1

CORPORATE FINANCE

Fall 2015 – Period I

Lecturer: Bünyamin ‘Ben’ Önal

2

Course objective• Purpose of the course

• Provide a basic understanding of the financial decisions anybusiness enterprise faces

• Key financial decisions:• Investment decisions

• Capital budgeting• M&A

• Financing decisions• Capital structure• Securities offerings• Financial planning• Credit management

• Payout decisions• Dividends, Stock repurchases

3

Why “corporate” finance?• Most corporate finance textbooks are intended for

publicly traded (large) corporations• In financial theory, (public) financial markets have an

important role in corporate decision making• Most small firms do not operate on financial markets (i.e., not

listed on stock exchanges and have no bond issues)• However, the underlying principles generally apply to

smaller firms too• Financial markets have a less important role in e.g.

financial planning, credit and cash management• Theories related to these issues are directly applicable to

smaller companies

4

What this course requires• Good command of the material covered in the Introduction to

Finance (Rahoituksen perusteet, 28A00110) course / Chapters1-13 of Brealey-Myers-Allen textbook 11th edition

• No additional math skills required• Good work ethics

• Large sample evidence (own questionnaire, response rate 90%)• Statistics on hours worked on this course:

– Mean: 130-160 hours– Median: 120-130 hours

• Other same level courses with same number of credit units:– Mean: 80-90 hours– Median: 70-80 hours

• Small sample evidence (official questionnaire, response rate 10%)• Amount of effort spent relative to 160 hours

– Much more effort: 28%; somewhat more effort: 48%; effort equals 160 hours:16%; somewhat less effort: 8%; much less effort: 0%

5

Readings / class material

• Brealey-Myers-Allen, Principles of Corporate Finance,6th, 7th, 8th, 9th,10th or 11th edition• McGraw-Hill 11th edition, chapters 14-19, 25, 28-33

(students are required to be familiar with chapters 1-13)• Lecture notes• Guest lecture slides• Exercises• Any other material posted on course webpage

6

12 Lectures: time, topic and materialTime and topic

08.09. Introduction: Overview ofcorporate finance

10.09. How corporations issue securities15.09. Payout policy17.09. Guest lecture on IPOs

22.09. Capital structure24.09. Capital structure and valuation29.09. Leasing

Textbook chapters / Other

• Ch. 14

• Ch. 15• Ch. 16• Material provided by Antti Niini

(Goldman Sachs)• Ch. 17• Ch. 18-19• Ch. 25

7

Lectures: time, topic and materialTime and topic

01.10. Financial planning06.10. Working capital management08.10. Mergers and acquisitions13.10. Guest lecture on M&As

15.10. Control, governance, andcorporate restructuring

Textbook chapters / Other

• Ch. 28 and 29• Ch. 30• Ch. 31• Material provided by Timo

Pohjakallio (Bain & Company)• Ch. 32-33

8

Exercises: practicalities

• Exercises should be done in groups consisting of nomore than three (3) students

• Co-operation among groups or individuals belongingto different groups is prohibited

• To help preserve your privacy, include a personal aliasalong with your name and student number in eachexercise report• Alias must not be confused with a student number and

should not consist solely of numbers

9

Exercises: Deadlines

• Exercises are due at the following times:• Tuesday 12:00 (sharp!) in the week the exercise is due• Deadlines are the same for both groups

• Exercises should be placed on instructor’s desk at U2• If none of the group members cannot make the class that

day, you can also drop it into the course box in Chydenia, by10:00 (Sharp!)

10

Accessing course material

• Textbook: Amazon / bookstore or library• The graphs in the lecture notes where source is not

mentioned are obtained from the course book – check thesources there if you are interested

• Lecture notes, exercises and results: course web site• Course home page can be accessed via the MyCourses

portal: https://mycourses.aalto.fi/• You need to log in to access exercises, lectures, grading and

possible other materials• Let me know if you do not have personal login for the

network

11

Grade• Part I. Exam: 60%

• Closed-book exam; two make-up exams• 5 True-False questions; 10 points• 5 problems; 50 points• Problems also have verbal parts; overall 15-20% verbal

• Part II. Exercises: 40%• 4 Exercise sets; points are not evenly distributed

• Minimum requirement for a “passing” grade: 40% ofpoints on each part• Must score at least 16 points on the exercises• Must score at least 24 points on the exam

Scholastic honesty and academicintegrity

• We expect adherence to highest standards of scholastic honesty

• Examples of scholastic dishonesty are:- sharing exercise answers between groups- presenting answers as own work without proper citation tothe sources (plagiarism)- sharing answers during the final exam

• All classwork must be done by the students that return the work,co-operation in preparing answers to the exercises betweengroups (i.e., any individuals not belonging to the same group) isstrictly prohibited

12

Scholastic honesty and academicintegrity

• However, you are allowed to discuss the exercise problems withfellow students in general terms: the definition of terms andconcepts in the questions, and what issues are central to aparticular question. Every group should proceed on their ownfrom there

• Failure to adhere to these guidelines is subject to disciplinaryaction, varying from receiving no points on the particular exerciseor exam to complete removal from the course. Turning in classassignments is considered acknowledgement of these guidelines

• For more information, consult the section Academic Integrity andHandling Violations Thereof at Into for Aalto Students

13

14

FAQs related to exam

• Do we need to memorize the formulas for the exam?• You are expected to know the basic formulas by heart, e.g., value of a

right, WACC, etc.• But you do NOT need to know the derivation of the formulas• Complex formulas or schedules such as MACRS depreciation schedules

will be provided to you if a related problem appears in the exam, no needto memorize those

• Do we need to memorize verbal concepts for the exam?• You are expected to know the basic concepts by heart, for ex. winner’s

curse, pecking order theory, etc.• But you do NOT need to know exact definitions or memorize long lists• I will never ask you questions such as “Define winner’s curse”, “List four

cases when potential gains to leasing are highest”

15

FAQs related to course administration

• Why don't you post model answers to exercises on the web?• Supply of high quality questions is limited• Giving out model answers in electronic format would, in the long run,

probably lead to a situation where there would be a full menu of modelanswers that could be applied without much thought to whatever questiontype we have in mind

• The learning experience, aggregated over all students, and taking intoaccount future students, would probably not improve from what it ispresently

• Do I need to register separately for the exam?• Yes! Via WebOodi as usual• Exam registration on WebOodi closes always 7 days before the exam!

16

FAQs related to course administration

• What is the idea behind closed-door policy?• Experience has shown that without the policy, many students

will arrive to the class late, one by one, mostly during thefirst 15 minutesThis is highly disturbing both to the instructor and manystudents

• Assuming that there are 200 students in the class and that10% of them arrive late within the first 15 minutes, thepolicy will waste on average 7.5 minutes of 20 students’ timewhile guaranteeing an uninterrupted learning experience forthe remaining 180 students

Course messengers

• As in all courses, I am going to collect student evaluationsduring the last lecture

• In addition, KY Finance has launched the “messenger students”channel for selected Bachelor’s level courses

• Two students will gather feedback from students during thecourse and provide it to the professors

• Corporate Finance is one of the selected courses• Your suggestions (especially those that are easy to implement

“during” the course) are welcome

17

Course messengers

• Juha Vänttinen & Risto Pitkänen• Facebook group: Corporate finance fall 2015 28C00100

18

Logistical and contact information• Lectures (see syllabus for details)

• Tuesdays 12:15-13:45 at U2• Thursdays 12:15-13:45 at U2

• Exercises (four demo and four exercise sessions; see the detailedschedule on the syllabus) and course administration• Demos: Thursdays 14:15-15:45 at U2• Exercises: Tuesdays 14:15-15:45 or 16:15-17:45 at U2

• Regular “Office” hours: Tue and Thu, 30 minutes followingthe sessions of the day. In addition:

• E-mail: [email protected] (for quick questions)• Office phone: 050 410 5011• By appointment

19

20

A detour: B.Sc. thesis seminar“The seminar is going to be the most important and educational finance classyou've taken so far…” – Student comment

• This course can help you find a good research idea for yourthesis. Some examples from previous years’ thesis titles:

• Top-tier Investment Banks and Bidders’ Announcement Returns: Evidencefrom European Mergers and Acquisitions

• Rationale for LBOs: Empirical Evidence from Europe• The Role of Women Directors in Finnish Boardrooms – Examination of

Committee Memberships

• Start thinking about your thesis topic!• Feel free to discuss topics and research questions with potential

supervisors

21

Lecture 1

IntroductionOverview of corporate financing

Overview

• Sources of funds• Internal• External

• External financing• Stages of external financing• Principal forms of capital

• Debt financing• Equity financing

– Venture capital– Next lecture: public equity issues

22

23

Sources of funds for non-financial firmsin the U.S.

24

Finnish corporate sector’sself-financing ratio

25

Life cycle of financing

Firm size

Own/family funds

Bank loans, venture capital

Public equity issues

Public debt issues

Amount of funds

26

Two principal forms of capital

• Equity capital• Gives ultimate control rights, subject to debt covenants• Provides residual cash flows

• Debt capital• Provides privileged cash flow rights• No control rights as long as the firm keeps its promises

• And there are hybrid securities• E.g., Preferred equity• Contain features of both equity and debt

27

Debt financing

• Different features:• Private vs. public• Maturity• Convertibility• Callability• Seniority and collateral• Fixed vs. floating rate• Country and currency• Default risk• On- vs. off-balance sheet financing

Example: Apple’s recent debt moves• Apple issued debt (worth $17 billion) in 2013 for the

first time since 1994• Despite sitting on $145 billion of cash ($100 billion abroad)• Issued to partly finance the promised $100 billion cash return

to shareholders• It included 3-year, 5-year, 10-year and 30-year fixed-rate

bonds and 3-year and 5-year floating-rate notes• 3-year floating rate bonds were sold at 5bp and 5-year ones

for 25bp over the LIBOR• Continued to sell bonds in 2014, including 8 and 12-

year euro-denominated bonds worth €2.8bn28

Apple was not alone

29

In Finland

30

Finnish non-financial corporations’interest-bearing debt

31

32

Role of venture capitalists• Who are venture capitalists?

• Financial institutions, wealthy individual investors (businessangels) and some large technology firms (i.e., corporate VCs)

• What do venture capital firms do?• Pool investors’ cash and invest it in new businesses• Bring in managerial/tech expertise and contacts• Provide these benefits at a high “price” (a large equity stake and

say in decision-making)• Venture capitalists expect to be able to make an exit – to

sell their stake in an IPO or buyout transaction – withinseveral years from their investment• Most VC funds are limited partnerships and have a fixed life of

about 10 years

VC game on TV• e.g., Shark tank:

• First an example: https://www.youtube.com/watch?v=opNiKBP7hQo• $20 million invested in 109 companies, 84% of offers accepted by sharks• Average $182k raised; relative to $210k asked• Average 40% equity stake taken; relative to 20% offered• Sharks’ average valuation $465k; relative to entrepreneurs’ average valuation

$1.06 million• Source: http://www.sharktank.tvquotes.net/

• VC market for internet/software startups:• Median of $900k raised in convertible notes at $6 million valuation• Corresponds to 15% of company given up• Source: http://www.forbes.com/sites/georgedeeb/2013/10/09/comparing-shark-

tank-to-venture-capital-reality/

33

34

Venture capital payoff patterns• Venture capitalists tend to invest in companies which

have a chance of becoming highly successful• Expect to be able to earn a very high return on their capital• Venture capital is expensive

• Venture capitalists tend to be selective in theirinvestments• E.g., Finnish venture capitalists tend to accept less than one-

tenth of the applications for capital• Distribution of the outcome from a venture capital

(VC) investment tends to be very skew• For every ten first-stage venture capital investments,

• only two or three may survive as successful businesses• only one may pay off big (e.g., Facebook)

35

Elements of venture capital• VC investments tend to be made in several stages

• New ventures often have very large financing needs andmajor uncertainties

• There are significant asymmetries of information (andrelated agency problems) between the founding owners andthe venture capitalistsIt makes little sense to provide venture financing for a longperiod at any one time

• Venture capitalists tend to seek for boardrepresentation in the company they invest in• Allows them to monitor their investment and to help in the

strategic management of the company

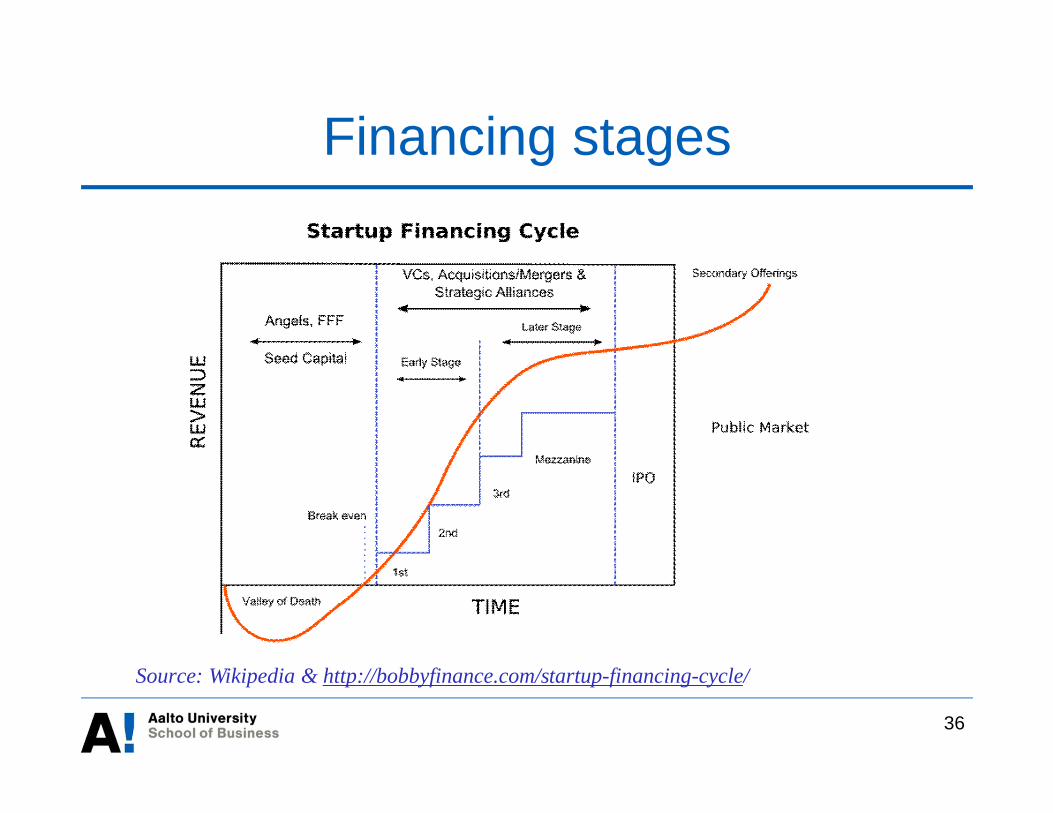

Financing stages

36

Source: Wikipedia & http://bobbyfinance.com/startup-financing-cycle/

37

Venture capital investments in the US

Top 10 largest VC deals in the US

38

Source: PEREP_Analytics, Finnish Venture Capital Association, www.fvca.fi

39

Venture capital investments as % ofcountry GDP in Europe

40

Venture investments made inFinnish portfolio companies

Source: PEREP_Analytics, Finnish Venture Capital Association, www.fvca.fi

41

Lecture 2

How corporations issue securities

42

Overview

• Equity offerings: key concepts

• IPOs• Motives for going public• Short-term performance

• Underpricing and winner’s curse hypothesis• Timing

• Long-term performance

• SEOs• Announcement effect• Rights offer

43

Equity offerings: key concepts

• Three questions(1) Have the shares been listed before?

• In an initial public offering (IPO) the issuer sells its shares (on averageabout a third of the stocks outstanding) to the market for the first time

• In an seasoned equity offering (SEO) the share is already listed at thetime of the issue

(2) Who are the shares sold to?• Rights offerings are targeted to current stockholders• General cash offerings are targeted to the investing public in general

(3) Who gets the money?• In a primary offering the issuer issues new shares• In a secondary offering the original owners sell their shares to investors

44

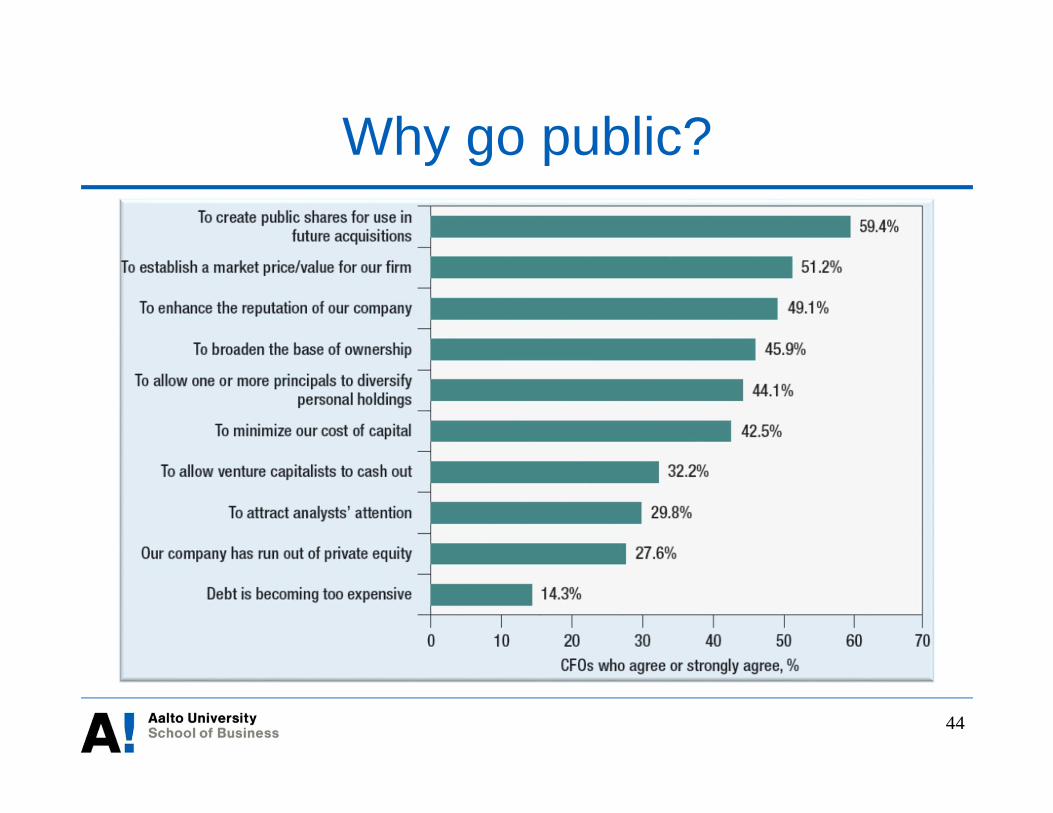

Why go public?

Example: Facebook’s acquisition spree

45

46

Key (hidden) cost: IPO underpricing• IPO firms and their original shareholders leave

substantial amounts of money on the table• Most IPO shares trade initially at substantial premiums

relative to offer price• Initial IPO return in Finland and in U.S. has been on average

15-20%• These returns are typically realized during a short period of

time (a few days or so)• This initial return is frequently called the "underpricing"

of IPOs• IPOs by small and risky firms tend to be most

underpriced

Examples: Money left on the table

47

Source: Jay Ritter, http://bear.warrington.ufl.edu/ritter/ipodata.htm

48

Average initial IPO returns (1975-2014)

0%

10%

20%

30%

40%

50%

60%

Aver

age

first

-day

retu

rns

Source: Jay Ritter, http://bear.warrington.ufl.edu/ritter/ipodata.htm

49

Initial returns of recent Finnish IPOs

Source: Nasdaq OMX

50

Winner’s curse problem• Starting point: informed and uninformed investors• Information and underpricing in IPOs

• More demand for underpriced than overpriced IPOs(informed investors only take part in underpriced IPOs)Underpriced offers need to be rationed more than overpricedoffersUninformed investors participating in the market will getrelatively more overpriced than underpriced shares

• Conclusion: If IPOs are not underpriced on average,uninformed investors will always suffer losses andwithdraw from the market

51

Winner’s curse: simple example• Two equally-likely offerings:

• Underpriced - initial return: + 40%• Overpriced - initial return: - 30%

• You ask for 1000 shares of each with the offer price of €1• You are allocated 500 shares of underpriced, 1000 shares

of overpriced stock• With full-allocation, your initial euro return would be:

€1000x40% - €1000x30% = €100 (or 5% of investment)

• Due to rationing in the “hot” IPO, your actual return is:€500x40% - €1000x30% = - €100 (or -6.67% of investment)

Empirical Evidence on Winner’sCurse (e.g., Keloharju, 1993)

52

53

How to reduce IPO underpricing?• Under the winner’s curse and alternative hypotheses,

underpricing is driven by ‘information asymmetry’ or“castes” between the participants in the IPO process

• Potential solution: reducing information asymmetries orpreferential treatment among investors• Book-building

• Investment bank obtains non-binding demand info (indications ofinterest) from investors before setting the final price

• Informed or favored investors obtain desired allocations of “hot” issuesin return

• Auctions• Offer price based directly on investor bids

54

Hot new-issue periods• Equity offerings, particularly IPOs, tend to be clustered in hot-

issue periods, i.e., when stock prices are in general at historicalhighs:• IPOs are timed to coincide with these periods – leading to

IPO waves• Hot issue markets are often driven by issuers in a given industry

The Economist (2011)

55

IPO volume in the U.S.In 1980-2000, an average of 310 firms went public every yearIn 2001-2014, an average of 111 firms went public every year

Aggregate IPO proceeds in 2014: $ 42.30 billion

Source: Jay Ritter, http://bear.warrington.ufl.edu/ritter/ipodata.htm

56

IPO volume in Europe

Source: IPO Watch Europe, PWC

57

IPO volume in European stockexchanges (2014)

Source: IPO Watch Europe, PWC

IPOs in Finland

58

Source: Economic Growth Through IPOs, NASDAQ OMX Helsinki, May 2014

“In Sweden, over 160 smallgrowth companies have

already got listed on the FirstNorth market since 2005; inFinland, only 6 have done so

during the same period”

“The only major differencebetween the two countries is

taxation.”

59

Long-term performance

• IPOs (and SEOs) tend to underperform similar firms inthe long run, both in terms of operating performanceand stock market performance

• The underperformance appears to last at least 3 years

Source: Loughran and Ritter (Journal of Finance, 1995)

”An investor would have toinvest 44% more money in theIPO firms than non-issuers to

have the same wealth five yearsafter the offering.”

60

Long-run performance of IPOs inFinland

-60%-50%

-40%-30%-20%

-10%0%

10%

20%30%

0 5 10 15 20 25 30 35 40 45 50 55 60

Months in relation to date of IPO

CARMarketRaw

Source: Kulp (1995)

61

Seasoned Equity Offerings• General cash offers

• As in IPOs, securities are sold to an underwriter who thenoffers them to the public

• Rights offers• Targets existing shareholders• Each stock has one subscription right• A given number of subscription rights (N in the formula

given later) gives the right to purchase one additional stockat a pre-specified price during a pre-specified time period

• Subscription rights are traded separately for a pre-specifiedtime period

62

SEO announcement effect

• Announcement of seasoned equity offerings tend tolead to adverse price effects• In the U.S., announcement of an SEO typically results in a 3-

4% decline in the stock price• This decline is economically important

• On average, the fall in the stock value is equivalent to about a third ofthe new money raised by the offering

• Why?• Greater supply of stocksè lower stock price? Not so much!• Information revealed by the stock issue

SEOs in Europe

63

Source: IPO Watch Europe, PWC

“Total money raised by FOs in 2014 increased by 19% from €120.1bn in 2013 to €143.2bn in2014.• 63% of FO proceeds was raised via primary offerings, where the companies themselves receive

the money instead of shareholders selling down their positions. As in the previous year, 2014primary proceeds have mainly been driven by funds being raised by European banks torecapitalize and strengthen their balance sheets due to more stringent capital requirements.

• Seven of the top ten FOs were by banks, raising over €27bn. This includes Deutsche Bank inGermany, Lloyds Banking Group in the UK, Monte dei Paschi in Italy and Eurobank Ergasias inGreece.”

64

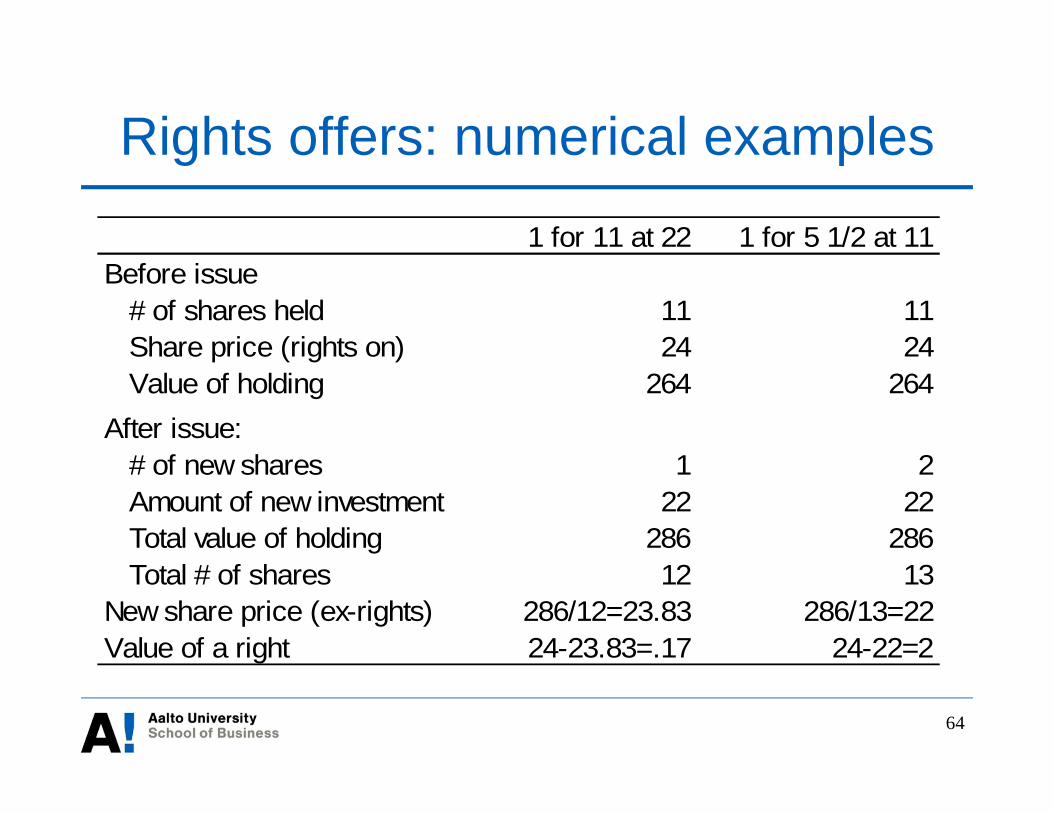

Rights offers: numerical examples

1 for 11 at 22 1 for 5 1/2 at 11Before issue # of shares held 11 11 Share price (rights on) 24 24 Value of holding 264 264After issue: # of new shares 1 2 Amount of new investment 22 22 Total value of holding 286 286 Total # of shares 12 13New share price (ex-rights) 286/12=23.83 286/13=22Value of a right 24-23.83=.17 24-22=2

65

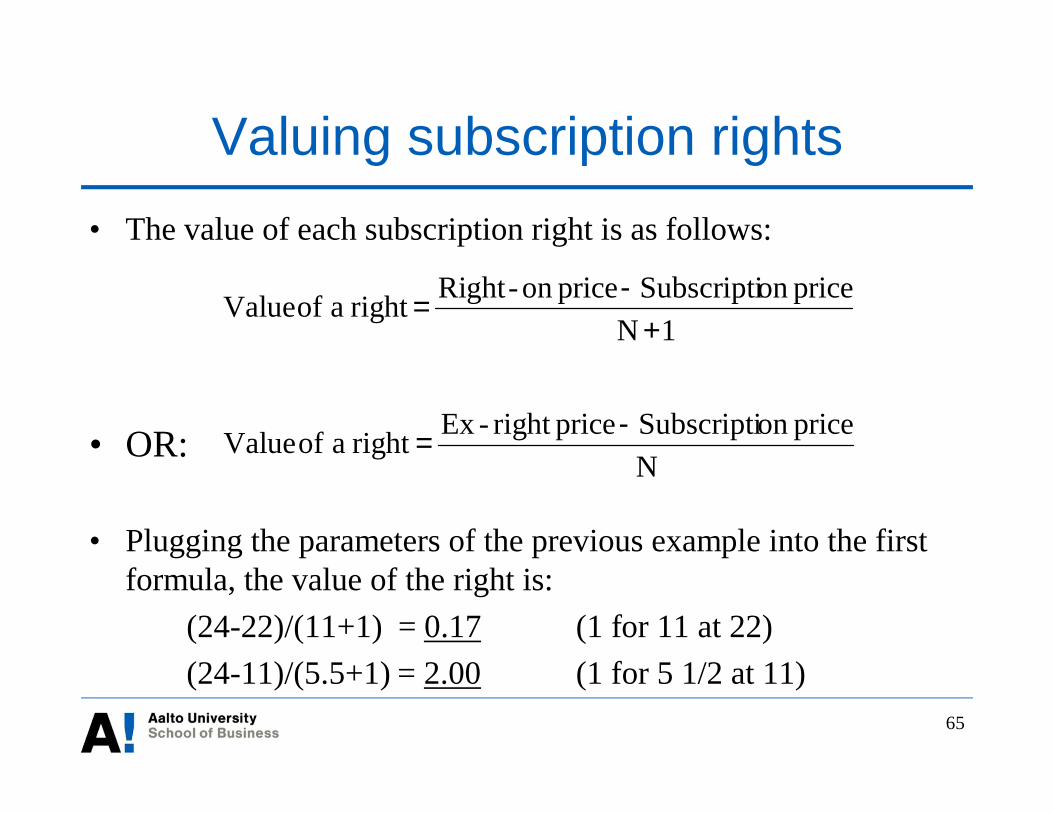

Valuing subscription rights• The value of each subscription right is as follows:

• OR:

• Plugging the parameters of the previous example into the firstformula, the value of the right is:

(24-22)/(11+1) = 0.17 (1 for 11 at 22)(24-11)/(5.5+1) = 2.00 (1 for 5 1/2 at 11)

1NpriceonSubscriptipriceon-RightrightaofValue

+-

=

NpriceonSubscriptipriceright-ExrightaofValue -

=

66

Rights issue price is irrelevant but...• Subscription price for rights issues is irrelevant for the

owners if all existing owners participate in the issue• Easy to see that this holds in the previous example

• In both cases the amount of new investment and the value of theportfolio after the offering is the same, although terms of the tworights offers are very different

• In practice some subscription rights are sold tooutsiders• This matters if existing shareholders (i.e. the investors who

sell their rights) have inside information• If all rights are sold to outsiders, rights offers should have

similar adverse selection effects as general cash offerings

67

Signaling with rights offers

• Rights offers may act as a signal of the management’sintentions or expectations

• A lower offer price:• May be a good signal implies a larger increase in the

future dividends• Companies tend to be reluctant to decrease the dividend per share

• But may also signal management’s concern of offer failure ata higher price

• Evidence so far: It doesn’t matter in the US and Norway, butproduces a positive reaction in Italy

68

Direct costs of raising capital

69

Underwriting spreads

”7-percent puzzle”

• Notation:

• Terms of offer:• Shareholder wealth before and after

70

Appendix: Value of a right formula

71

• Formula derivation:

Appendix: Value of a right formula

72

Appendix: Value of a right formula

• Alternative formula:

73

Lecture 3

Payout policy

74

Overview• Dividends: key concepts• Share repurchases• Payout decisions in practice

• Time trends• Survey evidence

• Do dividends matter? Three opposing views:• Center – Dividends are irrelevant• Rightists – Dividends are valuable• Leftists – Tax considerations

• Dividends and taxes in Finland

75

Dividends: important concepts• Dividend per share• Dividend yield = Dividend per share / Stock price• Dividend payout ratio = Dividend per share / Earnings

per share• Timeline of events

• Announcement date = Board’s suggestion for dividend per shareis announced

• Ex-dividend date = First day on which the stock trades withoutthe dividend; 1-2 business days before record date

• Record date = Date by which a shareholder must officially ownshares in order to be entitled to a dividend

• Date of payment

76

Exxon Mobil’s dividend

Close on Feb 7: $86.34

Open on Feb 8: $85.83

How firms repurchase stock1. Open market repurchases (most common), with restriction such

as it cannot exceed a fraction of daily trading volume• Typically 25%. But 50% in Finland since its stock exchange has limited

liquidity

2. Tender offer: Offer to buyback at a premium (about 20%).Shareholders decide whether to accept the offer or not

3. Dutch auction: Series of prices at which the firm is prepared tobuy backà Shareholders declare how many they are willing tosell at each priceà Firm chooses lowest price at which it canbuy the desired number of shares.

4. Negotiation with a major shareholder

77

78

Dividends and repurchases in U.S.

”The repurchase revolution”or bubble

79

Source: http://www.economist.com/news/business/21616968-companies-have-been-gobbling-up-their-own-shares-exceptional-rate-there-are-good-reasons

“Today no chief executive can ignore buybacks. Theyare an idea that has conquered the world …… However, among fund managers and someexecutives, there is little doubt that the pressure to boostcash returns can contribute to low investment. SimonHenry, the finance chief of Shell, …, “The longevity ofthe firm is what matters...executives need to hold theirnerve against short-term pressure so that they can investfor the long run…”“… there are signs that buy-back boom ispeaking…There are even signs that investing may beback in fashion. Exxon, the biggest spender onbuybacks thus far, has recently tempered them in favorof long-term projects…”

80

Dividends and repurchases in Europe

Source: Bloomberg, S&P, Gutmann KAG

Figure: Dividend payouts and share repurchases by Stoxx 600 companies

Dividends vs. Repurchases in Europe

81

82

Dividend decision in practice

Share repurchase decision

83

A 2004 survey of financial executives asked them to state the importance of different factors tothe repurchase decision.

Source: a. Brav, J.R. Graham, C.R. Harvey, and R. Michaely, "Payout Policy in the 21st Century,"Journal of Financial Economics 77 (September 3005), pp. 483-527.

0 10 20 30 40 50 60 70 80 90 100

The influence of institutional shareholders

Having surplus liquid assets

A sustainable change in earnings

Stability of future earnings

Mergers and acquisitions strategy

Lack of good investment opportunities

Our stock is undervalued

Executives who stated factor was important or very important, %

84

Does payout policy matter?

• Three schools of thought:• “Middle-of-the-roaders”

• Miller and Modigliani (1961)• Payout decision is value-irrelevant and should just be a by-product of

profitability and (positive-NPV) investments, keeping financingpolicy fixed

• “Leftists”• Dividends are wrong because capital gains are historically taxed at

lower rates than dividends

• “Rightists”• Dividends are preferred by certain investors

85

Does payout policy matter?

• Payout decision may be flip side of an investmentdecision or a financing decision• Pay out cash or set it aside for investment• Pay out cash and borrow or use the cash to finance

investments• To understand payout decisions, we must think of them

independently from investment and borrowingdecisions

Miller-Modigliani irrelevancy theorem

86

Dividend irrelevancy theorem• Miller-Modigliani (1961)

• Useful starting point for analysis of dividend policy• Assume:

• No taxes, transaction costs or other imperfections• A fixed capital investment program• A financing policy in which borrowing is set• Remaining needed funds come from retained earnings, and

extra cash is paid as dividends• Capital markets are efficient and transactions take place at fair

prices• No information asymmetry and signaling

87

Dividend irrelevancy theorem

• Given the assumptions, if a firm wants to increase itsdividends it needs to finance it with an equity issue• Consequently, each share is worth less because more shares

have to be issued against the firm’s assets• In an efficient market, the decrease in share price is

exactly worth the dividend per shareDividend policy is irrelevant!Firms should let dividends fluctuate as a by-product of theirinvestment and financing decisions

88

• Current dividend policy:• Pay the €1 surplus cash per share on 1 million shares outstandingè Ex-dividend price: €10; and market cap= €10million

• Change of plans:• Increase dividend payout to €2 a shareè Ex-dividend price: €9

• Borrowing and investments are fixed! The extra $1 a share must comefrom issuing new shares:

• Sell €1 million/€9= 111,111 new shares• After the issue:

• About 1.11 million shares outstanding; Market cap still €10 millionbut share price = €9

• Old stockholders’ wealth before and after:• €10 a share + €1 dividend = €9 a share + €2 dividend

Dividend irrelevancy: example

89

Dividend irrelevancy theorem

89

90

Home-made dividends

• Underlying idea behind dividend irrelevancy theoremcan also be understood by the concept home madedividends• Investors can do or undo at no cost anything the firm can do

• Example• Investors who want more cash income than the company

distributes as dividends can sell some of their shares atmarket pricesInvestors will not be willing to pay anything for somethingthey can do themselves at a zero cost

91

Irrelevancy of repurchases

• Dividend irrelevancy argument also applies to sharerepurchases• In a perfect market, shares will be repurchased at the market

price stock price will not be affected• In the Miller-Modigliani world, dividends and

repurchases can be viewed as substitutes to each other• Only difference between dividends and repurchases

• When paying dividends, the stock price after the dividend paymentwill be less than in the case of repurchase

• This difference will be compensated by the dividend

92

Dividends vs. repurchases: example• Assume: equity: €10 million (1 million shares); no debt;

non-cash assets: €9 million; cash: €1 million• Payout decision 1: Pay dividend of €1 million

• Dividend per share: €1• Stock price on ex-dividend date: (10mn-1mn)/1mn = €9

• Payout decision 2: Repurchase 100,000 shares at €10• Equivalent to the dividend payout• Share price: (€10mn- €1mn)/(1mn-0.1mn) = €10

• Summa summarum for shareholders:• Decision 1: €9+ €1; Decision 2: €10

93

“Middle of the roaders”:Dividends are irrelevant

• A company’s value is not affected by its dividendpolicy• Doesn’t mean payout decisions are random, they should be

based on the life cycle of the firm• Young, growth companies retain and reinvest all earnings to

maximize the cash for investments in positive-NPV projects• Maturing, profitable companies see positive-NPV investments

disappear over time and are left with excess cash that enable largepayouts

• Fixing debt policy, payout decisions are by-product ofinvestments and profitability

94

Life cycle of the firm:Apple’s cash holdings

“They have a ridiculousamount of cash… There is nofeasible acquisition that Applecould do that would need thatmuch cash” Douglas Skinner,Chicago Booth School ofBusiness

“On March 19, 2012, Appleannounced it would pay aquarterly dividend of $2.65per share and spend 10 billionfor share buybacks.”

95

“Right-Wing”:Dividends are valuable

• In practice, firms do not behave as if dividends areirrelevant• E.g., Dividend smoothing

• Natural clientele of investors that prefer regular, stable cashdividends• Legally restricted financial institutions, older individual investors• Does supply of dividend paying firms meet demand? If so, no need

to change dividend policy (middle-of-the-roaders win)• Management can use dividend policy to signal their private

information about the future prospects of the company• Dividend increases send good news about cash flows and earnings• Dividend cuts or omissions send bad news

96

• Most convincing: Commitment to dividends can act asa disciplinary mechanism

• Investors demand high dividends because they do notfully trust the managers with free cash flow

If not paid out, surplus cash can be used for empire-buildingor excessive executive pay and perk consumption (or both)Dividends can also force managers to raise additionalfinancing from capital markets which comes with externalforces of discipline

“Right-Wing”:Dividends are valuable

97

“Left-wing”: Dividends and taxes• If dividends are taxed relatively more than capital

gains (as they are in many countries), companiesshould distribute a relatively smaller fraction of theirprofits as dividends and a relatively larger fraction asrepurchases

• Example: What is the current price of two identicalfirms, except that one pays dividend (firm B) while theother pays no dividend (firm A)?• Suppose that the tax rate on capital gains is zero and the tax

rate on dividends is 30% for all investors• Assume a discount rate of 10% a year

98

Firm A Firm B(No dividend) (High dividend)

Next year's price 110 100Dividend 0 10Total pretax payoff 110 110Today's stock price PA = 100 PB = ?Capital gain 10 100 - PB

Taxes 0 3After-tax gain 10 7 + (100 - PB)

“Left-wing”: Dividends and taxes

99

• We find the equilibrium level of PB by equating theafter-tax rates of returns on the two firms

10/100 = [7 + (100 - PB)] / PB

PB = 107 / 1.1 = 97.27

• PB is less than PA (= 100)• More generally, whenever the tax rate on dividends is

higher than the tax rate on capital gains, PB would beless than PA

“Left-wing”: Dividends and taxes

100

Postponing capital gains tax

• Unlike dividend tax, capital gains tax can be postponed• Assume: An investor’s stock portfolio includes several

stocks with capital gains and losses on paper• Investor wants to sell stocks with paper gains

• Solution: Sell also stocks with losses on paper• Use realized losses to offset capital gains in personal taxation• Repurchase these stocks (or similar stocks) at a price lower than

original purchase price, possibly after a delay

• In 2004, the Finnish Supreme Administrative Courtdeclined for the first time the tax deduction for such aloss realizing transaction (in an extreme case)

101

Dividends and taxes in Finland• In Finland, corporate taxation is linked to financial

reporting• Corporate tax is paid from reported earnings before tax• In practice, companies can delay paying corporate taxes by

managing earnings downward, BUT• Companies cannot pay dividends without reporting profits

• Current corporate tax rate in Finland is 20%• Capital income – interest income, capital gains, and

dividends – is taxed using a 30% rate (32% for incomeabove €40,000)• However, only 85% of dividend income from publicly listed

companies is considered taxable in personal taxation• Some investor categories, such as foundations and pension funds,

are not subject to taxation

102

Dividends and taxes in Finland

• Both capital gains and dividends are double taxed• First at the company level at the corporate tax rate• Second at the investor level at the capital income tax rate

• Foreign investors are subject to the tax laws of theirhome country

103

Empirical evidence

• The empirical evidence of which of these views(leftist, rightist, or middle-of-the-roader) is mostcorrect seems ambiguous There is some truth to all

104

Lecture 4

IPOsGuest lecturer: Antti Niini

105

Lecture 5

Capital structure and valuation –Part 1

Overview – Part 1

• Irrelevance of capital structure• Modigliani and Miller (1958) Proposition 1: Value of a

business is independent of its financing decisions• How leverage affects returns

• Higher expected return to shareholders• How leverage affects risk

• Higher risk faced by shareholders• Financial innovation

• Angel or evil?

106

107

Debt ratios in the US

Average Debt Ratios in Europe

108

Debt ratios across industries

109

110

MM on Capital structure

• Modigliani-Miller (1958, 1963)• Assume:

(1) Markets are perfect(2) No taxes(3) Symmetric information(4) Firms’ future cash flows are independent of capital structure

• Given these assumptions, the market value of a firm isindependent of its capital structure (= mix of debt and equity)

• Intuition: If (1)-(4) hold, an investor can do or undo whateverthe firm doesà “Home-made leverage”

111

Irrelevance of capital structure: example• Consider two firms which generate identical streams of

operating income:• Firm U: Unlevered. Value of equity (EU) = Value of firm (VU)• Firm L: Levered. Value of equity (EL) = VL - DL (value of debt)

• (a) Consider a 10% investment in Firm U:• Investment 0.1· VU

• Return 0.1· Profit

• (b) Consider a 10% investment in debt and equity of Firm L:• Investment 0.1· (DL + EL) = 0.1· VL

• Return 0.1· Interest + 0.1 · (Profit - Interest) = 0.1· Profit

• Since portfolios (a) and (b) have the same payoff, they musthave the same equilibrium price: VU= VL

112

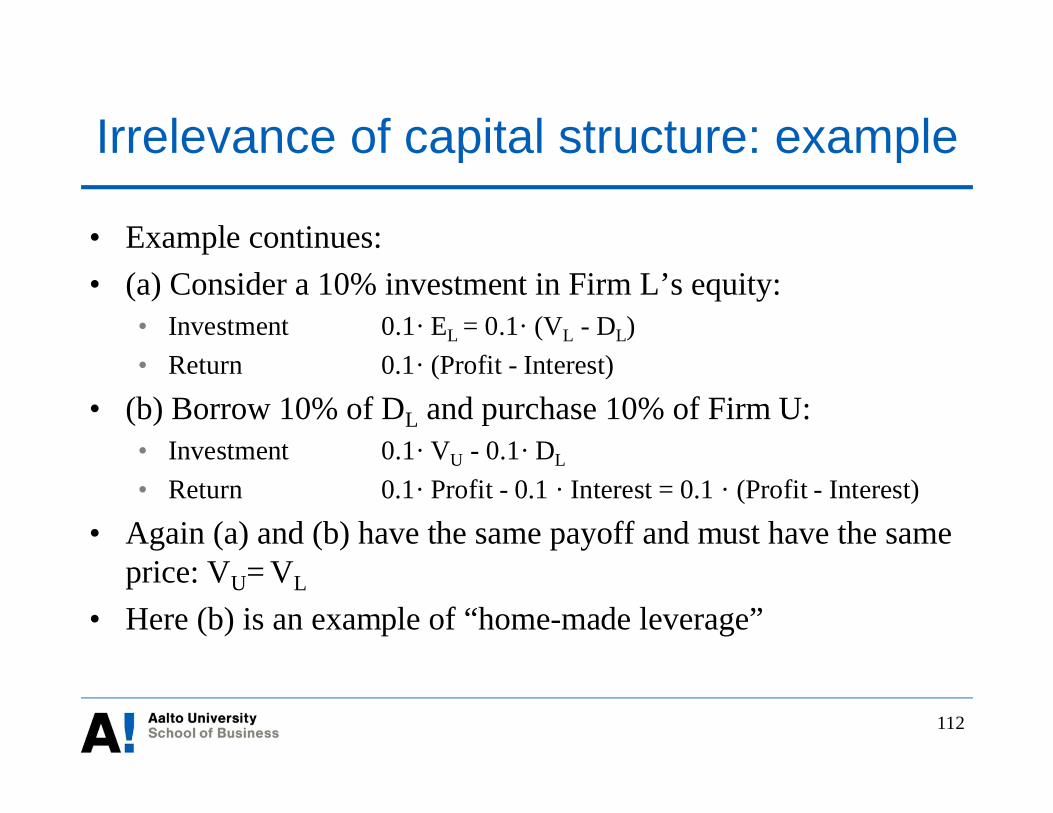

Irrelevance of capital structure: example

• Example continues:• (a) Consider a 10% investment in Firm L’s equity:

• Investment 0.1· EL = 0.1· (VL - DL)• Return 0.1· (Profit - Interest)

• (b) Borrow 10% of DL and purchase 10% of Firm U:• Investment 0.1· VU - 0.1· DL

• Return 0.1· Profit - 0.1 · Interest = 0.1 · (Profit - Interest)

• Again (a) and (b) have the same payoff and must have the sameprice: VU= VL

• Here (b) is an example of “home-made leverage”

113

How leverage affects returns: example

• Assume an unlevered firm with:• 1000 shares outstanding• Price $10 per share• Expected earnings $1500 per year, to be paid out as

dividends• Expected return:

• $1.50 per share / $10 per share = 15%• Now, suppose that:

• The firm issues $5000 worth of debt at 10% interest• Uses the proceeds to buy back 500 shares

114

How leverage affects returns: example

• M-M proposition says the value of the firm isunchanged, i.e. $10,000• Since value of debt = $5000, value of equity must be $5000

and price per share = $10 as before• BUT! With leverage:

Expected earnings $1500- Interest $500= Dividends $1000

Dividend per share = $2 per share.

Expected return = $2/$10 = 20% > 15%!

115

Earnings and return: all equity financing

116

Earnings and return: 50% debt financing

117

Borrowing and EPS

118

Individual investors can replicateleverage

• Investor borrows $10 at 10% and buys another share ofthe unlevered firm

• Expected return is the sameà VU=VL!

119

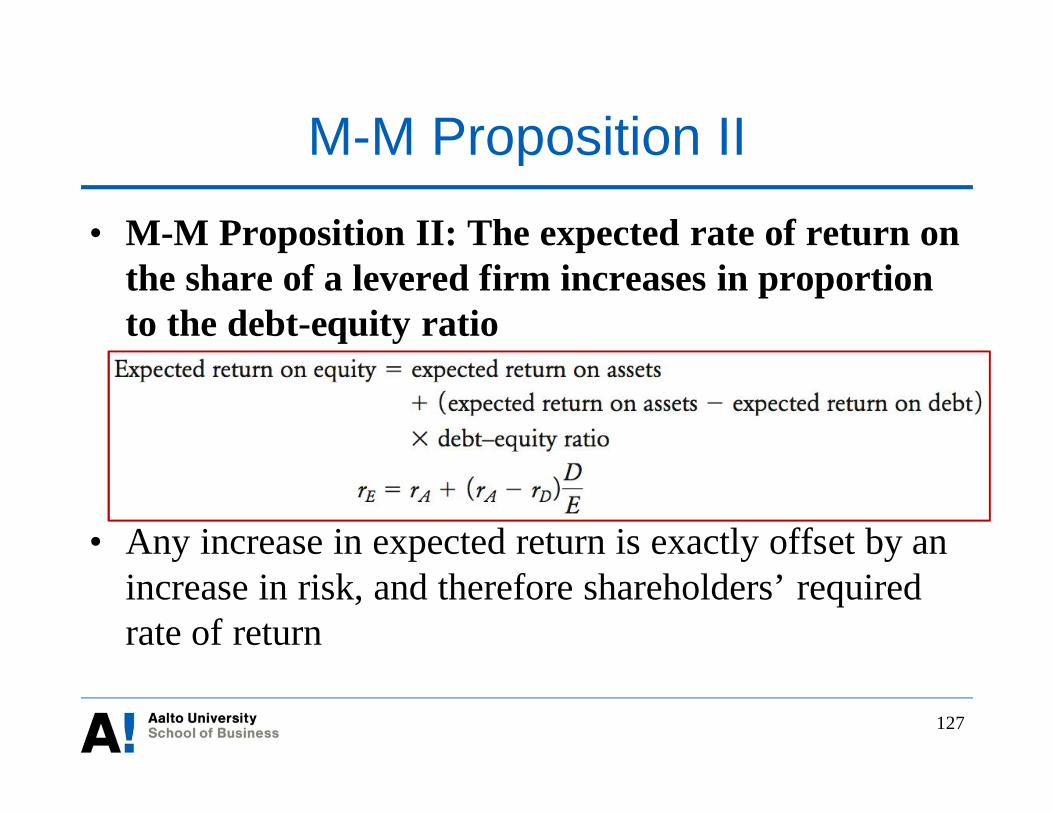

M-M Proposition I

• M-M Proposition I: The market value of any firm isindependent of its capital structure

• Leverage increases expected EPS but not the shareprice

• Increase in expected EPS is exactly offset by increasein the rate at which earnings are discounted

• M-M Proposition II explains how

120

How leverage affects returns

• No-tax weighted average cost of capital (rA, WACC) isas follows:

• where rD and rE refer to cost of debt and equity,respectively

,EDA rED

ErED

DrWACC+

++

==

121

How leverage affects returns• Re-arranging the equation yields:

As D/E increases, rE increases• Why? What happens to risk of shareholders?

• where ßA, ßD, and ßE refer to the betas of the firm’s assets,debt, and equity, respectively

).( DAAE rrEDrr -+=

EDA EDE

EDD bbb

++

+=

122

How leverage affects returns:riskless debt

0

0.02

0.04

0.06

0.08

0.1

0.12

0.14

0.16

0 0.5 1 1.5 2 2.5 3 3.5

D/E

Req

uire

dra

teof

retu

rn

rArDrE

123

How leverage affects returns:risky debt

0

0.02

0.04

0.06

0.08

0.1

0.12

0 0.5 1 1.5 2 2.5

D/E

Req

uire

dra

teof

retu

rn

rArDrE

124

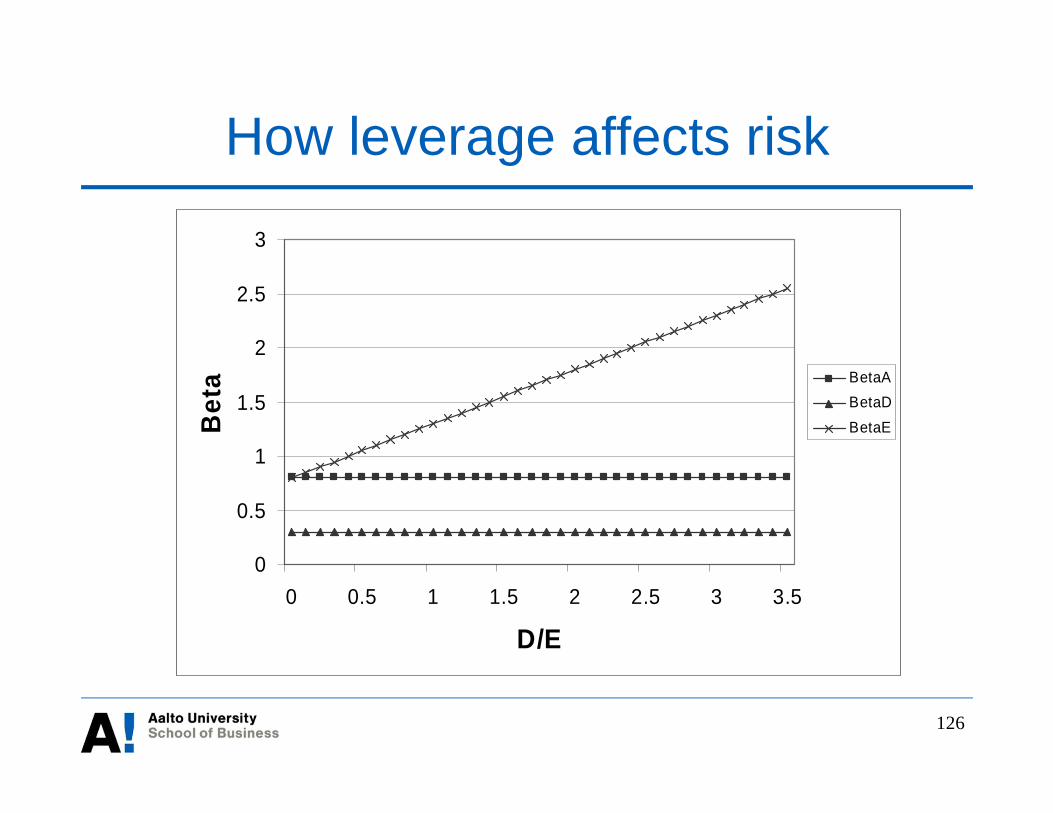

How leverage affects returns

• Rearranging yields

As D/E increases, ßE increasesRaising D/E is analogous to borrowing to buy thestock

• Q: Why does the expected return on equity go up from15% to 20%?• A: Because the stock is more risky

).( DAAE ED bbbb -+=

125

How leverage affects returns: example

• Example revisited:• Suppose actual earnings = $500

• Unlevered firm:• Return = $0.5/$10 = 5%

Return is 15% - 5% = 10 percentage points below expected• Levered firm:

• Return = 0/$10 = 0%Return is 20% - 0% = 20 percentage points below expected

The equity beta of the levered firm is twice the equitybeta of the unlevered firm (assuming riskless debt)

126

How leverage affects risk

0

0.5

1

1.5

2

2.5

3

0 0.5 1 1.5 2 2.5 3 3.5

D/E

Bet

a BetaABetaDBetaE

127

M-M Proposition II

• M-M Proposition II: The expected rate of return onthe share of a levered firm increases in proportionto the debt-equity ratio

• Any increase in expected return is exactly offset by anincrease in risk, and therefore shareholders’ requiredrate of return

128

Financial innovation

• Important implication of the irrelevancy theorem isthat innovations creating exotic financial products donot add value• This is not true if the assumptions of the model do not hold

Financial innovations are likely to be successful onlyif they take advantage of the loopholes in the model

129

Financial innovation

• Qualities that can make financial innovations beneficialfor investors and perhaps the whole economy:• Reduction of transaction costs• Improvement in liquidity• Reallocation of risk• Reduction of taxes• Circumvention of regulation• Reduction of agency costs that arise from conflicts of interest

between different stakeholders

Example: The case of Kinder Morgan“…Kinder Morgan has created value ($12 billion) from nothing… Of course, it did this by reversingfinancial engineering, which is a bit of an embarrassment, but a contingent one. If financialengineering can have negative value then it can have positive value too. Some ways of slicing upcash flows seem to be more valuable than others, so it can be worth billions of dollars to find justthe right way to slice up your cash flows. If you're a skeptic of financial engineering this shouldtrouble you, even though Kinder Morgan is scrapping its particular flavor of financial engineeringas over-complicated and unworkable.”

“Now, there are explanations of where Kinder Morgan found all this value, but they mostly won't bethat satisfying for skeptics... (rules out other explanations)… But there's one other place to look forvalue. If you see a piece of financial engineering that makes everyone involved better off, then areasonable guess is that it makes somebody who's not involved worse off. There are various possibleuninvolved parties, but none is more popular with financial engineers than the IRS. If you canshuffle some papers in a way that saves money on taxes, why wouldn't you?”

“… But mostly it seems to have created some value from the usual place: by reducing its tax bill.And no one doubts that financial engineering is good for that…”

Source: http://www.bloombergview.com/articles/2014-08-11/pipeline-giant-reverse-engineers-itself-12-billion

130

Financial Innovation: Word of caution• Not enough studies on causes and consequences of financial

innovation• Challenges laid out by Lerner and Tufano (2011)

• Financial crisis in 2007-2009• Volcker: ”I wish someone would give me one shred of neutral evidence that financial

innovation has led to economic growth”• Stiglitz: ” Regrettably, many of the worst elements of the US financial system - toxic

mortgages and the practices that led to them - were exported to the rest of the world…It was all done in the name of innovation, and any regulatory initiative was fought awaywith claims that it would suppress that innovation. They were innovating, all right, butnot in ways that made the economy stronger. Some of America's best and brightest weredevoting their talents to getting around standards and regulations designed to ensurethe efficiency of the economy and the safety of the banking system. Unfortunately, theywere far too successful, and we are all - homeowners, workers, investors, taxpayers -paying the price.”.

131

Financial InnovationèSystemic Risk

132

Source: http://urbanlogic.org/2008credit-crisis-goodbankio-and-high-transparency-impacts-aware-banking/

133

Lecture 6

Capital structure and valuation –Part 2

134

Overview• Capital structure theory

• Trade-off theory• Tax benefit of debt• Disciplinary benefit of debt• Financial distress costs• Agency costs of debt

• Pecking order theory• Debt policy in practice• Valuation

• Adjusted discount rate method• Adjusted present value method

0% 5% 10% 15% 20% 25% 30% 35% 40% 45%

Ireland

Finland

United Kingdom

Estonia

Switzerland

Sweden

Germany

France

United States

Tax rate, %

135

Corporate income tax rates around theworld

Source: OECD

136

Corporate taxes and capital structure:example

Unlevered LeveredEBIT 1000 1000Interest (5% on 1000) 0 50EBT 1000 950Corporate tax (20%) 200 190CF to shareholders 800 760CF to debt holders 0 50

CF to share- and debt-holders 800 810Interest tax shield(= 20% x Interest) 0 10

137

Corporate taxes and capital structure

• Interest tax shield = tax savings resulting fromdeductibility of interest payments• Assume that 1000 debt is permanent• PV of stream of interest tax shields = 10/0.05

= 200 (i.e., 20% of 1000)

• PV of interest tax shield assuming fixed, perpetual debt= [(Debt ·Interest(%)] · Tax(%) / Interest(%) = Debt · Tax(%)

VL = VU + tc·Debt

If we incorporate only corporate taxes into the MMmodel, optimal capital structure should be 100% debt?!

138

Corporate and personal taxes andcapital structure: example

Unlevered LeveredEBIT 1000 1000Interest (5% on 1000) 0 50EBT 1000 950Corporate tax (20%) 200 190CF to shareholders before personal taxes 800 760CF to shareholders after personal taxes (30%) 560 532CF to debt holders before personal taxes 0 50CF to debt holders after personal taxes (30%) 0 35

CF to share- and debt-holders after personal taxes 560 567Value of tax shield 0 7

139

Corporate and personal taxes andcapital structure

140

Relative advantage formula

• The relative advantage formula shows the effect ofconsidering personal taxes

• If (1 TP)/[(1 TPE) (1 TC)] >1 debt is preferred• If (1 TP)/[(1 TPE) (1 TC)] <1 equity is preferred• The relative advantage of debt depends on the

differential personal tax rate

1-Tp

1-TpE( ) 1-Tc( )

141

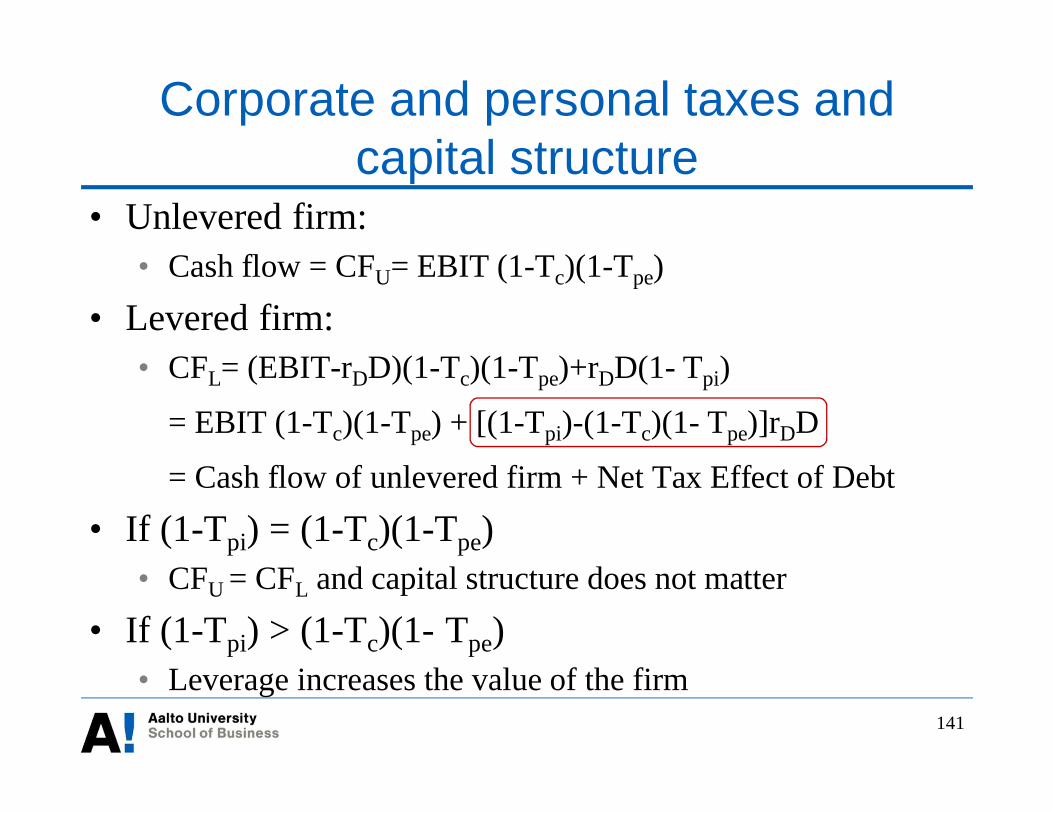

Corporate and personal taxes andcapital structure

• Unlevered firm:• Cash flow = CFU= EBIT (1-Tc)(1-Tpe)

• Levered firm:• CFL= (EBIT-rDD)(1-Tc)(1-Tpe)+rDD(1- Tpi)

= EBIT (1-Tc)(1-Tpe) + [(1-Tpi)-(1-Tc)(1- Tpe)]rDD

= Cash flow of unlevered firm + Net Tax Effect of Debt• If (1-Tpi) = (1-Tc)(1-Tpe)

• CFU = CFL and capital structure does not matter• If (1-Tpi) > (1-Tc)(1- Tpe)

• Leverage increases the value of the firm

142

Leverage clientelesand optimal capital structure

• If (1-Tpi) = (1-Tc)(1- Tpe), capital structure does notmatter

• Suppose now: Tpe = 0 (defer capital gains until death)• Then, capital structure does not matter if Tpi = Tc

• Variation in leverage ratios across firms and in marginaltax rates among investors gives also rise to leverageclienteles• Some investors prefer levered firms for tax reasons, others

prefer unlevered firms

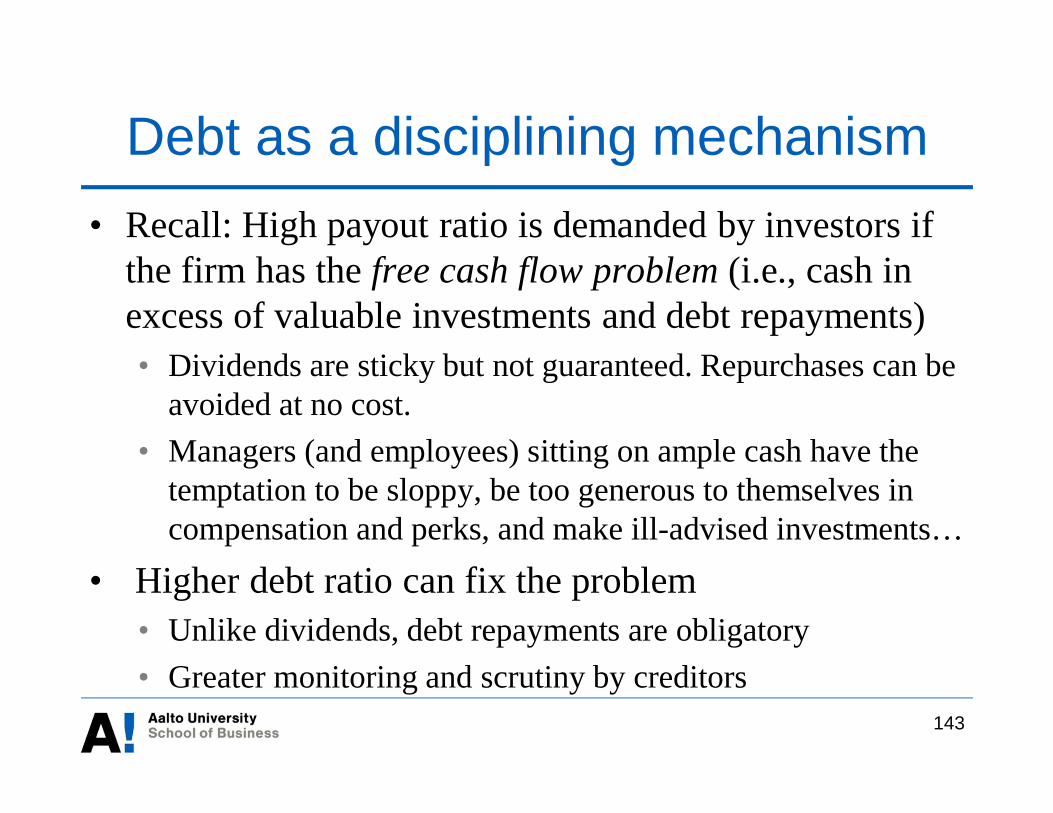

Debt as a disciplining mechanism• Recall: High payout ratio is demanded by investors if

the firm has the free cash flow problem (i.e., cash inexcess of valuable investments and debt repayments)• Dividends are sticky but not guaranteed. Repurchases can be

avoided at no cost.• Managers (and employees) sitting on ample cash have the

temptation to be sloppy, be too generous to themselves incompensation and perks, and make ill-advised investments…

• Higher debt ratio can fix the problem• Unlike dividends, debt repayments are obligatory• Greater monitoring and scrutiny by creditors

143

144

Costs of Debt: Financial distress

• Firms with high debt ratios face the likelihood offinancial distress and even bankruptcy

• Experienced when debt repayments are covered withdifficulty or cannot be coveredExpected Cost of F.D.= Probability of F.D. x Costs of F.D.

• At small debt levels financial distress is unlikely takingon extra debt is not too costly

• At high debt levels taking on extra debt can be very costlydue to increased likelihood of financial distress

145

Costs of financial distress: examples

• Costs of financial distress without bankruptcy• Damage to customer & supplier relations and talent retention• Agency costs /conflict of interests between borrowers and

creditors• e.g., Risk shifting, refusing to contribute new equity capital• Credit rationing and debt covenants

• Costs of financial distress with bankruptcy• Direct costs

• Legal and administrative costs

• Indirect costs• Management of bankrupt firm

146

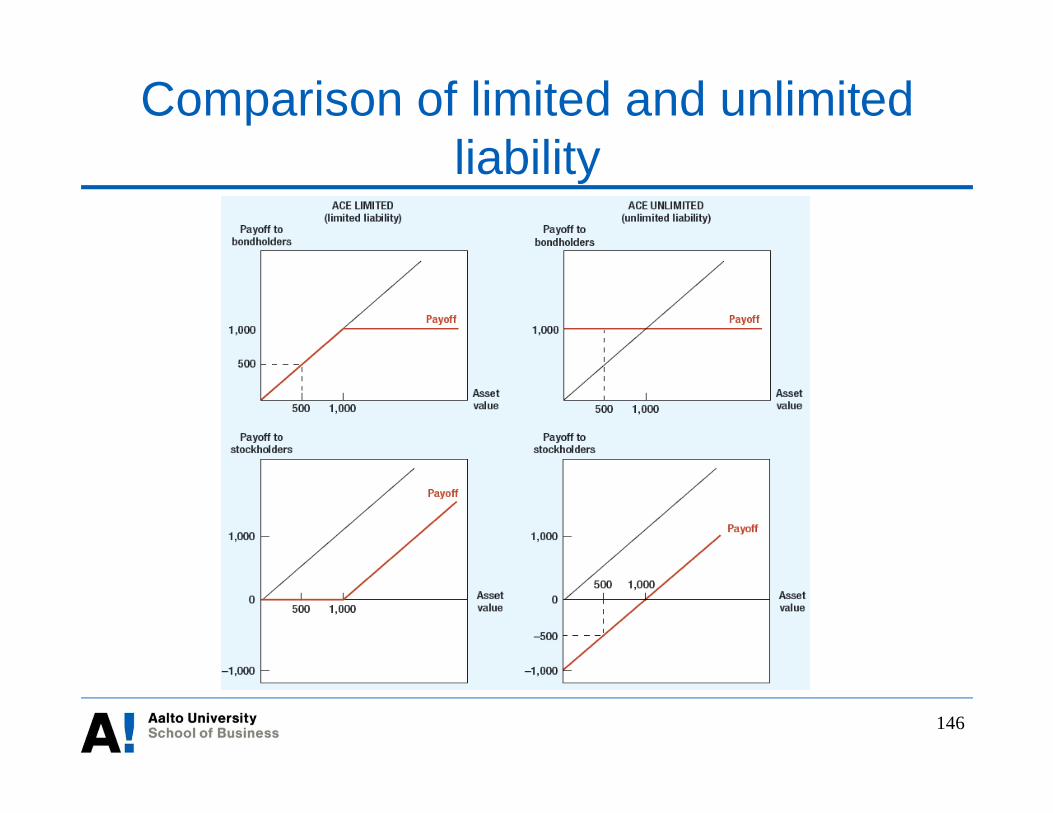

Comparison of limited and unlimitedliability

147

Payoff to security holders of a limitedliability company

148

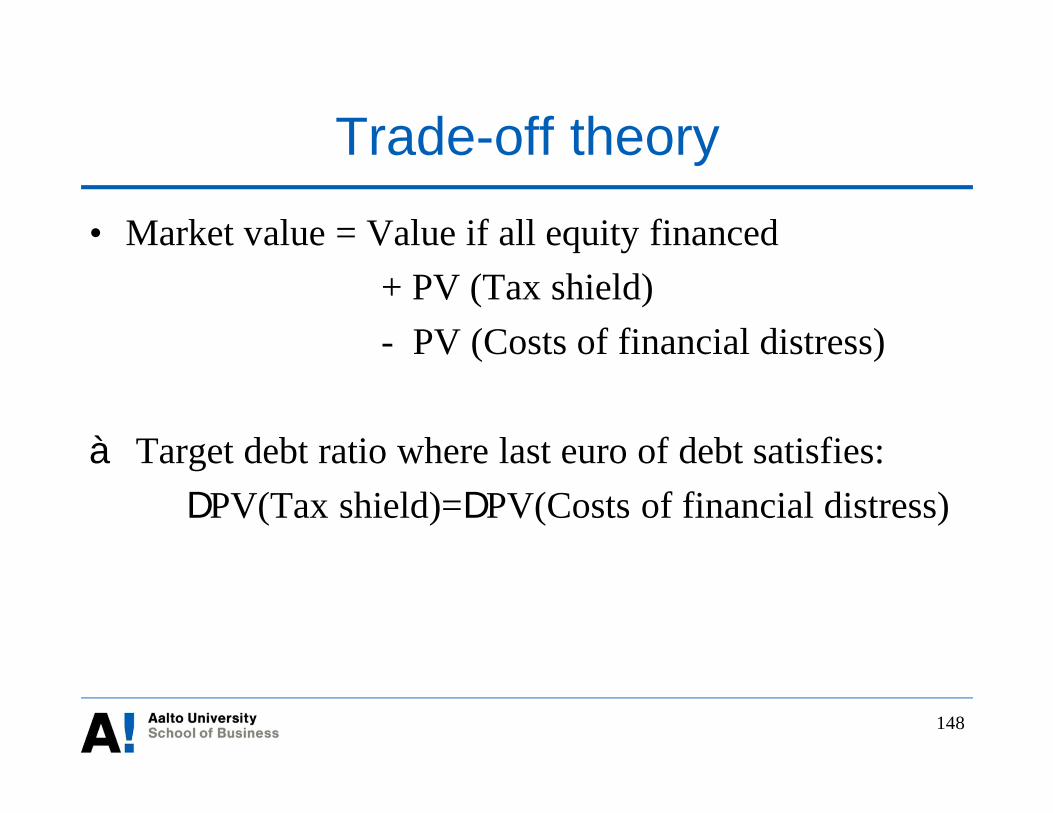

Trade-off theory

• Market value = Value if all equity financed+ PV (Tax shield)- PV (Costs of financial distress)

à Target debt ratio where last euro of debt satisfies:DPV(Tax shield)=DPV(Costs of financial distress)

149

Trade-off theory

Do firms have a target debt ratio?

150

Source: John R. Graham and Campbell Harvey, "The Theory and Practice ofCorporate Finance: Evidence from the Field," Journal of Financial Economics60, 2001, pp. 187-243.

37%

34% 10%

19%

Trade-off theory: Empirical Evidence• Explains, for example:

• Why high-tech, growth companies use little debt• Why larger firms and firms with tangible assets use more debt• Firms with long-lasting relationships with customers/suppliers use less

debt

• Cannot explain:• Why highly profitable companies use little or no debt (e.g., Apple,

Microsoft, Johnson and Johnson etc.)– Graham (2000): Average tax-paying firm can add 7.5% to firm value

by increasing leverage moderately• Why interest tax shields do not add to firm value (Fama and French, 1998)• Large and permanent variations within industries• Variations across time and countries

151

152

Pecking order theory: motivation• Starts with asymmetric information• Press releases of two seemingly identical companies:

• Company A will issue 120 million EUR five-year seniordebt

• Company B plans to issue 1.2 million new shares ofcommon stock; expects to raise 120 million EUR

• Stock prices based on current information: 100 – truevalue could be higher or lower

• What do rational investors learn from theseannouncements?

153

Pecking order theory

• Assume managers are better informed than investorsand maximize the wealth of existing shareholders• Firm will sell equity only if management knows their stock

is overvalued (i.e., true value < 100)• If firm announces an equity issue, market participants can

infer that management thinks the shares are overvalued Negative stock price reaction!

• If there is no other way to raise capital, the fear of adversestock price reaction can even lead to rejection of a positiveNPV investment

154

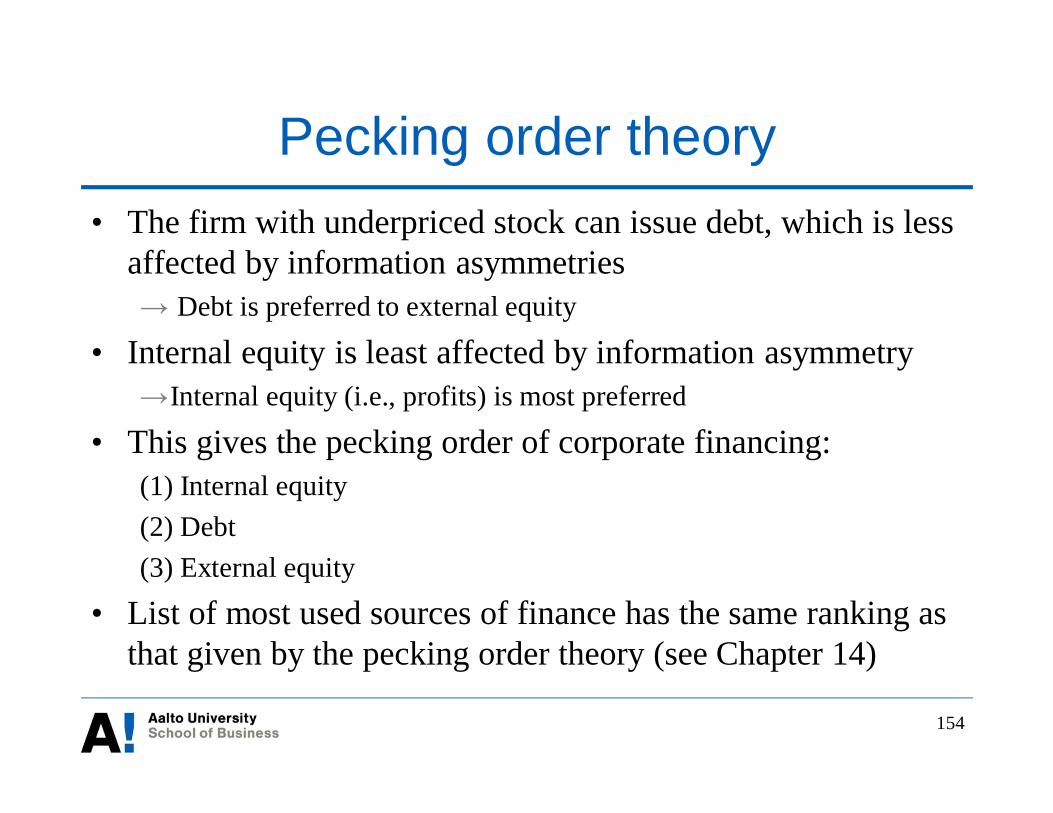

Pecking order theory• The firm with underpriced stock can issue debt, which is less

affected by information asymmetriesDebt is preferred to external equity

• Internal equity is least affected by information asymmetryInternal equity (i.e., profits) is most preferred

• This gives the pecking order of corporate financing:(1) Internal equity(2) Debt(3) External equity

• List of most used sources of finance has the same ranking asthat given by the pecking order theory (see Chapter 14)

155

Choice of debt level in practice

Source: Bancel and Mittoo (2004)

156

Valuation

• How to value a project including the valuecontributed by financing decisions?

• Two ways:1. Adjust the discount rate

• Modify the discount rate to reflect capital structure,bankruptcy risk, and other factors

2. Adjust the present value• Assume an all equity financed firm and then make

adjustments to value based on financing

• Either, not both!

157

After-tax weightedaverage cost of capital

• The after-tax weighted average cost of capital:

• Important: WACC is applicable to projects that are“carbon copies” of the company. Otherwise:• If investment project or division is riskier (less risky) than

company on average, it needs to use a larger (smaller)discount rate

• If the project will lead the company to change its debt ratiopermanently, WACC should change accordingly

EcD rED

ETrED

DWACC+

+-+

= )1(

After-tax WACC at varying debtratios

158

Differently from the MM-based graph, WACC decreasesas debt ratio increases thanksto tax-deductibility of interest!

How to calculate WACC at adifferent debt ratio?

à Follow the three-step process:Step 1: Calculate r = WACC as if

there are no taxes. This alsogives rE at D/E=0

Step 2: Estimate rD at the newD/E and calculate rE at the new

D/EStep 3: Recalculate WACC using

the new weights, rD and rE

Correction: The x-line plots D/E, not D/V.

159

Most common ways of determining thediscount rate in Finland

Source: Keloharju and Puttonen (1995)

160

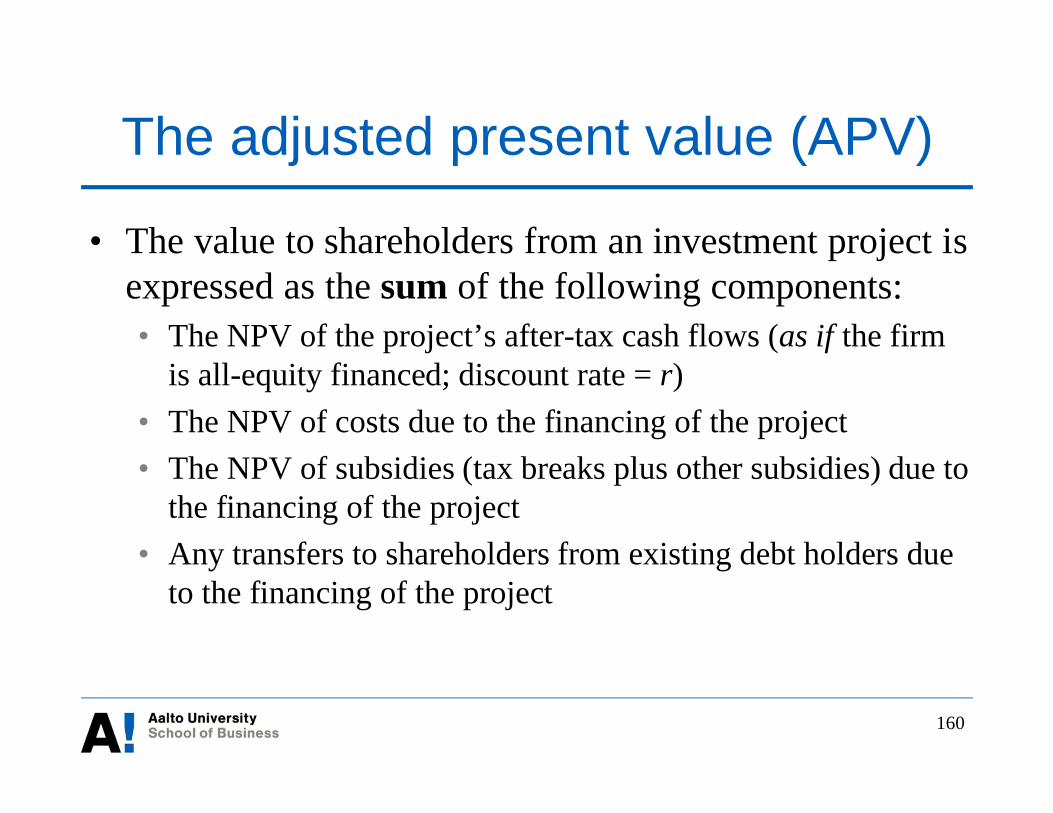

The adjusted present value (APV)

• The value to shareholders from an investment project isexpressed as the sum of the following components:• The NPV of the project’s after-tax cash flows (as if the firm

is all-equity financed; discount rate = r)• The NPV of costs due to the financing of the project• The NPV of subsidies (tax breaks plus other subsidies) due to

the financing of the project• Any transfers to shareholders from existing debt holders due

to the financing of the project

161

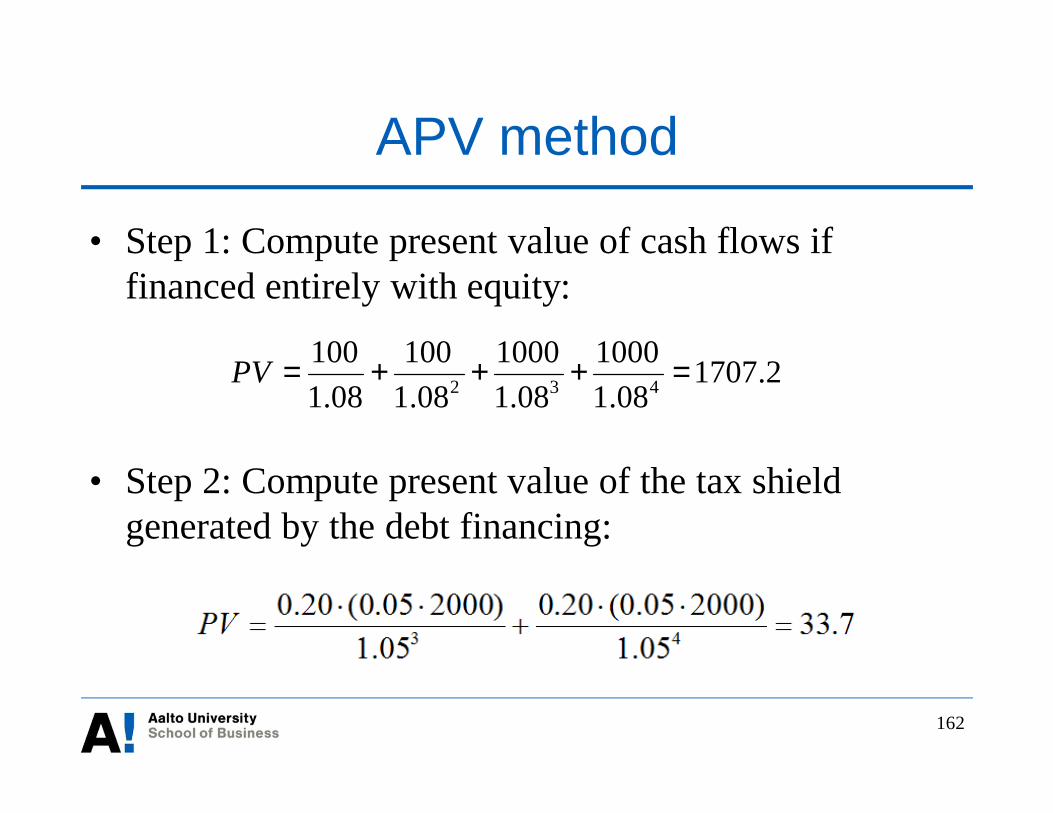

APV method• Example: Consider a project with a cost of capital of 8% if

financed entirely with equity• Project is expected to generate the following after-tax cash flows at the

end of each year:Year 1 Year 2 Year 3 Year 4100 100 1000 1000

• The project will be initially financed with equity capital• At the start of year 3 the firm will repurchase some of its equity and

borrow 2000 to finance for the two remaining years• Risk-free rate is 5% and corporate tax rate is 20%

• What is the present value for the project given the plan fordebt financing?

162

APV method

• Step 1: Compute present value of cash flows iffinanced entirely with equity:

• Step 2: Compute present value of the tax shieldgenerated by the debt financing:

2.170708.1

100008.1

100008.1

10008.1

100432 =+++=PV

163

APV method

• Step 3: The present value of the project given itsoperating and financing aspects is:

• 1707.2 + 33.7 = 1740.9

• Benefits of the APV method:• Exposes each financing side effect distinctly and how much

it adds or takes away from project (and firm) value• In the WACC method, they will all be hidden in the WACC estimate

• Doesn’t require a fixed debt ratio (i.e., continuousrebalancing) assumption as WACC method

Lecture 7

Leasing

164

Overview

• Leasing: key concepts• Operating vs. financial leases• Lease accounting in Finland• Why lease?

• Sensible reasons• Dubious reasons

• Agency problems in leasing and some solutions• Valuation of financial leases• International leasing

165

Leasing volumes by asset type inEurope

Source: Leaseurope, http://www.leaseurope.org/index.php?page=key-facts-figures

166

New leasing volumes in Europe

167

Leasing agreement• Lease = Rental agreement that extends for a year or more and

involves a series of fixed payments• A lease agreement is made between the lessor (= the owner of

the leased property) and the lessee (= the user)• Ownership of the asset makes a difference on

• who gets the salvage value at the end of the lease period• who gets the tax privileges

• Lease agreement gives lessee control over the asset for a pre-specified period of time• At end of the leasing period lessee often has the option to purchase the

asset from lessor• Typical leased assets include automobiles, airplanes, machinery

and industrial equipment, computers, real estate

168

Operating and financial leases: generalcharacteristics

• Operating lease• Short-term lease• Cancelable at the option of the lessee

• Financial lease• Non-cancelable• Long-term lease for most of the asset’s economic life

Operating leases are much riskier for the lessor thanfinancial leases

In operating leases, lessor must consider the risk that theasset will stay idle at least for some of the time

169

Leasing: further definitions

• Full-service or rental lease• Lessor maintains, insures, and pays taxes on the equipment

• Net lease• Lessee maintains, insures, and pays taxes on the property

• Sale and leaseback• Arrangement where a firm sells an asset to the lessor and

leases it back from the lessor• Leveraged lease

• Financial lease where the lessor borrows part of the purchaseprice using the leased equipment as collateral

170

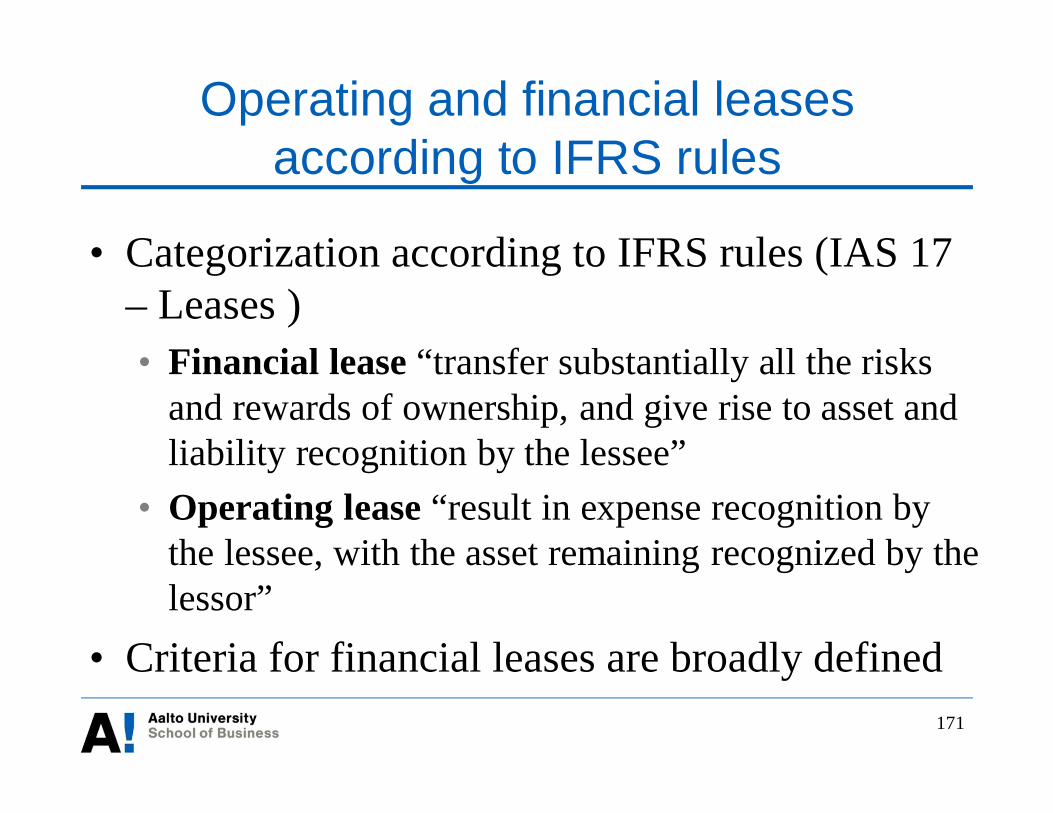

Operating and financial leasesaccording to IFRS rules

• Categorization according to IFRS rules (IAS 17– Leases )• Financial lease “transfer substantially all the risks

and rewards of ownership, and give rise to asset andliability recognition by the lessee”

• Operating lease “result in expense recognition bythe lessee, with the asset remaining recognized by thelessor”

• Criteria for financial leases are broadly defined171

Lease accounting in Finland

• Listed Finnish companies have to conform toIFRS rules• Financial leases have to be reported on the balance

sheet as equivalent ownership of the asset with thelease obligations capitalized and shown on theliability side

• Non-listed Finnish companies do not need toreport financial leases on their balance sheets

172

Accounting Analysis

• Objective: To what extent the firm’s accountingnumbers capture its business reality?

• Identify any significant distortions where there isaccounting flexibility and using cash flow informationand notes to adjust accounting numbers to “undo” thedistortions

• Sound accounting analysisè sound financial analysis

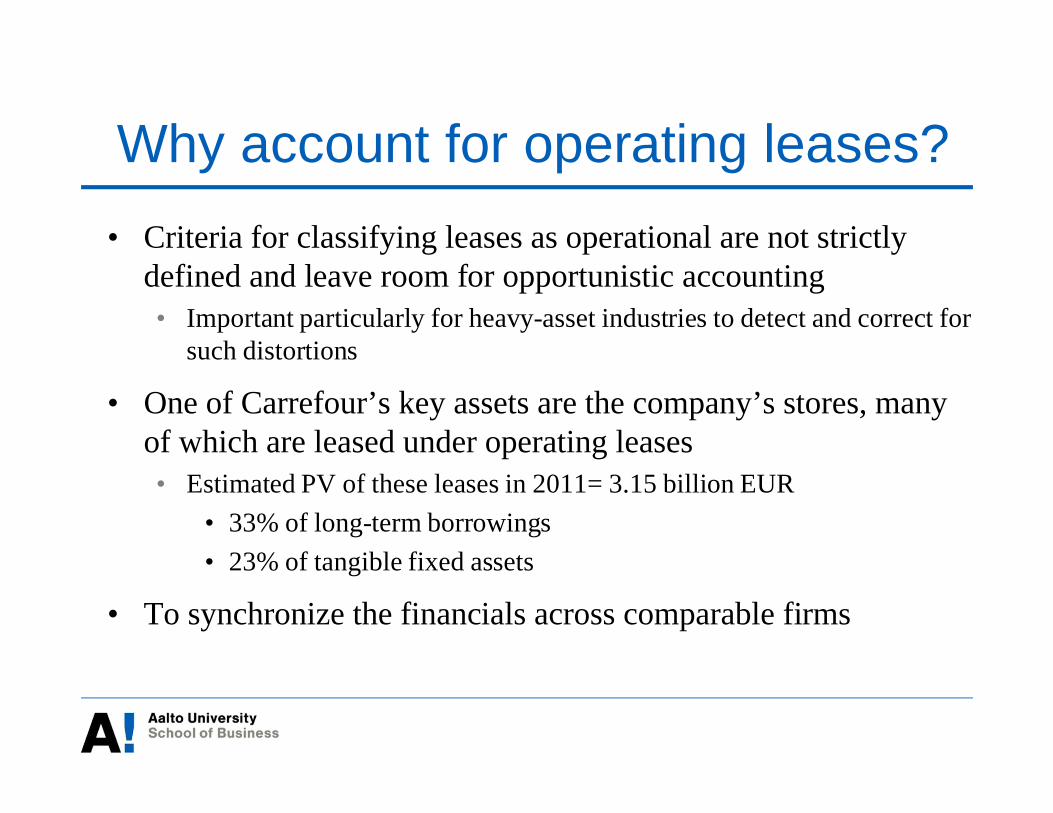

Why account for operating leases?“On December 27, 2011, the Group sold a portfolio of 97 supermarketproperties owned by Carrefour Property for 365 million euros. Thesupermarkets will continue to be operated under the Carrefour Marketbanner under long-term fixed rent leases with an indexation clause.

The transaction qualifies as a sale-and-leaseback transaction under IAS 17 –Leases. The leases with the new owner of the properties, for an initial term of12 years with multiple renewal options, fulfill the criteria for classification asoperating leases, as substantially all the risks and rewards incidental toownership of the asset are retained by the lessor.

The properties were sold at market price and the capital gain, net oftransaction costs, was recognized in full in the 2011 income statement in theamount of 229 million euros.”

Source: Carrefour, 2011 Financial Report

• Criteria for classifying leases as operational are not strictlydefined and leave room for opportunistic accounting• Important particularly for heavy-asset industries to detect and correct for

such distortions

• One of Carrefour’s key assets are the company’s stores, manyof which are leased under operating leases• Estimated PV of these leases in 2011= 3.15 billion EUR

• 33% of long-term borrowings• 23% of tangible fixed assets

• To synchronize the financials across comparable firms

Why account for operating leases?

Sensible reasons for leasing

• Given the Modigliani-Miller assumptions, thereis no difference between owning an asset andleasing an assetLeasing policy is just a special case of financialpolicy, and can matter if at least one of thefollowing is true:• Financial policy affects a firm’s tax obligations• Financial policy affects contracting costs• Financial policy affects real investment policy

176

Sensible reasons for leasing

• Convenience• Flexibility• Shifting the risk of obsolescence• Standardization leads to low costs• Lessor may be able to use tax breaks from

depreciation more effectively• Additional source of financing, less susceptible

to financial distress177

Dubious reasons for leasing

• Leasing avoids internal capital expenditurecontrols

• Leasing preserves capital• Leases may be off balance sheet financing• Leasing increases book rate of return

• In early years, lease payments < interest + depreciation• Off-balance sheet assets may never appear in the

denominator

178

Agency problems and leaseprovisions

• Leasing separates rights to the cash flows of the asset from itssalvage value

• This generates incentives for agency problems such as assetabuse, under-maintenance

• Provisions in lease contracts are designed to solve theseproblems. For example:

• Deposits and penalty clauses• Options to extend/purchase or cancel• Restrictions to sublease• Metering: a contractual provision that ties lease payments to some measure of

the intensity of the asset’s use• Tie-in sale: a contractual requirement to use a specified nondurable input in the

operation of the leased asset

179

Evaluating financial leases• Example: A company is evaluating the lease of a new

computer (cost: 150)• The computer’s economic life is 5 years after which it is

obsolete• The annual lease payments are 31, payable in five

installments, the first being payable when the contract issigned

• The firm can borrow at the long term rate of 9%, the tax rateis 20%, and depreciation is straight line in 5 years (the firstinstallment after one year)

• Should the company lease or borrow to buy theasset?

180

Evaluating financial leases

• The NPV of the lease contract is +17.1The company should lease rather than borrow to buy thecomputer

181

Yr 0 Yr 1 Yr 2 Yr 3 Yr 4 Yr 5

Initial cost 150

Depreciation 30 30 30 30 30

Lost depreciation tax shield -6 -6 -6 -6 -6

Lease payment -31 -31 -31 -31 -31

Tax shield on lease payment 6.2 6.2 6.2 6.2 6.2

Cash flow 125.2 -30.8 -30.8 -30.8 -30.8 -6

NPV at after-tax rate 9%* (1-0.20) 17.1

Evaluating financial leases

• Now suppose that the purchase of the computer had aNPV of –2 if the company financed it with debt

Computer should not be purchased if there are no otherfinancing options

• When the possibility of advantageous lease financingis considered, the adjusted present value (APV) of theproject is:• -2 + 17.1 = 15.1

The company should go ahead with the project andlease the computer

182

Formal analysis of lease vs. borrow to buy• Denote corporate tax rate with Tc, lease payment with

L, and depreciation with Dep• Leasing instead of buying generates the following

income stream every year:• -[(1-Tc)Lt + TcDept ]

This reflects the fact that the lessee will lose the depreciationtax shield in addition to having to pay the lease payments

• Therefore, the NPV of the lease decision (vs. borrow tobuy) is:

where I0 is the cost of the asset and (1-Tc)r is the after-taxborrowing rate for the company

183

å= -+

-+-=

n

tt

c

tctc

rTLTDepTILeaseNPV

10 ])1(1[

)1()(

When is leasing most taxadvantageous?

• Other things being equal, the potential gains tolessor and lessee are highest when:• The lessor’s tax rate is substantially higher than the

lessee’s• The depreciation tax shield is received early in the

lease period• The lease period is long and the lease payments are

concentrated toward the end of the period• The interest rate is high

184

Cross-border leasing• Cross-border leasing contracts can take advantage of

asymmetric tax treatment of leasing in the countries thelessee and the lessor are domiciled

• Multinational companies may use cross-border leasing• To limit the ownership of assets by subsidiaries in politically

unstable countries• In the event of nationalization, there will be higher chance of

recovering assets if they are not owned by local subsidiary

• To extract cash more easily from affiliates located incountries that have exchange controls

• Lease payments may be a more acceptable method to repatriate fundsthan dividends, interest, or royalty payments

185

186

Lecture 8

Financial planning

187

Overview

• What is financial planning?• Strategic planning and finance• Long-term planning

• Financial planning models: key concepts• Example of financial planning model• External financing and growth

• Short-term planning• Cash budgeting• Sources of short-term financing

188

What is financial planning?• Financial planning is a process consisting of

(1) Identification: Analyzing the investment and financingchoices open to the firm(2) Modeling: Projecting the future consequences of currentdecisions(3) Decision: Deciding which alternatives to undertake(4) Monitoring: Measuring subsequent performance against thegoals set forth in the financial plan

• It is customary to analyze different scenarios (e.g. bestcase, normal case, and worst case) to find out howvulnerable the financial plan is to its assumptions

189

Contribution of finance to strategicplanning

• Financial tools are used to determine the feasibility ofa strategic plan, given firm’s existing and prospectivesources of funding

• Finance has control of the implementation of strategicplans• Financial analysts prepare cash budgets that help avoid

liquidity problems• Finance also contributes to strategic planning through

risk management

190

Long-term planning: financial planningmodels

• Financial planning models• Help to explore the consequences of alternative strategies• Are particularly useful for firms with changing capital needs

• Growth firms• Financially distressed firms

• Financial planning models often start from identifyingsales• Costs and variables such as net working capital are often

defined as proportional to sales

191

Long-term planning: financial planningmodels

• The outputs of financial planning models are calledpro formas (= projected or forecast financialstatements)• ”Top-down” approach uses macroeconomic and industry

forecasts to establish sales goals• ”Bottom-up” approach forecasts sales on a customer-by-

customer basis• The balancing item, or the plug, is the variable that

adjusts to maintain the consistency of a financial plan

192

Financial planning model: example

• Income statement 2014:

Revenue 2000 - COGS 1800 90% of sales= EBIT 200 - Interest 40 10% of debt= EBT 160 - Tax 64 40% of EBT= Net income 96

Dividends 64 Payout ratio 2/3Retained earnings 32 Net income - div.

193

Financial planning model: example

• Balance sheet 2014:

Assets:Net working capital 200 10% of salesFixed assets 800 40% of salesNet assets 1000

Liabilities & equity:Long-term debt 400Equity 600Totals 1000

194

Financial planning model: example

• Pro forma financial statement for 2015• Assume:

• Sales and operating costs increase by 10%• Interest rates remain at the current level• Dividend policy is unchanged• Fixed assets and net working capital will need to

increase 10% to support the larger sales volume

195

Financial planning model: example

• Pro forma income statement for 2015:

Revenue 2200 10% higher - COGS 1980 10% higher= EBIT 220 - Interest 40 Unchanged= EBT 180 - Tax 72 40% of EBT= Net income 108

Dividends 72 Payout ratio 2/3Retained earnings 36 Net income - div.

196

Financial planning model: example

• Pro forma balance sheet 2015:Assets:Net working capital 220 10% higherFixed assets 880 10% higherNet assets 1100

Liabilities & equity:Long-term debt 400 Temp. held fixedEquity 636 600+36Totals 1036

Requiredexternal financing 64 1100-1036

197

Financial planning model: example

• Pro forma statement of sources and uses of funds for2015:

The company needs additional borrowing of 64

Sources:Retained earnings 36New borrowing 64Total sources 100Uses:Investment in working capital 20Investment in fixed assets 80Total uses 100

198

External financing and growth

• Assuming (as in the example before) that a givenincrease in sales requires a similar increase in assets,the requirement for new investment is simply:• New investment = Growth rate x Initial assets

• Since part of the investment requirement can befinanced with retained earnings, the amount ofrequired external financing is:• Required external financing

= New investment - Retained earnings= Growth rate x Initial assets – Retained earnings

199

External financing and growth• Example continues: Using the above formula, the

required external financing is:• 10% × 1,000 - 36 = 64

This is exactly the same result as that obtained from theearlier financial planning modelA company can finance its growth itself only to the extent itcan generate retained earnings

• The internal growth rate is the maximum rate ofgrowth that a company can achieve without externalfinancing:

AssetsearningsRetainedrategrowthInternal =

200

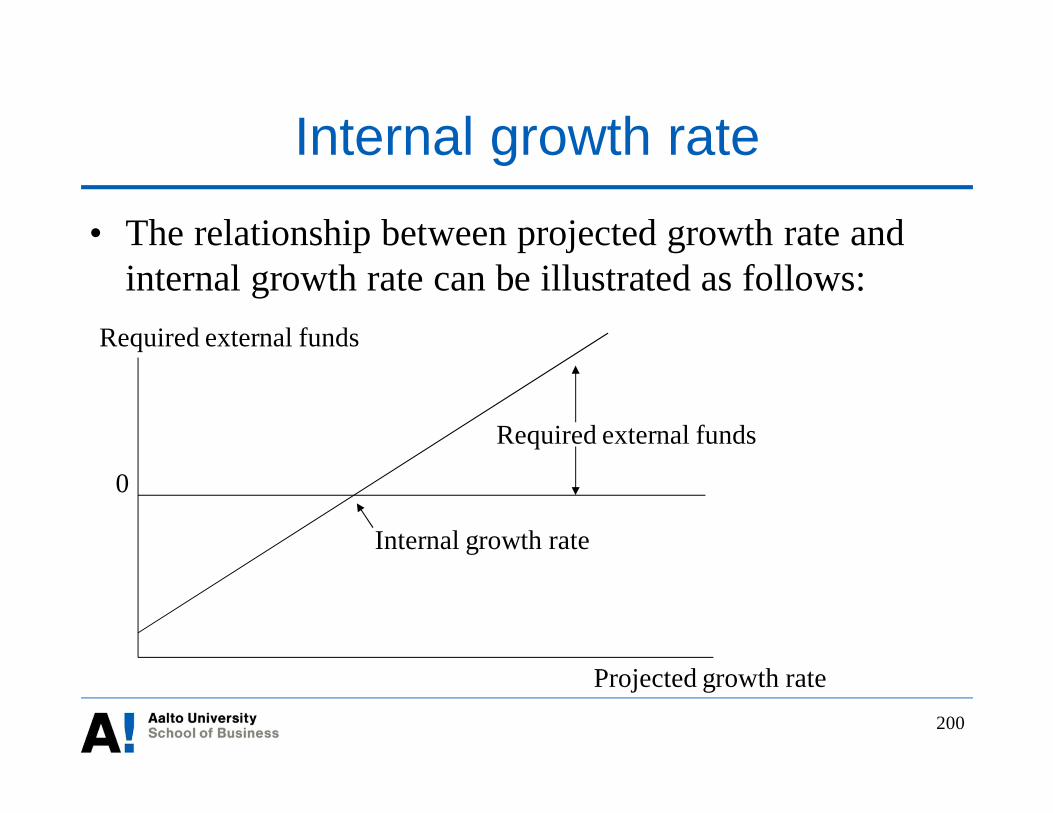

Internal growth rate

• The relationship between projected growth rate andinternal growth rate can be illustrated as follows:

Internal growth rate

Required external funds

0

Projected growth rate

Required external funds

201

External financing and growth• The internal growth rate can be further divided into

several components:

• A firm can achieve a high growth rate without externalcapital if it• Plows back a high proportion of its earnings• Has a high return on equity (ROE)• Has a low total debt ratio

Assets

Equity

Equity

incomeNet

incomeNet

earningsRetainedrategrowthInternal ´´=

Assets

EquityequityonReturnratioPlowback ´´=

202

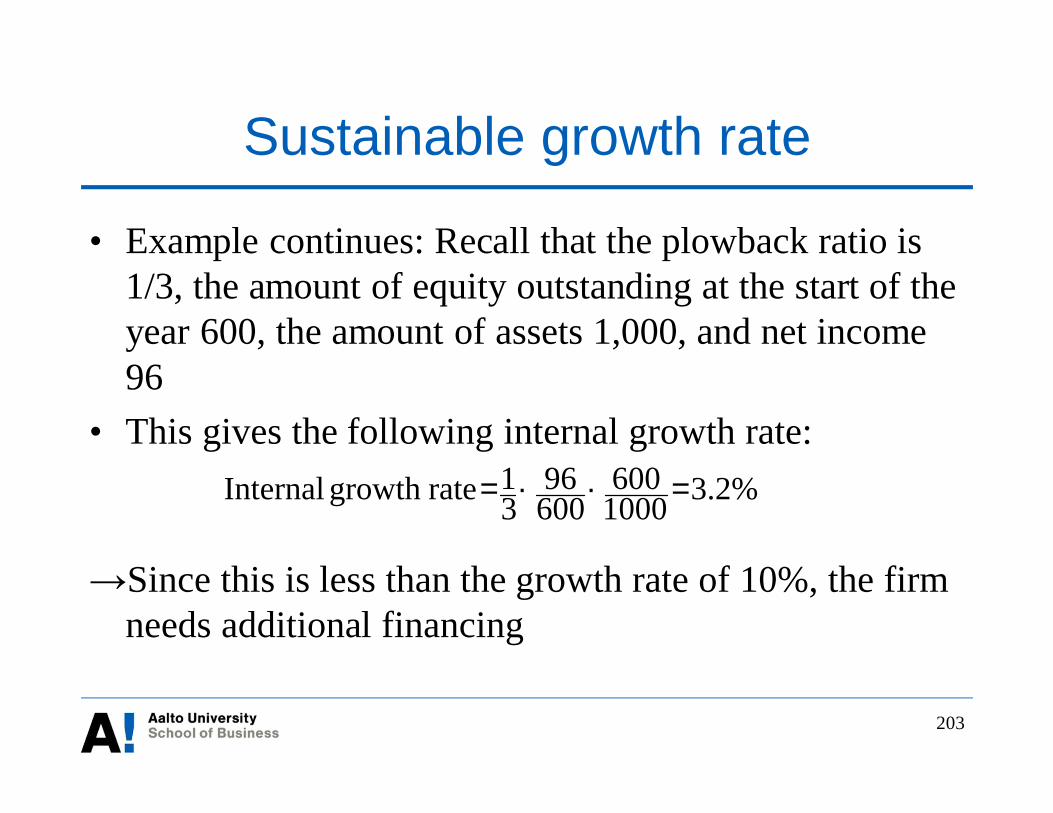

Sustainable growth rate• Sustainable growth rate

• Growth rate that can be maintained without any furtherequity issues

• Allows further debt issues which maintain the capitalstructure, i.e. the level of Equity/Assets, at the presentlevel

• The sustainable growth rate can be determined asfollows:• Sustainable growth rate

= Plowback ratio x Return on equity

203

Sustainable growth rate

• Example continues: Recall that the plowback ratio is1/3, the amount of equity outstanding at the start of theyear 600, the amount of assets 1,000, and net income96

• This gives the following internal growth rate:

Since this is less than the growth rate of 10%, the firmneeds additional financing

3.2%1000600

60096

31rategrowthInternal =´´=

204

Sustainable growth rate

• The sustainable growth rate is:

This number is also smaller than the projected growthrate• The firm not only requires additional borrowing but also has

to increase its total debt ratioIn the long run, the company either has to raiseadditional equity or cut back its growth rate

5.3%60096

31rategrowtheSustainabl =´=

205

A firm’s cumulative capital requirement

• Line A: Permanent cash surplus• Line B: Short-term lender for part of year, borrower for remainder• Line C: Permanent short-term borrower

206

Short-term planning: cash budget

• Cash budget (for time periods of less than 1 year)• Is a schedule of cash inflows and outflows in the near future• It is necessary for maintaining liquidity at all times

• A firm should have at the same time several cashbudgets for different time periods• E.g. a daily, a weekly, and a monthly cash budget

• The more the cash flows fluctuate, the more importantthe cash budgets are

• The more there are customers, the easier it is to predictcash flows

Value of cash holdings• US and European non-financial firms hold more cash today

than they used to• Advantages of holding more cash

• Readiness for unexpected contingencies• Smaller growth firms facing high costs of raising external capital

• For such firms, value of a $1 of cash is worth $1.2 to investors(Pinkowitz and Williamson, 2007)

• Disadvantage of excess cash• Tax disadvantage of lending (i.e., investing in marketable securities)• Agency problems

• For firms with poor corporate governance or facing financialdistress, a$1 of cash is worth less than a dollar to investors

207

208

Working capital: cycle of operations

208

209

Cash budgeting: example

2014Q4 Q1 Q2 Q3 Q4

1. Receivables, start of period 30 32,5 30,7 38,22. Sales 75 87,5 78,5 116 1313. Collections Sales in current period (80%) 70 62,8 92,8 104,8 Sales in last period (20%) 15 17,5 15,7 23,2 Total collections 85 80,3 108,5 1284. Receivables, end of period 4= 1+2-3 32,5 30,7 38,2 41,2

2015

210

Cash budgeting: example

Q1 Q2 Q3 Q4Sources of cash 85 80,3 108,5 128Uses of cash 131,5 95,3 95 931. Cash at start of period 5 -41,5 -56,5 -432. Change in cash balance (sources - uses) -46,5 -15 13,5 353. Cash at end of period (3 = 1 + 2) -41,5 -56,5 -43 -84. Minimum operating cash balance 5 5 5 55. Cumulative financing required (5 = 4 - 3) 46,5 61,5 48 13

2015

211

Sources of short-term financing• Line of credit

• Agreement with a bank that a company may borrow any time up to anestablished limit

• Typically unsecured, i.e. with no collateral, and reviewed annually• Revolving credit arrangement is a similar agreement but

usually lasts for several years• Factoring

• Company sells its receivables to a factor who then takes care ofcollecting the receivables

• Secured loans which use e.g. accounts receivable or inventoriesas collateral

• Delay payment of accounts payable• Expedite payment of receivables

212

Lecture 9

Working capital management

213

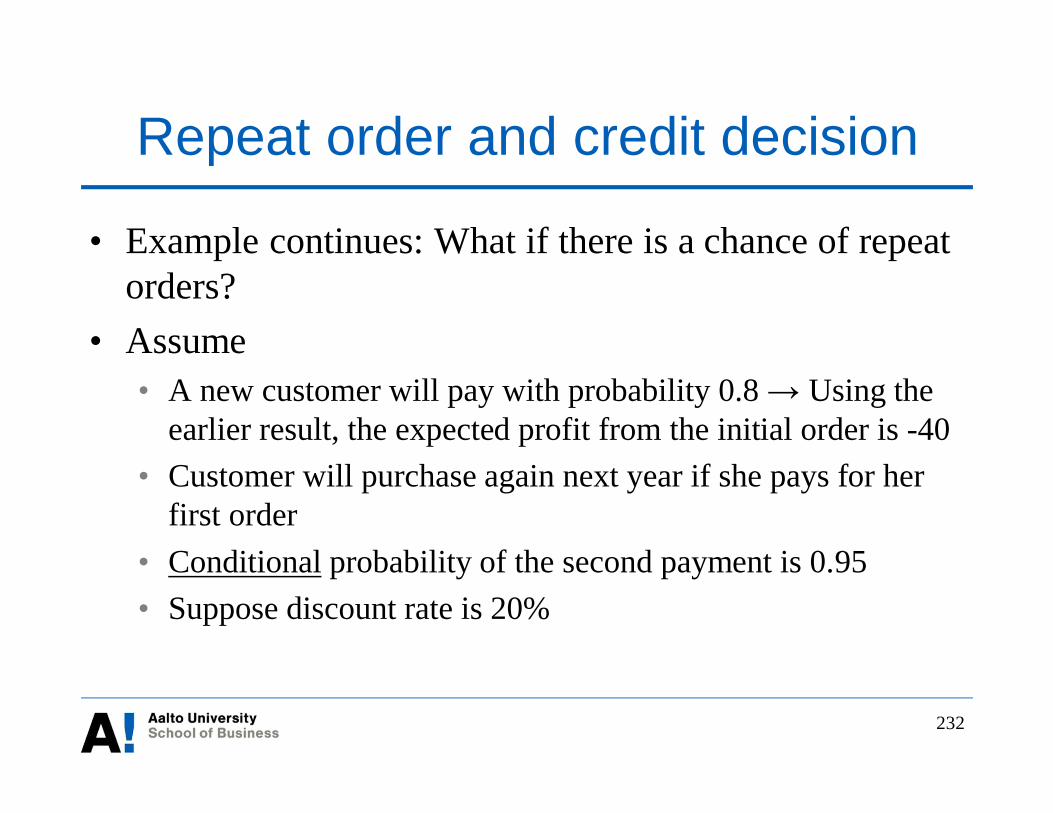

Overview• How to evaluate working capital management• Inventory management

• Optimal order size (i.e., economic order quantity)

• Credit management• Cost of cash allowance• Credit decision• Credit check• Repeat orders• Analysis of credit risk

• Cash management• Cash vs. marketable securities

How to evaluate working capitalmanagement

• Operating cycle• Number of days from purchases of inventory materials to the collection of cash

from customers

• Cash (conversion) cycle• Number of days from cash payment to suppliers to the collection of cash from

customers

214

Cash cycle: Examples

215

• In Finland, for a typical non-financial company:Cash cycle = Inventory period + Collection period – Payables period

= 100.6 + 47 – 53.4= 101.7 days (Median)

Source: Enqvist, Graham, and Nikkinen (2014)

216

Working capital composition in differentindustries

Mean percentagesfor firms in theS&P CompositeIndex in 2011

217

Working capital management in Finland

Source: Enqvist, Graham, and Nikkinen (2014)

218

Inventory management