© 2010 AT&T Intellectual Property. All rights reserved. AT&T, the AT&T logo and all other AT&T marks contained herein are trademarks of AT&T Intellectual Property and/or AT&T affiliated companies. All other marks contained herein are the property of their respective owners.

Can mHealth be a profitable Can mHealth be a profitable business?

Perspectives from a leading carrier

Chris Hill, VP

AT&T Mobility Enterprise Solutions

Feb 14, 2011

2011 AT&T Intellectual Property. All rights reserved. AT&T, the AT&T logo and all other AT&T marks contained herein are trademarks of AT&T Intellectual Property and/or AT&T affiliated companies. All other marks contained herein are the property of their respective owners

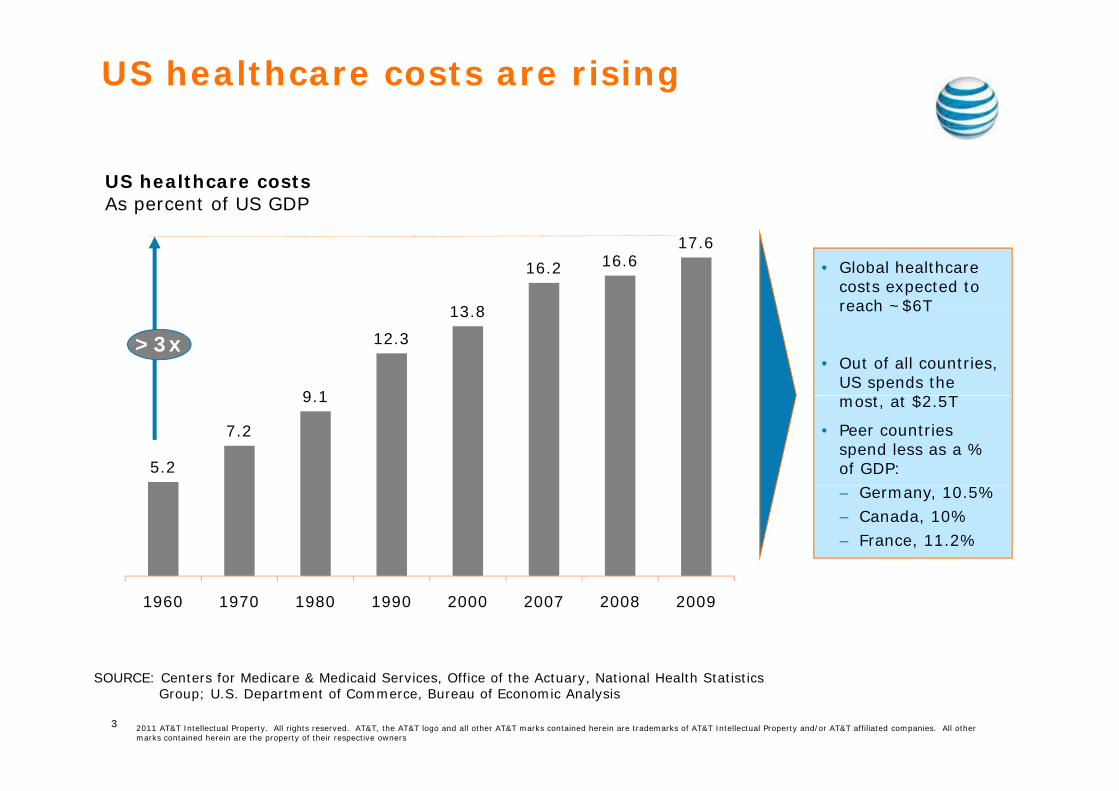

US healthcare costs are rising

US healthcare costsAs percent of US GDP

• Global healthcare costs expected to reach ~$6T13 8

16.2 16.617.6

reach ~$6T

• Out of all countries, US spends the

$2 5T9 1

12.3

13.8

>3x

most, at $2.5T

• Peer countries spend less as a % of GDP:5.2

7.2

9.1

– Germany, 10.5%– Canada, 10%– France, 11.2%

1960 1970 1980 1990 2000 2007 2008 2009

© 2010 AT&T Intellectual Property. All rights reserved. AT&T, the AT&T logo and all other AT&T marks contained herein are trademarks of AT&T Intellectual Property and/or AT&T affiliated companies. All other marks contained herein are the property of their respective owners.

2011 AT&T Intellectual Property. All rights reserved. AT&T, the AT&T logo and all other AT&T marks contained herein are trademarks of AT&T Intellectual Property and/or AT&T affiliated companies. All other marks contained herein are the property of their respective owners

SOURCE: Centers for Medicare & Medicaid Services, Office of the Actuary, National Health Statistics Group; U.S. Department of Commerce, Bureau of Economic Analysis

3

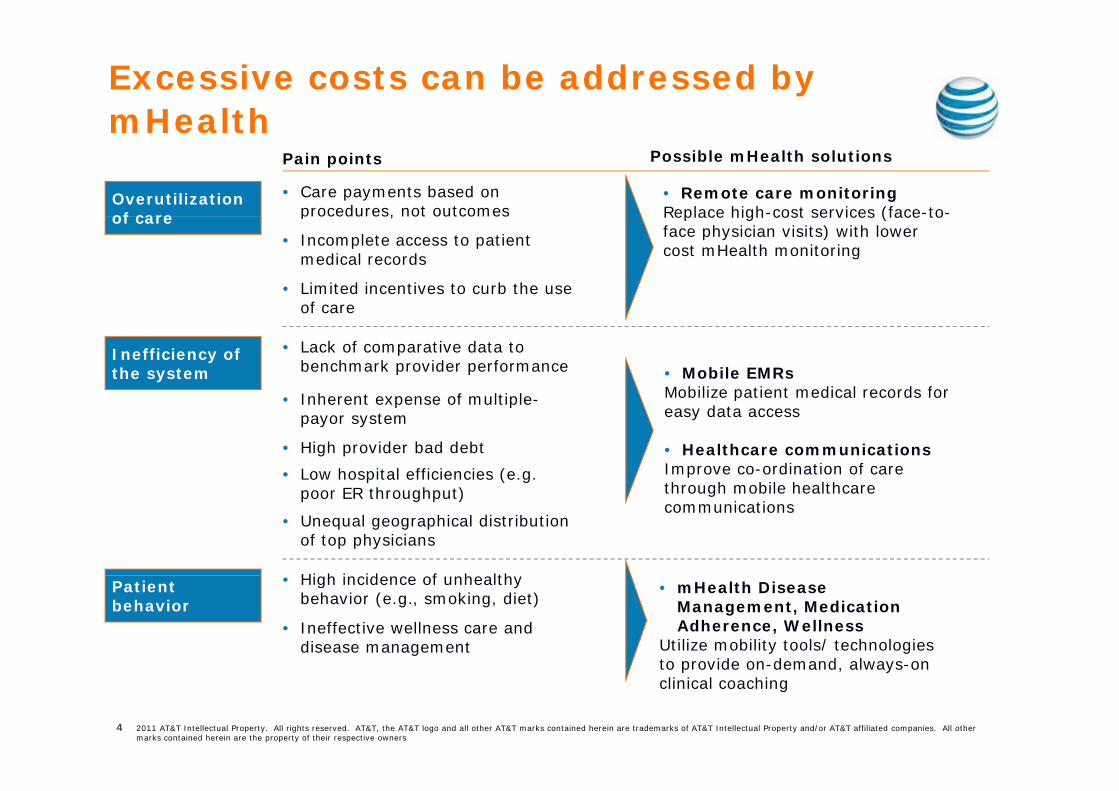

Excessive costs can be addressed by mHealthmHealth

Overutilization of care

Pain points

• Care payments based on procedures, not outcomes

• Remote care monitoringReplace high-cost services (face-to-

Possible mHealth solutions

of care• Incomplete access to patient

medical records

procedures, not outcomes

• Limited incentives to curb the use of care

Replace high cost services (face toface physician visits) with lower cost mHealth monitoring

Inefficiency of the system

of care

• Lack of comparative data to benchmark provider performance

I h t f lti l

• Mobile EMRsMobilize patient medical records for

• High provider bad debt

• Inherent expense of multiple-payor system

• Low hospital efficiencies (e.g.

Mobilize patient medical records for easy data access

• Healthcare communications Improve co-ordination of care through mobile healthcare

Hi h i id f h lth

• Unequal geographical distribution of top physicians

poor ER throughput) through mobile healthcare communications

Patient behavior

• Ineffective wellness care and disease management

• High incidence of unhealthy behavior (e.g., smoking, diet)

• mHealth Disease Management, Medication Adherence, Wellness

Utilize mobility tools/ technologies to provide on-demand always-on

© 2010 AT&T Intellectual Property. All rights reserved. AT&T, the AT&T logo and all other AT&T marks contained herein are trademarks of AT&T Intellectual Property and/or AT&T affiliated companies. All other marks contained herein are the property of their respective owners.

2011 AT&T Intellectual Property. All rights reserved. AT&T, the AT&T logo and all other AT&T marks contained herein are trademarks of AT&T Intellectual Property and/or AT&T affiliated companies. All other marks contained herein are the property of their respective owners

to provide on-demand, always-on clinical coaching

4

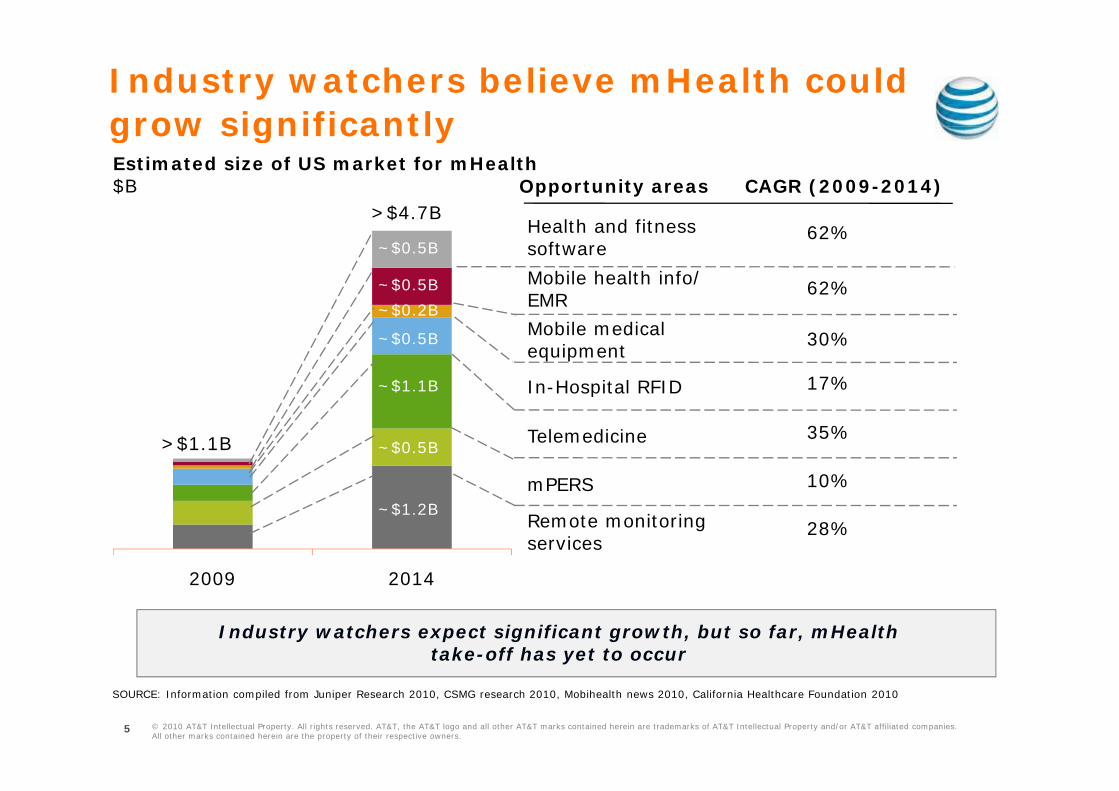

Industry watchers believe mHealth couldgrow significantlygrow significantlyEstimated size of US market for mHealth$B Opportunity areas CAGR (2009-2014)

>$4 7B>$4.7B

~$0.5B

~$0.5B

$0 2B

Mobile health info/ EMR

Health and fitness software

62%

62%

~$0.2B

~$0.5B

~$1.1B In-Hospital RFID

Mobile medical equipment

EMR

17%

30%

>$1.1B ~$0.5B

mPERS

Telemedicine

p

10%

35%

2009 2014

~$1.2BRemote monitoring services

mPERS

28%

10%

2009 2014

Industry watchers expect significant growth, but so far, mHealthtake-off has yet to occur

© 2010 AT&T Intellectual Property. All rights reserved. AT&T, the AT&T logo and all other AT&T marks contained herein are trademarks of AT&T Intellectual Property and/or AT&T affiliated companies. All other marks contained herein are the property of their respective owners.

SOURCE: Information compiled from Juniper Research 2010, CSMG research 2010, Mobihealth news 2010, California Healthcare Foundation 2010

5

mHealth market “take-off” limited by a number of challenges

• >6,000 healthcare and fitness apps – of which only 200+ are

Example

a number of challenges

>6,000 healthcare and fitness apps of which only 200+ are “enterprise” backed

• Difficult for healthcare enterprise customers (providers, payors) to distinguish winners from “me too’s”

Profusion of products

Fragmented solutions

• Current solutions are not plug-and-play; each has their own proprietary “back-end”/ platform

• Do not cover the full extent of care (linking patient, device, wireless li ti d t l ith li i l i t ti )

Competingstandards

• Unclear which standard will prevail (e.g., Zigbee vs. LP Bluetooth, ANT+ etc.)

application, data algorithms, clinical interventions)

Unclear b i

standards

• Current solutions targeted at providers (hospitals/ physicians) who are slow adopters due to reimbursement issues or direct-to-business

models

are slow adopters due to reimbursement issues, or direct-to-consumers (patients) who have low appetite for out-of-pocket expenses

© 2010 AT&T Intellectual Property. All rights reserved. AT&T, the AT&T logo and all other AT&T marks contained herein are trademarks of AT&T Intellectual Property and/or AT&T affiliated companies. All other marks contained herein are the property of their respective owners.

6

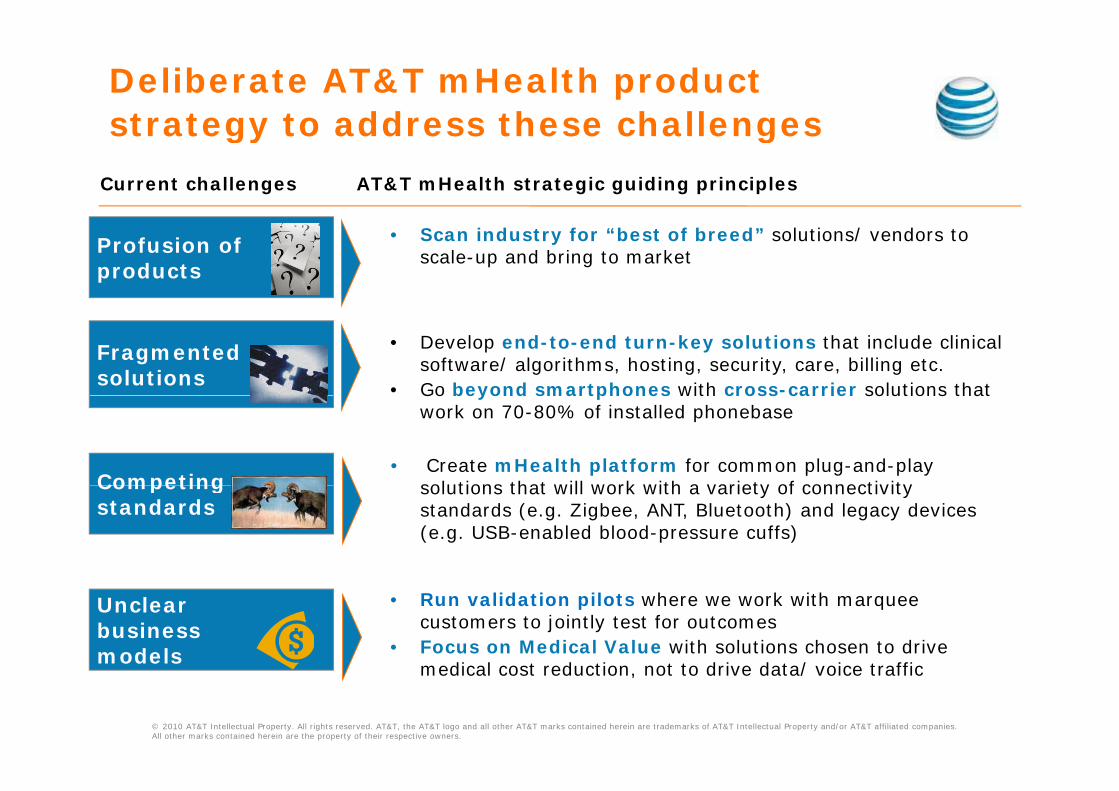

Deliberate AT&T mHealth product strategy to address these challenges

Current challenges AT&T mHealth strategic guiding principles

strategy to address these challenges

• Scan industry for “best of breed” solutions/ vendors to scale-up and bring to market Profusion of

products

• Develop end-to-end turn-key solutions that include clinical software/ algorithms, hosting, security, care, billing etc.

• Go beyond smartphones with cross-carrier solutions that

Fragmented solutions Go beyond smartphones with cross carrier solutions that

work on 70-80% of installed phonebase

• Create mHealth platform for common plug-and-play solutions that will work with a variety of connectivity Competing solutions that will work with a variety of connectivity standards (e.g. Zigbee, ANT, Bluetooth) and legacy devices (e.g. USB-enabled blood-pressure cuffs)

Competingstandards

• Run validation pilots where we work with marquee customers to jointly test for outcomes

• Focus on Medical Value with solutions chosen to drive di l t d ti t t d i d t / i t ffi

Unclear business models

© 2010 AT&T Intellectual Property. All rights reserved. AT&T, the AT&T logo and all other AT&T marks contained herein are trademarks of AT&T Intellectual Property and/or AT&T affiliated companies. All other marks contained herein are the property of their respective owners.

medical cost reduction, not to drive data/ voice traffic

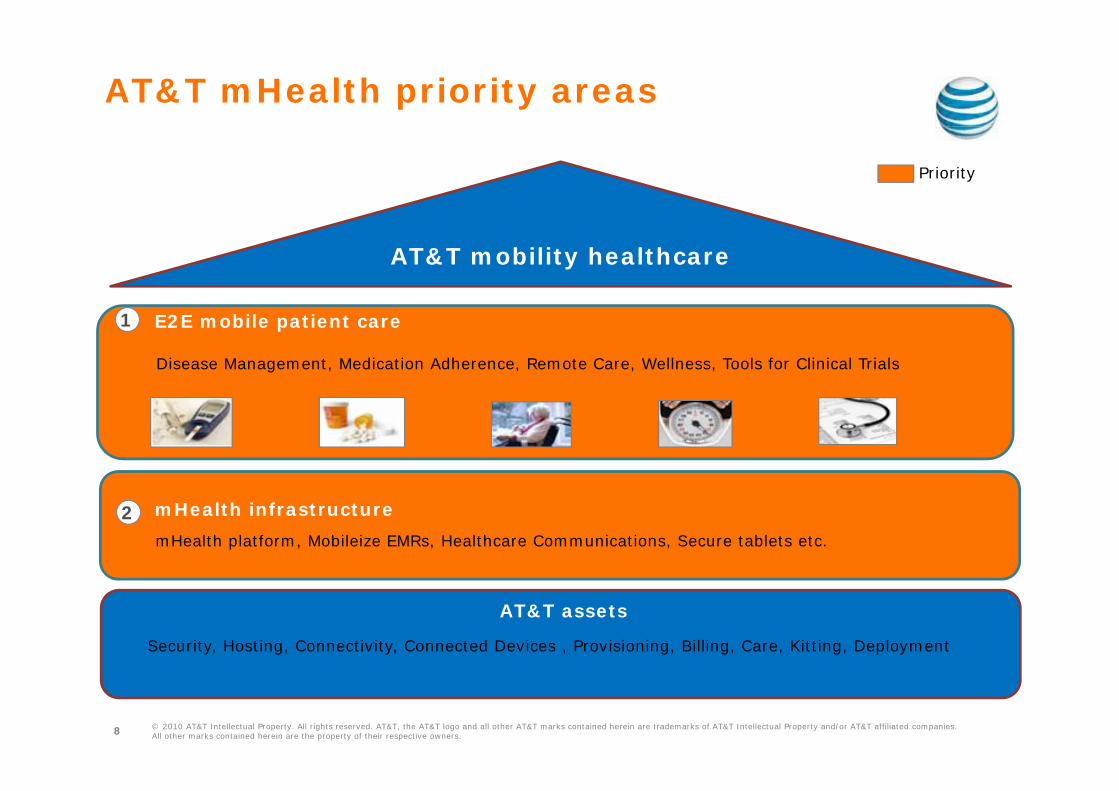

AT&T mHealth priority areas

AT&T

Priority

AT&T Mobility Enabled Healthcare

SolutionsAT&T mobility healthcare

E2E mobile patient care

Disease Management, Medication Adherence, Remote Care, Wellness, Tools for Clinical Trials

1

mHealth platform, Mobileize EMRs, Healthcare Communications, Secure tablets etc.

2 mHealth infrastructure

AT&T assets

Security, Hosting, Connectivity, Connected Devices , Provisioning, Billing, Care, Kitting, Deployment

© 2010 AT&T Intellectual Property. All rights reserved. AT&T, the AT&T logo and all other AT&T marks contained herein are trademarks of AT&T Intellectual Property and/or AT&T affiliated companies. All other marks contained herein are the property of their respective owners.8

© 2010 AT&T Intellectual Property. All rights reserved. AT&T, the AT&T logo and all other AT&T marks contained herein are trademarks of AT&T Intellectual Property and/or AT&T affiliated companies. All other marks contained herein are the property of their respective owners.

9

© 2010 AT&T Intellectual Property. All rights reserved. AT&T, the AT&T logo and all other AT&T marks contained herein are trademarks of AT&T Intellectual Property and/or AT&T affiliated companies. All other marks contained herein are the property of their respective owners.

© 2010 AT&T Intellectual Property. All rights reserved. AT&T, the AT&T logo and all other AT&T marks contained herein are trademarks of AT&T Intellectual Property and/or AT&T affiliated companies. All other marks contained herein are the property of their respective owners.

© 2010 AT&T Intellectual Property. All rights reserved. AT&T, the AT&T logo and all other AT&T marks contained herein are trademarks of AT&T Intellectual Property and/or AT&T affiliated companies. All other marks contained herein are the property of their respective owners.