Download - Corporate Presentation - September 2016

1

TSX: GCMOTC: TPRFFSeptember 2016

The leading high‐grade gold producer in Colombia

Corporate PresentationSeptember 2016

2

TSX: GCMOTC: TPRFFSeptember 2016

Forward‐Looking Statements DISCLAIMER

This presentation contains "forward‐looking information", which may include, but is not limited to, statements withrespect to the future financial or operating performance of the Company and its projects, and, specifically, statementsconcerning anticipated growth in annual gold production, reduction of cash costs and AISC, future G&A, capex andexcess cash flow, interest payments on the senior debt and future purchases and/or redemptions of the senior debt.Often, but not always, forward‐looking statements can be identified by the use of words such as "plans", "expects","is expected", "budget", "scheduled", "estimates", "forecasts", "intends", "anticipates", or "believes" or variations(including negative variations) of such words and phrases, or state that certain actions, events or results "may","could", "would", "might" or "will" be taken, occur or be achieved. Forward‐looking statements involve known andunknown risks, uncertainties and other factors which may cause the actual results, performance or achievements ofGran Colombia to be materially different from any future results, performance or achievements expressed or impliedby the forward‐looking statements. Factors that could cause actual results to differ materially from those anticipatedin these forward‐looking statements are described under the caption "Risk Factors" in the Company's AnnualInformation Form dated as of March 30, 2016 which is available for view on SEDAR at www.sedar.com. Forward‐looking statements contained herein are made as of the date of this presentation and Gran Colombia disclaims, otherthan as required by law, any obligation to update any forward‐looking statements whether as a result of newinformation, results, future events, circumstances, or if management's estimates or opinions should change, orotherwise. There can be no assurance that forward‐looking statements will prove to be accurate, as actual resultsand future events could differ materially from those anticipated in such statements. Accordingly, the reader iscautioned not to place undue reliance on forward‐looking statements.

3

TSX: GCMOTC: TPRFFSeptember 2016

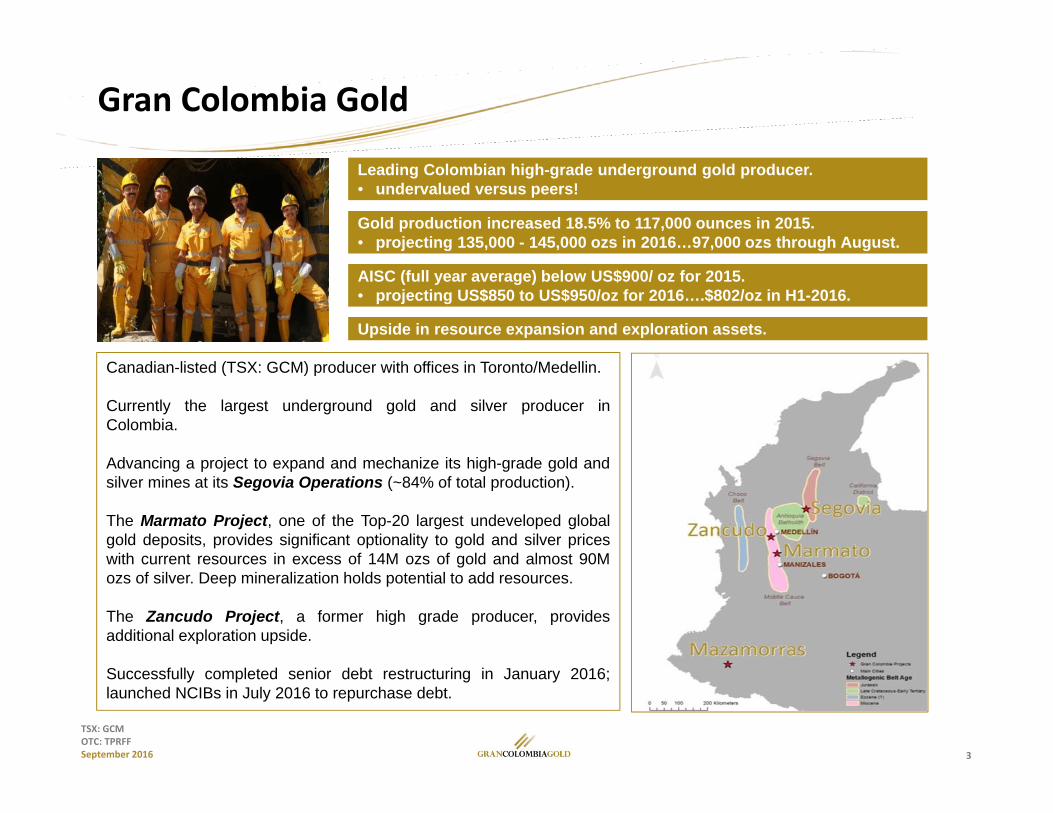

Canadian-listed (TSX: GCM) producer with offices in Toronto/Medellin.

Currently the largest underground gold and silver producer inColombia.

Advancing a project to expand and mechanize its high-grade gold andsilver mines at its Segovia Operations (~84% of total production).

The Marmato Project, one of the Top-20 largest undeveloped globalgold deposits, provides significant optionality to gold and silver priceswith current resources in excess of 14M ozs of gold and almost 90Mozs of silver. Deep mineralization holds potential to add resources.

The Zancudo Project, a former high grade producer, providesadditional exploration upside.

Successfully completed senior debt restructuring in January 2016;launched NCIBs in July 2016 to repurchase debt.

Gold production increased 18.5% to 117,000 ounces in 2015.• projecting 135,000 - 145,000 ozs in 2016…97,000 ozs through August.

AISC (full year average) below US$900/ oz for 2015.• projecting US$850 to US$950/oz for 2016….$802/oz in H1-2016.

Upside in resource expansion and exploration assets.

Leading Colombian high-grade underground gold producer. • undervalued versus peers!

Gran Colombia Gold

4

TSX: GCMOTC: TPRFFSeptember 2016

SEGOVIA OPERATIONS

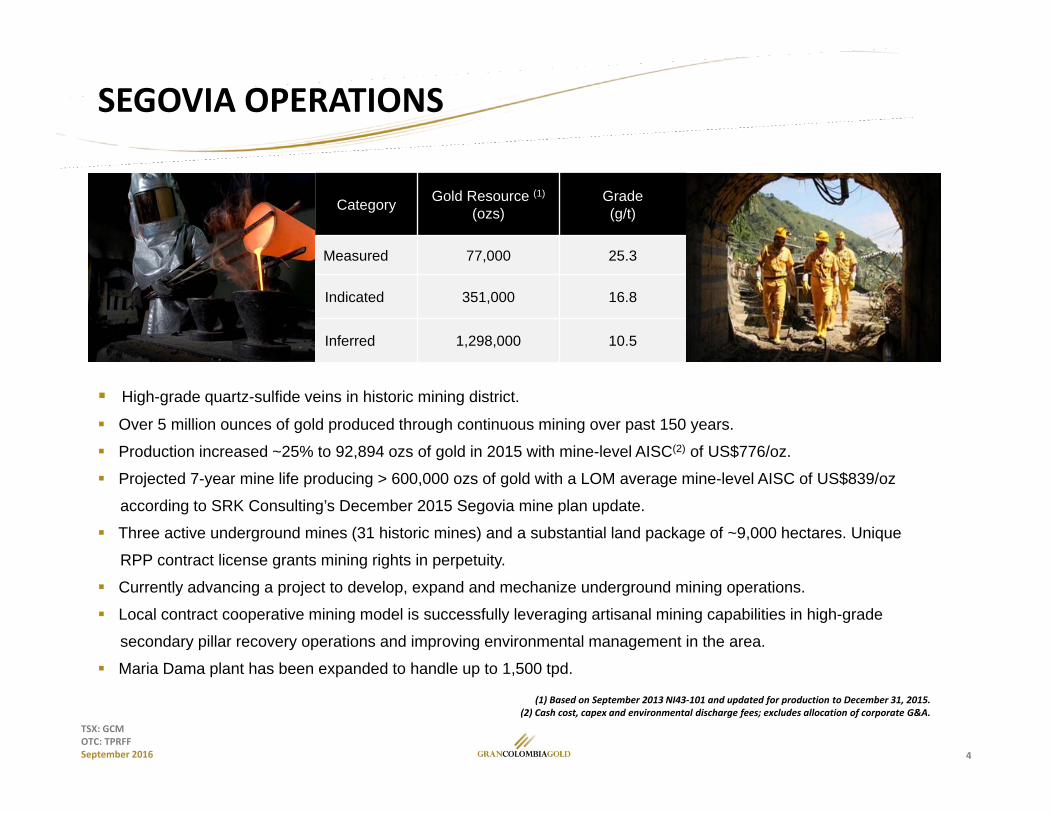

Category Gold Resource (1)

(ozs)Grade (g/t)

Measured 77,000 25.3

Indicated 351,000 16.8

Inferred 1,298,000 10.5

High-grade quartz-sulfide veins in historic mining district.

Over 5 million ounces of gold produced through continuous mining over past 150 years.

Production increased ~25% to 92,894 ozs of gold in 2015 with mine-level AISC(2) of US$776/oz.

Projected 7-year mine life producing > 600,000 ozs of gold with a LOM average mine-level AISC of US$839/oz

according to SRK Consulting’s December 2015 Segovia mine plan update.

Three active underground mines (31 historic mines) and a substantial land package of ~9,000 hectares. Unique

RPP contract license grants mining rights in perpetuity.

Currently advancing a project to develop, expand and mechanize underground mining operations.

Local contract cooperative mining model is successfully leveraging artisanal mining capabilities in high-grade

secondary pillar recovery operations and improving environmental management in the area.

Maria Dama plant has been expanded to handle up to 1,500 tpd.

(1) Based on September 2013 NI43‐101 and updated for production to December 31, 2015.(2) Cash cost, capex and environmental discharge fees; excludes allocation of corporate G&A.

5

TSX: GCMOTC: TPRFFSeptember 2016

MARMATO PROJECT

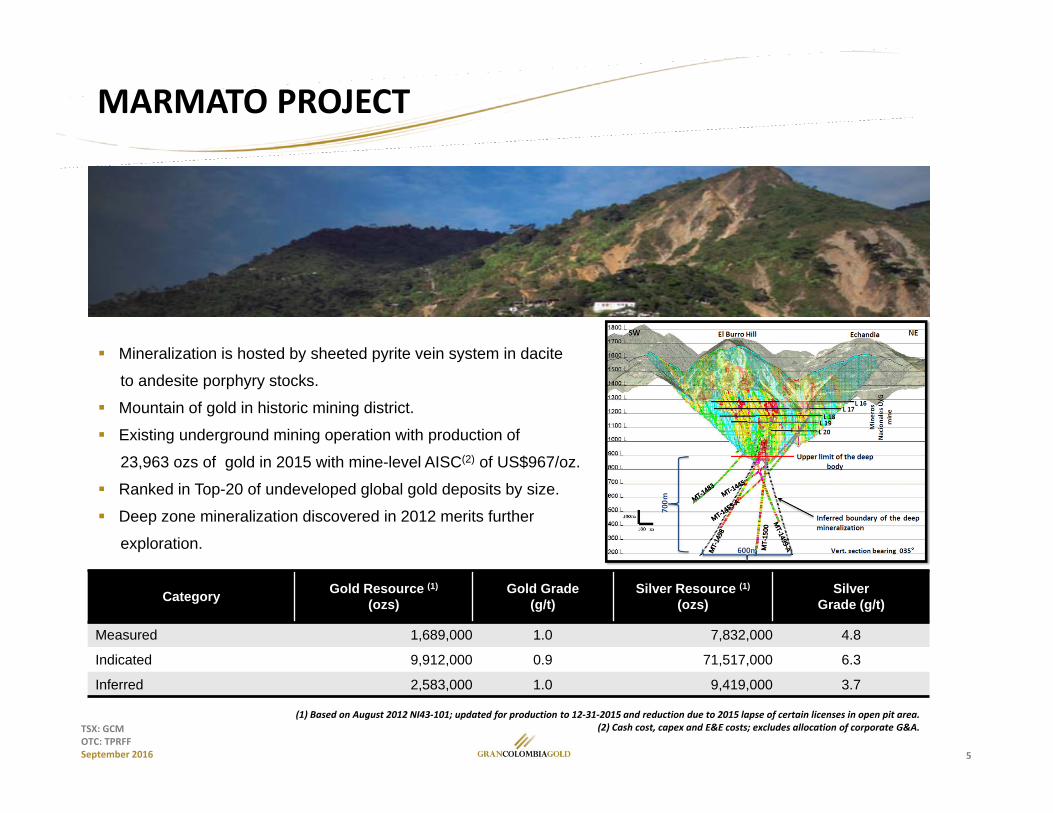

Category Gold Resource (1)

(ozs)Gold Grade

(g/t)Silver Resource (1)

(ozs)Silver

Grade (g/t)

Measured 1,689,000 1.0 7,832,000 4.8

Indicated 9,912,000 0.9 71,517,000 6.3

Inferred 2,583,000 1.0 9,419,000 3.7

Mineralization is hosted by sheeted pyrite vein system in dacite

to andesite porphyry stocks.

Mountain of gold in historic mining district.

Existing underground mining operation with production of

23,963 ozs of gold in 2015 with mine-level AISC(2) of US$967/oz.

Ranked in Top-20 of undeveloped global gold deposits by size.

Deep zone mineralization discovered in 2012 merits further

exploration.

(1) Based on August 2012 NI43‐101; updated for production to 12‐31‐2015 and reduction due to 2015 lapse of certain licenses in open pit area.(2) Cash cost, capex and E&E costs; excludes allocation of corporate G&A.

6

TSX: GCMOTC: TPRFFSeptember 2016

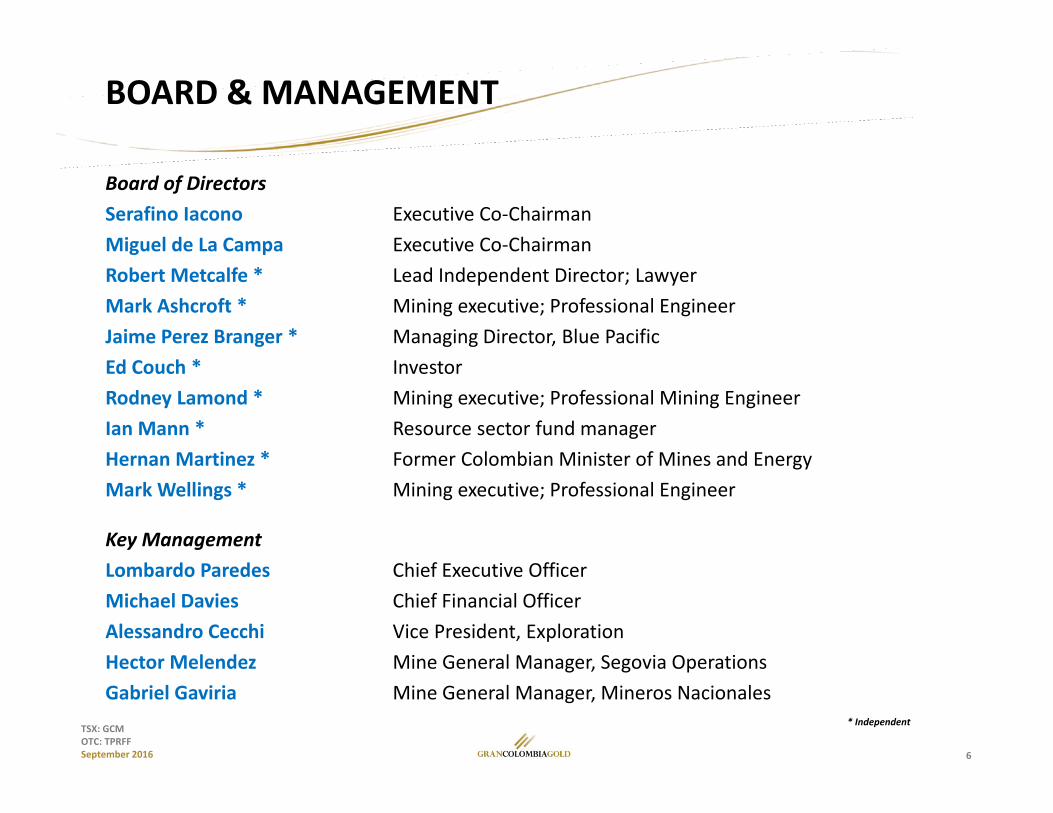

BOARD &MANAGEMENT

Board of DirectorsSerafino Iacono Executive Co‐ChairmanMiguel de La Campa Executive Co‐ChairmanRobert Metcalfe * Lead Independent Director; LawyerMark Ashcroft * Mining executive; Professional EngineerJaime Perez Branger * Managing Director, Blue PacificEd Couch * InvestorRodney Lamond * Mining executive; Professional Mining EngineerIan Mann * Resource sector fund managerHernan Martinez * Former Colombian Minister of Mines and EnergyMark Wellings * Mining executive; Professional Engineer

Key ManagementLombardo Paredes Chief Executive OfficerMichael Davies Chief Financial OfficerAlessandro Cecchi Vice President, ExplorationHector Melendez Mine General Manager, Segovia OperationsGabriel Gaviria Mine General Manager, Mineros Nacionales

* Independent

7

TSX: GCMOTC: TPRFFSeptember 2016

DEBT RESTRUCTURING2020 Debentures (TSX: GCM.DB.V)• Maturity – January 2, 2020• Coupon – 6% cash, paid monthly• Convertible – holder option – US$0.13/ share• Redeemable/ open market repurchases permitted• At Maturity – settle in cash• Senior secured, no changes to ranking, security or

covenants

Gold Notes(US$100M*)

Silver Notes(US$78.6M*)

2018 Debentures (TSX: GCM.DB.U)• Maturity – August 31, 2018• Coupon – 1% cash, paid monthly• Convertible – holder option – US$0.13/ share• Redeemable/ open market repurchases permitted• At Maturity – Company option to settle in shares or in

shares/cash if price < US$0.13/share• Senior unsecured, no changes to covenants or events

of default

New Sinking Funds• 100% of Excess Free Cash Flow• 75% for 2020 Debentures, 25% for 2018 Debentures• To fund redemptions, repurchases, maturity

* Principal amount excluding accrued and unpaid interest and a 2% restructuring fee.

January 20, 2016

8

TSX: GCMOTC: TPRFFSeptember 2016

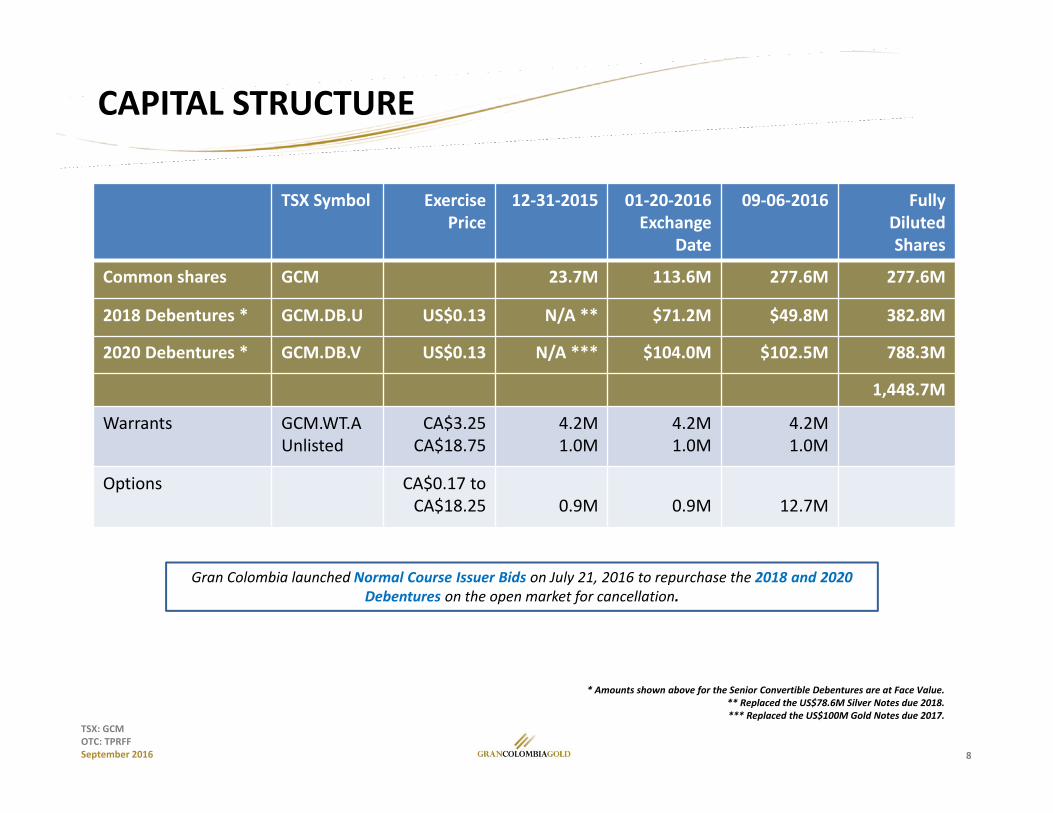

CAPITAL STRUCTURE

TSX Symbol Exercise Price

12‐31‐2015 01‐20‐2016Exchange

Date

09‐06‐2016 FullyDilutedShares

Common shares GCM 23.7M 113.6M 277.6M 277.6M

2018 Debentures * GCM.DB.U US$0.13 N/A ** $71.2M $49.8M 382.8M

2020 Debentures * GCM.DB.V US$0.13 N/A *** $104.0M $102.5M 788.3M

1,448.7M

Warrants GCM.WT.AUnlisted

CA$3.25CA$18.75

4.2M1.0M

4.2M1.0M

4.2M1.0M

Options CA$0.17 to CA$18.25 0.9M 0.9M 12.7M

Gran Colombia launched Normal Course Issuer Bids on July 21, 2016 to repurchase the 2018 and 2020 Debentures on the open market for cancellation.

* Amounts shown above for the Senior Convertible Debentures are at Face Value.** Replaced the US$78.6M Silver Notes due 2018.*** Replaced the US$100M Gold Notes due 2017.

9

TSX: GCMOTC: TPRFFSeptember 2016

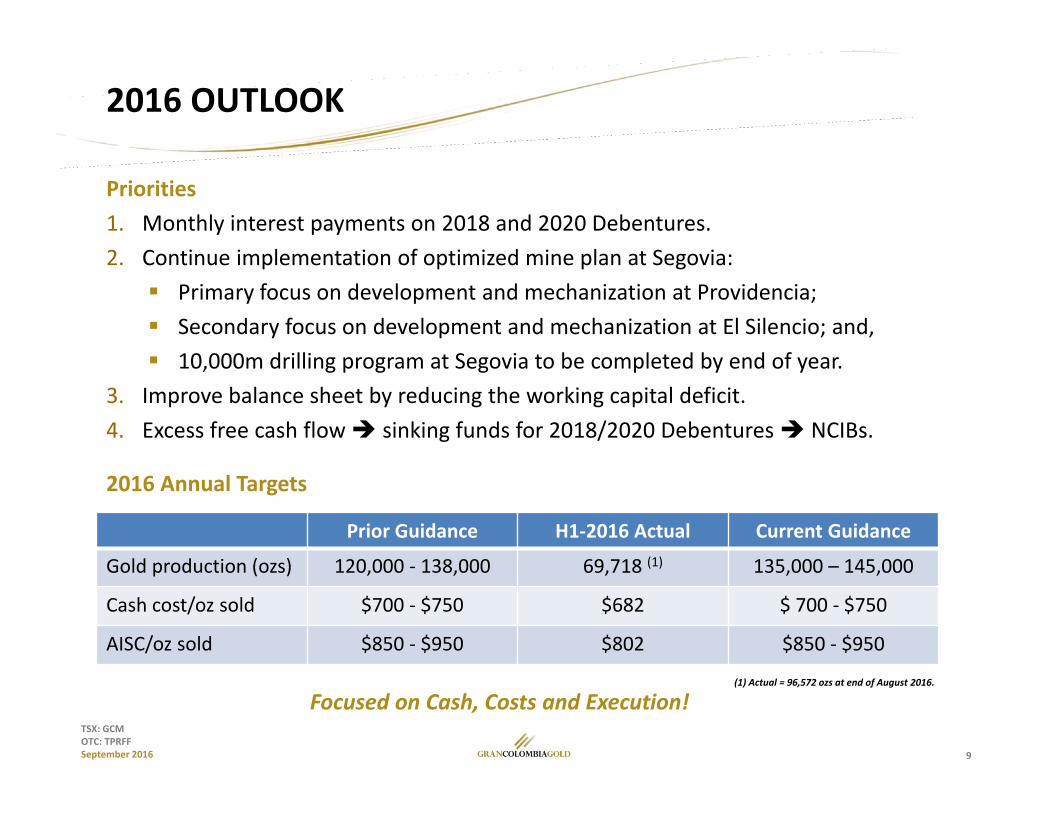

2016 OUTLOOK

Focused on Cash, Costs and Execution!

Priorities1. Monthly interest payments on 2018 and 2020 Debentures.2. Continue implementation of optimized mine plan at Segovia: Primary focus on development and mechanization at Providencia; Secondary focus on development and mechanization at El Silencio; and, 10,000m drilling program at Segovia to be completed by end of year.

3. Improve balance sheet by reducing the working capital deficit.4. Excess free cash flow sinking funds for 2018/2020 Debentures NCIBs.

2016 Annual Targets

Prior Guidance H1‐2016 Actual Current Guidance

Gold production (ozs) 120,000 ‐ 138,000 69,718 (1) 135,000 – 145,000

Cash cost/oz sold $700 ‐ $750 $682 $ 700 ‐ $750

AISC/oz sold $850 ‐ $950 $802 $850 ‐ $950

(1) Actual = 96,572 ozs at end of August 2016.

10

TSX: GCMOTC: TPRFFSeptember 2016

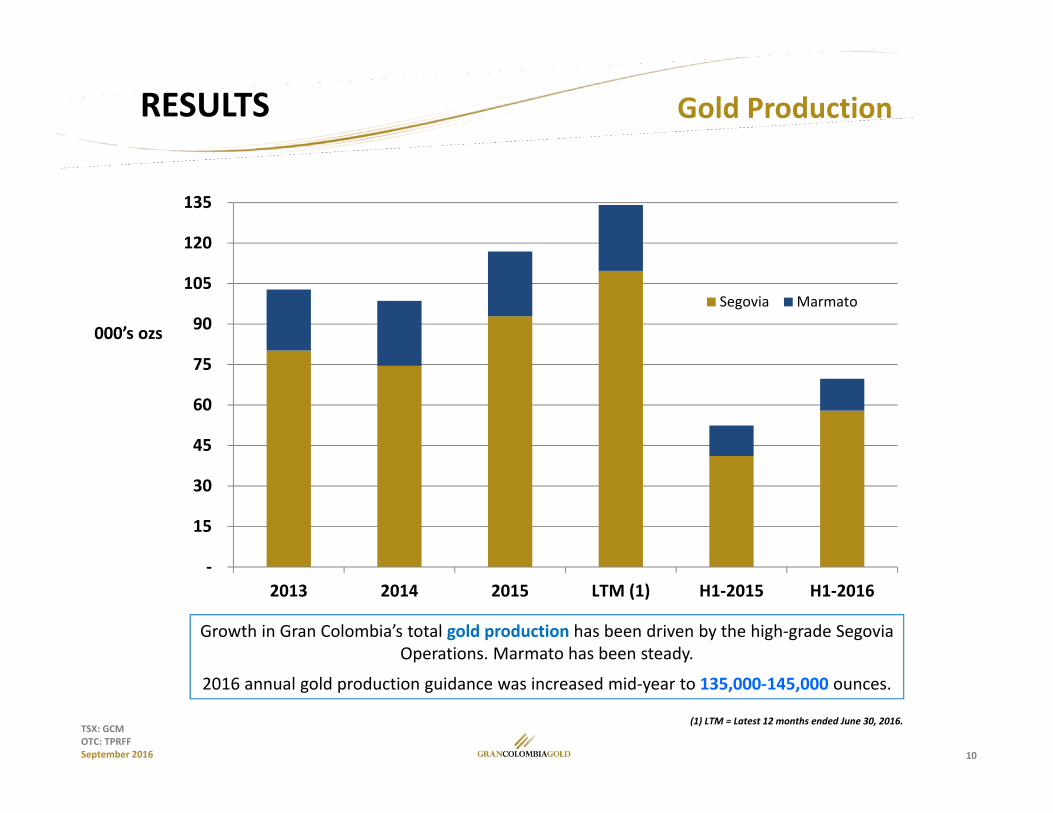

Growth in Gran Colombia’s total gold production has been driven by the high‐grade Segovia Operations. Marmato has been steady.

2016 annual gold production guidance was increased mid‐year to 135,000‐145,000 ounces.

Gold ProductionRESULTSAISC (‐23%

)

000’s ozs

‐

15

30

45

60

75

90

105

120

135

2013 2014 2015 LTM (1) H1‐2015 H1‐2016

Segovia Marmato

(1) LTM = Latest 12 months ended June 30, 2016.

11

TSX: GCMOTC: TPRFFSeptember 2016

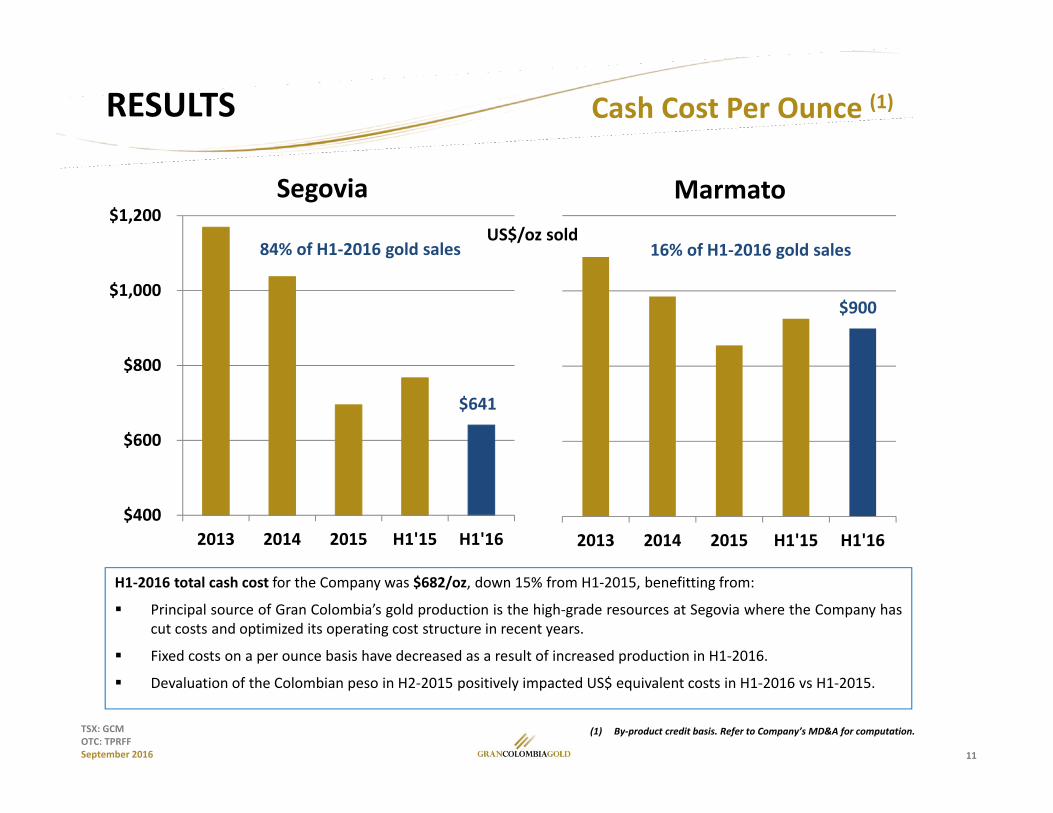

Cash Cost Per Ounce (1)RESULTS

117

89 $400

$600

$800

$1,000

$1,200

2013 2014 2015 H1'15 H1'16

Segovia

2013 2014 2015 H1'15 H1'16

Marmato

$900

16% of H1‐2016 gold salesUS$/oz sold

$641

84% of H1‐2016 gold sales

H1‐2016 total cash cost for the Company was $682/oz, down 15% from H1‐2015, benefitting from:

Principal source of Gran Colombia’s gold production is the high‐grade resources at Segovia where the Company hascut costs and optimized its operating cost structure in recent years.

Fixed costs on a per ounce basis have decreased as a result of increased production in H1‐2016.

Devaluation of the Colombian peso in H2‐2015 positively impacted US$ equivalent costs in H1‐2016 vs H1‐2015.

(1) By‐product credit basis. Refer to Company’s MD&A for computation.

12

TSX: GCMOTC: TPRFFSeptember 2016

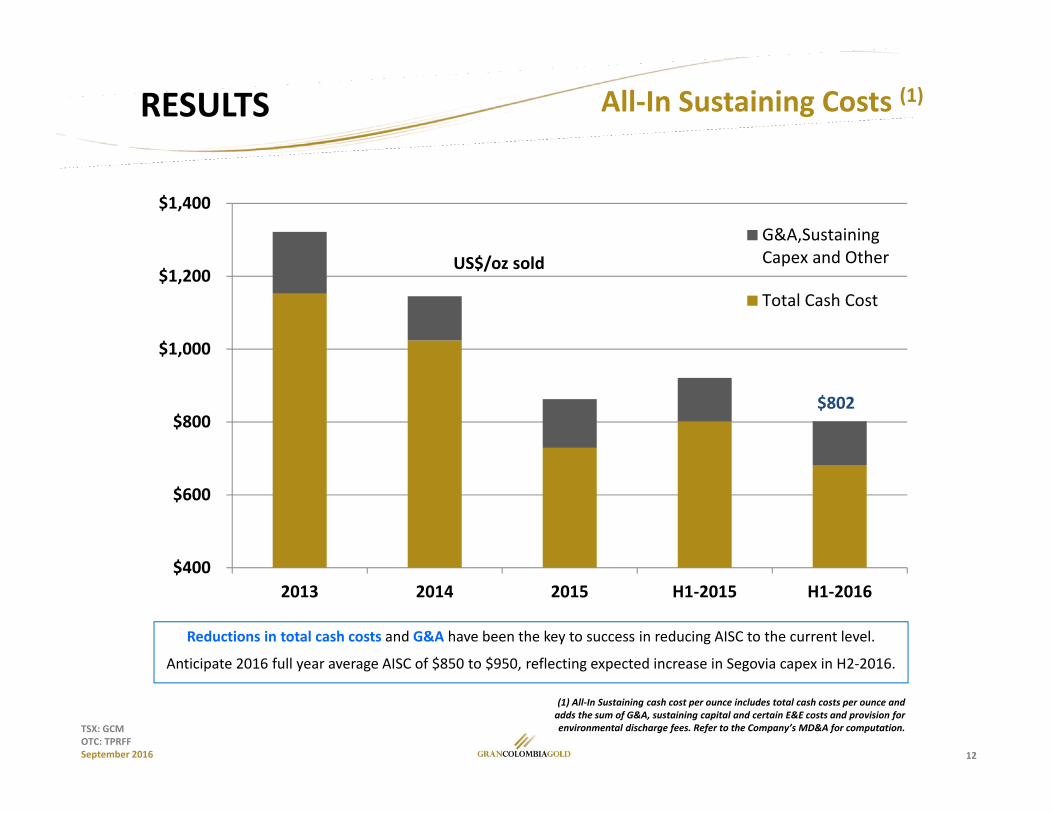

All‐In Sustaining Costs (1)

(1) All‐In Sustaining cash cost per ounce includes total cash costs per ounce and adds the sum of G&A, sustaining capital and certain E&E costs and provision for environmental discharge fees. Refer to the Company’s MD&A for computation.

RESULTSAISC (‐23%

)

US$/oz sold

$400

$600

$800

$1,000

$1,200

$1,400

2013 2014 2015 H1‐2015 H1‐2016

G&A,SustainingCapex and Other

Total Cash Cost

$802

Reductions in total cash costs and G&A have been the key to success in reducing AISC to the current level.

Anticipate 2016 full year average AISC of $850 to $950, reflecting expected increase in Segovia capex in H2‐2016.

13

TSX: GCMOTC: TPRFFSeptember 2016

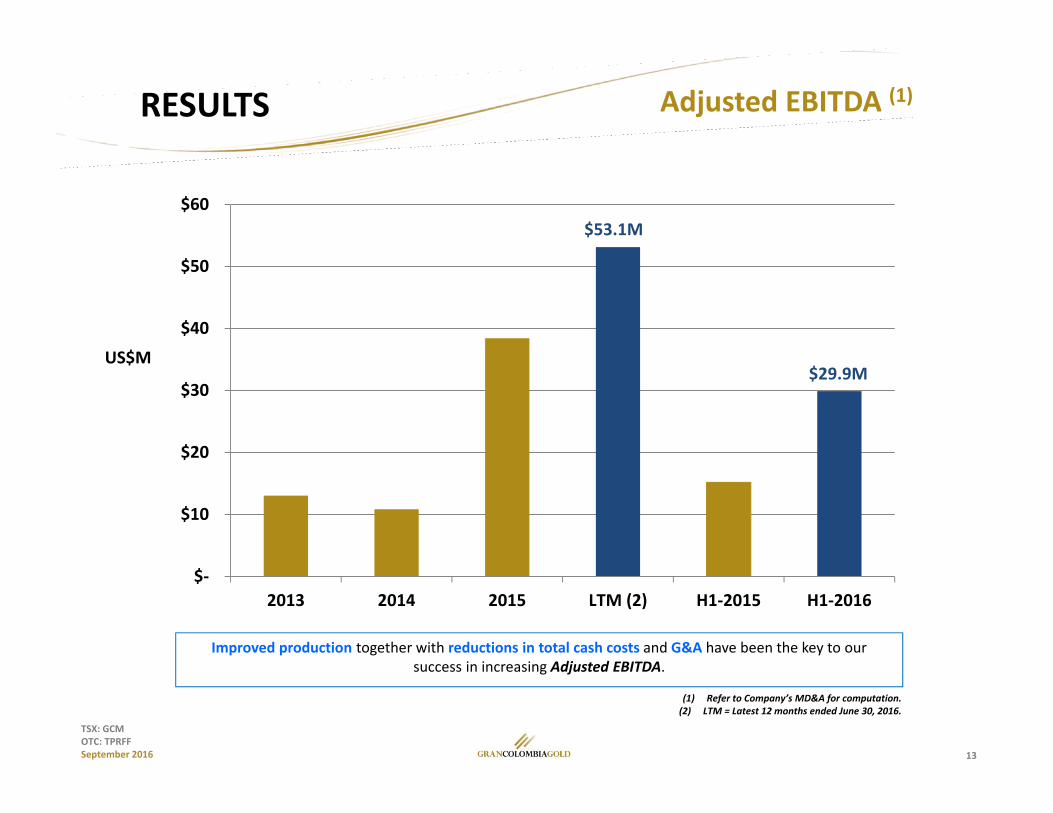

Adjusted EBITDA (1)RESULTS

(1) Refer to Company’s MD&A for computation.(2) LTM = Latest 12 months ended June 30, 2016.

$‐

$10

$20

$30

$40

$50

$60

2013 2014 2015 LTM (2) H1‐2015 H1‐2016

$29.9M

$53.1M

US$M

Improved production together with reductions in total cash costs and G&A have been the key to our success in increasing Adjusted EBITDA.

14

TSX: GCMOTC: TPRFFSeptember 2016

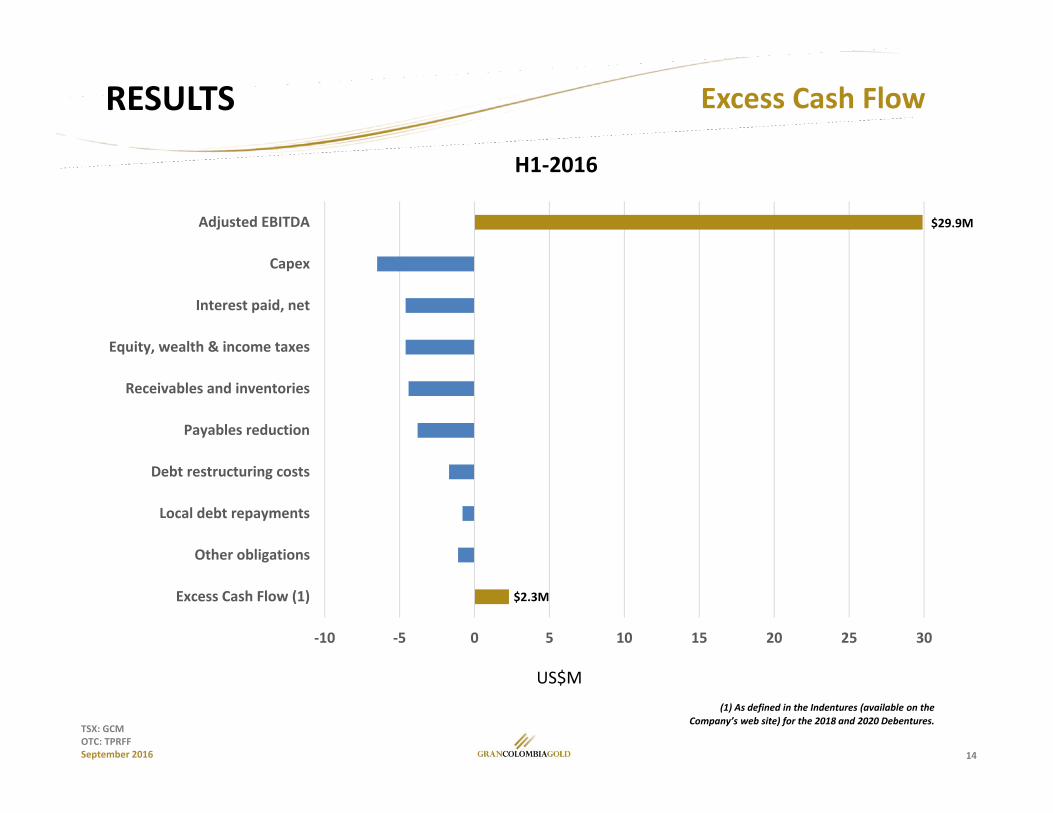

Excess Cash FlowRESULTS

(1) As defined in the Indentures (available on the Company’s web site) for the 2018 and 2020 Debentures.

‐10 ‐5 0 5 10 15 20 25 30

Excess Cash Flow (1)

Other obligations

Local debt repayments

Debt restructuring costs

Payables reduction

Receivables and inventories

Equity, wealth & income taxes

Interest paid, net

Capex

Adjusted EBITDA

$2.3M

US$M

H1‐2016

$29.9M

15

TSX: GCMOTC: TPRFFSeptember 2016

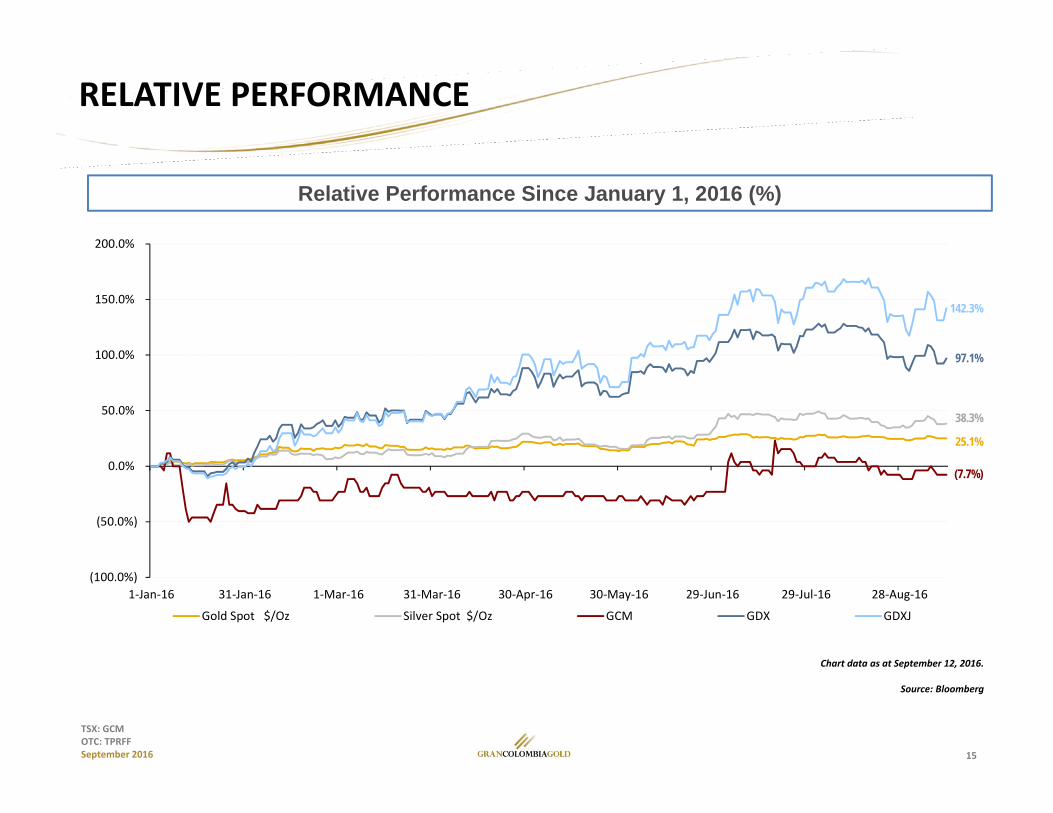

RELATIVE PERFORMANCE

Relative Performance Since January 1, 2016 (%)

Chart data as at September 12, 2016.

Source: Bloomberg

(100.0%)

(50.0%)

0.0%

50.0%

100.0%

150.0%

200.0%

1‐Jan‐16 31‐Jan‐16 1‐Mar‐16 31‐Mar‐16 30‐Apr‐16 30‐May‐16 29‐Jun‐16 29‐Jul‐16 28‐Aug‐16

Gold Spot $/Oz Silver Spot $/Oz GCM GDX GDXJ

142.3%

97.1%

38.3%

25.1%

(7.7%)

16

TSX: GCMOTC: TPRFFSeptember 2016

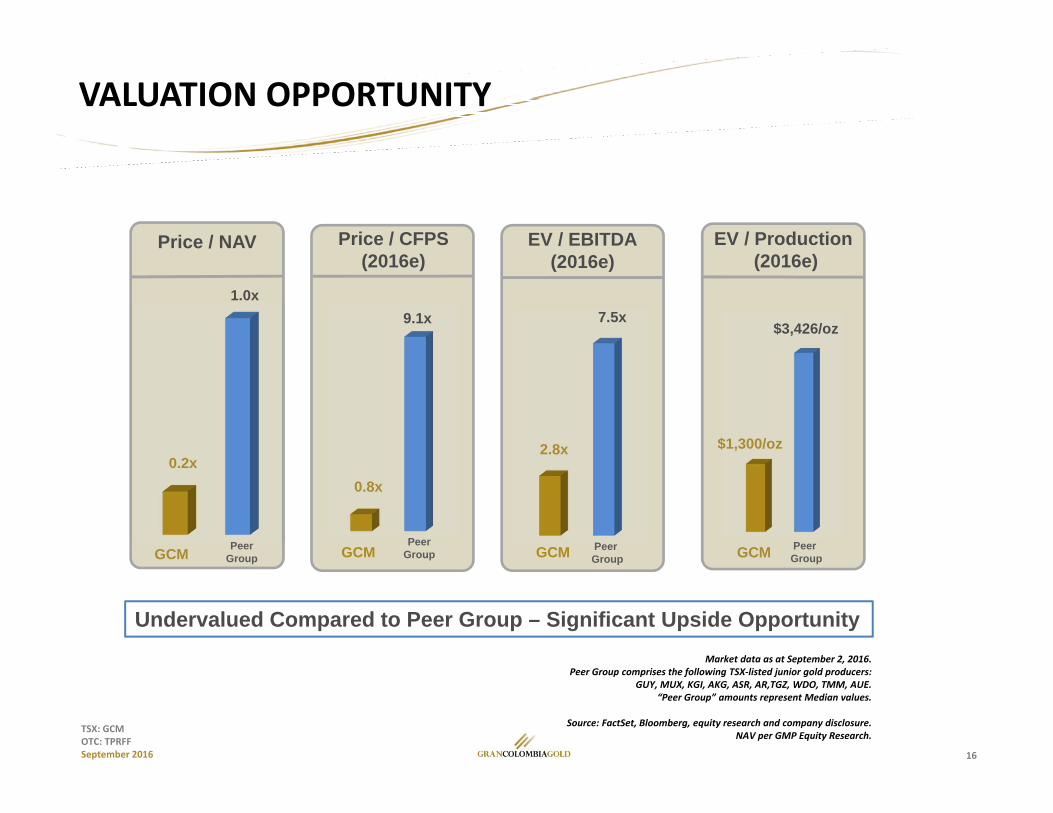

VALUATION OPPORTUNITY

Undervalued Compared to Peer Group – Significant Upside Opportunity

GCM GCM GCMPeerGroup

0.2x2.8x

7.5x

$1,300/oz

$3,426/oz

1.0x

Price / NAV EV / EBITDA(2016e)

EV / Production(2016e)

Peer Group

Peer Group

Market data as at September 2, 2016.Peer Group comprises the following TSX‐listed junior gold producers:

GUY, MUX, KGI, AKG, ASR, AR,TGZ, WDO, TMM, AUE.“Peer Group” amounts represent Median values.

Source: FactSet, Bloomberg, equity research and company disclosure. NAV per GMP Equity Research.

GCMPeer

Group

Price / CFPS(2016e)

0.8x

9.1x

17

TSX: GCMOTC: TPRFFSeptember 2016

Follow us on:

@GCMGold