PAKISTANMICROFINANCEREVIEW2015ANNUAL ASSESSMENT OFTHE MICROFINANCE INDUSTRYF I N A N C I A L S E R V I C E S F O R A L L

Produced by Pakistan Microfinance NetworkDesign and Layout by O3 Interfaces

www.o3interfaces.com

ANNUAL ASSESSMENTOF THE MICROFINANCE INDUSTRY

PAKISTAN MICROFINANCEREVIEW2015

Financial Services for all

Pakistan Microfinance Review 2015

i

EDITORIAL BOARD

Mr. Ghalib NishtarChairperson, Editorial Board,President, Khushhali Bank Limited (KBL)

Mr. Yasir AshfaqGroup Head, Financial Services Group,Pakistan Poverty Alleviation Fund (PPAF)

Syed Samar HusnainExecutive Director, Development Finance Group, State Bank of Pakistan (SBP)

Mr. Azfar JamalExecutive Vice President, Head Payment Services & E-Banking, National Bank of Pakistan (NBP)

Mr. Blain StephensCOO and Director of Analysis,Microfinance Information eXchange, Inc. (MIX)

Mr. Masood Safdar GillDirector Programme, Urban Poverty Alleviation Pro-gramme, National Rural Support Programme (NRSP)

Ms. Gemma StevensonPrivate Sector Development Advisor,Finance, Markets and Jobs Team, Economic Growth Group,Department for International Development (UK)

Annual Assessment of the Microfinance Industry

Financial Services for all ii

PMR TEAM

Mr. Ali BasharatAuthor and Managing Editor

Ms. Saquiba AzizData Collection

Mr. Ammar ArshadCo-Author and Data Collection

Ms. Saba AbbasCo-Author and Data Collection

Financial Services for all

Pakistan Microfinance Review 2015

iii

ACRONYMS AND ABBREVIATIONS

AC&MFD Agriculture and Microfinance Division

ADB Asian Development Bank

AMRDO Al-Mehran Rural Development Organization

AML Anti-Money Laundering

BPS Basis Points

CAR Capital Adequacy Ratio

CIB Credit Information Bureau

CDD Customer Due Diligence

CGAP Consultative Group to Assist the Poor

CNIC Computerized National Identity Card

CPP Client Protection Principles

CPI Consumer Price Index

CPC Consumer Protection Code

DFI Development Financial Institution

DFID Department for International Development, UK

DPF Depositor’s Protection Fund

ECA Eastern and Central Europe

ESM Environment and Social Management

EUR Euro

FATF Financial Action Task Force

FIP Financial Inclusion Program

FMFB The First Microfinance Bank Ltd.

FSS Financial Self Sufficiency

FY Financial Year

G2P Government to Person

GBP Great Britain Pound

GDP Gross Domestic Product

GLP Gross Loan Portfolio

GNI Gross National Income

Annual Assessment of the Microfinance Industry

Financial Services for all ivAcronyms and Abbreviations

GoP Government of Pakistan

IAFSF Improving Access to Financial Services Support Fund

IFAD International Fund for Agricultural Development

IFC International Finance Corporation

JIWS Jinnah Welfare Society

KBL Khushhali Bank Ltd.

KF Kashf Foundation

KIBOR Karachi Inter-Bank Offering Rate

KMFBL Kashf Microfinance Bank Ltd.

KP Khyber Pakhtunkhwa

MCGF Microfinance Credit Guarantee Facility

MCR Minimum Capital Requirement

MENA Middle East and North Africa

MFB Microfinance Bank

MFCG Microfinance Consultative Group

MF-CIB Microfinance Credit Information Bureau

MFP Microfinance Providers

MFI Microfinance Institution

MIS Management Information System

MSME Micro, Small and Medium Enterprises

MIV Microfinance Investment Vehicle

MO Micro-Options

NADRA National Database and Registration Authority

NGO Non-Governmental Organization

NFLP National Financial Literacy Program

NMFB Network Microfinance Bank Limited

NPLs Non-Performing Loans

NRDP National Rural Development Program

NRSP National Rural Support Programme

OPD Organization for Participatory Development

OSS Operational Self Sufficiency

P2P Person to Person

PAR Portfolio at Risk

PBA Pakistan Banks Association

PKR Pakistan Rupee

PMN Pakistan Microfinance Network

PO Partner Organization

PPAF Pakistan Poverty Alleviation Fund

Financial Services for all

Pakistan Microfinance Review 2015

v

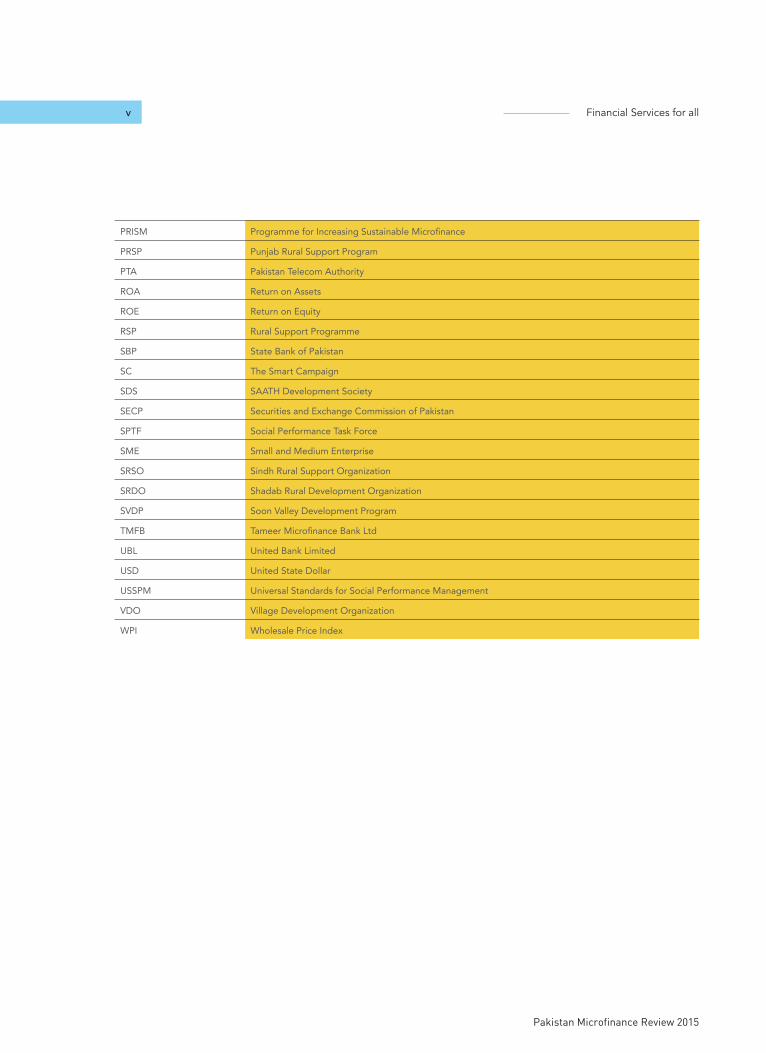

PRISM Programme for Increasing Sustainable Microfinance

PRSP Punjab Rural Support Program

PTA Pakistan Telecom Authority

ROA Return on Assets

ROE Return on Equity

RSP Rural Support Programme

SBP State Bank of Pakistan

SC The Smart Campaign

SDS SAATH Development Society

SECP Securities and Exchange Commission of Pakistan

SPTF Social Performance Task Force

SME Small and Medium Enterprise

SRSO Sindh Rural Support Organization

SRDO Shadab Rural Development Organization

SVDP Soon Valley Development Program

TMFB Tameer Microfinance Bank Ltd

UBL United Bank Limited

USD United State Dollar

USSPM Universal Standards for Social Performance Management

VDO Village Development Organization

WPI Wholesale Price Index

Annual Assessment of the Microfinance Industry

Financial Services for all viHighlights

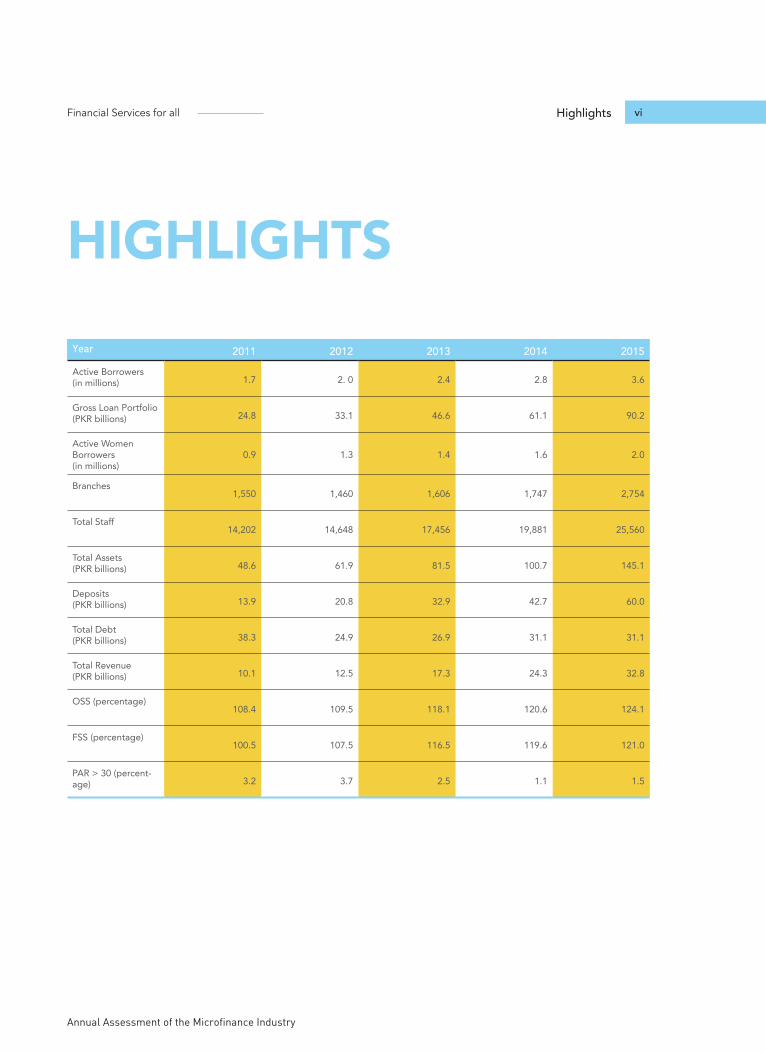

HIGHLIGHTSYear 2011 2012 2013 2014 2015Active Borrowers (in millions) 1.7 2. 0 2.4 2.8 3.6

Gross Loan Portfolio(PKR billions) 24.8 33.1 46.6 61.1 90.2

Active Women Borrowers(in millions)

0.9 1.3 1.4 1.6 2.0

Branches1,550 1,460 1,606 1,747 2,754

Total Staff 14,202 14,648 17,456 19,881 25,560

Total Assets (PKR billions) 48.6 61.9 81.5 100.7 145.1

Deposits (PKR billions) 13.9 20.8 32.9 42.7 60.0

Total Debt (PKR billions) 38.3 24.9 26.9 31.1 31.1

Total Revenue(PKR billions) 10.1 12.5 17.3 24.3 32.8

OSS (percentage)108.4 109.5 118.1 120.6 124.1

FSS (percentage)100.5 107.5 116.5 119.6 121.0

PAR > 30 (percent-age) 3.2 3.7 2.5 1.1 1.5

Financial Services for all

Pakistan Microfinance Review 2015

vii

PAKISTAN MICROFINANCEREVIEW2015ANNUAL ASSESSMENTOF THE MICROFINANCE INDUSTRYFinancial services for all

Annual Assessment of the Microfinance Industry

Financial Services for all viii

CONTENTSTHE YEAR IN REVIEW

SOCIAL PERFORMANCE

ANNEXURES

FINANCIAL PERFORMANCE REVIEW

CHALLENGES AND OPPORTUNITIES

01

41

73

17

61

Macro-Economy and The Microfinance Industry

02

Policy and Regulatory Environment 03

Microfinance Industry Initiatives 05

Conclusion 13

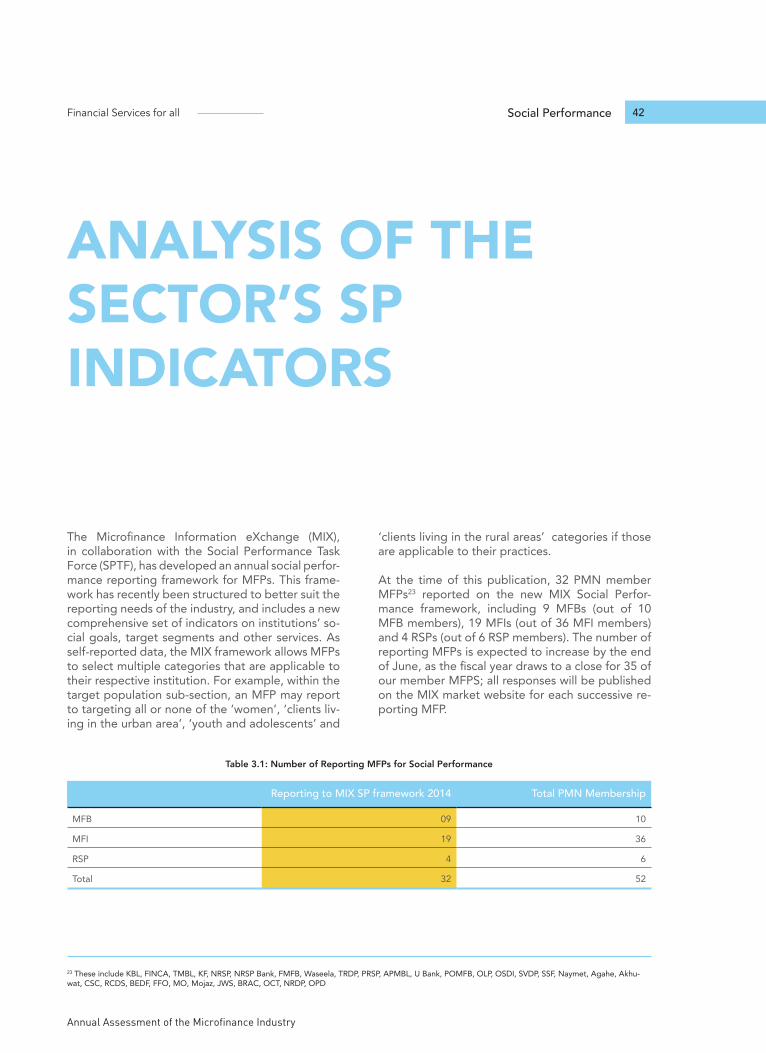

Introduction 41

Analysis of The Sector’s SP Indicators

42

Target Market 43

Development Goals 43

Poverty Measurement Tools 45

Governance & HR 46

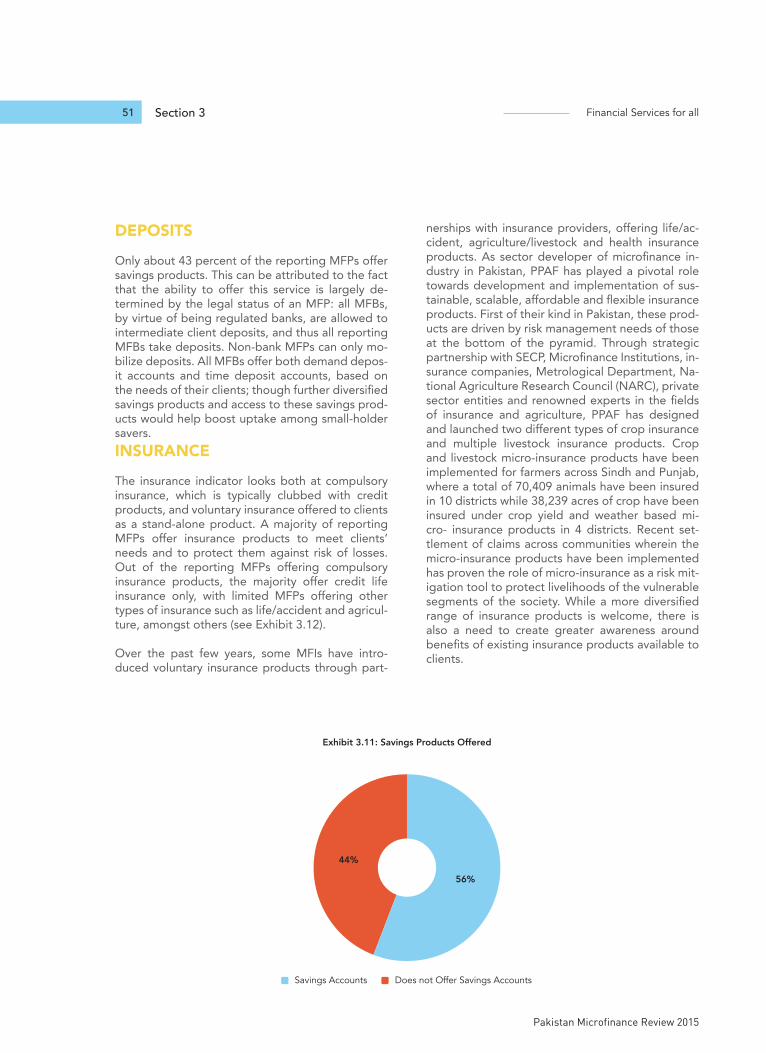

Products and Services: Financial 49

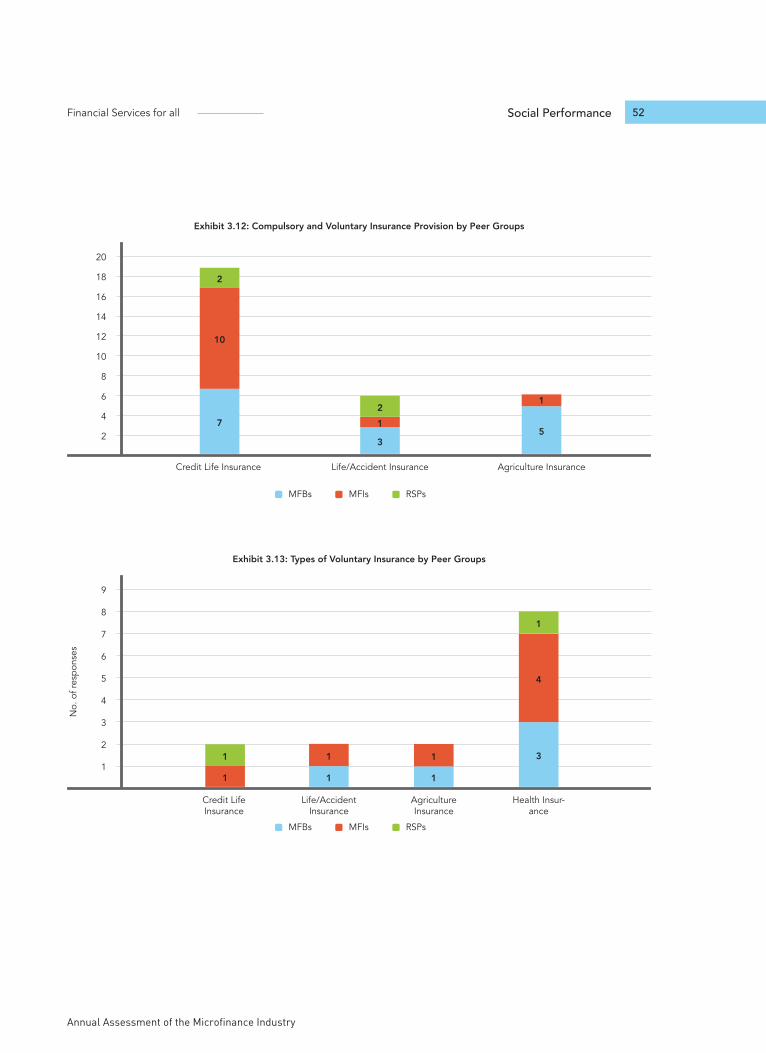

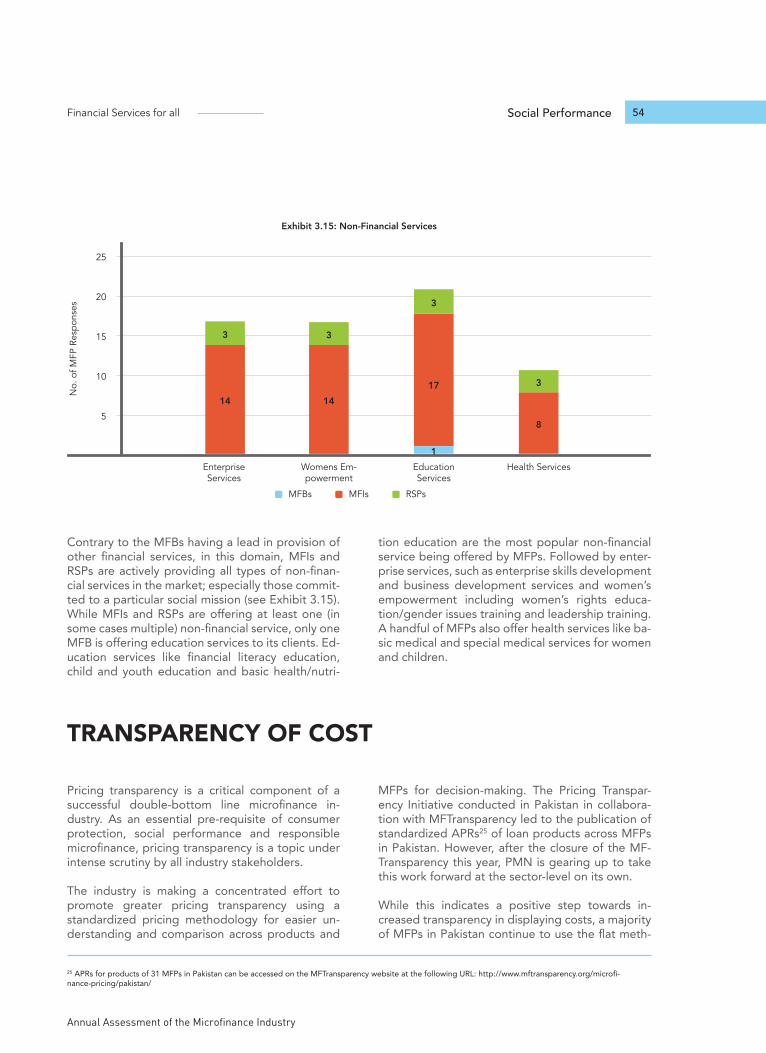

Products and Services: Non-Financial

53

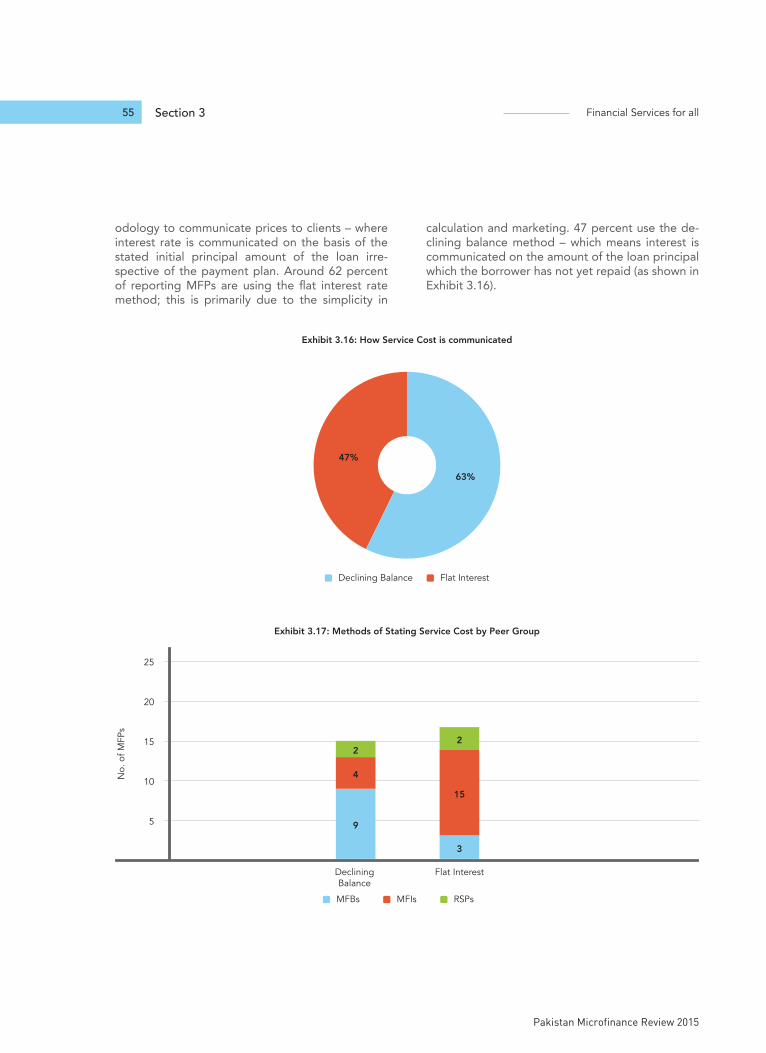

Transparency of Cost 54

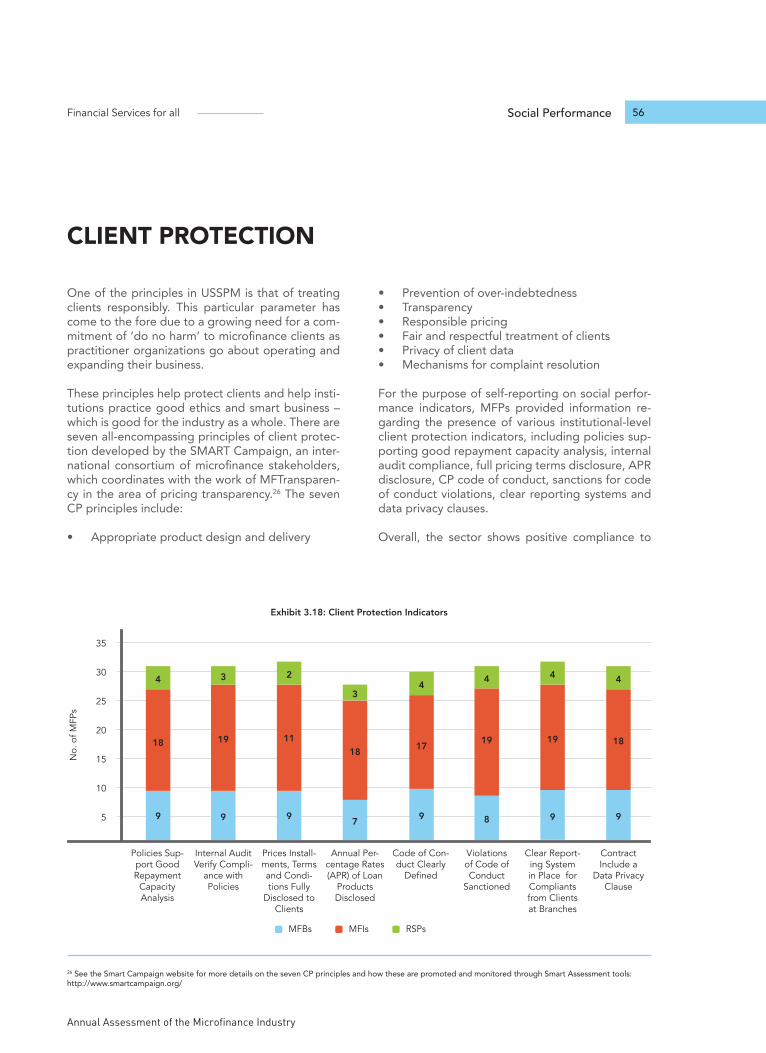

Client Protection 56

Environmental Policies 57

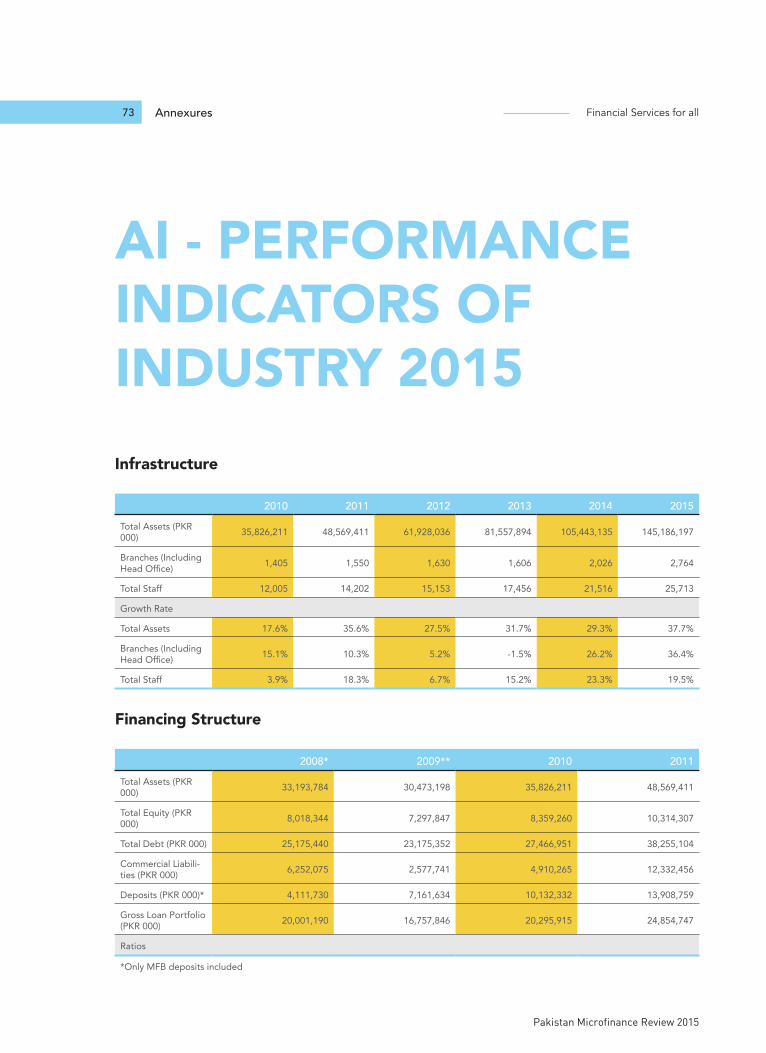

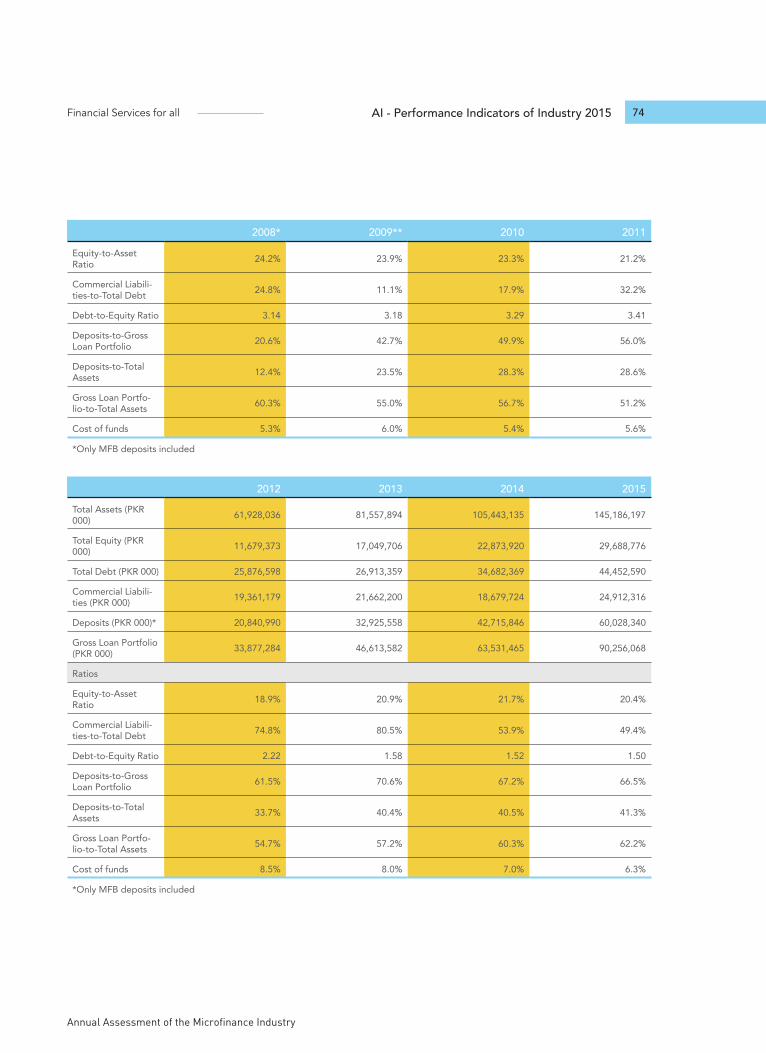

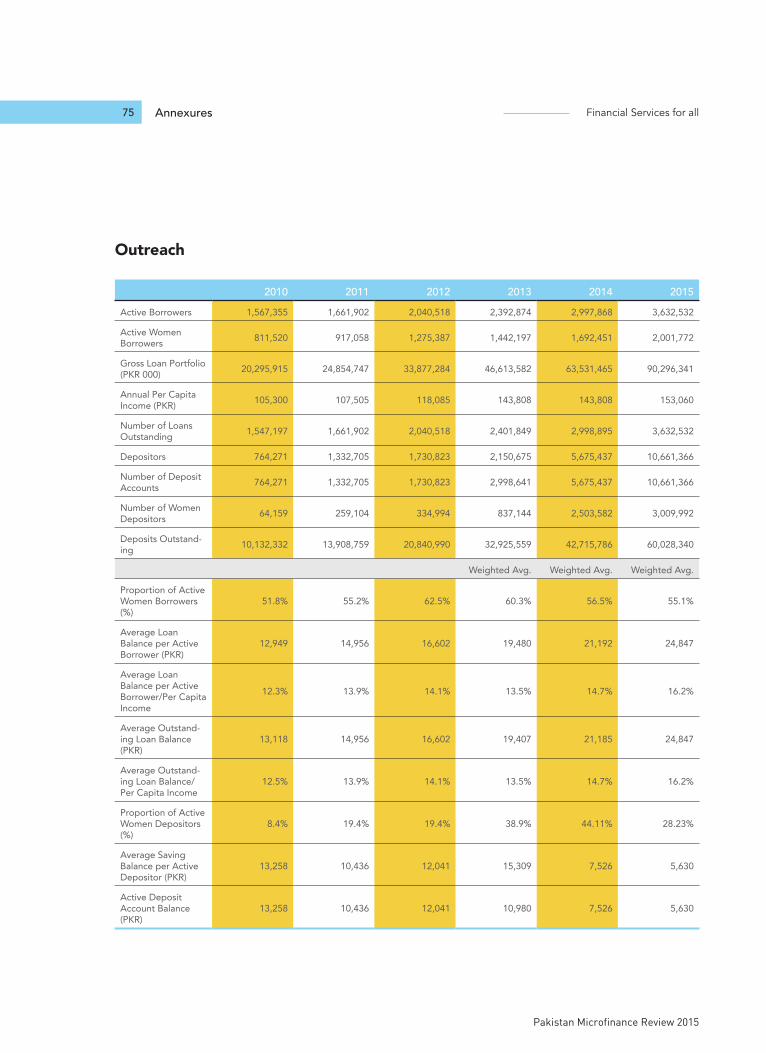

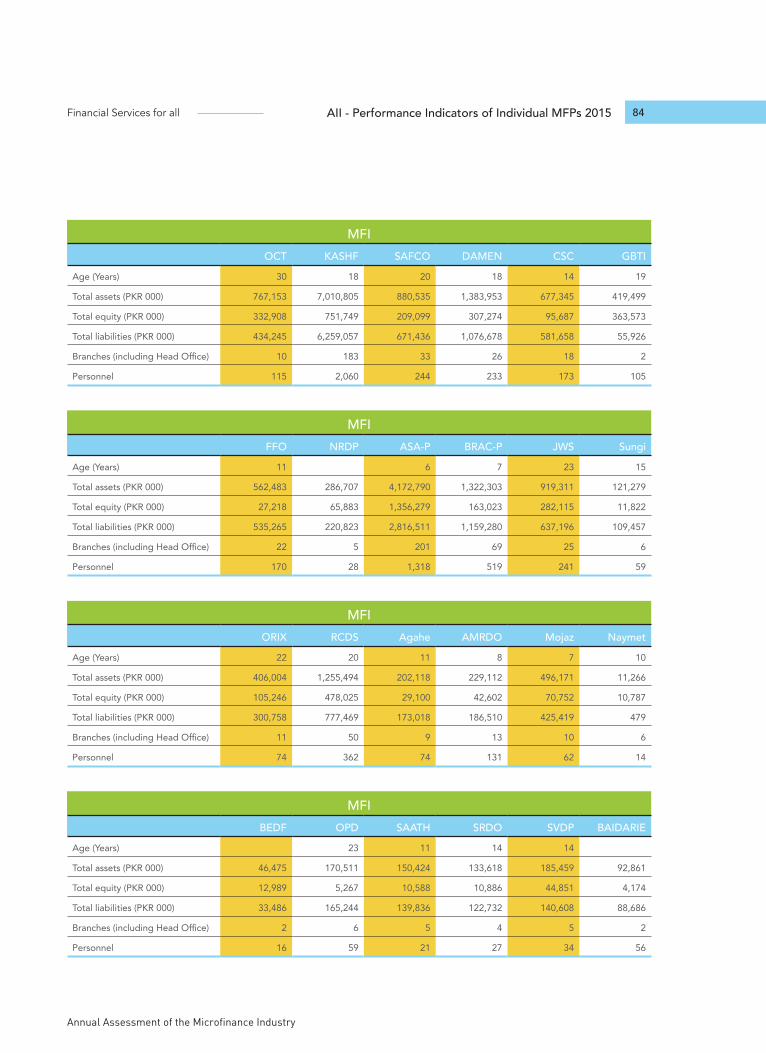

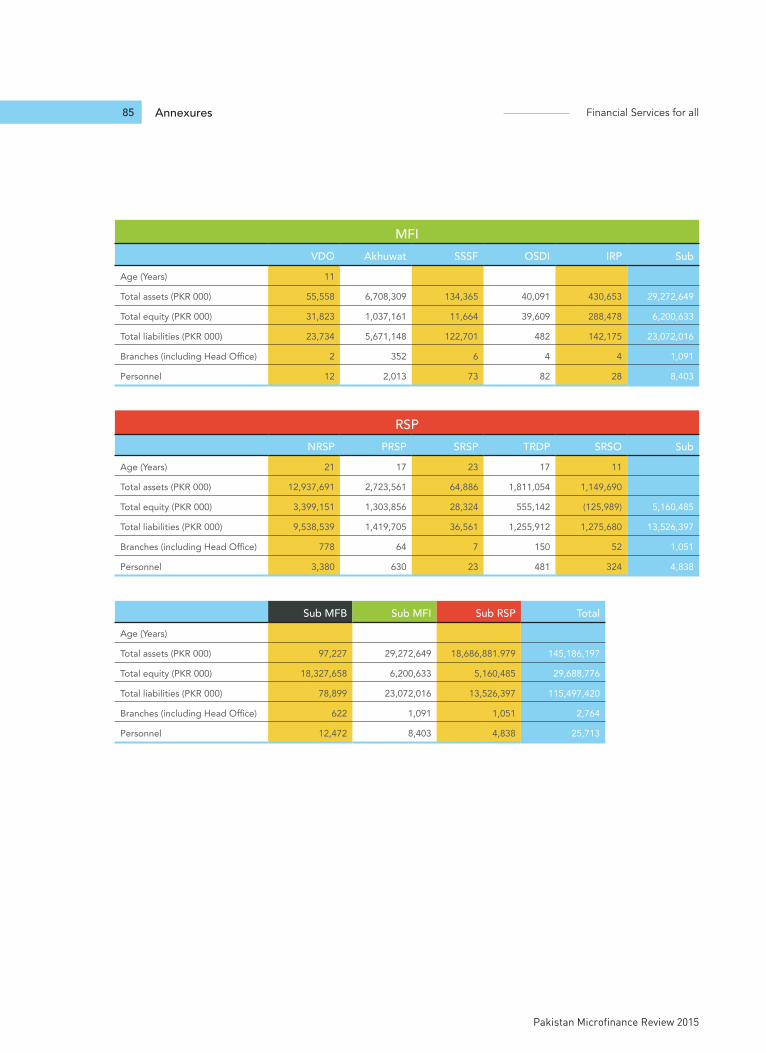

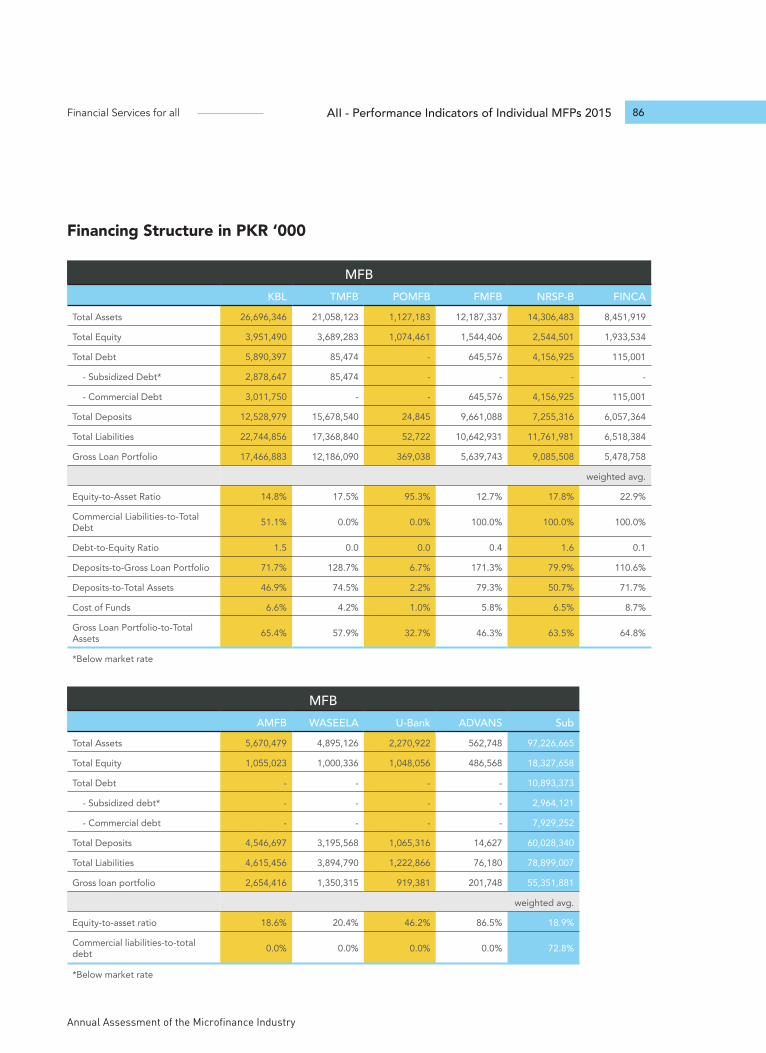

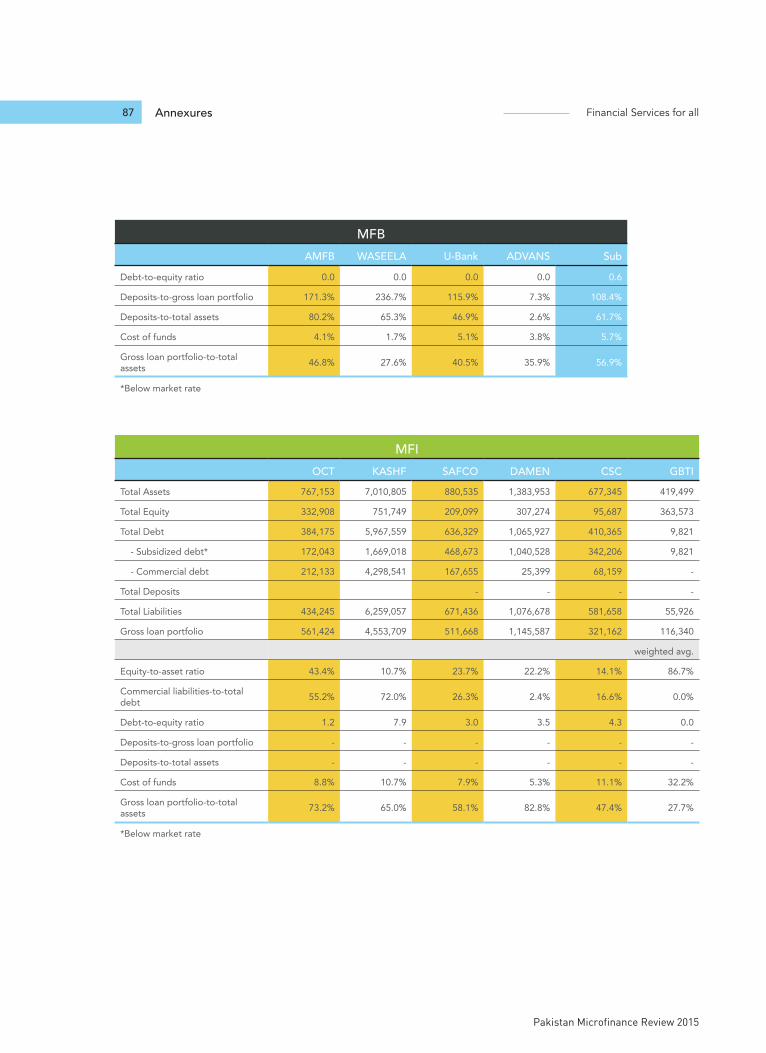

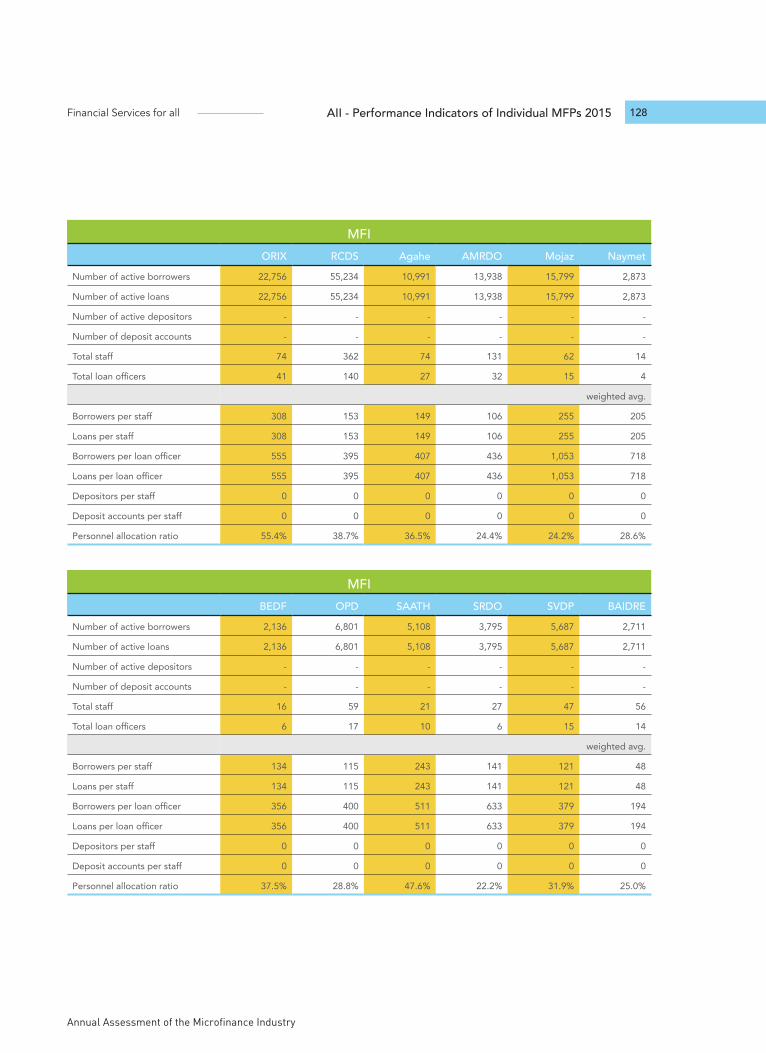

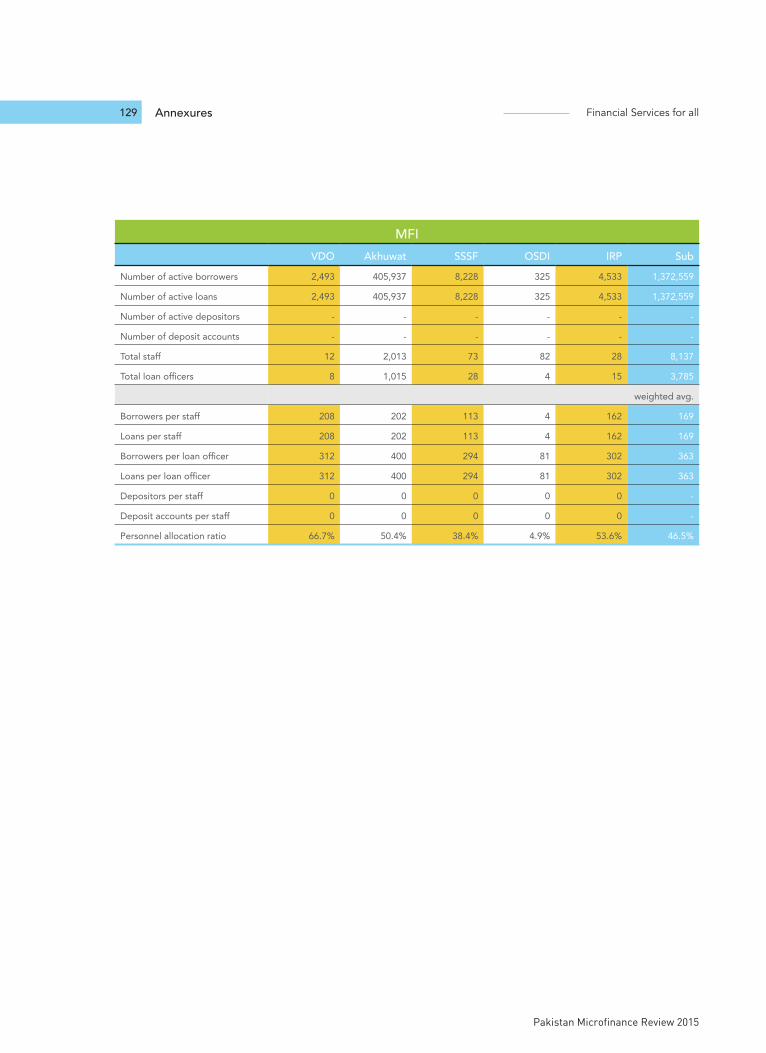

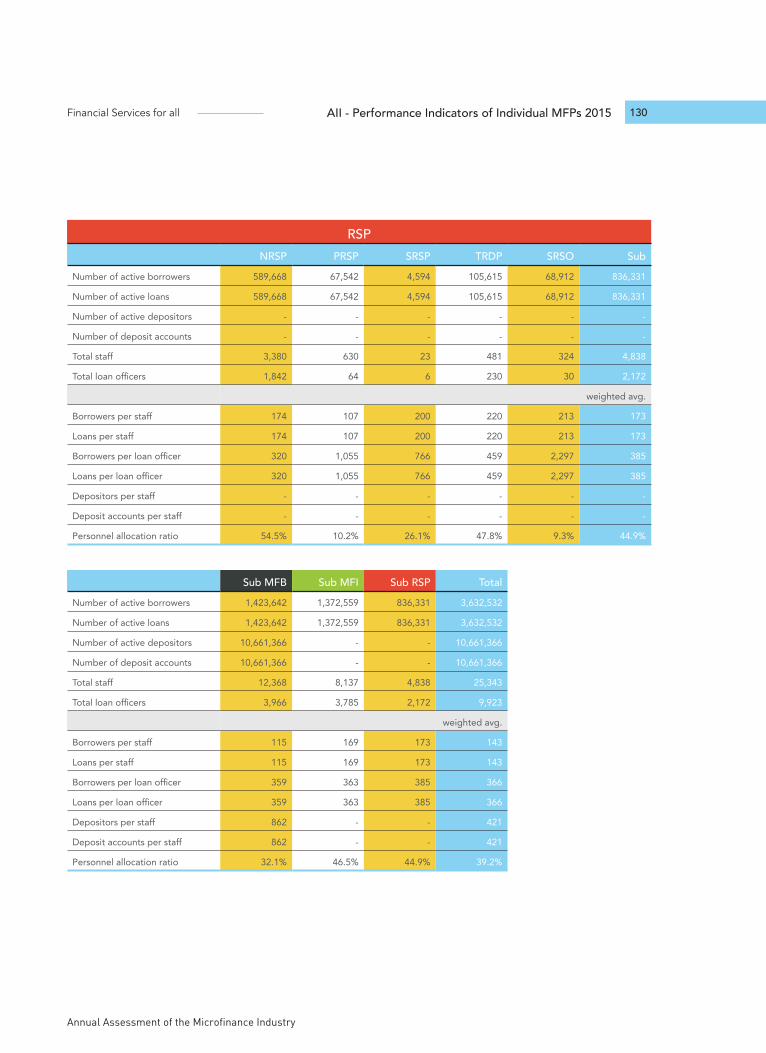

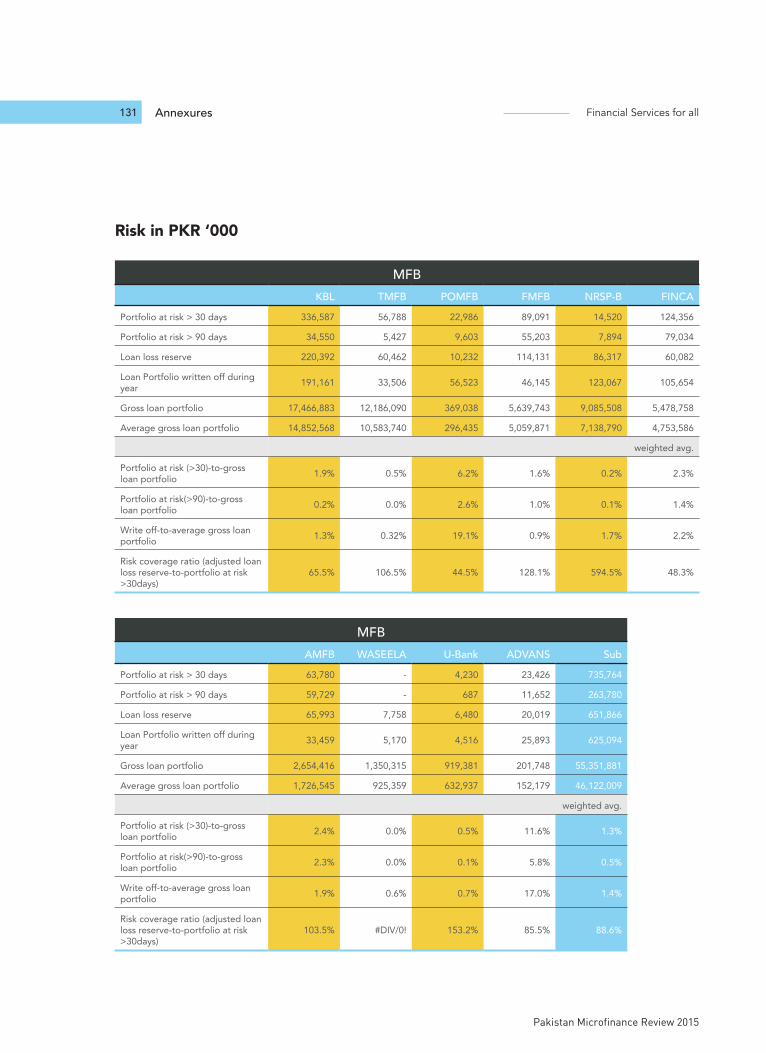

AI – Performance Indicators of Industry 2015

73

AII – Performance Indicators of Individual MFPs 2015

83

Scale and Outreach 18

Financial Structure 27

Profitability and Sustainability 31

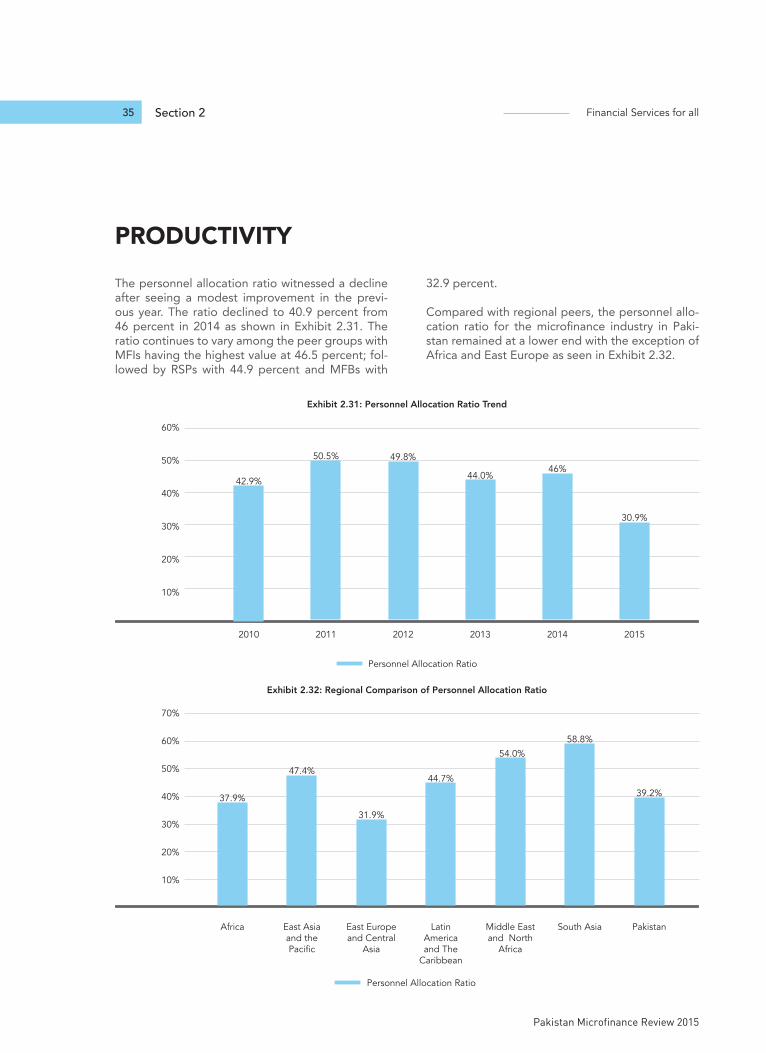

Productivity 35

Risk 36

Conclusion 37

Role of Microfinance in Financial Inclusion In Pakistan

61

Mainstreaming Non-Bank Microfinance Players

62

Credit Scoring 63

Mobile Wallets 63

Exploring New Horizons: Serving New Markets

64

Deposit Protection Fund: Moving Towards A Secure Financial Landscape

67

Deposits Mobilization: Untying Gordian’s Knot

68

Funding 68

Setting Up of Pakistan Microfinance Investment Company Limited (PMIC)

69

SECTION 1

THE YEAR IN REVIEW

Section 1 Financial Services for all

Pakistan Microfinance Review 2015

1

The microfinance industry witnessed continued growth and expansion in outreach in the year 2015. There were also notable developments in the poli-cy environment which can lead to strengthening of players such that the sector will be positioned to play a crucial role in furthering the agenda of finan-cial inclusion in the country.

Major developments were witnessed on the policy and regulatory fronts such as the launch of the Na-tional Financial Inclusion Strategy (NFIS) and the in-troduction of a regulatory framework for Non-Bank Microfinance Institutes (NBMFI) by the Securities & Exchange Commission of Pakistan (SECP). In addi-tion, results of the second Access to Finance Survey were launched. With the launch of NFIS, a road-map for achievement of financial inclusion in the country has been laid out. A key challenge facing the microfinance industry has been the absence of a regulatory framework for non-bank microfinance players. Now with the introduction of the rules and regulations for NBMFI a level playing field has been created in the industry and provides an opportunity for non-bank players to scale up their businesses.

The improving security situation, low inflation and subsequent reduction in the policy rate by the cen-tral bank bode well for the industry. However, fall-ing agriculture commodity prices could adversely affect the industry particularly those providers op-erating predominantly in the rural areas.

A number of new initiatives were launched in 2015 while existing ones were improved upon. One of the main initiatives last year was the re-estimation of the microfinance market in the country. In ad-

dition, 2015 saw the completion of three years of the Client Protection Initiative (CPI), funded by the State Bank of Pakistan (SBP) under the auspices of the Financial Inclusion Program (FIP). Moreover, the Microfinance Credit Information Bureau (MF-CIB) has become an essential component of the credit approval process by practitioners and credit scor-ing models are being developed based on its data. Branchless banking continues to witness huge trac-tion on all fronts stimulated by an enabling environ-ment. Moreover, a number of microfinance banks (MFBs) have initiated lending to micro-enterprises.

The Microfinance Growth Strategy 2020 launched by PMN during the year forecasts that the sector would require additional debt for on-lending of up to PKR 300 billion to reach the 10 million borrower mark. In order to meet the funding demands of the sector, PPAF, the Department for International De-velopment (DFID) through Karandaaz Pakistan, and the German Development Bank, KfW, have joined hands to establish Pakistan Microfinance Invest-ment Company Limited (PMICL), a private-sector investment finance company. The major objective of the new entity is to attract commercial funding to serve the increasing demand of those who are financially excluded and further improve the capa-bility and capacity of the sector to absorb these funds. The NFIS also recognizes microfinance as an important instrument for increasing financial inclu-sion in the country and an important milestone of the strategy is enhancing commercial funding for the microfinance sector through the creation of PMIC.

THE YEAR IN REVIEW

Annual Assessment of the Microfinance Industry

Financial Services for all 2The Year in Review

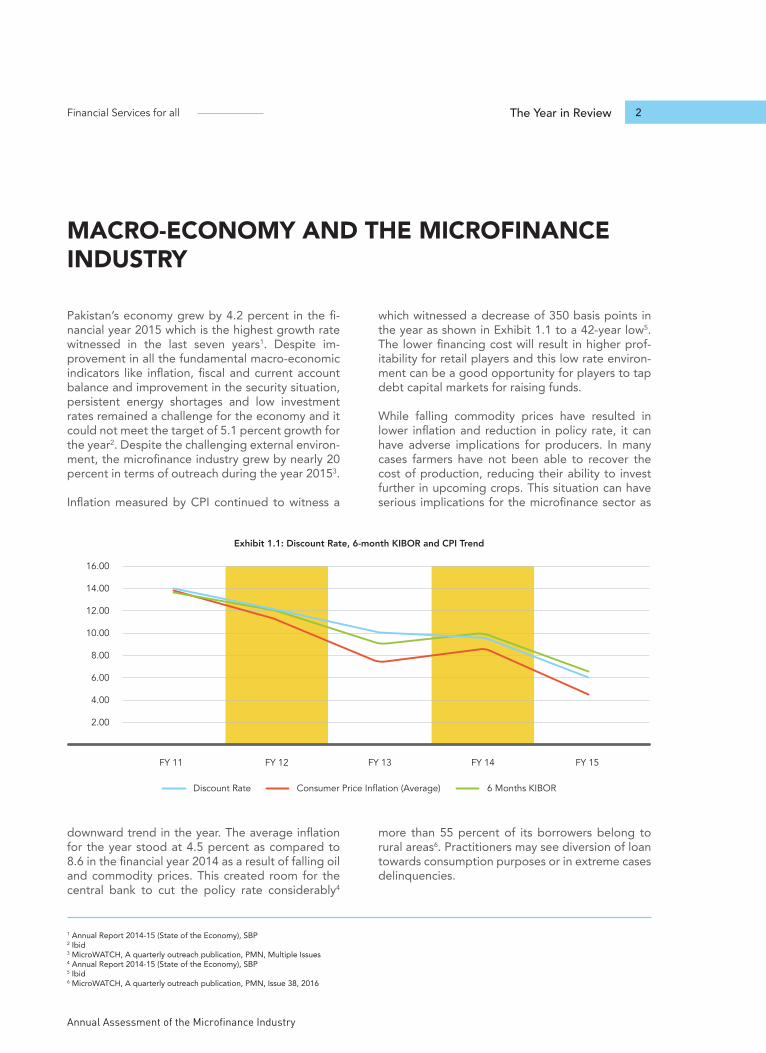

Pakistan’s economy grew by 4.2 percent in the fi-nancial year 2015 which is the highest growth rate witnessed in the last seven years1. Despite im-provement in all the fundamental macro-economic indicators like inflation, fiscal and current account balance and improvement in the security situation, persistent energy shortages and low investment rates remained a challenge for the economy and it could not meet the target of 5.1 percent growth for the year2. Despite the challenging external environ-ment, the microfinance industry grew by nearly 20 percent in terms of outreach during the year 20153.

Inflation measured by CPI continued to witness a

downward trend in the year. The average inflation for the year stood at 4.5 percent as compared to 8.6 in the financial year 2014 as a result of falling oil and commodity prices. This created room for the central bank to cut the policy rate considerably4

which witnessed a decrease of 350 basis points in the year as shown in Exhibit 1.1 to a 42-year low5. The lower financing cost will result in higher prof-itability for retail players and this low rate environ-ment can be a good opportunity for players to tap debt capital markets for raising funds.

While falling commodity prices have resulted in lower inflation and reduction in policy rate, it can have adverse implications for producers. In many cases farmers have not been able to recover the cost of production, reducing their ability to invest further in upcoming crops. This situation can have serious implications for the microfinance sector as

more than 55 percent of its borrowers belong to rural areas6. Practitioners may see diversion of loan towards consumption purposes or in extreme cases delinquencies.

MACRO-ECONOMY AND THE MICROFINANCE INDUSTRY

2.00

FY 11 FY 12 FY 13 FY 14 FY 15

4.00

6.00

8.00

10.00

12.00

14.00

16.00

Discount Rate Consumer Price Inflation (Average) 6 Months KIBOR

Exhibit 1.1: Discount Rate, 6-month KIBOR and CPI Trend

1 Annual Report 2014-15 (State of the Economy), SBP 2 Ibid3 MicroWATCH, A quarterly outreach publication, PMN, Multiple Issues 4 Annual Report 2014-15 (State of the Economy), SBP5 Ibid6 MicroWATCH, A quarterly outreach publication, PMN, Issue 38, 2016

Section 1 Financial Services for all

Pakistan Microfinance Review 2015

3

Despite the policy rate touching a historical low, ex-pansion in the private sector credit remained low as compared to the previous year7. Commercial banks continued to invest in the government securities in order to generate risk-less returns. With most of the existing private sector concentrated towards

manufacturing sector, areas like SMEs and agricul-ture continue to remain unserved. In this situation, MFPs will continue find it challenging to raise funds from commercial banks.

Pakistan’s overall regulatory environment continues to be ranked among the best globally8. Key devel-opments were witnessed in the industry on the pol-icy and regulatory domain in 2015. Last year saw the launch of the National Financial Inclusion Strat-egy (NFIS) and roll-out of regulations for non-bank MFPs which was among the key challenges being faced by the sector.

NATIONAL FINANCIAL INCLUSION STRATEGY (NFIS)

The National Financial Inclusion Strategy (NFIS) has outlined a roadmap for financial inclusion in the country. Developed by the State Bank of Pa-kistan with active assistance from The World Bank, the strategy aims to “build a dynamic and inclusive financial sector to support Pakistan’s growth in 21st century”9. The strategy will direct efforts and ini-tiatives to expand and deepen financial inclusion during the course of five years (2015-2020) and has set objectives to be achieved through a compre-hensive and well-thought action plan.

The state of financial inclusion in Pakistan depicts a dismal picture. Only 16 percent of the adult population can be categorized as banked and 23 percent of the population use formal financial services10. The situation worsens in the rural areas where only 14 percent of the adult population is banked. In the case of women, only 11 percent are banked. The state of financial inclusion is no more evident when compared regionally as shown in Table 1.1 where Pakistan continues to lag behind

other countries. Despite sustained efforts by the policy makers, regulators and donors and enjoying an enviable enabling environment a lot more needs to be done. In this regard, NFIS will play a crucial role in furthering financial inclusion in the country by coordinating the efforts of all the stakeholders, by defining responsibilities among them and by de-veloping a comprehensive approach to promoting access and usage of formal financial services.

The framework for action for the strategy identi-fies four targeted actions or key drivers to achieve financial inclusion in the country. These four drivers are 1) promoting digital transactions and reaching scale through bulk payments; 2) expanding and di-versifying access points; 3) improving capacity of financial services providers; and 4) increasing levels of financial capability. The success of these drivers is dependent upon meeting four preconditions or key enablers which have been identified as:

• Public and private sector commitment to NFIS• Enabling Legal and Regulatory Requirements • Adequate supervisory and judicial capacity • Financial payments, information and communi-

cation technology

Achievement of financial inclusion in the country requires efforts from a wide range of stakeholders and in order to direct their efforts a coordination mechanism has been developed which includes a NFIS Council to be chaired by the Finance Minister, a steering committee headed by the Governor SBP and the establishment of an NFIS Secretariat.

POLICY AND REGULATORY ENVIRONMENT

7 Annual Report 2014-15 (State of the Economy), SBP 8 The Global Microscope 2015: The enabling environment for financial inclusion, EIU,20159 National Financial Inclusion Strategy (NFIS), SBP10 www.a2f2015.com

Annual Assessment of the Microfinance Industry

Financial Services for all 4The Year in Review

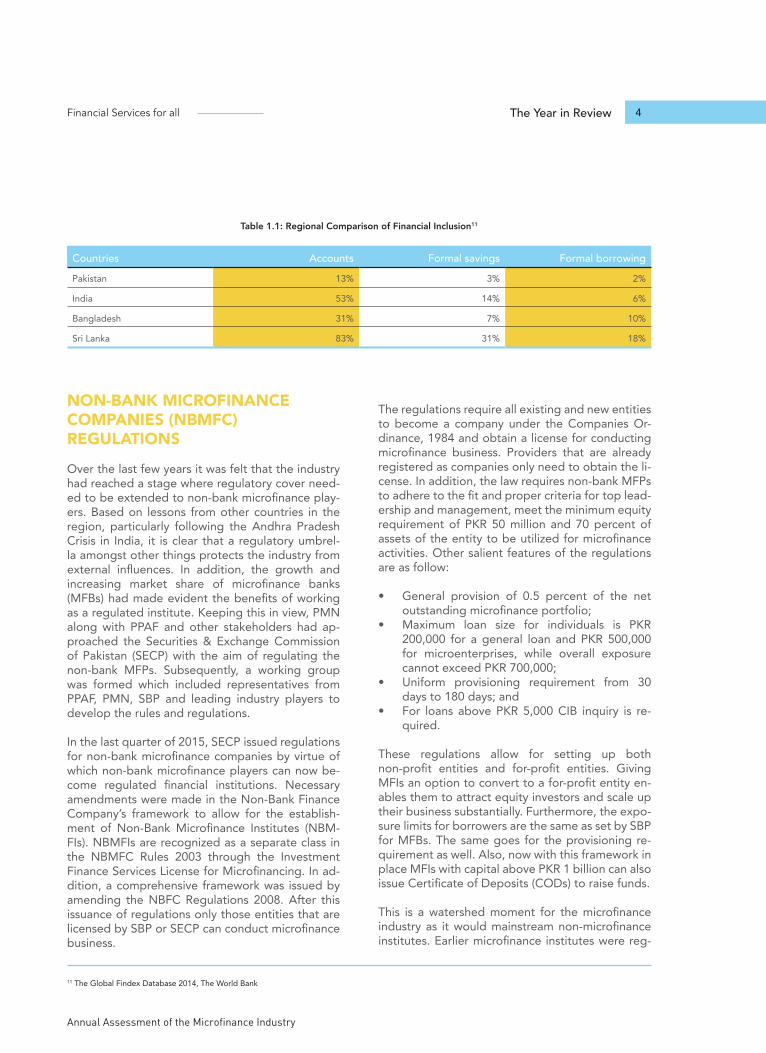

NON-BANK MICROFINANCE COMPANIES (NBMFC) REGULATIONS

Over the last few years it was felt that the industry had reached a stage where regulatory cover need-ed to be extended to non-bank microfinance play-ers. Based on lessons from other countries in the region, particularly following the Andhra Pradesh Crisis in India, it is clear that a regulatory umbrel-la amongst other things protects the industry from external influences. In addition, the growth and increasing market share of microfinance banks (MFBs) had made evident the benefits of working as a regulated institute. Keeping this in view, PMN along with PPAF and other stakeholders had ap-proached the Securities & Exchange Commission of Pakistan (SECP) with the aim of regulating the non-bank MFPs. Subsequently, a working group was formed which included representatives from PPAF, PMN, SBP and leading industry players to develop the rules and regulations.

In the last quarter of 2015, SECP issued regulations for non-bank microfinance companies by virtue of which non-bank microfinance players can now be-come regulated financial institutions. Necessary amendments were made in the Non-Bank Finance Company’s framework to allow for the establish-ment of Non-Bank Microfinance Institutes (NBM-FIs). NBMFIs are recognized as a separate class in the NBMFC Rules 2003 through the Investment Finance Services License for Microfinancing. In ad-dition, a comprehensive framework was issued by amending the NBFC Regulations 2008. After this issuance of regulations only those entities that are licensed by SBP or SECP can conduct microfinance business.

The regulations require all existing and new entities to become a company under the Companies Or-dinance, 1984 and obtain a license for conducting microfinance business. Providers that are already registered as companies only need to obtain the li-cense. In addition, the law requires non-bank MFPs to adhere to the fit and proper criteria for top lead-ership and management, meet the minimum equity requirement of PKR 50 million and 70 percent of assets of the entity to be utilized for microfinance activities. Other salient features of the regulations are as follow:

• General provision of 0.5 percent of the net outstanding microfinance portfolio;

• Maximum loan size for individuals is PKR 200,000 for a general loan and PKR 500,000 for microenterprises, while overall exposure cannot exceed PKR 700,000;

• Uniform provisioning requirement from 30 days to 180 days; and

• For loans above PKR 5,000 CIB inquiry is re-quired.

These regulations allow for setting up both non-profit entities and for-profit entities. Giving MFIs an option to convert to a for-profit entity en-ables them to attract equity investors and scale up their business substantially. Furthermore, the expo-sure limits for borrowers are the same as set by SBP for MFBs. The same goes for the provisioning re-quirement as well. Also, now with this framework in place MFIs with capital above PKR 1 billion can also issue Certificate of Deposits (CODs) to raise funds.

This is a watershed moment for the microfinance industry as it would mainstream non-microfinance institutes. Earlier microfinance institutes were reg-

Countries Accounts Formal savings Formal borrowing Pakistan 13% 3% 2%

India 53% 14% 6%

Bangladesh 31% 7% 10%

Sri Lanka 83% 31% 18%

Table 1.1: Regional Comparison of Financial Inclusion11

11 The Global Findex Database 2014, The World Bank

Section 1 Financial Services for all

Pakistan Microfinance Review 2015

5

istered in multiple legal jurisdictions and operated under a legal framework that can be categorized as ambiguous at best. Lastly, it is hoped that the SECP will play a similar role to that played by the SBP in nurturing MFBs and interact frequently with the players for the benefit of the industry.

LIMIT TO FINANCING AGAINST GOLD BACKED LOANS

Financing against gold backed loans by Microfi-nance Banks (MFBs) had gained widespread pop-ularity in the last few years. It had allowed MFBs to move from traditional group lending to individ-ual lending and also, increase their loan sizes. This mode of financing drew its strength from the fact that gold and gold ornaments have been a tradi-tional mode of savings among the masses which in times of emergency is liquidated often at a deep discount. Obtaining a loan against this gold without having to liquidate provided a better alternative to potential borrowers and saw to its massive popular-ity. This product effectively transformed gold from a non-liquid asset into a liquid and earning asset. Pioneered by Tameer Microfinance Bank (TMFB), it was soon adopted by other MFBs. At this time up to 5 MFBs are dealing in this product and the per-

centage of the gross loan portfolio (GLP) financed against gold ranges from 20 percent to 55 percent. However, concerns were raised about the practice especially whether the loan were being utilized for consumption purposes rather than productive ones. Also, were the loan amounts being determined based on the value of the gold or based on the repayment capacity of the client? These concerns led to strengthening of the belief that gold backed loans were against the spirit of microfinance which promotes lending without physical collateral. This coupled with falling gold prices leading to reduced value of collateral available with MFBs led the cen-tral bank to place a limit on financing against gold.

SBP by virtue of an amendment in the prudential regulation R-5 dealing with maximum loan size and eligibility of borrowers for MFBs placed a limit that aggregate loan exposure of a MFB cannot exceed 35 percent of its GLP12. Existing MFBs having an exposure of more than 35 percent were given two years to bring their portfolios in compliance with the above regulation. In addition, SBP also stressed that MFBs develop a collateral handling policy duly approved by their Board for managing the security, procedures and contingency planning for the gold collateral.

The year saw a number of new initiatives being undertaken including most significantly the re-es-timation of the microfinance market potential and successful completion of the Client Protection Ini-tiative (CPI).

BRANCHLESS BANKING

With a firmly established regulatory environment and a supporting institutional framework, the branchless banking sector of Pakistan continued to excel on all fronts in the calendar year 2015. The mandatory biometric SIM verification for all new and existing mobile phone customers in the same year, as instructed by the Pakistan Telecommunica-tion Authority (PTA), also played a crucial role in

stimulating branchless banking activity.

As of September 30, 2015, the value of branchless banking transactions stood at PKR 526 billion as compared to PKR 376 billion in the same period for the previous year13 – depicting an increase of 40 percent. Moreover, the number of branchless banking transactions, for the first time, crossed the 100-million mark resting at 101 million as of Sep-tember 30, 2015.

It is important to note that approximately 5 per-cent of the 101 million transactions were carried out by agents for liquidity management, whereas, the remaining 95 percent were customer oriented transactions (which include over-the-counter and

MICROFINANCE INDUSTRY INITIATIVES

12 AC & MFD Circular 02 of 2015, June 18, 2015, SBP13 Branchless Banking Newsletter, Issue 17, 2015, State Bank of Pakistan (SBP)

Annual Assessment of the Microfinance Industry

Financial Services for all 6The Year in Review

m-wallet transactions). However, branchless bank-ing agents had a significant share (of 40 percent) in the value of transactions – PKR 208 billion worth of transactions were conducted for liquidity man-agement.

In terms of customer oriented transactions, over-the-counter transactions amounted to 69 percent of the total number of transactions and 71 percent of the total value of transactions. Fund transfers through CNIC (sending and receiving) remained the top contributor in terms of volume and value of transactions with a share of 33 percent and 44 percent respectively. Bill payments (utility and in-ternet) had the second largest share in terms of both, volume (29 percent) and value (18 percent) within customer oriented transactions14.

The branchless banking platform is also proving to be an effective instrument in channeling govern-ment-to-person payments of salary disbursements, pensions, and tax collection services. An amount of PKR 22 billion was disbursed to 4.5 million bene-ficiaries during the third quarter of 2015 as com-pared to PKR 16 billion disbursed to 5.5 million beneficiaries during the same quarter of 2014. The majority of the G2P payment beneficiaries are as-sociated with the Benazir Income Support Program (BISP), followed by internally displaced people.

Lately, branchless banking operators have also in-troduced innovative Person-to-Government (P2G) payment products for the collection of taxes, traf-fic penalties and other payments to government agencies. Mobile network operators are partnering with public entities to enhance the scope of digital financial services that can be accessed quickly and at the convenience of the users, thus facilitating both the government and individuals.

Telenor’s EasyPaisa was the first service provider to set foot in this domain by offering the option to pay for traffic penalties through the branchless banking platform – including mobile wallets. Mobilink’s Mo-bicash has recently introduced a product where consumers can pay for their passport fee through any Mobicash agent or via their m-wallet account.

MICROFINANCE CREDIT INFORMATION BUREAU (MF-CIB)

MF-CIB is a key part of the microfinance industry infrastructure in Pakistan. Established with the as-sistance of the International Finance Corporation (IFC), the Department for International Develop-ment (DFID) and the Pakistan Poverty Alleviation Fund (PPAF), the credit registry is increasingly used for risk mitigation by the players. The bureau aims to curtail the practice of multiple borrowing leading

14 Ibid15 DataCheck (Pvt.) Limited, Credit Bureau Organization housing MF-CIB

Exhibit 1.2: Month-on-month Comparison of MF-CIB Inquiries15

50,000

2014 2015

100,000

150,000

200,000

250,000

MF-

CIB

Inqu

iries

JAN FEB MAR APR MAY JUN JUL AUG SEP OCT NOV DEC

Section 1 Financial Services for all

Pakistan Microfinance Review 2015

7

to over-indebtedness, moral hazard and adverse se-lection in the sector. In addition, the bureau’s abil-ity to generate both positive and negative reports allows for developing and utilizing credit histories.

Since its nationwide roll-out in 2012, the bureau is now an integral part of the ecosystem with eighty percent of the players making inquiries from the bu-reau. As seen in Exhibit 1.2 below, there has been a substantial increase in inquiries being generated as compared to the previous year with maximum number of inquiries being generated per month reaching 198 thousand in December 2015.

With the regulations for non-bank microfinance players requiring an inquiry to be generated for loans over PKR 5000 and continued increase in out-reach we are likely to see a further increase in the inquires being generated.

The bureau as of December 2015, holds over 9.5 million records and efforts are underway to de-velop a credit scoring model based on the data sourced from it. Credit scoring will assist lenders in determining who qualifies for a loan, how much loan amount they should get and also help in deter-mining the risk in lending. Since the score is based on actual data its remains a reliable assessment of a client. Moreover, it will assist members in customer acquisition and retaining good clients. In addition,

bad debtors can be isolated and monitored closely. Lastly, credit scoring can also lead players to apply a risk-based pricing mechanism by rewarding good client by charging them less and charging a higher rate to higher risk borrowers.

With MF-CIB taking an increasingly important role in the context of microfinance industry it is natural that the microfinance clients need to be educated about the role and importance of bureau in the lending process. How will good credit history be rewarded? What will be the effect of taking loans from multiple lenders? How badly will be the im-pact of default or delayed payments on the credit worthiness of a client? In order to address these is-sues, a literacy program has been launched for the microfinance borrowers by PMN in collaboration with IFC. The programme aims to develop aware-ness amongst the borrowers about credit reports being generated by the MFPs and how they should manage their credit histories.

ESTIMATING MICROFINANCE MARKET POTENTIAL16

While there is reliable, up-to-date and periodic in-formation available on industry benchmarks and in-dicators, there is an information gap related to the potential size of the market. The current figure of

16 Estimating Potential Market Size for Microcredit in Pakistan, MicroNOTE No. 27, Dec 2015

Exhibit 1.2: Month-on-month Comparison of MF-CIB Inquiries

50,000

2014 2015

100,000

150,000

200,000

250,000

MF-

CIB

Inqu

iries

JAN FEB MAR APR MAY JUN JUL AUG SEP OCT NOV DEC

Annual Assessment of the Microfinance Industry

Financial Services for all 8The Year in Review

27 million individual borrowers based on PMN’s old methodology was dated and had not been revised since 2007. A revised and up-to-date estimation will provide invaluable information for the donors, policy makers and most importantly, practitioners.

The parameters and dataset of the old methodol-ogy lack relevance to the present day outlook of the industry. PMN’s proposed/current methodolo-gy uses a more robust and up-to-date framework to calculate the market potential for microcredit. A nationally representative dataset is used with sup-porting parameters or filters with germane under-lying assumptions. This potential is further sliced into different segments such as occupation, labor market status and gender.

Using up-to-date nationally representative survey data (HIES - PSLM 11-12), PMN has built a pyra-mid model whose main parameters include willing-ness to demand a loan in the past or propensity to borrow in the future, income ranges and cred-it worthiness. There is anecdotal evidence which shows that willingness or propensity to take a loan could be a good starting point whilst calculating market potential. The dataset contains information on socio-economic indicators that are periodically available, credible, and easily accessible and has the level of detail that would allow segmentation. The survey is carried out by the Pakistan Bureau of Statistics (PBS) every alternative year and contains information on socio-economic factors such as in-come, expenditure and employment status.

The framework encompasses the following: those individuals who have an outstanding loan from any source at the time of the survey or have borrowed in the year immediately before are selected, indi-viduals in the age bracket of 18-65, an average loan range of PKR 20, 00 – 150,000 is selected (along with another loan range for a sensitivity analysis) and finally the total potential is divided into differ-ent segments. PMN has used statistical software using all these parameters and filters to calculate the total potential. The total potential market for microcredit has been calculated to be at 17 million individual borrowers.

Furthermore, the old methodology did not have an estimate for ‘micro-enterprises’. Using the same

dataset (HIES 2011-12), our proposed framework for estimating microenterprises is built around a section of the survey that contains data on house-hold heads who are either proprietors or partners in a non-agricultural, non-financial establishment, business or shop (mobile or fixed) that employs less than 10 persons at any given time during the year.

The information in HIES is limited to certain enter-prises that are related to manufacturing, mining, quarrying, transportation, wholesale/retail trade, hospitality, construction and other service related businesses. However, there are some enterprises that are not captured in HIES which includes the agricultural, livestock and fisheries sectors. The to-tal market potential estimated for microenterprises has been estimated to be 6.5 million enterprises.

Agriculture activities in Pakistan mostly take the form of farming and livestock rearing. PMN uses a framework whereby it used land sizes defined by the Federal Land Commission throughout Pa-kistan. Since the activities carried out on the farm by the household are indivisible and Pakistan hasn’t reached a level of mechanization that would enable specialization to take place at this scale, we pro-posed that the unit of measurement to be the farm size under any of three predominantly prevalent land tenure arrangements in Pakistan, namely own-er cultivated, share cropped and tenant farming types. As such, we use subsistence and economic land holdings across all provinces to be used as the cut-off for small and micro agricultural farms. The total potential for farm microenterprises comes out to be 1 million enterprises.

MICRO-ENTERPRISE LENDING

Enterprise lending has been in vogue ever since State Bank of Pakistan (SBP) allowed MFBs to up-scale their loan sizes from PKR 150 thousand to PKR 500 thousand through amendments in the Pruden-tial Regulations in 2012. The inability of commercial banks to scale down to serve the lower end of SME or very Small Enterprises (VSE) and the similarity of dynamics between the SME and microfinance mar-ket led to policymakers turning to the microfinance industry to serve these markets. At present MFBs can lend up to 40 percent of the GLP to microen-terprises.

Section 1 Financial Services for all

Pakistan Microfinance Review 2015

9

VSE or microenterprises make up nearly 99 per-cent of the SMEs in the country and play a crucial role in income and employment generation17. The segment is viewed as more stable as compared to microfinance as it has a higher degree of formaliza-tion, a designated business premises and possess-es some fixed assets. Lending to this particular seg-ment allows, MFPs to retain graduating clients who have grown to size where micro-loans cannot meet their funding needs and diversify into a newer mar-ket segment. In addition, it provides an opportuni-ty to increase profitability as enterprise loans have lower operational costs as compared to microloans and allows for risk-based pricing of loans.

Currently, eight out of ten MFBs have started lend-ing to this segment. Out of these eight, six are at the pilot stage. Consolidated figures for the seven MFBs lending to this particular segment are shown in Table 1.2.

According to a survey conducted by IFC regarding lending to microenterprises by MFBs, most players have built the capacity of their staff to serve this particular segment. In addition, separate risk as-sessment methodologies and IT system have been developed. Moreover, specialized staff has been dedicated for enterprise lending grouped in a separate division. Generally, MFBs are not extend-ing loans to microenterprises through all of their branches and tend to serve the same sectors as microfinance clients. Most of the clients belong to the transport sector, followed by services and re-tail. Potential clients are acquired in the same man-ner as microfinance clients and traditional delivery channels are commonly used. However, there is a growing awareness among the players to utilize branchless banking channels for distribution. Key

challenges include ability of loan officers and con-cern over lack of capacity to analyze micro-enter-prises.

PRIME MINISTER INTEREST FREE LOAN SCHEME

The Government of Pakistan (GoP) launched an interest-free microloan scheme in 2014 to address the issues of poverty and rising unemployment in the country. Under the scheme, PKR 3.5 billion were allotted from the federal budget to facilitate the poor and destitute segments of the popula-tion in generating livelihood. However, in order to safeguard the interests of the MFPs it was decided that the funds under this scheme would be routed through the national apex, PPAF, and would only be extended in Union Councils that have low or no penetration of conventional microfinance.

As of December 2015, PKR 2.25 billion have been disbursed under the scheme to approximately 110,000 beneficiaries – out of which 66,000 were female and 44,000 were male applicants19. These interest free loans are being made available to men and women from households with a score of up to 40 on the Poverty Score Card (PSC) and with little or no access to banks or microcredit institutions. Most of the loans have been utilized in the livestock sector, followed by business and trading, services and agriculture.

Twenty-four MFPs have partnered with PPAF in extending interest free loans under the PM Inter-est-Free Loan scheme. It is hoped that the scheme would lead to over 1 million additional active bor-rowers over the next three years. Since this scheme is targeted toward those areas where conventional

Year 2013 2014 2015Number of Loans 136 2,185 12,612

GLP 33,902,858 530,587,461 3,061,824,879

Average Loan Size 249,286 242,832 242,771

PAR > 30 Days 0% 1.0% 1.3%

Table 1.2: Trend of Micro-Enterprise Lending by Selected MFBs18

17 Federal Bureau of Statistics, Government of Pakistan, 2005 18 Figures obtained from 7 MFBs19 http://www.pmifl.com.pk/

Annual Assessment of the Microfinance Industry

Financial Services for all 10The Year in Review

microfinance has little or no penetration, it pro-vides MFPs an opportunity to expand outreach in newer geographic markets. Moreover, it has the potential to allow borrowers of interest free loans to graduate to conventional microfinance. This is ensured as the interest free loan would be provided only once to an individual and after the completion of the first cycle he/she would be eligible only for a conventional microfinance loan.

CREDIT GUARANTEE SCHEME FOR SMALL & MARGINALIZED FARMERS

In 2015, the Government of Pakistan launched a credit guarantee scheme for small and marginalized farmers to ensure greater access to bank loans for production purposes. The scheme provides 50 per-cent risk coverage against the principal outstand-ing on loans to small and marginalized farmers by commercial, specialized and microfinance banks.

The federal government made an initial allocation of PKR 1 billion in the federal budget FY 2015-16, for the scheme which may be topped up annually. The allocated funds will be used to create a guaran-tee fund for farmers having up to 5 acres irrigated and 10 acres non-irrigated land holdings.

The objective of the scheme is to encourage par-ticipating commercial, specialized and microfi-nance banks to lend collateral-free to small and marginalized farmers to meet their working capital requirements. Credit Guarantee Limits (CGLs) will be assigned to all financial institutions involved in agriculture financing based on their exposure and potential in agricultural credit disbursements. The scheme is also open to all those banks which are not currently involved in agricultural financing by expressing their willingness to participate in the said scheme.

The scheme aims to benefit 300,000 farmer house-holds with production loans of up to PKR 100,000 and the loan tenor will be based on the cropping cycle up to a maximum period of one year20.

The scheme will exclusively apply to small and mar-ginalized farmers across the country owning/culti-

vating irrespective of land ownership. According to SBP, as per the Agriculture Census 2010, 5.35 million farm households (out of total 8.3 million) have landholding up to five acres in Pakistan. These small farmers have a significant share in the nation-al agricultural output. Despite their significance, they face difficulties in accessing formal credit due to size of the landholding and lack of collateral. As a result, they are forced to borrow from informal sources on unfair terms. Therefore, the scheme has been designed to enhance access of small and mar-ginalized farmers to formal credit.

CLIENT PROTECTION INITIATIVE (CPI)

The microfinance sector in Pakistan has shown an increasing focus on balancing social performance and financial sustainability among microfinance providers (MFPs). There is an understanding of mi-crofinance as a double-bottom line industry, where sustainability is not an end in itself but rather a means to achieving social goals. These goals can differ; while some MFPs may have a vision of pov-erty alleviation or women and rural community em-powerment, others focus on increasing access to formal finance for the poor and low-income strata of the population. In all cases, it has become im-portant for MFPs to track their progress towards achieving their respective social goals, using social performance and client protection parameters in the same way that financial data is used to manage the financial bottom line.

In tandem with its commitment to responsible fi-nance principles, PMN implemented the Client Protection Initiative (CPI), a 3-year project, funded under the State Bank of Pakistan (SBP) Financial Inclusion Program (FIP), which advocated client protection processes at industry level. The year in review saw the closing of the said project, culminat-ing in a series of lessons for the industry and paving the road forward.

The project consisted of two components:

20 Credit Guarantee for Small & Marginalized Farmers (CGSMF) Circular No.1, State Bank of Pakistan

Section 1 Financial Services for all

Pakistan Microfinance Review 2015

11

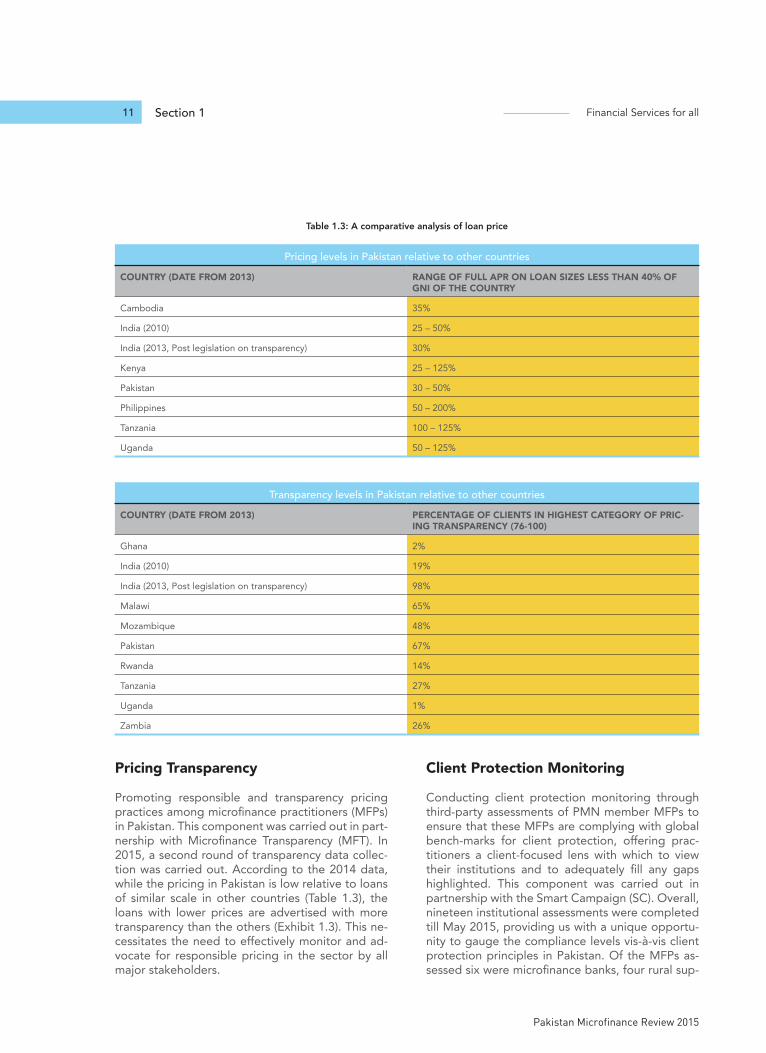

Pricing Transparency

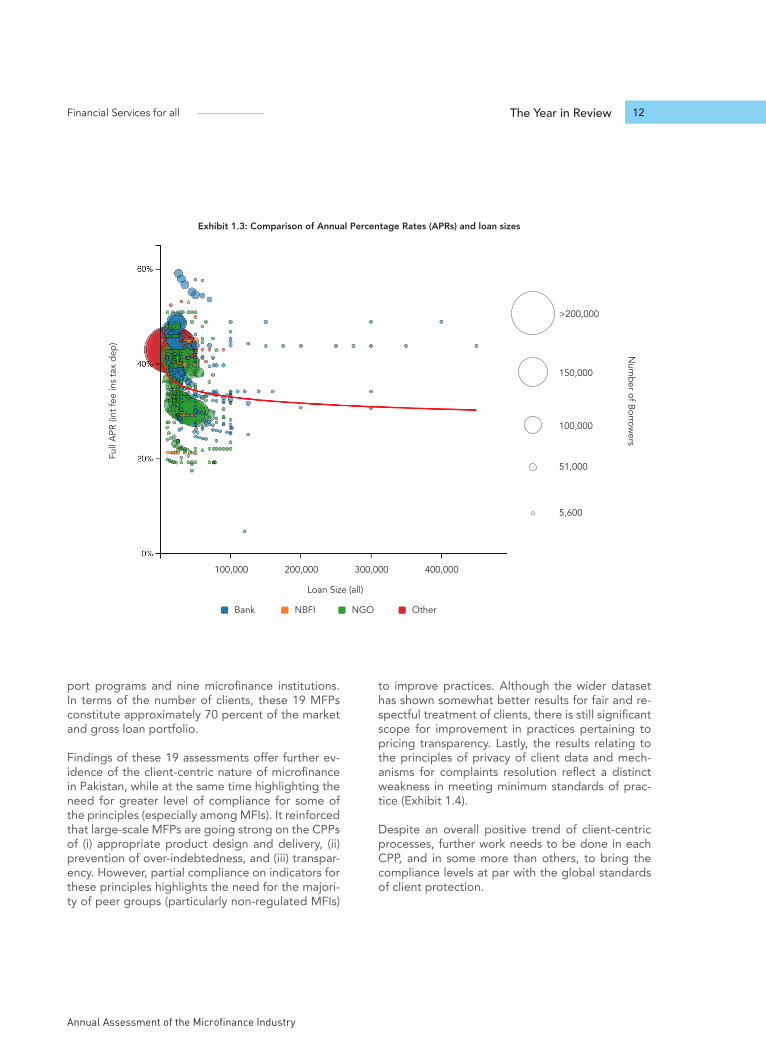

Promoting responsible and transparency pricing practices among microfinance practitioners (MFPs) in Pakistan. This component was carried out in part-nership with Microfinance Transparency (MFT). In 2015, a second round of transparency data collec-tion was carried out. According to the 2014 data, while the pricing in Pakistan is low relative to loans of similar scale in other countries (Table 1.3), the loans with lower prices are advertised with more transparency than the others (Exhibit 1.3). This ne-cessitates the need to effectively monitor and ad-vocate for responsible pricing in the sector by all major stakeholders.

Client Protection Monitoring

Conducting client protection monitoring through third-party assessments of PMN member MFPs to ensure that these MFPs are complying with global bench-marks for client protection, offering prac-titioners a client-focused lens with which to view their institutions and to adequately fill any gaps highlighted. This component was carried out in partnership with the Smart Campaign (SC). Overall, nineteen institutional assessments were completed till May 2015, providing us with a unique opportu-nity to gauge the compliance levels vis-à-vis client protection principles in Pakistan. Of the MFPs as-sessed six were microfinance banks, four rural sup-

Pricing levels in Pakistan relative to other countriesCOUNTRY (DATE FROM 2013) RANGE OF FULL APR ON LOAN SIZES LESS THAN 40% OF

GNI OF THE COUNTRY

Cambodia 35%

India (2010) 25 – 50%

India (2013, Post legislation on transparency) 30%

Kenya 25 – 125%

Pakistan 30 – 50%

Philippines 50 – 200%

Tanzania 100 – 125%

Uganda 50 – 125%

Transparency levels in Pakistan relative to other countriesCOUNTRY (DATE FROM 2013) PERCENTAGE OF CLIENTS IN HIGHEST CATEGORY OF PRIC-

ING TRANSPARENCY (76-100)

Ghana 2%

India (2010) 19%

India (2013, Post legislation on transparency) 98%

Malawi 65%

Mozambique 48%

Pakistan 67%

Rwanda 14%

Tanzania 27%

Uganda 1%

Zambia 26%

Table 1.3: A comparative analysis of loan price

Annual Assessment of the Microfinance Industry

Financial Services for all 12The Year in Review

Exhibit 1.3: Comparison of Annual Percentage Rates (APRs) and loan sizes

Full

APR

(int

fee

ins

tax

dep) N

umber of B

orrowers

100,000

5,600

51,000

100,000

150,000

>200,000

200,000 300,000

Loan Size (all)

400,000

Bank NGONBFI Other

port programs and nine microfinance institutions. In terms of the number of clients, these 19 MFPs constitute approximately 70 percent of the market and gross loan portfolio.

Findings of these 19 assessments offer further ev-idence of the client-centric nature of microfinance in Pakistan, while at the same time highlighting the need for greater level of compliance for some of the principles (especially among MFIs). It reinforced that large-scale MFPs are going strong on the CPPs of (i) appropriate product design and delivery, (ii) prevention of over-indebtedness, and (iii) transpar-ency. However, partial compliance on indicators for these principles highlights the need for the majori-ty of peer groups (particularly non-regulated MFIs)

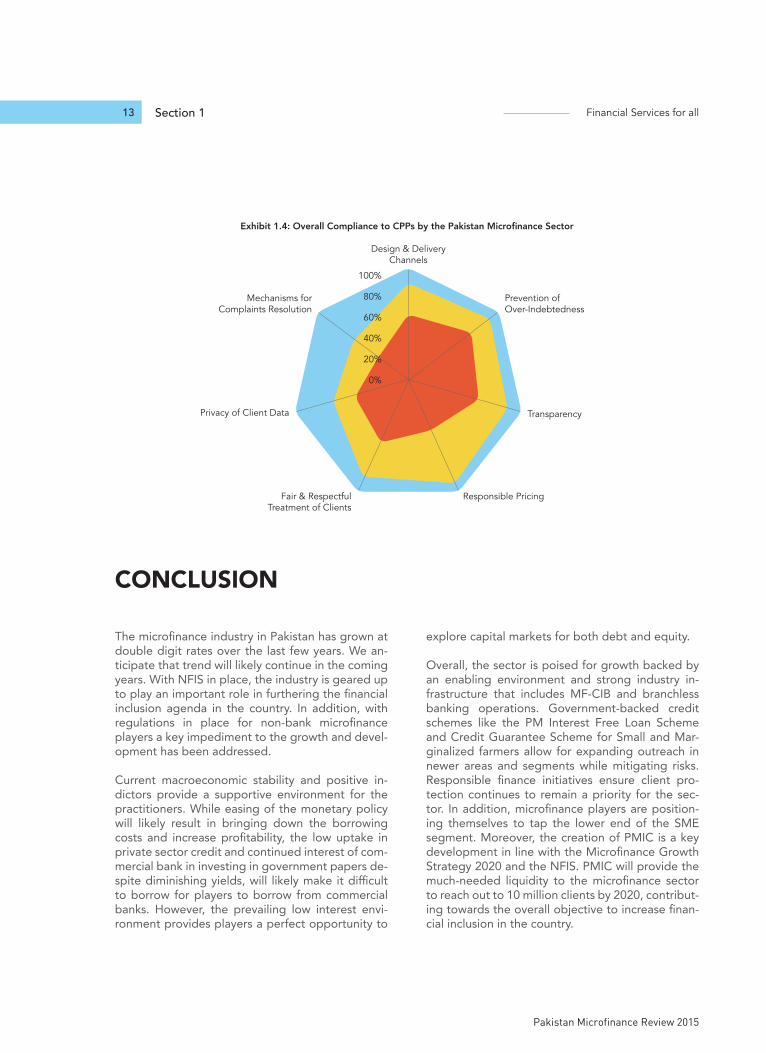

to improve practices. Although the wider dataset has shown somewhat better results for fair and re-spectful treatment of clients, there is still significant scope for improvement in practices pertaining to pricing transparency. Lastly, the results relating to the principles of privacy of client data and mech-anisms for complaints resolution reflect a distinct weakness in meeting minimum standards of prac-tice (Exhibit 1.4).

Despite an overall positive trend of client-centric processes, further work needs to be done in each CPP, and in some more than others, to bring the compliance levels at par with the global standards of client protection.

Section 1 Financial Services for all

Pakistan Microfinance Review 2015

13

The microfinance industry in Pakistan has grown at double digit rates over the last few years. We an-ticipate that trend will likely continue in the coming years. With NFIS in place, the industry is geared up to play an important role in furthering the financial inclusion agenda in the country. In addition, with regulations in place for non-bank microfinance players a key impediment to the growth and devel-opment has been addressed.

Current macroeconomic stability and positive in-dictors provide a supportive environment for the practitioners. While easing of the monetary policy will likely result in bringing down the borrowing costs and increase profitability, the low uptake in private sector credit and continued interest of com-mercial bank in investing in government papers de-spite diminishing yields, will likely make it difficult to borrow for players to borrow from commercial banks. However, the prevailing low interest envi-ronment provides players a perfect opportunity to

explore capital markets for both debt and equity.

Overall, the sector is poised for growth backed by an enabling environment and strong industry in-frastructure that includes MF-CIB and branchless banking operations. Government-backed credit schemes like the PM Interest Free Loan Scheme and Credit Guarantee Scheme for Small and Mar-ginalized farmers allow for expanding outreach in newer areas and segments while mitigating risks. Responsible finance initiatives ensure client pro-tection continues to remain a priority for the sec-tor. In addition, microfinance players are position-ing themselves to tap the lower end of the SME segment. Moreover, the creation of PMIC is a key development in line with the Microfinance Growth Strategy 2020 and the NFIS. PMIC will provide the much-needed liquidity to the microfinance sector to reach out to 10 million clients by 2020, contribut-ing towards the overall objective to increase finan-cial inclusion in the country.

CONCLUSION

PAK

ISTA

N M

ICR

OFI

NA

NC

E R

EV

IEW

201

5

Privacy of Client Data

Mechanisms forComplaints Resolution

0%

20%

40%

60%

80%

100%

Fair & RespectfulTreatment of Clients

Design & DeliveryChannels

Prevention ofOver-Indebtedness

Responsible Pricing

Transparency

Exhibit 1.4: Overall Compliance to CPPs by the Pakistan Microfinance Sector

Annual Assessment of the Microfinance Industry

Financial Services for all 14The Year in Review

PAK

ISTA

N M

ICR

OFI

NA

NC

E R

EV

IEW

201

5

Section 1 Financial Services for all

Pakistan Microfinance Review 2015

15

Annual Assessment of the Microfinance Industry

Financial Services for all 16Financial Performance Review

SECTION 2

FINANCIAL PERFORMANCE REVIEW

Section 2 Financial Services for all

Pakistan Microfinance Review 2015

17

This section provides a detailed analysis of the fi-nancial performance of Pakistan’s microfinance in-dustry in 2015. Performance has been assessed on three levels: industry wise, across peer groups and institution wise. The analysis is backed by 88 finan-cial indicators, calculated from the audited financial statements of the reporting organizations. These

indicators have been compared across time and regions to develop a reliable and fair assessment of sector.

Detailed financial information is provided in the An-nex A-I and A-II of the PMR. Aggregate data has been reproduced for five years, whereas, the peer

FINANCIAL PERFORMANCE REVIEW

BOX 2.1PEER GROUPS

Microfinance InstitutionA non-bank non-government organization (NGO) providing microfinance services. Organizations in this group are registered under a variety of regulations, including the Societies Act, Trust Act, and the Companies Ordinance. The MFI peer group includes local as well as multinational NGOs such as BRAC-Pakistan and ASA-Pakistan. As of now these organizations are in process of transformation into Non-Bank MFIs under the new regulatory frame-work laid out for non-bank players by SECP.

Microfinance BankA commercial bank licensed and prudentially regulated by the SBP to exclusively service the microfinance market. The first MFB was established in 2000 under a presidential decree. Since then, 11 MFBs have been licensed under the Microfinance Institutions Ordinance, 2001. MFBs are legally empowered to accept and intermediate deposits from the public. Currently there are 11 MFBs operating in the country.

Rural Support ProgrammeAn NGO registered as a non-profit company under the Companies Ordinance. An RSP is differentiated from the MFI peer group based on the purely rural focus of its credit operations. As of now these organizations are in process of transformation into Non-Bank MFI under the new regulatory framework laid out for non-bank players by SECP.

Annual Assessment of the Microfinance Industry

Financial Services for all 18Financial Performance Review

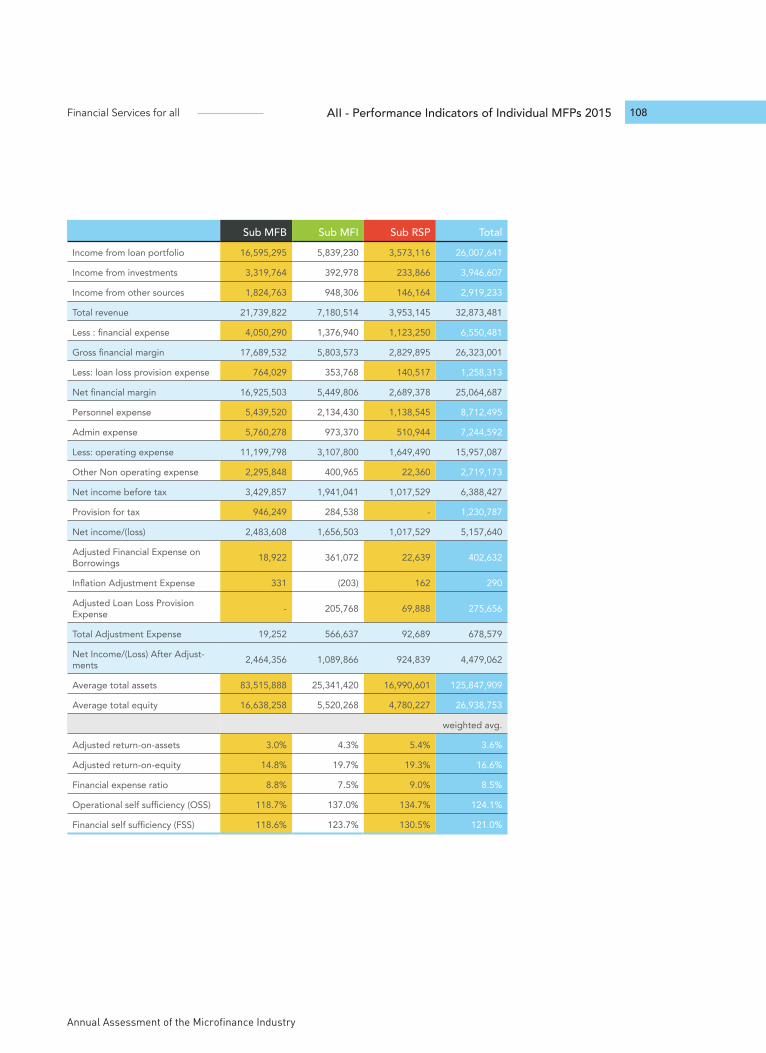

group and institution specific data has been made available only for the year 2015.

A total of 44 MFPs submitted their audited finan-cial statements for PMR 2015. During the period, three new respondents provided their dataset for the first time. For a complete list of reporting orga-nizations refer to Annex B.

Industry players are categorized into three groups for benchmarking and comparison purposes: Mi-

crofinance Banks (MFBs), Microfinance Institutions (MFIs) and Rural Support Programmes (RSPs). See Box 2.1 for detailed definitions.

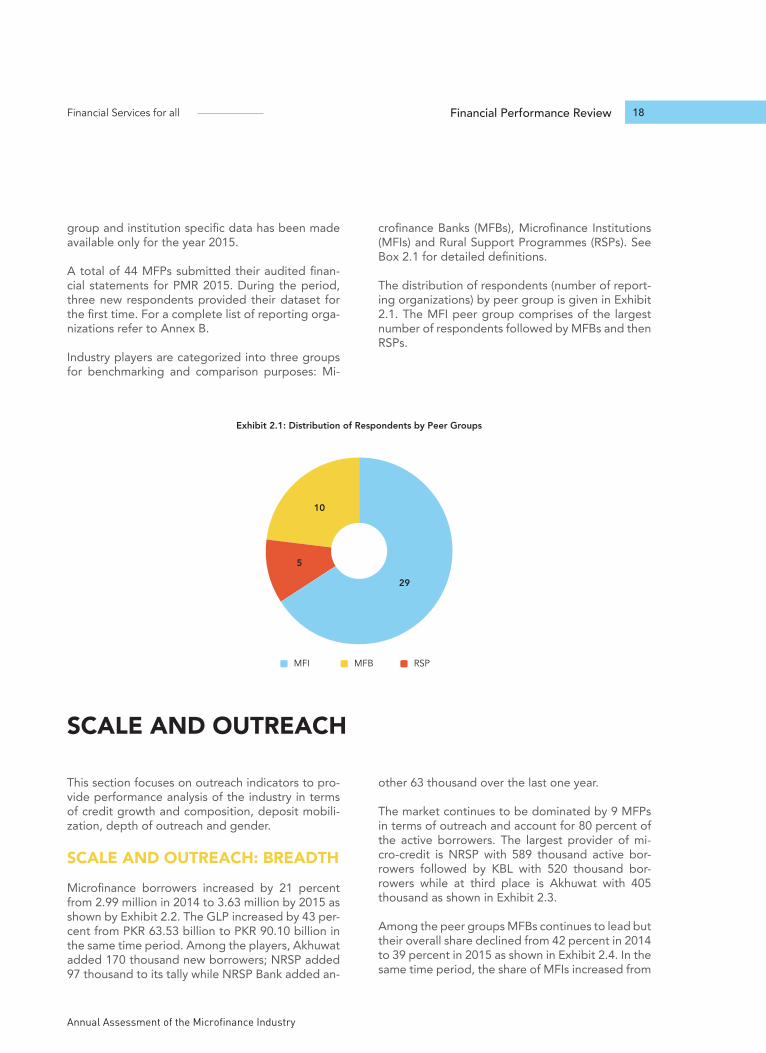

The distribution of respondents (number of report-ing organizations) by peer group is given in Exhibit 2.1. The MFI peer group comprises of the largest number of respondents followed by MFBs and then RSPs.

29

10

5

MFI RSPMFB

Exhibit 2.1: Distribution of Respondents by Peer Groups

This section focuses on outreach indicators to pro-vide performance analysis of the industry in terms of credit growth and composition, deposit mobili-zation, depth of outreach and gender.

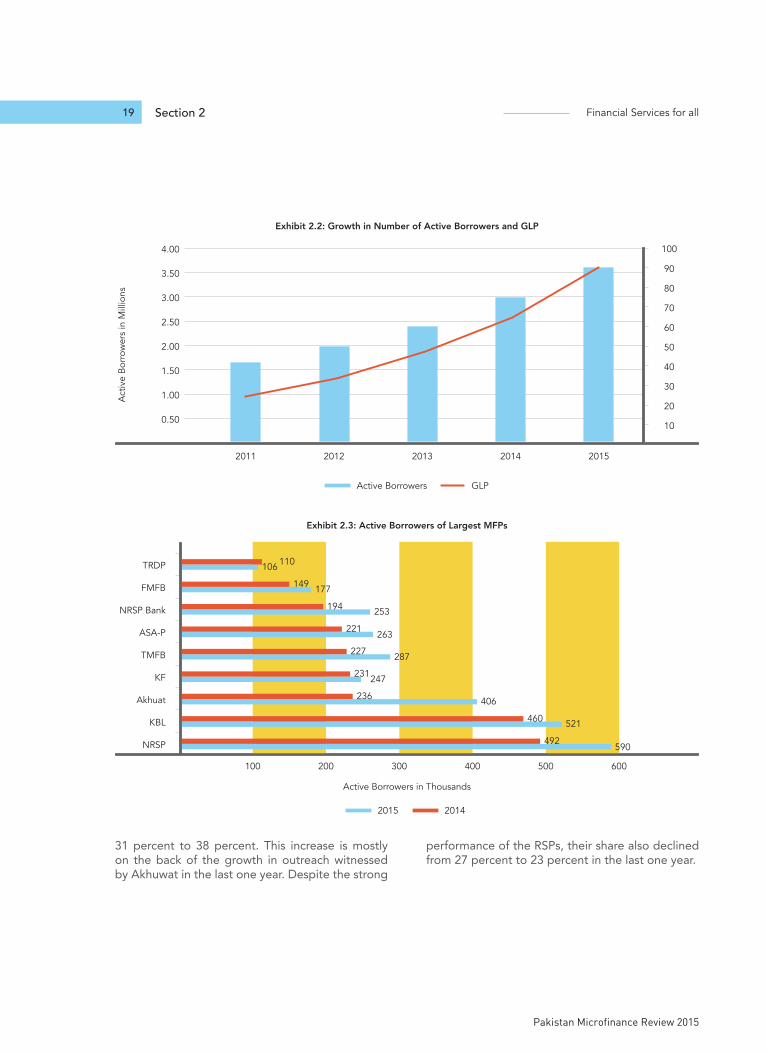

SCALE AND OUTREACH: BREADTH

Microfinance borrowers increased by 21 percent from 2.99 million in 2014 to 3.63 million by 2015 as shown by Exhibit 2.2. The GLP increased by 43 per-cent from PKR 63.53 billion to PKR 90.10 billion in the same time period. Among the players, Akhuwat added 170 thousand new borrowers; NRSP added 97 thousand to its tally while NRSP Bank added an-

other 63 thousand over the last one year.

The market continues to be dominated by 9 MFPs in terms of outreach and account for 80 percent of the active borrowers. The largest provider of mi-cro-credit is NRSP with 589 thousand active bor-rowers followed by KBL with 520 thousand bor-rowers while at third place is Akhuwat with 405 thousand as shown in Exhibit 2.3.

Among the peer groups MFBs continues to lead but their overall share declined from 42 percent in 2014 to 39 percent in 2015 as shown in Exhibit 2.4. In the same time period, the share of MFIs increased from

SCALE AND OUTREACH

Section 2 Financial Services for all

Pakistan Microfinance Review 2015

19

31 percent to 38 percent. This increase is mostly on the back of the growth in outreach witnessed by Akhuwat in the last one year. Despite the strong

performance of the RSPs, their share also declined from 27 percent to 23 percent in the last one year.

Exhibit 2.2: Growth in Number of Active Borrowers and GLP

0.50

1.00

1.50

2.00

2.50

3.00

3.50

4.00

Act

ive

Bor

row

ers

in M

illio

ns

2011 2012 2013 2014 2015

10

20

30

40

50

60

70

80

90

100

GLPActive Borrowers

NRSP

100 200 300 400 500 600

KBL

Akhuat

KF

TMFB

ASA-P

NRSP Bank

FMFB

TRDP

20142015

590492

521460

406236

247231

287227

263221

253194

177149

106 110

Active Borrowers in Thousands

Exhibit 2.3: Active Borrowers of Largest MFPs

Annual Assessment of the Microfinance Industry

Financial Services for all 20Financial Performance Review

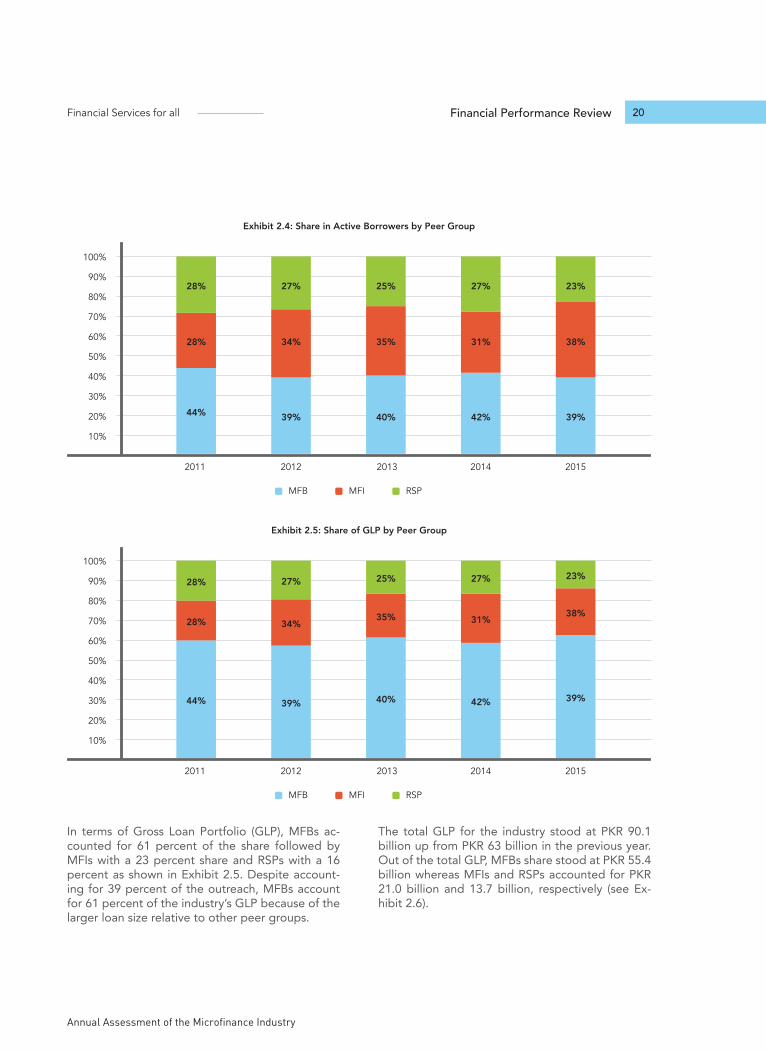

In terms of Gross Loan Portfolio (GLP), MFBs ac-counted for 61 percent of the share followed by MFIs with a 23 percent share and RSPs with a 16 percent as shown in Exhibit 2.5. Despite account-ing for 39 percent of the outreach, MFBs account for 61 percent of the industry’s GLP because of the larger loan size relative to other peer groups.

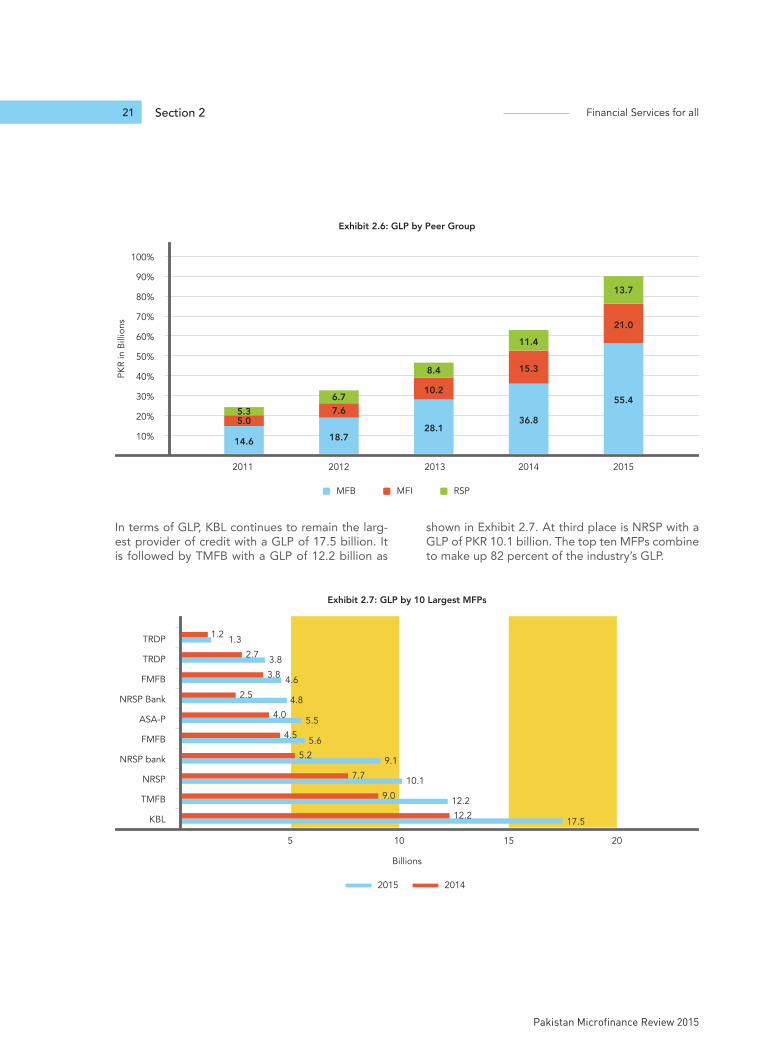

The total GLP for the industry stood at PKR 90.1 billion up from PKR 63 billion in the previous year. Out of the total GLP, MFBs share stood at PKR 55.4 billion whereas MFIs and RSPs accounted for PKR 21.0 billion and 13.7 billion, respectively (see Ex-hibit 2.6).

Exhibit 2.4: Share in Active Borrowers by Peer Group

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2011

44%

28%

28%

2012

39%

34%

27%

2013

40%

35%

25%

2014

42%

31%

27%

2015

39%

38%

23%

MFB RSPMFI

Exhibit 2.5: Share of GLP by Peer Group

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2011

44%

28%

28%

2012

39%

34%

27%

2013

40%

35%

25%

2014

42%

31%

27%

2015

39%

38%

23%

MFB RSPMFI

Section 2 Financial Services for all

Pakistan Microfinance Review 2015

21

Exhibit 2.6: GLP by Peer Group

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2011

14.6

5.05.3

2012

18.7

7.66.7

2013

28.1

10.2

8.4

2014

36.8

15.3

11.4

2015

55.4

21.0

13.7

MFB RSPMFI

PKR

in B

illio

ns

In terms of GLP, KBL continues to remain the larg-est provider of credit with a GLP of 17.5 billion. It is followed by TMFB with a GLP of 12.2 billion as

shown in Exhibit 2.7. At third place is NRSP with a GLP of PKR 10.1 billion. The top ten MFPs combine to make up 82 percent of the industry’s GLP.

KBL

5 1510 20

TMFB

NRSP

NRSP bank

FMFB

ASA-P

NRSP Bank

FMFB

TRDP

TRDP

20142015

17.512.2

12.29.0

10.17.7

9.15.2

5.64.5

5.54.0

4.82.5

4.63.8

3.82.7

1.31.2

Billions

Exhibit 2.7: GLP by 10 Largest MFPs

Annual Assessment of the Microfinance Industry

Financial Services for all 22Financial Performance Review

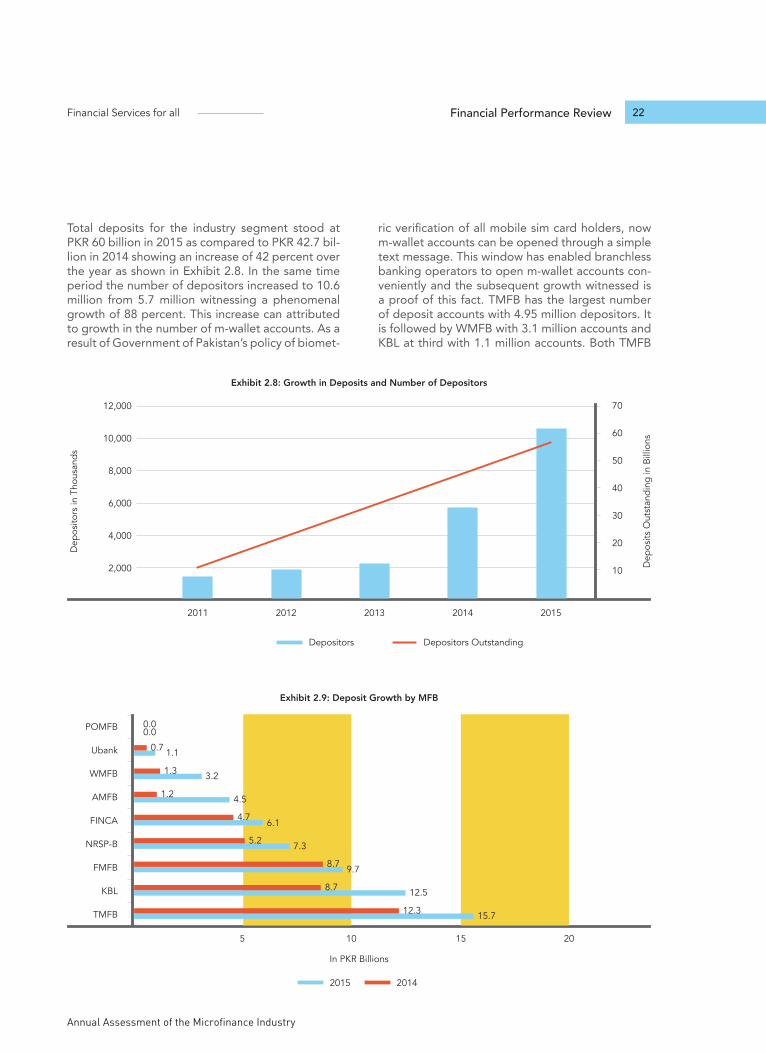

Total deposits for the industry segment stood at PKR 60 billion in 2015 as compared to PKR 42.7 bil-lion in 2014 showing an increase of 42 percent over the year as shown in Exhibit 2.8. In the same time period the number of depositors increased to 10.6 million from 5.7 million witnessing a phenomenal growth of 88 percent. This increase can attributed to growth in the number of m-wallet accounts. As a result of Government of Pakistan’s policy of biomet-

ric verification of all mobile sim card holders, now m-wallet accounts can be opened through a simple text message. This window has enabled branchless banking operators to open m-wallet accounts con-veniently and the subsequent growth witnessed is a proof of this fact. TMFB has the largest number of deposit accounts with 4.95 million depositors. It is followed by WMFB with 3.1 million accounts and KBL at third with 1.1 million accounts. Both TMFB

Exhibit 2.8: Growth in Deposits and Number of Depositors

2,000

4,000

6,000

8,000

10,000

12,000

Dep

osito

rs in

Tho

usan

ds

Dep

osits

Out

stan

ding

in B

illio

ns

2011 2012 2013 2014 2015

10

20

30

40

50

60

70

Depositors OutstandingDepositors

5 1510 20

TMFB

KBL

FMFB

NRSP-B

FINCA

AMFB

WMFB

Ubank

POMFB

20142015

15.712.3

12.58.7

9.78.7

7.35.2

6.14.7

4.51.2

3.21.3

1.10.7

0.00.0

In PKR Billions

Exhibit 2.9: Deposit Growth by MFB

Section 2 Financial Services for all

Pakistan Microfinance Review 2015

23

and WMFB have been allowed to open m-wallet accounts using USSD string and bulk of the deposit accounts are m-wallet accounts.

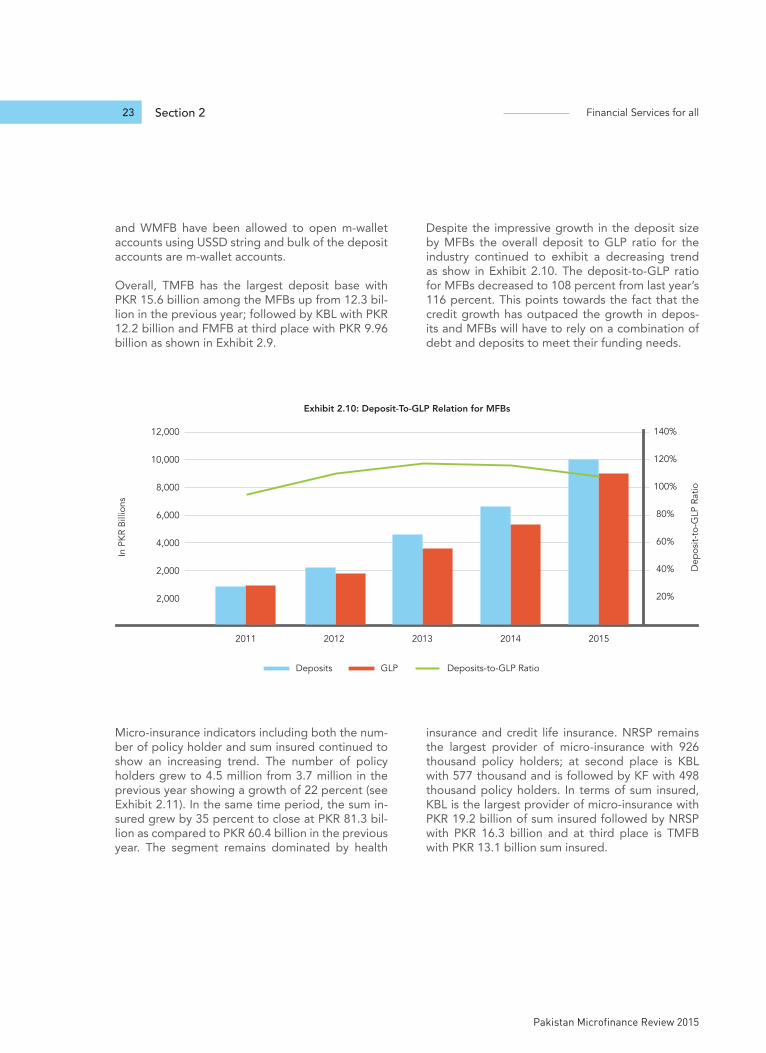

Overall, TMFB has the largest deposit base with PKR 15.6 billion among the MFBs up from 12.3 bil-lion in the previous year; followed by KBL with PKR 12.2 billion and FMFB at third place with PKR 9.96 billion as shown in Exhibit 2.9.

Despite the impressive growth in the deposit size by MFBs the overall deposit to GLP ratio for the industry continued to exhibit a decreasing trend as show in Exhibit 2.10. The deposit-to-GLP ratio for MFBs decreased to 108 percent from last year’s 116 percent. This points towards the fact that the credit growth has outpaced the growth in depos-its and MFBs will have to rely on a combination of debt and deposits to meet their funding needs.

Micro-insurance indicators including both the num-ber of policy holder and sum insured continued to show an increasing trend. The number of policy holders grew to 4.5 million from 3.7 million in the previous year showing a growth of 22 percent (see Exhibit 2.11). In the same time period, the sum in-sured grew by 35 percent to close at PKR 81.3 bil-lion as compared to PKR 60.4 billion in the previous year. The segment remains dominated by health

insurance and credit life insurance. NRSP remains the largest provider of micro-insurance with 926 thousand policy holders; at second place is KBL with 577 thousand and is followed by KF with 498 thousand policy holders. In terms of sum insured, KBL is the largest provider of micro-insurance with PKR 19.2 billion of sum insured followed by NRSP with PKR 16.3 billion and at third place is TMFB with PKR 13.1 billion sum insured.

Exhibit 2.10: Deposit-To-GLP Relation for MFBs

2,000

2,000

4,000

6,000

8,000

10,000

12,000

In P

KR

Bill

ions

Dep

osit-

to-G

LP R

atio

2011 2012 2013 2014 2015

20%

40%

60%

80%

100%

120%

140%

GLP Deposits-to-GLP RatioDeposits

Annual Assessment of the Microfinance Industry

Financial Services for all 24Financial Performance Review

Exhibit 2.11: Growth in Number of Policy Holders & Sum Insured

2.70

1.70

2.20

1.20

3.20

3.70

4.20

4.70

5.20

Polic

y H

olde

rs in

Mill

ions

Sum

Insu

red

in P

KR

Bill

ions

2011 2012 2013 2014 2015

30

20

10

40

50

60

70

80

90

Sum InsuredPolicy Holders

Exhibit 2.12: Depth of Outreach by Peer Groups

10%

5%

15%

20%

25%

30%

Ave

rage

Loa

n B

alan

ce P

er G

DP

per C

apita

2011 2012 2013 2014 2015

Cut-off MFI MFBIndustry RSP

SCALE AND OUTREACH: DEPTH

The depth of outreach in microcredit operations is measured by a proxy indicator: average loan bal-ance per borrower in proportion to per capita Gross National Income (GNI). A value below 20 percent is assumed to mean that the MFP is poverty focused.

Comparison across peer groups shows that the ra-tio of average loan balance to per capita GNI for MFBs has been on the rise for the past three years (see Exhibit 2.12). MFBs tend to target the upper end of the market through relatively larger loan siz-es, and hence have a ratio of 25 percent compared to MFIs and RSPs which have a ratio of 10 percent and 11 percent, respectively.

Section 2 Financial Services for all

Pakistan Microfinance Review 2015

25

Here it must be kept in mind that low account size does not guarantee a lower income clientele nor does a higher loan size means that the MFPs are moving out of their target markets. Since, many of the MFPs use a graduation model of loan sizes, over time first time borrowers decline resulting in increasing of loan sizes. This situation holds true for MFPs in Pakistan which have large numbers of re-turning clients among its active borrowers. This is particularly true for MFBs who are upscaling loan sizes to cater to funding needs of micro-enterpris-es. Another reason can be the realization among practitioners that the loan sizes are unnecessarily conservative and increasing loan sizes is not related to catering for lower income segments. This is also

true for players in Pakistan as a number of them have lately recalibrated their loan sizes to keep up with the requirements of their clients and inflation.

Lending Methodology

Overall, group lending methodology continues to dominate the industry; however, individual lending is gaining popularity. This is evident from the in-crease in the share of individual borrowing which increased from 24 percent in 2014 to 27 percent in

2015. For higher loan sizes, players have shown a clear inclination towards individual lending. Among the peer groups, MFBs have shown a preference towards individual lending as compared to group lending. Moreover, for larger loan sizes players have shown a clear bias towards individual lending.

Gender Distribution

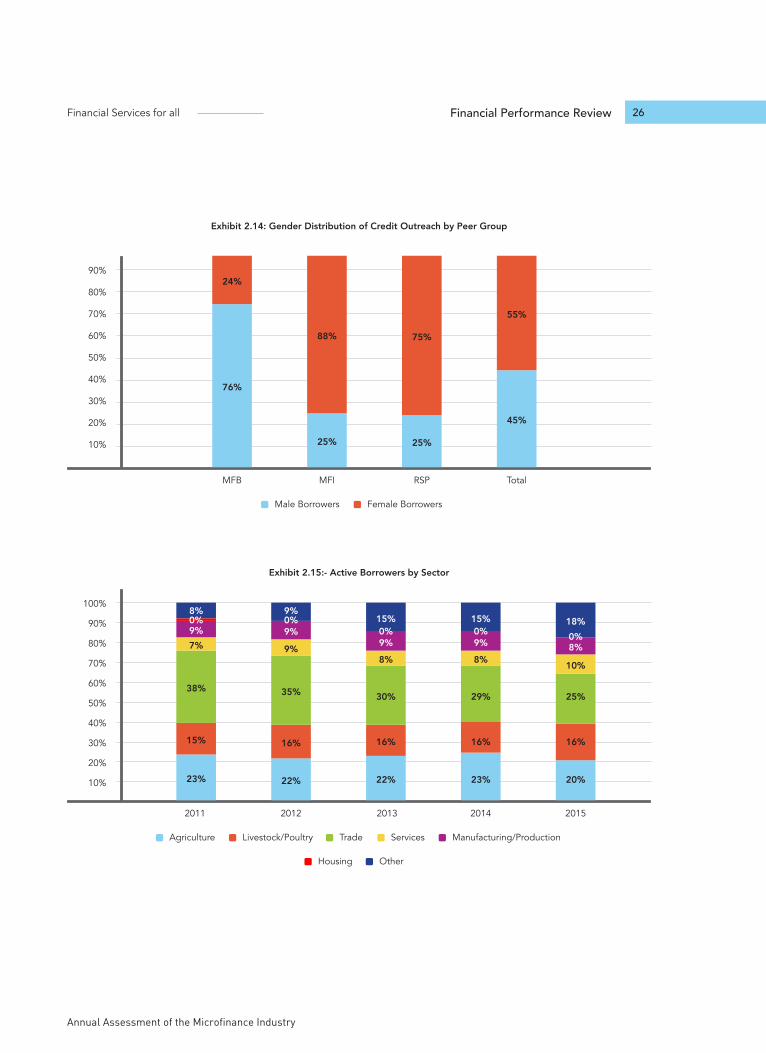

Women borrowers continue to account for the majority of microfinance borrowers in the coun-try. Nearly 55 percent of the active borrowers are women as compared to 58 percent in 2014. The situation varies among the three peer groups with 75 percent of borrowers of the RSPs and MFIs are

women whereas only 24 percent of borrowers of MFBs are women as shown in Exhibit 2.14.

Portfolio Distribution by Sector

Credit portfolio distribution by sector exhibited lit-tle change over the last one year. Agriculture and livestock continued to account for the majority of the borrowers with 39 percent share, followed by service and trade making up 35 percent of the mar-ket share and manufacturing accounting for 8 per-cent of the industry’s borrowers.

Exhibit 2.13: Lending Methodology Trend

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

2011

10%

90%

2012

12%

88%

2013

22%

78%

2014

24%

76%

2015

27%

73%

Group Borrowing Individual Borrowing

Act

ive

Bor

row

ers

In T

hous

ands

21 Measuring Results of Microfinance Institutions, Richard Rosenberg, June 2009, CGAP22 Ibid

Annual Assessment of the Microfinance Industry

Financial Services for all 26Financial Performance Review

Exhibit 2.14: Gender Distribution of Credit Outreach by Peer Group

10%

20%

30%

40%

50%

60%

70%

90%

80%

MFB

76%

24%

MFI

25%

88%

RSP

25%

75%

Total

45%

55%

Male Borrowers Female Borrowers

Exhibit 2.15:- Active Borrowers by Sector

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2011

23%

38%

15%

9%0%8%

7%

2012 2013 2014 2015

Housing Other

Agriculture Trade Services Manufacturing/ProductionLivestock/Poultry

22%

35%

16%

9%

9%

9%

0%

22%

30%

16%

9%

15%

8%

0%

23%

29%

16%

9%

15%

8%

0%

20%

25%

16%

8%

18%

10%

0%

Section 2 Financial Services for all

Pakistan Microfinance Review 2015

27

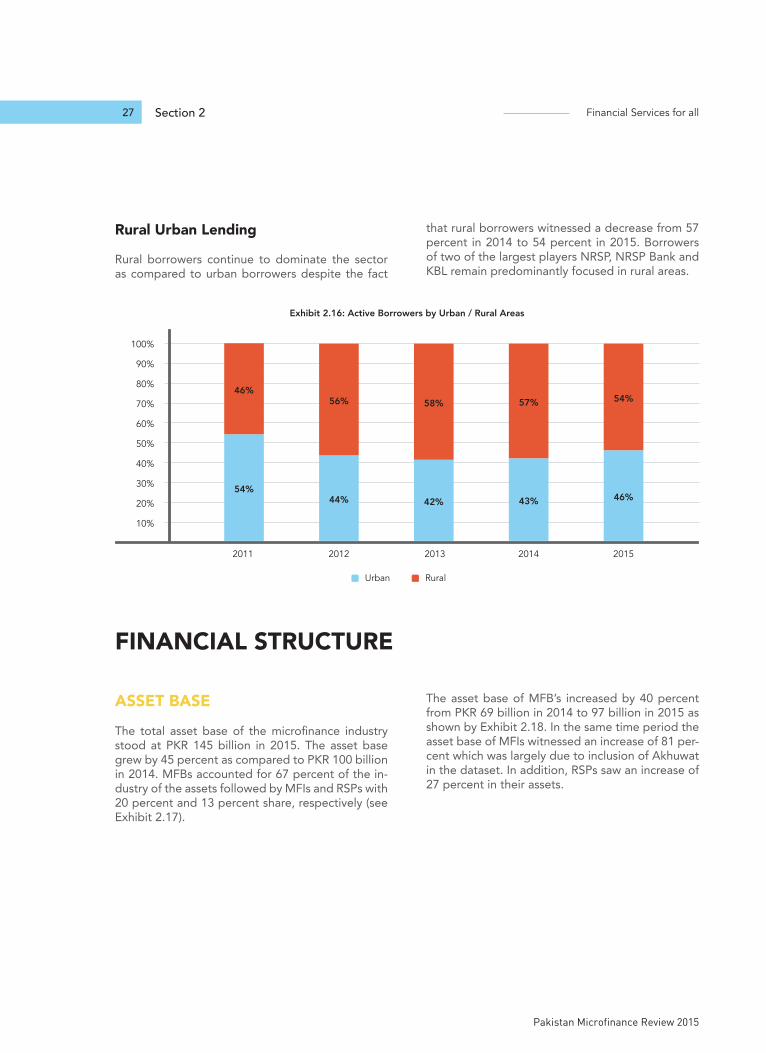

Rural Urban Lending

Rural borrowers continue to dominate the sector as compared to urban borrowers despite the fact

that rural borrowers witnessed a decrease from 57 percent in 2014 to 54 percent in 2015. Borrowers of two of the largest players NRSP, NRSP Bank and KBL remain predominantly focused in rural areas.

Exhibit 2.16: Active Borrowers by Urban / Rural Areas

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2011

54%

46%

2012

44%

56%

2013

42%

58%

2014

43%

57%

2015

46%

54%

Urban Rural

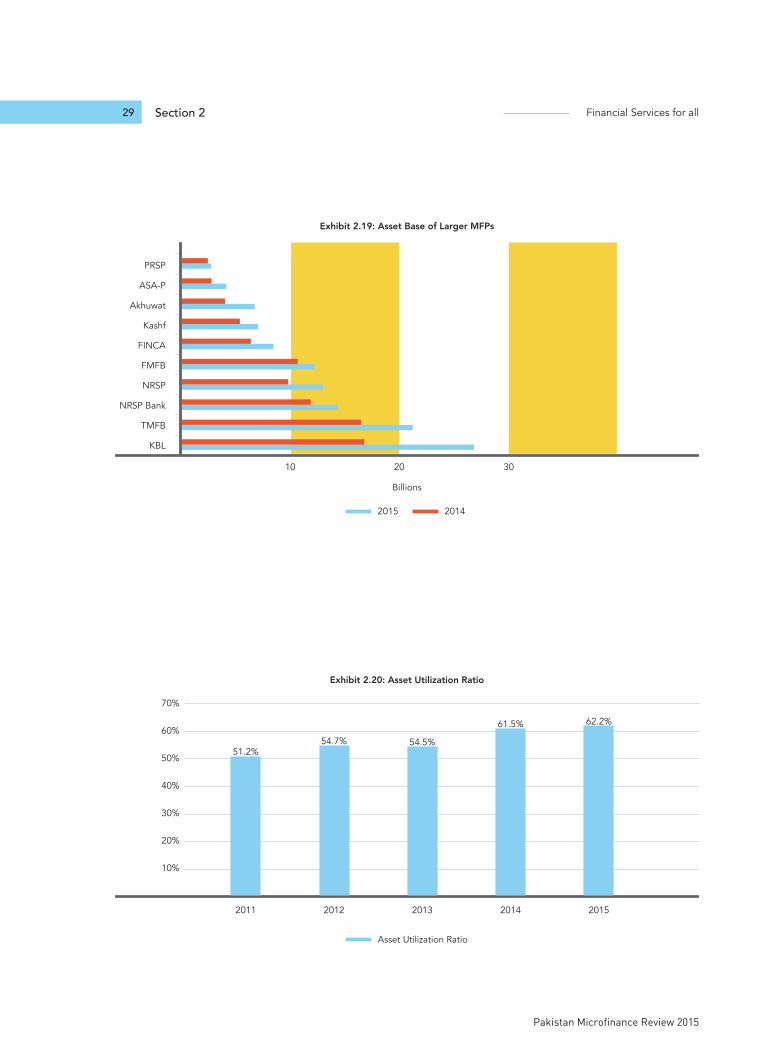

ASSET BASE

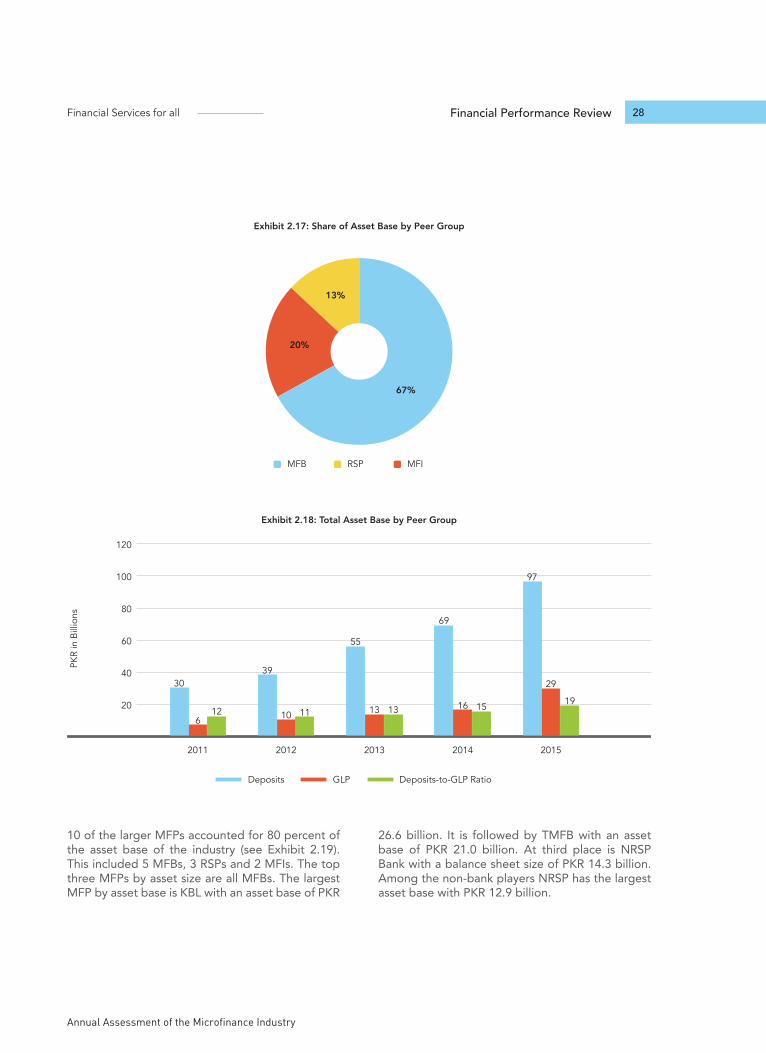

The total asset base of the microfinance industry stood at PKR 145 billion in 2015. The asset base grew by 45 percent as compared to PKR 100 billion in 2014. MFBs accounted for 67 percent of the in-dustry of the assets followed by MFIs and RSPs with 20 percent and 13 percent share, respectively (see Exhibit 2.17).

The asset base of MFB’s increased by 40 percent from PKR 69 billion in 2014 to 97 billion in 2015 as shown by Exhibit 2.18. In the same time period the asset base of MFIs witnessed an increase of 81 per-cent which was largely due to inclusion of Akhuwat in the dataset. In addition, RSPs saw an increase of 27 percent in their assets.

FINANCIAL STRUCTURE

Annual Assessment of the Microfinance Industry

Financial Services for all 28Financial Performance Review

10 of the larger MFPs accounted for 80 percent of the asset base of the industry (see Exhibit 2.19). This included 5 MFBs, 3 RSPs and 2 MFIs. The top three MFPs by asset size are all MFBs. The largest MFP by asset base is KBL with an asset base of PKR

26.6 billion. It is followed by TMFB with an asset base of PKR 21.0 billion. At third place is NRSP Bank with a balance sheet size of PKR 14.3 billion. Among the non-bank players NRSP has the largest asset base with PKR 12.9 billion.

67%

13%

20%

MFB MFIRSP

Exhibit 2.17: Share of Asset Base by Peer Group

Exhibit 2.18: Total Asset Base by Peer Group

20

40

60

80

100

120

PKR

in B

illio

ns

2011 2012 2013 2014 2015

GLP Deposits-to-GLP RatioDeposits

39

10 11

55

13 13

97

29

19

69

16 15

30

612

Section 2 Financial Services for all

Pakistan Microfinance Review 2015

29

KBL

10 3020

TMFB

NRSP Bank

NRSP

FMFB

FINCA

Kashf

Akhuwat

ASA-P

PRSP

20142015

Billions

Exhibit 2.19: Asset Base of Larger MFPs

Exhibit 2.20: Asset Utilization Ratio

20%

10%

51.2%54.7% 54.5%

61.5% 62.2%

30%

40%

50%

60%

70%

2011 2012 2013 2014 2015

Asset Utilization Ratio

Annual Assessment of the Microfinance Industry

Financial Services for all 30Financial Performance Review

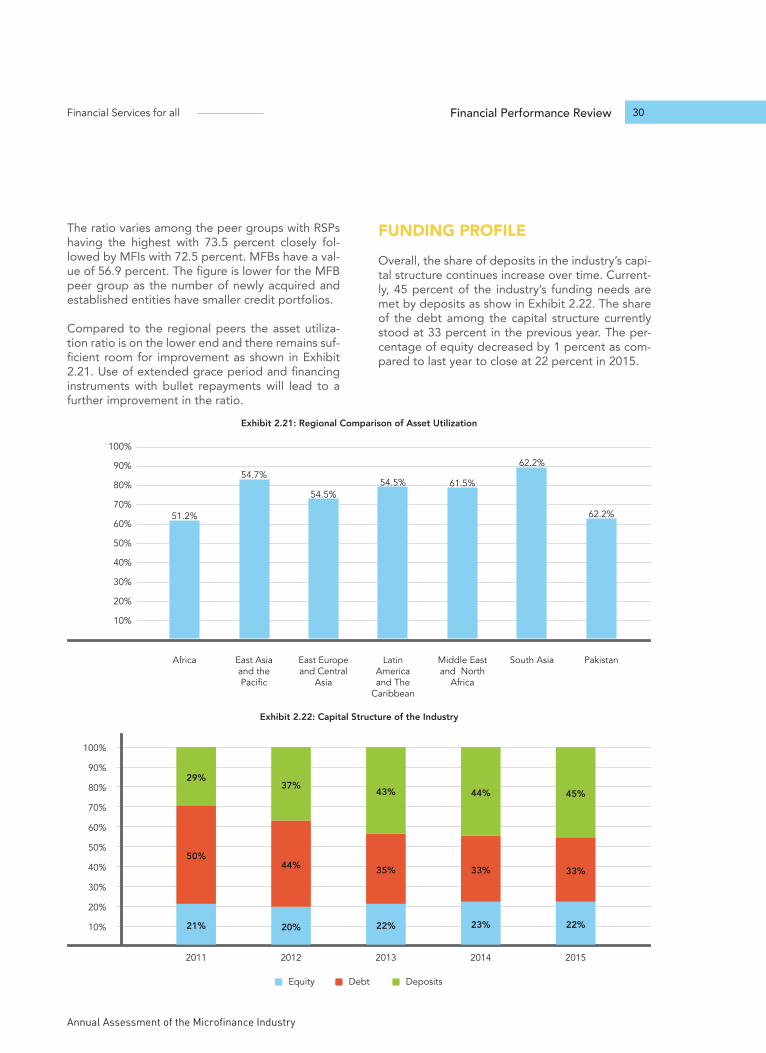

The ratio varies among the peer groups with RSPs having the highest with 73.5 percent closely fol-lowed by MFIs with 72.5 percent. MFBs have a val-ue of 56.9 percent. The figure is lower for the MFB peer group as the number of newly acquired and established entities have smaller credit portfolios.

Compared to the regional peers the asset utiliza-tion ratio is on the lower end and there remains suf-ficient room for improvement as shown in Exhibit 2.21. Use of extended grace period and financing instruments with bullet repayments will lead to a further improvement in the ratio.

FUNDING PROFILE

Overall, the share of deposits in the industry’s capi-tal structure continues increase over time. Current-ly, 45 percent of the industry’s funding needs are met by deposits as show in Exhibit 2.22. The share of the debt among the capital structure currently stood at 33 percent in the previous year. The per-centage of equity decreased by 1 percent as com-pared to last year to close at 22 percent in 2015.

Exhibit 2.21: Regional Comparison of Asset Utilization

50%

40%

30%

20%

10%

60%

70%

80%

90%

100%

Africa East Asia and the Pacific

East Europe and Central

Asia

Latin America and The

Caribbean

Middle East and North

Africa

South Asia Pakistan

51.2%

54.7%

54.5%54.5% 61.5%

62.2%

62.2%

Exhibit 2.22: Capital Structure of the Industry

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2011

21%

50%

29%

2012

20%

44%

37%

2013

22%

35%

43%

2014

23%

33%

44%

2015

22%

33%

45%

Equity DepositsDebt

Section 2 Financial Services for all

Pakistan Microfinance Review 2015

31

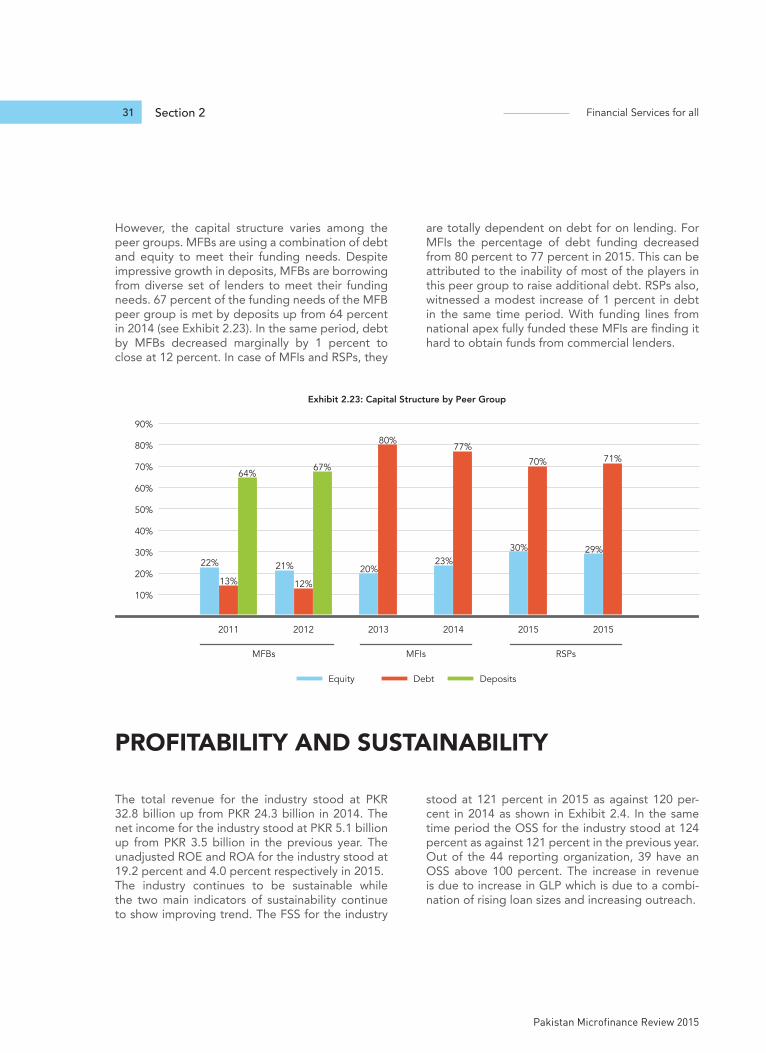

However, the capital structure varies among the peer groups. MFBs are using a combination of debt and equity to meet their funding needs. Despite impressive growth in deposits, MFBs are borrowing from diverse set of lenders to meet their funding needs. 67 percent of the funding needs of the MFB peer group is met by deposits up from 64 percent in 2014 (see Exhibit 2.23). In the same period, debt by MFBs decreased marginally by 1 percent to close at 12 percent. In case of MFIs and RSPs, they

are totally dependent on debt for on lending. For MFIs the percentage of debt funding decreased from 80 percent to 77 percent in 2015. This can be attributed to the inability of most of the players in this peer group to raise additional debt. RSPs also, witnessed a modest increase of 1 percent in debt in the same time period. With funding lines from national apex fully funded these MFIs are finding it hard to obtain funds from commercial lenders.

Exhibit 2.23: Capital Structure by Peer Group

10%

20%

30%

40%

50%

60%

70%

MFBs MFIs RSPs

80%

90%

2011 2012 2013 2014 2015 2015

Debt DepositsEquity

21%

12%

67%

20%

80%

30%

70%

29%

71%

23%

77%

22%

13%

64%

The total revenue for the industry stood at PKR 32.8 billion up from PKR 24.3 billion in 2014. The net income for the industry stood at PKR 5.1 billion up from PKR 3.5 billion in the previous year. The unadjusted ROE and ROA for the industry stood at 19.2 percent and 4.0 percent respectively in 2015. The industry continues to be sustainable while the two main indicators of sustainability continue to show improving trend. The FSS for the industry

stood at 121 percent in 2015 as against 120 per-cent in 2014 as shown in Exhibit 2.4. In the same time period the OSS for the industry stood at 124 percent as against 121 percent in the previous year. Out of the 44 reporting organization, 39 have an OSS above 100 percent. The increase in revenue is due to increase in GLP which is due to a combi-nation of rising loan sizes and increasing outreach.

PROFITABILITY AND SUSTAINABILITY

Annual Assessment of the Microfinance Industry

Financial Services for all 32Financial Performance Review

The year saw a decline in the total revenue ratio for the industry which fell from 29 percent in 2014 to 26 percent in 2015 (see Exhibit 2.25). This can be partially attributed to the decrease in the yield of gross portfolio which fell from 36 percent to 35 percent in the same time period.

Despite the decrease in the yield on loan portfo-lio, it remains on a higher end when compared to regional peers as shown in Exhibit 2.26. As the in-dustry matures and reaches scale the yield will de-crease further. Moreover, rising loan sizes will also play a crucial role in decreasing operating costs leading to decrease in the yield.

Exhibit 2.24: OSS and FSS Trend

60%

40%

20%

80%

100%

120%

140%

2011 2012 2013 2014 2015

Operational Self Sufficiency (OSS)Financial Self Sufficiency (FSS)

Exhibit 2.25: Total Revenue Ratio & Yield on Portfolio

20%

15%

5%

10%

25%

30%

35%

40%

2011 2012 2013 2014 2015

Yeild on Gross Portfolio (Nominal) Yeild on Gross Portfolio (Real)Total Revenue Ratio

Section 2 Financial Services for all

Pakistan Microfinance Review 2015

33

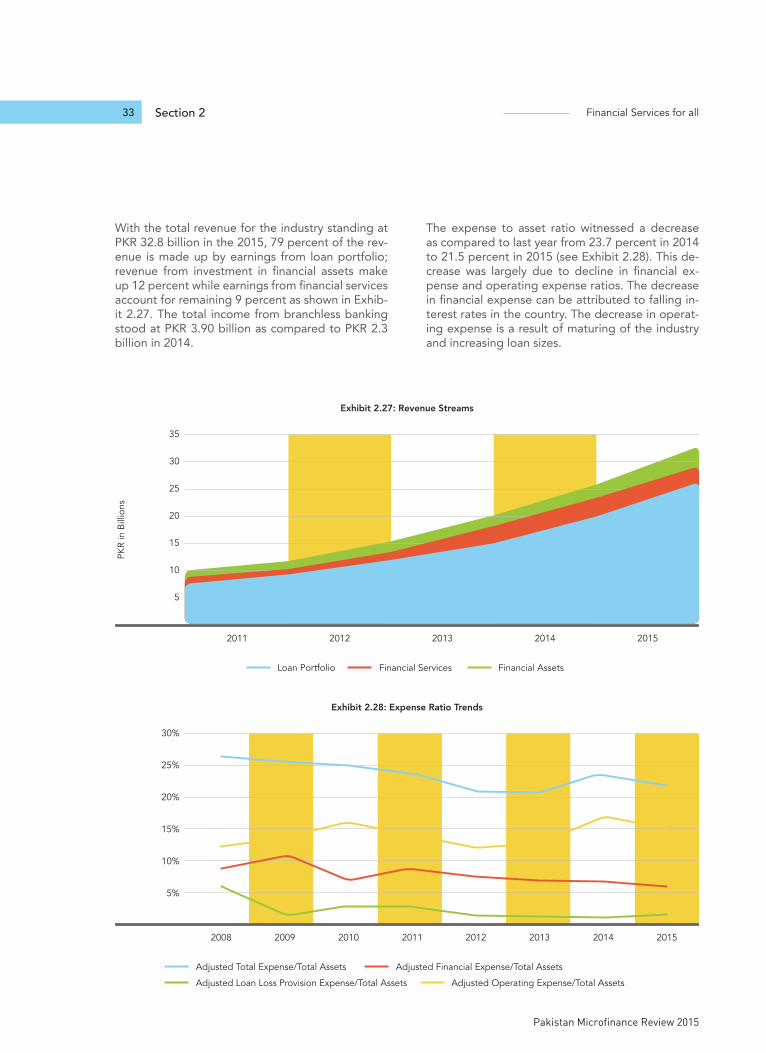

With the total revenue for the industry standing at PKR 32.8 billion in the 2015, 79 percent of the rev-enue is made up by earnings from loan portfolio; revenue from investment in financial assets make up 12 percent while earnings from financial services account for remaining 9 percent as shown in Exhib-it 2.27. The total income from branchless banking stood at PKR 3.90 billion as compared to PKR 2.3 billion in 2014.

The expense to asset ratio witnessed a decrease as compared to last year from 23.7 percent in 2014 to 21.5 percent in 2015 (see Exhibit 2.28). This de-crease was largely due to decline in financial ex-pense and operating expense ratios. The decrease in financial expense can be attributed to falling in-terest rates in the country. The decrease in operat-ing expense is a result of maturing of the industry and increasing loan sizes.

Exhibit 2.27: Revenue Streams

15

10

5

20

25

30

35

2011 2012 2013 2014 2015

Financial Services Financial AssetsLoan Portfolio

PKR

in B

illio

ns

Exhibit 2.28: Expense Ratio Trends

10%

5%

15%

20%

25%

30%

2008 20102009 2011 20132012 20152014

Adjusted Financial Expense/Total Assets

Adjusted Loan Loss Provision Expense/Total Assets Adjusted Operating Expense/Total Assets

Adjusted Total Expense/Total Assets

Annual Assessment of the Microfinance Industry

Financial Services for all 34Financial Performance Review

Operating expense to GLP ratio continued to ex-hibit a declining trend after witnessing a small in-crease last year. The ratio declined to 21.7 percent from 22.8 percent in 2014 (see Exhibit 2.29). The decrease was on the back of declining administra-tive and personnel expense. Increasing loan sizes especially as the sector expands credit operations to cover microenterprises this ratio will witness fur-

ther decline in coming years.

In comparison to regional peers, the unadjusted operating expense/asset for Pakistan lies close to the average (see Exhibit 2:30). However, it is on the higher end as compared to South Asia. There is a need for players to make concentrated efforts to work on reducing costs and improving efficiency.

Exhibit 2.29: Operating Expense to GLP Trend

20%

15%

5%

10%

25%

30%

2010 2011 2012 2013 2014 2015

Admin Expense/Gross Loan Portfolio

Operating Expense/Gross Loan Portfolio Personnel Expense/Gross Loan Portfolio