Download - CEE Leasing market

Central & Eastern Europe and the Financial Crisis: the Impact on the Banking Sector and the Leasing Market

Matteo Ferrazzi, CEE Strategic Analysis, UniCredit Group

Thursday, 2 April 2009 – Istanbul, Turkey

2

AGENDA

The global financial crisis and the effects on Central Eastern Europe

The banking sectors in CEE

The challenges for the leasing market

Conclusions

3

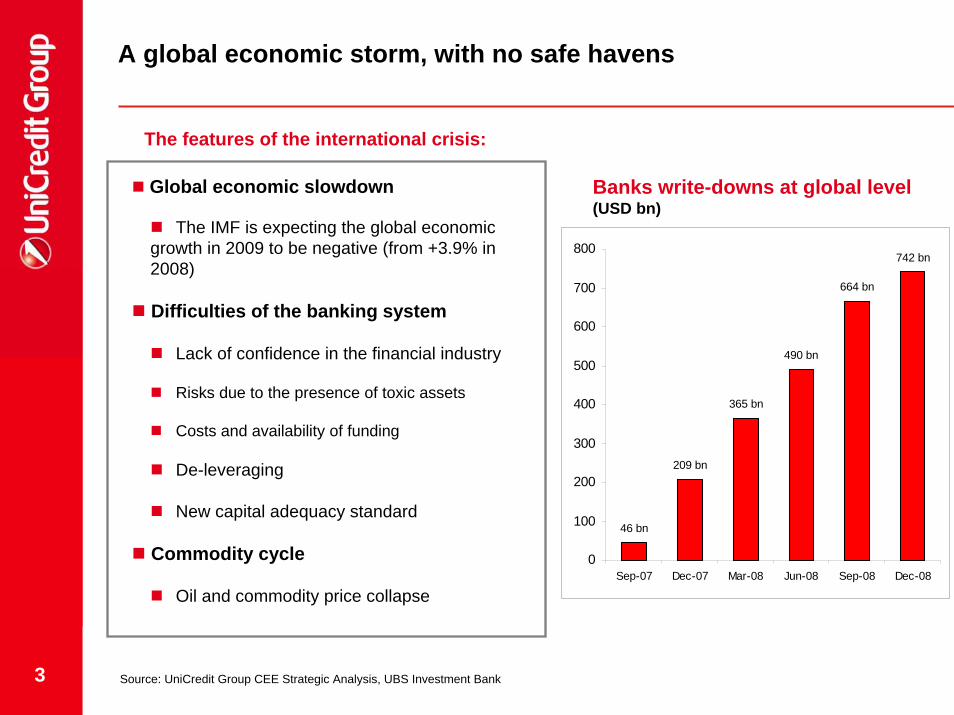

A global economic storm, with no safe havens

The features of the international crisis:

Banks write-downs at global level (USD bn)

Global economic slowdown

The IMF is expecting the global economic growth in 2009 to be negative (from +3.9% in 2008)

Difficulties of the banking system

Lack of confidence in the financial industry

Risks due to the presence of toxic assets

Costs and availability of funding

De-leveraging

New capital adequacy standard

Commodity cycle

Oil and commodity price collapse

46 bn

209 bn

365 bn

490 bn

664 bn

742 bn

0

100

200

300

400

500

600

700

800

Sep-07 Dec-07 Mar-08 Jun-08 Sep-08 Dec-08

Source: UniCredit Group CEE Strategic Analysis, UBS Investment Bank

4

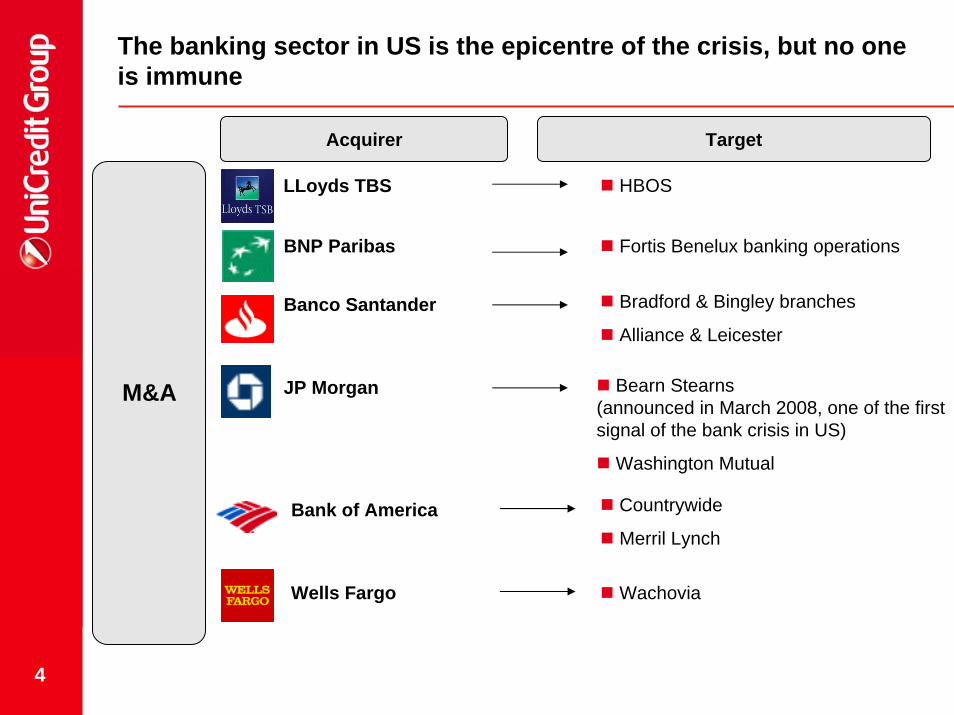

The banking sector in US is the epicentre of the crisis, but no one is immune

Acquirer Target

M&A

LLoyds TBS HBOS

BNP Paribas Fortis Benelux banking operations

Bradford & Bingley branches

Alliance & LeicesterBanco Santander

JP Morgan Bearn Stearns(announced in March 2008, one of the first signal of the bank crisis in US)

Washington Mutual

Countrywide

Merril LynchBank of America

Wells Fargo Wachovia

5

With the governments recently active in rescuing some important players

State intervention

The US Government is directly participating in the rescue of:

CitiGroup

Freddy Mac

Fannie Mae

AIG

The German Government has bought important participations into:

Commerzbank

Hypo Real estate

The English Government has bought important participations into:

Northern Rock (March 2008)

Royal Bank of Scotland

Lloyds

Other governments which intervened nationalizing some banks were: Iceland (four major banks), Ireland (Anglo Irish Bank, third major bank in the country), Latvia,Ukraine, Kazakhstan, etc.

6

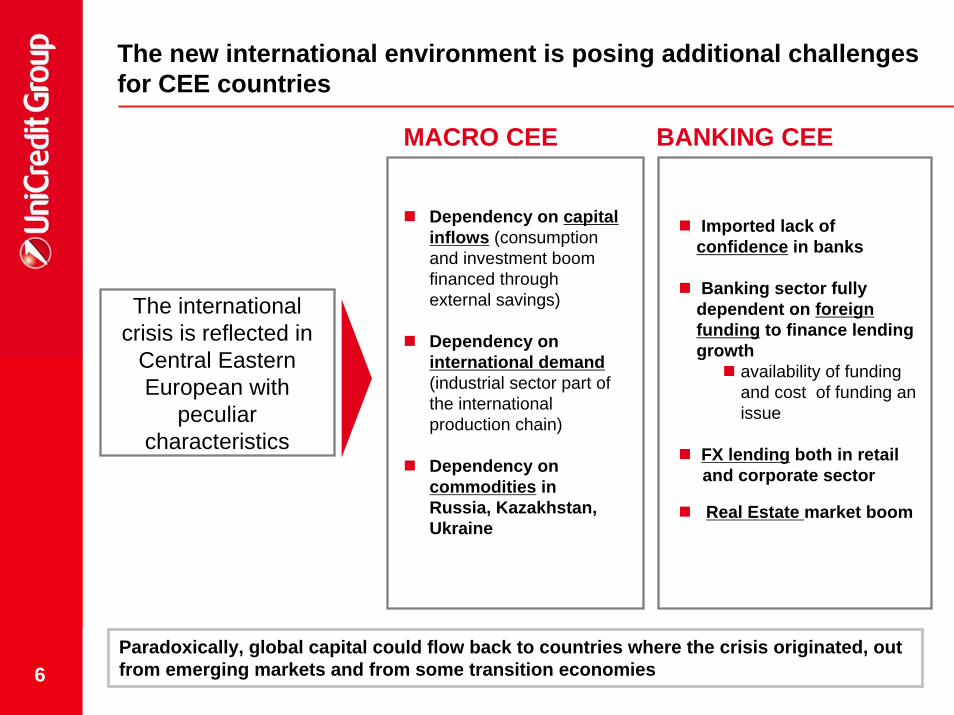

The new international environment is posing additional challenges for CEE countries

MACRO CEE BANKING CEE

Dependency on capital inflows (consumption and investment boom financed through external savings)

Dependency on international demand(industrial sector part of the international production chain)

Dependency on commodities in Russia, Kazakhstan, Ukraine

Imported lack ofconfidence in banks

Banking sector fully dependent on foreign funding to finance lending growth

availability of funding and cost of funding an issue

FX lending both in retail and corporate sector

Real Estate market boom

The international crisis is reflected in

Central Eastern European with

peculiar characteristics

Paradoxically, global capital could flow back to countries where the crisis originated, out from emerging markets and from some transition economies

7

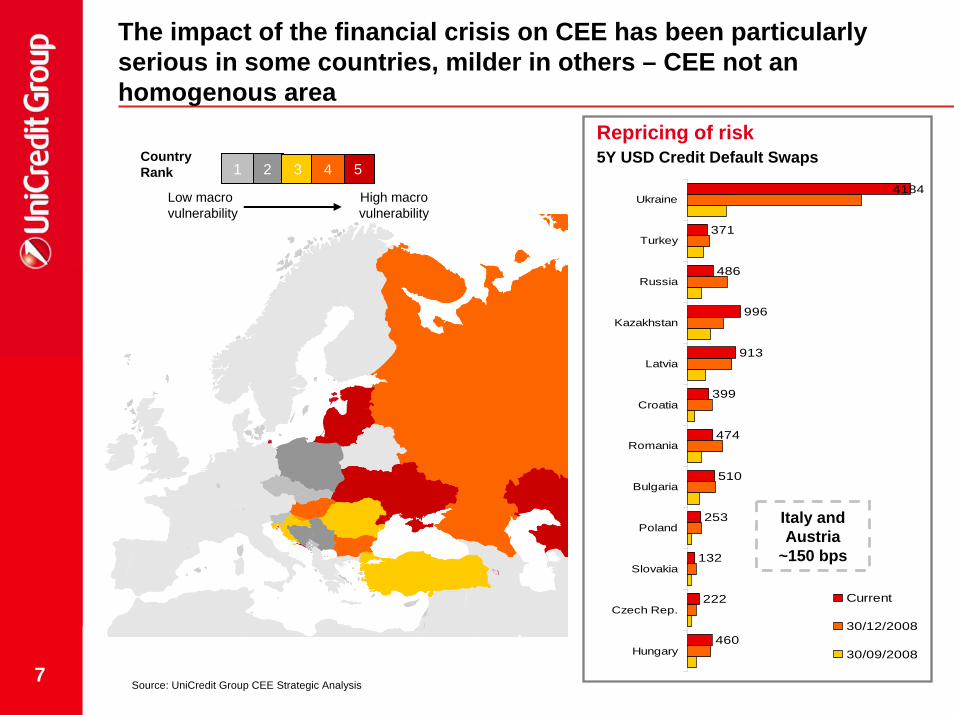

The impact of the financial crisis on CEE has been particularly serious in some countries, milder in others – CEE not an homogenous area

Source: UniCredit Group CEE Strategic Analysis

Low macro vulnerability

2 5

High macro vulnerability

3 41Country Rank

460

222

132

253

510

474

399

913

996

486

371

4184

Hungary

Czech Rep.

Slovakia

Poland

Bulgaria

Romania

Croatia

Latvia

Kazakhstan

Russia

Turkey

Ukraine

Current

30/12/2008

30/09/2008

Repricing of risk5Y USD Credit Default Swaps

Italy and Austria

~150 bps

8

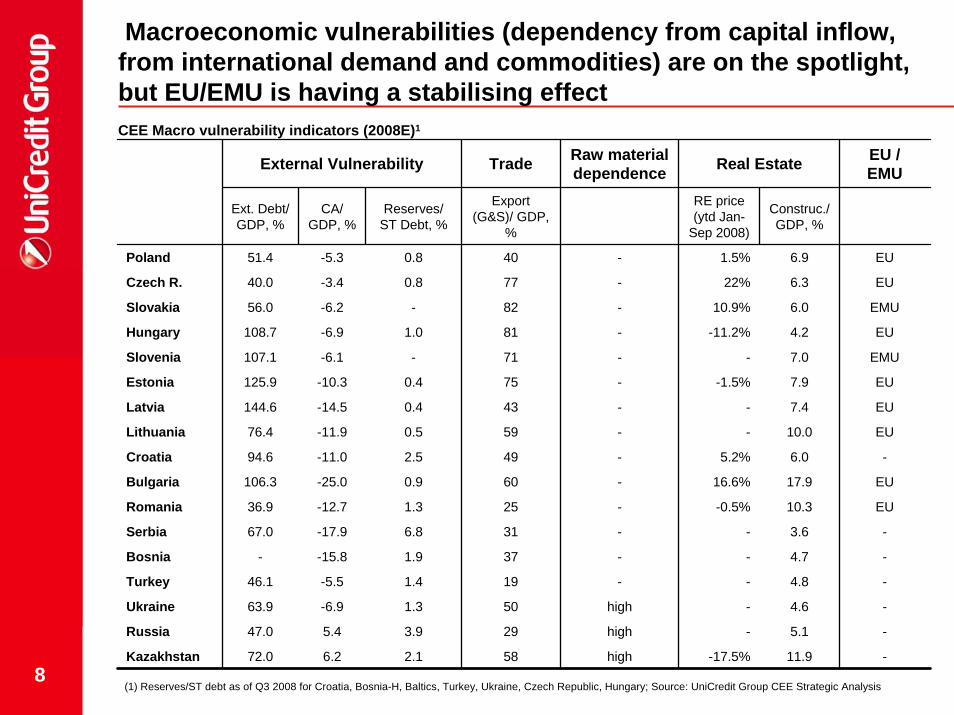

Macroeconomic vulnerabilities (dependency from capital inflow, from international demand and commodities) are on the spotlight,but EU/EMU is having a stabilising effectCEE Macro vulnerability indicators (2008E)1

External Vulnerability Trade Raw material dependence Real Estate EU /

EMU

Ext. Debt/GDP, %

CA/ GDP, %

Reserves/ ST Debt, %

Export (G&S)/ GDP,

%

RE price(ytd Jan-

Sep 2008)

Construc./ GDP, %

Poland 51.4 -5.3 0.8 40 - 1.5% 6.9 EU

Czech R. 40.0 -3.4 0.8 77 - 22% 6.3 EU

Slovakia 56.0 -6.2 - 82 - 10.9% 6.0 EMU

Hungary 108.7 -6.9 1.0 81 - -11.2% 4.2 EU

Slovenia 107.1 -6.1 - 71 - - 7.0 EMU

Estonia 125.9 -10.3 0.4 75 - -1.5% 7.9 EU

Latvia 144.6 -14.5 0.4 43 - - 7.4 EU

Lithuania 76.4 -11.9 0.5 59 - - 10.0 EU

Croatia 94.6 -11.0 2.5 49 - 5.2% 6.0 -

Bulgaria 106.3 -25.0 0.9 60 - 16.6% 17.9 EU

Romania 36.9 -12.7 1.3 25 - -0.5% 10.3 EU

Serbia 67.0 -17.9 6.8 31 - - 3.6 -

Bosnia - -15.8 1.9 37 - - 4.7 -

Turkey 46.1 -5.5 1.4 19 - - 4.8 -

Ukraine 63.9 -6.9 1.3 50 high - 4.6 -

Russia 47.0 5.4 3.9 29 high - 5.1 -

Kazakhstan 72.0 6.2 2.1 58 high -17.5% 11.9 -

(1) Reserves/ST debt as of Q3 2008 for Croatia, Bosnia-H, Baltics, Turkey, Ukraine, Czech Republic, Hungary; Source: UniCredit Group CEE Strategic Analysis

9

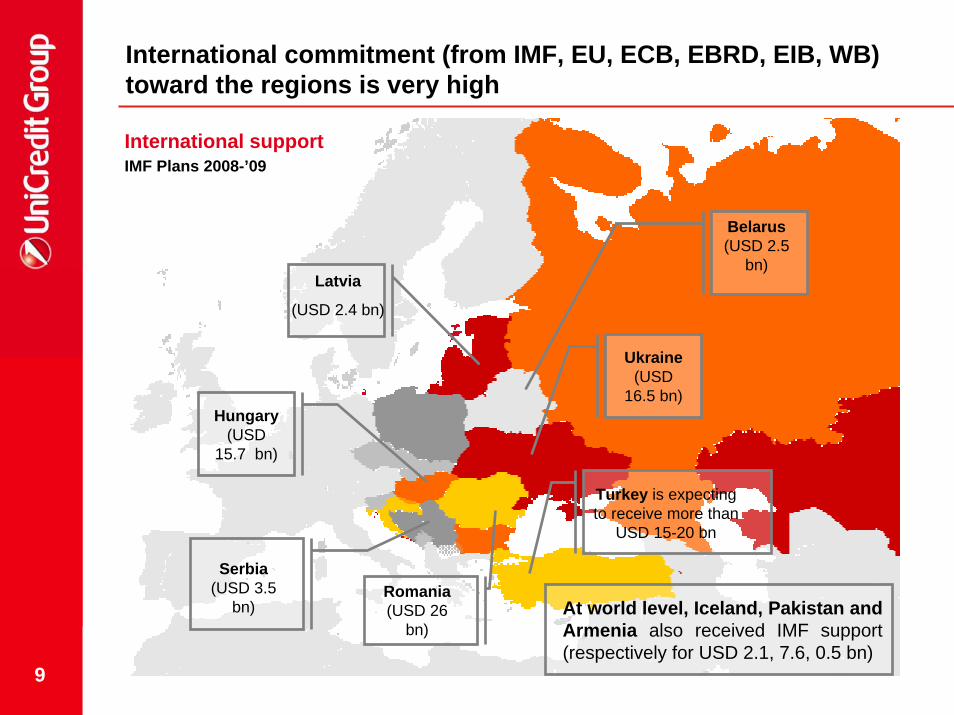

International commitment (from IMF, EU, ECB, EBRD, EIB, WB) toward the regions is very high

Ukraine (USD

16.5 bn)Hungary

(USD 15.7 bn)

Belarus(USD 2.5

bn)Latvia

(USD 2.4 bn)

Serbia (USD 3.5

bn)

Turkey is expecting to receive more than

USD 15-20 bn

At world level, Iceland, Pakistan and Armenia also received IMF support (respectively for USD 2.1, 7.6, 0.5 bn)

Romania (USD 26

bn)

International supportIMF Plans 2008-’09

10

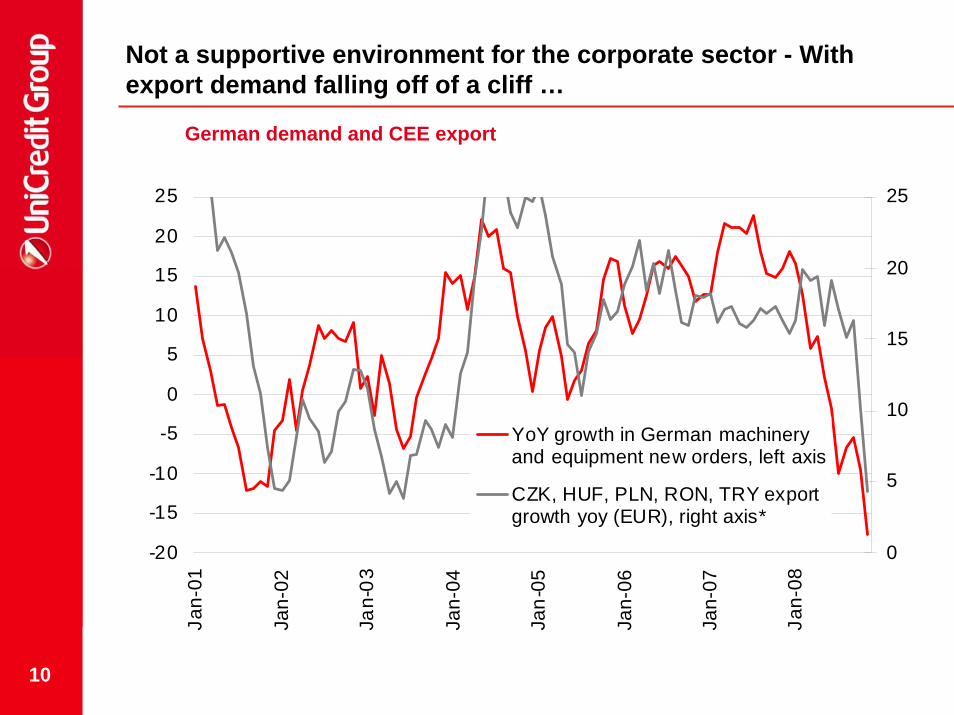

Not a supportive environment for the corporate sector - With export demand falling off of a cliff …

German demand and CEE export

-20

-15

-10

-5

0

5

10

15

20

25Ja

n-01

Jan-

02

Jan-

03

Jan-

04

Jan-

05

Jan-

06

Jan-

07

Jan-

08

0

5

10

15

20

25

YoY growth in German machineryand equipment new orders, left axis

CZK, HUF, PLN, RON, TRY exportgrowth yoy (EUR), right axis*

11

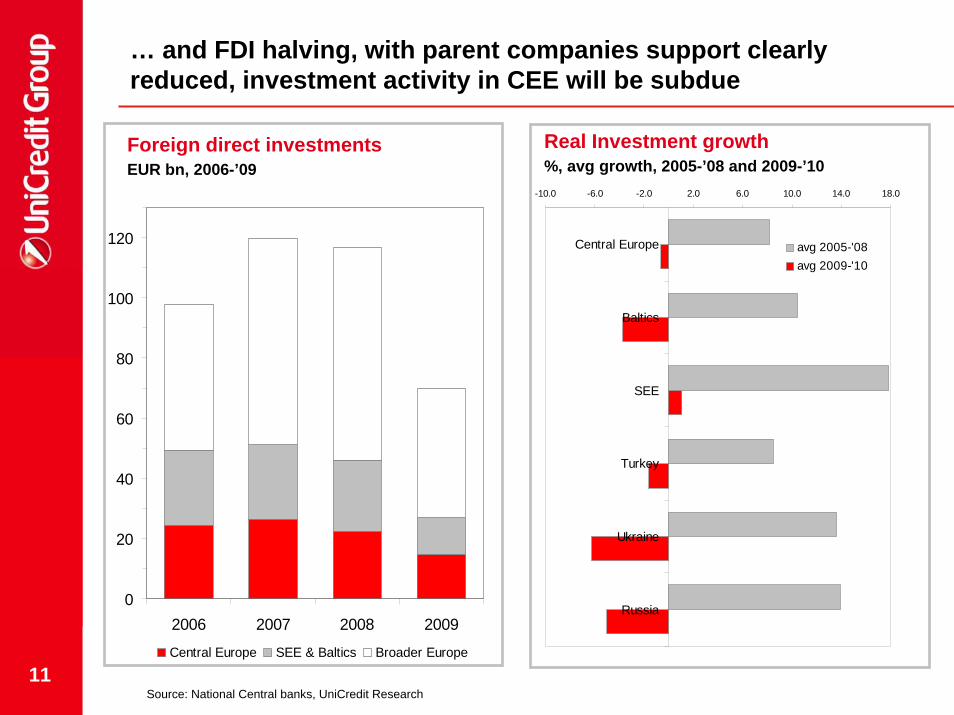

… and FDI halving, with parent companies support clearlyreduced, investment activity in CEE will be subdue

0

20

40

60

80

100

120

2006 2007 2008 2009

Central Europe SEE & Baltics Broader Europe

Foreign direct investmentsEUR bn, 2006-’09

-10.0 -6.0 -2.0 2.0 6.0 10.0 14.0 18.0

Central Europe

Baltics

SEE

Turkey

Ukraine

Russia

avg 2005-'08avg 2009-'10

Real Investment growth%, avg growth, 2005-’08 and 2009-’10

Source: National Central banks, UniCredit Research

12

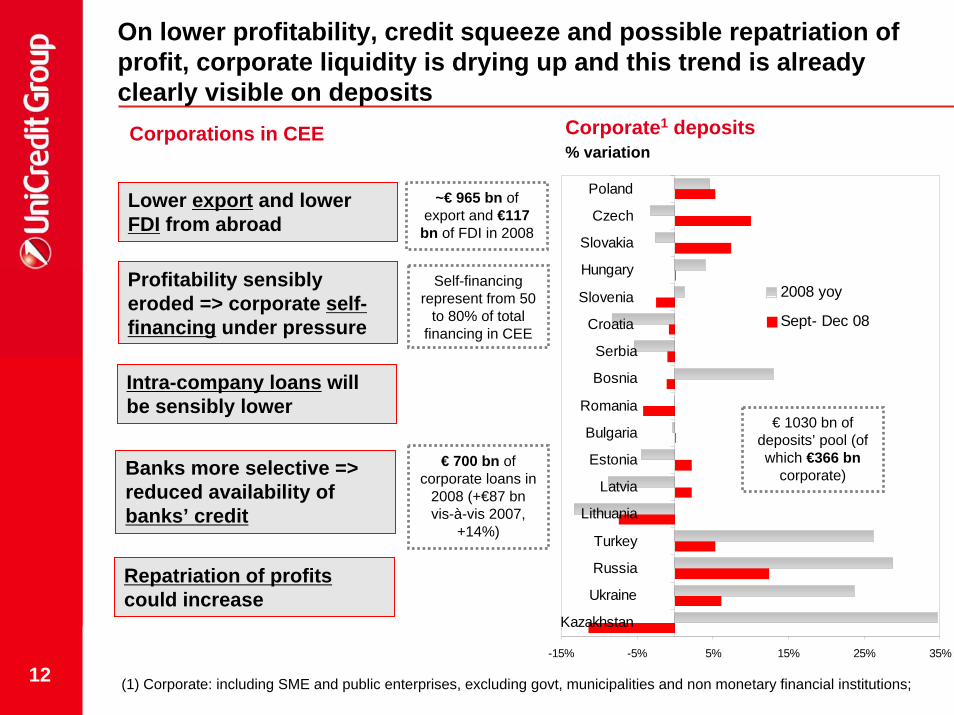

On lower profitability, credit squeeze and possible repatriation of profit, corporate liquidity is drying up and this trend is already clearly visible on deposits

Corporate1 deposits% variation

Corporations in CEE

-15% -5% 5% 15% 25% 35%

Poland

Czech

Slovakia

Hungary

Slovenia

Croatia

Serbia

Bosnia

Romania

Bulgaria

Estonia

Latvia

Lithuania

Turkey

Russia

Ukraine

Kazakhstan

2008 yoy

Sept- Dec 08

(1) Corporate: including SME and public enterprises, excluding govt, municipalities and non monetary financial institutions;

Profitability sensibly eroded => corporate self-financing under pressure

Repatriation of profitscould increase

Banks more selective => reduced availability of banks’ credit

Intra-company loans will be sensibly lower

Lower export and lower FDI from abroad

Self-financing represent from 50

to 80% of total financing in CEE

~€ 965 bn of export and €117

bn of FDI in 2008

€ 700 bn of corporate loans in

2008 (+€87 bnvis-à-vis 2007,

+14%)

€ 1030 bn of deposits’ pool (of which €366 bn

corporate)

13

The manufacturing sector in CEE: a stronger industry after the crisis or the end of a successful story?

CEE became in the last decade the manufacturing arm of “Old Europe”. But the financial crisis is affecting significantly CEE countries:

Is the end of the “successful story” in producing in CEE or will the crisis create a further incentive to move production towards more efficient locations in Eastern Europe (creating even a stronger industry in CEE in the long run)?

Some considerations:

Incentives for some industries in Western Europe (for cars and durable goods) could favor Western factories, even if protectionism risks will not materialize;

Labor flexibility is higher in some CEE countries (it’s easier to cut production in CEE rather than in Western Europe)

Pressures on labor cost in CEE will be lower than before (CEE is even more an efficient location)

Competitive pressures intensifies, ie. stronger incentive to look for efficiency

14

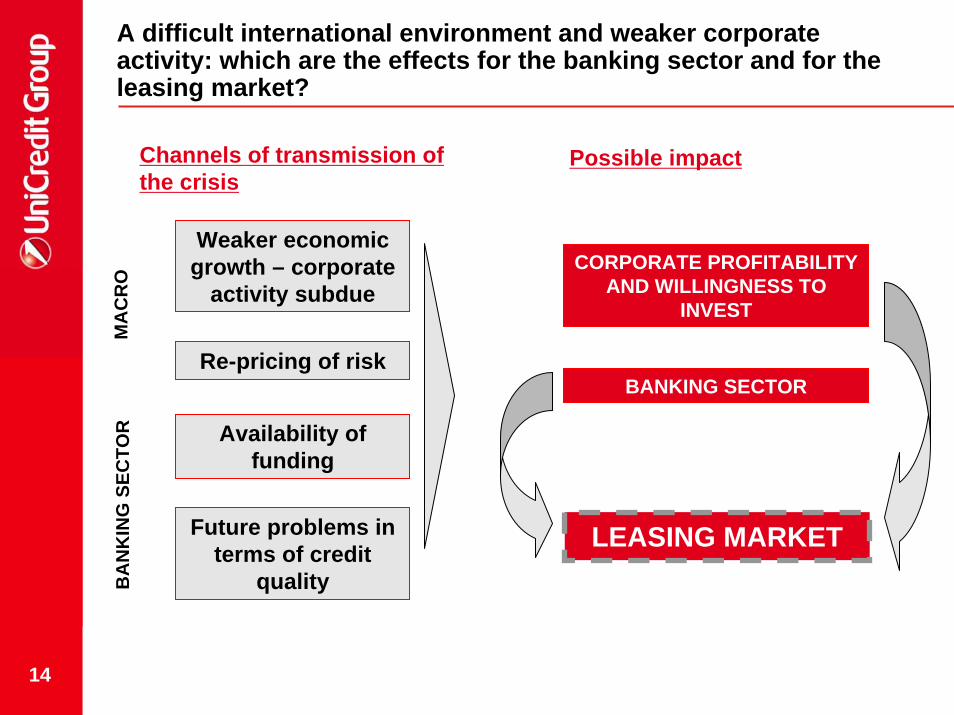

A difficult international environment and weaker corporate activity: which are the effects for the banking sector and for the leasing market?

Channels of transmission of the crisis

Possible impact

Weaker economic growth – corporate

activity subdueCORPORATE PROFITABILITY

AND WILLINGNESS TO INVEST

MA

CR

O

Re-pricing of riskBANKING SECTOR

LEASING MARKET

Availability of funding

BA

NK

ING

SEC

TOR

Future problems in terms of credit

quality

15

AGENDA

The global financial crisis and the effects on Central Eastern Europe

The banking sectors in CEE

The challenges for the leasing market

Conclusions

16

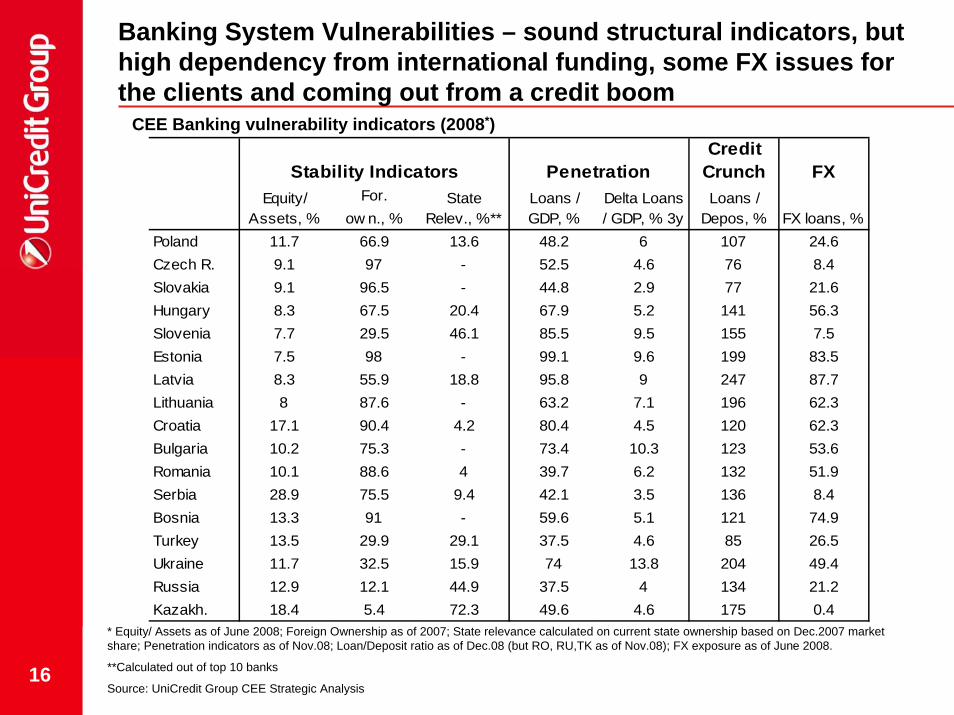

Banking System Vulnerabilities – sound structural indicators, but high dependency from international funding, some FX issues for the clients and coming out from a credit boom

* Equity/ Assets as of June 2008; Foreign Ownership as of 2007; State relevance calculated on current state ownership based on Dec.2007 market share; Penetration indicators as of Nov.08; Loan/Deposit ratio as of Dec.08 (but RO, RU,TK as of Nov.08); FX exposure as of June 2008.

**Calculated out of top 10 banks

Source: UniCredit Group CEE Strategic Analysis

CEE Banking vulnerability indicators (2008*)Credit

Crunch FXFor.

ow n., %Poland 11.7 66.9 13.6 48.2 6 107 24.6Czech R. 9.1 97 - 52.5 4.6 76 8.4Slovakia 9.1 96.5 - 44.8 2.9 77 21.6Hungary 8.3 67.5 20.4 67.9 5.2 141 56.3Slovenia 7.7 29.5 46.1 85.5 9.5 155 7.5Estonia 7.5 98 - 99.1 9.6 199 83.5Latvia 8.3 55.9 18.8 95.8 9 247 87.7Lithuania 8 87.6 - 63.2 7.1 196 62.3Croatia 17.1 90.4 4.2 80.4 4.5 120 62.3Bulgaria 10.2 75.3 - 73.4 10.3 123 53.6Romania 10.1 88.6 4 39.7 6.2 132 51.9Serbia 28.9 75.5 9.4 42.1 3.5 136 8.4Bosnia 13.3 91 - 59.6 5.1 121 74.9Turkey 13.5 29.9 29.1 37.5 4.6 85 26.5Ukraine 11.7 32.5 15.9 74 13.8 204 49.4Russia 12.9 12.1 44.9 37.5 4 134 21.2Kazakh. 18.4 5.4 72.3 49.6 4.6 175 0.4

FX loans, %

Stability Indicators PenetrationEquity/

Assets, %State

Relev., %**Loans / GDP, %

Delta Loans / GDP, % 3y

Loans / Depos, %

17

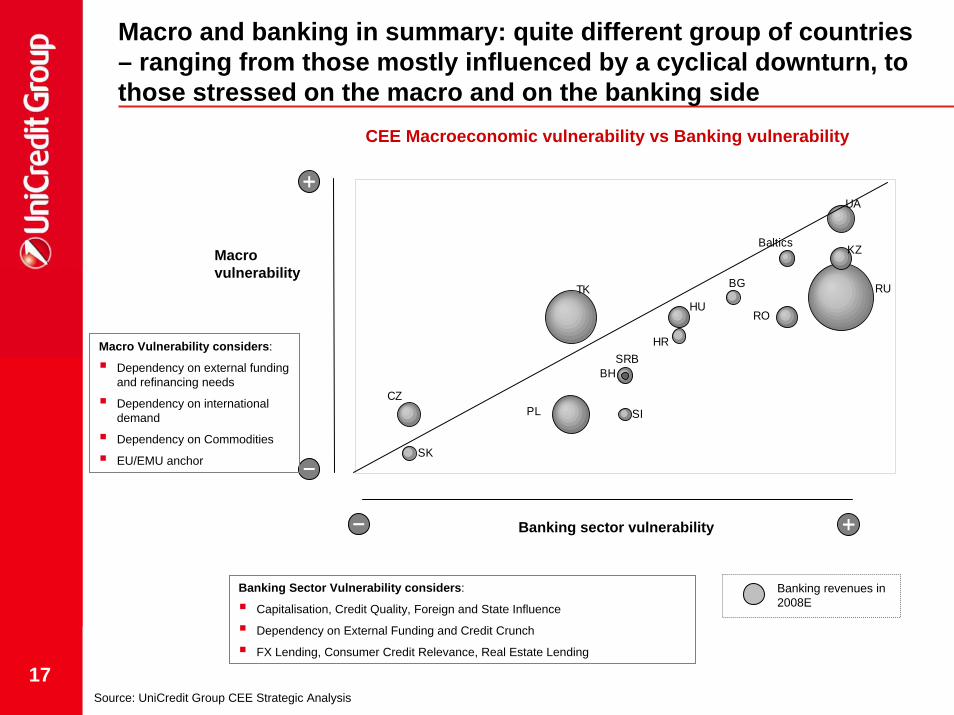

Macro and banking in summary: quite different group of countries– ranging from those mostly influenced by a cyclical downturn, tothose stressed on the macro and on the banking side

CEE Macroeconomic vulnerability vs Banking vulnerability

SK

CZSIPL

SRBBH

TKHU

HR

RO

BG

Baltics KZ

RU

UA

Macro vulnerability

Source: UniCredit Group CEE Strategic Analysis

Macro Vulnerability considers:

Dependency on external fundingand refinancing needs

Dependency on international demand

Dependency on Commodities

EU/EMU anchor

Banking sector vulnerability

Banking revenues in 2008E

Banking Sector Vulnerability considers:

Capitalisation, Credit Quality, Foreign and State Influence

Dependency on External Funding and Credit Crunch

FX Lending, Consumer Credit Relevance, Real Estate Lending

18

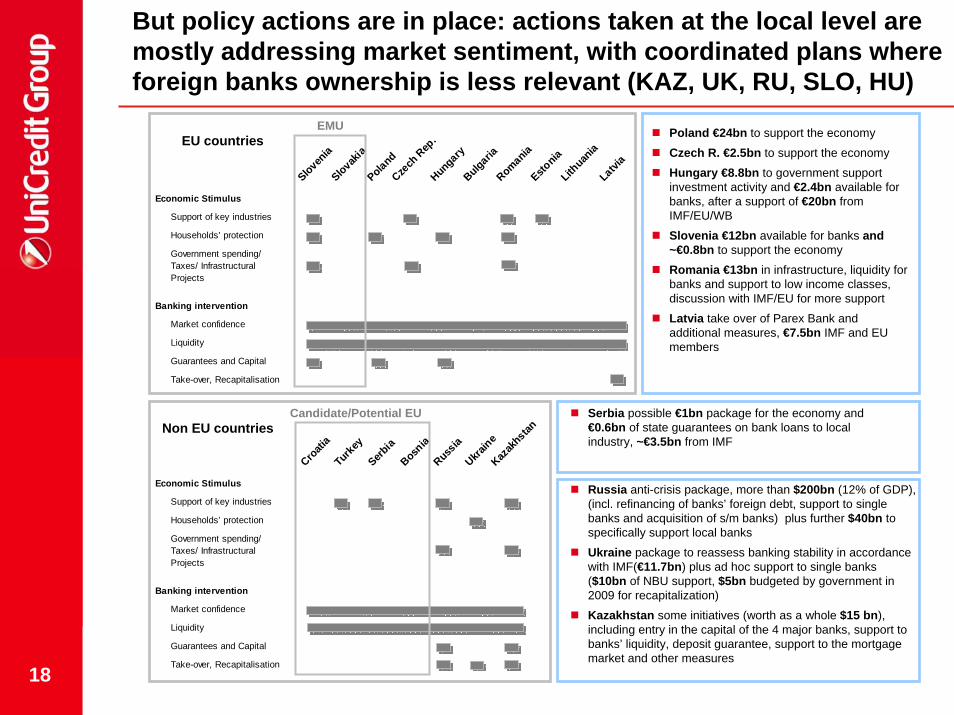

But policy actions are in place: actions taken at the local level are mostly addressing market sentiment, with coordinated plans whereforeign banks ownership is less relevant (KAZ, UK, RU, SLO, HU)

Slovenia

Slovakia

PolandCze

ch R

ep.

HungaryBulgariaRomaniaEsto

niaLith

uania

Latvia

Economic Stimulus

Support of key industries

Households’ protection

Government spending/ Taxes/ Infrastructural Projects

Banking intervention

Market confidence

Liquidity

Guarantees and Capital

Take-over, Recapitalisation

Croati

aTurk

eySerb

iaBosn

iaRuss

iaUkra

ineKaz

akhstan

Economic Stimulus

Support of key industries

Households’ protection

Government spending/ Taxes/ Infrastructural Projects

Banking intervention

Market confidence

Liquidity

Guarantees and Capital

Take-over, Recapitalisation

EU countries

Non EU countries

EMU

Candidate/Potential EU

Poland €24bn to support the economy

Czech R. €2.5bn to support the economy

Hungary €8.8bn to government support investment activity and €2.4bn available for banks, after a support of €20bn from IMF/EU/WB

Slovenia €12bn available for banks and ~€0.8bn to support the economy

Romania €13bn in infrastructure, liquidity for banks and support to low income classes, discussion with IMF/EU for more support

Latvia take over of Parex Bank and additional measures, €7.5bn IMF and EU members

Serbia possible €1bn package for the economy and €0.6bn of state guarantees on bank loans to local industry, ~€3.5bn from IMF

Russia anti-crisis package, more than $200bn (12% of GDP), (incl. refinancing of banks’ foreign debt, support to single banks and acquisition of s/m banks) plus further $40bn to specifically support local banks

Ukraine package to reassess banking stability in accordance with IMF(€11.7bn) plus ad hoc support to single banks ($10bn of NBU support, $5bn budgeted by government in 2009 for recapitalization)

Kazakhstan some initiatives (worth as a whole $15 bn), including entry in the capital of the 4 major banks, support to banks’ liquidity, deposit guarantee, support to the mortgage market and other measures

19

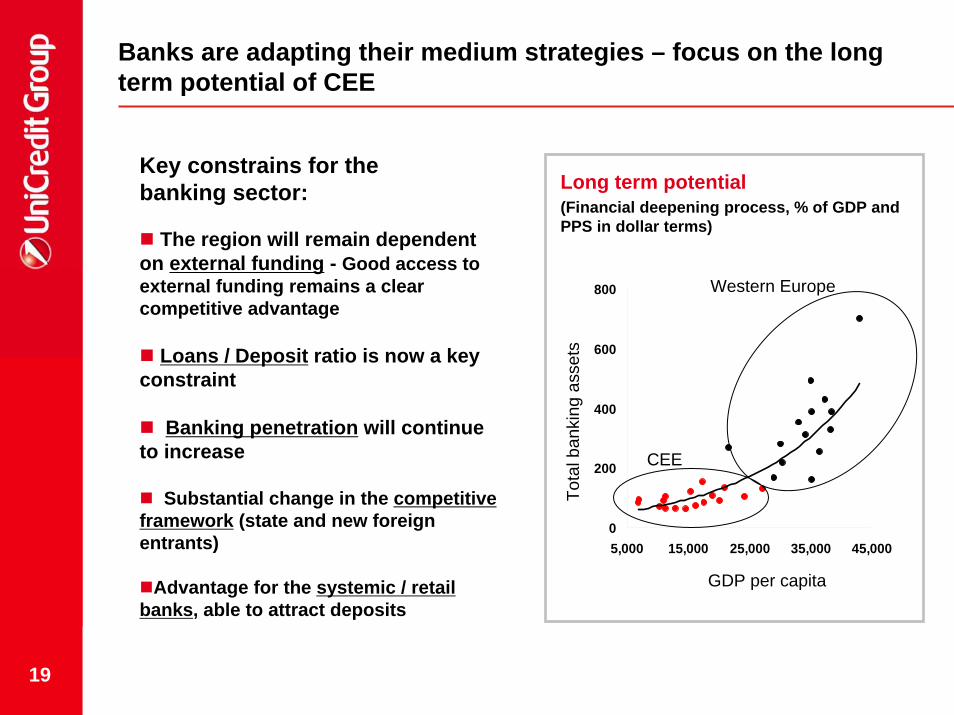

Banks are adapting their medium strategies – focus on the long term potential of CEE

Key constrains for the banking sector:

0

200

400

600

800

5,000 15,000 25,000 35,000 45,000

Long term potential (Financial deepening process, % of GDP and PPS in dollar terms)

GDP per capitaTo

tal b

anki

ng a

sset

s

Western Europe

CEE

The region will remain dependent on external funding - Good access to external funding remains a clear competitive advantage

Loans / Deposit ratio is now a key constraint

Banking penetration will continue to increase

Substantial change in the competitiveframework (state and new foreign entrants)

Advantage for the systemic / retail banks, able to attract deposits

20

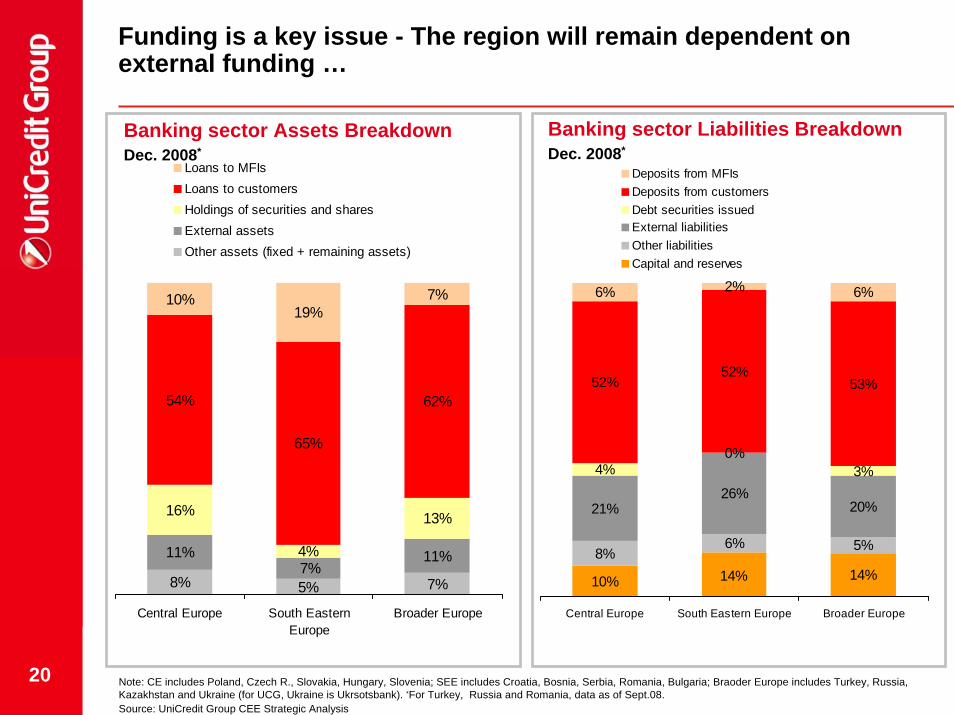

8% 7%

11% 11%

16%

4%

13%

54%

65%

62%

10%19%

7%

5%7%

Central Europe South EasternEurope

Broader Europe

Loans to MFIsLoans to customersHoldings of securities and sharesExternal assetsOther assets (fixed + remaining assets)

10%

8%6% 5%

21%26%

20%

4%0%

3%

52%52%

53%

6% 2% 6%

14% 14%

Central Europe South Eastern Europe Broader Europe

Deposits from MFIsDeposits from customersDebt securities issuedExternal liabilitiesOther liabilitiesCapital and reserves

Banking sector Assets BreakdownDec. 2008*

Banking sector Liabilities BreakdownDec. 2008*

Funding is a key issue - The region will remain dependent on external funding …

Note: CE includes Poland, Czech R., Slovakia, Hungary, Slovenia; SEE includes Croatia, Bosnia, Serbia, Romania, Bulgaria; Braoder Europe includes Turkey, Russia, Kazakhstan and Ukraine (for UCG, Ukraine is Ukrsotsbank). *For Turkey, Russia and Romania, data as of Sept.08.Source: UniCredit Group CEE Strategic Analysis

21

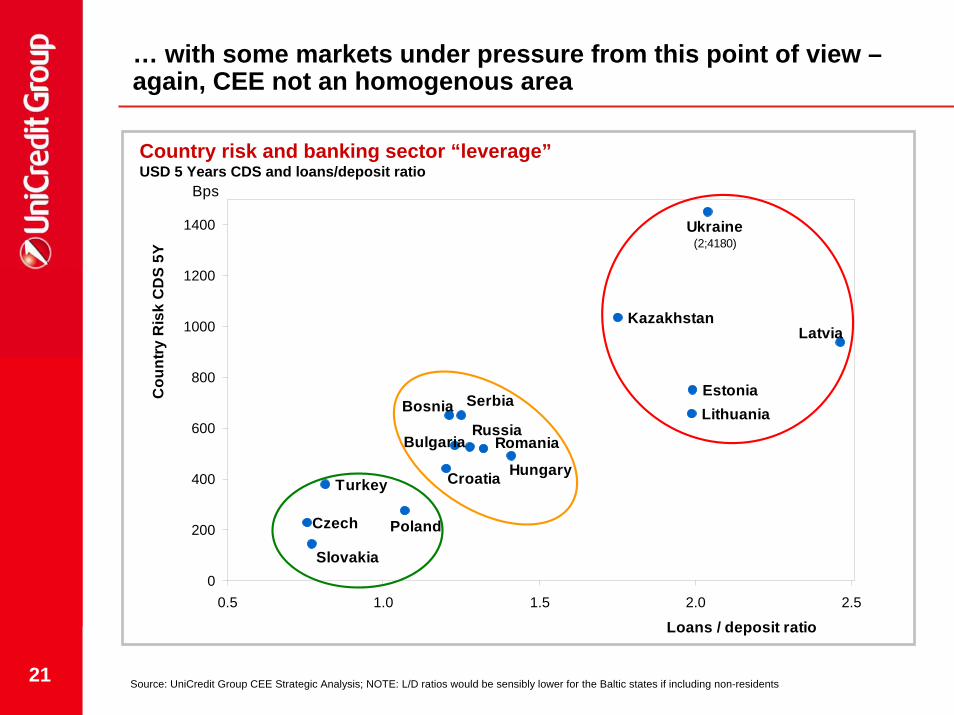

… with some markets under pressure from this point of view –again, CEE not an homogenous area

Bosnia

Kazakhstan

Russia

Ukraine(2;4180)

Turkey

Serbia

Croatia

Bulgaria Romania

Estonia

Latvia

Lithuania

Slovakia

Czech

Hungary

Poland

0

200

400

600

800

1000

1200

1400

0.5 1.0 1.5 2.0 2.5

Bps

Cou

ntry

Ris

k C

DS

5Y

Loans / deposit ratio

Country risk and banking sector “leverage”USD 5 Years CDS and loans/deposit ratio

Source: UniCredit Group CEE Strategic Analysis; NOTE: L/D ratios would be sensibly lower for the Baltic states if including non-residents

22

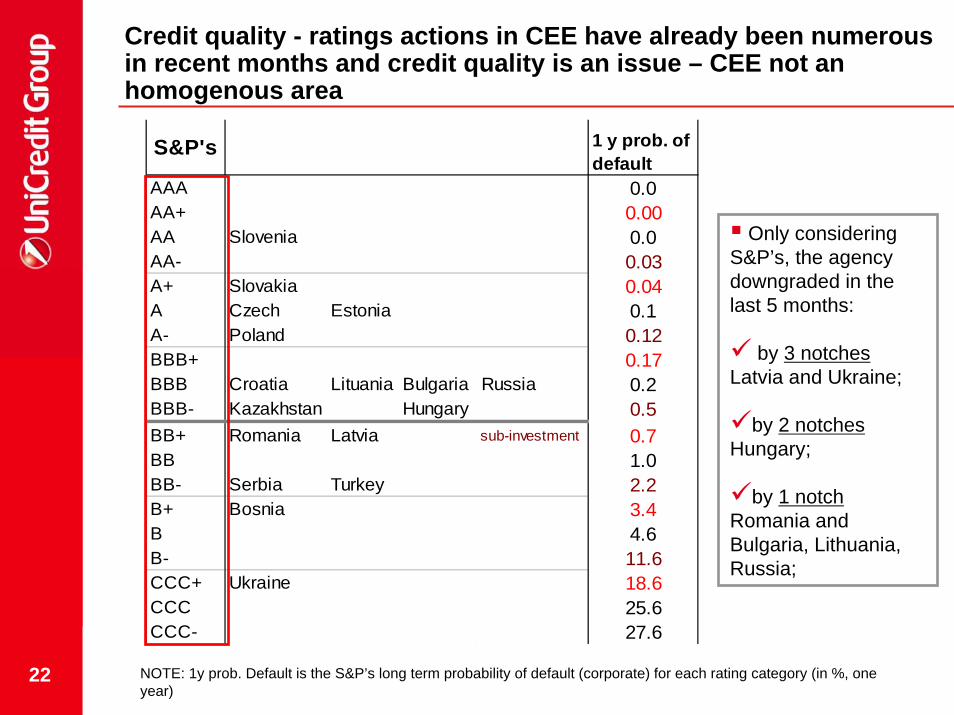

Credit quality - ratings actions in CEE have already been numerous in recent months and credit quality is an issue – CEE not an homogenous area

S&P's 1 y prob. of default

AAA 0.0AA+ 0.00AA Slovenia 0.0AA- 0.03A+ Slovakia 0.04A Czech Estonia 0.1A- Poland 0.12BBB+ 0.17BBB Croatia Lituania Bulgaria Russia 0.2BBB- Kazakhstan Hungary 0.5BB+ Romania Latvia sub-investment 0.7BB 1.0BB- Serbia Turkey 2.2B+ Bosnia 3.4B 4.6B- 11.6CCC+ Ukraine 18.6CCC 25.6CCC- 27.6

Only considering S&P’s, the agency downgraded in the last 5 months:

by 3 notchesLatvia and Ukraine;

by 2 notchesHungary;

by 1 notchRomania and Bulgaria, Lithuania, Russia;

NOTE: 1y prob. Default is the S&P’s long term probability of default (corporate) for each rating category (in %, one year)

23

AGENDA

The global financial crisis and the effects on Central Eastern Europe

The banking sectors in CEE

The challenges for the leasing market

Conclusions

24

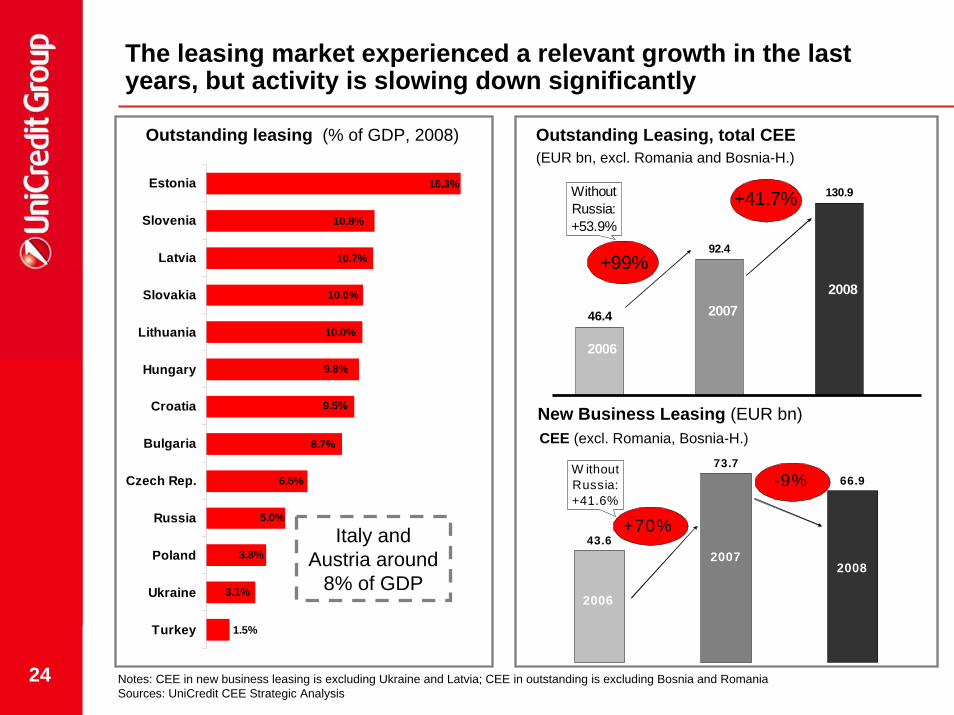

The leasing market experienced a relevant growth in the last years, but activity is slowing down significantly

73.766.9

43.6

2006

20072008

+70%

-9%W ithout Russia: +41.6%

1.5%

3.1%

3.8%

5.0%

6.5%

8.7%

9.5%

9.8%

10.0%

10.0%

10.7%

16.3%

10.8%

Turkey

Ukraine

Poland

Russia

Czech Rep.

Bulgaria

Croatia

Hungary

Lithuania

Slovakia

Latvia

Slovenia

Estonia

92.4

130.9

46.4

2006

20072008

+99%

+41.7%Without Russia: +53.9%

Outstanding Leasing, total CEE(EUR bn, excl. Romania and Bosnia-H.)

CEE (excl. Romania, Bosnia-H.)

Outstanding leasing (% of GDP, 2008)

New Business Leasing (EUR bn)

Italy and Austria around

8% of GDP

Notes: CEE in new business leasing is excluding Ukraine and Latvia; CEE in outstanding is excluding Bosnia and RomaniaSources: UniCredit CEE Strategic Analysis

25

The growth of the leasing business surpassed corporate loans growth in most of the countries – leasing can continue to bridge the gap between investments and banks’ long term loans

0%

10%

20%

30%

40%

50%

60%

70%

80%

Poland

Czech

Slovakia

Slovenia

LithuaniaLatvi

aEsto

niaBulgar

iaCro

atiaTurk

eyUkra

ineRussia CEE

Corporate loans avgGrowth 2007-2008

Leasing OutstandingAvg Growth 2007-2008

Source: UniCredit CEE Strategic analysis

Outstanding Leasing and corporate loansAvg % 2007-’08 growth

Growth of leasing business in EMU area was around 9% nominally

during the last decade

26

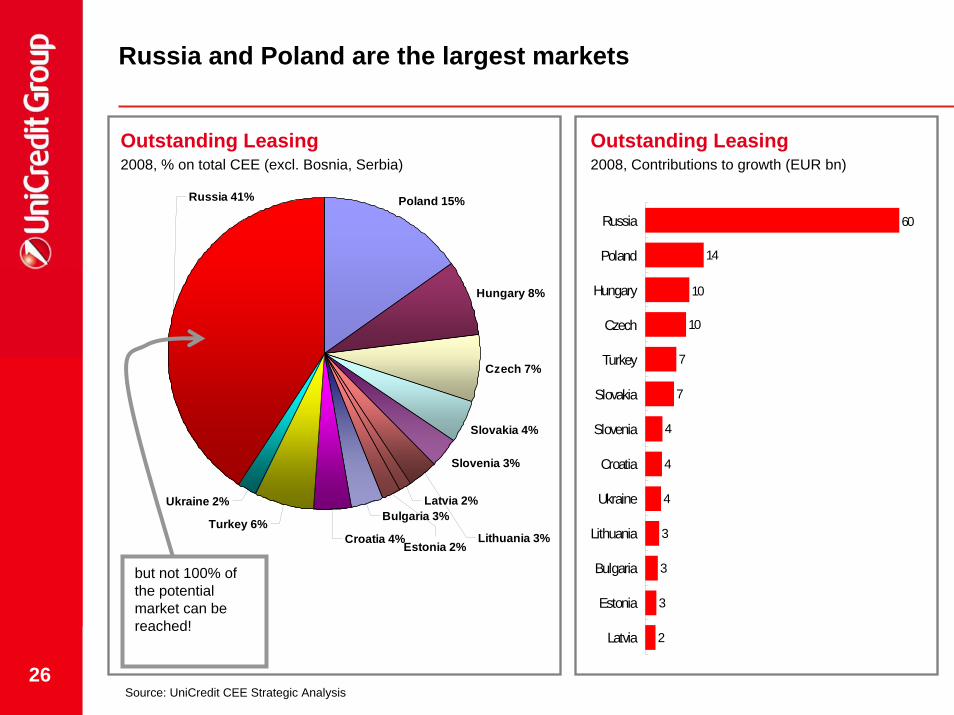

Russia and Poland are the largest markets

2

3

3

3

4

4

4

7

7

10

10

14

60

Latvia

Estonia

Bulgaria

Lithuania

Ukraine

Croatia

Slovenia

Slovakia

Turkey

Czech

Hungary

Poland

Russia

Outstanding Leasing2008, % on total CEE (excl. Bosnia, Serbia)

Outstanding Leasing2008, Contributions to growth (EUR bn)

Poland 15%

Hungary 8%

Czech 7%

Slovakia 4%

Slovenia 3%

Bulgaria 3%

Croatia 4%Turkey 6%

Ukraine 2%

Russia 41%

Estonia 2%

Latvia 2%

Lithuania 3%

but not 100% of the potential market can be reached!

Source: UniCredit CEE Strategic Analysis

27

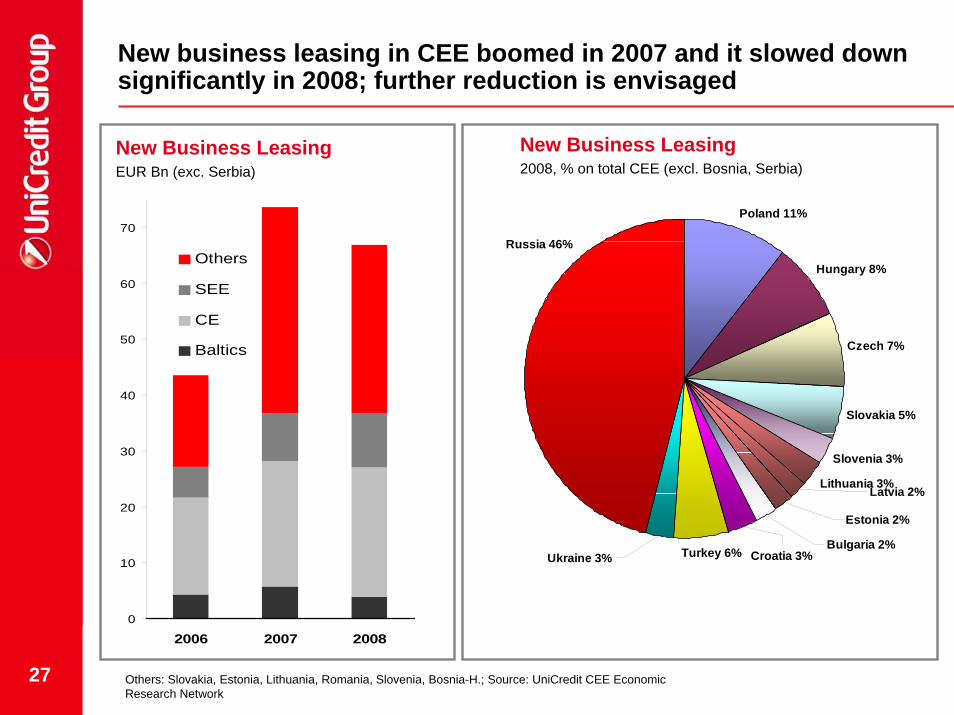

New business leasing in CEE boomed in 2007 and it slowed down significantly in 2008; further reduction is envisaged

New Business LeasingEUR Bn (exc. Serbia)

New Business Leasing2008, % on total CEE (excl. Bosnia, Serbia)

0

10

20

30

40

50

60

70

2006 2007 2008

Others

SEE

CE

Baltics

Poland 11%

Hungary 8%

Czech 7%

Slovakia 5%

Slovenia 3%

Lithuania 3%

Turkey 6%Ukraine 3% Croatia 3%

Russia 46%

Estonia 2%

Latvia 2%

Bulgaria 2%

Others: Slovakia, Estonia, Lithuania, Romania, Slovenia, Bosnia-H.; Source: UniCredit CEE EconomicResearch Network

28

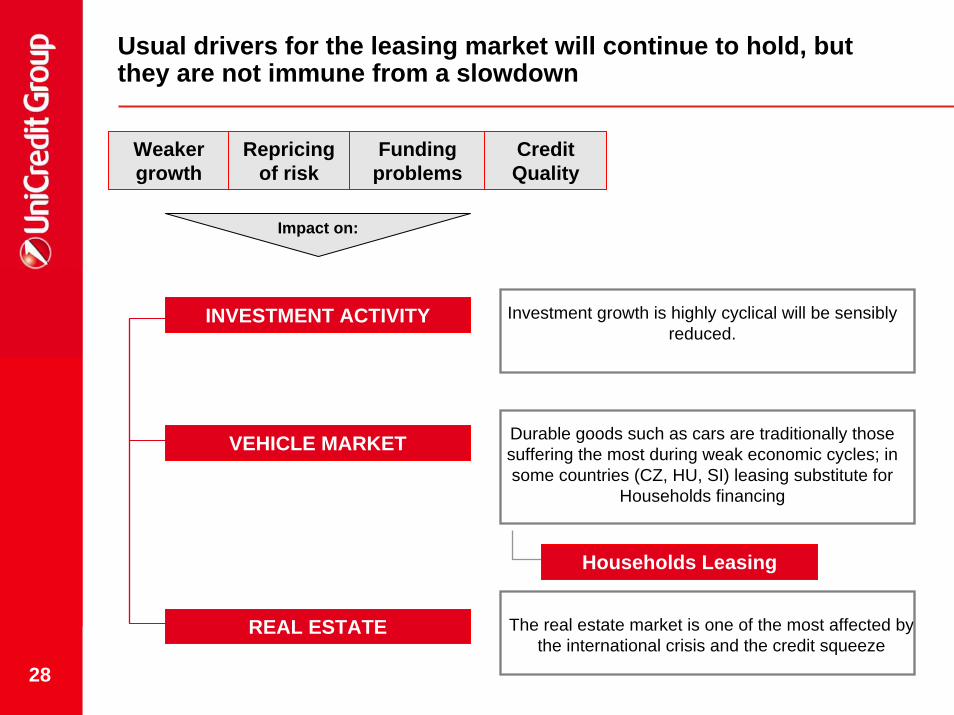

Usual drivers for the leasing market will continue to hold, but they are not immune from a slowdown

Weaker growth

Repricingof risk

Funding problems

Credit Quality

Impact on:

INVESTMENT ACTIVITY

VEHICLE MARKET

REAL ESTATE

Investment growth is highly cyclical will be sensibly reduced.

Durable goods such as cars are traditionally those suffering the most during weak economic cycles; in some countries (CZ, HU, SI) leasing substitute for

Households financing

Households Leasing

The real estate market is one of the most affected by the international crisis and the credit squeeze

29

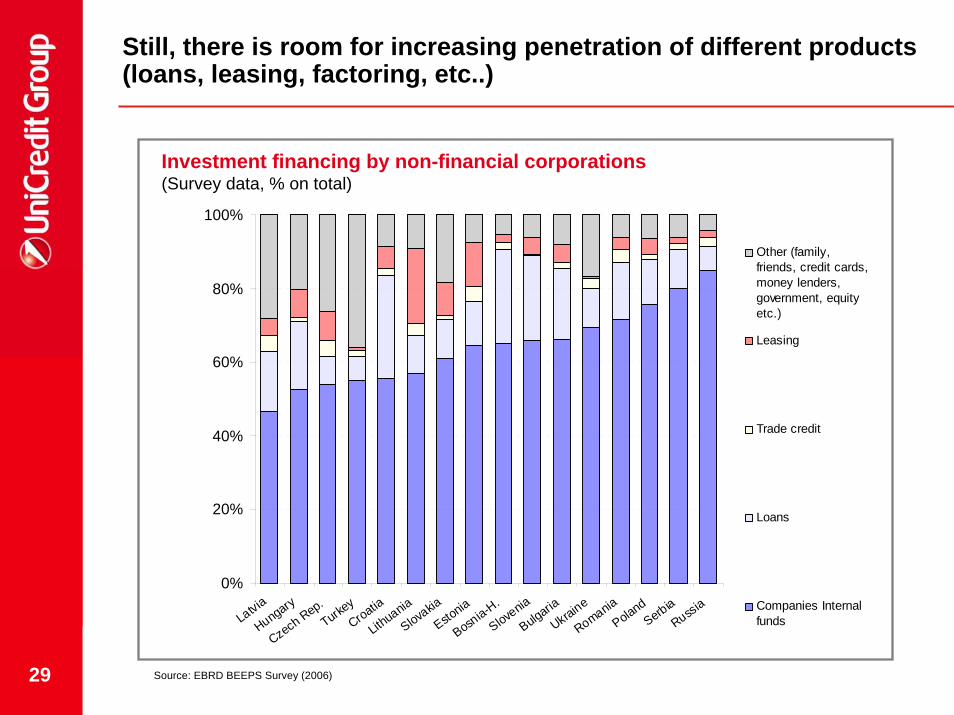

Still, there is room for increasing penetration of different products (loans, leasing, factoring, etc..)

Investment financing by non-financial corporations (Survey data, % on total)

0%

20%

40%

60%

80%

100%

Latvia

Hungary

Czech Rep.Turke

yCroatia

Lithuania

Slovakia

Estonia

Bosnia-H.

Slovenia

Bulgaria

Ukraine

RomaniaPoland

SerbiaRussia

Other (family,friends, credit cards,money lenders,government, equityetc.)

Leasing

Trade credit

Loans

Companies Internalfunds

Source: EBRD BEEPS Survey (2006)

30

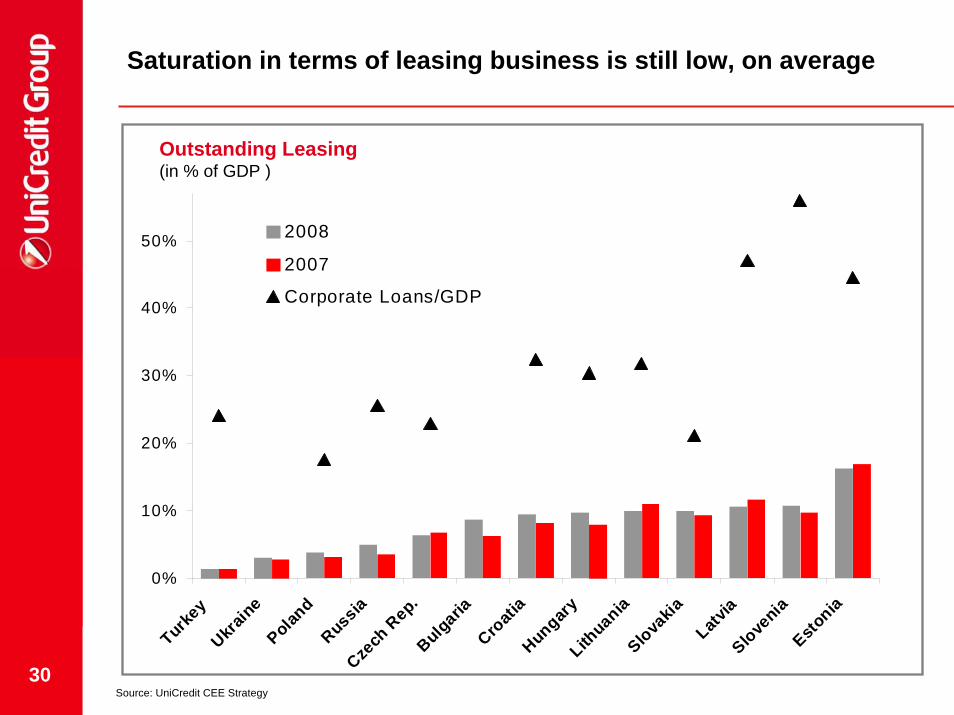

Saturation in terms of leasing business is still low, on average

0%

10%

20%

30%

40%

50%

Turkey

Ukrain

ePolan

dRussia

Czech

Rep.

BulgariaCro

atia

Hungary

Lithuania

Slovakia

Latvia

Slovenia

Estonia

2008

2007

Corporate Loans/GDP

Source: UniCredit CEE Strategy

Outstanding Leasing (in % of GDP )

31

AGENDA

The global financial crisis and the effects on Central Eastern Europe

The banking sectors in CEE

The challenges for the leasing market

Conclusions

32

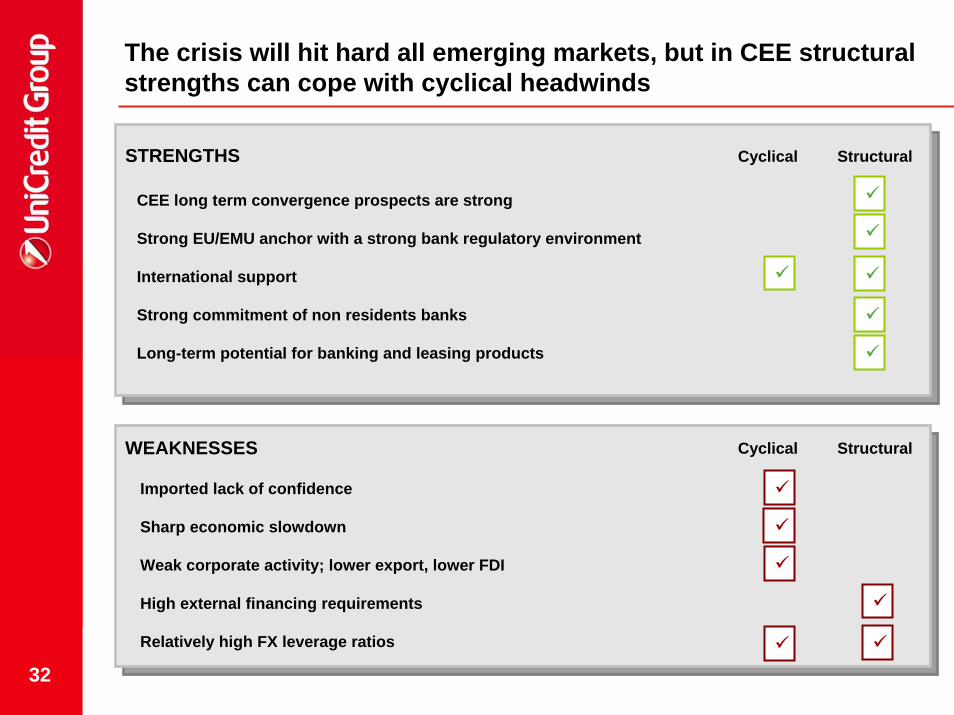

The crisis will hit hard all emerging markets, but in CEE structural strengths can cope with cyclical headwinds

STRENGTHS

CEE long term convergence prospects are strong

Strong EU/EMU anchor with a strong bank regulatory environment

International support

Strong commitment of non residents banks

Long-term potential for banking and leasing products

Cyclical Structural

WEAKNESSES Cyclical Structural

Imported lack of confidence

Sharp economic slowdown

Weak corporate activity; lower export, lower FDI

High external financing requirements

Relatively high FX leverage ratios

33

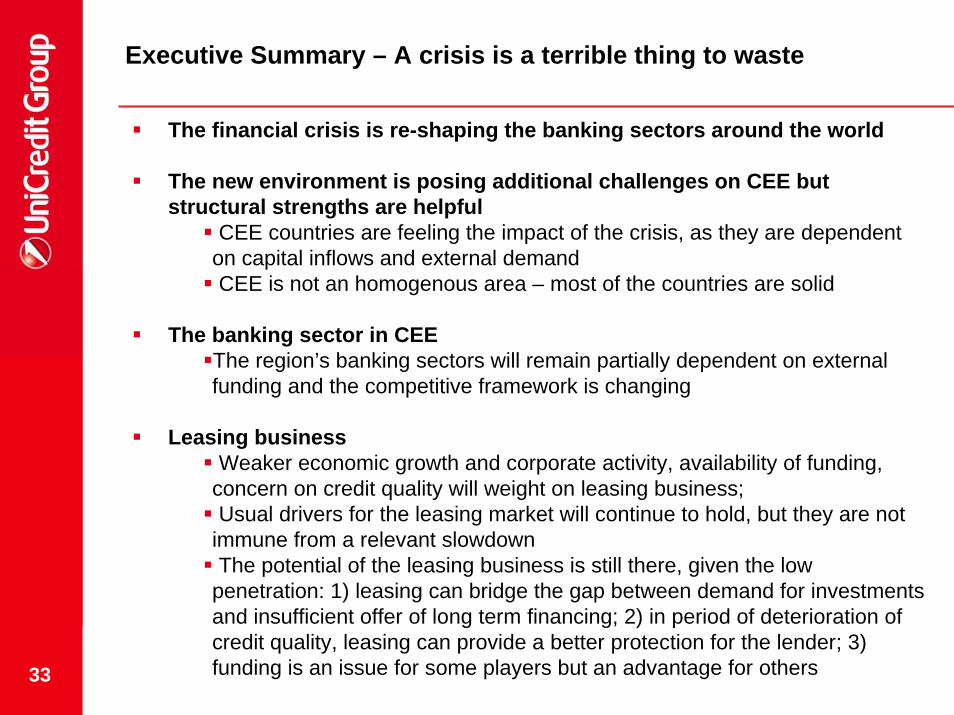

Executive Summary – A crisis is a terrible thing to waste

The financial crisis is re-shaping the banking sectors around the world

The new environment is posing additional challenges on CEE but structural strengths are helpful

CEE countries are feeling the impact of the crisis, as they are dependent on capital inflows and external demandCEE is not an homogenous area – most of the countries are solid

The banking sector in CEE The region’s banking sectors will remain partially dependent on external funding and the competitive framework is changing

Leasing business Weaker economic growth and corporate activity, availability of funding,

concern on credit quality will weight on leasing business; Usual drivers for the leasing market will continue to hold, but they are not

immune from a relevant slowdownThe potential of the leasing business is still there, given the low

penetration: 1) leasing can bridge the gap between demand for investments and insufficient offer of long term financing; 2) in period of deterioration of credit quality, leasing can provide a better protection for the lender; 3) funding is an issue for some players but an advantage for others

34

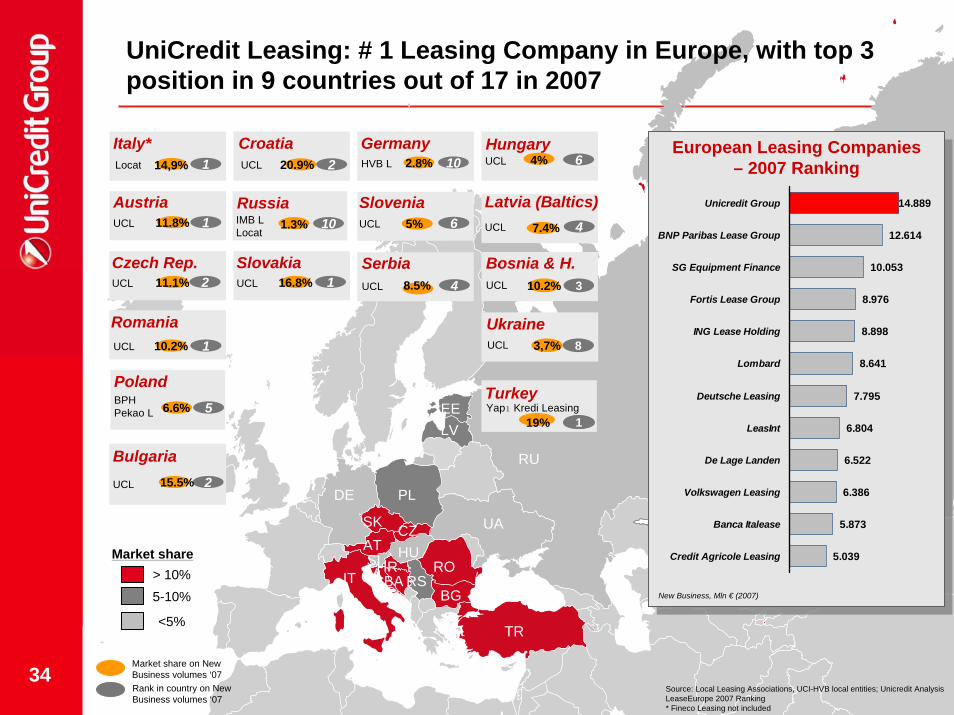

PL

RU

ROIT

SI

TR

DE

ATSK CZ

HUHRBA RS

BG

LVEE

UA

> 10%5-10%

<5%

Market share

Rank in country on New Business volumes ‘07

Market share on New Business volumes ‘07

GermanyHVB L 102.8%

Czech Rep.UCL 211.1%

RomaniaUCL 110.2%

Italy*Locat 114,9%

AustriaUCL 111.8%

RussiaIMB LLocat

101.3%

PolandBPH Pekao L 56.6%

SlovakiaUCL 116.8%

BulgariaUCL 215.5%

Bosnia & H. UCL 10.2% 3

CroatiaUCL 220.9%

Ukraine3,7% 8UCL

Source: Local Leasing Associations, UCI-HVB local entities; Unicredit AnalysisLeaseEurope 2007 Ranking* Fineco Leasing not included

UCL

Slovenia65%

HungaryUCL 64%

SerbiaUCL 48.5%

Latvia (Baltics)UCL 47.4%

TurkeyYapı Kredi Leasing

119%

14.889

12.614

10.053

8.976

8.898

8.641

7.795

6.804

6.522

6.386

5.873

5.039

Unicredit Group

BNP Paribas Lease Group

SG Equipment Finance

Fortis Lease Group

ING Lease Holding

Lombard

Deutsche Leasing

LeasInt

De Lage Landen

Volkswagen Leasing

Banca Italease

Credit Agricole Leasing

European Leasing Companies– 2007 Ranking

New Business, Mln € (2007)

UniCredit Leasing: # 1 Leasing Company in Europe, with top 3 position in 9 countries out of 17 in 2007

36

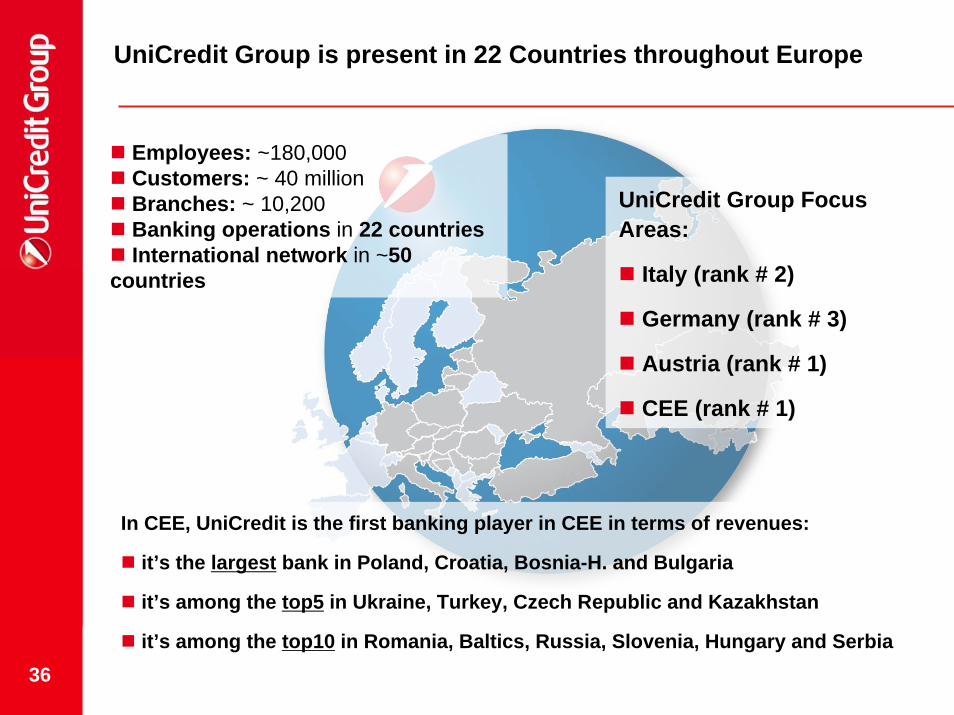

UniCredit Group is present in 22 Countries throughout Europe

In CEE, UniCredit is the first banking player in CEE in terms of revenues:

it’s the largest bank in Poland, Croatia, Bosnia-H. and Bulgaria

it’s among the top5 in Ukraine, Turkey, Czech Republic and Kazakhstan

it’s among the top10 in Romania, Baltics, Russia, Slovenia, Hungary and Serbia

Employees: ~180,000Customers: ~ 40 millionBranches: ~ 10,200Banking operations in 22 countriesInternational network in ~50

countries

UniCredit Group Focus Areas:

Italy (rank # 2)

Germany (rank # 3)

Austria (rank # 1)

CEE (rank # 1)

37

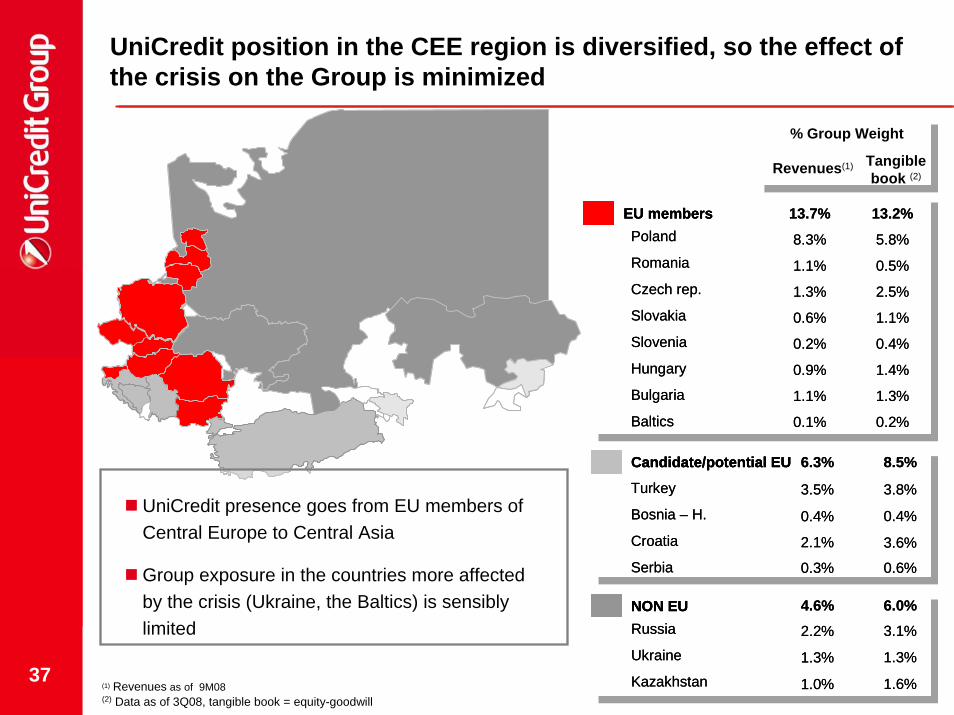

UniCredit position in the CEE region is diversified, so the effect of the crisis on the Group is minimized

UniCredit presence goes from EU members of Central Europe to Central Asia

Group exposure in the countries more affected by the crisis (Ukraine, the Baltics) is sensibly limited

% Group Weight

Revenues(1) Tangiblebook (2)

EU membersPoland

Romania

Czech rep.

Slovakia

Slovenia

Hungary

Bulgaria

Baltics

13.7% 13.2%

8.3% 5.8%

1.1% 0.5%

1.3% 2.5%

0.6% 1.1%

0.2% 0.4%

1.1% 1.3%

0.1% 0.2%

0.9% 1.4%

EU membersEU membersPoland

Romania

Czech rep.

Slovakia

Slovenia

Hungary

Bulgaria

Baltics

13.7% 13.2%

8.3% 5.8%

1.1% 0.5%

1.3% 2.5%

0.6% 1.1%

0.2% 0.4%

1.1% 1.3%

0.1% 0.2%

0.9% 1.4%

Candidate/potential EU

Turkey

Bosnia – H.

Croatia

Serbia

6.3% 8.5%

3.5% 3.8%

0.4% 0.4%

0.3%

3.6%2.1%

0.6%

Candidate/potential EUCandidate/potential EU

Turkey

Bosnia – H.

Croatia

Serbia

6.3% 8.5%

3.5% 3.8%

0.4% 0.4%

0.3%

3.6%2.1%

0.6%

NON EURussia

Ukraine

Kazakhstan

4.6% 6.0%

2.2% 3.1%

1.3% 1.3%

1.0% 1.6%

NON EUNON EURussia

Ukraine

Kazakhstan

4.6% 6.0%

2.2% 3.1%

1.3% 1.3%

1.0% 1.6%(2) Data as of 3Q08, tangible book = equity-goodwill(1) Revenues as of 9M08