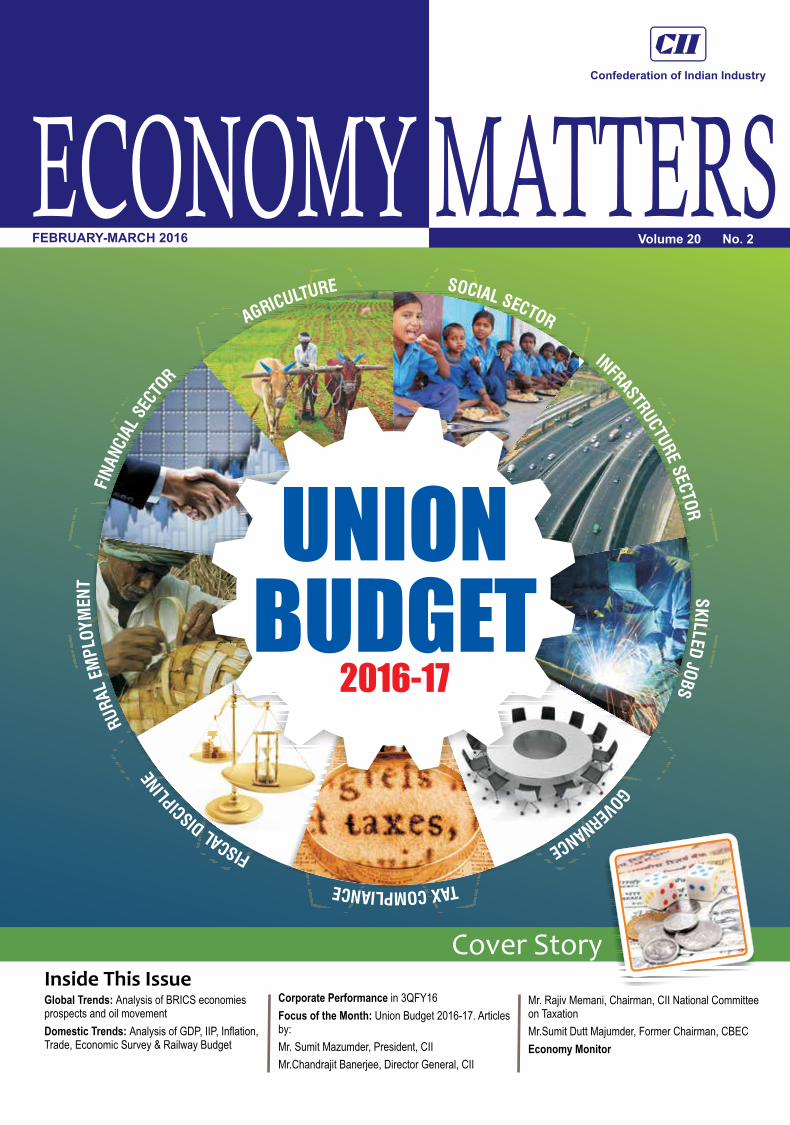

economy matters february 2016

TRANSCRIPT

ECONOMY MATTERS 2

1

FOREWORD

FEB-MAR 2016

The Finance Minister presented a well-rounded package of reforms and growth-oriented meas-ures in the Union Budget 2016-17. The Budget proposals addressed issues in nine critical ar-eas ranging from agriculture and the rural sector to financial sector and banking. Given the

current global context of slowing growth and threat of financial turbulence, the Budget needs to be commended for giving a boost to growth and investment without disturbing the path for fiscal consolidation.

In line with recommendations made by CII, the Budget has announced critical interventions in areas such as agriculture, infrastructure, education and skills. Financial sector reforms have been taken forward including a plan for revitalising public sector banks. A lot of emphasis has been given to ac-celerated implementation of direct benefits transfer through the widespread use of JAM trinity, so that subsidies reach the intended beneficiaries.

Budget 2016-17 has undertaken several key initiatives for job creation in the formal sector, which have been taken up consistently by CII. Contribution of EPF for new employees for three years, en-trepreneurship development courses, changes in the transport sector, and so on would encourage job generation. Low-cost housing will be a huge demand multiplier, and CII welcomes the many ini-tiatives on this. CII also welcomes the measures to revive infrastructure investment such as the new credit rating system and the commitment to issue guidelines for renegotiation of PPPs.

Industry had been facing some issues in tax administration and is therefore happy with the emphasis given to the dispute resolution mechanism. Further, in order to speed up the settlement of disputes, 11 new benches of Customs, Excise and Service Tax Appellate Tribunal shall be set up.

Budget 2016-17 has many tax and spending measures that will go a long way in promoting investment and growth. The well-thought out interventions presented in the Budget make it a growth and development oriented Budget as a result it will be appreciated by all sections of society. Finally, the RBI will perceive the government’s attempt to maintain its fiscal path as a positive. It is hoped it will agree to reduce its policy rate.

Chandrajit BanerjeeDirector General, CII

3 FEB-MAR 2016

5

EXECUTIVE SUMMARY

FEB-MAR 2016

Global TrendsIn the largest emerging markets—the heterogeneous group of BRICS (Brazil, Russia, India, China, and South Africa)— growth has slowed from almost 9 per cent in 2010 to about 4 per cent in 2015, on average, with India being a notable exception. This slowdown reflects both easing growth in China, persistent weakness in South Africa, and steep recessions in Russia since 2014 and in Brazil since 2015. Low global oil prices have also contrib-uted to providing a fillip to BRIC economies growth in the last year. Global oil supply growth is plunging as an extended period of low prices takes its toll, the Interna-tional Energy Agency (IEA) said in its annual Medium-Term Oil Market Report released in February 2016. How-ever, the report points to the risk of an oil price spike in the later part of the outlook period arising from insuf-ficient investment.

Domestic TrendsAs per the advance estimates released by Central Statis-tical Organisation (CSO), GDP growth is expected to rise to 7.6 per cent in FY16 as compared with the revised es-timates of 7.2 per cent in the previous year, aided large-ly by growth in the manufacturing sector. If the new projection materialises, India will be the fastest grow-ing major economy in the world, overtaking China. On the inflation front, it is heartening to note that the Janu-ary 2016 CPI print came 30 basis points (bps) lower than the RBI’s target of 6.0 per cent. Inflation pressures are expected to remain benign as global commodity prices are anticipated to remain subdued in the year ahead. On the external front, merchandise exports in January 2016 fell 13.6 per cent from a year earlier to US$21.07 billion - declining for the 14th consecutive month - while a contraction in imports narrowed the trade gap to an 11-month low.

Corporate Performance in Q3FY16The corporate results at the end of the third quarter of

current fiscal continued to remain subdued as the finan-cial performance of Indian companies, especially manu-facturing sector firms, came lower. While the growth in expenditure costs stood somewhat curbed, fading growth of net sales as well as decline in PAT added to the prevalent despair. Net sales on an aggregate basis decelerated steeply to 1.2 per cent at the end of the third quarter of 2015-16. While moderation in growth of expenditure has to some extent mitigated the impact of the current bout of economic crisis characterized by falling growth in net sales, the reduction was not large enough to provide cushion to the bottom-line of the corporate. Over the past nine quarters, while net sales and expenditure has mostly followed a downward trend, profitability has displayed wide fluctuations.

Focus of the Month: Union Budg-et 2016-17The Finance Minister has presented a bold, pragmatic and growth-driven Budget which has attempted a cred-ible balancing act of scripting a blueprint for sustaining the growth momentum in the Indian economy in the coming year on the one hand while taking up issues of social inclusion on the other. Fiscal prudence has been a cornerstone of the budget strategy with the deficit pegged at 3.9 per cent and 3.5 per cent of GDP for FY16 and FY17 respectively without compromising the devel-opmental agenda. The adherence to the fiscal deficit target would help open up access to funds for other sectors to spend, maintain a level of confidence in mac-roeconomic management and contain inflation within the desired band. It is also heartening to note that the Budget has a plan for social inclusion. A package of measures including a broad agriculture thrust and social security measures, which seek to address rural stress. In this month’s Focus of the month, we provide a de-tailed analysis of the Union Budget: 2016-17 through the eyes of the experts.

ECONOMY MATTERS 6

GLOBAL TRENDS

Economic Prospects of BRICS Economies: How do the Current Numbers Stack up and Looking Ahead in 2016

Global growth again fell short of expectations in 2015, slowing to 2.4 per cent from 2.6 per cent in 2014. The disappointing performance was

mainly due to a continued deceleration of economic activity in emerging and developing economies amid weakening commodity prices, global trade, and capi-tal flows. Going forward, global growth is projected to edge up, according to the January 2016 edition of the Global Economic Prospects by the World Bank, reach-ing 2.9 per cent in 2016 and 3.1 per cent in 2017-18. In

developing countries, growth in 2015 is estimated at a post-crisis low of 4.3 per cent, down from 4.9 per cent in 2014. The economic rebalancing in China is continuing and accompanied by slowing growth. Brazil and Rus-sia have been going through severe adjustments in the face of external and domestic challenges. In the largest emerging markets—the heterogeneous group of BRICS (Brazil, Russia, India, China, and South Africa)— growth has slowed from almost 9 per cent in 2010 to about 4 per cent in 2015, on average, with India being a notable exception. This slowdown reflects both easing growth in China, persistent weakness in South Africa, and steep recessions in Russia since 2014 and in Brazil since 2015.

7

GLOBAL TRENDS

FEB-MAR 2016

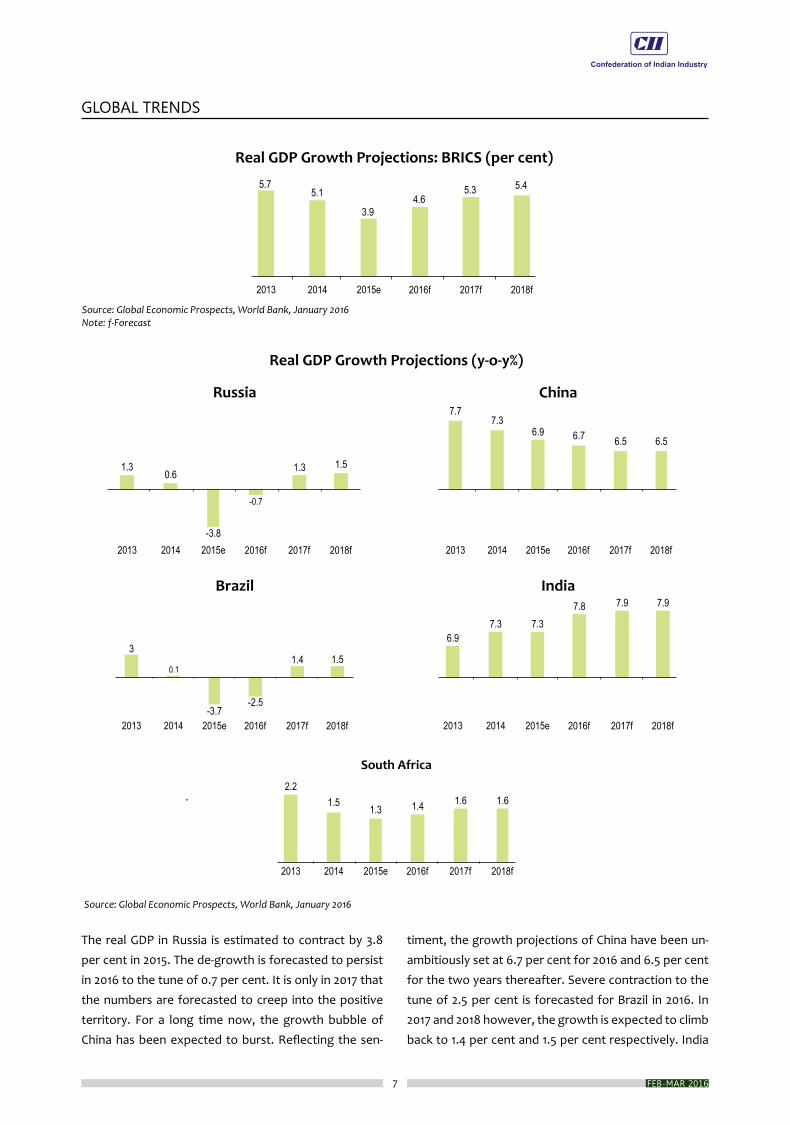

The real GDP in Russia is estimated to contract by 3.8 per cent in 2015. The de-growth is forecasted to persist in 2016 to the tune of 0.7 per cent. It is only in 2017 that the numbers are forecasted to creep into the positive territory. For a long time now, the growth bubble of China has been expected to burst. Reflecting the sen-

timent, the growth projections of China have been un-ambitiously set at 6.7 per cent for 2016 and 6.5 per cent for the two years thereafter. Severe contraction to the tune of 2.5 per cent is forecasted for Brazil in 2016. In 2017 and 2018 however, the growth is expected to climb back to 1.4 per cent and 1.5 per cent respectively. India

ECONOMY MATTERS 8

GLOBAL TRENDS

has the most ambitious forecasts amongst all the BRICS countries. Growth in GDP in 2016 is expected to be 7.8 per cent, even as 7.5 per cent growth has been estimat-ed in 2015. In 2017 and 2018, the growth is forecasted at 7.9 per cent. Growth in GDP in South Africa is expected to improve to 1.4 per cent in 2016, and further to 1.6 per cent in the two years thereafter.

A growth slowdown in BRICS could have global reper-cussions. A sustained 1 per cent decline in growth in the BRICS would reduce growth in other emerging and de-veloping economies by around 0.8 per centand global growth by 0.4 per cent.Growth shocks in Russia would reverberate across the East and Central Asian(ECA) re-gion, reducing ECA growth almost one-for-one. In con-trast, the international spillovers from growth shocks in Brazil, India, and South Africa are not likely to be widespread. In the event of acute stress in any of the BRICS, confidence in emerging market assets more broadly could suffer from contagion effects, in which case spillovers could be considerably larger. China is deeply integrated into supply chains in East Asia and the Pacific, and constitutes a large export market for commodity-exporting countries in Sub-Saharan Africa and Latin America. Brazil trades significantly with neigh-boring Latin American countries, partly as a result of regional free trade agreements. Remittances from Rus-sia account for more than 10 per cent of GDP in several countries in the Caucasus and Central Asia. India is an important source of FDI and official development assis-tance for neighboring countries.

BRICS growth has been slowing since 2010, increasingly because of moderating potential growth. Until 2013, the slowdown was predominantly driven by external factors, but the role of domestic factors has increased since 2014. Among the most important external fac-tors are weak global trade, a steady decline in com-modity prices since 2011, and tightening global financial conditions.A steady decline in commodity prices has set back growth in commodity-exporting BRICS (Russia, Brazil, and South Africa). Prices of oil and metals have declined by 50-60 per cent from their 2011 peaks and are expected to remain low for the next decade. Agricultur-al prices are about 30 per cent below their 2011 peaks. This has sharply worsened the terms of trade of Brazil, Russia, and South Africa. Slowing growth in commodity-

importing BRICS (China, India) itself contributes to sof-tening commodity prices.

Net capital flows to BRICS have undergone bouts of volatility, culminating in sharp and sustained capital outflows in the first half of 2015. The decline in net capi-tal flows largely reflected developments in China: in the first half of 2015, portfolio outflows from China rose ten-fold and net other investment inflows fell by four-fifths from the second half of 2014. Remittance inflows to BRICS have also slowed sharply, from a rate of increase of 15.4 per cent in 2010 to under 3 per cent in 2015. The volatility of capital flows to BRICS has weighed on in-vestment. Since 2010, investment growth in BRICS has slowed from 16 per cent in 2010 to 5 per cent in 2014. A series of country-specific factors have contributed to this, including political and geopolitical uncertainty, structural bottlenecks and uncertainty about major re-form initiatives. The slowdown in remittances may di-rectly impact consumption in these economies.Domes-tic factors include a sustained productivity slowdown and bouts of policy uncertainty. Since 2014 these have overtaken external factors as the main contributors to decelerating BRICS output.Deceleration in productiv-ity growth suggests that a return to pre-global crisis rates of BRICS growth is unlikely. While the productivity growth was slightly above 4 per cent in 2010 and around 1.5 per cent in 2013, it softened further to slightly below the 1 per cent mark in 2014. While it averaged 2 per cent over 1990-08, the average improved to around 4.5 per cent in 2003-08.

The growth slowdown in BRICS has been part cyclical decline from the immediate post-crisis rebound in 2010, part structural slowdown. Hence, a mix of counter -cy-clical fiscal or monetary policy stimulus and structural reforms could be used to support activity. A renewed structural reform push could help lift growth prospects and, to the extent it encourages investment, support domestic demand, as well as help improve investor sen-timent and capital flows. This would be especially useful for countries that have limited room for expansionary fiscal and monetary policies. Since the crisis, the fiscal positionsof BRICS have deteriorated considerably. On average, their fiscal balance has weakened from near-balance in2007 to minus 4 per cent of GDP in 2014. In South Africa, debthas increased by about 19 percentage

9

GLOBAL TRENDS

FEB-MAR 2016

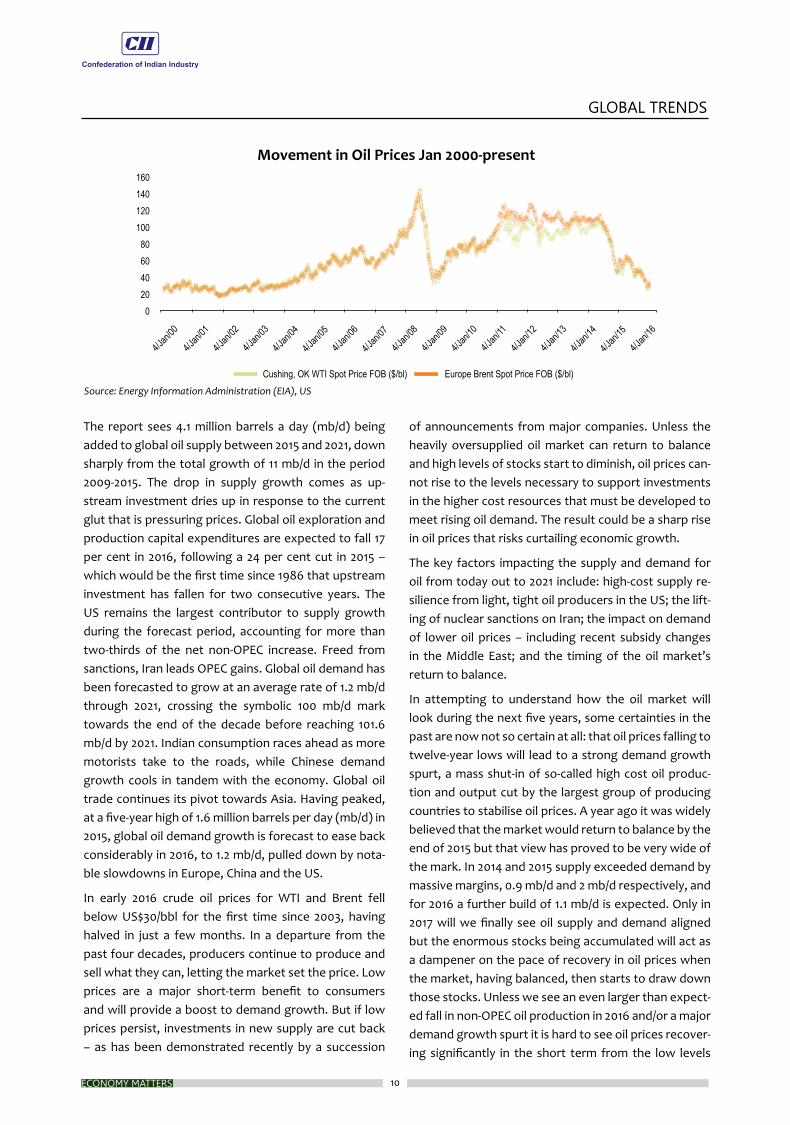

Global oil supply growth is plunging as an extended pe-riod of low prices takes its toll, the International Energy Agency (IEA) said in its annual Medium-Term Oil Market Report released in February 2016. While U.S. light, tight oil (LTO) output is falling steeply for now, the market will begin rebalancing in 2017 – and by 2021 the US and Iran are seen leading production gains among non-OPEC

and OPEC countries, respectively. The report notes that while oil prices should start to rise gradually once the market begins rebalancing, the availability of resources that can be easily and quickly tapped will limit the scope of rallies – at least in the near term. However, the report points to the risk of an oil price spike in the later part of the outlook period arising from insufficient investment.

Tracking the Dynamics of Oil Price Movement: Current Trends and Way Forward

points of GDP since2007, and Brazil and India’s debt lev-els are in excess of 60 per cent of GDP. Monetary policy space has divergedbetween commodity exporters and importers. In Braziland Russia, monetary policy is con-strained by above-target inflation, partly as a result of depreciation. In contrast, low oil prices have reduced inflation and increased room forrate cuts in China and India. However, this room may diminish if inflation re-bounds once oil prices stabilize.

The appropriate policy response also depends onthe source of the external shock. A growth shockmay be more appropriately addressed with fiscalpolicy and structural reforms whereas a financialshock may be more effectively mitigated bymonetary, exchange rate, or financial policies. Theboundaries between these shocks and policies,however, may at times be blurred. This argues,again, for a policy mix of fiscal, monetary, andexchange rate policy coupled with struc-turalreforms.The BRICS slowdown mayturn out to be a sustained, structural decline ingrowth potential rather than a temporary cyclicaldownturn. Structural reforms have collateral benefits ofbuttressing investor confi-dence and liftingdomestic demand—whether in the event ofcyclical or structural external shocks.

Over the next few years, growth in BRICS is likely to face persistent headwinds from low commodity prices, weak

trade, and higher borrowing costs. Meanwhile, produc-tivity growth is likely to remain weak as populations age in large emerging markets, and investment weakness slows the adoption of new technologies. A weaker ex-ternal environment, and slowing growth, may further erode policy buffers and constrain the use of counter-cyclical stimulus to support activity. The strengthen-ing recovery in advanced markets is expected to only partially offset these risks. Continued weakness or a further slowdown in BRICS growth could add to the challenges faced by emerging and frontier markets from a deteriorating external environment. Activity in close trading partners of BRICS and in commodity ex-porters would be particularly susceptible to a setback. If, instead of the projected pickup, BRICS growth slows further—by as much as the average growth disappoint-ment over 2010-14—and if financial conditions tight-ened moderately—such as during the financial market turmoil of the summer of 2015—global growth could be cut by one-third in 2016. Policy makers in emerging mar-kets may need to support activity with fiscal and policy stimulus, at least where policy buffers are sufficient. In all cases, countries could derive substantial gains from well-designed, credible structural reforms that retain investor confidence and capital flows in the short-run, and that lift growth prospects for the long-run.

ECONOMY MATTERS 10

GLOBAL TRENDS

The report sees 4.1 million barrels a day (mb/d) being added to global oil supply between 2015 and 2021, down sharply from the total growth of 11 mb/d in the period 2009-2015. The drop in supply growth comes as up-stream investment dries up in response to the current glut that is pressuring prices. Global oil exploration and production capital expenditures are expected to fall 17 per cent in 2016, following a 24 per cent cut in 2015 – which would be the first time since 1986 that upstream investment has fallen for two consecutive years. The US remains the largest contributor to supply growth during the forecast period, accounting for more than two-thirds of the net non-OPEC increase. Freed from sanctions, Iran leads OPEC gains. Global oil demand has been forecasted to grow at an average rate of 1.2 mb/d through 2021, crossing the symbolic 100 mb/d mark towards the end of the decade before reaching 101.6 mb/d by 2021. Indian consumption races ahead as more motorists take to the roads, while Chinese demand growth cools in tandem with the economy. Global oil trade continues its pivot towards Asia. Having peaked, at a five-year high of 1.6 million barrels per day (mb/d) in 2015, global oil demand growth is forecast to ease back considerably in 2016, to 1.2 mb/d, pulled down by nota-ble slowdowns in Europe, China and the US.

In early 2016 crude oil prices for WTI and Brent fell below US$30/bbl for the first time since 2003, having halved in just a few months. In a departure from the past four decades, producers continue to produce and sell what they can, letting the market set the price. Low prices are a major short-term benefit to consumers and will provide a boost to demand growth. But if low prices persist, investments in new supply are cut back – as has been demonstrated recently by a succession

of announcements from major companies. Unless the heavily oversupplied oil market can return to balance and high levels of stocks start to diminish, oil prices can-not rise to the levels necessary to support investments in the higher cost resources that must be developed to meet rising oil demand. The result could be a sharp rise in oil prices that risks curtailing economic growth.

The key factors impacting the supply and demand for oil from today out to 2021 include: high-cost supply re-silience from light, tight oil producers in the US; the lift-ing of nuclear sanctions on Iran; the impact on demand of lower oil prices – including recent subsidy changes in the Middle East; and the timing of the oil market’s return to balance.

In attempting to understand how the oil market will look during the next five years, some certainties in the past are now not so certain at all: that oil prices falling to twelve-year lows will lead to a strong demand growth spurt, a mass shut-in of so-called high cost oil produc-tion and output cut by the largest group of producing countries to stabilise oil prices. A year ago it was widely believed that the market would return to balance by the end of 2015 but that view has proved to be very wide of the mark. In 2014 and 2015 supply exceeded demand by massive margins, 0.9 mb/d and 2 mb/d respectively, and for 2016 a further build of 1.1 mb/d is expected. Only in 2017 will we finally see oil supply and demand aligned but the enormous stocks being accumulated will act as a dampener on the pace of recovery in oil prices when the market, having balanced, then starts to draw down those stocks. Unless we see an even larger than expect-ed fall in non-OPEC oil production in 2016 and/or a major demand growth spurt it is hard to see oil prices recover-ing significantly in the short term from the low levels

11

GLOBAL TRENDS

FEB-MAR 2016

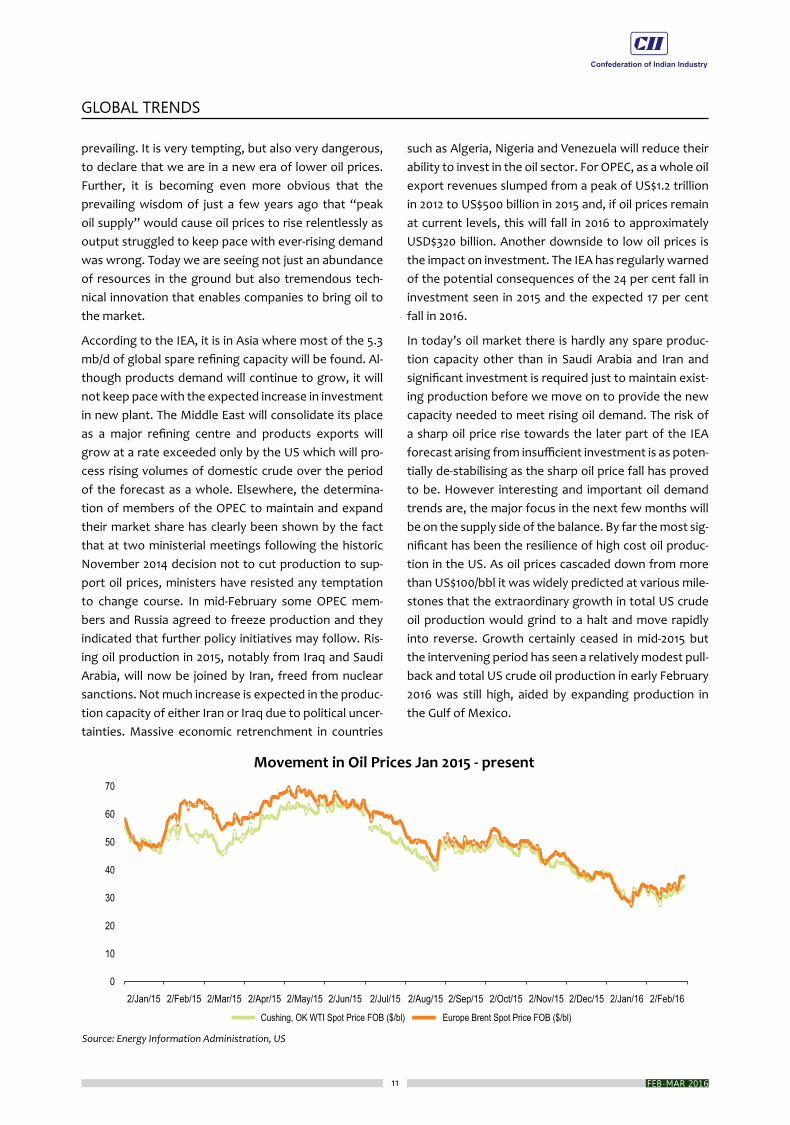

prevailing. It is very tempting, but also very dangerous, to declare that we are in a new era of lower oil prices. Further, it is becoming even more obvious that the prevailing wisdom of just a few years ago that “peak oil supply” would cause oil prices to rise relentlessly as output struggled to keep pace with ever-rising demand was wrong. Today we are seeing not just an abundance of resources in the ground but also tremendous tech-nical innovation that enables companies to bring oil to the market.

According to the IEA, it is in Asia where most of the 5.3 mb/d of global spare refining capacity will be found. Al-though products demand will continue to grow, it will not keep pace with the expected increase in investment in new plant. The Middle East will consolidate its place as a major refining centre and products exports will grow at a rate exceeded only by the US which will pro-cess rising volumes of domestic crude over the period of the forecast as a whole. Elsewhere, the determina-tion of members of the OPEC to maintain and expand their market share has clearly been shown by the fact that at two ministerial meetings following the historic November 2014 decision not to cut production to sup-port oil prices, ministers have resisted any temptation to change course. In mid-February some OPEC mem-bers and Russia agreed to freeze production and they indicated that further policy initiatives may follow. Ris-ing oil production in 2015, notably from Iraq and Saudi Arabia, will now be joined by Iran, freed from nuclear sanctions. Not much increase is expected in the produc-tion capacity of either Iran or Iraq due to political uncer-tainties. Massive economic retrenchment in countries

such as Algeria, Nigeria and Venezuela will reduce their ability to invest in the oil sector. For OPEC, as a whole oil export revenues slumped from a peak of US$1.2 trillion in 2012 to US$500 billion in 2015 and, if oil prices remain at current levels, this will fall in 2016 to approximately USD$320 billion. Another downside to low oil prices is the impact on investment. The IEA has regularly warned of the potential consequences of the 24 per cent fall in investment seen in 2015 and the expected 17 per cent fall in 2016.

In today’s oil market there is hardly any spare produc-tion capacity other than in Saudi Arabia and Iran and significant investment is required just to maintain exist-ing production before we move on to provide the new capacity needed to meet rising oil demand. The risk of a sharp oil price rise towards the later part of the IEA forecast arising from insufficient investment is as poten-tially de-stabilising as the sharp oil price fall has proved to be. However interesting and important oil demand trends are, the major focus in the next few months will be on the supply side of the balance. By far the most sig-nificant has been the resilience of high cost oil produc-tion in the US. As oil prices cascaded down from more than US$100/bbl it was widely predicted at various mile-stones that the extraordinary growth in total US crude oil production would grind to a halt and move rapidly into reverse. Growth certainly ceased in mid-2015 but the intervening period has seen a relatively modest pull-back and total US crude oil production in early February 2016 was still high, aided by expanding production in the Gulf of Mexico.

ECONOMY MATTERS 12

DOMESTIC TRENDS

GDP Growth Seen Accelerating to 7.6% in FY16

As per the advance estimates released by Central Statistical Organisation (CSO), GDP growth is expected to rise to 7.6 per cent in FY16 as com-

pared with the revised estimates of 7.2 per cent in the previous year, aided largely by growth in the manufac-turing sector. If the new projection materialises, India will be the fastest growing major economy in the world, overtaking China. The latest projection is a shade bet-ter than the finance ministry’s earlier estimate of seven to 7.5 per cent. The acceleration in the manufacturing sector shows that the government’s policy direction is bearing fruit. The Make in India campaign with its objec-tive of raising the growth rate in the manufacturing sec-tor has begun to make an impact. Policy measures need to focus on a revival in project execution in manufactur-ing, real estate and infrastructure.

The Economic Survey FY16 which was released recently has enunciated that in a weak global scenario, India’s

growth has been largely positive on the back of con-sumption. Industry growth is estimated to have accel-erated while services growth remained robust. Growth in agricultural slackened due to two successive years of below average monsoon.As per the Survey, GDP growth is expected to reach 7.0-7.75 per cent (GDP at market prices) inFY2017, lower than its potential GDP growth of 8.0-10.0 per cent, on the assumption of a fa-vourable monsoon and possible boost to consumption from implementation of 7th Pay Commission. However, weakness in global demand and drag on consumption from a rise in oil prices were cited as key risks to this outlook.

Looking ahead, the macro-economic prospects for the Indian economy have improved considerably in the last few quarters. The International Monetary Fund (IMF) in January 2016 kept its growth forecast for India un-changed at 7.5 per cent in 2016-17 while it lowered its global growth projection in an update to the World Economic Outlook released in October.India’s economy is buoyant in the global context, but from a domestic perspective, it may require some support to revive rural demand and rejuvenate public sector banks.

13

DOMESTIC TRENDS

FEB-MAR 2016

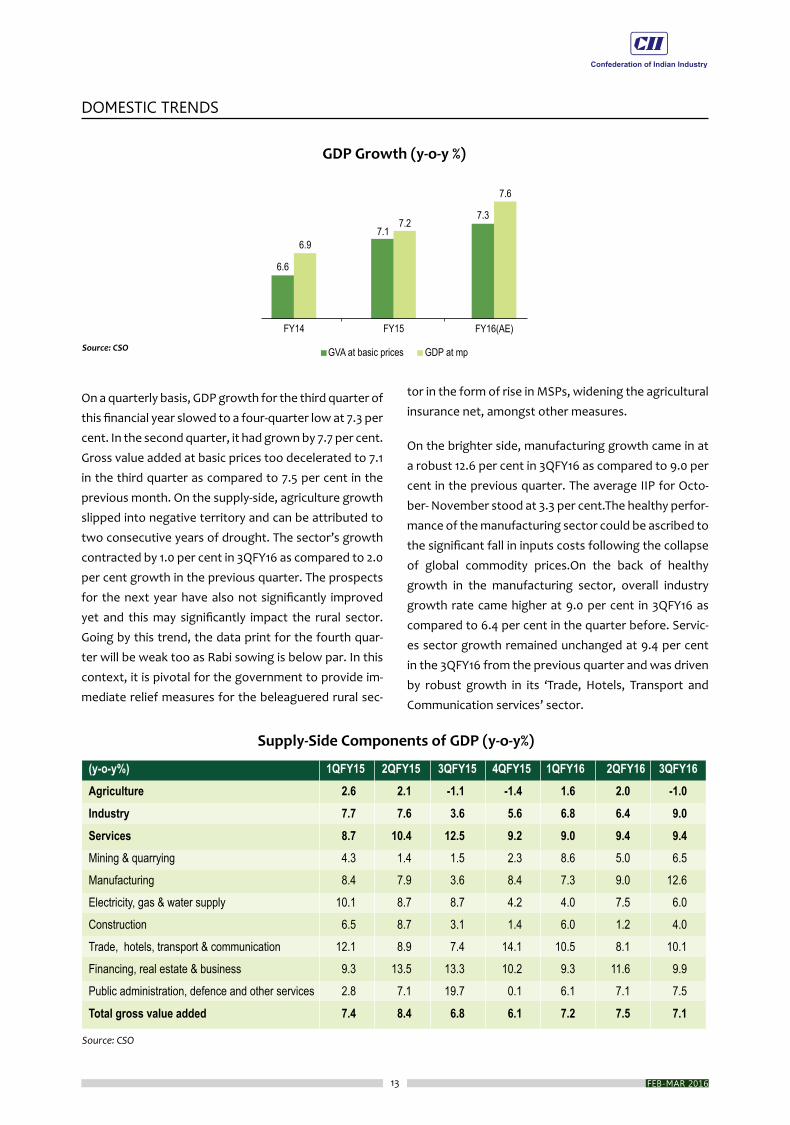

On a quarterly basis, GDP growth for the third quarter of this financial year slowed to a four-quarter low at 7.3 per cent. In the second quarter, it had grown by 7.7 per cent. Gross value added at basic prices too decelerated to 7.1 in the third quarter as compared to 7.5 per cent in the previous month. On the supply-side, agriculture growth slipped into negative territory and can be attributed to two consecutive years of drought. The sector’s growth contracted by 1.0 per cent in 3QFY16 as compared to 2.0 per cent growth in the previous quarter. The prospects for the next year have also not significantly improved yet and this may significantly impact the rural sector. Going by this trend, the data print for the fourth quar-ter will be weak too as Rabi sowing is below par. In this context, it is pivotal for the government to provide im-mediate relief measures for the beleaguered rural sec-

tor in the form of rise in MSPs, widening the agricultural insurance net, amongst other measures.

On the brighter side, manufacturing growth came in at a robust 12.6 per cent in 3QFY16 as compared to 9.0 per cent in the previous quarter. The average IIP for Octo-ber- November stood at 3.3 per cent.The healthy perfor-mance of the manufacturing sector could be ascribed to the significant fall in inputs costs following the collapse of global commodity prices.On the back of healthy growth in the manufacturing sector, overall industry growth rate came higher at 9.0 per cent in 3QFY16 as compared to 6.4 per cent in the quarter before. Servic-es sector growth remained unchanged at 9.4 per cent in the 3QFY16 from the previous quarter and was driven by robust growth in its ‘Trade, Hotels, Transport and Communication services’ sector.

ECONOMY MATTERS 14

DOMESTIC TRENDS

Industrial production growth contracted by 1.5 per cent in January 2016 – its third consecutive month of de-growth. Weaker financial market sentiment, slower investment revival, vulnerable external demand and dis-ruption in production on account of Chennai rains were the key factors impacting production. Sector-wise, man-

ufacturing, capital goods and consumer non-durable were the key drag on the IIP print during the month. On a cumulative basis, IIP growth remained steady at 2.7 per cent during April-January FY16 period. In FY16, we expect industrial production to grow at a higher rate as compared to the previous fiscal on the back of policy aided domestic upturn and lower commodity prices.

OutlookSignificant improvement anticipated in GDP growth which is expected to go up to 7.6 per cent in 2015-16 as against 7.2 per cent in the corresponding period last year is noteworthy & indicates that Indian economy is at the threshold of a cyclical upturn. Economic conditions would improve in the coming quarters and the new growth opportunities would emerge once reform initiatives announced by the government take root. CII looks forward to a reform-centric budget which would put in place bold measures to remove supply bottlenecks and in turn spark a virtuous cycle of investment and growth.

Industrial Production Continues to Remain in Red

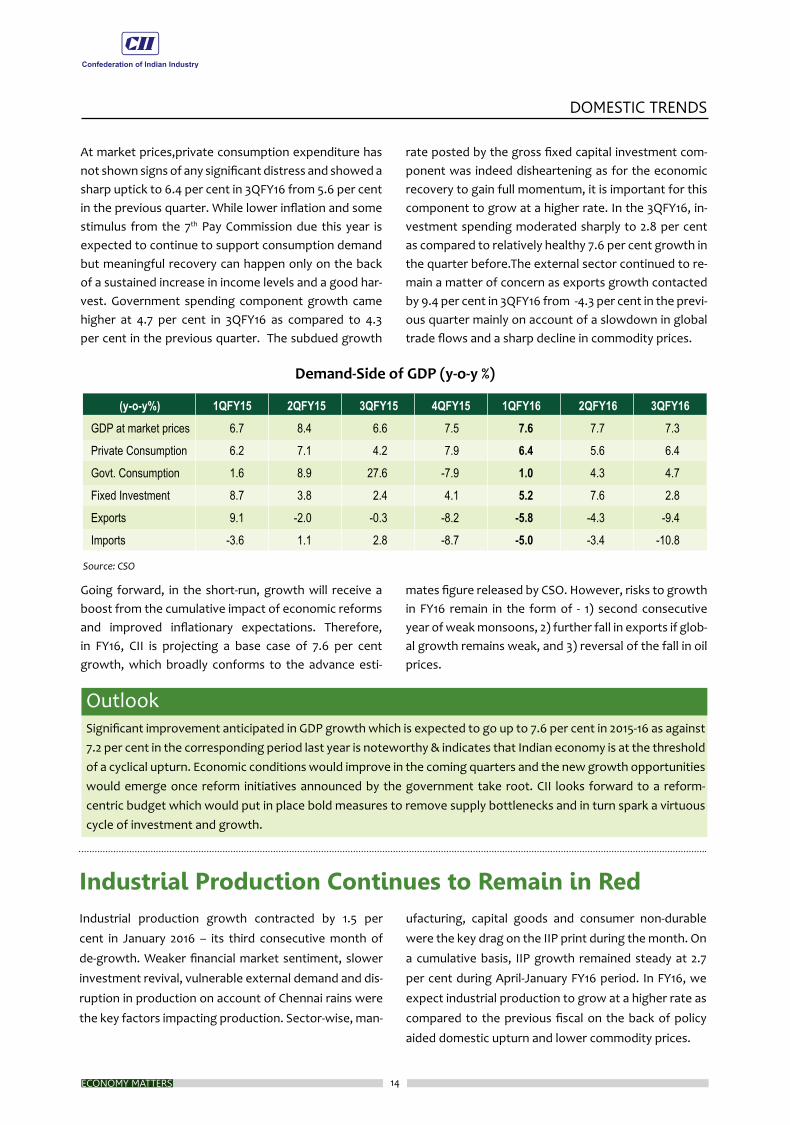

At market prices,private consumption expenditure has not shown signs of any significant distress and showed a sharp uptick to 6.4 per cent in 3QFY16 from 5.6 per cent in the previous quarter. While lower inflation and some stimulus from the 7th Pay Commission due this year is expected to continue to support consumption demand but meaningful recovery can happen only on the back of a sustained increase in income levels and a good har-vest. Government spending component growth came higher at 4.7 per cent in 3QFY16 as compared to 4.3 per cent in the previous quarter. The subdued growth

Going forward, in the short-run, growth will receive a boost from the cumulative impact of economic reforms and improved inflationary expectations. Therefore, in FY16, CII is projecting a base case of 7.6 per cent growth, which broadly conforms to the advance esti-

rate posted by the gross fixed capital investment com-ponent was indeed disheartening as for the economic recovery to gain full momentum, it is important for this component to grow at a higher rate. In the 3QFY16, in-vestment spending moderated sharply to 2.8 per cent as compared to relatively healthy 7.6 per cent growth in the quarter before.The external sector continued to re-main a matter of concern as exports growth contacted by 9.4 per cent in 3QFY16 from -4.3 per cent in the previ-ous quarter mainly on account of a slowdown in global trade flows and a sharp decline in commodity prices.

mates figure released by CSO. However, risks to growth in FY16 remain in the form of - 1) second consecutive year of weak monsoons, 2) further fall in exports if glob-al growth remains weak, and 3) reversal of the fall in oil prices.

15

DOMESTIC TRENDS

FEB-MAR 2016

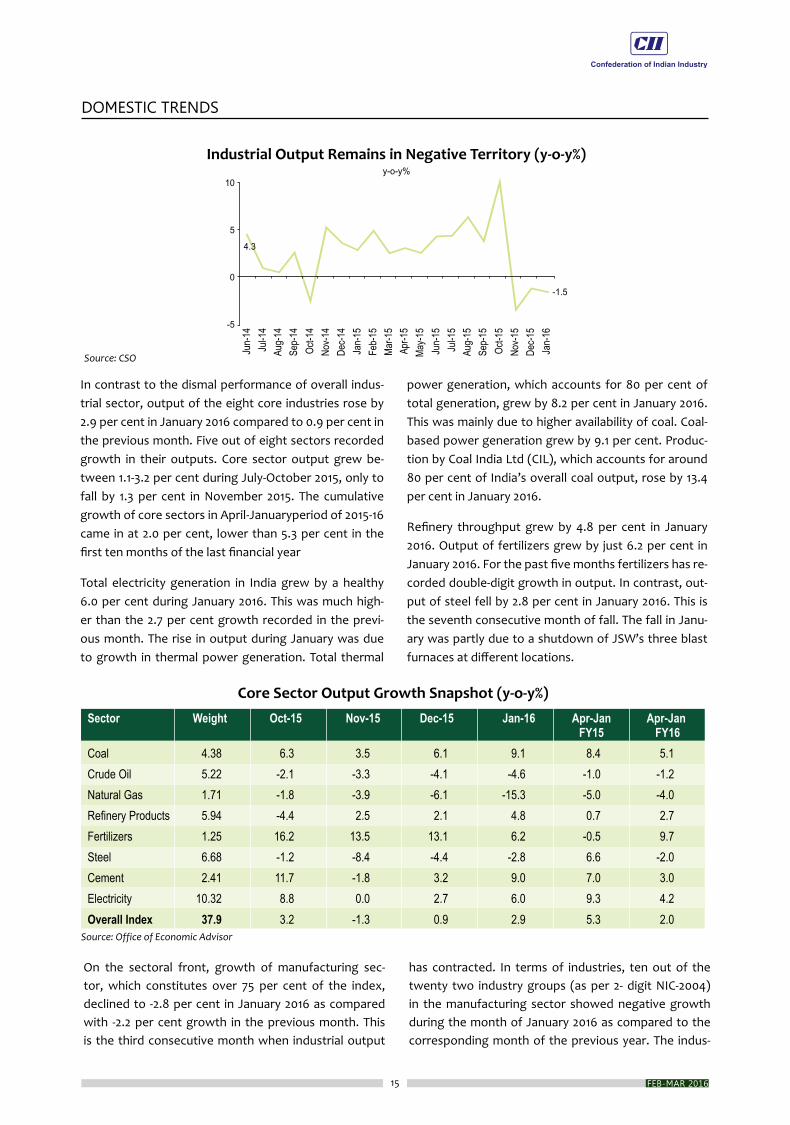

In contrast to the dismal performance of overall indus-trial sector, output of the eight core industries rose by 2.9 per cent in January 2016 compared to 0.9 per cent in the previous month. Five out of eight sectors recorded growth in their outputs. Core sector output grew be-tween 1.1-3.2 per cent during July-October 2015, only to fall by 1.3 per cent in November 2015. The cumulative growth of core sectors in April-Januaryperiod of 2015-16 came in at 2.0 per cent, lower than 5.3 per cent in the first ten months of the last financial year

Total electricity generation in India grew by a healthy 6.0 per cent during January 2016. This was much high-er than the 2.7 per cent growth recorded in the previ-ous month. The rise in output during January was due to growth in thermal power generation. Total thermal

power generation, which accounts for 80 per cent of total generation, grew by 8.2 per cent in January 2016. This was mainly due to higher availability of coal. Coal-based power generation grew by 9.1 per cent. Produc-tion by Coal India Ltd (CIL), which accounts for around 80 per cent of India’s overall coal output, rose by 13.4 per cent in January 2016.

Refinery throughput grew by 4.8 per cent in January 2016. Output of fertilizers grew by just 6.2 per cent in January 2016. For the past five months fertilizers has re-corded double-digit growth in output. In contrast, out-put of steel fell by 2.8 per cent in January 2016. This is the seventh consecutive month of fall. The fall in Janu-ary was partly due to a shutdown of JSW’s three blast furnaces at different locations.

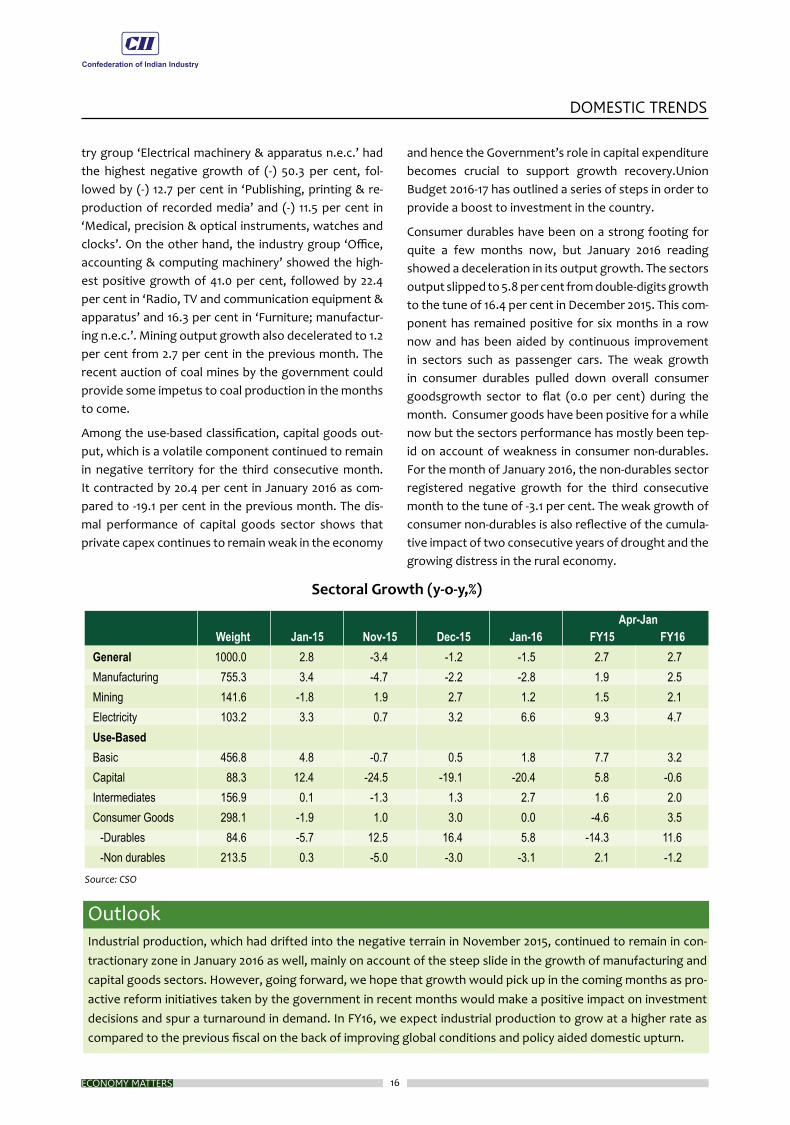

On the sectoral front, growth of manufacturing sec-tor, which constitutes over 75 per cent of the index, declined to -2.8 per cent in January 2016 as compared with -2.2 per cent growth in the previous month. This is the third consecutive month when industrial output

has contracted. In terms of industries, ten out of the twenty two industry groups (as per 2- digit NIC-2004) in the manufacturing sector showed negative growth during the month of January 2016 as compared to the corresponding month of the previous year. The indus-

ECONOMY MATTERS 16

DOMESTIC TRENDS

OutlookIndustrial production, which had drifted into the negative terrain in November 2015, continued to remain in con-tractionary zone in January 2016 as well, mainly on account of the steep slide in the growth of manufacturing and capital goods sectors. However, going forward, we hope that growth would pick up in the coming months as pro-active reform initiatives taken by the government in recent months would make a positive impact on investment decisions and spur a turnaround in demand. In FY16, we expect industrial production to grow at a higher rate as compared to the previous fiscal on the back of improving global conditions and policy aided domestic upturn.

try group ‘Electrical machinery & apparatus n.e.c.’ had the highest negative growth of (-) 50.3 per cent, fol-lowed by (-) 12.7 per cent in ‘Publishing, printing & re-production of recorded media’ and (-) 11.5 per cent in ‘Medical, precision & optical instruments, watches and clocks’. On the other hand, the industry group ‘Office, accounting & computing machinery’ showed the high-est positive growth of 41.0 per cent, followed by 22.4 per cent in ‘Radio, TV and communication equipment & apparatus’ and 16.3 per cent in ‘Furniture; manufactur-ing n.e.c.’. Mining output growth also decelerated to 1.2 per cent from 2.7 per cent in the previous month. The recent auction of coal mines by the government could provide some impetus to coal production in the months to come.

Among the use-based classification, capital goods out-put, which is a volatile component continued to remain in negative territory for the third consecutive month. It contracted by 20.4 per cent in January 2016 as com-pared to -19.1 per cent in the previous month. The dis-mal performance of capital goods sector shows that private capex continues to remain weak in the economy

and hence the Government’s role in capital expenditure becomes crucial to support growth recovery.Union Budget 2016-17 has outlined a series of steps in order to provide a boost to investment in the country.

Consumer durables have been on a strong footing for quite a few months now, but January 2016 reading showed a deceleration in its output growth. The sectors output slipped to 5.8 per cent from double-digits growth to the tune of 16.4 per cent in December 2015. This com-ponent has remained positive for six months in a row now and has been aided by continuous improvement in sectors such as passenger cars. The weak growth in consumer durables pulled down overall consumer goodsgrowth sector to flat (0.0 per cent) during the month. Consumer goods have been positive for a while now but the sectors performance has mostly been tep-id on account of weakness in consumer non-durables. For the month of January 2016, the non-durables sector registered negative growth for the third consecutive month to the tune of -3.1 per cent. The weak growth of consumer non-durables is also reflective of the cumula-tive impact of two consecutive years of drought and the growing distress in the rural economy.

17

DOMESTIC TRENDS

FEB-MAR 2016

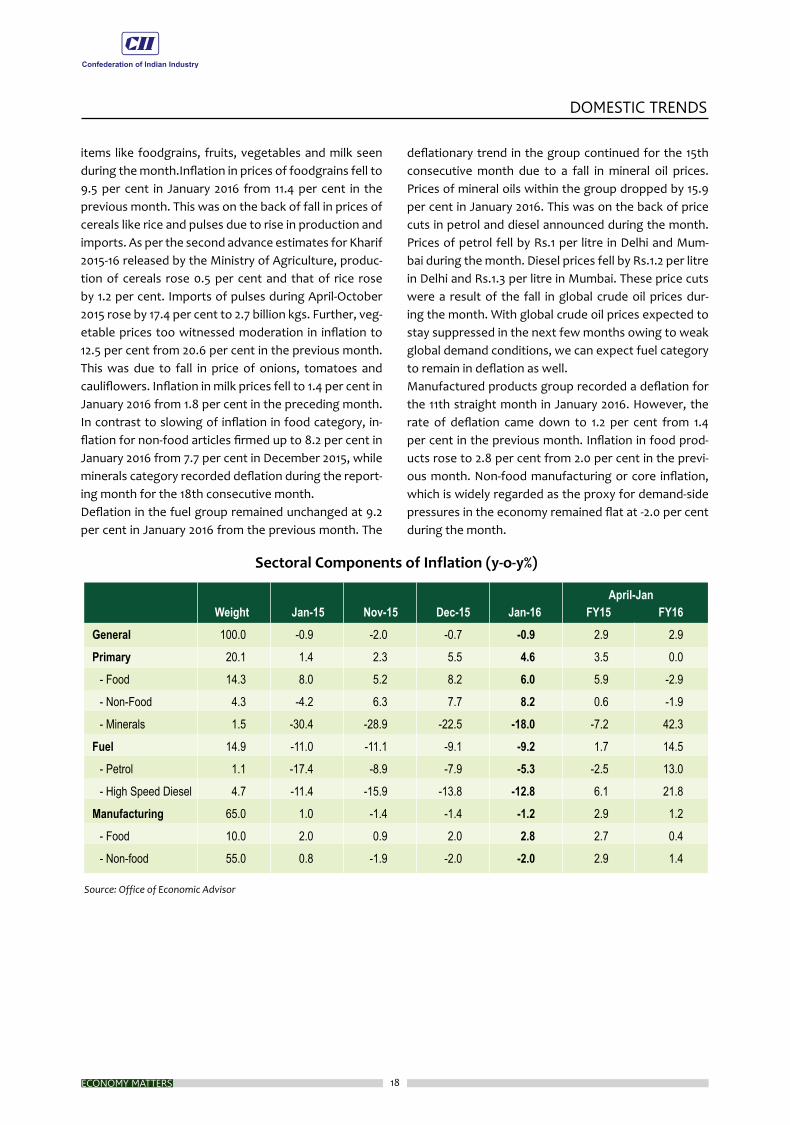

CPI Inflation 30 bps Lower than RBI’s Target of 6% for Jan 2016Wholesale Price Index (WPI)-based inflation print showed that the current deflationary spell has extend-ed by yet another month. Wholesale price inflation turned negative in November 2014, after falling continu-ously for a year. The rate of deflation stood at 0.9 per cent in January 2016 as compared to -0.7 per cent in the previous month. This marks the 15th consecutive month of year-on-year fall in wholesale prices. Also, this is the most prolonged deflationary phase the country has witnessed in at least the last three decades. Deflation in fuel and manufacturing groups were the key drivers behind the negative WPI print in the month of January 2016. Going ahead, we expect WPI to remain in negative zone till atleast Q1FY17 as crude oil prices still remain be-nign and demand pressures remain subdued. Sustained decline in WPI is however good news for corporate as WPI is input price for manufacturing process.Meanwhile, CPI based inflation, the one which the Cen-tral Bank tracks in taking its monetary policy decisions remained sticky at 5.7 per cent in January 2016 as com-

Inflation in primary article prices fell to 4.6 per cent in January 2016 from 5.5 per cent in the previous month. This was on account of a fall in inflation in food articles. The deceleration in primary food articles inflation was in contrast with the rise in CPI food inflation seen dur-ing the month. It is normally observed that CPI food

pared to 5.6 per cent in the previous month. It is heart-ening to note that the January 2016 print is 30 basis points (bps) lower than the RBI’s target of 6.0 per cent. However, the sequential momentum of CPI inflation edged up to 0.2 per cent on a month-on-month basis as compared to -0.4 per cent on month-on-month basis posted in the previous month. The main driver behind CPI inflation during the month was food inflation, which rose to 6.8 per cent as compared to 6.4 per cent posted in December 2015. However, in some good news, pulses inflation fell for the first time in 13 months, but still high at 43.3 per cent. Two consecutive years of draught and untimely rainfall last year have raised the upside risks for food inflation going forward as well. Core inflation came at 5.2 per cent in January 2016 as compared to 5.4 per cent in the previous month. Going ahead, the subdued domestic demand coupled with weak interna-tional crude prices are likely to support core inflation, which we expect to stay below 5 per cent in the coming months.

prices start reflecting the trend in WPI food articles prices with a lag of 2-3 months.Prices of primary food articles witnessed an inflation to the tune of 6 per cent during January 2016 as compared to high of 8.2 per cent witnessed in the last month. The primary drivers of fall in primary food inflation were deceleration in prices of

ECONOMY MATTERS 18

DOMESTIC TRENDS

items like foodgrains, fruits, vegetables and milk seen during the month.Inflation in prices of foodgrains fell to 9.5 per cent in January 2016 from 11.4 per cent in the previous month. This was on the back of fall in prices of cereals like rice and pulses due to rise in production and imports. As per the second advance estimates for Kharif 2015-16 released by the Ministry of Agriculture, produc-tion of cereals rose 0.5 per cent and that of rice rose by 1.2 per cent. Imports of pulses during April-October 2015 rose by 17.4 per cent to 2.7 billion kgs. Further, veg-etable prices too witnessed moderation in inflation to 12.5 per cent from 20.6 per cent in the previous month. This was due to fall in price of onions, tomatoes and cauliflowers. Inflation in milk prices fell to 1.4 per cent in January 2016 from 1.8 per cent in the preceding month. In contrast to slowing of inflation in food category, in-flation for non-food articles firmed up to 8.2 per cent in January 2016 from 7.7 per cent in December 2015, while minerals category recorded deflation during the report-ing month for the 18th consecutive month.Deflation in the fuel group remained unchanged at 9.2 per cent in January 2016 from the previous month. The

deflationary trend in the group continued for the 15th consecutive month due to a fall in mineral oil prices.Prices of mineral oils within the group dropped by 15.9 per cent in January 2016. This was on the back of price cuts in petrol and diesel announced during the month. Prices of petrol fell by Rs.1 per litre in Delhi and Mum-bai during the month. Diesel prices fell by Rs.1.2 per litre in Delhi and Rs.1.3 per litre in Mumbai. These price cuts were a result of the fall in global crude oil prices dur-ing the month. With global crude oil prices expected to stay suppressed in the next few months owing to weak global demand conditions, we can expect fuel category to remain in deflation as well.Manufactured products group recorded a deflation for the 11th straight month in January 2016. However, the rate of deflation came down to 1.2 per cent from 1.4 per cent in the previous month. Inflation in food prod-ucts rose to 2.8 per cent from 2.0 per cent in the previ-ous month. Non-food manufacturing or core inflation, which is widely regarded as the proxy for demand-side pressures in the economy remained flat at -2.0 per cent during the month.

19

DOMESTIC TRENDS

FEB-MAR 2016

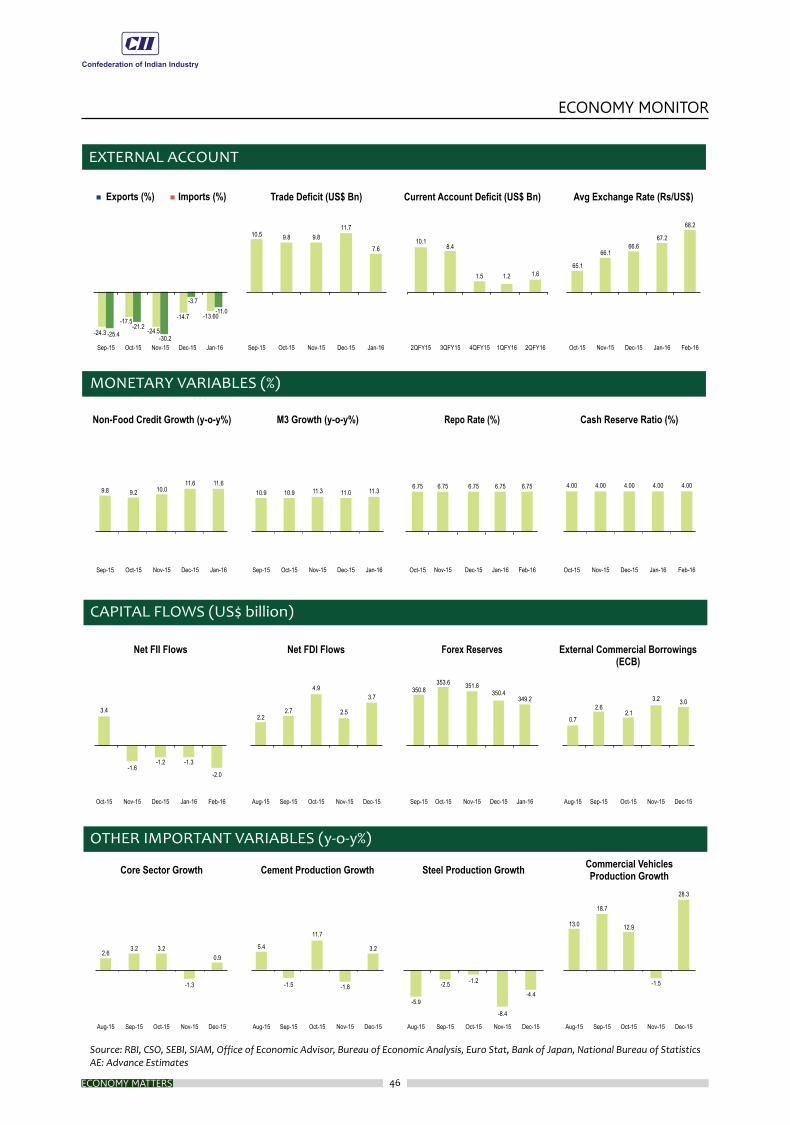

Merchandise exports in January 2016 fell 13.6 per cent from a year earlier to US$21.07 billion - declining for the 14th consecutive month - while a contraction in imports narrowed the trade gap to an 11-month low. Contrac-tion remained widespread, with petroleum products, iron ore, engineering goods, oil seeds and cereals post-ing the steepest declines (on a year-on-year basis). Meanwhile, tea, jute manufactures, drugs and pharma-ceuticals recorded positive growth. The weak exports performance reflects weakness in global demand envi-ronment as well as steep decline in commodity prices. On a cumulative basis, cumulative exports contracted by 17.5 per cent to US$218 billion as against US$264 bil-lion during the same period last year.

Exports of drugs and pharmaceuticals (22.05 per cent), chemicals (8.03 per cent), electronic goods 16.49 per cent), gems and jewellery (12.33 per cent) increased in January 2016, while exports of leather & leather prod-ucts (-5.0 per cent), engineering goods (-21.76 per cent) and petroleum products (-29.94 per cent) contracted. Given the recent trend, exports are likely to fall below US$300 billion mark, for the first time since FY11.This is certainly not good news as India aims to take exports

Merchandise trade deficit narrowed to US$7.6 billion in January 2016 as against the prior reading of US$ 11.7 bil-lion deficit and the lowest since February 2015. Both exports and imports contracted during the month. On a cumulative basis, the trade deficit for April-January FY16 is lower at US$ 106.85 billion as compared to US$119.6

of goods and services to US$900 billion by 2020 and raise the country’s share in world exports to 3.5 per cent from 2 per cent now. Exports in the past four fiscal years have been hovering at around US$300 billion.

Worried by the continuous decline in exports, the gov-ernment has raised duty drawback rates for exporters and implemented the interest stabilization scheme in November 2015. While the increase in duty drawback rates will help exporters recover higher input tax outgo that they pay during the process of making the final product, the interest stabilization scheme will allow ex-porters to receive bank loans at a lower rate of inter-est.

Imports too contracted by 11.1 per cent in January 2016 as against contraction of 3.7 per cent posted in Decem-ber 2015. During April-January FY16, India’s cumulative imports were US$324.5 billion. This is a 15 per cent drop from US$383.8 billion, the cumulative figure for the same period last year. Oil imports dropped 39.0 per cent to US$5.02 billion while non-oil imports declined 1.4 per cent to US$23.68 billion. Non-oil, non-gold im-ports, seen as a measure of domestic demand, fell 7.4 per cent to US$20.78 billion during the month.

billion in the same period last fiscal year. Though im-proving domestic competitiveness through structural reforms is crucial to improve exports performance, we believe that can only materialize in the medium-term. In the near-term, a weaker Rupee can act as a catalyst to revive competitiveness.

Trade Deficit Narrows in January 2016

ECONOMY MATTERS 20

DOMESTIC TRENDS

RBI in its policy document mentioned that in keeping with the Government’s Start-up India initiative, it will take steps to ease doing business and contribute to an ecosystem that is conducive for growth of start-ups. These measures will create an enabling framework for receiving foreign venture capital, differing contractual structures embedded in investment instruments, defer-ring receipt of considerations for transfer of ownership, facilities for escrow arrangements and simplification of documentation and reporting procedures.

On the growth front, RBI noted that for 2016-17, “Growth is expected to strengthen gradually, not-withstanding significant headwinds. Expectations of a normal monsoon after two consecutive years of rain-fall deficiency, the large positive terms of trade gain, improving real incomes of households and lower input

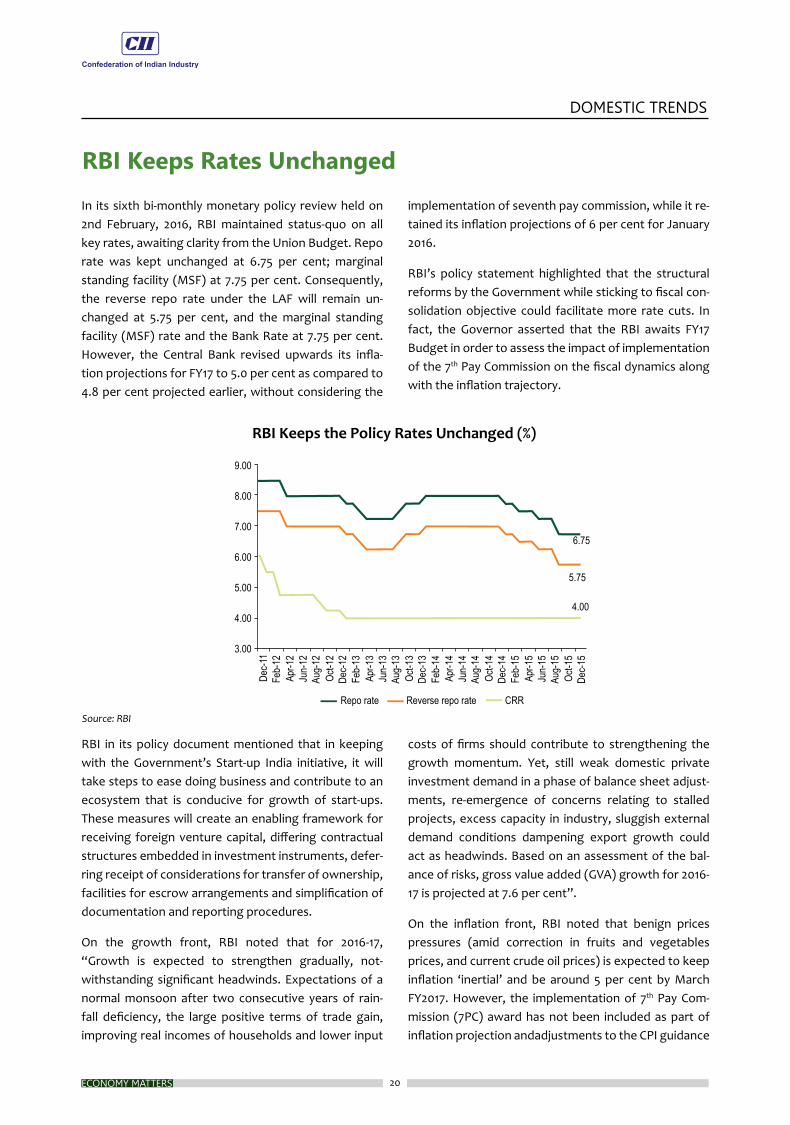

In its sixth bi-monthly monetary policy review held on 2nd February, 2016, RBI maintained status-quo on all key rates, awaiting clarity from the Union Budget. Repo rate was kept unchanged at 6.75 per cent; marginal standing facility (MSF) at 7.75 per cent. Consequently, the reverse repo rate under the LAF will remain un-changed at 5.75 per cent, and the marginal standing facility (MSF) rate and the Bank Rate at 7.75 per cent. However, the Central Bank revised upwards its infla-tion projections for FY17 to 5.0 per cent as compared to 4.8 per cent projected earlier, without considering the

costs of firms should contribute to strengthening the growth momentum. Yet, still weak domestic private investment demand in a phase of balance sheet adjust-ments, re-emergence of concerns relating to stalled projects, excess capacity in industry, sluggish external demand conditions dampening export growth could act as headwinds. Based on an assessment of the bal-ance of risks, gross value added (GVA) growth for 2016-17 is projected at 7.6 per cent”.

On the inflation front, RBI noted that benign prices pressures (amid correction in fruits and vegetables prices, and current crude oil prices) is expected to keep inflation ‘inertial’ and be around 5 per cent by March FY2017. However, the implementation of 7th Pay Com-mission (7PC) award has not been included as part of inflation projection andadjustments to the CPI guidance

implementation of seventh pay commission, while it re-tained its inflation projections of 6 per cent for January 2016.

RBI’s policy statement highlighted that the structural reforms by the Government while sticking to fiscal con-solidation objective could facilitate more rate cuts. In fact, the Governor asserted that the RBI awaits FY17 Budget in order to assess the impact of implementation of the 7th Pay Commission on the fiscal dynamics along with the inflation trajectory.

RBI Keeps Rates Unchanged

21

DOMESTIC TRENDS

FEB-MAR 2016

will be made once clarity on the seventh pay commis-sion emerges.The Central Bank will adjust its forecast path as and when more clarity emerges on the timing of implementation. Vagaries in the spatial and temporal

The Economic Survey 2015-16 which was tabled in the Parliament on 26th February, 2016, pointed out the positives which are there in the current Indian situation, despite the challenges posed by the global economic slowdown. CII has often highlighted the need for spe-cial attention to the impaired financial positions of Pub-lic Sector Banks, and some corporate houses and happy to see a significant portion of the commentary in the Economic Survey being dedicated to that problem. It is key to set up the National Asset Management Company which would be able to wipe the toxic assets off the books of banks.

The Economic Survey quoted twin balance sheet (TBS) challenge (i.e., the impaired financial positions of the Public Sector Banks (PSBs) and some large cor-porate houses) as a critical impediment to private investment and full-fledged recovery in the Indian economy. The Survey enunciated that for solving this challenge would require the 4 Rs: Recognition (valu-ing assets as close to their true value as possible), Recapitalization(safeguarding capital positions via say, infusion of equity), Resolution (selling/rehabilitating stressed assets), and Reform(setting incentives to pre-vent future repetition of the problem).

Further on the growth front, the Survey projected gross domestic product (GDP) growth of 7.0-7.75 per cent in 2016-17 at a time the Central Statistics Office has esti-mated economic growth at 7.6 per cent for 2015-16, signalling the economy may either slow or is unlikely

distribution of the monsoon and the impact of adverse geo-political events on commodity prices and financial markets add additional uncertainty to the baseline fore-cast.

to see any significant acceleration next year. “With global slowdown likely to persist, the chances of In-dia’s growth rate in 2016-17 increasing significantly be-yond 2015-16 levels are not very high. The wider range in the forecast this time reflects the range of possibili-ties for exogenous developments, from a rebound in agriculture to a full-fledged international crisis; it also reflects uncertainty arising from the divergence be-tween growth in nominal and real aggregates of eco-nomic activity,” it said. The Survey mentioned that the correlation between India’s growth rate and that of the world has risen sharply to reasonably high levels in re-cent years.

On the inflation front, the Economic Survey emphasised that the hike in the pay of government employees due to the implementation of the 7th Pay Commission will have negligible impact on inflation as the wage increas-es are unlikely to spill over to the private sector. The sur-vey projected retail inflation to remain between 4.5-5.0 per cent in 2016-17, implying that the RBI will be able to achieve its 5 per cent CPI inflation target by March 2017. This would allow RBI to ease liquidity conditions and further lower the policy rate, consistent with meeting the inflation target, the survey said.Uncertainty regard-ing China, impending Iranian oil supply and moderation in demand from the rest of the world are likely to keep oil prices in check.However, supply side constraints on pulses, vegetables and edible oils are likely to cause an uptick in inflation.

OutlookRBI’s monetary policy announcement focuses more on reining in inflationary expectations. Although the policy statement does hint at opening the space for easing interest rates in the near future, the Central Bank has chosen to make it conditional on fiscal tightening and implementation of structural reforms by the government. A rate cut would have been spot on for rejuvenating the investment cycle. CII hopes that the RBI would resume the rate cutting cycle in the subsequent monetary policy, soon after the Union Budget, to complement the government’s efforts to revive private investments and bring the economy back to the path of sustained growth.

Economic Survey FY16 Emphasises on Growth

ECONOMY MATTERS 22

DOMESTIC TRENDS

On the external risks, the Survey said foreign demand for India’s goods and services will remain weak in the short run, forcing the country to find and activate do-mestic sources of demand to prevent the growth mo-mentum from weakening. “At the very least, a tail risk event would require Indian monetary and fiscal policy not to add to the deflationary impulses from abroad. The consolation would be that weaker oil and com-modity prices would help keep inflation and the twin deficits in check,” it said. India’s merchandise exports contracted for 14 consecutive months till January due to declining demand from its key markets and softening crude oil prices.

On the fiscal side, while the Survey indicated that the current fiscal target 3.9 per cent of GDP remains com-fortable, it suggested that the Government should stick to its FY17 fiscal deficit, thereby reinforcing its credibil-ity. The high debt-to-GDP ratio of the consolidated Gov-ernment strengthens the case for the same. The Survey highlighted 2 key risks to the fiscal arithmetic: imple-mentation of the 7th Pay Commission and increased pub-lic spending to meet pressing infrastructure needs.It also said aggressive fiscal consolidation was a risk to de-

Presenting his second Railway Budget, Honorable Rail-way Minister, Shri Suresh Prabhuemphasised the key focus areas in the budget as - improving customer sat-isfaction, improving operational efficiency, broadening the scope of capex for the sector and use of innovative means of financing the capex.The broad theme of Budg-et was ‘Overcoming challenges - Reorganize, Restruc-ture Rejuvenate Indian Railways: ‘Chalo, MilkarKuch-Naya Karen’. As far as the fiscal situation of the railways is concerned, the Railway Budget has had to execute a fine balancing act between shrinking traffic receipts and keeping its growth oriented focus intact. In this regard, the savings generated to offset some revenue shortfall and the adoption of alternative sources of financing in-dicates that the Ministry remains cognizant of budget targets.

The budget highlighted that the operating ratio for the current fiscal came in at 90 per cent but is targeted at

mand revival, warning that the magnitude of the drag on demand and output will be largely equal to the size of consolidation. However, the survey said despite the decline in nominal GDP growth relative to the budget assumption (11.5 per cent in budget 2015-16 vis-à-vis 8.6 per cent in the advance estimates), the central govern-ment will meet its fiscal deficit target of 3.9 per cent of GDP, continuing the commitment to fiscal consolida-tion.

On future prospects, the Survey highlighted that India should adopt a three-pronged strategy to achieve its long-term potential growth rate of around 8.0-10.0 per cent by promoting competition and investing in health and education, while not neglecting agriculture. First, would be to create a more competitive environment for the markets. Second, in order to fully exploit the demo-graphic dividend, the Survey said India needed to invest more on health and education, including in human capi-tal, maternal health and early life interventions. Third, the Survey said the agriculture sector needed urgent focus as smaller farmers and landless labourers espe-cially were highly vulnerable to productivity, weather and market shocks that affect their incomes.

92 per cent for next fiscal on account of 7th Pay Com-mission commitments. Fare receipts showed a marked slowdown and FY16 budgeted targets were not met and gross traffic receipts fell short by over Rs 15000 crores for FY16. Growth budgeted for traffic receipts for FY17 is 10 per cent over RE and almost flat over BE. If this weakness in traffic earnings were to persist then next fiscal’s receipts could come under pressure. The plan outlay has been increased to Rs 1.21 trillion for FY2017 as compared to Rs 1 trillion in FY16 revised estimates, which will be implemented through joint ventures with states, developing new frameworks for PPP, etc.

Following were recognised as the key thrust areas of the Railway Budget:

Resource mobilization:

• Tap international markets for rupee bonds

• Secured funding from LIC at favourable terms; LIC

Highlights of the Railway Budget 2016-17

23

DOMESTIC TRENDS

FEB-MAR 2016

to invest Rs 1.5 trillion over a period of 5 years

• Partnership with SAIL, NTPC, coal ministry on fund-ing

• Encourage multilateral financing for station devel-opment

• Finalise standard document for undertaking work via EPC mode

• Examining feasibility for a holding company to monetise assets

Revival of freight traffic:

• Need to revive freight traffic through tariff rational-ization, focus on last minute connectivity, expand-ing the freight basket, and signing long term freight rate contracts with big customers

• To allow existing terminal sheds to access contain-er traffic

• To set up rail auto hub in Chennai

• To start timetable-based container trains this year

• To permit container freight operators to offer par-cel service

• To capture incremental freight traffic of 50 million tonnes in FY17

Enhancing Customer Experience:

• Railway Budget spared passengers and goods movement from any increase in tariffs

• Railways intend to commence sale of tickets through hand held terminals for the benefit of the suburban and short distance travellers

• Overnight double-decker, Utkrisht Double Decker Air-conditioned Yatri (UDAY) Express will be intro-duced on the busiest routes

• Railways will install information boards in trains enumerating the onboard services and also GPS based digital displays inside coaches to provide real time information regarding upcoming halts

• Introduce ‘Clean my Coach’ service on Pan-India ba-sis, where a passenger can request cleaning of his/her coach/toilets on demand through SMS

• To minimize the financial loss to passengers from untoward incidents, Railways is working with insur-ance companies to offer optional travel insurance for rail journeys at the time of booking.

• There are plans to progressively ensure CCTV cover-age at tatkaal counters

• Tejas railway service will showcase the future of train travel in India. Operating at speeds of 130 kmph and above, it will offer onboard services such as entertainment, local cuisine, Wi-Fi, etc. through one service provider for ensuring accountability and improved customer satisfaction.

• For the unreserved passenger, Antyodaya Express and DeenDayalu coaches will be introduced on the busiest routes.

ECONOMY MATTERS 24

CORPORATE PERFORMANCE

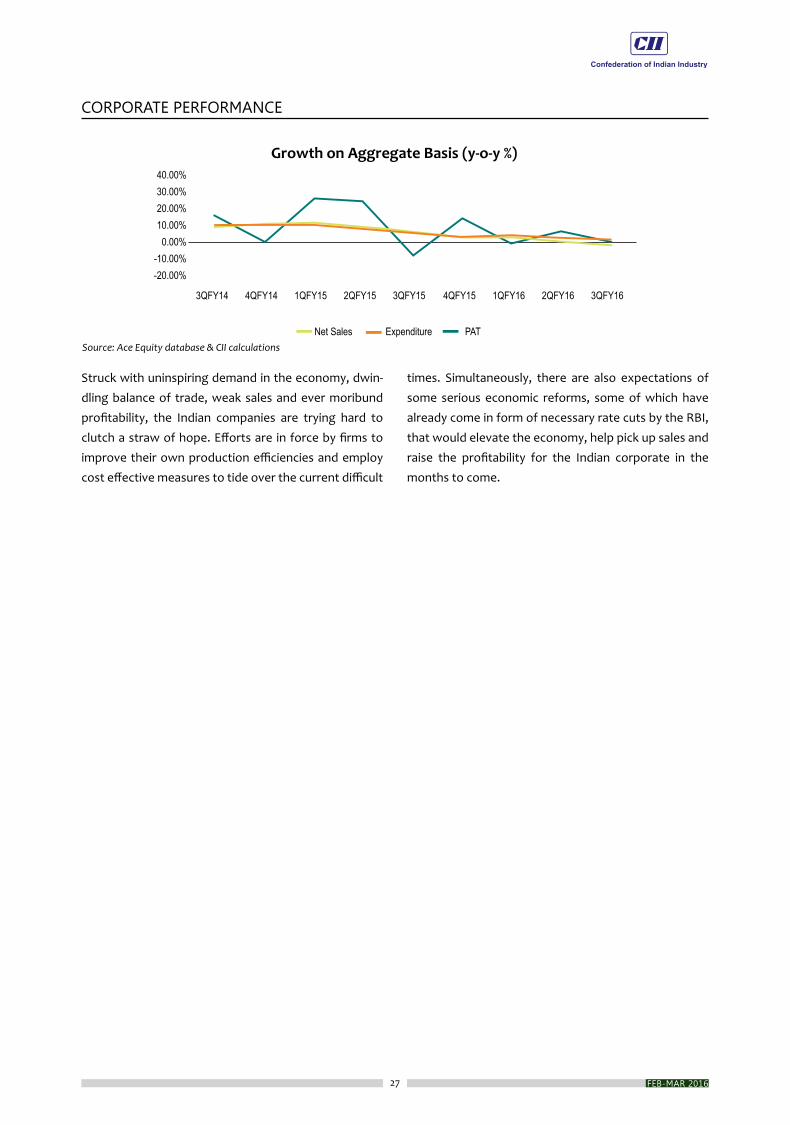

Corporate Performance in Q3FY16

The corporate results at the end of the third quarter of current fiscal continued to remain subdued as the financial performance of Indian

companies, especially manufacturing sector firms,came lower. The subdued performance of manufacturing sec-tor is in tandem with the deceleration in GDP growth to 7.3 per cent in the quarter ended December 2015 from 7.7 per cent in the previous quarter. While the growth in expenditure costs stood somewhat curbed, fading growth of net sales as well as decline in PAT stood out.

The analysis factors in the financial performance during the third quarter of 2015-16 of a balanced panel of 1168 manufacturing companies (excluding oil and gas com-

panies) and 608 service firms extracted from the Ace Equity database.

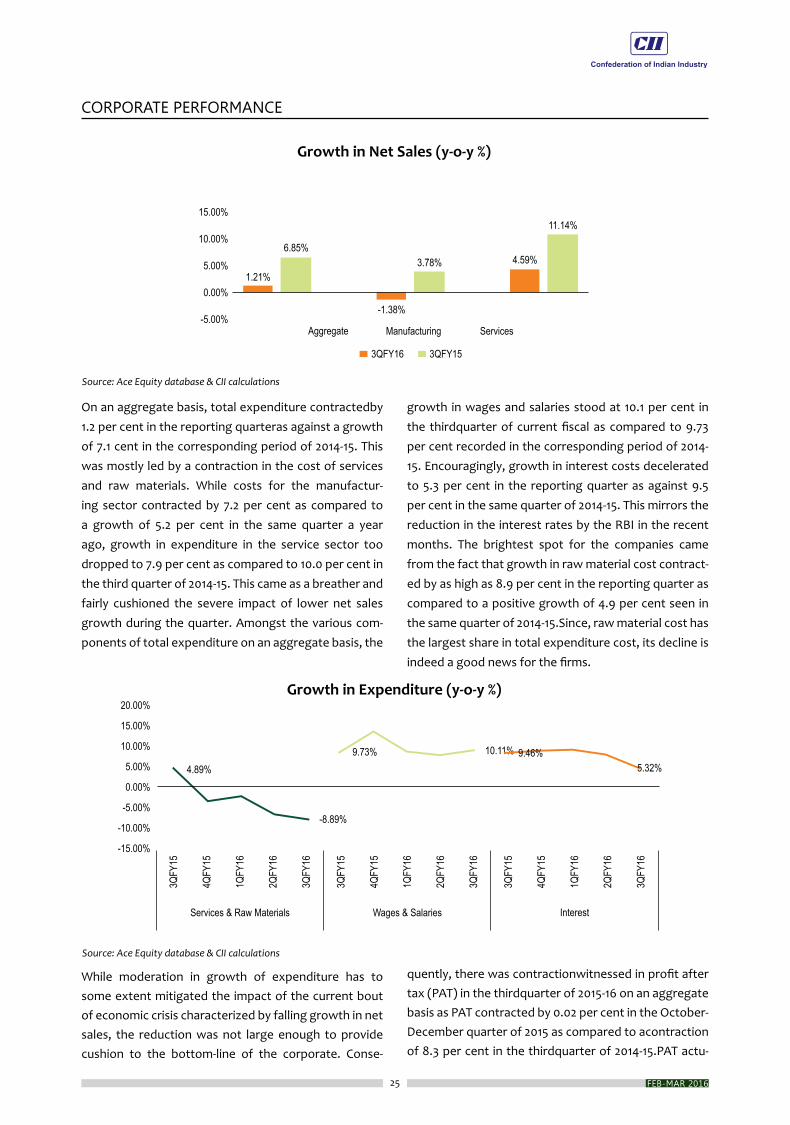

Net sales on an aggregate basis deceleratedto 1.2 per cent at the end of the thirdquarter of 2015-16, as com-pared to a growth of 6.8 per cent in the same quarter a year ago. In fact the growth in net sales has been de-cliningnow for the past seven quarters straight now. The net sales for manufacturing firms showed contrac-tion by 1.4per cent during the quarter as compared to a growth of 3.8 per cent in the same quarter a year ago.Firms in the service sector showed moderate drop in their net sales to4.6 per cent in the third quarter of cur-rent fiscal as compared to a growth of 11.1 per cent in the same quarter in the previous year. The low net sales of firms were reflective of the lack of ample demand in the economy, a scenario that has been persistent for quite some time now. The slowing demand in the exter-nal markets has been doing no good either.

25

CORPORATE PERFORMANCE

FEB-MAR 2016

On an aggregate basis, total expenditure contractedby 1.2 per cent in the reporting quarteras against a growth of 7.1 cent in the corresponding period of 2014-15. This was mostly led by a contraction in the cost of services and raw materials. While costs for the manufactur-ing sector contracted by 7.2 per cent as compared to a growth of 5.2 per cent in the same quarter a year ago, growth in expenditure in the service sector too dropped to 7.9 per cent as compared to 10.0 per cent in the third quarter of 2014-15. This came as a breather and fairly cushioned the severe impact of lower net sales growth during the quarter. Amongst the various com-ponents of total expenditure on an aggregate basis, the

While moderation in growth of expenditure has to some extent mitigated the impact of the current bout of economic crisis characterized by falling growth in net sales, the reduction was not large enough to provide cushion to the bottom-line of the corporate. Conse-

growth in wages and salaries stood at 10.1 per cent in the thirdquarter of current fiscal as compared to 9.73 per cent recorded in the corresponding period of 2014-15. Encouragingly, growth in interest costs decelerated to 5.3 per cent in the reporting quarter as against 9.5 per cent in the same quarter of 2014-15. This mirrors the reduction in the interest rates by the RBI in the recent months. The brightest spot for the companies came from the fact that growth in raw material cost contract-ed by as high as 8.9 per cent in the reporting quarter as compared to a positive growth of 4.9 per cent seen in the same quarter of 2014-15.Since, raw material cost has the largest share in total expenditure cost, its decline is indeed a good news for the firms.

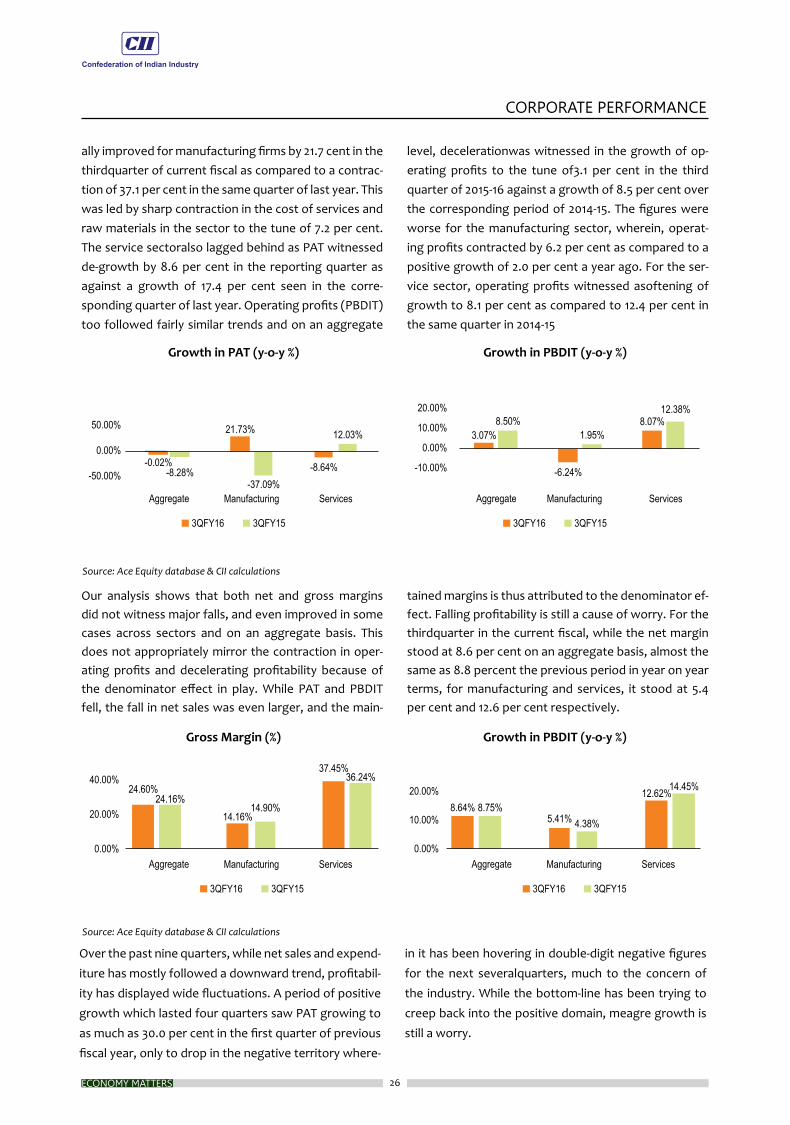

quently, there was contractionwitnessed in profit after tax (PAT) in the thirdquarter of 2015-16 on an aggregate basis as PAT contracted by 0.02 per cent in the October-December quarter of 2015 as compared to acontraction of 8.3 per cent in the thirdquarter of 2014-15.PAT actu-

ECONOMY MATTERS 26

CORPORATE PERFORMANCE

ally improved for manufacturing firms by 21.7 cent in the thirdquarter of current fiscal as compared to a contrac-tion of 37.1 per cent in the same quarter of last year. This was led by sharp contraction in the cost of services and raw materials in the sector to the tune of 7.2 per cent. The service sectoralso lagged behind as PAT witnessed de-growth by 8.6 per cent in the reporting quarter as against a growth of 17.4 per cent seen in the corre-sponding quarter of last year. Operating profits (PBDIT) too followed fairly similar trends and on an aggregate

Our analysis shows that both net and gross margins did not witness major falls, and even improved in some cases across sectors and on an aggregate basis. This does not appropriately mirror the contraction in oper-ating profits and decelerating profitability because of the denominator effect in play. While PAT and PBDIT fell, the fall in net sales was even larger, and the main-

Over the past nine quarters, while net sales and expend-iture has mostly followed a downward trend, profitabil-ity has displayed wide fluctuations. A period of positive growth which lasted four quarters saw PAT growing to as much as 30.0 per cent in the first quarter of previous fiscal year, only to drop in the negative territory where-

level, decelerationwas witnessed in the growth of op-erating profits to the tune of3.1 per cent in the third quarter of 2015-16 against a growth of 8.5 per cent over the corresponding period of 2014-15. The figures were worse for the manufacturing sector, wherein, operat-ing profits contracted by 6.2 per cent as compared to a positive growth of 2.0 per cent a year ago. For the ser-vice sector, operating profits witnessed asoftening of growth to 8.1 per cent as compared to 12.4 per cent in the same quarter in 2014-15

tained margins is thus attributed to the denominator ef-fect. Falling profitability is still a cause of worry. For the thirdquarter in the current fiscal, while the net margin stood at 8.6 per cent on an aggregate basis, almost the same as 8.8 percent the previous period in year on year terms, for manufacturing and services, it stood at 5.4 per cent and 12.6 per cent respectively.

in it has been hovering in double-digit negative figures for the next severalquarters, much to the concern of the industry. While the bottom-line has been trying to creep back into the positive domain, meagre growth is still a worry.

27

CORPORATE PERFORMANCE

FEB-MAR 2016

Struck with uninspiring demand in the economy, dwin-dling balance of trade, weak sales and ever moribund profitability, the Indian companies are trying hard to clutch a straw of hope. Efforts are in force by firms to improve their own production efficiencies and employ cost effective measures to tide over the current difficult

times. Simultaneously, there are also expectations of some serious economic reforms, some of which have already come in form of necessary rate cuts by the RBI, that would elevate the economy, help pick up sales and raise the profitability for the Indian corporate in the months to come.

ECONOMY MATTERS 28

FOCUS OF THE MONTH

Union Budget: 2016-17

The Finance Minister has presented a bold, prag-matic and growth-driven Budget which has at-tempted a credible balancing act of scripting a

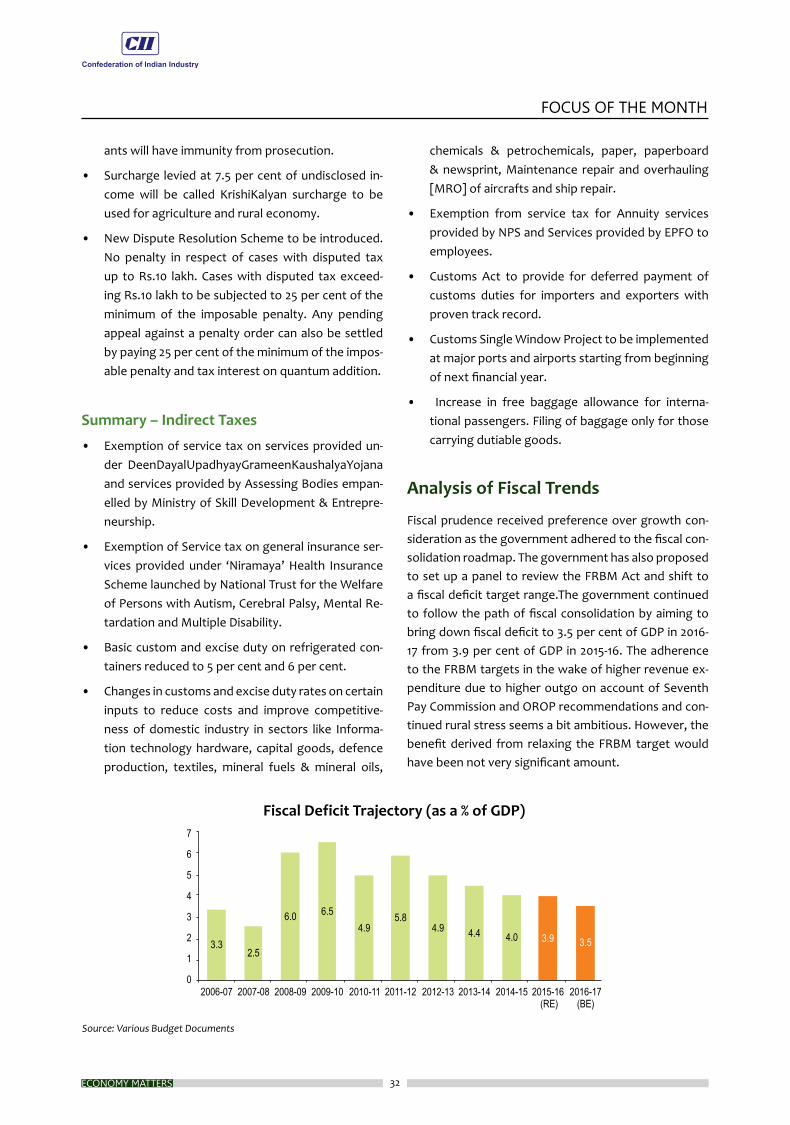

blueprint for sustaining the growth momentum in the Indian economy in the coming year on the one hand while taking up issues of social inclusion on the other. At the current growth pivot point, addressing the fiscal deficit was top of the macroeconomic agenda and the Budget has addressed this with customary sagacity and vision. Fiscal prudence has been a cornerstone of the budget strategy with the deficit pegged at 3.9 per cent and 3.5 per cent of GDP for FY16 and FY17 respectively without compromising the developmental agenda. The adherence to the fiscal deficit target would help open up access to funds for other sectors to spend, maintain a level of confidence in macroeconomic management and contain inflation within the desired band. Besides, closer adherence to the path of fiscal rectitude would meet the expectations of rating agencies.

The Budget has done much to reignite the investment cycle by enhancing allocations for the infrastructure sector. Reducing the infrastructure gap is critical to ac-

celerate manufacturing growth and attract foreign in-vestment. While augmenting the allocation on roads, railways, ports and airports is significant, the Budget has rightly announced measures to revitalise public-private partnership (PPP) through the introduction of Public Utility (Resolution of Disputes) Bill, formulating guidelines for renegotiation of PPP Concession Agree-ments and introducing a new credit rating system for infrastructure projects.

It is also heartening to note that the Budget has a plan for social inclusion. A package of measures including a broad agriculture thrust and social security measures, which seek to address rural stress on account of two consecutive droughts, is timely. The Budget has come out with a package of measures to boost farm produc-tivity, reduce costs, facilitate greater access to credit, reform agriculture marketing and, most importantly, generate more employment in the rural economy. With suitable provisions announced for flagship campaigns such as ‘Make in India’ ‘Startup India’, ‘Digital India’ and ‘Skill India’ among others, the Budget would go a long way to boost manufacturing, foster innovation, attract investment, nurture entrepreneurship and create jobs. In this month’s Focus of the month, we provide a de-tailed analysis of the Union Budget: 2016-17 through the eyes of the experts.

29

FOCUS OF THE MONTH

FEB-MAR 2016

Key Features of the Union Budget 2016-17

Following are the key features of Union Budget 2016-17:

Fiscal Discipline

• Fiscal deficit in RE 2015-16 and BE 2016-17 retained at 3.9 per cent and 3.5 per cent respectively.

• Revenue Deficit target reduced from 2.8 per cent to 2.5 per cent in RE 2015-16

• Total expenditure projected at Rs. 19.78 lakh crore

• Plan expenditure pegged at Rs. 5.50 lakh crore

• Non-Plan expenditure kept at Rs. 14.28 lakh crore

• Mobilisation of additional finances to the extent of Rs. 31,300 crore by NHAI, PFC, REC, IREDA, NABARD and Inland Water Authority by raising Bonds.

• Plan / Non-Plan classification to be done away with from 2017-18.

• Every new scheme sanctioned will have a sunset date and outcome review.

• Rationalised and restructured more than 1500 Cen-tral Plan Schemes into about 300 Central Sector and 30 Centrally Sponsored Schemes.

• Committee to review the implementation of the FRBM Act.

Agriculture and Farmers’ Welfare

• Allocation for Agriculture and Farmers’ welfare is Rs. 35,984 crore

• ‘PradhanMantriKrishiSinchaiYojana’ to be imple-mented in mission mode. 28.5 lakh hectares will be brought under irrigation.

• Implementation of 89 irrigation projects under AIBP

• A dedicated Long Term Irrigation Fund will be cre-ated in NABARD with an initial corpus of about Rs. 20,000 crore

• Programme for sustainable management of ground water resources with an estimated cost of Rs. 6,000 crore will be implemented through multilat-eral funding

• 5 lakh farm ponds and dug wells in rain fed areas and 10 lakh compost pits for production of organic

manure will be taken up under MGNREGA

• Soil Health Card scheme will cover all 14 crore farm holdings by March 2017

Rural Sector

• Allocation for rural sector – Rs. 87,765 crore.

• Rs. 2.87 lakh crore will be given as Grant in Aid to Gram Panchayats and Municipalities as per the rec-ommendations of the 14th Finance Commission

• Every block under drought and rural distress will be taken up as an intensive Block under the DeenDay-alAntyodaya Mission

• A sum of Rs. 38,500 crore allocated for MGNREGS.

• 300 Rurban Clusters will be developed under the Shyama Prasad Mukherjee Rurban Mission

• 100 per cent village electrification by 1st May, 2018

Social Sector Including Health Care

• Allocation for social sector including education and health care – Rs.1,51,581crore.

• Rs. 2,000 crore allocated for initial cost of providing LPG connections to BPL families.

• New health protection scheme will provide health cover up to Rs. One lakh per family. For senior citi-zens an additional top-up package up to Rs. 30,000 will be provided.

• 3,000 Stores under Prime Minister’s Jan Aushadhi-Yojana will be opened during 2016-17.

• ‘National Dialysis Services Programme’ to be start-ed under National Health Mission through PPP mode

Education, Skills and Job Creation

• 62 new NavodayaVidyalayas will be opened

• SarvaShikshaAbhiyan for increasing focus on qual-ity of education

• Regulatory architecture to be provided to ten pub-lic and ten private institutions to emerge as world-class Teaching and Research Institutions

ECONOMY MATTERS 30

FOCUS OF THE MONTH

• Higher Education Financing Agency to be set-up with initial capital base of Rs. 1000 Crores

• Digital Depository for School Leaving Certificates, College Degrees, Academic Awards and Mark sheets to be set-up

• GoI will pay contribution of 8.33 per cent for of all new employees enrolling in EPFO for the first three years of their employment. Budget provision of Rs. 1000crore for this scheme

Infrastructure and Investment

• Total investment in the road sector, including PMG-SY allocation, would be Rs. 97,000 crore during 2016-17

• India’s highest ever kilometres of new highways were awarded in 2015. Nearly 10,000 kms of Nation-al Highways to be approved in 2016-17.

• Allocation of Rs. 55,000 crore in the Budget for Roads. Additional Rs. 15,000 crore to be raised by NHAI through bonds

• To provide calibrated marketing freedom in order to incentivise gas production from deep-water, ul-tra deep-water and high pressure-high temperature areas

• Comprehensive plan, spanning next 15 to 20 years, to augment the investment in nuclear power gen-eration to be drawn up

• Reforms in FDI policy in the areas of Insurance and Pension, Asset Reconstruction Companies, Stock Exchanges

• 100 per cent FDI to be allowed through FIPB route in marketing of food products produced and manu-factured in India

• A new policy for management of Government in-vestment in Public Sector Enterprises, including dis-investment and strategic sale, approved

Financial Sector Reforms

• A comprehensive Code on Resolution of Financial Firms for insolvency and bankruptcy issues to be in-troduced

• Statutory basis for a Monetary Policy framework and a Monetary Policy Committee through the Fi-

nance Bill 2016 to be introduced under committee based approach for monetary policy

• A Financial Data Management Centre to be set up

• RBI to facilitate retail participation in Government securities

• New derivative products will be developed by SEBI in the Commodity Derivatives market

• Amendments in the SARFAESI Act 2002 to enable the sponsor of an ARC to hold up to 100 per cent stake in the ARC and permit non institutional inves-tors to invest in Securitization Receipts

• Allocation of Rs. 25,000 crore towards recapitalisa-tion of Public Sector Banks

Providing Certainty in Taxation

• Committed to providing a stable and predictable taxation regime and reduce black money.

• Domestic taxpayers can declare undisclosed income or such income represented in the form of any as-set by paying tax at 30 per cent, and surcharge at 7.5 per cent and penalty at 7.5 per cent, which is a total of 45 per cent of the undisclosed income. De-clarants will have immunity from prosecution.

• New Dispute Resolution Scheme to be introduced. No penalty in respect of cases with disputed tax up to Rs. 10 lakh. Cases with disputed tax exceed-ing Rs. 10 lakh to be subjected to 25 per cent of the minimum of the imposable penalty. Any pending appeal against a penalty order can also be settled by paying 25 per cent of the minimum of the impos-able penalty and tax interest on quantum addition.

Simplification and Rationalization of Taxes

• 13 cesses, levied by various Ministries in which rev-enue collection is less than Rs. 50 crore in a year, to be abolished.

• For non-residents providing alternative documents to PAN card, higher TDS not to apply.

• Revision of return extended to Central Excise as-sesses.

• Additional options to banking companies and fi-nancial institutions, including NBFCs, for reversal of input tax credits with respect to non- taxable ser-

31

FOCUS OF THE MONTH

FEB-MAR 2016

vices.

• Customs Act to provide for deferred payment of customs duties for importers and exporters with proven track record.

• Customs Single Window Project to be implemented at major ports and airports starting from beginning of next financial year.

• Increase in free baggage allowance for internation-al passengers. Filing of baggage only for those car-rying dutiable goods.

Summary – Direct Taxes

• Deduction under Section 80JJAA of the Income Tax Act will be available to all assessees who are subject to statutory audit under the Act.

• Raise the ceiling of tax rebate under section 87A from Rs.2000 to Rs.5000 to lessen tax burden on individuals with income upto Rs.5 lakhs.

• Increase the limit of deduction of rent paid un-der section 80GG from Rs.24000 per annum to Rs.60000, to provide relief to those who live in rented houses.

• Increase the turnover limit under Presumptive taxa-tion scheme under section 44AD of the Income Tax Act to Rs.2 crores to bring big relief to a large num-ber of assessees in the MSME category.

• Extend the presumptive taxation scheme with prof-it deemed to be 50 per cent, to professionals with gross receipts up to Rs.50 lakh.

• Accelerated depreciation wherever provided in IT Act will be limited to maximum 40 per cent from 1.4.2017.

• The weighted deduction under section 35CCD for skill development will continue up to 1.4.2020.

• New manufacturing companies incorporated on or after 1.3.2016 to be given an option to be taxed at 25 per cent + surcharge and cess provided they do not claim profit linked or investment linked deduc-tions and do not avail of investment allowance and accelerated depreciation.

• Lower the corporate tax rate for the next financial year for relatively small enterprises i.e, companies with turnover not exceeding Rs.5 crores (in the fi-nancial year ending March 2015), to 29 per cent plus

surcharge and cess.

• 100 per cent deduction of profits for 3 out of 5 years for start-ups setup during April, 2016 to March, 2019. MAT will apply in such cases.

• 10 per cent rate of tax on income from worldwide exploitation of patents developed and registered in India by a resident.

• Determination of residency of foreign company on the basis of Place of Effective Management (POEM) is proposed to be deferred by one year.

• Commitment to implement General Anti Avoidance Rules (GAAR) from 1.4.2017.

• Withdrawal up to 40 per cent of the corpus at the time of retirement to be tax exempt in the case of National Pension Scheme (NPS). Annuity fund which goes to legal heir will not be taxable.

• In case of superannuation funds and recognized provident funds, including EPF, the same norm of 40 per cent of corpus to be tax free will apply in re-spect of corpus created out of contributions made on or from 1.4.2016.

• Limit for contribution of employer in recognized Provident and Superannuation Fund of Rs.1.5 lakh per annum for taking tax benefit.

• 100 per cent deduction for profits to an undertak-ing in housing project for flats upto 30 sq. metres in four metro cities and 60 sq. metres in other cities approved during June 2016 to March 2019 and com-pleted in three years. MAT to apply.

• Surcharge to be raised from 12 per cent to 15 per cent on persons, other than companies, firms and cooperative societies having income above Rs.1 crore.

• Tax to be deducted at source at the rate of 1 per cent on purchase of luxury cars exceeding value of Rs.10 lakh and purchase of goods and services in cash exceeding Rs.2 lakh.

• Domestic taxpayers can declare undisclosed income or such income represented in the form of any asset by paying tax at 30 per cent, and surcharge at 7.5 per cent and penalty at 7.5 per cent, which is a total of 45 per cent of the undisclosed income. Declar-

ECONOMY MATTERS 32

FOCUS OF THE MONTH