dr. james p. gaines - narcnarc.org/uploads/jim gaines.pdf · dr. james p. gaines research economist...

TRANSCRIPT

Dr. James P. Gaines Research Economist Real Estate Center

at Texas A&M University www.recenter.tamu.edu

Publications Tierra Grande

is our quarterly magazine with

timely research and analysis of the

trends and events shaping Texas

real estate today. Experts on

appraisal, housing , finance, law,

demography, economics,

investment and other areas share

insights unavailable anywhere

else.

Planning to invest in Texas real estate? Are you

looking for local real estate market information for

Texas cities? Click here for extensive data for every

metro area in the Lone Star state. Our reports include

employment trends, population, residential, multi-

family, office, industrial and retail information.

Market Reports

http://recenter.tamu.edu

REAL ESTATE CENTER at TEXAS A&M UNIVERSITY

Mays Business School

Data Building permits

Employment

Home Sales

Housing

Affordability

Population Rural Land

RECON Newsletter You'll be an insider – if you subscribe to

our electronic newsletter RECON.

RECON is an acronym for Real Estate

Center Online News. It's a twice-weekly

briefing on Texas real estate news.

Currently more than 20,000 subscribers

worldwide are signed on. Best of all,

RECON is free. RECON

News Releases

Events

Calendar

Videos

TRECI Index

News

Happy New Year! The staff of the Real

Estate Center wish you and yours a happy

and prosperous new year! This year marks

the 35th anniversary of the Real Estate

Center. In 1971, Gov. Preston Smith signed

legislation creating the Texas Real Estate

Research Center and placed it at Texas

A&M University.

Instructor Training Courses, May 18-19,

College Station, Texas. The Legal Update

and Ethics instructor training courses

include credit for the required 3-hour Legal

Update course and the required 3-hour

Ethics course. In addition, each instructor

training course will include a brief orientation

to the teacher’s manuals for each course as

well as a discussion of training issues.

Events Calendar

We’ve Spent a Lot of Time Around the Ole Water Cooler

3

Characteristics of This Recession

4

• A 0% funds rate, $1.4 trillion budget deficit and a $2.2

trillion Fed balance sheet

• Nearly one-third of homeowners have negative equity

• 1 in 6 are either unemployed or underemployed.

• 1 in 7 homeowners either delinquent or in the foreclosure

process

• 20% - 30% slide in home prices

• 40% - 50% plunge in commercial real estate values

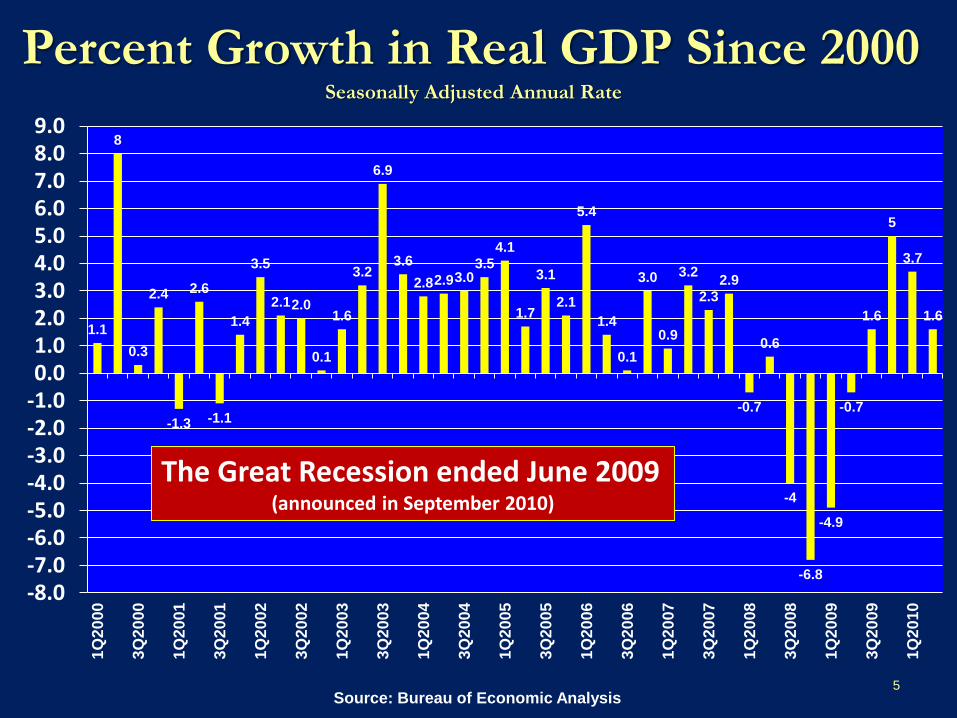

Percent Growth in Real GDP Since 2000 Seasonally Adjusted Annual Rate

1.1

8

0.3

2.4

-1.3

2.6

-1.1

1.4

3.5

2.1 2.0

0.1

1.6

3.2

6.9

3.6

2.8 2.9 3.0 3.5

4.1

1.7

3.1

2.1

5.4

1.4

0.1

3.0

0.9

3.2

2.3

2.9

-0.7

0.6

-4

-6.8

-4.9

-0.7

1.6

5

3.7

1.6

-8.0-7.0-6.0-5.0-4.0-3.0-2.0-1.00.01.02.03.04.05.06.07.08.09.0

1Q

20

00

3Q

20

00

1Q

20

01

3Q

20

01

1Q

20

02

3Q

20

02

1Q

20

03

3Q

20

03

1Q

20

04

3Q

20

04

1Q

20

05

3Q

20

05

1Q

20

06

3Q

20

06

1Q

20

07

3Q

20

07

1Q

20

08

3Q

20

08

1Q

20

09

3Q

20

09

1Q

20

10

5 Source: Bureau of Economic Analysis

The Great Recession ended June 2009 (announced in September 2010)

Personal Consumption Expenditures

Source: Department of Commerce, SAAR

6,000

7,000

8,000

9,000

10,000

11,000J

an

-00

Ma

y-0

0

Se

p-0

0

Ja

n-0

1

Ma

y-0

1

Se

p-0

1

Ja

n-0

2

Ma

y-0

2

Se

p-0

2

Ja

n-0

3

Ma

y-0

3

Se

p-0

3

Ja

n-0

4

Ma

y-0

4

Se

p-0

4

Jan

-05

Ma

y-0

5

Se

p-0

5

Ja

n-0

6

Ma

y-0

6

Se

p-0

6

Ja

n-0

7

May-0

7

Se

p-0

7

Ja

n-0

8

Ma

y-0

8

Se

p-0

8

Ja

n-0

9

Ma

y-0

9

Se

p-0

9

Ja

n-1

0

Ma

y-1

0

Se

p-1

0

Ja

n-1

1

Bil

lio

ns

of

Do

lla

rs

Personal consumption represents

about 70% of US economy and is

showing signs of recovery

Annual Employment Growth Rates

for US and Texas

-6.0

-5.0

-4.0

-3.0

-2.0

-1.0

0.0

1.0

2.0

3.0

4.0

5.0

Jan

-01

Ma

y-0

1

Sep

-01

Jan

-02

Ma

y-0

2

Sep

-02

Jan

-03

Ma

y-0

3

Sep

-03

Jan

-04

Ma

y-0

4

Sep

-04

Jan

-05

Ma

y-0

5

Sep

-05

Jan

-06

Ma

y-0

6

Sep

-06

Jan

-07

Ma

y-0

7

Sep

-07

Jan

-08

Ma

y-0

8

Sep

-08

Jan

-09

Ma

y-0

9

Sep

-09

Jan

-10

Ma

y-1

0

Sep

-10

Jan

-11

7

Texas

US

Source: BLS

Measures of Un- and Underemployment

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

8 Source: BLS

Percent SA

U-6, the broadest measure

Headline Rate Texas

Unemployment Rate by Level of Education June 2010

14.1

10.8

8.2

4.4

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

18.0

No High SchoolDiploma

High School Diploma Some College College Degree+

2008 2009 Current

9 Source: BLS , 25-years old +; Seasonally adjusted rates

Even Universities Laying People Off , Faculty Are Taking Whatever Jobs They find

Are There Secular Changes Going On

Given Economy, Credit Collapse and

Household Net Worth Implosion?

• Debt vs. Savings

– Credit Contraction & Thrift

• Discretionary spending patterns

– Marginal spending vs. savings in period

of declining personal income

• Homeownership

– Maybe everyone doesn’t need to own a

home

• Deflationary vs. Inflationary Expectations 11

Monthly Core Inflation Rate (CPI Minus Food & Energy)

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

Jan

-96

Ap

r-96

Ju

l-96

Oct-

96

Jan

-97

Ap

r-97

Ju

l-97

Oct-

97

Jan

-98

Ap

r-98

Ju

l-98

Oct-

98

Jan

-99

Ap

r-99

Ju

l-99

Oct-

99

Jan

-00

Ap

r-00

Ju

l-00

Oct-

00

Jan

-01

Ap

r-01

Ju

l-01

Oct-

01

Jan

-02

Ap

r-02

Ju

l-02

Oct-

02

Jan

-03

Ap

r-03

Ju

l-03

Oct-

03

Jan

-04

Ap

r-04

Ju

l-04

Oct-

04

Jan

-05

Ap

r-05

Ju

l-05

Oct-

05

Jan

-06

Ap

r-06

Ju

l-06

Oct-

06

Jan

-07

Ap

r-07

Ju

l-07

Oct-

07

Jan

-08

Ap

r-08

Ju

l-08

Oct-

08

Jan

-09

Ap

r-09

Ju

l-09

Oct-

09

Jan

-10

Ap

r-10

Ju

l-10

Oct-

10

Jan

-11

12

Source: Bureau of Labor Statistics Yr/Yr Rate of Change in the Monthly Index, US Urban, All Items

Deflationary pressures building for short-term;

long-term may be another matter

Summary

13

• American Consumers are fixing their balance sheet

and returning to the stores.

• American businesses have right-sized and returned to

profitability.

• Business owners are still frozen with uncertainty and

sitting on cash.

• States, cities, counties and school districts will have to

right-size their spending.

• Federal policies may create long-term problems with

tighter credit and higher taxes.

• The “extend and pretend” gambit in the banking

system will retard growth until it’s resolved.

• Housing not leading US economy out of recession

Wow, back in 1990, the Government

seized the Mustang Ranch brothel in

Nevada for tax evasion and, as

required by law, tried to run it.

They failed, and it closed.

A Thought from Maxine "BAIL EM OUT! ????”

Now we are trusting the auto industry, the

banking system and healthcare to the

same nit-wits who couldn't make money

running a whore house and selling

whiskey! 14

15

The Housing Market

Current Housing Issues

• Tax credit limited impact

• Lower demand, foreclosures and homebuilder

concessions depressing home prices

• Foreclosures still major concern nationally

• Appraisals are major issue in purchases

• Lenders making mortgages difficult to obtain

• ADC loans virtually non-existent in most of the

country

• Lowest mortgage rates in 50 years, no help

• Affordability operative market word

16

17

Bentley's First Law of Economics: The only

thing more dangerous than an economist is

an amateur economist!

Bentley's Second Law of Economics :

"The only thing more dangerous than an

amateur economist is a professional

economist."

Lost Wealth: Households’ Equity in Real

Estate 2005, $13,139

2Q2010, $6,968

0

2,000

4,000

6,000

8,000

10,000

12,000

14,00019

55

19

561

957

19

581

959

196

01

961

19

621

963

19

6419

65

19

661

967

19

681

969

197

01

971

19

721

973

19

7419

75

19

761

977

19

781

979

19

801

981

19

821

983

19

841

985

19

861

987

19

881

989

19

901

991

19

921

993

19

941

995

19

961

997

19

981

999

20

002

001

20

022

003

20

042

005

20

062

007

20

082

009

2Q2

01

0

Bill

ion

s $

Source: Federal Reserve, Flow of Funds, B-100

$6.2 trillion or 47% in lost real estate equity

19

62.0

63.0

64.0

65.0

66.0

67.0

68.0

69.0

70.0

2Q

197

1

2Q

197

2

2Q

197

3

2Q

197

4

2Q

197

5

2Q

197

6

2Q

1977

2Q

197

8

2Q

197

9

2Q

198

0

2Q

198

1

2Q

198

2

2Q

198

3

2Q

198

4

2Q

198

5

2Q

198

6

2Q

198

7

2Q

198

8

2Q

198

9

2Q

199

0

2Q

199

1

2Q

199

2

2Q

199

3

2Q

199

4

2Q

199

5

2Q

199

6

2Q

199

7

2Q

199

8

2Q

199

9

2Q

2000

2Q

200

1

2Q

200

2

2Q

200

3

2Q

200

4

2Q

200

5

2Q

200

6

2Q

200

7

2Q

200

8

2Q

200

9

2Q

2010

US Homeownership Rate

Source: US Census Bureau; FHLMC (4-quarter moving average homeownership rate)

1970s

Baby Boomers enter

market;

homeownership grows 1995-2005

Low interest

rates and new

mortgage

products;

Homeownership

explodes

(Percent)

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

18.0

20.0

22.0

24.0

26.0

28.0

30.01Q

1998

2Q

1998

3Q

1998

4Q

1998

1Q

1999

2Q

1999

3Q

1999

4Q

1999

1Q

2000

2Q

2000

3Q

2000

4Q

2000

1Q

2001

2Q

2001

3Q

2001

4Q

2001

1Q

2002

2Q

2002

3Q

2002

4Q

2002

1Q

2003

2Q

2003

3Q

2003

4Q

2003

1Q

2004

2Q

2004

3Q

2004

4Q

2004

1Q

2005

2Q

2005

3Q

2005

4Q

2005

1Q

2006

2Q

2006

3Q

2006

4Q

2006

1Q

2007

2Q

2007

3Q

2007

4Q

2007

1Q

2008

2Q

2008

3Q

2008

4Q

2008

1Q

2009

2Q

2009

3Q

2009

4Q

2009

1Q

2010

2Q

2010

Pe

rce

nt

of

Lo

an

s

Source: Mortgage Bankers Association, National Delinquency Survey

US Mortgage Delinquency Rates

All Mortgages

Prime Mortgages

Subprime Mortgages

US mortgage delinquency rate set all

time high in 4Q2009

Monthly Foreclosure Filings

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

90,000

100,000

110,000

120,000

130,000

140,000

150,000

160,000J

un

-05

Au

g-0

5

Oct-

05

De

c-0

5

Fe

b-0

6

Ap

r-06

Ju

n-0

6

Au

g-0

6

Oct-

06

De

c-0

6

Fe

b-0

7

Ap

r-07

Ju

n-0

7

Au

g-0

7

Oct-

07

De

c-0

7

Fe

b-0

8

Ap

r-08

Ju

n-0

8

Au

g-0

8

Oct-

08

De

c-0

8

Fe

b-0

9

Ap

r-09

Ju

n-0

9

Au

g-0

9

Oct-

09

De

c-0

9

Fe

b-1

0

Ap

r-10

Ju

n-1

0

Au

g-1

0

US

Texas

Source: RealtyTrac, Inc. Data include Notices of Trustee Sales plus Notices of Foreclosure Sale

21

Texas foreclosures have been

far more stable than US

Foreclosure Filings and the U.S.

Unemployment Rate

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

9.0

10.0

11.0

0

15,000

30,000

45,000

60,000

75,000

90,000

105,000

120,000

135,000

150,000

165,000

180,000J

an

-06

Ma

r-0

6

Ma

y-0

6

Ju

l-06

Sep

-06

No

v-0

6

Jan

-07

Ma

r-0

7

Ma

y-0

7

Ju

l-07

Sep

-07

No

v-0

7

Jan

-08

Ma

r-0

8

Ma

y-0

8

Ju

l-08

Sep

-08

No

v-0

8

Jan

-09

Ma

r-0

9

Ma

y-0

9

Ju

l-09

Sep

-09

No

v-0

9

Jan

-10

Ma

r-1

0

Ma

y-1

0

Ju

l-10

Un

em

plo

ym

en

t R

ate

Fo

rec

los

ure

Filin

gs

22 Sources: BLS, RealtyTrac, Inc. Foreclosure Filings include Notices of Trustee Sales plus Notices of Foreclosure Sale

23

$75,000

$100,000

$125,000

$150,000

$175,000

$200,000

$225,000

$250,000

Ja

n-9

0

Ju

l-90

Ja

n-9

1

Ju

l-91

Ja

n-9

2

Ju

l-92

Ja

n-9

3

Ju

l-93

Ja

n-9

4

Ju

l-94

Ja

n-9

5

Ju

l-95

Ja

n-9

6

Ju

l-96

Ja

n-9

7

Ju

l-97

Ja

n-9

8

Ju

l-98

Ja

n-9

9

Ju

l-99

Ja

n-0

0

Ju

l-00

Ja

n-0

1

Ju

l-01

Ja

n-0

2

Ju

l-02

Ja

n-0

3

Ju

l-03

Ja

n-0

4

Ju

l-04

Ja

n-0

5

Ju

l-05

Ja

n-0

6

Ju

l-06

Ja

n-0

7

Ju

l-07

Ja

n-0

8

Ju

l-08

Ja

n-0

9

Ju

l-09

Ja

n-1

0

Ju

l-10

Source: NAR, Real Estate Center at Texas A&M University

US Median Home Prices Since 1990

National House Price Bubble

12-Month Moving Average

Since 2001

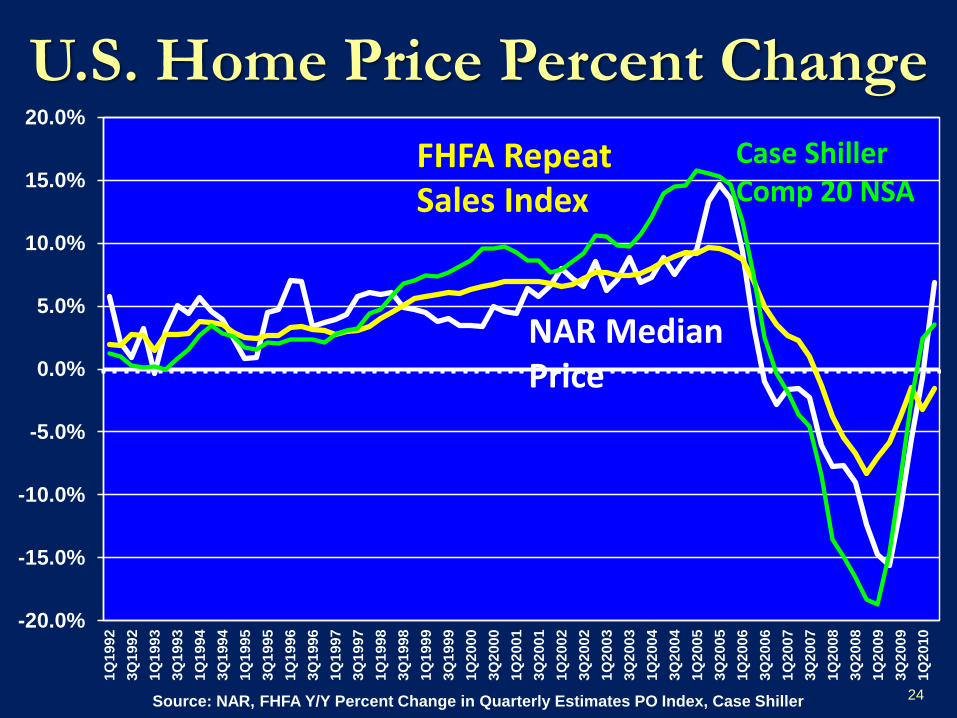

U.S. Home Price Percent Change

-20.0%

-15.0%

-10.0%

-5.0%

0.0%

5.0%

10.0%

15.0%

20.0%1Q

1992

3Q

1992

1Q

1993

3Q

19

93

1Q

1994

3Q

1994

1Q

1995

3Q

1995

1Q

1996

3Q

1996

1Q

1997

3Q

1997

1Q

1998

3Q

1998

1Q

1999

3Q

1999

1Q

2000

3Q

2000

1Q

2001

3Q

2001

1Q

2002

3Q

2002

1Q

2003

3Q

2003

1Q

2004

3Q

2004

1Q

2005

3Q

2005

1Q

2006

3Q

2006

1Q

20

07

3Q

2007

1Q

2008

3Q

2008

1Q

2009

3Q

2009

1Q

2010

24 Source: NAR, FHFA Y/Y Percent Change in Quarterly Estimates PO Index, Case Shiller

FHFA Repeat Sales Index

NAR Median Price

Case Shiller Comp 20 NSA

National Housing Affordability Index

Feb-99, 146.9

Jul-00, 122.8

Apr-03, 145.4

Jul-06, 99.6

Apr-09, 184

90

100

110

120

130

140

150

160

170

180

190

Jan

-94

Ju

l-9

4

Jan

-95

Ju

l-9

5

Jan

-96

Ju

l-96

Jan

-97

Ju

l-9

7

Jan

-98

Ju

l-9

8

Jan

-99

Ju

l-9

9

Jan

-00

Ju

l-0

0

Jan

-01

Ju

l-0

1

Jan

-02

Ju

l-0

2

Jan

-03

Ju

l-0

3

Jan

-04

Ju

l-0

4

Jan

-05

Ju

l-0

5

Jan

-06

Ju

l-0

6

Jan

-07

Ju

l-0

7

Jan

-08

Ju

l-0

8

Jan

-09

Ju

l-0

9

Jan

-10

Ju

l-1

0

Jan

-11

25 Source: NAR Composite Index

Average 1994-2003 = 132.4

Drop of 31.5% from

April 2003 to July

2006

Existing Home Sales

1567 1593 1613

2021

2254 2334 2273

2480

3066

3646

3987 3828

2972

2418

1990

2684 2817

3122

3478 3428 3483

3010 2914 2885

3150

3427 3544 3519

3797 3964

4495 4651 4604

4733

4,974

5,443

5,959

6,179

5,677

4,939

4,350

4,566

0

1,000

2,000

3,000

4,000

5,000

6,000

7,0001

96

8

196

9

197

0

197

1

197

2

197

3

197

4

197

5

197

6

197

7

197

8

197

9

198

0

198

1

198

2

198

3

198

4

198

5

198

6

198

7

198

8

198

9

199

0

199

1

199

2

199

3

199

4

199

5

199

6

199

7

199

8

199

9

200

0

200

1

200

2

200

3

200

4

200

5

200

6

200

7

200

8

200

9

Tho

usa

nd

s

26 Source: NAR

1978-1982 sales declined 50%

2005-2009YTD sales down 34%

27

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000Jan

-95

Ju

l-95

Jan

-96

Ju

l-96

Jan

-97

Ju

l-97

Jan

-98

Ju

l-98

Jan

-99

Ju

l-99

Jan

-00

Ju

l-00

Jan

-01

Ju

l-01

Jan

-02

Ju

l-02

Jan

-03

Ju

l-03

Jan

-04

Ju

l-04

Jan

-05

Ju

l-05

Jan

-06

Ju

l-06

Jan

-07

Ju

l-07

Jan

-08

Ju

l-08

Jan

-09

Ju

l-09

Jan

-10

Ju

l-10

Jan

-11

Sources: US Census Bureau , NAR, NAHB, NBER

(000s)

Existing SF sales are down 21% from 2005 peak

New SF sales are down 78% from 2005 peak

New and Existing SF Home Sales U.S.

Average Annual Home Sales:

Years New Homes Existing Homes

1990-1997 650,000 3.4 million

1998-2002 900,000 4.7 million

2003-2007 1,078,000 5.7 million

2008- 2009 428,000 4.45 million

Months Inventory of New and

Existing Homes 12.1

11.0

3.0

4.0

5.0

6.0

7.0

8.0

9.0

10.0

11.0

12.0

13.0

Jan

-00

Ap

r-00

Ju

l-00

Oct-

00

Jan

-01

Ap

r-01

Ju

l-01

Oct-

01

Jan

-02

Ap

r-02

Ju

l-02

Oct-

02

Jan

-03

Ap

r-03

Ju

l-03

Oct-

03

Jan

-04

Ap

r-04

Ju

l-04

Oct-

04

Jan

-05

Ap

r-05

Ju

l-05

Oct-

05

Jan

-06

Ap

r-06

Ju

l-06

Oct-

06

Jan

-07

Ap

r-07

Ju

l-07

Oct-

07

Jan

-08

Ap

r-08

Ju

l-08

Oct-

08

Jan

-09

Ap

r-09

Ju

l-09

Oct-

09

Jan

-10

Ap

r-10

Ju

l-10

Oct-

10

Jan

-11

New Homes Existing Homes

28

Sources: US Census Bureau , NAR, NAHB (SAAR)

29

560 565 575

461 488 490

449

486

657

718

633

519

550

647

820 818

709

545

436 413

622 639

688

748

672 675 650

535 507

608

666 670 665

758

805

885 881 877

909

972

1,088

1,203

1,283

1,051

776

485

375

338

200

300

400

500

600

700

800

900

1,000

1,100

1,200

1,300

1,4001

96

3

196

4

196

5

196

6

196

7

196

8

196

9

197

0

197

1

197

2

197

3

197

4

197

5

197

6

197

7

197

8

197

9

198

0

198

1

198

2

198

3

198

4

198

5

198

6

198

7

198

8

198

9

199

0

199

1

199

2

199

3

199

4

199

5

199

6

199

7

199

8

199

9

200

0

200

1

200

2

200

3

200

4

200

5

200

6

200

7

200

8

200

9

201

0p

Annual New Home Sales

Source: US Census Bureau, NAHB, Real Estate Center

(000, SAAR)

Average Annual Sales by Decade:

60s 513

70s 656

80s 609

90s 698

00-06 1,055

07-09 533 -50% 1977

Peak to Trough

-32% 1986

Peak to Trough

-74% 2005 Peak

to Current

Trough

-28% 1972

Peak to Trough

NAHB HMI and Housing Starts

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

0

10

20

30

40

50

60

70

80

90

100J

an

-85

Jan

-86

Jan

-87

Jan

-88

Jan

-89

Jan

-90

Jan

-91

Jan

-92

Jan

-93

Jan

-94

Jan

-95

Jan

-96

Jan

-97

Jan

-98

Jan

-99

Jan

-00

Jan

-01

Jan

-02

Jan

-03

Jan

-04

Jan

-05

Jan

-06

Jan

-07

Jan

-08

Jan

-09

Jan

-10

Sta

rts

(00

0’s

SA

)

HM

I

Housing Market Index Single-Family Starts

30 Source: NAHB, Census Bureau, Real Estate Center at Texas A&M University

Median New Home Price

$160,000

$180,000

$200,000

$220,000

$240,000

$260,000

$280,000

Jan

-00

Ju

l-00

Jan

-01

Ju

l-01

Jan

-02

Ju

l-02

Jan

-03

Ju

l-03

Jan

-04

Ju

l-04

Jan

-05

Ju

l-05

Jan

-06

Ju

l-06

Jan

-07

Ju

l-07

Jan

-08

Ju

l-08

Jan

-09

Ju

l-09

Jan

-10

Ju

l-10

31 Source: US Census Bureau, NAHB

12-Month

Moving Average

Median new home price

is about the same as

around January 2004

Number of Housing Units Vacant

and Held Off Market “Other”

2,000

2,200

2,400

2,600

2,800

3,000

3,200

3,400

3,600

3,800

4,0001

Q1

990

3Q

19

90

1Q

19

91

3Q

19

91

1Q

19

92

3Q

19

92

1Q

19

93

3Q

19

93

1Q

19

94

3Q

19

94

1Q

19

95

3Q

19

95

1Q

19

96

3Q

19

96

1Q

19

97

3Q

19

97

1Q

19

98

3Q

19

98

1Q

19

99

3Q

19

99

1Q

20

00

3Q

20

00

1Q

20

01

3Q

20

01

1Q

20

02

3Q

20

02

1Q

20

03

3Q

20

03

1Q

20

04

3Q

20

04

1Q

20

05

3Q

20

05

1Q

20

06

3Q

20

06

1Q

20

07

3Q

20

07

1Q

20

08

3Q

20

08

1Q

20

09

3Q

20

09

1Q

20

10

Tho

usa

nd

s

32 Source: US Census Bureau, Quarterly Estimates of the Total Housing Inventory for the United States: 1965-Present

Maybe only part of the “shadow inventory”

Has the Housing Market

Bottomed? Answer: maybe… hopefully … probably. But we

will not really know for sure for some time.

Can the market sustain itself without massive Federal

government help

Defaults and foreclosures will stay high.

The health of the housing market, nationally and locally,

depends on a general economic recovery.

The housing market may have bottomed out, but

probably a long, slow recovery – think 5 to 10 years, not

just one or two.

33

Texas – Poised for a 21st

Century Boom

• Population and Economic growth

• Low cost, available labor

• Pro Growth Attitude

• Migration into State from elsewhere

• Attractive Retirement Area

• Pressure on infrastructure, government services, public finance

• Most affordable state for land, housing and overall cost of living

34

35

South Padre Island 2050

2000 – 2009 States with

Population Increases > 1 million

Source: U.S. Census Bureau Table 4: Cumulative Estimates of the Components of Resident Population Change for the United States, Regions, States, and

Puerto Rico: April 1, 2000 to July 1, 2009 36

State Population

Increase Percent Increase

2009 Population

Texas 3,930,484 18.8% 24,782,302

California 3,090,016 9.1% 36,961,664

Florida 2,555,130 16.0% 18,537,969

Georgia 1,642,430 20.1% 9,829,211

Arizona 1,465,171 28.6% 6,595,778

North

Carolina 1,334,478 16.6% 9,380,884

2000 – 2009 States with Population

Increases > 1 million

State

Total Population

Increase Natural Foreign

Immigration Domestic

Immigration

Texas 3,930,484 2,124,124 933,083 848,702

California 3,090,016 2,878,482 1,816,633 -1,509,708

Florida 2,555,130 479,586 851,260 1,182,974

Georgia 1,642,430 684,445 281,998 567,135

Arizona 1,465,171 464,238 272,410 714,354

North

Carolina 1,334,478 457,927 214,573 675,016

37

Source: U.S. Census Bureau

Texas Urban Triangle

38

In 2007, 15.3

million people,

about 90% of

the total

population in

the area, lived

in the four

principal metro

areas in the

triangle

By 2040, 33.7

million people

will live in the

four principal

metro areas in

the triangle, a

120% increase

58,410 square

miles

Source: Department of Landscape Architecture and Urban Planning, Texas A&M University

Percent Growth 1980-1990

Source: Texas State Data Center, Office of the State Demographer

Percent Growth 1990-2000

Source: Texas State Data Center, Office of the State Demographer

Percent Growth 2000-2008

Source: Texas State Data Center, Office of the State Demographer

Percent Change in Metropolitan and

Micropolitan Areas: 2000 - 2009

42 Source: U.S. Census Bureau, Population Change in Central and Outlying Counties of

Metropolitan Statistical Areas: 2000 to 2007, June 2009.

The Texas Urban Triangle

Projected Percent Growth 2008-2040

43

Source: Texas State Data Center, Office of the State Demographer

Projected Population by County 2040

44

2040 Population

P_40

36 - 1000

1001 - 10000

10001 - 50000

50001 - 100000

100001 - 500000

500001 - 1000000

1000001 - 8000000

Source: Texas State Data Center, Office of the State Demographer

45

20,852

22,811

24,782

31,831

37,285

41,118

15,000

20,000

25,000

30,000

35,000

40,000

45,00020

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

. .

.

20

10

20

10

20

10

20

15

20

15

20

15

20

20

20

20

20

20

20

25

20

25

20

25

20

30

20

30

20

30

Source: U.S. Census Bureau, Texas State Demographer 2008 Projections

(000s)

Projected Texas Population 2000 - 2030

At 50% 1990-2000 rate of immigration

At 2000-2007 rate of immigration

At 100% 1990-2000 rate of immigration

Between 9 and 18 million more

residents between 2005 and 2030

46

Averaging the projections results in an

increase of 13.9 million people by 2030.

another 12-county Dallas-Ft.

Worth metropolitan area, plus

another 10-county Houston metropolitan area, plus

another 8-county San Antonio metropolitan area, plus

Over the next 25 years, equivalent of adding:

another Corpus Christi

Percent of Total Texas Population by Race Anglo and Hispanic Proportions Reverse by 2030

53.1%

49.5%

45.9%

42.4%

39.0%

35.7%

32.5%

11

.6%

11

.4%

11

.2%

10

.8%

10

.5%

10

.0%

9.5

%

3.3

%

3.8

%

4.3

%

4.9

%

5.4

%

6.1

%

6.7

%

0%

10%

20%

30%

40%

50%

60%

2000 2005 2010 2015 2020 2025 2030

Anglo Black Hispanic Other

Source: Texas State Data Center and Demographer, Average of Projections

48

Age Distribution of the United States 2005-2030

500,000

1,000,000

1,500,000

2,000,000

2,500,000

3,000,000

3,500,000

4,000,000

4,500,000

5,000,000

5,500,000

6,000,000

6,500,000

7,000,000

7,500,000

0 5

10

15

20

25

30

35

40

45

50

55

60

65

70

75

80

85

+

Boomers 41-59 2005

500,000

1,000,000

1,500,000

2,000,000

2,500,000

3,000,000

3,500,000

4,000,000

4,500,000

5,000,000

5,500,000

6,000,000

6,500,000

7,000,000

7,500,000

0 5

10

15

20

25

30

35

40

45

50

55

60

65

70

75

80

85

+

Age

Boomers 46-64 2010

500,000

1,000,000

1,500,000

2,000,000

2,500,000

3,000,000

3,500,000

4,000,000

4,500,000

5,000,000

5,500,000

6,000,000

6,500,000

7,000,000

7,500,000

0 5

10

15

20

25

30

35

40

45

50

55

60

65

70

75

80

85+

Age

Boomers 56-74 2020

500,000

1,000,000

1,500,000

2,000,000

2,500,000

3,000,000

3,500,000

4,000,000

4,500,000

5,000,000

5,500,000

6,000,000

6,500,000

7,000,000

7,500,000

0 5

10

15

20

25

30

35

40

45

50

55

60

65

70

75

80

85+

Age

2030 Boomers 66-84

49

Texas Age Distribution 2005-2030

0

50,000

100,000

150,000

200,000

250,000

300,000

350,000

400,000

450,000

500,000

550,000

600,000

650,000

0 5

10

15

20

25

30

35

40

45

50

55

60

65

70

75

80

85+

Age

Boomers

0

50,000

100,000

150,000

200,000

250,000

300,000

350,000

400,000

450,000

500,000

550,000

600,000

650,000

0 5

10

15

20

25

30

35

40

45

50

55

60

65

70

75

80

85+

Age

Boomers

0

50,000

100,000

150,000

200,000

250,000

300,000

350,000

400,000

450,000

500,000

550,000

600,000

650,000

0 5

10

15

20

25

30

35

40

45

50

55

60

65

70

75

80

85+

Age

2020 Boomers

0

50,000

100,000

150,000

200,000

250,000

300,000

350,000

400,000

450,000

500,000

550,000

600,000

650,000

0 5

10

15

20

25

30

35

40

45

50

55

60

65

70

75

80

85

+

Age

2030 Boomers

2005 2010

Educational Attainment (%) of Adults

Age 25+, Texas vs. Rest of the US

4.3%

10.3%

28.8% 28.8%

17.5%

10.3% 8.6%

11.8%

25.4%

28.8%

17.1%

8.3%

0.0

0.1

0.1

0.2

0.2

0.3

0.3

0.4

Rest of US Texas

Source: American Community Survey 2008

Projected Percent of Labor Force by Educational

Attainment in Texas, 2000 and 2040

* Proj ections are shown for the 1.0 scenario

18.8

29 28.7

18.2

5.3

30.128.7

23.9

12.9

4.4

No High

School Diploma

High School

Graduate

Some

College

Bachelor's

Degree

Graduate/Prof.

Degree

0

5

10

15

20

25

30

35

Percent

2000 2040

Source: Texas State Data Center, Office of the State Demographer

Dr. James P. Gaines Research Economist Real Estate Center

at Texas A&M University www.recenter.tamu.edu