dr. cpa, cs. jt nyangenya, ph.d managing partner, jt ... · jt nyangenya, ph.d jt nyangenya &...

TRANSCRIPT

INTERNAL AUDITORS FORUM

2ND FEBRUARY 2018

Dr. CPA, CS. JT Nyangenya, Ph.D

JT Nyangenya & Associates.

INTERNAL AUDITORS FORUM

FEBRUARY 2018

Dr. CPA, CS. JT Nyangenya, Ph.DManaging Partner,

JT Nyangenya & Associates.

FINANCIAL STATEMENT FRAUD

OR

FRAUDULENT FINANCIAL REPORTING

FINANCIAL STATEMENT FRAUD

FRAUDULENT FINANCIAL REPORTING

PRESENATION OUTLINE

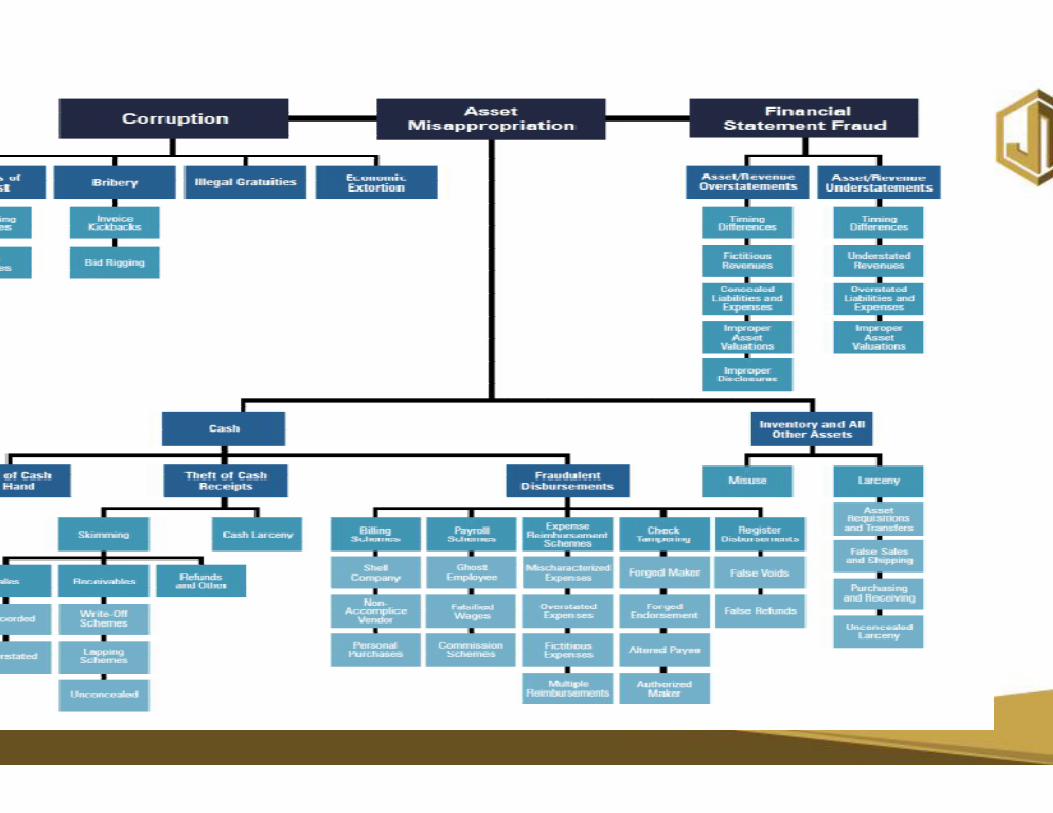

1. Fraud Tree2. Breakdown of Major Accounting3. Financial Mis - Statement Fraud4. Fraud Theory5. Recognize the most common

schemes6. Identify the red flags of financial7. Understand the fraud implications

financial reporting

PRESENATION OUTLINE

Accounting ScandalsFraud Definition

common financial statement fraud

financial statement fraudimplications of emerging issues in

ANANIAS AND SAPPHIRA New International Version (NIV)]

Now a man named Ananias, togetheralso sold a piece of property. 2 Withkept back part of the money forand put it at the apostles’ feet.

Then Peter said, “Ananias, howyour heart that you have lied to theyourself some of the money youbelong to you before it was sold?the money at your disposal? What

thing? You have not lied just to

ANANIAS AND SAPPHIRA – [Acts 5:1-11 New International Version (NIV)]

together with his wife Sapphira,With his wife’s full knowledge

for himself, but brought the rest

how is it that Satanhas so filledthe Holy Spirit and have kept forreceived for the land? 4 Didn’t

sold? And after it was sold, wasn’tWhat made you think of doing such

to human beings but to God.”

DEFINITIONSFinancial statement frauds is the

the financial conditions ofthrough the intentional misstatement

disclosures in the financial statementsstatement usersAccording to a study conductedCertified Fraud Examinersstatement accounts for approximatelyconcerning white collar crimecorruption tend to occur at a muchfinancial impact of these latter

the deliberate misrepresentationof an enterprise accomplished

misstatement or omission of amountsstatements to deceive financial

conducted by the Association(ACFE), fraudulent financial

approximately 10% of incidentscrime. Asset misappropriation and

much greater frequency, yetcrimes is much less severe.

Financial Statement Fraud Defined

Deliberate misstatements ordisclosures of financial statementsstatement users, particularly

Falsification, alteration, orfinancial records, supportingtransactions

Financial Statement Fraud Defined

or omissions of amounts orstatements to deceive financial

investors and creditors

manipulation of materialsupporting documents, or business

Defining Financial Statement Fraud

Material intentional omissionsevents, transactions, accounts,information from which financialDeliberate misapplication ofand procedures used to measure,disclose economic events andIntentional omissions of disclosuresinadequate disclosures regardingpolicies and related financial

Defining Financial Statement Fraud

omissions or misrepresentationsaccounts, or other significant

financial statements are preparedaccounting principles, policies,

measure, recognize, report, andand business transactionsdisclosures or presentation

regarding accounting principles andamounts

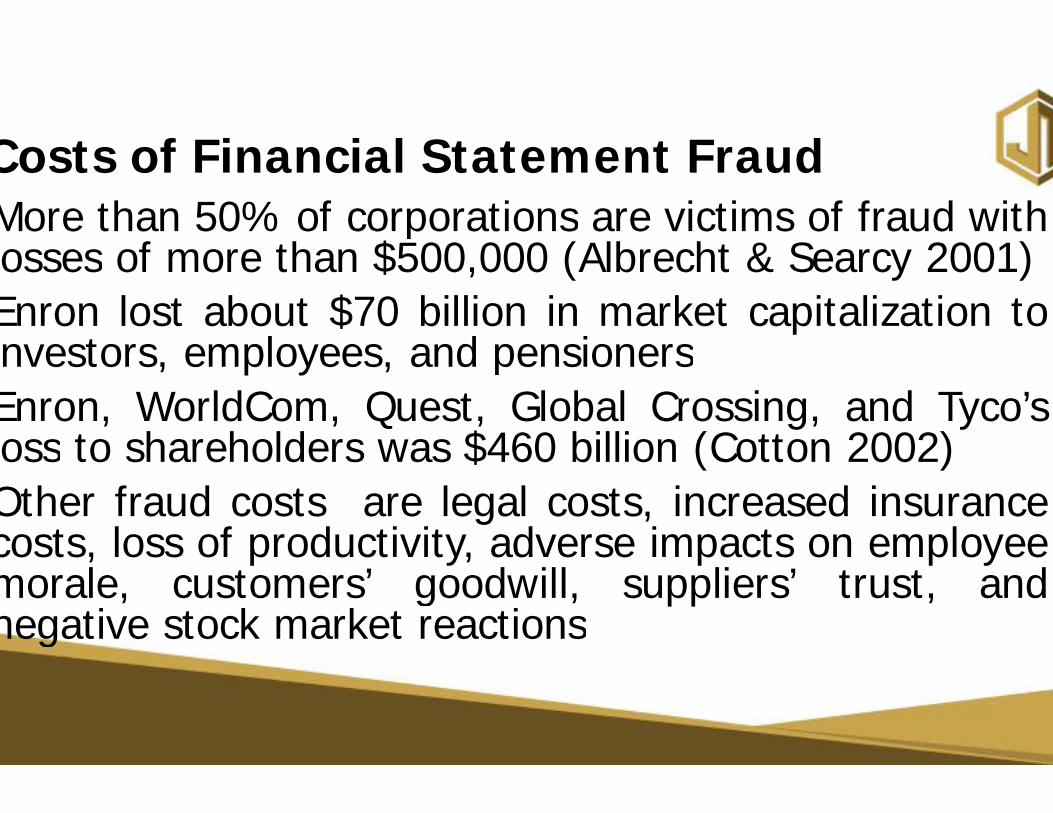

Costs of Financial Statement FraudMore than 50% of corporationslosses of more than $500,000Enron lost about $70 billioninvestors, employees, and pensionersEnron, WorldCom, Quest, Globalloss to shareholders was $460Other fraud costs are legalcosts, loss of productivity, adversemorale, customers’ goodwill,negative stock market reactions

Costs of Financial Statement Fraudcorporations are victims of fraud with

000 (Albrecht & Searcy 2001)billion in market capitalization to

pensionersGlobal Crossing, and Tyco’s

460 billion (Cotton 2002)legal costs, increased insurance

adverse impacts on employeegoodwill, suppliers’ trust, andreactions

WHY FINANCIAL STATEMENT FRAUD IS COMMITTED“cook the books "to “buy more

To quietly fix current problemsTo obtain or renew financingTo inflate company share pricesprofitTo obtain bonus pay linked to

WHY FINANCIAL STATEMENT FRAUD IS

more time”. The main reasonsproblems

prices or exercise stock options

to company performance

WHY FINANCIAL STATEMENT FRAUD IS COMMITTED5. To encourage investment6. To demonstrate increased

allowing increased dividend7. To cover inability to generate8. To dispel negative market9. To receive higher purchase10. To demonstrate compliance11. To meet company goals and

WHY FINANCIAL STATEMENT FRAUD IS COMMITTED

investment through the sale of stockincreased earnings per share thus

dividend payoutsgenerate cashflow

market perceptionspurchase prices for acquisitions

compliance with financing covenantsand objectives

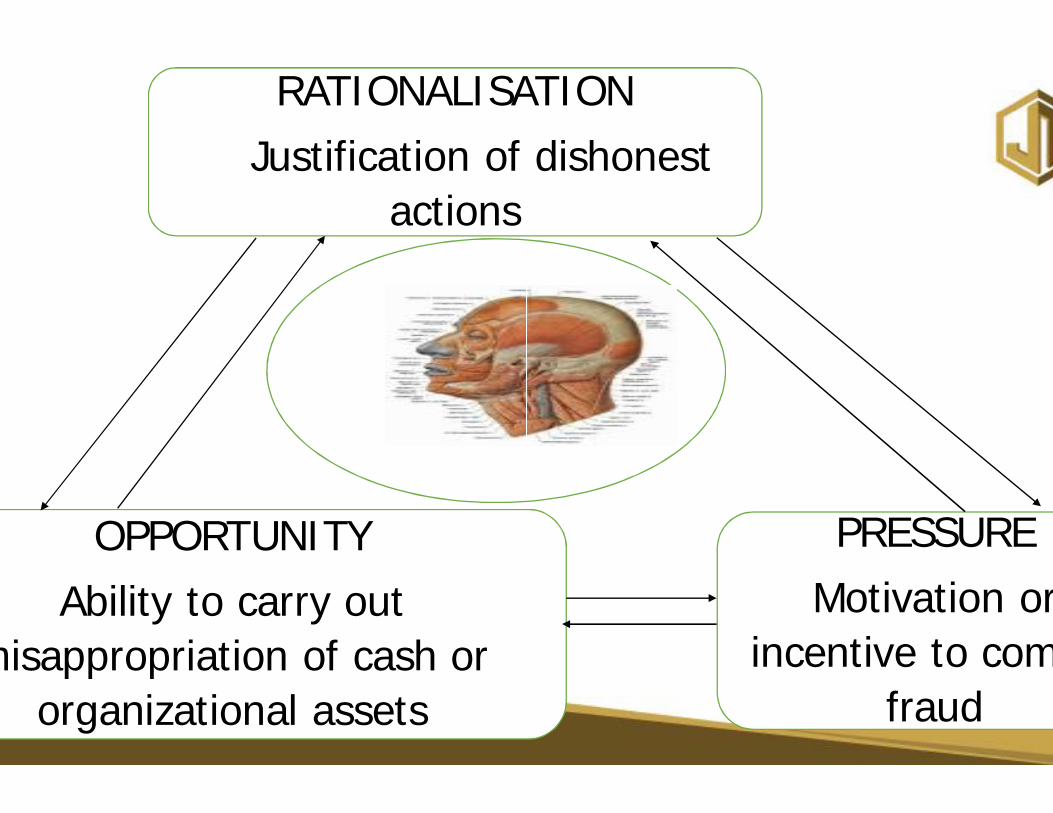

CAUSES OF FINANCIAL STATEMENTS FRAUD

Motivation for financial fraudpersonal financial gain.The cause of financial statement

• Situational pressure on the• Opportunity to commit fraud

CAUSES OF FINANCIAL STATEMENTS FRAUDfraud does not always involve direct

statement fraud is;manager or company.

fraud.

RATIONALISATIONJustification of dishonest

actions

OPPORTUNITYAbility to carry out

misappropriation of cash or organizational assets

RATIONALISATIONJustification of dishonest

PRESSUREMotivation or

incentive to commit fraud

SITUATIONAL PRESSURES

Sudden decrease in revenueFinancial pressures resultingdepend on short-term economicUnrealistic budget pressuresresults

SITUATIONAL PRESSURES

revenue by a company or industryresulting from bonus plans thateconomic performance

pressures particularly for short term

OPPORTUNITY

Absence of a board of directorsWeak board of directorsWeak or no-existent internalIneffective internal audit staffUnusual or complex transactionsFinancial estimates thatjudgment by management

directors or audit committees

internal controlsstaff and lack of external audits

transactionsrequire significant subjective

BREAKDOWN OF MAJOR ACCOUNTING SCANDALSBREAKDOWN OF MAJOR ACCOUNTING SCANDALS

WASTE MANAGEMENT COMPANY Company: Houston-basedmanagement companyWhat happened: ReportedMain players: Founder/CEO/Chairmanand other top executives(auditors)How they did it: Theincreased the depreciationplant and equipment on theHow they got caught: Ateam went through the books

WASTE MANAGEMENT COMPANY - 1998based publicly traded waste

Reported $1.7 billion in fake earningsFounder/CEO/Chairman Dean L. Buntrockexecutives; Arthur Andersen Company

The company allegedly falselytime length for their property,

the balance sheets.A new CEO and management

books.

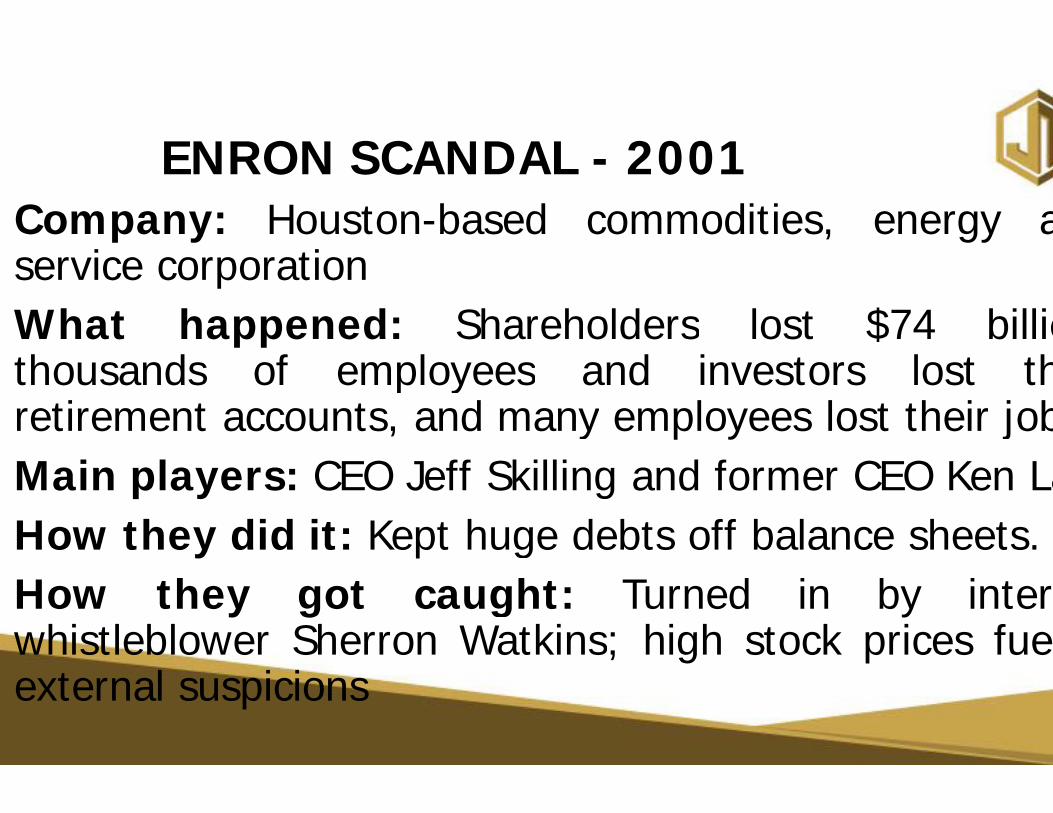

ENRON SCANDAL Company: Houston-basedservice corporationWhat happened: Shareholdersthousands of employeesretirement accounts, and manyMain players: CEO Jeff SkillingHow they did it: Kept hugeHow they got caughtwhistleblower Sherron Watkinsexternal suspicions

ENRON SCANDAL - 2001based commodities, energy and

Shareholders lost $74 billion,employees and investors lost their

many employees lost their jobsSkilling and former CEO Ken Lay

huge debts off balance sheets.caught: Turned in by internal

Watkins; high stock prices fueled

Company: Houston-basedservice corporationWhat happened: Shareholdersthousands of employeesretirement accounts, and manyMain players: CEO Jeff SkillingHow they did it: Kept hugeHow they got caughtwhistleblower Sherron Watkinsexternal suspicions

WORLDCOM SCANDAL

based commodities, energy and

Shareholders lost $74 billion,employees and investors lost their

many employees lost their jobsSkilling and former CEO Ken Lay

huge debts off balance sheets.caught: Turned in by internal

Watkins; high stock prices fueled

WORLDCOM SCANDAL - 2002

TYCO SCANDAL 2002

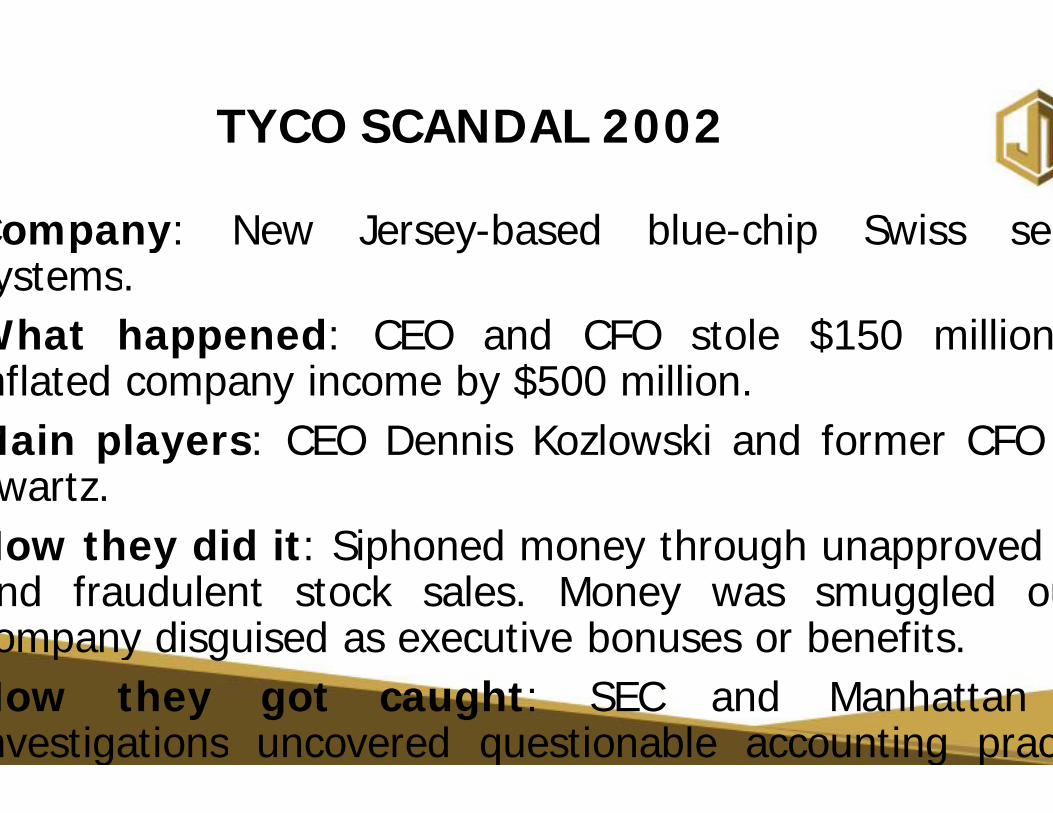

Company: New Jersey-basedsystems.What happened: CEO andinflated company income by $Main players: CEO DennisSwartz.How they did it: Siphoned moneyand fraudulent stock sales.company disguised as executiveHow they got caught:investigations uncovered questionableincluding large loans made

TYCO SCANDAL 2002

based blue-chip Swiss security

and CFO stole $150 million$500 million.Kozlowski and former CFO

money through unapproved. Money was smuggled out

executive bonuses or benefits.: SEC and Manhattan

questionable accounting practices,made to Kozlowski that were

HEALTHSOUTH SCANDAL (2003)Company: Largest publiclycompany in the U.S.What happened: Earningsinflated $1.4 billion toexpectations.Main player: CEO RichardHow he did it: Allegedlyup numbers and transactionsHow he got caught: Soldday before the companytriggering SEC suspicions.

HEALTHSOUTH SCANDAL (2003)publicly traded health care

Earnings numbers were allegedlyto meet stockholder

Scrushy.told underlings to make

transactions from 1996-2003.Sold $75 million in stock a

company posted a huge loss,

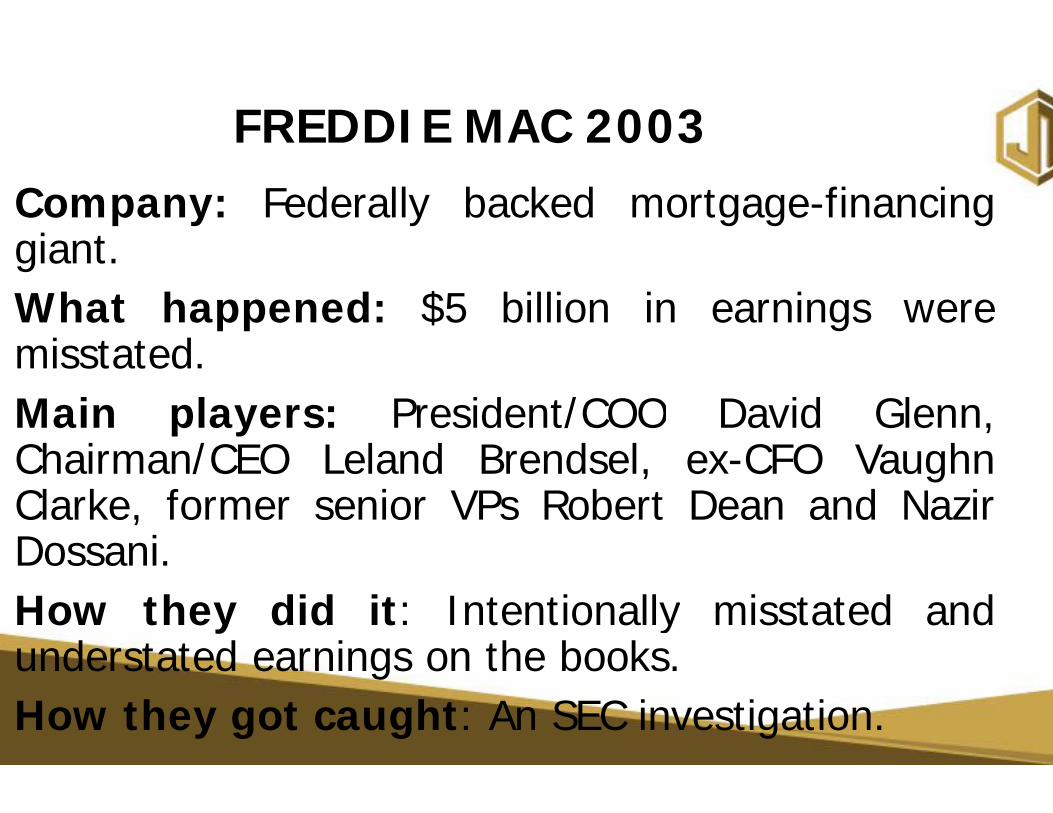

FREDDIE MAC 2003Company: Federally backedgiant.What happened: $5 billionmisstated.Main players: President/COOChairman/CEO Leland BrendselClarke, former senior VPsDossani.How they did it: Intentionallyunderstated earnings on theHow they got caught: An

FREDDIE MAC 2003backed mortgage-financing

billion in earnings were

President/COO David Glenn,Brendsel, ex-CFO Vaughn

Robert Dean and Nazir

Intentionally misstated andthe books.An SEC investigation.

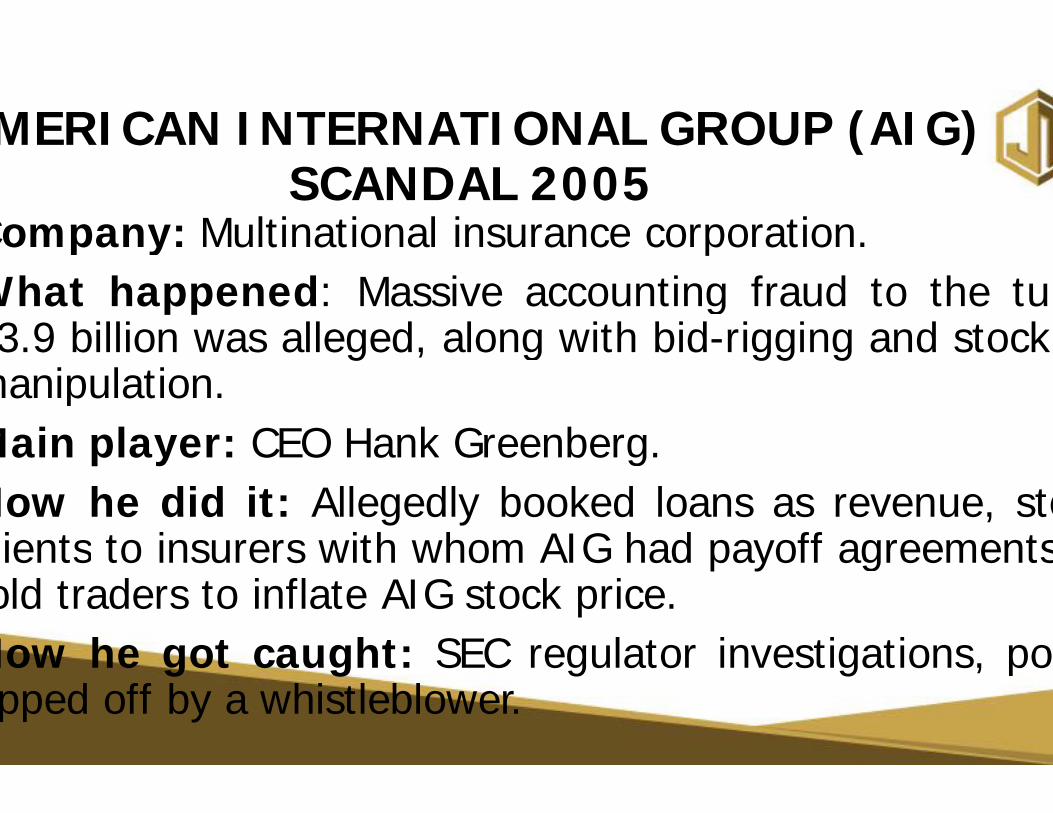

AMERICAN INTERNATIONAL GROUP (AIG) SCANDAL 2005

Company: Multinational insuranceWhat happened: Massive accounting3.9 billion was alleged, along

manipulation.Main player: CEO Hank GreenbergHow he did it: Allegedly bookedclients to insurers with whomtold traders to inflate AIG stockHow he got caught: SECtipped off by a whistleblower.

AMERICAN INTERNATIONAL GROUP (AIG) SCANDAL 2005

insurance corporation.accounting fraud to the tune

along with bid-rigging and stock

Greenberg.booked loans as revenue, steered

AIG had payoff agreements,stock price.

regulator investigations, possibly

LEHMAN BROTHERS SCANDAL 2008

Company: Global financial servicesWhat happened: Hid oversales.Main players: Lehman executivesauditors, Ernst & Young.How they did it: AllegedlyIsland banks with the understandingbought back eventually. Created50 billion more cash and $50really did.

How they got caught: Went

LEHMAN BROTHERS SCANDAL 2008

services firm.$50 billion in loans disguised

executives and the company's

Allegedly sold toxic assets to Caymanunderstanding that they wouldCreated the impression Lehman

50 billion less in toxic assets

Went bankrupt.

BERNIE MADOFF SCANDAL 2008

Company: Bernard L. MadoffWall Street investment firm

What happened: Trickedthrough the largest Ponzi schemeMain players: Bernie Madoff,and Frank DiPascalli.How they did it: Investorsown money or that of other investorsHow they got caught: Madoffscheme and they reported himthe next day.

BERNIE MADOFF SCANDAL 2008

Madoff Investment Securities LLCfounded by Madoff.investors out of $64.8 billion

scheme in history.Madoff, his accountant, David Friehling

Investors were paid returns out ofinvestors rather than from profitsMadoff told his sons abouthim to the SEC. He was arrested

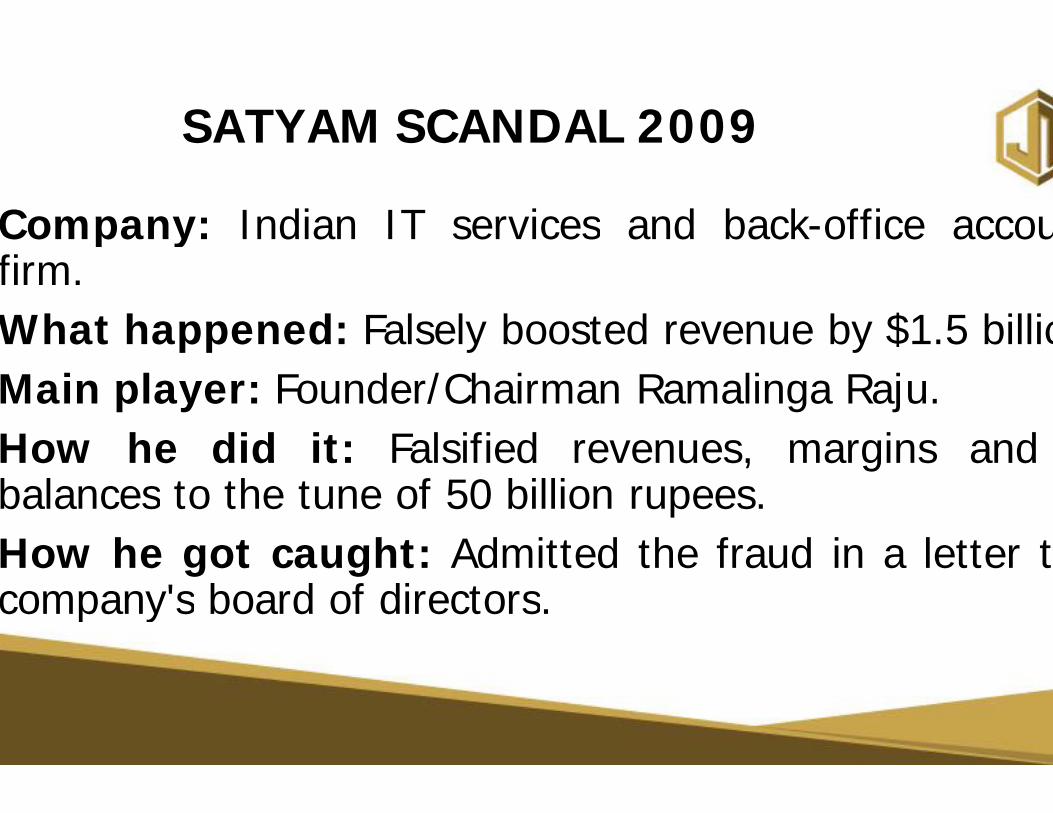

SATYAM SCANDAL 2009

Company: Indian IT servicesfirm.What happened: Falsely boostedMain player: Founder/ChairmanHow he did it: Falsifiedbalances to the tune of 50 billionHow he got caught: Admittedcompany's board of directors

SATYAM SCANDAL 2009

services and back-office accounting

boosted revenue by $1.5 billionFounder/Chairman Ramalinga Raju.

Falsified revenues, margins andbillion rupees.

Admitted the fraud in a letter todirectors.

Effects of Financial Statement Fraud

• Undermines the reliability,integrity of the financial reporting

• Jeopardizes the integrity andprofession, especially auditors

• Diminishes the confidencewell as market participants,information

• Makes the capital markets less

Effects of Financial Statement Fraud

reliability, quality, transparency, andreporting processand objectivity of the auditing

auditors and auditing firmsof the capital markets, as

participants, in the reliability of financial

less efficient

Effects of Financial Statement Fraud

• Adversely affects the nation’sprosperity

• Results in huge litigation costs• Destroys careers of individualsstatement fraud.

• Causes bankruptcy or substantialthe company engaged in financial

Effects of Financial Statement Fraud

nation’s economic growth and

costsindividuals involved in financial

substantial economic losses byfinancial statement fraud

Effects of Financial Statement Fraud

• Encourages regulatory intervention• Causes devastation in theperformance of alleged companies

• Raises serious doubt aboutstatement audits

• Erodes public confidence andand auditing profession

Effects of Financial Statement Fraud

interventionthe normal operations and

companiesabout the efficacy of financial

and trust in the accounting

Who Commits Financial Statement Fraud

• Senior management• Mid- and lower-level employees• Organized criminals

Who Commits Financial Statement Fraud

employees

Why Do People Commit Financial Statement Fraud• To conceal true business performance• To preserve personal status/control• To maintain personal income/wealth

Why Do People Commit Financial

performancestatus/controlincome/wealth

Why Senior Management Will Overstate Business Performance• To meet or exceed the earningsexpectations of stock market

• To comply with loan covenants• To increase the amount ofasset-based loans

• To meet a lender’s criteriafacilities

• To meet corporate performanceparent company

Why Senior Management Will Overstate

earnings or revenue growthmarket analysts

covenantsof financing available from

for granting/extending loan

performance criteria set by the

Why Senior Management Will Overstate Business PerformanceTo defer “surplus” earnings toTo take all possible write-offsfuture earnings will be consistentlyTo reduce expectations now soperceived and rewarded.To preserve a trend of consistentresults.To reduce the value of anpurposes of a divorce settlementTo reduce the value ofmanagement is planning a buyout

Why Senior Management Will Overstate

to the next accounting period.offs in one “big bath” now so

consistently higher.so future growth will be better

consistent growth, avoiding volatile

owner-managed business forsettlement.

a corporate unit whosebuyout

How Do People Commit Financial Statement Fraud

• Playing the accounting system

• Beating the accounting system

• Going outside the accounting

How Do People Commit Financial

system

system

accounting system

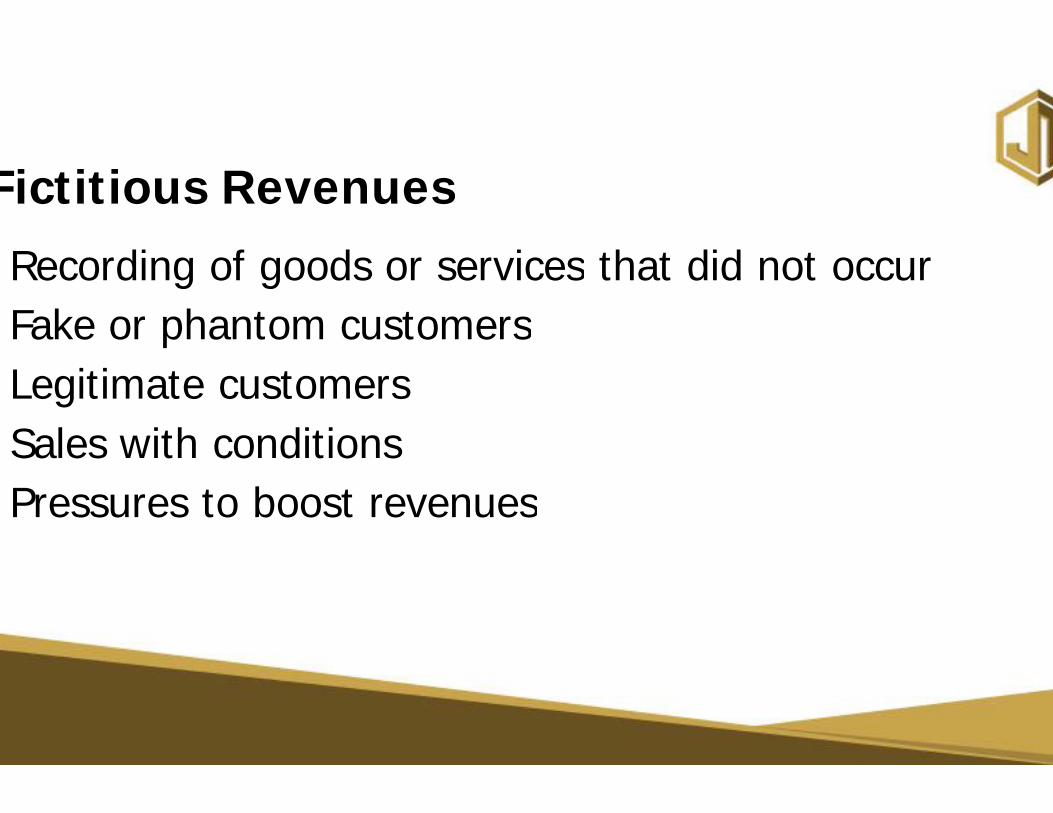

Methods of Financial Statement Fraud• Fictitious revenues• Timing differences• Improper asset valuations• Concealed liabilities and expenses• Improper disclosures

Methods of Financial Statement Fraud

expenses

Financial Statement Schemes by Category

0% 10% 20%

Timing Diff.

Conceal Liab.

Fict. Rev.

Disclosures

Asset Value

Financial Statement Schemes by

25.0%

40.0%

45.0%

47.5%

52.5%

30% 40% 50% 60%

Fictitious Revenues• Recording of goods or services• Fake or phantom customers• Legitimate customers• Sales with conditions• Pressures to boost revenues

services that did not occurcustomers

revenues

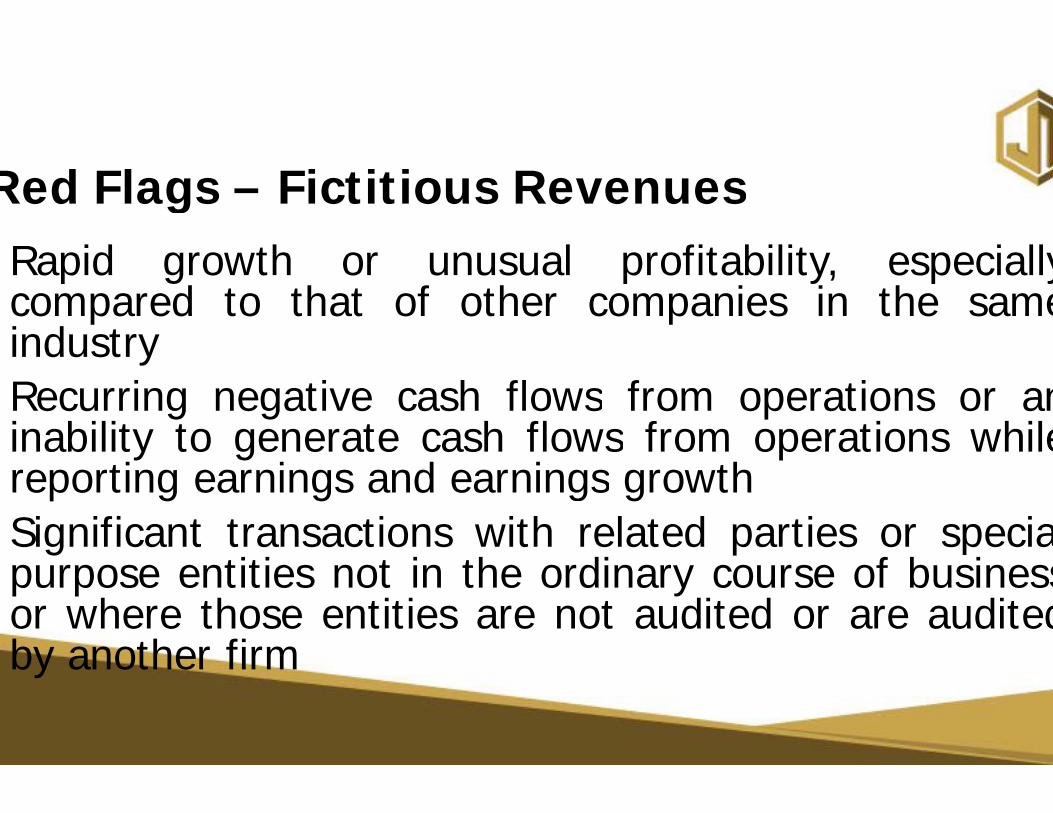

Red Flags – Fictitious Revenues• Rapid growth or unusualcompared to that of otherindustry

• Recurring negative cash flowsinability to generate cash flowsreporting earnings and earnings

• Significant transactions withpurpose entities not in theor where those entities areby another firm

Fictitious Revenuesunusual profitability, especially

other companies in the same

flows from operations or anflows from operations while

earnings growthwith related parties or special

ordinary course of businessare not audited or are audited

Red Flags – Fictitious Revenues

Significant, unusual, or highlyespecially those close to period“substance over form” questionsUnusual growth in the numberreceivablesA significant volume ofsubstance and ownership is notAn unusual surge in sales bycompany, or of salesheadquarters

Fictitious Revenues

highly complex transactions,period end that pose difficult

questionsnumber of days’ sales in

sales to entities whosenot knowna minority of units within arecorded by corporate

Timing Differences• Recording revenue and/or expenses• Shifts revenues or expensesthe next, increasing or decreasing

expenses in improper periodsexpenses between one period and

decreasing earnings as desired

Red Flags – Timing DifferencesRapid growth or unusual profitability,to that of other companies inRecurring negative cash flowsinability to generate cashreporting earnings and earningsSignificant, unusual, or highlyespecially those close to period“substance over form” questionsUnusual increase in gross marginindustry peersUnusual growth in the numberUnusual decline in the numberaccounts payable

Timing Differencesprofitability, especially compared

the same industryflows from operations or an

flows from operations whileearnings growth

highly complex transactions,period end that pose difficult

questionsmargin or margin in excess of

number of days’ sales in receivablesnumber of days’ purchases in

Concealed Liabilities………..• Liability/expense omissions• Capitalized expenses• Failure to disclose warranty

Concealed Liabilities………..

costs and liabilities

Red Flags – Concealed Liabilities• Recurring negative cash flowsinability to generate cash flowsreporting earnings and earnings

• Assets, liabilities, revenues,significant estimates that involveor uncertainties that are difficult

• Non-financial management’sor preoccupation with theprinciples or the determination

Concealed Liabilitiesflows from operations or anflows from operations while

earnings growthrevenues, or expenses based on

involve subjective judgmentsdifficult to corroborate

management’s excessive participation inthe selection of accounting

determination of significant estimates

Improper Disclosures…………….• Liability omissions• Subsequent events• Management fraud• Related-party transactions• Accounting changes

Improper Disclosures…………….

Red Flags – Improper DisclosuresDomination of managementgroup (in a non-ownercompensating controlsIneffective board of directorsover the financial reporting processIneffective communication,enforcement of the entity’s valuesmanagement or the communicationor ethical standardsRapid growth or unusual profitability,to that of other companies in

Improper Disclosuresby a single person or small

managed business) without

directors or audit committee oversightprocess and internal control

implementation, support, orvalues or ethical standards by

communication of inappropriate values

profitability, especially comparedthe same industry

Red Flags – Improper Disclosures

Significant, unusual, or highlyespecially those close to period“substance over form” questionsSignificant related-party transactionscourse of business or withor audited by another firmSignificant bank accountsoperations in tax haven jurisdictionsappears to be no clear businessOverly complex organizationalunusual legal entities or managerial

Improper Disclosures

highly complex transactions,period end that pose difficult

questionstransactions not in the ordinary

related entities not audited

accounts or subsidiary or branchjurisdictions for which there

business justificationorganizational structure involving

managerial lines of authority

Red Flags – Improper Disclosures• Known history of violationslaws and regulations, or claimssenior management, or boardor violations of laws and regulations

• Recurring attempts by managementor inappropriate accounting

• Formal or informal restrictionsinappropriately limit accessthe ability to communicatedirectors or audit committee

Improper Disclosuresviolations of securities laws or other

claims against the entity, itsboard members alleging fraudregulations

management to justify marginalon the basis of materiality

restrictions on the auditor thatto people or information oreffectively with the board of

committee

Red Flags – Concealed Liabilities• Unusual increase in gross marginindustry peers

• Allowances for sales returns,that are shrinking in percentageout of line with industry peers

• Unusual reduction in the numberaccounts payable

• Reducing accounts payablestretching out payments to

Concealed Liabilitiesmargin or margin in excess of

returns, warranty claims, and so onpercentage terms or are otherwise

peersnumber of days’ purchases in

payable while competitors arevendors

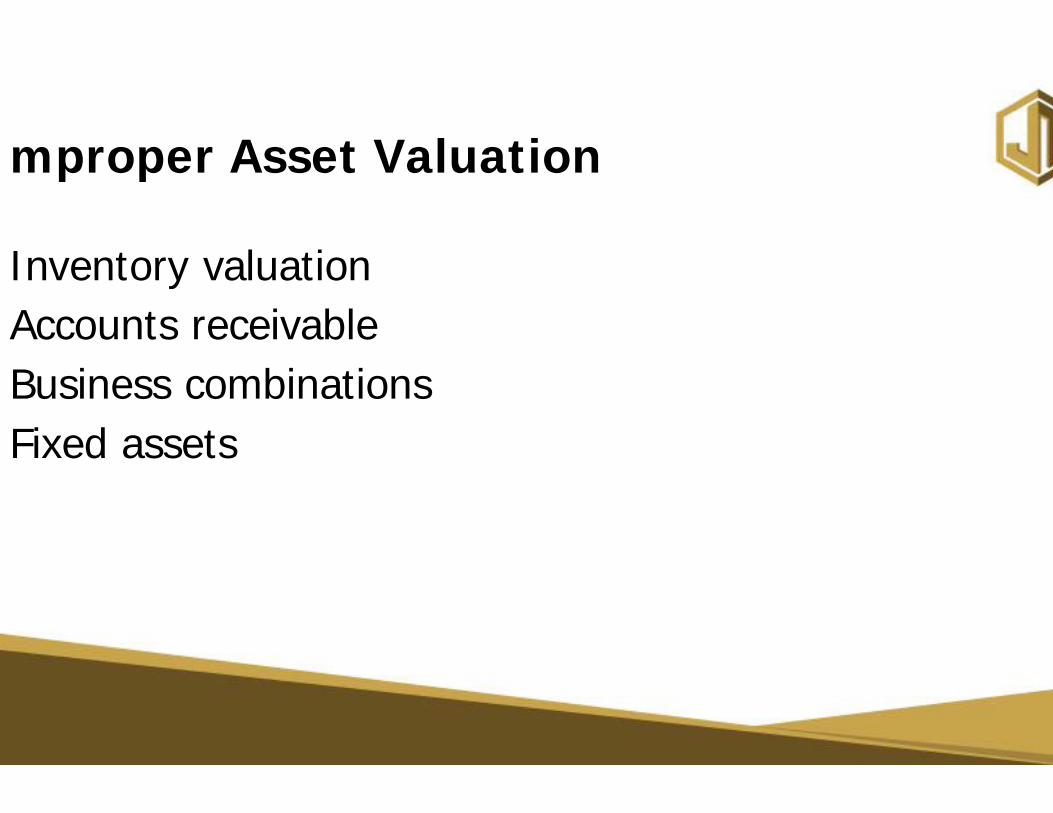

Improper Asset Valuation

• Inventory valuation• Accounts receivable• Business combinations• Fixed assets

Improper Asset Valuation

Red Flags – Improper Asset ValuationRecurring negative cash flows

generate cash flows fromearnings and earnings growthSignificant declines in customerbusiness failures in either the industryAssets, liabilities, revenues, orestimates that involve subjectivethat are difficult to corroborateNon-financial management’spreoccupation with the selectionthe determination of significantUnusual increase in gross marginindustry peers

Improper Asset Valuationfrom operations or an inability

from operations while reporting

customer demand and increasingindustry or overall economy

or expenses based on significantsubjective judgments or uncertainties

corroborateexcessive participation in

selection of accounting principlessignificant estimates

margin or margin in excess

Red Flags – Improper Asset Valuation• Unusual growth in the numberreceivables

• Unusual growth in the numberinventory

• Allowances for bad debts,inventory, and so on thatterms or are otherwise out of

• Unusual change in the relationshipand depreciation

• Adding to assets while competitorstied up in assets

Improper Asset Valuationnumber of days’ sales in

number of days’ purchases in

debts, excess and obsoleteare shrinking in percentageof line with industry peers

relationship between fixed assets

competitors are reducing capital

Financial Statement Analysis• Vertical analysis

• Analyzes the relationshipson an income statement,statement of cashcomponents as percentages

• Horizontal analysis• Analyzes the percentagefinancial statement items

• Ratio analysis• Measures the relationshipdifferent financial statement

Financial Statement Analysis

relationships between the itemsstatement, balance sheet, or

flows by expressingpercentages

percentage change in individualitems

relationship between twostatement amounts

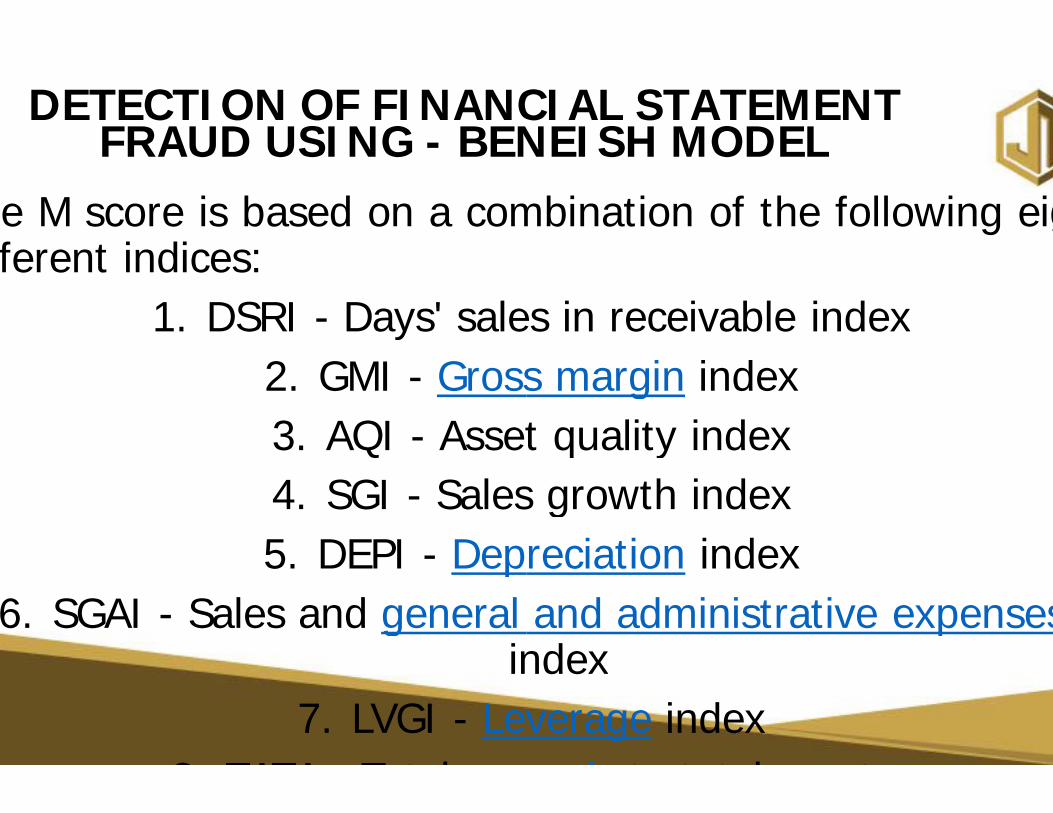

DETECTION OF FINANCIAL STATEMENT FRAUD USING - BENEISH MODEL

The Beneish model is afinancial ratios calculated withcompany in order to checkthat the reported earningsmanipulated.

The M score is basedfollowing eight different indices

DETECTION OF FINANCIAL STATEMENT BENEISH MODEL

statistical model that useswith accounting data of a specific

if it is likely (high probability)of the company have been

on a combination of theindices or ratios:

DETECTION OF FINANCIAL STATEMENT FRAUD USING - BENEISH MODEL

The M score is based on a combinationdifferent indices:

1. DSRI - Days' sales in receivable index2. GMI - Gross margin3. AQI - Asset quality index4. SGI - Sales growth index5. DEPI - Depreciation

6. SGAI - Sales and general and administrative expensesindex

7. LVGI - Leverage8. TATA - Total accruals

DETECTION OF FINANCIAL STATEMENT BENEISH MODELcombination of the following eight

Days' sales in receivable indexGross margin indexAsset quality indexSales growth indexDepreciation index

general and administrative expensesindex

Leverage indexaccruals to total assets

Deterrence of Financial Statement Fraud

Reduce pressuresstatement fraud

Reduce the opportunityfinancial statement

Reduce rationalizationstatement fraud

Deterrence of Financial Statement Fraud

to commit financial

opportunity to commitfraud

rationalization of financial

Reduce Pressures to Commit Financial Statement Fraud

Establish effective board oversightcreated by management.Avoid setting unachievable financialAvoid applying excessive pressureachieve goals.Change goals if changed marketEnsure compensation systemstoo much incentive to commitDiscourage excessive externalcorporate performance.Remove operational obstaclesperformance.

to Commit Financial

oversight of the “tone at the top”

financial goals.pressure on employees to

market conditions require itsystems are fair and do not create

fraud.external expectations of future

obstacles blocking effective

Reduce the OpportunityFinancial Statement FraudMaintain accurate and complete internalCarefully monitor the businessrelationships of suppliers, buyers,representatives, and others whobetween financial units.Establish a physical security systemincluding finished goods, cash, capitalvaluable items.Maintain accurate personnel recordson new employees.Encourage strong supervisory andgroups to ensure enforcement ofEstablish clear and uniform accountingexception clauses.

Opportunity to Commit Financial Statement Fraud

internal accounting records.business transactions and interpersonal

buyers, purchasing agents, saleswho interface in the transactions

system to secure company assets,capital equipment, tools, and other

records including background checks

and leadership relationships withinof accounting procedures.

accounting procedures with no

Reduce RationalizationStatement Fraud

• Promote strong values, basedthe organization.

• Have policies that clearlywith respect to accountingfraud.

• Provide regular training to allprohibited behavior.

Rationalization of Financial

based on integrity, throughout

define prohibited behavioraccounting and financial statement

all employees communicating

Reduce RationalizationStatement Fraud

• Have confidential advice andcommunicate inappropriate

• Have senior executives communicateintegrity takes priority andachieved through fraud.

• Ensure management practicessets an example by promotingaccounting area.

• The consequences of violatingpunishment of violators should

Rationalization of Financial

and reporting mechanisms tobehavior.

communicate to employees thatand that goals must never be

practices what it preaches andpromoting honesty in the

violating the rules and theshould be clearly communicated

These Are Interesting Times

• Number and size of financial statement frauds are increasing

• Number and size of frauds against organizations are increasing

• Some recent frauds include several people20 or 30 (seems to indicate moral decay)

• Many investors have lost confidence in credibility of financial statements and corporate reports

• More interest in fraud than ever beforeon many college campuses

These Are Interesting Times

Number and size of financial statement frauds are

Number and size of frauds against organizations are

Some recent frauds include several people—as many as 20 or 30 (seems to indicate moral decay)Many investors have lost confidence in credibility of financial statements and corporate reportsMore interest in fraud than ever before—now a course

ANANIAS AND SAPPHIRA New International Version (NIV)]When Ananias heard this, he fell down and

heard what had happened. 6 Then some young men came forward, wrapped up his body, and carried him out and buried him. came in, not knowing what had happened. price you and Ananias got for the land?” “Yes,” she said, “that is the price.”

Peter said to her, “How could you conspire to test the Spirit of the Lord? Listen! The feet of the men who buried your husband are at the door, and they will carry you out also.”

At that moment she fell down at his feet and died. Then the young men came in and, finding her dead, carried her out and buried her beside her husband. Great fear seized the whole church and all who heard about these events.

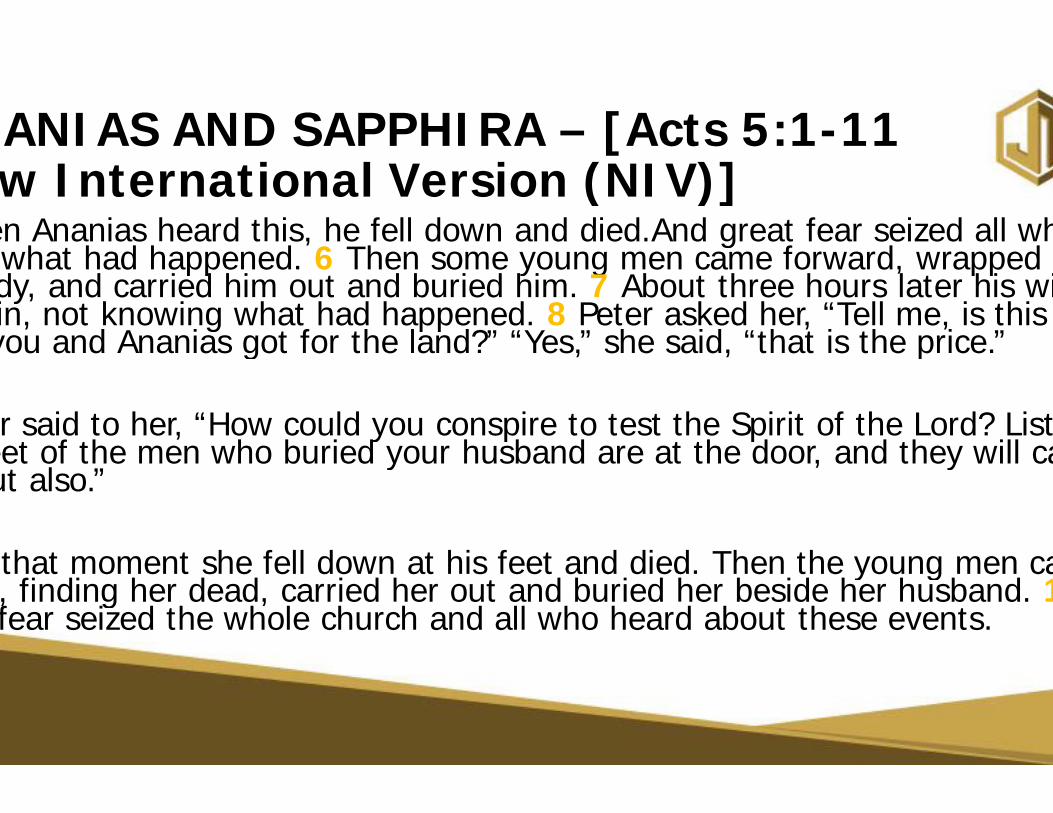

ANANIAS AND SAPPHIRA – [Acts 5:1-11 New International Version (NIV)]When Ananias heard this, he fell down and died.And great fear seized all who

Then some young men came forward, wrapped up his body, and carried him out and buried him. 7 About three hours later his wife came in, not knowing what had happened. 8 Peter asked her, “Tell me, is this the price you and Ananias got for the land?” “Yes,” she said, “that is the price.”

Peter said to her, “How could you conspire to test the Spirit of the Lord? Listen! The feet of the men who buried your husband are at the door, and they will carry

At that moment she fell down at his feet and died. Then the young men came in and, finding her dead, carried her out and buried her beside her husband. 11 Great fear seized the whole church and all who heard about these events.

What should internal auditor do?

• Assess the impact of thestatements

• Consult with legal counsel and• Report the acts to audit committee• Consider client’s remedial actions• Disciplinary actions• Controls to safeguard against• Reporting effects of the acts• Consider withdrawing from

What should internal auditor do?

the acts on the financial

and other specialistscommittee

actions

against recurrenceacts

engagement

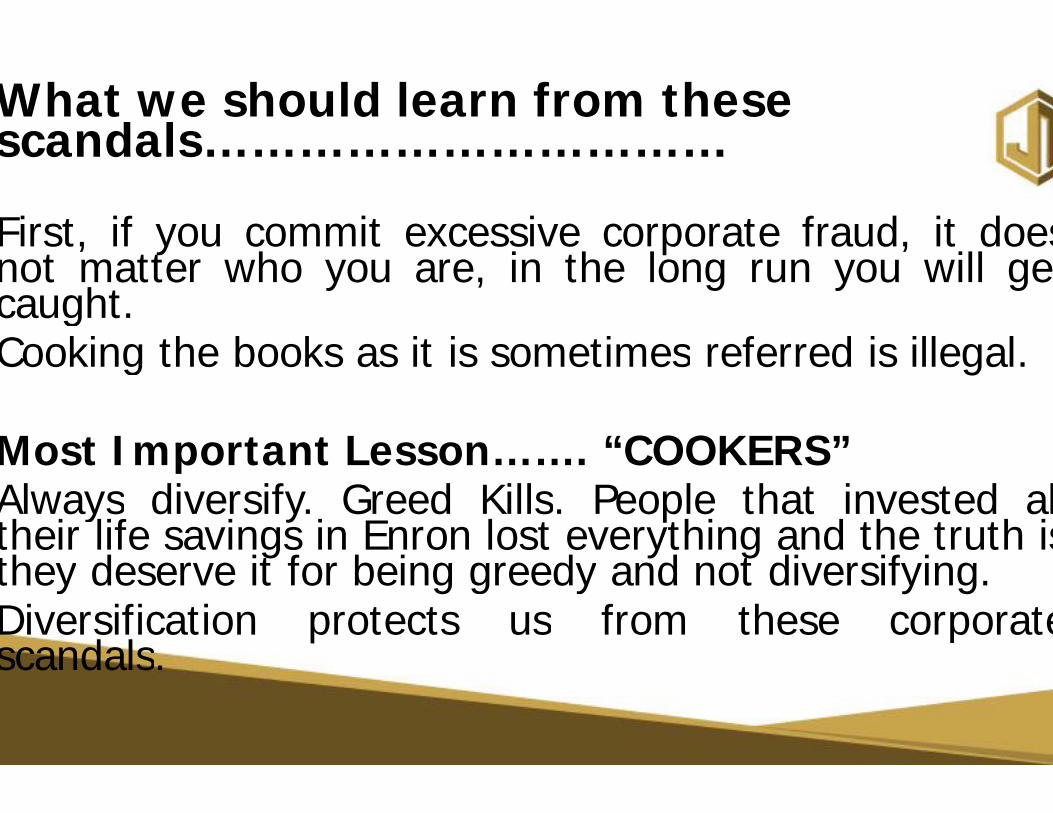

What we should learn from these scandals……………………………

First, if you commit excessivenot matter who you are, incaught.Cooking the books as it is sometimes

Most Important Lesson……Always diversify. Greed Killstheir life savings in Enron lostthey deserve it for being greedyDiversification protects usscandals.

What we should learn from these scandals……………………………

excessive corporate fraud, it doesin the long run you will get

sometimes referred is illegal.

……. “COOKERS”Kills. People that invested alllost everything and the truth is

greedy and not diversifying.us from these corporate

Thank You!Thank You!