Download - Healthcare Vertical Integration and Internal Audit’s Role in Strategic Transactions September 2014

Healthcare Vertical Integration and Internal Audit’s Role in Strategic Transactions

September 2014

Page 2

Agenda

I. Healthcare vertical integration

II. Internal Audit’s role in strategic transactions

Page 3

Health industry integration is not black or whiteShades of collaboration exist, although the trend is strongly to the right

Source: www.accountablecarefacts.org

Single MDs; small

groups; single

hospitals

Independent physician

associations, single specialty

groups, hospital chains

Hospital staffs (primary care

physicians employed by

hospitals), some university/faculty

practices

Multispecialty group practices (primary care-

based practices with full

complement of specialty services)

Clinically integrated

delivery systems (multispecialty

groups with hospitals)

Clinically and financially integrated systems

(multispecialty medical groups integrated with hospitals and health plans)

Less integrated or organized systems More integrated or organized systems

Horizontal Vertical

Most ACOs are formed in this space

Page 4

Vertical integration has three primary objectivesPayers and health systems are increasingly willing to accept non-traditional risks to preserve their positions in the healthcare supply chain

Objective Acquirer Target Benefit Risk

1. Strengthen revenue streams

Health System

Physicians Increase referrals and admissions

Provider productivity decline post acquisition, inability to influence physician decisions

Health System

Payer Increase patient volume and reimbursement rates through a restricted network and reduction in payer margin

Financial losses due to under-estimation of member utilization and unit cost

Payer Health System Capture enrollment through health system regional presence and brand

Acquire disproportionately high-cost members due to health system loyalty

2. Improve control of supply costs

Payer Health System,Physicians

Improve ability to manage population health and control medical expense

Capital-intensive investment erodes financial viability and flexibility without improving health cost management

3. Defend against disintermediation or exclusion

Payer Health System Guard against integrated delivery systems contracting directly with employers or government payers as ACOs

Lose network breadth due to reluctance of providers to participate in network of a direct competitor

Health System

Payer Offset potential exclusion from narrow networks

Lose overall managed care volume due to commercial payers unwilling to contract with a direct competitor

Health System

Physicians Avoid disproportionate admissions to competing health systems

Physician unwillingness to modify referral or admission practices

Page 5

Integration activity has come in wavesBeginning in the 1980s, a surge in managed care growth fueled health industry integration, both horizontal and vertical

ElementTrends

1980 – 2000sObservations

Payers- Managed care organizations grew membership and

implemented cost control techniques- Payers consolidated

- Large managed care organizations used their leverage to negotiate lower cost provider contracts

Health Systems- Hospital networks, such as HCA, began to expand by

acquiring other hospitals- Hospitals began to form managed care networks- Health systems formed health plans

- Larger health systems struggled to create economies of scale or reduce cost

- Provider-sponsored health plans initially generated large cash flow; however, months/years later struggled with growth and survival

Physicians

- Physicians tended to operate independently from each other

- Hospitals experimented with employing physicians - Physician groups experimented with starting health

plans

- Care coordination hampered by a lack of communication channels and incentives

- Hospital-physician organizations and physician group-owned HMOs disintegrated over time due to poor management and diverging interests

Reform- No economic or political forces driving for lowering

the cost of care- Expected Clinton-era reforms failed to become a reality

- Providers were not externally incentivized to coordinate care. Revenue could still be driven through volume.

Reimbursement- Fee for service (FFS) reimbursement was the industry

standard

- FFS created an environment where providers and payers existed with inherent, opposing interests

- Providers were not incentivized to reduce the cost of care

Page 6

Vertical integration failure is commonWhile the benefits of integration are appealing, realization has been a challenge for most organizations

1945: Permanente Health Plan (later named Kaiser) opens to the public, providing both health coverage and access to hospitals

20101965

Rise of managed care organizations and new reimbursement methodologies (e.g., DRGs, per diems, case rates, carve outs)

1992: Humana spins off 77 hospitals as Galen Health

Care to focus exclusively on insurance

1972: Humana shifts focus from nursing homes to hospitals, eventually acquiring

77 facilities

Traditional fee for service dominated the market

1947: Group Health Cooperative opens in Seattle Washington as a PSHP

1980: Geisenger Medical Center starts the Geisenger Health

System (a PSHP)

1969: Harvard Community Health Plan opens as a PSHP

2013: Kaiser sells Ohio health plan to

Catholic Health Partners (Health

Innovations Ohio)

2014: North Shore LIJ opens CareConnect

2014: Piedmont Healthcare and Wellstar

Health System start Piedmont Wellstar Plan

2000: Rush University Medical Center sells

Anchor HMO to WellPoint

1971: Rush Univ. Medical Center opens Anchor HMO

1980 1995

1998: UPMC launches UPMC Health Plan

1984: Sentara opens Optima HMO Health

Plan

Passage of the Affordable Care Act

1983: Intermountain Healthcare creates SelectHealth, a non-profit health plan

2002: Piedmont separates from Promina Health, exiting the health plan market

1994: Promina Health founded by Piedmont

Healthcare

2012: Sutter Health

launches Sutter Health Plus

2001: UniHealth divests its

medical and insurance practices

1993: Sutter Health opens

Omni Healthcare Plan

1999: Sutter Health sells Omni Healthcare

to BCBSCA

1986: HealthWest (later UniHealth)

launches CareAmerica

2011: Highmark acquires West Penn Allegheny

Health System

2011: Humana acquires 300 clinic Concentra

Health

2011: UnitedHealth Group acquires 2,300

physician Monarch Healthcare

1990: Cigna acquires majority ownership of Lovelace Health Systems

2002: Cigna sells Lovelace to Ardent Health Services

1998: AHERF files

for bankruptcy

1986: Allegheny Health, Education, and

Research Foundation (AHERF) begins

integration efforts, purchasing physician

organizations and hospitals

Page 7

Strategic, Financial

and Operational

Risk

Vertical integration is fraught with riskEndeavors have failed for myriad reasons, but at the core is typically an under-estimation of the risks to be managed

Limiting financial wherewithal by taking on too much at once

Inadequate physician alignment,

particularly within primary care

Paying for productivity gains that do not align with the acquired entity’s new incentives

Inability to effectively

coordinate care across the

integrated delivery system

Insufficient capability to execute core new functions (e.g., pricing, reserving, practice management)

Not clearly defining each entity’s role within the system

Developing organizational

capabilities too far in advance of

market demand

Optimistic assumptions regarding willingness of business partners to make concessions

Page 8

ElementTrends

2010-2014Observations

Payers

- Slower membership growth due to escalating premiums- Reduced ability to limit risk through underwriting; forced

to manage risk once “in house” - New regulations and taxes negatively impact profitability - Selective vertical integration through medical group or

facility acquisition, or partnerships with health systems

- Pressured to effectively manage medical expense- Working towards ACO-like payment methodologies

(rewarding quality and care coordination)- Increasing member engagement

Health Systems

- Renewed focused on acquisition/merger activity to increase scale

- Rapid EHR adoption driven by financial and care coordination incentives

- Payments increasingly tied to quality metrics- Increasing acceptance of risk through ACOs

- Positioning for inclusion in narrow payer networks and alternative contract arrangements

- Focused on clinical/operational excellence - Patient demand for price transparency - Technological advancement opening new

communication channels for providers and patients

Physicians

- Rapid movement towards health system employment- Physician group consolidation- Primary care shortage - Broader acceptance of evidence-based medicine,

standards of practice and clinical pathways

- Improved ability to coordinate care and control costs

- Gradual movement towards transparency of outcomes

Reform

- ACO and patient centered medical home development- Health Insurance Exchanges provide new forum for

individual and small group market competition- Increasing public acceptance of cost control techniques

(e.g., narrow networks, Medicare Shared Savings Services Program)

- Health Insurance Exchanges increasing patient volume will likely challenge primary care capacity

- Quality programs are necessary core capabilities - Transparency in quality measurements is increasing

consumer driven health care

Reimbursement- Value-based reimbursement models- Shared reward systems (e.g., MSSP)- Compliance contingent reimbursement (Meaningful Use,

Medicare STARS Program)

- Increased provider risk acceptance - Payer and provider incentive alignment- Risk-based payer revenue

The next wave is upon usRegulatory and market changes are prompting both defensive and opportunistic integration moves

Page 9

Integration is being initiated from all directionsHealth systems and payers are both testing new positions along the supply chain

► Provider sponsored health plans– Sutter Health Plus (Sutter Health)– CareConnect (North Shore Long Island Jewish)– Piedmont Wellstar Health Plans (Piedmont and Wellstar Health Systems)

► Health plan hospital/provider acquisitions– West Penn Allegheny (Highmark)– Concentra clinics (Humana)– Diagnostic Clinic Medical Group (Florida Blue)

► Accountable Care Organizations (ACOs)– More than 500 Medicare and Commercial ACOs have formed since 2010– Most are hospital or health system led– More than 10 million members are enrolled in commercial ACOs– Major, national health insurers have announced intentions to significantly

increase their volume of ACO contracts

Page 10

Where to begin?Avoiding the mistakes of the past begins with an assessment of the factors that drive success and failure

Gate 1

Objectives and risk identification

► Clarify strategic intent and desired competitive position within market context

► Identify licensure requirements

► Perform high-level capability analysis– Patient services

and network coverage

– Financial risk management

– Payer or provider operations

► Identify risks and potential mitigation actions

Gate 2

Capability assessment

► Identify the core capabilities required to effectively manage population health to create a positive return on investment

► Determine the level of capability maturity needed to successfully compete in the targeted market

► Identify the capability gaps to be addressed before launching new product or services

Gate 3

Build versus buy analysis

► Evaluate the feasibility and level of effort required to develop required capabilities in house

► Assess the opportunity and associated risks of partnership arrangements

► Determine the costs and advantages of acquiring existing capability providers

► Conduct initial due diligence on acquisition targets

► Develop a recommended approach to obtaining each capability

Gate 4

Business case development

► Determine availability and cost of capital

► Determine start up costs, to include capability investments, capital requirements, talent acquisition and marketing

► Forecast cash inflows driven by patient and premium revenue and investment income

► Estimate cash outflows based on the timing and magnitude of claims payments, operating expenses, interest payments and taxes

► Determine NPV and/or ROI of the health plan investment

Page 11

Agenda

I. Healthcare vertical integration

II. Internal Audit’s role in strategic transactions

Page 12

Background

Strategic transactions like mergers and acquisitions (M&A) and divestitures remain some of the most risk-heavy initiatives that any organization can undertake.

The proactive involvement of Internal Audit (IA) before, during and after the merger, acquisition or divestiture can help management identify issues and opportunities related to the transaction that might not otherwise be addressed.

Acting as an advisor to the program management team, IA is ideally positioned to assess and monitor program management activities, review controls and provide key insights while maintaining independence and objectivity.

Page 13

How IA can help during strategic transactions

► Provide increased visibility into key risks related to strategic transaction changes (e.g., Finance, IT, HR, Operational risks)

► Reinforce that risks and controls are the responsibility of management

► Identify gaps in the integration or separation project management plan

► Suggest opportunities for synergies that would boost the acquisition’s return on investment (ROI) or actions to increase separation-related cost savings

► Highlight the impact that the acquisition and its integration, or the divestiture, may have on other parts of the business

► Identify potential gaps in the internal control structure

► Support management’s prioritization of transition and organizational readiness risks

Page 14

Role of IA during M&A

► There are four key areas where IA can play a crucial role in an organization’s M&A lifecycle:

Throughout the M&A process, IA should form a part of the program

management team so that it can assess and monitor activities and

provide key insights. IA can also audit program management activities

to highlight process gaps and areas of future improvements.

Page 15

Role of IA during M&A: Strategy

Page 16

Role of IA during M&A: Due diligence

Page 17

Role of IA during M&A: Deal approval and close

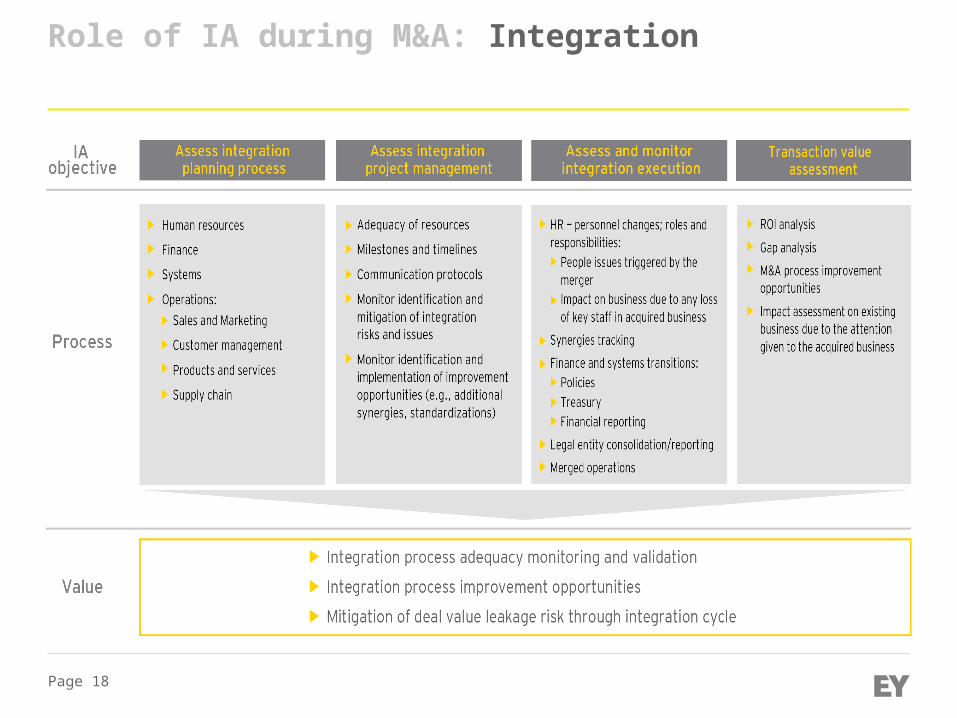

Page 18

Role of IA during M&A: Integration

Page 19

The role of IA during divestitures

► There are four key areas where IA can play a role in the divestiture lifecycle:

Leading practice calls for IA to be embedded as part of the program

management team and be involved throughout the divestiture life cycle.

Page 20

The role of IA during divestitures: Strategy

Page 21

The role of IA during divestitures: Due diligence

Page 22

The role of IA during divestitures: Deal approval and close

Page 23

The role of IA during divestitures: Separation

Page 24

Key benefits

IA provides a critical perspective to strategic transaction deals that many executives may not consider. Without that perspective — right from the start — the organization could find out far too late that the price was not right, or that it has to spend a significant amount of money to fix issues that IA could have identified and helped the organization avoid

► Strategically, IA can determine an organization’s readiness for the transaction

► During due diligence, IA can alert the organization to potential risk, control or regulatory issues that would cause the organization to overpay or undervalue

► Prior to deal close, IA can help prevent deal value leakage

► Post-transaction, IA’s involvement can lead to organizational efficiencies and strengthened control monitoring

Page 25

For further information

► See the full “Internal Audit’s role during the strategic transactions life cycle” report

► For further GRC thought leadership, please refer to our Insights on governance, risk and compliance series on:www.ey.com/GRCinsights

► Please contact:► Sean Lueck, EY Healthcare Advisory (904-505-6572)► Wally Ward, EY Healthcare Advisory (704-331-1907)