early warning strategies for governments: … · early warning strategies for governments:...

TRANSCRIPT

1

EARLY WARNING STRATEGIES FOR GOVERNMENTS: NAVIGATING THROUGH TROUBLED TIMES

KANSAS GOVERNMENT FINANCE OFFICERS ASSOCIATION

OCTOBER 18, 2013

Nancy L. Zielke, Senior Director

Alvarez & Marsal Public Sector Services

Nancy L. Zielke

1

Senior Director

Alvarez & Marsal

Public Sector Services, LLC

Prior to joining Alvarez & Marsal, Ms. Zielke worked in state and local governments where she served in senior financial and administrative

positions (University of Missouri - Kansas City; Unified Government of Wyandotte County/City of Kansas City, Kansas; Kansas City Board of

Public Utilities; and the State of Kansas). During her public sector career she led significant organizational change management and process

improvement initiatives; redesigned a budgeting for excellence with responsibility centered management; improved procurement practices;

consolidated governmental operations including shared services; developed competitive economic development incentive policies;

outsourced programs and services; and restructured the financial and operational elements of local governments.

Since joining A&M, Ms. Zielke has been a key project leader on numerous public sector financial and operational improvement

analyses/studies including: State of LA Department of Revenue; State of South Carolina Department of Employment & Workforce and

Department of Health and Human Services; Unified Government of Wyandotte County//Kansas City, Kansas, Maricopa County Community

College; San Jacinto Community College; Detroit Public Schools; Pittsburgh Public Schools; Humble Texas Independent Schools District;

Kansas City Kansas Board of Public Utilities; Cities of Harrisburg, PA; Leawood, KS; Overland Park, KS; Olathe, KS; Louisburg, KS;

Riverside, MO; Louisburg, KS; Lees’ Summit, MO; Huntsville, TX; Seabrook, TX; and numerous other governments.

She has been a key project lead on various distressed municipal government financial advisory service projects assisting in measuring the

financial health of communities and the development of strategic initiatives to address operating shortfalls. Ms. Zielke has recently served as

the acting Deputy CFO for Detroit Public Schools and Interim Director of Planning and Budget for the South Carolina Department of Health

and Human Services overseeing transformation of these entities’ budget planning and financial reporting operations.

Ms. Zielke received an undergraduate degree in business administration, with concentrations in economics and marketing, from Adrian

College, and a master's degree in public administration from the University of Kansas. As an author and speaker, she has made numerous

presentations on a wide variety of topics, including strategies for business process improvement, leadership, and best practices in budgeting

and resource allocation strategies. She is holds a certification as an Emergency Manager from Michigan State University.

Ms. Zielke has been a member of Government Finance Officers Association (GFOA), where she served on the Executive Board for six years

and was the elected 2004-2005 National President of GFOA. She is a member of Women in Public Finance, GFOA, Alpha Kappa Psi, and the

Kansas University City Management in Training Association and formerly active in the National Institute of Government Purchasing

Association and the National Association of College & University Business Officers. She serves as an advisor to the GFOA Governmental

Budgeting and Fiscal Policy Standing Committee and a reviewer for the GFOA Awards for Excellence Program.

Nancy Zielke is a Senior Director with Alvarez & Marsal Public Sector Services, LLC.

With more than 25 years of public sector experience, Ms. Zielke brings deep expertise

in state and local government budgeting; operational and financial improvement

strategies; and fiscal sustainability planning within complex government organizations.

Specializing in providing restructuring and business advice to troubled public sector

entities and creditor groups on governmental financial and operational issues, her

primary areas of focus include: cost structure and revenue enhancement analysis,

financial and operational management, budget redesign and reporting processes, cash

flow forecasting, financial modeling, debt capacity analysis, and evaluation of strategic

alternatives.

2

© Copyright 2013 Alvarez & Marsal Holdings, LLC. All rights reserved. ALVAREZ & MARSAL®,

® and A&M® are trademarks of Alvarez & Marsal Holdings, LLC.

PRESENTATION OUTLINE

I. Governments in Distress

II. Lessons Learned to Navigate Through Financial Difficulty

Develop Monitoring Systems to Track Financial Health

Provide Timely Reporting of Financial Results

Understand Cash and Financial Position

Prioritize Government Services and Operational Reviews

Provide for Accountability in Financial Management

Be Willing to Spend Money to Save Money

III. Conclusions & Wrap-up Questions

2

WHAT KEEPS A FINANCE OFFICER UP AT NIGHT:

Could I have seen this coming?

Was there an important ratio or audit note I

missed?

Are there other entities facing this same issue?

What can I learn from other distressed cities?

3

3

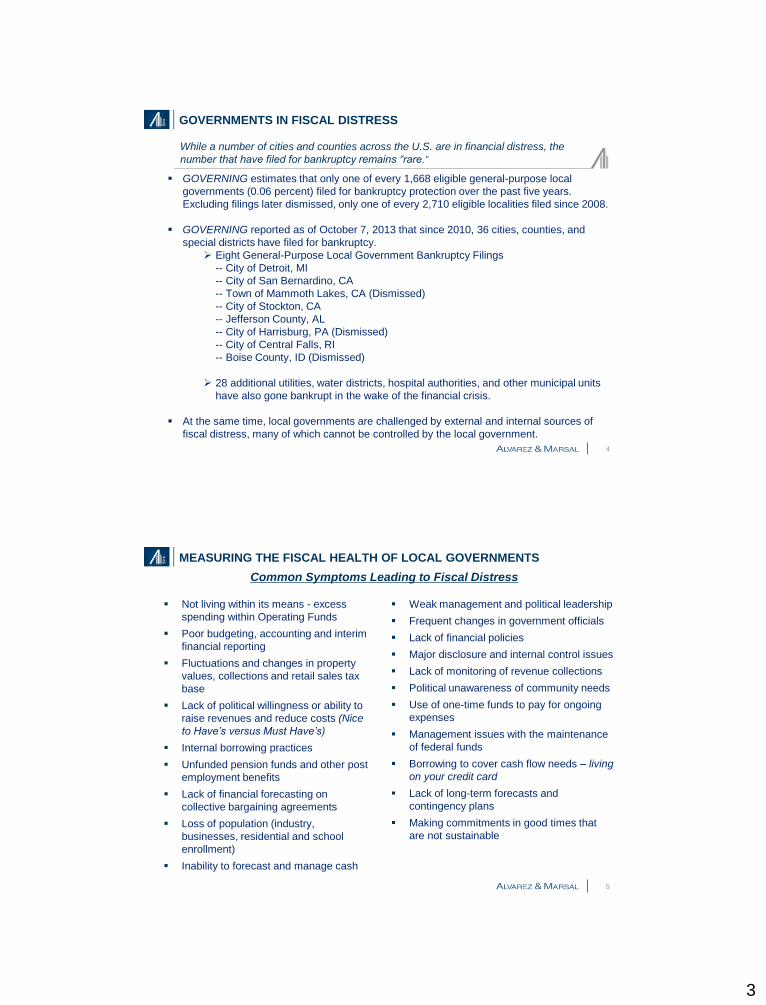

GOVERNMENTS IN FISCAL DISTRESS

GOVERNING estimates that only one of every 1,668 eligible general-purpose local

governments (0.06 percent) filed for bankruptcy protection over the past five years.

Excluding filings later dismissed, only one of every 2,710 eligible localities filed since 2008.

GOVERNING reported as of October 7, 2013 that since 2010, 36 cities, counties, and

special districts have filed for bankruptcy.

Eight General-Purpose Local Government Bankruptcy Filings

-- City of Detroit, MI

-- City of San Bernardino, CA

-- Town of Mammoth Lakes, CA (Dismissed)

-- City of Stockton, CA

-- Jefferson County, AL

-- City of Harrisburg, PA (Dismissed)

-- City of Central Falls, RI

-- Boise County, ID (Dismissed)

28 additional utilities, water districts, hospital authorities, and other municipal units

have also gone bankrupt in the wake of the financial crisis.

At the same time, local governments are challenged by external and internal sources of

fiscal distress, many of which cannot be controlled by the local government.

While a number of cities and counties across the U.S. are in financial distress, the

number that have filed for bankruptcy remains “rare.”

4

MEASURING THE FISCAL HEALTH OF LOCAL GOVERNMENTS

Common Symptoms Leading to Fiscal Distress

5

Not living within its means - excess

spending within Operating Funds

Poor budgeting, accounting and interim

financial reporting

Fluctuations and changes in property

values, collections and retail sales tax

base

Lack of political willingness or ability to

raise revenues and reduce costs (Nice

to Have’s versus Must Have’s)

Internal borrowing practices

Unfunded pension funds and other post

employment benefits

Lack of financial forecasting on

collective bargaining agreements

Loss of population (industry,

businesses, residential and school

enrollment)

Inability to forecast and manage cash

Weak management and political leadership

Frequent changes in government officials

Lack of financial policies

Major disclosure and internal control issues

Lack of monitoring of revenue collections

Political unawareness of community needs

Use of one-time funds to pay for ongoing

expenses

Management issues with the maintenance

of federal funds

Borrowing to cover cash flow needs – living

on your credit card

Lack of long-term forecasts and

contingency plans

Making commitments in good times that

are not sustainable

4

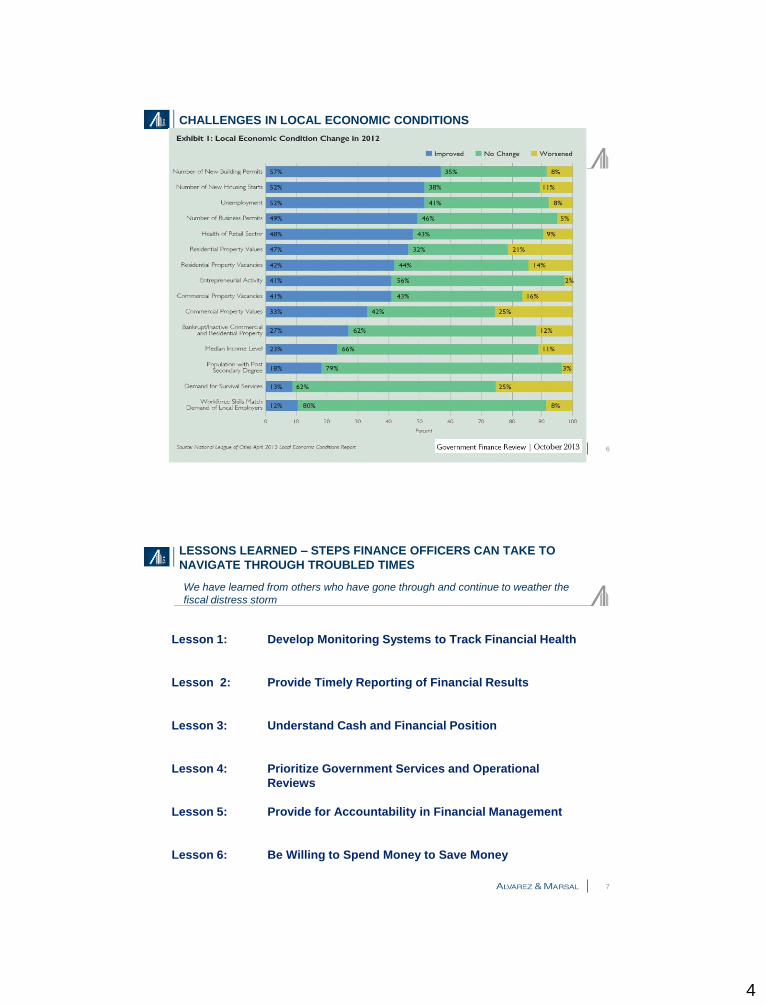

CHALLENGES IN LOCAL ECONOMIC CONDITIONS

6

LESSONS LEARNED – STEPS FINANCE OFFICERS CAN TAKE TO

NAVIGATE THROUGH TROUBLED TIMES

Lesson 1: Develop Monitoring Systems to Track Financial Health

Lesson 2: Provide Timely Reporting of Financial Results

Lesson 3: Understand Cash and Financial Position

Lesson 4: Prioritize Government Services and Operational

Reviews

Lesson 5: Provide for Accountability in Financial Management

Lesson 6: Be Willing to Spend Money to Save Money

We have learned from others who have gone through and continue to weather the

fiscal distress storm

7

5

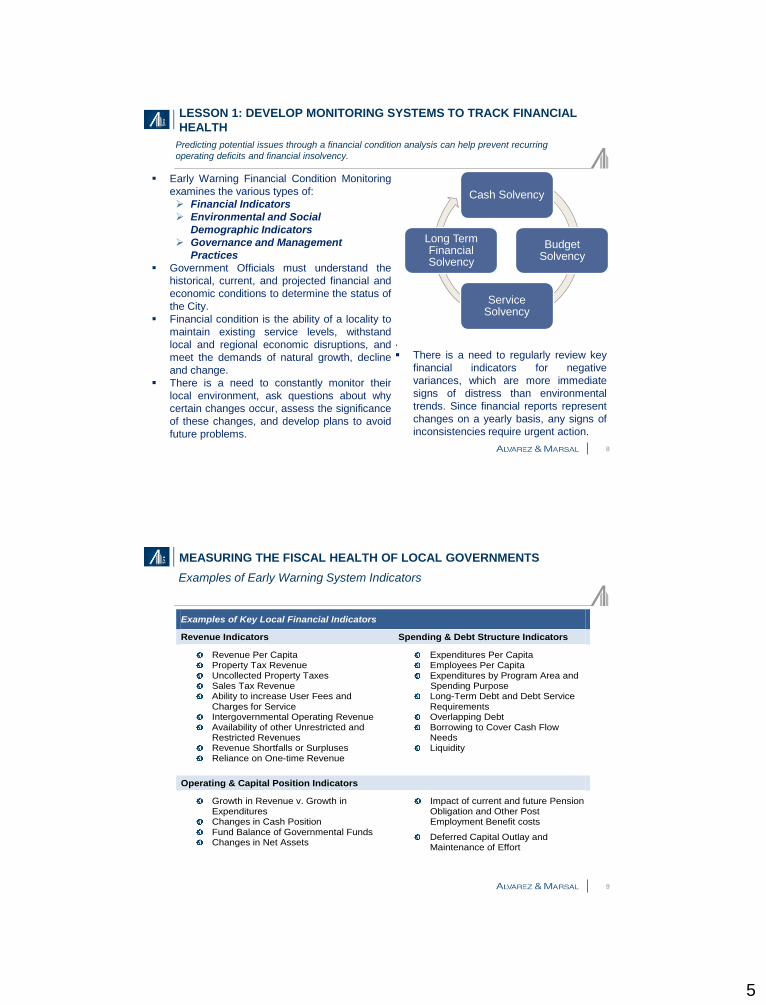

LESSON 1: DEVELOP MONITORING SYSTEMS TO TRACK FINANCIAL

HEALTH

Predicting potential issues through a financial condition analysis can help prevent recurring

operating deficits and financial insolvency.

8

Cash Solvency

Budget Solvency

Service Solvency

Long Term Financial Solvency

Early Warning Financial Condition Monitoring

examines the various types of:

Financial Indicators

Environmental and Social

Demographic Indicators

Governance and Management

Practices

Government Officials must understand the

historical, current, and projected financial and

economic conditions to determine the status of

the City.

Financial condition is the ability of a locality to

maintain existing service levels, withstand

local and regional economic disruptions, and

meet the demands of natural growth, decline

and change.

There is a need to constantly monitor their

local environment, ask questions about why

certain changes occur, assess the significance

of these changes, and develop plans to avoid

future problems.

.

There is a need to regularly review key

financial indicators for negative

variances, which are more immediate

signs of distress than environmental

trends. Since financial reports represent

changes on a yearly basis, any signs of

inconsistencies require urgent action.

MEASURING THE FISCAL HEALTH OF LOCAL GOVERNMENTS

Examples of Early Warning System Indicators

9

Examples of Key Local Financial Indicators

Revenue Indicators Spending & Debt Structure Indicators

Revenue Per Capita Property Tax Revenue Uncollected Property Taxes Sales Tax Revenue Ability to increase User Fees and

Charges for Service Intergovernmental Operating Revenue Availability of other Unrestricted and

Restricted Revenues Revenue Shortfalls or Surpluses Reliance on One-time Revenue

Expenditures Per Capita Employees Per Capita Expenditures by Program Area and

Spending Purpose Long-Term Debt and Debt Service

Requirements Overlapping Debt Borrowing to Cover Cash Flow

Needs Liquidity

Operating & Capital Position Indicators

Growth in Revenue v. Growth in Expenditures

Changes in Cash Position Fund Balance of Governmental Funds Changes in Net Assets

Impact of current and future Pension Obligation and Other Post Employment Benefit costs

Deferred Capital Outlay and Maintenance of Effort

6

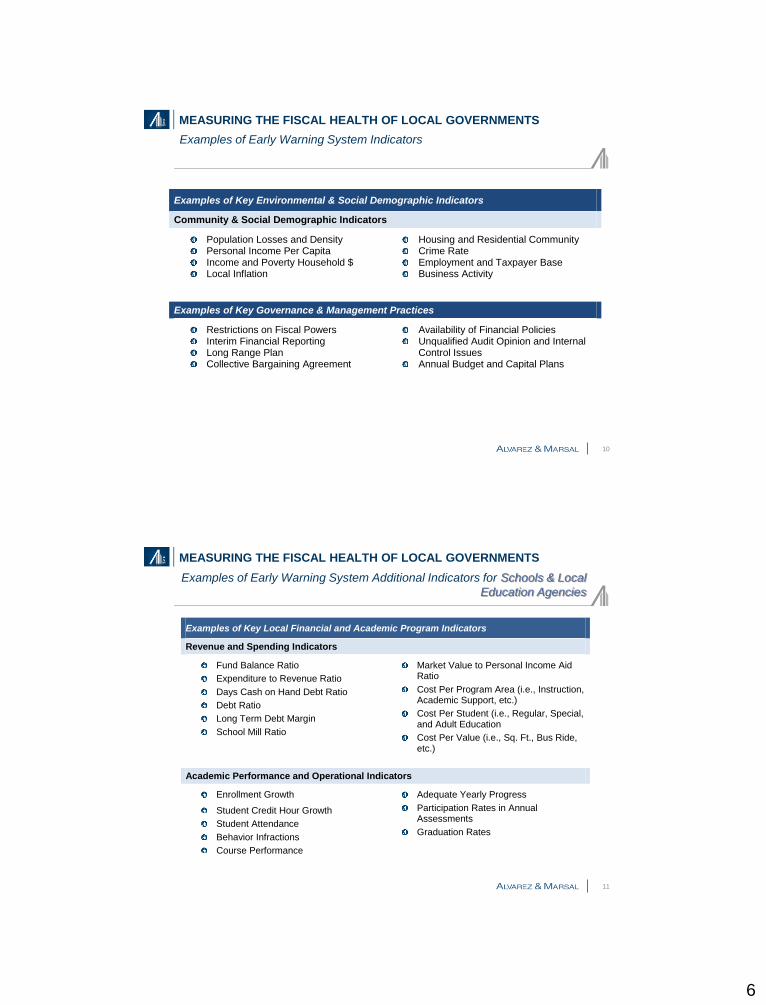

MEASURING THE FISCAL HEALTH OF LOCAL GOVERNMENTS

Fiscal Health Warning Signs

10

Examples of Early Warning System Indicators

Examples of Key Environmental & Social Demographic Indicators

Community & Social Demographic Indicators

Population Losses and Density Personal Income Per Capita Income and Poverty Household $ Local Inflation

Housing and Residential Community Crime Rate Employment and Taxpayer Base Business Activity

Examples of Key Governance & Management Practices

Restrictions on Fiscal Powers Interim Financial Reporting Long Range Plan Collective Bargaining Agreement

Availability of Financial Policies Unqualified Audit Opinion and Internal

Control Issues Annual Budget and Capital Plans

MEASURING THE FISCAL HEALTH OF LOCAL GOVERNMENTS

Examples of Early Warning System Additional Indicators for Schools & Local

Education Agencies

11

Examples of Key Local Financial and Academic Program Indicators

Revenue and Spending Indicators

Fund Balance Ratio

Expenditure to Revenue Ratio

Days Cash on Hand Debt Ratio

Debt Ratio

Long Term Debt Margin

School Mill Ratio

Market Value to Personal Income Aid Ratio

Cost Per Program Area (i.e., Instruction, Academic Support, etc.)

Cost Per Student (i.e., Regular, Special, and Adult Education

Cost Per Value (i.e., Sq. Ft., Bus Ride, etc.)

Academic Performance and Operational Indicators

Enrollment Growth

Student Credit Hour Growth

Student Attendance

Behavior Infractions

Course Performance

Adequate Yearly Progress

Participation Rates in Annual Assessments

Graduation Rates

7

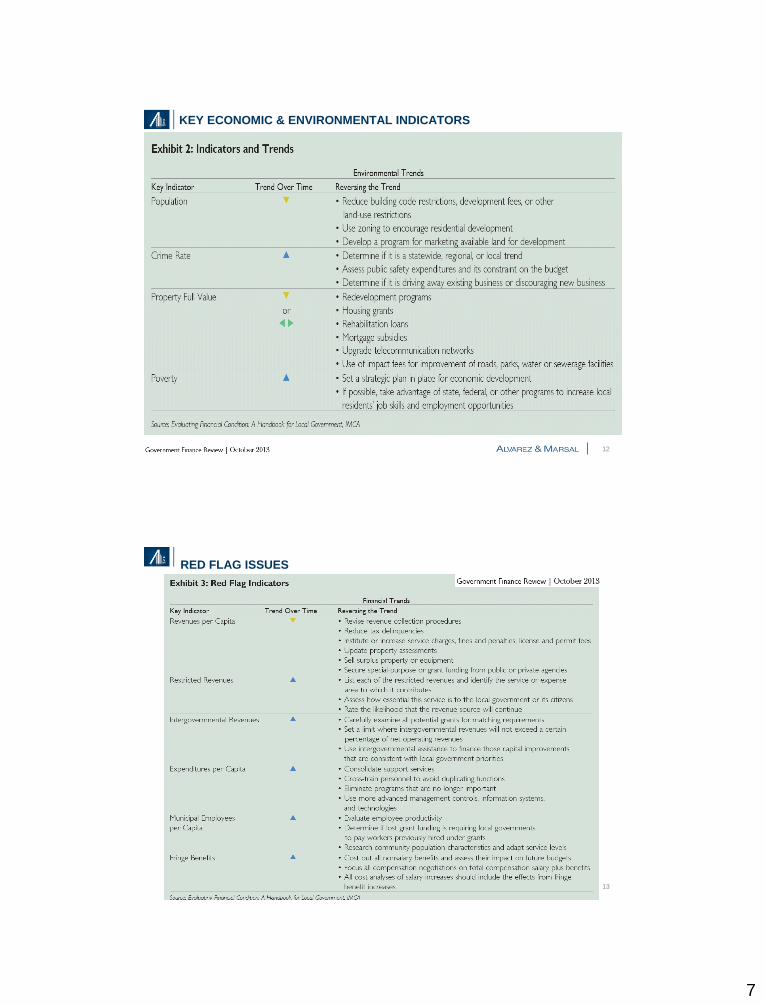

KEY ECONOMIC & ENVIRONMENTAL INDICATORS

12

RED FLAG ISSUES

13

8

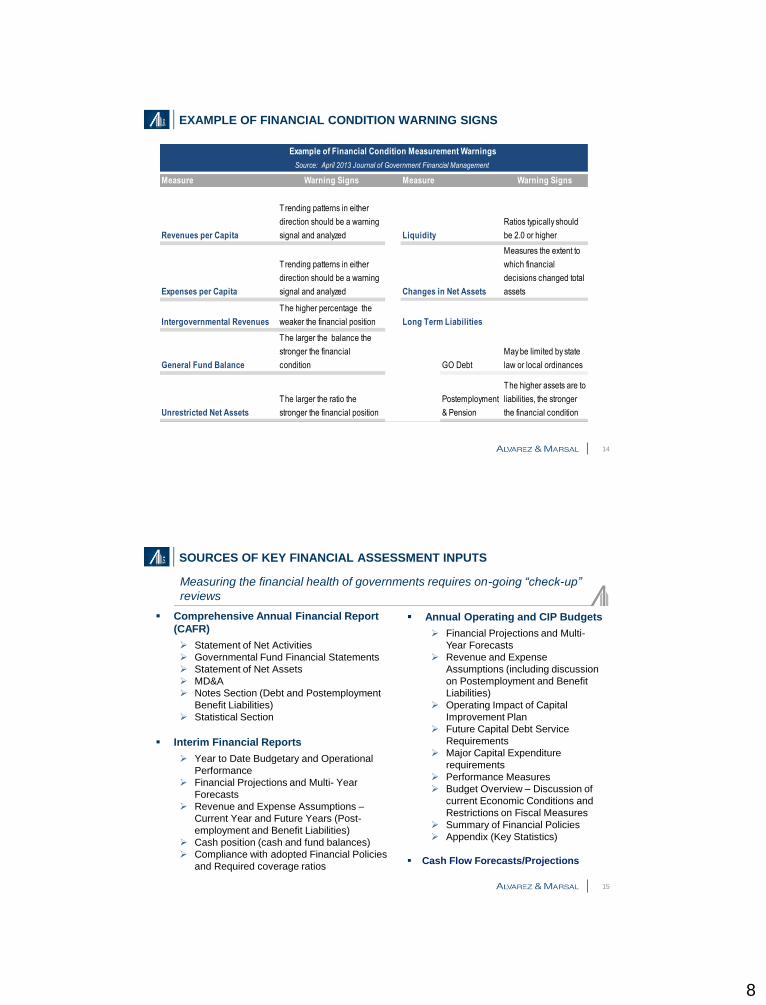

EXAMPLE OF FINANCIAL CONDITION WARNING SIGNS

14

Example of Financial Condition Measurement Warnings

Source: April 2013 Journal of Government Financial Management

Measure Warning Signs Measure Warning Signs

Revenues per Capita

Trending patterns in either

direction should be a warning

signal and analyzed Liquidity

Ratios typically should

be 2.0 or higher

Expenses per Capita

Trending patterns in either

direction should be a warning

signal and analyzed Changes in Net Assets

Measures the extent to

which financial

decisions changed total

assets

Intergovernmental Revenues

The higher percentage the

weaker the financial position Long Term Liabilities

General Fund Balance

The larger the balance the

stronger the financial

condition GO Debt

May be limited by state

law or local ordinances

Unrestricted Net Assets

The larger the ratio the

stronger the financial position

Postemployment

& Pension

The higher assets are to

liabilities, the stronger

the financial condition

SOURCES OF KEY FINANCIAL ASSESSMENT INPUTS

Comprehensive Annual Financial Report

(CAFR)

Statement of Net Activities

Governmental Fund Financial Statements

Statement of Net Assets

MD&A

Notes Section (Debt and Postemployment

Benefit Liabilities)

Statistical Section

Interim Financial Reports

Year to Date Budgetary and Operational

Performance

Financial Projections and Multi- Year

Forecasts

Revenue and Expense Assumptions –

Current Year and Future Years (Post-

employment and Benefit Liabilities)

Cash position (cash and fund balances)

Compliance with adopted Financial Policies

and Required coverage ratios

Measuring the financial health of governments requires on-going “check-up”

reviews

15

Annual Operating and CIP Budgets

Financial Projections and Multi-

Year Forecasts

Revenue and Expense

Assumptions (including discussion

on Postemployment and Benefit

Liabilities)

Operating Impact of Capital

Improvement Plan

Future Capital Debt Service

Requirements

Major Capital Expenditure

requirements

Performance Measures

Budget Overview – Discussion of

current Economic Conditions and

Restrictions on Fiscal Measures

Summary of Financial Policies

Appendix (Key Statistics)

Cash Flow Forecasts/Projections

9

EXAMPLE OF DASHBOARD – CITY OF STOCKTON

16

Description

Per Capita Income of the City compared to the State

average determines the wealth within the municipality. Per

capita income as an important measure of a City’s ability to

meet its financial obligations.

The measure reflects the community’s ability to pay taxes.

Generally, the higher the per capita income, the more

property taxes, sales taxes, user fees, and business taxes

the City can generate. If income is distributed evenly, a

higher per capita income may mean a lower dependency on

governmental services, depending on the mix of services

provided.

A decline in per capita income results in loss of consumer

purchasing power and can provide advance notice that

businesses, especially in the retail sector, will suffer a

decline that can ripple through the rest of the City’s

economy.

Formula

City Per Capita Income

State Per Capita Income

Income Per Capita

Warning Trend

Above 120% Per Capita Not in Stress (Green)

Between 70 and 120% Nearing or Moderate

Stress (Yellow)

Below 70% Distressed (Red)

Analysis & Trend

The City of Stockton has had per capita income levels

between 70 and 72% since 2001. This ratio is near the

lower end of the nearing to moderate per capita levels

and nearing the distressed level.

This indicator received a yellow rating

Calendar Year - As of January 1

2006 2007 2008 2009 2010 2011

Income Per Capita

Stockton Per Capita Income 29,383$ 31,012$ 31,250$ 29,995$ 30,251$ 31,013$

CA Per Capita Income 41,518$ 43,211$ 44,003$ 41,034$ 41,893$ 43,647$

Ratio 70.8% 71.8% 71.0% 73.1% 72.2% 71.1%

Source: Federal Reserve Economic Data (January 1 of each year)

$-

$10,000

$20,000

$30,000

$40,000

$50,000

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Local to State Per Capita Income

CA Per Capita Income Stockton Per Capita Income

74.8% 75.6% 75.7% 74.4% 71.9% 70.8% 71.8% 71.0% 73.1% 72.2% 71.1%

EXAMPLE OF DASHBOARD – EXAMPLE

17

Description

Each year, a certain percentage of property taxes are not

collected because of property owners’ inability to pay, intentional

deferral of payments, deficiencies in collection methods, policies

and procedures, or a declining economy. Property taxes are

collected by the county and distributed based on the amount

levied by separate taxing entities.

If the percentage of uncollected property taxes increases over

time, it may indicate a decline in the City’s overall economic

health.

Warning Trend

Increasing amount of uncollected property taxes as a percentage

of net property tax levy.

An uncollectible rate of 2% or 3% per year normal. If the

delinquency rate rises for two consecutive years or more to 5% to

8%, it may signal potential problems in the stability of the property

tax base or collection methods.

Formula

Uncollected property taxes

Net property tax levy

Uncollected Property Taxes

Analysis & Trend

The City’s delinquent property taxes have ranged

from a low of 1% in 2006 to a high of 5.6% in

2010. In most years the delinquent property taxes

have ranged between 1% and 3%.

The warning trend was observed since 2007 for

this indicator. The credit rating agencies consider

an uncollectible rate of 2% or 3% per year

normal. If the delinquency rate rises for two

consecutive years or more to 5% to 8%, it may

signal potential problems in the stability of the

property tax base or collection methods.

This indicator received a red rating

FY 2006 FY 2007 FY 2008 FY 2009 FY 2010

Delinquent Property Tax 93,980$ 328,568$ 325,421$ 430,202$ 561,968$

Net Property Tax Levy 8,990,268$ 9,409,338$ 9,409,228$ 10,354,161$ 10,276,906$

% of Net Property Tax Levy 1.0% 3.5% 3.5% 4.2% 5.5%

10

MEASURING THE FISCAL HEALTH OF LOCAL GOVERNMENTS

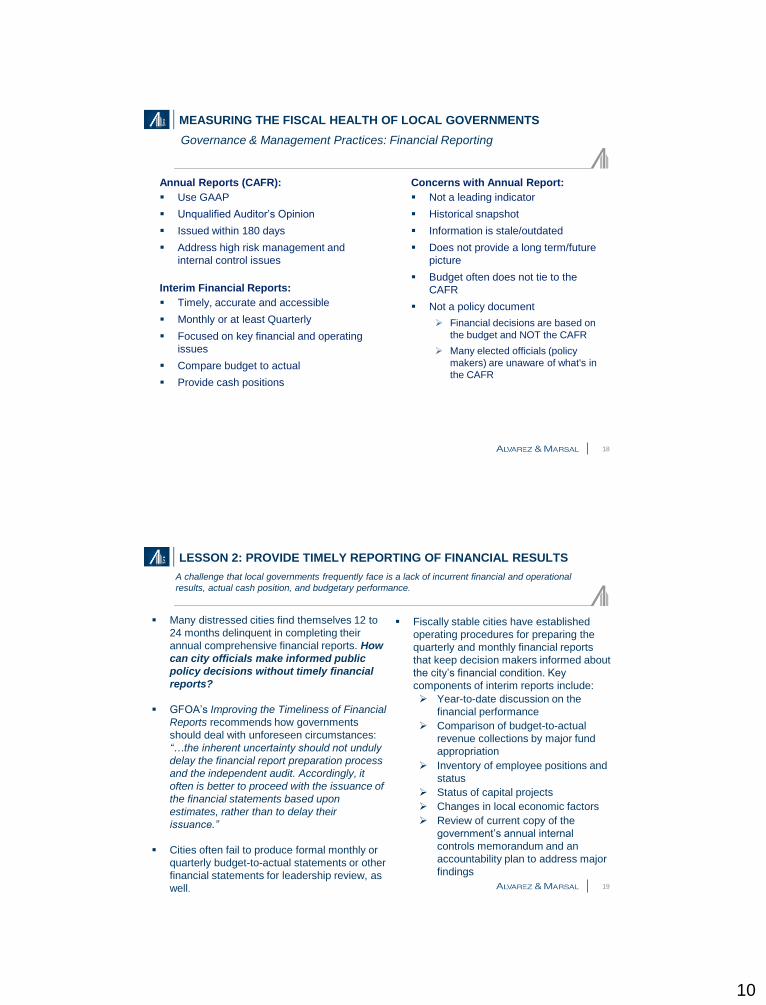

Annual Reports (CAFR):

Use GAAP

Unqualified Auditor’s Opinion

Issued within 180 days

Address high risk management and

internal control issues

Interim Financial Reports:

Timely, accurate and accessible

Monthly or at least Quarterly

Focused on key financial and operating

issues

Compare budget to actual

Provide cash positions

Fiscal Health Warning Signs

18

Concerns with Annual Report:

Not a leading indicator

Historical snapshot

Information is stale/outdated

Does not provide a long term/future

picture

Budget often does not tie to the

CAFR

Not a policy document

Financial decisions are based on

the budget and NOT the CAFR

Many elected officials (policy

makers) are unaware of what's in

the CAFR

Governance & Management Practices: Financial Reporting

LESSON 2: PROVIDE TIMELY REPORTING OF FINANCIAL RESULTS

A challenge that local governments frequently face is a lack of incurrent financial and operational

results, actual cash position, and budgetary performance.

19

Many distressed cities find themselves 12 to

24 months delinquent in completing their

annual comprehensive financial reports. How

can city officials make informed public

policy decisions without timely financial

reports?

GFOA’s Improving the Timeliness of Financial

Reports recommends how governments

should deal with unforeseen circumstances:

“…the inherent uncertainty should not unduly

delay the financial report preparation process

and the independent audit. Accordingly, it

often is better to proceed with the issuance of

the financial statements based upon

estimates, rather than to delay their

issuance.”

Cities often fail to produce formal monthly or

quarterly budget-to-actual statements or other

financial statements for leadership review, as

well.

Fiscally stable cities have established

operating procedures for preparing the

quarterly and monthly financial reports

that keep decision makers informed about

the city’s financial condition. Key

components of interim reports include:

Year-to-date discussion on the

financial performance

Comparison of budget-to-actual

revenue collections by major fund

appropriation

Inventory of employee positions and

status

Status of capital projects

Changes in local economic factors

Review of current copy of the

government’s annual internal

controls memorandum and an

accountability plan to address major

findings

11

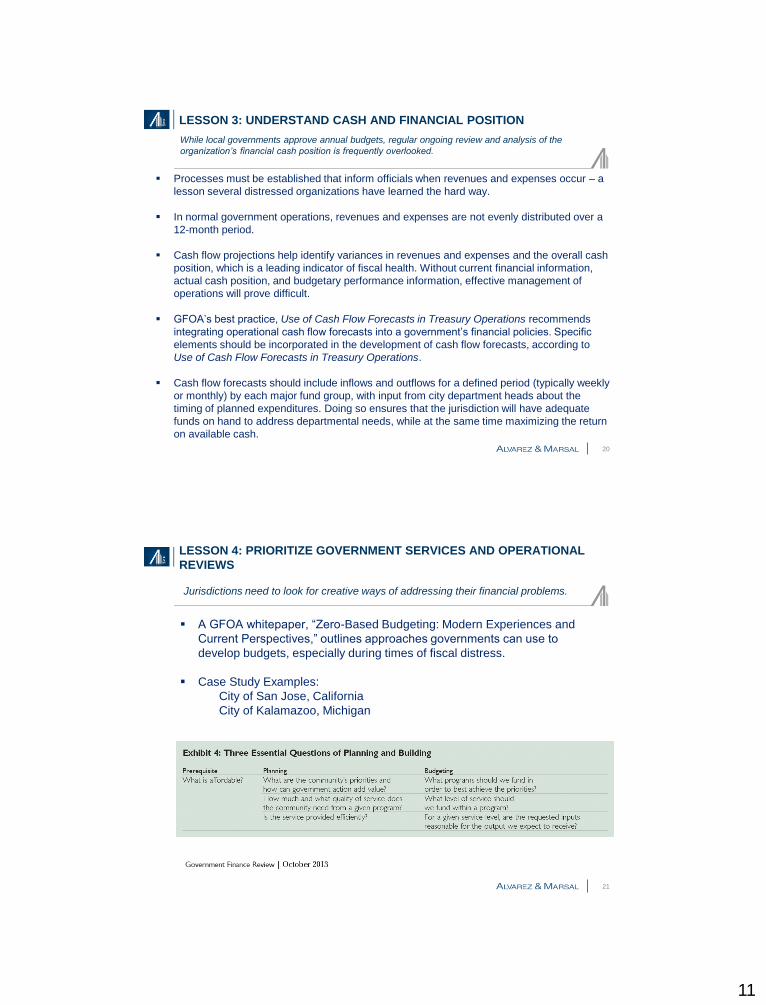

LESSON 3: UNDERSTAND CASH AND FINANCIAL POSITION

Processes must be established that inform officials when revenues and expenses occur – a

lesson several distressed organizations have learned the hard way.

In normal government operations, revenues and expenses are not evenly distributed over a

12-month period.

Cash flow projections help identify variances in revenues and expenses and the overall cash

position, which is a leading indicator of fiscal health. Without current financial information,

actual cash position, and budgetary performance information, effective management of

operations will prove difficult.

GFOA’s best practice, Use of Cash Flow Forecasts in Treasury Operations recommends

integrating operational cash flow forecasts into a government’s financial policies. Specific

elements should be incorporated in the development of cash flow forecasts, according to

Use of Cash Flow Forecasts in Treasury Operations.

Cash flow forecasts should include inflows and outflows for a defined period (typically weekly

or monthly) by each major fund group, with input from city department heads about the

timing of planned expenditures. Doing so ensures that the jurisdiction will have adequate

funds on hand to address departmental needs, while at the same time maximizing the return

on available cash.

While local governments approve annual budgets, regular ongoing review and analysis of the

organization’s financial cash position is frequently overlooked.

20

LESSON 4: PRIORITIZE GOVERNMENT SERVICES AND OPERATIONAL

REVIEWS

Jurisdictions need to look for creative ways of addressing their financial problems.

21

A GFOA whitepaper, “Zero-Based Budgeting: Modern Experiences and

Current Perspectives,” outlines approaches governments can use to

develop budgets, especially during times of fiscal distress.

Case Study Examples:

City of San Jose, California

City of Kalamazoo, Michigan

12

22

ACTION 4: PRIORITIZE GOVERNMENT SERVICES AND OPERATIONAL

REVIEWS

23

ACTION 4: PRIORITIZE GOVERNMENT SERVICES AND OPERATIONAL

REVIEWS

13

LESSON 5: PROVIDE FOR ACCOUNTABILITY IN FINANCIAL

MANAGEMENT

Revenue and expenditure policies foster a complete understanding of revenue sources

and thus provide a basis for prudent planning, but they are often missing from the critical

checklist.

Best practices promote that governments should have detailed financial management

policies in place to support sustainable and accountable organizations.

Financial planning policies which address both the need for a long-term view and the

fundamental principle of a balanced budget.

Revenue policies which seek stability to avoid potential service disruptions caused by

revenue shortfalls. Understanding the revenue stream is essential to prudent planning.

Expenditure policies lead to fiscal stability by ensuring prudent planning for

expenditures of jurisdictions, which define ongoing public service commitment.

Governments must use transparency and accountability in monitoring and reporting

financial results. In many instances, local governments have approved policies but fail to

follow them.

Finance offices need to monitor and report the outcomes of approved policies and make

adjustments as needed.

Without approved financial and management policy safeguards, there is no basis for

sustainable financial stewardship.

24

MEASURING THE FISCAL HEALTH OF LOCAL GOVERNMENTS

Expenditure Policies

Debt Capacity, Issuance, and

Management

Reserve or Stabilization Accounts

OPEB and Pension Liabilities

Cost Recovery

Business Preparedness and Continuity

Policies

Annual Budget Plan

Capital Improvements Plan

Long-Term Fiscal Forecasts

Cash Flow Plan

Contingency Plan

Fiscal Health Warning Signs

25

Financial Planning Policies

Balanced Budget

Long-Range Planning

Asset Inventory

Cash Management

Revenue Policies

Revenue Diversification

Fees and Charges

Use of One-time Revenues

Use of Unpredictable Revenues

Fund Balance

Governance & Management Practices: Examples of Financial Policies and Plans

14

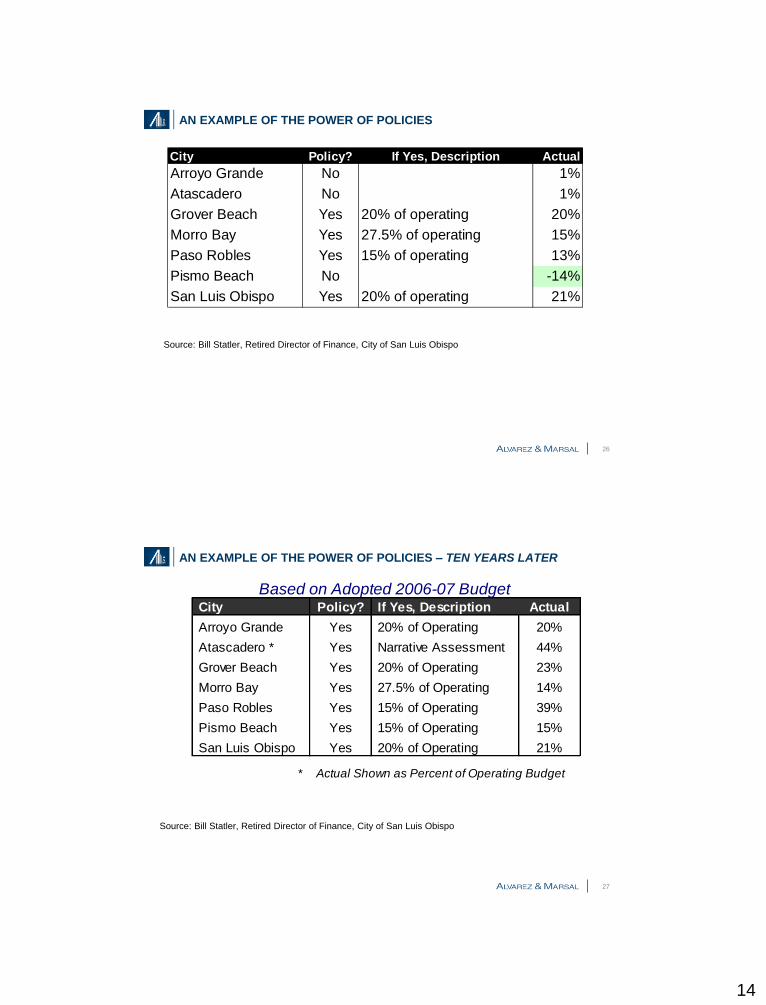

AN EXAMPLE OF THE POWER OF POLICIES

City Policy? If Yes, Description Actual

Arroyo Grande No 1%

Atascadero No 1%

Grover Beach Yes 20% of operating 20%

Morro Bay Yes 27.5% of operating 15%

Paso Robles Yes 15% of operating 13%

Pismo Beach No -14%

San Luis Obispo Yes 20% of operating 21%

Source: Bill Statler, Retired Director of Finance, City of San Luis Obispo

26

AN EXAMPLE OF THE POWER OF POLICIES – TEN YEARS LATER

City Policy? If Yes, Description Actual

Arroyo Grande Yes 20% of Operating 20%

Atascadero * Yes Narrative Assessment 44%

Grover Beach Yes 20% of Operating 23%

Morro Bay Yes 27.5% of Operating 14%

Paso Robles Yes 15% of Operating 39%

Pismo Beach Yes 15% of Operating 15%

San Luis Obispo Yes 20% of Operating 21%

* Actual Shown as Percent of Operating Budget

Based on Adopted 2006-07 Budget

Source: Bill Statler, Retired Director of Finance, City of San Luis Obispo

27

15

MEASURING THE FISCAL HEALTH OF LOCAL GOVERNMENTS

Key Financial Analyst Questions:

Does the “government” have them (policies and plans)?

Do they cover the key financial issues?

Are they reasonable?

Do they follow best practices and industry benchmarks?

Are they followed?

Are the assumptions clearly stated?

What do they do with the results?

Fiscal Health Warning Signs

28

Governance & Management Practices: Financial Policies and Plans

LESSON 6: BE WILLING TO SPEND MONEY TO SAVE MONEY

Governments sometimes need to

identify initiatives that will cut costs

and improve efficiency in the long

run.

GFOA’s Fiscal First Aid Strategies

website (www.gfoa.org) support the

notion that governments need to

make use of external resources that

create value.

The services of external industry professionals can help validate the organization’s

financial position and condition. .

29

Examples of external validation

analysis: Cash-flow analysis

Sale of assets

Efficiency reviews

OPEB and Pension analysis

Economic impact of developments

(Loss/Gain)

Labor analysis

Cost of service

Revenue and rate forecasts

Accounts receivable and write-off

analysis

Financial/operational reports &

dashboards and ratio analysis

Business process review

Shared services and smart

government operations

16

SUMMARY & CONCLUSIONS

While the actions of finance officers

do not directly affect the local

housing market, property values, or

crime rates, they can still provide

fiscal relief for their organizations by

taking immediate steps toward sound

financial management policies and

practices.

A number of best practices are

available for finance officers to use in

guiding their organizations to fiscal

stability and long-term sustainability

To navigate these turbulent times, local governments need proactive approaches and

strategies that address critical fiscal management issues.

30

Financial and Demographic ratios can

provide a snapshot of historical to

develop projections and predictive

models Sources (CAFR, Budget, CIP, Bureau of

Census, EMMA, Chamber of Commerce,

Regional Economic Forecasts and Studies,

Peer Analysis, Interviews and On-site

Visits)

Understanding of Government and

Financial Management Practices Policies

Plans

Financial Reporting

Organizational culture

Community engagement

Transparency and Accountability

Independent advise from industry

experts in government finance and

operations

QUESTIONS & DISCUSSION

31

17

A&M OVERVIEW

32

For nearly three decades, Alvarez & Marsal has set the standard for working with

organizations to tackle complex business issues, boost operating performance and maximize

stakeholder value.

About A&M Founded in 1983 by co-CEOs Tony Alvarez II and Bryan Marsal

2,200+ professionals

42 cities; 18 nations; 4 continents

300+ Managing Directors

North America New York (Global HQ)

Atlanta

Birmingham

Boston

Charlotte

Chicago

Dallas

Denver

Detroit

Houston

Kansas City

Los Angeles

Miami

Nashville

Philadelphia

Phoenix

San Antonio

San Francisco

Seattle

Toronto

Vancouver

Washington, D.C.

Europe and the Middle East London (European HQ)

Amsterdam

Athens

Dubai

Madrid

Milan

Latin America São Paulo (Latin American HQ)

Bogotá

Asia Hong Kong (Asian HQ)

Mumbai

Mexico City

Moscow

Munich

Paris

Warsaw

PUBLIC SECTOR SERVICES

33

Alvarez & Marsal helps public sector entities identify new ways to overcome challenges and

implement sustainable change – pioneering an approach based on operational and financial

improvement principles that have proven powerful in the private sector.

As the only traditional

restructuring firm with a

dedicated Public Sector

practice, A&M helps public

sector entities identify new

ways to overcome

challenges and implement

sustainable change.

A&M Public Sector

professionals – qualified

experts with an average of

20 to 25 years of

experience – have

extensive experience

managing critical

performance improvement

initiatives, combined with a

profound personal

commitment to assist

organizations in

overcoming the hurdles of

service delivery in

resource-constrained

environments.

Examples of Representative Public Sector Experience

Unified Government of Wyandotte County /

Kansas City, KS

Kansas City Board of Public Utilities

City of Leawood, KS

City of Overland Park, KS

City of Olathe, KS

City of Louisburg, KS

City of Houston, TX

City of Huntsville, TX

City of Seabrook, TX

Los Angeles Unified School District

State of Louisiana Department of Revenue

City of Stockton, CA (Creditor Representation)

City of Mammoth Lakes, CA (Creditor

Representation)

Jefferson County, AL (Creditor Representation)

City Council of Harrisburg, PA

Government of Guam (Third Party Fiduciary

Agent)

Government of U.S. Virgin Islands (Third Party

Fiduciary Agent)

New Orleans Public Schools

St. Louis Public Schools

Detroit Public Schools

District of Columbia Public Schools

New York City Department of Education

State of North Carolina – Department of HHS

State of South Carolina – Department of HHS

State of Pennsylvania – Department of Public

Welfare

State of South Carolina – Department of

Employment & Workforce

State of Alabama DOT

U.S. Army Corps of Engineers and U.S. Air

Force

Chicago Transit Authority

U.S. Environmental Protection Agency

U.S. Department of Energy

Washington DC Planning and Economic

Development

City of Jacksonville, FL

Multiple Education Focused Philanthropies

U.S. Department of Education

Maricopa County Community College District

Baltimore City Schools

City of Lees’ Summit, MO

City of Riverside, MO

City of Independence, MO

Pittsburgh, Pennsylvania Public Schools

Fairfax County, VA

City of Greenwood, MO

Charleston, South Carolina Public Schools

33

18

OUR APPROACH TO MUNICIPAL SOLVENCY & LIQUIDITY ANALYSIS

Evaluate cash flow forecast

Evaluate existing revenue estimates and

projection assumptions for all major revenue

sources

Evaluate budget spending assumptions

including proposed employee salary and

wages, employee retirement systems, other

fringe benefits, debt retirements, intra-fund

transfers, capital expenses, and other

operating expenditures

Identify opportunities for new/expanded

revenues, expenditure consolidation or deferral

and cost reduction initiatives

Identify opportunities for sale, lease or

monetization of assets

Evaluate priority of near term capital

expenditure projections

As Public Sector Financial Advisors, A&M’s bottom up approach of reviewing distressed governments

promotes an independent review of opportunities to address cash, budget, and service solvency while

striving to achieve long term sustainability

34

Determine debt capacity of the City over a

five year period and future borrowing

options

Evaluate financing plan for costs associated

with pension and post-employment health

care

Create a financial conditional assessment

based on key indicators

Compare government costs to peer entities

and industry best practices

Review financial policies to validate

compliance

Provide recommendations on financial

restructuring requirements and operational

improvements

Nancy L. Zielke, Senior Director

Alvarez & Marsal Public Sector Services

1100 Walnut Street – Suite 2970

Kansas City, Missouri 64106

Office 816.412.6511

Mobile 913.548.6245

www.alvarezandmarsal.com