An overview of the key success factors for automotive OEMs entering the Iranian market

Munich, March 2016

Iran – A historic opportunity for automotive OEMs

2 Roland Berger_Iran_A historical opportunity_Final.pptx

Your Iran experts at Roland Berger

Philipp Grosse Kleimann

Senior Partner Munich

+49 89 9230 8718 [email protected]

Alexander Brenner

Principal Hamburg

+49 40 37631 4318 [email protected]

Santiago Castillo

Principal Dubai

+971 4446 4080 [email protected]

3 Roland Berger_Iran_A historical opportunity_Final.pptx

Contents Page

A. Iran – Status quo 5

B. Why enter the Iranian market – 6 opportunities for growth 11

C. How to enter the Iranian market – 9 key success factors 20

D. What to do now – Next steps 31

4 Roland Berger_Iran_A historical opportunity_Final.pptx

Management summary

Source: Roland Berger

A

Iran – Status quo

> Iran is the 18th largest economy globally with a positive trade balance and strong focus on oil products and car manufacturing

> IAEA confirmed that Iran met the relevant requirements under the JCPOA and all nuclear sanctions were lifted on January 16, 2016

B Why enter the Iranian market – 6 opportunities for growth

> Lifting of major sanctions provides a historical opportunity for foreign automakers to re-enter the attractive Iranian automotive market – 6 opportunities for growth

C How to enter the Iranian market – 9 key success factors

> OEMs need to thoroughly understand the national specifics before entering the Iranian market – 9 key success factors identified

D

What to do now – Next steps

> Think: Thoroughly understand the Iranian market and analyze the existing dealership network

> Act: Decide on whether to take a greenfield approach or to partner with a local dealership network and define for each model a CBU vs. SKD/CKD strategy

5 Roland Berger_Iran_A historical opportunity_Final.pptx

A. Iran – Status quo

6 Roland Berger_Iran_A historical opportunity_Final.pptx

As populated as Germany, Iran is the world's oldest country, boasting a sophisticated education system and excellent growth potential

Source: Goldman Sachs; Boston Consulting Group; UN population division; World Bank; CIA World Factbook; Roland Berger

Key facts and figures

Iran is almost as populated as Germany > Iran ranks 19th in the world in terms of population, only 150,000 inhabitants short of Germany

in 18th place (July 2014). Also, Iran's population is relatively young with a median age of 28.3 in 2014 (Germany: 46.1)

Iran is the oldest country in the world today > Iran's history as a nation dates back to 3,200 BC, making it the oldest country

in the world today

> All of this has been entirely witnessed by Sarv-e-Abarkooh, the world's third oldest tree at over 4,000 years of age

Iran is one of the "Next-11" countries > Goldman Sachs identified Iran as one of the Next-11 countries offering the best growth

potential beyond BRIC nations. It is estimated that growth of the Next-11 countries will outperform Triad and BRIC markets in the coming years

Iran has 2nd largest university globally and more female than male students > The Islamic Azad University Tehran is the 2nd largest university in the world with 2 m

students. Iran also has the best educated population in the Middle East & North Africa

> In 2012, approximately 60% of enrolled university students were female

7 Roland Berger_Iran_A historical opportunity_Final.pptx

Iran is centrally located between the Caspian Sea and Indian Ocean – Major cities are Tehran, Mashhad and Isfahan

Source: Statistical Centre of Iran; Roland Berger

Geographical overview

Markazi

Hormozgan

Ilam Lorestan

Chahar Mahall/

Bakhtiari Khuzestan

Isfahan

Yazd

Kohgiluyeh/ Buyer Ahmad

Fars

Bushehr

Kerman

Sistan and Baluchestan

South Khorasan

Razavi Khorasan

North Khorasan Golestan

Semnan

Qom

Tehran

Mazandaran

Qazvin

Zanjan

Hamadan

Kermanshah

Kordestan

West Azarbaijan

Gilan

Ardebil

East Azarbaijan

Ahvaz

Isfahan

Shiraz

Mashad

Qom Tehran

Orumieh

Tabriz

Karaj

Kermanshah

1) Based on 2011 census data 2) Share of total population

Capital Tehran, Tehran province

Country size ['000 km²] 1,648.2

Top 10 cities

Tehran

Mashhad

Isfahan

Karaj

Tabriz

Shiraz

Ahvaz

Qom

Kermanshah

Orumieh

Inhabitants1) [m]

8.2

2.7

1.8

1.6

1.5

1.5

1.1

1.1

0.9

0.7

[%2)]

11%

4%

2%

2%

2%

2%

2%

1%

1%

1%

8 Roland Berger_Iran_A historical opportunity_Final.pptx

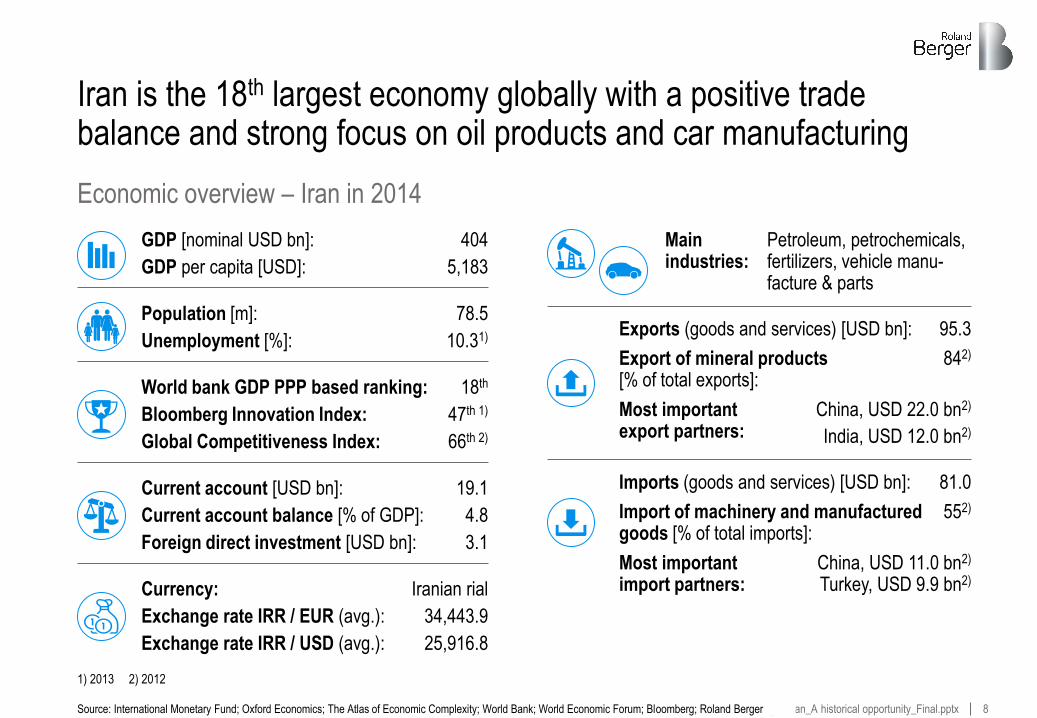

Iran is the 18th largest economy globally with a positive trade balance and strong focus on oil products and car manufacturing

Economic overview – Iran in 2014

1) 2013 2) 2012

Source: International Monetary Fund; Oxford Economics; The Atlas of Economic Complexity; World Bank; World Economic Forum; Bloomberg; Roland Berger

Current account [USD bn]: 19.1

Current account balance [% of GDP]: 4.8

Foreign direct investment [USD bn]: 3.1

Currency: Iranian rial

Exchange rate IRR / EUR (avg.): 34,443.9

Exchange rate IRR / USD (avg.): 25,916.8

GDP [nominal USD bn]: 404

GDP per capita [USD]: 5,183

Population [m]: 78.5

Unemployment [%]: 10.31)

Global Competitiveness Index: 66th 2)

Bloomberg Innovation Index: 47th 1)

World bank GDP PPP based ranking: 18th

Exports (goods and services) [USD bn]: 95.3

Export of mineral products [% of total exports]:

842)

Most important export partners:

China, USD 22.0 bn2)

India, USD 12.0 bn2)

Main industries:

Petroleum, petrochemicals, fertilizers, vehicle manu-facture & parts

Imports (goods and services) [USD bn]: 81.0

Import of machinery and manufactured goods [% of total imports]:

552)

Most important import partners:

China, USD 11.0 bn2)

Turkey, USD 9.9 bn2)

9 Roland Berger_Iran_A historical opportunity_Final.pptx

IAEA confirmed that Iran met the relevant requirements under the JCPOA and all nuclear sanctions were lifted on January 16, 2016

Details on sanction status

1) Comprehensive Iran Sanctions, Accountability and Divestment Act 2) In 2010, Iran imported about 30% of its refined petroleum 3) Joint Comprehensive Plan of Action

Source: U.S. Department of State; U.S. Department of the Treasury; UANI; O´Melveny & Myers LLP; Roland Berger

1997

2010

2013

2012 2014 2015 June

November March

January

2016

First sanctions imposed by USA

CISADA1) – expanded sanctions on supply of petroleum products2)

. Further expansion of existing sanctions on imports or exports with value >100 USD allowed

Executive order 13645 – authorizes a range of sanctions, also for non-US companies that continue to service the Iranian automotive industry (manufacturing side only). Non-US financial institutions are also subject of this Executive Act

Geneva Interim Agreement – temporary suspension of nuclear program on Iranian side triggers suspension of sanctions in the Iranian automotive segment. Automakers subsequently reactivated their assembly operations in Iran (e.g. Mercedes-Benz & Lexus)

Preliminary Agreement – provisional agreement on framework for permanent suspension of sanctions

JCPOA3) – phased sanction relief upon verification that Iran has implemented key nuclear commitments – January 16th the IAEA declares that Tehran has fulfilled its obligations and the lifting of sanctions is announced

> The history of sanctions on Iran dates back to 1979

> Several rounds of further reinforcement – latest in effect since 2013

> In July 2015, the 6 nations (P5 + 1) signed the Joint Comprehensive Plan of Action

> The plan includes a gradual process of sanction lifting based on IAEA-verified implemen-tation of agreed nuclear-related measures

10 Roland Berger_Iran_A historical opportunity_Final.pptx

Almost all economic and financial sanctions imposed by the EU and USA have been terminated – Certain restrictions still in place

Impact of lifting of nuclear-related sanctions – Selection

Source: Congressional Research Service; Iran Watch; Roland Berger

Iranian companies are again allowed to export Iranian oil, gas and petrochemical products as well as gold, precious metals and diamonds, and the delivery of Iranian banknotes and coinage is permitted

Most banking activities, including the opening of new branches of Iranian banks in the EU and the opening by EU entities of new offices, subsidiaries, joint ventures or bank accounts in Iran are allowed again – Also transfers of funds between EU entities, including financial and credit institutions, and Iran

Foreign companies are allowed to invest in and export equipment for Iran's oil, gas and petrochemical sectors

EU and USA lifted sanctions that impose asset freezes and travel bans on a set of companies and individuals (mostly in the financial, energy, shipping and transportation sectors)

Iran will also regain access to financial messaging services, including SWIFT, on Implementation Day, but banks that remain designated by the EU will remain cut off from those services until Transition Day

All sanctions by the UN and some EU sanctions are terminated or suspended. US has lifted its nuclear-related secondary sanctions, thus allowing other countries to do business with Iran. However, primary sanctions are still in place, prohibiting US companies from conducting commercial transactions with Iran (few exceptions). Other sanctions

imposed by the European Union, United States and United Nations due to funding of terrorism (e.g. ban on missile technology, conventional arms embargo) are still in place but have no effect on the automotive industry

Sanctions regarding specific industrial sectors have been lifted, e.g. automotive industry, shipping, shipbuilding and transportation sectors, and insurance and reinsurance of Iranian entities

11 Roland Berger_Iran_A historical opportunity_Final.pptx

B. Why enter the Iranian market – 6 opportunities for growth

12 Roland Berger_Iran_A historical opportunity_Final.pptx

Lifting of major sanctions provides a historic opportunity for foreign automakers to (re-)enter the attractive Iranian automotive market

Opportunities for growth in the Iranian market

Source: Roland Berger

Positive development of car sales in all segments

4

Following the waiving of sanctions, new car sales will grow from 2015 onward with a CAGR of 18% p.a. until 2020

Positive economic outlook

1

Economic outlook reflects positive influence of the JCPOA – Solid growth of almost 4.4% from 2016 onward

Legislative initiatives to foster modernization of car parc

5

Iran's authorities have introduced various initiatives to modernize the Iranian car parc – Increasing demand for foreign technology

Increasing customer base

2

Iran's baby boom generation born in the 1980s represents an emerging group of customers

Iran as an export hub

6

Iran is centrally located with good access to Middle Eastern and Asian markets

Demand for foreign products

3

Iranian customers prefer imported goods because of their perceived better quality

13 Roland Berger_Iran_A historical opportunity_Final.pptx

Economic outlook reflects the positive influence of the JCPOA – Solid growth of almost 4.4% from 2016 onward

Source: International Monetary Fund (IMF); Oxford Economics; The World Bank; Roland Berger

Economic outlook – Overview

Positive economic outlook 1

> Iran's economy suffered under the sanctions in recent years (2012 & 2013)

> Oxford Economics predicts medium-term growth rates of 4.0% (2016) and 3.7% (2017)

> Iran is an oil-dependent economy, but has gradually reduced its dependency since the 1990s from 80% to 50-60% (2013) of government revenues based on oil exports

> As of December 2015, the share of oil in Iran's budget was 26.1% representing a decrease of 13.8% from the same period in the prior year

> In the wake of the deal on the easing of sanctions, oil exports are expected to double to pre-sanction levels by 2017, from currently 1 m BBL per day to 2.5 m BBL per day

> Successfully implemented measures brought inflation down from their peak of >30% in 2013

> Furthermore, inflation is expected to decrease slightly and may have downward potential if imports (esp. food) cheapen after the lifting of sanctions

0

10

20

30

40

-8

-6

-4

-2

0

2

4

2017e 2016e 2012 2014 2013 2015e

Oxford Economics (Jul 2015) IMF (WEO; Apr 2015) IMF (WEO; Oct 2014)

Annual GDP growth [%]

Consumer price index inflation [%]

14 Roland Berger_Iran_A historical opportunity_Final.pptx

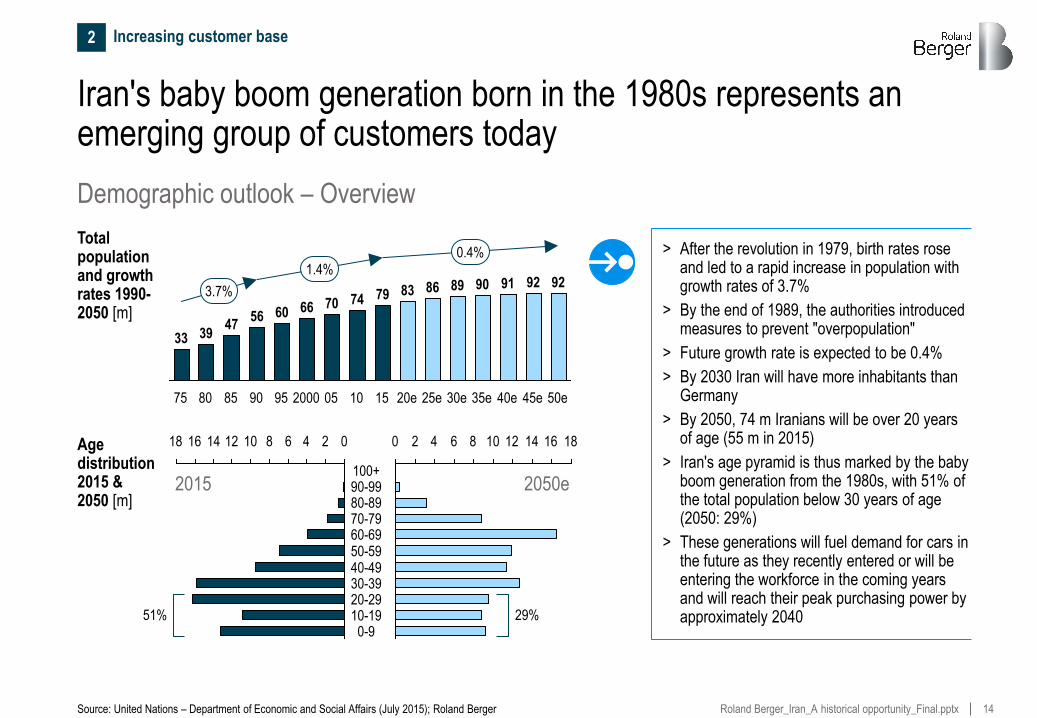

Iran's baby boom generation born in the 1980s represents an emerging group of customers today

Demographic outlook – Overview

Source: United Nations – Department of Economic and Social Affairs (July 2015); Roland Berger

Increasing customer base 2

> After the revolution in 1979, birth rates rose and led to a rapid increase in population with growth rates of 3.7%

> By the end of 1989, the authorities introduced measures to prevent "overpopulation"

> Future growth rate is expected to be 0.4%

> By 2030 Iran will have more inhabitants than Germany

> By 2050, 74 m Iranians will be over 20 years of age (55 m in 2015)

> Iran's age pyramid is thus marked by the baby boom generation from the 1980s, with 51% of the total population below 30 years of age (2050: 29%)

> These generations will fuel demand for cars in the future as they recently entered or will be entering the workforce in the coming years and will reach their peak purchasing power by approximately 2040

Age distribution 2015 & 2050 [m]

Total population and growth rates 1990-2050 [m]

25e 15

86

20e

47

79

56 74 70

89

05

60

85

66

80 90

83

2000 30e

90

35e 75

39 33

95 10

91 1.4%

50e

92 92

0.4%

40e

3.7%

45e

12 14 0 16 18 2 10 4 6 8

40-49 30-39

50-59

90-99 80-89

60-69 70-79

100+

20-29 10-19 0-9

18 0 2 4 6 8 10 14 12 16

2015 2050e

51% 29%

15 Roland Berger_Iran_A historical opportunity_Final.pptx

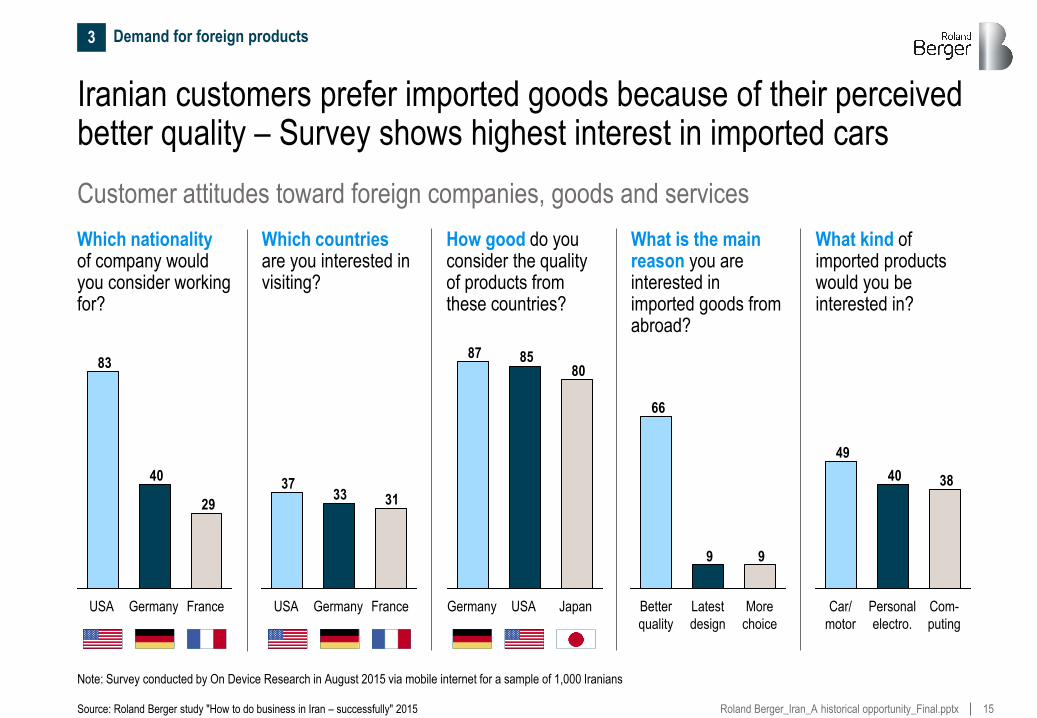

Iranian customers prefer imported goods because of their perceived better quality – Survey shows highest interest in imported cars

Source: Roland Berger study "How to do business in Iran – successfully" 2015

Demand for foreign products 3

Customer attitudes toward foreign companies, goods and services

Note: Survey conducted by On Device Research in August 2015 via mobile internet for a sample of 1,000 Iranians

Which nationality of company would you consider working for?

Which countries are you interested in visiting?

How good do you consider the quality of products from these countries?

What is the main reason you are interested in imported goods from abroad?

What kind of imported products would you be interested in?

29

40

83

France Germany USA

99

66

More

choice

Latest

design

Better

quality

3840

49

Car/

motor

Com-

puting

Personal

electro.

313337

France Germany USA

808587

Japan Germany USA

16 Roland Berger_Iran_A historical opportunity_Final.pptx

Following the waiving of sanctions, new car sales will grow from 2015 onward with a CAGR of 16% p.a. until 2020 in an optimistic scenario

Passenger car sales in Iran 2010-2020 [m units]

Source: IHS Global Insight; Frost & Sullivan; Roland Berger

2013

0.7

2012

0.9

2011

1.5

2010

1.4

2018e 2017e 2016e 2015

0.8

2014

1.0

16% p.a. -53%

2020e 2019e

1.4

1.8

Historic Forecast

Positive development of car sales in all segments 4

> Imposition of sanctions on Iran reversed the growth of the car market in 2011 and new car sales subsequently dropped to just 690,000 new cars sold in 2013 (-53% compared to 2011)

> After the Iranian vehicle market was reopened to foreign automakers in November 2013, positive effects materialized as early as 2014

> The positive outlook with a CAGR of 16% is based on the assumption of a gradual waiving of sanctions – 2015, however, was characterized by postponed purchases due to the anticipated lifting of sanctions

Base scenario Additional volumes in optimistic scenario

17 Roland Berger_Iran_A historical opportunity_Final.pptx

Premium car sales will outperform the overall market with expected growth of ~66% p.a. between 2015 and 2020

Passenger car sales in Iran by price segment 2010-2020 ['000 units]

Source: IHS Global Insight; Roland Berger

> Import tariffs on new cars (CBUs) have been lowered to 40% in 2013, supporting new car sales going forward

> The market collapsed in 2011/2012 due to the political situation

> The six-month period of eased sanctions starting on January 18, 2014 and later extended to November 2014 has given a boost to Iran's auto sales

> Premium market is expected to outpace the overall market, highlighting the shift in demand toward premium products

Volume car sales

66% p.a.

90

7 7 6 4 4 5 50

1,300

1,000

2013

700

2012

900

2011

1,500

2010

1,400 16% p.a.

2020e

1,700

2019e 2018e 2017e 2016e 2015

800

2014

Premium car sales

Other Volvo

Lexus

Audi

Mercedes-Benz

BMW

Group

Others

Hyundai KIA

Renault

Peugeot

Toyota

2015

2015

Positive development of car sales in all segments 4

Base scenario Additional volumes in optimistic scenario

18 Roland Berger_Iran_A historical opportunity_Final.pptx

Iran's authorities have introduced various initiatives to cut emissions and modernize the car parc – Opportunity for foreign OEMs

Details on legislative initiatives

Source: IHS Global Insight; Roland Berger

Initiative

1) <6 l/100 km, 2 cars; 6-10 l/100 km, 4 cars; >10 l/100 km, 10 cars 2) Restriction is expected to be withdrawn when sanctions are lifted

Details > Iran in the past followed EU emission standards:

– In March 2005, Euro II standards were adopted for all gasoline and diesel vehicles – Euro III norms followed in March 2008

– Since March 2012, compliance with Euro IV standards is mandatory for all locally produced gasoline and diesel vehicles and Euro V for import vehicles

– It is expected that from 2016 onward imported vehicles will have to comply with Euro VI

– Authorities also reacted to air pollution with the introduction of restricted traffic zones

> The government wants to foster the shift from petrol to natural-gas-powered vehicles

> As of 2015, Iran has the second largest fleet of CNG powered vehicles globally

> 60% of the total number of vehicles sold in the country must run on natural gas or on dual-fuel – However, this regulation is currently not enforced as it is not technically feasible

> Focus has recently shifted toward hybrid powertrains (lower import tariffs, fewer restrictions, etc.)

> As of today, around 2.2 million vehicles are affected by the scrappage program introduced to reduce the average fuel consumption of the current car parc

> Authorities want to put some 200,000 vehicles per year out of the market, eventually to be replaced by newer, more efficient cars

> Expected duration of this measure is 10–15 years

> Program so far successfully reduced average age of vehicles in use from 17 years (2005) to 10.6 years (2013)

Legislative initiatives to foster modernization of car parc 5

Emission standards

Alternative powertrains

Scrappage program

19 Roland Berger_Iran_A historical opportunity_Final.pptx

Iran is centrally located with good access to Middle Eastern and Asian markets – Tax breaks to foster export of local goods

Iran as a gateway to other budget markets

Source: Iran Khodro, PSA; Press research; Roland Berger

Iran as an export hub 6

Potential export markets

Algeria

Morocco Tunisia

Libya Egypt

Lebanon Syria

Turkey

Russia

Turkmenistan

Afghanistan

Pakistan

Azerbaijan

Georgia

Armenia

Iran Iraq

> Due to its central geographic location and further positive location factors, Iran could serve as an export hub to other budget markets in the Middle East, CIS, Africa and Latin America

> Local manufacturers such as Iran Khodro are already exporting their cars to countries like Russia, Syria, Turkey, Iraq, Azerbaijan, Ukraine, Egypt, Algeria, Bulgaria and Venezuela

> Foreign manufacturer PSA has also announced plans to export 30% of their locally produced vehicles after re-launching manufacturing operations

> Iranian authorities announced a 50% tax break besides other incentives for foreign investors who build factories in Iran and export more than 30% of their products

Belarus

Ukraine

Sudan

Bulgaria

20 Roland Berger_Iran_A historical opportunity_Final.pptx

C. How to enter the Iranian market – 9 key success factors

21 Roland Berger_Iran_A historical opportunity_Final.pptx

OEMs need to thoroughly understand the national specifics before entering the Iranian market – 9 key success factors identified

Key success factors in the Iranian market

Source: Roland Berger

How to import cars How to sell cars

Know the complex import and taxation regulations

1

Establish a strong relationship with the relevant stakeholders

2

Assess, for each model individually, whether to produce locally

3

Leverage the existing supplier and manufacturing base

4

Know your customer requirements 5

Know the competitive environment 6

Cover the relevant markets with your sales & after-sales network

7

Provide the best sales & after-sales service in your segment

8

How to grow in the market

Decide on the right market entry strategy: Greenfield vs. existing local partner 9

22 Roland Berger_Iran_A historical opportunity_Final.pptx

Iran's authorities have introduced various initiatives to cut emissions and modernize the car parc – Opportunity for local production

Import and taxation regulations

Source: IHS Global Insight; Roland Berger

1) Based on CIF 2) Based on FOB

> Various charges are applied on the vehicle FOB/CIF

– Import duty of 32-75% depending on powertrain type and engine capacity

– Standard inspection, Red Crescent and other import and governmental charges amount to an additional ~7.5%

> Importers also need to prove scrappage of cars in order to get import allowances:

– Number of cars to be scrapped is staggered and depends on fuel consumption of the imported car

> Since 2013, the import of cars with engines above 2,500cc has been banned – Recently a change to the import duty regulation was proposed that would allow engines up to 3,000cc, but the proposal is still pending

Overview of import regulations

Import legislation Import costs

Engine capacity

> Limitation to 2,500cc for gas and diesel

> No limitation for hybrid/electric

Import tariffs1) 40-75% depending on engine capacity

Standard inspection1)

Check of conformity with vehicle standards

Red Crescent1) -

Other govern-ment charges2)

Add. charges imposed by different govern-ment stakeholders

Other import costs2)

Costs, e.g. for ware-house & transportation

Scrapping of old cars

1, 4 or 10 cars have to be scrapped for each imported car depen-ding on the fuel consumption

Emission standard

> EURO 5 and EURO 6 for new homologation

Fuel con-sumption

> Limited

Further legislation

> Homologation standards

> Scrapping requirement

Know the complex import and taxation regulations 1

23 Roland Berger_Iran_A historical opportunity_Final.pptx

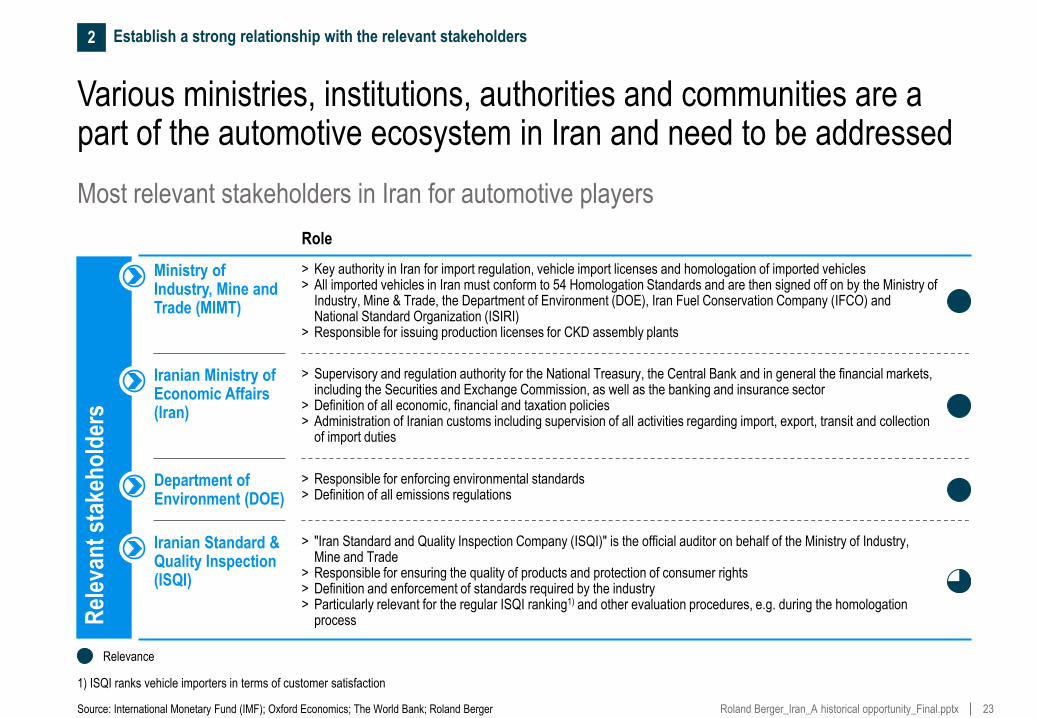

Various ministries, institutions, authorities and communities are a part of the automotive ecosystem in Iran and need to be addressed

Most relevant stakeholders in Iran for automotive players

Source: International Monetary Fund (IMF); Oxford Economics; The World Bank; Roland Berger

Rel

evan

t st

akeh

old

ers

Role

Ministry of Industry, Mine and Trade (MIMT)

> Key authority in Iran for import regulation, vehicle import licenses and homologation of imported vehicles > All imported vehicles in Iran must conform to 54 Homologation Standards and are then signed off on by the Ministry of

Industry, Mine & Trade, the Department of Environment (DOE), Iran Fuel Conservation Company (IFCO) and National Standard Organization (ISIRI)

> Responsible for issuing production licenses for CKD assembly plants

Iranian Ministry of Economic Affairs (Iran)

> Supervisory and regulation authority for the National Treasury, the Central Bank and in general the financial markets, including the Securities and Exchange Commission, as well as the banking and insurance sector

> Definition of all economic, financial and taxation policies > Administration of Iranian customs including supervision of all activities regarding import, export, transit and collection

of import duties

Department of Environment (DOE)

> Responsible for enforcing environmental standards > Definition of all emissions regulations

Iranian Standard & Quality Inspection (ISQI)

> "Iran Standard and Quality Inspection Company (ISQI)" is the official auditor on behalf of the Ministry of Industry, Mine and Trade

> Responsible for ensuring the quality of products and protection of consumer rights > Definition and enforcement of standards required by the industry > Particularly relevant for the regular ISQI ranking1) and other evaluation procedures, e.g. during the homologation

process

1) ISQI ranks vehicle importers in terms of customer satisfaction

Establish a strong relationship with the relevant stakeholders 2

Relevance

24 Roland Berger_Iran_A historical opportunity_Final.pptx

Local CKD assembly results in significantly lower retail prices compared to CBU imports – Lower import duty is the main factor

Source: Roland Berger

Note: Minimum local content assumed to achieve lower import tariff; retail price excluding all costs paid by customer (VAT, registration tax, mandatory 3rd party insurance); HEV = hybrid electric vehicle, BEV = battery electric vehicle

Market price comparison CBU vs. CKD

85%

100%

Retail

price CKD

Savings Additional

cost

Retail

price CBU

Dealer

margin

Sales &

Distribution

Landed

cost

~80%

Scrapping Other import

related cost

Import

tariffs

CIF

~52%

FOB cost

& Shipping

Wholesale

price

~50%

Share [%]

20 21 32 39 33

Exemplary calculation

Value [EUR '000]

> Wholesale vehicle price accounts for only ~50% of the retail car price in Iran

> Main factors in the price increase are import tariffs, scrappage other import related costs

> No scrappage requirements and lower import tariffs/cost of CKD production result in total cost savings of ~20% and a retail price difference of ~15%

> CKD business case to be validated for each model – Low volume models to remain CBU

Assess, for each model individually, whether to produce locally 3

Import of HEV & BEV highly attractive due to low import duty of 4% and no scrapping requirement

25 Roland Berger_Iran_A historical opportunity_Final.pptx

Markazi

Hormozgan

Ilam Lorestan

Chahar Mahall

and Bakhtiari Khuzestan

Isfahan

Yazd

Kohgiluyeh and Buyer

Ahmad

Fars

Bushehr

Kerman

Sistan and Baluchestan

South Khorasan

Razavi Khorasan

North Khorasan

Golestan

Semnan

Qom

Tehran

Mazandaran

Qazvin

Zanjan

Hamadan

Kermanshah

Kordestan

West Azarbaijan

Gilan

Ardebil

East Azarbaijan

Ahvaz

Isfahan

Shiraz

Mashad

Qom

Tehran

Orumieh

Tabriz

Karaj

Kermanshah

Kashan

Babol

Golpaigan

Tehran is the automotive manufacturing hub in Iran, home to the main plants of IKCO and SAIPA and also various smaller producers

Main automotive plants and supplier network in Iran

Source: Press research; SAIPA; GTAI; IHS Global Insight; Roland Berger

> Iran Khodro and SAIPA are Iran's main automotive producers with capacities of more than 800,000 vehicles each – Total production capacity of 2.0 m units estimated

> Besides CBU production of local brands or older Peugeot/Renault models, typically Chinese and Korean brands are manufactured as CKD versions together with Iranian partners

> The vehicle manufacturing industry is backed by a strong supply network of more than 1,000 active parts manufacturers

Focus regions of Iran's automotive parts manufacturing industry

Leverage the existing supplier and manufacturing base 4

City with major production facilities

26 Roland Berger_Iran_A historical opportunity_Final.pptx

Customers have clearly defined expectations of a dealer, on the basis of which they make a purchase decision

Key success factors for Iranian customers

Source: Customer survey conducted by Roland Berger in Iran in April 2015; Roland Berger

Network coverage 1

Provision of other offers – Customer club, memberships, etc. 10

Knowledgeable, professional and friendly staff 2

Availability of the full range of technical support in workshops 3

Quality & speed of after-sales service 4

Availability of options, parts and accessories for cars 5

Reasonable cost of after-sales service 6

Favorable warranty options 7

Dealership appearance 8

Dealership brand image 9

Key success factors for the Iranian car market

Know your customer requirements 5

27 Roland Berger_Iran_A historical opportunity_Final.pptx

LON-35187-002-01-34.ppt

So far, only two dealers are official licensed by the OEM, but almost all brands have an officially recognized importer active in Iran

Overview of car importers

1) Officially recognized by Iranian authorities but, except for Setareh (Mercedes-Benz) and Ati Motors, not by the respective OEM 2) Currently only service center

Source: Roland Berger

Arta Motor Iran

Limited activities2) due to import restrictions

Car Importers

Ati Motors Persia Khodro

Multiple grey market players Irtoya

Afra Motors Alfa Motors

Ramak Khodro

Moin Motors

Setareh

Dealers officially licensed by OEM

Officially recognized importers by the Iranian authorities1)

Grey-market importers

Know the competitive environment 6

28 Roland Berger_Iran_A historical opportunity_Final.pptx

The top 10 car markets in Iran account for ~85% of automotive sales volumes – Majority sold through grey-market importers

Top 10 car markets in Iran

Source: Roland Berger

Top 10 car markets in Iran

Cover the relevant markets with your sales & after-sales network 7

> Iranian car customers are concentrated in 10 cities, which account for over 85% of automotive sales volumes in Iran

> Officially recognized importers by the Iranian authorities and dealers that are officially licensed by the respective OEMs focus on those main markets

> However, grey importers are active all around the country – In 2015, 88% of imported vehicles were imported by grey importers

> Grey market typically offers better prices due to lower regulatory charges (e.g. no warranty costs1))

> Since grey market importers can purchase cars through various sources they have a greater choice to offer the customers – Cars are mostly ordered on demand

Isfahan

Tabriz

Urmie Amol

Tehran

Shiraz

Karaj

Yazd

Kerman

Mashad

1) Warranty can be transferred to official dealer for a fixed amount

29 Roland Berger_Iran_A historical opportunity_Final.pptx

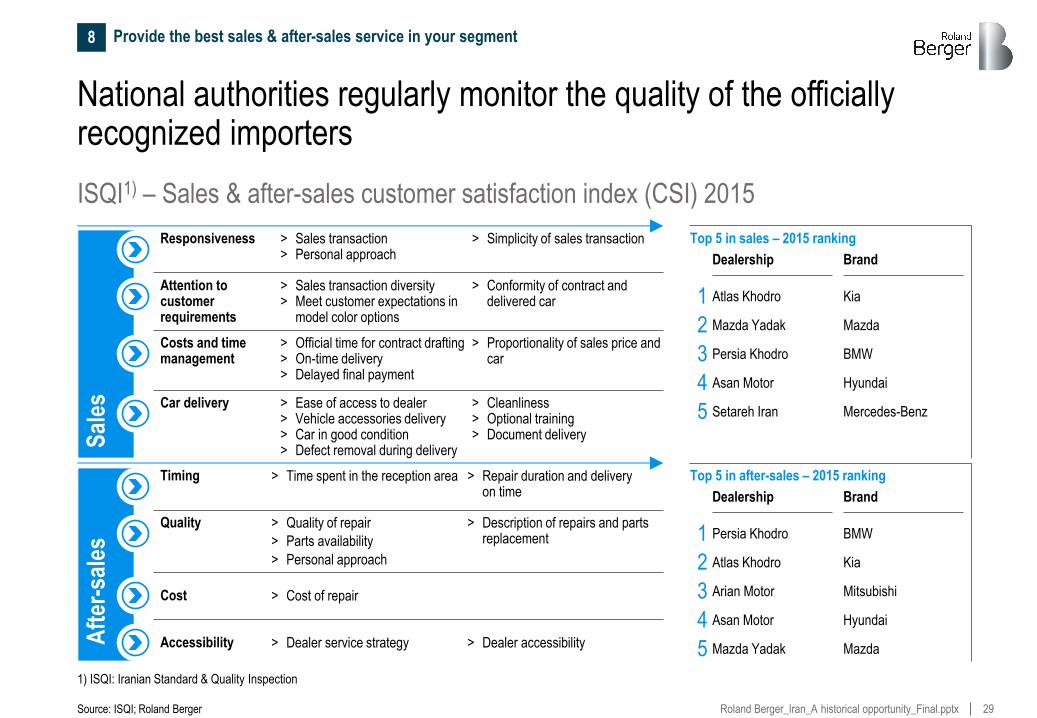

National authorities regularly monitor the quality of the officially recognized importers

ISQI1) – Sales & after-sales customer satisfaction index (CSI) 2015

1) ISQI: Iranian Standard & Quality Inspection

Source: ISQI; Roland Berger

Provide the best sales & after-sales service in your segment 8

Aft

er-s

ales

S

ales

Responsiveness > Sales transaction > Personal approach

> Simplicity of sales transaction

Attention to customer requirements

> Sales transaction diversity > Meet customer expectations in

model color options

> Conformity of contract and delivered car

Costs and time management

> Official time for contract drafting > On-time delivery > Delayed final payment

> Proportionality of sales price and car

Car delivery > Ease of access to dealer > Vehicle accessories delivery > Car in good condition > Defect removal during delivery

> Cleanliness > Optional training > Document delivery

> Time spent in the reception area > Repair duration and delivery on time

Timing

> Quality of repair

> Parts availability

> Personal approach

> Description of repairs and parts replacement

Quality

> Cost of repair Cost

> Dealer service strategy > Dealer accessibility Accessibility

Top 5 in after-sales – 2015 ranking

1

2

3

4

5

Dealership Brand

Persia Khodro BMW

Atlas Khodro Kia

Arian Motor Mitsubishi

Asan Motor Hyundai

Mazda Yadak Mazda

Top 5 in sales – 2015 ranking

1

2

3

4

5

Dealership Brand

Atlas Khodro Kia

Mazda Yadak Mazda

Persia Khodro BMW

Asan Motor Hyundai

Setareh Iran Mercedes-Benz

30 Roland Berger_Iran_A historical opportunity_Final.pptx

OEMs can leverage a local partner – Greenfield approach more difficult due to existing officially recognized importers

Assessment of market entry strategy: Greenfield vs. local partner

Source: Roland Berger

Decide on the right market entry strategy: Greenfield vs. local partner 9

> Build up a network with a clear strategy in mind

> Set up tight processes according to OEM standard

> Leverage know-how from other markets

> Full control over management

> Existing dealer and after-sales infrastructure

> Extensive knowledge of import regulations

> Typically, close relationships with the key decision makers within the respective authorities

> Existing brand image for Iranian customers

> Slower market penetration, due to lack of knowledge of customer requirements, import legislation, etc.

> Strong competition from existing dealer networks

> Unclear legal situation regarding officially recognized dealers – Potential lawsuits could delay an immediate market entry

> Lack of relationship with key decision makers within the respective authorities – May lead to time-consuming homologation, registration, etc.

> Processes not according to OEM standard

> Competence of management unclear

> Network to be reviewed strategically

Greenfield Local partner

31 Roland Berger_Iran_A historical opportunity_Final.pptx

D. What to do now – Next steps

32 Roland Berger_Iran_A historical opportunity_Final.pptx

With the lifting of sanctions, automotive OEMs must now quickly take the next steps to successfully (re-)enter the Iranian market

Next steps for automotive OEMs to enter Iran

Source: Roland Berger

Roland Berger has the necessary experience, in-depth knowledge and relationships with key stakeholders to provide you with further advice on entering the Iranian market

> Thoroughly understand the specifics of the Iranian market

> Analyze the existing dealership network

THINK

> Decide on whether to take a greenfield approach or to partner with a local dealership network

> Define for each model a CBU vs. CKD strategy

ACT