ebooksclub.org applied eco no metric time series1

TRANSCRIPT

).-.

tt

J .#

Applied EconometricTime Series

WALTER ENDERSloWaState University

Jox wILEY & soNs.mc.

PREFACE

'This book was borne out of fnlstration. After returning from aI1 cnjoyable and pro-ductivesabbatical at the University of California at San Diego, I bcgan expanding

7 the empirical content of my graduate-level classcs in macroecohomics and intelma-.

' M' ---

.

.;; tional t'inance.Students' interest surged as lhey began to understand th concunzntdevelopmcntof macroeconomic theot'y and time-series econometrcs. The differ-

' ence between Keynesins. monetarists. the rational expectations school. and thcir ability to explain me

71''

realbusiness cycle approach could best be understood by the. .

,i)empiricalregularities in the economy. Old-style macroeconomic mtdels were dis- 'carded becausc of their empirical inadequacies, not because of any logicltl inconsis- k,' '

'';!r7: ltencies. )

.'

,

''

.,

'

.

..

j

Iowa State University has a world-class Statistics Department, and most of our EE '

,

. ..j

,.

r,yeconomicsstudents take thrce of four statistics classes. Nevertheless. students' '' r ,

. q.. ).t ) rjbackgroundswere inadequate for the empirical portion of my courses. 1 needed to ttk '

. q .( k;. . ..;.,. !present A feasmable number of lectures on the topics covered in this book. M7 ;)'

t ?.7

frustrationwas that the journal articles were written for those already technically E5. ..)

. .

r',q'

,

proficientin time-selies' economctrics. The existing time-sdries texts were inade-.) kt'(

quate to the task. Some focsed on forecasting, others on theoretical econometric..j.issues, and still others on tecbniques that are intrequently used in the economics lit- i

erature. The idea for this text began as my class notes and use of handouts grew in- C. . l

ordinately.Finally, l began teaching a new coursc in applied time-series economet- E t.

)li CS . ( ' l

... j tMy orignal intent was to write a text on time-serits macroeconometrics. Fprtu- : rh ,

nately,my colleagues at Iowa State convinced me to broaden the focus; applied mi- ' ;' L

g.: r. - . ycroeconomistswere also cmbracing time-series methods. I decided to include ex- .,

;,q .:y

amplesdrawn from agricultural economics, international finance. and some of my i '. $.76. .)yk...j.gtt)work with Todd Sandlcr on thc study of transnational terrorism. You should find' .

: j.,.r

..

,. jjjt:.

:Ltc.,ytj.the examples in the text to provide a reasonable balance between macfoeconomic ' .

y',4

. .1.: .p.iri .-.;

and microeconomic applications. , 4 )! jk tThc text is intended for those with some background in fultiple regresslon '.

.

!rj :-j t

. jy. . .r.rjy.!:.jj(). y.) .analysis. I presulne the reder understands the assumptions underlying the tlse of .

.'L:).!.

.

,))t.. ?

ordina:yleast squarcs. X11of my students are familiar with the concepts of correla- l j ):y( :. . .y.;tiin and covariation', they also know how to tlse t-tests and Fltests within a regres- Sj. '$,?

j.

.t... , ,. c, . hi ;. .,7t..

.

-

.sion framework. I use terms juch as titean square drr/r, lgnycance fev'f. anq un- i ,l' ? k

. ..

tL'!)7# .#. jsbiased estimate without cxplaining thcir meaning. The last two chplers o the text 's. j'examine multiple time-jeries techniques. To work through these chapters, it is nec- 'it' 3. tf

. . . . . .). (.

),.ry jrf:..)jy

essae to know bow to solve a system of equations using mtrx algebra. Cbapter 1, ..s.y t tt. .

..

..

.. ! k.' tfentitled tDifference Equations. ' is the cornerstone of the text. In my cxperience.) . .t . '. i

. . .). ., . . 4 .. 1)

this material and a knowledge of regressipn are sufcient to bring students to th . );jT

. . ,.

. . yj.pointwhere they are able to read (he profesional jouimalsand to embark on a seri- ' rt lr.

tu dy ..

..

'

. l) . ., jous applird s

I bclicvc in tcaching by induction. Thc mcthotl is to take a simple example and.

build towards more general and more complicattld models and econometric proce- E

.(dures. Detailed examples of each procedure are provided. Each concludcs with a .

;

L'

'.

step-by-stepsummary of tlle stages typically employed in using that procedure. eae'

'

approach is one of learning by doing. A large number of solved problems are in- .

cluded in the body of each chapter. The Questionsand Exercises at the end of each'

chapter are especially important. ney have been designed to complement the ma- '

tedal in the text. In order to work through the excrcises, it is necessary to have ac-!

cess to a soware package such as RATS. SAS, SHAZAM, or TSP. Matrix pack-ages stlch as MARAB and GAUSS are not as convenient for univariate models.Packages such as MINITAB. SPSSX. and MICROFIT can perform many of theprocedurescovered in te exercises. You are encouraged to work through as manyof the examples and exercises as possible. The answers to all qnestions are con-tained in the lnstructor's Manual. Most of thc questions are answered in great de-tail. In addition, the Insructor's Manual contaias the data disk and the computerprograms that can be used to answer the end of chapter exerciscs. Programs areprovided for the most popular software packages.

In spite of a11 my efforts. some errors have undoubtedly crept into thc tcxt.Portions of the manuscript that are crystal clear to me, will surely be opaque to oth-ers. Towards this end, I plan to keep a list of corrections and clalifications. You canreceive a copy (ofwhat I hope is a short list) from my lnternet address [email protected].

Many pcople made valuable suggestions for improving the manuscript. I am .grateful to my students who kept me challenge and were quick to point out errors.Pin Chung was especially helpful in carefully reading the many dras of the manu-script and ferreting out numerous mistakes. Selahattin Dibooglu at the Universityof Illinois at Carbondalc and Harvey Cutlcr at Colorado State University used por-tions of thc text in their own courses; thcir comments concerning the organization,style. and clarity of presentation are mucl) appreciated. My collengue Ban'y Falk

was more than willing to answcr my questions und make helpful suggestions. Hae-Shin Hwang, Texas A and M University; Paul D. McNelis, Georgetown University;H ad i Es ta l! a n , Un iv e rs ity o f I ll in o is ; M . Da n ie l W e s tbr ook , Ge o rge t o w nUniversity'. Beth Ingram. University of Iowa'. and Subhash C. Ray, University ofConnecticut al1 providcd insightful reviews of various stages of the manuscript.Julio Herrera and Nifacio Velasco, the

''food

gurus'' at the. Univers'ityof Valladolid.hclped me survive the final stages of proofreading. Most of all, I would like tothank my lovillg wife Linda for putting up with me while 1 was working on the text.

CHAPTER 1: Difference Equations1. Time-series Modeis2. Difference Equations and Their Solutions3. Solution by Iteration4. An Alternative Solution Methodology .

(.'

? .. . E.'

, .. '.

..2.

5. ne Cobweb Model6. Solving Homogeneous Diference Equations7. Finding Pmicular Solutions for Deterministic Processes8. The Method of Undetermined'cocfficients9 Lag Operators

l0. Forward-versus Backward-Looking SolutionsSummary and Conclusions

i 0 6 i 1 li lQuestons an xerc sesEndnotesAppendix l : Imaginary Roots and de Moivre's TheoremAppendix 2: Characteristic Roots in Higher-order Equations

CHAPTER 2: Stationary Time-series Models1. Stochastic Difference Equation Models2. ARMA Models

3. Stationarity4. Stationazity Restrictions for an

ARMAWV Model5. ne Autocorrelation Function6. ne Partial Autocorrelation Function7. Sample Autocorrelations of Stationa:y Series8. Box-lenkins Model Selection9. The Forccast Function

10. A Model of the WPl11. Seasonality

Summary and ConclusionsQuestionsand Exercises

EndnotesAppendix: Expected Values and Variance

CHAPTER 3: Modeling Economic Time Sries:t Trnds nd Volatility .

' 1.

'y 1. Economic Tim Series: The Stylized F@cts @i 2. ARCH Proc ssts

'

@t

. .

3. ARCH and GARCH Estqmatesof lnGation i494 . Estim :1l ing :) GARCH N1odel ( ) f'llle j'V1D1

J A 11 ! x :1!1)p1c 1525

.A GA 1)

-.

l 1 N1ol)tt 1 ( l' I-tisk 1566. Thc ARCH-M Model 158

, uaximumuikelihoouEstimation osoAucu anu ARcu-k. uo,il,. l6c8. Detenministic and Stochastic Trends : .

'

E' ): E ! 1669. Removing the Trend 176

l0. Are There Business Cycles? 18 1l 1. Stochastic Trends and Univariate Decompositions l85

Surllary and Conclusions 195Questionsand Exercises 196

Endnotes 204Appendix: Signl Extraction and Minimum Mcan Square Errors 206.

2112t222l22523323924325126026l265265

REFERENCES

AUTHORINDEX

SUBJECTINDEX

:T-i k..

,

)

X

35535636336537337738l3852933964O04O44054l0412

4l942042l

423

427

429

Chapter 1

DIFFERENCEEQUATIONS y' . . . ..

.... . ..

.. ).y)''.''.

' )..

he theory of difference equations underlies all the time-sefies methods employedin later chapters of this text. lt is fair to say that time-series econometrics is con-cerned with thc estimation of differcnce equatjons containing stochastic compo-nents.The traditional use of tim-series analysis was to forecast thu time path of avmiable.Uncovering the dynamic path of a series improves forecasts since the pre-dictablecomponents of the series can be extrapolated into the futurc. The growing

'

interest in economic dynamics has given a new emphasis to time-scries economst- jlics. Stochastic difference equations arise quire naturally from 'dynamic economic i .i

. .j.ymodels. Appropriately estimated equations can be used for the intepretation of lrlk

.

'

. .!'

.. .1

economicdata and for hypotesis testing.. r.?,'lyj

'I'he aims of this introductory chapter are to: , . t.7)t

.1'( ..g(

. yyk. .

. r.... . ... . tjrjj.: y.

l . Explain how stochastic difference equations can be used for forecasting and to 7Ei) 'q:i

,

. q, yillustrate how such equaiions can arise from familiar economic models. Tlie.

: 7 ,h

. j.' .-.'.

:'

.;(;;,.. .

-

. .

.

).'(j;l;,.j@,k.':.y'

'chapteris not meant to be a treatise on the theory:of differenc quations. Only #r'. (1 rty.

;. k. ! ;;

those techniques that are essential to the appropriate estimation f Iiner tim- '..:. t1,: ltik- 7)

L 'on single-eqation 'models: ''

''hEi' :X)$1tseries models are presented. This chapter focus s ( y. j:.

. .

..

. . y).. . jy ,.

multivariatemodels are considered in Chapters 5 and 6. :,. ; .y. ty tq

. k . . . y yjku)yj' $ '' difference equation. The solution will deter- -. i'z'2. Explain what it means to slve a . ).y j. jy; .., .. .. .

minewhether a variable has a stable or an explosive tifne path. A knwledge of r. :.. ' .

''

. ..

' ''m.

. ) f,..

xf.

the stability conditions is essential to undetstanding the recent innovaiions in.' F 7( '

). . . . . ..

q..J. :..;

. !..

time-selieseconometricsk' The contemporary time-series literature pays. special. . . t(.. (:;

')'

. . . ' . ) :.j..t

. ..

'y

attention to the issue ot- stationary versus nonstationary variablesr The stability.

'

t t:tt'.: .,

jt.jconditionsunderlie the conditions for statioarity. : ' ' ptk ); . ..

.

. ; :

., y , y N. ,.

3. Demonstrate how to fld the solution to a stochastic difference equation. There ' , )'jt.

. . :' - E' '; ''.

.. .

are Several differcnt techniques that can be used: each haj its own relative mer- ''','

. :' '

' its. A nuniber of examplej are presented to hlp yo uriderstand th: different ''

''

: 7 tjt.i. j

methods. Try to' work throuch each example carfully. For extra practice. you .

' '.,

should complete the exercises at the end of the chapter. '-.

(' 7 ''

. t .('

i

Dtfference f't?l/tJ/?'f.)tl'

1. TIME-SERIES MODELS

The task facing thc modern time-serics economtrtrician is to develop reasonablysimple models capable o forecasting, interpreting. nnd testing hypotheses conccrn-ing economic data. The challenge has grown ovcr time'. the original use of time-series analysis was primarily as an aid to forccastillg. As such. a methodology wasdevcloped to decompose a scfies into a trend. seasonal, cyclical, and an irregularcomponent.Uncovcring thc dynamic path of a st'ries improves forecast accuracysince each of the predictable components can 1,e extrapolated into the future.Suppose you observe the 50 data points show 11 il1 Figure 1. l and are interested inforecastingthc subsequent values. ausingthe time-series methods discussed inthe next several chapters. it is possible to decomplpse this series into the trend. sea-

Obsewed data

yrend

..-...- .- seasona l

1rre g u1a r Forecasts

Tme-series Models

sonal,and irregular components shown in the lower part of tbe figure. As you cansee, the trend changes the mean of the seres and the seasonal component imparts aregularcylical pattern with peaks occurring every 12 units ot-time. ln practice, thetrend and seasonal components will not be the simplistic detenninistic functionsshownin .the Ggure. With economic data, it is typical to t'indthat a series containsstochasticelements in the trend, seasonal, and irregular components. For the timebeing. it is wise to sidestep these complications so that the projection of the trendandseasonal components into periods 51 and beyond is straightfolvard.

Notice that the irregular component, whilc not having a well-dened pattem. issomewhat predictablc. lf you examine thc figure closcll'. you will see that thc posi-tivc and negative values occur in runs', the occurrence of a large value in any periodtends to be followed by another lftrge value. Short-run forcasts will make use ofthis positive correlation in the irregular component. Ovcr the entire span, however.the irregular component exhibits a te dency to revert to zero. As shown in thelower part of the figure, the projection ot- the irregular component past period 50rapidlyklecays toward zero.

'rhe

overall forecast, shown in the top part of the f'ig-ure, is the sum of each forecasted component.

The general methodology used to make such forecasts entails i'inding the 'tequa-

7, tion of motion'' driving a stochastic process and nsing that equation to predict sub-. )

,

j . jj- wg use tjjjs2: senuent outcomes. Let y, enote the value of a data point at neriod t.

:'

1'*

.

'''

'''

.

''t 'K ''

.

.

: . notation. the cxnmple in Figure 1.1

asFumed wa observed y! throtlgh yso. For l = 1( ! ; .

i.

y. : to 50. the enuations of motion used to construct components of the y, series are

:'.q'

;

' ''

.

!F Trend: Tt = 1 + 0. 1t!

Seasonal: St = 1.6

sintrn/z)Irregular: J, = 0.7 /,-1 + t

k'?'re Tr = value of the trend component in period t

.,= value of the seasonal component in t

I = the value of the irregular component in tt

6, = a pure random disturbance in f

Thus, the in-egular disturbance in l is 70% of the previous period's irregular distur-bance plus a random disturbnce tefm.

Each of these three equations is a type of diference equation. ln its most gen-erat form, a difference equation expresses the value of a variable as a function of itsown lagged values, time, and other variables. The trend and easonl tenns are bothfunctionsof time and the in-egular tenn is a function cf its own lagged valtle and

the stcchastic variable E,. The reason for introducing this set of equations is to makc

the point that tme-series economerics is ctpnccrzlct with lhe estimator of Jt/-/r-

enceecyltcrfapTs contakning slochastic co??lponcnrj. Thc tim-seris econometrician

mayestimate the propcrties of a single series or a vcctor containin: mahyin'terde-'

.endent series. Both univariate and multivariate torecastingmetbods are prejented. Pin tbe text. Chapter 2 shows how to estimate the irrejular part of a series. The firsthalfof Chapter 3 considers estimating the variance when the dta exhibit je'Iiods o

' 4

I=)',)

lrt l

1 '.

DIfJerence f'l/t:f I'o?T.y

volatility and tranquility. Estimation of the trend is considered in thc last half ofChapter 3 and in Chapter 4. Chaptcr 4 pays particular attcntion to the issue ofwhether the trend is deterministic or stochastic. Chapter 5 discusses the propertiesof a vector of stochastic difference equations nnd Chapter 6 is conccrned with theestimatiopof trends in a multivariate model.

Although forecasting was the mainstay of time-series analysis. the growing im-portance of economic dynamics has gencrated ncw uses for time-series analysis.Many economic theories have natural reprcselllations as stochastic diffcrcnce equa-tions. Moreover, many of these models have tcstablc implications concerning thetime path of a key economic valiable. Considcr the following three examples.

l . The Random Walk Hypothesis: In its simp+st form, the random walk model 'suggests that day-to-day changes in the plice of a stock should have a meanvalueof zcro. Aer all, if it is known that a capital gain can bc made by buyinga shnre on day J and sclling it for an cxpccted proflt hhc very next day. efficientspeculationwill drive up the current price. Similarly, no one will want to hold astock if it is expected to depreciate. Formall. tl4e model asserts that the price of

a stock should exolve according to the stochastic difference equation:

)' l=

v'l + f.,+I14'

y:., = 6,+ ,

wlere y, = the price of. a share of stock on day

6,+1= a random disturbance tcrm that llas an expected value of zero

N()w consider tLe more general stochastic diflrel:ce equation:

AA',+l= W)+ tlt11'/ + Er+ 1

The random wnlk llypothesis requires thc tcstable restriction cto = aj = 0.Rcjccting this rcstriction is cquivalent to rcjccting thc thcory. Givcn thc infor-nlation availablc in period , the theory also rcquires that the mean of 6.,+1 beequal to zero', evidence that 6.,.1 is predictable inval kdates the random'walk hy-pothesis.Again, the appropriate estimnlion o a singlc-equation model is consid-ered in Chapters 2 through 4.

2. Reduced Forms and Structural Equations: Oftcn. it is useful to collapse asystem of difference equations into separate single-equation models. To' illus-trate the key issues involved. consider a stochastic version of Samuelson's(l 939) classic model:

> T''!

';

)1

l.3

) T-11r*.kjl.;.

: !**1 !1

.!

y:= cr + it

c, = ayf- l + ecr O < (y, < 1il= fstcf- cr- I ) + E,., f.l> 0

wherey,, c,, and I', denote real GNP, consumption, and investment in time period

t, respetively. ln this Keynesian model, y,, c,. and i, are endogenous valiables.

The previous peliod's GNP and consumption. yt-l and c,-,, are called predeter-minedor lagged endogehous variables. The terms E, and 6,., are zero mean ran-dom disturbances for consumption and investment and the coefticients c, and ;$are parameters to be estimated.

The first equaton equates aggregate output (GNP) with the sum of consump-tion and investment spending. The sccond cquation asserts that conspmptiol)

spendingis proportional to the previous period's income plus a random distr-bance term. The third tquatioil illustrates the accclcrator principle. Investmentspendingis proportional to thi chnge in consumption; (he idea is tllat growth inconsumptionnecessitates new investment spenzing-E ne error tenns Ec, and Eg,

represent the poflions of consumption and investmnt'not

explained by the be-havioralequations of the model.

Equation (1.3)is a structural equation since ii expresses tc endogcnousl

variable i: as being dcpendent ori t current realiz tion of another endogenousvariableG. A reduced-fonn equation is one expressing the value of a variable

in tenns of its own lggs. lags of other endogtnous variables, current and past1 s of exogenous variables and disturbace tens. As formulated, the con-va ue ,

; sumption function is already in reduced fonn; cufrent consumption depends( j b tennonly on lagged income and th current value of the stochastic d stur ance

Ecr Investment is not in reduced form since lt depends on current period con-sumption.

To derive a reduced-fonn equation for investment, substitute (1.2)into the inr

vestmentequation to obtain

it= f'5(a.y,-,+ ec, - c?-l) + ei:

= txl3yl.-, - pcr-l+ f'JEc? + E,.,

Notice that the reduced-fonn equation for investment is not unique. You canlag'(1.2)one period to obtain c,-) = co-c + Ec,-l. Using this expression, we canalso write the reduced-fonn investment equation as

it= t:/,f5.F1-:- 2(t7..J,/-2 + Ecr-l) + Ec, + Ef?

= (7.fJ(.),,-!- y,-c) + 0(Ec, - ecr-l) + it

Similarly, a reduced-form equation for GNP can be obtainrd by substituting

( 1.2)

and (1.4)

into (1 . 1):

y,= ayr-, + Ec, + l3t-yl-.,- yr-z) + p(Ecr - Ec,-,) + Ef,

= c,41 + jJ)y,..j= ajx-.a + (1 + j)Ew + ir- j'Je.w..l ( l

.!)

Equation (1.5) is a univariate reduced-orm tqation; y, is expressed solelyas a function of its own lags anl disturbance terms. A univariate model is partic-ularly useful for forecastinj since it enasles you to jredict'a series based iolely

Tme-seres Models

lr-1;

D ./J relce E lztl/lo?l' ' ' '

l e q

on its own currcnt and past realizations. 11is possible to estmate (1.5) using theunivariate time-series techniques explained il1Chapters 2 through 4. Once youobtain estimates ot- (x and I),it is straightfonvard to use the observed values of ylthrough y, to predlct all future values in the series (i.., y,+!, y/.c, ... ).

Chapter 5 considers the estimation of multivariate models when al1 variablesCtI'c trcatctl as joiIltly cntlogenous. The chapl cr also discusses the restrictionsnccded to recovel' ( i .c.. idcllti fy) thtt strtlcttl l':t1 model from the estimated rc-duccd-forfn model.

Error Correction: Forward and Spot Pricts. Certain commodities antl finan-cial instruments can be bought nd sold on thc spot market for immediate deliv-el'yor for delive:y at some specified future date. For example. suppose that the'pfice of a particular foreign currency on the spot market is J, dollars and theprice of the currency for delivery one-pefiod into the future is S dollars. Now,consider :t speculator who purchased fonvard currcncy nt !he price dollnrs perunit. At tbe beginning of period t + 1, hc speculator receives the currency andpays.j dollars per unt received. Since spot forcign exchange can be sold at stwj,the spcculator can earn a prot'it (orloss) of .,.j

-f

per unt transactek..

The unbinsed forward rate (UFR) hypothesis asserts that expected profitsfrom such spcculative behavior should be zero. Formally. the hypothesis positsthe following relationship between fonvard and spot exchange rates:

u ! =J?+ E,.,

where E,.) has a mean value of zero from the Tlerspective of time period t.ln (1

.6).

the ronvardratc in t is an unbiascd estimate of the spot rate in t + 1.Thus. suppose you collccted data on the two rates and estimated the regression:

sl..t= Czo + Czl./i + E?+,

If you werc able to concludc thal co = 0s a! = J and lhe regrcssion residuals

6.,+1have a mean valuc of zcro from the pcrspcctive of time period t. the UFRhypothcsis could be maintained.

The spot and forward markets are said to bc il1A'long-rtln cquflibrium'' when

q,+, = 0. Nvhencvcr &,+) turns ont to dif-ferfrom. some sort of adjustment mustoccur to restorc the equiliblium in thc stlbsequent period. Consider the adjust-

m (')11t g)I-OCCSr;:

Dtjerence f'llalEfp/l.$' fznd Their Solutions

tion model since the movement of the variables in any pcriod is related to thcpreviousperiod's gap from long-run equilibrium. If the spot rate .,.I turns out toequal the forward ratef. ( l

.7)

and (1.8)

state that the spot and folavard rates are' h d lf there is a positive gap between the spot andexpected to remain unc ange .

fonkard rates so that st-vt-./)

> 0, ( l.7)

and (1.8)

lead to the prediction that the

spot rate wil! fatl and the forward ratc will rise.

DIFFERENCE EQUATIONS AND THEIR SOLUTIONS

Although many of the idcas in the previous section wcre probably familiar to you.it is necessary to fonnalie some of the concepts used. lh this section. we will ex-amine the type of difference equation used in econometric analysis and make ex-plicitwhat it means to e'solve'' such equations. To begin our examination of diffes

ence quations. consider the function y =X1).If we evaluate the function when theindependentvariable t takes on the specific value l*, we get a specc value for the

dependentvaliable called y,.. Formally, y,. = jt*l. lf we use this same notation,

y,.+, represents the value of y when t takes on the specitsc value t* + h. The firstdifferenceof y is defined to be the value of the function when evaluated at t =

1*+ h mnus the value of the funtion evaluated at f*: '

tsyts..h EX XJ* + /l) -XJ*)O 9t.+h - yt.

Differential calculus allows the change in the independent variable (i.e., the termh) to approach zero. Since most economic data are collected ver disrete periods. 'however,it is more useful to allow the length of the tme period to be greater than

zero. Usng difference equations. we normalize units so that h represents a unit

change in' t (i.e., = 1) and considcr the sequence of equally spaced vzlues or the

independentvariable. Without any loss of generality, we can always drop the asler-iskon J*. We can then form the first differences:

32J c:z y() - / ..- J) & y .-. yj-yy I

A)',+l=.It + '+, 'jy' :

j uu .Apg+a=ht+ 2) -X! + ) j't-z Fl+l

%t+z= st.. - a(.,+.$

-./;)

+ E,?+a t: > 0)'t+l

=./;+ 7(5.,+.1-.J,)+ 6.?i., ;$> 0

whcre E,.a and 6y,.1 both have a mean valuc ('f zel k) from the perspective of timeperiod t + 1 and 1. respectively.

Equations (1.7)and (1.8) illustrale the type of silnultaneous adjustment mech-anlsm considcred in Chapter 6. This dynamic model is called an error-correc- .

Often, it will be convenient to exprcss the entire sequence of values (... )'t.n . y?-,.

y,. y?.! ? yr.ez.... ) as fy,). We can thcn refer to any one particulnr value in the se-

quence as y,. Unless specified, the index t runs from -e,o to +e.o. In time-series .

econometric models. we will use t to rcpresertttme'' and h the length of a time pr- ''

. .'''

. .

riod. Thus, y, and y,.1 might rcpresent the realizations of the (y;j sequcnce. n the .

first and second quarters of 1995. rcspcctively.

ln thc same way, we can form the second diffrenc as the chang in the firstdi ffkrcnce. Considi r '

Digerettce kuclrln.

A2y, H A()',) = A(.,y,- yt- I) = (A',- y,- I) - (-5.,-)- .v,-2) = yt - 2y,-1+ y,-.cA2v,+

Ir'B (AA',..1) = (.,?+r

- y,) = (.vtvt-

.y,)

- ('.vt-.v,-

I) = A'/+1- 2y, + yt-.t

Thc ?2th diffrrencc (c) is dfzfincdanalogotlsly. At lllis point, we risk taking thelheory of differcnce equatons too far. As you wi1l sce. (he need to use second dif-fcrences.rarelyarises in timc-series analysis. lt is safe to say that third- and higher-order differences are. never used in applied work.

Since this text cons iders lincar time-series mc (llotlrk, it is possible to examineonly the special case of an rlth-order linear differencc etluation with constant coeffi-cients, Thc form rtlrthis special type of di f'fcrcncc cqualion is given by

The order of the difference equation is given by the value of n. The equation is lin-ear because a1l values of the dependent variabkc are raised to the first power.Economic theory may dictate instances in which the various ai are functions e 'variables within the economy. However. as long a's thcy do not depcnd on any ofthe values of y, or -vs

we can regard tlem as paramcters. The tem xt is called theforcing process. The form of the forcing process cktn be very general',x, can be anyfunctionor time, cufrent and lagged values of othcs' variables, and/or stochastic dis-turbances.By appropriate cloice of the forcing prbcess. we can obtain a wide vari-

ety of important macroeconomic models. Rcexamine Equation (1.5),

the reducedfonmequation for GNP. This equation is a second-tlrder difference equation since y,depends on yr-c. The forcing process is the expression (1 + j)Ec, + Ef, - pEc?-I. YOu

will note that (1,5)

has no intercept term corresponding to the expression av in( ) . 10).

An important special case for the (.'r,)scquence is

...

..'

..

t'

' ' '.'

whcre thc k'Jfare constants (someqf which can cqual zcl'kll and the individual elc-

ments of tbe sequence (e,) are not functions of the yt. At ths point, it is useful toallow the (E,Jsequencc to be nothing more than a sequcnce of unspecified exoge-nous variables. For example, let (6.Jbe a random cn'or term and set fsa= l and f5l=f'Ja= ... = 0, then Equation ( i

.1

0) bcconlcs the auttregression equation:

Let n = l , ao = 0, and ak = 1 tcl obtain tllc random wktlk Iltldel. Notice that Equation(1. 10) can be . vritten in terms of the difference operato) (A). Subtracting y,-l from( 1. 1O). Nve obtt Lin

.: :'.'' E.. .'.'

.:.. .

t'

.'

k diisng yL:;.F(aj - l)?w.eg44

xttitk, ELy = t'a + YA'r-1+ aiyt-i + A'tf ..'

i= 2

Clearly, Equation (1.1l ) is just a moditied version of (1. l0).A solution to a difference equation expresses the value of y, as a function of the

) lues of the (y,) se-elementsof the (m) sequence and t (andpossibly some g vcn va

quence called initial conditions). Examining (1.1

1) makes it clear that there is a

stronganalogy to integral calculus when the problem is to find a primitivc ftlnctionfrom a given derivative. We seek to nd the ptimitive function

./(f)

given an equa-tion expressed in the fonn of (l

.10)

or (1.11). Notice that a solution is a functionrather than a number. The key property of a solution is tat it satisfies the differ-

ence equation for all pennissible values of l and (.x,J. Thus, the substitution of a so-lution into the difference equation must result in an identity, For example, considerthe simple difference equation Ay,'= 2.(ory, = y,-1 + 2). You can easily' kerify that asolutionto this difference equation is yt = 2/ + c, where 'c is any arbitrary constant.By definition, if 2t + c is a solution, it must hold for a11permissible values of t.Thus for peliod t - 1,yr-, = 2(I - 1) + c. Now substitute the solution into the differ-

encc equation to fonn

2J + c M 2(J - 1) + c + 2

It is straightforward to carry out the algebra and verify tat ( l.12)

is an identity.This simple example also illustrates that the solution to a difference equation need

not be unique', there is a solution for any arbitrary value of c.Another useful example is provitled by the irregul:tr tenm shown in Figure 1

.1

;

11that the equation for this expression is It = 0.7/,-, + e,.rou

can vertfy that therecasolutionto this first-ordcr equation is

''N iIt = (0.7) El-,f

/=0

: Since' ( l.13)

holds for a1l time periods, the value ot- the ifregular cmponent iny ,

.

. ; .

' ( - l is tivenby :': ; E! . ,(J. j .'

, .:.j'. .i)

-'

7-

i .2J = (0.7) e I-f

:( ( l . l4)1- l 1- ; ..

i=0 ''

.

Dilje re n ce I:-f.pIz (1 l io n .

Thc two sidcs of (1.1

5) are identical-, this proves that (1 . 13) is a solution to thefirst-orcter stochastic difference equation lt = 0.7/,-1 + E,. Bc aware of the distinctionbetwcen reduced-form equations and solutions. Since /, = 0.7J,-) + E, holds for a1lvalucs of J, it follows that lt-, = 0.7-c + E,-1 . Combining thcse two equations yields

l = 0.7(0.71 + E 1) + E, ' !,. t $

. ..''.. t t -- ;! f-- .

= 0.49/,-a + 0.7E,-) + e, : 'q :, E.

E:' . .. .. .. ... .. . .

' . '. . ' ' . t..)

Equation (1.16)

is a reduced-form cquation sillce it expresses h in terms of itsown lags nnd distnrbance tenns. Howcver. (1. 1(?) does not qualify as a solutionsincc it contains the ''unknown'' valuc of It-z. To qualify as a solution. (1.16)mustexprcssf, in tcnms of the elcments of x,. J, and any given initial conditions.

3. SOLUTION BY ITERATION

The solution given by ( l.13)

was simply postulated. The remaining portions of thischapterdevelop the methods you can use to obtain soch solutions. Each method hasits own merits; kmowing the most apprriat: to use in a particular circumstance isa skill tat comes only with practice. This section develops the method of iteration.Although iteration is the most cumbersome and tinhe-intensive method, most peoplefind it to be NeT'y intuitive. '

lf thc value of y in somc specific period is known. a direct method of solution isto terate fomard from that peliod to obtain the subsequent time path of thc entire y

'

' !sequence.Refr to this known value of y as the inktial condition or value of y in .

time period 0 (denotedby y. lt is easiest to illustrate the jterative technique usingthe first-order difference equation:

y: = ao + a lF,-1 + tr

)'1= flo + (1 j)'f' + E 1

In the samc way, y2 must be

h'z= az + t;l)'I + E2

= ao + f/ltt')l, + tzls + E!) + Ea

= ao + tatltz, + (7,)2y()+ t?16 t + Ez

.yy= ao + a Iyz + 6a2 3 2

''

ri !

=a 1 + t7l + (5$) 1+ (t7y)yz + clqt + t7(Ez + *' E E '' '

o

.M8.u.'en :jily verify that for a1l t > 0. repeated iteration yields

Equation (1.18)is a solution to (l.17)

since it expfesses yt as a function of J, theforcingprocess xt = 1Rt7l)%,-f,and the known value of yo. As an exercise, it is uszful

to show that itcration from y, back to yo yields exactly the formla given by (1.18).Since y, = av + Jl.yr-, + Ep it follows that

h't = t70 + t21(/0 + t71X-2+ E?-l) + t

= ao 1 + tzjl + a, E,-j + 6, + Jzjttzo + atyt-, + E,-z)

Continuing te iteration back to peliod 0 yields Equation (1.18).

Iteration Without an lnitial Condition

Suppose you were not provided wit.h the initial condition for yy The solution given

by (1.18)would not be appropriate since the value of ytl is an unknown. You could

not select this initjal value of y nnd iteratc fonvard. nor could you iterate backwrd

fromy, and simply choose to stop at t = tw Thtls. suppose we continucd to iteratebackwardby substittlting tzo + cly-, + Ef) fOr yo in (1.18):

( l.20).

1l

You should take a few minutes to cllllvincc yourself that (1.2

l ) is a solution tothc original diffrcnce equation ( 1. l7)., substitution ofb(1

.2l

) into (1.17) yields anidentity. Howcver. (l

.2

I) is not a ulliqttc solurion. For any arbitrary value ol-A, asolutionto (1. 17) is givcn by

11

To verify that/br any tzrlrtzr' ptl/lf e ofA, (1.22)

is a solution, substitute (1.22)

into(1. l 7) to obtain

i

1

k.

;(.

Reconciling the Two lleralive Methods i:

Given the iterative solution (1.22). suppose that you are now given an initial condi-tion concerning the value of y in the arbitra:'y period fo. It is straightforward to ,

show that we can ilmpose the initial condition on (1.22)to yield the same solution1 18) Since (1.22) must be valid for a11periods (includingfa), then when t = 0,as ( . .

it must be true that'

(..1:1,7:5.)4..

Since A'()t .$ given. we can view ( l.23)

as the value of zt that renders (1.22)

a solu-tion to (1.

17) given the initial conditioll. Hcnce. the presence ot-the initial condition

eliminatesthe ttarbitrariness'' of A. Substituting this value of A into ( l.22)

yields

!

You should take a moment to velify that (1.25)

is identical to (1. l8)z

Nonconvergent Sequences

Given that I ,, l < 1, (1.21)is thc Iimiting value of (1.20)as ?,, grows incnitelylarge. What happens to the solution in other circumstances? If 1t:, l > l . it is notpossible to move from ( l

.20)

to (1.21) since the expression it'Il l'*mgroFs inti-

nitely large'as

l + m approaches infinity-' However, if there is an initial conditionw

there s no need to obtain the infinite summation. Simply select the nitial condition

yj and iterate fonvard; the result will be (l . 18):

r' - l ' t - li f i

y = ao tzj + tzjytl + cj et-it

i zr 0 i us 0 '

yt = h +.%-

I + 6,

j

!i

Djrence t/fft'zl///??. Stllt4tionby /l' rtltiet H

that the solution contains summation of a11disturbances from 61 through E,. Thus.when at = l . each disturbance has a permancnt nondccaying effcct on thc value of

vt.You shob'ld compare this result to the soltltion found in (1.21). For the case in-whichla I < 1. lt:zt 1'is a decreasing fbnction of- : so that (he effects of past distur-bances become successively smaller over time.

The importance of the magnitude of tz! is illustrated in Figure 1.2.

Twenty-tiverandom numbers with a theoretical mean equal to zero were computer-generatedand denoted by q, through e.25.Then the value of ya was set equal to unity and the next25 values of the (y?Jsequence were constDctcd using the formula y, = 0.9y,-1 + E,.

The result is shown by the thin line in part (a)of Figure l.2.

lf you substitute tlo = 0and t7l = 0.9 into (1. 18), you will see that the time path of (y,)consists of two pans.The first part, 0.9', is shown by the slowly decaying thick line in the (a)panel of thefigure. This term dominates the solution for relatively small values of t. The influ-ence of the random part is shown by thc diffrence between thc thin and thick lines;you can sce lhat the first scvcral kalucs of (E,) are negative. As t increases, thc in-tluenceof the rantlom component becomes more pronounced.

Using the prcviously drawn random numbers, we again set yn equal to unity and

a second sequence was constructd using the fbnnul yt = 0.5y,-I + 6,. This second

sequenceis shown by the thin line in part (b) of Figure 1.2.

The influence of the ex-pression0.5' is shown by the rapidly decaying thick line. Again. as.l increases. therandomportion of the solution becomes more dominant in the time path of (y,).

ducing the magntude'

When we compare the first two panels, it is clear t at re' of (trll ( increases the rate of convergence. Moreover. the discrepancies between thei i ulatekl values of y, and the thick line are less pronounced in the sec6nd part. As! s m' qj .

you can se in ( l . l 8), each value of E,-/ enters the solution for yt with a coemcienth .

.

'1 of (aj)'. The smaller value of t7) means that the past realizations of E?-,. have a. smaller influence of the current value of y,.it

'..q Simulating a third squence with :Jl =-0.5

yields the thn line shown in part (c).:; The oscillations arc dae to the negativc value of tzj. The expression (-0.5)0,sbown;: by the thick line, is positive when t is even and negative when t is odd. Since itzj lki < 1 the oscillations arc dampened.:.i.

#'

.i The next three parts of Figure 1.2

all show nonconvergent sequences. Ech usesk .. the initial condition y() = l and the same 25 values of (4,) used in the other simula-tions.The thin line in part (d) shows the time path of y, = y,-) + 6.,. Since each value

o 6/ has an expected value of zero, paf't (d) illustrates a random walk proccss. Her,yr = 6, so thnt the change in )', is random. The noncopvergnce is shown by the

tendencyof (y,) to meander. In par't (c). the thick line representing the explosivecxpfession(1

.2)/

dolninates the random portion of the (y,) seqtlence. Also notice

that the discrepancy between the simulated (y,Jsetiuence and the thick line widens

. as t increases. The reason is tbat past values of E,-,. enyer the solution for yt wit the

. coefikient (1.2). As i increases, the importance of ihese jrevious discr pancies be-'

7 comes increasingly significant. Similarly, setting tzj =-1 .2

results i' the explodingillations shown in the lower-right parl of Figum 1

.2.'the

value (-1.l)t

is posi-osctivc for even values of t and negative for otld values of 1.

20 Dtfference krftzl/fpzTx

5. THE COBWEB MODEL

.'

( ' '!.':. . .: .

''

' ' ' ' ''''

' '

An interesting way to illustrate the methodology outlincd in the previous section isto consider a stochaslic version of the traditional cobweb model. Since the modelwas originally dcveloped to explain the volatility in agricultural priccs, let the mar-ket for a product say. wheat be represented by

. ' ). .r . . 1.' ' . ..''

.( j . g!5)

( j.g.r

6)

. ( j.l

)' .. ' :.. .

'

.. . ... . ') ...

, .

El: . .y:. .

J d d for wheat in pefiod I ''.' ' ' ''

t= Cman 7

.'

. . . .:) .':. (.. T ' .; .z'

'' 'r. ' .'

s: = supply of whcat in J. . , . .. ;..) .. '.. . .

.;.)j.' ... .' E.; .L.?'. . ..' J

.1 .1. : ' ' '. . .

p, = markct price of wheat in t. . ' . '

!'

(.

7*)q'

'

;''

.E.'' .

1*'

' E

''

.'.'

'

' ' E'

''

'

* = rice that farmers expect to prcvail :lt r'

' '! 2p' pE = a zcro mean stochastic supply shock

l

:/. ac (1 -- );), )( 7> ()

s: = b + pt + e, ;$> 0

= J' l t

r-nh'

p .f lt

and parametcrs t2, b, g and jsare a11positive sucll tllat (1 > b.4Tl'le nature of the model is such that consumers buy as much wheat as desired at

the market clearing plice p,. At planting time, farmers do not know the price pre-vailing at harvest time; they base their supply decision on the expected price pt).The actual quantity produced depends on the planned quantity b + pt plus a ran-dorn supply shock e,. Once the product is harvested, market equilibrium requires

that the quantity supplied equals thc quantigy demanded. Unlike the actual market

for whcat, the model ignores thc possibility of storage. The essence of the cobweb

model is that farmers form their expectations in a naive fashion', 1et farmcrs use last

year's price as the expccted market price:

Point E in Figure 1.3

rcplresents the long-run equilibrium price and quantity com-bination. Not that (he cquilibsum concept in this stochastic model differs fromthat of the traditional cobweb model. lf the system is stable, successive prices willJc?TJ to convcrge to point E. However, the nature of tht stochastic equilibritlm isstlch lhal hc ever-present supply shocks prevent lllc system from rmaining at E.

'

Neverthelcss, it ksuseful to solve for the long-run pricc. lf w'e set a11values of thc'

! r'-' (Er l Sequence equal to zero. set p, = p;-, = ... = p, and cquate supply and demand.

t

.the long-run equilibfium Iricc is given by /? = (47- Illlnf + ;J). Similarly. the equilib-

; t riurn quantity (-) is givcn by s = ltzj + j'bql-f + j).To tlndersland thc dynamics of the system, supptlse that farmers in l plan to pro-

duce the euilibrium quantity J. However. let therc be a ncgative supply shock suchthat thtr Ctctual quantity produced turns out to be .s:. As shown by point l in Figure1

.3.

consumcrs arc willing to pay pt for the quantity .,: hencc. market cquilbrium inJ occurs at point l . Updating one period allows us to scc the main result of the cob-web modcl. For simplicity. assume that all subscquent values of the supply shock

The CobbvebModel

arc zero (i.e-,6,+1 = E,+2 = ... = 0). At thc btlgining of period t + l . farmers expectthe price at harvest time to be that oi- the previous period; thus, 'p/..j = p,.Accordingly,' they produce and market quantity .,+: (seepoint 2 in the tigurel; con-sumers,howcver, are willing to buy quantity ',.j only if the price falls to tllat indi-cated by ,,+1 (see point 3 in the Iigre). The next period begins with farmers ex-pectingto be at point 4. The process continually repeats itself until the equilibriulnpointE is attained.

As drawn, Figure l.3

styggcsts that the market $$.iI1 always converge to (he long-run equilibrium point. This result does not hold for a11demankl and supply curxes.To formally derive the stability condition, combine (1

.35)

through (l.38)

to obtain

pt= (-fV')#r-l + (J - bsl-f - E,/-

Clearly, (1.39)is a stochastic tirst-orderlinear difference equation with constantffi ients. To obtain the g neral solution, proceed using the four steps listcd atcoe c

the end of the last section:.

1. Fonn the homogeneous equatiop: p. = .4-fVy),,-1.In the next section, you willlearnhow to fnd the solutionts) to a homogeneous equatio'n. For now, it is suffi-cient to velify that the homogeneous solution is

22 Dillrqnq nuqtions

If qlyk 1, the insnite summation in (1.40)

is not convergent. As discussed inthe last section. it is necessary to impose an initial condition on (l

.40)

if ly l .

3. The general solution is the sum of thc htlmogeneous and particular solutions; ifwe combinc these two solutions, thc gcncral solution is

'.

..)

We can intcpret ( !.42)

in tenns of Figure 1.3.

ln order to focus on the stablityof the system. temporarily nssume that a1l values of the (e;1 seqnece are zcro.Subsequently. we will return to a consderation of the effects of supply shocks. Ifthe system begins in long nln equilibrium. the initia! condition is such that po =a - ,)/(y+ ;$).ln this case. inspection of Equation (l

.42)

indicates that pt = a - btI(y + jJ). 'rhus,

if we begin the process at point E. the system remains in long-runequilibrium.lnstead, supposc that the process begins' at a price below long-runequilibrium:po < (5 - )/(y+ ). Equation (1.42) tells tls that pt is

J'l = (z - btl't + ;5)+ U?o-

a - ?))/(,/+ f5)J(-$/$'Since po< a - b4l1 + ;$)and

-l''f

< 0, it follows that pt will be above the long- '

run equilibrium price (t2- blly.. 0).In period 2,

pz= a - d7)/(.7+;5)+ Epo- (t7- bsl-f + j!)1(-fV-/)2Although po < a - yyy + jg,

-gjpz

js positve; hence, pg js below the long-runequilibrium. For the subsequent periods, note that (-;/y)r wilj he posstjve for evenvalues of t and negative for odd values of t. Just as we found graphically, the suc-cessive values of the (p ) sequence wilj oscillate above and below the lopg-ant

yequilibrumprice. sjnce(j/ylzgoes to zero if 1.$< y and expjodes if ; s y the mag-nitudeof ly determines whether the price actually converges to the long-run equf-librium.If iy < 1, the oscgllations wfll dimfnlsh fn magnitude, and if )ly > 1, theoscillationswill be explosive..n

e economic interpretation of this stability condition is straighlfonvard. Theslopeof the supply curve gi.e.,dptfdylj js lyj and the absolute value slope of thedemandcurve (i.e.,-ap,

yst(y,ll js lyy. Ij- ())e suppjy cnwe s steeper oan te de-,mandcurve 1/fJ> 1/y or gyy< 1 so tlaj oe'system Js stable.'rhts

is precisely the,ocaseillustfated in Figure 1.3

As an exercise you shculd draw a diagram with thedemandcurve steeper than the supply cuae and show tha! the prjc: oscfllates anddiverjes from the Iong-run equilibrium,Now consider theeffects of the supply shockj. 'I''j)econtemporaneous effect of asupplyshock on the pce of wheat fs the par'al dvrivative of p wjtjl resject to 6 ;from(1

.42).

we obtain t ,

.. .'

'(')#?/()E, = - 1l-f

Equation ( 1.44) is called the impact multiplier since it shows the impact effectof a change in zt on the price in f. In terms of Figure 1.3,

a negalive value of e, im-

4. ln (1.41),A is an arbitrary constant that can be eliminated if we know tbe plicein some initial period. For convenience, 1et this initial period have a time sub-sclipt of zero. Since the solution must hold for every period. ncluding perl'od

'

zero, it must be tle case that

since (-fLq/)0= 1, the value of z't is given by

26 DtLgrena uzfln.s

Sincc g., and c.c each solvc (1.45),

both tcrms in brackets mustequal zero. Assuch. the complctc homogeneous solution in thc sccond-order cas is

y =,4l(al)' + z4ctctzl'

l

Without knowing the specific values of 4), and tza. we cannot t'indthe two charac-teristic roots al and cez.Nevertheless, it is possible to characterize the nature of thesolution', there are threc possible cases tbat are dcpcndent on the value of thk; dis-criminantd.

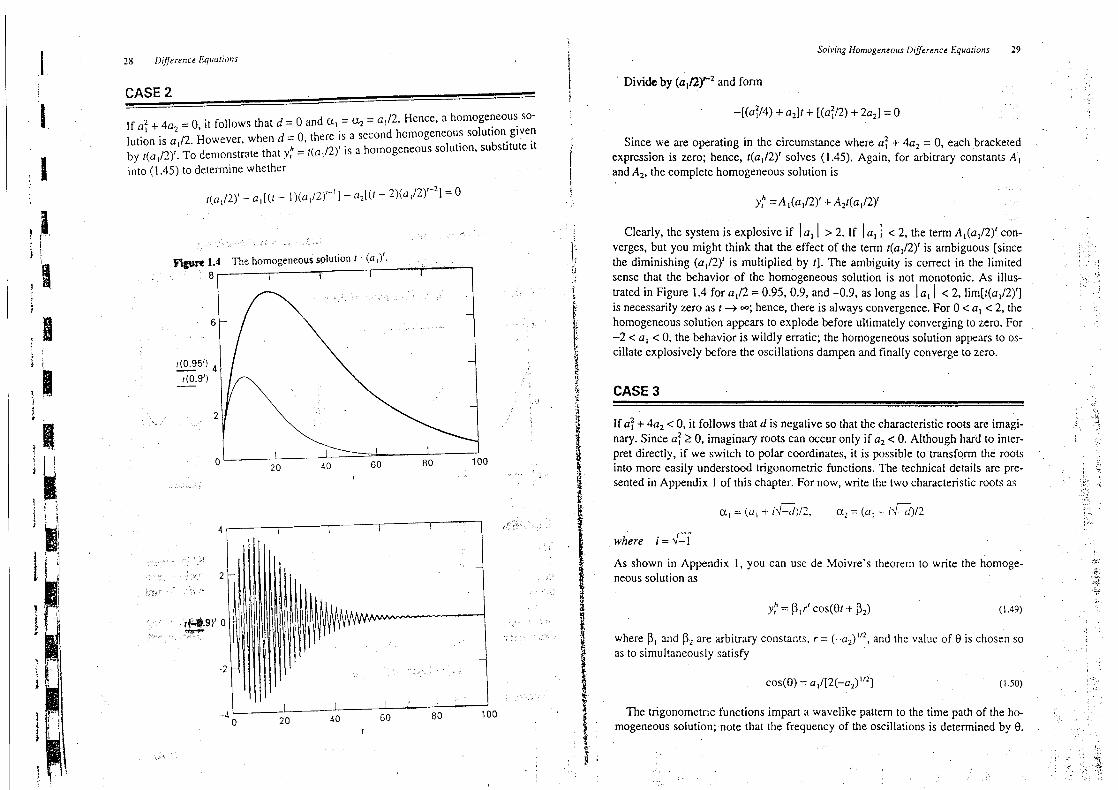

!k'

CASE 1(

.) TJ-JLk. .( E (

' 2

If tj + 4z2 > 0. d is a real number and there will be two distinct real characteristgcrootstHence, there are two separate solutions to the homogeneous equation denotedby (a1)'and (c.,:1.We already know that any linear combination (lf the two is also asolution.Hence,

c., = ().5

. (a , +n-'d

)-

=0.? e,a= 0.5 . (a, - AJ-)=

-p.5

'l'he homogeneos solution is j' 0.7' + z

' (-0.5)'.The graph shows the.

time path of this solution for the casc in which the arbitrary constantyequalunity and t nans from 1 to 20.

CA';t 2: yj,) = 0.7y(, - )) + 0.35y(, - a). Hence, tzj = 0.7, al = t?.3.For'm the homogeneous equation'. y(,) - 0.7./,(,- 1)

- 0.35y(,- z? v 0.A check of the discririnant reveals J = (t2!)2+ 4 . az so that d = 1.89.

' g ' .. ..'.( '

., .Given that d > 0, the roots will be real and distinct..'ll'.'i : i

...' . Fonn the characteristic equation'. u' - 0.7 . a-l - 0.35 - a'-2 = 0

' ' Computethe two characteristic roots'.

c., = 0.5 .

a l + f-d),

= l.037 =(). 5 - (a ,

- T-d)=

-0.337

The homogeneous solution is A)- 1.037/ + Az . (-0.337),. The graphshowsthe time path of tlis solution for the case in which tbe 'arbitrary con-smntsequal unity and t nlns from 1 to 20.

Case 11

0.5.

5

0 10 20

Case 22.5

1.5

0 10 20

In he second 'exmple, y, = 0.7y,-, + 0.35y,-2.The worksheet indicats how to '.

E

. .obtainthe solution for the tp'o characteristic roots. Givn that one characteristicr .root is (1.037)1.the (y,) sequence explodcs. 'I'he intluence of the negative root. ,

; jj skrjtya' (a =

-0.337)

is responsibl for the nonmonotonicity of the t me pat .(-0.337)'quickly apprmches zero. the dominant root is tlie explosive value 1.037.

. )-' j

1

I

E tIj-M(

' yh = zt (aI)' + gztc.al'l

lt should be clear that if the absolute value of either c.! or c,zexceeds unity. thehomogeneoussolution will explode. Worksheet l

.1

examines two second-orderequationsshowng real and distinct characteristic roots. ln the first example. y, =

0.2y,-!+ 0.35y,-c, the characteristic rxt.s are shown to be aj = 0.7 and cta = -Q..Hence, the full homogeneous solution is yth= z4l (0.7)r+ z't:t (-0.5)r.Since both roots

are less than unity in absolute value, the homogeneous solution is convergent. As

you can see in the graph on the bottom left-hand sde of Worksheet 1.1, conver-

genceis not monotonic because of the influence of the expression (-0.57.

WORKSHEET 1.1 Homogeneous Solutions: Second-order Equllons

CASE -i

: ' '(,) = 0.2y(, - j ) + 0.35y(?- c). l-lcncc, rJ1 = ().2. az = 0.35. .

Fof'm the homogeneous equation'. )'j.) - 0.2y(,- 1)- 0.35y(,- )

= 0.

A check of the discriminnnt reveals d = (/1)2+ 4 .

az, so that d = 1.44.

Given that d > 0, the roots will bc real and distinct.

Let tbc trial solution have the form y(,) = a?. Substitute into the homoge-nous equation a' .=

0.2 . (f-' - 0.35 - a'-2 = 0

Divide by ct'-2 in ordcr to Obtnin the chnractelistic equation:ctl- 0.2a - 0.35 = 0 ;; ., , ,' .E. ) ,t .'

Compute the two characteristic roots:

!

f

I

Dtjlrence Equations

CASE 2.

; r LU '7f LQ-JJL---.--V q7 T 2

lf (zl + zlwz = 0, it follows that d = 0 and aj = h = akll. Hence, a homogeneous so-

lution is akrl. However.when d = 0. there is a second homogencous solution given

ph l

'

by latrl) . To demonstrate that y, = tajllq is a homogeneous solution. substitute it

into(1.45)

to determine whether

Solving Homoseneous Dllrrrlce Equa:ions 29

Divide by apjbn and fonn

-((422j/4)+ (7l + ((J21/2) + 2tzz) = 0

Since we are operating in the circumstance where tz2, + 4/: = 0, each bracketedexpressionis zcro; hence, taqlllt solves (1.45).Again, for arbitrary constants

,4l

and#z, the complete homogeneous solution is

nh=A!(J,/2)' + hztatllkf ' E.'

. . .'

. ,;

;. .

Clearly, the system is explo'sive if ltz, I> 2. If 1tz, l < 2. the term z4,(J,/2)' con-verges,but you might think that the effect of the tenn tablll' is ambiguous (sincethe diminishing abllj' is multiplied by J). The ambiguity is correct in the limitedsense that the behavior of the homogeneous solution is not nionotonic. As illus-

d in Figure 1.4 for akll = 0.95, 0.9, and-0.9,

as long as Itz: l < 2, limEl(ul/2)')tratei aril t

-+

co; hence there is always cnvergence. For 0 < a < 2 thes necess y zero as , ,

homogeneous solution appears to explode Yfore ultimately converging to zero. For-2 < tzl < 0, the behavior is wildly erratic; the homogeneous solution appears to os-cillateexplosively bcfore the oscillations dampen and nally converge to zero.

CASE 3

If (z2, + 4/: < 0, it follows that d is negative so that the characteristic roots are imagi-nary.Since (22, k 0, imaginary roots can occur only if az < 0. Altiough hafd to inter-pret directly, if we switch to polar coordinates, it is possible to transfrm th rootsinto more easily understood trigonometric functions. ne tecnical details are pre-sentedin Appendix l of this chapter. For now, write the two chafacteristic roots as

(y,I = ((zI + if-jlll, (y,z = (t7) - fV.C/24

:E j(.

. .L.,1.((7...

.'

:

..E.. ;

.,.j 1.E. :;8!*'''''''

lE'jj6.:1'Lq.'i'''.'.' ...

' '(.' .T:'.'7!

qtq3L.'.E:.

'. .

'.. jyWq'''' 14)4ijt (g)) . ..

?)tE kE

.#,

r

-2

-40 20 40 60 80 100

where i =-1

As shown in Appendix l , you can use de Moivre's theortm to Write the homoge-neoussolution as

yh = jlygcosto; + %)t

wherei'Jjand jz are arbitrary constants, r =(-a)lJ2. and the value of () is chosen so

as to simultaneously satisfy

l r2coslo) = (z1/(2(-tu) )

ne Zgonometric functions impart a wavelike pattern to the time path of the ho-

mogeneoussolution; note that the frequcncy of the osillations is determincd by 0.,

'

) '.

. j,

,

' ) .' ; '

34 Dtgrence Equotions

Sincc costgl) = costza + 0. thc stability condition is determined solely by the:J2. lf Iaz I= l . the oscillations are ofbunchanginj amplitude;magnitudcor r = (-t7z)

the homogcneous solution is pefiodic. The oscillations will dampen if az 1< l andexplodeif Iaz I> 1.

EXAMPLE: It is worthwhile to work through an exercise using an equaton withimginary roots. The left-hand side of Worksheet l

.2

examines the behavior of theequation y, = 1.6y,-j - 0.9y?-c.A quick check shows that tbe discriminant d is nega-tive so that (he characteristic roots are imaginary. lf we transfbrm to polar coordi-nates, the value of r is given by (0.9)1r2= 0.949. From ( l

.50).

coslo) = l.6/(2

x0.949) = 0.843. You can tlse a trig table or calculator to show that 0 = 0.567 (i.e.,ifcosto) = 0.843. 0 = 0.567). Thus. the homogeneous solution is

..) yth= ;j(O.949)' cos(0.567l + pzl

''f'hegraph on thc left-hand side of Workshcet 1.2

sets j)l= l and j:t = 0 and plotsthe homogeneous solution for t = 1. ..., 25. Case 2 uses the same value of az (hence,r = 0.949) but sets aL =

-.0.6.

Again, the valne ot-J is negative; however, for this set'

of calculations, costo) =-0.316

so that 8 is 1.25. Comparing the two graphsk youcnn sce tat increasing the value of 0 acts to increase the frequency of the oscilla-tions.

Given costo), use a tlig table to find 6

t; - 3.567 ij = l.25

WORKSHEET1.2 IMAGINARY ROOTS

CASE 1

y,- l

.6.3,,-,

+ 0.9y,-a

CASE 2

y, + 0.6y,-I + 0.9yt-c

(d) Form the homogeneous solution:y) = glP costof + j3z)y? = )1(0.949/cos(0.567? + ;$a) y) = j,(0.949)'cost l

.25/

+ )a)For jsy= 1 amdX = 0, the time paths of the homogeneous solution arr

2

g'

$'

E.

;'''.

.'.'

.'

:..

;'

tk7!1--...

1 25

Stabilitv Conditionsne general subility conditions can be surnmarized using triangle ABC in Figure1.5.Arc A0; is the boundary between Cascs 1 and 3) it iq the locus of points suchthatd = cl + 4c: = 0. ne region above z40# cohzsmnds to Case l (sinced > 0) andtheregion below A0# corresponds to Case3 (sinced < 0).In Case 1 (in which the roots are real and distinct), stability requircs that thelargestroot be less than unity and the smllest root be greatr than

-1.

ne largestcharacteristicroot, (r,: = (f)j+ VJ1/2,will be less than unity ifi

i t: + (u2+ g.u )1r2< 2,I 2!? Hence,t71 + zuc < 4 - zkzt + (24

lror

)'

.-

' i.

j '1

:

z j. ja g ..

u(ck+ a < !

(a) Check the discriminant # = tz2, + 4th

d = (0.6)2- 4(0.9)

=-3.24

H4peekthe roots are imaginary. Thc homogencous solution has the form

yh = jjr.fcostol + )al!

Where ;J1and fzare ttrbitrar'y constants.

(b) Obtttin the value of r = (-az)'r2

r = (0.9):C2

. .. ).2

E'.. ;. ..: i.

. t i (.k

= 0.949

A F''-'''j,

j! .j''

a- (t?2+ 4c )1'2>

-2

.

1 1 2

az < 1 + a ,

Thus. the region of stability in Case l consists of a1l points in (he region bounded

by KQBC.For any point in AORC,conditions (l.52)

and (1.53) hold and d > 0.

ln Case 2 (repeatedroots), tz12 + 4tz: = 0. The stability condition is Itz, l < 2.

Hcnce, the region of stability in Case 2 consists of a1l points on arc d4OS.In Case 3

(d < 0). the stability condition is r = (-f7c)lf2< ! - Hence,j .

..

.

(wherea: < 0)

Thus, the region of stability' in Casc 3 consists of a1l points in region z10P. F9r

anypoint in z10S,(l.54)

is satisfied and J < 0.

A succint way to charactelize the stzbility conditions is to state that the charac-

teristicroots must 1ie within the unit circle. Consider the semicircle drawn in Figure

I.6.

Rcal numbers are measured on the horizontal axis and imaginary numbers on

Sclvfng Homoseneous Di/yrencr E'tputlltm.s 33

Figure 1-6 Choctehstic roots and the unit circle.

t)!

thevertical axis. If the characteristic roots al and c.zare bot real, they can be plot-tedon the horizonul axis. Stability requires that they 1iewithin a eiwleof radius 1.

Complex roots Fill lie somewhere in the complex plane. If a: > 0, the roots al =

ltzj+ i-dyl and tra = (tzI - if-dlll can bc represented by the two Xintsshown iFi ure 1.6. For example, (y,l is drawn by moving atll units along the real axis and

J/2 units along the imaginary axis. Using the distance formula, we can give thelengtl of tle radius r by

r = (Jj/2)2+ dnilzjl

andusing the fact that il =

-i,

we obtain

r = (-tzz)IN.

.. (E

','I'he subility condition requires that r < l . Hence, wben plotted on the corplexplane,the two roots aj and c.cmust 1ie within a circle of radius equat to unity. In '

''

th i-selies

literature, it is simply stated that stbilty requires that all charac-e t me )i tic roots lie wthn the unit circle. .' ; )l r J

. .'(Higher-order Systems. .r

differenceequatiohs. ne homogeneousequatid foi (1.10)i;

Dljjrena Equations

a . = jl

i = I

Given the results in Section 4, you should suspect each homogeneAi solution tohave the form y) = Aa', where ,4 is an arbitrary constant. Tbus, to 111'1tbe valuets)of a, we seek the solution for

1 -

cl - c; - fla > 01+ t:I -

a; + ca > 01 - a l az + az - c2,> O3 + t:j + al - 3;3 > 0 orr, dividing through by '-n

wz seek the values ot- a that solve. 9

zl . a (y,a- 1

- a a.n-2. . . .( 2 :z: ()Q 1 2 n

3 - t'j + az + 3f)3> 0Given that the first threc inequalities are satissed, cither of the last two can bechected. One of the last conditions is redundant given tht the othor three hold.

7. FINDINGPARTIUULAR SOLUTIONSFORDETERMINISTIC PROCESSES

'Finding the particular solution to a difference equation is often a matter of ingcnu-ity and perseverance. ne appropriate technique depends crucially on the form ofthe (x,)process. We begin by considering thosc processes that contain only deter-ministiccommnents. Of course, in econometric analysiss tile forcing process willcontainboth deterrninistic and stochastic components.

CASE 1. --. -- ).. )-..L-

- -. .. . . . .. ).- . - . . . -- . -. . --..-- -- J'

..-

kt - 0. When a11elements of te (1,)process are zero, the difference equation e-Comes.

j?t = Jo + fzll'r-t + t7zFf-z+ ''' + anyt-nIntuition suggests that an unchanging value of y (i.t., y, = y,-) = ... = c) Shouldsolvethe equation. Substitute the Zal solution y, = c into (1.58)to obtain

1 t30 a

(1.57)

This nth-order mlynomialwill yield n solutions fbr a. Denote these n character-istic roots by aj. aa. ..., aa. iven the results.in Secton 4, the linear combinatibnAlal + Ac + ... + Ana'a is also a solution. The arbitrary constants Al through hncan be eliminated by imposing n initial conditions on the general solution. The .ai

(may be real or complex numbers. Stability requires that a11 real-valued (y,j be lessthan unity in absolute value. Complex roots will necessarily comc in pairs. Stability''requires that a11rot?ts lie within the unit circle shown in Figure 1.6.

iln most circumstances, there is little need to directly calculate the characteristicroots of higher-order systems. Many of the technical details are included inAppendix 2 to this chapter. However, there are some useful rules to check the sta-bility conditions in higher-order systems.

1. In an nth-order equation, a necessary condition for a11characteristic roots to 1ieinsidethe unit circlc is

2. Sincc thc valucs of tlle ai can bc positive or negative, a suftscient condition fora11charactcfistic roots to 1ieinside the unit circlc is

nju

ju j' i

.'.

. . . . .. i = 1 .) (

.:. ..'

. ( . ': . . .;r . . ... ; . .r.:. . t .. . .

.'.

..,qj.t

: ..., .? ...: . :.(..?..... .. .. .. ..: .q....

.E :.( ;

.

.'.'. .;. . ,.:.t.....

.;.)i;.?tEt@'t!!.;. : .j;;3.L.i ;...

... :, .. ..

: '

. ... E !

3

Aj ryt jv: , t,,!

g j g ji. : guajj; u j) ktj. ;fi '

. . . . . .:

... . ) .. . .. .

,.r ..

g.(.

#>i

1!iI

:..'

! c''i.4;.,*Til'l.p;d1C'

''

'

4

D1J-ere n ce Equa f t'o n .

As long as- a - (;z -. - (1,,) doq)s j1':)( ttqual zcro. lhe valuc of c givcn by

(1.5t.))

is a solution to (l.58).

Hence, thtt particular solution to (i.5s)

is given by

v,P = t7(/( 1 - tzj - az - ... - av,).

If l - t7: - az- ... - an = 0, the value of c in ( l

..59)

is undefined-. it is necessafy to

try some other form for the solution. The key insight is that (yp) is a unit root

processif L'zk= 1. Since fyf) is not convergent. it stands to reason that the constany

solutiondoes not work. Instead, recail equations ( l . 12) and (1.26),.

thesc solutions

suggestthat a linear timc trend can appear in thc qolution of a unit root process. As

snch. t;'y thc solution yr = cJ. For CJ to be a solutitln. it must be the case that

or combining like terms. wc obtain

For example. !et

y, = 2 + 0.75:,-1 + 0.25y,-:.

Here, t7I = 0.75 and az = 0.25) (y,) is a unit root process since tzy + az = l .

'f'he

particular solution has the form cJ, where c' = 2/:0.75 + 2(0.25)) = 1.6. ln the event

that the solution ct fails, sequentially (1-y the solutions y: = cr2, cP, -..

, cf. For an

nth-order tquation. one of these solutions will always be thc particular solution.

CASE 2.

The Exponential Case. Let A; have the exponential form bd)r where b, ti and r

are constants. Since r has the natural interprcttltion as a growth rate, we would ex-

pect to encounter this type of forcing process case in a growth context. We illus-

trate thc solution procedure using the tirst-orderaquation;

= t2 + a 4y,- I + ltr

A ()

To try to gain an intuitive fcel for tbe form of thc solution. notice that if b = 0.

( l.60)

is a special case of (1.58).

Hence, you shoul expect a constant to appear in

the pmicular solution. Moreover. the expression t/r' grows at the constant ratc r.

Thus, you might expect the particular solutit'n to have the fonn y; = ctj + cslrr,

where ctl and c! are constants. If thts equation is actually a solution. you sbould be

Finding rtzrficulcrSolutionsjr Delennfafllic Procenes

able to substitute it back into (1.60) and (lbtain an identity. Making the appropriatcsubstitutions,we get

c + c,r = a, + c,fco + c,'t-l'j + bro

For this solution to e'work.'' it is necessary to select co and cl such that

o = a4 ! - t:1)

Thus, a particular solution is

The nature of the solution is that.yr

equals the constant t7J(1- t7I) plus an ex-ipressionthat grows at the rate r. Note that for Idr 1< 1, the particular soluticn con-yergesto al 1 - tzl).2 ('

.,f'.b

If eithcr tzl::lz 1 olr tzl = dr%use the Sttrick'' suggested in Case 1. lf a ;

= 1, try the .'

I

solutiono = ct, and if tzl = Jr, trv the solution cj = tbdrydr- tzI). Use precisely the'

t.v'

.j... .y..,...j

samemethodology in higher-order systems.

ASE 3

Determlnistic time trend. In this case let the (x ) sequence be represented by the' l

relationshipxt = btd where b is a constant and d a msitiveinteger. Hence,

Since yt depends on td, it follows that y,-, depends on (J - 1F,yp-z depends onu .

.

(1 - 2),i etc. As such, the particular solution has the form yr = o + cII + c1f + ''' +

cZ.To find the values of the ci, substitute the particular solution into (1.62). Then . . E

1 t the value of each c that rcsult in an identity. Although various values of d areseec i

Nssible, in economic applications it is common to see models incorporating a lin-ear time trend d = 1). For illustrative puqoses. consider the second-order equation

y,= av + tzyyf-: + aob-z + bt. Posit the solution yr = o + ckt, where co and cl are un-determinedcoefficients. Substituting this Stchallnge solution'' into the second-orderdifference equation yields

( l.63)

Now select values of co and cj so as to force Equation (1.63) to be an 'identity fora1lXssiblevalues of J. If we combine a11constant terms and a1l terms involving 1.

therequired values of co and cj are

R

311 Dtgerence Eclzzllftpl.s

so tha:

Thus. the parlicular solution wil! alsw wkplltain

a linear time trend. You shouldhave no difficulty foresceing thc solution technique if tzl + az = 1. ln this circum-qtance which is applicable to higher-order cases als-t:'y multiplying the originalchallenge solution by 1.

8. THE METHOD OF UNDETERMINED COEFFICIENTS

At this point, it is appropriate to introduce the tirst of two useful methods of sndingparticularsolutions when there are stochastic components'in the (y,)process. nekey insight of te method of undetermined coemcients is tat the particular solu-.tion to a linear difference equation is neccssarily lincar. Moreover, thc solution candependonly on time. a constant. and the elements of the forcing prcess (xr).nus,it is often possible to know the exact/br?n of the solution even though the coeffi-cients of the solution are unknown. ne techniquc involves posiling a solutioncalled a challenge solution-tat is a linear fundtion of a11terms thought to appearin actual solution. ne problem becomes one of Iinding the set of values for theseundetenninedcoefficients that solve the difference equation.

ne actual technique for finding the coefscients is straightfonvard. Substitute thecballengesolution into the otiginal difference equation and solvc for the values ofthe undetennined coefficients that yield an identity for al1possible values of the in-cludedvariables. lf it is not possible to obtain an identity, te form of tlle challengesolution is incon-ect. T:-,,/ new trial solution and repeat the process. In fact, weuscd thc mctod of undetennined coefficients when positing te challenge solu-tionsy,# = co + cl drt and y,# = o + cj t for Cases 2 and 3 in Section 7.

To begins reconsider thc simple first-order equation yt = ao + tzly/-j + E?. Sinceyou have solved this equation using the iterative method. the equation is useful forillustratingthc method of undctennined coefficients. ne ature of the ly,)processis such that the particular solution can depend only on a constant term, time. andthe individual elements of the (6,) sequence. Since t does not explicitly appear inthe forcing process. , can be in the particular solution only if the characteristic rootis unity. Since the goal is to illustratc tc method, posit the challenge solution:

yt = h + bjt + ktt-i

j'= ()

wherc bok 1. and a11the xt are the coefficicnts to be dctermined.

Substitute (1.64)

into the original difference equation to form

Collecting like terms, we obtain

Equation (1.65)

mnst hold for a11valucs of t and all mssiblevalues of the (E,)sequence. Thus, each of the following conditions must hold;E

ao - 1 = 0c.l -

a l %.= 0cta- tzjtzj = 0

bo-

ao - tzl)o + tz1?, = 0bL - tzjl'j = 0

Notice that the fifst ser of condions can l)e solved for theqc./recursively. ne so-lutionof the first condition enmils setting W)= 1. Given this solution for cmvthenext equation rcquires a: = cl . Moving down the list, we obtain az = tzlat ortt,z = tzl. Continning te recursive process, we 5nd cg = f'j. Now consider th lasttwo equations. nere are two possible cases dernding on the value of aj. If 411 # 1.it immediately follows tbat bk = 0 and bv = a 1 - t71). For this case, te particularsolution is

Compare this result to (1.2

1)-.you will see that it is precisely the same solutionfound using the iterative method. Tbe general solution is the sum of this particularsolution plus the homogeneous solution z4cj. Hence, the generl solutitm is

Now. if there is Rn initial condition fof yo, it follows that

I)'

, !

It

Thr Afz-r/ltlt/of L/nt/crt.r?rl/lirr/Cotpjlcirnts

h +#!f + Jwa4,s.*,% '#J. I h + bt t - 1)+ (&E?-!-'. + s.+ ;$1E,-,

i;zz() .. k.tE;. ()

Mixch.ing oeflicients on all terms containing E,, E,-: . E,-2, ... yields

! ( ( ( :y ( W = )c.l = a 1+) + ;J, (so that aj = a j + flll)ac = t7l(y,l (sothat cec= t'J,((J: + ;'$j))az cut tzjaz . (sothat aa = (t7l)2(c;+ ;Jj))

a.i = a jaj-: tso that t.i= (z,)i-'(Jl + j1))

bv= ao + tzlbo - fzlbl

b j= a 1b!

To take A 'cotjd' example. consider the equation

y,= t'o + a .y?-I + E, + ;Jlt,.-!

Again, the solution can depend only on a constant, the elements of the (E,) se-quence.and t raised to the Grst mwer.As in the previous example, l does not need

to be included in the challengr solution if the characteristic root differs from nity.

To reinforce this point. use the challenge solution given by (1.64).Substitute tis 'tenmtivesolution into (1.67) to obtain $

. .:'.. . . .

The general solution augments the particular solution with the term.4t7l.

You areleftwith th'e exercise of imposing the initial condition for yll on thc general solution.Now consider the case in which cl = l . The undetermined coeficients are such that

''

:j = ao and bo is an arbitra:'y constant. The improper form of the solution is .'

42 trencefvualion.

.'

. . . ' . . . . . '.

.

'' ..': .: ...'. .1'!' '. E.

'. ..

z.' (.. ...

' ' 1:'?

Higher-order SystemsThe identical procedure is used for higher-ordcr systclni .iA.wtlexarttj 1tj ld ut hdthe particular solution to the scconfl-rnrtl'zr equation: E.. .'

',' = /7 + a jyr-j + aj ,-a + et.1 O

Sincc we have a sccond-order equation. wc use tllc challengc solution:

= bo + bLt + 172r2+ %e, + a1E?-l + (.cEt-2 + .'.F,

43

( l.69)

must equal zero for a1l values of J. First, consider the case inwhichfll + (72 # 1. Since (1 - t:21 - azj does not vanish. it is necessaly to sct thevalue of bz equal to zero. Given that bz = 0 and the coefticient of l must cqtlalzero, it follows that bt must also be set equal to zero. Finallg, gi.ven thatb, = bz = 0, w.e mtlst set bo = J#(1 - (71 - azj. instcad. ir Jt + tzz = 1. the solu-tions for tht bi depend on the specitk values of aw t7:. and tzz. 'I'he key point isthat he .&J2!)ifl'ly condition for the homogeneous equation is precisely the condi-tionfor convergence of the particular solution. J./-the characteristic roots of thetprrlo/anct?lt.tequation are elftzl to uafy, a polynomal time trend will appearin the particular solution. ne order 4./ the polynomal is the number of unitarycharacterisc roots. This result generalizes to higher-order equations.

Equation

If you are really clever, you can combine te discussion of the last section withthe method of undetermined coefficiene. Find the detemnistic portion of the par-tcular solution usihg the techniques discussed in the last section. Then use themethodof undetcrmined cllefficient-s to find the sthastic portion of the particularsolution.In (1.67).for example, set E, = E,-) = 0 and obtain the solution :(/(1 - /j).Now use the method of undetermind cfficients to find the prticular solution ofyt = (7lyf-, + Ef + pIe,-1. Add together the deterministic and stochastic componentstoobtain a11commnents of the particular solution.

A Solved ProblemTo illustrate the methodology using a second-order equation, aagment (1.28) wiihte stochastic tefm G so that

= 3 + 0.9y,-l - 0.2y,-z + 6,F?( l

.70)

Yot) hnve already vrfifittd tlmt the two homogeneous Solutions are Aj(0.5)' andz(0.4)'and tlle deterministic Portion of the particular solution is y,# =) 10. To findthestochastic portion of te particular solution, fonn the challenge solution-. '

*

y: = aiEt-

=0!

:

. y. .

;'

2. 4

'

1ln contrast to (1.64),

the intercept term bo is eicluded (sincc we have already.'''

)ftmndte deterministic portion of the particular solution) and the timc trend btt isli h teristic roots are less than unity). For this clk.v -rige

toexclnded(sincebot .c arac

. ., .

,

%%W0rk'* it must satisfy%

09( E + a E + ct E + d E +.1.

)''

l%6, + (:16,..1 + Xg't-.z + (2t3G.-:I + .*. =

. (1(j ,-1 j t-, c ,..:j zj tu. .. ;- 0 ztc/oe+ a E + %et-4+ daE,-,s + ... J + e (1.71)> t--:j l 1-- :1.

r

where#o, '1, bz. and the (J.; are thc undetennined coefficients.Substituting the challengc solution into (1.68) yields

The necessary and sufficient conditions for tlle values of the af's to render theequation above an identity for a11possible rcaliz:ltions of the (E,) sequcnce are

co = 1c,, = llao gsothal ct! = 21)

cf.a= clay + azp (sothat ty.a= (tzl)2+ c(Ezy= 7ja..z + Jzty,! (sothat aa = (N$)3 + 2t7cz)

.. '

..

,'

'

q Cqq.. .... :q(F.

j

Norice that for any value of j 2 2. the coefscients solve the second-order diffef- )

encefrquation

c.y= tzlcs: + azhn. Since we know ao and ay. we can solve for all 7,the a, iteratively. The properties of the coeffidients will be precisely' those dis- 8

Jcussetlwhen considering homogencous soluticns. nantely the following: 5t

1. Convergence necessitates laz 1< 1, t?) + az < l . and az - cj < 1. Notice that con- (vergenceimplies that past values of the (E?) Fequence ultimately have a succes- t

sivelysmaller inuence on the currentvaluc of y,.2. lf the coefscients converge, convergence will be direct if (tz2j+ 4tzc) > 0, will

follow a sine/cosine pattern if tt + 4(7a) < 0. and will t'explode'' and then con-verge if tty+ 4az) = 0. Appropriatcly setting the i. we are left with the remain-ing expression: '

Dtjference Equa:ions

Sincc ( l.7

l ) must hold for a1l possible realizIgions gf :r, E,-y, Et-zy ---. ah of th

followingconditions must hold: ' ,,

fwg Oprralors 45

9. LAGOPEBATORS

If it is not important to know the actual values of tlle coefficients appearing in thepafticularsolution, it is often more convenient to usc lag operators than the methodof undetermined coefticients. The Iag operator L is defined to bc a Inear operatorsuchthat for any value y,

.' .,

i.- ,isa ) ,-i

Thus, Li prcceding y, silllply means to lag yf b i periods. 1(is useful to rememberthe following properties of 1agoperators:

1. The 1agof a constant is a constant: ,c

= c.2. The distributive law holds for lag o'perators. We can set (/ + Lhy',= Eiyt+ Liyt =

X-/ +.%-j.