Value Chain and Policy Analysis of Fossil Fuel Trade, Subsidy and Tax in Viet Nam

By: PeaPros Consulting JSC

Hanoi, May 2011 (with minor revisions in December 2011)

Package 1, under the UNDP Viet Nam research project “Research on fossil fuel prices and taxes, and their effects on economic development and income distribution in Viet Nam” The opinions, analyses and recommendations contained in this document do not necessarily reflect the opinions of the United Nations Development Programme in Viet Nam. The Report is an independent publication commissioned by UNDP.

i

Table of Contents

List of Figures ii

List of Tables iii

Abbreviations iv

1. Introduction 1 1.1. Methodology 1 1.2. Study Constraints 2 1.3. The cost of subsidies 2

2. Energy Use in general in Viet Nam 4

3. Electricity Generation and Use In Viet Nam 5 3.1. Electricity generation in Viet Nam, 2009 5 3.2. Master plan directions 9

3.2.1. Constraints in meeting National Plan VI 12 3.3. The Electricity Market in Viet Nam 13

3.3.1. The Role of EVN 13 3.3.1. Market revenue 15

3.4. Electricity usage in Viet Nam 20 3.5. Key constraints and implications 21

3.5.1. Pricing constraints 21 3.5.2. The Role of Coal 22

3.6. Electricity Fossil Fuel use Conclusion 25

4. Refined Petroleum market 27 4.1. Refined Petroleum Demand 27 4.2. Users of Refined Petroleum in Viet Nam 29 4.3. Refined Petroleum market structure 30 4.4. State Revenues 31 4.5. Price fluctuations and stabilization 32 4.6. Refined Petroleum products conclusion 34 4.7. Map of the refined petroleum market 36

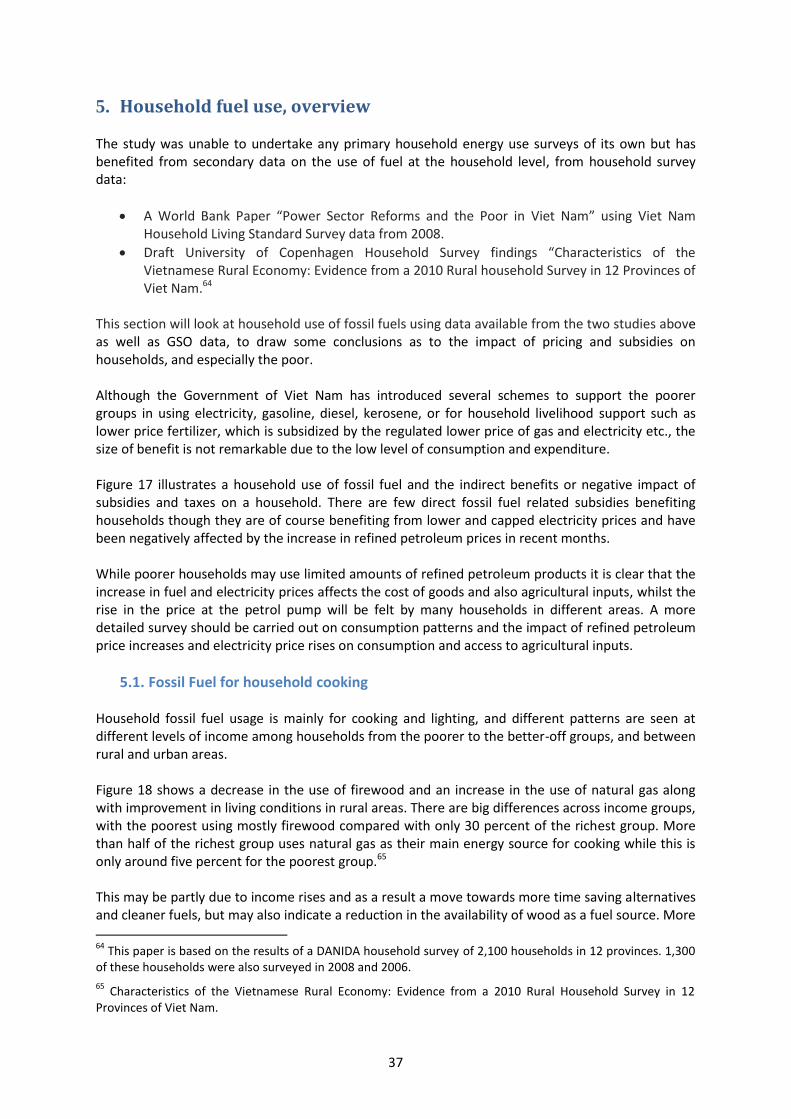

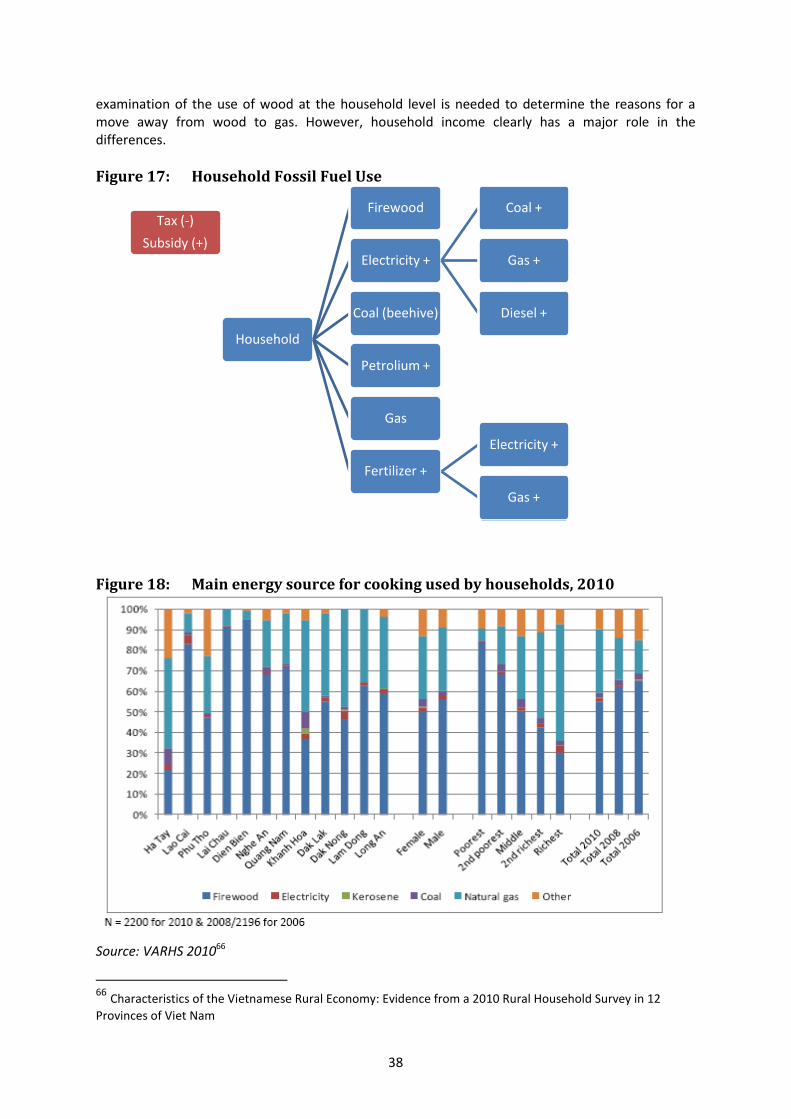

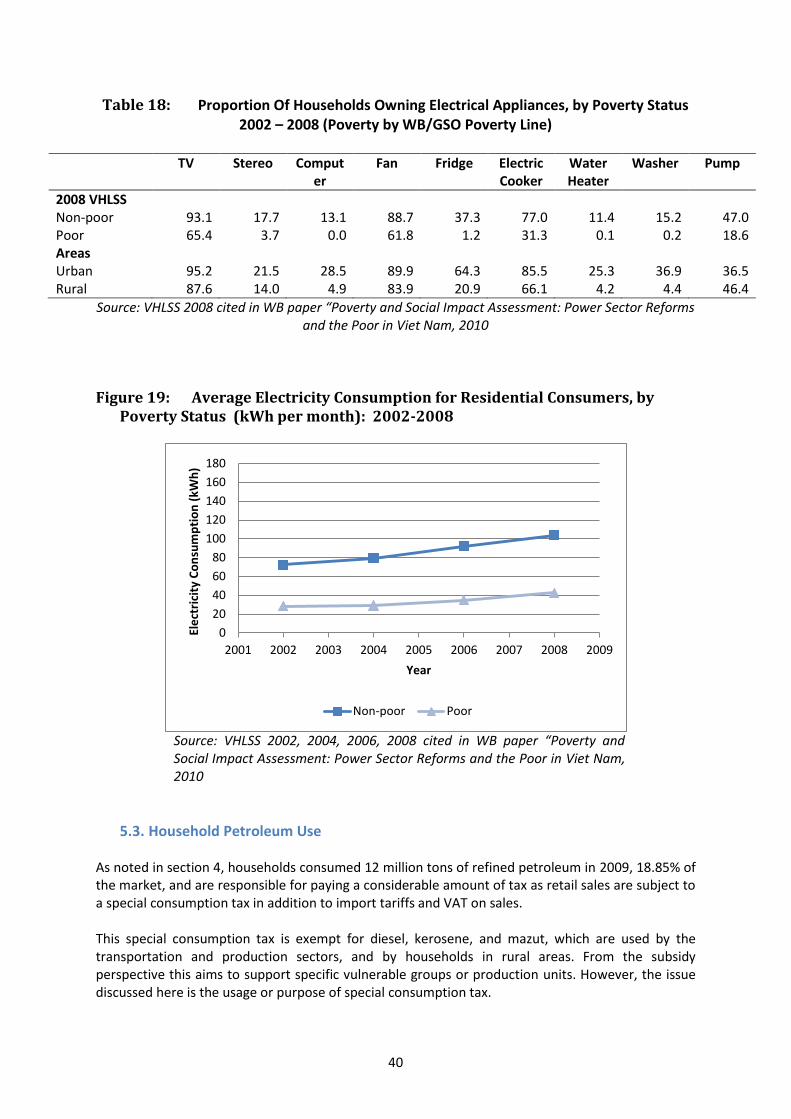

5. Household fuel use, overview 37 5.1. Fossil Fuel for household cooking 37 5.2. Household Electricity Use 39 5.3. Household Petroleum Use 40 5.4. Gas, Coal and firewood 42

6. Conclusion 42 6.1. Electricity market 42 6.2. Refined Petroleum 43 6.3. Government Subsidies 43 6.4. Next Steps 45

References 47

ANNEX 1: Terms of Reference for the study 53

ANNEX 2: ASEAN Electricity Tariffs, February 2011 56

ANNEX 3: Retail Petroleum Prices in ASEAN Member Countries 59

ANNEX 4: Regulations guiding the Fossil Fuel Market 60

ii

List of Figures Figure 1: Energy Consumption by Fuel 2008, ktoe .......................................................................... 4 Figure 2: Energy Consumption by Economic Sector, 2008 ktoe ...................................................... 4 Figure 3: Electricity Production and Use Growth and GDP Growth, 2000-2009 ............................. 6 Figure 4: Viet Nam’s Electricity Generation by Source, 2000 and 2009 .......................................... 7 Figure 5: Changes in Viet Nam’s Electricity production structure 2000-2010(est.) MW ................. 8 Figure 6: Change in electricity generation structure 2009 to 2025, MW ...................................... 10 Figure 7: Production comparison, the World, China and Viet Nam ............................................... 13 Figure 8: Viet Nam’s Electricity Market Structure.......................................................................... 14 Figure 9: Electricity Production Share ............................................................................................ 15 Figure 10: Electricity Generation, Transmission and Retail Market in 2009 .................................... 17 Figure 11: Main users of Electricity .................................................................................................. 20 Figure 12: Coal and Electricity Production ....................................................................................... 23 Figure 13: Volume sales of refined petroleum products, 2007 to 2009 .......................................... 27 Figure 14: Transportation 2000 to 2009, million person kilometers ............................................... 28 Figure 15: Volume of Freight 2000 to 2009, thousands of tons ...................................................... 29 Figure 16: Import and Export of Petroleum products, 2003 to 2009 .............................................. 31 Figure 17: Household Fossil Fuel Use ............................................................................................... 38 Figure 18: Main energy source for cooking used by households, 2010 ........................................... 38 Figure 19: Average Electricity Consumption for Residential Consumers, by Poverty Status (kWh

per month): 2002-2008 ............................................................................................................... 40

iii

List of Tables Table 1: Electricity Generating Capacity and Production, 2009 .......................................................... 7 Table 2: Viet Nam energy capacity projections, 2009 to 2025 ........................................................... 9 Table 3: Total Costs of Generating Electricity in US cents per Kilowatt-hour ................................... 11 Table 4: Market value and tax revenues, 2007 to 2010 .................................................................... 16 Table 5: Minimum Wholesale and Retail Price Structure per Kwh (excl. VAT) under Decision

24/2011, 2011 .............................................................................................................................. 18 Table 6: Average price data for users across ASEAN, 2010 ............................................................... 19 Table 7: Share of electricity consumption by sector , 2015 to 2030 ................................................. 20 Table 8: Percentage of market by key industry................................................................................. 21 Table 9: Demand for Coal, 2010 to 2015 (1,000 Tons) ..................................................................... 23 Table 10: Direct and Indirect Subsidies to the Electricity sector .................................................... 26 Table 11: Growth in passenger and freight transport and the demand for refined petroleum

products ....................................................................................................................................... 28 Table 12: Sector use of refined petroleum, 2007 to 2009 .............................................................. 29 Table 13: Use of refined petroleum, 2007 to 2009......................................................................... 30 Table 14: Revenues from Petroleum, 2007 to 2009 ....................................................................... 31 Table 15: Retail Price structure for Refined Petroleum, April 2011 ............................................... 33 Table 16: ASEAN Prices of Gasoline and Diesel, February 2011 ..................................................... 34 Table 17: Direct and Indirect Subsidies to the Refined Petroleum Sector ..................................... 35 Table 18: Proportion Of Households Owning Electrical Appliances, by Poverty Status 2002 – 2008

(Poverty by WB/GSO Poverty Line) .............................................................................................. 40 Table 19: List of 31 eligible provinces (Zone 2) for fix 2% top-up ................................................... 41 Table 20: List of eligible districts (Zone 2) in 9 other provinces for fix 2% top-up ......................... 41 Table 21: Direct and Indirect Subsidies to the Energy Sector ......................................................... 44

iv

Abbreviations ADB Asian Development Bank bcm billion cubic meters BOO Build-operate-own BOT Build-operate-transfer CGE Computable general-equilibrium ERAV The Electricity Regulatory Authority of Vietnam EVN Electricity Vietnam GDP Gross Domestic Product GW Giga Watts GSO General Statistics Office IEA International Energy Association ktoe Kilo ton of oil equivalent Kwh Kilo watt hour MoF Ministry of Finance MoIT Ministry of Industry and Trade MoNRE Ministry of Natural Resources and Environment MW Mega Watts OECD Organisation of Economic Cooperation and Development PetroVietnam Vietnam Oil and Gas Group PPA Power Purchasing Agreement PVN Vietnam Oil and Gas Group UNDP United Nations Development Programme UNEP United Nations Environment Programme UNIDO United Nations Industrial Development Organisation VAT Value Added Tax Vinacomin The Vietnam National Coal and Mineral Industries Group VNEEP Vietnam Energy Efficiency Programme

1

1. Introduction This study was commissioned as part of a three phase in-depth examination of the fossil fuel market in Viet Nam and the role of subsidies and taxes in the use of fossil fuels (see also Annex I for the Terms of Reference). The three study areas included:-

Package 1: Value Chain and Policy Analysis of Fossil Fuel Trade, Subsidy and Tax.

Package 2: A Computable general-equilibrium (CGE) Model of the fiscal and social impacts of fuel taxation in Viet Nam.

Package 3: Environmental Assessment of the Potential Effects and Impacts of removal of Fuel Subsidies and Fuel Taxes

Under this value chain study (package 1) fossil fuel use was examined for electricity generation (coal, oil and gas), the use of refined fossil fuels in transportation (gasoline, diesel etc.) and the use of fossil fuels at the household level (electricity, bottled gas, kerosene as well as transportation). In addition to mapping the value chain for these fossil fuel markets and uses a key focus of the study was the identification of different subsidies and taxes across the various value chains for fossil fuels. Through the identification of these subsidies and examination of the regulations for these subsidies the study hoped to pin point the main beneficiaries of fossil fuel subsidies and also the main payer of fossil fuel taxes. The package 1 study has two objectives:

1. Analysis of the current energy landscape and the energy market in Viet Nam 2. Recommendations on the potential effects of removal of subsidies and introduction of fossil

fuel taxes on revenue collection.

Due to time and data access constraints the majority of the study’s work was spent on objective 1.

1.1. Methodology In order to map the movement of value and the benefits from subsidies and taxes to the government, producers and users, the study team did the following:

i. Desk Review of key fossil fuel and industry reports for Viet Nam as well as background materials on the role and impact of subsidies in fossil fuel markets.

ii. Collection and review of regulations guiding the use of fossil fuels: a database of regulations, master plans and strategies detailing price controls and structures, taxes and subsidies was built up. A brief literary review covering these regulations is available in the annexes.

iii. Gather key data on production and use of fossil fuels in the three main areas. Key data is presented in this report with more detailed data available separately in an excel sheet

iv. Interview key stakeholders in the regulation of fossil fuel as well as key producers and users. This included interviews with representatives of government ministries and institutions and leading state owned enterprises in the fossil fuel market.

v. Map the value chains of the markets and provide analysis: This focused mostly on the structure of two main fossil fuel markets, for electricity and transportation.

vi. Coordination with package 2 and 3: Throughout the study the team coordinated with package 2 and 3 in the provision of data as well as the market structure for each area to ensure key lessons and information supported their work.

2

1.2. Study Constraints The study was commissioned and finalized between January and February 2011 and initial deskwork began in March 2011. Initial work had to be reviewed as considerable movements occurred in the fossil fuel markets in the first quarter of 2011 including:

Increased global oil prices and the almost collapse of the Government’s oil stabalisation fund which led to a considerable revision of the retail price for refined oils in April 2011 include the deference of several taxes1.

Revised regulations in the electricity market allowing for quarterly revisions of the price of electricity2.

Acceleration of the move towards a more competitive market for electricity generation in line with 2004 Electricity Law3.

Further adjustments to the sales price of coal to industrial users though not for electricity producers4

For the purposes of this study we have taken January 2011 as the focal point for the market structures in different fossil fuel use areas though consideration is given throughout our analysis of these changes within the fossil fuel use market and what they mean for the value chain for fossil fuels. We have also considered policy changes between January 2011 and May 2011. Accessing specific data and qualifying data was a further hindrance to the study. Aggregated data for most fossil fuel production and usages is available from a variety of sources (GSO, ERAV, EVN, PVN). However, more detailed disaggregated data especially on usage was difficult to access as in many cases disaggregated data has only recently started to be collected by these agencies5. In other areas information was commercially sensitive. This was especially the case for coal sales to different power plants and also electricity sales prices to EVN under power purchasing agreements (PPAs). These issues will be highlighted throughout the report.

1.3. The cost of subsidies The International Energy Association (IEA) estimated that fossil fuel consumption subsidies cost governments across the world US$557 billion per year in fuel consumption subsidies. Subsidies to producers are estimated at US$100 million in 2008.6 While subsidies may help to ensure some equitable access to energy, such as petrol and electricity, it is recognized that subsidies often benefit the more well off in society as their use of energy is higher

1 http://bizvietnam.com/2011/02/oil-price-stabilization-fund-has-run-out-of-money/

2 Decision 24/2011D-TTg dated 16th

April 2011 on the adjustment of electricity selling

price according to market mechanism

3http://www.erav.vn/index.php?option=com_content&view=article&id=180%3Athang-72011-vn-hanh-thi-im-

th-trng-phat-in-cnh-tranh&catid=55%3Atin-tc-th-trng-in&Itemid=129&lang=vi3

4http://www.vinacomin.vn/temps/home/template2/defaultE.asp?Newid=17019&rootcate=1247

5 This was especially the case for disaggregated data on refined oil usage (gasoline, Diesel etc.) by industrial

sector for the 26 production areas identified by package two for analysis.

6 World Bank, IEA and OECD, 4:2008, “Analysis of the Scope of Energy Subsidies and Suggestions for the G-20

Initiative”

3

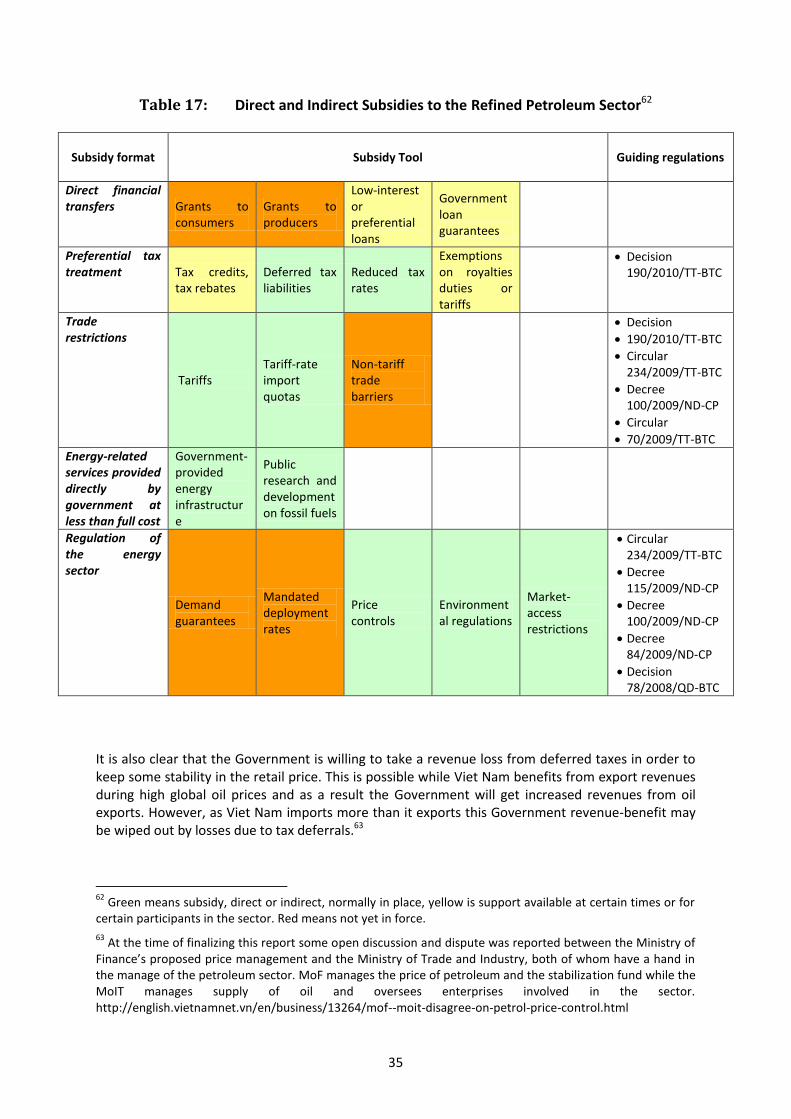

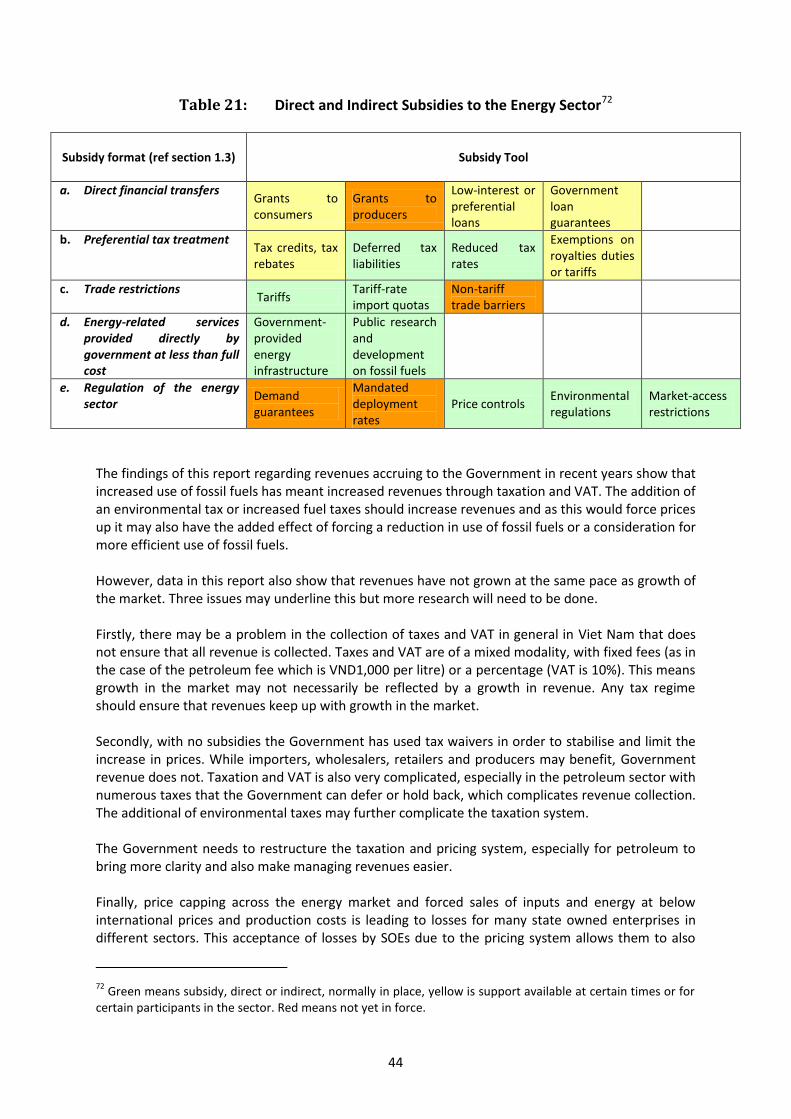

than the poorer groups. Though subsidies may be aimed at poorer groups and rural populations they tend to spend less of their incomes on energy. As IEA figures show, subsidies also incur high revenue costs for governments while the taxation of fossil fuels can both provide governments revenues while also providing a strong tool to encourage lower fossil fuel usage, energy savings and the adoption of cleaner energy and more efficient energy saving equipment. The IEA estimates that OECD countries collected revenues of US$400 billion between each year between 2003 and 2008 from taxes and VAT on fossil fuel.7 Subsidies come in a variety of formats, both direct and (increasingly) indirect. Over the last 20 years Viet Nam has moved away from a system of direct subsidies to energy but pressures to keep prices low and stable are leading to more indirect methods. These indirect tools maybe more damaging to a government’s revenues and oversight of state assets as it is difficult to quantify these tools and analyse their financial impact, as we will see. There are a number of different approaches to identifying direct and indirect subsidies, for the purposes of this paper we have used a framework developed by the OECD (2002) and the UNEP (2008) who categorized subsidies into five key areas.8

a. Direct financial transfers: grants to consumers, grants to producers, low-interest or preferential loans and government loan guarantees;

b. Preferential tax treatment: tax credits, tax rebates, exemptions on royalties, duties or tariffs, reduced tax rates, deferred tax liabilities and accelerated depreciation on energy-supply equipment;

c. Trade restrictions: tariffs, tariff-rate import quotas and non-tariff trade barriers; d. Energy-related services provided directly by government at less than full cost: government-

provided energy infrastructure, public research and development on fossil fuels; and e. Regulation of the energy sector: demand guarantees, mandated deployment rates, price

controls, environmental regulations and market-access restrictions. To some degree each of these five methods are used in Viet Nam though direct transfers as illustrated in the first method above, are less common today. However, preferential loans to producers as well as loan guarantees are still strongly used for state owned enterprises in the energy sector such as PetroViet Nam, EVN and Vinacomin. The survey uses the above framework of direct and indirect subsidies when looking at fossil fuel use in electricity and transportation to identify where the subsidies are and their nature.

7 World Bank, IEA and OECD, 4:2008, “Analysis of the Scope of Energy Subsidies and Suggestions for the G-20

Initiative” 8 GSI/ iisd, 11:2010, “The Effects of Fossil-Fuel Subsidy Reform: A review of modeling and empirical studies”

4

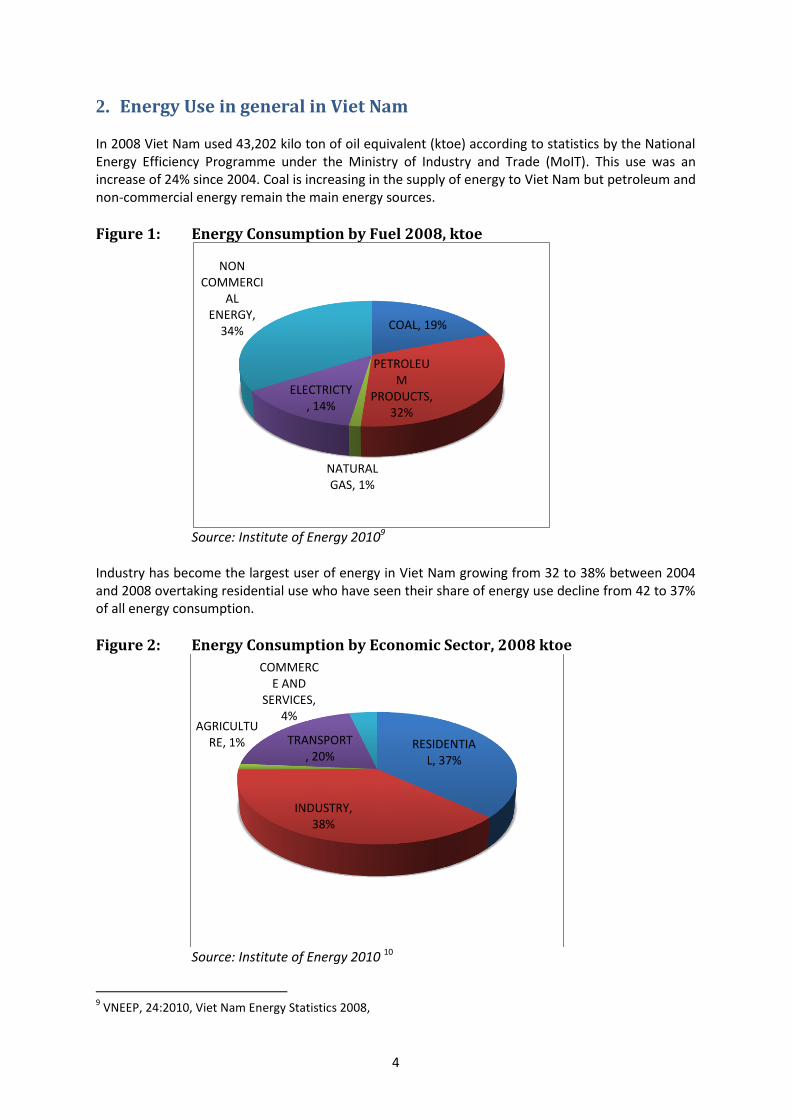

2. Energy Use in general in Viet Nam In 2008 Viet Nam used 43,202 kilo ton of oil equivalent (ktoe) according to statistics by the National Energy Efficiency Programme under the Ministry of Industry and Trade (MoIT). This use was an increase of 24% since 2004. Coal is increasing in the supply of energy to Viet Nam but petroleum and non-commercial energy remain the main energy sources.

Figure 1: Energy Consumption by Fuel 2008, ktoe

Source: Institute of Energy 20109

Industry has become the largest user of energy in Viet Nam growing from 32 to 38% between 2004 and 2008 overtaking residential use who have seen their share of energy use decline from 42 to 37% of all energy consumption.

Figure 2: Energy Consumption by Economic Sector, 2008 ktoe

Source: Institute of Energy 2010 10

9 VNEEP, 24:2010, Viet Nam Energy Statistics 2008,

COAL, 19%

PETROLEUM

PRODUCTS, 32%

NATURAL GAS, 1%

ELECTRICTY, 14%

NON COMMERCI

AL ENERGY,

34%

RESIDENTIAL, 37%

INDUSTRY, 38%

AGRICULTURE, 1% TRANSPORT

, 20%

COMMERCE AND

SERVICES, 4%

5

3. Electricity Generation and Use In Viet Nam Viet Nam’s electricity market remains a key sector for Viet Nam’s economic development and as a result gets considerable focus and guidance. The sector has seen considerable changes in electricity generation over the last decade and an increasing number of non EVN actors are entering the electricity sector, mostly other state owned enterprises such as Vinacomin and PetroVietnam. However, in the transmission and retail sector EVN continues to hold a monopoly position with no competition to be allowed for sometime to come. The sector has many challenges in meeting electricity demand as well as attracting investment. As a key sector and one that has a strong influence on economic growth as well as inflation the government has continued to treat the sector as a key area for National security and growth. Management has often focused on using EVN as a policy instrument ensuring that pricing is controlled to avoid negative affects on households as well as on inflation. Overall management of EVN’s operations has caused some concerns with EVN failing to invest adequately in its core business area of electricity generation while it is still allowed to invest in a broad range of non-core business interests, including banking and telecommunications. In recent years there have been no direct subsidies within the electricity sector, including electricity generation, the purchase of inputs for production, sales to EVN and then retail pricing. But different markets remain complex and price caps across the value chain imposed on different producers and input suppliers has a considerable effect on the market structure and demand for electricity by both household and industrial users. This section will firstly look closely at the current market structure for electricity as well as the future generation structure before looking at demand by users and different industries. We will then look at the market structure for electricity and analyse the impact of price capping on generation and retail sales. Due to the increased role that coal will play in electricity generation we will look closely at the coal industry and its importance for electricity generation.

3.1. Electricity generation in Viet Nam, 2009 Viet Nam’s electricity generation capacity has grown considerably over the last 15 years, from a generation capacity of just 2,796 MW in 1995 to 18,268 MW in 200911. This growth has continued since 2000 with electricity production growing from 26,562 million kwh in 2000 to 84,765 million kwh in 2009 (an average of 13.82% per year between 2000 and 2009)12.

10

VNEEP, 26:2010, Viet Nam Energy Statistics 2008,

11 ERAV data 2010

12 EVN production data, 2011

6

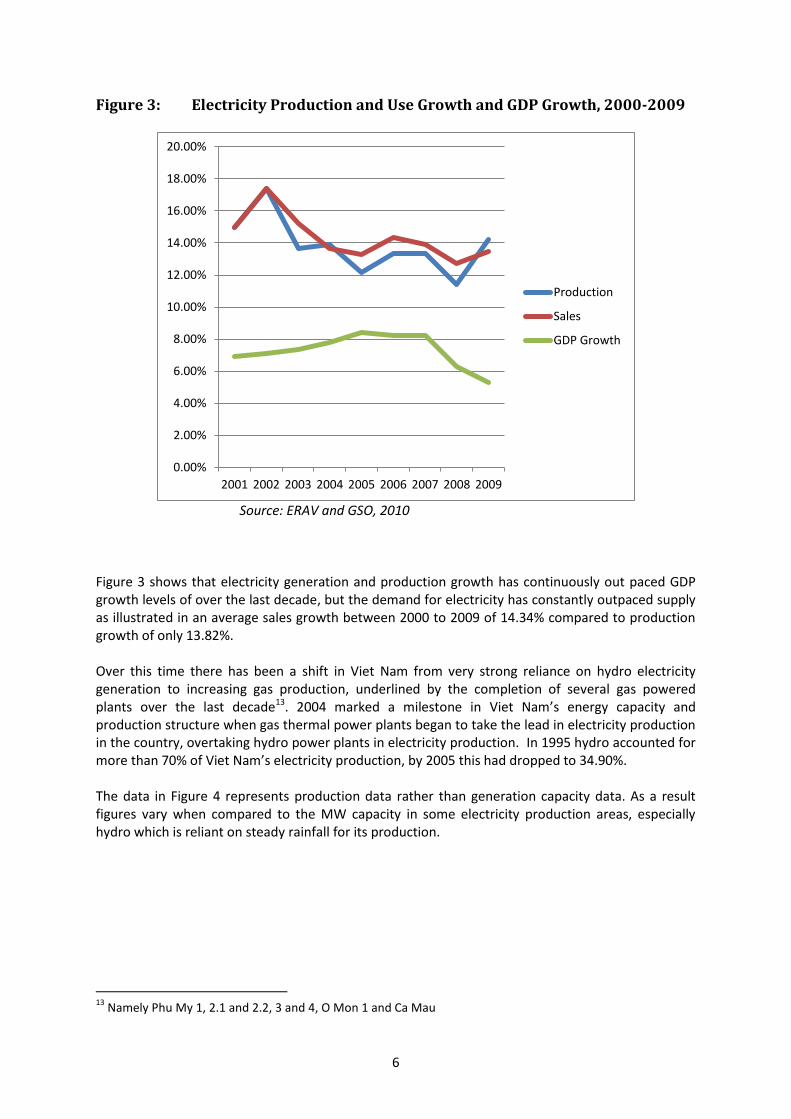

Figure 3: Electricity Production and Use Growth and GDP Growth, 2000-2009

Source: ERAV and GSO, 2010 Figure 3 shows that electricity generation and production growth has continuously out paced GDP growth levels of over the last decade, but the demand for electricity has constantly outpaced supply as illustrated in an average sales growth between 2000 to 2009 of 14.34% compared to production growth of only 13.82%. Over this time there has been a shift in Viet Nam from very strong reliance on hydro electricity generation to increasing gas production, underlined by the completion of several gas powered plants over the last decade13. 2004 marked a milestone in Viet Nam’s energy capacity and production structure when gas thermal power plants began to take the lead in electricity production in the country, overtaking hydro power plants in electricity production. In 1995 hydro accounted for more than 70% of Viet Nam’s electricity production, by 2005 this had dropped to 34.90%. The data in Figure 4 represents production data rather than generation capacity data. As a result figures vary when compared to the MW capacity in some electricity production areas, especially hydro which is reliant on steady rainfall for its production.

13

Namely Phu My 1, 2.1 and 2.2, 3 and 4, O Mon 1 and Ca Mau

0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

12.00%

14.00%

16.00%

18.00%

20.00%

2001 2002 2003 2004 2005 2006 2007 2008 2009

Production

Sales

GDP Growth

7

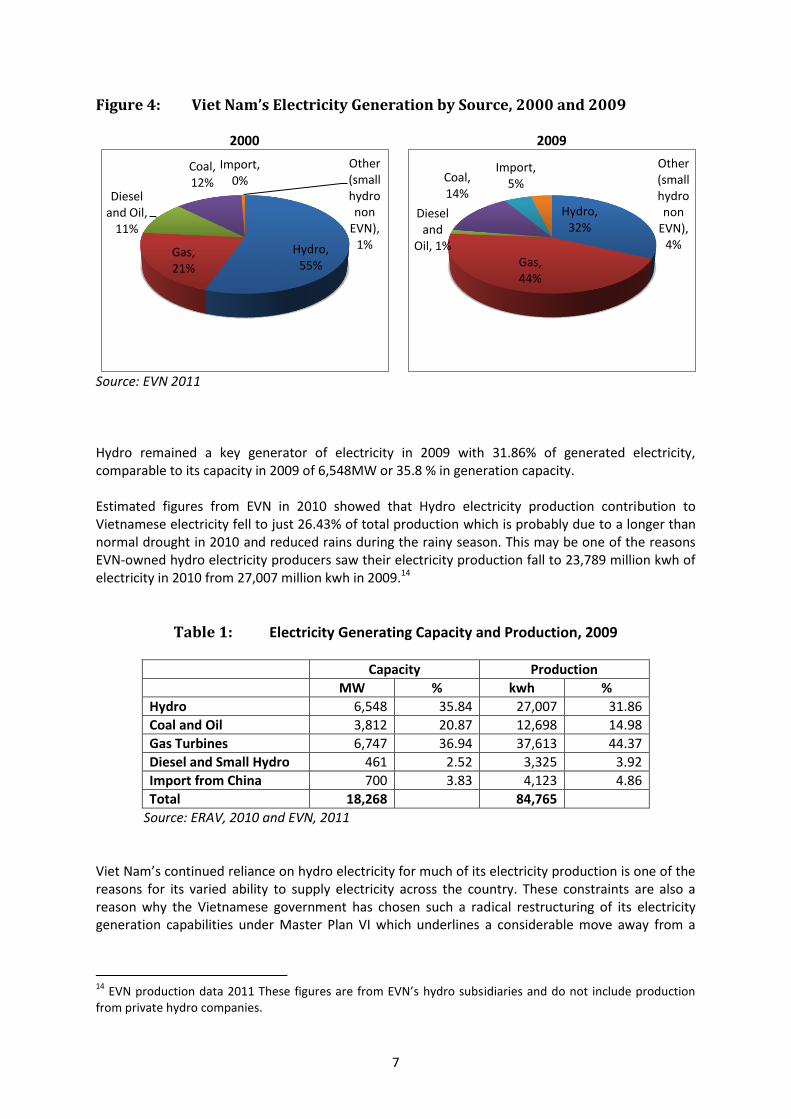

Figure 4: Viet Nam’s Electricity Generation by Source, 2000 and 2009

2000 2009

Source: EVN 2011 Hydro remained a key generator of electricity in 2009 with 31.86% of generated electricity, comparable to its capacity in 2009 of 6,548MW or 35.8 % in generation capacity. Estimated figures from EVN in 2010 showed that Hydro electricity production contribution to Vietnamese electricity fell to just 26.43% of total production which is probably due to a longer than normal drought in 2010 and reduced rains during the rainy season. This may be one of the reasons EVN-owned hydro electricity producers saw their electricity production fall to 23,789 million kwh of electricity in 2010 from 27,007 million kwh in 2009.14

Table 1: Electricity Generating Capacity and Production, 2009

Capacity Production

MW % kwh %

Hydro 6,548 35.84 27,007 31.86

Coal and Oil 3,812 20.87 12,698 14.98

Gas Turbines 6,747 36.94 37,613 44.37

Diesel and Small Hydro 461 2.52 3,325 3.92

Import from China 700 3.83 4,123 4.86

Total 18,268 84,765

Source: ERAV, 2010 and EVN, 2011 Viet Nam’s continued reliance on hydro electricity for much of its electricity production is one of the reasons for its varied ability to supply electricity across the country. These constraints are also a reason why the Vietnamese government has chosen such a radical restructuring of its electricity generation capabilities under Master Plan VI which underlines a considerable move away from a

14

EVN production data 2011 These figures are from EVN’s hydro subsidiaries and do not include production from private hydro companies.

Hydro, 55%

Gas, 21%

Diesel and Oil,

11%

Coal, 12%

Import, 0%

Other (small hydro non

EVN), 1%

Hydro, 32%

Gas, 44%

Diesel and

Oil, 1%

Coal, 14%

Import, 5%

Other (small hydro non

EVN), 4%

8

reliance on hydro and gas electricity generation towards increased coal powered electricity production. The sixth Master Plan for Power Development states the following principles for the development of the electricity sector without giving a rational for the move towards coal over other forms of electricity generation. The development of electric facilities must meet the demand of load as mentioned

above (growth levels); it must ensure the construction schedules of hydro-electric plants that offer the general benefits such as: flood control, water supply, electric generation; there must be rational & efficient development of gas-operated electric plants & acceleration in the construction of thermal electric plants;15

It goes on to suggest that the development of small hydro and renewable energy will only be developed to service remote areas.

Development of small-scale hydroelectric plants, use of renewable energy & recycled materials for electric generation to serve the remote & far flung regions, mountainous areas, border land, sea islands16

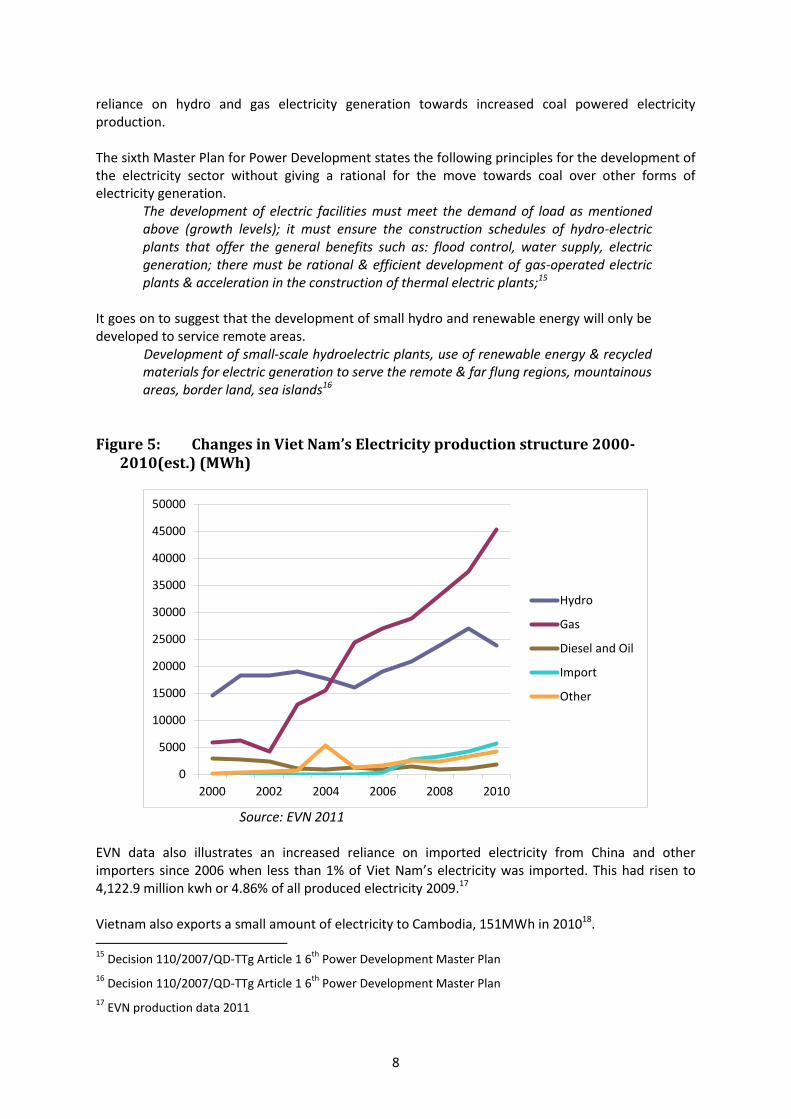

Figure 5: Changes in Viet Nam’s Electricity production structure 2000-2010(est.) (MWh)

Source: EVN 2011 EVN data also illustrates an increased reliance on imported electricity from China and other importers since 2006 when less than 1% of Viet Nam’s electricity was imported. This had risen to 4,122.9 million kwh or 4.86% of all produced electricity 2009.17 Vietnam also exports a small amount of electricity to Cambodia, 151MWh in 201018. 15

Decision 110/2007/QD-TTg Article 1 6th

Power Development Master Plan

16 Decision 110/2007/QD-TTg Article 1 6

th Power Development Master Plan

17 EVN production data 2011

0

5000

10000

15000

20000

25000

30000

35000

40000

45000

50000

2000 2002 2004 2006 2008 2010

Hydro

Gas

Diesel and Oil

Import

Other

9

3.2. Master plan directions The National Plan for Electric Power Development, National Plan VI19 outlines the Vietnamese government’s strategy for electricity generation from 2006 to 2015 with consideration to 2025. A seventh national plan has been drafted by the Ministry of Industry and Trade (MOIT) and is, at the time of writing, with the Prime Minster for consideration. Stakeholders interviewed believe the VII National plan will not deviate too much from the VI plan. The national plan is detailed in its identification of plants to be built over the 2006 to 2015 period and also assigns responsibility to a variety of agencies, such as EVN, Vinacomin, Lilama and construction and contract options such as BOO/ BOT. There is a recognition that the National Plan is some way behind schedule due to limited access to finance for many large state owned enterprises as well as limited interest in investment in the power sector in Viet Nam due to a regressive pricing structure that favors equitable access to electricity but which is forcing prices increasingly below generation costs. This will be discussed further on in the report. With electricity demand and generation growth due to increase considerably between 2006 and 2015, and on to 2025, considerable investment is also needed in the electricity industry. The World Bank estimated in 2008 that Viet Nam would need to invest $4 billion annually between 2006 and 2020 in order to develop the electricity generation, transmission and retail sectors20.

Table 2: Viet Nam energy capacity projections, 2009 to 2025

Actual National Plan VI goals

2009 2010 2015 2020 2025

Total MW 18,268 26,000 40,770 60,300 85,200

5-year period Increase 57% 48% 41%

Source: ERAV 2009 and the National Plan VI, 2010 to 2025 EVN has found it difficult to meet its responsibilities under the National Plan VI and announced in 2008 that it would be handing back planned investments in 13 power plants due to a shortage of finances21. EVN continues to account for most electricity generation in Viet Nam, i.e. for 67.25% in 200922, though this share is steadily decreasing. PetroVietnam, Vinacomin and Lilama as well as several small hydro companies and generators that are providing industrial parks are increasingly expanding their electricity generation capacity and reducing EVN’s generation market share.

18

http://vietnambusiness.asia/vietnam-provides-nearly-70pct-of-cambodias-electricity-import/

19 Decision 110/2007 Sixth Power Development Master Plan. At the time of writing this paper the Seventh

Master Plan was not yet available but has since been published

20 World Bank 2008, Project Appraisal Document Rural Distribution Program

21 http://asianenergy.blogspot.com/2008/11/vietnam-to-allow-foreign-companies-for.html

22 EVN production data 2011

10

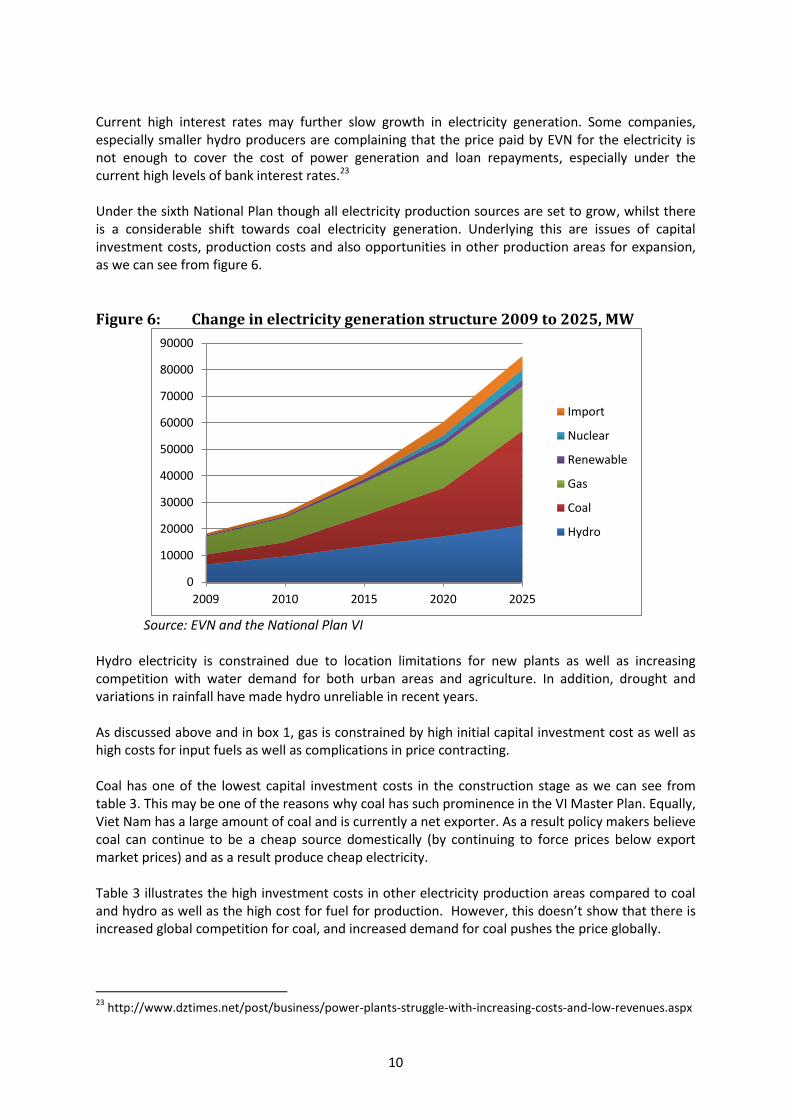

Current high interest rates may further slow growth in electricity generation. Some companies, especially smaller hydro producers are complaining that the price paid by EVN for the electricity is not enough to cover the cost of power generation and loan repayments, especially under the current high levels of bank interest rates.23 Under the sixth National Plan though all electricity production sources are set to grow, whilst there is a considerable shift towards coal electricity generation. Underlying this are issues of capital investment costs, production costs and also opportunities in other production areas for expansion, as we can see from figure 6.

Figure 6: Change in electricity generation structure 2009 to 2025, MW

Source: EVN and the National Plan VI Hydro electricity is constrained due to location limitations for new plants as well as increasing competition with water demand for both urban areas and agriculture. In addition, drought and variations in rainfall have made hydro unreliable in recent years. As discussed above and in box 1, gas is constrained by high initial capital investment cost as well as high costs for input fuels as well as complications in price contracting. Coal has one of the lowest capital investment costs in the construction stage as we can see from table 3. This may be one of the reasons why coal has such prominence in the VI Master Plan. Equally, Viet Nam has a large amount of coal and is currently a net exporter. As a result policy makers believe coal can continue to be a cheap source domestically (by continuing to force prices below export market prices) and as a result produce cheap electricity. Table 3 illustrates the high investment costs in other electricity production areas compared to coal and hydro as well as the high cost for fuel for production. However, this doesn’t show that there is increased global competition for coal, and increased demand for coal pushes the price globally.

23

http://www.dztimes.net/post/business/power-plants-struggle-with-increasing-costs-and-low-revenues.aspx

0

10000

20000

30000

40000

50000

60000

70000

80000

90000

2009 2010 2015 2020 2025

Import

Nuclear

Renewable

Gas

Coal

Hydro

11

Table 3: Total Costs of Generating Electricity in US cents per Kilowatt-hour Fixed Fuel O&M Total

Hydro 3.5 -- 0.2 3.7

Large Coal 2.0 4.2 0.8 7.0

Chinese Coal 1.2 4.3 1.0 6.5

Combined Cycle Gas 1.2 6.7 0.4 8.3

Gas Turbine 2.6 9.0 0.7 12.3

Diesel 1.6 30.0 1.0 32.6

Source: David Dapice, 200824

BOX 1: Gas and Power in Viet Nam Gas may offer an opportunity for expansion with estimated production rising from 6.9 bcm in 2005 to 9.1bcm in 2010 and estimated to reach 22 bcm by 201525. In the past, infrastructure and investment in gas pipelines has constrained the expansion of gas for electricity in Viet Nam. The US$1.3 billion Nam Con Son Pipeline, Viet Nam’s first gas pipeline, came online in 2002 and transfers 4 billion cubic meters of gas annually from Bloc 6.1 in the Nam Con Son Basin along a 362km high pressure offshore pipeline. A second $1 billion pipeline from Block B in Southern Vietnamese waters was announced in 2010 and is to be built by PetroVietnam and Chevron. Demand for gas is growing and the National Plan VI continues to see an increasing role for gas in electricity generation in Viet Nam, but constraints continue. Infrastructure and finalisation of gas to power agreements remain problematic. The Chevron/ PetroVietnam pipeline power deal was two years overdue. Changes in gas pricing between gas suppliers and users are also problematic. In 2009 changes in gas prices from the Cuu Long Basin fields required Prime Ministerial approval and a recommendation from both the Ministry of Finance and the Ministry of Industry and Trade26. PVN had called for higher prices due to increased gas field maintenance costs in the field.27 The newly approved Gas Development Master plan 2016 to 202528, attempts to address some of these pricing concerns and establishes a pricing framework that will see gas pricing for electricity and household use move to a more competitive structure. 90% of the gas produced in Viet Nam is used for power generation29.

24

Dapice notes that these prices are indicative based and can change based on a different set of assumptions from those in the paper.

25 BMI, 2011, Viet Nam Oil and Gas Report Quarter 1, 2011. Gas reserves are estimated by BMI to have been

557 bcm and may rise to 630 bcm.

26 http://www.monre.gov.vn/v35/default.aspx?tabid=675&CateID=57&ID=65641&Code=SMNGX65641

27 World Bank, 2010, Viet Nam Gas Sector Development Framework

28 Decision 459/QD-TTg, “Master plan for the development of the gas industry in Viet Nam, to 2015 and

orientation to 2025”

29 World Bank xv:2010

12

3.2.1. Constraints in meeting National Plan VI

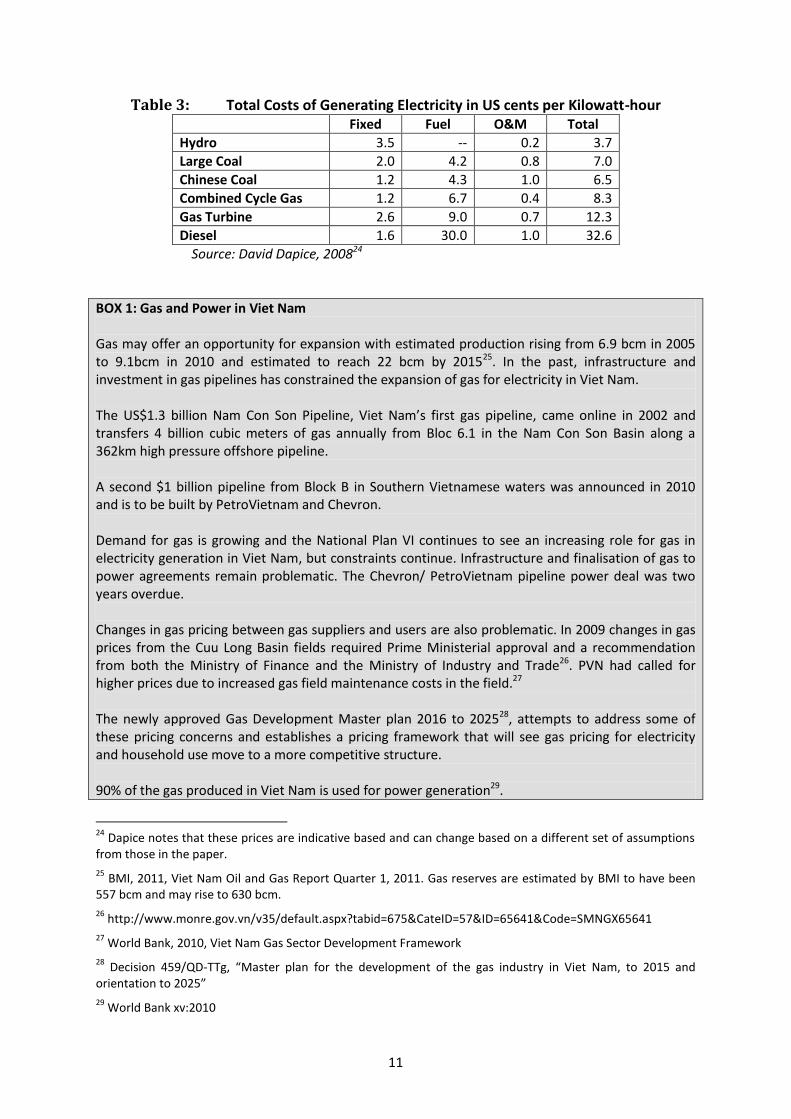

The growth in the development of electricity generation as well as the change in structure in electricity generation as laid out in National Plan VI may find itself hindered by constraints in the electricity market. These constraints will not only hinder the development of the plan and the achievement of its goals but are also underlying the general failure for Viet Nam’s electricity market to grow at the same rate as demand for electricity. Firstly, despite increased competition in the generation market and the declining monopoly of EVN, the economic group continues to control the wholesale electricity purchase markets as well as the retail market. This control and EVNs role as generator and buyer as well as retailer, and conflicts of interest in the form of EVN’s own power generating units, means there is an inherent bias for EVN to purchase electricity from its own subsidiaries. Secondly, the levels of investment needed in the electricity sector for generation, transmission and distribution are beyond the capabilities of Electricity Viet Nam (EVN). The current pricing system makes investment in the Vietnamese electricity market unattractive, as returns on investment are both low and uncertain. Thirdly, as mentioned, Viet Nam’s electricity pricing system does not yet reflect production costs and low prices are unattractive for investors including EVN as well as domestic and international investors. The proposal for the changes and increased market competition planned for June/ July 2011 will implement a complicated sales structure for generators to the sole retailer EVN, though retail prices to users can now be adjusted on a quarterly basis. Finally, Viet Nam continues to rely on and invest in hydroelectric power plants for a large percentage of electricity generation. Fluctuations in rainfall as well as demands from agriculture mean investments in hydro plants operate at levels considerably under design capacity. Furthermore, the considerable move into coal power generation will have both an environment and economic costs. The environmental cost is well known, but as Viet Nam begins to move to becoming a net coal importer (by 2012 by some accounts), it will begin to compete for coal in an increasingly challenging international market. Figure 7 shows the electricity generation sources for the world, Viet Nam and China. Unsurprisingly, world sources of electricity show a wide a variety, and coal is the leading source of electricity. In some ways Viet Nam’s move towards an increased role of coal for electricity generation mirrors that of the current global situation. China however is a very different case who rely on coal for over 70 % of their electricity production as discussed in box 3.

13

Figure 7: Production comparison, the World, China and Viet Nam

Source: IEA, 2010 World data, Chinese Academy of Engineering, 2007, EVN, 2010

3.3. The Electricity Market in Viet Nam

3.3.1. The Role of EVN State owned enterprise Electricity Viet Nam (EVN) continues to dominate the electricity market, including generation, transmission and retail. The 2004 Electricity Law does lay out a long-term vision for the restructuring of the electricity market, between 2005 and 2025 but postpones the opportunity for other actors to take part in retail until 2022 or 2024.

Coal/ Peat

Coal/ Peat

Coal/ Peat

Oil

Oil

Gas

Gas

Gas

Nuclear Nuclear

Nuclear

Hydro Hydro

Hydro

Import Import

Import

Other Other Other

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

World China Vietnam

2008 2010 2009

Other

Import

Hydro

Nuclear

Gas

Oil

Coal/ Peat

14

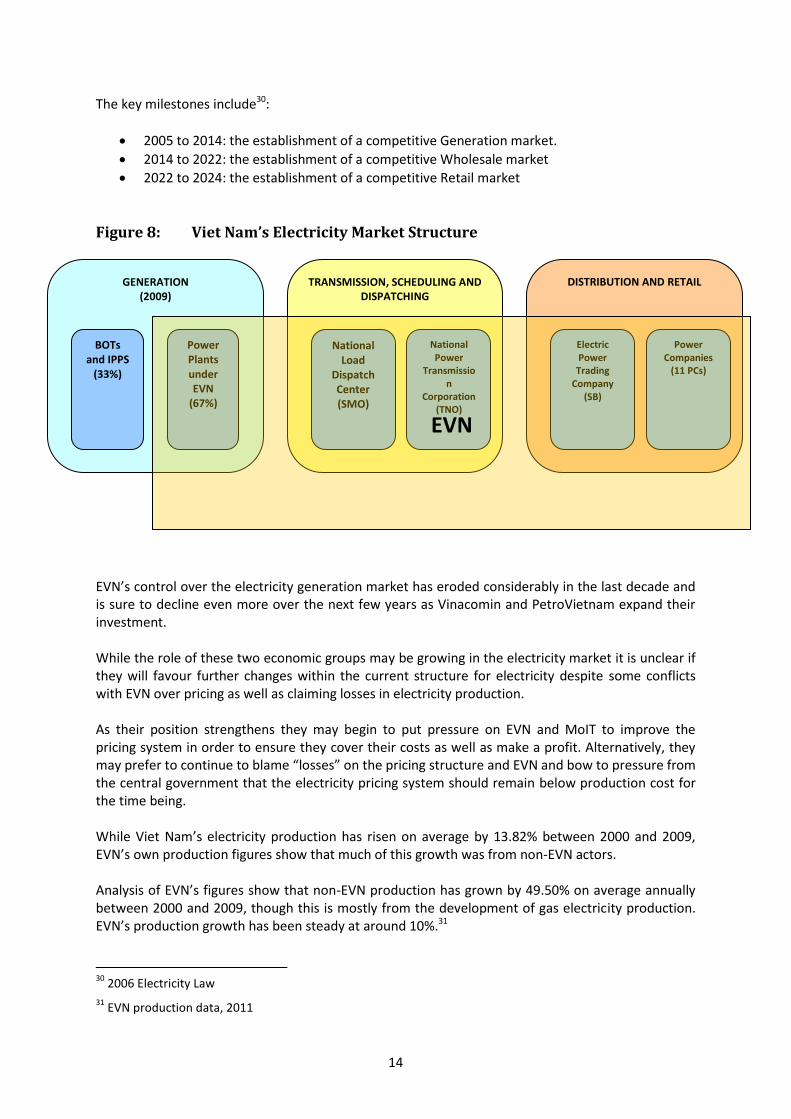

The key milestones include30:

2005 to 2014: the establishment of a competitive Generation market.

2014 to 2022: the establishment of a competitive Wholesale market

2022 to 2024: the establishment of a competitive Retail market

Figure 8: Viet Nam’s Electricity Market Structure

EVN’s control over the electricity generation market has eroded considerably in the last decade and is sure to decline even more over the next few years as Vinacomin and PetroVietnam expand their investment. While the role of these two economic groups may be growing in the electricity market it is unclear if they will favour further changes within the current structure for electricity despite some conflicts with EVN over pricing as well as claiming losses in electricity production. As their position strengthens they may begin to put pressure on EVN and MoIT to improve the pricing system in order to ensure they cover their costs as well as make a profit. Alternatively, they may prefer to continue to blame “losses” on the pricing structure and EVN and bow to pressure from the central government that the electricity pricing system should remain below production cost for the time being. While Viet Nam’s electricity production has risen on average by 13.82% between 2000 and 2009, EVN’s own production figures show that much of this growth was from non-EVN actors. Analysis of EVN’s figures show that non-EVN production has grown by 49.50% on average annually between 2000 and 2009, though this is mostly from the development of gas electricity production. EVN’s production growth has been steady at around 10%.31

30

2006 Electricity Law

31 EVN production data, 2011

GENERATION (2009)

TRANSMISSION, SCHEDULING AND DISPATCHING

DISTRIBUTION AND RETAIL

BOTs and IPPS

(33%)

Power Plants under EVN

(67%)

National Load

Dispatch Center (SMO)

National Power

Transmission

Corporation (TNO)

Electric Power Trading

Company (SB)

Power Companies

(11 PCs)

EVN

15

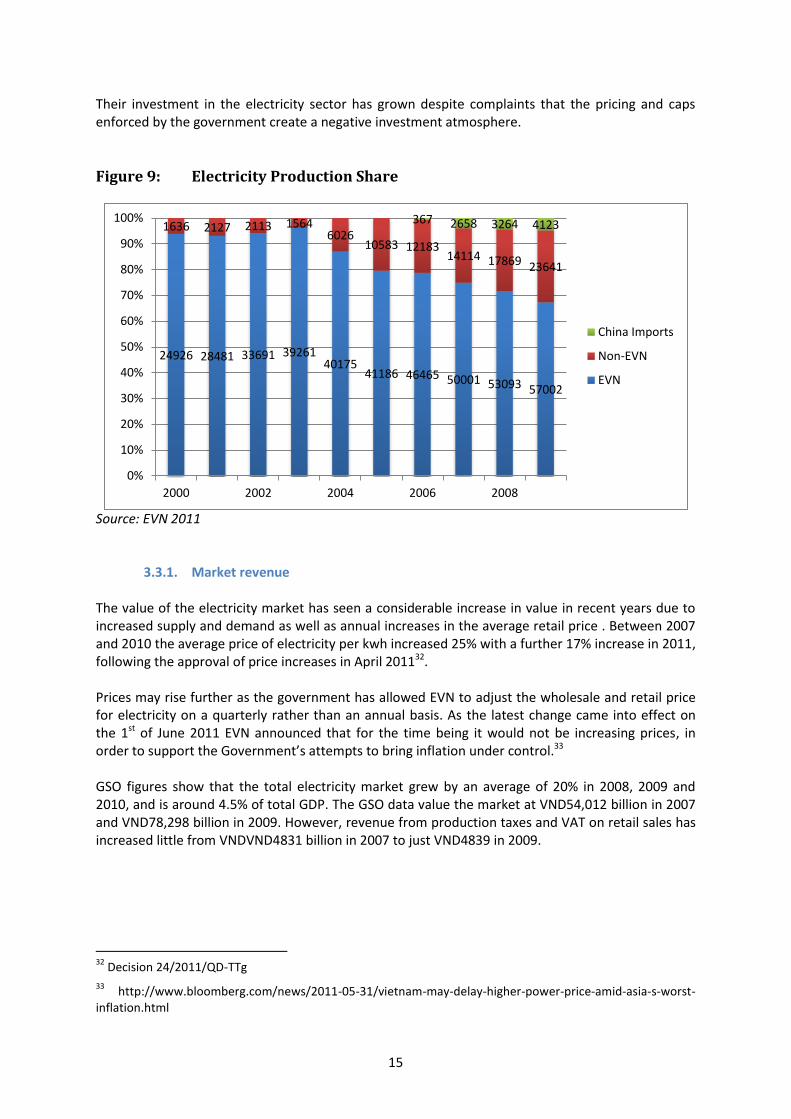

Their investment in the electricity sector has grown despite complaints that the pricing and caps enforced by the government create a negative investment atmosphere.

Figure 9: Electricity Production Share

Source: EVN 2011

3.3.1. Market revenue The value of the electricity market has seen a considerable increase in value in recent years due to increased supply and demand as well as annual increases in the average retail price . Between 2007 and 2010 the average price of electricity per kwh increased 25% with a further 17% increase in 2011, following the approval of price increases in April 201132. Prices may rise further as the government has allowed EVN to adjust the wholesale and retail price for electricity on a quarterly rather than an annual basis. As the latest change came into effect on the 1st of June 2011 EVN announced that for the time being it would not be increasing prices, in order to support the Government’s attempts to bring inflation under control.33 GSO figures show that the total electricity market grew by an average of 20% in 2008, 2009 and 2010, and is around 4.5% of total GDP. The GSO data value the market at VND54,012 billion in 2007 and VND78,298 billion in 2009. However, revenue from production taxes and VAT on retail sales has increased little from VNDVND4831 billion in 2007 to just VND4839 in 2009.

32

Decision 24/2011/QD-TTg

33 http://www.bloomberg.com/news/2011-05-31/vietnam-may-delay-higher-power-price-amid-asia-s-worst-

inflation.html

24926 28481 33691 39261 40175

41186 46465 50001 53093 57002

1636 2127 2113 1564 6026

10583 12183 14114 17869 23641

367 2658 3264 4123

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2000 2002 2004 2006 2008

China Imports

Non-EVN

EVN

16

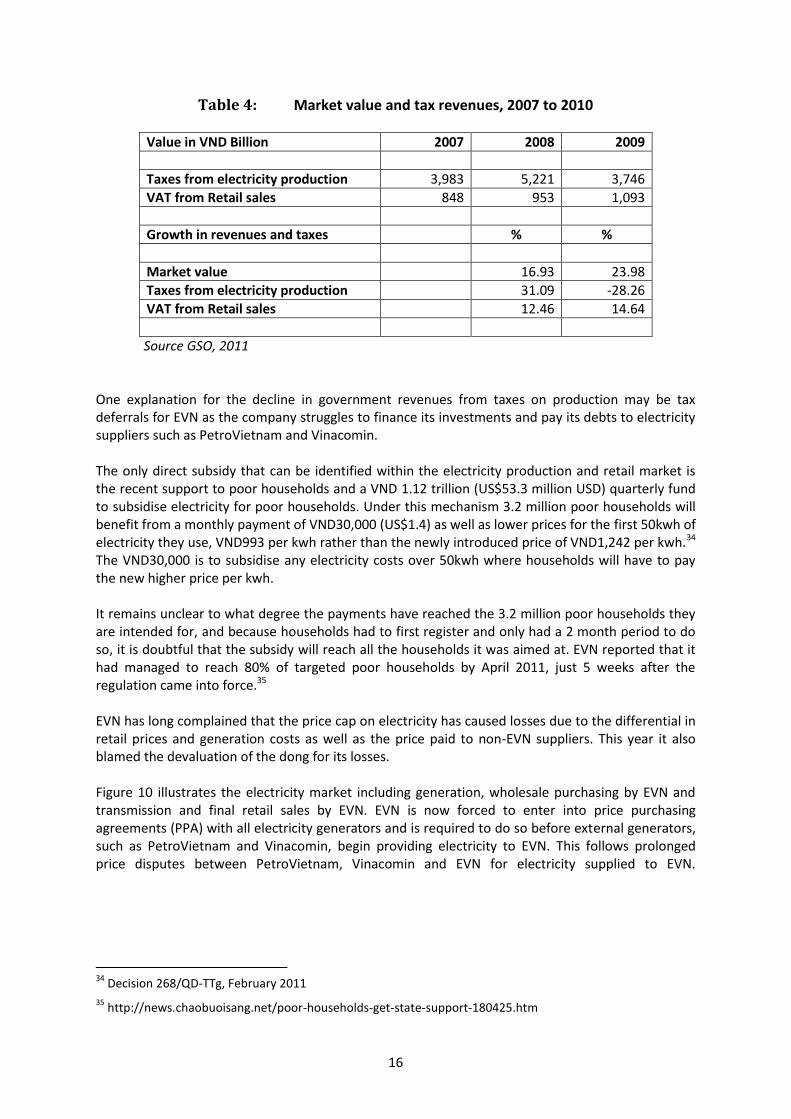

Table 4: Market value and tax revenues, 2007 to 2010

Value in VND Billion 2007 2008 2009

Taxes from electricity production 3,983 5,221 3,746

VAT from Retail sales 848 953 1,093

Growth in revenues and taxes % %

Market value 16.93 23.98

Taxes from electricity production 31.09 -28.26

VAT from Retail sales 12.46 14.64

Source GSO, 2011 One explanation for the decline in government revenues from taxes on production may be tax deferrals for EVN as the company struggles to finance its investments and pay its debts to electricity suppliers such as PetroVietnam and Vinacomin. The only direct subsidy that can be identified within the electricity production and retail market is the recent support to poor households and a VND 1.12 trillion (US$53.3 million USD) quarterly fund to subsidise electricity for poor households. Under this mechanism 3.2 million poor households will benefit from a monthly payment of VND30,000 (US$1.4) as well as lower prices for the first 50kwh of electricity they use, VND993 per kwh rather than the newly introduced price of VND1,242 per kwh.34 The VND30,000 is to subsidise any electricity costs over 50kwh where households will have to pay the new higher price per kwh. It remains unclear to what degree the payments have reached the 3.2 million poor households they are intended for, and because households had to first register and only had a 2 month period to do so, it is doubtful that the subsidy will reach all the households it was aimed at. EVN reported that it had managed to reach 80% of targeted poor households by April 2011, just 5 weeks after the regulation came into force.35 EVN has long complained that the price cap on electricity has caused losses due to the differential in retail prices and generation costs as well as the price paid to non-EVN suppliers. This year it also blamed the devaluation of the dong for its losses. Figure 10 illustrates the electricity market including generation, wholesale purchasing by EVN and transmission and final retail sales by EVN. EVN is now forced to enter into price purchasing agreements (PPA) with all electricity generators and is required to do so before external generators, such as PetroVietnam and Vinacomin, begin providing electricity to EVN. This follows prolonged price disputes between PetroVietnam, Vinacomin and EVN for electricity supplied to EVN.

34

Decision 268/QD-TTg, February 2011

35 http://news.chaobuoisang.net/poor-households-get-state-support-180425.htm

17

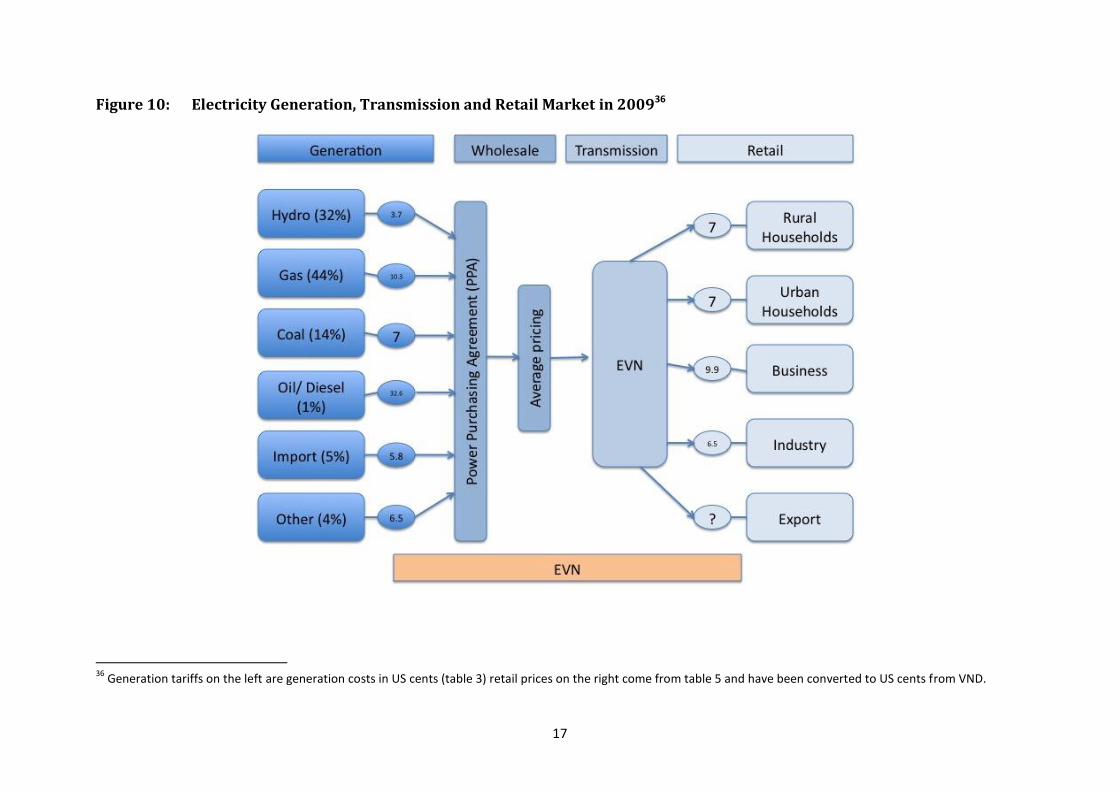

Figure 10: Electricity Generation, Transmission and Retail Market in 200936

36

Generation tariffs on the left are generation costs in US cents (table 3) retail prices on the right come from table 5 and have been converted to US cents from VND.

18

As we have discussed the wholesale price cap of VND891.4 kwh detailed in Circular 05/2011/TT-BCT dictates the price that EVN is prepared to pay electricity producers. The same Circular dictates the retail price for 2011 of VND1,242 kwh. EVN is now allowed to review electricity prices on a quarterly rather than a annual basis. It is also allowed to increase prices up to 5% on a quarterly basis without approval from the MoF, but above this EVN needs to seek government approval. Decision 24/2011 allows EVN to increase electricity prices by 20% per year without seeking government approval37. Previously EVN lobbied the government annually for price rises and the final decision on increases were made by the Government.

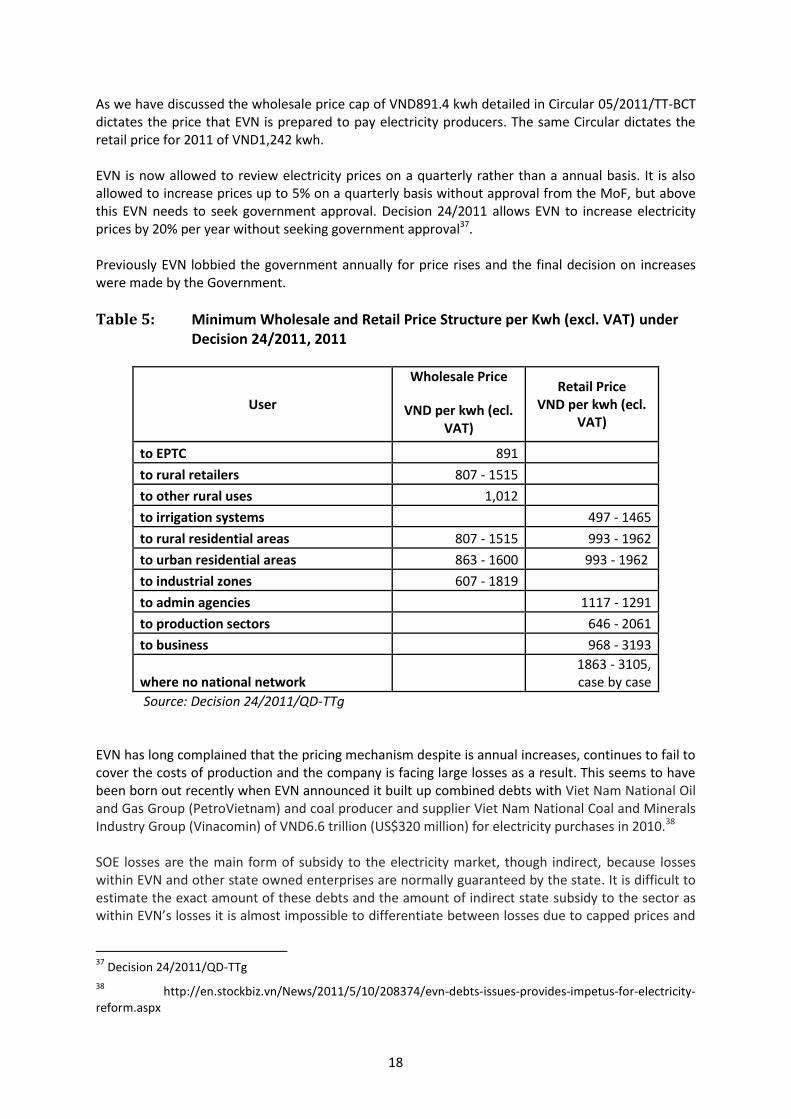

Table 5: Minimum Wholesale and Retail Price Structure per Kwh (excl. VAT) under Decision 24/2011, 2011

User

Wholesale Price

VND per kwh (ecl. VAT)

Retail Price VND per kwh (ecl.

VAT)

to EPTC 891

to rural retailers 807 - 1515

to other rural uses 1,012

to irrigation systems 497 - 1465

to rural residential areas 807 - 1515 993 - 1962

to urban residential areas 863 - 1600 993 - 1962

to industrial zones 607 - 1819

to admin agencies 1117 - 1291

to production sectors 646 - 2061

to business 968 - 3193

where no national network 1863 - 3105, case by case

Source: Decision 24/2011/QD-TTg EVN has long complained that the pricing mechanism despite is annual increases, continues to fail to cover the costs of production and the company is facing large losses as a result. This seems to have been born out recently when EVN announced it built up combined debts with Viet Nam National Oil and Gas Group (PetroVietnam) and coal producer and supplier Viet Nam National Coal and Minerals Industry Group (Vinacomin) of VND6.6 trillion (US$320 million) for electricity purchases in 2010.38 SOE losses are the main form of subsidy to the electricity market, though indirect, because losses within EVN and other state owned enterprises are normally guaranteed by the state. It is difficult to estimate the exact amount of these debts and the amount of indirect state subsidy to the sector as within EVN’s losses it is almost impossible to differentiate between losses due to capped prices and

37

Decision 24/2011/QD-TTg

38 http://en.stockbiz.vn/News/2011/5/10/208374/evn-debts-issues-provides-impetus-for-electricity-

reform.aspx

19

the structure of the electricity market and inefficiencies in EVN’s management, poor investment and operating decisions. This form of subsidy, allowing losses by a company does not clearly fall within the OECD framework introduced in section 1.3. Enterprise losses may fall most closely into category a. of direct financial transfers to producers and soft loans, as losses will ultimately be covered by the Government (see section1.3). However, the below market price for electricity also acts as an indirect transfer to consumers. One way to identify to what degree Viet Nam’s pricing structure is causing losses is to compare Viet Nam’s electricity prices with other countries in the region or a regional average. This helps identify some losses (and gains) in the market due to the pricing structure as well as state revenue losses (or gains) due to a below region pricing structure. This is however, just indicative and may not correctly reflect losses (or gains) due to the current price cap structure as other countries in the region may have considerably different power generation source structures (hydro, gas, coal, oil etc.), which in turn allow countries to charge higher or lower prices than Viet Nam. At the same time the region has a varied level of competition in the electricity sector, which will also affect prices.

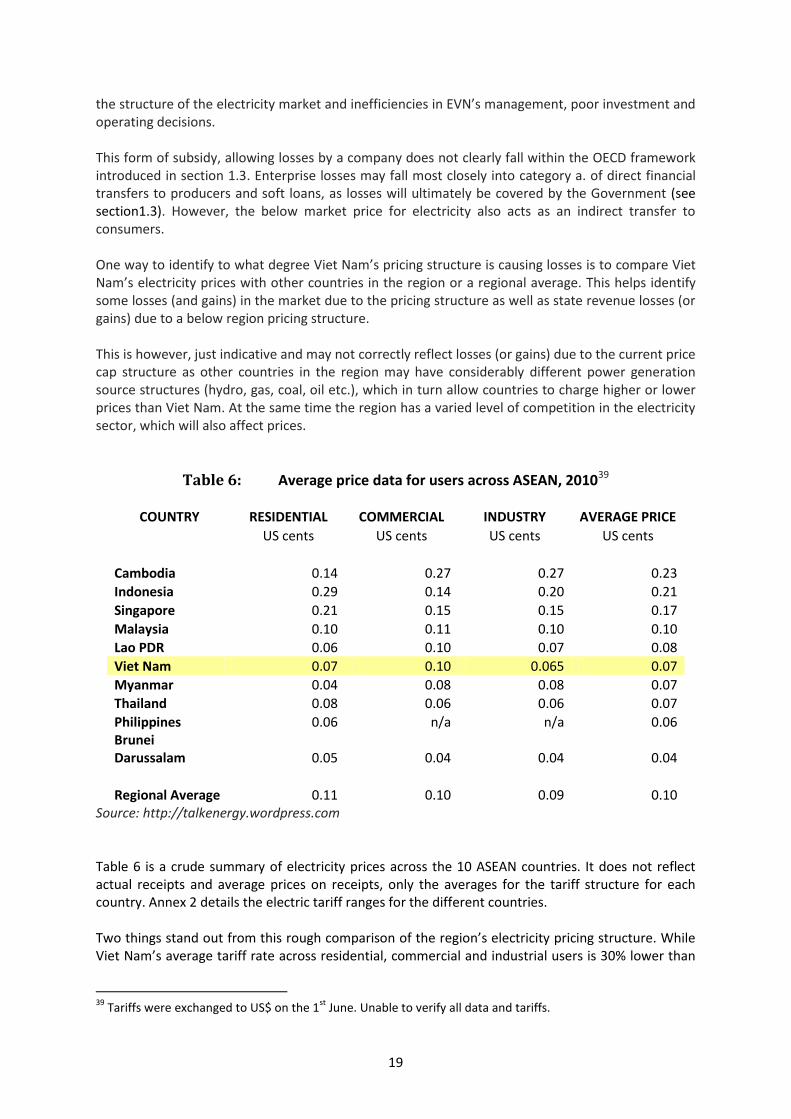

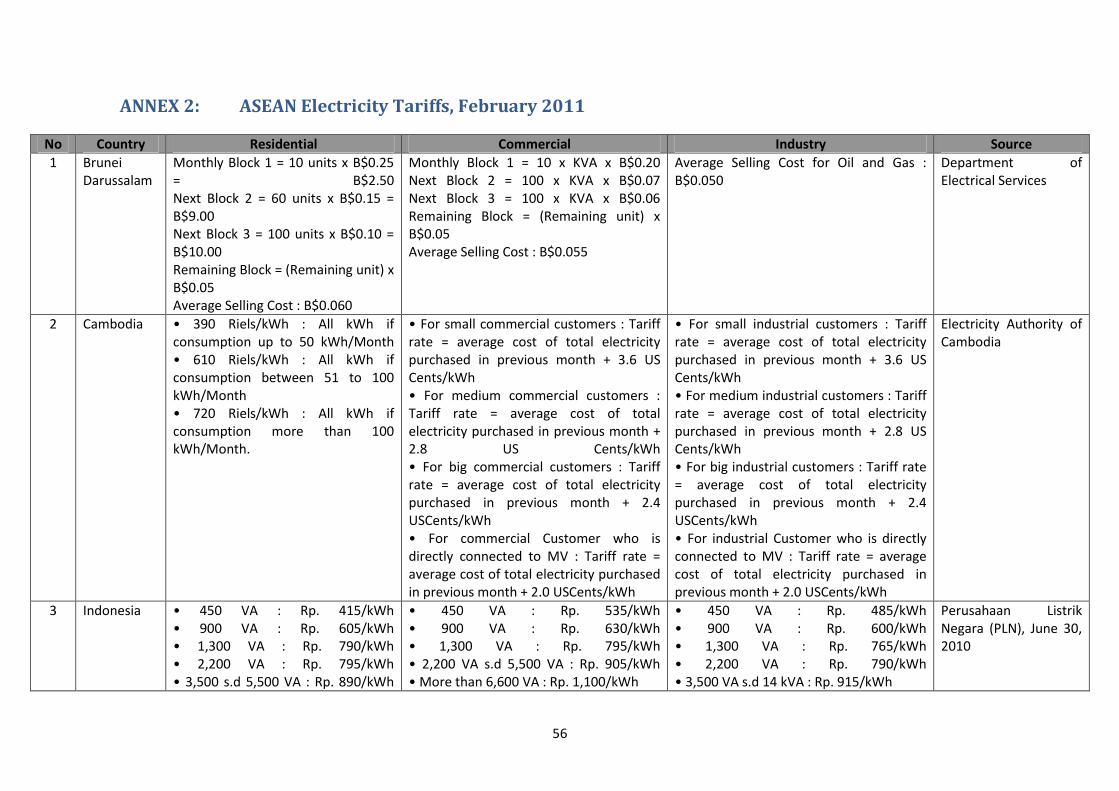

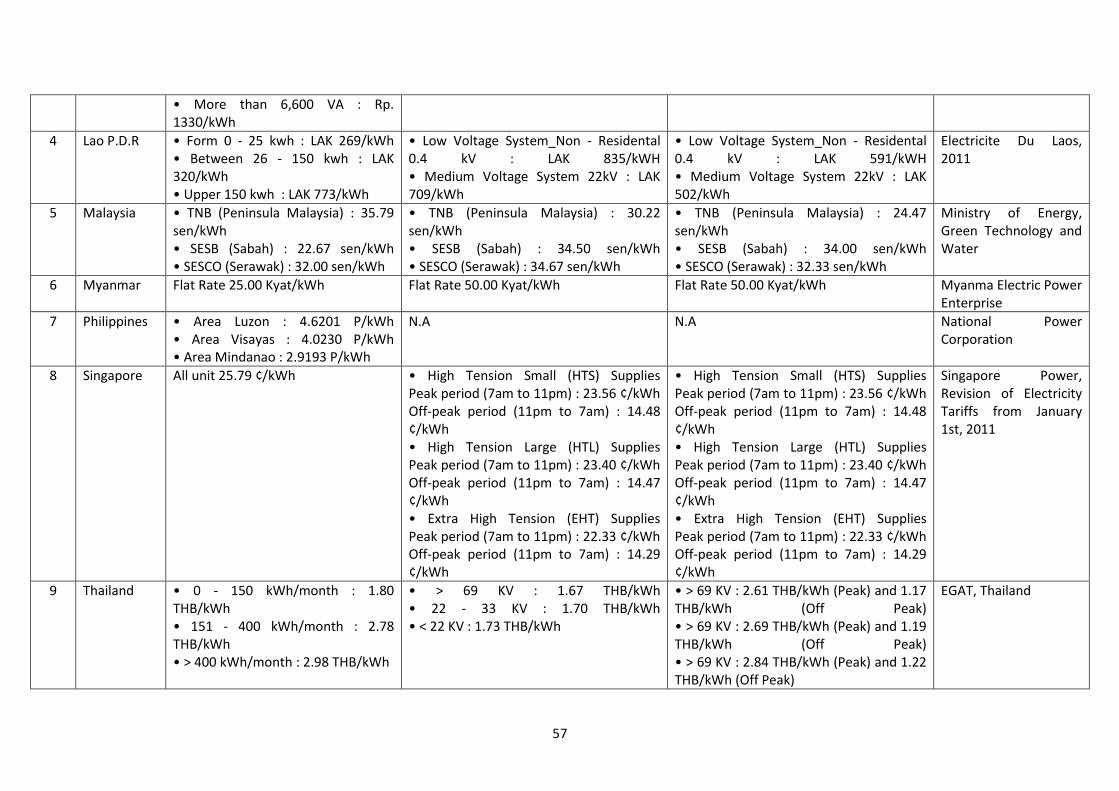

Table 6: Average price data for users across ASEAN, 201039

COUNTRY RESIDENTIAL COMMERCIAL INDUSTRY AVERAGE PRICE

US cents US cents US cents US cents

Cambodia 0.14 0.27 0.27 0.23

Indonesia 0.29 0.14 0.20 0.21

Singapore 0.21 0.15 0.15 0.17

Malaysia 0.10 0.11 0.10 0.10

Lao PDR 0.06 0.10 0.07 0.08

Viet Nam 0.07 0.10 0.065 0.07

Myanmar 0.04 0.08 0.08 0.07

Thailand 0.08 0.06 0.06 0.07

Philippines 0.06 n/a n/a 0.06 Brunei Darussalam 0.05 0.04 0.04 0.04

Regional Average 0.11 0.10 0.09 0.10 Source: http://talkenergy.wordpress.com Table 6 is a crude summary of electricity prices across the 10 ASEAN countries. It does not reflect actual receipts and average prices on receipts, only the averages for the tariff structure for each country. Annex 2 details the electric tariff ranges for the different countries. Two things stand out from this rough comparison of the region’s electricity pricing structure. While Viet Nam’s average tariff rate across residential, commercial and industrial users is 30% lower than

39

Tariffs were exchanged to US$ on the 1st

June. Unable to verify all data and tariffs.

20

the regional average it is in line with several comparator countries, namely Thailand and the Philippines. The comparison also shows that residential tariffs are 65% of the regional average less than those in Thailand and Malaysia but higher than those in the Philippines. Industrial tariffs show a similar pattern and amount to 72% of the regional average tariff and is lower than rates in Indonesia and Malaysia but still higher than those in Thailand. A move in pricing towards the regional average, as is generally happening, would expand the market as a whole and also provide higher revenues for the government, and it would attract investment into the electricity sector.

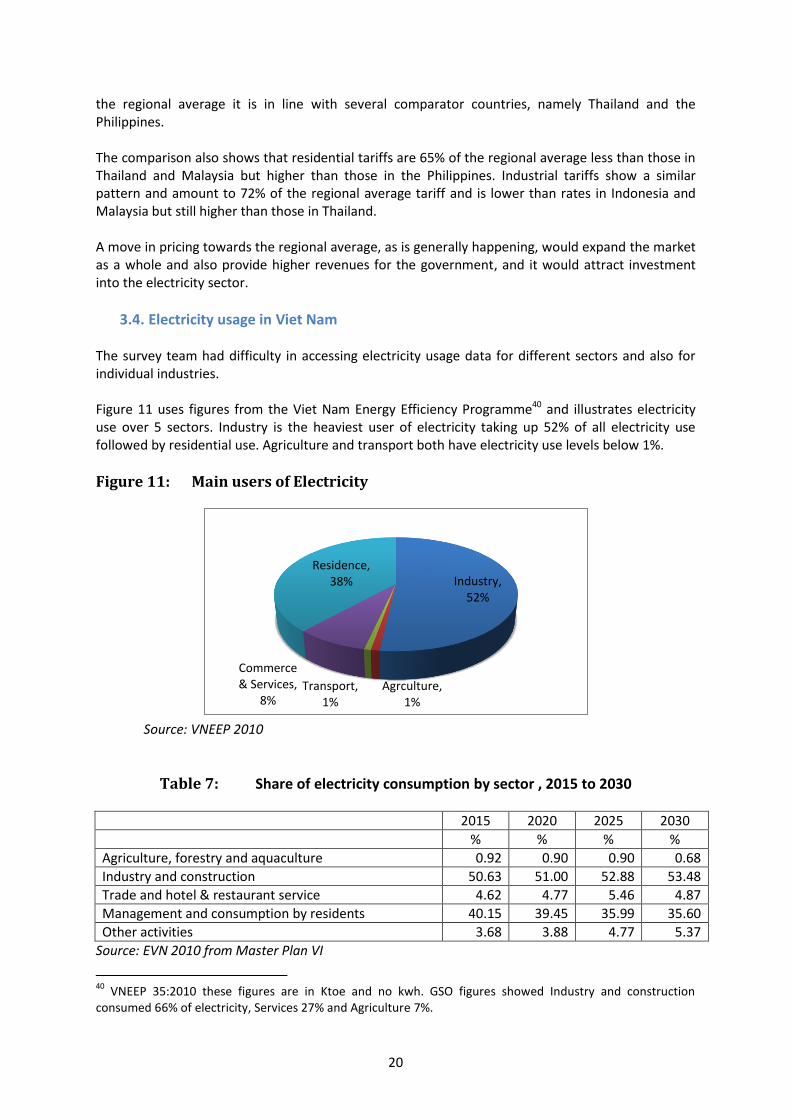

3.4. Electricity usage in Viet Nam The survey team had difficulty in accessing electricity usage data for different sectors and also for individual industries. Figure 11 uses figures from the Viet Nam Energy Efficiency Programme40 and illustrates electricity use over 5 sectors. Industry is the heaviest user of electricity taking up 52% of all electricity use followed by residential use. Agriculture and transport both have electricity use levels below 1%.

Figure 11: Main users of Electricity

Source: VNEEP 2010

Table 7: Share of electricity consumption by sector , 2015 to 2030

2015 2020 2025 2030

% % % %

Agriculture, forestry and aquaculture 0.92 0.90 0.90 0.68

Industry and construction 50.63 51.00 52.88 53.48

Trade and hotel & restaurant service 4.62 4.77 5.46 4.87

Management and consumption by residents 40.15 39.45 35.99 35.60

Other activities 3.68 3.88 4.77 5.37

Source: EVN 2010 from Master Plan VI

40

VNEEP 35:2010 these figures are in Ktoe and no kwh. GSO figures showed Industry and construction consumed 66% of electricity, Services 27% and Agriculture 7%.

Industry, 52%

Agrculture, 1%

Transport, 1%

Commerce & Services,

8%

Residence, 38%

21

Master Plan VI figures show that little change is expected in the consumption pattern over the next 20 years with a decline in agricultural consumption as well as residential consumption and growth in Industry and construction consumption41. The main industrial users of electricity as well as coal are given in Table 8.

Table 8: Percentage of market by key industry

2007 2008 2009 2010

Electricity use

Steel 1.90% 2.08% 2.66% 4.22%

Fertilizers 0.39% 0.43% 0.55% 0.88%

Cement 2.08% 2.28% 2.92% 4.63%

Paper 2.43% 2.66% 3.40% 5.39%

Coal use Steel 10.76% 10.43% 10.27% 10.40% Fertilizers 6.85% 6.54% 6.57% 6.54% Cement 7.56% 7.42% 7.44% 7.55% Paper 3.78% 3.78% 3.65% 3.65% Source: GSO 2011

3.5. Key constraints and implications

3.5.1. Pricing constraints We have discussed the role of the current pricing policy on the expansion of the electricity sector in the future, and the negative effect that a constrained market will have on new investment. But Viet Nam will need to attract an estimated US$4 billion a year in investment between now and 2025 if supply is to keep up with demand. The pricing structure has favoured hydro in recent years but has led to purchasing constraints between coal producers such as Vinacomin and gas electricity producers such as PetroVietnam, but has most recently also caused problems of small hydro producers who complain of high interest rates. While households have benefited from the low prices, industry has also greatly benefited and some industries may have developed not due to a comparative advantage but rather because of cheap inputs. While the pricing policy may have ensured that households have access to cheap electricity it has also meant that many industries and businesses have been supported. However, as Viet Nam has to release its hold on prices many businesses may find themselves no longer competitive when input prices increase. This is illustrated by Box 2 and Table 8.

41

EVN and Master Plan VI based on base plan projections. The Master Plan also forecasts use for high and low demand.

22

BOX 2: Subsidising Viet Nam‘s Steel Industry Many industries benefit from Viet Nam’s capped electricity pricing system, notably the cement, fertilizer, paper and steel industry that are using an increasingly large a share of electricity.42 The steel industry expanded hugely between 2009 and 2010 producing 9.2 million tons an increase of 33% and as a result an increase in the use of electricity in the sector. In 2010 the Steel industry consumed 4.67 billion kwh of electricity, 4.22% of total electricity produced for the year.43 The steel industry has increasingly had to pay market (export) prices for coal as does the cement industry, however they continue to benefit from low electricity prices, which is also a key input. A UNIDO study in 2010 found that Vietnamese steel manufacturers used coal for only 10% of their energy needs but relied on electricity for 64% of embodied energy. As a result recent increases in the price of coal for steel producers will have little impact on their production costs. However, any increase in the price of electricity will impact on their costs significantly, especially since recently key industries have increased their use of electricity drastically. It is clear that price caps in the electricity sector are an indirect subsidy to the steel industry, as well as other industries.44 One former vice minister of Ministry of Industry and Trade dismissed Viet Nam’s steel industry and said the country “did not export steel, it exported electricity” through the steel industry. Price increases may indeed have a high inflationary impact, especially for the construction sector, but they will also force these industries to begin to operate more competitively.

3.5.2. The Role of Coal While the role of the coal industry in electricity generation was small at 14% in 2009 the National Plan VI shows coal’s increasing role in power generation over the next 15 years, with coal set to take a leading role in electricity generation by 2020. However, the current coal export and pricing structure is causing Viet Nam’s mining monopoly some headaches. Viet Nam produced 43.7 million tonnes of coal in 2009, 25 million tonnes of which was exported. Viet Nam holds considerable deposits of Anthracite coal in Quang Ninh province as well as lower deposits of sub-bituminous coal in the Red River Delta. Viet Nam is currently a net exporter of coal through Vinacomin, who controls over 94% of the coal mining in the country. However, due to the growth in demand for coal in the power sector, as well as in industry (cement, chemicals, metallurgy and other industries) this export is expected to reduce considerably as Viet Nam moves to becoming a net importer of coal between 2012 and 2015. 42

GSO figures for the value of electricity sold show that the Steel, cement, fertilizer and paper industries consumed electricity worth VND4.7 trillion in 2009, 7% of all market receipts. By 2010 these four industries provided 15% of the market for electricity consuming VND14.24 trillion in electricity.

43 http://english.vietnamnet.vn/en/business/9035/mof-attempts-to-raise-export-tariffs-on-some-steel-products.html

44 UNIDO, 2010, “Energy and Resource Efficiency in the Vietnamese Steel Industry”

23

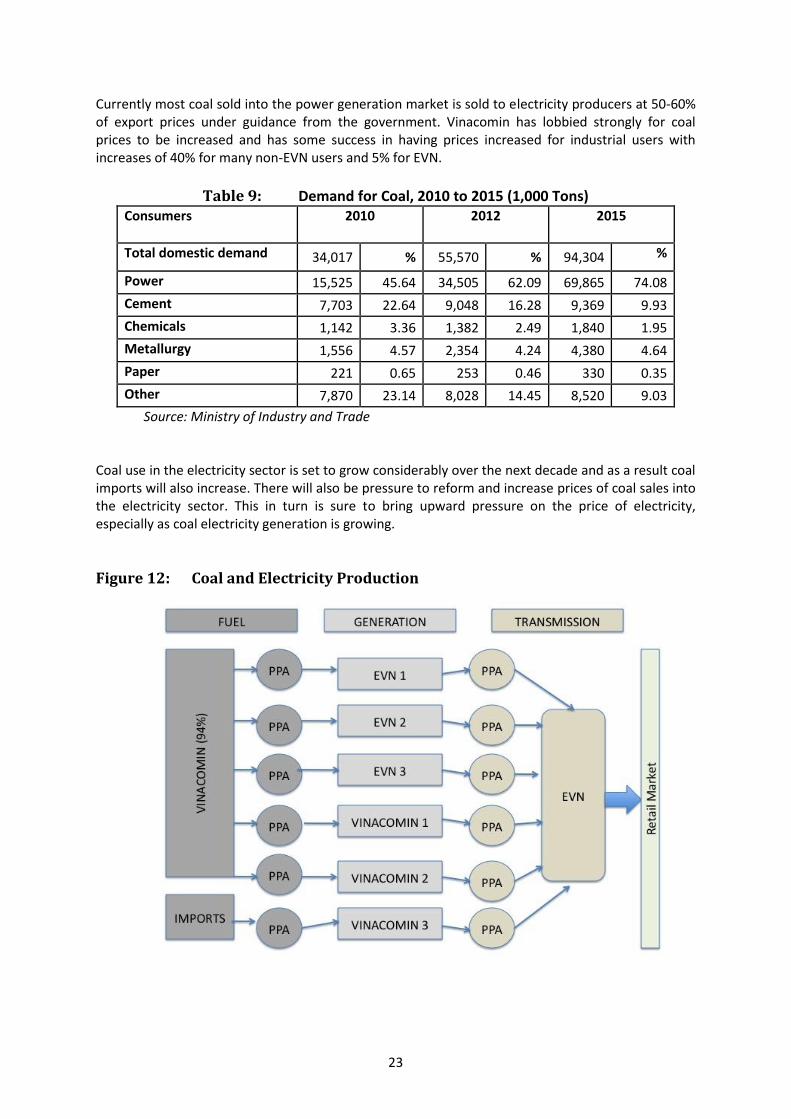

Currently most coal sold into the power generation market is sold to electricity producers at 50-60% of export prices under guidance from the government. Vinacomin has lobbied strongly for coal prices to be increased and has some success in having prices increased for industrial users with increases of 40% for many non-EVN users and 5% for EVN.

Table 9: Demand for Coal, 2010 to 2015 (1,000 Tons)

Consumers 2010

2012

2015

Total domestic demand 34,017 % 55,570 % 94,304 %

Power 15,525 45.64 34,505 62.09 69,865 74.08

Cement 7,703 22.64 9,048 16.28 9,369 9.93

Chemicals 1,142 3.36 1,382 2.49 1,840 1.95

Metallurgy 1,556 4.57 2,354 4.24 4,380 4.64

Paper 221 0.65 253 0.46 330 0.35

Other 7,870 23.14 8,028 14.45 8,520 9.03

Source: Ministry of Industry and Trade Coal use in the electricity sector is set to grow considerably over the next decade and as a result coal imports will also increase. There will also be pressure to reform and increase prices of coal sales into the electricity sector. This in turn is sure to bring upward pressure on the price of electricity, especially as coal electricity generation is growing.

Figure 12: Coal and Electricity Production

24

BOX 3: China’s Coal Conundrum China is currently suffering an electricity crisis due to its continued control of the pricing of electricity into the domestic and industrial market and its reliance on coal for electricity production. China relies on coal for 73% of its electricity production and the price of coal has been steadily rising as demand for electricity has grown across the country to power growth in industry and also a growing consumer market. Yet while coal prices are allowed to increase in line with domestic and import costs, electricity producers are forced to keep their prices in line with government guidelines. As a result electricity generators are suffering increasing financial losses as input price rise and retail prices remain steady. This is now hindering China’s economic growth as electricity generators and utility companies, the majority of whom are state owned, are showing increased displeasure at the situation and the fact that the Chinese Government is allowing them to accrue ever-increasing losses. Many electricity generators have decided to cut production rather than continue to incur ever-increasing losses. This is impacting industry across China as many factories are forced to cut production due to brown outs and black outs, and it is impacting commodity markets as far away as Australia who are suffering from a down turn in demand for coal as well as inputs such as copper and tin, used in China’s manufacturing industry. The obvious lesson is that the Vietnamese government should be careful in how it introduces competition into the electricity market and should ensure that input markets move at the same time. It is also a warning that input suppliers and producers can suffer losses for only so long and as Viet Nam’s demand for electricity grows so will the strength of those participants in the electricity sector.45 Despite China’s reliance on coal and its new position as the leading emitter of greenhouse gases it is also the world’s leading producer of renewable electricity producing 537 billion kilo watt hours in 2008. The United States produced 393 billion kwh in 2008.

45

http://www.nytimes.com/2011/05/25/business/energy-environment/25coal.html?_r=1&ref=china

25

3.6. Electricity Fossil Fuel use Conclusion Table 10 illustrates the various direct and indirect subsidies that might be available in the electricity sector when using the OECD (2002) and the UNEP (2008) structure given in section 1.3. The electricity sector is key for the Vietnamese economy and society and several of the tools discussed below have been used at one time or another to support the electricity sector. However, the survey found few direct subsidies beyond the recent support to poor households due to price increases across the sector. Most subsidies are indirect subsidies and as a result are difficult to quantify. As we can see form table 10 there are in fact few direct subsidies to the electricity sector. Most support using the OECD/ UNEP approach is focused on infrastructure and research support as well as a regulated market with restricted access. Other areas of support are somewhat irregular and are taken as a given due to the nature of state owned participation in Viet Nam. As mentioned, the current subsidies for the poor are not a long-term measure. However, state owned enterprises such as EVN, PetroVietnam and Vinacomin benefit from priority access to finance as well preferential loans and loan rates, if not directly from the government then from many of their subsidiaries which include financing and banking. EVN is a key investor in An Binh Commercial Bank (AB Bank), with AB Bank stating in its Annual Report for 2010 that “AB BANK continuously developed new products to meet the highest demand of EVN, member entities, associate entities as well as power project contractors”.46 EVN also has a finance branch. PetroVietnam Finance is also a strategic shareholder in AB Bank. PetroVietnam owns a 20% stake in Ocean Bank and controls PetroVietnam Finance.47 Vinacomin doesn’t have a banking subsidiary but does have the Viet Nam National Coal and Mineral Industries Group (Vinacomin)'s Finance one-member Ltd Co (CMF). CMF and the Military Bank appear to have close connections.48 As we will see in the petroleum industry the government is ready to use tax deferrals to ensure a stable price in certain fossil fuels rather than to subsidise a particular sector. However, the loss of revenue could be considered a subsidy of sorts. Again, these losses taken by firms and covered by the Government are difficult to categorise under the OECD framework for subsidies but are likely to be resolved with direct financial transfers and low interest loans to producers (ref category a.; section 1.3). Other areas are not being used at the moment and are also not currently given any consideration within the current regulatory framework. However, as we have seen with support for the poor as well as the change to quarterly electricity pricing, the Government is not adverse to make ad hoc changes to the regulatory framework of the electricity sector and therefore may consider these areas at some moment in the future.

46

http://www.abbank.vn/Upload/file/thongtincodong/bieumau/ABBANK_BCTN_2010_TiengAnh.pdf

47 http://www.vnstocknews.com/2008/10/petrovietnam-buys-20-pct-in-ocean-bank.html

48 http://www.vnstocknews.com/2009/08/military-bank-signs-comprehensive.html

26

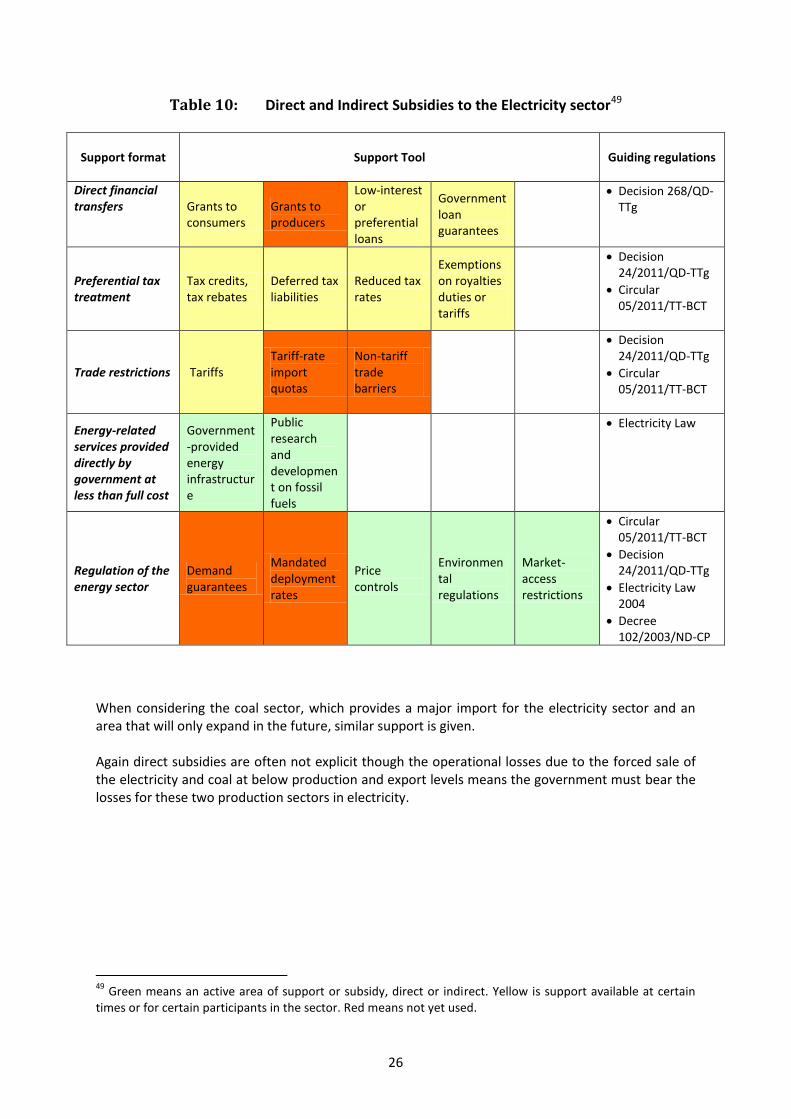

Table 10: Direct and Indirect Subsidies to the Electricity sector49

Support format Support Tool Guiding regulations

Direct financial transfers Grants to

consumers Grants to producers

Low-interest or preferential loans

Government loan guarantees

Decision 268/QD-TTg

Preferential tax treatment

Tax credits, tax rebates

Deferred tax liabilities

Reduced tax rates

Exemptions on royalties duties or tariffs

Decision 24/2011/QD-TTg

Circular 05/2011/TT-BCT

Trade restrictions Tariffs Tariff-rate import quotas

Non-tariff trade barriers

Decision 24/2011/QD-TTg

Circular 05/2011/TT-BCT

Energy-related services provided directly by government at less than full cost

Government-provided energy infrastructure

Public research and development on fossil fuels

Electricity Law

Regulation of the energy sector

Demand guarantees

Mandated deployment rates

Price controls

Environmental regulations

Market-access restrictions

Circular 05/2011/TT-BCT

Decision 24/2011/QD-TTg

Electricity Law 2004

Decree 102/2003/ND-CP

When considering the coal sector, which provides a major import for the electricity sector and an area that will only expand in the future, similar support is given. Again direct subsidies are often not explicit though the operational losses due to the forced sale of the electricity and coal at below production and export levels means the government must bear the losses for these two production sectors in electricity.

49

Green means an active area of support or subsidy, direct or indirect. Yellow is support available at certain times or for certain participants in the sector. Red means not yet used.

27

4. Refined Petroleum market Despite the large growth in demand for fossil fuels for electricity in Viet Nam over the last decades figure 1 in section 2 shows that petroleum products continue to be one of the leading providers of energy in Viet Nam, accounting for 26.3% of energy supplies in 2008, slightly behind renewable energy. It is likely that petroleum products will have taken the lead today but figures were unavailable for this study.50 This section will look at the use of refined petroleum products in Viet Nam, including the share of use by different fuels (gasoline, diesel, kerosene etc) and their means of use (transportation, domestic transport, Air etc). Viet Nam has been very proactive in implementing increasingly market based pricing for refined petroleum products due to the growth in refined petroleum use as well as fluctuations in world market prices and Viet Nam’s lack of a refinery until 2009. However, the Government has attempted to influence the price of retail of refined petroleum through a stabilisation fund contributed to by enterprises in the retail petroleum market. The Government has also used tax and tariff waivers in order to ensure a low price and a reduced impact of rising global prices for refined products on inflation. However, this reduced Government revenues from refined petroleum, as we will see. This section will not look at oil production and exploration in Viet Nam beyond its relationship to Viet Nam’s first refinery (Dung Quat in Quang Ngai province, which opened in February 2009 and now satisfies around 30% of Vietnamese refined petroleum demand).

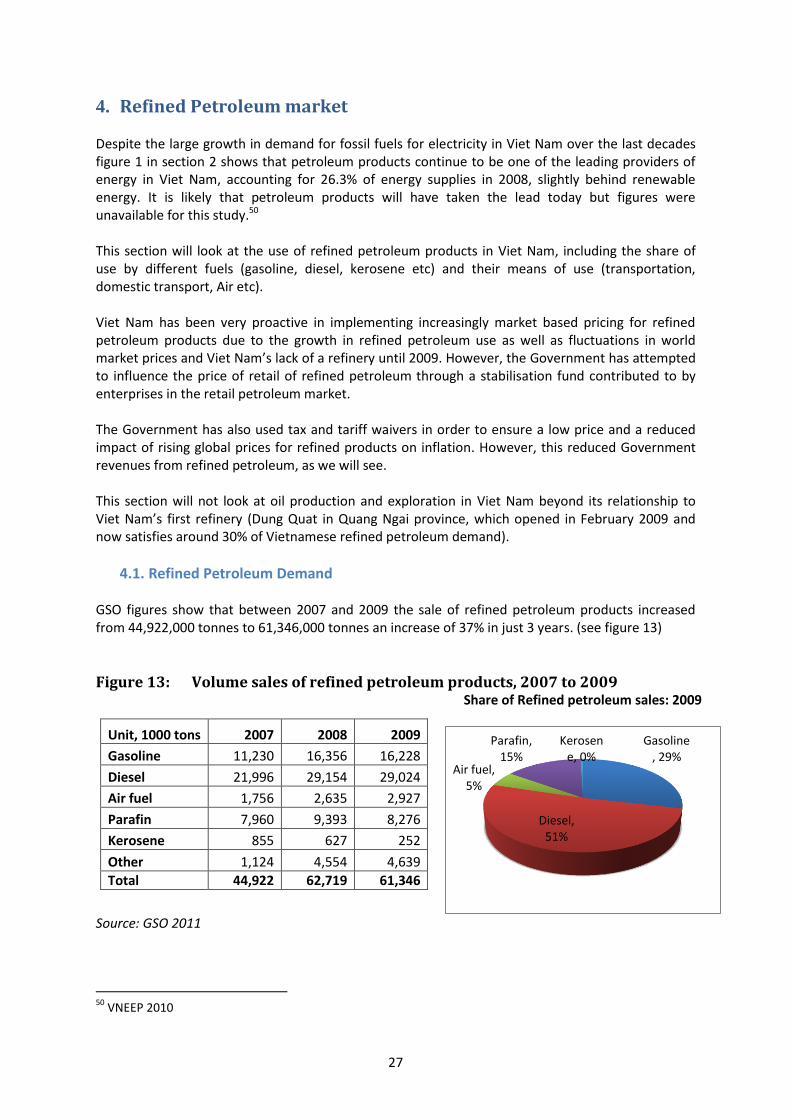

4.1. Refined Petroleum Demand GSO figures show that between 2007 and 2009 the sale of refined petroleum products increased from 44,922,000 tonnes to 61,346,000 tonnes an increase of 37% in just 3 years. (see figure 13)

Figure 13: Volume sales of refined petroleum products, 2007 to 2009

Unit, 1000 tons 2007 2008 2009

Gasoline 11,230 16,356 16,228

Diesel 21,996 29,154 29,024

Air fuel 1,756 2,635 2,927

Parafin 7,960 9,393 8,276

Kerosene 855 627 252

Other 1,124 4,554 4,639

Total 44,922 62,719 61,346

Share of Refined petroleum sales: 2009

Source: GSO 2011

50

VNEEP 2010

Gasoline, 29%

Diesel, 51%

Air fuel, 5%

Parafin, 15%

Kerosene, 0%

28

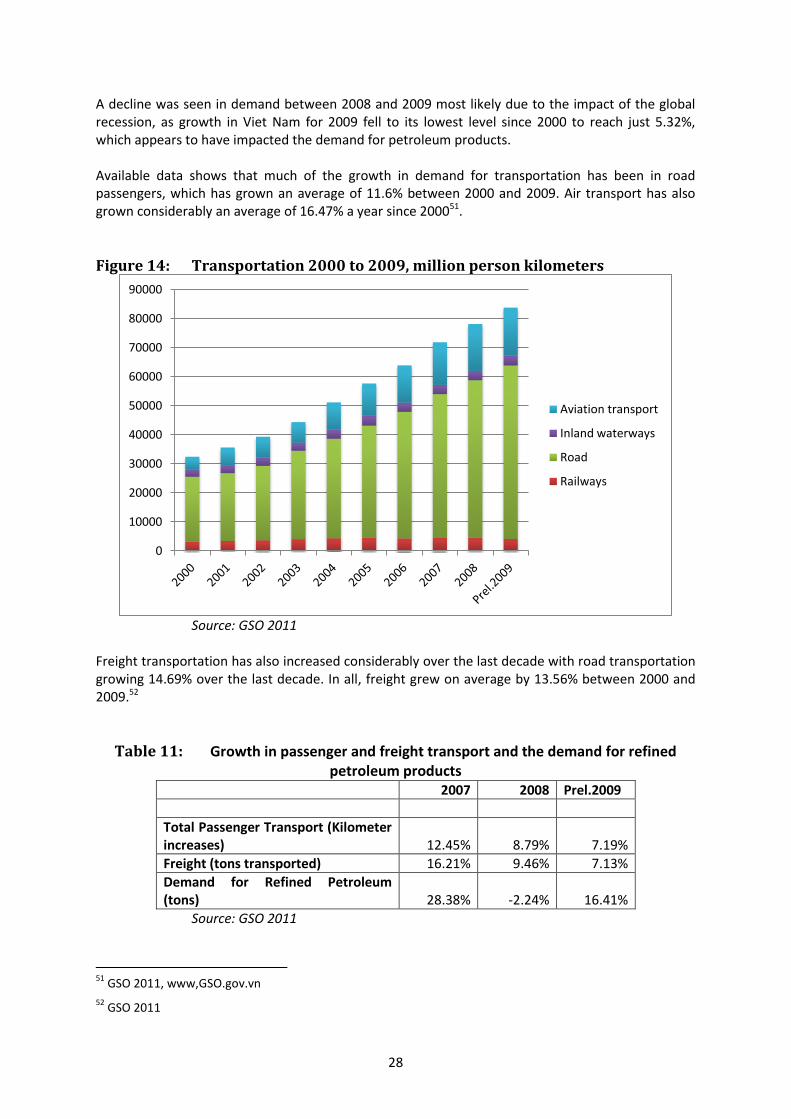

A decline was seen in demand between 2008 and 2009 most likely due to the impact of the global recession, as growth in Viet Nam for 2009 fell to its lowest level since 2000 to reach just 5.32%, which appears to have impacted the demand for petroleum products. Available data shows that much of the growth in demand for transportation has been in road passengers, which has grown an average of 11.6% between 2000 and 2009. Air transport has also grown considerably an average of 16.47% a year since 200051.

Figure 14: Transportation 2000 to 2009, million person kilometers

Source: GSO 2011 Freight transportation has also increased considerably over the last decade with road transportation growing 14.69% over the last decade. In all, freight grew on average by 13.56% between 2000 and 2009.52

Table 11: Growth in passenger and freight transport and the demand for refined petroleum products

2007 2008 Prel.2009

Total Passenger Transport (Kilometer increases) 12.45% 8.79% 7.19%

Freight (tons transported) 16.21% 9.46% 7.13%

Demand for Refined Petroleum (tons) 28.38% -2.24% 16.41%

Source: GSO 2011

51

GSO 2011, www,GSO.gov.vn

52 GSO 2011

0

10000

20000

30000

40000

50000

60000

70000

80000

90000

Aviation transport

Inland waterways

Road

Railways

29

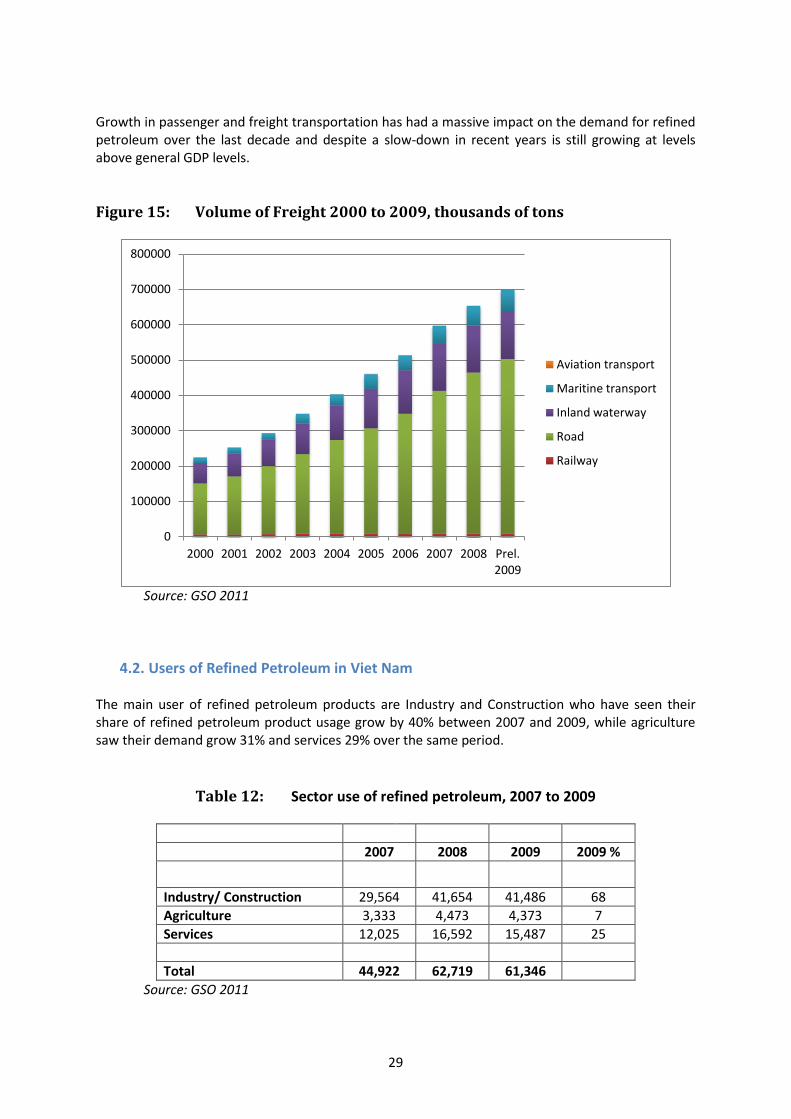

Growth in passenger and freight transportation has had a massive impact on the demand for refined petroleum over the last decade and despite a slow-down in recent years is still growing at levels above general GDP levels.

Figure 15: Volume of Freight 2000 to 2009, thousands of tons

Source: GSO 2011

4.2. Users of Refined Petroleum in Viet Nam The main user of refined petroleum products are Industry and Construction who have seen their share of refined petroleum product usage grow by 40% between 2007 and 2009, while agriculture saw their demand grow 31% and services 29% over the same period.

Table 12: Sector use of refined petroleum, 2007 to 2009

2007 2008 2009 2009 %

Industry/ Construction 29,564 41,654 41,486 68

Agriculture 3,333 4,473 4,373 7

Services 12,025 16,592 15,487 25

Total 44,922 62,719 61,346

Source: GSO 2011

0

100000

200000

300000

400000

500000

600000

700000

800000

2000 2001 2002 2003 2004 2005 2006 2007 2008 Prel. 2009

Aviation transport

Maritine transport

Inland waterway

Road

Railway

30

Urban users remain the main users of refined petroleum consuming 71% of refined petroleum products in 2009 and increasing their use by 42% over the 2007 to 2009 period from 30,693,000 tons in 2007 to 43,449,000 tons in 2009 while rural use has grown from 14,229,000 tons in 2007 to 17,346,000 tons in 2009. Looking at specific industries there has been little change in the structure of refined petroleum use between 2007 and 2009, with household use making up the majority of use (personal motorbikes and cars), followed by transportation and then logistics.

Table 13: Use of refined petroleum, 2007 to 2009

2007 2008 2009

1,000 tons % 1,000 tons % 1,000 tons %

Household (motorbikes and cars) 8,162 18.17 12,277 19.57 11,566 18.85

Transportation (bus/ train) 7,071 15.74 10,134 16.16 9,777 15.94

Logistics (lorries etc.) 3,303 7.35 4,662 7.43 4,869 7.94

Shipping 4,206 9.36 6,180 9.85 5,605 9.14

Airlines 7,483 16.66 10,403 16.59 10,420 16.99

Other 14,697 32.72 19,064 30.40 19,109 31.15

Units: 1000 tons 44,922 62,719 61,346 Source: GSO 2011

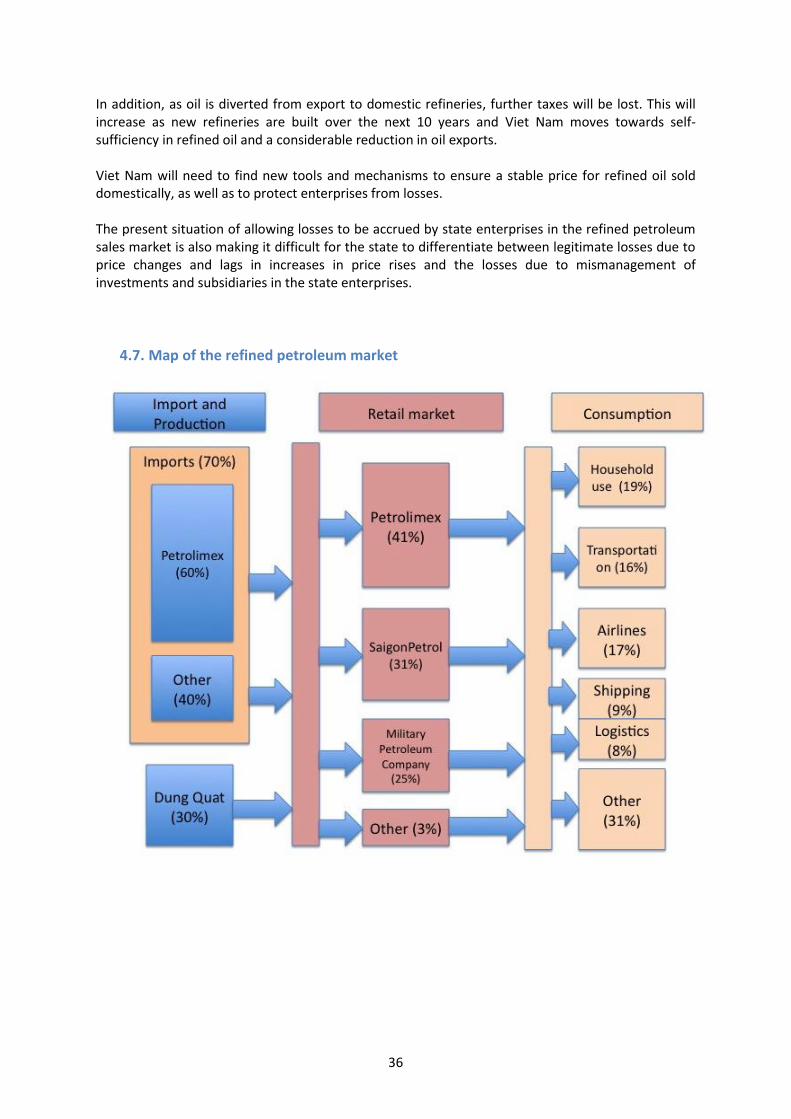

4.3. Refined Petroleum market structure As with the electricity sector and other sectors in Viet Nam, refined petroleum imports and retail sales are dominated by a state owned enterprise, the Viet Nam National Petroleum Corp (Petrolimex), as well as other state owned enterprises including the Military Petroleum Company and Saigon Petro (under Ho Chi Minh City People’s Committee). Until February 2009 all of Viet Nam’s refined petroleum products were imported and Viet Nam was a net exporter of crude oil. The completion of Dung Quat Oil refinery in February 2009 slowly brought a range of domestically produced refined petroleum products onto the market. A mixture of domestic Bac Ho sweet crude, Nam Rong-Doi Moi oil from Vietnamese fields as well as imported crude oil from Malaysia53. This is impacting on Viet Nam’s exports of crude oil and government revenues from exports54. The completion and full operation of Dung Quat refinery had no affect on the sale price of refined petroleum into the domestic market as from the outset Dung Quat was selling all production at global market prices. By 2008 Viet Nam became a net importer of oil by value though not in volume.

53

http://www.vneconomynews.com/2011/01/dung-quat-refinery-to-import-malaysia.html

54 http://www.intellasia.net/news/articles/resources/111288874.shtml

31

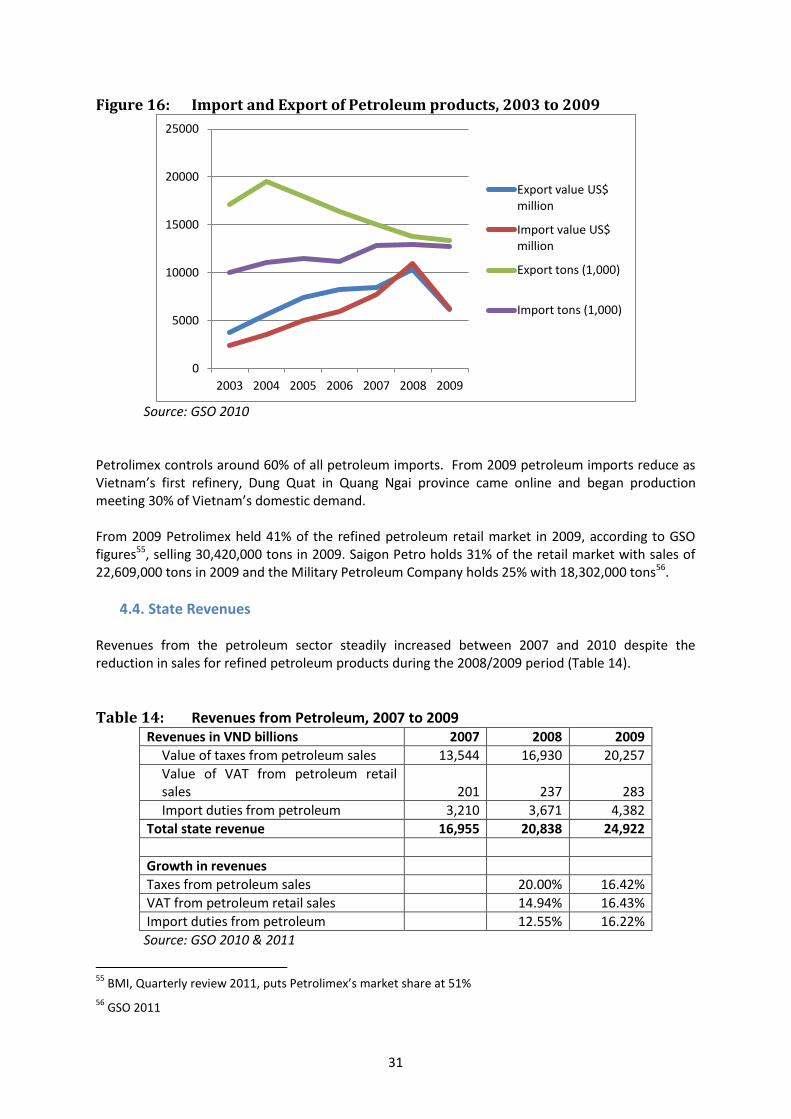

Figure 16: Import and Export of Petroleum products, 2003 to 2009

Source: GSO 2010

Petrolimex controls around 60% of all petroleum imports. From 2009 petroleum imports reduce as Vietnam’s first refinery, Dung Quat in Quang Ngai province came online and began production meeting 30% of Vietnam’s domestic demand. From 2009 Petrolimex held 41% of the refined petroleum retail market in 2009, according to GSO figures55, selling 30,420,000 tons in 2009. Saigon Petro holds 31% of the retail market with sales of 22,609,000 tons in 2009 and the Military Petroleum Company holds 25% with 18,302,000 tons56.

4.4. State Revenues Revenues from the petroleum sector steadily increased between 2007 and 2010 despite the reduction in sales for refined petroleum products during the 2008/2009 period (Table 14).

Table 14: Revenues from Petroleum, 2007 to 2009 Revenues in VND billions 2007 2008 2009

Value of taxes from petroleum sales 13,544 16,930 20,257

Value of VAT from petroleum retail sales 201 237 283

Import duties from petroleum 3,210 3,671 4,382

Total state revenue 16,955 20,838 24,922

Growth in revenues

Taxes from petroleum sales 20.00% 16.42%

VAT from petroleum retail sales 14.94% 16.43%

Import duties from petroleum 12.55% 16.22%

Source: GSO 2010 & 2011

55

BMI, Quarterly review 2011, puts Petrolimex’s market share at 51%

56 GSO 2011

0

5000

10000

15000

20000

25000

2003 2004 2005 2006 2007 2008 2009

Export value US$ million

Import value US$ million

Export tons (1,000)

Import tons (1,000)

32

Revenues from refined petroleum are considerably higher than those from electricity shown in table 5, reflecting both the desire for the government to keep electricity prices low and the difficulty in controlling the price of refined petroleum products . Total revenues from petroleum sales shown above amounted to VND24,922 billion in 2009 compared to VND4,839 billion for electricity illustrating the importance of oil taxes for government revenues. Import duties from petroleum are comparable to taxes from electricity production, however VAT from petroleum in 2009, VND283 billion, was considerably lower than that from electricity sales, VND1,093 billion.

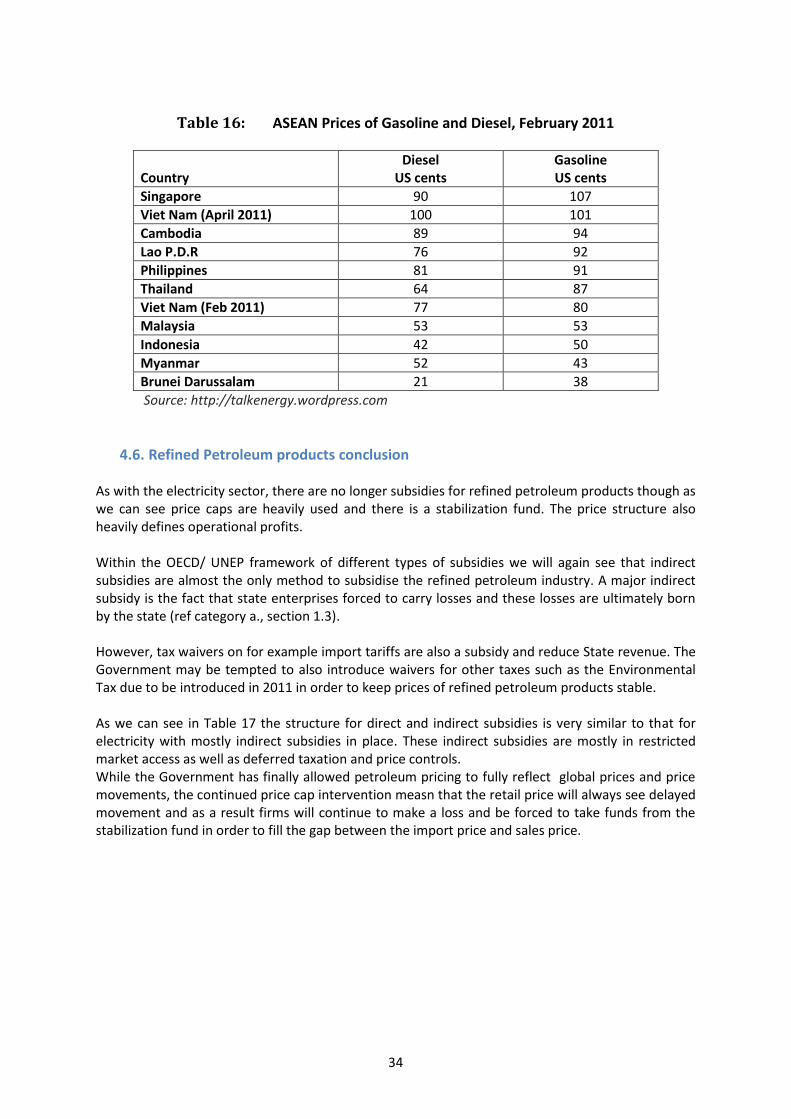

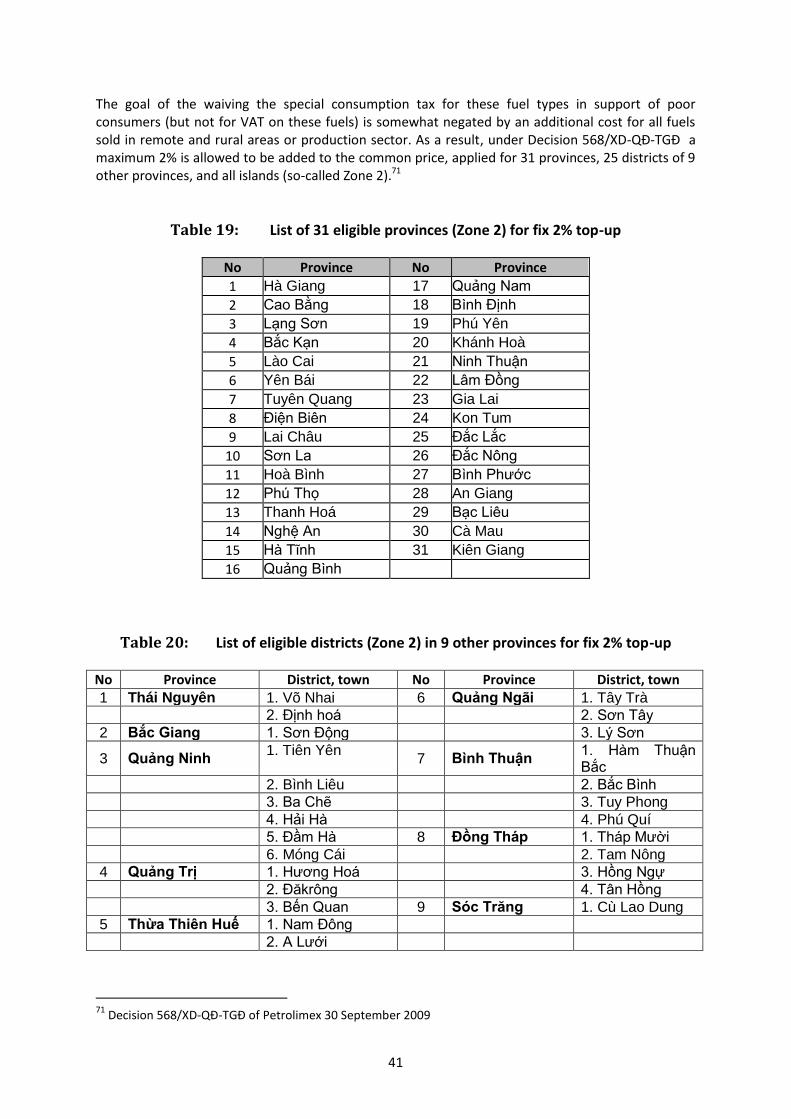

4.5. Price fluctuations and stabilization Refined petroleum retailers have had some freedom in setting their own prices in recent years. Retailers have been allowed to increase prices if global prices increase by more than 7% without seeking approval from the Ministry of Finance57 58However, in 2010 the Government has asked retailers not to increase prices in order to dampen inflationary pressures.59 Since 2009 a stabilisation fund has been in place to try to slow price increases of refined petroleum, should global prices increase. Under Circular 234/2009/TT-BTC a levy of VND300 to VND500 has been added to every litre of petroleum, which is placed in the stabilization fund. Consumers are paying for the stabilization fund and should also benefit from lower prices when the fund is used. As global prices started to increase in late 2010 petroleum retailers began to draw on the fund and effectively emptied the fund by February 2011 due to high global oil prices and continued losses due to forced caps in retail pricing.60 By April 2011 the government was forced to considerably reconsider the retail pricing structure in light of the exhaustion of the stabilization fund, continued global price pressures and enterprise losses. It was reported that some retailers had stopped supplying gasoline altogether due to continued losses. In order to relieve pressure on retailers the government has temporarily suspended import tariffs and allowed the retail price to increase by 15% in order to reduce losses, keep prices at affordable levels and reduce pressures on inflation.61 Under a revised structure a payment for the stabilization fund will still be made by consumers while companies will also continue to have their profits and operational costs dictated to them by the Ministry of Finance. As we can see from table 15, enterprises will still be making a loss but can continue to draw to a lesser extent from the stabilisation fund. Under 2009 legislation several provinces and districts were placed in Zone 2 areas, mostly remote areas, where petroleum prices are allowed to be 2% higher than those above due to the cost of transporting fuel to these areas.

57

Circular 234/2009/TT-BTC

58 http://www.vietnam-briefing.com/news/vietnam-allow-oil-importers-set-prices.html/

59 http://www.lookatvietnam.com/2010/03/vietnam-fuel-companies-dont-have-total-pricing-freedom-

official.html

60 http://bizvietnam.com/2011/02/oil-price-stabilization-fund-has-run-out-of-money/

61 http://blogs.voanews.com/breaking-news/2011/03/30/vietnam-raises-fuel-prices-to-record-levels/

33

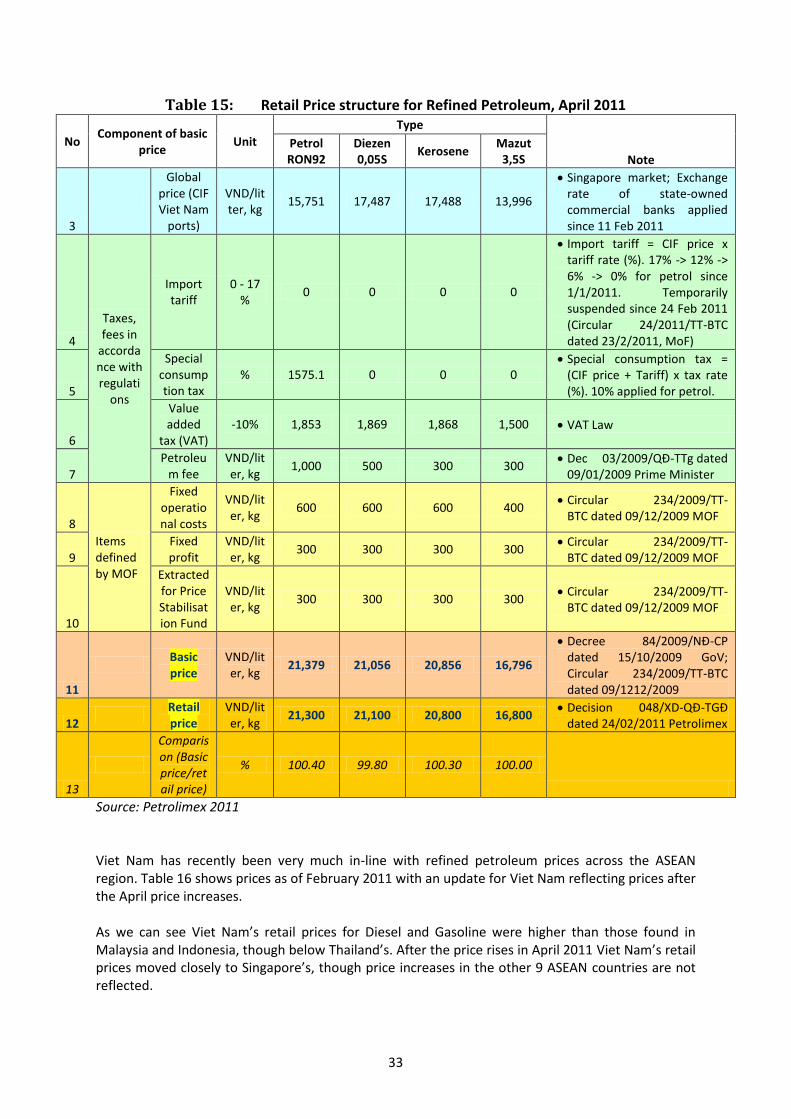

Table 15: Retail Price structure for Refined Petroleum, April 2011

No Component of basic

price Unit

Type

Note

Petrol RON92

Diezen 0,05S

Kerosene Mazut

3,5S

3

Global price (CIF Viet Nam

ports)

VND/litter, kg

15,751 17,487 17,488 13,996

Singapore market; Exchange rate of state-owned commercial banks applied since 11 Feb 2011

4

Taxes, fees in

accordance with regulati

ons

Import tariff

0 - 17 %

0 0 0 0

Import tariff = CIF price x tariff rate (%). 17% -> 12% -> 6% -> 0% for petrol since 1/1/2011. Temporarily suspended since 24 Feb 2011 (Circular 24/2011/TT-BTC dated 23/2/2011, MoF)

5

Special consumption tax

% 1575.1 0 0 0 Special consumption tax =

(CIF price + Tariff) x tax rate (%). 10% applied for petrol.

6