Download - HPC Computing Trends

Intersect360 Research in 2017

10 year history of HPC analyst business

Covering “high performance data center” markets, including traditional HPC and supercomputing, high-performance enterprise,

cloud, big data, and hyperscale

New hyperscale advisory service

Weekly podcast, “This Week in HPC”

Contributing editors to The Next Platform, market research partners of TOP500.org, media partnerships with HPCwire, insideHPC

Sponsors of HPC Advisory Council

Key Topics from Yesterday

• Architecture specialization

• HPC in the Cloud

• HPC vs. Hyperscale

• Machine learning and AI

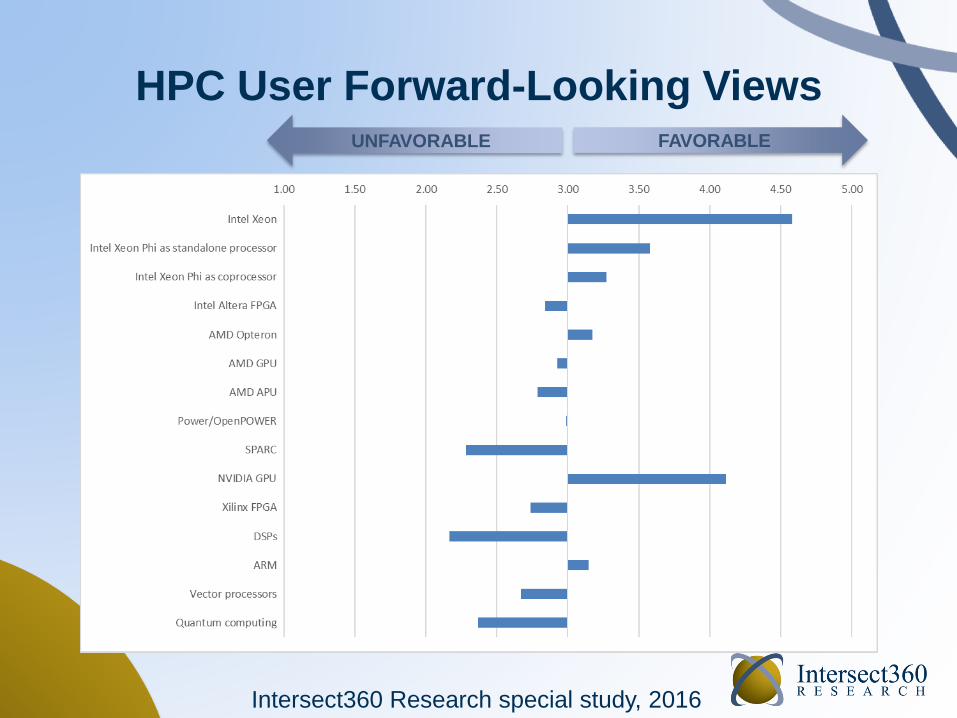

HPC User Forward-Looking ViewsFAVORABLEUNFAVORABLE

Intersect360 Research special study, 2016

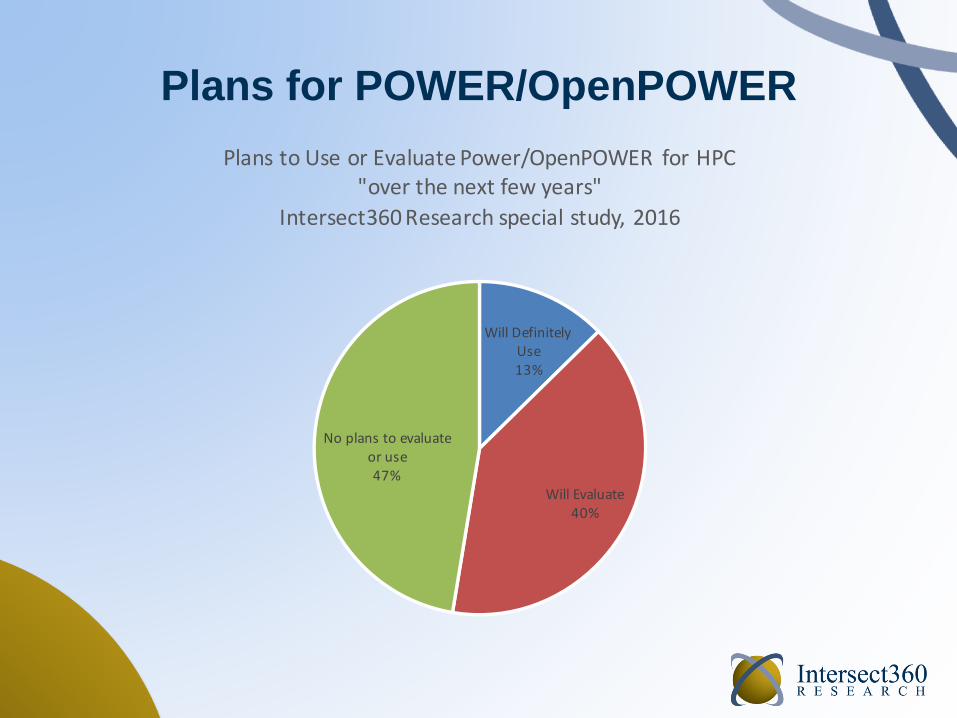

Plans for POWER/OpenPOWER

WillDefinitelyUse13%

WillEvaluate40%

Noplanstoevaluateoruse47%

PlanstoUseorEvaluatePower/OpenPOWERforHPC"overthenextfewyears"

Intersect360Researchspecialstudy,2016

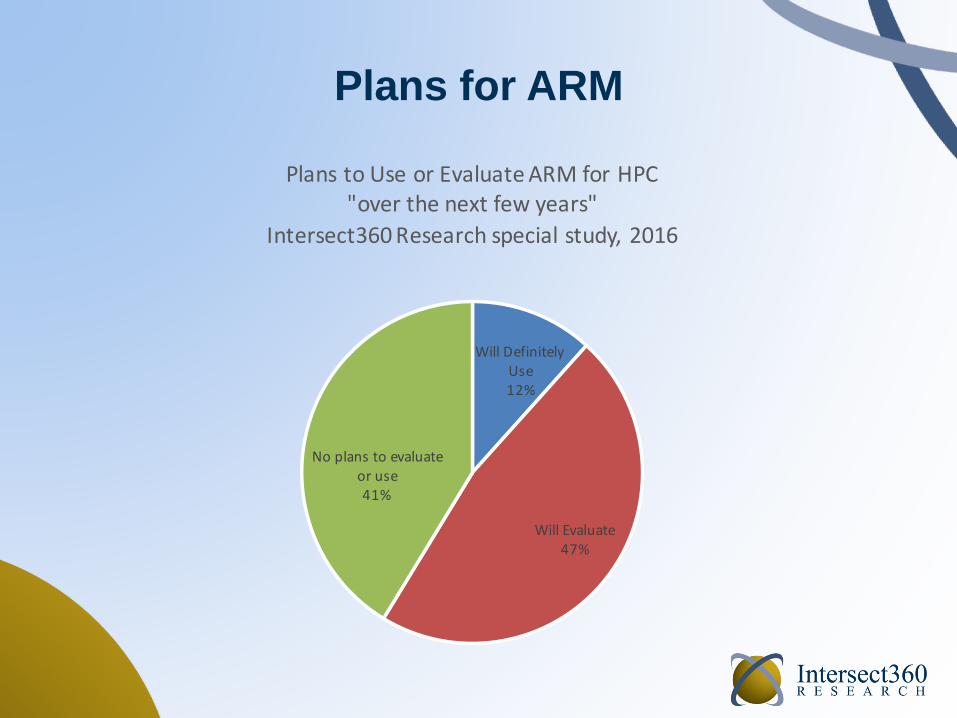

Plans for ARM

WillDefinitelyUse12%

WillEvaluate47%

Noplanstoevaluateoruse41%

PlanstoUseorEvaluateARMforHPC"overthenextfewyears"

Intersect360Researchspecialstudy,2016

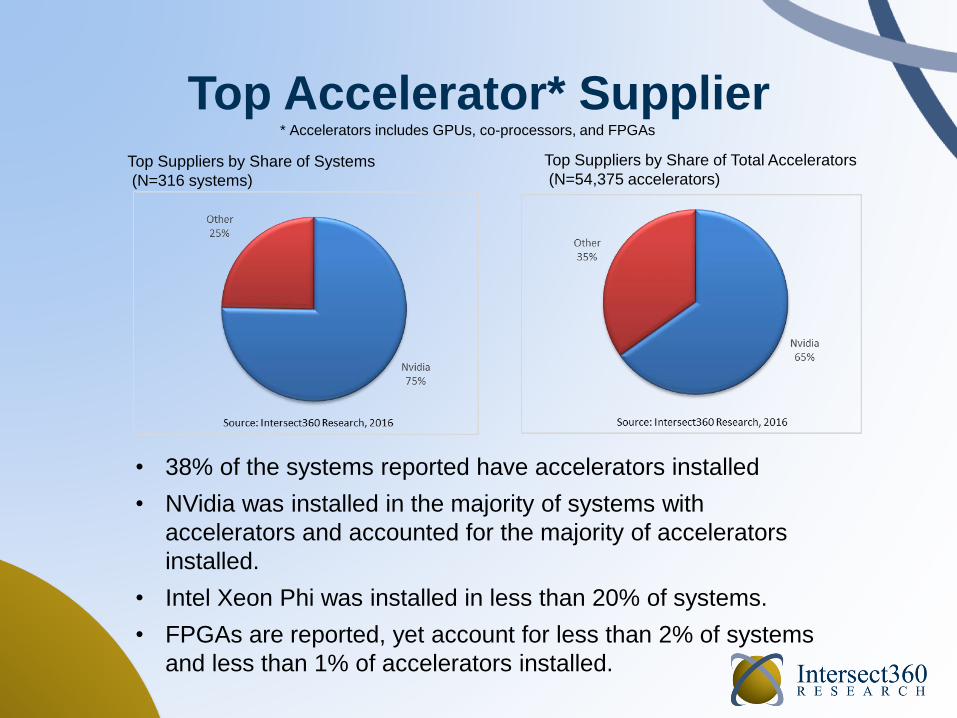

Top Accelerator* Supplier

• 38% of the systems reported have accelerators installed

• NVidia was installed in the majority of systems with

accelerators and accounted for the majority of accelerators

installed.

• Intel Xeon Phi was installed in less than 20% of systems.

• FPGAs are reported, yet account for less than 2% of systems

and less than 1% of accelerators installed.

Top Suppliers by Share of Systems

(N=316 systems)

Top Suppliers by Share of Total Accelerators

(N=54,375 accelerators)

* Accelerators includes GPUs, co-processors, and FPGAs

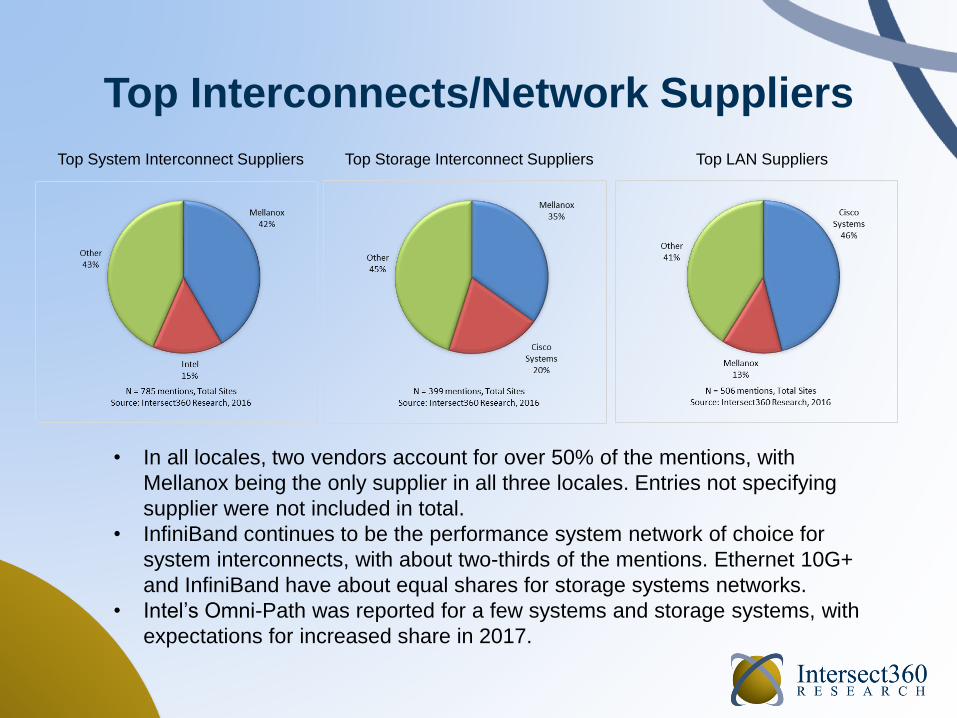

Top Interconnects/Network Suppliers

• In all locales, two vendors account for over 50% of the mentions, with

Mellanox being the only supplier in all three locales. Entries not specifying

supplier were not included in total.

• InfiniBand continues to be the performance system network of choice for

system interconnects, with about two-thirds of the mentions. Ethernet 10G+

and InfiniBand have about equal shares for storage systems networks.

• Intel’s Omni-Path was reported for a few systems and storage systems, with

expectations for increased share in 2017.

Top System Interconnect Suppliers Top Storage Interconnect Suppliers Top LAN Suppliers

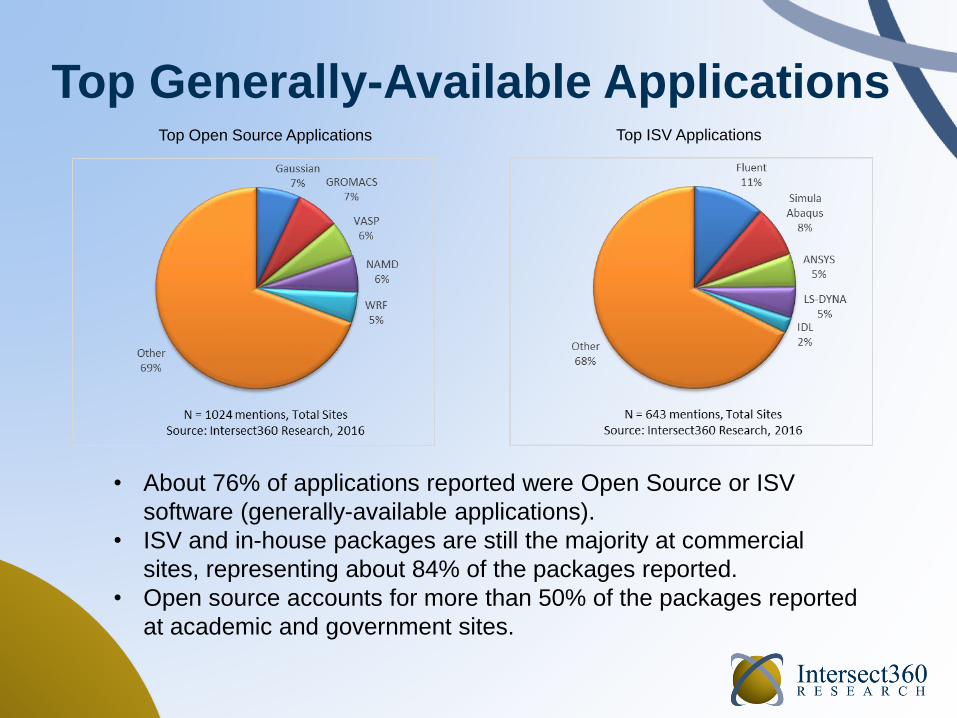

• About 76% of applications reported were Open Source or ISV

software (generally-available applications).

• ISV and in-house packages are still the majority at commercial

sites, representing about 84% of the packages reported.

• Open source accounts for more than 50% of the packages reported

at academic and government sites.

Top Generally-Available ApplicationsTop Open Source Applications Top ISV Applications

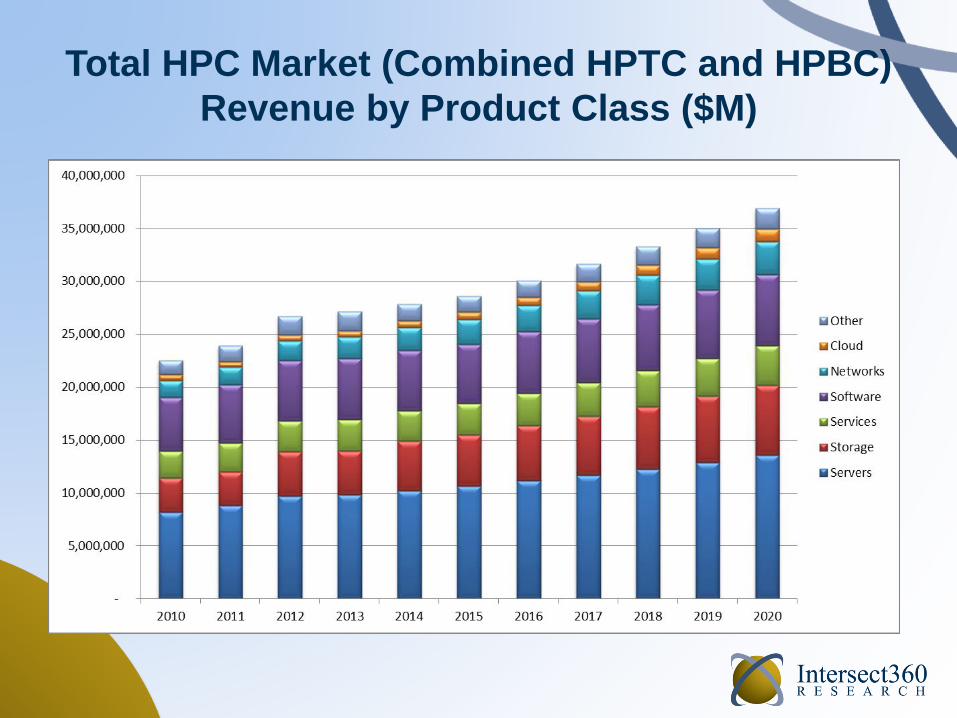

Total HPC Market (Combined HPTC and HPBC)

Revenue by Product Class ($M)

The Hyperscale Market

• Included since our 2007 HPC methodology as

“ultrascale internet”

• In 2015, recognized “Hyperscale” as distinct

market in proximity to HPC; began process of

separating it from HPC

• Defined hyperscale methodology with market

research and feedback from interested clients

• Published definitions and methodology report in

April 2016

Hyperscale Market Definition

The hyperscale market consists of arbitrarily scalable, web-facing application infrastructure that is distinct from general IT investment

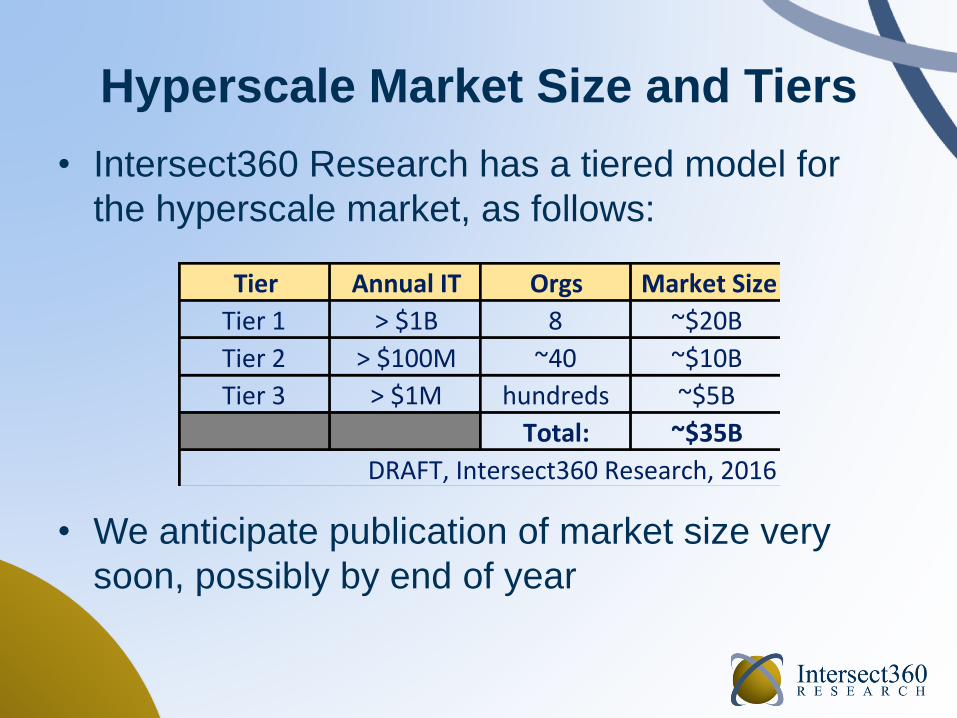

Hyperscale Market Size and Tiers

• Intersect360 Research has a tiered model for

the hyperscale market, as follows:

Tier AnnualIT Orgs MarketSize

Tier1 >$1B 8 ~$20B

Tier2 >$100M ~40 ~$10B

Tier3 >$1M hundreds ~$5B

Total: ~$35B

DRAFT,Intersect360Research,2016

• We anticipate publication of market size very

soon, possibly by end of year

Deep Learning

• Intersect360 Research tracks AI (including deep

learning, machine learning, cognitive computing,

etc.) as part of the hyperscale market

– Similar to but distinct from HPC

– Low precision, intensely parallel, strong affinity to

public cloud

• DL is not a vertical market. It is more akin to an

algorithm or method of computation, like an FFT

• Cloud providers and end users are in early

stages of investment for their applications

Sizing Deep Learning

• We have looked at the size of the deep learning

market opportunity from several angles:

– Supplier-side information on market expansion

– Demand-side market analysis on acquisitions

– Top-down analysis of the hyperscale market

– Analyst opinion

• Our independent methods have produced

consistent views of the current opportunity in

deep learning

Deep Learning Size and Growth

• According to our analysis, the deep learning

market opportunity is $2.0B to $2.5B for 2016

– Represents about 6.5% of the hyperscale market

– This is a pre-publication figure

• We expect growth rate to be very high for the

next two years, 2017-18, close to 100% Y/Y

• After that, growth will moderate, and possibly

even contract by end of five-year period

The Next Ten Years in HPC

(Write These Down; Grade Me in 2027)

1. Fundamental drivers of HPC remain strong. Forever.

2. Specialization proliferates again. Custom architectures will

reemerge in the market.

3. Public cloud (utility) remains well below 10% of the HPC market

through the next 10 years.

4. Object storage will take off in commercial markets.

5. The hyperscale market will have a tremendous effect:

– Consuming HPC-associated technologies like GPU, InfiniBand

– Defining system configurations and product specifications

– Influencing software and middleware

– Introducing new revolutionary applications based on AI

(including deep learning) and augmented reality. These are

hyperscale applications that will predominant be run on cloud-

based resources.