ecb project

DESCRIPTION

masters project on ECBTRANSCRIPT

EXTERNAL COMMERCIAL BORROWINGS

EXTERNAL COMMERCIAL BORROWING

The commercial borrowings consists of:-

- Internal Commercial Borrowings AND

- External Commercial Borrowings

1. INTERNAL COMMERCIAL BORROWINGS

1.1 INTRODUCTION

Internal commercial borrowings are those borrowings, which are borrowed internally

and these borrowings may be receive from the same country like any bank or any

institution may borrow form same countries institution or bank. Like wise any small

institution or any small-scale industry can borrow loan or make the borrowings form

same countries bank.

1.2) WORKING CAPITAL FINANCE FROM BANK: -.

Working capital is an essential requirement for any business activity. Banks in India

today constitute the major suppliers of working capital credit to any business activity.

Recently, however, some term lending financial institution has also announced

schemes for working capital financing.

Before the TONDON AND CHORE committees, bank were employing different

methods for assessing working capital and after the limits sanctioned were either

excess of the requirement or short of them. The former led to division or overtrading

while the latter to outside borrowings. The two committees have evolved definite

guidelines and parameters in working capital financing, which have laid the

foundations for development and innovation in the area.

1

EXTERNAL COMMERCIAL BORROWINGS

1.3) BANK OVERDRAFT: -

Short-term borrowings of the kind made available principally by the clearing banks

in the forms of overdraft is very flexible. When the borrowed funds are no longer

required they can quickly and easily be repaid. It is also comparatively cheap. The

banks will impose limits on the amount they can lend.

The bank issue overdraft with the right to call them in a short notice. Bank advances

are, in fact, legally repayable on demand, through enforcing the letter of the law on

this point is often impractical since it would hardly be in the bank’s interest to drive

its client into a dangerous financial position if that looked likely. Normally the bank

assures the borrower that he can rely on overdraft not being recalled for a certain

period of time, say one year or six month. Any plans that involves an overdraft or

short terms loans should, therefore, refer closely to the Company’s Cash Flow

analysis that it is quite clear how long the funds will be needed and when they can be

repaid.

When credit conditions are normal, the Clearing Banks are generally prepared to lend

to a client whose business sows a healthy state of profitability and liquidity. Usually,

the Bank will require fixed or floating charges on assets as security for advances or in

the case of private companies, to obtain a personal guarantee from the owners.

Banks prefer self-liquidating loans – those likely to be repaid automatically and

reasonably and quickly. These might include, e.g. cash to finance a specified

contract that will eventually result in cash flow for the company.

Firm which carry large stocks of material may obtain a loan or an overdraft secured

by pledging their stocks. The stocks are held in bond and all movements thereof are

reported to the Bank. Banks assist in providing temporary funds to finance

production on the assumption that the goods or products will be sold in a later

season. The cost to a company of bank borrowing depends on the credit worthiness

of the borrower and upon the general interest level in the market.

2

EXTERNAL COMMERCIAL BORROWINGS

1.4) BRIDGE LOANS.

Bridge loans are available from the banks and financial institution when the source

and timing of the funds to be raised is known with certainty. When there is a time

gap for access of funds, then for speeding up of implementation of the projects,

bridge loans will be provided, such loans are repaid immediately after the raising of

funds. The cost of bridge loans is normally higher than the working capital facilities

provided by banks. At present RBI has put a restriction on banks in giving bridge

loans to curb the malpractices in capital market dealing.

1.5) PUBLIC DEPOSITS

Deposits from the public are one of the important sources of finance particular for

well-established big companies with huge capital base. The period of public deposits

is restricted to maximum three year at a time and hence, this source can provide

finance only for a short term to medium term, which could be more useful for

meeting working capital needs of the company. It is advisable to use the amounts of

public deposits for acquiring assets of long-term nature unless its pay back is very

short.

1.6) COMMERCIAL PAPER

The commercial paper introduced into financial market, on the recommendation of

VAGHUL Committee has become a popular debt instrument of the corporate world.

CP is a debt instrument for short-term borrowings, that enables highly rated corporate

borrowers to diversify their sources of short-term borrowings, and provides an

additional financial instrument to investors with free negotiable interest rate. The

maturity period ranges from three months to less than 1 year. Since it is a short-term

debt, the issuing company is required to meet dealers’ fees, rating agency fees and

any other relevant charges. Commercial paper is short term unsecured promissory

note issued by corporations with high credit rating.

3

EXTERNAL COMMERCIAL BORROWINGS

ADVANTAGE OF ISSUE OF COMMERCIAL PAPER

High credit rating fetch a lower cost of capital.

Wide range of maturities provided more flexibility.

It does not create any lien on asset of the company.

Tradability of commercial paper provides investors with exit options.

DIS-ADVANTAGES OF ISSUE OF COMMERCIAL PAPER.

Its usage is limited to only blue chip companies

Issuance of commercial paper bring down the bank credit limits.

A high degree of regulatory control is exercised on issue of commercial

papers

Standby credit may become necessary.

1.7) Unit Trust Of India:

Unit trust of India was floated in 1964 in the public sector to harness the saving from

and medium income groups with an objective to make investement in equity shares

and other securities of corporate sector. UTI makes investement in equity shares and

as well as in fixed income bearing securities from UTI is available in the following

forms:

Subscription to secured long-term privately placed debentures.

Underwriting of equity and debentures issue.

Participation in project financing.

Participation in project financing by UTI is based on detailed appraisal carried by

IDBI, IFCI, and ICICI on the lines as by Life Insurance Corporation Of India.

4

EXTERNAL COMMERCIAL BORROWINGS

1.8) National Bank For Agriculture And Rural Development

(NABARD)

NABARD was established in 1982 with primary objective of providing credit for

promotion of agricultural, small- scale industries, cottage and village industries,

handicraft and other allied activities in the rural sector. The bank does not extend any

direct assistance to borrower but allows refining however, actively associated with

policy formulation for integrated rural development.

1.9) The Industrial Development bank of India: -

The industrial development Bank Of India was established on July 1, 1964 under the

act of parliament as the principal financial institution for industrial development in

the country. IDBI caters to the growing and diverse needs of medium and large scale

industries wit the main object of providing financial assistance and coordinating the

working of institutions engaged in financing, promoting and developing industries.

IDBI provides direct finance by way of loans, both in rupees and foreign currencies

besides providing support by way of underwriting and direct subscription to

shares/debentures and in the forms of deferred payment guarantees. It also refinances

term loan given by state level institution or banks to medium scale units and

rediscounts or discounts bills of exchange and promissory notes rising out of the sale

or purchase of machinery and equipment IDBI extends loans to makes investments in

shares and bonds of various intermediaries. In response to the growing needs of

various segments of industries and on-going changes in the finance sector, IDBI has

taking various steps to re-orient its business strategies and expand the range of its

products and services. Instead of this IDBI also provides the Merchant Banking

debentures and trusteeship to various clients

5

EXTERNAL COMMERCIAL BORROWINGS

1.10) SIDBI (Small Industries Development Bank OF India)

Small Industries Development Bank Of India (SIBDI), a wholly- owned subsidiary

of Industrial Development Bank Of India, set up by an Act of parliament, is the

principal financial institution for the promotion, financing and development of

industry in the small, tiny and cottage sectors and for coordinating the functions of

the similar activities. It commenced its operation on April 2, 1990 by taking over the

outstanding portfolio and activities of IDBI pertaining to the small tiny and cottage

sectors.

Given the apex role, the approach of SIDBI has been to supplement the efforts of

existing institution, strengthening their capabilities trough financial and support

services and instituting suitable co-ordination mechanism while providing assistance

for the small-scale sector. While continuing with the schemes operated by IDBI

under Small Scale Industries Development Fund (SIDF), the bank look activities by

identifying the gaps in existing credit delivery system and divides tailor-made

schemes for direct lending to small scale sector as to supplement the efforts of

primary lending institutions (PLIs), which includes State Financial Corporation

(SFCs) State Industrial Development Corporation (SIDCs) (including twin function

IDCs), Scheduled Commercial Banks (SCBs) both in public and private sector, State

Co-operative Banks, scheduled urban Co-operative Banks And Regional Rural Banks

(RRBs).

Under indirect assistance, assistance, assistance to small scale sector is channelised

through the large network of PLIs across the country by way of refinance, bills

rediscounting and resource support in the form of lines of credit in lieu of refinance

etc.

6

EXTERNAL COMMERCIAL BORROWINGS

2 .EXTERNAL COMMERCIAL BORROWINGS

2.1) INTRODUCTION

In the emerging border-less world, comparative cost of Capital has assumed

increased significance. In the Indian context, the recommendations of the Committee

on "Capital Account Convertibility [CAC]" (Tarapore Committee) would be highly

relevant. While Rupee has been made convertible on the Current Account, the days

of Capital Account convertibility may not be far off. One of the avowed objectives of

CAC is to make Available Capital at internationally competitive rates. It would,

therefore, emerge that non-availability of domestic capital or availability of domestic

capital at higher costs owing to the domestic market conditions, need not be a

deterrent factor hindering the growth of the economy, once the various controls on

cross-border flows are gradually eased.

External Commercial Borrowings (ECBs), in a limited sense, seek out to bridge by

ensuring availability of cross-border financing vis-à-vis sourcing of capital locally.

ECBs should not be regarded as straightjacket solutions for easing the capital

requirements of the industry by providing alternate avenues of financing but should

be understood properly together with the attendant risks associated with such types of

financing. The recent South East Asian economic crisis can be attributed to the

unbridled approach adopted by certain countries in the matter of encouraging

external sources of financing forgetting the fundamentals there of. External

Commercial borrowings are one of the modes for sourcing of funds for Corporate.

The Government of India has come out with guidelines for approval of external

commercial borrowings. These guidelines reflect the government's desire of

maintaining prudent limits for total external borrowings and at the same time give

flexibility to Corporate. The guiding principles of ECB policy are to keep borrowing

maturities long, costs low, and encourage infrastructure and export sector financing

which are crucial for overall growth of the economy.

7

EXTERNAL COMMERCIAL BORROWINGS

Therefore, the borrowings raised by the Indian corporate from confirmed banking

sources outside India are called "External Commercial Borrowings" (ECBs).

The Reserve Bank of India has been empowered to give ECB approvals under the US

$ 5 million scheme and to approve ECBs upto US $ 10 million under all other ECB

windows. Corporate are now eligible for ECBs even for project related rupee

expenditure up to 35% of the total project cost and are permitted to obtain credit

enhancements from international banks / international financial institutions / joint

venture partners for their domestic rupee denominated structural obligations.

ECBs are being permitted by the Government as a source of finance for Indian

Corporate for expansion of existing capacity as well as for fresh investment. These

ECBs can therefore be raised within the Policy guidelines of Govt. of India/ Reserve

Bank of India applicable from time to time.

The policy seeks to keep an annual cap or ceiling on access to ECB, consistent with

prudent debt management. The policy also seeks to give greater priority for projects

in the infrastructure and core sectors such as Power, Oil Exploration, Telecom,

Railways, Roads & Bridges, Ports, Industrial Parks and Urban Infrastructure etc. and

the export sector. Development Financial Institutions, through their sub- lending

against the ECB approvals are also expected to give priority to the needs of medium

and small- scale units. Applicants will be free to raise ECB from any internationally

recognized source such as banks, export credit agencies, suppliers of equipment,

foreign collaborators, foreign equity-holders, international capital markets etc. Offers

from unrecognized sources will not be entertained.

8

EXTERNAL COMMERCIAL BORROWINGS

2.2) INTERNATIONAL MONETORY FUND

Introduction: -

The IMF was conceived in July 1944 at an international conference held at Bretton

Woods, New Hampshire, U.S.A., when delegates from 44 governments agreed on a

framework for economic cooperation partly designed to avoid a repetition of the

disastrous economic policies that had contributed to the Great Depression of the

1930s.

The IMF came into existence in December 1945, when the first 29 countries signed

its Articles of Agreement. The statutory purposes of the IMF today are the same as

when they were formulated in 1944. Since then, the world has experienced

unprecedented growth in real incomes. And although the benefits of growth have not

flowed equally to all—either within or among nations—most countries have seen

increases in prosperity that contrast starkly with the interwar period, in particular.

Part of the explanation lies in improvements in the conduct of economic policy,

including policies that have encouraged the growth of international trade and helped

smooth the economic cycle of boom and bust. The IMF is proud to have contributed

to these developments.

The expansion of the IMF's membership, together with the changes in the world

economy, have required the IMF to adapt in a variety of ways to continue serving its

purposes effectively.

Purposes Of International Monitory Fund

i) To promote international monetary cooperation through a permanent institution

which provides the machinery for consultation and collaboration on international

monetary problems.

ii) To facilitate the expansion and balanced growth of international trade, and to

contribute thereby to the promotion and maintenance of high levels of employment

9

EXTERNAL COMMERCIAL BORROWINGS

and real income and to the development of the productive resources of all members

as primary objectives of economic policy.

iii) To promote exchange stability, to maintain orderly exchange arrangements

among members, and to avoid competitive exchange depreciation.

iv) To assist in the establishment of a multilateral system of payments in respect of

current transactions between members and in the elimination of foreign exchange

restrictions which hamper the growth of world trade.

v) To give confidence to members by making the general resources of the Fund

temporarily available to them under adequate safeguards, thus providing them with

opportunity to correct maladjustments in their balance of payments without resorting

to measures destructive of national or international prosperity.

vi) In accordance with the above, to shorten the duration and lessen the degree of

disequilibrium in the international balances of payments of members.

Who Makes Decisions at the IMF?

The IMF is accountable to its member countries, and this accountability is essential

to its effectiveness. The day-today work of the IMF is carried out by an Executive

Board, representing the IMF's 184 members, and an internationally recruited staff

under the leadership of a Managing Director and three Deputy Managing Directors—

each member of this management team being drawn from a different region of the

world. The powers of the Executive Board to conduct the business of the IMF are

delegated to it by the Board of Governors, which is where ultimate oversight rests.

The Board of Governors, on which all member countries are represented, is the

highest authority governing the IMF. It usually meets once a year, at the Annual

Meetings of the IMF and the World Bank. Each member country appoints a

Governor—usually the country's minister of finance or the governor of its central

10

EXTERNAL COMMERCIAL BORROWINGS

bank—and an Alternate Governor. The Board of Governors decides on major policy

issues but has delegated day-to-day decision-making to the Executive Board.

Key policy issues relating to the international monetary system are considered twice-

yearly in a committee of Governors called the International Monetary and Financial

Committee, or IMFC (until September 1999 known as the Interim Committee). A

joint committee of the Boards of Governors of the IMF and World Bank called the

Development Committee advises and reports to the Governors on development

policy and other matters of concern to developing countries.

The Executive Board consists of 24 Executive Directors, with the Managing Director

as chairman. The Executive Board usually meets three times a week, in full-day

sessions, and more often if needed, at the organization's headquarters in Washington,

D.C. The IMF's five largest shareholders —the United States, Japan, Germany,

France, and the United Kingdom—along with China, Russia, and Saudi Arabia, have

their own seats on the Board. The other 16 Executive Directors are elected for two-

year terms by groups of countries, known as constituencies.

Where Does the IMF Get Its Money?

The IMF's resources come mainly from the quota (or capital) subscriptions that

countries pay when they join the IMF, or following periodic reviews in which quotas

are increased. Countries pay 25 percent of their quota subscriptions in Special

Drawing Rights or major currencies, such as U.S. dollars or Japanese yen; the IMF

can call on the remainder, payable in the member's own currency, to be made

available for lending as needed. Quotas determine not only a country's subscription

payments, but also the amount of financing that it can receive from the IMF, and its

share in SDR allocations. Quotas also are the main determinant of countries' voting

power in the IMF.

If necessary, the IMF may borrow to supplement the resources available from its

quotas. The IMF has two sets of standing arrangements to borrow if needed to cope

with any threat to the international monetary system:

11

EXTERNAL COMMERCIAL BORROWINGS

The New Arrangements to Borrow (NAB), introduced in 1997, with 25 participating

countries and institutions. Under the two arrangements combined, the IMF has up to

SDR 34 billion (about $50 billion) available to borrow.

What is an SDR?

The SDR, or special drawing right, is an international reserve asset introduced by the

IMF in 1969 (under the First Amendment to its Articles of Agreement) out of

concern among IMF members that the current stock, and prospective growth, of

international reserves might not be sufficient to support the expansion of world trade.

The main reserve assets were gold and U.S. dollars, and members did not want global

reserves to depend on gold production, with its inherent uncertainties, and continuing

U.S. balance of payments deficits, which would be needed to provide continuing

growth in U.S. dollar reserves. The SDR was introduced as a supplementary reserve

asset, which the IMF could "allocate" periodically to members when the need arose,

and cancel, as necessary.

The SDR's value is set daily using a basket of four major currencies: the euro,

Japanese yen, pound sterling, and U.S. dollar. On July 1, 2004, SDR 1 = US$1.48.

The composition of the basket is reviewed every five years to ensure that it is

12

EXTERNAL COMMERCIAL BORROWINGS

representative of the currencies used in international transactions, and that the

weights assigned to the currencies reflect their relative importance in the world's

trading and financial systems.

How Does the IMF Serve Its Members?

The IMF helps its member countries by:

Reviewing and monitoring national and global economic and financial

developments and advising members on their economic policies;

Lending them hard currencies to support adjustment and reform policies

designed to correct balance of payments problems and promote sustainable

growth; and

Offering a wide range of technical assistance, as well as training for

government and central bank officials, in its areas of expertise

IMF Operations

The IMF has gone through two distinct phases in its 50-year history. During the first

phase, ending in 1973, the IMF oversaw the adoption of general convertibility among

the major currencies, supervised a system of fixed exchange rates tied to the value of

gold, and provided short-term financing to countries in need of a quick infusion of

foreign exchange to keep their currencies at par value or to adjust to changing

economic circumstances.

How in practice does the IMF assist its members? The key opening the door to IMF

assistance is the member's balance of payments, the tally of its payments and receipts

with other nations. Foreign payments should be in rough balance: a country ideally

should take in just about what it pays out. When financial problems cause the price of

a member's currency and the price of its goods to fall out of line, balance of payments

13

EXTERNAL COMMERCIAL BORROWINGS

difficulties are sure to follow. If this happens, the member country may, by virtue of

the Articles of Agreement, apply to the IMF for assistance.

To illustrate, let us take the example of a small country whose economy is based on

agriculture. For convenience in trade, the government of such a country generally

pegs the domestic currency to a convertible currency: so many units of domestic

money to a U.S. dollar or French franc. Unless the exchange rate is adjusted from

time to time to take account of changes in relative prices, the domestic currency will

tend to become overvalued, with an exchange rate, say, of one unit of domestic

currency to one U.S. dollar, when relative prices might suggest that two units to one

dollar is more realistic. Governments, however, often succumb to the temptation to

tolerate overvaluation, because an overvalued currency makes imports cheaper than

they would be if the currency were correctly priced.

In addition to assisting its members in this way, the IMF also helps by providing

technical assistance in organizing central banks, establishing and reforming tax

systems, and setting up agencies to gather and publish economic statistics. The IMF

is also authorized to issue a special type of money, called the SDR, to provide its

members with additional liquidity. Known technically as a fiduciary asset, the SDR

can be retained by members as part of their monetary reserves or be used in place of

national currencies in transactions with other members. To date the IMF has issued

slightly over 21.4 billion SDRs, presently valued at about U.S. $30 billion.

Over the past few years, in response to an emerging interest by the world community

to return to a more stable system of exchange rates that would reduce the present

fluctuations in the values of currencies, the IMF has been strengthening its

supervision of members' economic policies.

Provisions exist in its Articles of Agreement that would allow the IMF to adopt a

more active role, should the world community decide on stricter management of

flexible exchange rates or even on a return to some system of stable exchange rates.

14

EXTERNAL COMMERCIAL BORROWINGS

Size of International Monitory Fund

The IMF is small (about 2,300 staff members) and, unlike the World Bank, has no

affiliates or subsidiaries. Most of its staff members work at headquarters in

Washington, D.C., although three small offices are maintained in Paris, Geneva, and

at the United Nations in New York. Its professional staff members are for the most

part economists and financial experts.

15

EXTERNAL COMMERCIAL BORROWINGS

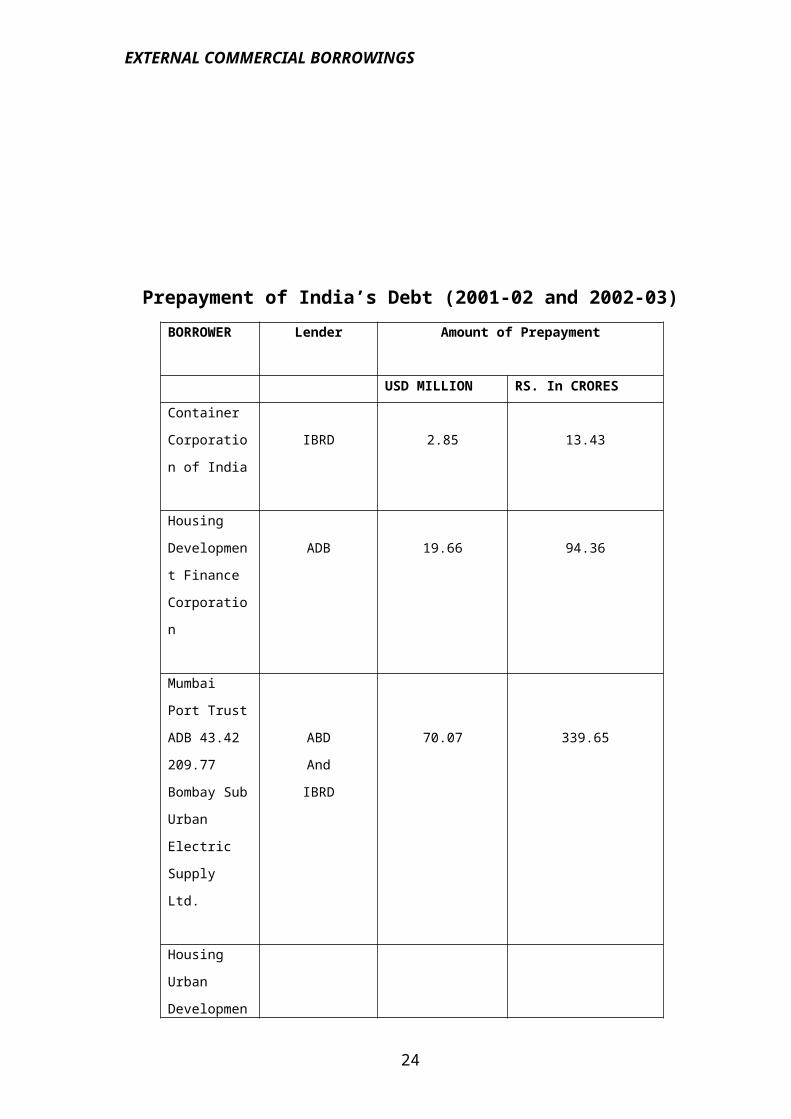

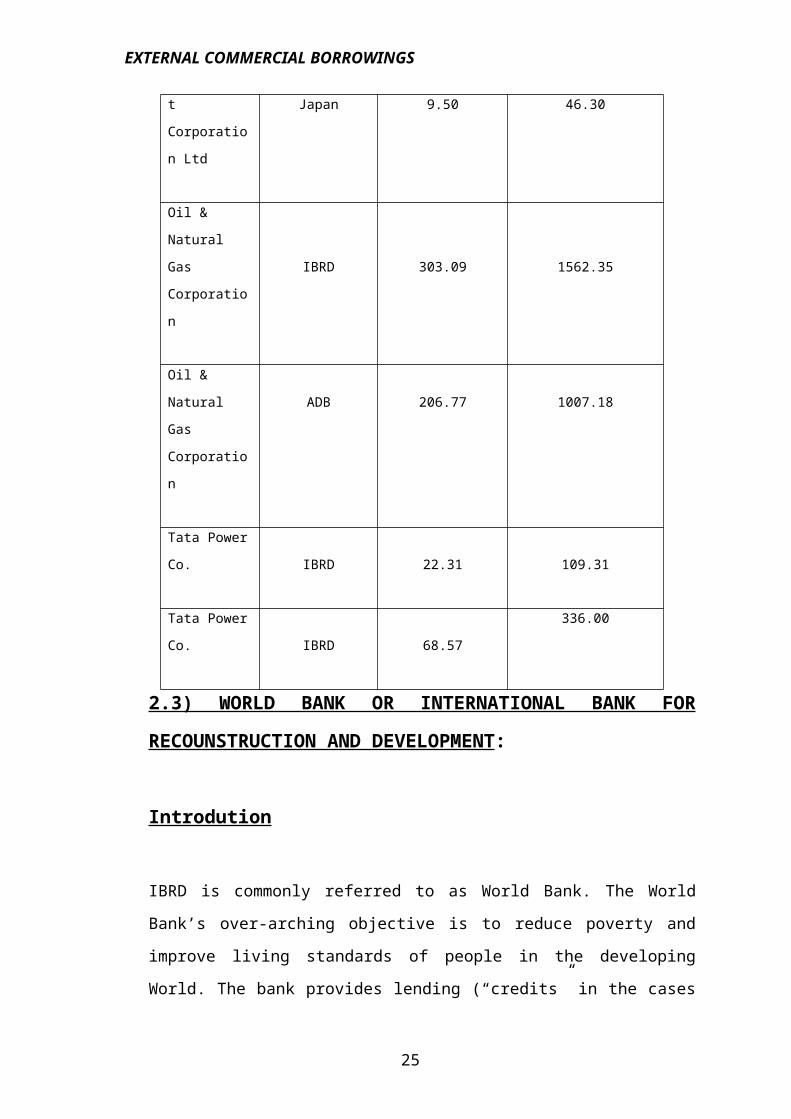

Prepayment of India’s Debt (2001-02 and 2002-03)

BORROWER Lender Amount of Prepayment

USD MILLION RS. In CRORES

Container

Corporation of

India

IBRD 2.85 13.43

Housing

Development

Finance

Corporation

ADB 19.66 94.36

Mumbai Port

Trust ADB

43.42 209.77

Bombay Sub

Urban Electric

Supply Ltd.

ABD

And

IBRD

70.07 339.65

Housing Urban

Development

Corporation

Ltd

Japan 9.50 46.30

Oil & Natural

Gas

Corporation IBRD 303.09 1562.35

Oil & Natural

Gas

Corporation

ADB 206.77 1007.18

Tata Power Co.

IBRD 22.31 109.31

Tata Power Co.

IBRD 68.57

336.00

16

EXTERNAL COMMERCIAL BORROWINGS

2.3) WORLD BANK OR INTERNATIONAL BANK FOR

RECOUNSTRUCTION AND DEVELOPMENT:

Introdution

IBRD is commonly referred to as World Bank. The World Bank’s over-arching

objective is to reduce poverty and improve living standards of people in the

developing World. The bank provides lending (“credits” in the cases of IDA and

technical assistance) and non lending (policy advice on the basis of economic and

sector work and increasing global knowledge and experience sharing) services to its

client countries. IBRD rises most of its money from bonds and other debt securities

issued in world financial markets, based on the guarantee of share capital

subscription from its members.other sources of banks funds are shareholders’ capital

and retained earnings. IBRD loans, though non-concessional, are available at

relatively more favorable term than commercial sources. The repayment period for

India is at present 20 years, inclusive of 5 years grace period. The bank offers three

types of loans presently (1) single currency variables spread loans, single currency

fixed spread loans (2) local currency loans. India was earlier borrowing under

currency pool loans. Presently India is borrowing under variable spread single

currency loans.

The currency rate of interest per annum on World Bank/IBRD loans is depending

upon the type of loan, currency mix of loan and year of negotiation.

The World Bank and IDA make loans for high priority projects and programs in

member countries to further their development programmes. These loans are made to

sovereign governments or to entities enjoying the full faith and credit of sovereign

governments.

17

EXTERNAL COMMERCIAL BORROWINGS

At the end of 1994 over 180 billion dollars had been subscribed but of this only about

3.36 percent is paid in. the bank’s lending programmes is financed in part through the

paid-in-capital, but mainly through commercial borrowings on the international

capital market.

Strength Through Diversity

The World Bank is a specialized agency of the United Nations, devoted to economic

and social development in its member countries. It now has 181 member countries,

each with different historical experiences, social dynamics, and economic and

political systems. The Bank's Articles of Agreement set out its broad scope of

activity in economic and social development. They also establish guidelines that limit

the range of its activities. In particular, the Articles state that, in all its decisions,

"only economic considerations shall be relevant."

World Bank Operations

The World Bank exists to encourage poor countries to develop by providing them

with technical assistance and funding for projects and policies that will realize the

countries' economic potential. The Bank views development as a long-term,

integrated endeavor.

During the first two decades of its existence, two thirds of the assistance provided by

the Bank went to electric power and transportation projects. Although these so-called

infrastructure projects remain important, the Bank has diversified its activities in

recent years as it has gained experience with and acquired new insights into the

development process.

In transportation projects, greater attention is given to constructing farm-to-market

roads. Rather than concentrating exclusively on cities, power projects increasingly

provide lighting and power for villages and small farms. Industrial projects place

greater emphasis on creating jobs in small enterprises. Labor-intensive construction

is used where practical. In addition to electric power, the Bank is supporting

18

EXTERNAL COMMERCIAL BORROWINGS

development of oil, gas, coal, fuel wood, and biomass as alternative sources of

energy.

Of the 34 very poor countries that borrowed money from IDA during the earliest

years, more than two dozen have made enough progress for them no longer to need

IDA money, leaving that money available to other countries that joined the Bank

more recently. Similarly, about 20 countries that formerly borrowed money from the

IBRD no longer have to do so. An outstanding example is Japan. For a period of 14

years, it borrowed from the IBRD. Now, the IBRD borrows large sums in Japan.

Source of Funding

The World Bank is an investment bank, intermediating between investors and

recipients, borrowing from the one and lending to the other. Its owners are the

governments of its 180 member nations with equity shares in the Bank, which were

valued at about $176 billion in June 1995. The IBRD obtains most of the funds it

lends to finance development by market borrowing through the issue of bonds (which

carry an AAA rating because repayment is guaranteed by member governments) to

individuals and private institutions in more than 100 countries. Its concessional loan

associate, IDA, is largely financed by grants from donor nations.

The Bank is a major borrower in the world's capital markets and the largest

nonresident borrower in virtually all countries where its issues are sold. It also

borrows money by selling bonds and notes directly to governments, their agencies,

and central banks. The proceeds of these bond sales are lent in turn to developing

countries at affordable rates of interest to help finance projects and policy reform

programs that give promise of success.

Although under special and highly restrictive circumstances the IMF borrows from

official entities (but not from private markets), it relies principally on its quota

subscriptions to finance its operations. The adequacy of these resources is reviewed

every five years.

19

EXTERNAL COMMERCIAL BORROWINGS

Recipients of Funding

Neither wealthy countries nor private individuals borrow from the World Bank,

which lends only to creditworthy governments of developing nations. The poorer the

country, the more favorable the conditions under which it can borrow from the Bank.

Developing countries whose per capita gross national product (GNP) exceeds $1,305

may borrow from the IBRD.

(Per capita GNP, a less formidable term than it sounds, is a measure of wealth,

obtained by dividing the value of goods and services produced in a country during

one year by the number of people in that country.)

Structure of World Bank

The structure of the Bank is somewhat more complex. The World Bank itself

comprises two major organizations: the International Bank for Reconstruction and

Development and the International Development Association (IDA). Moreover,

associated with, but legally and financially separate from the World Bank are the

International Finance Corporation, which mobilizes funding for private enterprises in

developing countries, the International Center for Settlement of Investment Disputes,

and the Multilateral Guarantee Agency. With over 7,000 staff members, the World

Bank Group is about three times as large as the IMF, and maintains about 40 offices

throughout the world, although 95 percent of its staff work at its Washington, D.C.,

headquarters. The Bank employs a staff with an astonishing range of expertise:

economists, engineers, urban planners, agronomists, statisticians, lawyers, portfolio

managers, loan officers, project appraisers, as well as experts in telecommunications,

water supply and sewerage, transportation, education, energy, rural development,

population and health care, and other disciplines.

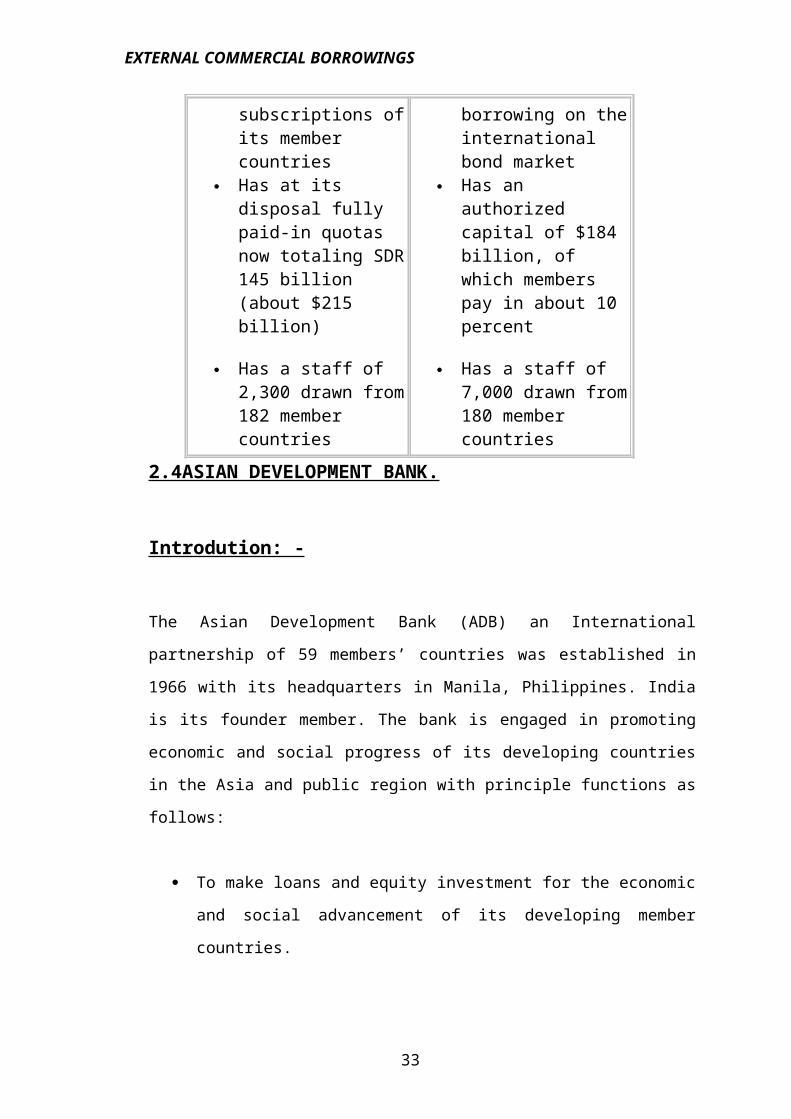

The International Monetary Fund and the World Bank at a Glance

International Monetary World Bank

20

EXTERNAL COMMERCIAL BORROWINGS

Fund Oversees the

international monetary system

Promotes exchange stability and orderly exchange relations among its member countries

Assists all members--both industrial and developing countries--that find themselves in temporary balance of payments difficulties by providing short- to medium-term credits

Supplements the currency reserves of its members through the allocation of SDRs (special drawing rights); to date SDR 21.4 billion has been issued to member countries in proportion to their quotas

Draws its financial resources principally from the quota subscriptions of its member countries

Has at its disposal fully paid-in quotas now totaling SDR 145 billion (about $215 billion)

Has a staff of 2,300 drawn from 182 member countries

Seeks to promote the economic development of the world's poorer countries

Assists developing countries through long-term financing of development projects and programs

Provides to the poorest developing countries whose per capita GNP is less than $865 a year special financial assistance through the International Development Association (IDA)

Encourages private enterprises in developing countries through its affiliate, the International Finance Corporation (IFC)

Acquires most of its financial resources by borrowing on the international bond market

Has an authorized capital of $184 billion, of which members pay in about 10 percent

Has a staff of 7,000 drawn from 180 member countries

2.4ASIAN DEVELOPMENT BANK.

Introdution: -

21

EXTERNAL COMMERCIAL BORROWINGS

The Asian Development Bank (ADB) an International partnership of 59 members’

countries was established in 1966 with its headquarters in Manila, Philippines. India

is its founder member. The bank is engaged in promoting economic and social

progress of its developing countries in the Asia and public region with principle

functions as follows:

To make loans and equity investment for the economic and social

advancement of its developing member countries.

To provide technical assistance for the preparation and execution of

development projects and programmes and advisory services.

To response to the requests for assistance in coordinating development

policies and plans of developing member countries.

ADB’s primary operational strategy is to assist government of India in rapid

industrlization. ADB provides finances to projects aimed at improving the structure

of the industrial sector, increasing its share of GDP, export earnings and employment

and making more effective use of productivity capacity. The Bank may also provide

the loans for big light energy programmes, transport, communication, industries and

non-fuel minerals, social infrastructure and multi-secton.

ADB’s Charter requires it to “foster economic growth and cooperation in the region”

and “to contribute to the acceleration of the process of economic development of the

developing member countries in the region, collectively and individually.” The

Charter states that “the operations of the Bank shall provide principally for the

financing of specific projects…” In its initial years, ADB translated this mandate into

the role of a project financing institution. This approach was based on the assumption

that growth and development would result from the transfer of capital and technology

to ADB’s developing member countries (DMCs). For 20 years, under this paradigm,

ADB successfully implemented an extensive project finance program in its DMCs.

22

EXTERNAL COMMERCIAL BORROWINGS

ADB has adopted poverty reduction as its overarching goal, and developed a

comprehensive strategy to combat poverty in the region. Building on this strategy as

well as other policy initiatives, ADB has recently adopted its LTSF, which commits

ADB to supporting the International Development Goals. Recognizing the important

role of the private sector in development, ADB has also adopted a wide-ranging

private sector development strategy.7 The Medium-Term Strategy (MTS),8 which has

been submitted to the Board, provides more detailed guidance on how ADB should

work with its DMCs to achieve these goals. With this, the strategic reorientation

process has been completed.

“To remain an effective institution relevant to the changing needs of the region,

ADB has continually been adapting its priorities, assistance modalities, and

organizational structure, and has transformed itself from what was essentially a

project financier to a full-fledged development institution. On the organizational

front, major changes have included

a) Creating regional vice presidencies, each with one programs and two projects

departments (east and west);

b) Establishing the Office of Pacific Operations (OPO);

c) Merging the Office of Environment and the Social Dimensions Unit into the

Office of Environment and Social Development (OESD), reporting to the

President;

d) Merging the Development Policy Office and Strategic Planning Unit to create

the Strategy and Policy Office, (now Strategy and Policy Department [SPD]);

and

e) Upgrading the Co financing Division into the Office of Co financing

perations; and

f) Strengthening resident missions (RMs) under a new policy (2000).

23

EXTERNAL COMMERCIAL BORROWINGS

In response to these imperatives for change, ADB has already started to address

organizational issues with the redesign of operational business processes and the RM

Policy. These changes must now be carried forward in a more comprehensive way.

Organization

ADB is managed by a Board of Director, a Board of Director a President, four Vice-

Presidents, and the Heads Of Departments And Offices.

Each member country nominates one Governor and an Alternate Governor to vote on

its behalf.

The Board of Governors elects the 12 Directors (each with an alternate)—eight

representing countries within the Asia-Pacific region and four representing countries

outside the region.

The Board of Governors also elects the President for a term of five years, with the

possibility of reelection. The President chairs the Board of Directors and follows its

directions in conducting the business of ADB.

Objective and Principles of Asian development bank:

The overall objective of organizational change is to enhance ADB’s development

impact by strengthening its capacity to deliver its strategic agenda through a carefully

planned, selective, country-focused, and technically excellent program of assistance

to its DMCs and subregions. Drawing on the discussion in chapter III, a number of

principles have been developed to guide the analysis of options to meet this

objective.

Mainstream: Governance and Capacity Building, Environmental and Social

Development, and Private Sector Development. Operational departments should be

responsible for addressing and delivering products for meeting these objectives—a

process often known as “mainstreaming.” Delivery of products and services in these

24

EXTERNAL COMMERCIAL BORROWINGS

areas should be organizationally separated from policy development and compliance

oversight.

Balance Country and Sector Considerations: Country considerations and priorities

should drive sector and project decisions. However, measures are also needed to

ensure that sectoral expertise is preserved. The functional responsibilities of sector

units should be realigned with ADB’s current strategic priorities.

Strengthen ADB’s Regional Role and Identity: The country and sector focus

should also support ADB’s regional role. The organization structure should

institutionalize the regional role of ADB and facilitate linkage with regional

institutions.

Greater Client and Stakeholder Orientation: Whatever organization structure is

adopted, ADB should become a more outward-looking, client focused, and

collaborative development partner.

Maintain Technical Excellence and Skills: Maintenance of technical excellence is

essential for effective project design and delivery.

Emphasize Effectiveness and Efficiency: Development impact depends on the

efficiency and effectiveness of assistance. ADB justifiably takes pride in being the

most “efficient” of the MDBs. It is also important to find means to enhance

effectiveness through structural changes that emphasize implementation and outputs

that can be monitored for their impact.

Maintain Checks and Balances Consistent with Effectiveness: Every organization

needs a clear set of checks and balances to ensure compliance with its policies and

procedures; maintain the quality of its output, and reduce the impact of conflicts of

interest. However, such checks and balances should not stifle initiative or reduce the

effectiveness of delivery of services to DMCs.

Clarity of responsibility and Value Addition: Each separate unit and position

within an organization should be justified on the basis of the value it adds to output

25

EXTERNAL COMMERCIAL BORROWINGS

and should be held accountable for a unique set of results. There is great potential to

streamline, increase productivity, and improve motivation by the application of the

value-added principle to units, positions, and processes, all of which finally

contribute to overall organizational effectiveness. Duplication of responsibility

should be avoided.

Ownership of Change: Organizational change must have the backing and ownership

of the staff affected by it, so that staff morale is maintained and the changes can be

smoothly and successfully implemented.

Procedural Aspects:

1. In processing a sector loan, the following procedures should be

followed:

(i) The borrowing DMC should submit to the Bank (a) an acceptable medium-or

long-term sector/subsector development plan or program; (b) a statement on sector

policies that affect the development of the sector/subsector concerned; and (c) an

assessment of the technical and managerial capabilities of the sector institutions to

develop, process, and implement projects.

(ii) Subject to general acceptability to the Bank of the sector plan, policies, and

institutions, and prima facie justification of Bank assistance, the Bank will send a

fact-finding mission to hold preliminary discussions with the borrower; to assess

broadly the sector development plan, the financing needs of the sector, and the

adequacy of the institutional arrangements available or proposed for implementing

the sector loan; and to identify key sector policy issues including cost recovery

aspects.

(iii) Based on the findings of the mission and after a management review meeting has

cleared the loan proposal, an appraisal mission will be dispatched to the field. The

mission should determine the scope and amount of the proposed sector loan; examine

the availability and types of subprojects for financing; assess the technical and

managerial capabilities of the executing agencies, and whether technical assistance is

26

EXTERNAL COMMERCIAL BORROWINGS

needed; formulate the relevant technical, financial, and economic criteria for

selection and appraisal of subprojects; agree on the threshold for approval of

subprojects by the Bank; assess the institutional risks in regard to processing and

implementing capabilities; and assess the scope for resolution of key policy issues,

including cost recovery aspects, necessary to achieve sectoral objectives.

2. The processing stages applicable for a project loan 1 will also apply to

sector loans.

Supervision and Monitoring

Direct supervision of subproject implementation and monitoring of subproject

operation and performance are the primary responsibility of the borrower or its

executing agency. Bank staff will, however, review the execution of subprojects on a

selective basis. Bank staff will also monitor, at appropriate time intervals, the

capability and performance of the executing agency, and any change in

circumstances that would have a bearing on the sector development program in

general and on the implementation and operation of the sector projects in particular.

Disbursement

The Bank's standard disbursement procedures are normally used. For qualified

executing agencies, the Bank may agree to the use of an imprest account for

payments of goods and services related to subloans or subprojects, not exceeding six

months' estimated expenditures; statement of expenditures procedures up to the free

limit for subloans may also be used.

Lending and Re-lending polices: -

Article 9 of the Bank's Articles of Agreement (the Charter) states that the Bank's

lending operations will consist of ordinary operations and special operations; the

former are financed from the ordinary capital resources (OCR) and the latter from the

27

EXTERNAL COMMERCIAL BORROWINGS

Special Funds resources. Articles 19 and 20 of the Charter describe the establishment

and utilization of Special Funds resources.

The Asian Development Fund (ADF), established in 1974, is a Special Fund under

the Charter for carrying out the Bank's concessional lending operations.2

Eligibility for and Allocation of ADF Assistance

DMCs are classified by the Bank into three Groups (A, B, and C) primarily on

considerations of gross national product (GNP) and debt repayment capacity.3 The

eligibility of a DMC for ADF resources is broadly related to the Group to which it

belongs. In principle, Group A countries are fully eligible for ADF financing, Group

B countries are eligible for limited amounts in particular circumstances, and Group C

countries are not eligible. Special consideration is given to certain Pacific island

DMCs in determining their eligibility for ADF resources.

While ADF eligibility criteria have remained unchanged since the establishment of

the ADF, the changing economic environment in certain DMCs, together with the

availability of ADF resources, determines the actual allocation of ADF resources

from time to time.

Terms of Lending

ADF loans for ADF-only countries have a fixed repayment period of 40 years

including a grace period of 10 years. Principal repayment is at the rate of 2 percent of

the total amount of principal outstanding each year for the first 10 years after the

grace period, and 4 percent a year thereafter. ADF loans to OCR/ADF blend

countries have a repayment period of 35 years including a grace period of 10 years;

the principal repayment is at the rate of 2.5 percent of the total amount of principal

outstanding each year for the first 10 years after the grace period, and 5 percent a

year thereafter. There is a service charge of 1 percent for ADF loans, payable on the

principal amount disbursed and outstanding from time to time, but no commitment

fee.

28

EXTERNAL COMMERCIAL BORROWINGS

The terms of loans committed from ADF resources may be adjusted to reflect

substantial changes in individual countries' economic circumstances. Accordingly,

repayments of principal on an outstanding ADF loan to a particular country will be

increased by 100 percent of the originally scheduled amount if (i) the per capita GNP

of the country has remained above the ADF eligibility benchmark for five

consecutive years, and (ii) the country has achieved the capacity to repay debt on

OCR terms. In lieu of increasing repayments of some or all remaining principal, the

borrower may request the payment of interest at an annual rate agreed upon with the

Bank on the loan amount disbursed and outstanding, provided that the resulting grant

element would be the same as the one resulting from increasing the remaining

principal repayments by 100 percent. In no case will an adjustment of terms be

considered during the 10-year grace period. If after such an adjustment a country

experiences economic deterioration, the Bank will have the flexibility to allow the

country to revert to its original repayment schedule and service charge.

The standard ADF terms will apply to all lending modalities, including project and

program loans, supplementary loans, and technical assistance loans.

Re-payment of Loan

A borrower can repay all or part of a loan in advance of the maturity specified in the

loan agreement by giving notice to the Bank 45 days in advance (this can be reduced

or waived by the Bank) and upon payment of all accrued service charges.12 On the

date of prepayment of only a portion of the loan, there should not be outstanding any

portion of the loan maturing after the portion to be prepaid.

2.5) FIXED-RATE BORROWINGS INCLUDES:

29

EXTERNAL COMMERCIAL BORROWINGS

1. BUYER’S CREDIT

2. SUPPLIER’S CREDIT

3. FIXED-RATE LOANS.

1) Buyer’s Credit

Under Buyer’s credit arrangements, a specific Long-Term loans is granted by a

designated lending agency in the exporter’s country to the buyer in the importer

country against a guarantee by an acceptable bank or financial institution. The

supplier receives payment for the exports on his delivering to the lending agency the

requisite documents specified in loan agreement and the relative commercial

contract. The lending agency realizes the payment from buyer (importer) in

installment as and when they fall due. Ordinarily, the period of credit is reckoned as

the duration form the date of completion by the supplier of his obligation under the

contract to the date of final payment by the buyer under the credit.

Supplier’ Credit

Supplier’s Credit, on the other hand, is extended to the supplier’s (exporter) by the

financial institutions (in the exporter-country) to finance his deferred receivables.

The buyer required to provide the requisite guarantee from an acceptable bank or

financial institution in the importer country.

Credit may also be extended by the supplier (exporter) directly to his buyer

(importer) on the deferred payment terms against his providing guarantee as above.

In this case, the supplier will realies the precedes for his exports by the discounting

the bills of exchange (Drawn on and accepted by buyer) with his bank or the

designated government agency in his country. Such credits, however, are not really

supplier’s credit in technical sense. Technically both supplier’s credit and buyer’s

credit are extended by the lending agency in the exporter’s country; when it is

granted to the supplier (exporter), it is a supplier’s credit and when it is granted to the

30

EXTERNAL COMMERCIAL BORROWINGS

buyer (importer), it is buyer credit. The credit extended by the supplier directly to his

buyer is in the nature of trade credit.

Fixed-Rate Loan

In addition to above two methods, fixed-rate loans can also be raised through

commercial banks. Such loans are normally arranged for a period upto 8 years and

are priced at a specific spread above the going rare is concerned country of the

chosen currency.

Comparative Cost Of Advantage.

Of the above three type of credit, supplier’s credit may, in many cases, prove to be

more expensive as the supplier is likely to add a premium in the price quoted for the

goods or in the rate of interest so as to compensate him for the additional cost

incurred by him in the process. As against this buyer’s credit may be relatively as the

supplier under this arrangement is paid of immediately and the lender realises the

payment from buyer as per agreed terms. The interest rate quoted on the fixed-rate

loan by the commercial banks depends upon the comparative edge of the concerned

bank in the particular Euro-currency market.

31

EXTERNAL COMMERCIAL BORROWINGS

2.6) INTERNATIONAL DEVELOPMENT ASSOCIATION: -

What is International Development Association?

The International Development Association (IDA), established in 1960, is the part of

the World Bank Group that provides long-term interest-free loans (credits) and grants

to the poorest of the developing countries. It does this to support economic growth,

reduce poverty and improve living conditions. IDA is now the single largest source

of donor funds for basic social services in the poorest countries. In the 12 months to

June 30, 2003, IDA’s support for projects was targeted at human development such

as education, health, social safety nets, water supply and sanitation (44%),

infrastructure (26%), and agriculture and rural development (11%).

IDA, the Soft-Loan affiliate of the bank, depends almost entirely on contributions

made from time to time by the wealthier member governments for its financial

resources, repayment for earlier credits and transfer from the net income of IBRD.

Being the Soft Loan counterpart of the bank, IDA has concentrated its lending in

social sectors consisting of poverty reduction, human development and agricultural/

rural sector, each accounting for about a third of total of IDA commitments in recent

years. The other sectors of funding have been infrastructure, economic adjustment

and natural resources.

Which countries are eligible to borrow IDA resources?

Following three factors determine whether countries are eligible for IDA assistance:

Relative poverty, defined as Gross National Product (income) per person

below an established threshold, currently US$865 per year.

Lack of creditworthiness to borrow on market terms and therefore a need for

concessional resources to finance the country's development program.

32

EXTERNAL COMMERCIAL BORROWINGS

Good policy performance, defined as the implementation of economic and

social policies that promote growth and poverty reduction.

Some countries, such as India and Indonesia, are eligible for IDA assistance due to

their low per person incomes, but are also creditworthy for some IBRD borrowing.

These countries are known as "Blend" borrowers.

Where do IDA resources come from?

The largest source of IDA resources is new contributions from donor countries. This

accounts for about $13 billion of approximately $23 billion in resources which will

be made available to IDA borrowers during the three year period of IDA13. The

second largest source is internal resources, which include repayments from graduated

and current IDA borrowers, investment income, and other resources including

residual resources from past replenishments. The bulk of internal resources are

repayments, which amount to approximately $4 billion in IDA13. An additional

source of funds is transfers from IBRD net income, which will total about $900

million in IDA13. The largest pledges to IDA13 were made by the United States,

Japan, Germany, United Kingdom, France, Canada and Italy. Combined, these

countries account for about 70% of donor contributions to IDA13.

Performance Ratings

Every year World Bank staff assesses the quality of each borrower's policy

performance on the following parameters.

Economic Management

Structural Policies

Policies for Social Inclusion/Equity

Public Sector management and Institutions

33

EXTERNAL COMMERCIAL BORROWINGS

Finally, the performance assessment also takes into account the performance of the

country's active project portfolio performance. The combined rating is scaled up or

down depending on the strength of the country's performance.

Allocation Process

The allocation of IDA's resources is determined primarily by each borrower's rating

in the annual country performance and institutional assessment. In addition, the

IDA14 Agreement recommends that because the acceleration of economic and social

development in Sub-Saharan Africa remains foremost among IDA's priorities, these

countries should receive priority in the allocation process, provided that policy

performance warrants it. Finally, for borrowers that are eligible for both IDA and

IBRD funds ("Blend countries"), allocations must take into account those countries'

creditworthiness for and access to other sources of funds as well as their ability to use

IDA resources effectively to tackle poverty.

Individual country performance-based allocations serve as an anchor for the

formulation of Country Assistance Strategy (CAS) lending programs.

34

EXTERNAL COMMERCIAL BORROWINGS

2.7) International Finance Syndication Of Loans: -

International finance plays a very important role in financing the cost of capital of

projects the corporate sector.

International finance in Indian private business has been encouraged by the

government in a selective and phased manner. After independence the inflow took

shape of collaboration and foreign loans and grant on government basis from

different countries as also international agencies like International Bank For

Reconstruction and development (IBRD) and International Development Association

(IDA) are mainly utilize for financing the public sector projects and meeting the

countries deficit. Foreign capital in private company came through investment made

by multinational corporation (MNCs) in Indian subsidiaries. In 1973, Govt. of India

enacted Foreign Exchange Regulation Act (FERA) with a view to synchronizing the

inflow of foreign investment with the changing need of the country.

Today, international finance for the development of industry in India is coming

through many channels viz., Bilateral arrangement of Government as discussed

above, all India financial Institutions, Foreign Banks operating in international

markets, Indian Banks operating in international market.

All India Financial Institutions raise their resources in foreign currencies to enable

the Indian entrepreneurs the import of capital goods, technical know-how and

technology in India for accelerating the pace of industrial development. These

institutions raised the resources in foreign currencies through prescribed modes.

Besides the above, finance in international market is being arranged by private

organisations with the permission of Central Govt. through bond issue or syndicated

loan arranged through Commercial Banks and Foreign Banks.

35

EXTERNAL COMMERCIAL BORROWINGS

2.8) INTRNATIONAL FINANCE MARKET :

In international financial market, the borrow from one country may seek lenders in

other countries in specific currencies which need not be of the participant country. In

International Finance market, the availability of foreign currency is assured under

four main systems:

I. Euro Currency Market;

II. Export Credit Facilities;

III. Bond Issue, and,

IV. Financial Institutions

I. Euro Currency Market

Here funds are made available as loans through syndicated Euro credits or

instruments known as floating rate notes (FRNS). Interest rates very every six

months based on London-inter bank offered – rate (LIBOR). Syndicated Euro

currency bank loan has developed into one of the most important instruments for

international lending. Syndicated Euro credit is available through instruments viz.,

Term Loan Revolving Line Facility.

II Export Credit Facility:

Export Credit facilities are made available by several countries through an

institutional frame work in which EXIM Banks play a prominent role EXIM of India

is playing a significant role in financing export and other off-shore deals.

III. Bond Markets :

International bond market provided facilities to raise long term funds by using

different types of instruments. The bond market is generally known as Euro bond

market

36

EXTERNAL COMMERCIAL BORROWINGS

IV Financial Institution:

UN Agency Financial Institution Viz. IMF of World Bank and its allied agencies,

IFC(W), ADB, etc. provides finance foreign currency.

New International Instruments:

Swap is an international finance market instruments for managing funds. The basic

concept involved in Swaps is matching of difference between spot exchange rate for

a currency and the forward rate. The Swap rate is the cost of exchange one currency

into another for a specified period of time. The Swap will represent an increase in the

value of forward exchange rate. The Swap will represent an increase in the value of

the forward exchange rate (premium of a decrease discount). There are main three

types of Swaps (a) interest Swap (b) currency Swap (c) combination of both.

Nonetheless, the amount of foreign direct investment in these has been rising over

the past few years. To attract funds from foreign investors, well-functioning domestic

financial system must exist and particularly interest rates need to be market

determined. Two factors viz. lack of credit worthiness and standards of investor

protection on domestic financial market prevent fuller utilization of international

financial markets by developing countries. International financial markets offer

developing countries the possibilities of attracting the funds they need for their

development. The share of development countries utilization of international bonds is

negligible.

Syndicated Eurocurrency Loans:

The Eurocurrency market refers to the availability of a particular currency in the

international financial market outside the ‘Home country’ of that currency. For

example, the Eurodollar market refers to the financial market for US dollars in

England, France, West Germany, Hong Kong and other financial centres outside the

37

EXTERNAL COMMERCIAL BORROWINGS

US. The Eurodoller borrowing may be evidence by issue of commercial paper in the

form of promissory notes, or by subscription to bond/debentures or it may be

syndicated loan type.

Main Objectives of Syndication (Borrower’ point of view)

Large sums is arranged without delay and at least cost.

Gets better introduction to enter into international loan market without much

difficulty.

Funds are made available easily for meeting balance of payment deficit and

for financing large industrial projects.

The borrower is allowed to select the length of the roll over period and in

choosing different currencies to repay or cancel agreement after a short notice

period without penalty.

Lenders’ point of view

It helps the bank to share large credits with other bank, to finance many

borrowers.

Different size banks can participate.

It provides more profitability to banks as cost are relatively low.

Syndicated loans is under-written by a small group banks which resell

portions of the commitments to other banks.

Type of Euro-bond market instruments- There are four types of

Eurobond instrument Viz.

1. Straight-debt Eurobond carrying a fixed rate of interest.

2. Convertible bonds having a fixed rate of interest with option of conversion

into equity of the borrowing company.

3. Currency option bonds, giving the option of buying them into one currency

while taking payments of interest and principle in another.

38

EXTERNAL COMMERCIAL BORROWINGS

4. Floating rate notes, where rate of return is adjusted at regular intervals to

reflect changes in short-term money market rates.

During the last more than four decades the syndicated loan market, has developed

into a vital source of foreign capital and the major international banks have

‘syndicated’ to provide billon of dollars worth of foreign capital to finance medium

term requirements of five to eight years for all categories of borrowers comprising

governments, public and private sectors.

39

EXTERNAL COMMERCIAL BORROWINGS

2.9) INTERNATIONAL FINANCE CORPORATION: -

INTRODUCTION

The International Finance Corporation (IFC) is a member of the World Bank Group,

which also includes the International Bank for Reconstruction and Development

(IBRD), the International Development Association (IDA), and the Multilateral

Investment Guarantee Agency (MIGA). IFC’s business is investment in private

sector projects through loans, equity investment, and other financial instruments. It is

IFC policy that all its operations are carried out in an environmentally and socially

responsible manner. To this end, IFC projects must comply with applicable IFC

environmental, social and disclosure policies. In addition, IFC applies World Bank

Group environmental, health and safety guidelines to all projects. In sectors where no

appropriate IFC policies or guidelines exist, IFC applies relevant internationally

recognized standards. Furthermore, the project sponsor must ensure compliance with

host country requirements.

IFC’s client base and project cycle are different from those of the World Bank. IFC’s

environmental and social policies, while harmonized with World Bank policies, are

adapted to the private sector nature of IFC’s business.

IFC reviews prospective projects for soundness before it invests, focusing on

economic, financial, technical, legal, environmental and social issues during the

project appraisal process. This environmental and social review procedure has been

prepared for IFC staff and project sponsors for the review of a prospective project. A

separate environmental procedure applies to small projects approved under delegated

authority to management (e.g., Africa Enterprise Fund).

IFC’s Environment and Social Development Department is responsible for the

environmental and social review, clearance and supervision of projects in a manner

consistent with the requirements contained in this review procedure. The Director of

the Environment and Social Development Department reports to IFC’s Executive

40

EXTERNAL COMMERCIAL BORROWINGS

Vice President. In addition, to achieve better integration of environmental and social

considerations within IFC operations and to ensure high performance standards, an

IFC Vice President has corporate oversight for environmental and social issues and

disclosure matters.

The procedure: (a) discusses applicable environmental and social policies; (b)

outlines applicable environmental and other guidelines; (c) describes the project

cycle which IFC uses in evaluating a prospective project and highlights where in the

cycle IFC Environment and Social Development staff are required to provide input;

and (d) details the procedures that IFC staff must follow to ensure that projects meet

IFC’s commitment to environmentally sustainable and socially responsible projects.

Polices Of International Finance Corporation

IFC environmental and social policies are fundamental to the project appraisal,

approval and supervision process. Applicable operational policies are: OP 4.01,

Environmental Assessment; OP 4.04, Natural Habitats; OP 4.09, Pest Management;

OP 4.10, Indigenous Peoples (forthcoming); OP 4.11, Safeguarding Cultural Property

in IFC-Financed Projects (forthcoming); OP 4.12, Involuntary Resettlement

(forthcoming); OP 4.36, Forestry; OP 4.37, Safety of Dams (forthcoming); and OP

7.50, Projects on International Waterways.

Description of Policies of International Finance Corporation

Environmental Assessment: -

IFC policy on environmental assessment (EA) states that all projects proposed for

IFC financing require an EA to ensure that they are environmentally and socially

sound and sustainable. EA is a process whose breadth, depth and type of assessment

varies according to the type of project. Various instruments are used to perform the

EA depending on the complexity of the project. They include: an environmental

impact assessment (EIA), an environmental audit, a hazard or risk assessment, and an

41

EXTERNAL COMMERCIAL BORROWINGS

environmental action plan (EAP). The policy requires that all IFC projects be

categorized. Categories are: ‘A’, ‘B’, ‘C’, and ‘FI’. Definitions of each of these

categories are described later in the procedure. OP 4.01 also sets forth the minimum

requirements for public consultation and public disclosure for projects.

Natural Habits: -

This policy affirms IFC’s commitment to promote and support natural habitat

conservation and improved land use, and the protection, maintenance, and

rehabilitation of natural habitats and their functions in its project financing. IFC does

not support projects that involve significant conversion or degradation of critical

natural habitats.

Pest Management: -

IFC supports the use of biological or environmental control methods rather than the

use of pesticides where there is a need for pest management. Where pesticides are

required, this policy sets forth the criteria for their use.

Indigenous People: -

[Forthcoming] Pending finalization of this OP, IFC projects must comply with the

World Bank’s OD 4.20, Indigenous Peoples, as appropriate in a private sector

context.

Safeguarding Cultural Property in IFC Financed Projects: -

[Forthcoming] Pending finalization of this OP, IFC projects must comply with the

World Bank’s OPN 11.03, Cultural Property, as appropriate in a private sector

context.

Involuntary Restatements: -

[Forthcoming] This policy is applied wherever land, housing or other resources are

taken involuntarily from people. It sets out the objectives to be met and procedures to

42

EXTERNAL COMMERCIAL BORROWINGS

be followed for carrying out baseline studies, impact analyses, and mitigation plans

when affected people must move or lose part or all of their livelihoods. An annex to

OP 4.30 presents the outline for a Resettlement Plan, the key document to be

prepared by the project sponsor.

Safety Of Dames: -

This policy sets forth IFC’s requirements for projects where dams are to be

constructed. The owner of a dam has full responsibility for the safety of the dam. IFC

requires that dams be designed and constructed by experienced and competent

professionals. For large dams (over 15 meters high) and dams between 10 and 15

meters that present special design complexities, IFC requires reviews by a panel of

independent experts, preparation of detailed plans, and periodic safety inspections.

The policy covers mine tailings dams and dams containing other material such as ash

from power plants, as well as water storage dams.

43

EXTERNAL COMMERCIAL BORROWINGS

44

EXTERNAL COMMERCIAL BORROWINGS

Monitoring and Supervision

IFC uses the term "supervision" differently from the Bank, due to differences in

project cycles of the two institutions. Accordingly, the Bank’s OD 13.05 Project

Supervision does not apply to IFC.

IFC monitors the environmental and social performance of projects in its investment

portfolio. Project monitoring usually occurs in one or more of the following ways:

Supervision missions carried out by the Investment Department and the Technical

and Environment Department; and/or Project site visits by staff of the Environment

Division. The frequency of the site visits depend on the environmental and social

complexity of a project.

The investment officer, in cooperation with the technical specialist and after

consultation with the environmental and social development specialists, is

responsible for ensuring that supervision reports include information on the project

company’s compliance with environmental and social requirements. The investment

officer is also responsible for ensuring that annual environmental monitoring reports

are provided to the Environment Division as required in the legal documentation for

the project. The Environment Division is responsible for reviewing such reports and

determining whether the project company’s compliance with environmental and

social requirements is satisfactory. In the case of non-compliance, the Environment

Division discusses an appropriate course of action with the Investment and Legal

Departments and specialists in the Technical and Environment Department. The

investment officer notifies the project company of this action and any necessary

follow-up requirements. The investment officer is responsible for follow-up with

both the project company and the Environment Division until the non-compliance

situation is resolved.

Project Supervision Reports (PSRs), which IFC prepares at least annually, must

include a section on environmental and social compliance with regard to covenants in

the investment agreement. In addition, the PSR must state whether the Environment

45

EXTERNAL COMMERCIAL BORROWINGS

Division has received the Annual Monitoring Report (as required in the investment

agreement), the date submitted to IFC and the date reviewed by the Environment

Division.

Evaluation

During the course of selected projects an Investment Assessment Report (IAR) is

prepared which summarizes the evaluations of the actual environmental and social

impacts of the project against the impacts anticipated in the EA report, and assesses

the effectiveness of the mitigating measures. The Environment Division provides