due diligence: how buyers can protect themselves in purchasing a company

TRANSCRIPT

DUE DILIGENCE: HOW BUYERS CAN PROTECT THEMSELVES IN PURCHASING A COMPANY

Neil [email protected]

P. Haans [email protected]

Agenda

Overview of Process

Defining Due Diligence

Due Diligence Process• Pre-Letter of Intent • Post-Letter of Intent• Post Definitive

Agreement and Closing

Questions

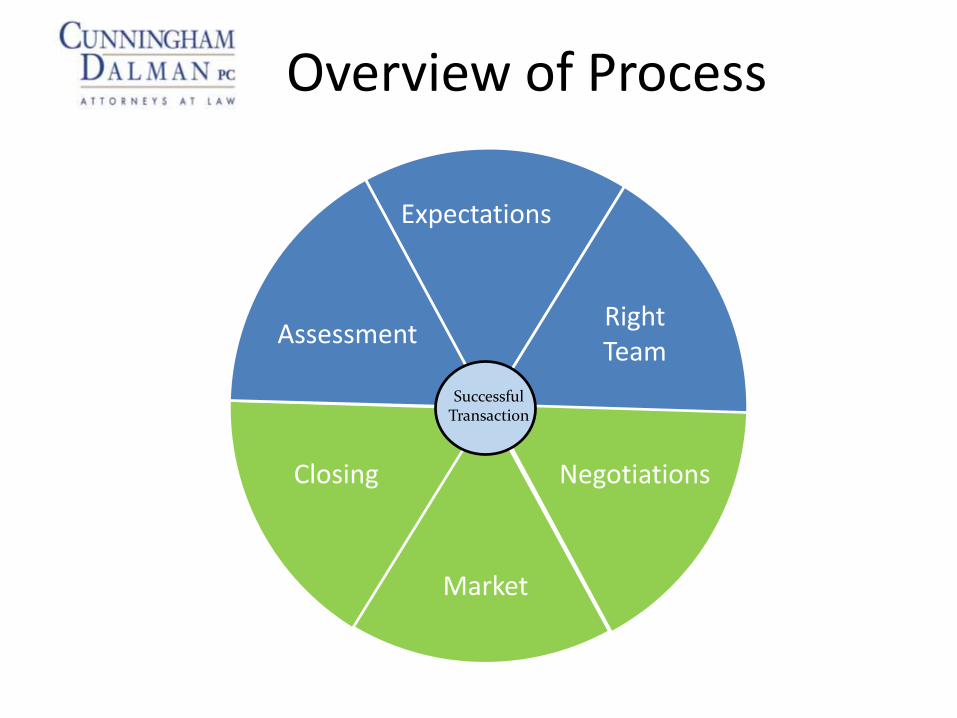

Successful Transaction

Expectations

Right Team

Negotiations

Market

Closing

Assessment

Overview of Process

1. Seller Expectations

SellerExpectations

• Summary• Same Page

SellerExpectations

2

1

3

456

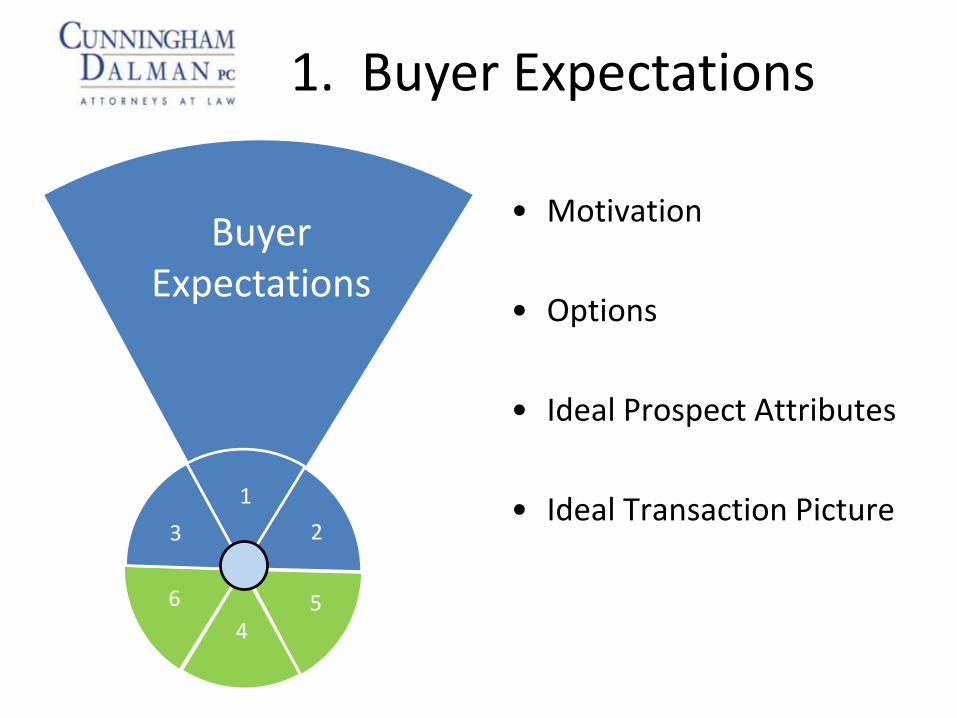

• Motivation

• Options

• Ideal Prospect Attributes

• Ideal Transaction Picture

1. Buyer Expectations

SellerExpectations

• Summary• Same Page

BuyerExpectations

2

1

3

456

• Motivation

• Options

• Ideal Prospect Attributes

• Ideal Transaction Picture

Viability of Options

Grow Organically

New Products/Services

New Markets

Gain Market Share

Grow Through Acquisitions

Buy Suppliers

Buy Customers

Buy Competitors

Buy Complimentary

Companies

Internal Sale

Family

Shareholder Buyout

Management Buyout

ESOP

External Sale

Liquidation

3rd Party

Recapitalization

Right Team• Right Seat• Right People

21

3

456

2. Right Team

3. Assessment

Assessment• Quantitative• Qualitative 2

13

456

4. Market

MarketMarketing Plan

Qualification

21

3

456

5. Negotiations

21

3

456

Negotiations• Proposal Elements• Financing Feasibility

6. Closing

Closing• 90-Day Checklist• Alignment

21

3

456

Due Diligence

What is it?

Why is it important?

How do you do it?

• Do further due diligence

• Schedule disclosures

• Negotiate a lower purchase price

• Abandon the deal

The result may be to:

Due Diligence

Due Diligence

Create a system for managing the process

Bank underwriting

Reps, warranties, and indemnification

Due Diligence Process

Pre-Letter of Intent

Post-Letter of Intent

Post Definitive Agreement and Closing

Pre-Letter of Intent

Background Information

Tax issues for transaction structure-asset v. entity purchase

Analyze sales, income/profit, cash flow, and growth potential

Pre-Letter of Intent

Confidentiality

Legal structure

• Is it an asset or entity interest purchase?

• What assets are being sold?

• Are liabilities being assumed?

• Is the seller “staying on” after the closing?

• What are “deal breakers?”

• What due diligence is vital?

Review letter of intent

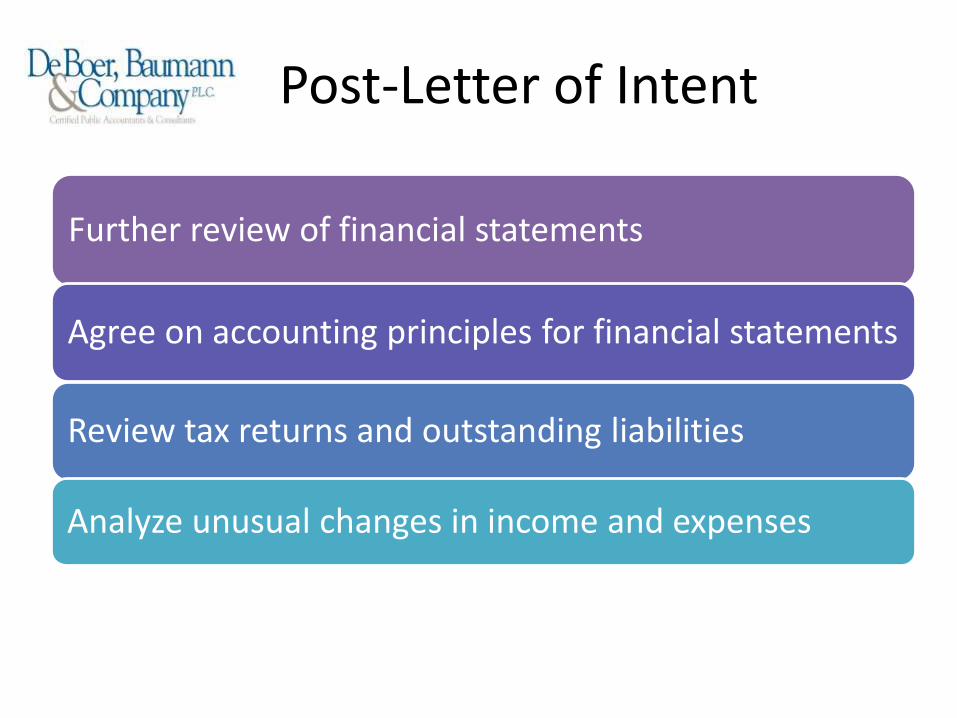

Post-Letter of Intent

Further review of financial statements

Agree on accounting principles for financial statements

Review tax returns and outstanding liabilities

Analyze unusual changes in income and expenses

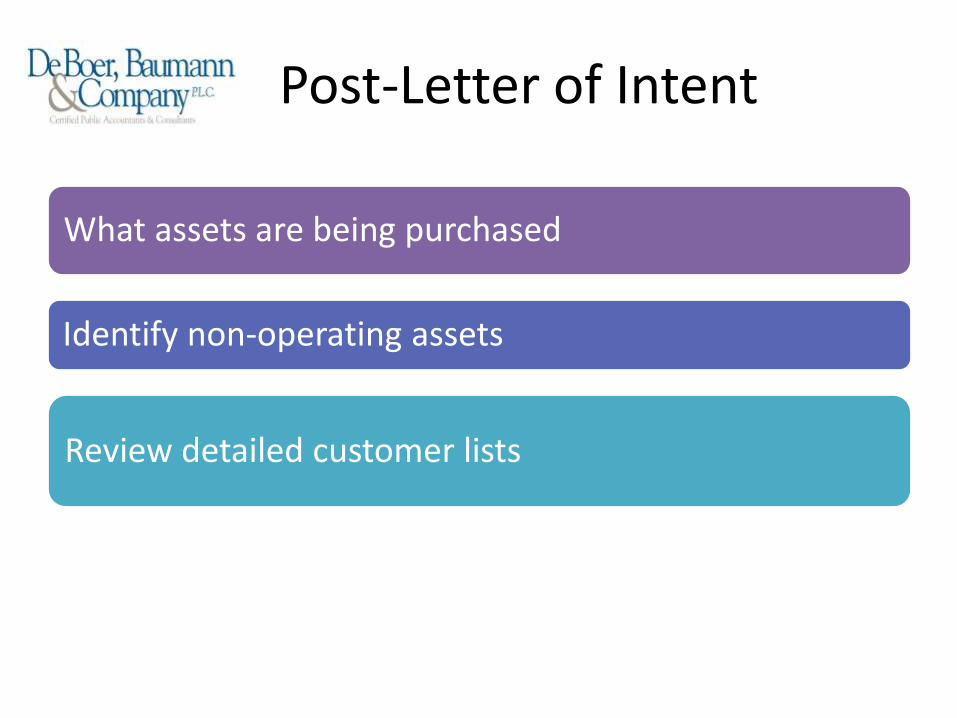

Post-Letter of Intent

What assets are being purchased

Identify non-operating assets

Review detailed customer lists

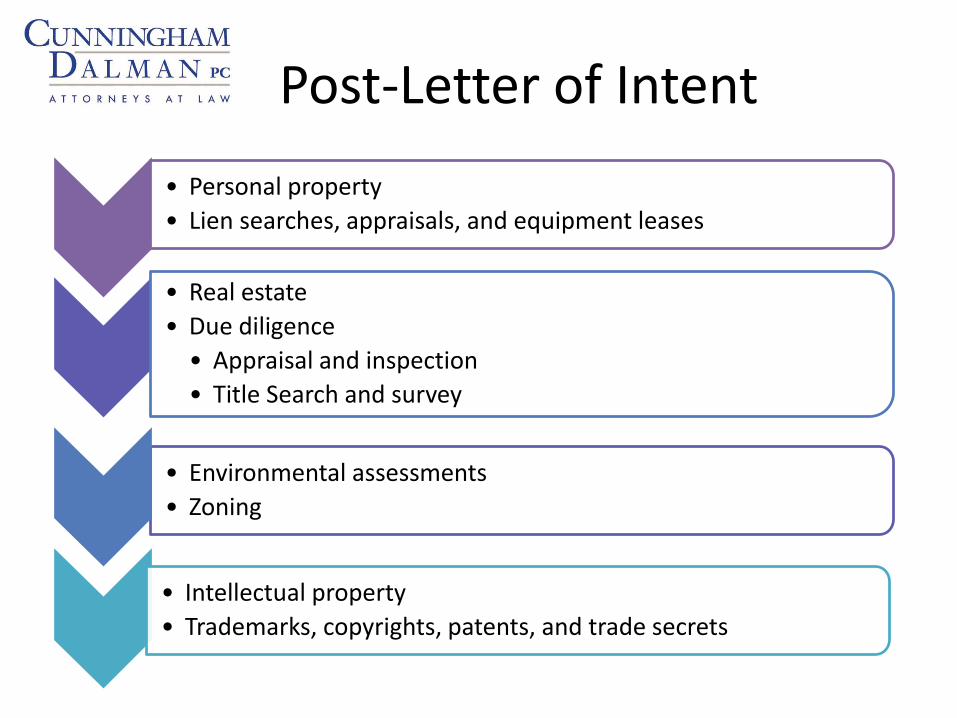

• Personal property

• Lien searches, appraisals, and equipment leases

• Environmental assessments

• Zoning

• Real estate

• Due diligence

• Appraisal and inspection

• Title Search and survey

• Intellectual property

• Trademarks, copyrights, patents, and trade secrets

Post-Letter of Intent

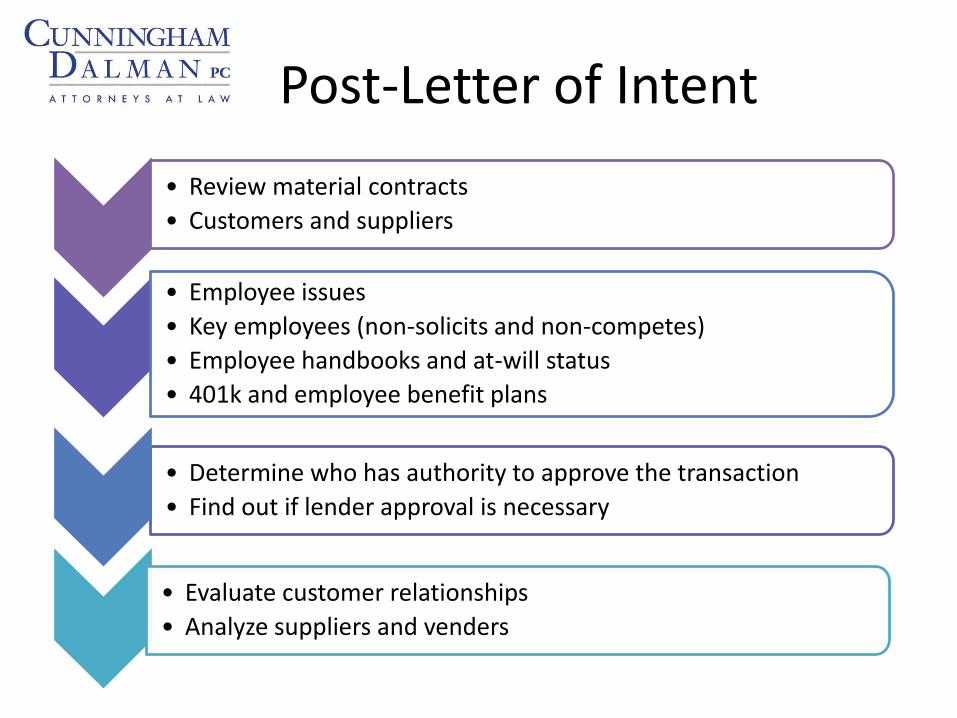

• Review material contracts

• Customers and suppliers

• Determine who has authority to approve the transaction

• Find out if lender approval is necessary

• Employee issues

• Key employees (non-solicits and non-competes)

• Employee handbooks and at-will status

• 401k and employee benefit plans

• Evaluate customer relationships

• Analyze suppliers and venders

Post-Letter of Intent

Post-Letter of Intent

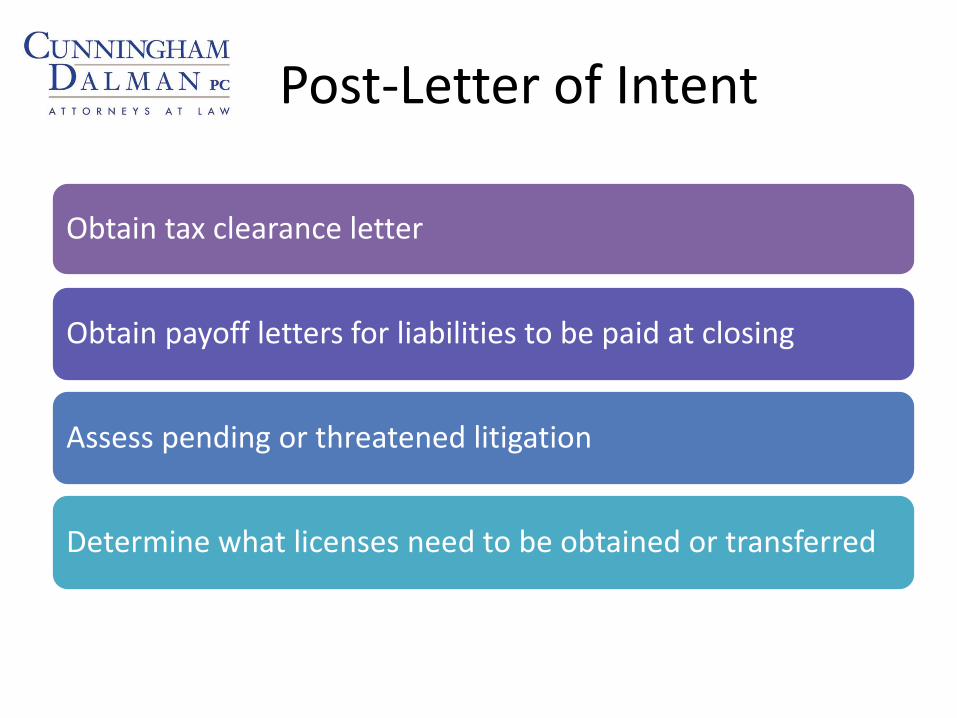

Obtain tax clearance letter

Obtain payoff letters for liabilities to be paid at closing

Assess pending or threatened litigation

Determine what licenses need to be obtained or transferred

Post Definitive Agreement and Closing

1. Inventory valuation

2. Working capital

3. Transfer titles

4. Assign intellectual property

5. Title policy issued

6.Discharges/releases for liabilities