Download - Canada's Top 50 Advisors

WWW.WEALTHPROFESSIONAL.CA

ISSUE 1.2 | $6.95

JOHN CUCCHIELLAINDEPENDENT TAKES ON

THE COMPETITION

PERFECTION PERSONIFIEDTHE IDEAL ‘FEE CLIENT’

REVEALED

LEADER OF THE PACKLEARN FROM

THE NO. 1 ADVISOR

TOP

ADVISORSCANADA’S BEST FINANCIAL ADVISORS REVEALED >>

Cover_IFC.indd 1 09/01/2014 2:13:36 PM

18 | JANUARY 2014

SPECIAL REPORT

WEA

LTH

PROFESSIONAL

ADVISOR 201

4

The time has come to recognize the country’s finest planners as we unveil Wealth Professional’s inaugural list of the top 50 financial

advisors in Canada. In a trailblazing initiative, the industry’s top performers are finally being rewarded for their excellence

TOP

SPECIAL REPORT / TOP 50 ADVISORS

JANUARY 2014 | 18

Too often the tireless and vital work that financial planners perform is overlooked in terms of recognition. Wealth Professional would like to put that right. This issue is dedicated to making heroes out of the most hard-working and successful advisors in Canada, which was the driving force behind this presentation of the top 50 advisors in Canada.

Of course it fell to you to make a submission, but what was the methodology behind the rankings? The results are purely objective and based on fixed criteria of performance. The first two aspects we ranked were the increase of assets under management (AUM) in the financial year ended October 31, 2013, and revenue the individual contributed to the business. Due to their vital role, these aspects of performance were given heavy weighting.

Other aspects ranked were client retention, new clients introduced to the business, new business as a percentage of total client base and AUM per client managed by the individual planner. This is all designed to provide a good cross section of well-rounded planners.

Thanks to all the advisors who took the time to enter and congratulations to all those who made the cut. As part of Wealth Professional’s wider ethos to not just inform our readers, but also actively find ways to improve their business and profitably, we hope making the rankings will have a profound impact on your reputation.

We hope you enjoy the rundown and if you did not enter this year, we hope that you will do so the next time.

ADVISORS

18-33_TOP_50(2).indd 18 09/01/2014 2:20:43 PM

THE TOP 50

JANUARY 2014 | 19

WEALTHPROFESSIONAL.CA

GENDER DIVIDE

40 VS. 10

AVERAGE YEARS IN THE BUSINESS

MONEY MATTERS

18

25 298$1.2M

YEARS

AVG. AUM GROWTH YOY (%) AVG. NUMBER OF CLIENTSAVG. REVENUE

20%

80%

British Columbia: 14

Quebec: 5

Ontario: 20

P.E.I.: 1Manitoba: 3Saskatchewan: 1Alberta: 6

BY THE PROVINCE

18-33_TOP_50(2).indd 19 09/01/2014 2:20:57 PM

TOP 50 AdvisorsOVERALL RANKING NAME COMPANY

BROKERAGE/DEALER GROUP NAME

AUM GROWTH YOY (%)

REVENUE CONTRIBUTED ($)

CLIENTS OCT. 31, 2013

1 Bill McElroy The William Douglas Group Inc. Manulife Securities Incorporated 87 500,000 1200

2 Léony deGraaf deGraaf Financial Strategies MGA - Gryphin Advantage 50 250,000 225

3 Nathan Leibowitz Assante Wealth Management Assante Wealth Management 32 350,000 250

4 Anita Dalakoti Dalakoti Financial & Insurance Services Inc. Sun Life Financal 25 2,500,000 925

5 Charles Jiang Queen Financial Group Inc. Queen Financial Group Inc. 19 280,000 330

6 Nick BakishInvestors Group Financial Services Inc., Financial Services Firm

Investors Group Financial Services Inc., Financial Services Firm

17 600,000 1103

7 Stephen Jones Assante Financial Managment Ltd Assante Financial Managment Ltd 34 600,000 115

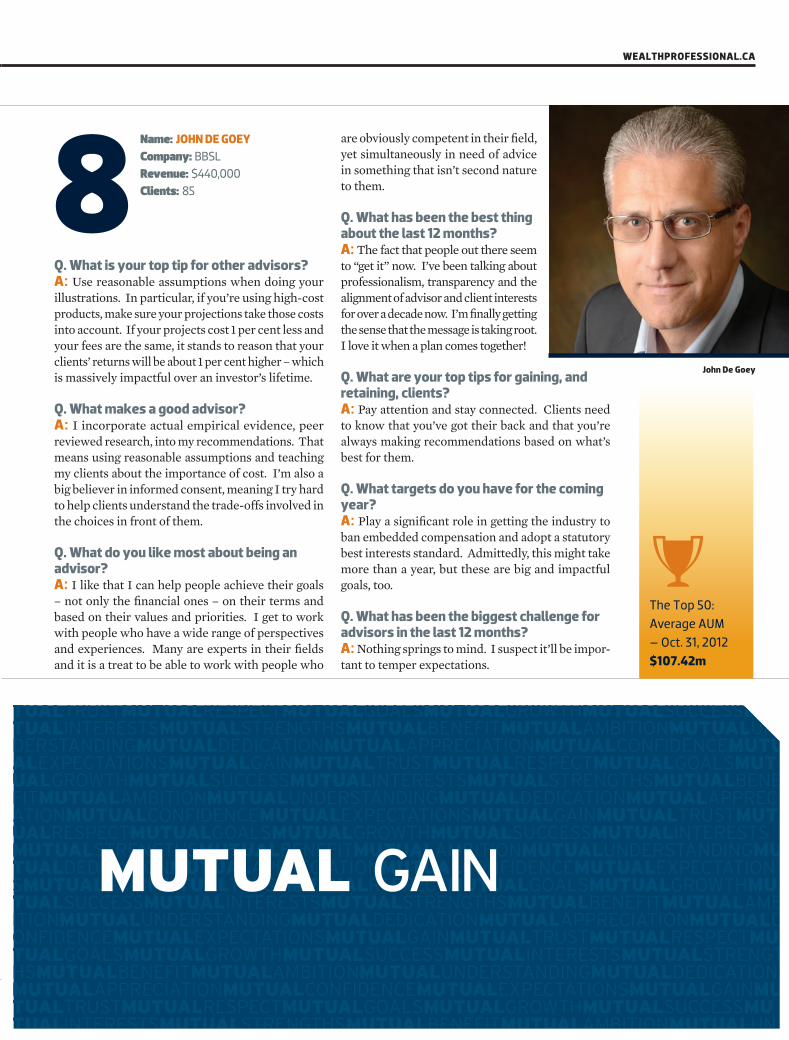

8 John De Goey BBSL BBSL 49 440,000 85

9 Cyrilla Saunders Saunders Wealth Advisory Group (SWAG) CIBC Wood Gundy 43 1,200,000 250

10 Tim Kelly Tim Kelly Sun Life Financial Sun Life Financial 20 2,600,000 800

11 Gene Kim Summit Private Wealth Inc. Manulife Securities Incorporated 25 500,000 100

12 Don Taylor Taylor Spies Wealth Management Nesbitt Burns 37 1,600,000 260

13 Eva Rubinstein RD Wealth Management BMO Nesbitt Burns 16 850,000 450

14 Luke Kratz Kratz Group CIBC Wood Gundy 29 1,077,865 205

15 Chad Price Odlum Brown Limited Odlum Brown Limited 21 480,000 110

16 Shafik Hirani Shafik Hirani Private Wealth Managment Investors Group 43 4,000,000 610

17 Reg Jackson JMRD Wealth Management Team National Bank Financial 16 2,000,000 725

18 Peter Boronkay The Boronkay Team Raymond James Ltd. 25 350,000 67

19 Chet Brothers Brothers & Company Financial FundEX Investments Inc. 14 625,000 238

20 Rob McClelland The McClelland Financial Group Assante Capital Management Ltd. 19 3,000,000 694

21 Laurie Bonten The Bonten Group National Bank Financial 22 1,300,000 250

22 Brian McGorman The McGorman Investment Team CIBC Wood Gundy 31 2,295,135 345

23 Wolfgang Klein Canaccord Genuity Wealth Management Canaccord Genuity 29 1,200,000 190

24 Michael Trklja CDSPI Advisory Services CDSPI Advisory Services 11 650,000 218

25 Mike Lakhani Tax Matters for Dentists (TMFD) Assante Wealth Management 28 2,800,000 376

26 Paul Johnson Johnson Legacy Wealth Management Raymond James Ltd. 28 1,000,000 125

27 Elie Nour Elie Nour Group Manulife Securities Inc. 36 2,000,000 140

28 William Vastis The William Vastis Wealth Management GroupRBC Wealth Management Dominion Securities Inc

50 5,100,000 115

29 Eric Davis Davis Wealth Management Team TD Wealth 25 1,400,000 200

30 Brian S. Jones Brian Jones Wealth Management TD Waterhouse/ TD Wealth 18 1,100,000 205

31 Rona Birenbaum Caring for Clients Queensbury Strategies Inc. 16 850,000 155

32 David Christianson Christianson Wealth AdvisorsNational Bank Financial Wealth Management

21 1,100,000 78

33 Penny Meadows CIBC CIBC Imperial Investor Services 20 682,921 245

34 Gillian Stovel Rivers Assante Financial Management Assante Wealth Managememt 19 1,253,862 140

35 Neil R. McIver McIver Wealth Management Consulting Group Richardson GMP 21 1,310,000 84

36 Kevin Webber Webber Brodlieb and Associates BMO Nesbitt Burns 17 2,370,000 248

37 Joel David CIBC Wood Gundy CIBC World Markets Inc. 19 1,013,000 27

38 David Allard Navigation Wealth Management ScotiaMcleod 14 1,150,000 105

39 Ronald Rusnak Rusnak Financial Ltd. Manulife Securities 20 550,000 500

40 Amod P. Lokre Edward Jones Investments Edward Jones Investments 57 300,000 250

41 Jeff Watchorn CIBC Wood Gundy CIBC Wood Gundy 33 750,000 200

42 Oliver Gilbert CIBC Wood Gundy CIBC Wood Gundy 33 1,000,000 200

43 Jim Baumgartner National Bank Financial National Bank Financial 0 741,000 163

44 Brian Lonsdale Lonsdale Financial Group CIBC Wood Gundy 8 700,000 400

45 David J. Ritcey The Ritcey Team ScotiaMcLeod 5 725,000 221

46 Terry Heavisides Prarieview Wealth Management ScotiaMcLeod 13 1,558,345 380

47 Lyle Rouleau Rouleau Investment Group CIBC Wood Gundy 1 1,465,000 220

48 Jack Panteluk The Panteluk Wealth Advisory Group BMO Nesbitt Burns 8 1,200,000 210

49 Paul Hurwitz Raymond James Ltd. Raymond James Ltd. 0 1,040,000 215

50 Glen Lyster Lyster Financial SunLife 30 750,000 N/A

With rising interest rates on the horizon, clients need a plan to protect portfolios. Renaissance has partnered with the experts at Ares Management to bring demonstrated, institutional fl oating rate debt investment management exclusively to individual Canadian investors.

RISING RATE PROTECTION

Help clients prepare for what lies ahead with Renaissance Floating Rate Income Fund.

renaissanceinvestments.ca

A STRONG DEFENSE ISN’T

BUILT BY THOSE WHO GO

HALFWAY. Exclusive Access to Ares Institutional Floating Rate Expertise

®Renaissance Investments is offered by and is a registered trademark of CIBC Asset Management Inc.Commissions, trailing commissions, management fees, and expenses all may be associated with mutual fund investments. Please read the prospectus before investing. Mutual funds are not guaranteed, their values change frequently, and past performance may not be repeated.

With rising interest rates on the horizon, clients need a plan to protect portfolios. Renaissance has partnered with the experts at Ares Management to bring demonstrated, institutional fl oating rate debt investment management exclusively to individual Canadian investors.

RISING RATE PROTECTION

Help clients prepare for what lies ahead with Renaissance Floating Rate Income Fund.

renaissanceinvestments.ca

A STRONG DEFENSE ISN’T

BUILT BY THOSE WHO GO

HALFWAY. Exclusive Access to Ares Institutional Floating Rate Expertise

®Renaissance Investments is offered by and is a registered trademark of CIBC Asset Management Inc.Commissions, trailing commissions, management fees, and expenses all may be associated with mutual fund investments. Please read the prospectus before investing. Mutual funds are not guaranteed, their values change frequently, and past performance may not be repeated.20 | JANUARY 2014

SPECIAL REPORT

WEA

LTH

PROFESSIONAL

ADVISOR 201

4

18-33_TOP_50(2).indd 20 09/01/2014 2:20:52 PM

22 | JANUARY 2014

SPECIAL REPORT

WEA

LTH

PROFESSIONAL

ADVISOR 201

4

Cyrilla Saunders

MUTUAL GAIN

file name: NWBR13147_WealthProfAdsArtist: Nicole date: 2014-01-02 colours: 4 media:

description: WP 1/3pg ads trim size: 8.25” x 3.625”

c m # #

market/city:

publication: Wealth Prof.

insertion date: YYYY-MM

shipping date: YYYY-MM-DD

ad #: NW-BR-13-147-M-D1

client: NEI safety/live: 7.5” x 2.875”

built size: 100% bleed size: 8.75” x 4.125”

y k # ## of sides: 1 folded size: 00.00” x 00.00”

d&s signoffs copywriter: creative: account:

client final approval via e-mail from: date:

380 wellington st. west toronto ontario canada m5v1e3 t 416 203 3470 Laser output may not be to size.

Q. What makes a good advisor?A: I believe a good financial planner must be client goal-driven. This means the planner and his client share the same financial goals and objectives.

Q. What do you like most about being an advisor? A: The satisfaction of helping people reach their goals. Providing clients with wealth-building, asset preserva-tion and lifetime income.

Q. What is your top tip for other advisors? A: Listen! Listen! Listen! to your clients’ needs.

Q. What are your top tips for gaining, and retaining, clients? A: Client service and a disci-plined approach to regular com-munication. My office is always dialoguing with clients! Recog-nizing their milestones and cel-ebrating with them.

Q. What has been the biggest challenge for advisors in the last 12 months? A: Tempering client excitement. Let’s face it, markets have been quite volatile up until last year. Clients must be reminded above-average returns cannot happen every year. It’s my job to reassure them to maintain their goals.

Q. How do you plan to adapt to the many regulatory changes that are set to affect the industry? A: I am already adapting. My dealer and retailers have done an exceptional job of informing us about the up-coming changes. And if clients need to understand any of the changes I will be prepared for them.

Q. How do you plan to adapt to the regulatory changes that are set to affect the industry?A: We have already embraced the full disclosure of fees strategy, where for the past eight years, we disclose to each client relationship via our customized IPSs, the fees they are paying on each strategy in each account. Additionally, if the fees are intended to be used as a tax-deductible expense, we council our clients to discuss this matter with the tax accountant/advisor. In the past, as additional regulatory changes became mandatory, we have always found a way to encourage client participation in gaining knowledge.

Q. What makes a good advisor?A: An individual who has the ability to be trusted and draw appropriate information from clients, listen carefully to their responses in both language and feeling and then be able to interpret this into a “financial plan” that is credible and easy to understand for the client. Finally, the actual implemen-tation and subsequent timely follow-ups to ensure the path still suits is the key to success.

Q. What is your top tip for other advisors?A: It is all about the client. Stay true to your core beliefs. Knowledge and education will always serve you and your clients well. Create a circle of knowledgeable professionals around you, both in-house and in the commu-nity you serve . . . these people will benefit your clients.

Name: TIM KELLYCompany: Sun Life Financial InvestmentsRevenue: $2,600,000 Clients: 800

Name: CYRILLA SAUNDERSCompany: Saunders Wealth Advisory Group (SWAG) Revenue: $1,200,000 Clients: 250

10

9Tim Kelly

The advisor in our Top 10 with the most revenue was Tim Kelly with $2,600,000

18-33_TOP_50(2).indd 22 09/01/2014 2:21:01 PM

JANUARY 2014 | 23

WEALTHPROFESSIONAL.CA

MUTUAL GAIN

file name: NWBR13147_WealthProfAdsArtist: Nicole date: 2014-01-02 colours: 4 media:

description: WP 1/3pg ads trim size: 8.25” x 3.625”

c m # #

market/city:

publication: Wealth Prof.

insertion date: YYYY-MM

shipping date: YYYY-MM-DD

ad #: NW-BR-13-147-M-D1

client: NEI safety/live: 7.5” x 2.875”

built size: 100% bleed size: 8.75” x 4.125”

y k # ## of sides: 1 folded size: 00.00” x 00.00”

d&s signoffs copywriter: creative: account:

client final approval via e-mail from: date:

380 wellington st. west toronto ontario canada m5v1e3 t 416 203 3470 Laser output may not be to size.

Q. What is your top tip for other advisors? A: Use reasonable assumptions when doing your illustrations. In particular, if you’re using high-cost products, make sure your projections take those costs into account. If your projects cost 1 per cent less and your fees are the same, it stands to reason that your clients’ returns will be about 1 per cent higher – which is massively impactful over an investor’s lifetime.

Q. What makes a good advisor? A: I incorporate actual empirical evidence, peer reviewed research, into my recommendations. That means using reasonable assumptions and teaching my clients about the importance of cost. I’m also a big believer in informed consent, meaning I try hard to help clients understand the trade-offs involved in the choices in front of them.

Q. What do you like most about being an advisor? A: I like that I can help people achieve their goals – not only the financial ones – on their terms and based on their values and priorities. I get to work with people who have a wide range of perspectives and experiences. Many are experts in their fields and it is a treat to be able to work with people who

Name: JOHN DE GOEYCompany: BBSLRevenue: $440,000 Clients: 858

John De Goey

are obviously competent in their field, yet simultaneously in need of advice in something that isn’t second nature to them.

Q. What has been the best thing about the last 12 months? A: The fact that people out there seem to “get it” now. I’ve been talking about professionalism, transparency and the alignment of advisor and client interests for over a decade now. I’m finally getting the sense that the message is taking root. I love it when a plan comes together!

Q. What are your top tips for gaining, and retaining, clients? A: Pay attention and stay connected. Clients need to know that you’ve got their back and that you’re always making recommendations based on what’s best for them.

Q. What targets do you have for the coming year? A: Play a significant role in getting the industry to ban embedded compensation and adopt a statutory best interests standard. Admittedly, this might take more than a year, but these are big and impactful goals, too.

Q. What has been the biggest challenge for advisors in the last 12 months? A: Nothing springs to mind. I suspect it’ll be impor-tant to temper expectations.

The Top 50:Average AUM – Oct. 31, 2012 $107.42m

18-33_TOP_50(2).indd 23 09/01/2014 2:21:02 PM

24 | JANUARY 2014

SPECIAL REPORT

WEA

LTH

PROFESSIONAL

ADVISOR 201

4

Stephen Jones

Q. What has been the best thing about the last 12 months?A: My investment style (a conservative, globally diversified, tax-optimized program) has yielded tremendous result. In a year where bonds are negative, and

Canadian equities earn ~ 6 per cent, we have provided returns at much higher levels, using a pension style approach that incorporates both low-cost indexes provided by DFA and active management through CI’s Evolution program.

Q. What makes a good advisor?A: A good advisor must have a servant’s attitude, and an open mind. We are here to help, using our experience, ideas, and sound judgement to present the best ideas possible. The client then decides what is best for them, and what can be done today versus tomorrow.

Q. What is your top tip for other advisors?A: I often say that I am in “the client retention business.” Focus on activities today that lead to clients who will be there 20 years down the road. Q. What are your top tips for gaining, and retaining, clients?A: I take the time to do “my homework.” This means looking at every detail of a client’s financial situation. For example, where many advisors looks at CRA tax assessments on, I need to review the full tax return, and all of the slips. And not just for mom and dad, but for the whole family as well. This extra time allows me to make better recommendations.

Q. What are your top tips for gaining, and retaining clients?A: Being consistent in your work ethic is a main tip for retaining clients but even more so is servicing your clients and following up with those services. Following up with clients has been one of the best ways for my team and I to grow our practice and maintain our clients. Alongside those points, understanding your target clientele and where your strengths lie is one aspect that can allow an advisor to grow yearly.

Q. What makes a good advisor?A: I have always felt listening was the main characteristic defining a good advisor. A good advisor will not only listen to his client’s needs, but will always pay close attention to detail, maintain a high level of professionalism and integrity for every client and prospect.

Q. What do you like most about being an advisor?A: There are many aspects I enjoy but the biggest reward has always been seeing people reach their retirement goals. Knowing I played a small role in allowing people to retire comfortably has always been extremely enjoyable. In addition to that, I have always felt a great sense of accomplishment helping young pro-fessionals understand and develop ways to reach their financial goals.

Q. What has been the best thing about the last 12 months?A: In the past 12 twelve months my team and I have expanded and grown in various ways. I think developing new strategies and enhancing our team dynamic has had a positive influence with regards to our public appearance and has had a tremendous effect on how we conduct ourselves throughout this business.

Name: STEPHEN JONESCompany: Assante Financial Management Ltd.Revenue: $600,000Clients: 115

Name: NICK BAKISHCompany: Investors Group Financial Services Inc., Financial Services FirmRevenue: $600,000Clients: 1,103

7

6

MUTUAL BENEFIT

file name: NWBR13147_WealthProfAdsArtist: Nicole date: 2014-01-02 colours: 4 media:

description: WP 1/3pg ads trim size: 8.25” x 3.625”

c m # #

market/city:

publication: Wealth Prof.

insertion date: YYYY-MM

shipping date: YYYY-MM-DD

ad #: NW-BR-13-147-M-D2

client: NEI safety/live: 7.5” x 2.875”

built size: 100% bleed size: 8.75” x 4.125”

y k # ## of sides: 1 folded size: 00.00” x 00.00”

d&s signoffs copywriter: creative: account:

client final approval via e-mail from: date:

380 wellington st. west toronto ontario canada m5v1e3 t 416 203 3470 Laser output may not be to size.

Nick Bakish

Q. What is your top tip for other advisors?A: One tip I can give to other advisors is always be ready to learn as much as you can and teach whenever there is an opportunity. I believe in contin-uously learning as much as possible and there is always room to keep learning.

The Top 50:Average number of clients lost (FY 2013) 4.7

18-33_TOP_50(2).indd 24 09/01/2014 2:21:06 PM

JANUARY 2014 | 25

WEALTHPROFESSIONAL.CA

MUTUAL BENEFIT

file name: NWBR13147_WealthProfAdsArtist: Nicole date: 2014-01-02 colours: 4 media:

description: WP 1/3pg ads trim size: 8.25” x 3.625”

c m # #

market/city:

publication: Wealth Prof.

insertion date: YYYY-MM

shipping date: YYYY-MM-DD

ad #: NW-BR-13-147-M-D2

client: NEI safety/live: 7.5” x 2.875”

built size: 100% bleed size: 8.75” x 4.125”

y k # ## of sides: 1 folded size: 00.00” x 00.00”

d&s signoffs copywriter: creative: account:

client final approval via e-mail from: date:

380 wellington st. west toronto ontario canada m5v1e3 t 416 203 3470 Laser output may not be to size.

Q. What makes a good advisor?A: A good advisor should love his or her job, and be able to provide some good, solid advice. He or she should be experienced, knowledgeable, profession-al, holding industry standard designations, a member of a leading professional organization, and embrac-es continuing education and attends conferences. A good planner takes a holistic, planning based ap-proach, designs appropriate asset allocations and follows a process for discerning the clients’ needs and offering recommendations. He or she should always be an objective and independent advisor.

Q. What do you like most about being an advisor?A: I feel great when my advice and professional service really helps the client to solve their financial problems and provide solutions to reach their finan-cial goals. I feel great when I am respected for a professional job I’ve rendered to my clients. I feel great when I could guide clients, to walk them

Name: CHARLES JIANGCompany: Queen Financial Group Inc.Revenue: $280,000Clients: 3305

Charles Jiang

through market turmoil during the financial crisis. I convinced them to stick to their goals and the ob-jectives we set for them during the first few meet-ings.

Q. What has been the best thing about the last 12 months?A: The market has been recovering and the leading markets in the U.S. and Europe have been performing well. Investors are feeling better now that they see the recovery. The leading indicators in USA and Europe are relatively pos-itive. Many new jobs have been created and the un-employment rate in the USA has been decreasing.

Q. What are your top tips for gaining, and retaining, clients?A: Ultimately, service is what differentiates a good advisor from a mediocre one. Good service will help to gain and retain clients. Good service will also help to get referrals from trusted clients. By the same token, bad service will lead to loss of clients and assets.

The Top 50:Average AUM – Oct. 31, 2013 $142.16m

18-33_TOP_50(2).indd 25 09/01/2014 2:21:11 PM

26 | JANUARY 2014

SPECIAL REPORT

WEA

LTH

PROFESSIONAL

ADVISOR 201

4

Anita Dalakoti

Q. What do you like most about being an advisor? A: Being an integral part of my client’s lives. Providing solutions for finan-cial problems and realities - preparing them financially to face whatever life may throw at them. Preparing a plan to suit what the client wants and needs and watching those plans materialize through life events of the birth of a child, professional growth, promotions, marriages, teenager pains , growing older, retiring and finally passing away.

Q. What makes a good advisor? A: A good listener with a balanced and practical approach. The planning approach should take into consideration mathematical realities of a situation and at the same time incorporate the dreams and aspirations of our clients, finding a realistic path to achieving those dreams and aspirations. Creating an achievable financial plan empowers our clients and sets them up for continued success.

Q. What has been the best thing about the last 12 months? A: Unsolicited positive feedback from my clients is an affirmation that I am on the right track. I think that is by far the best thing that can happen to me in any given year. It did this year, too.

Q. What are your top tips for gaining, and retaining, clients? A: Empower yourself with knowledge so that you can add value to the ser-vices you provide your client. If you don’t do that you are simply an interme-diary and can be replaced by another intermediary. Do not mistake the word advisor to mean “salesperson.” I don’t believe one can replace a knowledge-able advisor — a wise client can certainly add to their repertoire of advisors, but will not replace you if you add value. It is very easy to replace a salesper-son, though, because they are intermediaries. Be a knowledgeable Advisor.

Q. What has been the biggest challenge for advisors in the last 12 months?A: Interest rates. For most of our portfolios that have a balanced mandate, the choice of how to struc-ture the fixed-income aspect has been challenging. The correction mid-year highlighted the risk inher-ent in bonds. Moving out on the risk curve may mitigate the interest rate risk, but does not provide protection from market corrections. I see this as being the biggest challenge moving forward as well.

Q. What makes a good advisor?A: A good advisor is a good friend. Getting to know and understand your client’s situation and profile is critical. Using a needs-based approach to formulate their plan is what the clients appreciate the most as there will not be any surprises. Finally, it is protecting them from their own potential mistakes. Q. What do you like most about being an advisor? A: People. I enjoy the diversity of people and helping them get where they only dreamed of by taking small steps at a time. We never try to reinvent the wheel overnight. In an industry that clients have many trust issues towards, it’s nice to hear clients praising the fact that you are trustworthy and introducing you to the next generation of their families.

Q. What has been the best thing about the last 12 months?A: Seeing the markets provide significant returns and we were still able to attract many new clients. This highlight-ed the fact that our approach is not only about investment returns. Our value-added approach is appreciated by clients and the referrals are starting to generate themselves.

Q. What is your top tip for other advisors?A: Wealth management is all the craze now, but I think the most critical is to find a niche that will drive your practice and allow you to spend your time ensuring that you are up to date on all facets of their needs, not only directly related to their financial planning.

Name: ANITA DALAKOTICompany: Dalakoti Financial & Insurance Services Inc.Revenue: $2,500,000Clients: 925

Name: NATHAN LEIBOWITZCompany: Assante Wealth ManagementRevenue: $350,000Clients: 250

4

3

MUTUAL SUCCESS

file name: NWBR13147_WealthProfAdsArtist: Nicole date: 2014-01-02 colours: 4 media:

description: WP 1/3pg ads trim size: 8.25” x 3.625”

c m # #

market/city:

publication: Wealth Prof.

insertion date: YYYY-MM

shipping date: YYYY-MM-DD

ad #: NW-BR-13-147-M-D3

client: NEI safety/live: 7.5” x 2.875”

built size: 100% bleed size: 8.75” x 4.125”

y k # ## of sides: 1 folded size: 00.00” x 00.00”

d&s signoffs copywriter: creative: account:

client final approval via e-mail from: date:

380 wellington st. west toronto ontario canada m5v1e3 t 416 203 3470 Laser output may not be to size.

Nathan Leibowitz

The Top 50:Average revenue per client $6,456

18-33_TOP_50(2).indd 26 09/01/2014 2:21:15 PM

JANUARY 2014 | 27

WEALTHPROFESSIONAL.CA

MUTUAL SUCCESS

file name: NWBR13147_WealthProfAdsArtist: Nicole date: 2014-01-02 colours: 4 media:

description: WP 1/3pg ads trim size: 8.25” x 3.625”

c m # #

market/city:

publication: Wealth Prof.

insertion date: YYYY-MM

shipping date: YYYY-MM-DD

ad #: NW-BR-13-147-M-D3

client: NEI safety/live: 7.5” x 2.875”

built size: 100% bleed size: 8.75” x 4.125”

y k # ## of sides: 1 folded size: 00.00” x 00.00”

d&s signoffs copywriter: creative: account:

client final approval via e-mail from: date:

380 wellington st. west toronto ontario canada m5v1e3 t 416 203 3470 Laser output may not be to size.

Q. What targets do you have for the coming year?A: I am looking forward to 2014, increasing the number of education seminars I offer, touching base with centres of influence and increasing sales to at least $300,000 of income.

Q. What makes a good advisor?A: A good advisor listens to what the client says, ordoesn’t say, and formulates recommendations to best match the client’s goals and family dynamics. A good planner is knowledgeable, trustworthy and client focused.

Q. What do you like most about being a financial planner?A: I like the satisfaction I receive from clients whenI have put their minds at ease over their retirement or estate plans. They are typically very grateful for the guidance, experience and solutions I can provide.

Q. What has been the best thing about the last 12 months?A: That it is over! Sentiment over the past year seemsto have been a little gloomy. I’m also happy to have my CFP studies behind me, which have been a big distrac-

Name: LÉONY DEGRAAF HASTINGSCompany: deGraaf Financial Strategies Revenue: $250,000Clients: 2252

tion over the past two years.

Q. What is your top tip for other advisors?A: If you listen to your clients and always put your clients needs first, you can’t go wrong!

Q. What are your top tips for gaining, and retaining, clients?A: I offer a complimentary con-sultation so the client and I can get an idea if we are a good fit for each other. Once they are a client, they know they can reach out to me for guidance on any financial matter. I pride myself on ...treating clients how I would like to be treated, as a valued client.

Q. What has been the biggest challenge for financial planners in the last 12 months?A: The unknown of how industry changes will affect our practices and our ability to deliver comprehensive advice to all clients of all asset levels. I don’t require minimum account sizes, as I believe no matter how much someone has been able to save, that is all they have and it is very important to them. I believe all clients deserve the same level of advice, regardless of their asset base.

Q. What are the biggest issues facing the financial advice industry today?A: I don’t feel regulators are obtaining enough inputfrom advisors in the field on how or if the industry requires changes.

Léony deGraaf Hastings

18-33_TOP_50(2).indd 27 09/01/2014 2:21:20 PM

WEA

LTH

PR

OFESSIONAL

ADVISOR 201

4

Q. What makes a good advisor? A: A good advisor listens to clients and talks to them attheir level. I have acquired many large clients and the complaints that they have about the previous advisor are usually one of two things: the advisor doesn’t understand what the client is looking for; the client doesn’t under-stand a word out of the advisor’s mouth.

If you have the credentials, you don’t have to impress the client with your jargon and a bunch of graphs and charts. The client can’t trust you if they don’t feel comfortable with you. That means listen and communicate on their level.

Q. What do you like most about being an advisor?A: I like helping people, whether that means makingthem money, saving them taxes or providing them with viable solutions to improve their financial situation. Whatever it is I do for my clients, I enjoy the personal satisfaction of being appreciated for what I do for them.

Q. What has been the best thing about the last 12 months? A: A lot has happened: I bought an existing practice, moved my office to a larger location, got my CIM and qualified for Manulife’s prestigious Five-star Master Builder award. It’s been a year of change for me. I would say that the best thing has been my renewed enthusiasm for this business. It can be very exciting and fast paced if you work at it.

Q. What is your top tip for other advisors?A: Diversify. I have built a multi-income-streamedoffice by focusing on the three things that are impor-tant to businessowners: Life insurance, investments and Group Benefits. When the financial markets are not attractive to investors, I always have something to fall back on. I have become the “go to” person at my clients’ company. Whether it’s a buy/sell, group benefits, pensions or the personal needs of the staff, I can help them out.

There are going to be a lot of questions asked of advisors and the big one is going to be “What am I paying you for?”

Bill McElroy

Name: BILL MCELROYCompany: The William Douglas Group Inc. Revenue: $500,000Clients: 1,2001

28 | JANUARY 2014

SPECIAL REPORT

WEA

LTH

PR

OFESSIONAL

ADVISOR 201

4

Q. What are your top tips for gaining, and retaining, clients? A: I would say the number one tip is get IIROC li-censed. Clients are becoming more sophisticated and want more out of their advisors. If you cannot provide them with stocks and ETFs you will surely lose them over the long term.

My second tip would be to develop and nurture as many COIs (centres of influence) as you possibly can. These people are the gatekeepers to potential new clients and if you have their blessing, you don’t even need to be a great salesperson, just deliver the product/solution.

Q. What targets do you have for the coming year? A: I hope to increase the size of my business by aminimum of 10 per cent in assets per year not includ-

18-33_TOP_50(2).indd 28 09/01/2014 2:21:26 PM

MUTUAL FUNDSDONE DIFFERENTLY.

data source: morningstar as at november 30, 2013. copyright© 2013 morningstar research inc. all rights reserved. the information contained herein (1) is proprietary to morningstar and/or its content providers; (2) may not be copied or distributed; and (3) is not warranted to be accurate, complete or timely. neither morningstar nor its content providers are responsible for any damages or losses arising from any use of this information. commissions, trailing commissions, management fees and expenses all may be associated with mutual funds investments. please read the prospectus before investing. mutual funds are not guaranteed, their values change frequently and past performance may not be repeated. nei investments and working harder. investing smarter. are registered trademarks owned by northwest & ethical investments l.p.

1.888.809.3333 | NEIinvestments.com | @NEIinvestmentsWoRkiNg hARdeR. iNvestiNg smARteR.

like With oUR Nei NoRthWest tACtiCAl Yield FUNd.In an environment where yield is imperative, the Morningstar Rated™ NEI Northwest Tactical Yield Fund has an established track record of delivering strong and stable returns since its inception thanks to our unique and active approach to fund management. It’s just another shining example of how we do mutual funds differently.

Active, tactical multi-manager approach • Alternative income strategy • Risk management focus

ComPoUNd RetURN (as of Nov. 30, 2013) Ytd 1 YR 3 YR si*

NEI Northwest Tactical Yield Fund 12.21% 13.20% 8.49% 8.27%

Canada Tactical Balanced 9.50% 10.94% 4.62% --

file name: NWBR13147_WealthProfAdsArtist: Nicole date: 2014-01-02 colours: 4 media:

description: WP 1/2pg ads trim size: 7.25” x 5”

c m # #

market/city:

publication: Wealth Prof.

insertion date: YYYY-MM

shipping date: YYYY-MM-DD

ad #: NW-BR-13-147-M-D4

client: NEI safety/live: 7.0” x 4.75”

built size: 100% bleed size: 0.00” x 0.00”

y k # ## of sides: 1 folded size: 00.00” x 00.00”

d&s signoffs copywriter: creative: account:

client final approval via e-mail from: date:

380 wellington st. west toronto ontario canada m5v1e3 t 416 203 3470 Laser output may not be to size.

ing market growth.

Q. What has been the biggest challenge for advisors in the last 12 months?A: The biggest challenge has also been the biggestopportunity. Although many people are still con-cerned about the markets, and cash flow into the markets by the retail investor is still low, there are many potential clients out there with complacent agents. Either they are not contacting the clients or they are only reactive to client calls. Whether it was poor investment choices or home-country bias that has caused a potential client’s portfolio to perform poorly, there are so many options and alternative solutions to prove your worth to prospective clients and quickly gain their trust.

Q. How do you plan to adapt to the many regulatory changes that are set to affect the financial planning industry?

A: I have made a conscious effort since the tech bubbleto invest all of my clients in either a 0% front-end fund or a fee-for-service account. I do not sell anything on a deferred sales charge basis. I think going forward, there are going to be a lot of questions asked of advisors and the big one is going to be “What am I paying you for?” I personally feel more comfortable explaining my 1 per cent fee on a million-dollar account than I would trying to explain a 5.5 per cent upfront commission plus a 0.5 per cent trailer to any client.

Q. What are the biggest issues facing the financial advice industry today?A: I think there are several problems out there. Thebiggest one is churning followed by DSC (deferred sales charge) sales method. I prefer to be transparent, our offering consists of investments we think will outperform the market and I choose the one’s that I think will benefit the client the most based on their risk tolerance. WP

The advisor in our Top 10 with the most clients was Bill Mcelroy with 1,200

JANUARY 2014 | 29

WEALTHPROFESSIONAL.CA

18-33_TOP_50(2).indd 29 09/01/2014 2:21:29 PM

30 | JANUARY 2014

SPECIAL REPORT

WEA

LTH

PROFESSIONAL

ADVISOR 201

4

GILLIAN STOVEL RIVERSQ. What makes a good advisor? A: Use of smart technology, sometimes more than one if it means a clearer message to the client that can create momentum and confidence. This means the momentum and confidence also has to come from the practitioner, which in our case, we believe that means the Advisor’s team. We leverage smart planning and communications technology and software, a 4-person client process, and ultimately a dashboard based set of communication tools to explain matters to clients. The result is simplified statements of the information, clearly stated options for discussion, so that the client can select their own focused pathway forward with confidence and momentum.

TIM KELLY Q. What do you like to do outside of the office? A: I’m a big sports fan so I golf quite a bit in the summer and follow the NBA and NHL during the winter- especially the Toronto Raptors and The Montreal Canadiens.

JEFF WATCHORN & OLIVER GILBERT Q. What are the biggest issues facing the financial advice industry today? A: We see a lot variance in advice across the industry, however at the higher end of the advisory market, the advice tends to be more consistent and generally of higher quality. I think there are issues surrounding regulation and transparency of fees, but rather than issues we see these as making the industry better for advisors and clients. Moves toward transparency are good for our industry.

CYRILLA SAUNDERS Q. What targets do you have for the coming year?

A: Professionally, growing my practice: AUM at

approximately $120 million, Gross production $1.7 million; encouraging my team members to attain more knowledge through education; contining to have great client retention and satisfaction. And to continue to be the rock that stays focused on the needs of both my team and our client relationships

Personally: to spend more time with my family; pay attention to my physical and mental wellbeing by slowing down, practicing yoga and using my sauna on a frequent basis.

LUKE KRATZ Q. What are your top tips for gaining, and retaining, clients? A: Establish a belief system based on your strongest convictions and then consistently communicate what you believe and what you stand for, letting the chips fall where they may. Many advisors fall into the trap of attempting to be all things to all people. It is much better to be all things to a set number of people – those who share your principals and value what you do for them.

JOHN DE GOEY Q. What targets do you have for the coming year? A: Play a significant role in getting the industry to ban embedded compensation and adopt a statutory best interests standard. Admittedly, this might take more than a year, but these are big and impactful goals, too.

CHAD PRICE Q. What are the biggest issues facing the financial advice industry today? A: Too much information. We live in a world where you can watch global news 24 hours a day. You can also watch your investment portfolio by the second and that causes many investors to panic and react to breaking news which can lead to a desire to liquidate their portfolios at the wrong time.

TOP 50 INSIGHTS

Join us on LinkedIN or visit FundSERV.com to find out more.

Powered by:

Celebrating 20 Years of Service

The New FUNDcomBetter, Easier, and Mobile!

18-33_TOP_50(2).indd 30 09/01/2014 2:21:35 PM

32 | JANUARY 2014

SPECIAL REPORT

WEA

LTH

PROFESSIONAL

ADVISOR 201

4

caused market nervousness and concerns among investors.

PETER BORONKAY Q. What do you like most about being an advisor?A: The knowledge and experience to strive to make a difference in our clients lives. We cannot control the wind but we can adjust the sails to best align our work with the needs of the client. This profession gives us a clear canvas to make a financial painting for our clients. We have the freedom on how we apply the strokes to this painting.

ANITA DALAKOTI Q. What has been the biggest challenge for advisors in the last 12 months? A: I’m not sure about other financial planners. I suppose you are talking about the economic climate. Well, to me those are a given and I don’t consider them challenges -- we have good times and we have bad times, this is a historical fact. Look at an [Morningstar] Andex Chart – a seasoned planner know how to deal with these challenges. For me, every client is a challenge and an opportunity. These are perennial challenges not restricted to a 12-month time frame. A challenge because I wish to create a plan that they can identify with and implement without taking away the their joys of living - easier said than done. An opportunity because every client is different and, in dealing with them, I get to learn skills that can be implemented with other clients.

NATHAN LEIBOWITZ Q. What are the biggest issues facing the financial advice industry today? A: Being able to maintain and grow your practice while properly servicing your existing clients. With client needs changing, and the expectation that advisors should handle all aspect of their situation – such as insurance, will planning, charity etc. you need to automate your practice and have seamless communication with all members of your team. This will be a key differentiating factor as more firms offer the total wealth management package.

LÉONY DEGRAAF HASTINGS Q. How do you plan to adapt to the many regulatory changes that are set to affect the financial planning industry? A: I have been proactive with clients in helping them understand their choices and what they are paying for. WP

STEPHEN JONES Q. How do you plan to adapt to the many regulatory changes that are set to affect the financial planning industry? A: Our industry’s biggest challenge moving forwards is “fee disclosure”. We will spend the next two years, using many different methods, to show our clients our value.

LAURIE BONTEN Q. What is your top tip for other advisors? A: Look at the big picture and don’t focus on the short term. Build solid relationships with superior service. Know all the rules surrounding the industry along with the types of service and advice you can provide. You cannot control the markets so control what you can....your knowledge.

NICK BAKISH Q. How do you plan to adapt to the many regulatory changes that are set to affect the financial planning industry? A: Adapting to the many regulatory changes that will affect this profession will happen in a few ways. Staying on top of legislation will be one of them, in addition utilizing internal and external communications and staying compliant at the minimum cost to the business.

ROB MCCLELLAND Q. How do you plan to adapt to the many regulatory changes that are set to affect the financial planning industry?A: Luckily we moved to a fee-based practise in 2008 and have always provided detailed financial planning to our clients not just investment advice.

CHARLES JIANG Q. What has been the biggest challenge for advisors in the last 12 months? A: These are challenging times for financial advisors, who are not only trying to navigate choppy markets but also maintain strong ties with their clients. These challenges include: increasing compliance requirements and the volatile market during the year. Increasing compliance demands and requirements force advisors to do a better job. But it is definitely good for the clients, and eventually good for the advisors and the industry. The US budget impasse and the tapering of monetary stimulus

WHAT IS THE EXEMPT MARKET?

WHO QUALIFIES TO INVEST IN THE EXEMPT MARKET?

WHAT ARE KEY FEATURES OF EXEMPT MARKET SECURITIES?

HOW DO YOU INVEST IN THE EXEMPT MARKET?

WHAT IS THE STRUCTURE OF THE EXEMPT MARKET?

ANSWERS TO THESE QUESTIONS & MUCH MORE AT:

EXEMPTEDUCATION.CA

Educational Information For Investors.Sponsored by The National Exempt Market Association and it’s members.

READ THE EXEMPT EDGE AT WWW.NEMAONLINE.CA/EXEMPT-EDGETHE NATIONAL PUBLICATION ON PRIVATE INVESTING

YOUR WORST

NIGHTMARECEASE TRADE ORDERS

HOW THEY HAPPEN, WHY THEY HAPPEN,

AND HOW TO DEAL WITH THEM

BY MATTHEW EPP & CRAIG L. BENTHAM

ALSO IN THIS ISSUE:

INTERVIEW WITH CSA & ASC CHAIRMAN BILL RICE

IN GREED THEY TRUST

50 SHADES OF COMPLIANCE

THE MARATHON OF PRIVATE CAPITAL CHANGE

IN CANADA

ISSUE 4

SPRING 2013

NEMAonline.ca

@ NEMACanada

BY CRAIG SKAUGE Pg. 30

Pg. 16

Pg. 34

BY RYAN HOULT Pg. 8

BY KATHLEEN BLACK Pg. 10

eF

ISSUE 5SUMMER 2013

NEMAONLINE.CA@ NEMACANADA

SPINOFFHOW THE EXEMPT MARKET IS HELPING REVIVE THE ECONOMYBY MATT MCKELLAR & BILL MCNARLAND|PAGE 22

1ST

ANNIVER

SARY

ISSU

E

ALSO IN THIS ISSUE:THE MARKETING MOUSE TRAP BY ZACK SIEZMAGRAF W/NEIL HUTTON|PAGE 32

LITIGATION NATIONBY MATTHEW EPP|PAGE 18

US EQUITY MARKET STRUCTURE BY THOMAS CALDWELL|PAGE 10

P.10WHEN PIGS FLYTHE OM EXEMPTION’S PENDING ARRIVAL IN ONTARIO

- CRAIG SKAUGE

P.14WHAT’S IN A RATE OF RETURN?

- CHRISTOPHE VOEGELI

UNITYTHE EXEMPT MARKET COMES TOGETHER FOR THE GREATER GOOD- CORA PETTIPASPAGE 28

P.18

Q&A W/DRAGONW. BRETT WILSON

1

2

3

4

5

6

7

8

9

10

F

ISSUE 6FALL 2013NEMAONLINE.CA@ NEMACANADA

18-33_TOP_50(2).indd 32 09/01/2014 2:21:49 PM