Quarter 2 2013

Our second edition of 2013 starts with adetailed look at the IASB’s new proposalson accounting for the impairment offinancial instruments before consideringother items in the IASB’s ‘pipeline’.

We then go on to IFRS-related newsat Grant Thornton before turning to amore general round-up of financialreporting developments relevant to IFRSpreparers. We finish with theimplementation dates of newer Standardsthat are not yet mandatory and a list ofIASB publications that are out forcomment.

Welcome to IFRS News – a quarterly update fromthe Grant ThorntonInternational IFRS team.IFRS News offers asummary of the moresignificant developments in International FinancialReporting Standards (IFRS)along with insights intotopical issues and commentsand views from the GrantThornton InternationalIFRS team.

IFRS News

IASB unveils new proposals forimpairment of financial assets

2 IFRS News Quarter 2

Long-awaited proposals vie foracceptance with alternative USapproachThe IASB has issued the Exposure Draft‘Financial Instruments: Expected CreditLosses’. It contains proposals aimed atrectifying what was perceived to be amajor weakness in accounting during thefinancial crisis of 2007/8, namely therecognition of credit losses at too late astage.

The proposals follow on from twoearlier exposure documents, aNovember 2009 Exposure Draft and a‘Supplementary Document’ published inJanuary 2011. Should these latestproposals be finalised, they will beincorporated as a chapter in IFRS 9‘Financial Instruments’ – the Standardthat will eventually replace IAS 39‘Financial Instruments: Recognition andMeasurement’. The proposals will affectall entities that hold debt-type financialassets or issue commitments to extendcredit that are not accounted for at fairvalue through profit or loss.

Background to the proposalsDuring the financial crisis, the delayedrecognition of credit losses on loans (andsome other financial assets) wasidentified as a major weakness in theperformance of IAS 39. This was becausethe ‘incurred loss’ model used under thatStandard delays the recognition of creditlosses until there is evidence that a creditloss event has occurred. In addition, IAS 39 was criticised for the complexityarising from the use of different ways ofmeasuring impairment for differentcategories of asset.

The main proposalsThe Exposure Draft proposes analternative to the incurred loss modelthat would use more forward-lookinginformation. The perceived complexityof IAS 39 would also be addressed byapplying the same impairment model toall financial instruments that are subjectto impairment accounting.

Under the proposals, recognition ofcredit losses would no longer bedependent on the entity first identifyinga credit loss event. An entity wouldinstead consider a broader range ofinformation when assessing credit riskand measuring expected credit losses,including:• past events, such as experience of

historical losses for similar financialinstruments

• current conditions• reasonable and supportable forecasts

that affect the expected collectabilityof the future cash flows of thefinancial instrument.

In applying this more forward-lookingapproach, a distinction is made between:• financial instruments that have not

deteriorated significantly in creditquality since initial recognition orthat have low credit risk and

• financial instruments that havedeteriorated significantly in creditquality since initial recognition andwhose credit risk is not low.

‘12-month expected credit losses’ arerecognised for the first of these twocategories while ‘lifetime expected creditlosses’ are recognised for the secondcategory.

Instruments that will be within the scope of the proposals:• loans and other debt-type financial assets measured at amortised cost

• loans and other debt-type financial assets measured at fair value through other

comprehensive income*

• trade receivables

• lease receivables

• loan commitments (for the issuer)

• financial guarantee contracts (for the guarantor)

* the IASB has proposed the introduction of this measurement category in its November 2012 Exposure Draft‘Classification and Measurement: Limited Amendments to IFRS 9 (Proposed amendments to IFRS 9 (2010)’.

IFRS News Quarter 2 3

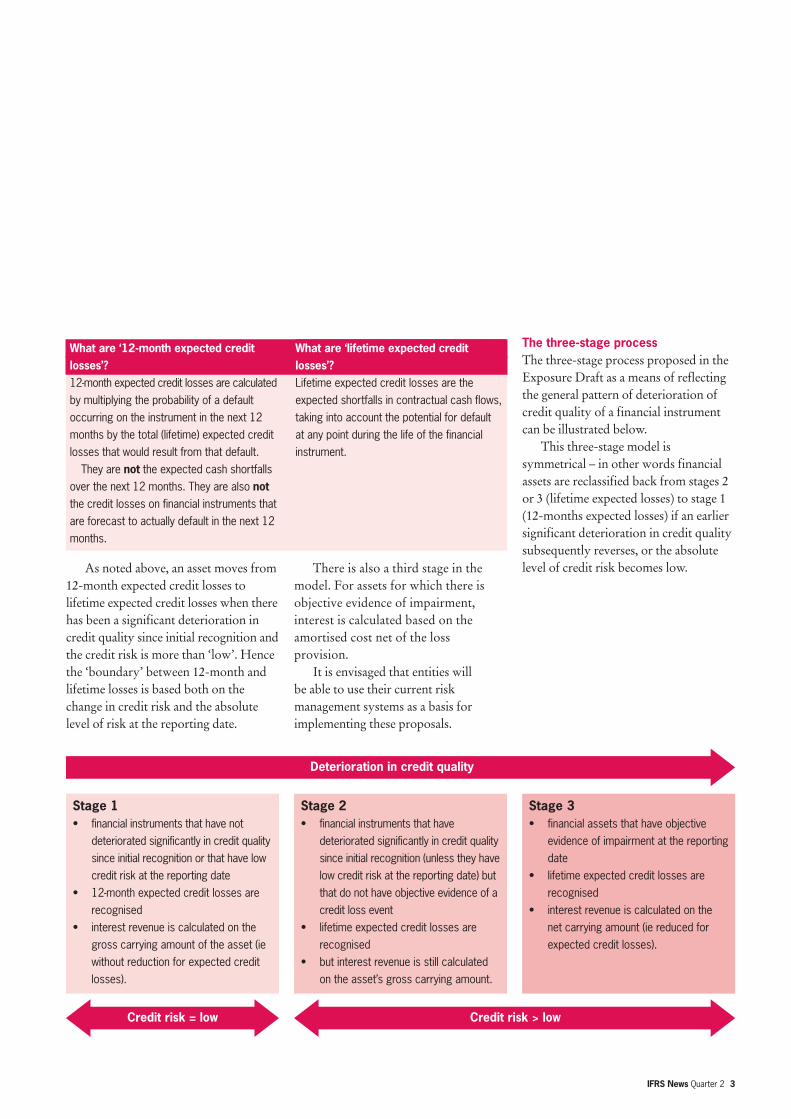

As noted above, an asset moves from12-month expected credit losses tolifetime expected credit losses when therehas been a significant deterioration incredit quality since initial recognition andthe credit risk is more than ‘low’. Hencethe ‘boundary’ between 12-month andlifetime losses is based both on thechange in credit risk and the absolutelevel of risk at the reporting date.

There is also a third stage in themodel. For assets for which there isobjective evidence of impairment,interest is calculated based on theamortised cost net of the lossprovision.

It is envisaged that entities will be able to use their current riskmanagement systems as a basis forimplementing these proposals.

The three-stage processThe three-stage process proposed in theExposure Draft as a means of reflectingthe general pattern of deterioration ofcredit quality of a financial instrumentcan be illustrated below.

This three-stage model issymmetrical – in other words financialassets are reclassified back from stages 2or 3 (lifetime expected losses) to stage 1(12-months expected losses) if an earliersignificant deterioration in credit qualitysubsequently reverses, or the absolutelevel of credit risk becomes low.

What are ‘12-month expected credit losses’?

What are ‘lifetime expected creditlosses’?Lifetime expected credit losses are the

expected shortfalls in contractual cash flows,

taking into account the potential for default

at any point during the life of the financial

instrument.

12-month expected credit losses are calculated

by multiplying the probability of a default

occurring on the instrument in the next 12

months by the total (lifetime) expected credit

losses that would result from that default.

They are not the expected cash shortfallsover the next 12 months. They are also notthe credit losses on financial instruments that

are forecast to actually default in the next 12

months.

Stage 1• financial instruments that have not

deteriorated significantly in credit quality

since initial recognition or that have low

credit risk at the reporting date

• 12-month expected credit losses are

recognised

• interest revenue is calculated on the

gross carrying amount of the asset (ie

without reduction for expected credit

losses).

Stage 2• financial instruments that have

deteriorated significantly in credit quality

since initial recognition (unless they have

low credit risk at the reporting date) but

that do not have objective evidence of a

credit loss event

• lifetime expected credit losses are

recognised

• but interest revenue is still calculated

on the asset’s gross carrying amount.

Stage 3• financial assets that have objective

evidence of impairment at the reporting

date

• lifetime expected credit losses are

recognised

• interest revenue is calculated on the

net carrying amount (ie reduced for

expected credit losses).

Deterioration in credit quality

Credit risk = low Credit risk > low

4 IFRS News Quarter 2

A simplified approach for certainassetsIn developing the proposals, there wasconcern that the process of determiningwhether to recognise 12-month orlifetime expected credit losses was notjustifiable for instruments such as tradereceivables and lease receivables.

As a result, the IASB has includedtwo simplifications in its proposals: 1) for ‘short term’ trade receivables, an

entity should always recognise a lossallowance at an amount equal tolifetime expected credit losses.Practical expedients, such as use of aprovisioning matrix, are permitted.

2) for ‘long-term’ trade receivables(ones which constitute financingtransactions under IAS 18 ‘Revenue’)and lease receivables, entities wouldbe allowed to choose an accountingpolicy to always recognise a lossallowance at an amount equal tolifetime expected credit losses.

Convergence with US GAAPLike the IASB’s current standard IAS 39,US GAAP also uses an incurred lossimpairment model at the moment. Thetwo Boards have therefore been workingtogether to develop a more forward-looking model based on expected creditlosses and in December 2012, the USFinancial Accounting Standards Board(FASB) issued its proposals for a‘current expected credit loss’ (CECL)model.

Unlike the IASB Exposure Draft,however, the FASB proposals make nodistinction between those financialinstruments that have deteriorated incredit quality since initial recognition andthose that have not. Instead expectedcredit losses are always recognised atwhat the IASB describes in its proposalsas lifetime expected credit losses.

Accordingly, the FASB proposal wouldgenerally result in larger loan lossprovisions. Both proposals would result in so-called ‘day-1 losses’ (lossesarising immediately on originating orpurchasing debt assets) – an outcomethat some commentators considercounter-intuitive – but the day-1 losswould be higher under the FASBproposal. While some of the informationthat is used to estimate and measureexpected credit losses is consistent underboth the IASB and FASB models, this isa significant difference.

Grant Thornton International commentGiven that the comment periods on the IASB Exposure Draft and on the FASB’s CECL

Exposure Draft overlap, we can expect respondents to compare and contrast the two

expected credit loss models and to express a preference for one over the other. Loan loss

provisioning is an area where an internationally-converged solution would be highly preferable

– even if the two Boards’ overall financial instruments reforms are not fully converged in other

areas. It is therefore encouraging that the Boards have committed to jointly re-deliberate their

proposals in the light of respondents’ comments. We acknowledge that achieving

convergence in this area will be challenging but we encourage the Boards to use their best

endeavours to do so.

IFRS News Quarter 2 5

EFRAG to conduct field-testing of impairment proposals in Europe

EFRAG and the National StandardSetters ANC, ASCG, FRC and OIChave invited companies to participate ina field-test on how the IASB’s proposedimpairment requirements will affect theassessment of the amount, timing anduncertainty of future cash flows offinancial assets that are measured atamortised cost and fair value throughother comprehensive income, includingtrade receivables and lease receivables.

The purpose of the exercise is toidentify whether or not the proposals forthe expected credit losses model addressthe weaknesses of the existing incurredloss impairment model in IAS 39.Additionally, the exercise addresses theoperationality and the impact and costsrelated to the expected credit lossesmodel. In particular, the field-test asksquestions on:

• how the expected credit losses modelreflects the amount, timing anduncertainty of future cash flows

• whether the requirements are clearand operational

• the impact of the proposed expectedcredit losses model

• the costs and benefits of theproposed expected credit lossesmodel.

The field test started on 15 April 2013and completed questionnaires should bereturned by 2 June 2013.

6 IFRS News Quarter 2

Grant Thornton Internationalresponds to the IASB’s proposals to amend IFRS 9’s classificationand measurement criteria

Grant Thornton International’s IFRSTeam has submitted its comment letter on the IASB Exposure Draft‘Classification and Measurement:Limited Amendments to IFRS 9 –Proposed amendments to IFRS 9 (2010)’.

In our letter we express support forthe Board’s efforts to provide relief forcertain types of financial instrumentswhich would be classified at fair value

under the current requirements of IFRS 9 ‘Financial Instruments’. Wesuggest however that the proposals donot go far enough to address legitimateconcerns raised and that as a result,certain types of financial instrument forwhich amortised cost measurement mayprovide more meaningful informationwill continue to be classified at fairvalue.

With regard to the other mainproposal in the Exposure Draft, theintroduction of an additional ‘fair valuethrough other comprehensive income’(FVTOCI) category, we note that itsintroduction will compromise thereduction in complexity that was offeredby the original version of IFRS 9. Onbalance, however, we support itsintroduction.

Proposed amendments to IAS 19

The IASB has issued ‘Defined BenefitPlans: Employee Contributions(Proposed amendments to IAS 19)’. TheExposure Draft proposes a simplifiedapproach for accounting for somearrangements in which employees orthird parties contribute to the cost ofdefined benefit pension plans. It alsoaims to clarify how such contributionsshould be attributed to periods of servicewhen required.

Some defined benefit plans requireemployees or third parties to contributeto the cost of the plan. Contributions byemployees reduce the cost of the benefitsto the entity. The Exposure Draft

addresses the accounting forcontributions from employees or thirdparties when the requirement for suchcontributions is set out in the formalterms of a defined benefit plan. Itproposes that such contributions may berecognised as a reduction in the servicecost in the same period in which they arepayable if, and only if, they are linkedsolely to the employee’s service renderedin that period. An example would becontributions that are a fixed percentageof an employee’s salary, so thepercentage of the employee’s salary doesnot depend on the employee’s numberof years of service to the employer.

The suggested change is in effect apractical expedient to help users inaccounting for such situations, and alsoreflects common practice under the pre-2011 version of IAS 19. Without it,all contributions from employees orthird parties to a defined benefit planthat relate to service would need to beattributed to periods of service as anegative benefit. This would involvecomplex calculations however, whichcould potentially lead to confusion inpractice.

IFRS News Quarter 2 7

Novation of derivatives andcontinuation of hedge accounting

The IASB has published proposals foramendments to IAS 39 ‘FinancialInstruments: Recognition andMeasurement’ relating to the novation ofderivatives and the continuation ofhedge accounting.

The objective of the proposedamendments is to introduce a narrowscope exception to the requirement forthe discontinuation of hedge accountingin IAS 39. Specifically, they propose anexception when a derivative that hasbeen designated as a hedging instrument,is novated from one counterparty to a

central counterparty as a consequence ofnew laws or regulations, providedspecific conditions are met.

In the context of the Exposure Draft,novation of the derivative contract is thesubstitution of the original counterpartyto the contract for a new centralcounterparty. Legislative changes arisingfrom the G20’s (Group of TwentyFinance Ministers and Central BankGovernors) commitment to improve thetransparency and regulatory oversight ofover-the-counter derivatives in aninternationally consistent and

non-discriminatory way has meant thatthis is a current issue for many entitiesholding derivatives. As these new lawsor regulations could come into effect insome jurisdictions very soon, the IASBpublished its Exposure Draft with ashort (30-day) comment period whichexpired on 2 April.

IASB issues request for informationon rate regulation

IASB looks to identify a range of rate-regulatory schemes in order to helpdetermine scope of research projectThe IASB has issued a Request forInformation as an early step in itsreactivated ‘Rate-regulated Activities’research project.

In July 2009 the IASB published theExposure Draft ‘Rate-regulatedActivities’, which focused on a particulartype of rate-regulatory scheme.Respondents at the time expresseddivergent views as to how theconsequences of rate regulation should bereflected in financial statements, if at all.

Many suggested that the scope of theproject should be expanded to look at awider variety of rate regulation in orderto identify common characteristics fromwhich accounting guidance might bedeveloped.

The original rate-regulated activitiesproject was suspended in September2010 but has recently been restarted. Theobjective of the Request for Informationis to identify a range of rate-regulatoryschemes to help determine the scope ofthe research project. In particular it asksspecific questions about the objectives ofrate regulation and how those objectivesare reflected in the rate-settingmechanisms employed by rate regulators.

The IASB intends to use the factsgathered through this process along withother research to develop a DiscussionPaper that will analyse the commonfeatures of rate regulation.

8 IFRS News Quarter 2

Deferred tax – a Chief FinancialOfficer’s guide to avoiding the pitfalls

Deferred tax – a Chief FinancialOfficer’s guide to avoiding the pitfalls

UNDERSTANDING DEFERRED TAX UNDER IAS 12 INCOME TAXES FEBRUARY 2013

Grant Thornton International IFRSTop 20 Tracker – 2013 edition

2013 EDITION

IFRS Top 20 Tracker

The Grant Thornton International IFRSteam has published the 2013 edition ofits ‘IFRS Top 20 Tracker’.

The 2013 edition again takesmanagement through twenty of the topdisclosure and accounting issuesidentified by Grant ThorntonInternational as potential challenges forIFRS preparers.

Key themes driving selection of theissues in the 2013 edition are:• the need for consistency between a

company’s financial statements andits management commentary

• the effect that adverse economicconditions may have on a company’sfinancial statements, with particularemphasis on the applicability of thegoing concern assumption

• key areas of interest for regulators • challenging areas of accounting• recent and forthcoming changes in

financial reporting.

To obtain a copy of the publication,please get in touch with your local IFRScontact.

Grant Thornton International hasreleased a revised version of its guide‘Deferred tax – a Chief FinancialOfficer’s guide to avoiding the pitfalls’.

The revised guide has been updatedto reflect changes and updates made to IAS 12 ‘Income Taxes’ up to 31 December 2012 and is intended forChief Financial Officers (CFOs) ofbusinesses that prepare financialstatements under IFRS. It illustrates IAS 12’s approach to the calculation ofdeferred tax balances and summarisesthe approach to calculating the deferredtax provision in order to help CFOsprioritise and identify key issues.

To obtain a copy of the publication,please get in touch with your local IFRScontact.

IFRS News Quarter 2 9

US firm reports on latest revenuerecognition deliberations

Updated version of guide to liabilityor equity classification under IAS 32

Liability or equity?

A PRACTICAL GUIDE TO THE CLASSIFICATION OF FINANCIAL INSTRUMENTS UNDER IAS 32 MARCH 2013

Grant Thornton International hasreleased a revised version of its guide‘Liability or equity? A practical guide tothe classification of financial instrumentsunder IAS 32’.

The new edition reflectsamendments that have been made to IAS 32 ‘Financial Instruments:Presentation’ since the Guide was firstpublished in 2009 together with ourlatest thinking on some of the moreproblematic areas of interpretation in the Standard.

To obtain a copy of the publication,please get in touch with your local IFRScontact.

Our US member firm Grant ThorntonLLP, has released a ‘New DevelopmentsSummary’ outlining the latestdeliberations of the IASB and the USFinancial Accounting Standards Board(FASB) as they move towards finalisingtheir joint project on revenuerecognition.

For several years now, the FASB andthe IASB have been discussing their jointproject with the objective of developinga single comprehensive, convergedrevenue recognition model. Thosediscussions have resulted in a number ofdocuments being issued for publicdiscussion, the most recent being the2011 Exposure Draft ‘Revenue fromContracts with Customers’.

Since the publication of thatExposure Draft, the two Boards haveundertaken extensive outreach. Our USfirm’s bulletin updates the proposalsincluded in the 2011 ED to reflect thetentative decisions reached by theBoards in their latest redeliberations.

Barring any unforeseen problems,the Boards plan to issue a final standardwith converged guidance on revenuerecognition in the middle of 2013. Whenfinalised, the proposed guidance willreplace IAS 18 ‘Revenue’, IAS 11‘Construction Contracts’ and most ofthe revenue recognition guidance in USGAAP. The Bulletin entitled ‘Revenuerecognition project nearing end’ can beviewed on our US firm’s websitewww.grantthornton.com.

10 IFRS News Quarter 2

Grant Thornton International’s IFRSTeam has announced its plans for globalIFRS training in 2013. Partners and stafffrom Grant Thornton member firmswill be able to attend training in fourregions throughout the world:• Miami • Dubai • Dusseldorf • Singapore.

The provision of global training is justone of a number of means by whichGrant Thornton International promoteshigh-quality, consistent application ofIFRSs throughout its internationalnetwork of member firms.

The course content will focus on:

New standards and interpretations

Addressing practical application issues related to

those IFRSs and amendments that have recently

come into effect, including:

• the ‘consolidation package’ guidance (IFRS 10,

11, 12 and the revised IAS 27, 28)

• latest developments for investment entities

(amendments to IFRS 10);

• fair value (IFRS 13)

• employee benefits (IAS 19)

Common application issues

Topical focus on

• IAS 37 ‘Provisions, Contingent Liabilities and

Contingent Assets’

• IAS 40 ‘Investment Properties’

• IAS 16 ‘Property, Plant and Equipment’

targeting common regulatory report findings

General IFRS update

Analysis of the latest IASB and IFRIC developments

and reminder of IFRS resources provided by Grant

Thornton International.

Grant Thornton Internationalannounces 2013 IFRS regional training

Spotlight on our IFRS InterpretationsGroup

Grant Thornton International’s IFRSInterpretations Group (IIG) consists ofa representative from each of ourmember firms in the United States,Canada, Singapore, Australia, SouthAfrica, India, the United Kingdom,France, Sweden and Germany as wellas members of the Grant ThorntonInternational IFRS team. It meets inperson twice a year to discuss technicalmatters which are related to IFRS.

Each quarter we throw a spotlighton one of the members of the IIG. Thisquarter we focus on Sweden’srepresentative:

Eva Törning, SwedenEva Törning is the accounting technicalpartner of Grant Thornton Sweden.Eva joined Grant Thornton in 2009and has over thirty years’ experience infinancial reporting. During that timeshe has worked at the Ministry ofJustice, with the Swedish AccountingStandards Board and as auditor andfinancial manager both in Sweden andoverseas. Eva is currently a member ofthe Accounting Policy Group withinthe Institute for the AccountancyProfession in Sweden. Eva has writtenthree books in accounting and financialreporting – one of which is aimed atuniversity studies. Eva also lecturesextensively and writes articles onfinancial reporting.

Round-up

IFRS News Quarter 2 11

Highlights of IASB survey on financialinformation disclosuresThe IASB has released highlights of asurvey conducted recently on financialinformation disclosures. The IASBreceived 225 responses from acrossAfrica, Asia, Europe and North America,identifying various factors that havecontributed to what is commonlyperceived to be a disclosure overloadproblem. The highlights included:• over 80 per cent of respondentsagreed that improvements could bemade to the way financial informationis disclosed

• most preparers of financial statementsidentified the primary problem asdisclosure requirements being tooextensive with not enough being doneto exclude immaterial information

• concerns that preparers, auditors andregulators are approaching financialreporting as an exercise in compliancerather than as a means ofcommunication.

The full results of the IASB’s survey will bepublished as part of a FeedbackStatement, which will also summarisefeedback received from the DisclosureForum hosted by the IASB in January andhow the IASB intends to respond to thatfeedback.

FEE analysis of combined and carve-out financial statements under IFRS The European Federation of Accountants(FEE) has published a paper entitled‘Combined and Carve-out FinancialStatements – Analysis of CommonPractices’. The paper is intended to enhance the

debate and share common practices onwhat FEE regards as being the highlytechnical and insufficiently exploredsubject matter of combined and carve-outfinancial statements.The paper builds on a 2011 FEE

Discussion Paper ‘Combined FinancialStatements’, reflecting comment lettersthat were received on that paper andadditional research subsequentlyundertaken by FEE. It summarises themost common issues and challengesencountered when preparing combinedand carve-out financial statements incompliance with IFRS as well as the mostcommon practices used to address them.The paper is available on the FEE

website (http://www.fee.be).

EFRAG publishes three Bulletins onthe revision of the IFRS ConceptualFrameworkEFRAG and the national standard-settersof France, Germany, Italy and the UnitedKingdom have announced that they willwork together in partnership to promotediscussion, and to ensure that Europeanviews are influential in the debate on theIFRS Conceptual Framework. In relation tothis objective, they have published thefollowing three Bulletins on this topic:• Prudence – considering the role ofprudence when developing accountingstandards.

• Reliability of financial information– discussing whether the replacementof reliability with faithful representationand the loss of the idea of a trade-offbetween relevance and reliability isappropriate.

• Uncertainty – considering whetheruncertainty is best dealt with solely asa matter of measurement or whetherit should continue to play a role ineither or both the definition of anelement and the recognition criteria.

Comments on the three Bulletins areinvited by 5 July 2013.

12 IFRS News Quarter 2

EFRAG letter on macro hedging The European Financial ReportingAdvisory Group (EFRAG) has submitted aletter to the IASB outlining the results ofits analysis of the impact on macro hedgerelationships of the consequentialamendments proposed by the September2012 Review Draft ‘IFRS 9 General hedgeaccounting’ on existing macro hedgerelationships under IAS 39.The letter highlights a number of

concerns including: • significant uncertainty over whetherexisting IAS 39 compliant portfoliohedge accounting practices willcontinue to be possible under theReview Draft

• the significant risk that entities will berequired to change their IAS 39compliant portfolio hedge accountingpractices twice.

The IASB is currently deliberating itsgeneral hedge accounting projectfollowing comments on the Review Draft.It will address macro hedging separatelylater in the year.

ESMA publishes enforcementdecisionsThe European Securities and MarketsAuthority (ESMA) has published a freshbatch of extracts from its confidentialdatabase of enforcement decisions takenby European national enforcers.The publication of these decisions is

designed to inform market participantsabout European national enforcers’ views

on whether various accounting practicesare in accordance with IFRS (as adoptedin the European Union). ESMA considersthat the publication of these decisions,together with the rationale behind them,will contribute to a consistent applicationof IFRS in the European Union.Topics covered in the latest batch of

extracts, thirteenth in the series, include:

Standard Topic

• recognition of financial expense on financial

liabilities measured at amortised cost

• intangible assets with indefinite useful life

• presentation of revenue and expenses related

to service concession arrangements

• value in use calculation

• assessment of materiality of an error

• related party disclosures in interim financial

statements

• definition of a business

• disclosures related to fair value of financial

instruments

• discount rate in value in use calculation

• residual value of property

Standard

IAS 39 ‘Financial Instruments: Recognition and

Measurement’

IAS 38 ‘Intangible Assets’

IFRIC 12 ‘Service Concession Arrangements’

IAS 36 ‘Impairment of Assets’

IAS 8 ‘Accounting Policies, Changes in Accounting

Estimates and Errors’ and IAS 40 ‘Investment

Property’

IAS 24 ‘Related Party Disclosures’ and IAS 34

‘Interim Financial Reporting’

IFRS 3 ‘Business Combinations’

IFRS 7 ‘Financial Instruments: Disclosures’ and

IAS 39 ‘Financial Instruments: Recognition and

Measurement’

IAS 36 ‘Impairment of Assets’

IAS 16 ‘Property, Plant and Equipment’

UK issues its version of the IFRS forSMEsThe UK’s Financial Reporting Council hasissued FRS 102 ‘The Financial ReportingStandard applicable in the UK andRepublic of Ireland’ providing succinctaccounting and reporting requirements forunlisted entities in the UK.The requirements in FRS 102 are

based on the IASB’s International FinancialReporting Standard for Small and Medium-sized Entities (IFRS for SMEs) but withsignificant alterations based on feedbackreceived during the UK’s consultationprocess. Most notably the UK hasamended the IFRS for SMEs to includeaccounting options in current FRS andpermitted by IFRS, but not included in theIFRS for SMEs. For example, the ability torevalue property, plant and equipment.The UK has also modified the IFRS forSMEs in terms of the scope of entitieseligible to apply it.The Standard will be effective from

1 January 2015, but may be adoptedearly for accounting periods ending on or after 31 December 2012.

Korea reports on its move to IFRSThe Korean Accounting Standards Board(KASB) has released a report on thelessons learned from the country’sadoption of IFRS (listed companies inKorea have been required to use IFRSsince 2011). The report outlines thebackground to Korea’s adoption of IFRS,the steps it undertook in preparation forand during the transition to IFRS, andrecommendations for countries andcompanies considering the move to IFRS.

International Integrated ReportingCouncil (IIRC)On 16 April the IIRC published aconsultation draft of an InternationalFramework for Integrated Reporting. TheIIRC is a coalition of regulators, investors,companies, standard setters, theaccounting profession and non-governmental organisations. The goal ofintegrated reporting is to providestakeholders with a concisecommunication about how anorganisation’s strategy, governance,performance and prospects lead to thecreation of value over the short, mediumand long term. The draft frameworkproposes various guiding principles as tothe content of an integrated report andhow information is presented. Such reportswould complement rather than replacemore established forms of corporatereporting, including financial statements,and would include elements of:

• organisational overview and externalenvironment

• governance• opportunities and risks• strategy and resource allocation• business model• performance• future outlook.

The IIRC and IASB recently haveformalised an agreement for the twoorganisations to deepen their cooperationon the IIRC’s work to develop anintegrated corporate reportingframework. Grant Thornton has supportedthis work in various ways includingparticipating in the IIRC’s pilotprogramme.The consultation draft can obtained at

www.theiirc.org and is open forcomment until 15 July 2013.

IFRS News Quarter 2 13

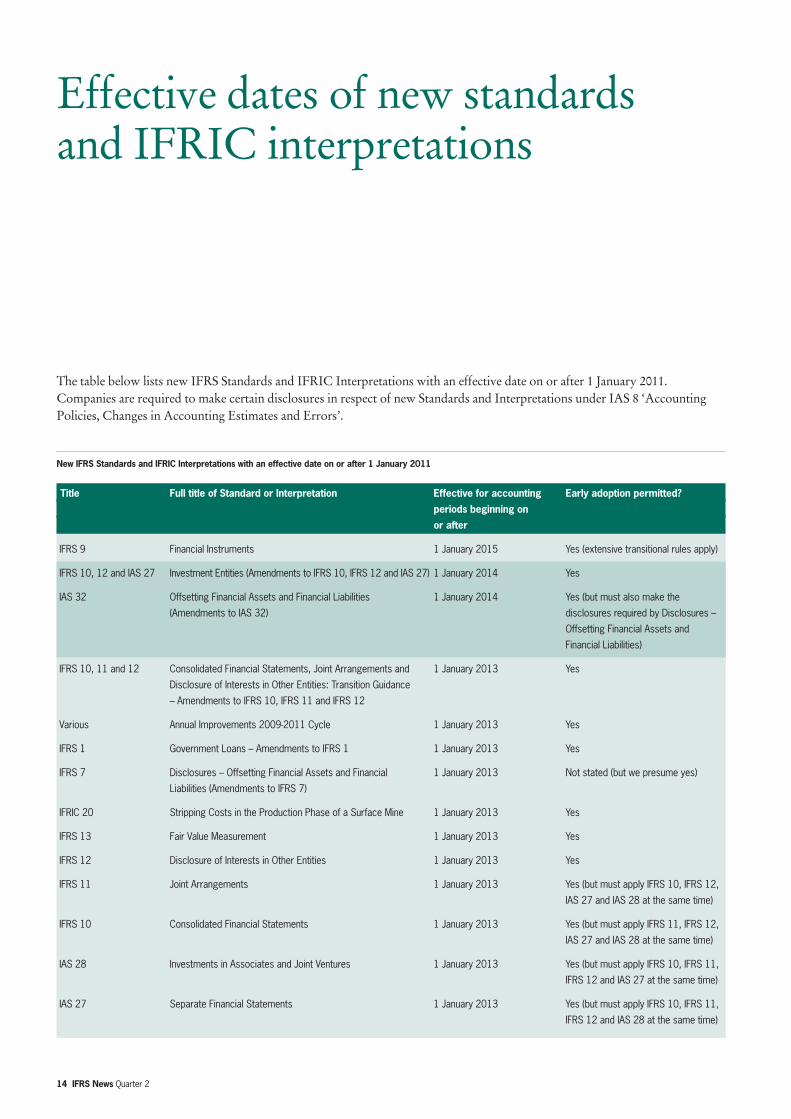

The table below lists new IFRS Standards and IFRIC Interpretations with an effective date on or after 1 January 2011.Companies are required to make certain disclosures in respect of new Standards and Interpretations under IAS 8 ‘AccountingPolicies, Changes in Accounting Estimates and Errors’.

Effective dates of new standards and IFRIC interpretations

New IFRS Standards and IFRIC Interpretations with an effective date on or after 1 January 2011

Title Full title of Standard or Interpretation Effective for accounting Early adoption permitted?

periods beginning on

or after

IFRS 9 Financial Instruments 1 January 2015 Yes (extensive transitional rules apply)

IFRS 10, 12 and IAS 27 Investment Entities (Amendments to IFRS 10, IFRS 12 and IAS 27) 1 January 2014 Yes

IAS 32 Offsetting Financial Assets and Financial Liabilities 1 January 2014 Yes (but must also make the

(Amendments to IAS 32) disclosures required by Disclosures –

Offsetting Financial Assets and

Financial Liabilities)

IFRS 10, 11 and 12 Consolidated Financial Statements, Joint Arrangements and 1 January 2013 Yes

Disclosure of Interests in Other Entities: Transition Guidance

– Amendments to IFRS 10, IFRS 11 and IFRS 12

Various Annual Improvements 2009-2011 Cycle 1 January 2013 Yes

IFRS 1 Government Loans – Amendments to IFRS 1 1 January 2013 Yes

IFRS 7 Disclosures – Offsetting Financial Assets and Financial 1 January 2013 Not stated (but we presume yes)

Liabilities (Amendments to IFRS 7)

IFRIC 20 Stripping Costs in the Production Phase of a Surface Mine 1 January 2013 Yes

IFRS 13 Fair Value Measurement 1 January 2013 Yes

IFRS 12 Disclosure of Interests in Other Entities 1 January 2013 Yes

IFRS 11 Joint Arrangements 1 January 2013 Yes (but must apply IFRS 10, IFRS 12,

IAS 27 and IAS 28 at the same time)

IFRS 10 Consolidated Financial Statements 1 January 2013 Yes (but must apply IFRS 11, IFRS 12,

IAS 27 and IAS 28 at the same time)

IAS 28 Investments in Associates and Joint Ventures 1 January 2013 Yes (but must apply IFRS 10, IFRS 11,

IFRS 12 and IAS 27 at the same time)

IAS 27 Separate Financial Statements 1 January 2013 Yes (but must apply IFRS 10, IFRS 11,

IFRS 12 and IAS 28 at the same time)

14 IFRS News Quarter 2

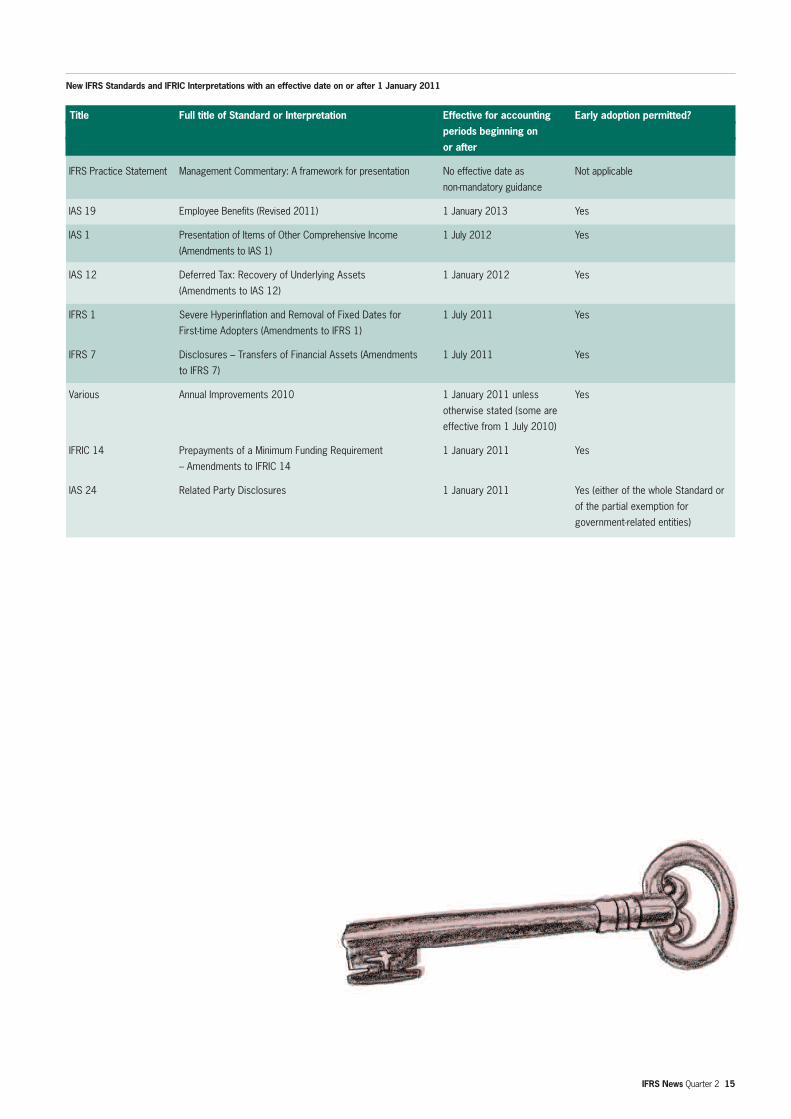

New IFRS Standards and IFRIC Interpretations with an effective date on or after 1 January 2011

Title Full title of Standard or Interpretation Effective for accounting Early adoption permitted?

periods beginning on

or after

IFRS Practice Statement Management Commentary: A framework for presentation No effective date as Not applicable

non-mandatory guidance

IAS 19 Employee Benefits (Revised 2011) 1 January 2013 Yes

IAS 1 Presentation of Items of Other Comprehensive Income 1 July 2012 Yes

(Amendments to IAS 1)

IAS 12 Deferred Tax: Recovery of Underlying Assets 1 January 2012 Yes

(Amendments to IAS 12)

IFRS 1 Severe Hyperinflation and Removal of Fixed Dates for 1 July 2011 Yes

First-time Adopters (Amendments to IFRS 1)

IFRS 7 Disclosures – Transfers of Financial Assets (Amendments 1 July 2011 Yes

to IFRS 7)

Various Annual Improvements 2010 1 January 2011 unless Yes

otherwise stated (some are

effective from 1 July 2010)

IFRIC 14 Prepayments of a Minimum Funding Requirement 1 January 2011 Yes

– Amendments to IFRIC 14

IAS 24 Related Party Disclosures 1 January 2011 Yes (either of the whole Standard or

of the partial exemption for

government-related entities)

IFRS News Quarter 2 15

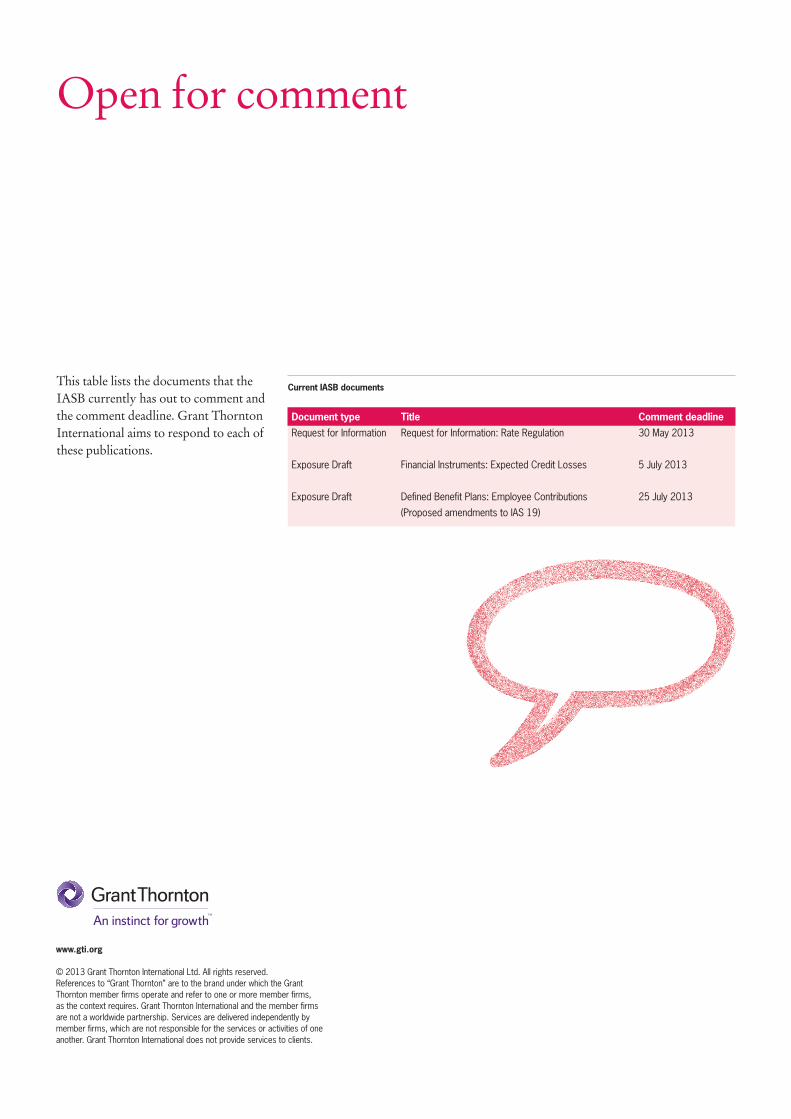

This table lists the documents that theIASB currently has out to comment andthe comment deadline. Grant ThorntonInternational aims to respond to each ofthese publications.

Open for comment

www.gti.org

© 2013 Grant Thornton International Ltd. All rights reserved.References to “Grant Thornton” are to the brand under which the GrantThornton member firms operate and refer to one or more member firms, as the context requires. Grant Thornton International and the member firmsare not a worldwide partnership. Services are delivered independently bymember firms, which are not responsible for the services or activities of oneanother. Grant Thornton International does not provide services to clients.

Current IASB documents

Document type Title Comment deadline

Request for Information Request for Information: Rate Regulation 30 May 2013

Exposure Draft Financial Instruments: Expected Credit Losses 5 July 2013

Exposure Draft Defined Benefit Plans: Employee Contributions 25 July 2013

(Proposed amendments to IAS 19)